MAY 4/2023 · by harveyorgan · in Uncategorized · Leave a comment·Editi

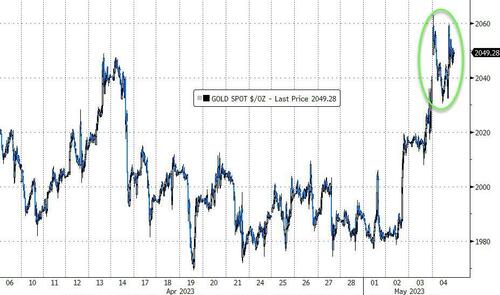

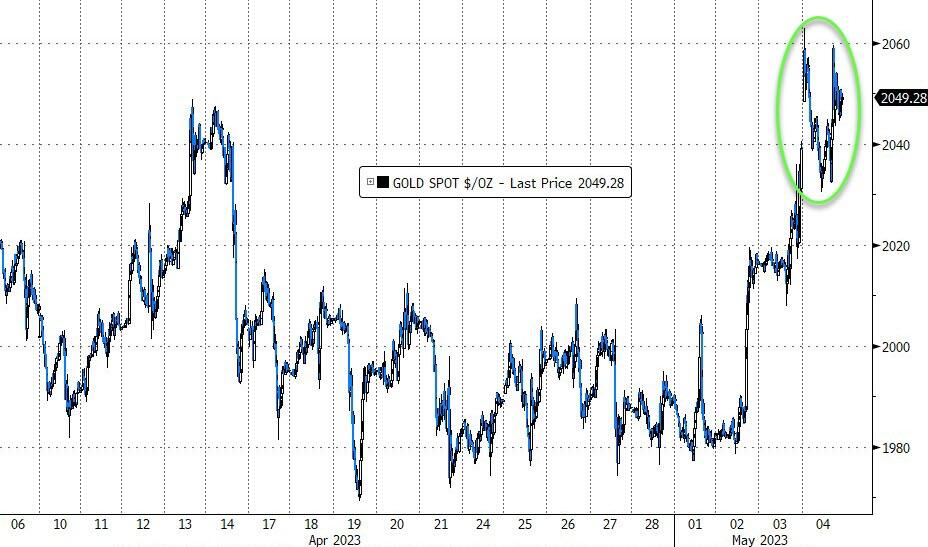

GOLD PRICE CLOSED: UP $19.00 TO $2047.20

SILVER PRICE CLOSED: UP 53 CENTS AT $25.95

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE $2050.00

Silver ACCESS CLOSE: 26.06

GOLD AND SILVER ARE BREAKING OUT. GOLD INTRADAY SURPASSED ITS RECORD HGH OF 2069 BUT FELL BACK ON BANK SHORT SELLING. THE KEY TO WATCH IS SILVER IF IT BREAKS 26.25. IT BROKE INTO THE $26.00 LATE THIS AFTERNOON.

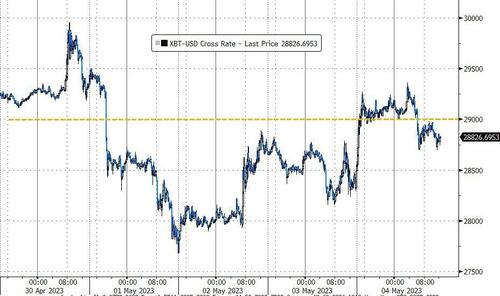

Bitcoin morning price:, $29,209 UP 419 Dollars

Bitcoin: afternoon price: $28,845 UP 55 dollars

Platinum price closing $1041.25 DOWN $16.75

Palladium price; $1458.69 UP $26.90

“Our government… teaches the whole people by its example. If the government becomes the lawbreaker, it breeds contempt for law; it invites every man to become a law unto himself; it invites anarchy.” … Louis D Brandeis (former Supreme Court Justice)

GO GATA!

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,775.35 UP 10.20 CDN dollars per oz (ALL TIME HIGH 2,775.35*) ALL TIME HIGH HIT TODAY//CLOSING

BRITISH GOLD: 1630.29 UP 13.20 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)*ALL TIME CLOSING HIGH TODAY

EURO GOLD: 1861.21 UP 7.56 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)*//ALL TIME CLOSING HIGH

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

CAPITAL 4

624 H BOFA SECURITIES 1100

657 C MORGAN STANLEY 6

661 C JP MORGAN 242 264

726 C CUNNINGHAM COM 1

737 C ADVANTAGE 18 2

800 C MAREX SPEC 9

880 H CITIGROUP 1234

905 C ADM 1

TOTAL: 1,503 1,503

JPMorgan stopped 264/1503 contracts

FOR MAY:

