MAY 3/2023 · by harveyorgan · in Uncategorized · Leave a comment·Editi

GOLD PRICE CLOSED: UP $13.90 TO $2028.20

SILVER PRICE CLOSED: UP 11 CENTS AT $25.42

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE $2030.65

Silver ACCESS CLOSE: 25.49

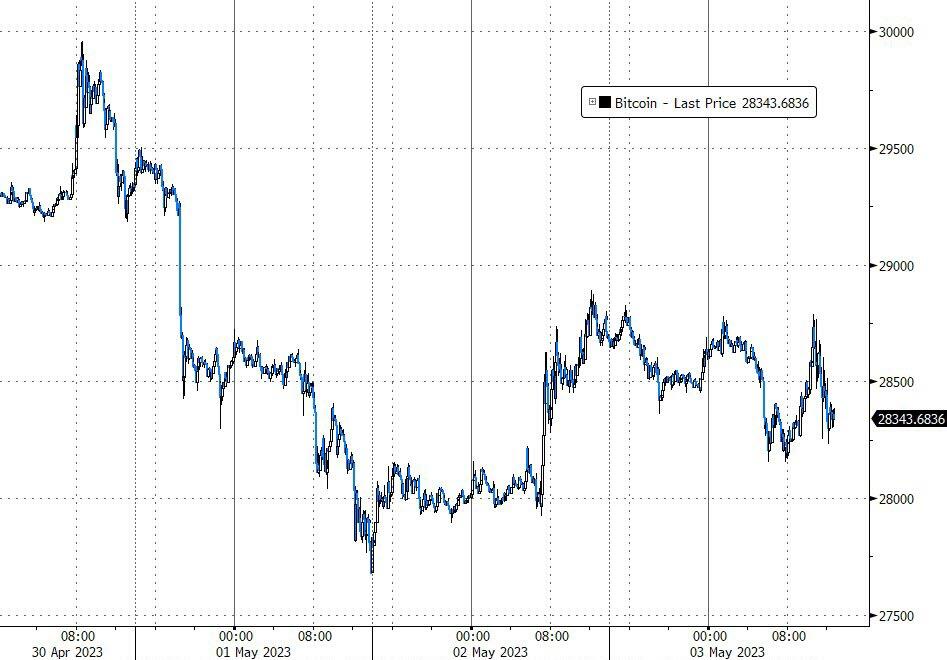

Bitcoin morning price:, $28,496 DOWN 133 Dollars

Bitcoin: afternoon price: $28,790 DOWN 179 dollars

Platinum price closing $1058.00 DOWN $8.80

Palladium price; $1431.70 DOWN $14.200

“Our government… teaches the whole people by its example. If the government becomes the lawbreaker, it breeds contempt for law; it invites every man to become a law unto himself; it invites anarchy.” … Louis D Brandeis (former Supreme Court Justice)

GO GATA!

TODAY WE HAD ANOTHER GREAT DAY FOR GOLD AND SILVER. LET US SEE HOW THE WEEK PLAYS OUT!! THE BANKERS ARE HAVING A TOUGHER TIME MANIPULATING OUR TWO PRECIOUS METALS.

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,765.51 UP 18.80 CDN dollars per oz (ALL TIME HIGH 2,765.51*) ALL TIME HIGH HIT TODAY

BRITISH GOLD: 1617.55 UP 1.838 pounds per oz//(ALL TIME HIGH//1629.84)

EURO GOLD: 1837,04 UP 6,19 euros per oz //(ALL TIME HIGH//1860.82)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

CONTRACT: MAY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,014.300000000 USD

INTENT DATE: 05/02/2023 DELIVERY DATE: 05/04/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 214

323 C HSBC 200

363 H WELLS FARGO SEC 309

435 H SCOTIA CAPITAL 42

624 H BOFA SECURITIES 889

661 C JP MORGAN 40 256

685 C RJ OBRIEN 1

690 C ABN AMRO 1

737 C ADVANTAGE 3 18

800 C MAREX SPEC 9

880 H CITIGROUP 1500

905 C ADM 6

TOTAL: 1,744 1,744

MONTH TO DATE: 2,992

JPMorgan stopped 256/1744 contracts

FOR MAY:

GOLD: NUMBER OF NOTICES FILED FOR MAY/2023. CONTRACT: 1744 NOTICES FOR 174,000 OZ or 5.4245 TONNES

total notices so far: 2992 contracts for 299,200 oz (9.3069 tonnes)

FOR MAY:

SILVER NOTICES: 0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month : 1687 for 8,435,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $13.90

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:///.A DEPOSIT OF 3.47 TONNES FROM THE GLD/

INVENTORY RESTS AT 928.30 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 11 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV???//: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 467.070 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 743 CONTRACTS TO 142,538 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS STRONG SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.34 GAIN IN SILVER PRICING AT THE COMEX ON MONDAY. WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.34). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A GIGANTIC GAIN ON OUR TWO EXCHANGES OF 1265 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 0 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 522 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.105 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 195,000 OZ9E.FP.’S LOWER THE AMOUNT OF SILVER STANDING)+ 0 MILLION OZ OF EXCHANGE FOR RISK:THUS TOTAL OF 12.740 MILLION OZ OF STANDING FOR DELIVERY V) HUGE SIZED COMEX OI GAIN/ STRONG SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –67 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTRACTS for 3 days, total 1410 contracts: OR 7.050 MILLION OZ . (470 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 7.050 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 7.050 MILLION OZ/INITIAL

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 743 CONTRACTS WITH OUR $0.34 GAIN IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 522 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 13.105 MILLION OZ//FIRST DAY NOTICE FOLLOWED BY TODAY’S E.F.P. JUMP OF 195,000 OZ (DECREASES THE AMOUNT OF SILVER STANDING) +// + 0 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //TOTAL STANDING 12.740 MILLION OZ// .. WE HAVE A HUGE SIZED GAIN OF 1265 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A HUGE SIZED 12,270 CONTRACTS TO 493,804 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: removed 735 CONTRACTS

WE HAD A HUGE SIZED INCREASE IN COMEX OI ( 12,270 CONTRACTS) WITH OUR $32.70 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR MAY. AT 3.5085 TONNES ON FIRST DAY NOTICE // PLUS A MONSTROUS 180,100 OZ QUEUE. JUMP :(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)////YET ALL OF..THIS HAPPENED WITH OUR $32.70 GAIN IN PRICE WITH RESPECT TO TUESDAY’S TRADING.WE HAD A GIGANTIC SIZED GAIN OF 17,232 OI CONTRACTS (53.598 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4762 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 493,804

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 17,232 CONTRACTS WITH 12,270 CONTRACTS INCREASED AT THE COMEX AND 4962 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 17,232 CONTRACTS OR 53.598 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4962 CONTRACTS) ACCOMPANYING THE HUGE SIZED GAIN IN COMEX OI (12,270 //TOTAL GAIN IN THE TWO EXCHANGES 17,270 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 3.5085 TONNES FOLLOWED BY TODAY’S MONSTROUS QUEUE JUMP OF 180,100 OZ // NEW STANDING: 9.9782 TONNES // ///3) ZERO LONG LIQUIDATION//4) HUGE SIZED COMEX OPEN INTEREST GAIN/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 8823 CONTRACTS OR 882,300 OZ OR 27.443 TONNES IN 3 TRADING DAY(S) AND THUS AVERAGING: 2941 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES 27.443 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 27.443/3550 x 100% TONNES 0.771% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES ( MUCH SMALLER THAN LAST MONTH)

MAY: 27.443 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A STRONG SIZED 743 CONTRACTS OI TO 142,538 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 522 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 522 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 522 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 743 CONTRACTS AND ADD TO THE 522 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1265 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 6.325 MILLION OZ

OCCURRED WITH OUR $0.34 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED //Hang Seng CLOSED DOWN 234.65 POINTS OR 1.18% /The Nikkei closed UP 34,77 PTS OR 0.12% //Australia’s all ordinaries CLOSED DOWN 0.95 % /Chinese yuan (ONSHORE) closed /OFFSHORE CHINESE YUAN UP TO 6.9209 /Oil UP TO 69.42 dollars per barrel for WTI and BRENT AT 73.23 / Stocks in Europe OPENED MOSTLY GREEN// ONSHORE YUAN TRADING XXX LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING XXX AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A HUGE SIZED 12,270 CONTRACTS UP TO 493,804 WITH OUR STRONG GAIN IN PRICE OF $32.70 ON TUESDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF MAY… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4962 EFP CONTRACTS WERE ISSUED: : JUNE 4962 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4962 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GIGANTIC SIZED TOTAL OF 17,232 CONTRACTS IN THAT 4962 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A HUGE SIZED GAIN OF 12,270 COMEX CONTRACTS..AND THIS GIGANTIC SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $32.70. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (4.3763) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 9.9782 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $32.70) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR GIGANTIC SIZED GAIN OF 17,232 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 53.598 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY. (3.5085 TONNES) FOLLOWED BY TODAY’S RECORD SETTING QUEUE JUMP OF 180,100 oz (5.601 TONNES)//NEW STANDING 9.9782 TONNES ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $32.70

WE HAD +REMOVED 735 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 17,232 CONTRACTS OR 1,723,200 OZ OR 53.598 TONNES.

