APRIL 3//OPEC+ LOWERS PRODUCTION LEVELS AND THAT SETS OFF GOLD/SILVER ON A ROLLER COASTER RIDE WITH GOLD FINISHING UP $14.20 TO $1983.50//SILVER FINISHED DOWN 14 CENTS TO $23.86//PLATINUM LOWERS IN PRICE BY $4,45 TO $989.95//PALLADIUM WAS UP $19.30 TO $1485.60//COVID UPDATES//VACCINE IMPACT/DR PAUL ALEXANDER//SLAY NEWS/UPDATES UKRAINE VS RUSSIA//SWAMP STORIES FOR YOU TONIGHT///

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2664.15 UP 12.15 CDN dollars per oz (ALL TIME HIGH 2732.50)

BRITISH GOLD: 1597.50 UP 1.50 pounds per oz//(ALL TIME HIGH//1629.84)

EURO GOLD: 1819.15 UP 3.88 euros per oz //(ALL TIME HIGH//1860.82)

COMEX DATA EXCHANGE:

JPMORGAN stopped 1650/16923 contracts

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2023. CONTRACT: 2255 NOTICES FOR 225500 OZ or 7.0139 TONNES

total notices so far: 19,178 contracts for 1,917,800 oz (59.651 tonnes)

SILVER NOTICES: 31 NOTICE(S) FILED FOR 155,000 OZ/

total number of notices filed so far this month : 198 for 990,000 oz

END

GLD

WITH GOLD UP $14.20

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:////// A HUGE WITHDRAWAL OF 1.44TONNES FROM THE GLD.

INVENTORY RESTS AT 928.02 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 14 CENTS

WOW!! WHAT CROOKS:

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF OF 4.779 MILLION OZ FROM THE SLV: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 465.412 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A TINY SIZED 5 TO 121,387 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS GIGANTIC SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.14 GAIN IN SILVER PRICING AT THE COMEX ON FRIDAY. WITH THIS WEEK’S READING AT THE COMEX , WE HAVE NOW SET ANOTHER RECORD LOW AT 117,395 CONTRACTS , MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.14). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A HUGE GAIN ON OUR TWO EXCHANGES 1155CONTRACTS. WE HAD ANOTHER 1000 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 6.0 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS( 1149CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.055 MILLION OZ(FIRST DAY NOTICE)+ THE 6.0 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 7.110 MILLION OZ/ //// V) HUGE SIZED COMEX OI GAIN/ HUGE SIZED EFP ISSUANCE/. WE HAVE NOW REACHED THE POINT THAT THE CROOKS CANNOT LIQUIDATE ANY MORE SILVER SPEC LONGS.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –42 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 1 days, total 1149 contracts: OR 5.745 MILLION OZ . (1149 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 5.745 MILLION OZ

.

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE BUT BELOW LAST MONTH

APRIL 5.745 MILLION OZ

RESULT: WE HAD A TINY SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 5 CONTRACTS WITH OUR $0.14 GAIN IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1149 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 1.055 MILLION OZ//FIRST DAY NOTICE// 55,000 OZ QUEUE JUMP (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 5.0 MILLION NEW EXCHANGE FOR RISK ISSUED EARLY IN APRIL (INCREASES THE AMOUNT OF SILVER STANDING) //NEW STANDING 7.110 MILLION OZ .. WE HAVE A GIGANTIC SIZED GAIN OF 1155 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 31 NOTICE(S) FILED TODAY FOR 155,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GIGANTIC SIZED 18,345 CONTRACTS TO 456,507 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED + 1532 CONTRACTS.

WE HAD A HUGE SIZED DECREASE IN COMEX OI ( 18,345 CONTRACTS) WITH OUR $10.30 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR APR. AT 66.892 TONNES ON FIRST DAY NOTICE // PLUS A 24,400 OZ QUEUE JUMP:(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)YET ALL OF..THIS HAPPENED WITH OUR $10.30 LOSS IN PRICEWITH RESPECT TO FRIDAY’S TRADING.WE HAD A HUGE SIZED LOSS OF 15,659 OI CONTRACTS (48.71 PAPER TONNES) ON OUR TWO EXCHANGES, WITH ALL OF THE LOSS DUE TO THE FINALIZATION OF SPREADER LIQUIDATION.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2686 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 456,507

IN ESSENCE WE HAVE A GIGANTIC SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 15,659 CONTRACTS WITH 18,345 CONTRACTS DECREASED AT THE COMEX AND 2686 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 15,659CONTRACTS OR 48,71 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2686 CONTRACTS) ACCOMPANYING THE GIGANTIC SIZED LOSS IN COMEX OI (15,659) //TOTAL LOSS IN THE TWO EXCHANGES 15,659 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 66.892 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 24,400 OZ//NEW STANDING 67.651 TONNES // ///3) ZERO LONG LIQUIDATION (ALL SPREADERS) //4) HUGE SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

TOTAL EFP CONTRACTS ISSUED: 2656 CONTRACTS OR 265,600 OZ OR 8.2612 TONNES IN 1 TRADING DAY(S) AND THUS AVERAGING: 2656 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1TRADING DAY(S) IN TONNES 8.2612 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 8.2612/3550 x 100% TONNES 0.02% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 8.2612 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A TINY SIZED 5 CONTRACTS OI TO 121,4429 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 1149 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1149 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1149 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 5 CONTRACTS AND ADD TO THE 1149 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE GAIN OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1155 CONTRACTS.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES //5.775 MILLION OZ

OCCURRED WITH OUR $0.14 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

NORTH KOREA/SOUTH KOREA

i)MONDAY MORNING//SUNDAY NIGHT

SHANGHAI CLOSED UP 24.70 PTS OR 0.72% //Hang Sang CLOSED UP 9.07 PTS OR 0.04% /The Nikkei closed UP 146.67 PTS OR 1.52 % //Australia’s all ordinaries CLOSED UP 0.58 % /Chinese yuan (ONSHORE) closed DOWN TO 6.8789 /OFFSHORE CHINESE YUAN UP TO 6.8636 /Oil UP TO 80.04 dollars per barrel for WTI and BRENT AT 84.03/ Stocks in Europe OPENED MOSTLY GREEN// ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GIGANTIC SIZED 18,345 CONTRACTS UP TO 456,507 WITH OUR LOSS IN PRICE OF $10.30 ON FRIDAY, ALL OF THE LOSS BEING FROM SPREADER LIQUIDATION.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF APRIL… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2686 EFP CONTRACTS WERE ISSUED: : APRIL 2686 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2686 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GIGANTIC TOTAL OF 15,659 CONTRACTS IN THAT 2686 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GIGANTIC SIZED LOSS OF 18,345 COMEX CONTRACTS..AND THIS HUGE SIZED LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $10.30 WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: APRIL (67.654) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 67.654 tonnes

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $10.30 //// AND WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD OUR HUGE SIZED LOSS OF 15,659 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE LOST A TOTAL OI OF 48.71 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL. (66.892 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 24,500 OZ… ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $12.25

WE HAD -1532 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 15,659 CONTRACTS OR 1,565,900 OZ OR 48.71 TONNES. ALL OF THIS HUGE LOSS WAS DUE TO FINALIZATION OF SPREADER LIQUIDATION

Total monthly oz gold served (contracts) so far this month

19,178 notices 1,917,800 OZ 59.651 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: NIL oz

customer withdrawals: 0

total withdrawals: NIL oz

in tonnes:0.

