April 19/2023 · by harveyorgan · in Uncategorized · Leave a comment·Editi

GOLD PRICE CLOSED: DOWN $12.00, TO $1995.10

SILVER PRICE CLOSED:UP 11 CENTS AT $25.28

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE $1994.70

Silver ACCESS CLOSE: 25.37

Bitcoin morning price:, $29,171 DOWN 1033 Dollars

Bitcoin: afternoon price: $29,317 DOWN 887 dollars

Platinum price closing $1093.20 UP $8.15

Palladium price; $1611.60 DOWN $29.50

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2684.81 DOWN 1.01 CDN dollars per oz (ALL TIME HIGH 2732.50)

BRITISH GOLD: 1603.84 DOWN 10.41 pounds per oz//(ALL TIME HIGH//1629.84)

EURO GOLD: 1820.90 DOWN 6.67 euros per oz //(ALL TIME HIGH//1860.82)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

COMEX DATA EXCHANGE:

COMEX//NOTICES

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: APRIL 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,007.400000000 USD

INTENT DATE: 04/18/2023 DELIVERY DATE: 04/20/2023

FIRM ORG FIRM NAME ISSUED STOPPED

104 C MIZUHO 1

118 C MACQUARIE FUT 46

365 H MAREX CAPITAL M 1

435 H SCOTIA CAPITAL 54

523 H INTERACTIVE BRO 1

624 H BOFA SECURITIES 1

657 C MORGAN STANLEY 2

661 C JP MORGAN 20

732 C RBC CAP MARKETS 1

737 C ADVANTAGE 3

800 C MAREX SPEC 6 9

880 H CITIGROUP 136

905 C ADM 3

TOTAL: 142 142

JPMorgan stopped 20/142 contracts

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2023. CONTRACT: 142 NOTICES FOR 14200 OZ or 0.4416 TONNES

total notices so far: 23,408 contracts for 2,340,800 oz (72.808 tonnes)

SILVER NOTICES: 31 NOTICE(S) FILED FOR 155,000 OZ/

total number of notices filed so far this month : 344 for 1,720,000 oz

END

GLD

WITH GOLD DOWN $12.00

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD://////A WITHDRAWAL OF 0.94 TONNES OF GOLD INTO THE GLD

INVENTORY RESTS AT 924,26 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 11 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV.//: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 465,002 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 510 TO 158,371 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS STRONG SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG $0.18 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.18). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A MONSTER GAIN ON OUR TWO EXCHANGES 1210 CONTRACTS. WE HAD 1000 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 5.0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 25.83 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS( 700 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.055 MILLION OZ(FIRST DAY NOTICE)+ THE 25.83 MILLION OZ OF EXCHANGE FOR RISK/+ 1.825 MILLION OZ NORMAL SILVER STANDING FOR APRIL///THUS TOTAL NEW STANDING 27.655 MILLION OZ/ //// V) VERY STRONG SIZED COMEX OI GAIN/ STRONG SIZED EFP ISSUANCE/.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –369 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL:

TOTAL CONTRACTS for 12 days, total 17,475 contracts: OR 87,375 MILLION OZ . (1456 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 87.375 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE BUT ABOVE LAST MONTH

APRIL 87.375 MILLION OZ

RESULT: WE HAD A VERY STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 510 CONTRACTS WITH OUR $0.18 GAIN IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 700 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 1.055 MILLION OZ//FIRST DAY NOTICE// 170,000 OZ QUEUE JUMP (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 5.0 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //NEW EXCHANGE FOR RISK STANDING 25.83 MILLION OZ, THUS TOTAL SILVER OZ STANDING FOR DELIVERY IN APRIL TOTALS 27.655 MILLION .. WE HAVE A HUGE SIZED GAIN OF 1210 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 31 NOTICE(S) FILED TODAY FOR 155,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 722 CONTRACTS TO 482,254 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED 422 CONTRACTS

this is the 6th day in a row where contracts on the comex were added!!

WE HAD A SMALL SIZED INCREASE IN COMEX OI ( 722 CONTRACTS) WITH OUR $12.15 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR APR. AT 66.892 TONNES ON FIRST DAY NOTICE // PLUS A 500 OZ E.F.P. JUMP TO LONDON:(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)YET ALL OF..THIS HAPPENED WITH OUR $12,15 GAIN IN PRICE WITH RESPECT TO TUESDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 2981 OI CONTRACTS (9.303 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2691 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 481,832

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3413 CONTRACTS WITH 722 CONTRACTS INCREASED AT THE COMEX AND 2691 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3413 CONTRACTS OR 10.615 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2691 CONTRACTS) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (722 //TOTAL GAIN IN THE TWO EXCHANGES 3413 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 66.892 TONNES FOLLOWED BY TODAY’S E.F.P. JUMP OF 500 OZ//NEW STANDING 73.944 TONNES // ///3) ZERO LONG LIQUIDATION//4) SMALL SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 41,416 CONTRACTS OR 4,141,600 OZ OR 128.82 TONNES IN 12 TRADING DAY(S) AND THUS AVERAGING: 3451 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES 128.82 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 128.82/3550 x 100% TONNES 3.21% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 126.82 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A STRONG SIZED 510 CONTRACTS OI TO 158,371 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 700 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 700 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 700 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 879 CONTRACTS AND ADD TO THE 700 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE GAIN OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1210 CONTRACTS.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 6.050 MILLION OZ

OCCURRED DESPITE OUR $0.18 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED DOWN 23.20 PTS OR 0.28% //Hang Seng CLOSED DOWN 282.75 POINTS OR 1.37% /The Nikkei closed DOWN 52.07 PTS OR 0.18% //Australia’s all ordinaries CLOSED UP 0.07 % /Chinese yuan (ONSHORE) closed DOWN TO 6.8876/OFFSHORE CHINESE YUAN DOWN TO 6.8963 /Oil DOWN TO 79.78 dollars per barrel for WTI and BRENT AT 83/53 / Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 722 CONTRACTS DOWN TO 482,254 DESPITE OUR STRONG GAIN IN PRICE OF $12.15 ON TUESDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF APRIL… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2691 EFP CONTRACTS WERE ISSUED: : JUNE 2691 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2691 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3413 CONTRACTS IN THAT 722 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED GAIN OF 722 COMEX CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $12.15. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: APRIL (73.944) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 73.944 tonnes

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $12.15 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR FAIR SIZED GAIN OF 3413 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 10.615 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL. (66.892 TONNES) FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 500 OZ… ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $12.15

WE HAD + ADDED 422 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3413 CONTRACTS OR 341,300 OZ OR 10.615 TONNES.

