finalized

Mar 31.2023 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSED: DOWN $10.30 T0 $1969.30

SILVER PRICE CLOSED: UP $0.14 AT $23.98

work in progress.

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1969,00

Silver ACCESS CLOSE: 24.14

Bitcoin morning price:, $28,042 UP 168 Dollars

Bitcoin: afternoon price: $28,428 UP 554 dollars

Platinum price closing $994.40 UP $5.40

Palladium price; closing $1466.30DOWN $8.15

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2652.00 DOWN 17.00 CDN dollars per oz (ALL TIME HIGH 2732.50)

BRITISH GOLD: 1596.50 DOWN 1.50pounds per oz//(ALL TIME HIGH//1629.84)

EURO GOLD: 1816.50 DOWN 0.50 euros per oz //(ALL TIME HIGH//1860.82)

COMEX DATA EXCHANGE:

EXCHANGE: COMEX

CONTRACT: APRIL 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,980.300000000 USD

INTENT DATE: 03/30/2023 DELIVERY DATE: 04/03/2023

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 155 338

104 C MIZUHO 156

118 H MACQUARIE FUT 339

132 C SG AMERICAS 140

167 C MAREX 3

332 H STANDARD CHARTE 3672

357 C WEDBUSH 1

363 H WELLS FARGO SEC 1237

365 C MAREX CAPITAL M 12

435 H SCOTIA CAPITAL 825

523 H INTERACTIVE BRO 2

624 C BOFA SECURITIES 106

624 H BOFA SECURITIES 4368

657 C MORGAN STANLEY 2603

661 C JP MORGAN 2414 1650

661 H JP MORGAN 10682

685 C RJ OBRIEN 25

686 C STONEX FINANCIA 9

690 C ABN AMRO 21

732 C RBC CAP MARKETS 20

800 C MAREX SPEC 53

880 C CITIGROUP 1105

880 H CITIGROUP 3681

DLV615-T CME CLEARING

BUSINESS DATE: 03/30/2023 DAILY DELIVERY NOTICES RUN DATE: 03/30/2023

PRODUCT GROUP: METALS RUN TIME: 20:36:31

905 C ADM 229

TOTAL: 16,923 16,923

MONTH TO DATE: 16,923

JPMORGAN stopped 1650/16923 contracts

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2023. CONTRACT: 16,923 NOTICES FOR 1,692,300 OZ or 0.11244 TONNES

total notices so far: 16923 contracts for 1692300 oz (52.637 tonnes)

SILVER NOTICES: 167 NOTICE(S) FILED FOR 865,000 OZ/

total number of notices filed so far this month : 167 for 835,000 oz

END

GLD

WITH GOLD DOWN $4,85

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:////// A HUGE WITHDRAWAL OF 1.44TONNES FROM THE GLD.

INVENTORY RESTS AT 928.02 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 11 CENTS

WOW!! WHAT CROOKS:

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF OF 4.779 MILLION OZ FROM THE SLV: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 465.412 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 3065 TO 121,447 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS GIGANTIC SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.46 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. WITH THIS WEEK’S READING AT THE COMEX, WE HAVE NOW SET ANOTHER RECORD LOW AT 117,395 CONTRACTS , MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.46). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD AN ATMOSPHERIC GAIN ON OUR TWO EXCHANGES 5865 CONTRACTS. WE HAD ANOTHER 1000 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 5.0 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS( 2008 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.055 MILLION OZ(FIRST DAY NOTICE)+ THE 5.0 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 6.055 MILLION OZ/ //// V) HUGE SIZED COMEX OI GAIN/ HUGE SIZED EFP ISSUANCE/. WE HAVE NOW REACHED THE POINT THAT THE CROOKS CANNOT LIQUIDATE ANY MORE SILVER SPEC LONGS.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –XXX CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 23 days, total 22,516 contracts: OR 112,580 MILLION OZ . (978 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 99.07 MILLION OZ

.

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE BUT BELOW LAST MONTH

APRIL

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3065 CONTRACTS WITH OUR $0.46 GAIN IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 2700 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 1.055 MILLION OZ//FIRST DAY NOTICE// 0 QUEUE JUMP (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 5.0 MILLION OF EXCHANGE FOR RISK ISSUED EARLY IN APRIL (INCREASES THE AMOUNT OF SILVER STANDING) //NEW STANDING 6.055 MILLION OZ .. WE HAVE A GIGANTIC SIZED GAIN OF 5765 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 167 NOTICE(S) FILED TODAY FOR 835,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 1875 CONTRACTS TO 475,740 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED- XXX CONTRACTS.

WE HAD A FAIR SIZED INCREASE IN COMEX OI ( 4009 CONTRACTS) WITH OUR $4,85 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR APR. AT 66.892 TONNES ON FIRST DAY NOTICE //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)YET ALL OF..THIS HAPPENED WITH OUR $12.25 GAIN IN PRICE WITH RESPECT TO THURSDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 3487 OI CONTRACTS (66.892 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1612 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 475,740

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3487 CONTRACTS WITH 1875 CONTRACTS INCREASED AT THE COMEX AND 1612 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3487 CONTRACTS OR 10.846 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1612 CONTRACTS) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (1875) //TOTAL GAIN IN THE TWO EXCHANGES 3487 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 66.892 TONNES // ///3) ZERO LONG LIQUIDATION //4) FAIR SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

TOTAL EFP CONTRACTS ISSUED: 90,050 CONTRACTS OR 9,005,000OZ OR 280.09 TONNES IN 23 TRADING DAY(S) AND THUS AVERAGING: 3915 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 23 TRADING DAY(S) IN TONNES 280.09TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 280.09/3550 x 100% TONNES 7.75% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 3065 CONTRACTS OI TO 121,447 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 2700 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 2700 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2700 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3065 CONTRACTS AND ADD TO THE 2700 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC GAIN OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 5765 CONTRACTS.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES //28.825 MILLION OZ

OCCURRED WITH OUR $0.46 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

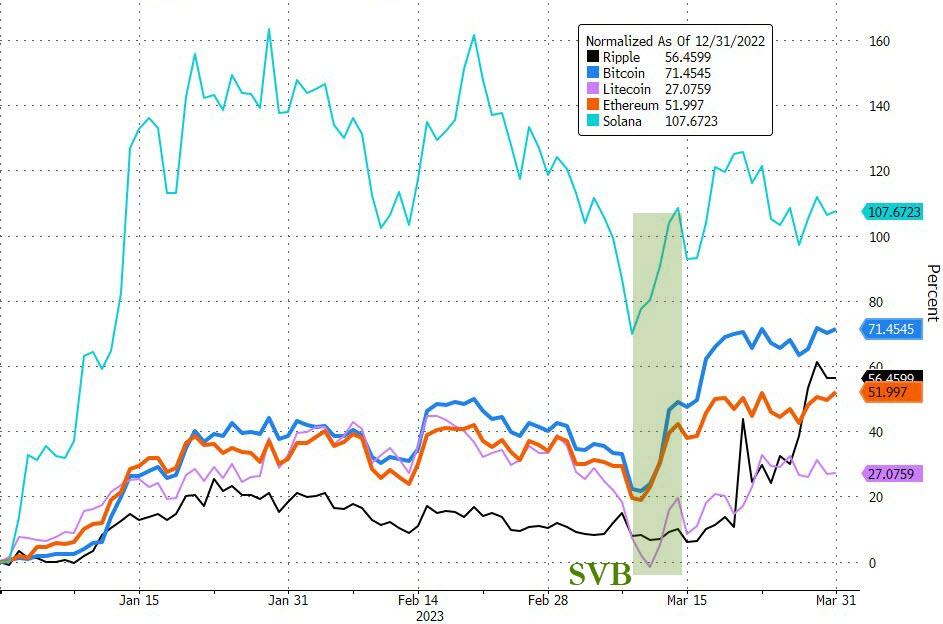

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

NORTH KOREA/SOUTH KOREA

i)FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED UP 11.61 PTS OR 0.36% //Hang Sang CLOSED UP 181.25 PTS OR 0.89% /The Nikkei closed UP 256.55 PTS OR 0.93 % //Australia’s all ordinaries CLOSED UP 0.93 % /Chinese yuan (ONSHORE) closed UP TO 6.8663/OFFSHORE CHINESE YUAN DOWN TO 6.8698 /Oil UP TO 74.51dollars per barrel for WTI and BRENT AT 78.41 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