Adjustments; 1

Out of JPMorgan: 578,710.938 customer to dealer

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of APRIL we have an oi of 4827 contracts having LOST 16,678 contracts.

We had 16,923 contracts filed on Friday, so we gained 245 contracts or 24500 oz (0.7620 tonnes)

May LOST 38 contracts to stand at 1539

JUNE LOST 2843 contracts to 390,875

We had 2255 notice(s) filed today for 225,500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 2412 notices were issued from their client or customer account. The total of all issuance by all participants equate to 2255 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1650 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2023. contract month,

we take the total number of notices filed so far for the month (19,178 x 100 oz ), to which we add the difference between the open interest for the front month of (APRIL. 4828 CONTRACTS) minus the number of notices served upon today 2255 x 100 oz per contract equals 2,175,100 OZ OR 67.654 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month:No of notices filed so far (19,178 x 100 oz+ 4827 OI for the front month minus the number of notices served upon today (16,923)x 100 oz} which equals 2,175,100 oz standing OR 67.654 TONNES in this active delivery month of APRIL..

TOTAL COMEX GOLD STANDING: 67.654 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

total pledged gold: 1,643,341.368 OZ 51.114 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,291,699.603 OZ

TOTAL REGISTERED GOLD: 12,097,362.125 (376,27 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 9,773,054.363 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,454,021 OZ (REG GOLD- PLEDGED GOLD) 325.16 tonnes//

END

SILVER/COMEX

APRIL 1/2023// THE APRIL 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

822,057.745oz Brinks

JPMorgan Loomis

.

Deposits to the Dealer Inventory

nil

Deposits to the Customer Inventory

1045.400 oz JPMorgan

No of oz served today (contracts)

31 CONTRACT(S) (155,000 OZ)

No of oz to be served (notices)

24 contracts (120,000 oz)

Total monthly oz silver served (contracts)

198 Contracts (990,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

Total deposits: nil oz

JPMorgan has a total silver weight: 144.828 million oz/278,057 million =52,15% of comex .//dropping fast

Comex withdrawals: 3

i)Out of Brinks 198,506.420 oz

ii) Out of Loomis 468,108.01

iii) Out of JPMorgan: 155,442.02 oz

Total withdrawals; 822,057.45 oz

adjustments: 3

Brinks 169,641,100 oz

Int Delaware: 67,641.810 oz

Loomis 85,293,700 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 35.809 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 279.086 million oz

CALCULATION OF SILVER OZ STANDING FOR MAR

silver open interest data:

FRONT MONTH OF APRIL /2023 OI: 55 CONTRACTS HAVING LOST 156 CONTRACT(S. WE HAD 167 NOTICES FILED ON FRIDAY SO WE GAINED 11 CONTRACTS OR AN ADDITIONAL 55,000 OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF APRIL.

MAY SAW A LOSS OF 1099 CONTRACTS DOWN TO 89,957.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 31 for 155,000 oz

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 198 x 5,000 oz = 990,000 oz

to which we add the difference between the open interest for the front month of APRIL(55) and the number of notices served upon today 31 X (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL/2023 contract month: 198(notices served so far) x 5000 oz + OI for the front month of MAR (55) – number of notices served upon today (31 )x 500 oz of silver standing for the APRIL. contract month equates 1.110 million oz +the NEW 1.0 million oz of exchange for risk//NEW EXCHANGE FOR RISK NOW TOTALS 6.0 MILLION OZ //new total standing 7.110 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

APRIL 3/WITH GOLD UP $14.20 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.02 TONNES

MARCH 31/WITH GOLD DOWN $10.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD////INVENTORY RESTS AT 928.02 TONNES

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

MARCH 15/THE IDES OF MARCH: WITH GOLD UP $18.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 913.27 TONNES

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

FEB 28/WITH GOLD UP $12.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 917.61 TONNES

FEB 27/WITH GOLD UP $6.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.32 TONNES

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917.32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

GLD INVENTORY: 928.02 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 1/WITH SILVER DOWN 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.412

MARCH 31/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD/: A MASSIVE 4.779 MILLION OZ DEPOSITED INTO THE SLV///INVENTORY RESTS AT465.412 MILLION OZ

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

MARCH 17/WITH SILVER UP 79 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 10.478 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 462.748 MILLION OZ//

MARCH 16/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 5.009 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 473.226 MILLION OZ//

MARCH 15/WITH SILVER DOWN 7 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 643,000 OZ INTO THE SLV//INVENTORY RESTS AT 478.235 MILLION OZ/

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWALOF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

FEB 28/WITH SILVER UP 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.241 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.188

FEB 27/WITH SILVER DOWN 15 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.471 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 482.429 MILLION OZ

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 465.412 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

nd

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards/John Rubino

3,Chris Powell of GATA provides to us very important physical commentaries

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

END

5.IMPORTANT COMMENTARIES ON COMMODITIES: LITHIUM

END

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 6.8789

OFFSHORE YUAN: 6.8636

SHANGHAI CLOSED UP 24.70 PTS OR 0.72%

HANG SANG CLOSED UP 9.07 PTS OR 0.04%

2. Nikkei closed UP 146.67 PTS OR 0.52%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 101.90 EURO RISES TO 1.0885 UP 5 2BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.377 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 132.36/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN-// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.2135 ***/Italian 10 Yr bond yield FALLS to 4,093*** /SPAIN 10 YR BOND YIELD FALLS TO 3.267…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.148

3j Gold at $1985.50 silver at: 23.98 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 10/100 roubles/dollar; ROUBLE AT 78,71//

3m oil into the 80 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 132.36 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .377% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9143 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9945 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.415 DOWN 8 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.652 DOWN 4 BASIS PTS/

