MAY 5/2023 · by harveyorgan · in Uncategorized · Leave a comment·Editi

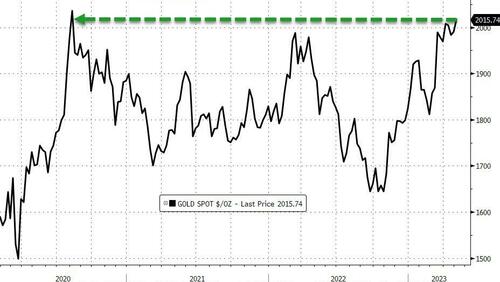

GOLD PRICE CLOSED: DOWN $30.30 TO $2016.90

SILVER PRICE CLOSED: DOWN 31 CENTS AT $25.64

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE $2050.00

Silver ACCESS CLOSE: 26.06

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

“America has been blessed never to have a native criminal class. Excepting Congress, of course.” … Mark Twain

GO GATA!

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Pay no attention to today’s action with respect to gold and silver and the stock market.

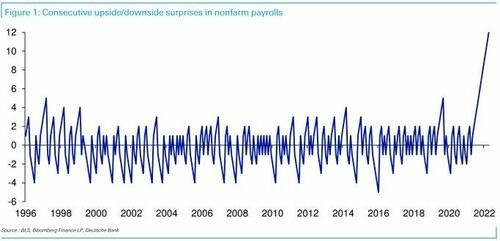

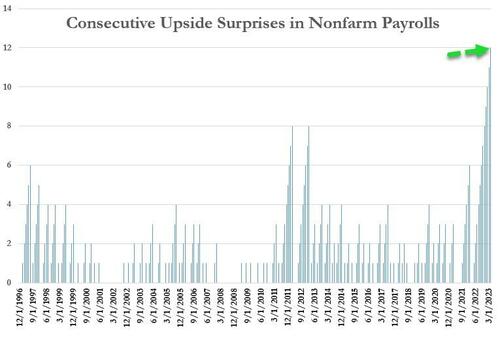

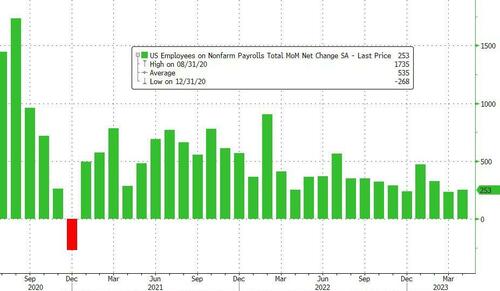

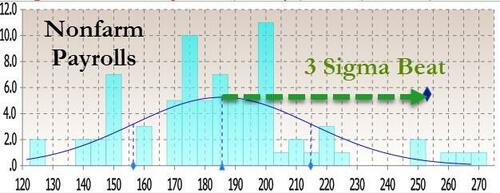

Nothing has changed. The Non Farm payroll report was a fraud, a phony!. There will be lots of revisions next month. There was lots of revisions to Jan, Feb, March but nobody pays attention to these. The economy is in big trouble. The crooks move was to save the banks for one more week, but many will succumb as trillions of dollars move into the money market funds from banks.

Bitcoin morning price:, $29,199 UP 354 Dollars

Bitcoin: afternoon price: $29,446 UP 107 dollars

Platinum price closing $1062.20 UP $20.95

Palladium price; $1504.40 UP $45.75

GO GATA!

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,698.98 DOWN 73.34 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1596.68 DOWN 32/44 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1830.70 DOWN 28.99 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: MAY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,048.000000000 USD

INTENT DATE: 05/04/2023 DELIVERY DATE: 05/08/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 81

323 C HSBC 131

365 H MAREX CAPITAL M 2

624 H BOFA SECURITIES 8

661 C JP MORGAN 502

690 C ABN AMRO 7

726 C CUNNINGHAM COM 10

737 C ADVANTAGE 2 4

880 H CITIGROUP 496

905 C ADM 1 54

TOTAL: 649 649

MONTH TO DATE: 5,144

JPMorgan stopped 502/649 contracts

FOR MAY:

GOLD: NUMBER OF NOTICES FILED FOR MAY/2023. CONTRACT: 649 NOTICES FOR 64,900 OZ or 2.0186 TONNES

total notices so far: 5144 contracts for 514400 oz (16.0000 tonnes)

FOR MAY:

SILVER NOTICES: 117 NOTICE(S) FILED FOR 535,000 OZ/

total number of notices filed so far this month : 1830 for 9,150,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $30.30

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:///A DEPOSIT OF 1.74 TONNES INTO THE GLD//

INVENTORY RESTS AT 930.04 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 31 CENTS AT THE SLV//

SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.368 MILLION OZ FROM THE SLV/: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 466.876 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 5,649 CONTRACTS TO 148,139 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.53 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.53). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A GIGANTIC GAIN ON OUR TWO EXCHANGES OF 7244 CONTRACTS. WE HAD 250 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 1.250 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 4.250 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A HUMONGOUS ISSUANCE OF EXCHANGE FOR PHYSICALS( 1595 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.105 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 60,000 OZ(E.FP.’S LOWER THE AMOUNT OF SILVER STANDING)+ 4.25 MILLION OZ OF EXCHANGE FOR RISK(RAISES THE AMOUNT OF SILVER STANDING):THUS TOTAL OF 16.925 MILLION OZ OF STANDING FOR DELIVERY V) HUGE SIZED COMEX OI GAIN/ HUMONGOUS SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –35 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTRACTS for 5 days, total 4866 contracts: OR 24.330 MILLION OZ . (973 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 24.330 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 24.330 MILLION OZ/INITIAL

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 5649 CONTRACTS WITH OUR $0.53 GAIN IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUMONGOUS SIZED EFP ISSUANCE CONTRACTS: 1595 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 13.105 MILLION OZ//FIRST DAY NOTICE FOLLOWED BY TODAY’S E.F.P. JUMP OF 60,000 OZ (DECREASES THE AMOUNT OF SILVER STANDING) +// + 4.25 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //TOTAL STANDING 12.675 MILLION OZ + 4.25 MILLION = 16.925 MILLION OZ// .. WE HAVE A HUGE SIZED GAIN OF 7244 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 117 NOTICE(S) FILED TODAY FOR 585,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A HUGE SIZED 16,460 CONTRACTS TO 520,664 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: removed 1295 CONTRACTS

WE HAD A HUGE SIZED INCREASE IN COMEX OI ( 16,460 CONTRACTS) WITH OUR $19.00 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR MAY. AT 3.5085 TONNES ON FIRST DAY NOTICE // PLUS A MONSTROUS 82,300 OZ QUEUE. JUMP :(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)////YET ALL OF..THIS HAPPENED WITH OUR $19.00 GAIN IN PRICE WITH RESPECT TO THURSDAY’S TRADING.WE HAD A GIGANTIC SIZED GAIN OF 19,861 OI CONTRACTS (61.776 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3401 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 520,664

IN ESSENCE WE HAVE A HUGE SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 19,861 CONTRACTS WITH 16,460 CONTRACTS INCREASED AT THE COMEX AND 3401 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 19,861 CONTRACTS OR 61.776 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3401 CONTRACTS) ACCOMPANYING THE HUGE SIZED GAIN IN COMEX OI (16,460 //TOTAL GAIN IN THE TWO EXCHANGES 19,861 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 3.5085 TONNES FOLLOWED BY TODAY’S MONSTROUS QUEUE JUMP OF 82,300 OZ // NEW STANDING: 16.541 TONNES // ///3) ZERO LONG LIQUIDATION//4) HUGE SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 15,595 CONTRACTS OR 1,559,500 OZ OR 48.50 TONNES IN 5 TRADING DAY(S) AND THUS AVERAGING: 3119 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAY(S) IN TONNES 48.50 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 48.50/3550 x 100% TONNES 1.36% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES ( MUCH SMALLER THAN LAST MONTH)

MAY: 48.50 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 5649 CONTRACTS OI TO 148,139 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 1595 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1595 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1595 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 5649 CONTRACTS AND ADD TO THE 1595 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 7244 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 36.22 MILLION OZ

OCCURRED WITH OUR $0.53 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED DOWN 15.96 PTS OR .48% //Hang Seng CLOSED UP 100.58 POINTS OR 0.50% /The Nikkei closed UP 34.77 OR .12% //Australia’s all ordinaries CLOSED UP 0.34 % /Chinese yuan (ONSHORE) closed UP 6.9088 /OFFSHORE CHINESE YUAN UP TO 6.9152 /Oil UP TO 70.47 dollars per barrel for WTI and BRENT AT 74.54 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A HUGE SIZED 16,460 CONTRACTS UP TO 520,664 WITH OUR STRONG GAIN IN PRICE OF $19.00 ON THURSDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF MAY… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3401 EFP CONTRACTS WERE ISSUED: : JUNE 3401 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3401 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GIGANTIC SIZED TOTAL OF 19,861 CONTRACTS IN THAT 3401 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A HUGE SIZED GAIN OF 16,460 COMEX CONTRACTS..AND THIS GIGANTIC SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $19.00. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (16.541) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 16.541 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $19.00) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR GIGANTIC SIZED GAIN OF 19,861 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 61.776 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY. (3.5085 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 82,300 oz (2.559 TONNES)//NEW STANDING 16.540 TONNES ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $19.00

WE HAD –REMOVED 1295 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 19,861 CONTRACTS OR 1,986,100 OZ OR 61.776 TONNES.