Estimated gold comex today 216,913 FAIR

final gold volumes/yesterday 170,249 POOR

//APRIL 19/ APRIL 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 321.51 oz 10 kilobars Brinks . |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | NIL OZ |

| No of oz served (contracts) today | 142 notice(s) 14200 OZ 0.4416 TONNES |

| No of oz to be served (notices) | 365 contracts 36,500 oz 1.135 TONNES |

| Total monthly oz gold served (contracts) so far this month | 23,408 notices 2,340,800 OZ 72.808 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: NIL oz

customer withdrawals: 1

i) Out of Brinks: 321.51 oz (10 kilobars)

total withdrawals: 321.51 oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL

For the front month of APRIL we have an oi of 527 contracts having LOST 103 contracts. We had 98 contracts served ON TUESDAY so we LOST 5 contracts or 500 oz will not stand at the comex and these guys were EFP’d to London.

May lost 21 contracts up to 1757.

June GAINED 326 contracts UP to 402,529 contracts.

We had 142 contracts filed for today representing 14,200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 142 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 20 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2023. contract month,

we take the total number of notices filed so far for the month (23,408 x 100 oz ), to which we add the difference between the open interest for the front month of (APRIL. 507 CONTRACTS) minus the number of notices served upon today 142 x 100 oz per contract equals 2,377,300 OZ OR 73.944 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month: No of notices filed so far (23,408 x 100 oz)+ 507 OI for the front month minus the number of notices served upon today (142)x 100 oz} which equals 2,377,300 oz standing OR 73.944 TONNES in this active delivery month of APRIL..

TOTAL COMEX GOLD STANDING: 73.944 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,703,295.912 OZ 52,97 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,943,132.493 OZ

TOTAL REGISTERED GOLD: 12,292,837.996 (382.358 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 9,650,294.497 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,589,542 OZ (REG GOLD- PLEDGED GOLD) 329.379 tonnes//

END

SILVER/COMEX

APRIL 19//2023// THE APRIL 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 261,137.720 oz CNT . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 786,152.915 oz Delaware |

| No of oz served today (contracts) | 31 CONTRACT(S) (255,000 OZ) |

| No of oz to be served (notices) | 21 contracts (105,000 oz) |

| Total monthly oz silver served (contracts) | 344 Contracts (1,720,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i)Into Delaware 786,152.915 oz

Total deposits: 786,152.915 oz

JPMorgan has a total silver weight: 141.154 million oz/273.704 million =51.51% of comex .//dropping fast

Comex withdrawals: 1

i) Out of CNT 261,137.720 oz

Total withdrawals; 261,137.720 oz

adjustments: 1

Int Delaware, dealer to customer: 10,004.790 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 34.048 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 273.704 million oz

CALCULATION OF SILVER OZ STANDING FOR MAR

silver open interest data:

FRONT MONTH OF APRIL /2023 OI: 52 CONTRACTS HAVING GAINED 34 CONTRACT(S). WE HAD 0 NOTICES FILED ON TUESDAY SO WE GAINED 34 CONTRACTS OR AN ADDITIONAL 170,000 OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF APRIL.

MAY SAW A LOSS OF 5631 CONTRACTS DOWN TO 66,264

JUNE HAD A 93 CONTRACTS GAIN TO 248

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 31 for 105,000 oz

Comex volumes// est. volume today 90,083 strong

Comex volume: confirmed yesterday: 64,312 fair

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 344 x 5,000 oz = 1,720,000 oz

to which we add the difference between the open interest for the front month of APRIL(52) and the number of notices served upon today 31 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL/2023 contract month: 344 (notices served so far) x 5000 oz + OI for the front month of APRIL (52) – number of notices served upon today (31 )x 500 oz of silver standing for the APRIL. contract month equates to 1.835 million oz +/ NEW EXCHANGE FOR RISK TODAY: 5.0 MILLION OZ //NEW TOTALS EXCHANGE FOR RISK FOR MONTH OF APRIL: 25.83 MILLION OZ// THUS TOTAL SILVER OZ STANDING: 27.655 MILLION OZ//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

APRIL 19//WITH GOLD DOWN $12.00 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A HUGE WITHDRAWAL OF .94 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 924.26 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

APRIL 10/WITH GOLD DOWN $21.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91 TONNES

APRIL 6//WITH GOLD DOWN $9.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91

APRIL 5//WITH GOLD UP 0 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04

APRIL 4/WITH GOLD UP $36.30 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

APRIL 3/WITH GOLD UP $14.20 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.02 TONNES

MARCH 31/WITH GOLD DOWN $10.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD////INVENTORY RESTS AT 928.02 TONNES

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

MARCH 15/THE IDES OF MARCH: WITH GOLD UP $18.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 913.27 TONNES

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

GLD INVENTORY: 924.26 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 19/WITH SILVER UP 11 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.2021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 10/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 6/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 4.643 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 468.585 MILLION OZ//

APRIL 5/WITH SILVER DOWN 4 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.942 MILLION OZ

APRIL 4/WITH GOLD UP $1.11 TODAY CRIMINAL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.47 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 463,942 MILLION OZ

APRIL 1/WITH SILVER DOWN 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.412

MARCH 31/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD/: A MASSIVE 4.779 MILLION OZ DEPOSITED INTO THE SLV///INVENTORY RESTS AT465.412 MILLION OZ

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

MARCH 17/WITH SILVER UP 79 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 10.478 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 462.748 MILLION OZ//

MARCH 16/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 5.009 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 473.226 MILLION OZ//

MARCH 15/WITH SILVER DOWN 7 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 643,000 OZ INTO THE SLV//INVENTORY RESTS AT 478.235 MILLION OZ/

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWALOF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

CLOSING INVENTORY 465.002 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//