USA 2 YR BOND YIELD: 4.1389 UP 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.20…

GREAT BRITAIN/10 YEAR YIELD: DOWN 5 BASIS PTS AT 3.4355

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Oil Soars, Futures Flat After Shock OPEC Output Cut

MONDAY, APR 03, 2023 – 03:10 PM

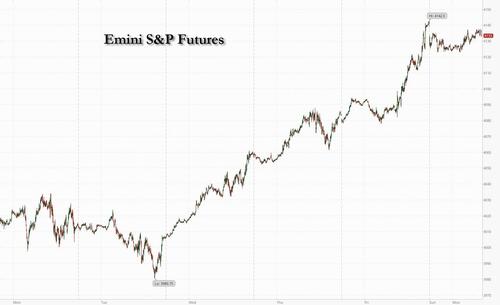

Last week’s torried rally in US equities hit the brakes on Monday as investors digested the shocking move by OPEC+ to cut oil production by a total of 1.66 million barrels a day. S&P futures were lower by 0.1% following a 3.5% gain last week, while Nasdaq 100 contracts – which entered a bull market last week – lose 0.6% as Tesla shares fell in the premarket after 1Q deliveries fell short of expectations. Spot gold falls 0.2% to $1,964. Bitcoin rises 0.9%.

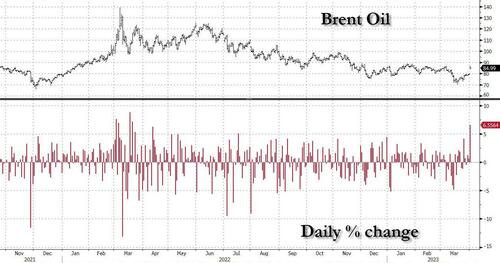

Brent crude headed for the biggest gain since April 2022 while West Texas Intermediate was poised for the best day since May. The Organization of Petroleum Exporting Countries and allies including Russia pledged on Sunday to make the cuts from next month that will exceed 1 million barrels a day, with Saudi Arabia leading the way with 500,000 barrels. Brent crude futures are up 5.3% at around $84.15, the biggest one-day gain in almost a year, while WTI adds 5.5% to trade near $79.80 lifting energy stocks: Chevron and Exxon Mobil rallied in premarket trading.

In other notable premarket moves, Tesla slipped after the electric-carmaker’s first-quarter deliveries fell short of the pace required to meet Elon Musk’s long-held goal of 50% annual growth. World Wrestling Entertainment shares fell after Bloomberg News reported that entertainment conglomerate Endeavor Group Holdings Inc. is near a deal to acquire the wrestling company for about $9 billion. Here are the other notable premarket movers:

Apellis Pharmaceuticals (APLS) rose 17% after the biotech firm drew takeover interest from larger drugmakers. The company is speaking to advisers to consider its options amid the interest, according to a Bloomberg News report citing people familiar.

Energy stocks rallied in premarket trading as the price of oil jumped following OPEC+’s announcement of a surprise production cut. Chevron (CVX US) +4.4%, Exxon (XOM US) +4.3%, ConocoPhillips (COP US) +5%, Marathon Oil (MRO US) +7%; oil-field services provider Schlumberger (SLB US) +4.6%, Halliburton (HAL US) +4.9%.

Intel Corp. (INTC) is upgraded to market perform from underperform at Bernstein, which writes that things may be starting to turn around for the chipmaker. Shares little changed premarket.

Micron (MU) shares were set to extend losses after Beijing launched a cybersecurity review of imports from the largest US memory-chip maker, escalating a semiconductor battle between the two countries. Morgan Stanley, however, said there shouldn’t be any near-term impact.

Shares of US-listed casino operators that operate in Macau surge in premarket trading, after data showed that the city’s gaming revenue soared 247% in March, buoyed by a return of tourists from mainland China as Covid restrictions ease.

Monday’s market moves presented a contrast to a consensus view that drove up asset prices at the end of the first quarter, when Treasuries and stocks rallied amid expectations the banking turmoil in rich nations will encourage the Fed to pause interest-rate hikes and opt for a cut later this year. Those bets were now being revised: Money markets raised the probability of a quarter-point interest-rate hike in May to 65% from 55% seen earlier.

“The impact of this will feed into inflation data globally and means that inflation may take longer to return to target,” said Mark Dowding, the chief investment officer at BlueBay Asset Management. “This will mean that interest rates, once they peak, will need to stay at higher levels for longer.”

Inflation “just doesn’t go away,” said Marija Veitmane, senior multi-asset strategist at State Street Global Markets. “We have a strong labor market, a consumer who can spend, and now oil prices are coming up. It’s increasingly challenging for central banks,” she said in an interview with Bloomberg Television. “Equities are really at risk because inflation fighting is not over. The Fed needs to get aggressive and keep policy tight, and that will crater earnings.”

Meanwhile, Morgan Stanley’s Michael Wilson who has become a bearish broken record, warned the rally in tech stocks that has exceeded 20% isn’t sustainable and that the sector will return to new lows. Wilson said the rotation into tech is taking place partly because it’s being viewed as a traditional defensive sector, though he disagrees with that thesis and sees utilities, staples and health care as having the better risk-reward profile.

Outside of the energy sector, however, the equity-market sentiment was muted. Europe’s Stoxx 600 index was little changed as 14 0f its 20 subgroups posted losses. Energy stocks outperformed and helped push the major European equity benchmarks higher with the Stoxx 50 rising 0.2% and the FTSE 100 up 0.7%. Here are the notable premarket movers:

Siemens Energy rises as much as 6.6% after being rated overweight at Morgan Stanley, which sees significant upside for the gas turbines and wind energy group

Burford Capital shares rise as much as 42% in London, after the litigation financing firm got a boost in its bet on a lawsuit involving Argentinian oil company YPF

European energy stocks outperform Monday, after an unexpected crude output cut from OPEC+ sent crude futures soaring

Hennes & Mauritz shares rise as much as 1.8%, after Credit Suisse upgrades the clothing retailer to neutral from underperform

Industrials REIT shares jump as much as 39%, after Blackstone agrees the key financial terms of a final proposal for a possible cash offer at 168p/ share

Anglo American fluctuates between gains of 2.1% and 0.6% decline after Barclays upgrades the miner to overweight from equal-weight, citing a pullback in shares

Oil tanker company shares extend declines, after a shock OPEC+ output cut sent crude futures soaring as much as 8%, delivering a fresh jolt to the world economy.