Estimated gold comex today 285,584// fair

final gold volumes/yesterday 341,944 good

//MAY 5/ MAY 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 9683.123 oz HSBC Manfra . |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 649 notice(s) 64900 OZ 2.0186 TONNES |

| No of oz to be served (notices) | 174 contracts 17400 oz 0.5412 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5144 notices 514,400 OZ 16.0000 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 2

i) Out of HSBC: 5287.487 oz

ii) Out of Manfra: 3795.636 oz

total withdrawals: 9683.123 oz

Adjustments; 2

i) customer to dealer Manfra: 12,365.343 oz

ii) dealer to customer jPMorgan: 12,057.97 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 823 contracts having LOST 695 contracts. We had 1518 contracts filed

on THURSDAY, so we gained a monstrous 823 contracts or an additional 82,300 oz (2.559 tonnes) will stand for gold in this non active delivery month of May.

June GAINED 3796 contracts UP to 385,184 contracts.

July added 396 contracts to stand at 1156 contracts.

AUGUST GAINED 10,799 contracts up to 85,278 contracts

We had 649 contracts filed for today representing 64,900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 649 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 502 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2023. contract month,

we take the total number of notices filed so far for the month (5,144 x 100 oz ), to which we add the difference between the open interest for the front month of MAY 823 CONTRACTS) minus the number of notices served upon today 649 x 100 oz per contract equals 531,800 OZ OR 16.541 TONNES the number of TONNES standing in this NON- active month of May.

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (5,144 x 100 oz)+823 OI for the front month minus the number of notices served upon today (649)x 100 oz} which equals 531,800 oz standing OR 16.541 TONNES

TOTAL COMEX GOLD STANDING: 16.541 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,666,085.702 OZ 51.822 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,509,203.896 OZ

TOTAL REGISTERED GOLD: 12,385,679.388 (385,24 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,123,524.508 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,719,594 OZ (REG GOLD- PLEDGED GOLD) 333.42 tonnes//

END

SILVER/COMEX

MAY 5//2023// THE MAY 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 138,240.030 oz Brinks CNT Manfra . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 600,282.300 oz Loomis |

| No of oz served today (contracts) | 117 CONTRACT(S) (585,000 OZ) |

| No of oz to be served (notices) | 705 contracts (3.525,000 oz) |

| Total monthly oz silver served (contracts) | 1830 Contracts (9,150,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) into Loomis: 600,382.300 oz

Total deposits: 600,382.300 oz

JPMorgan has a total silver weight: 139,607 million oz/269.484 million =51.75% of comex .//dropping fast

Comex withdrawals: 3

i) Out of Brinks 15,712.880 oz

ii) Out of CNT: 101,844.240 oz

iii) Out of Manfra 20,683,510 oz

Total withdrawals; 138,240.630 oz

adjustments: customer to dealer

a) 323,570.182 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 31.674 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 269.484 million oz

CALCULATION OF SILVER OZ STANDING FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2023 OI: 822 CONTRACTS HAVING LOST 38 CONTRACT(S). WE HAD 26 CONTRACTS FILED

ON THURSDAY, SO WE LOST 12 CONTRACT OR AN ADDITIONAL 60,000 OZ OF SILVER WILL NOT STAND FOR DELIVERY IN THIS VERY

ACTIVE DELIVERY MONTH OF MAY AS, FOR THE 4TH DAY IN A ROW, THESE GUYS WERE E.F.P.’d TO LONDON AS NO SILVER COULD BE FOUND OVER HERE..

.JUNE HAD A 42 CONTRACT GAIN TO 950

JULY HAD A 4631 CONTRACT GAIN TO 125,341 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 117 for 585,000 oz

Comex volumes// est. volume today 68,434 GOOD

Comex volume: confirmed yesterday: 76,702 good

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 1830 x 5,000 oz = 9,150,000 oz

to which we add the difference between the open interest for the front month of MAY(822) and the number of notices served upon today 117 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2023 contract month: 1830 (notices served so far) x 5000 oz + OI for the front month of May (822) – number of notices served upon today (117 )x 500 oz of silver standing for the MAY contract month equates to 12.675 million oz + THE CRIMINAL 1.250 MILLION OZ EXCHANGE FOR RISK TODAY//NEW TOTAL EXCHANGE FOR RISK: 4.250//NEW TOTAL 16.925 MILLION OZ//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MAY 5/WITH GOLD DOWN $30.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AS DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

MAY 4/WITH GOLD UP $19.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.30 TONNES

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

APRIL 10/WITH GOLD DOWN $21.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91 TONNES

APRIL 6//WITH GOLD DOWN $9.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91

APRIL 5//WITH GOLD UP 0 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04

APRIL 4/WITH GOLD UP $36.30 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

APRIL 3/WITH GOLD UP $14.20 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.02 TONNES

MARCH 31/WITH GOLD DOWN $10.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD////INVENTORY RESTS AT 928.02 TONNES

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

GLD INVENTORY: 930.04 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 5/WITH SILVER DOWN 31 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 466.876 MILLION OZ//

MAY 4/WITH SILVER UP 53 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF .174 MILLION OZ INTO SLV.//INVENTORY RESTS AT 467.174 MILLION OZ//

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 10/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 6/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 4.643 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 468.585 MILLION OZ//

APRIL 5/WITH SILVER DOWN 4 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.942 MILLION OZ

APRIL 4/WITH GOLD UP $1.11 TODAY CRIMINAL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.47 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 463,942 MILLION OZ

APRIL 1/WITH SILVER DOWN 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.412

MARCH 31/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD/: A MASSIVE 4.779 MILLION OZ DEPOSITED INTO THE SLV///INVENTORY RESTS AT465.412 MILLION OZ

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

CLOSING INVENTORY 466.876 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

3,Chris Powell of GATA provides to us very important physical commentaries

Your weekend reading material

(Alasdair Macleod)

Alasdair Macleod: Why gold is always money

Submitted by admin on Thu, 2023-05-04 11:56Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, May 4, 2023

That America faces a severe banking crisis has become plain to see, but the authorities’ response less so. Almost certainly the crisis has much further to go in America, spreading to other jurisdictions. We can only hope that central banks will protect all depositors, but that is far from certain in this early stage.

These febrile conditions are made infinitely more difficult by the contraction of bank credit. The cyclical nature of bank credit means that the shortage of credit will intensify, driving up borrowing costs even in the face of a recession. Interest rates are no longer under the control of central banks, though market participants have yet to realise it.

It has important implications for the valuation of credit. In order to understand the consequences, this article draws out the legal and practical distinctions between money, defined as gold and silver but principally gold, and credit in the form of banknotes and bank deposits.

The value of credit is a matter of the confidence in it. You may think that your dollars, euros, or pounds are money, but you would be wrong. They are credit. The cost of being wrong will not be just to see your bank deposits threatened systemically, but potentially the entire currency system undermined by loss of faith in it.

To properly understand these dangers, this article defines and describes the differences between credit and money. It is credit which is threatened with collapse. Only true money, which very few Westerners possess will survive. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/why-gold-is-always-money?gmrefcode=gata

END

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

Kamikaze Fed – Silver ejector seat – Time to bail out!