END

3,Chris Powell of GATA provides to us very important physical commentaries

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

END

5.IMPORTANT COMMENTARIES ON COMMODITIES: RICE

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

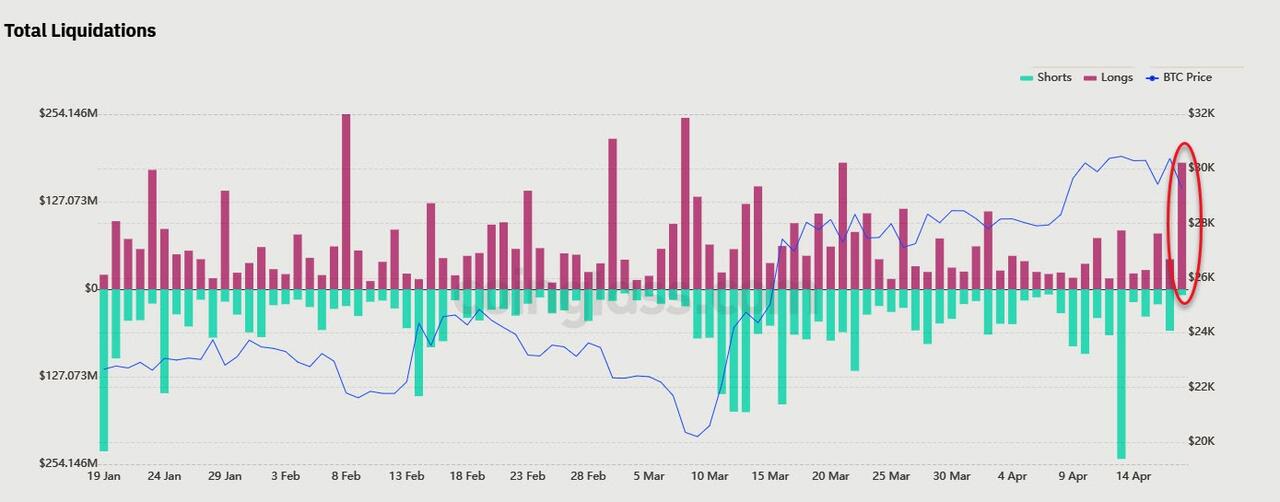

Crypto Crashes Amid Cascade Of Long Liquidations

WEDNESDAY, APR 19, 2023 – 08:12 AM

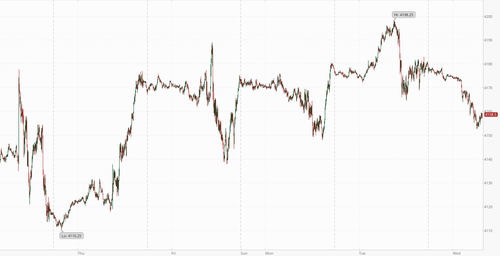

Bitcoin is making headlines this morning after a sudden plunge back to $29,000 as a cascade of long liquidations fueled fresh fears of downside risk.

Source: Bloomberg

The sudden drop followed yesterday’s almost-as-sudden surge back above the $30,000 mark.

“Deep correction on the markets, as Bitcoin can’t hold at $29,700-29,800 and shoots downwards through a cascade of liquidations,“ Michaël van de Poppe, founder and CEO of trading firm Eight, reacted.

As CoinTelegraph reports, hours prior, monitoring resource Material Indicators had flagged changing conditions on the Binance order book, arguing that the result could still swing both ways, with either bulls or bears profiting.

Notably, this was exacerbated by a so-called long-squeeze…

“The hotter-than-expected U.K. CPI may have weighed over risk assets, including BTC. But the gravity of the reaction has been far far more severe than in other asset classes,” Vetle Lunde, a senior analyst at K33 Research, told CoinDesk.

“Seems to be more of a leverage washout. Binance OI in BTCUSDT perps fell 5.1% in 15 minutes, effects more severe in ETH with larger liquidation volume than BTC,” Lunde said, referring to open interest, or the total number of contracts in the futures market.

Equity futures have seen waves of selling pressure overnight too…

Prominent Crypto Twitter trader @52kskew pointed out that a 16,000 bitcoin sell order, worth over $467 million at current prices, preceded the dump, which may have initiated the long squeeze.

“16K BTC is unusual size to be market sold solely from Binance spot usually the kind of sale happens before bad news comes out,” @52kskew opined in a follow-up tweet.

At the time of writing, total crypto long liquidations for April 19 stood at around $185 million on platforms monitored by data resource Coinglass.

In fact, the selling pressure is across all crypto with Ethereum underperforming Bitcoin (after rallying post-Shapella hard-fork)…

Source: Bloomberg

…as ETH liquidations in the last four hours ($38.4mm) topped BTC liquidations in the same period ($28.9mm)…

Finally, we note that options traders have leaned bearish in recent days…

Since April 5, Bitcoin’s put-to-call ratio has been either balanced or favoring protective put options. The current 0.60 indicator slightly shows higher demand for neutral-to-bearish option strategies, although there is nothing out of the ordinary.

Gold has also been hit this morning, back below $2000…

…perhaps lending some credence to this event having been triggered by UK CPI.

1.YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//,WEDNESDAY MORNING.11:30 AM

ONSHORE YUAN: CLOSED DOWN TO 6.8876

OFFSHORE YUAN: 6.8963

SHANGHAI CLOSED DOWN 23.20 POINTS OR 0.68%

HANG SENG CLOSED DOWN 282.75 PTS OR 1.37%

2. Nikkei closed DOWN 52.07 PTS OR 0.18%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 101.57 EURO FALLS TO 1.0961 DOWN 45 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.470Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 134.59 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.5025***/Italian 10 Yr bond yield RISES to 4.345*** /SPAIN 10 YR BOND YIELD RISES TO 3.535…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.297

3j Gold at $1995.00 silver at: 25.25 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 28 /100 roubles/dollar; ROUBLE AT 81.74//

3m oil into the 80 dollar handle for WTI and 83 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 134.59 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .470% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8982 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9846 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.629 UP 6 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.820 UP 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.2756 UP 8 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.40…

GREAT BRITAIN/10 YEAR YIELD: UP 14 BASIS PTS AT 3.8795

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Slide After Hawkish Bullard Comments, Red Hot UK Inflation

WEDNESDAY, APR 19, 2023 – 07:45 AM

US equity futures fell following hawkish comments from FOMC non-voter Jim Bullard and another double digit CPI print out of the UK; China was weak with property names dropping -2% led by Hong Kong developers which dropped after city leader John Lee dismissed calls by the industry to scrap property cooling measures. Sentiment was also dented by news Tesla cut prices again – just hours before it reports Q1 earnings -which is likely to not be well received by auto sector. Netflix tumbled as much as 12% on Tuesday before recouping almost all losses after a miss on subscribers but after boosting cash flow. Regional banks within a hair of new lows but WAL numbers overnight should give some support to the sector.

Contracts on the S&P 500 fell 0.5% at 7:15 a.m. ET Nasdaq 100 futures slipped 0.8% as the yield on the 10-year Treasury rose to nearly 3.62%, mirroring larger moves in UK gilts following the abovementioned CPI print. The Bloomberg Dollar Spot Index traded near the day’s highs, pressuring most Group-of-10 currencies. Oil, gold and Bitcoin all fall in tandem.