“We’re now probably about to enter a very short-term down leg again,” Paul Gambles, MBMG Group co-founder and managing partner, said on Bloomberg Television. “We’ve had a year of pretty irresponsible policy guides and all the damage that they’ve done is now starting to show up.”

Earlier in the session, Asian stocks dropped as a surprise announcement by OPEC+ to cut crude outputs sparked concerns over further inflation risks. The MSCI Asia Pacific Index fell as much as 0.4%, dragged by tech stocks. Energy shares were the biggest gainers on the regional gauge. Benchmarks in Japan, mainland China, Australia and Singapore rose while those in South Korea fell. The unexpected production cut by OPEC+ overshadowed Friday’s data that indicated US inflation was cooling, which may cloud outlook on the Fed’s rate hike path. Asian stocks are still relatively well-positioned to weather any shocks compared to other markets due to their high growth potential and as the Fed is seen to near the peak of its hiking cycle, according to strategists. “Asia ex Japan, the one region where we see growth strong and accelerating this year, should be a relative outperformer,” Morgan Stanley strategist Andrew Sheets said in a report. The bank remains cautious on global equities as “a sharp slowing of a previously strong economy has repeatedly been poor for stocks relative to high grade bonds.” Asian stocks gained in the past two weeks, rising about 4% from its mid-March low, as concerns over a banking crisis eased. The main Asian stock gauge is still about 5% below its late-January high.

Japanese stocks climbed, as investors looked to cooling US inflation data and as OPEC+ cut its oil production, weakening the yen. The Topix Index rose 0.7% to 2,017.68 as of market close Tokyo time, while the Nikkei 225 advanced 0.5% to 28,188.15. Toyota Motor contributed the most to the Topix gain, increasing 0.9%. Out of 2,160 stocks in the index, 1,648 rose and 445 fell, while 67 were unchanged. “The PCE seems to have calmed down and is well received in the markets.” said Masahiro Ichikawa, chief market strategist at Sumitomo Mitsui DS Asset Management. “Mining and petroleum are rising due to high crude oil prices, but caution is required as it may lead to high resource costs.”

The commodity-heavy Australian market rose with the S&P/ASX 200 index up 0.6% to close at 7,223.00, extending gains for a sixth day, boosted by a rally in energy stocks. Oil shares jumped after OPEC+ announced a surprise oil production cut of more than 1 million barrels a day. On Tuesday, Australia’s central bank will deliver a rate decision. Economists are divided over whether the Reserve Bank of Australia will raise interest rates for an 11th consecutive meeting or pause its most aggressive tightening cycle since 1989 amid cooling economic momentum.

In FX, commodity related currencies also received a boost with the Norwegian krone and Aussie dollar the best performers among the G-10’s while the Canadian dollar climbed to a five-week high versus the greenback. The Bloomberg Dollar Index was up earlier after rising oil prices worsened jitters around US inflation, but later turned negative.

In rates, treasuries remained cheaper across the curve after yields gapped higher at the open as oil surged on OPEC+ group’s surprise plan to cut production. US two-year yields have added 8bps to 4.10% as traders bet higher oil prices will have implications for inflation and monetary policy. Monday’s losses unwind a portion of last week’s steep gains into quarter-end. Yields are higher by 5bp to 3bp across the curve with front-end-led losses flattening 2s10s, 5s30s spreads by ~2bp and ~1bp on the day; 10-year around 3.50% underperforms bunds and gilts by 1.5bp and 2bp in the sector. Money markets raised the odds on a quarter-point interest-rate hike from the Federal Reserve in May to 65% from 55%, while a half-point of subsequent easing remained priced by year-end.

In commodities, oil prices are sharply higher following the surprise move by OPEC+ to cut production. Brent crude futures are up 5.3% at around $84.15 while WTI adds 5.5% to trade near $79.80. WTI crude futures pared an 8% earlier advance to around 6%, while Fed rate-hike premium has increased slightly for the May policy announcement.

Looking at today’s calendar, US economic data slate includes March S&P Global US manufacturing PMI (9:45am), February construction spending and March ISM manufacturing (10am); week also includes durable goods orders, JOLTS, ISM services and March.

Market Snapshot

S&P 500 futures down 0.2% to 4,128.00

MXAP little changed at 161.99

MXAPJ down 0.3% to 522.58

Nikkei up 0.5% to 28,188.15

Topix up 0.7% to 2,017.68

Hang Seng Index little changed at 20,409.18

Shanghai Composite up 0.7% to 3,296.40

Sensex down 0.1% to 58,924.87

Australia S&P/ASX 200 up 0.6% to 7,223.02

Kospi down 0.2% to 2,472.34

STOXX Europe 600 little changed at 458.01

German 10Y yield little changed at 2.36%

Euro little changed at $1.0838

Brent Futures up 5.2% to $84.07/bbl

Gold spot down 0.3% to $1,963.28

U.S. Dollar Index up 0.20% to 102.72

Top overnight News

The China reopening effect that’s been highly anticipated — and at times, perhaps dangerously so — around the world is starting to emerge. Some promising readings in the forward-looking purchasing managers’ indexes show that factory managers are seeing a healthy flow of orders ahead, and putting the quirks of the Lunar New Year season behind them. BBG

Macau’s casinos had their best month since the earliest days of the pandemic, with gaming revenue surging 247% in March after Chinese tourists flocked to the gambling hub as the end of Covid Zero sparks a travel boom. BBG

China’s biggest banks say they have escaped unscathed from the financial crisis in the US and Europe, following the collapse of Silicon Valley Bank and Credit Suisse. China’s top lenders — Industrial and Commercial Bank of China, China Construction Bank, Agricultural Bank of China and Bank of China — have all reported there was no direct damage to their books from last month’s emergency rescue of Credit Suisse by UBS and failures in the US banking sector. FT

Chinese authorities warned the nation’s top banking executives that the crackdown on the $60 trillion industry is far from over in a private meeting late Friday, just as they were about to announce the probe of the most senior state banker in nearly two decades. BBG

OPEC+ on Sunday announced a surprise cut to production of >1M BPD, with Saudi Arabia accounting for ~500K of the reduction (while Russia said the previously announced production cut it planned to implement from March to June would continue until the end of 2023). BBG

Switzerland’s Federal Prosecutor has opened an investigation into the state-backed takeover of Credit Suisse by UBS Group the office of the attorney general said on Sunday. The prosecutor, based in the Swiss capital Bern, is looking into potential breaches of the country’s criminal law by government officials, regulators and executives at the two banks, which agreed on an emergency merger last month to avoid a meltdown in the country’s financial system. RTRS