Estimated gold comex today 197,424 fair//

final gold volumes/yesterday 264,647 fair

//MAY 3/ MAY 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 707.322 oz 22 KILOBARS Int Delaware . |

| Deposit to the Dealer Inventory in oz | 21,798.378 OZ Brinks 678 kilobars |

| Deposits to the Customer Inventory, in oz | 160,755.000 Oz JPM 5,000 kilobars |

| No of oz served (contracts) today | 1744 notice(s) 174400 OZ 5.4245 TONNES |

| No of oz to be served (notices) | 216 contracts 21,600 oz 0.6718 TONNES |

| Total monthly oz gold served (contracts) so far this month | 2992 notices 299,200 OZ 9.3069 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 1

i) Out of Int. Delaware: 707.322 oz (22 kilobars)

total withdrawals: 707.322 oz

Adjustments;

ii) customer to dealer Manfra: 23,148.730 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 1960 contracts having GAINED 1759 contracts. We had 42 contracts filed

on TUESDAY, so we gained a monstrous 1801 contracts or an additional 180,100 oz (5.6 tonnes) will stand for gold in this non active delivery month of May.

This is the highest ever recorded queue jump in comex history surpassing last year’s 5.3 tonne queue jump.

June GAINED 4350 contracts UP to 378.608 contracts.

July added 147 contracts to stand at 624 contracts.

AUGUST GAINED 4724 contracts up to 67,443 contracts

We had 1744 contracts filed for today representing 174,400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 40 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1744 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 256 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2023. contract month,

we take the total number of notices filed so far for the month (2,992 x 100 oz ), to which we add the difference between the open interest for the front month of MAY 1960 CONTRACTS) minus the number of notices served upon today 1744 x 100 oz per contract equals 320,800 OZ OR 9.9782 TONNES the number of TONNES standing in this NON- active month of May.

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (2992 x 100 oz)+1960 OI for the front month minus the number of notices served upon today (1744)x 100 oz} which equals 320,800 oz standing OR 9.9782 TONNES

TOTAL COMEX GOLD STANDING: 9.9782 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,713,349.037 OZ 53.29 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,591,465.739OZ

TOTAL REGISTERED GOLD: 12,381,513,895 (385,11 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,137,951.844 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,668,164 OZ (REG GOLD- PLEDGED GOLD) 331.824 tonnes//

END

SILVER/COMEX

MAY 3//2023// THE MAY 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 337,478.190 oz Brinks CNT Delaware . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 0 CONTRACT(S) (nil OZ) |

| No of oz to be served (notices) | 861 contracts (4,305,000 oz) |

| Total monthly oz silver served (contracts) | 1687 Contracts (8,435,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

Total deposits: nil oz

JPMorgan has a total silver weight: 139,607 million oz/269.687 million =51.76% of comex .//dropping fast

Comex withdrawals: 3

i) Out of Brinks 315,383,930 oz

ii) Out of CNT: 19,991.69 oz

iii) Out of Delaware 2102,570 oz

Total withdrawals; 337,478.190 oz

adjustments: 1 dealer to customer JPMorgan 717,302.930oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 32.487 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 269.687 million oz

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY /2023 OI: 861 CONTRACTS HAVING LOST 52 CONTRACT(S). WE HAD 13 CONTRACTS FILED

ON TUESDAY, SO WE LOST 39 CONTRACTS OR AN ADDITIONAL 195,000 OZ OF SILVER WILL NOT STAND FOR DELIVERY IN THIS VERY

ACTIVE DELIVERY MONTH OF MAY AS, FOR THE 2ND DAY IN A ROW, THESE GUYS WERE E.F.P.’d TO LONDON AS NO SILVER COULD BE FOUND OVER HERE..

.JUNE HAD A 1 CONTRACT GAIN TO 872

JULY HAD A 523 CONTRACT GAIN TO 121,227 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for nil oz

Comex volumes// est. volume today 45,226 fair

Comex volume: confirmed yesterday: 69,956 good

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 1687 x 5,000 oz = 8,435,000 oz

to which we add the difference between the open interest for the front month of MAY(861) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2023 contract month: 1687 (notices served so far) x 5000 oz + OI for the front month of May (861) – number of notices served upon today (0 )x 500 oz of silver standing for the MAY contract month equates to 12.740 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

APRIL 10/WITH GOLD DOWN $21.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91 TONNES

APRIL 6//WITH GOLD DOWN $9.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91

APRIL 5//WITH GOLD UP 0 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04

APRIL 4/WITH GOLD UP $36.30 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

APRIL 3/WITH GOLD UP $14.20 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.02 TONNES

MARCH 31/WITH GOLD DOWN $10.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD////INVENTORY RESTS AT 928.02 TONNES

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

GLD INVENTORY: 928.34 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 10/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 6/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 4.643 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 468.585 MILLION OZ//

APRIL 5/WITH SILVER DOWN 4 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.942 MILLION OZ

APRIL 4/WITH GOLD UP $1.11 TODAY CRIMINAL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.47 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 463,942 MILLION OZ

APRIL 1/WITH SILVER DOWN 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.412

MARCH 31/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD/: A MASSIVE 4.779 MILLION OZ DEPOSITED INTO THE SLV///INVENTORY RESTS AT465.412 MILLION OZ

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

CLOSING INVENTORY 467.070 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

The US Banking System Is Sound?

A must read

(Michael Maharrey/SchiffGold)

WEDNESDAY, MAY 03, 2023 – 07:20 AM

Authored by Michael Maharrey via SChiffGold.com,

Treasury Secretary Janet Yellen keeps insisting that the banking system is “sound.”

Is it though? Because it doesn’t look particularly sound.