GOLD: NUMBER OF NOTICES FILED FOR MAY/2023. CONTRACT: 1503 NOTICES FOR 150,300 OZ or 4.6749 TONNES

total notices so far: 4495 contracts for 449,500 oz (13.981 tonnes)

FOR MAY:

SILVER NOTICES: 26 NOTICE(S) FILED FOR 130,000 OZ/

total number of notices filed so far this month : 1718 for 8,565,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $13.90

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/NO CHANGES IN GOLD INVENTORY AT THE GLD:///

INVENTORY RESTS AT 928.30 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 11 CENTS AT THE SLV//

SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.174 MILLION OZ FROM THE SLV/: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 467.244 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A TINY SIZED 85 CONTRACTS TO 142,490 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS STRONG SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.11 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.11). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A GIGANTIC GAIN ON OUR TWO EXCHANGES OF 1861 CONTRACTS. WE HAD 600 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 3 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 3 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A HUMONGOUS ISSUANCE OF EXCHANGE FOR PHYSICALS( 1861 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.105 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 5,000 OZ(E.FP.’S LOWER THE AMOUNT OF SILVER STANDING)+ 3.0 MILLION OZ OF EXCHANGE FOR RISK(RAISES THE AMOUNT OF SILVER STANDING):THUS TOTAL OF 15.735 MILLION OZ OF STANDING FOR DELIVERY V) TINY SIZED COMEX OI GAIN/ HUMONGOUS SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –133 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTRACTS for 4 days, total 3271 contracts: OR 16.355 MILLION OZ . (818 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 16.355 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 16.355 MILLION OZ/INITIAL

RESULT: WE HAD A TINY SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 85 CONTRACTS WITH OUR $0.11 GAIN IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUMONGOUS SIZED EFP ISSUANCE CONTRACTS: 1861 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 13.105 MILLION OZ//FIRST DAY NOTICE FOLLOWED BY TODAY’S E.F.P. JUMP OF 5,000 OZ (DECREASES THE AMOUNT OF SILVER STANDING) +// + 3.00 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //TOTAL STANDING 12.735 MILLION OZ + 3.0 MILLION = 15.735 MILLION OZ// .. WE HAVE A HUGE SIZED GAIN OF 1813 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 26 NOTICE(S) FILED TODAY FOR 130,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A HUGE SIZED 10,400 CONTRACTS TO 504,938 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: removed 734 CONTRACTS

WE HAD A HUGE SIZED INCREASE IN COMEX OI ( 11,134 CONTRACTS) WITH OUR $13.90 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR MAY. AT 3.5085 TONNES ON FIRST DAY NOTICE // PLUS A MONSTROUS 130,200 OZ QUEUE. JUMP :(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)////YET ALL OF..THIS HAPPENED WITH OUR $13.90 GAIN IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING.WE HAD A GIGANTIC SIZED GAIN OF 13,770 OI CONTRACTS (42.830 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3370 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 504,938

IN ESSENCE WE HAVE A HUGE SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 13,770 CONTRACTS WITH 10,400 CONTRACTS INCREASED AT THE COMEX AND 3370 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 13,770 CONTRACTS OR 42.830 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3370 CONTRACTS) ACCOMPANYING THE HUGE SIZED GAIN IN COMEX OI (10,400 //TOTAL GAIN IN THE TWO EXCHANGES 13,770 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 3.5085 TONNES FOLLOWED BY TODAY’S MONSTROUS QUEUE JUMP OF 130,200 OZ // NEW STANDING: 14.0281 TONNES // ///3) ZERO LONG LIQUIDATION//4) HUGE SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 12,193 CONTRACTS OR 1,219,300 OZ OR 37.925 TONNES IN 4 TRADING DAY(S) AND THUS AVERAGING: 3040 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAY(S) IN TONNES 37.925 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 37.925/3550 x 100% TONNES 1.070% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES ( MUCH SMALLER THAN LAST MONTH)

MAY: 37.925 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A TINY SIZED 48 CONTRACTS OI TO 142,490 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 1861 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1861 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1861 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 48 CONTRACTS AND ADD TO THE 1891 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1813 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 9.065 MILLION OZ

OCCURRED WITH OUR $0.11 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED UP 27.18 PTS OR .82% //Hang Seng CLOSED UP 249.57 POINTS OR 1.27% /The Nikkei closed //Australia’s all ordinaries CLOSED DOWN 0.01 % /Chinese yuan (ONSHORE) closed UP 6.9120 /OFFSHORE CHINESE YUAN UP TO 6.9153 /Oil DOWN TO 68.49 dollars per barrel for WTI and BRENT AT 73.54 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING 6.9120 AGAINST US DOLLAR/OFFSHORE STRONGER AT 6.9153