Banks are still struggling to offload ~$25-30B of “hung” debt related to LBOs, including a large chunk related to Twitter that’s increasingly unattractive. WSJ

Donald Trump will plead not guilty when he appears in a Manhattan court tomorrow to face charges related to alleged hush money payments to porn star Stormy Daniels during the 2016 campaign, his lawyer told CNN. His team may also ask to move the case to the more conservative NY borough of Staten Island out of concern he won’t get a fair trial. He leaves Mar-a-Lago at noon today. BBG

Auto discounts are creeping higher as OEMs work to move inventory amid tightened lending availability owing to Fed rate hikes and March’s regional banking turmoil. FT

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly positive amid strength in the energy sector after oil prices were boosted by a surprise voluntary output cut by OPEC+ members although gains in the broader market were capped heading into this week’s key events and as participants digested a slew of data releases including disappointing Chinese Caixin Manufacturing PMI. ASX 200 was underpinned by the energy-related gains and with money market pricing leaning heavily towards a pause at tomorrow’s RBA meeting, while analysts are near-evenly split between a hike and a pause. Nikkei 225 notched modest gains with upside capped following the mixed Tankan survey in which the large manufacturers’ sentiment index deteriorated for the 5th consecutive quarter and fell to its lowest since December 2020. Hang Seng and Shanghai Comp. were mixed with price action cautious after Chinese Caixin Manufacturing PMI showed activity was flat in March and following a substantial liquidity drain by the PBoC.

Top Asian News

PBoC called for stronger defences against a financial crisis and said that China should accelerate legislation of the Financial Stability Law, as well as improve other legal arrangements to prevent and dispose of financial risks, according to three central bank officials in PBoC-affiliated publication China Finance.

Japanese Foreign Minister Hayashi met with Chinese Foreign Minister Qin and expressed concern regarding the situation in Hong Kong and Xinjiang, while Hayashi raised the issue with Premier Li regarding a detained Japanese national who was trying to promote Japanese investment in China and Hayashi was also reported to have met with Politburo member Wang Yi. Furthermore, Japan urged China to view the Ukraine war from a rule of law perspective and take responsible actions in the UN Security Council, while China pressed Japan to change course on chip export curbs, according to Reuters and FT.

US called for joint G7 action against China’s economic bullying, according to Nikkei.

US lawmakers are to meet with Taiwanese President Tsai, Apple (AAPL) CEO Cook and Disney (DIS) CEO Iger, according to Bloomberg.

Equities are broadly mixed/tentative as markets digest elevated oil prices against the potential inflation/Central Bank implications, Euro Stoxx 50 +0.2%. FTSE 100 +0.7% is the current outperformer given its Energy exposure, with the sector leading the European upside while Travel & Leisure names lag given higher fuel costs. Stateside, futures are softer but similarly tentative with the NQ -0.6% lagging as yields increase ahead of Fed speak and ISM Manufacturing to kick off the shortened week. Switzerland’s Attorney General is to investigate whether the Credit Suisse (CSGN SW) takeover by UBS (UBSN SW) broke Swiss criminal law and is looking into potential breaches by government officials, regulators and bank executives, according to The Guardian. Credit Suisse (CSGN SW) expands its sustainability offering for corporate clients through a new partnership with Act Cleantech Agentur Schweiz, while it was separately reported that UBS (UBS SW) shortlisted four consultants for the Credit Suisse integration and UBS will cut its workforce by between 20%-30% after completing the takeover.

Top European News

Hundreds of UK travellers faced disruptions for the third day at the Port of Dover as ministers insisted that the cause for the Channel crossing delays was not linked to Brexit, according to FT.

ECB’s de Guindos said headline inflation is likely to decline considerably this year but added that underlying inflation dynamics will remain strong, while he noted that feedback between higher profit margins, wages and prices could pose more lasting upside risks to inflation. De Guindos also stated that the ECB is monitoring broad risks across the financial sector and will act to preserve liquidity in the euro area, as well as noted the Euro area banking sector is resilient with strong capital and liquidity conditions although vulnerabilities in the financial system prevail in the non-bank financial sector which grew rapidly and increased its risk-taking during the low interest rate environment, according to Reuters.

ECB’s Panetta said there is a lot of discussion on wage growth and that they are probably paying insufficient attention to the other component of income which is profit.

BoE Chief Economist Pill says inflation is still much too high. UK banking system is strong, via Le Temps.

Italian Economy Minister Giorgetti said forecasts for 2023 are improving and they expect GDP variation in H1 to push overall projections up slightly but warned that higher interest rates intended to curb inflation could pose a threat to growth and said a recession should not be the price paid for fighting inflation via monetary policy, according to Reuters. – Fitch affirmed Germany at AAA; Outlook Stable.

French President Macron and European Commission President von der Leyen are to visit China between April 5th-7th, via Chinese Foreign Ministry

Finland’s opposition right-wing National Coalition Party is on course to win Sunday’s parliamentary election in a tight race with 48 out of 200 seats and the nationalist Finns Party are set to win 46 seats, while PM Marin’s Social Democrats are on track to win 43 seats. Furthermore, the National Coalition leader Orpo said it was a big win and that they will negotiate to form a new coalition government, according to Reuters.

FX

The USD derived initial support from the surprise OPEC+ move, pre-JMMC, which sent the DXY to a 103.06 peak as yields climb; however, it has since waned and is now in proximity to 102.50.

A pullback which has aided peers with petro-FX outperforming, USD/CAD below 1.35, while AUD outperforms and is back above 0.67 ahead of the RBA.

JPY resides at the other end of the spectrum as yield differentials weigh and the Tankan survey provided no support; USD/JPY eclipsed 133.50 from a 132.83 base.

GBP and EUR are near unchanged but well off initial lows as the USD’s strength wanes, with no real/sustained movement on Central Bank speak or final PMIs.

PBoC set USD/CNY mid-point at 6.8805 vs exp. 6.8820 (prev. 6.8717)

Fixed Income

Bonds are pressured by the OPEC+ action and associated inflation/monetary implications, though the complex has since pared much of the decline.

Action which has seen a spike in yields that is more pronounced at the short-end; German and US 10yr yields above 2.35% and 3.53% respectively.

Gilts and the EZ periphery have been moving in tandem with the above that has seen USTs pare to downside of less than 10 ticks ahead of Fed speak and ISM Manufacturing.

Commodities

Crude is bolstered though slightly off best levels after jumping at the resumption of trade following the surprise OPEC+ voluntary production cut.