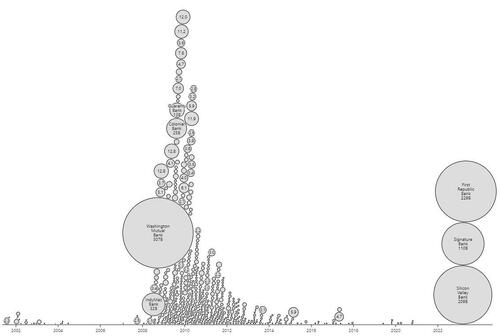

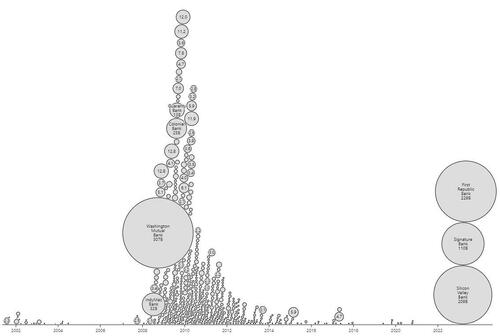

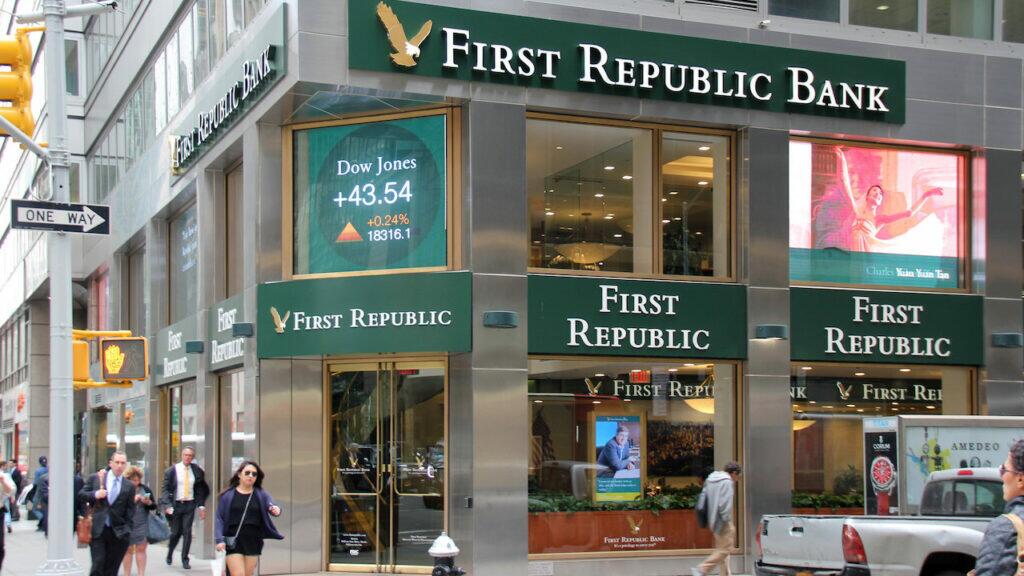

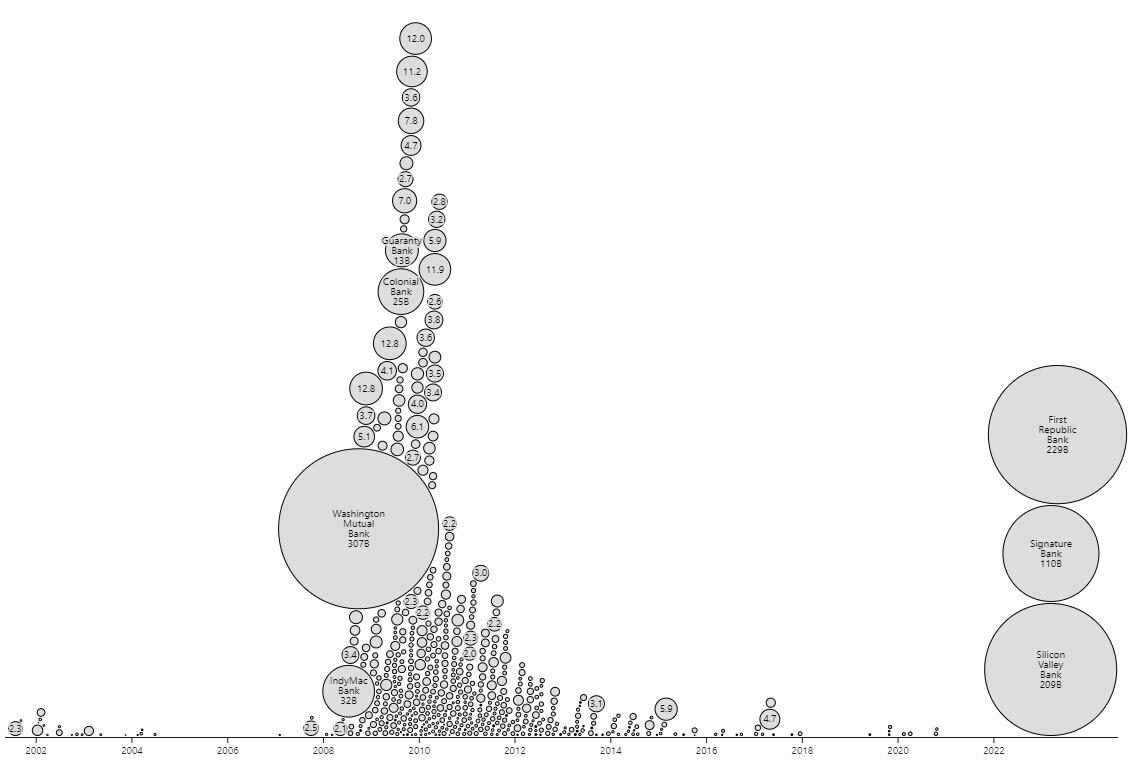

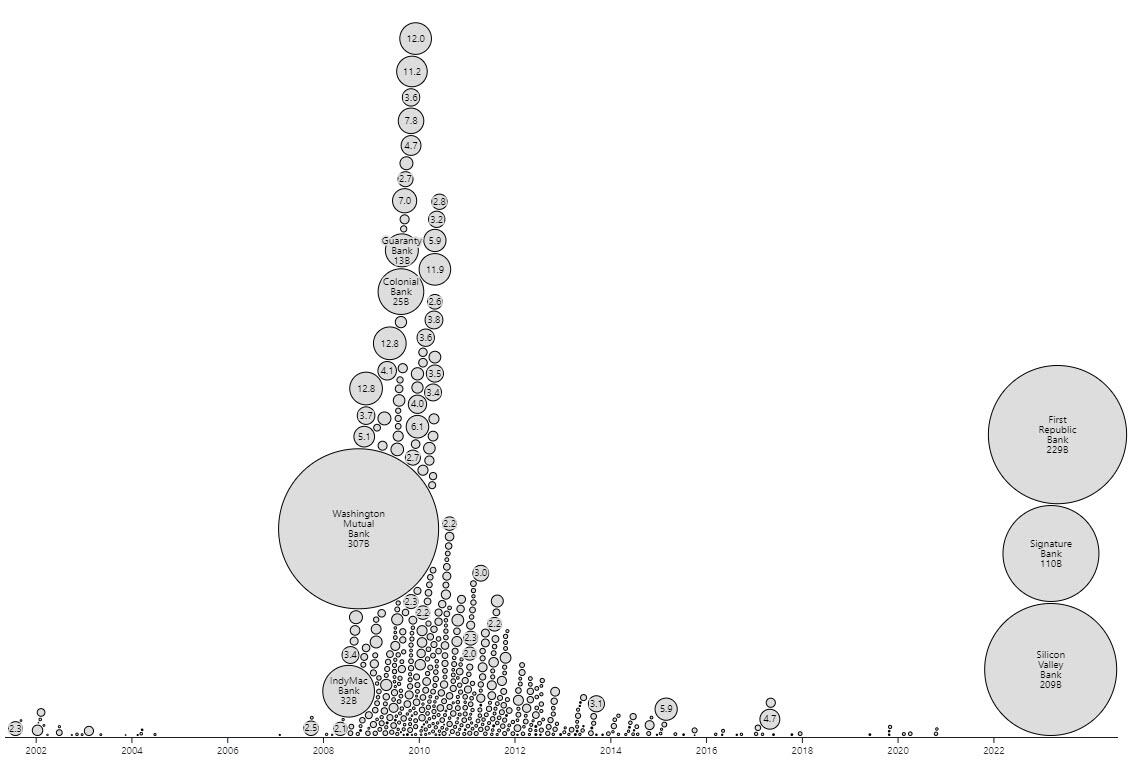

In fact, we just witnessed the second-largest US bank failure ever.

Government regulators seized control of First Republic Bank on May 1 and sold the majority of the bank’s operations to JP Morgan Chase. It was the third major bank failure this year and the biggest bank to collapse since the 2008 financial crisis. It was the second-largest bank by assets to fail in US history.

First Republic went under after it revealed $100 billion in deposit losses in the first quarter.

The beleaguered bank has been struggling for a while. It was initially bailed out back in March with $30 billion in deposits from several large banks, including JP Morgan and Wells Fargo. The bank also borrowed heavily from the Federal Reserve’s bank bailout program. First Republic shares tumbled 75% last week before the FDIC stepped in.

While JP Morgan is taking over First Republic’s business, the FDIC will provide “shared-loss agreements.” As the FDIC website explains it, “the FDIC absorbs a portion of the loss on a specified pool of assets sold through the resolution of a failing bank – in effect sharing the loss with the purchaser of the failing bank.”

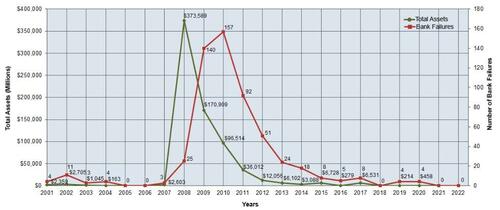

If we are to believe the mainstream narrative, the failures of Silicon Valley Bank, Signature Bank and First Republic Bank were isolated events and do not reflect a broader problem in the banking system. But as we have reported, these bank failures are just the tip of the iceberg. A report by the Wall Street Journal cites a study from Stanford and Columbia Universities that found 186 US banks are in distress.

And as Manuel Garcia Gojon pointed out in an article published by the Mises Wire, it’s not just the small and medium-sized banks. Charles Schwab and other big banks may also be insolvent.