In premarket trading, Tesla dropped 2% after further cutting prices on some models in what is an increasingly bitter price war to capture EV market share ahead of first-quarter results due later Wednesday. Netflix dipped after the video-streaming firm added fewer subscribers than anticipated in the first quarter. Here are some other notable premarket movers:

- Western Alliance rises as much as 18%, boosting shares in fellow regional lenders, as analysts viewed the bank’s balance-sheet repositioning positively, highlighting measures to improve liquidity. The company said deposits rose $2 billion this month through April 14, an encouraging signal given March’s turmoil in the industry following the collapse of SVB.

- Netflix falls 1.3% after the video-streaming company added fewer subscribers than had been anticipated in the first quarter. However, analysts remain positive on the stock’s long-term prospects as the company raised its full-year free cash flow forecast. UBS upgraded to buy from neutral. Shares of video streaming companies were lower after Netflix added fewer subscribers than had been anticipated in the first quarter. FuboTV -3.2%, Roku -1.3%.

- Intuitive Surgical jumps 7.1% after the maker of surgical tools reported procedure growth for the first quarter that beat the average analyst estimate, sending analyst price targets higher. Brokers said Intuitive’s results bode well for peers, and show the environment is improving for such companies as they recover from pandemic-related disruptions to medical procedures.

- United Airlines climbs as much as 0.8% after the carrier reported a narrower-than-estimated loss for the first quarter. Analysts said the company’s outlook was strong and showed that demand for travel is holding up.

- Riot Platforms and Marathon Digital lead fellow cryptocurrency- exposed stocks lower as Bitcoin records its biggest drop in over a month, falling back below the $30,000 mark.

With tax receipts filtering in expect to see a broad based liquidity drain over the next few weeks. CTA positioning is approaching fully long, macro buying has persisted for 6 weeks (nets have crept higher ) and the Goldman trading desk has already seen quite substantial vol control demand with vix back to a 16 handle.

Investors are monitoring earnings to assess how companies have grappled with headwinds including slowing demand and higher interest rates. At the same time, they’re looking for clues if and when the Federal Reserve will end its tightening policy amid fears of a recession and more bank failures.

“Central banks, for now, will keep hiking until they see more evidence of lower inflation down the road,” Barclays Plc strategist Emmanuel Cau said on Bloomberg Television. “Inflation is still high and to some extent growth is resilient at the same time, so I think the resolve of central banks to hike and to see more evidence of inflation coming down is still here.” Separately, Cau said in a note that there’s scope for first-quarter earnings to beat estimates given that growth momentum has rebounded in China, and held up better than expected in the US and Europe.

Globally, volatility has remained at low levels leading many bearish strategists to warn of complacency. Bank of Atlanta President Raphael Bostic said he favors raising rates one more time and then holding them above 5% for some time to curb inflation, while his St. Louis counterpart James Bullard said he prefers getting rates into a 5.5% to 5.75% range. Global markets appear to be overbought and “people should not be too complacent” about the reduced volatility, JPMorgan Asset Management’s Head of Investment Specialists for Asia excluding Japan Jonathan Liang said in a Bloomberg Television interview. He added that a US recession has not yet been priced in.

DAX and CAC lose 0.1%, while UK stocks underperformed their regional peers following another month of hotter than expected double-digit CPI, pushing the FTSE 100 down 0.3%. Here are the biggest European movers:

- Worldline shares jump as much as 9.4%, most since July, after the French payments company launched a joint-venture in merchant payments with Credit Agricole

- Heineken shares rise as much as 3.9% after 1Q update, with analysts saying the Dutch brewer’s pricing power helped offset some expected but unwelcome volume weakness in key markets

- Kuehne + Nagel climbs as much as 2.2% after the Swiss logistics giant was upgraded to buy from hold at Deutsche Bank, which cited better freight data

- National Express shares rise as much as 5.8%, with analysts saying the transport operator delivered a strong first-quarter revenue performance that will underpin its guidance

- ASML shares fall as much as 3.5% in Amsterdam after the semiconductor-equipment maker reported its lowest quarterly order intake since 2020 amid an industry downturn

- Renault falls as much as 4.4% was downgraded to neutral from buy at BofA amid higher EV competition and price pressures. Renault is also set to release 1Q sales figures tomorrow

- Just Eat Takeaway shares dip as much as 6.1% in Amsterdam, paring gains of as much as 5.1%, after the food-delivery company reported first-quarter orders that were below expectations

Earlier in the session, Asian stocks fell as Chinese shares struggled to find footing after mixed economic data released Tuesday, while investors parsed the latest comments from Federal Reserve officials on interest-rate hikes. The MSCI Asia Pacific Index dropped as much as 0.9%, led by consumer discretionary and technology shares. Hong Kong and Chinese benchmarks led losses around the region, while South Korea edged closer to a bull market. Australia also advanced. The latest set of Chinese economic data showed an uneven recovery picture, while hopes for further stimulus have been dampened. That has kept a lid on investor enthusiasm as it signals China’s recovery will likely be gradual, even though the worst may be over after its reopening from Covid Zero.

Japanese stocks declined, halting an eight-day rally, as investors remained concerned about the risk of higher US interest rates and Chinese equities were hit by shareholders’ plans to trim their stakes. The Topix was virtually unchanged at 2,040.38 as of the market close in Tokyo, while the Nikkei 225 declined 0.2% to 28,606.76. Out of 2,158 stocks in the index, 753 rose and 1,251 fell, while 154 were unchanged. “With the stock indexes at a high level, profit-taking selling is prevailing,” said Hideyuki Suzuki, a general manager at SBI Securities.

Australian stocks edged higher, with the S&P/ASX 200 index rising just 0.1% to close at 7,365.50, buoyed by miners as most sectors dropped. Asian shares fell with US stock futures as traders weighed earnings from Wall Street and as Chinese equities were hit by shareholders’ plans to trim their stakes.

In FX, the Bloomberg Dollar Spot Index is up 0.3% having risen versus the rest of its G-10 rivals amid some modest risk-off. US and German short-end yields have followed their UK counterparts higher, rising by 7bps and 5bps respectively.

“The picture being painted by the data released so far this week will likely be raising concerns inside the BOE,” said Stuart Cole, chief macro economist at Equiti Capital in London. “This likely means a continuation of its hiking cycle, a lengthening that will come at a time when peers such as the Federal Reserve will likely have paused with their own cycle of interest-rate rises.”