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A HUGE SIZED 10,400 CONTRACTS UP TO 504,204 WITH OUR STRONG GAIN IN PRICE OF $13.90 ON WEDNESDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF MAY… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3370 EFP CONTRACTS WERE ISSUED: : JUNE 3370 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3370 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GIGANTIC SIZED TOTAL OF 13,770 CONTRACTS IN THAT 4470 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A HUGE SIZED GAIN OF 10,400 COMEX CONTRACTS..AND THIS GIGANTIC SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $13.90. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (14.028) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 14.028 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $13.90) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR GIGANTIC SIZED GAIN OF 13,770 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 45.113 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY. (3.5085 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 130,200 oz (4.049 TONNES)//NEW STANDING 14.028 TONNES ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $13.90

WE HAD –REMOVED 734 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 13,770 CONTRACTS OR 1,377,000 OZ OR 42.830 TONNES.

Estimated gold comex today 319.984// GOOD

final gold volumes/yesterday 250,847 fair

//MAY 4/ MAY 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 578.72 oz 18 KILOBARS Brinks . |

| Deposit to the Dealer Inventory in oz | 21,798.378 OZ Brinks 678 kilobars |

| Deposits to the Customer Inventory, in oz | 160,755.000 Oz JPM 5,000 kilobars |

| No of oz served (contracts) today | 1503 notice(s) 150,300 OZ 4.6749 TONNES |

| No of oz to be served (notices) | 15 contracts 1500 oz 0.0466 TONNES |

| Total monthly oz gold served (contracts) so far this month | 4495 notices 449,500 OZ 13.981 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 1

i) Out of Brinks: 578.720 oz (18 kilobars)

total withdrawals: 578.72 oz

Adjustments; 1

ii) customer to dealer Manfra: 3,858.125 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 1518 contracts having LOST 442 contracts. We had 1744 contracts filed

on WEDNESDAY, so we gained a monstrous 1302 contracts or an additional 130,200 oz (4.049 tonnes) will stand for gold in this non active delivery month of May.

June GAINED 2780 contracts UP to 381,388 contracts.

July added 135 contracts to stand at 759 contracts.

AUGUST GAINED 6765 contracts up to 74,503 contracts

We had 1518 contracts filed for today representing 151,800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 240 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1503 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 264 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2023. contract month,

we take the total number of notices filed so far for the month (4,495 x 100 oz ), to which we add the difference between the open interest for the front month of MAY 1518 CONTRACTS) minus the number of notices served upon today 1503 x 100 oz per contract equals 451,000 OZ OR 14.028 TONNES the number of TONNES standing in this NON- active month of May.

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (4,495 x 100 oz)+1518 OI for the front month minus the number of notices served upon today (1503)x 100 oz} which equals 451,000 oz standing OR 14.028 TONNES

TOTAL COMEX GOLD STANDING: 14.028 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,678,143.492 OZ 52.197 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,518,837.019 OZ

TOTAL REGISTERED GOLD: 12,385,372.015 (385,23 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,133,515.004 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,707,229 OZ (REG GOLD- PLEDGED GOLD) 333.03 tonnes//

END

SILVER/COMEX

MAY 4//2023// THE MAY 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 988,476.636 oz Brinks CNT Manfra . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 323,570.182 oz Manfra |

| No of oz served today (contracts) | 26 CONTRACT(S) (130,000 OZ) |

| No of oz to be served (notices) | 834 contracts (4,170,000 oz) |

| Total monthly oz silver served (contracts) | 1713 Contracts (8,565,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) into Manfra: 323,570.182 oz

Total deposits: 323,570.182 oz

JPMorgan has a total silver weight: 139,607 million oz/269.022 million =51.67% of comex .//dropping fast

Comex withdrawals: 3

i) Out of Brinks 4916.450 oz

ii) Out of CNT: 393,973.800 oz

iii) Out of manfra 589,586.380 oz

Total withdrawals; 988,476.636 oz

adjustments: 3 all dealer to customer

a)JPMorgan 880,618.750 oz

b)Brinks 54,341.420 oz

c) Manfra: 251,190.610 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 31.301 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 269.022 million oz

CALCULATION OF SILVER OZ STANDING FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2023 OI: 860 CONTRACTS HAVING LOST 1 CONTRACT(S). WE HAD 0 CONTRACTS FILED

ON WEDNESDAY, SO WE LOST 1 CONTRACT OR AN ADDITIONAL 5,000 OZ OF SILVER WILL NOT STAND FOR DELIVERY IN THIS VERY

ACTIVE DELIVERY MONTH OF MAY AS, FOR THE 3RD DAY IN A ROW, THESE GUYS WERE E.F.P.’d TO LONDON AS NO SILVER COULD BE FOUND OVER HERE..