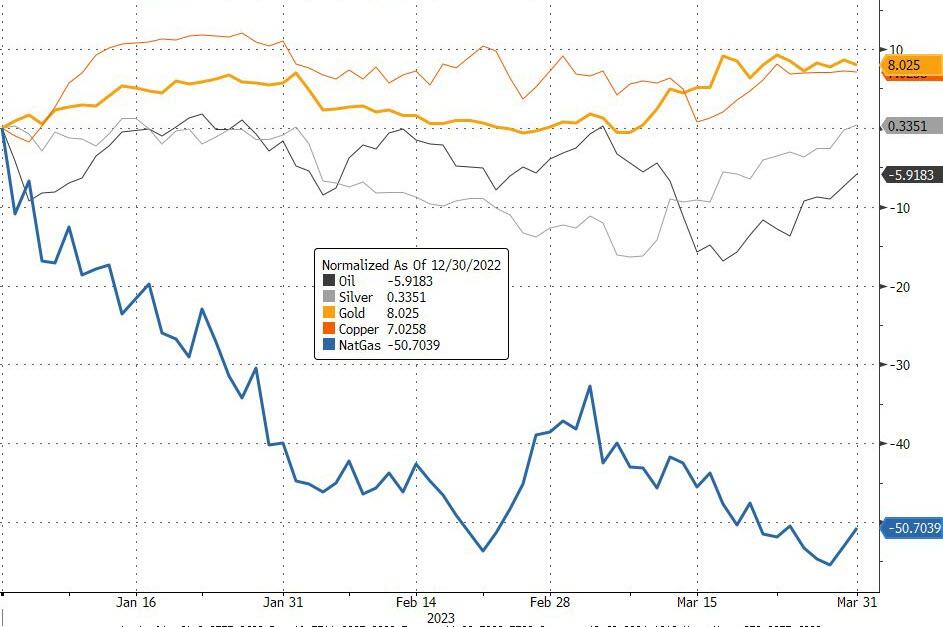

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1875 CONTRACTS UP TO 475,740 WITH OUR GAIN IN PRICE OF $12.25 ON THURSDAY

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF APRIL… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1612 EFP CONTRACTS WERE ISSUED: : APRIL 1612 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1612 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR TOTAL OF 3487 CONTRACTS IN THAT 1662 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED GAIN OF 1875 COMEX CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $12.25, WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: APRIL (66.892) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 66.892 tonnes

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $12.25 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR FAIR SIZED GAIN OF 3487 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 10.846 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL. (66.892 TONNES) ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $12.25

WE HAD -XX CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3487 CONTRACTS OR 348,700OZ OR 10.846 TONNES

TONNES

Estimated gold comex today 153,473 //poor

final gold volumes/yesterday 188,272//poot

//MARCH 31/ APRIL 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | NIL . |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | n782.370oz |

| No of oz served (contracts) today | 16,923 notice(s) 1,692,300 OZ 52.637TONNES |

| No of oz to be served (notices) | 4583 contracts 458,300 oz 14.255TONNES |

| Total monthly oz gold served (contracts) so far this month | 16923notices 1,692,300 OZ 52.637 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: NIL oz

customer withdrawals: 0

total withdrawals: NIL oz

in tonnes:0.

Adjustments; 1

Out of JPMorgan: 578,710.938 customer to dealer

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of APRIL we have an oi of 21,506 contracts having LOST 5409 contracts.

Thus by definition, the initial amount of gold standing for April is as follows:

21509 contracts x 100 oz per contract equals 2,150900 oz or 66.892 tonnes

May LOST 9 contracts to stand at 1584

JUNE gained 5822 contracts to 394,663.

We had 16,923 notice(s) filed today for 1,692,300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 2412 notices were issued from their client or customer account. The total of all issuance by all participants equate to 16,923 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1650 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2023. contract month,

we take the total number of notices filed so far for the month (16,923 x 100 oz ), to which we add the difference between the open interest for the front month of (APRIL. 21,506 CONTRACTS) minus the number of notices served upon today 16,923 x 100 oz per contract equals 2,150,600 OZ OR 66.892 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month:No of notices filed so far (16,923 x 100 oz+ 21,506 OI for the front month minus the number of notices served upon today (16,923)x 100 oz} which equals 2,150,600 oz standing OR 66.892 TONNES in this active delivery month of APRIL..

TOTAL COMEX GOLD STANDING: 19.073 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,643,341.368 OZ 51.114tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,291,699.603 OZ

TOTAL REGISTERED GOLD: 12,097,362.125 (376,27 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 9,773,054.363 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,454,021 OZ (REG GOLD- PLEDGED GOLD) 325.16 tonnes//

END

SILVER/COMEX

MAR 31/2023// THE APRIL 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 822,057.745oz Brinks JPMorgan Loomis . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 1045.400 oz JPMorgan |

| No of oz served today (contracts) | 167 CONTRACT(S) (835,000 OZ) |

| No of oz to be served (notices) | 44 contracts (220,000 oz) |

| Total monthly oz silver served (contracts) | 167 Contracts (835,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0deposits into the customer account

Total deposits: nil oz

JPMorgan has a total silver weight: 144.828million oz/278,057million =52,15% of comex .//dropping fast

Comex withdrawals: 3

i)Out of Brinks 198,506.420 oz

ii) Out of Loomis 468,108.01

iii) Out of JPMorgan: 155,442.02 oz

Total withdrawals; 822,057.45 oz

adjustments: 3

i

Brinks 169,641,100 oz

Int Delaware: 67,641.810 oz

Loomis 85m293,700 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 35.809 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 279.086 million oz

CALCULATION OF SILVER OZ STANDING FOR MAR

silver open interest data:

FRONT MONTH OF APRIL /2023 OI: 211 CONTRACTS HAVING LOST 26 CONTRACT(S.

THUS BY DEFINITION THE INITIAL AMOUNT OF SILVER STANDING IN THIS NON ACTIVE DELIVERY MONTH OF APRIL IS AS FOLLOWS:

211 NOTICES X 5000 OZ PER NOTICE = 1,055,000 OZ

May GAINED 1316 CONTRACTS UP TO 91,113

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 167 for 835,000 oz

Comex volumes// est. volume today 56,271 good

Comex volume: confirmed yesterday: 72,805 Contracts ( strong

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 167 x 5,000 oz = 835000 oz

to which we add the difference between the open interest for the front month of APRIL(211) and the number of notices served upon today 167 X (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL/2023 contract month: 167 (notices served so far) x 5000 oz + OI for the front month of MAR (211) – number of notices served upon today (867 )x 500 oz of silver standing for the APRIL. contract month equates 1.055 million oz +the 5.0million oz of exchange for risk//new total standing 6.055 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MARCH 31/WITH GOLD DOWN $10.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD////INVENTORY RESTS AT 928.02 TONNES

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

MARCH 15/THE IDES OF MARCH: WITH GOLD UP $18.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 913.27 TONNES

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

FEB 28/WITH GOLD UP $12.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 917.61 TONNES

FEB 27/WITH GOLD UP $6.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.32 TONNES

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917.32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

GLD INVENTORY: 928.02 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 31/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD/: A MASSIVE 4.779 MILLION OZ DEPOSITED INTO THE SLV///INVENTORY RESTS AT465.412 MILLION OZ

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

MARCH 17/WITH SILVER UP 79 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 10.478 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 462.748 MILLION OZ//

MARCH 16/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 5.009 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 473.226 MILLION OZ//