In rates, treasuries fell, lifting the 10-year yield 6bps higher to 3.63%, the highest since March 22, as BOE and Fed rate hike bets mount following higher-than-forecast UK inflation figures. US yields cheaper by 2bp-7bp across the curve at highest levels this month, with front-end-led losses flattening 2s10s, 5s30s spreads by ~2bp and ~3bp on the day. Money markets price 23bps of Fed hikes next month and 31bps by June; 46bps of easing is priced by year-end. Gilts are sharply lower and the pound has outperformed as traders ramp up bets on additional rate hikes from the Bank of England after UK inflation surprised to the upside. UK two-year yields have jumped 14bps to a six-week high of 3.83% while the pound gains 0.2% versus the greenback. BOE rate hike wagers surge even more, pricing a 5.03% peak rate by November — the highest since October — compared to 4.86% on Monday. Treasury auctions resume with $12b 20-year bond reopening at 1pm; $21b 5-year TIPS new-issue is ahead Thursday

In commodities, crude futures decline with WTI falling 1.9% to trade near $79.30. Spot gold is down 1.4% around $1,978.

Bitcoin has come under marked pressure this morning, with BTC dropping from USD 30k to a test of USD 29k in minutes. At the time, there was no clear fundamental catalyst with the likes of Coindesk subsequently suggesting it may have been spurred by long-liquidations. US House Financial Services Committee will hold a hearing on stablecoin regulation on Wednesday, according to Cointelegraph.

To the day ahead now, and data releases include the UK CPI reading for March. From central banks, the Fed will be releasing their Beige Book, and we’ll hear from the Fed’s Goolsbee, the ECB’s Lane, Knot, de Cos, and Schnabel, as well as the BoE’s Mann. Finally, earnings releases include Tesla, Morgan Stanley and IBM.

Market Snapshot

- S&P 500 futures down 0.4% to 4,162.75

- STOXX Europe 600 down 0.3% to 467.44

- MXAP down 0.8% to 162.36

- MXAPJ down 0.9% to 523.41

- Nikkei down 0.2% to 28,606.76

- Topix little changed at 2,040.38

- Hang Seng Index down 1.4% to 20,367.76

- Shanghai Composite down 0.7% to 3,370.13

- Sensex down 0.4% to 59,470.47

- Australia S&P/ASX 200 little changed at 7,365.54

- Kospi up 0.2% to 2,575.08

- German 10Y yield little changed at 2.52%

- Euro down 0.1% to $1.0960

- Brent Futures down 1.7% to $83.37/bbl

- Gold spot down 1.0% to $1,985.90

- U.S. Dollar Index up 0.14% to 101.89

Top Overnight News

- Washington and Beijing tensions continue to creep higher, w/the White House set to unveil stringent new rules limiting American investments on the mainland. Politico

- South Korea’s CPI for Mar overshoots the St, coming in at +7.1% (vs. the consensus forecast of +6.9% and up from +7% in Feb). BBG

- India has surpassed China as the world’s most populous country, according to UN data released on Wednesday, marking a historic crossover moment for the two Asian neighbors and geopolitical rivals. According to the UN’s Population Dashboard, India’s population has surpassed 1.428bn, just overtaking China’s more than 1.425bn people. FT

- Russian officials quietly raised concerns last year about the risks of becoming too reliant on Chinese technologies after sanctions shut off access to other suppliers. The memo suggests some are worried Chinese firms such as Huawei may come to dominate the Russian market and threaten information security and networks, people familiar said. BBG

- UK inflation for Mar overshoots the St, coming in at +10.1% on the headline (vs. the St consensus of +9.8% and down only modest from +10.4% in Feb). RTRS

- Passenger-car registrations across the EU rose in March on the year as each of the bloc’s largest markets saw double-digit growth, the European Automobile Manufacturers Association, or ACEA, said Wednesday. New car registrations, which reflect sales, rose to 1,087,939 units, a 29% increase compared with March 2022, while registrations in the first quarter rose 18% to almost 2.7 million units, the ACEA said. WSJ

- The EU is storing record levels of natural gas after a milder than anticipated winter, bolstering hopes that the bloc can wean itself off imports from Russia. The bloc’s storage totaled 55.7 per cent of capacity at the start of the month according to the industry body Gas Infrastructure Europe — the highest level for early April since at least 2011. FT

- US crude inventories fell by 2.7 million barrels last week, the API is said to report. That would take total holdings to the lowest in two months if confirmed by the EIA. Gasoline supplies declined by 1 million, dropping for a ninth week ahead of the summer driving season. Distillate stocks also dropped. Elsewhere in oil, a rush in Asia to secure supplies after OPEC+’s output-cut surprise is fading. BBG

- CDW a large distributor of IT products, announced a negative preannouncement (they see Q1 revenue of $5.1B vs. the Street consensus of $5.57B and full-year EPS is now seen falling Y/Y vs. the St consensus of +6%). RTRS

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were lacklustre in the absence of any major positive macro drivers and following the flat handover from Wall St where risk sentiment was clouded amid mixed data releases and earnings results. ASX 200 was kept afloat amid outperformance in the mining and materials sectors although gains were limited by weakness in energy and consumer stocks, as well as uninspiring data with Westpac Leading Index flat. Nikkei 225 declined after the latest Reuters Tankan survey for April showed Japanese manufacturers remained glum with the Large Manufacturing Index stuck in negative territory. Hang Seng and Shanghai Comp were subdued with underperformance in Hong Kong amid losses in autos, property and tech, while the mainland was also cautious ahead of US Treasury Secretary Yellen’s major speech on Thursday regarding US-China Economic ties where she will outline US economic priorities on China.

Top Asian News

- BoJ is reportedly wary of tweaking yield control in April, via Bloomberg; BoJ is reportedly likely to mull of guidance change can wait or not; smoother yield curve is said to suggest no need for a move now; seeing elevated uncertainties after the banking crisis.

- China’s NDRC said it is studying and drafting documents to recover and expand consumption, while it added that it will work hard to stabilise auto consumption, according to Reuters.

- UBS raises it FY23 Chinese GDP forecast to 5.7% Y/Y from 5.4%.

European bourses are in the red, Euro Stoxx 50 -0.4%, after the index’s largest weighted component ASML drops post-earnings despite beating estimates as it highlights caution among customers. Elsewhere, the macro backdrop has been influenced by hotter-than-expected UK CPI data with a hawkish move seen in Europe/UK at the time, FTSE 100 -0.4%. Given the above, sectors have a negative skew with Real Estate lagging as yields increase while Tech names slip given ASML, at the other end of the spectrum Food, Beverage and Tobacco outperforms after Heineken’s update. Stateside, futures are in the red with the Nasdaq lagging as yields increase while banking names are deriving support from WAL’s after-hours update. Netflix Inc (NFLX): Top- and bottom-lines were broadly in line with expectations, although net subscriber additions were short in the quarter, and guidance for the next quarter was soft relative to analyst expectations; some analysts suggested that the soft subscriber guidance was a result of pushing back the launch of its paid-sharing service into Q2. Western Alliance Bancorp (WAL): The regional bank reported that deposits stabilised in Q1, and profits topped expectations.