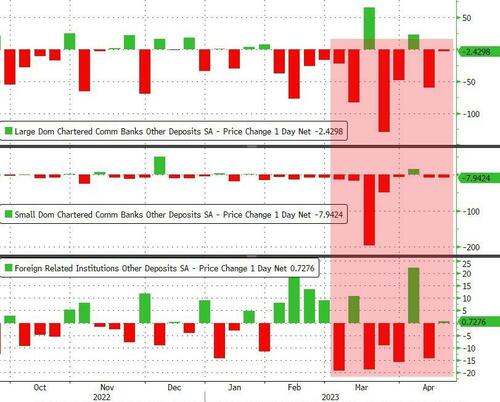

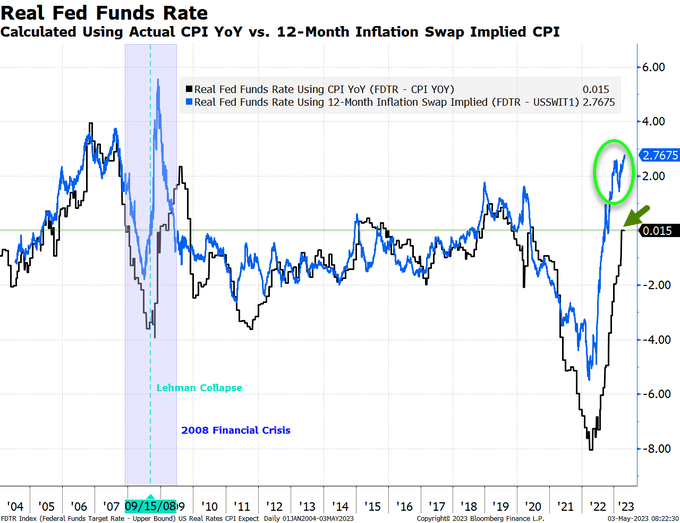

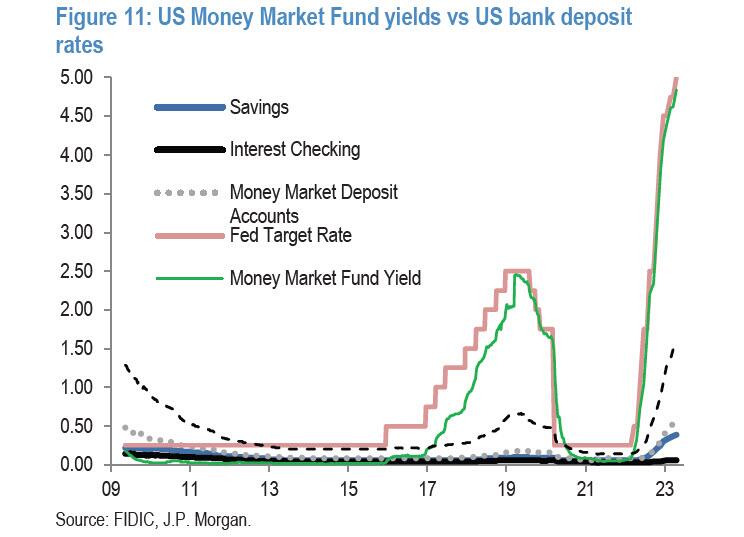

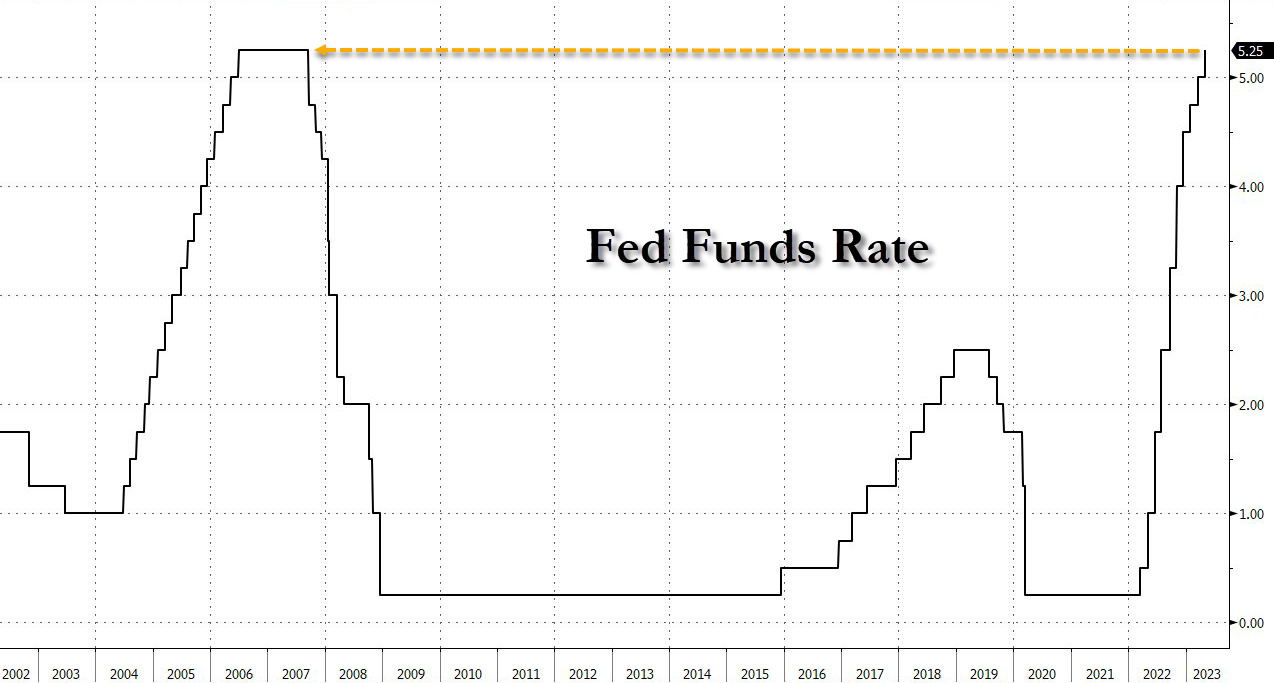

One of the biggest problems facing banks is the rapid devaluation of their bond portfolios.

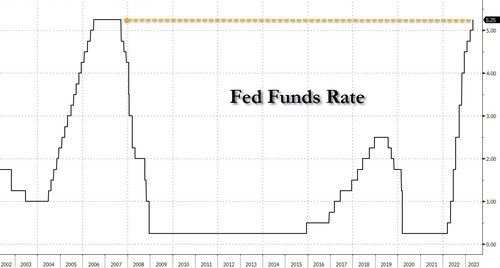

Banks were incentivized to load up on high-priced, low-yield bonds thinking that the Fed would keep interest rates low forever. As the Fed jacked up interest rates to fight price inflation, it decimated the bond market. (Bond prices and interest rates are inversely correlated. As interest rates rise, bond prices fall.) With interest rates rising so quickly, banks have not been able to adjust their bond holdings. As a result, many banks have become undercapitalized on paper as the value of the bond portfolios shrinks. The banking sector was buried under some $620 billion in unrealized losses on securities at the end of last year, according to the Federal Deposit Insurance Corp.

As the Washington Post reported, this means banks would face unprecedented losses if they were forced to liquidate their bond portfolios. In fact, that is exactly what doomed Silicon Valley Bank. The plan was to sell the longer-term, lower-interest-rate bonds and reinvest the money into shorter-duration bonds with a higher yield. Instead, the sale dented the bank’s balance sheet and caused worried depositors to pull funds out of the bank.

According to the Post, the total capital buffer in the US banking system totals $2.2 trillion. Meanwhile, total unrealized losses in the system based on a pair of academic papers is between $1.7 and $2 trillion.

Gojon explains how the big banks have dealt with this problem

Many big banks in the United States have substantially increased their use of an accounting technique that allows them to avoid marking certain assets at their current market value, instead using the face value in their balance sheet calculations. This accounting technique consists of announcing that they intend to hold such assets to maturity.”

In other words, this accounting trick makes the bank look far more solvent than it actually is.

At the end of 2022, Charles Schwab had the largest amount of assets marked as “held to maturity” relative to capital. According to data cited by Gojon, Schwab had over $173 billion in assets marked as “held to maturity,” while its capital (assets minus liabilities) stood at under $37 billion. At that time, the difference between the market value and face value of assets held to maturity was over $14 billion.

If the accounting technique had not been used the capital would have stood at around $23 billion. This amount is under half the $56 billion Charles Schwab had in capital at the end of 2021. This is also under 15 percent of the amount of assets held to maturity, under 10 percent of securities, and under 5 percent of total assets. An asset ten years from maturity is reduced in present value by 15 percent with a 3 percent increase in the interest rate. An asset twenty years from maturity is reduced in present value by 15 percent with a 1.5 percent increase in the interest rate.”

Other banks that may be close to effective insolvency include the Bank of Hawaii and the Banco Popular de Puerto Rico (BPPR). According to Gojon, the Bank of Hawaii, BPPR, and Charles Schwab have lost between one-third and one-half of their market capitalization over the last month.

Gojon concedes that it’s hard to know how this will play out, but he said there is clearly a large amount of risk in the banking system.

It is difficult to say with certainty whether they are indeed secretly close to insolvency as they may have some form of insurance that could absorb some of the impact from a loss of value in their assets, but if this were the case it is not clear why they would need to employ this questionable accounting technique so heavily. The risk of insolvency is currently the highest it’s been in over a decade.”

Gojon said the Fed can solve liquidity problems even as it continues to raise interest rates to fight inflation. That’s the whole point of the bank bailout program. But he said the Fed can’t fix solvency problems without pivoting to looser monetary policy or through more blatant bank bailouts. Those scenarios would both raise inflation expectations.

The bottom line is that despite Janet Yellen’s constant assurances, the banking system is not sound. It is a house of cards that could fall down at any time.

end

Peter Schiff: The Fed Has Screwed Up Everything That Is A Function Of Interest Rates

WEDNESDAY, MAY 03, 2023 – 10:20 AM

The failure of First Republic Bank reveals that the banking system isn’t nearly as sound as Treasury Secretary Janet Yellen and Federal Reserve Chairman Jerome Powell would have us believe. But as Peter explained in a recent podcast, it’s not just the banking system that’s messed up. The Fed has screwed up everything that is a function of interest rates by keeping rates at zero for so long.

First Republic was the third major bank failure this year and the biggest bank to collapse since the 2008 financial crisis. It was the second-largest bank by assets to fail in US history. Peter said the whole banking system is a house of cards that is now collapsing one card at a time.

We’re still in the early days of the 2023 financial crisis.”

Of course, the mainstream media remains reluctant to call it a financial crisis. But if not, what is it?

Banks keep failing. Aren’t banks financial institutions? But no, they don’t want to do it because they don’t want to evoke the memory of 2008. They don’t want anyone to think that what we’re experiencing is another 2008. Now, in a way they’re right, because it’s not another 2008. It’s going to be way worse than 2008. But it is a financial crisis.”

And Peter said it’s not just banks.

The Fed screwed up everything that is a function of interest rates. Anything that is rate-sensitive is all screwed up because rates were so low for so long.”

This includes the auto market and the housing market.

Fed monetary policy also facilitated massive government budget deficits.