Andrew Maguire reveals the truth about sanctioned “too big to fail” bank bailouts and the eff…

END

5.IMPORTANT COMMENTARIES ON COMMODITIES:

end

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS// FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 6.9088

OFFSHORE YUAN: 6.9152

SHANGHAI CLOSED DOWN 15.96 PTS OR .48%

HANG SENG CLOSED UP 100.58 PTS OR 0.50%

2. Nikkei closed UP 34.77 PTS OR .12%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 101.14 EURO FALLS TO 1.1016 DOWN 8 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.415 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 134.46 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.2610***/Italian 10 Yr bond yield RISES to 4.177*** /SPAIN 10 YR BOND YIELD RISES TO 3.354…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.064

3j Gold at $2036.60 silver at: 25.83 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 88 /100 roubles/dollar; ROUBLE AT 77.16//

3m oil into the 70 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 134.22 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .415% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8918 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9823 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.401 UP 5 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.754 UP 3 BASIS PTS/

USA 2 YR BOND YIELD: 3.8248 UP 10 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.50…

GREAT BRITAIN/10 YEAR YIELD: UP 13 BASIS PTS AT 3.7855

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

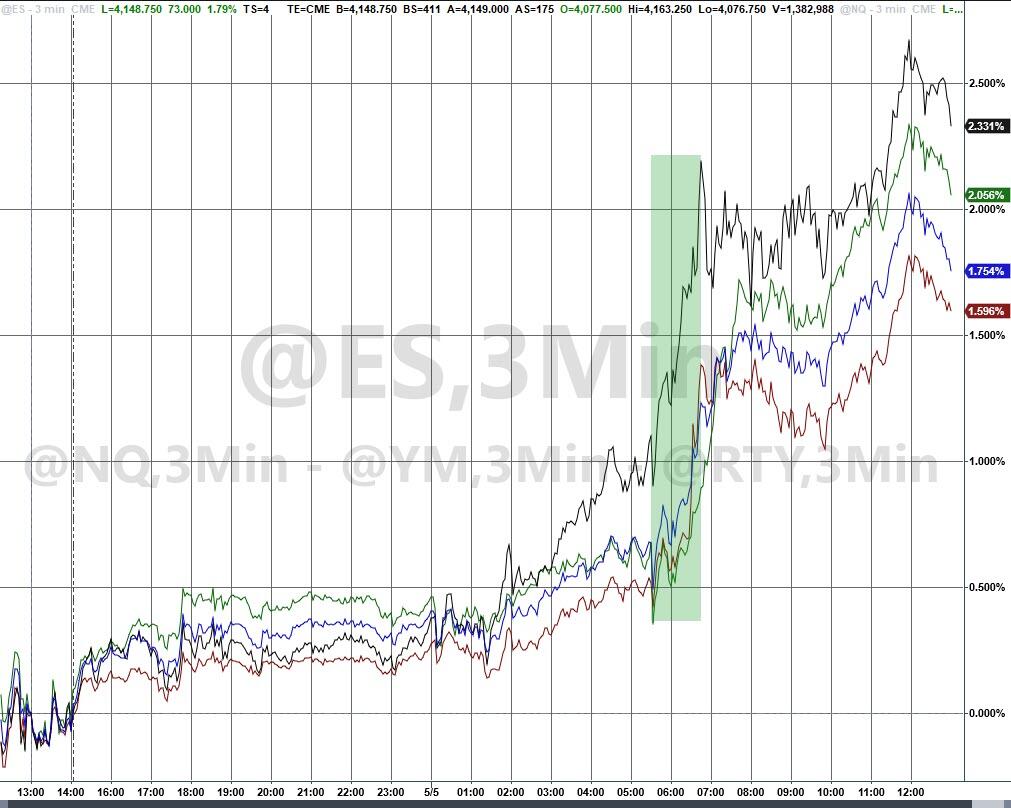

Futures Rise Ahead Of Payrolls To End Week Of Bank Turmoil

FRIDAY, MAY 05, 2023 – 07:55 AM

US futures entered the last day of a brutal week in the green ahead of key US jobs data, as regional banks clawed back some of their recent selloff, even as the S&P 500 benchmark was still poised for its worst weekly performance in almost two months. The S&P 500 contracts climbed 0.7% as of 7:30 a.m. ET while Nasdaq 100 futures gained 0.6%. European stocks were higher but on pace for their biggest weekly drop in 7 weeks. Treasury yields are ticking higher amid a more risk-on day, while the dollar is still weakening on recession risks and a potential pause in interest rate hikes. Oil is staging a rebound, though is still set for the worst week since mid-March, continuing its third weekly decline. Meanwhile, gold is headed for its biggest weekly advance since the middle of March, up around 2% this week, as traders look for havens. Iron ore slides, while copper is little changed.

In premarket trading, distressed bank PacWest added 13% in US premarket trading, after it slumped 69% in the previous four sessions amid concerns that the collapse of First Republic Bank may not be the last in the troubled industry. Western Alliance Bancorp also rose 12% in premarket trading, having wiped out 51% of its market value earlier this week. While some investors have warned of further pain to come, others have suggested the bank rout has gone too far. “The tension between poor market sentiment and strong liquidity at regional banks is difficult to reconcile,” said Bloomberg Intelligence analyst Herman Chan. Apple rose as much as 2.5% after it reported better-than-expected revenue on robust iPhone sales, raised its dividend and expanded its buyback program. Coinbase and dating app Bumble were also among the best performers on Friday. Here are some other notable premarket movers:

- Atlassian falls as much as 16% in premarket trading after the software company forecast revenue for the fourth quarter that missed the average estimate. Analysts noted that a steep deceleration at its cloud business and the weak current-quarter forecast offset better-than-expected 3Q results.

- Carvana shares surge as much as 37% in US premarket trading, and are set for their biggest one-day gain in three months after the online second- hand-car retailer’s earnings beat estimates and it predicted a return to profitability in the second quarter. Analysts raised their price targets, positive on the company’s cost-cutting efforts even as challenges remain.

- Lyft slumped as much as 17% in premarket trading after the company forecast revenue for the second quarter that trailed the average analyst estimate. New CEO David Risher faces several challenges as he attempts to turn around the struggling ride-hailing company.

- Trupanion tumbled 48% in premarket trading, on course for its biggest-ever drop, after the pet-health insurer reported a first-quarter loss per share that was more than twice the average analyst estimate. Analysts note that price increases at vets during the quarter deepened losses.

- DoorDash shares rose as much as 5.1% in premarket trading, after the food-delivery company beat estimates, driven by strong demand for deliveries despite higher prices and a cloudy economic outlook.

- Bill Holdings Inc. shares climbed 15% in extended trading, after the financial software company raised its full-year forecast. Analysts are positive on the report.

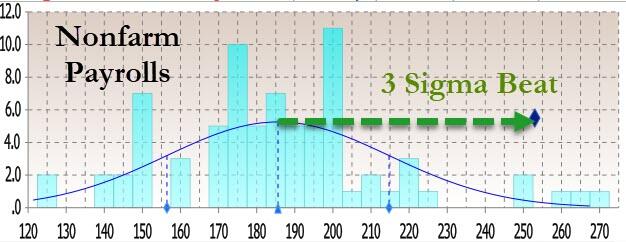

While banking jitters will remain front and center, the focus on Friday shifts to the US jobs report (full preview here) and speculation that the Federal Reserve might start lowering interest rates in response to tighter credit conditions. Swap contracts are now showing around one-in-two odds of a cut as soon as July. Economists forecast that employers scaled back hiring in April, adding 185,000 jobs, and that the unemployment rate ticked up slightly from historically low levels last month; risks could be skewed to upside following blowout ADP report that estimated private payrolls rose 296k in April (vs. consensus 150k). Gordon Shannon, portfolio manager at TwentyFour Asset Management, predicts a jobs print below 150,000. “That’s going to cause a rally in risk assets as that further feeds into the idea that Powell is data-driven and therefore going to pivot soon,” he said in an interview with Bloomberg Television.

Following two months of gains, the S&P 500 kicked off May with a drop as investors fret over rising recession risks and the regional banking crisis. At the same time, swap traders are betting that the Federal Reserve is likely to reverse this week’s quarter-point interest-rate increase by July in response to tightening credit conditions. The Fed tightening pause, combined with signs of a slowing inflation and cooling labor market suggest the US might avoid a recession after all, according to Aneka Beneby, a senior portfolio manager at Julius Baer.

“I think equities are going to keep climbing the wall of worry because of the lack of a recession this year,” she said on Bloomberg TV. “The sectors that we like are tech, and those mega cap stocks show that they’ve been quite resilient. We also like healthcare, which is still quite cheap.”

While the Fed may have signaled this week its willingness to pause rate hikes, BofA’s Michael Hartnett said it’s not yet time to buy equities as outflows accelerate amid elevated inflation and recession fears. Redemptions from global stock funds reached $6.6 billion in the week through May 3 — the most in more than two months, according to a note from the bank citing EPFR Global data. A “new structural bull market requires big Fed easing,” which in turn needs a “big recession,” Hartnett said.

To protect themselves against that threat of a downturn, investors are likely to favor gold and technology stocks as those bets are expected to provide a buffer, strategists at JPMorgan Chase & Co. said. “The US banking crisis has increased the demand for gold as a proxy for lower real rates as well as a hedge against a ‘catastrophic scenario,’” strategists including Nikolaos Panigirtzoglou and Mika Inkinen wrote in a note.