Top European News

- Morgan Stanley now expects the BoE to hike rates by 25bps in May vs. prev. view of unchanged.

- Central London property prices fell nearly 5% in the 12 months to March which is the largest annual decline since 2019, according to FT

FX

- Overall, the session is characterised by broad USD strength which is seemingly being fuelled by yield action and associated JPY underperformance alongside dovish-sounding BoJ commentary.

- Thus far, the DXY has eclipsed the 102.00 handle to a 102.18 peak from a 101.65 base, with upside initially capped by GBP outperformance after hotter-than-expected CPI data; Cable peaked at 1.2472, but has since been drawn back to 1.2400.

- Returning to the JPY, USD/JPY has most recently pulled-back from the 135.00 mark to circa. 134.75 after source reports suggest the BoJ is wary of tweaking yield control in April, via Bloomberg.

- Elsewhere, peers are broadly-speaking softer against the USD with EUR unreactive to final HICP as marked OpEx draws interest while the CHF experienced only a fleeting upside from SNB’s Maechler.

- Note, given the marked crude move petro-FX has been coming under slightly more pressure as the session progressed, with USD/CAD below the 200-DMA and towards its 10-DMA.

- SNB’s Maechler says inflation is back with a vengeance and monetary policy is back to the traditional tools. Ready to sell foreign currencies..

- PBoC set USD/CNY mid-point at 6.8731 vs exp. 6.8728 (prev. 6.8814)

Fixed Income

- Gilts once again underperform after hawkish UK data ahead of the May BoE, with 25bp now fully priced compared to circa. 80% before-hand.

- As such, Gilts have been down to 99.85 with the associated 10yr yield above 3.85%

- Action which has been seen, though to a lesser extent, in EGBs and USTs and has served as another bout of concession before the well-received Bund outing and the upcoming US 20yr; albeit, limited upside from the German sale.

- Stateside, USTs remain pressured pre-supply/Goolsbee with the curve elevated and action again most pronounced at the short-end.

Commodities

- WTI and Brent are under marked pressure that has seen the benchmarks move below the last two week’s lows amid broad USD strength; note, the move occurred despite a lack of timely drivers and the initial bout did not coincide with Dollar action.

- Specifically, the benchmarks have moved below USD 79/bbl and USD 83/bbl respectively, from initial USD 81.24/bbl and USD 85/15/bbl peaks.

- China’s NDRC said it will speed up the construction of iron ore projects and will firmly curb an irrational rise in iron ore prices, according to Reuters.

- China’s Huayou Cobalt is looking to build a nickel ore processing plant in the Philippines, according to an industry source cited by Reuters.

- Spot gold has succumbed to the firmer USD and has surrendered the USD 2k/oz handle to a USD 1972/oz trough, with base metals under similar pressure though ranges are somewhat more contained in the likes of LME Copper.

- Ukraine’s Deputy PM says ship inspections are recommencing under the Black Sea grain initiative and grain transit through Poland is to open overnight Thursday/Friday.

Geopolitics

- US did not issue visas to all members of the Russian delegation going to the UN, according to RIA.

- UK government cyber defence agency warned of a threat to Western infrastructure from hackers sympathetic to Russia and its war on Ukraine, according to Reuters.

- South Korean President Yoon said South Korea may consider providing military aid for Ukraine if a large attack on civilians occurs and it will take the most appropriate measures considering battlefield developments in Ukraine. Yoon also commented that he won’t hold a summit with North Korean leader Kim for show but the door for dialogue to promote peace remains open, while South Korea is developing ultra-high performance and high-power weapons to respond to North Korea’s emerging threats and is discussing extended deterrence plans with the US including information sharing, joint planning and joint execution, according to Reuters.

- North Korean leader Kim ordered the preparation to launch a military spy satellite as planned and ordered the deployment of a series of spy satellites to boost reconnaissance capabilities, according to KCNA.

- US House China Select Committee will be war-gaming a scenario of China invading Taiwan, according to Axios

- A leaked US military assessment stated that China’s military could soon deploy a high-altitude supersonic spy drone unit, according to Washington Post.

US event calendar

- 07:00: April MBA Mortgage Applications, prior 5.3%

- 14:00: Federal Reserve Releases Beige Book

Central Banks

- 14:00: Federal Reserve Releases Beige Book

- 17:30: Fed’s Goolsbee Interviewed on Marketplace

- 19:00: Fed’s Williams Speaks in New York

DB’s Jim Reid concludes the overnight wrap

I’m in the US showing off my panda eye ski tan for the rest of the week. Before I left I had the weirdest, nostalgic dollop of deja-vu. Unbeknown to me my wife had bought our five-year-old twins their first Panini football card album. To say they were immediately obsessed was an understatement. It brought back memories of me desperate to swap my excess cards for one Ian Rush sticker over 40 years ago. From my brief interactions before I left it seems they’ll do anything for a pack of new cards now to expand their set. So we have a list of chores that completing will gain a set. I’ve written to Panini to see if they’ll do an Investment Bank edition. Imagine the excitement of getting the full house of DB Research professionals’ stickers in your book before one of our rivals!

The market has been collecting a few duller days of late but it probably wouldn’t want to swap for those seen a month or so ago. The last 24 hours fitted into that narrative with most major assets closing either side of unchanged. We did get several earnings releases to chew over, but they were pretty mixed overall and didn’t point to an obvious conclusion for investors, and it was much the same from yesterday’s limited round of data. So with all said and done, the S&P 500 ultimately ended the day just +0.08% higher, remaining in its narrow band over April that’s left it within a range of little more than 1% either side of its level at the start of the month.