MARCH 15/WITH SILVER DOWN 7 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 643,000 OZ INTO THE SLV//INVENTORY RESTS AT 478.235 MILLION OZ/

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWALOF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

FEB 28/WITH SILVER UP 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.241 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.188

FEB 27/WITH SILVER DOWN 15 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.471 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 482.429 MILLION OZ

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 465.412 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

nd

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards/John Rubino

3,Chris Powell of GATA provides to us very important physical commentaries

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

END

5.IMPORTANT COMMENTARIES ON COMMODITIES: LITHIUM

END

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 6.8663

OFFSHORE YUAN: 6.8698

SHANGHAI CLOSED UP 11.61 PTS OR 0.36%

HANG SANG CLOSED UP 181.25 PTS OR 0.89%

2. Nikkei closed UP 256.55 PTS OR 0.93%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 101.896 EURO FALLS TO 1.0899 DOWN 5 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.322 J apan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 132.95 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.3780***/Italian 10 Yr bond yield RISES to 4,219*** /SPAIN 10 YR BOND YIELD RISES TO 3.390…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.263

3j Gold at $1976.20.75 silver at: 23.381am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 2/100 roubles/dollar; ROUBLE AT 77,10//

3m oil into the 74 dollar handle for WTI and 78 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 132.40 10 YEAR YIELD AFTER BREAKING .54%, RISESTO .321% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9145 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.99525well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.564 UP 1 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.756 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.1389 UP 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.19…

GREAT BRITAIN/10 YEAR YIELD: UP 3 BASIS PTS AT 3.545

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

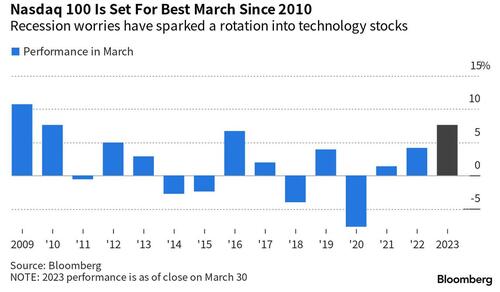

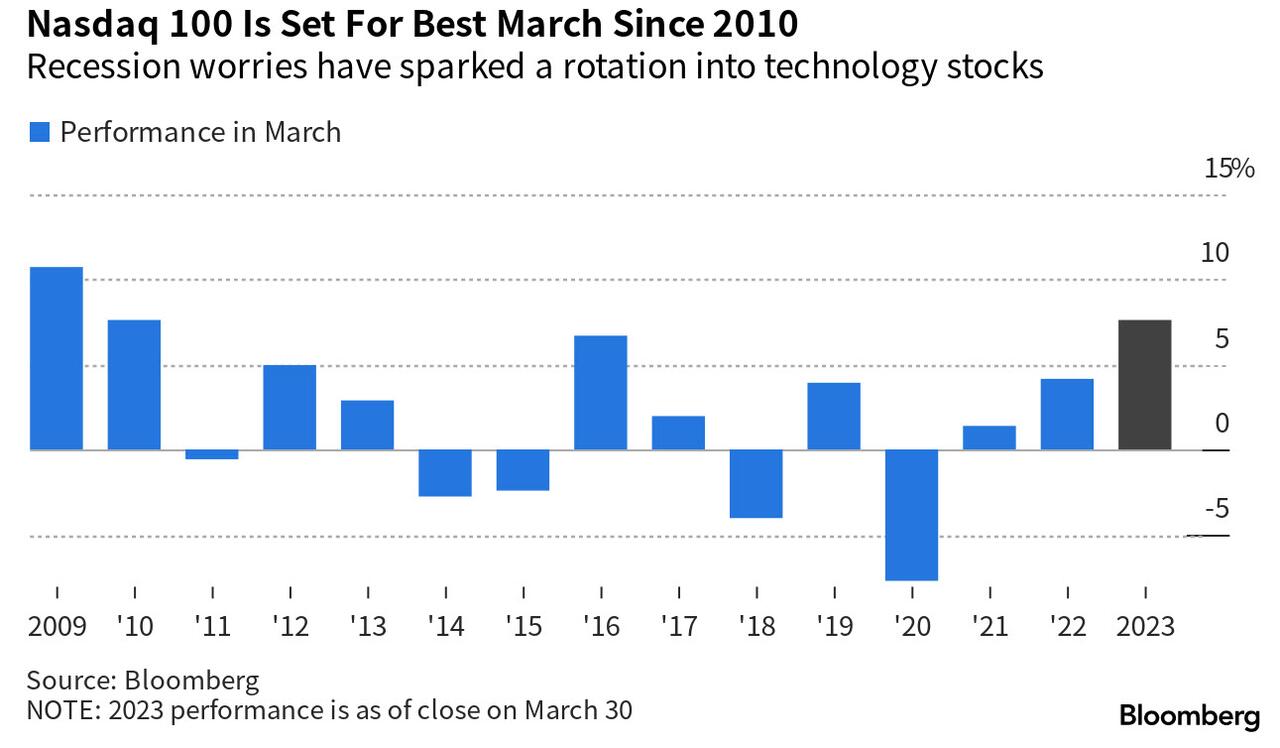

S&P Futures Hit 6 Week High, Nasdaq Set For Best March Since 2010 Ahead Of Quarter-End Fireworks

BY TYLER DURDEN

FRIDAY, MAR 31, 2023 – 03:17 PM

US futures extended gains for the 3rd straight day and are on pace to rise 6 of the past 7 days, led by the Nasdaq 100 which is set for its best March in more than a decade as investors bet on a softening in central-bank policy amid worries about a recession while the slowdown in new money market fund injections eased fears about the ongoing bank run.

Contracts on the Nasdaq 100 were up 0.3% as of 7:45 a.m. in New York, while S&P 500 futures also rose 0.2% hitting the highest level in 6 weeks.

For the month, the tech-heavy gauge is tracking an increase of about 7.7%, its biggest March advance since 2010. The benchmark S&P 500 is also set for a small monthly gain as the rates outlook overshadowed concerns about turmoil in the banking sector and a possible economic contraction.

The dollar strengthened Friday, trimming some of its sharp declines this month. Treasury yields steadied at the end of a quarter of wild swings. Investors have struggled to adjust for banking collapses and the shifting outlook for interest rates amid high inflation and threats to economic growth. The two-year yield was around 4.13% Friday while the 10-year maturity was about 3.55%.

Among notable premarket movers, Nikola Corp. dropped 8.6% after a $100 million share offering priced at a 20% discount to the stock’s last close. Digital World Acquisition Corp., the special-purpose acquisition company merging with Trump Media, rallied as much as 16% following former President Donald Trump’s indictment. Virgin Orbit shares slump a record 40% after the satellite launch provider said it’s ceasing operations indefinitely. Here are the other notable premarket movers:

- Digital World Acquisition, the blank-check firm taking Trump Media public, rallied 8% in premarket trading, advancing along with other stocks tied to Donald Trump after the indictment of the former president. Phunware , a software firm that worked on Trump’s reelection campaign, rose 2.5%, while video platform Rumble gained 14%.

- Advance Auto Parts upgraded to equal-weight at Barclays, which says that rather than a positive call it is based on significant year-to-date underperformance. The stock gains 1.1%.

- Alphabet Inc.’s price target is lowered to $117 from $120 at Piper Sandler, which cites concerns about competition in artificial intelligence technology.

- Blackberry shares drop 3.8% after the cybersecurity company’s fourth- quarter revenue missed analyst estimates, with brokers flagging the impact of some large government deals slipping, as well as needing more convincing that important metrics were recovering.

- Generac shares are down 3% after BofA Global Research downgrades the generator company to underperform from neutral.

- IonQ shares are up more than 4% after the quantum-computing company reported fourth-quarter results that beat expectations and gave a full-year revenue forecast that was ahead of the consensus estimate.

