MAY 2/2023 · by harveyorgan · in Uncategorized · Leave a comment·Editi

GOLD PRICE CLOSED: UP $32.70 TO $2014.20

SILVER PRICE CLOSED: UP 34 CENTS AT $25.31

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE $2016.70

Silver ACCESS CLOSE: 25.37

Bitcoin morning price:, $28,066 UP 62 Dollars

Bitcoin: afternoon price: $28,790 UP 786 dollars

Platinum price closing $1066.80 DOWN $12.00

Palladium price; $1445.90 DOWN $59.80

“Our government… teaches the whole people by its example. If the government becomes the lawbreaker, it breeds contempt for law; it invites every man to become a law unto himself; it invites anarchy.” … Louis D Brandeis (former Supreme Court Justice)

GO GATA!

TODAY WE HAD A GREAT DAY FOR GOLD AND SILVER. LET US SEE HOW THE WEEK PLAYS OUT!! THE BANKERS ARE HAVING A TOUGHER TIME MANIPULATING OUR TWO PRECIOUS METALS.

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,747.55 UP 62.34 CDN dollars per oz (ALL TIME HIGH 2,747.55*) ALL TIME HIGH HIT TODAY

BRITISH GOLD: 1617.15 UP 30.24 pounds per oz//(ALL TIME HIGH//1629.84)

EURO GOLD: 1833.01 UP 26.71 euros per oz //(ALL TIME HIGH//1860.82)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

CONTRACT: MAY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,983.400000000 USD

INTENT DATE: 05/01/2023 DELIVERY DATE: 05/03/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 25

435 H SCOTIA CAPITAL 6

661 C JP MORGAN 8

737 C ADVANTAGE 15 3

800 C MAREX SPEC 19

880 C CITIGROUP 4

905 C ADM 4

TOTAL: 42 42

MONTH TO DATE: 1,248

JPMorgan stopped 8/42 contracts

FOR MAY:

GOLD: NUMBER OF NOTICES FILED FOR MAY/2023. CONTRACT: 42 NOTICES FOR 4200 OZ or 0.1306 TONNES

total notices so far: 1248 contracts for 124800 oz (3.8818 tonnes)

FOR MAY:

SILVER NOTICES: 13 NOTICE(S) FILED FOR 65,000 OZ/

total number of notices filed so far this month : 1687 for 8,435,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $32.70

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:///.A WITHDRAWAL OF 1.45 TONNES FROM THE GLD//?? ( DOES NOT MAKE SENSE)

INVENTORY RESTS AT 924.83 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 37 CENTS AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV://: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 468.264 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1542 CONTRACTS TO 141,795 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.01 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.01). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A GIGANTIC GAIN ON OUR TWO EXCHANGES OF 2310 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 0 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 653 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.105 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 190,000 OZ9E.FP.’S LOWER THE AMOUNT OF SILVER STANDING)+ 0 MILLION OZ OF EXCHANGE FOR RISK:THUS TOTAL OF 12.935 MILLION OZ OF STANDING FOR DELIVERY V) HUGE SIZED COMEX OI GAIN/ STRONG SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –1 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL:

TOTAL CONTRACTS for 2 days, total 888 contracts: OR 4.440 MILLION OZ . (444 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 4.440 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 4.440 MILLION OZ/INITIAL

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1542 CONTRACTS DESPITE OUR $0.01 LOSS IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 653 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 13.105 MILLION OZ//FIRST DAY NOTICE FOLLOWED BY TODAY’S E.F.P. JUMP OF 1900,000 OZ (DECREASES THE AMOUNT OF SILVER STANDING) +// + 0 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //TOTAL STANDING 12.935 MILLION OZ// .. WE HAVE A HUGE SIZED GAIN OF 2145 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 13 NOTICE(S) FILED TODAY FOR 65,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 5717 CONTRACTS TO 481,534 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: removed 379 CONTRACTS

WE HAD A STRONG SIZED INCREASE IN COMEX OI ( 6096 CONTRACTS) DESPITE OUR $8.85 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR MAY. AT 3.5085 TONNES ON FIRST DAY NOTICE // PLUS A 17,700 OZ QUEUE. JUMP :(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)////YET ALL OF..THIS HAPPENED WITH OUR $8.85 LOSS IN PRICE WITH RESPECT TO MONDAY’S TRADING.WE HAD A STRONG SIZED GAIN OF 6347 OI CONTRACTS (19.7418 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 630 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 481,534

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6347 CONTRACTS WITH 5717 CONTRACTS INCREASED AT THE COMEX AND 630 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 6347 CONTRACTS OR 19l7418 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (630 CONTRACTS) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (5717 //TOTAL GAIN IN THE TWO EXCHANGES 6347 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 3.5085 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 17,700 OZ // NEW STANDING: 4.3763 TONNES // ///3) ZERO LONG LIQUIDATION//4) STRONG SIZED COMEX OPEN INTEREST GAIN/ 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 3861 CONTRACTS OR 386100 OZ OR 12.009 TONNES IN 2 TRADING DAY(S) AND THUS AVERAGING: 1930 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY(S) IN TONNES 12.009 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 12.009/3550 x 100% TONNES 0.338% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES ( MUCH SMALLER THAN LAST MONTH)

MAY: 12.009 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A GIGANTIC SIZED 1542 CONTRACTS OI TO 141,795 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 653 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 653 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 653 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1542 CONTRACTS AND ADD TO THE 653 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2145 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 10.975 MILLION OZ

OCCURRED DESPITE OUR $0.01 LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED //Hang Seng CLOSED UP 39.24 POINTS OR 0.20% /The Nikkei closed UP 24,27 PTS OR 0.13% //Australia’s all ordinaries CLOSED DOWN 0.86 % /Chinese yuan (ONSHORE) closed /OFFSHORE CHINESE YUAN DOWN TO 6.9471 /Oil UP TO 75.32 dollars per barrel for WTI and BRENT AT 79.11 / Stocks in Europe OPENED MOSTLY RED// ONSHORE YUAN TRADING XXX LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 5717 CONTRACTS UP TO 481,534 DESPITE OUR LOSS IN PRICE OF $8.85 ON MONDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF MAY… THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 630 EFP CONTRACTS WERE ISSUED: : JUNE 630 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 630 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 6347 CONTRACTS IN THAT 630 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED GAIN OF 5717 COMEX CONTRACTS..AND THIS STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $8.85. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (4.3763) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 4.3763 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $8.85) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR STRONG SIZED GAIN OF 6347 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 20.920 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY. (3.5085 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 17,700 oz//NEW STANDING 4.3763 TONNES ALL OF THIS WAS ACCOMPLISHED WITH OUR FALL IN PRICE TO THE TUNE OF $8.85

WE HAD +REMOVED 379 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 5717 CONTRACTS OR 571,700 OZ OR 19.7418 TONNES.