In geopolitics, the Pentagon is seeking a meeting between US Defense Secretary Lloyd Austin and his Chinese counterpart Li Shangfu in Singapore next month, in a renewed effort by the Biden administration to restart lines of communication with China’s military leaders. If Beijing accepts, this would represent the most senior in-person meeting between the two sides since an alleged Chinese spy balloon transited the US in February and sent relations to a new low. China has rebuffed multiple requests for a phone call with Austin or the chairman of the joint chiefs of staff, General Mark Milley, since then. A long-anticipated call between US President Joe Biden and China’s President Xi Jinping has also yet to take place.

European stocks are higher although still on course for their largest weekly fall in seven weeks. The Stoxx 600 is up 0.2% led by outperformance in the energy, mining and bank sectors. Adidas shares rise as much as 7.6%, the most intraday since February, after the German sportswear maker reported first quarter results that beat estimates and kept its outlook for the year. IAG shares gain as much as 5.8%, with analysts saying consensus estimates are likely to rise after a very strong first quarter, with the British Airways owner delivering an operating profit in the quarter. Here are some of the other most notable movers:

- Grifols gains as much as 6.7% after Citi said it expects the blood plasma producer to report 1Q results at the top end of guidance, while fresh data from Argenx will be a “clearing event” for Grifols

- Scatec gains as much as 14%, the most since November, after the Norwegian renewables firm beat expectations on operating profit and Ebitda, marking a “good start to the year,” DNB writes

- Arkema shares climb as much as 3.1% after the France-based chemicals company reported 1Q Ebitda beat. Company confirms full-year 2023 Ebitda guidance, with Citi attributing the beat to core divisions

- Raiffeisen bounces as much as 4.3% after the Austrian lender’s earnings topped expectations and it raised its guidance, even as analysts flagged that it did not provide any update on its Russia operations

- Evotec shares fall as much as 10% after the German stock exchange operator said the biotech firm will be removed from the MDAX, HDAX and TecDAX indexes following the delaying of the release of its annual report

- InterContinental Hotels shares fall as much as 3.1% with analysts saying the net unit growth for the hotel operator in the first quarter was a touch light, as it also announced an unexpected CEO change

- Moncler falls as much as 2.7% after earnings, with analysts saying the solid print may not be enough to excite given high expectations into the print after a strong season for its luxury rivals

- Galp shares drop as much as 3.5% after the Portuguese oil company’s first quarter adjusted net income missed the average analyst estimate, with Jefferies highlighting weak operating cash flow

- Clariant falls as much as 2% after the Swiss chemical company’s 1Q adjusted Ebitda missed estimates, as analysts flag weaker demand and a difficult macroeconomic environment

Earlier in the session, Asian stocks advanced for a second day as the dollar continued to weaken, with traders shrugging off concerns over further stress among regional US banks. The MSCI Asia Pacific Index rose as much as 0.4%, led by real estate shares. Some markets in the region, including Japan and South Korea, were shut for holidays. Hong Kong shares outperformed their regional peers. Asian lenders have been resilient amid deepening US banking woes, with a regional financials gauge poised for a 0.8% increase this week. Investors will watch for any potential moves by US authorities to limit further contagion risks. Also helping sentiment were signs that the Federal Reserve may be reversing its policy tightening campaign. The regional stock benchmark headed for a 1.2% increase this week, the first weekly gain in three. US payroll figures due later Friday will give further cues on the strength of the job market and where interest rates are headed.

Mainland Chinese stocks slipped on Friday after latest data showed the pace of expansion in services activity softened in April, adding to jitters about an uneven economic recovery. The surge in tourism spending during the Golden Week holidays did little to offset the surprise weakness in the manufacturing sector and lackluster earnings. Right now sentiment is “frustratingly weak” as the market is looking at economic data “with a glass-half-empty lens,” James Wang, head of China strategy at UBS Investment Bank, told Bloomberg TV. “Investors will be more ‘data-dependent’ going forward, and they are also wondering if they should invest directly through Chinese equities or other asset classes.”

Australian stocks gained led by property: the S&P/ASX 200 index rose 0.4% to close at 7,220.00, boosted by real estate and mining shares. Still, the benchmark dropped 1.2% for the week, a third straight loss. The advance comes as investors weighed the prospect of the Federal Reserve reversing its policy-tightening campaign ahead of US jobs data due later Friday. Oil edged higher. In New Zealand, the S&P/NZX 50 index fell 0.7% to 11,889.01.

Indian equities were the worst performers in Asia, dragged down by a sharp selloff in top lender HDFC Bank and its mortgage lender parent, which plunged on worries over potential outflows upon completion of their merger. The S&P BSE Sensex fell 1.1% to 61,054.29 in Mumbai, while the NSE Nifty 50 Index declined 1%. For the week, the gauges were little changed. Domestic stocks had largely rallied from their April lows through Thursday as the earnings season progressed, with banks reporting strong profit growth for the March quarter. The gains were also a result of inflows from foreign investors. “The market has rallied sharply in the last one month and such short term corrections would relieve the overbought set-ups and form a base for the next rally,” according to Ruchit Jain, analyst with 5paisa.com said.

In FX, a gauge of the dollar fell as much as 0.2% as traders waited for US jobs data due later on Friday for more clues on the Federal Reserve’s interest-rate path. The Swiss franc is the weakest of the G-10 currencies, falling 0.6% versus the Greenback after data showed CPI slowed in April. “Markets will watch closely the US non-farm payrolls tonight,” Michael Wan, senior currency analyst at MUFG Bank Ltd., wrote in a note. “Any whiff of meaningful labor market softening will be seen as validating the Fed’s recent decision to turn more data dependent and dovish”

In rates, treasuries were slightly cheaper across the curve ahead of April jobs report, as stock futures advance and pare portion of Thursday losses. Regional banks are higher in pre-market, while Apple also rose after reporting that sales of iPhones rebounded last quarter. Wider losses seen across core European rates adds to downside pressure on Treasuries. Treasury yields cheaper by 2bp to 3bp across the curve with spreads broadly within one basis point of Thursday close; 10- year yields up to around 3.40%, toward top of Thursday range with bunds and gilts underperforming by 5.5bp and 8bp in the sector. Bunds have given back some of Thursday’s post-ECB rally with German two-year yields rising 6bps to 2.54%. Treasuries are also lower ahead of the US jobs report due later today.

In commodities, crude futures advance with WTI rising 1.4% to trade near $69.50. Spot gold falls 0.6% to $2,039.

Bitcoin is firmer and holding steady above the USD 29k, holding towards the top-end of USD 28.7-29.5k.

To the day ahead now, and the main data highlight will be the US jobs report for April. Otherwise, we’ll get German factory orders and French industrial production for March. From central banks, we’ll hear from the Fed’s Bullard and Book, along with the ECB’s Simkus and Elderson.

Market Snapshot

- S&P 500 futures up 0.3% to 4,089.50

- MXAP up 0.3% to 162.20

- MXAPJ up 0.4% to 517.18

- Nikkei up 0.1% to 29,157.95

- Topix down 0.1% to 2,075.53

- Hang Seng Index up 0.5% to 20,049.31

- Shanghai Composite down 0.5% to 3,334.50

- Sensex down 0.8% to 61,250.67

- Australia S&P/ASX 200 up 0.4% to 7,220.01

- Kospi little changed at 2,500.94

- STOXX Europe 600 little changed at 460.59

- German 10Y yield little changed at 2.24%

- Euro up 0.1% to $1.1026

- Brent Futures up 1.1% to $73.32/bbl

- Gold spot down 0.5% to $2,039.77

- U.S. Dollar Index down 0.11% to 101.29

Top Overnight News from Bloomberg

- China’s Caixin services PMI for April falls a bit short, but holds solidly above 50 (it came in at 56.4, down from 57.8 in Mar and below the Street’s 57 forecast). BBG

- Australia’s RBA cut its forecasts for inflation, wages, and GDP this year as monetary tightening weighs on the economy. BBG

- Eurozone retail sales dropped by a bigger than expected 1.2 per cent as inflation and rising borrowing costs took their toll on consumer spending in March. The decline meant retail sales had fallen 0.4 per cent in the first quarter, following a 1 per cent drop in the previous quarter, economists said, as they pointed to a weakness in underlying demand. FT

- German factory orders fell 10.7 per cent in March from the previous month, a much bigger drop than economists expected, raising concerns about a sharp slowdown in Europe’s biggest economy. The slide in new orders for manufacturers, the biggest since pandemic lockdowns hit in April 2020, reflected declines in all sectors except consumer goods, the federal statistical office said on Friday. FT

- Rishi Sunak’s Conservatives on Friday faced crushing losses in UK local elections as voters in many parts of England turned against the party after a tumultuous year. FT