US stocks have experienced a big sector rotation this month with technology stocks rallying amid bets of lower interest rates, while economically-linked cyclical sectors lagged behind following their outperformance at the start of the year. The Nasdaq 100 is up nearly 19% in the first quarter, its best January-March performance since 2012. That rotation prompted momentum-chasing penguins, pardon strategists at Citigroup to upgrade US stocks to overweight from underweight, saying they “perform more defensively than other markets” during earnings recessions.

Michael Hewson, chief market analyst at CMC Markets UK, said US stock markets “have undergone a bit of a crisis of confidence with concern about the effects of much higher rates giving way to concern about the health of the US banking system.”

On the outlook for rates, all eyes Friday are on the so-called PCE Core Deflator, which is expected to show a slight easing of price pressures in February, though it should still be well above target. A round of Fed speakers on Thursday suggested more monetary tightening was necessary to quell inflation, even after the collapse of three US banks this month.

“The Fed’s preferred measure of inflation could generate some volatility within the fixed income markets if we see any surprises,” economists at Rand Merchant Bank in Johannesburg wrote in a note. “Risks are tilted to the upside, and if the data shows that inflation pressures remained strong in February, the inversion of the US yield could deepen even further.”

Traders will also be on guard for any choppiness amid quarter-end rebalancing from pension funds and options hedging activity, especially the famous JPM collar which has a 4065 strike. And they continue to debate the extent to which policy makers may cut interest rates this year. Several strategists have said markets are wrong to expect easing by the Fed this this year as the labor market remains robust, though US unemployment claims ticked up for the first time in three weeks.

European stocks are ahead with the Stoxx 600 up 0.3% and on course for a third day of gains. Personal care, retailers and consumer products are the strongest-performing sectors while miners and banks fall. Here are some notable premarket movers:

- Air France-KLM rises as much as 4.5%, IAG 3.2%, Lufthansa 3.3% and EasyJet 3.8% following bullish notes on the sector from Deutsche Bank and Barclays and a slew of upgrades

- Ocado gains as much as 7.9%, while AutoStore falls as much as 12% after a UK court invalidated the two remaining patent lawsuits the Norwegian firm had filed against Ocado

- SAF-Holland rises as much as 7.6%, extending gains following Thursday morning’s results, as Hauck & Aufhaeuser lifts its PT to a new Street high

- CD Projekt soars as much as 9.8% after posting the second-highest quarterly earnings fueled by stronger sales of Cyberpunk 2077 and Witcher 3 games

- Getin Holding soars as much as 27% after the company proposes a record dividend of 0.58 zloty per share, its first payout since 2013

- Computacenter shares gain as much as 3.2% on Friday after the IT reseller posted better-than-expected results, saying demand from most of its largest customers remains solid

- Torm rises as much as 9.6% after holder OCM Njord Holdings Sarl terminated a planned secondary public offering of 5 million class A shares in the Danish tanker operator

- Marston’s shares rise as much as 5.3%, with analysts saying the pub operator’s amendment and extension of its debt facilities should provide some relief for investors

- Jungheinrich shares slide as much as 9.2% after the forklifts and stackers manufacturer’s cautious outlook for 2023 overshadowed a strong end to 2022

- EMIS shares plunged as much as 24% after Britain’s competition regulator said it would investigate UnitedHealth’s deal to acquire the health-technology company

Earlier in the session, Asian stocks headed for a fourth day of gains as data showed China’s economy gained momentum in March, while concerns about global banking turmoil and elevated interest rates eased. The MSCI Asia Pacific Index rose as much as 1.1%, set to cap a second-straight weekly gain, boosted by consumer discretionary and materials shares. Most regional markets gained, led by Japan, South Korea and Hong Kong. Indian shares jumped after returning from a holiday. Chinese stocks got a boost after a report that manufacturing continued to expand amid a strong pickup in services activity and construction. The report offered investors more confidence about an economic rebound after stringent Covid restrictions were dropped. Spinoff plans for JD.com and Alibaba units also lifted sentiment for tech shares. Read: China’s Strong PMIs Show Economic Recovery Gaining Traction The latest data “confirms the early cycle economic recovery is on track, paving the way for earning revisions to stabilize and improve from 2Q,” analysts at UBS Global Wealth Management’s chief investment office wrote in a report. “We expect over 20% upside for MSCI China by year-end, with the recent consolidation presenting an attractive entry point.” Globally, concerns over the financial sector continued to cool and investors digested a round of Federal Reserve commentary. Bank of Boston President Susan Collins said the banking system is sound and more interest-rate increases are needed to bring down inflation.

Japanese stocks rebounded, following US peers higher, as concerns over the financial sector continued to cool and investors digested a round of Fed commentary. The Topix Index rose 1% to 2,003.50 as of market close Tokyo time, while the Nikkei advanced 0.9% to 28,041.48. Mitsui & Co. contributed the most to the Topix Index gain, increasing 7.6%. Out of 2,160 stocks in the index, 1,471 rose and 588 fell, while 101 were unchanged. Meanwhile, Japanese semiconductor-related stocks pared earlier gains after Japan said it will tighten chip gear exports to help restrict tech shipments to China. Japan Trading Firms Gain on Reported Plans to Improve Returns “Besides the stabilizing overseas markets, expectations for firm corporate earnings outlooks are also boosting Japanese equities,” said Rina Oshimo, a senior strategist at Okasan Securities. “Japan’s macro economy this year is more resilient than overseas, mainly driven by reopening growth, and the government’s policy for childcare support is also positive material.

Australian stocks also advanced: the S&P/ASX 200 index rose 0.8% to close at 7,177.80, boosted by mining and bank shares. Stocks across Asia advanced with US and European equity futures, underscoring investor optimism in the face of banking turmoil and elevated interest rates. The benchmark snapped seven weeks of losses, rising 3.2% for the week, the most since the week of Nov. 11. The index also posted a second straight quarter of gains. The focus will now be on Australia’s central bank, which is set to make a rate decision Tuesday. The RBA is expected to keep borrowing costs unchanged at next week’s meeting, delivering its first pause since initiating a policy tightening cycle in May 2022. In New Zealand, the S&P/NZX 50 index fell 0.4% to 11,884.50.

India stocks rallied the most in more than four months on Friday bouncing back from their oversold levels to trim losses for the quarter. The S&P BSE Sensex Index rose 1.8% to 58,991.52 in Mumbai, while the NSE Nifty 50 Index advanced 1.6% to 17,359.75. The gauges posted their biggest single-day rallies since Nov. 11, narrowing their losses for the quarter to 3% and 4%, respectively. Even with the gains this week, the indices clocked their worst quarterly performance since June 2022 after scaling to their record peaks in December. Globally tightening monetary conditions and the impact of inflation have dampened the outlook for economic growth and shrunk the valuation gap that India enjoyed over its peers. Foreigners turned buyers of local shares in March after three straight months of outflows, purchasing a net of $1.4b of stocks through March 28, while domestic institutional investors remain supportive of equities. Reliance Industries contributed the most to the Sensex’s advance, increasing 4.3% after the company firmed up its plan for separating its financial services business, a move that will potentially result into value creation for the country’s biggest listed firm. Out of 30 shares in the Sensex index, 26 rose and 4 fell

In FX, the Bloomberg Dollar Spot Index rose 0.2%, boosted by gain versus the yen; the dollar is set to end the quarter 1.4% lower, its first consecutive quarterly loss in more than two years, amid easing concerns about the global banking sector and money market wagers on Federal Reserve interest-rate cuts. USD/JPY rallied as much as 0.8% as Japan’s fiscal year-end flows dominated and haven bids waned amid easing concerns about the global banking sector; International Monetary Fund said the nation’s central bank should avoid a premature exit from monetary easing.