Estimated gold comex today 243,000 fair//

final gold volumes/yesterday 183,027 poor

//MAY 2/ MAY 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil oz . |

| Deposit to the Dealer Inventory in oz | 21,798.378 OZ Brinks 678 kilobars |

| Deposits to the Customer Inventory, in oz | 160,755.000 Oz JPM 5,000 kilobars |

| No of oz served (contracts) today | 42 notice(s) 4200 OZ 0.1306 TONNES |

| No of oz to be served (notices) | 159 contracts 15900 oz 0.4945 TONNES |

| Total monthly oz gold served (contracts) so far this month | 1248 notices 124,800 OZ 3.8818 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 0

total withdrawals: nil oz

Adjustments;

ii) customer to dealer Brinks: 98.99 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 201 contracts having GAINED 28 contracts. We had 149 contracts filed

on MONDAY, so we gained 177 contracts or an additional 17,700 oz will stand for gold in this non active delivery month of May.

June GAINED 1211 contracts UP to 377,258 contracts.

July added its first 326 contracts to stand at 477 contracts.

AUGUST GAINED 4014 contracts up to 63,019 contracts

We had 42 contracts filed for today representing 4200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 42 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 8 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2023. contract month,

we take the total number of notices filed so far for the month (1,248 x 100 oz ), to which we add the difference between the open interest for the front month of MAY 201 CONTRACTS) minus the number of notices served upon today 42 x 100 oz per contract equals 140,700 OZ OR 4.3763 TONNES the number of TONNES standing in this NON- active month of May.

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (1248 x 100 oz)+201 OI for the front month minus the number of notices served upon today (42)x 100 oz} which equals 140,700 oz standing OR 4.3763 TONNES

TOTAL COMEX GOLD STANDING: 4.3763 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,713,349.037 OZ 53.29 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,359,418.061 OZ

TOTAL REGISTERED GOLD: 12,358,365.175 (384.39 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,001,052.886 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,654,917 OZ (REG GOLD- PLEDGED GOLD) 331.412 tonnes//

END

SILVER/COMEX

MAY 2//2023// THE MAY 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 868,633.824 oz Brinks CNT Delaware Loomis manfra . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 13 CONTRACT(S) (65,000 OZ) |

| No of oz to be served (notices) | 900 contracts (4,500,000 oz) |

| Total monthly oz silver served (contracts) | 1687 Contracts (8,435,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

Total deposits: nil oz

JPMorgan has a total silver weight: 139,607 million oz/270.024 million =51.70% of comex .//dropping fast

Comex withdrawals: 34

i) Out of Brinks 32,319.580 oz

ii) Out of CNT: 160,279.880 oz

iii) Out of Delaware 8061.980 oz

iv) Out of Loomis: 68,016.684 oz

v) Out of Manfra: 599,955.800 oz

Total withdrawals; 868,633.824 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 33.204 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 270.024 million oz

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY /2023 OI: 913 CONTRACTS HAVING LOST 697 CONTRACT(S). WE HAD 659 CONTRACTS FILED

ON FRIDAY, SO WE LOST 38 CONTRACTS OR AN ADDITIONAL 190,000 OZ OF SILVER WILL NOT STAND FOR DELIVERY IN THIS VERY

ACTIVE DELIVERY MONTH OF MAY AS THESE GUYS WERE E.F.P.’d TO LONDON AS NO SILVER COULD BE FOUND OVER HERE..

.JUNE HAD A 17 CONTRACTS GAIN TO 871

JULY HAD A 1945 CONTRACT GAIN TO 120,704 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 13 for 65,000 oz

Comex volumes// est. volume today 61,538 good

Comex volume: confirmed yesterday: 70,913 good

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 1687 x 5,000 oz = 8,435,000 oz

to which we add the difference between the open interest for the front month of MAY(913) and the number of notices served upon today 13 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2023 contract month: 1687 (notices served so far) x 5000 oz + OI for the front month of May (913) – number of notices served upon today (13 )x 500 oz of silver standing for the MAY contract month equates to 12.935 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

APRIL 10/WITH GOLD DOWN $21.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91 TONNES

APRIL 6//WITH GOLD DOWN $9.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91

APRIL 5//WITH GOLD UP 0 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04

APRIL 4/WITH GOLD UP $36.30 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

APRIL 3/WITH GOLD UP $14.20 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.02 TONNES

MARCH 31/WITH GOLD DOWN $10.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD////INVENTORY RESTS AT 928.02 TONNES

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

GLD INVENTORY: 924.83 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 10/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 6/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 4.643 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 468.585 MILLION OZ//

APRIL 5/WITH SILVER DOWN 4 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.942 MILLION OZ

APRIL 4/WITH GOLD UP $1.11 TODAY CRIMINAL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.47 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 463,942 MILLION OZ

APRIL 1/WITH SILVER DOWN 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.412

MARCH 31/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD/: A MASSIVE 4.779 MILLION OZ DEPOSITED INTO THE SLV///INVENTORY RESTS AT465.412 MILLION OZ

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

CLOSING INVENTORY 468.264 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

Peter Schiff: Joe Biden Is Rewarding People With Bad Credit

TUESDAY, MAY 02, 2023 – 01:30 PM

On May 1, new Federal Housing Finance Agency (FHFA) rules went into effect that will allow borrowers with lower credit ratings to qualify for better mortgage rates than they otherwise would have. Meanwhile, borrowers with better credit ratings will pay higher fees to subsidize the program. Peter Schiff recently appeared on Real America with Dan Ball to talk about the new rules.

Experts say a person with a credit score over 680 could pay an extra $40 to $70 per month.