With little volatility to speak of, that’s enabled a continued easing in financial conditions, with Bloomberg’s index hitting a post-SVB high yesterday. In fact, it’s now unwound around 90% of the tightening related to last month’s market turmoil, so it’s increasingly feeling like a bad dream with little lasting impact on market based financial conditions. We’ll see from the SLOOS report in a couple of weeks whether there has been scars from bank-based financial conditions. For now the looser market-based financial conditions have helped cement investors’ conviction that the Fed are set to deliver another hike in just two weeks’ from now, which was supported by the latest round of FOMC speakers. For instance, St Louis Fed President Bullard struck a bullish tone on the economy, saying that “Wall Street’s very engaged in the idea there’s going to be a recession in six months or something, but that isn’t really the way you would read an expansion like this.” Later on, Atlanta Fed President Bostic then said that his baseline was for one further hike and then a pause that left them there for “quite some time”. But even as officials offered more signals about another rate hike, 10yr Treasuries reversed a touch to end the day -2.5bps lower at 3.576%. Fed futures ticked slightly lower with the probability of a rate hike next month dropping 2 percentage points to 85.8% but this comes after increasing 64pp since the Monday after SVB failed.

When it came to equities, there was a reasonable amount of dispersion given the subdued movements for the broader indices. In fact, there was exactly 50% of constituents higher and lower on the day, with cyclicals outperforming defensives as industrials (+0.46%) and energy (+0.45%) stocks outpaced healthcare (-0.66%), communications (-0.65%) and utilities (-0.51%). In terms of the various earnings reports, the main highlights included Goldman Sachs (-1.70%), whose share price fell back after their FICC sales and trading revenue came in beneath expectations thanks to a -17% decline. Elsewhere, Bank of America’s (+0.63%) trading revenue beat expectations and overall revenue was up 9%. And away from the financials, Johnson & Johnson (-2.81%) was another that struggled, even as they raised their earnings forecast for this year. After the close, NFLX (initially down -12.5% before recovering to unchanged in after-market trading) missed on new subscriber growth (+1.75mn vs +2.41mn estimated) and lowered sales and profit guidance further than analysts expected. United Airlines was up +1.30% in after-market trading after reporting increased international travel that will see stronger 2Q results than analysts expected after posting a first-quarter adjusted loss of $0.63 EPS.

Over in Europe, the performance was a bit stronger yesterday, although in part that reflected a catchup to the US rally after Europe went home the previous day. That enabled the STOXX 600 (+0.38%) to hit a 14-month high, and the Euro STOXX 50 (+0.60%) is now just shy of its closing peak from November 2021, which if surpassed would leave the index at its highest level since late 2007. For bonds there was also a bit more of a risk-on tone, and yields on 10yr bunds ended the day up +0.4bps. That followed comments from ECB chief economist Lane that “I think the baseline is that we should indeed increase interest rates in May”.

Whilst most sovereign bonds in Europe were fairly steady yesterday, back in the UK, gilts were an underperformer thanks to data that showed stronger-than-expected wage growth, and the 10yr yield climbed +5.6bps on the day. The release showed that growth in average total pay was up +5.9% (vs. +5.1% expected) over the three months to February compared to the previous year. And with upward revisions to the previous month as well, the data added to fears that inflation would prove more persistent than expected, and that the Bank of England would need to hike rates yet further. Indeed, the chances of another 25bp rate hike at the May meeting moved up to 90.1% according to overnight index swaps, the highest level since SVB’s collapse. On that front, the next crucial component will be the CPI release this morning, which should be coming out around the time this email hits your inboxes.

Asian equity markets are mostly trading lower this morning following the lacklustre performance on Wall Street overnight. As I type, the Hang Seng (-0.60%) is leading losses across the region, pulled down by technology and real estate stocks, while the CSI (-0.50%), the Shanghai Composite (-0.21%) and the Nikkei (-0.24%) are also in the red amid the prospect of interest rate hikes from the Fed. Otherwise, the KOSPI (+0.23%) is bucking the regional market trend in early trading, albeit only just.

Outside of Asia, US stock futures are retreating with those on the S&P 500 (-0.12%) and NASDAQ 100 (-0.16%) inching downward following the latest round of earnings.

Running through yesterday’s other data, the German ZEW survey’s expectations component fell back for a second month running in April, with a decline to 4.1 (vs. 15.6 expected). In Canada, CPI inflation declined as expected in March, falling back to 4.3%. And finally in the US, housing starts decelerated in March, falling to an annualised rate of 1.42m (vs. 1.40m expected), with building permits also falling back to 1.413m (vs. 1.45m expected).

To the day ahead now, and data releases include the UK CPI reading for March. From central banks, the Fed will be releasing their Beige Book, and we’ll hear from the Fed’s Goolsbee, the ECB’s Lane, Knot, de Cos, and Schnabel, as well as the BoE’s Mann. Finally, earnings releases include Tesla, Morgan Stanley and IBM.

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

Marked USD strength as yields lift; hot UK CPI; ASML lower, WAL surges post-earnings – Newsquawk US Market Open

WEDNESDAY, APR 19, 2023 – 06:41 AM

- European bourses are in the red as ASML highlights caution among customers & with the macro backdrop influenced by hawkish UK CPI.

- Stateside, futures are in the red with the NQ lagging as yields increase while banking names are deriving support from WAL’s after-hours update.

- The session is characterised by broad USD strength, seemingly fuelled by yields and JPY underperformance.

- Though, the latter dynamic briefly lessened following a BoJ sources piece; GBP the relative outperformer post-CPI.

- As such, Gilts once again underperform with EGBs & USTs lower in sympathy, action which provided more pre-supply concessions.

- Crude benchmarks have experienced marked downside with fundamentals limited amid broad strength and the surrender of recent lows.

- Looking ahead, highlights include New Zealand CPI; Speeches from ECB’s Lane & Schnabel, Fed’s Goolsbee, BoE’s Mann, SNB’s Schlegel. Supply from the US. Earnings from American Airlines, IBM, Tesla, Morgan Stanley & Abbott.

View the full premarket movers and news report.

Or why not try Newsquawk’s squawk box free for 7 days?

EUROPEAN TRADE

EQUITIES

- European bourses are in the red, Euro Stoxx 50 -0.4%, after the index’s largest weighted component ASML drops post-earnings despite beating estimates as it highlights caution among customers.

- Elsewhere, the macro backdrop has been influenced by hotter-than-expected UK CPI data with a hawkish move seen in Europe/UK at the time, FTSE 100 -0.4%.

- Given the above, sectors have a negative skew with Real Estate lagging as yields increase while Tech names slip given ASML, at the other end of the spectrum Food, Beverage and Tobacco outperforms after Heineken’s update.

- Stateside, futures are in the red with the Nasdaq lagging as yields increase while banking names are deriving support from WAL’s after-hours update.

- Netflix Inc (NFLX): Top- and bottom-lines were broadly in line with expectations, although net subscriber additions were short in the quarter, and guidance for the next quarter was soft relative to analyst expectations; some analysts suggested that the soft subscriber guidance was a result of pushing back the launch of its paid-sharing service into Q2.