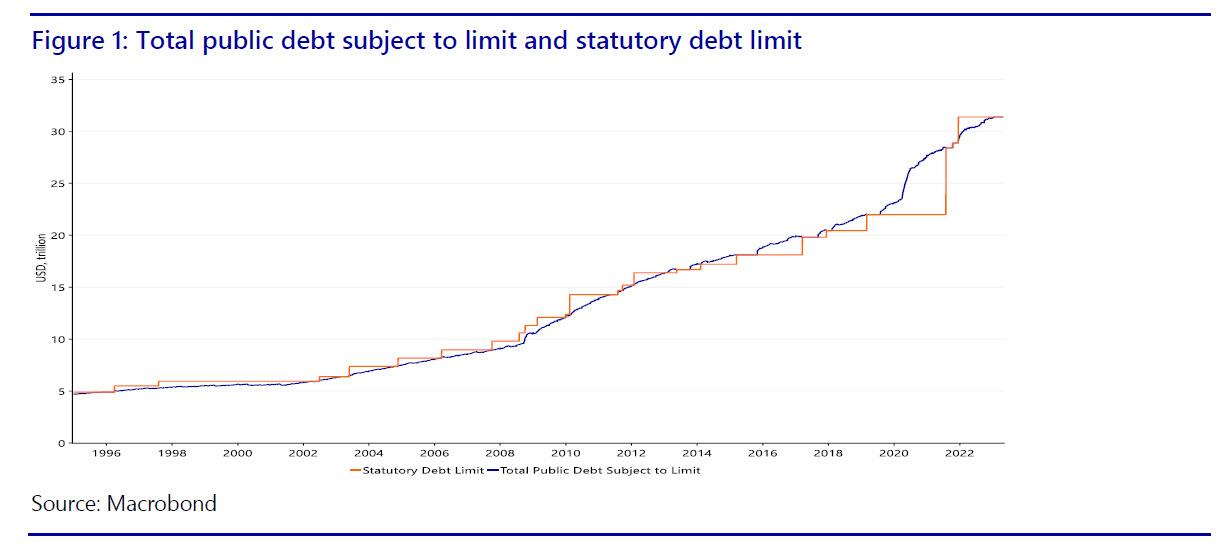

How are we able to sustain a $31.7 trillion national debt? It’s because interest rates were so low. If the Federal Reserve had not kept interest rates at zero for so long, had interest rates reflected the appropriate price of money that a free market would set, there is no way the government could have gotten away with this. Government could not be this big. Government could not have spent all this money because it couldn’t have afforded to pay the interest on the debt.”

Now that the Fed has let rates go up, everything that was built on a foundation of zero percent crashes – including the government.

The government is going to come crashing down if the Fed holds the line on fighting inflation. … We can’t have these deficits and normal interest rates to fight inflation. So, the government is going to be forced to downsize dramatically, make big cuts in government spending, if the Fed is going to continue to fight inflation and keep rates up, which I don’t think it’s going to do.”

Peter said he thinks the Fed is going to reverse course to keep banks from failing, stop the auto industry from imploding, save the housing market, and prop up the government.

And then there is corporate America, which has also levered up thanks to easy money.

What’s going to happen over the next year or two as all this cheap money that they borrowed to buy back their overpriced stock comes due? What about all of the junk bonds that are out there?”

We’re already starting to see bankruptcies. Bed Bath and Beyond recently filed Chapter 11. In fact, there have been 70 major bankruptcies already in 2023. It’s the third-worst start to a year ever. That compares with 71 bankruptcies in the early part of 2020 when governments shut down the economy for COVID. The only other year that was worse was 2009, in the depths of the Great Recession.

In this podcast, Peter also talks about the first quarter GDP data, noting that economic growth is slowing down even as inflation is picking up speed.

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDSJOHN RUBINO

PAM AND RUSS MARTENS://WALL STREET ON PARADE

By Pam Martens and Russ Martens: May 3, 2023

President Joe Biden is putting the national security of the United States at risk by not suspending the short-selling of federally-insured banks. Concerns over the safety and soundness of the U.S. financial system could cause money flight out of the U.S., impacting the strength of the U.S. dollar and a loss of confidence by our foreign allies.

This is also a matter that impacts the financial lives of every American, because every American – rich, poor or middle class – will suffer the consequences in terms of ability to access bank credit and higher fees on that credit as a result of rebuilding the rapidly depleting federal Deposit Insurance Fund that protects bank deposits.

The second, third and fourth largest bank failures in the history of the U.S. have now occurred in the span of seven weeks (First Republic Bank, Silicon Valley Bank and Signature Bank, respectively) with the Federal Deposit Insurance Corporation (FDIC) taking big hits in each case to its Deposit Insurance Fund.

At the time of First Republic Bank’s failure on Monday (with JPMorgan Chase given a very sweet deal by the FDIC to buy its underwater assets and take over the deposits that hadn’t yet fled), it was one of the most heavily shorted bank stocks with one-third of its outstanding shares shorted as of one week before it failed, according to a report from Reuters.

First Republic Bank was not a small bank. At the time of its demise, it had $207.5 billion in assets. According to a statement from the FDIC on Monday, it “estimates that the cost to the Deposit Insurance Fund will be about $13 billion. This is an estimate and the final cost will be determined when the FDIC terminates the receivership.”

The FDIC estimated the cost to the Deposit Insurance Fund in the failure of Silicon Valley Bank to be $20 billion, and the cost to the DIF in the failure of Signature Bank to be $2.5 billion.

All of these FDIC estimates seem very optimistic but even if they are accurate, that’s a combined hit thus far of $35.5 billion to a Deposit Insurance Fund that had just $128.2 billion as of December 31, 2022.

On April 18 – prior to the failure of First Republic Bank – the FDIC released the following statement:

“The Federal Deposit Insurance Act (FDI Act) requires that the FDIC’s Board of Directors adopt a restoration plan when the Fund’s reserves fall below 1.35 percent of all insured deposits held in FDIC-insured financial institutions. Extraordinary deposit growth during the first and second quarters of 2020 caused the Fund’s reserve ratio to decline below this statutory minimum. On September 15, 2020, the FDIC established a plan to restore the Fund’s reserves to at least 1.35 percent by September 30, 2028, while maintaining the assessment rate schedule in place at the time.”

In short, assessments on banks to restore the Deposit Insurance Fund are going to be going up as a result of these bank failures and attendant losses – which mean that banks are going to be passing those increased costs along to their customers. If more banks fail, those costs will rise exponentially, putting aside the more critical issue of loss of confidence in the U.S. banking system.

This is not some abstract theory. The newest target of the short sellers is PacWest Bancorp (ticker PACW). According to S&P Global Market Intelligence, as of March 31, 20.6 percent of PacWest’s shares outstanding were sold short, making it the third largest shorted bank stock at that point. (The bank stock with the largest percentage of shares shorted on March 31 was Silvergate Bank, which became an easy target of short sellers because it had entangled itself with crypto companies, including Sam Bankman-Fried’s house of frauds, FTX and Alameda Research. Silvergate wound itself down voluntarily by the end of the first quarter. The second largest short position in a bank as of March 31 was in First Republic Bank, which failed on Monday.)

PacWest Bancorp is showing similar distress. PacWest’s stock has lost 71 percent year-to-date. On Monday and Tuesday of this week, the stock has gone from a closing price of $10.15 on Friday to $6.55 at the close on Tuesday – a stunning collapse of 35 percent in just two trading sessions.

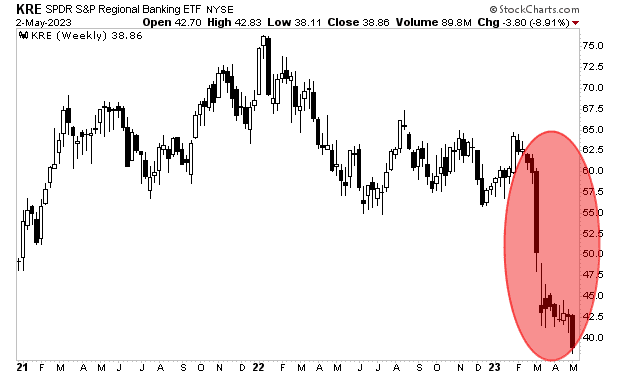

Other banks that are targets of short sellers that have seen outsized year-to-date losses in share price include Western Alliance, Comerica, Zions Bank, Republic First Bancorp (no relation to First Republic Bank other than similarity of its name, which may be why short sellers have piled on). Those stocks are down anywhere from 45 to 60 percent year-to-date versus a decline of 27 percent in the regional bank index (ticker KRX). See chart above.

The longer President Biden waits to sign an executive order suspending short sales in federally-insured banks, the faster the contagion will spread to other banks.

Editor’s Note: We believe that, in general, short sellers perform a critical role in U.S. markets – calling attention to corporate corruption and fraud that has been missed by regulators and the media. But the rapidly deteriorating condition of U.S. banks is a function of the unprecedented span of time that the Fed kept interest rates at the zero interest level, forcing banks to make fixed-rate mortgage loans at 3, 4 and 5 percent interest in order to remain competitive. Those loans and their related mortgage-backed securities are now underwater as a result of the Fed raising rates faster than at any time in the last 40 years. Exceptional times call for exceptional actions. President Biden needs to step up to the plate

END

END

3,Chris Powell of GATA provides to us very important physical commentaries

U.S. Rep. Alex Mooney, advocate of a free gold market, seeks West Virginia Senate seat

Submitted by admin on Wed, 2023-05-03 03:14Section: Daily Dispatches

Race for West Virginia U.S. Senate seat heating up

From WOWK-TV, Huntington, West Virginia

Tuesday, May 2, 2023

CHARLESTON, W. Va. — The race for a contested U.S. Senate seat in West Virginia is already getting heated. It also looks to get very expensive.

It is a contested Republican primary, and that usually means a lot of sharp elbows and advertising money being spent.

“Liberal Jim Justice just can’t be trusted,” says an attack ad produced for the U.S. Senate campaign of U.S. Rep. Alex Mooney, R-West Virginia.

The Mooney for Senate campaign is running critical ads against his Republican primary opponent, Gov. Jim Justice.

Justice was first elected as a Democrat and seven months into his first term switched to the Republican Party.

While Justice says he has a conservative record, Mooney claims that he is the more conservative of the two candidates.