When the news came out, Peter Schiff tweeted, “Just when you thought the Joe Biden administration couldn’t get any dumber, it does this. It’s a perfect example of why government shouldn’t have any involvement in the housing market and why the FHA, Fannie Mae and Freddie Mack should all be abolished.”

Dan said he’s about ready to buy a home and he’ll be punished if this plan goes through. Peter told Dan he didn’t have to get punished.

Just miss a few payments. Screw up your credit score. That will help your mortgage rate.”

https://www.zerohedge.com/political/peter-schiff-joe-biden-rewarding-people-bad-credit

Peter also noted that the plan will encourage homebuyers to make smaller down payments.

Normally, if you make a big downpayment, you get a better rate. But now, Biden wants the better rates to go to people that don’t make a big down payment. The worst part about this is that it’s going to further undermine the solvency of our banking system because banks are going to be encouraged and actually required to make more loans to riskier borrowers, which means more mortgages are going to end up in default.”

As Dan pointed out, this isn’t unlike the policies that helped blow up the subprime mortgage bubble leading up to the 2008 financial crisis.

During the Clinton and GW Bush administration, the government was pressuring banks to make loans to marginalized communities. But as Peter pointed out, banks are supposed to be colorblind.

They’re making loans based on the ability to repay. If somebody can repay the mortgage, they’re going to make it. So, if they’re denying mortgages, it’s not because they’re racist or sexist or homophobic or whatever. They’re denying the mortgage because the borrower probably can’t pay the money back.”

Peter said programs like this are really doing a disservice.

When the government encourages people who can’t afford houses to buy them anyway, they actually end up in over their heads, and they lose money because houses are very expensive. Take it from me; I own several. And you know, they’re money pits. You need money to afford to own a home. You can’t own a home when you’re broke.”

Looking at the broader Biden economy, Peter called it “a disaster” and said you can fit all of Biden’s economic accomplishments “on a chewing gum wrapper.”

In fact, you probably don’t even need all that paper, because I don’t even think he has any accomplishments to list. He’s just stumbled his way through the first couple of years in the White House and the economy is getting worse. Inflation is getting worse. All he’s done is worsen the problems that he inherited — not like everything was great when he stepped into office. But he’s made it worse.”

As just one example, Peter mentioned the surging deficits. The Biden administration ran a budget deficit of over $1 trillion in just the first six months of fiscal 2023. Meanwhile, the US continues to run a massive trade deficit.

Peter said Biden’s policies have complicated the Fed’s efforts to fight inflation. (Not that the Fed is doing a great job.)

It’s impossible to fight inflation when the Biden administration continues to create it by running massive deficits.”

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDSJOHN RUBINO

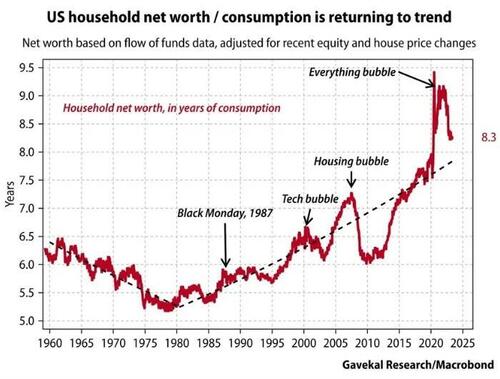

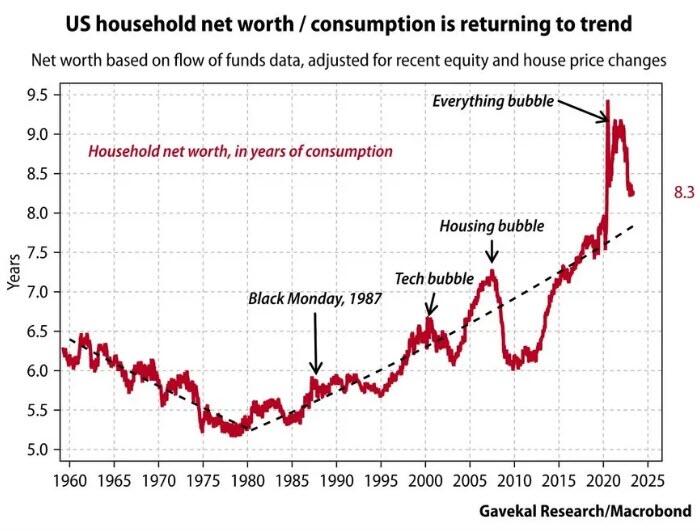

Fooling Us With Fake Stats: Household Net Worth

TUESDAY, MAY 02, 2023 – 03:20 PM

Authored by John Rubino via Substack,

Towards the end of a financial bubble, the people who benefit from the bubble’s continuation — politicians hoping to be reelected, bankers hoping to complete the next deal, money managers talking their books — start touting “record household net worth” as a sign of societal health.

But they’re wrong, for the following reasons:

Deceptive leverage.

Pretend that you borrow $1 million to buy some JPMorgan Chase shares and that this transaction pushes the value of the stock higher. Without realizing it, you’ve just raised the net worth of millions of other JPMorgan Chase stockholders. Total household net worth — that is, assets minus liabilities —increases by vastly more than the money you borrowed. Society gets “richer” and the economy gets more robust and “safer” because of its growing net worth cushion.

So far so good. But since leverage works both ways, as soon as you turn around and sell your stock, thus pushing down the price, that incremental net worth vanishes, because it never really existed.

False comparison.

Most adults understand that their stocks, bonds, and houses fluctuate in price, rising in good times and falling in bad, while their mortgages, credit card debts, and auto loans only fall as they’re paid off. Which is to say instead of falling, these obligations mostly just rise as new debts are incurred and old debts are rolled over. A statistic derived by combining things that can evaporate (asset prices) and things that generally can’t (debt balances) does not measure what they say it does.

The takeaway: In a society of borrowers and speculators, asset values increase because of borrowing and speculation, which makes rising household net worth both a negative indicator of future growth and a sign of fragility rather than strength. But until people figure this out, it remains a great tool for convincing consumers that everything is fine when it’s actually not.

The following chart (courtesy of European money manager Gavekal Research) shows household net worth peaking just before the onset of recessions and/or brutal bear markets.