- Western Alliance Bancorp (WAL): The regional bank reported that deposits stabilised in Q1, and profits topped expectations.

- ASML (ASML NA) Q1 2023 (EUR): Revenue 6.75bln (exp. 6.3bln), Net Income 1.95bln (exp. 1.64bln), EPS 4.96 (exp. 4.13), Gross Profit 3.4bln, Gross Margin 50.6% (exp. 49.8%). Total 2022 dividend of 5.80/shr (exp. 6.60/shr).

- Click here for more detail.

FX

- Overall, the session is characterised by broad USD strength which is seemingly being fuelled by yield action and associated JPY underperformance alongside dovish-sounding BoJ commentary.

- Thus far, the DXY has eclipsed the 102.00 handle to a 102.18 peak from a 101.65 base, with upside initially capped by GBP outperformance after hotter-than-expected CPI data; Cable peaked at 1.2472, but has since been drawn back to 1.2400.

- Returning to the JPY, USD/JPY has most recently pulled-back from the 135.00 mark to circa. 134.75 after source reports suggest the BoJ is wary of tweaking yield control in April, via Bloomberg.

- Elsewhere, peers are broadly-speaking softer against the USD with EUR unreactive to final HICP as marked OpEx draws interest while the CHF experienced only a fleeting upside from SNB’s Maechler.

- Note, given the marked crude move petro-FX has been coming under slightly more pressure as the session progressed, with USD/CAD below the 200-DMA and towards its 10-DMA.

- SNB’s Maechler says inflation is back with a vengeance and monetary policy is back to the traditional tools. Ready to sell foreign currencies..

- PBoC set USD/CNY mid-point at 6.8731 vs exp. 6.8728 (prev. 6.8814)

- Click here for more detail.

FIXED INCOME

- Gilts once again underperform after hawkish UK data ahead of the May BoE, with 25bp now fully priced compared to circa. 80% before-hand.

- As such, Gilts have been down to 99.85 with the associated 10yr yield above 3.85%

- Action which has been seen, though to a lesser extent, in EGBs and USTs and has served as another bout of concession before the well-received Bund outing and the upcoming US 20yr; albeit, limited upside from the German sale.

- Stateside, USTs remain pressured pre-supply/Goolsbee with the curve elevated and action again most pronounced at the short-end.

- Click here for more detail.

COMMODITIES

- WTI and Brent are under marked pressure that has seen the benchmarks move below the last two week’s lows amid broad USD strength; note, the move occurred despite a lack of timely drivers and the initial bout did not coincide with Dollar action.

- Specifically, the benchmarks have moved below USD 79/bbl and USD 83/bbl respectively, from initial USD 81.24/bbl and USD 85/15/bbl peaks.

- China’s NDRC said it will speed up the construction of iron ore projects and will firmly curb an irrational rise in iron ore prices, according to Reuters.

- China’s Huayou Cobalt is looking to build a nickel ore processing plant in the Philippines, according to an industry source cited by Reuters.

- Spot gold has succumbed to the firmer USD and has surrendered the USD 2k/oz handle to a USD 1972/oz trough, with base metals under similar pressure though ranges are somewhat more contained in the likes of LME Copper.

- Ukraine’s Deputy PM says ship inspections are recommencing under the Black Sea grain initiative and grain transit through Poland is to open overnight Thursday/Friday.

- Click here for more detail.

NOTABLE HEADLINES

- Morgan Stanley now expects the BoE to hike rates by 25bps in May vs. prev. view of unchanged.

- Central London property prices fell nearly 5% in the 12 months to March which is the largest annual decline since 2019, according to FT

DATA RECAP

- UK CPI YY (Mar) 10.1% vs. Exp. 9.8% (Prev. 10.4%); MM (Mar) 0.8% vs. Exp. 0.5% (Prev. 1.1%)

- UK CPI All Services 12-month rate 6.6% (prev. 6.6%)

- UK Core CPI YY (Mar) 6.2% vs. Exp. 6.0% (Prev. 6.2%); MM (Mar) 0.9% vs. Exp. 0.6% (Prev. 1.2%)

- EU HICP Final YY (Mar) 6.9% vs. Exp. 6.9% (Prev. 6.9%); X F&E Final YY (Mar) 7.5% vs. Exp. 7.5% (Prev. 7.5%); X F, E, A & T Final YY (Mar) 5.7% vs. Exp. 5.7% (Prev. 5.7%)

NOTABLE US HEADLINES

- US President Biden and Democratic congressional leaders Schumer and Jeffries agreed in a call that they won’t negotiate on the debt limit, while Biden said he was ready to separately negotiate regarding the budget once Republicans present their plan, according to the White House cited by Reuters.

- TSMC (2330 TT/TSM) is reportedly seeking up to USD 15bln from the US for semiconductor plans, but pushes back on conditions that require factory profits to be shared and for detailed operation information to be provided, according to WSJ sources.

- Synchrony Financial (SYF) Q1 2023 (USD): Diluted EPS 1.35 (exp. 1.46), total deposits USD 74.4bln (exp. 71.4bln)

- Click here for the US Early Morning Note.

GEOPOLITICS

- US did not issue visas to all members of the Russian delegation going to the UN, according to RIA.

- UK government cyber defence agency warned of a threat to Western infrastructure from hackers sympathetic to Russia and its war on Ukraine, according to Reuters.

- South Korean President Yoon said South Korea may consider providing military aid for Ukraine if a large attack on civilians occurs and it will take the most appropriate measures considering battlefield developments in Ukraine. Yoon also commented that he won’t hold a summit with North Korean leader Kim for show but the door for dialogue to promote peace remains open, while South Korea is developing ultra-high performance and high-power weapons to respond to North Korea’s emerging threats and is discussing extended deterrence plans with the US including information sharing, joint planning and joint execution, according to Reuters.

- North Korean leader Kim ordered the preparation to launch a military spy satellite as planned and ordered the deployment of a series of spy satellites to boost reconnaissance capabilities, according to KCNA.

- US House China Select Committee will be war-gaming a scenario of China invading Taiwan, according to Axios

- A leaked US military assessment stated that China’s military could soon deploy a high-altitude supersonic spy drone unit, according to Washington Post.

CRYPTO

- Bitcoin has come under marked pressure this morning, with BTC dropping from USD 30k to a test of USD 29k in a limited timeframe. At the time, there was no clear fundamental catalyst with the likes of Coindesk subsequently suggesting it may have been spurred by long-liquidations.

- US House Financial Services Committee will hold a hearing on stablecoin regulation on Wednesday, according to Cointelegraph.

APAC TRADE