In rates, US 10-year yields are down 2 bps at 3.537% ahead of the core PCE data due later today. Treasury 2-year yields cheaper by ~2bp on the day with 2s10s flatter by 3bp to -61bp from a high of around -50bp Thursday. Bunds outperform little-changed US 10-year by 2bp while gilts lag by 3bp. Earlier, ECB rate-hike premium was unwound slightly after euro-area core inflation accelerated to 5.7% in March, matching the median forecast. IG dollar issuance slate empty so far; a couple of names priced $1.4b Thursday, leaving March total around $100b vs $150b that was expected. Bund futures rallied as traders trimmed ECB rate bets after euro-area inflation slowed more than expected in March, although the core rate did accelerate. German 10-year yields are flat at 2.37% while the Euro is down 0.2% versus the greenback. US economic data slate includes February personal income/spending with PCE deflator (8:30am), March MNI Chicago PMI (9:45am) and March final University of Michigan sentiment (10am).

In commodites, US crude futures are little changed with WTI at $74.35. Spot gold is also flat around $1,980

Looking to the day ahead. We have quite a busy day data wise, with the US PCE deflator data, the March MNI Chicago PMI and the February personal spending and income data. In Europe, we have the Eurozone March CPI data and the February unemployment. We will also see the release of the Italian March CPI and the January industrial index, the German march unemployment change, February retail sales and the import price index, and lastly the French March CPI. February CPI and consumer spending. Finally, we will hear from several central bankers, including the ECB’s Lagarde and Kazaks, as well as the Fed’s Williams, Waller and Cook.

Market Snapshot

- S&P 500 futures little changed at 4,082.00

- MXAP up 0.6% to 161.90

- MXAPJ up 0.5% to 523.44

- Nikkei up 0.9% to 28,041.48

- Topix up 1.0% to 2,003.50

- Hang Seng Index up 0.4% to 20,400.11

- Shanghai Composite up 0.4% to 3,272.86

- Sensex up 1.7% to 58,952.31

- Australia S&P/ASX 200 up 0.8% to 7,177.75

- Kospi up 1.0% to 2,476.86

- STOXX Europe 600 up 0.2% to 455.58

- German 10Y yield little changed at 2.39%

- Euro down 0.3% to $1.0876

- Brent Futures down 0.9% to $78.54/bbl

- Gold spot down 0.3% to $1,975.10

- US Dollar Index up 0.30% to 102.45

Top Overnight News

- Former President Donald Trump faces a set of legal requirements no American leader has had to confront after being indicted by a Manhattan grand jury on Thursday in a probe of hush money payments to a porn star during his 2016 campaign — a historic event in American law and politics that is certain to divide an already polarized society and electorate: BBG

- The BOJ expanded the range of its planned bond purchases next quarter, giving itself the option to dial back buying. It will buy ¥100 billion to ¥500 billion ($750 million to $3.8 billion) of 10-to-25-year bonds per operation, compared with a range of ¥200 billion to ¥400 billion in the first quarter. It also widened the range of purchase amounts for other maturities above one year. BBG

- The China Securities Regulatory Commission last month released long-awaited guidelines that require all mainland Chinese companies planning share sales outside the domestic A-share market to inform the regulator beforehand. That applies to jurisdictions that have been popular venues for Chinese listings, including Hong Kong and the U.S. Companies in some technology fields that haven’t yet generated revenue will be able to explore listings in Hong Kong, after the city’s stock exchange last week finalized a new set of rules known as Chapter 18C. WSJ

- China’s economic recovery gathered pace in March, with gauges for manufacturing, services and construction activity remaining strong, boosting the outlook for growth this year: BBG

- The U.S. and South Korea are both seeking to extradite captured crypto entrepreneur Do Kwon from Montenegro, authorities in the tiny European nation said this week, setting up competing bids to prosecute him over criminal charges tied to the collapse of his TerraUSD stablecoin. WSJ

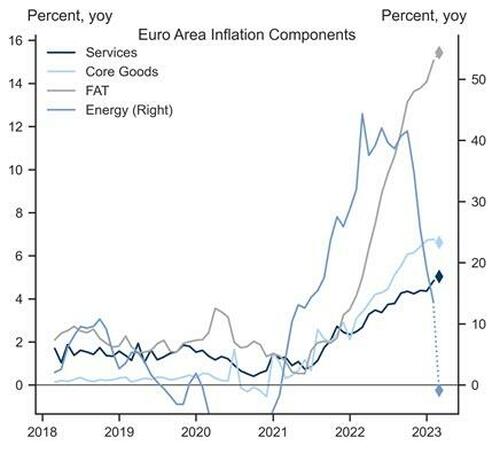

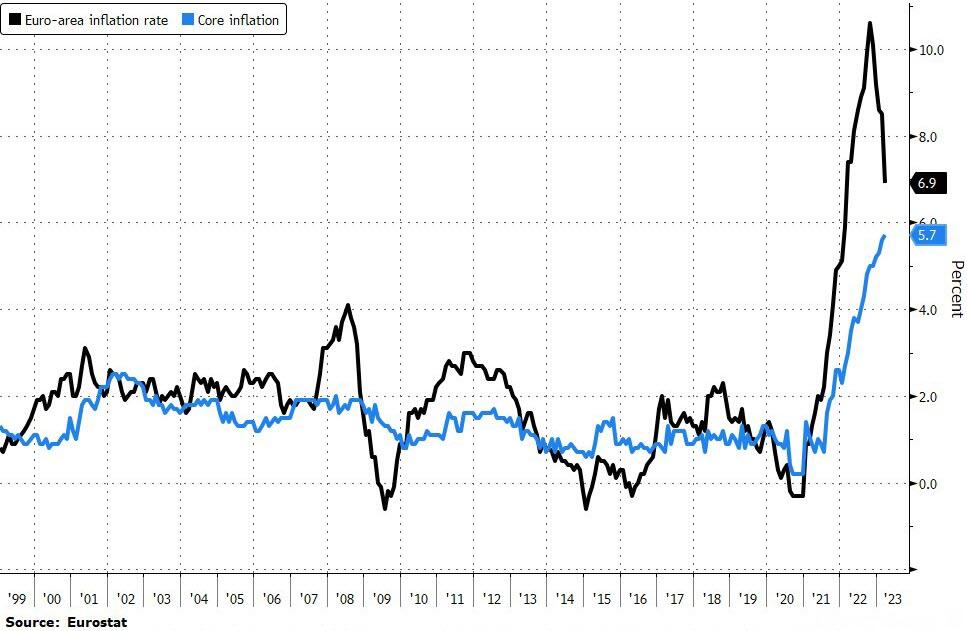

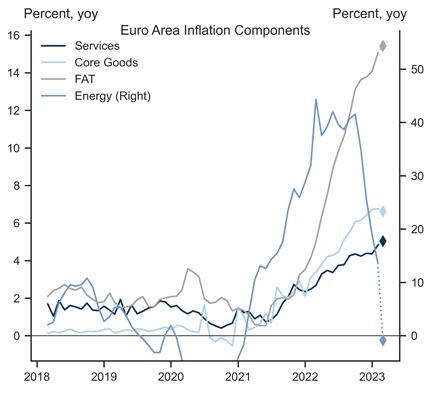

- Eurozone inflation has fallen sharply to its lowest level for a year after a decline in energy costs. Harmonized consumer prices in the euro area rose by 6.9 per cent in the year to March, down from 8.5 per cent the previous month, to reach their lowest level since February 2022. The drop, due to a 0.9 per cent fall in energy prices, was steeper than a forecast by economists polled by Reuters, who had expected March eurozone inflation of 7.1%. FT

- Underlying inflation in the euro area hit a record in March, handing ammunition to European Central Bank officials who say interest-rate increases aren’t over yet: BBG

- Banks reduced their borrowings from two Fed backstop lending facilities in the most recent week, a sign that liquidity demand may be stabilizing. US institutions had a combined $152.6 billion in outstanding borrowings, compared with $163.9 billion the previous week. But US banks are facing a new problem as savers flee for higher deposit rates. BBG

- Finland has cleared the last significant hurdle in its bid to join Nato after Turkey’s parliament approved the Nordic country’s accession to the western military alliance. FT

- Investors are still flooding into cash, with $60.1 billion entering money markets funds in the week through Wednesday, according to EPFR data. That brings the quarterly flow into cash to about $508 billion, the most since the very start of the pandemic. BBG