Notice how as the economy becomes more and more addicted to leverage, the volatility around the trend line increases, indicating that the next downturn — which we’ve already entered — will lop around 40% from household net worth via plunging asset prices.

And that’s assuming that the trendline itself is a real thing.

If the credit supercycle that began in the 1970s is now ending, we’re facing a generational, not a cyclical, mean reversion in which the other edge of the leverage sword cuts financial assets even more deeply.

Here’s how CNBC covered the subject last year, noting the increase in debt without exploring the link between debt and net worth:

Household wealth tops $150 trillion for the first time despite surge in debt

Americans got considerably richer as 2021 came to a close, thanks to a nice boost from their stock market holdings and an increase in real estate values, the Federal Reserve reported Thursday.

Household net worth in the fourth quarter eclipsed $150 trillion for the first time, rising at a healthy 8.2% pace from the previous quarter for the fastest growth period since the first quarter of 2020. The increase came thanks to a combined $4 trillion rise in holdings from corporate equities and housing.

The total level — $150.29 trillion, to be exact — represented a 14.4% increase from a year ago. The boost came with U.S. economic growth running at its fastest pace since 1984 and the stock market enjoying another robust year.

The move came despite a rapid increase in debt at all levels.

Total nonfinancial debt came to $65.1 trillion, including $17.9 trillion at the household level, $18.5 trillion in the business world and $28.6 trillion from government. Each category saw substantial rises.

Household debt jumped at an 8% annual rate, owing to a 6.9% rise in consumer credit and an 8% surge in mortgages. Nonfinancial business debt increased at a 6.7% clip, while federal government debt leaped by 10.8% after declining 1.3% in the third quarter.

The key sentence: “The move came despite a rapid increase in debt at all levels.”

The CNBC writer is apparently bemused that net worth would rise along with debt as if the two are unrelated, when if fact rising debt is the source of rising net worth.

Americans did not get “considerably richer in 2021.” They got considerably more leveraged and fragile, and one step closer to the mother of all mean reversions.

end

JAMES RICKARDS

Rickards: Fed’s Looking In Wrong Direction

TUESDAY, MAY 02, 2023 – 02:10 PM

Authored by James Rickards via DailyReckoning.com,

What’s the situation with the economy? The short answer is not good. Here’s why…

There are literally hundreds of economic indicators either as hard data or sentiment surveys released daily. It’s impossible for any analyst to keep up with all of them.

But with computers, natural language processing and charts, it is possible to follow broad trends. The key for any good analyst is to settle on a subset of data that has the greatest predictive power and a long track record of getting things right.

It’s equally important to know whether indicators are leading, concurrent or lagging.

A lagging indicator may be a measure of how bad things are, but it comes too late to do anything to stop the bad turn. By the time you see it, a recession has already begun.

Concurrent indicators are useful as validation of what leading indicators have been saying, but they don’t put you ahead of the curve.

Clearly, the most valuable indicators are leading indicators — signals that arise six months and sometimes a full year before trouble arrives. Those are the ones to watch most carefully if you want to be prepared in advance.

The Fed Lags Behind

For reasons that are not clear, the Federal Reserve is obsessed with lagging indicators. This partly explains why they always get policy wrong. They tighten monetary policy after recessions have already begun, making the recession worse. They ease monetary policy when booms are underway, making asset bubbles bigger.

Just think of the stock market crash of 1929, the Tequila Crisis of 1994, the Russia-LTCM crisis of 1998, the dot-com collapse in 2000 and the mortgage bubble in 2007. You’ll find a poorly timed monetary policy in every instance.

The two biggest failures in the Fed reading of economic signals relate to unemployment and inflation. The Fed considers low unemployment to be a sign of economic strength and a source of inflation.

But unemployment is a lagging indicator. When businesses see declining sales, lower profits and bulging inventories, they will do everything possible to cut costs including canceling new orders, dumping goods, holding sales and closing offices.

It’s only when those measures fail to stop the bleeding that owners begin to fire people. By the time unemployment goes up, the recession has already started.

Don’t Look to Inflation for Answers

Inflation is another misleading signal. It’s meaningful on its own but it has no correlation to the business cycle. In the early 1960s, we had low inflation and strong growth. In the late 1970s, we had high inflation and weak growth. In the late 1990s, we had moderate inflation and strong growth. In the 2010s, we had low inflation and low growth.

Does anyone see a correlation there? There isn’t one. Growth and inflation are empirically uncorrelated. We can agree that inflation is bad (although deflation is just as bad in different ways). But inflation tells us nothing about the prospects for growth.

The idea that low unemployment leads to inflation (which is what links the Fed’s obsessions with unemployment and inflation) is an artifact of the discredited Phillips curve beloved by Bernanke and Yellen and adhered to by Powell on the bad advice of Fed economists.

Why this is so is a debate for another day. For now, it’s enough to know that the Fed clings to two indicators that have no predictive value. They are lagging indicators. This is why Fed policy always lags behind the economy and never leads it.

Look Ahead, Not Behind

Fine. But what are the leading indicators? Where can we look to see what’s coming?

Several powerful leading indicators are hiding in plain sight. They are easy to find and have excellent track records as predictive analytic tools. The problem is that relatively few analysts have heard of them, and even fewer know how to interpret them.

Here’s the short list and what they’re telling us right now:

An inverted Treasury yield curve. One type of yield curve is just a graph of yields on like instruments of different maturities. The U.S. Treasury securities market is the largest and most liquid in the world. Treasury securities have almost no credit risk, so the yields reflect the time value of money, inflation expectations, liquidity preferences and not much else.

A normal yield curve is upward sloping, which means that longer maturities carry higher yields. That makes sense. If I’m going to lend you money for 10 years, I probably want a higher interest rate than if I’m going to lend you money for six months.

Right now, the Treasury yield curve is steeply inverted. This means that longer maturities actually have lower yields than shorter maturities.

The 10-year Treasury note yields 3.57%, the 2-year Treasury note yields 4.14%, while the 3-month Treasury bill yields 5.03%. The last time the Treasury yield curve was this inverted was — you guessed it — in mid-2007 and early 2008, just ahead of the global financial crisis.