“We’ll debate those issues as we go along. I’m the only candidate, I believe, with an A-plus rating from the National Rifle Association.” …

… For the remainder of the report:

https://www.wowktv.com/news/west-virginia/race-for-west-virginia-us-senate-seat-heating-up

end

A great read: Evans-Pritchard correctly states that over half of the USA banks may be insolvent

(zerohedge)

Ambrose Evans-Pritchard: Half of U.S. banks may be insolvent and this is how a credit crunch begins

Submitted by admin on Wed, 2023-05-03 00:10Section: Daily Dispatches

By Ambrose Evans-Pritchard

The Telegraph, London

Tuesday, May 2, 2023

The twin crashes in U.S. commercial real estate and the U.S. bond market have collided with $9 trillion uninsured deposits in the American banking system. In the cyber age such deposits can vanish in an afternoon.

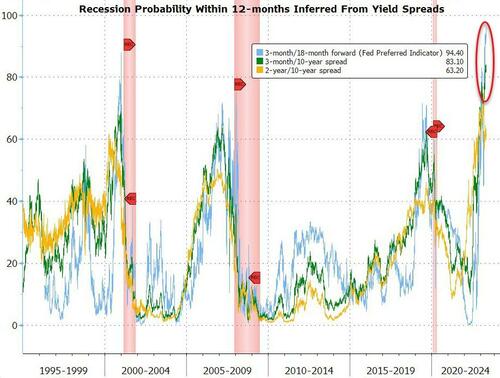

The second and third biggest bank failures in U.S. history have followed in quick succession. The U.S. Treasury and Federal Reserve would like us to believe that they are “idiosyncratic.” That is a dangerous evasion

Almost half of America’s 4,800 banks are already burning through their capital buffers. They may not have to mark all losses to market under U.S. accounting rules but that does not make them solvent. Somebody will take those losses.

“It’s spooky. Thousands of banks are under water,” said Professor Amit Seru, a banking expert at Stanford University. “Let’s not pretend that this is just about Silicon Valley Bank and First Republic. A lot of the U.S. banking system is potentially insolvent.”

The full shock of monetary tightening by the Fed has yet to hit. A great edifice of debt faces a refinancing cliff-edge over the next six quarters. Only then will we learn whether the U.S. financial system can safely deflate the excess leverage induced by extreme monetary stimulus during the pandemic. …

… For the remainder of the analysis:

END

The insolvencies of over 50% of the banks and the lousy JOLTS reports propels gold/silver

(zerohedge)

Craig Hemke at Sprott Money: Comex gold JOLTed again

Submitted by admin on Wed, 2023-05-03 00:00Section: Daily Dispatches

10:58a ICT Wednesday, May 3, 2023

Dear Friend of GATA and Gold (and Silver):

Writing at Sprott Money, Craig Hemke of the TF Metals Report says the latest U.S. jobs report’s indication of recession and the continued insolvencies of U.S. banks support expectations that Federal Reserve interest rate increases will be reversed and that the monetary metals will rise.

Hemke’s analysis is headlined “Comex Gold JOLTed Again” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/blog/comex-gold-jolted-again-may-02-2023

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

END

5.IMPORTANT COMMENTARIES ON COMMODITIES: RICE

Huge global rice shortage looms!

(zerohedge)

Global Rice Shortage Looms, Set To Be The Biggest In Decades

WEDNESDAY, MAY 03, 2023 – 05:45 AM

Rice is the primary food source for over half of the global population, especially in emerging markets, where it plays a crucial role in feeding people. Last year, we highlighted the potential for a severe global rice shortage. A new report reveals that rice production this year could be at its lowest in decades.

A report by Fitch Solutions forecasts this year’s global rice production will log its biggest shortfall in two decades. The deficit will be a major headache for countries relying on grain imports.

“At the global level, the most evident impact of the global rice deficit has been, and still is, decade-high rice prices,” Fitch Solutions’ commodities analyst Charles Hart told CNBC.

Sliding rice production in China, the US, and Europe is already causing grain prices to increase for 3.5 billion people, particularly in the Asia-Pacific region — this region of the world accounts for 90% of the world’s rice consumption.

“Given that rice is the staple food commodity across multiple markets in Asia, prices are a major determinant of food price inflation and food security, particularly for the poorest households,” Hart said.

Hart said this year’s global shortfall would be around 8.7 million tons, the largest global rice deficit since 2003/2004 of 18.6 million.

As a result of tightening global supplies, rough rice futures trading on the CBoT recently peaked at $18 per cwt, the highest level since September 2008. Cwt is a unit of measurement for certain commodities such as rice.

CNBC provides a breakdown of why rice supplies are strained.

There’s a short supply of rice as a result of the ongoing war in Ukraine, as well as bad weather in rice-producing economies like China and Pakistan.

In the second half of last year, swaths of farmland in the world’s largest rice producer China were plagued by heavy summer monsoon rains and floods.

The accumulated rainfall in the country’s Guangxi and Guangdong province, China’s major hubs of rice production, was the second highest in at least 20 years, according to agriculture analytics company Gro Intelligence.

Similarly, Pakistan — which represents 7.6% of global rice trade — saw annual production plunge 31% year-on-year due to severe flooding last year, said the US Department of Agriculture (USDA), labeling the impact as “even worse than initially expected.”

The shortfall is partly due to result of “an annual deterioration in the Mainland Chinese harvest caused by intense heat and drought as well as the impact of severe flooding in Pakistan,” Hart pointed out.

Rice is a vulnerable crop, and has the highest probability of simultaneous crop loss during an El Nino event, according to a scientific study.

Recall in the late summer of 2022. We told readers:

- The Stage Is Being Set For A Massive Global Rice Shortage

- “Situation Is Really Precarious”: World’s Largest Rice Exporter Faces Output Decline Amid Heatwave

… and just recently.

The takeaway is that a tight global rice market will raise food inflation for major rice importers such as Indonesia, the Philippines, Malaysia, and Africa. Elevated food inflation is dangerous for governments because it increases social instability risks.

end

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

We now know how JPMorgan received a $50 dollar loan to assist them in their takeover of First Republic Bank. Initially they stated that the loan must from the FDIC but they are not allowed to loan money. The answer came this morning, when the Treasury reported a massive $87 billion fall in their cash accounts. Thus the taxpayer loaned money to JPMorgan to bailout all the depositors of FRC. The problem now is the drop dead deadline for debt ceiling will now be May 15 or May 16. Again the Fed/Treasury lied when they stated that taxpayers will no longer bail out banks. Wrong!

1.YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS// WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED

OFFSHORE YUAN: 6.9209

SHANGHAI CLOSED

HANG SENG CLOSED DOWN 236.65 PTS OR 1.18%

2. Nikkei closed UP 34.77 PTS OR 0.12%

3. Europe stocks SO FAR: MOSTLY RED

USA dollar INDEX UP TO 101.31 EURO RISES TO 1.1043 UP 33 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.415 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 135.56 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: XX// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.2345***/Italian 10 Yr bond yield FALLS to 4.123*** /SPAIN 10 YR BOND YIELD FALLS TO 3.299…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.057

3j Gold at $2015.70 silver at: 25.29 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 33 /100 roubles/dollar; ROUBLE AT 79.28//

3m oil into the 69 dollar handle for WTI and 75 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 135.56 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .415% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8887 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9812 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.412 DOWN 3 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.698 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 3.974 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.48…

GREAT BRITAIN/10 YEAR YIELD: DOWN 11 BASIS PTS AT 3.6955

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Grind Higher Ahead Of Fed Hike Amid Continued Regional Bank Jitters, Oil Extends losses

WEDNESDAY, MAY 03, 2023 – 08:11 AM

S&P 500 futures are marginally higher on the day despite renewed pre-market weakness from US regional banks and a continued plunge in crude, which sent WTI futures lower by more than 3% on the day and below $70 per barrel on demand worries as the global economy slows. Contracts on the S&P 500 edged 0.1% higher while those on the Nasdaq 100 gained 0.2% by 7:30 a.m. ET, bouncing from yesterday’s losses ahead of the Fed decision. Treasury yields are lower, as traders seek out havens, while the Bloomberg dollar index weakened as traders eye recession risks alongside a potential pause in interest rate hikes. Meanwhile, most metals, including gold, decline slightly.

In premarket trading, regional banking stocks including PacWest Bancorp and Western Alliance Bancorp tumbled in early trading, dropping as much as 12% while Western Alliance Bancorp (WAL US) fell 7.8%. before recovering most losses ahead of a Fed rate hike that will only make the deposit outflow from small banks worse. Meanwhile, AMD shares fell as much as 6.3% in premarket trading, after the chipmaker gave a tepid forecast for the current quarter as it wades through a severe PC slowdown. Analysts highlighted mixed results for the quarter, but noted that its server and PC businesses should rebound in the second half of the year. Here are some other notable premarket movers:

- Starbucks shares slid as much as 5% in US premarket trading after the coffee chain operator left guidance for the fiscal year 2023 unchanged. The move disappointed analysts, who called it a conservative stance given the strong second quarter and sales beat, and said it suggests growth will weaken in the second half of the year.

- Ford declined in postmarket trading after the company reiterated its full-year forecast despite strong first-quarter results, and flagged headwinds including economic uncertainty around the globe and higher industrywide customer incentives.

- Amcor shares dropped as much as 8.3% in US premarket trading, set to hit their lowest level since June 2020, after the packaging company cuts its adjusted EPS forecast for the full year, with analysts flagging weakness in volumes. Amcor’s shares also declined 9.5% in Sydney trading.

- Chegg (rose as much as 9.5% in premarket trading, as the online educational services company attempts to recoup some losses after posting its biggest intra-day drop on Tuesday.

- Match Group gained in extended trading, after the online dating company reported its first-quarter results and gave an outlook. While the revenue forecast is below expectations, analysts note strength in the company’s Tinder business.