- A majority of Americans don’t think a college degree is worth the cost, according to a new Wall Street Journal-NORC poll, a new low in confidence in what has long been a hallmark of the American dream. The survey, conducted with NORC at the University of Chicago, a nonpartisan research organization, found that 56% of Americans think earning a four-year degree is a bad bet compared with 42% who retain faith in the credential. WSJ

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly firmer at quarter-end as they took impetus from the tech-led gains on Wall Street and with participants digesting a slew of data releases including better-than-expected Chinese PMI figures. ASX 200 was led by the mining and resources sectors after the strong data from Australia’s largest trading partner although the upside was capped ahead of next week’s RBA meeting with a recent Reuters poll showing near-even expectations amongst economists between a hike and a pause. Nikkei 225 gained heading into the end of the fiscal year and climbed back above the 28,000 level after encouraging Industrial Production and Retail Sales data but was off highs with chipmakers later pressured after Japan announced to impose new restrictions on chip-making gear. Hang Seng and Shanghai Comp. were positive after the strong Chinese PMI data in which Manufacturing PMI topped forecasts and Non-Manufacturing PMI rose to its highest since 2011, with the outperformance in Hong Kong led by tech as JD.com plans to spin off its industrials and property units. However, the gains in the mainland were limited amid a deluge of earnings releases including mixed results from China’s mega-banks and with the nation’s largest property developer Country Garden posting its first annual loss since its listing in 2007.

Top Asian News

- Chinese Vice Finance Minister Zhu said China needs to step up fiscal policy adjustments to support the economy and that China will move steadily in implementing preferential tax and fee policies. Zhu also stated that China will effectively ease tax burdens of small firms and household businesses, while he noted that recently announced preferential tax and fee policies will reduce companies’ burdens by CNY 480bln per year, according to Reuters.

- China’s Ambassador to the EU warned the bloc of ‘peril’ in following the US on trade curbs, while he urged resistance to ‘unwarranted’ pressure and said that Beijing will not be ‘trampled’, according to FT.

- Japan is to impose new restrictions of chip-making gear, according to Bloomberg and Reuters. Japan said it will impose restrictions on 23 types of chip-making equipment from July. Japanese officials said the scope of restrictions went further than the US measures imposed in 2022. Chip-equipment exporters would need licenses for all regions. The measures will affect a broader range of companies than previously expected, according to FT.

- Agricultural Bank of China (1288 HK) says NIM for the banking sector will continue to shrink in Q1; Co. says its NIM faces downward pressure in 2023. Bank of China (3988 HK) CFO says they are to face a mild decline in NIM this year.

- Japan is to end current COVID border measures on May 8th, via TBS; replaced with random genomic surveillance at airports.

European bourses are firmer, Euro Stoxx 50 +0.3%, continuing the positive APAC tone with incremental impetus from as-expected EZ Core HICP. Sectors are mixed with Banks lagging as yields retreat post-HICP while Personal Care/Drug names outperform. Stateside, futures are incrementally in the green with the tone more cautious ahead of PCE data and Fed speak, incl. Williams, thereafter.

Top European News

- UK PM Sunak’s office said Britain will join the Comprehensive and Progressive Agreement for Trans-Pacific Partnership Trans-Pacific after the bloc’s members reached an agreement on Britain joining the trade pact, while Japan’s Economy Minister said they aim for an early signing of UK joining the CPTPP, according to Reuters.

- Sartorius to Buy French Biotech Polyplus for $2.6 Billion

- DSV Slips as JPMorgan Cuts Rating, Prefers Kuehne + Nagel

- Energy Cliff-Edge Threatens Thousands of British Businesses

- German Unemployment Rises More Than Expected on Sluggish Economy

FX

- USD/JPY and Yen crosses still marching higher into month end as importer hedging and buy orders persist, headline pair popped above 133.50 before topping out and DXY holding 102.000+ status as a result.

- Aussie unable to keep hold of 0.6700 handle as AUD/NZD cross retreats through 1.0700 on divergent RBA/RBNZ rate expectations.

- Euro mixed after EZ inflation data showing a softer than forecast headline, but firmer than previous core, EUR/USD sub-1.0900, but EUR/CHF nearer parity than 0.9950.

- Cable unable to hold above 1.2400 irrespective of UK Q4 GDP upgrades as Buck bounces broadly pre-US PCE.

Fixed Income

- EGBs experienced a marked bounce following the EZ inflation measure after dipping on the initial French reading; with the EZ figure showing a larger than expected cooling in the headline while the core measures are stick but were as-expected.

- Specifically, Bunds have been up to a 135.64 peak which saw the associated yield pullback from 2.40% best towards the 2.30% mark.

- USTs and Gilts have been moving in tandem with EGBs; though, USTs are somewhat more cautious ahead of upcoming events with yields slightly firmer as it stands.

- BoJ Q2 Bond Purchase plans; expands range for mid-to-superlong purchases for Q2. Click here for more detail.

Commodities

- WTI and Brent are mixed/flat after settling higher by over USD 1.0bbl on Thursday with the overall tone tentative ahead of the US docket while crude specifically is cognisant of next week’s JMMC.

- Specifically, benchmarks are near-unchanged but at the upper-end of USD 73.77-74.67/bbl and USD 78.54-79.18/bbl parameters.

- Metals hold a slight downward bias in otherwise tentative trade for the space with the USD’s strength capping any potential upside from the somewhat cauutious tone.

Geopolitics

- Japanese Finance Minister Suzuki said Japan is to extend the suspension of its most favoured nation treatment on tariffs for Russia, while it was also reported that Japan banned Russia-bound exports of steel, aluminium and aircraft from April 7th, according to the Ministry of Economy, Trade and Industry cited by Reuters.

- Turkish parliament approved a bill to clear the way for Finland’s NATO accession, according to Reuters.

- Deputy Chairman of the Russian National Security Council says “our army will arrive in Kiev if necessary”.

- Belarusian President Lukashenko warns that the West seeks to invade his country with the aim of “destroying” it; The war is not far from us and there are attempts to drag us into it; return of nuclear weapons is not blackmail but a safeguard. Says, talks to resolve the conflict in Ukraine need to commence now, a ceasefire without pre-conditions should be declared.

- Russia’s Kremlin says Russian President Putin is to hold an “important” meeting of Security Council today; Foreign Ministry Lavrov to present a new concept of Russian foreign policy. Will talk to Belarussian President next week about Lukashenko’s call for immediate peace talks, cContinuation of special military operation is the only way to achieve goals at the moment.

US Event Calendar

- 08:30: Feb. Personal Income, est. 0.2%, prior 0.6%

- Personal Spending, est. 0.3%, prior 1.8%

- Real Personal Spending, est. -0.1%, prior 1.1%

- 08:30: Feb. PCE Deflator MoM, est. 0.3%, prior 0.6%

- Feb. PCE Core Deflator YoY, est. 4.7%, prior 4.7%

- Feb. PCE Deflator YoY, est. 5.1%, prior 5.4%

- Feb. PCE Core Deflator MoM, est. 0.4%, prior 0.6%

- 09:45: March MNI Chicago PMI, est. 43.0, prior 43.6

- 10:00: March U. of Mich. Sentiment, est. 63.2, prior 63.4

- Current Conditions, est. 66.4, prior 66.4

- Expectations, est. 61.4, prior 61.5

- 1 Yr Inflation, est. 3.8%, prior 3.8%

- 5-10 Yr Inflation, est. 2.8%, prior 2.8%

Central Banks

- 15:05: Fed’s Williams Speaks at Housatonic Community College

- 17:45: Fed’s Cook Discusses US Economy and Monetary Policy

- 22:00: Fed’s Waller Discusses the Phillips Curve

DB’s Karthik Nagalingam completes the overnight wrap

For a fourth straight day, market behaviour was rather benign with risk-sentiment remaining positive and volatility ebbing. Equity indices in both the US and Europe rose moderately, while longer-dated sovereign yields in the two regions diverged as inflation data is coming back to the foreground. Hotter-than-expected European inflation led to a selloff in bonds, and today we will get more inflation data from both sides of the pond.