When investors accept lower yields on longer maturities, it means they expect yields to drop like a rock because of recession or worse. That 4.14% yield on the Treasury note looks weak compared with 5.03% on the 3-month bill.

But the 3-month bill matures in three months. That 4.14% yield on the 2-year will look rich if rates drop to 2.00% by late this year in the depths of a recession. That’s why investors like it. They see the recession coming.

The Eurodollar

An inverted Eurodollar futures curve. This is a bit esoteric, but it’s an even better predictive indicator than the Treasury yield curve. Eurodollar rates are basically short-term interest rates that big banks pay each other for dollars in unregulated markets.

Investors can buy futures contracts on these rates out to five years forward, although the one- to two-year contracts are the most actively traded. Basically, these are long-term bets on short-term rates.

These contracts are priced as a percentage of par or 100.00. The lower the price, the higher the yield (because the discount to 100.00 is greater, so the return is greater). Right now, the June 2023 Eurodollar futures contract is priced at 94.5850. The September contract is 94.9650. The December 2023 contract is priced at 95.3300.

Notice how the price goes up over time? That means markets are betting short-term interest rates are going lower. That’s another recessionary bet. Rates can be expected to come down in a recession, which means those futures contracts could go deep in the money.

This inverted yield curve was also last seen in 2007 and 2008 ahead of the crash.

More Recessionary Omens

Negative Swap Spreads. U.S. Treasury securities dealers buy long-term notes and finance them in overnight repo markets. They receive the fixed rate on the notes and pay the floating overnight rate on the repo.

This same trade can be done in derivative form using an interest rate swap agreement. In the swap, a dealer can receive a fixed rate from the counterparty and pay a floating rate to the same counterparty.

The swap is the same as owning the bond with two differences: There is no bond involved; it’s just a contract. And the parties take credit risk with the counterparty, whereas when you own a Treasury note there’s almost zero credit risk.

It follows that the fixed-rate payment on the swap should be slightly higher than the fixed-rate payment on the actual bond to account for the credit risk in the swap. That’s not the case today. Fixed rates on interest rate swaps are significantly lower than what an investor can receive on the actual Treasury note.

Is this because dealers trust bank credit more than U.S. Treasury credit? Not at all. It’s because the swap does not use up balance sheet capacity, while the actual Treasury note does. It’s also because Treasury notes are in short supply whereas swaps can be written in unlimited quantities.

Both conditions — balance sheet constraints and shortages of Treasury notes — are indicative of ultra-tight monetary conditions that lead to recessions.

There are other technical monetary indicators that point in the same direction. In addition, there’s a flood of hard data from non-monetary channels including declining world trade, declining industrial production, falling house prices, deteriorating consumer credit, declining real wages and many other indicators that all point to a recession.

So the recession is definitely coming and may already be here, according to the best predictive analytic data. The Fed will be the last to know because they’re looking in the rearview mirror at lagging indicators.

Get ready for the recession and don’t expect the Fed to help you see it coming.

END

3,Chris Powell of GATA provides to us very important physical commentaries

Fed is ready to buy defaulted Treasuries, so debt ceiling matters little

Crazy!! the plan is to buy defaulted treasuries if the debt ceiling is not advanced:

(Tankus/Politico)

Submitted by admin on Tue, 2023-05-02 04:19Section: Daily Dispatches

Biden Can Steamroll Republicans on the Debt Ceiling

By Nathan Tankus

Politico, Washington

Wednesday, April 19, 2023

The threat of a real debt ceiling crisis is growing rapidly. House Republicans are still pushing steep spending cuts that the White House won’t countenance, even as the Republicans remain deeply divided on a strategy. And we’re now as little as eight weeks away from the “X date” when the Treasury Department no longer has legal authorization to issue new securities and fill up its checking account.

It’s past time for the White House to consider their unilateral options for avoiding economic disaster more seriousl

Perhaps the most prominent proposal to sideline Congress calls for the Treasury to mint a trillion-dollar platinum coin and deposit it with the Federal Reserve, ensuring the government has plenty of money to pay its bills. So far Treasury Secretary Janet Yellen has rejected the idea, warning that the Fed might not accept the coin and that, in her view, the central bank is not legally obligated to accept it.

There are other ideas floating around, but the one thing they all have in common is that they rely on the Federal Reserve’s cooperation and its willingness to continue acting as the government’s “fiscal agent” — essentially its banker, a role established by the Fed’s statute. …

Despite the Federal Reserve’s uneven record on transparency, it does eventually release transcripts of some of its most critical meetings in the years after they happen. And in an October 2013 conference call, Fed officials discussed a memo with options for how to respond to a government default.

On that call, Powell and most of his colleagues reluctantly endorsed buying defaulted Treasury securities — an unprecedented move to maintain financial stability — if a legislative debt ceiling solution did not come in time. …

… For the remainder of the analysis:

https://www.politico.com/news/magazine/2023/04/19/powell-debt-ceiling-fed-00092522

end

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

END

5.IMPORTANT COMMENTARIES ON COMMODITIES:

end

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

1.YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS// TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED

OFFSHORE YUAN: 6.9471

SHANGHAI CLOSED

HANG SENG CLOSED UP 39.24 PTS OR 0.20%

2. Nikkei closed UP 24.77 PTS OR 0.12%

3. Europe stocks SO FAR: MOSTLY RED

USA dollar INDEX UP TO 101.94 EURO FALLS TO 1.0969 DOWN 1 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.416Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 137.35 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: XX// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.361***/Italian 10 Yr bond yield RISES to 4.247*** /SPAIN 10 YR BOND YIELD RISES TO 3.418…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.160

3j Gold at $1986.52 silver at: 24.72 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 50 /100 roubles/dollar; ROUBLE AT 79.75//

3m oil into the 75 dollar handle for WTI and 79 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 137.35 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .416% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8972 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9843 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.554 DOWN 4 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.787 DOWN 4 BASIS PTS/

USA 2 YR BOND YIELD: 4.1348 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.47…

GREAT BRITAIN/10 YEAR YIELD: UP 8 BASIS PTS AT 3.8000

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Dip After Shock RBA Rate Hike As Fed Meeting Begins

TUESDAY, MAY 02, 2023 – 08:24 AM

US index futures saw modest declines on Tuesday as investors braced for this week’s Federal Reserve meeting where policymakers are expected to deliver another rate increase, and then pause the hiking cycle. S&P 500 contracts slid 0.1% as of 8:00 a.m. ET after earlier swinging between small gains and losses. Nasdaq 100 futures traded little changed. Both benchmarks closed steady on Monday after data showed that US factory activity contracted for a sixth-straight month in April, the longest such stretch since 2009.