- Adidas shares rally in Europe after the company’s Q1 results reassure investors (numbers came in ahead of plan and mgmt. reaffirmed guidance for the year). RTRS

- U.S. federal and state officials are assessing whether “market manipulation” caused the recent volatility in banking shares, a source familiar with the matter said on Thursday, as the White House vowed to monitor “short-selling pressures on healthy banks.” RTRS

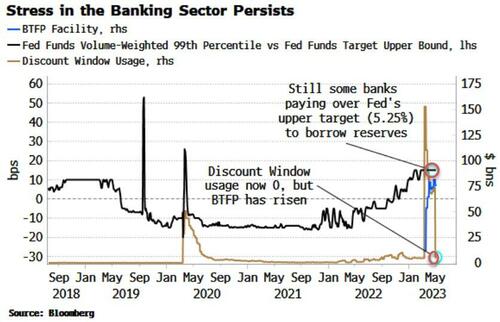

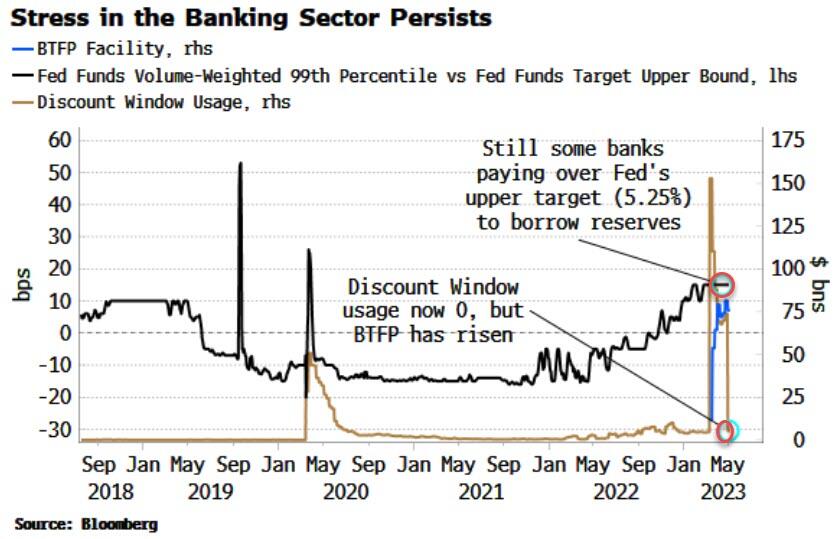

- Fed balance sheet data – outstanding balances on the Big 3 categories being watched closely (Primary Credit/Discount Window, Bank Term Funding Program, and Other Credit) totaled $309.2B as of 5/3, down from $325.4B as of 4/26. Fed

- Activist investor Nelson Peltz told the Financial Times that the deposit insurance limit should be increased, with wealthy account holders paying a small insurance premium to the federal insurance fund to safeguard balances of more than $250,000. FT

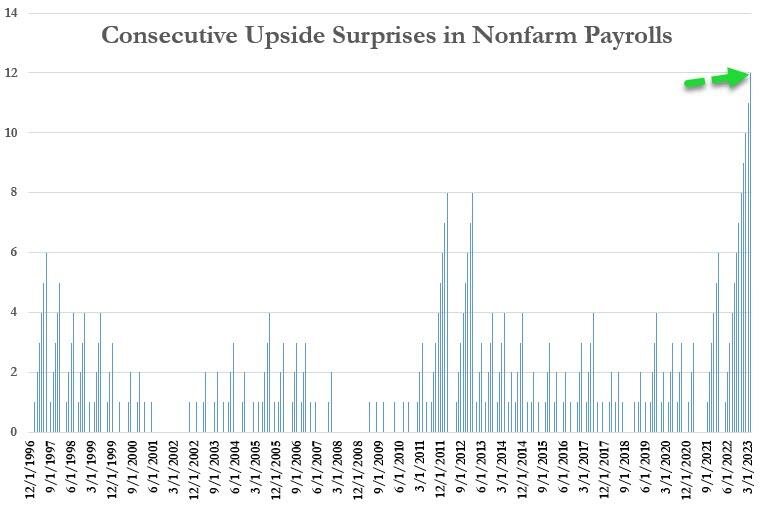

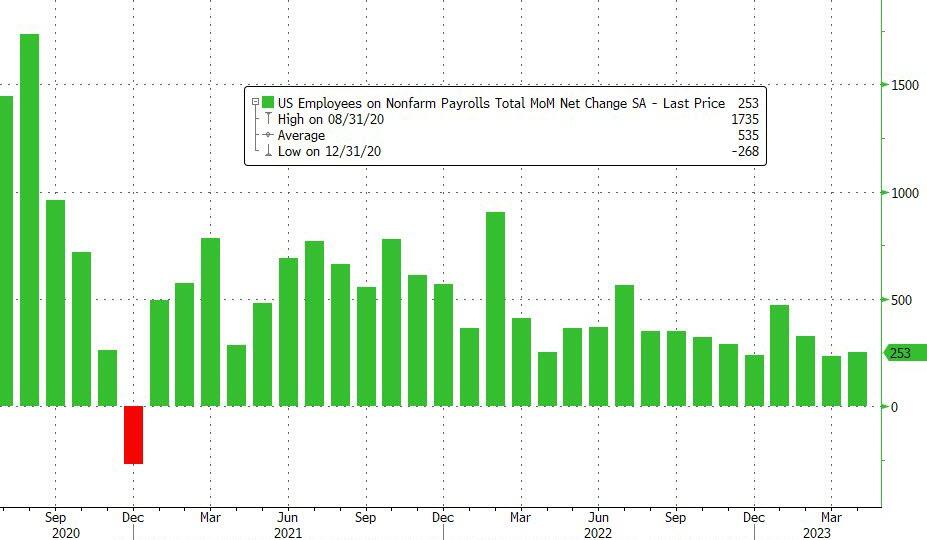

- GIR estimates nonfarm payrolls rose 250k in April (mom sa), above consensus of +182k but a slowdown from the +345k average pace of the last three months. We believe high but falling labor demand more than offset continued layoffs in the information and financial sectors and a roughly 25k hiring drag from reduced credit availability. Big Data employment indicators were strong on net, arguing against a large credit drag. GIR

A more detailed market look courtesy of Newsquawk

APAC stocks traded mixed after the weak lead from the US where risk sentiment was subdued by banking-related headwinds and amid holiday-thinned conditions in Asia due to closures in Japan and South Korea. ASX 200 was choppy amid indecision in the top-weighted financial industry after ANZ Bank’s earnings which showed H1 cash profit rose to a record although the Co. warned of increased difficulties in H2, while the RBA’s quarterly Statement on Monetary Policy stuck to the hawkish script. Hang Seng and Shanghai Comp. diverged with the Hong Kong benchmark led higher by strength in tech and property stocks, while the mainland is pressured after Chinese Caixin Services and Composite PMI data which showed the pace of China’s services activity slowed by more than expected but remained at a firm expansion.

Top Asian News

- A bipartisan group of US senators introduced legislation that would allow US President Biden to sign a tax agreement with Taiwan and which addresses an issue viewed as a barrier for further investment, according to Bloomberg.

- RBA Statement on Monetary Policy reiterated to do what is necessary to return inflation to the target and that some further tightening may be required to reach the target in a reasonable timeframe. RBA added that the longer inflation remains above target, the greater the risk of a price-wage spiral, as well as noted that goods disinflation is limited so far and energy price inflation is to stay high this year, while rent growth is to pick up and materially added to inflation out to mid-2025.

- Earthquake early warning issued for Japan’s Ishikawa prefecture, intensity of 6 on Japan’s 1-7 scale, prelim magnitude of 6.3 (rev. 6.5), according to JMA; Japan earthquake has shaking intensity of 6+ on scale of 7, according to NHK; No tsunami warning issued.

- China’s State Planner to study a new round of pork purchases for reserves, amid weakening prices..

European bourses are firmer, Euro Stoxx 50 +0.3%, somewhat shrugging off the mixed APAC handover where regional banking concerns served as a headwind in holiday thinned conditions. The DAX 40 +0.7% is the marked outperformer, aided by German electricity adjustments and strong Adidas earnings, +7.8%; sectors are more of a mixed bag, with Energy outperforming while Travel/Healthcare lag. Stateside, futures are firmer and have been edging slightly higher in typically contained pre-NFP trade after yesterday’s regional banking induced pressures, ES +0.5%. Alibaba’s (BABA) Ant Group’s transformation into a fully regulated company has reportedly been held up by a reshuffle of China’s financial-regulatory system, according to WSJ sources. Cigna Group (CI) Q1 2023 (USD): Adj. Operating EPS 5.41 (exp. 5.22), Revenue 46.4bln (exp. 45.55bln); raises FY23 outlook.