- Unisys shares jumped 12% in extended trading on Tuesday, after the IT services company reported first-quarter results that were stronger than expected.

- Paycom Software shares gained in extended trading after the human-capital-management software company reported first-quarter results that beat expectations and raised its full-year forecast. It also introduced a dividend.

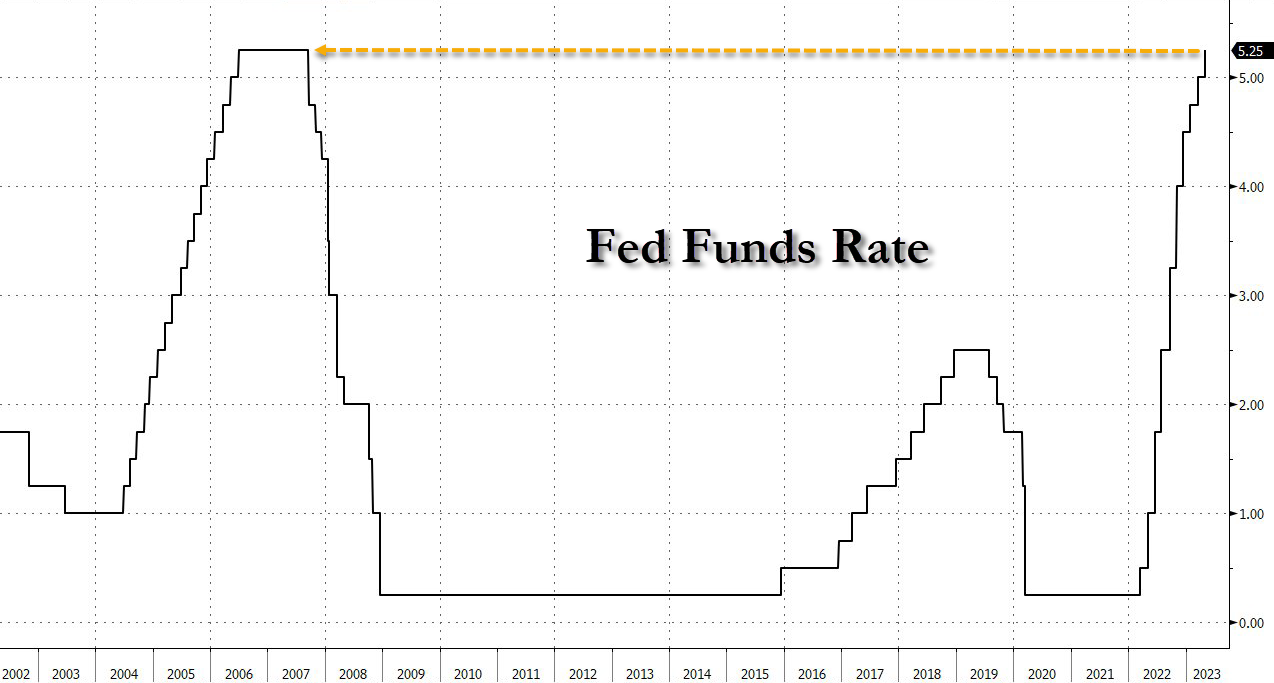

As we previewed previously, the Fed is expected to deliver a 25 basis-point interest-rate increase and signal a pause in its aggressive tightening campaign. Watchers anticipate the central bank will stop raising rates as tighter lending conditions and signs of a slowing economy suggest inflation will cool more meaningfully in the months ahead. Fed-dated OIS currently prices in around 23bp of rate hike premium for the meeting, little change vs Tuesday close. Investors will assess impact of current banking sector jitters on future monetary policy, though with inflation stubbornly elevated, Powell is expected to stop short of assuring markets that a pause is a done deal — or that rate cuts are imminent

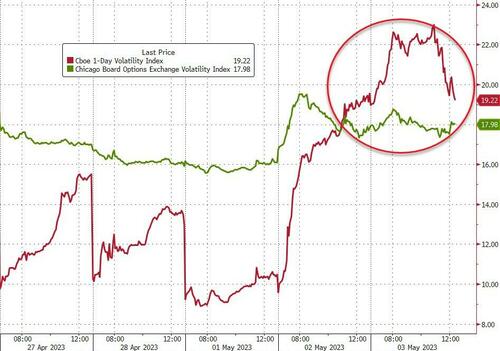

The US stock rally, supported by better-than-feared earnings and hopes for a less hawkish Fed, lost steam this week amid weak economic data and concerns about the banking sector. The selloff pushed the VIX Index toward 18 after the volatility gauge spent most of April near a 16 handle, while the VIX1D doubled yesterday from 10 to 20.

“When it comes to thinking about the potential for further hikes from here, I do think the Fed really wants to keep the door open specifically given the fact that the economy has been quite resilient,” said Madison Faller, global strategist at JPMorgan Private Bank. But “whether the last hike is today or even in June, we’re nearing the end of the Fed tightening cycle.”

In Europe, stocks are higher as they look to bounce back from their sharpest fall in five weeks on Tuesday. The Stoxx 600 is up 0.4% led by defensive sectors such as consumer products, miners and food and beverages the strongest-performing sectors while energy names have struggled as oil prices decline. Italian lenders rose on Wednesday, outperforming banks in the rest of the region, after UniCredit raised its full-year profit target and said it will boost shareholder payouts. UniCredit jumped as much as 6.9%, with Intesa Sanpaolo (+2.1%), FinecoBank (+2.1%) and Banco BPM (+1.8%) also among the top performers on the Stoxx 600 Banks Index, which was down 0.2% as of 12:33 p.m. in Milan. Here are all the most notable European mover:

- Colruyt shares rise as much as 18% with analysts saying the guidance raise from the Belgian retailer is encouragingly driven by cost savings and that this could drive a reassessment of its outlook

- Straumann gains as much as 2.1% after the Swiss dental equipment group’s first-quarter earnings arrived in line with expectations. Analysts said strength in the EMEA market offset weakness in APAC

- Auto1 rises as much as 7%, withCiti saying the used-car trading platform’s profitability metrics beat estimates in the first quarter, boosting confidence for adjusted Ebitda to break even before year end

- Deutsche Post advances 2.9% to 2022 highs after the logistics firm reported 1Q Ebit which beat the average analyst estimate and confirmed the forecast published in its 2022 annual report

- Orsted shares gain as much as 1.6% after Danish wind farm operator’s wind operations beat 1Q expectations, offsetting a miss in its gas marketing arm, which analysts said is a high-quality mix

- Signify shares drop as much as 11%, the most intraday since July, after 1Q comparable sales missed estimates due to persistent weakness in its consumer and indoor professional businesses

- Porsche falls as much as 2.8% in Frankfurt after the sports-car brand reported first-quarter operating profit that missed analyst estimates. Jefferies says first-quarter earnings are “a tad weak”

- Stellantis falls 2.4% as the carmaker’s weakness in Europe and slightly lower volumes offset an overall revenue beat. Morgan Stanley noted that rising inventory levels could threaten further upside

- Haleon shares fall as much as 4.3% after a Financial Times report that drugmaker Pfizer plans to start selling its stake within months overshadowed the consumer-health company’s 1Q results

- Lufthansa falls as much as 6.5% after the airline reported 1Q earnings that analysts said were below estimates. Bernstein attributed the miss to a softer performance in the carrier’s cargo business

Earlier in the session, Asia’s stock benchmark headed for its first decline in five sessions, with Hong Kong-listed Chinese shares leading losses ahead of the Federal Reserve’s policy decision. The MSCI Asia Pacific Index dropped as much as 0.6% in broad-based declines, following the selloff on Wall Street as worries about the financial sector amplified risk aversion ahead of the Fed. Energy stocks were among the biggest losers in the region after oil prices collapsed on Tuesday following softening US employment data that added to recession concerns. Benchmarks in Hong Kong led the region lower, with doubts remaining over the pace of China’s economic recovery.

“So far, the guidance hasn’t shown much improvement” in the first-quarter earnings season, said Ken Peng, head of Asia Pacific investment strategy at Citi Global Wealth Investments. “The continued geopolitical concerns are likely to be with us for quite some time and the immediate sharp recovery from exiting the lockdowns is behind us already,” he added. As the results season in Asia continues, investors will closely watch the Federal Reserve’s commentary and interest-rate move to assess any further impact to corporate profits. Traders are pricing in a 25-basis-point hike this week, followed by a pause in its aggressive hiking campaign. The onshore China market will reopen Thursday, while Japan’s will resume trading on Monday.

Australian stocks extended their recent rout: the commodity-heavy S&P/ASX 200 index fell 1% to close at 7,197.40, extending losses for second session as banks and mining shares slumped. The drop comes ahead of a Federal Reserve decision where policymakers are expected to add to their rate-hike cycle.

Stocks in India declined in line with most Asian peers ahead of the Federal Reserve’s policy decision. Index-heavy Reliance Industries and software exporter Tata Consultancy were among key drags on the benchmark gauge, which snapped its eight-day long run of advances. The S&P BSE Sensex fell 0.3% to 61,193.30 in Mumbai, while the NSE Nifty 50 Index declined by a similar measure. Out of 30 shares in the Sensex index, 11 rose, while 19 fell. Stocks of government-controlled firms were outperformers as those companies benefit from government’s spending on infrastructure. Nifty PSE Index, a gauge of state-run enterprises, surged to its all-time high since Jan. 1995 debut.