In premarket trading, Chegg fell over 40% after the online education company warned that ChatGPT was threatening growth of its homework-help services. Sprouts Farmers Market gained 8% after the grocer published better-than-expected results and guidance. Uber rallied as much as 11% after the ride-hailing firm reported earnings and revenue that beat analysts’ estimates. Shares of peer Lyft also rose 2.9%. Here are the other notable premarket movers:

- Arista Networks falls as much as 8.8% as analysts said the cloud networking company’s first-quarter results and forecast for the second-quarter were strong, but flagged a lack of visibility for the second half of the year, especially regarding the company’s “cloud titan” customers.

- LendingTree plunges 22% after the firm cut its revenue guidance for the full year, missing the average of analysts’ estimates.

- MGM Resorts dips 1%, set to slip from their highest level in more than a year, after the entertainment resort operator gave an update for the first quarter. Analysts noted that the company flagged a slightly sparser events calendar for its Las Vegas business.

- Oramed gained as much as 2% after US conservative media entrepreneur Ben Shapiro took a stake of more than 4% in the struggling Israeli pharma company and was named to its board.

- Penn Entertainment rises 3.8% after Roth MKM upgrades the casino and gaming company to buy from neutral, anticipating that better-than-expected property margins in the first quarter will prompt investors to reevaluate their 2023 projections.

- Pfizer gains as much as 2.8% after the drugmaker reported revenue for the first quarter that beat the average of analysts’ estimates.

- SoFi Technologies Inc. dips 1.1% after Wedbush downgraded the online lender to neutral from outperform noting that there may be “downside risk to its gain on sale margins and fair value marks of its loan portfolio.”.

- Sprouts Farmers Market jumps as much as 8% after the grocery-store operator’s first-quarter results beat estimates, as did guidance for the second quarter. Analysts are positive on the company’s strategy and margin performance.

- Stag Industrial gains 7% after S&P Dow Jones Indices said that the real estate investment trust will replace Axon Enterprise in the S&P MidCap 400, effective before the market opens on May 4.

Global sentiment was subdued ahead of tomorrow’s (final) 25bps rate hike by the Fed, especially after Australia unexpectedly hiked rates showing central banks remain in inflation-fighting mode, and renewing concerns about a deeper US economic slowdown.

JPMorgan strategists predicted stocks would remain under pressure for the rest of the year as monetary tightening cools the economy and earnings weaken after a strong first quarter. Still, a deal on Monday for JPMorgan to acquire the troubled First Republic Bank boosted optimism that the recent banking turmoil “could well be in the rear-view mirror,” said Michael Hewson, chief analyst at CMC Markets in London (narrator: it’s not).

“This would be extremely welcome to jittery markets at a time when yields are rising again and recent economic data suggests that central bank may well have to continue to raise rates,” he said.

And while the rescue of First Republic Bank drew a line for now under US banking turbulence, investors now fear lending will be crimped, slowing an economy already under pressure from the most aggressive rate-hike campaign in decades. Euro-zone data reinforced these fears, showing banks had curbed lending more than anticipated.

“The banking crisis appears to have been dealt with, now it’s again all about inflation,” said Fahad Kamal, chief investment officer at SG Kleinwort Hambros Bank Limited. “Markets are wobbly because of the dichotomy between reasonably strong data and weak forward expectations, as there is concern over what may happen to corporate earnings due to the delayed effects of monetary policy.”

Attention now turns to the Fed, whose two-day policy meeting kicks off Tuesday. The central bank is expected to raise rates by a quarter percentage point and potentially signal a willingness to hold off on further increases. Focus is also on policymakers in Washington after Treasury Secretary Janet Yellen said the government might run out of money to pay its bills as early as June. Investors will also watch US JOLTS job openings, factory and durable goods orders today. Earnings will also garner attention, with more than 35 S&P 500 firms slated to report Tuesday, including Starbucks and Uber Technologies. Apple Inc.’s report is due Thursday.

European stocks traded in the red after coming back from Monday’s holiday following a busy day of corporate earnings, economic data and central bank policy speculation. The Stoxx 600 is down 0.3% with real estate, energy and media the worst performing sectors. Banks have outperformed, led by HSBC after the UK lender announced a new $2 billion share buyback plan. Here are the biggest European movers:

- HSBC shares rise as much as 6.1% in London, the most since November, after the bank’s quarterly profit topped expectations on better trading revenue, lower costs and fewer provisions

- Persimmon gains as much as 6.5% alongside other UK homebuilders, boosted by a report in The Times that the UK government is working on a new policy to support first-time buyers

- Logitech gains as much as 7.2%, the most since October, after the Swiss manufacturer of computer peripherals beat analyst estimates in quarterly sales for the first time in a year

- Electrolux rises as much as 10% to later pare some gains after Bloomberg reported that China’s Midea Group is exploring a potential acquisition of the Swedish home appliance company

- Kambi shares gain as much as 11%, the most in nearly a year, after the Swedish online betting services firm announced a multi-year sportsbook deal with US gambling firm Bally’s

- BP drops as much as 5.6% after the energy giant slowed the pace of share buybacks after a sharp drop in quarterly profit; while earnings beat estimates, cash flow momentum is likely to weaken

- Pearson falls as much as 7.3% Chegg, an American firm providing online guidance for students preparing tests, saw shares plummeting in US postmarket trading after it warned of AI competition

- Evolution falls as much as 5.4% after the Swedish online gambling firm was downgraded to neutral from buy at Citi, which in note says there is now limited upside scope shares in the coming months

- Ams-OSRAM falls as much as 8.8% after the chipmaker’s 2Q sales forecast missed expectations, with a downturn in the semiconductor industry continuing to hit demand for its products

- Traton falls as much as 2.1%, reversing initial gains, after raised margin guidance from the German truckmaker failed to impress. After strong 1Q performance, “all eyes” are on 2H demand, Citi says

Earlier in the session, Asian stocks were little changed, with investors digesting a slew of economic data from China for clues on the strength of the nation’s recovery, as most of the region’s markets resumed trading after a holiday. The MSCI Asia Pacific Index swung in a narrow range, with declines in industrials and consumer staples moderating gains in utilities stocks. Hong Kong equities also fluctuated, while key gauges rose in South Korea and were mixed in Japan. The Hang Seng China Enterprises Index wiped out an early gain of 2.1% as traders assessed China’s shrinking manufacturing activity. The official manufacturing purchasing managers’ index unexpectedly fell to 49.2 in April from 51.9 in March. Mainland markets are shut through Wednesday.