Specifically, WTI and Brent remain at the top-end of USD 81.69-79.00/bbl and USD 86.44-83.50/bbl today’s parameters and well above Friday’s USD75.72/bbl and USD 79.80/bbl respective bests.

In metals, the complex is mostly lower with pressure stemming from the upside in yields and initial USD strength with the yellow metal moving below the USD 1968/oz 10-DMA.

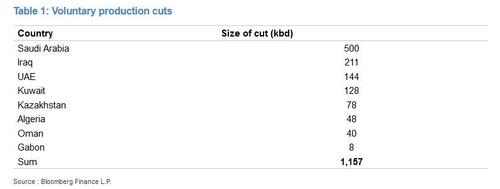

OPEC+ members announced voluntary oil output cuts with Saudi Arabia to reduce production by 500k bpd from May until year-end and Russia will also cut by 500k bpd until year-end as a precautionary measure against further market volatility. Furthermore, Iraq is to lower output by 211k bpd, UAE will cut output by 144k bpd, Kuwait will cut 128k bpd and Oman will reduce output by 40k bpd, according to Reuters. It was also separately reported that more OPEC+ member states are expected to announce voluntary cuts, according to Energy Intel’s Bakr.

Iraq’s oil exports averaged 3.26mln bpd in March (prev. 3.30mln bpd in Feb.), while it was separately reported that Iraq’s government reached an initial deal with KRG to resume northern oil exports this week, according to Reuters.

US National Security Council spokesperson said they do not think OPEC+ production cuts are advisable at this moment given market uncertainty which they have made clear and the Biden administration is focused on prices for US consumers and not barrels, while the Biden administration will continue to work with all producers and consumers to ensure energy markets support economic growth and lower prices for American consumers, according to Reuters.

EU Energy Commissioner Simson said the provision proposed by EU countries allowing a halt of Russian and Belarusian LNG imports is not yet law but is broadly supported and a very concrete step, while she added that the agreement on higher EU renewable targets is an ambitious deal and should help member states to upgrade national energy and climate plans, according to Reuters.

Russia has reportedly moved to Dubai benchmark in recent Indian oil deal for Urals, according to Reuters sources; Rosneft is to sell oil to India at a discount of USD 8-10/bbl to Dubai quotes, and on a delivered basis.

India extended export restrictions on gasoline and diesel as it seeks to ensure the availability of refined fuels for the domestic market, according to Reuters.

Geopolitics

Ukrainian President Zelensky said the military situation is especially hot around the city of Bakhmut in eastern Ukraine, according to Reuters. Furthermore, Ukraine said its army still holds Bakhmut although the founder of Russia’s Wagner Group said the Russian flag was raised over the administration of Bakhmut and that Ukrainian forces remained in western parts of the town.

Ukrainian military spokesperson says Bakhmut area is Ukrainian and Russian forecast are very far from capturing it.

A well-known Russian military blogger was killed and at least 25 people were injured from a bomb blast in a café in St Petersburg, Russia which was formally owned by Wagner Group head Prighozhin, according to BBC.

Russia’s ambassador to Belarus said Russian nuclear weapons in Belarus will be moved to the western borders of the country, according to RIA.

US Secretary of State Blinken held a call with Russian Foreign Minister Lavrov and discussed the arrest of US reporter Gerskovich who was accused of spying. Blinken conveyed US grave concern over the detention and called for an immediate release, while Russia said the reporter was caught red-handed and his fate will be determined by a court. Lavrov also said it was unacceptable for Washington to politicise the case and whip up a stir, according to Reuters.

North Korean leader Kim’s sister said Ukrainian President Zelensky is risking his country and being politically ambitious for wanting nuclear weapons, while she added that Zelensky is wrong to think the US nuclear umbrella could protect Ukraine from Russia, according to KCNA.

US think tank said satellite images show an increasing level of activity at North Korea’s main nuclear site and that it may be close to completing a new reactor, according to NBC News.

US Joint Chiefs of Staff Chair Milley said on Friday that his understanding and analysis of China is that at least their military, and perhaps others, have come to some sort of conclusion that war with the US is inevitable although he reiterated that he doesn’t believe war is inevitable.

Iran claimed it chased off a US spy plane that entered Iranian air space near the Gulf of Oman, according to Tasnim.

Large explosions were reported in Syria’s capital Damascus which state media said were caused by a car bomb around the Mezzah military airport area.

US Event Calendar

09:45: March S&P Global US Manufacturing PM, est. 49.3, prior 49.3

10:00: Feb. Construction Spending MoM, est. 0%, prior -0.1%

10:00: March ISM Manufacturing, est. 47.5, prior 47.7

March Wards Total Vehicle Sales, est. 14.6m, prior 14.9m

DB concludes the overnight wrap

This week marks the start of the second quarter of 2023. Before we dive into this week, we want to highlight the release of our regular performance review for Q1. It’s been a tumultuous start to the year in markets, with substantial volatility in March after the collapse of Silicon Valley Bank led to fears about broader contagion across the banking system. However, despite the recent turmoil and the weakness among bank stocks, financial assets more broadly managed to record some strong gains over the quarter as a whole, with advances for equities, credit, sovereign bonds, EM assets and crypto. The only major exception to that pattern were commodities, with oil prices losing ground in every month of Q1 despite a strong rally last week. The full report can be seen here.

With the calendar flipping over we also want to highlight our how credit has continued to largely fallow our 2023 playbook. Obviously, we did not expect a banking crisis, which has led to €IG underperforming more than we initially expected. However, our views that Europe’s gas premium to the US would recede, that a US recession was not imminent as the monetary policy lag would take longer to play, and that less supply could keep HY & Loans tighter than expected has largely played out. Q1 ended with $IG spreads at 138bps, while $HY spreads were at 455bps. Both levels were within striking distance of our forecast from November; 140bps and 465bps respectively. €IG starts Q2 at 170bps (150bps forecasted), while €HY spreads are up to 481bps (450bps forecasted).

Over the weekend, OPEC+ unexpectedly announced an output cut starting in May that will exceed 1 million barrels a day. Russia has agreed to keep production at their current reduced level, while Saudi Arabia will see the largest cuts, slowing production by 500k barrels a day. The White House came out strongly against the move, due to concerns with consumer prices and the inflationary effects of higher fuel costs. It will take some time to see exactly how much this impacts global prices as demand concerns linger, but this is another potential factor exerting upward pressure on inflation after largely being an ameliorating factors this year. As we note above, oil prices fell every month for the last quarter, leading to the worst Q1 performance since 2020 when global shutdowns throttled demand. Brent crude futures are starting this quarter up +5.60% to $84.24/bbl, with WTI futures up +5.58% to $79.89/bbl after both initially were more than 8% higher at the start of trading.