In FX, the Bloomberg Dollar spot Index is down 0.3% while the Japanese yen and Swiss franc sit atop the G-10 intraday rankings; the USDJPY falls as much as 0.8% to 135.53 after hitting a multi-month high (Tokyo markets are closed for a public holiday). EUR/USD rose 0.4% to 1.1045; GBP/USD up 0.5% at 1.2524, while AUD/USD was little changed at 0.6664; NZD/USD up 0.4%, after advancing as much as 0.7% to 0.6250, the highest since Apr. 14 on bets the central bank will tighten policy following better-than-expected employment data.

Investors will scrutinise the Fed’s policy statement and comments to see if Powell suggests that more rate rises may be possible even as the US banking sector has come under pressure from dramatic tightening over the past year. “Overall, we lean toward USD lower today, but suspect price action will continue to be choppy,” said Erik Nelson, FX strategist at Wells Fargo. “Powell will be walking a fine line, and probably wants to err on the side of caution given fragility of banking sector sentiment and cracks appearing in the labor market.” While markets are pricing in the possibility that the Fed will start cutting rates later in the year, Powell is unlikely to validate those expectations yet, Nelson said, adding that the dollar would likely avoid a deep selloff later in the day as a result.

In rates, treasuries advanced during London session and broadly held gains into early US, following gains in bunds while US regional bank stocks fall pre-market. US yields richer by 1bp to 2bp across the curve with 10-year around 3.40%, slightly lagging early bund gains over London session. Today’s 830am refunding announcement of next week’s auction sizes and projected sizes for other sales during the May-July period is expected to include no changes from last quarter as debt ceiling limits flexibility. Focal points of US session, following Treasury refunding announcement, include PMI and ISM services indexes during US morning and Fed rate decision at 2pm New York time.

In commodities, oil plunged for a second day, as Brent crude futures dropped 2% near $73.80 a barrel having dropped 5% on Tuesday while WTI slid below $70 a barrel in New York, falling to the lowest since March amid renewed anxiety over the financial stability of regional US lenders as well as signs of a cooling labor market. Spot gold is little changed around $2,016

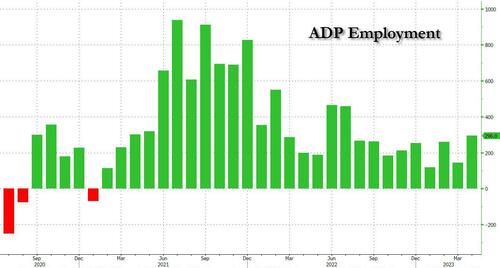

Looking to the day ahead now, and the main highlight will be the Federal Reserve’s policy decision and Chair Powell’s press conference. Otherwise, US data releases include the ISM services index for April and the ADP’s report of private payrolls in April. And in Europe, we’ll get the Euro Area unemployment rate for March.

Market Snapshot

- S&P 500 futures little changed at 4,140.50

- STOXX Europe 600 up 0.3% to 462.64

- MXAP down 0.3% to 160.32

- MXAPJ down 0.7% to 511.25

- Nikkei up 0.1% to 29,157.95

- Topix down 0.1% to 2,075.53

- Hang Seng Index down 1.2% to 19,699.16

- Shanghai Composite up 1.1% to 3,323.28

- Sensex down 0.4% to 61,136.04

- Australia S&P/ASX 200 down 1.0% to 7,197.40

- Kospi down 0.9% to 2,501.40

- Brent Futures down 2.2% to $73.68/bbl

- Gold spot down 0.1% to $2,015.20

- U.S. Dollar Index down 0.35% to 101.60

- German 10Y yield little changed at 2.23%

- Euro up 0.3% to $1.1036

Top Overnight News

- Malaysia becomes the second country in as many days (after Australia yesterday) to surprise markets with a rate hike (the central bank increased the policy rate by 25bp to 3% while investors were looking for it to stay on hold. BBG

- The end of pandemic-era restrictions has unleashed a luxury spending rebound in China. Luxury spending in China is bouncing back even faster than the country’s overall economy. Retail sales of jewelry, gold and silver soared 37.4 percent in March from a year earlier, more than three times as fast as the rebound in overall retail sales, according to China’s National Bureau of Statistics. NYT

- Iran seized another oil tanker in Middle East waters in a move that risks flaming US tensions. The Navy said a Panama-flagged ship was taken by Tehran in the Strait of Hormuz, the second incident in a week. The US has demanded the release of a Chevron-chartered ship that was intercepted at the end of April. BBG

- A Russian spy network has acquired sensitive technology from EU companies to fuel Vladimir Putin’s war in Ukraine even after a US-led crackdown on the covert smuggling ring. The network — set up to procure goods ranging from microchips to ammunition — has managed to obtain machine tools from Germany and Finland despite US sanctions imposed in March 2022. FT

- The Treasury will outline its issuance plans for longer-term debt and they’re likely to contain no change to the slate of coupon-bearing auctions that kicks off each three-month cycle. Most analysts see the combined size of the three securities held at $96 billion. The department on Monday ramped up its borrowing estimate for April-June to $726 billion from the $278 billion predicted in late January. BBG

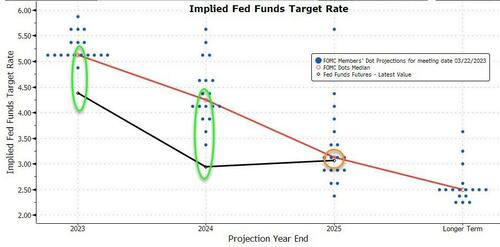

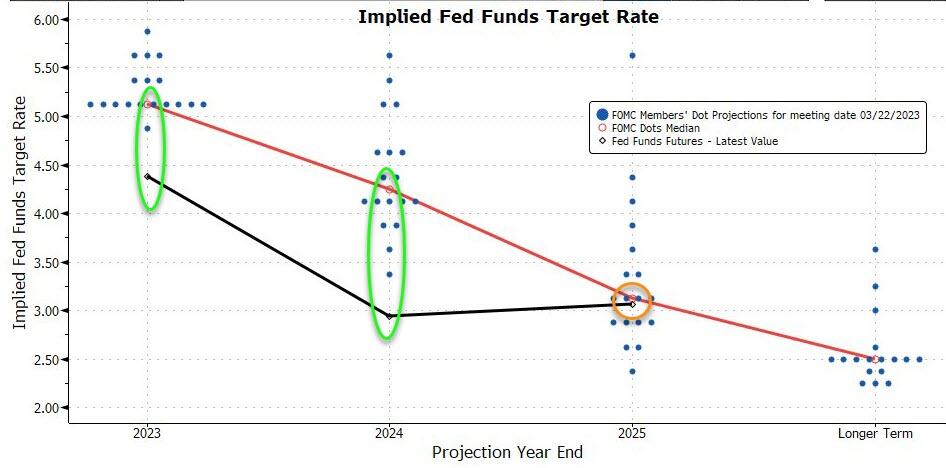

- The FOMC is likely to deliver a widely expected 25bp rate hike to 5-5.25% at its May meeting, but the focus will be on revisions to the forward guidance in its statement. We expect the Committee to signal that it anticipates pausing in June but retains a hawkish bias, stopping earlier than it initially envisioned because bank stress is likely to cause a tightening of credit. GIR

- Former Dallas Fed President Kaplan says he would be in favor of a “hawkish pause” whereby the Fed doesn’t hike rates today (but warns of potential further tightening down the road) as he thinks the regional bank situation is even worse than many imagine. BBG

- The White House may try and challenge the legality of the debt ceiling itself rather than negotiate a deal, a strategy that is certain to spook markets by injecting a whole new layer of uncertainty into the process. NYT

- House Democrats are pursuing a “discharge petition” option that could allow a debt ceiling bill to get to the floor without McCarthy’s consent. WSJ

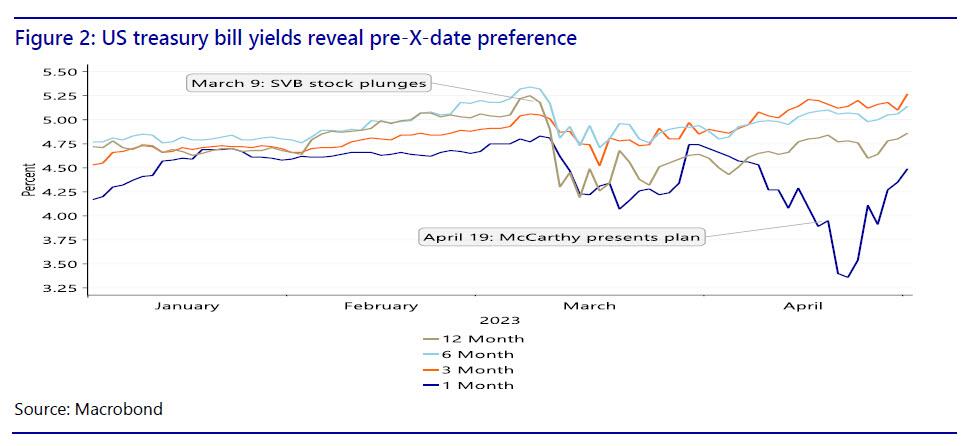

- Washington’s ability to avert a catastrophic US debt default risks coming down to as few as seven days in May, underscoring the enormous threat of the partisan impasse. Between now and June 1 — the date by which the Treasury Department could run out of sufficient cash — President Joe Biden and members of the House and Senate are scheduled to be in town at the same time for the sum total of one week.

A more detailed look at global markets courtesy of Newsquawk