“Data brought back risks that China’s recovery is losing steam, and built the case for further policy support,” Saxo Capital Markets strategists wrote in a note. On the other hand, “travel demand during the Golden Week has started on a positive note,” they said. Investors also awaited the Federal Reserve’s rate decision scheduled for Wednesday. The US central bank is widely expected to hike interest rates again.

Australian stocks fell after the country’s central bank unexpectedly raised interest rates by a quarter-percentage point and signaled further policy tightening ahead. The S&P/ASX 200 index fell 0.9% to close at 7,267.40; the Aussie and bond yields surged. “A potential higher terminal rate is a risk and negative for equities,” said Matthew Haupt, a fund manager at Wilson Asset Management in Sydney. “It’s becoming a credibility issue now, these shocks to markets, and we need to add discount due to policy uncertainty,” he said. Read: RBA Shock Hike Spurs Strategist Clash About Global Rate Bets In New Zealand, the S&P/NZX 50 index rose 0.3% to 12,037.81.

Japanese stocks ended mixed in thin trading as investors geared up for a US rate decision and a domestic holiday this week. The Topix Index fell 0.1% to end at 2,075.53, while the Nikkei advanced 0.1% to 29,157.95. Toyota Motor Corp. contributed the most to the Topix Index’s decline, decreasing 0.5%. Out of 2,160 stocks in the index, 768 rose and 1,257 fell, while 135 were unchanged. “Although the yen has weakened after the BOJ decision and interest rates have fallen, making it easier to take risks,” the holiday-shortened week and the upcoming FOMC meeting make it hard to take a position, said Hiroshi Matsumoto, a senior client portfolio manager at Pictet Asset Management. Japan’s financial markets will be closed Wednesday through Friday for holidays.

India’s benchmark stocks gauge gained for the eighth straight session, supported by foreign buying while banks led earnings outperformance. The S&P BSE Sensex rose 0.4% to 61,354.71 in Mumbai on Tuesday, its highest close since Dec. 20, while the NSE Nifty 50 Index advanced 0.5%. The Sensex is now trading at 14-day RSI of 71, a level that some traders see as overbought, for the first time since it peaked all-time high in early December. However, India VIX Index – a measure of volatility expectations – continues to trade near its lowest level in three years. Banks in India, including top lenders such as HDFC Bank and Kotak Mahindra have reported strong earnings for the March quarter amid sustained loan growth. Out of 21 Nifty companies, which have so far reported earnings, 11 have matched or exceeded average analyst expectations, while eight have trailed. Two companies didn’t have comparable estimates. Tata Steel will be releasing its numbers later Tuesday. Infosys contributed the most to the Sensex’s gain, increasing 2%. Out of 30 shares in the Sensex index, 16 rose, while 14 fell.

In FX, the Bloomberg Dollar Spot Index is up 0.1% while the Australian dollar was the clear outperformer among the G-10s, jumping with local yields after the Reserve Bank unexpectedly resumed policy tightening. AUD/USA climbed as much as 1.3% to 0.6717 while Australia’s 3-year yield rose as much as 25bps to 3.26%, the highest since March. The RBA lifted the cash rate by 25 basis points to 3.85% while economists expected the rate to be left unchanged after data last week showed growth in consumer prices slowed more than expected in the first quarter. “The RBA is clearly still focused on inflation and feels it is still too high,” said Nick Twidale, chief executive Asia Pacific at FP Markets. “You’ve got to look to get long Aussie for the short to medium term, and it’s much more preferable to do it on the crosses than the dollar because we have so much uncertainty coming up with the Federal Reserve”

In rates, treasuries were richer across the curve, paring a portion of Monday’s sharp rate-lock driven selloff (courtesy of FB’s massive $8.5 billion new bond offering) as stock futures extended a retreat from Monday’s highs. During Asia session the Reserve Bank of Australia hiked its benchmark rate by 25bp to 3.85%, saying inflation remained too high and further tightening may be required. US yields are richer by 1bp to 4bp across the curve with gains led by intermediates, tightening the 2s5s30s fly by 3bp on the day; 10-year yields around 3.53%, lower by 4bps vs Monday’s close. Bund futures gapped lower but have pared some of that drop after the ECB bank lending survey and euro-area CPI data supported the view that the central bank will slow the pace of rate hikes this week. German 10-year yields are still up 5bps on the day. US session features 10am data raft including JOLTS job openings — which sparked gains last month — and factory orders.

In commodities, crude futures decline with WTI falling 0.4% to trade near $75.40. Spot gold is flat around $1,981.

Bitcoin is modestly firmer though is yet to convincingly extend above the USD 28k mark and as such remains well within the parameters of recent action.

Now looking at the day ahead, in the US we will get the March JOLTS report, factory orders, and April total vehicle sales. Meanwhile in Europe the main datapoints are the UK April Nationwide house price index, German March retail sales, and a bevy of Italian releases including April CPI, budget balance, new car registrations, manufacturing PMI, and March PPI. Additionally, this morning we will learn the Eurozone April CPI and March M3 level. In terms of central banks, we will get the important Eurozone bank lending survey. On earnings we will hear from Pfizer, HSBC, AMD, Starbucks, BP, Uber, Marriott, and Ford amongst others.