Top European News

- German Economy Ministry is proposing a industrial electricity price of EUR 0.06/KWh until 2030, would cost EUR 25-30bn. Funding to be taken from fund initial created for COVID. Reduced price would be valid for 80% of base power consumption.

- Sky News noted it is early days regarding the UK local council election results but suggested there are currently encouraging signs in the data for the opposition Labour Party, whilst Conservative MP Mercer said his party is having a “really terrible night”.

- ECB’s Villeroy says the alteration in rate increase rhythm is an important signal, favours smaller ECB hiked. Will likely be several more hikes; though, we have done the essential. Goal is to win the fight against inflation, without sparking a recession. Will bring inflation back to target by 2025 maybe even by end-2024.

- ECB’s Simkus says May’s hike was not the last, concerns that core inflation remains high.

- ECB’s Muller says yesterday’s rate hike will not be the last; no sign yet of core inflation easing.

- ECB Survey of Professional Forecasters: 2023 inflation cut to 5.6% from 5.9%, 2023 growth upgraded to 0.6% from 0.2%.

FX

- Hawkish RBA SOMP helps Aussie outperform and probe 200 DMA vs Greenback at 0.6728.

- Franc deflated after softer than forecast Swiss CPI even though SNB Chief Jordan repeats that further hikes cannot be ruled out given still very high underlying inflation; USD/CHF and EUR/CHF above 0.8900 and 0.9800 respectively

- Dollar drifting into NFP with DXY keeping afloat to 101.000 within a tight 101.110-370 range.

- Sterling sets fresh 2023 best beyond 1.2600, Loonie pares losses on 1.3500 handle ahead of Canada’s LFS and Euro retains 1.1000+ status amidst more big option expiries, disappointing EZ data and hawkish ECB rhetoric.

- PBoC set USD/CNY mid-point at 6.9114 vs exp. 6.9128 (prev. 6.9054)

- Russia’s Lavrov says we accumulated billions of IMR in Indian banks and needs to convert them into other currencies.

Fixed Income

- Debt retraces further from post-Fed/ECB peaks as risk appetite recovers ahead of NFP.

- Bunds also take heed of hawkish-leaning ECB commentary between 136.74-19 bounds.

- Gilts down in sympathy within a 101.71-23 range and T-note treading water above 116-00 inside tight 116-03/12 band.

Commodities

- Crude benchmarks are firmer, in a continuation of the complex’s upward momentum which commenced in Thursday’s session; albeit, WTI and Brent are still markedly down on the week.

- Overall, the complex remains firmly focused on growth concerns and banking-sector woes with broader market action awaiting the upcoming NFP report for the next scheduled catalyst.

- Spot gold is incrementally lower, in a USD 2038-2053/oz range after a week of marked gains for the yellow metal. Conversely, base metals are predominantly softer as the DXY attempts to lift off worst levels and after the mixed APAC trade.

Geopolitics

- Chinese Foreign Minister Qin, on meeting with Russian Foreign Lavrov, said China will persist in promoting peace talks and is willing to maintain communication and coordination with Russia to make tangible contributions to a political settlement of the Ukraine crisis, according to Reuters.

- White House said it is not clear right now that China can put forth a peace plan that Ukrainian President Zelenskiy will support, according to MSNBC.

- White House National Security Adviser Sullivan said we will take the necessary action to ensure Iran does not acquire a nuclear weapon and said the US still wants a diplomatic solution to Iran’s nuclear program. Sullivan also commented that he will be in Saudi Arabia this weekend to meet with Saudi leaders and that the US is still working towards the goal of a deal normalising relations between Israel and Saudi Arabia.

- Reports suggest a drone attack causes fire at Ilsky refinery in Southern Russia, according to Tass.

- Russia’s Foreign Minister Lavrov reiterates we will not say if the drone attack on the Kremlin is a case for war, but we will respond.

- Russia’s Wagner group head Prigozhin says their forces will leave Bakhmut on May 10th, forces have to do this due to a lack of ammunition.

US event calendar

- 08:30: April Change in Nonfarm Payrolls, est. 185,000, prior 236,000

- Change in Private Payrolls, est. 160,000, prior 189,000

- Change in Manufact. Payrolls, est. -5,000, prior -1,000

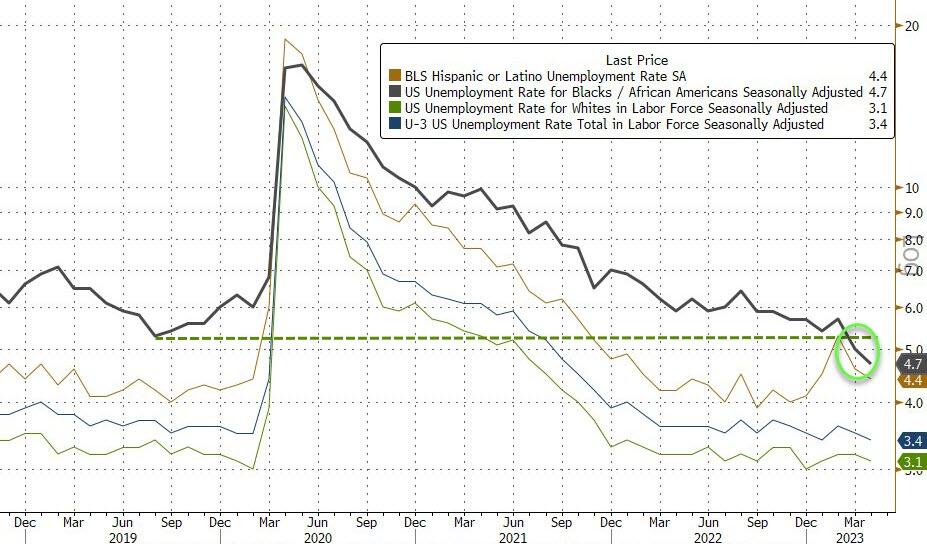

- Unemployment Rate, est. 3.6%, prior 3.5%

- Underemployment Rate, prior 6.7%

- Labor Force Participation Rate, est. 62.6%, prior 62.6%

- Average Weekly Hours est. 34.4, prior 34.4

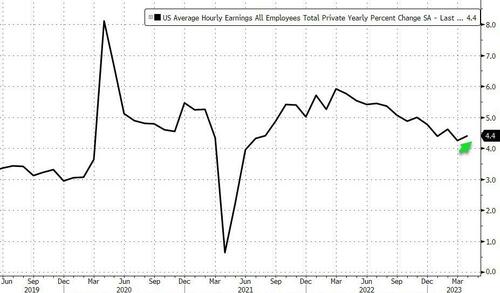

- Average Hourly Earnings YoY, est. 4.2%, prior 4.2%

- Average Hourly Earnings MoM, est. 0.3%, prior 0.3%

- 15:00: March Consumer Credit, est. $17b, prior $15.3b

DB’s Jim Reid concludes the overnight wrap

We have another bank holiday in the UK on Monday, and I’ll be going to my first ever street party to help celebrate the Coronation. I’ve done well to escape one so far in life but my luck has now run out. If something significant breaks in the US regional bank world over the weekend we may still do an EMR on Monday but if not we’ll see you on Tuesday.

There’s no doubt that this is a nervous time for markets as we wait for the next series of resolutions in the US regional banking crisis. Will there be broader deposit guarantees, agreed sales, stressed takeovers or will they manage to organically work their way through their issues? Whatever happens in the next few weeks, the problem is we are not yet in the likely recession where there will be economy-led asset write downs rather than just the mark to market ones, often on high quality bonds, that we have today. The other scary thing is that the attacks are increasingly looking speculative but risk becoming self fulfilling. So it’s certainly not just about fundamentals. Regardless, it’s going to be a long, bumpy and stressful ride over the next few quarters.