Given the calmer market narrative around the global banking system, focus today will be on the US PCE data. Fed members had an approximation of what PCE would look like given recent CPI and PPI prints when they rose rates 25bps last week but seeing how the underlying components are tracking may force market participants to refocus on pricing pressures. However, the market is likely to look through anything but an extraordinary print, given that the recent banking crisis will not be reflected in the data. Our US economists see a +0.36% advance for core PCE in February (+0.57% in January) and m/m declines for both income (-0.1% vs +0.6% in January) and consumption (-0.6% vs +1.8%).

Ahead of the PCE print there was a bevy of Fed speakers yesterday, all of whom highlighted the fact that inflation remained too hot. Boston Fed President Collins (non-voter), while at a conference in Washington DC said, “Inflation remains too high, and recent indicators reinforce my view that there is more work to do.” Separately, Minneapolis Fed President Kashkari (voter) said that the stresses on the banking sector could last longer than expected, but also said that “the services part of the economy has not yet slowed down and … wage growth is still growing faster than what is consistent with our 2% inflation target.” Lastly, Richmond President Barkin (non-voter) said that “if inflation persists, we can react by raising rates further,” and pointed out that the committee was discussing a 50bp hike just a few weeks ago. He had no stated preference on the size of a future rate hike, but he said that continuing to fight inflation was the priority.

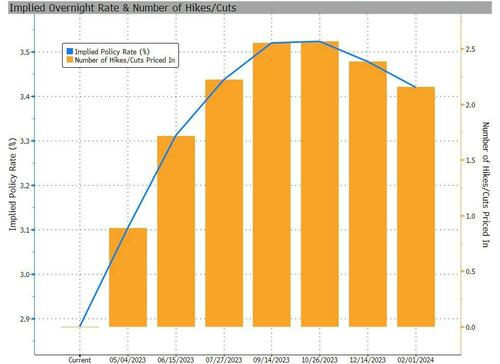

These comments did little to change fed futures yesterday, as the market priced in just an extra +4.0bps for the rate following the December Fed meeting, increasing expectations to 4.387%. That was their highest closing level since March 10 – the day of the collapse of Silicon Valley Bank. The expectations around the May meeting rose marginally, with futures now pricing in a 55% chance of a 25bp hike, up from 47% the day before. While fed speakers don’t seem ready to talk about cutting rates, the market is still pricing in over two 25bps rate cuts by year-end after hitting a terminal rate in May.

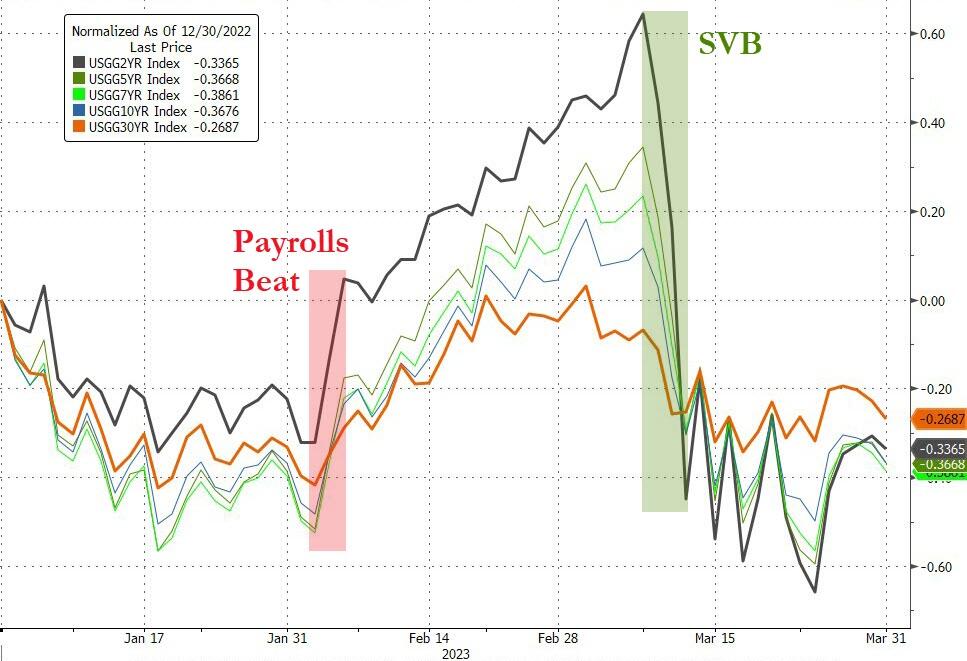

Against this backdrop, the more policy sensitive US 2yr yield was up +2.1bps to 4.12% – returning to roughly where they were before the most recent Fed rate hike on the 21 March. Meanwhile the US 10yr yield fell back -1.5bps after trading in a tight 6bp range all day, although yields have slightly pulled back (+1.51bps) overnight as we go to print. It was a different story in Europe, as 10yr bund yields rose +4.6bps to 2.37% and German 2yrs rose +9.5bps to 2.75%, their highest level since the third week of March. 10yr OATs (+5.2bps) and BTPs (+8.5bps) underperformed, while 10yr gilts yields rose by +4.6bps as well.

As noted above, the selloff in European bonds began after the German inflation print showed an unexpected acceleration in price growth, with German CPI up to +0.8% (vs +0.7% expected) month-on-month, and +7.8% year-on-year (vs +7.5% expected) on the EU-harmonised measure. Eurozone CPI data for March later today will complete the picture, and our European economists expect euro-area EU-harmonised CPI to fall from 8.6% in February to 7.1% year-on-year, but with risks slightly to the upside following the German print. See their note here.

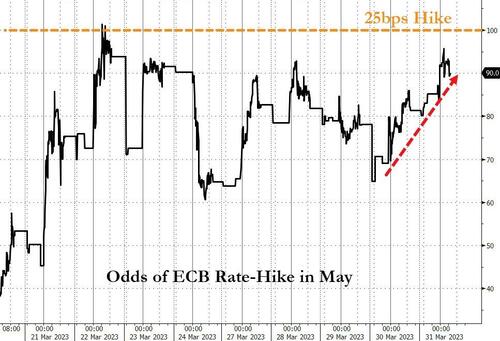

Following the upside surprise on German CPI, the terminal ECB rate priced in by overnight index swaps for the December meeting climbed +10.7bps to 3.44%, pricing in barely any cuts (5bps) by the end of 2023 with the terminal rate expected for October at 3.49%.

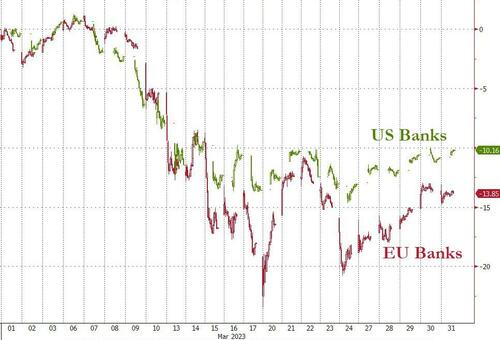

Turning to equities, the S&P 500 was up +0.57% with all but 3 of 24 industry groups gaining on the day. Semiconductors (+1.61%), consumer discretionary retail (+1.21%), and real estate (+1.19%) outperformed. The outperformance of technology continued, leading the NASDAQ (+0.73%) to maintain its trajectory for its best quarter since 2020. The only three S&P 500 industries down on the day were diversified financials (-0.13%), consumer durables (-0.21%) and banks (-1.00%). The underperformance in banks was primarily driven by the regionals with First Republic (-4.0%) the clear laggard, while Fifth Third (-2.6%), Zion (-2.4%), and M&T Bank (-2.3%) were in the next tier of underperformers. The larger banks outperformed with Citi (+0.3%) the only S&P bank constituent higher on the day, while JPM (-0.3%) and BofA (-1.3%) saw smaller losses.