Market Snapshot

- S&P 500 futures down 0.1% to 4,180.00

- MXAP little changed at 160.56

- MXAPJ little changed at 515.64

- Nikkei up 0.1% to 29,157.95

- Topix down 0.1% to 2,075.53

- Hang Seng Index up 0.2% to 19,933.81

- Shanghai Composite up 1.1% to 3,323.28

- Sensex up 0.5% to 61,424.73

- Australia S&P/ASX 200 down 0.9% to 7,267.40

- Kospi up 0.9% to 2,524.39

- STOXX Europe 600 down 0.3% to 465.62

- German 10Y yield little changed at 2.34%

- Euro little changed at $1.0972

- Brent Futures down 0.4% to $79.03/bbl

- Gold spot down 0.1% to $1,981.44

- U.S. Dollar Index little changed at 102.16

Top Overnight News

- Australia’s RBA catches markets off guard with a surprise 25bp rate hike to 3.85% (most assumed they would stay on hold for an extended period) as the central bank warns that further increases may be required as inflation is still too elevated. RTRS

- Europe’s CPI for April ran hot at +7% on the headline (up from +6.9% in Mar and higher than the Street’s +6.9% forecast) while core ticked down only slightly (+5.6%, inline with the Street but off just fractionally from +5.7% in March). BBG

- ECB’s latest bank lending survey reveals a “further substantial tightening in credit standards for loans to firms and for house purchases” (“pace of net tightening in credit standards remained at the highest level since the euro area sovereign debt crisis in 2011”) while “demand for loans decreased strongly”. ECB

- BlackRock will begin selling failed banks’ municipal securities today, starting with an auction of about $50 million of taxable bonds, according to people familiar with the matter. BBG

- The FDIC said in its report that switching to a “targeted coverage” approach, where business accounts get more coverage than the current cap, would be the best option for financial stability. Such a change, however, would require congressional action. Other options include maintaining coverage as is, or switching to cover all deposits, the FDIC said. BBG

- Morgan Stanley may axe about 3,000 jobs this quarter, people familiar said, roughly 5% of its workforce, excluding advisers and people supporting them in the wealth management business. The banking and trading group is expected to be hit hard. In other banking woes, hundreds of Credit Suisse AT1 bondholders sued the Swiss regulator over their $1.7 billion loss. BBG

- Janet Yellen warned the Treasury may run out of cash at the start of June and Joe Biden invited lawmakers to a May 9 meeting to discuss raising the debt ceiling. The market is unsure about the timing. T-bill yields rose yesterday and pricing shows growing concern about a default in June. But the highest yields are in late July and August, with rates now above 5%. BBG

- Investors warn of First Republic aftershocks. Attendees at Milken financial conference fear credit crunch and sharper slowdown after banking turmoil. “There is a little bit of a tendency to kind of breathe a sigh of relief on mornings like this,” David Hunt, chief executive of $1.2tn asset manager PGIM, told Milken attendees digesting the First Republic rescue. “Actually, we’re just starting the implications for the US economy.” FT

- JPMorgan was the only bank with the appetite to buy substantially all of First Republic at a competitive price, including mortgages that other banks didn’t want. That was a priority for the FDIC because it removed uncertainty over any assets left behind that it would have to sell. WSJ

- Chegg Inc. plummeted 42% after warning that the ChatGPT tool is threatening growth of its homework-help services, one of the most notable market reactions yet to signs that generative AI is upending industries.

- Banks in the euro zone curbed lending more than anticipated after borrowing costs jumped and turmoil gripped the financial sector, reinforcing calls for the European Central Bank to slow the pace of its interest-rate hikes.

- HSBC shares rose after the Asia- focused lender announced a fresh plan to return money to shareholders after reporting first-quarter results that beat estimates.

- Morgan Stanley is preparing a fresh round of job cuts amid a renewed focus on expenses as recession fears delay a rebound in dealmaking.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded with a slight positive bias as many of the regional participants returned to the market from the long weekend albeit with gains capped ahead of this week’s upcoming risk events. ASX 200 was pressured after the RBA surprised markets with a 25bps rate increase, while the central bank’s language remained hawkish with the Board expecting some further tightening of monetary policy will be needed. Nikkei 225 was indecisive and pulled back after briefly touching its highest level since January last year. Hang Seng initially surged on reopening from the holiday weekend and was led higher by strength in tech and casino stocks with the latter buoyed after a jump in Macau gaming revenue, although the index later faded most of its gains while the mainland remained shut for golden week.

Top Asian News

- Japanese, South Korean and Chinese finance ministers and central bank governors said they recognise the importance of strengthening economic and trade relations, while they fully support the implementation of the Regional Comprehensive Economic Partnership agreement. However, they also noted that despite close economic relations, they have observed a recent slowdown in economic relations, according to Reuters.

- US President Biden and Philippines President Marcos affirmed the importance of maintaining peace and stability across the Taiwan Strait, while President Biden confirmed the US will send a presidential trade and investment mission to the Philippines, according to Reuters.

- RBA unexpectedly hiked the Cash Rate Target by 25bps to 3.85% (exp. pause), while it stated that the Board expects some further tightening of monetary policy will be needed and remains resolute in its determination to return inflation to target and will do what is necessary to achieve that. RBA stated that inflation in Australia has passed its peak, but at 7% is still too high and it will be some time yet before it is back in the target range. Furthermore, it stated some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but will depend upon how the economy and inflation evolve.

European stocks mostly decline after a long weekend, Euro Stoxx 50 -0.2%, with traders keeping an eye on various upcoming risk events; US equity futures hold a downward bias, ES -0.1%. In earnings, HSBC +4.5% beat expectations while BP -4.5% missed on revenue and guided towards lower Q2 refining margins. Stateside, futures are modestly softer but have picked up off lows as the European session progresses with the focus remaining firmly on the Fed, debt ceiling and earnings.

Top European News

- ECB bank lending survey – Q1 2023; net 27% of EZ banks reported tightening of lending standards for companies, 38% reported fall in demand for credit from companies. Banks indicated that their credit standards for loans or credit lines to enterprises tightened further substantially in the first quarter of 2023. Firms’ net demand for loans fell strongly in the first quarter of 2023. The decline in net demand was stronger than expected by banks in the previous quarter and the strongest since the global financial crisis.. Click here for more detail & newsquawk analysis.

- UK Foreign Secretary Cleverly says a meeting with China’s Vice President Han Zheng is likely.

- Ukraine Latest: Russia Seen Buying Foreign Currency Reserves

- European Stocks Slip Amid Earnings, Data Before Rates Decisions