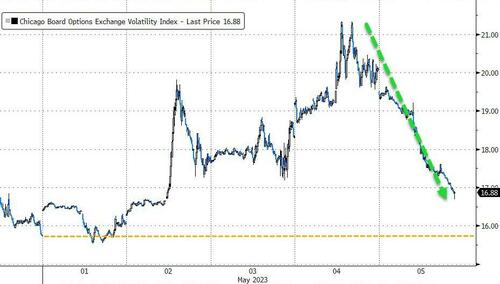

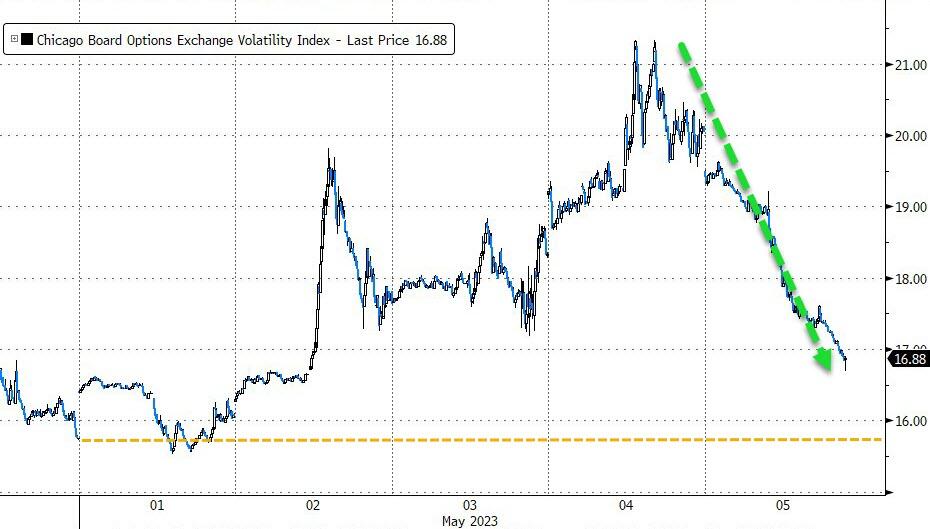

Indeed it’s a US regional bank headline crossfire at the moment and perhaps the most impressive thing over the last 24 hours was that the S&P 500 only closed -0.72% lower when the KRE regional bank index was down -5.45%. Having said that, the S&P 500 lost ground for a 4th consecutive day for the first time since February, just as the VIX index of volatility closed back above the 20-mark for the first time since March. The wider KBW Banks index (-3.82%) hit another two-and-a-half year low as every member of the index lost ground.

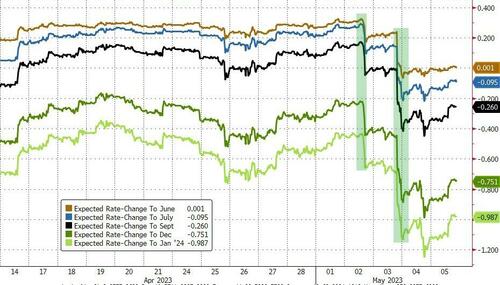

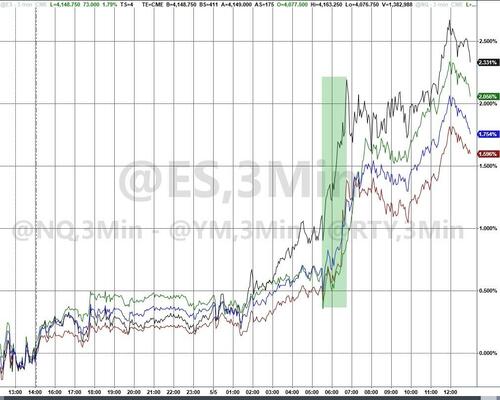

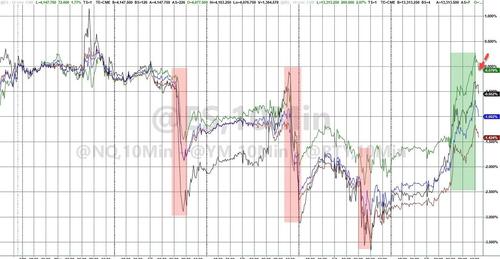

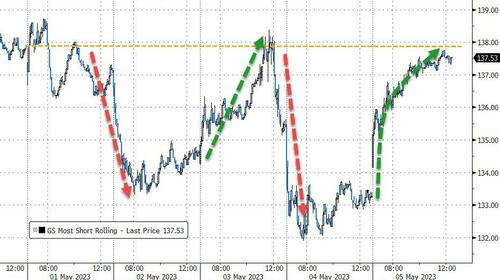

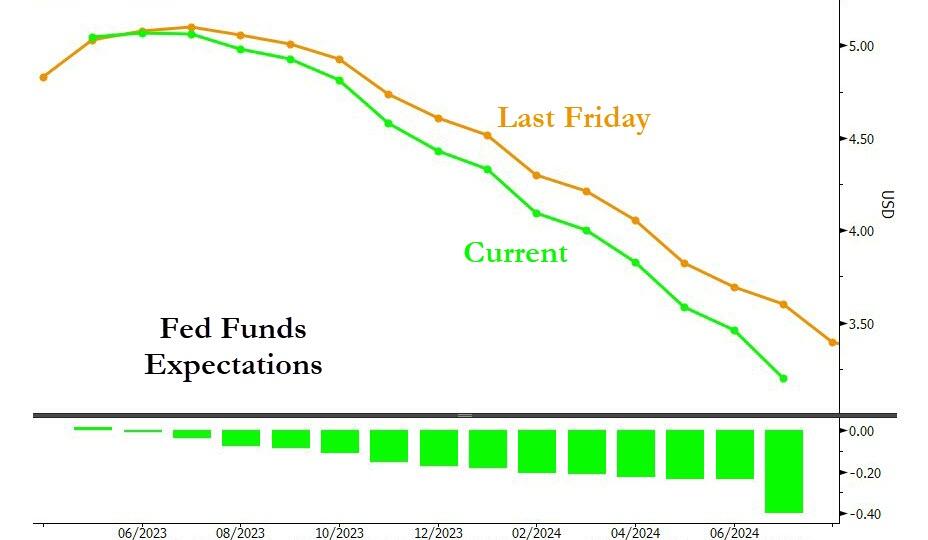

In terms of the latest developments, investors have continued to focus on a few specific regional banks, including PacWest Bancorp (-50.62%), Western Alliance Bancorp (-38.45%) and First Horizon (-33.16%). News about them continued to swirl through the day, with the FT reporting that Western Alliance were exploring options, “including a potential sale of all or part of its business”. However, Western Alliance themselves pushed back on this, saying that the story was “absolutely false”. Other banks weren’t immune to the contagion either, with losses for Zions Bancorp (-12.05%), Comerica (-12.28%), Citizens Financial Group (-5.22%) and Truist Financial Corp (-6.83%). Toward the end of the US trading session there were reports that the FDIC was planning to unveil a proposal as soon as next week that would see larger banks bear the majority of cost of refilling the Deposit Insurance Fund, which has been depleted in recent weeks. The reports indicated that banks with fewer than $10bn in assets would be exempt, additionally the size of deposits will also be a qualifying criteria. There was a bit of a recovery in US regionals after the bell with for example Western Alliance up around +9% and this erasing a quarter of its regular session losses. S&P futures are back up +0.38%, with the Nasdaq equivalent +0.48%, helped by Apple beating on earnings overnight.

Even in the regular session, the megacap tech stocks were impressively immune from the fallout, with the FANG+ index +0.95%. In terms of details on the Apple beat after the bell, they exceeded forecasts on revenue ($94.8bn vs $92.6bn estimates) even as sales fell 2.5% – which was not as bad as the company guided to. The technology company was trading up +2.5% in after-market trading even as revenues are expected to fall in the current quarter. Otherwise, the Dow Jones (-0.86%) was back in negative YTD territory (-0.06%) before this once again after its latest decline, with the Russell 2000 (-1.18%) index of small-cap stocks closing at a 6-month low.