Looking ahead to this week, the US jobs report on Friday should be the main focus. It will be the last jobs numbers before the next Fed meeting on May 3rd and markets will be looking for signs of cooling in the labour market after 475bps of tightening from the Fed over the last year. The report follows recent strong nonfarm payrolls beats, hotter-than-expected inflation data, and a 25bps Fed hike despite US regional bank concerns. Our US economists expect nonfarm payrolls to gain +250k (vs +311k in February) and both the unemployment rate and hourly earnings growth to remain unchanged (3.6% and +0.2%, respectively). Prior to the Friday’s report, JOLTS (Tuesday) and ADP (Wednesday) data will also be in focus.

Today we will get a sense of how global growth evolved over the course of the month with the release of US ISM manufacturing data later on, followed by services on Wednesday. Coupled with the jobs report, whether the ISM indices also show robust growth, especially in components like employment and prices, will be key to assess economy’s resilience. Still, factors like the recent banking turmoil may not yet feed through to major economic indicators. Our US economists see both gauges declining from February levels (manufacturing 47.1 vs 47.7 and services 54.4 vs 55.1).

In Europe, the key data releases include trade balance (Tuesday), factory orders (Wednesday) and industrial production (Thursday) for Germany, industrial production (Wednesday) and trade balance (Friday) in France as well as retail sales and PMIs for Italy. Our European economists overview what the latest prints on those indicators, among others, say about the European economy here, providing context for this week’s readings. Going forward, they underscore the recent banking stress as a new headwind and see risks as being tilted to the downside.

The major data points out of Asia include the China Caixin PMI data and Japan Tankan indices which we highlight below along with Japanese labour cash earnings and household spending on Friday. Friday’s data are expected to show total cash earnings per worker at 0.9% YoY, up from January’s 0.8%, and real household spending down -0.2% MoM vs 2.7% in January.

Asian equity markets are trading slightly higher, catching up to the late US rally last week and shrugging off the surprise production cut from OPEC+. As I type, the Nikkei (+0.33%), the KOSPI (+0.28%), the CSI (+0.40%) and the Shanghai Composite (+0.15%) are holding on to their opening gains whilst the Hang Seng (-0.27%) is bucking the regional trend. Outside of Asia, US stock futures are trading in the red with those tied to the S&P 500 (-0.33%) and NASDAQ 100 (-0.73%) edging lower after a spree of positive sessions last week. Meanwhile, yields on the 10yr Treasuries (+4.34bps) have risen to 3.51% with the 2yr Treasury yields jumping +7.85bps to 4.10% as fears over inflation are stoked by rising oil prices.

Overnight in Japan, the Tankan manufacturer sentiment index deteriorated to 1.0 in March (3.0 expected; 7.0 last quarter) for its fifth straight quarterly decline and reaching the worst level since December 2020. Meanwhile, the business mood among big non-manufacturers’ improved for a fourth quarter to +20.0 (20.0 expected) from +19.0 in December, as hopes of a recovery in tourism abound after the country reopened its borders.

Elsewhere, China’s Caixin manufacturing PMI for March dropped to 50.0 (51.4 expected) from a eight-month high of 51.6 in February, indicating that growth in the nation’s manufacturing sector remains subdued after an initial post-COVID bounce.

In FX, the euro is down -0.31% to $1.0805, hovering near a one-week low, while the Japanese yen weakened -0.18% to 133.10 per dollar as we go to press.

Now, looking back on last week. On Friday, we had a wave of key economic data, including the key US February Core PCE price index which came in softer than consensus at 0.3% month-on-month (+0.4% expected), down from 0.6%. In year-on-year terms the print was also below expectations, at 5.0% (vs. 5.1% expected). Along the same lines, the University of Michigan’s measure of 1 year inflation expectations came down two tenths to 3.6% (vs 3.8% expected), although 5-to-10-year expectations rose to 2.9% (vs 2.8% expected). We had a similar downside surprise for the March Euro Area CPI release, coming in at 0.9% month-on-month (vs 1.1% expected), and 6.9% year-on-year (vs 7.1% expected), down from 8.5% the previous month.There was little response in the fed futures market following said data releases. The rate priced in for the Fed’s next meeting in May climbed a modest +0.6bps on Friday, and +9.8bps on the week, leaving the market-implied probability of a hike in May at 58%.

With the inflation data clearly softer than anticipated, equity markets finished the week well in the green with the S&P 500 rising +3.48% (+1.44% on Friday), extending its rally for a third consecutive day. US banks have continued to recover from their turmoil in mid-March, with the S&P 500 banks climbing a strong +4.50% week-on-week (+0.93% on Friday) and the KBW index, which captures US regional banks, up +4.60% last week (+0.89% Friday). The NASDAQ closed the week up +3.37% (+1.74% on Friday) after a strong performance by the technology sector, locking in its best quarter since 2020. European equity outperformed, as the STOXX 600 climbed +4.03% week-on-week (+0.66% on Friday).

Although equities were on the up over last week, there was a large sell-off in weekly terms in fixed income as banking sector jitters subsided and risk-on sentiment prevailed. US 10yr Treasury yields rose +9.2bps (-8.1bps on Friday), their largest up move since the last week of February. The sell-off was greater for 2yrs as yields rose +25.9bps week-on-week (-9.4bps on Friday), the greatest gain since September. This story was echoed in Europe, as 10yr bund yields climbed +16.3bps (-8.4bps on Friday) last week in its largest up move since before Christmas. German 2yr yields fell back -6.6bps on Friday, while jumping +29.0bps week-on-week.

Finally in commodities, oil continued rallying on Friday as supply remains constrained as protests in Europe have shut down refineries and an Iraqi-Kurdish-Turkish dispute keeps a key pipeline turned off, with WTI crude (+1.75%) and brent crude (+0.63%) up on Friday to close the week at $75.67/bbl and $79.77/bbl respectively. In week-on-week terms, Brent crude closed up +6.37% and WTI contracts +9.25%. Gas also rallied, as European natural gas futures ended the week up +16.42%, with more than half of these gains occurring on Friday (+9.71%) on reports of cooler weather expected through April and supply risks of their own.