After markets closed, the Fed released their weekly H.4.1 balance sheet data showing how banks were using the Fed’s new bank lending facility and the discount window. Over the prior week, discount window borrowing was down from $110bn to $80bn, there was no further extension of credit to SVB or Signature, and the bank term funding program saw increased borrowing of $64bn from $54bn the week prior. The foreign repo facility, FIMA, saw use fall from $60bn to $55bn. Overall this shows modest improvement across the complex and should add to the narrative that the pain is mostly contained.

In Europe, the STOXX 600 similarly gained on the day (+1.03%), with real estate (+3.74%) as well as information technology (+2.54%) driving performance. Food and Beverage (-0.47%) was the only industry group weaker off the back of the German CPI data, as the finer details of the release showed price inflation for food inched higher. Additionally, unlike in the US, European financials continued to rally back yesterday with as European banks climbed +1.84% and are now up +6.62% on the year. Looking into other bourses, the CAC and the DAX were up +1.06% and +1.26% respectively.

This morning, Asian equity markets have carried over the overnight gains on Wall Street. Across the region, the Hang Seng (+1.46%) is leading gains with the KOSPI (+1.06%), Nikkei (+1.01%), CSI (+0.35%) and the Shanghai Composite (+0.33%) also rising. In overnight trading, US equity futures are pointing to further gains with those on the S&P 500 (+0.28%) and NASDAQ 100 (+0.34%) edging higher.

China equities are outperforming following the official manufacturing PMI beating expectations at 51.9, and the non-manufacturing PMI rising to 58.2 in March. That is the non-manufacturing index’s highest level since May 2011. This data suggests that the economic recovery in the world’s second biggest economy remains on track even amid weaker global demand and a continued property market downturn.

There was also a batch of economic data out of Japan indicating that inflation in Tokyo is still above trend after coming in at +3.3% y/y in March (vs +3.2% expected) compared to +3.4% recorded last month. At the same time, core Tokyo CPI rose +3.2% y/y (vs +3.1% expected) in March, following a peak of +4.3% back in December. So further improvement but not as much as the market was looking for. Labour market conditions loosened slightly as the unemployment rate unexpectedly rose to +2.6% in February from +2.4% in January, while the jobs to applicant ratio moved lower to +1.34 (vs +1.36 expected). Retail sales jumped +1.4% m/m in February, compared to January’s downwardly revised increase of +0.8%. Meanwhile, industrial production rebounded +4.5% m/m in February (vs +2.7% expected) on easing supply bottlenecks for carmakers.

It was a big day for data release yesterday. Starting with the US, weekly jobless claims came in at 198,000 (vs 196,000 expected) suggesting a slight softening in an otherwise tight labour market. Continued claims was lower than expected (1,689k vs 1,700k expected), having remained in a tight range over the past few months now. The third revision to 4Q’22 US GDP saw annualised quarter-over-quarter GDP taken down to 2.6% (2.7% prior) on the back of lower personal consumption (1.0% vs 1.4% prior). 4Q’22 PCE was revised +0.1pp higher to 4.4%.

In Europe, we had several confidence data points for March in the Eurozone demonstrating a slight weakening relative to February. Economic confidence was down to 99.3 (vs 100 expected), industrial confidence became negative at -0.2 (vs 0.5 expected) and services confidence fell a tenth to 9.4 (vs 10 expected). Consumer confidence remained steady at -19.2. This contrasted with the services-driven improvement in the PMIs for March. Looking on the individual country level, the Spanish CPI rose +1.1% month-on-month (vs +1.6% expected) and +3.1% year-on-year (vs +3.7% expected) year-on-year on the EU-harmonised measure. Italian February PPI came in at -1.3% month-on-month, and 10% year-on-year.

Finally on commodities, oil rose sharply again yesterday for its third gain out of the last 4 days, as Bloomberg reported that it is highly unlikely that exports from Iraq will resume this week. Officials from the Kurdistan Regional Government are set to re-enter discussions with Iraqi officials early next week. WTI crude contracts were up +1.92% to $74.37/bbl whilst Brent crude hit $79.27/bbl after climbing +1.26%.

Now to the day ahead. We have quite a busy day data wise, with the US PCE deflator data, the March MNI Chicago PMI and the February personal spending and income data. From the UK we have the March Lloyds business barometer and the Q4 current account balance. In Europe, we have the Eurozone March CPI data and the February unemployment. We will also see the release of the Italian March CPI and the January industrial index, the German march unemployment change, February retail sales and the import price index, and lastly the French March CPI. February CPI and consumer spending. Finally, we will hear from several central bankers, including the ECB’s Lagarde and Kazaks, as well as the Fed’s Williams, Waller and CookAND 2 b) NOW NEWSQUAWK (EUROPE/REPORT)

Chinese PMIs bolstered sentiment, EZ HICP & US PCE ahead – Newsquawk Euro Market Open

FRIDAY, MAR 31, 2023 – 08:46 AM

- APAC stocks were mostly firmer after taking impetus from the tech-led gains on Wall Street and better-than-expected Chinese PMI figures.

- Chinese Manufacturing PMI topped forecasts and Non-Manufacturing PMI rose to its highest since 2011.

- European equity futures are indicative of a marginally higher open with the Euro Stoxx 50 +0.1% after the cash market closed up 1.3% on Thursday.

- DXY is holding above the 102 mark, FX markets are overall relatively contained, NZD marginally outperforms, havens are a touch softer.

- Looking ahead, highlights include German retail sales, UK GDP (Q4), French CPI, Eurozone CPI, German labour market report, Canadian GDP, US PCE and core PCE, Chicago PMI, Uni. of Michigan (Final), Fed’s Collins, Williams, Barkin, Waller, Cook, ECB’s Lagarde.

View the full premarket movers and news report.

Or why not try Newsquawk’s squawk box free for 7 days?

US TRADE

EQUITIES

- US stocks were mostly higher amid continued strength in the tech sector which saw the Nasdaq 100 print fresh YTD highs, while the recent selling pressure in US treasuries further cooled after the mostly weaker-than-expected data releases from the US.

- SPX +0.57% at 4,051, NDX +0.91% at 12,963, DJIA +0.43% at 32,859, RUT -0.18% at 1,768.

- Click here for a detailed summary.

NOTABLE HEADLINES

- Fed’s Kashkari (voter) said they have very high inflation but it is not being driven by wages and that they have to bring down inflation. Kashkari added that once the Fed gets inflation down, they can get back to a pre-COVID economy with low inflation, low unemployment and decent wage growth.

- Fed’s Barkin (non-voter) said deposit flows among US banks are relatively stable and he is encouraged by evidence of resilience, while he added that the Fed will need to stay nimble in weighing the fallout from bank stress against incoming data on inflation. Barkin also stated that he has no view yet on the appropriate rate hike at the next meeting and there is still a lot of data to come before then.

- Fed’s Collins (non-voter) said they likely need to hike rates more with further work needed on inflation and the Fed’s SEP of one more hike seems reasonable. Collins stated tighter credit may offset the need for more rate hikes, while she added the banking system is strong and resilient but likely to pull back on lending which will restrain the economy.

- White House called on US regulators to reverse Trump-era rule changes for large regional banks and urged regulators to accelerate work on expanding long-term debt requirements to a broader set of banks. Furthermore, it stated the costs of replenishing the deposit insurance fund should not be borne by community banks and that proposed reforms can be accomplished under existing law.

- Fed’s Balance Sheet fell to USD 8.765tln (prev. 8.784tln), BTFP lending rose to USD 64.4bln (prev. 53.7bln) and Discount Window borrowing fell to 88.2bln (prev. 110.2bln). In relevant news, ECB tapped Fed Dollar swap lines for USD 487.5mln in the week to March 29th and SNB tapped Dollar swap lines for USD 100mln in the week to March 30th.

- US House Speaker McCarthy said Republicans could act on their own regarding the debt ceiling if US President Biden does not negotiate.