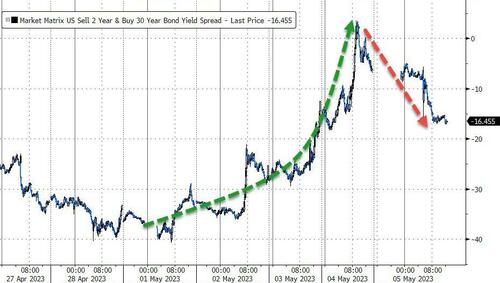

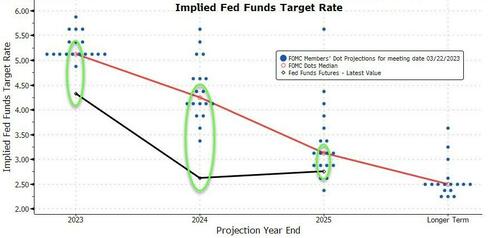

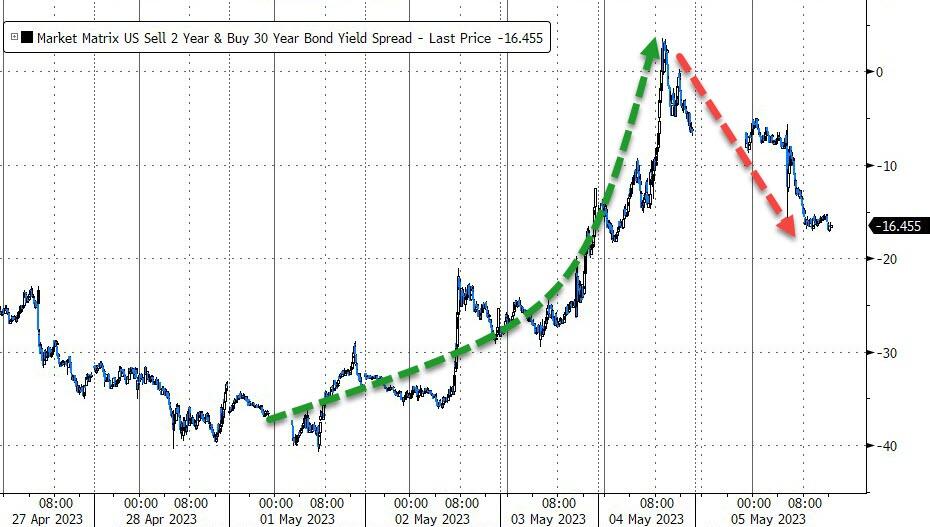

With the turmoil continuing to gather pace, investors moved to price in the growing chance of rate cuts from the Fed over the rest of the year. For instance, the rate priced in by the December meeting came down by -7.2bps on the day to 4.18%, which is its lowest in nearly a month. The July meeting now sees a 52% probability of a rate cut. This all helped drive a move lower in sovereign bond yields, particularly at the front end, where the 2yr Treasury yield fell -1.5bps to 3.790%, which was its lowest level in almost 8 months. In the meantime, the 10yr yield saw a +4.3bps increase to 3.379%, after being down -4.3bps midday. 2s10s is no more than a couple of basis points off it’s steepest levels of the last 7 months.

Back in Europe, the main news yesterday came from the ECB’s latest policy decision, where they announced a 25bps rate hike that leaves the deposit rate at a post-2008 high of 3.25%, in line with expectations. Although the hike was actually the smallest since their current hiking cycle began last July, there were plenty of hawkish details in the decision. First, they said that they expected to stop the reinvestments under their Asset Purchase Programme as of July. Second, ECB president Lagarde said there were still “significant” upside risks to the inflation outlook. And third, they made clear that there were more rate hikes to come, with Lagarde herself saying “we have more ground to cover and we are not pausing”. See our economists review of the meeting here. They continue to see a terminal of 3.75% with risks skewed towards 4% or even higher.

With the ECB striking a hawkish note, markets reacted by fully pricing in a 25bp hike at their next meeting in June. However, sovereign bond yields still fell back across the continent since investors were more concerned about the US banking system, meaning that yields on 10yr bunds (-5.7bps) and OATs (-3.9bps) were down while BTPs (+0.4bps) were just higher than unchanged on the day. It was much the same story for equities too, with the STOXX 600 (-0.47%) losing further ground as STOXX 600 banks (-1.46%) led the declines.

Whilst recession fears continued to gather pace in markets, one positive side effect for consumers has been the continued decline in commodity prices. Despite a marginal rise yesterday (+0.11%), the Bloomberg’s Commodity Spot Index hit its lowest level since December 2021 on Wednesday, which will be a positive tailwind on the inflation side over the coming months. In part that was driven by lower oil prices, with Brent crude down -8.80% on the week, despite a marginal rise yesterday (0.24%) to $72.50/bbl, which is a level we also haven’t seen since December 2021. At the same time, European natural gas prices (-2.72%) continued their relentless moves lower of late, with the latest move taking them to just €35.65/MWh, marking their lowest level since July 2021.

Looking forward now, the main highlight on today’s calendar will come from the US jobs report for April, which will be an important one for the Fed as they consider whether to pause on rate hikes at their next meeting. Our US economists at DB are looking for nonfarm payrolls to have grown by +150k, which if realised would actually be the slowest monthly growth since December 2020. In turn, that would lift the unemployment rate by a tenth to 3.6%. When it comes to wages, their view is that average hourly earnings growth will remain steady at +0.3%, keeping the annual rate at +4.2%. The release will set us up for the CPI report .

Asian equity markets are mixed this morning with the Hang Seng (+0.54%) leading gains alongside the S&P/ASX 200 (+0.30%). Meanwhile the CSI 300 (-0.58%) and the Shanghai Composite (-0.71%) are currently trading in the red. Elsewhere, markets in Japan and South Korea are closed for a holiday.

Early morning data showed that China’s service activity grew for a fourth straight month in April, continuing its post-Covid recovery, albeit with the Caixin services PMI falling to 56.4 in April from 57.8 in March. Meanwhile, in central bank news, the Reserve Bank of Australia (RBA) in its May statement on monetary policy indicated that it still sees ‘further tightening’ of monetary policy in order to return inflation to target.

Here in the UK, we got some more positive data releases yesterday, which comes ahead of the Bank of England’s decision next Thursday. That included mortgage approvals for March, which came in at a 5-month high of 52.0k (vs. 46.0k expected). Furthermore, the final composite PMI for April was revised up a full point from the flash reading to 54.9, which takes it to its highest level in a year. Keep an eye out on the UK political situation as well today, since local election results will be coming through that’ll offer a better sense of how the political parties are performing ahead of the next general election. Early results don’t look good for the ruling Conservative Party.

To the day ahead now, and the main data highlight will be the US jobs report for April. Otherwise, we’ll get German factory orders and French industrial production for March. From central banks, we’ll hear from the Fed’s Bullard and Book, along with the ECB’s Simkus and Elderson.

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

Sentiment steadies with stocks firmer post AAPL & pre-NFP/Fed speak – Newsquawk US Market Open

FRIDAY, MAY 05, 2023 – 06:35 AM

- European bourses and US futures are firmer despite the mixed APAC session as participants await NFP

- Within this, DAX 40 outperformers aided by German electricity adjustments and strong Adidas earnings.

- ABA is urging the SEC to investigate short-selling activity while the White House is hopeful on avoiding a debt default.

- AUD outperforms after hawkish-SOMP while CHF lags post-CPI; USD is softer but relatively rangebound.

- Core fixed benchmarks continue to pullback from post-Fed/ECB peaks, despite an uptick on German industrial data.

- Commodities are mixed with crude firmer in a continuation of recent price action while metals are generally softer.

- Looking ahead, highlights include US & Canadian Labour Market Reports. Speeches from Fed’s Cook & Bullard.

View the full premarket movers and news report.

Or why not try Newsquawk’s squawk box free for 7 days?

EUROPEAN TRADE

EQUITIES

- European bourses are firmer, Euro Stoxx 50 +0.3%, somewhat shrugging off the mixed APAC handover where regional banking concerns served as a headwind in holiday thinned conditions.

- The DAX 40 +0.7% is the marked outperformer, aided by German electricity adjustments and strong Adidas earnings, +7.8%; sectors are more of a mixed bag, with Energy outperforming while Travel/Healthcare lag.

- Stateside, futures are firmer and have been edging slightly higher in typically contained pre-NFP trade after yesterday’s regional banking induced pressures, ES +0.5%.

- Alibaba’s (BABA) Ant Group’s transformation into a fully regulated company has reportedly been held up by a reshuffle of China’s financial-regulatory system, according to WSJ sources.

- Cigna Group (CI) Q1 2023 (USD): Adj. Operating EPS 5.41 (exp. 5.22), Revenue 46.4bln (exp. 45.55bln); raises FY23 outlook.

- Click here and here for the European equity updates, highlights include: Adidas, IHG, Software AG & more.

- Click here for more detail.

FX

- Hawkish RBA SOMP helps Aussie outperform and probe 200 DMA vs Greenback at 0.6728.

- Franc deflated after softer than forecast Swiss CPI even though SNB Chief Jordan repeats that further hikes cannot be ruled out given still very high underlying inflation; USD/CHF and EUR/CHF above 0.8900 and 0.9800 respectively

- Dollar drifting into NFP with DXY keeping afloat to 101.000 within a tight 101.110-370 range.

- Sterling sets fresh 2023 best beyond 1.2600, Loonie pares losses on 1.3500 handle ahead of Canada’s LFS and Euro retains 1.1000+ status amidst more big option expiries, disappointing EZ data and hawkish ECB rhetoric.

- PBoC set USD/CNY mid-point at 6.9114 vs exp. 6.9128 (prev. 6.9054)

- Russia’s Lavrov says we accumulated billions of IMR in Indian banks and needs to convert them into other currencies.

- Click here for more detail.

- Click here for the notable FX expiries for today’s NY cut.

FIXED INCOME

- Debt retraces further from post-Fed/ECB peaks as risk appetite recovers ahead of NFP.

- Bunds also take heed of hawkish-leaning ECB commentary between 136.74-19 bounds.

- Gilts down in sympathy within a 101.71-23 range and T-note treading water above 116-00 inside tight 116-03/12 band.

- Click here for more detail.

COMMODITIES