2 b) NOW NEWSQUAWK (EUROPE/REPORT)

Crude outperforms after a surprise OPEC+ cut; US ISM & Bullard due – Newsquawk Euro Market Open

MONDAY, APR 03, 2023 – 08:46 AM

APAC stocks were mostly positive amid strength in the energy sector although gains in the broader market were capped as participants digested disappointing Chinese Caixin Manufacturing PMI.

Crude rose following the surprise voluntary output cuts by OPEC+ members totalling over 1mln bpd from May through to year-end.

Fed’s Waller (Voter) said the recent data is consistent with the idea that inflation can be brought down quickly with relatively little harm to the jobs market.

European equity futures are indicative of a marginally lower open with the Euro Stoxx 50 -0.2% after the cash market closed up 0.7% on Friday.

DXY is firmer vs. peers and on a 103 handle, JPY lags the majors, EUR/USD is sub-1.08.

Looking ahead, highlights include US ISM Manufacturing and Speech from Fed’s Bullard.

Or why not try Newsquawk’s squawk box free for 7 days?

US TRADE

EQUITIES

US stocks and bonds picked up into the close on Friday as month- and quarter-end flows made their mark, while Fed pricing moved marginally more dovish after the February Core PCE data came in below expectations and added weight to the month-end duration bid. Furthermore, the Chicago PMI data saw a surprise rise and the University of Michigan consumer survey was revised lower alongside the short-term inflation expectations (3.6% from 3.8%), although the longer-term measure saw a slight increase (2.9% from 2.8%).

SPX +1.44% at 4,109, NDX +1.68% at 13,181, DJIA +1.26% at 33,274, RUT +1.93% at 1,802.

Fed’s Cook (Voter) said she is weighing implications of stronger momentum in the economy against potential headwinds from recent developments and that US policy outlook must balance data dependence with forward-looking analysis. Cook also said that the appropriate path of Fed policy rate may be lower than otherwise if tighter conditions constrain the economy and noted that recent bank developments may suggest greater headwinds for financial conditions and the economy, while she added that they may have more work to do if data shows continued economic strength and that monetary policy is now in restrictive territory, according to Reuters.

Fed’s Waller (Voter) said the recent data is consistent with the idea that inflation can be brought down quickly with relatively little harm to the jobs market and defeating high inflation could require dramatic actions from the Fed to puncture expectations if people have started to believe that prices will just keep on rising, according to Reuters.

Former US President Trump faces multiple charges on falsifying business records and at least one felony charge in the New York hush money probe, according to sources cited by AP.

Tesla (TSLA) rolled out a record number of new cars in Q1 in which deliveries rose 4% Q/Q to around 422.9k vehicles, according to FT.

CREDIT SUISSE

Switzerland’s Attorney General is to investigate whether the Credit Suisse (CSGN SW) takeover by UBS (UBSN SW) broke Swiss criminal law and is looking into potential breaches by government officials, regulators and bank executives, according to The Guardian.

Credit Suisse (CSGN SW) expands its sustainability offering for corporate clients through a new partnership with Act Cleantech Agentur Schweiz, while it was separately reported that UBS (UBS SW) shortlisted four consultants for the Credit Suisse integration and UBS will cut its workforce by between 20%-30% after completing the takeover.

APAC TRADE

EQUITIES

APAC stocks were mostly positive amid strength in the energy sector after oil prices were boosted by a surprise voluntary output cut by OPEC+ members although gains in the broader market were capped heading into this week’s key events and as participants digested a slew of data releases including disappointing Chinese Caixin Manufacturing PMI.

ASX 200 was underpinned by the energy-related gains and with money market pricing leaning heavily towards a pause at tomorrow’s RBA meeting, while analysts are near-evenly split between a hike and a pause.

Nikkei 225 notched modest gains with upside capped following the mixed Tankan survey in which the large manufacturers’ sentiment index deteriorated for the 5th consecutive quarter and fell to its lowest since December 2020.

Hang Seng and Shanghai Comp. were mixed with price action cautious after Chinese Caixin Manufacturing PMI showed activity was flat in March and following a substantial liquidity drain by the PBoC.

US equity futures (ES -0.3%) lacklustre with markets second-guessing the ramifications of higher oil prices for Fed policy.

European equity futures are indicative of a marginally lower open with the Euro Stoxx 50 -0.2% after the cash market closed up 0.7% on Friday.

FX

DXY was kept afloat against its major peers and sits on a 103 handle amid higher yields as the boost in oil prices stoked inflationary pressures and after some comments from central bank officials including from Fed’s Cook who said they may have more work to do if data shows continued economic strength.

EUR/USD retreated beneath 1.0800 as it lost ground against the buck and with somewhat mixed rhetoric from ECB’s de Guindos that headline inflation is likely to decline considerably but underlying inflation dynamics will remain strong.

GBP/USD extended on Friday’s retreat to sub-1.2300 after a relatively quiet weekend for UK-specific newsflow.

USD/JPY was positive amid widening US-Japan short-end yield differentials and a mixed Tankan survey.

Antipodeans were subdued heading into this week’s central bank policy decisions from both the RBA and RBNZ.

PBoC set USD/CNY mid-point at 6.8805 vs exp. 6.8820 (prev. 6.8717)

FIXED INCOME

10yr UST futures pulled back after last Friday’s gains which were helped by the softer-than-expected PCE data, while the retreat was largely due to the advances in oil prices and their potential to spur inflationary concerns.

Bund futures traded rangebound with prices lacklustre after failing to hold above the 136.00 level.

10yr JGB futures were pressured amid the lack of additional purchases by the BoJ which also widened the ranges of potential buying amounts for this month’s scheduled government bond purchases.

COMMODITIES

Crude futures jumped around 7% at the reopening of futures trading following the surprise voluntary output cuts by OPEC+ members totalling over 1mln bpd from May through to year-end with the bulk of the reduction to come from Saudi Arabia, while Russia’s Deputy PM Novak also announced that their 500k bpd reduction will last to the end of the year.

OPEC+ members announced voluntary oil output cuts with Saudi Arabia to reduce production by 500k bpd from May until year-end and Russia will also cut by 500k bpd until year-end as a precautionary measure against further market volatility. Furthermore, Iraq is to lower output by 211k bpd, UAE will cut output by 144k bpd, Kuwait will cut 128k bpd and Oman will reduce output by 40k bpd, according to Reuters. It was also separately reported that more OPEC+ member states are expected to announce voluntary cuts, according to Energy Intel’s Bakr.

Iraq’s oil exports averaged 3.26mln bpd in March (prev. 3.30mln bpd in Feb.), while it was separately reported that Iraq’s government reached an initial deal with KRG to resume northern oil exports this week, according to Reuters.