.JUNE HAD A 36 CONTRACT GAIN TO 908

JULY HAD A 517 CONTRACT LOSS TO 120,710 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 26 for 130,000 oz

Comex volumes// est. volume today 70,169 GOOD

Comex volume: confirmed yesterday: 54,772 FAIR

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 1713 x 5,000 oz = 8,565,000 oz

to which we add the difference between the open interest for the front month of MAY(860) and the number of notices served upon today 26 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2023 contract month: 1713 (notices served so far) x 5000 oz + OI for the front month of May (860) – number of notices served upon today (26 )x 500 oz of silver standing for the MAY contract month equates to 12.735 million oz + THE CRIMINAL 3.0 MILLION EXCHANGE FOR RISK//NEW TOTAL 15.735 MILLION OZ//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MAY 4/WITH GOLD UP $19.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.30 TONNES

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

APRIL 10/WITH GOLD DOWN $21.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91 TONNES

APRIL 6//WITH GOLD DOWN $9.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91

APRIL 5//WITH GOLD UP 0 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04

APRIL 4/WITH GOLD UP $36.30 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

APRIL 3/WITH GOLD UP $14.20 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.02 TONNES

MARCH 31/WITH GOLD DOWN $10.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD////INVENTORY RESTS AT 928.02 TONNES

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

GLD INVENTORY: 928.34 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 4/WITH SILVER UP 53 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF .174 MILLION OZ INTO SLV.//INVENTORY RESTS AT 467.174 MILLION OZ//

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 10/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 6/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 4.643 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 468.585 MILLION OZ//

APRIL 5/WITH SILVER DOWN 4 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.942 MILLION OZ

APRIL 4/WITH GOLD UP $1.11 TODAY CRIMINAL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.47 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 463,942 MILLION OZ

APRIL 1/WITH SILVER DOWN 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.412

MARCH 31/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD/: A MASSIVE 4.779 MILLION OZ DEPOSITED INTO THE SLV///INVENTORY RESTS AT465.412 MILLION OZ

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

CLOSING INVENTORY 467.174 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

TODAY: MATHEW PEIPENBURG:

Matthew Piepenburg

May 4, 2023

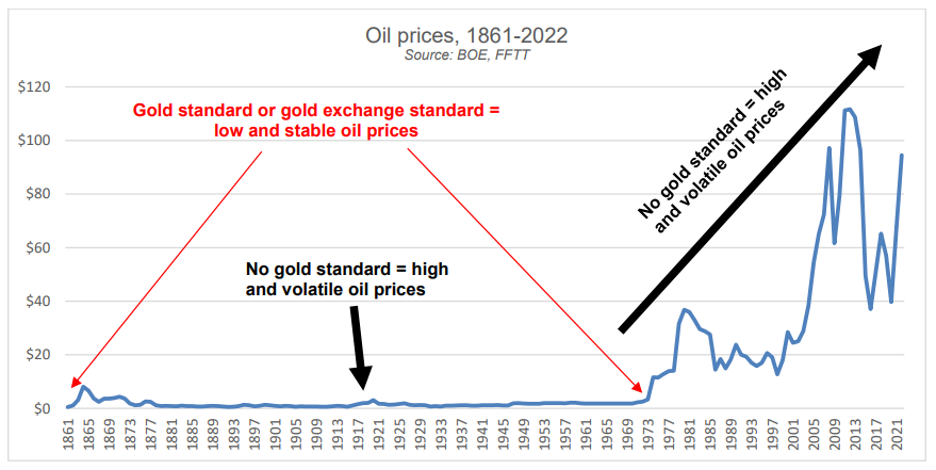

Below we look at the math, history and current oil environment in the backdrop of a global debt crisis to better predict currency and gold market direction without the need of tarot cards.

Seeing the Future: Math vs. Crystal Balls

Those looking forward only need to look at current and backward math to make relatively clear forecasts without risking the mug’s game of deriving crystal ball predictions.

Not surprisingly, the theme and math of simple (as well as appalling) US debt levels makes such forward-thinking almost too simple.

The Oil Issue: Is Anti-Shale Anti-American?

Although not as fluent as others in the oil trade or the green politics of the extreme US left, I’ve argued in prior reports that the current administration’s anti-shale policies make for some good (debatable?) environmental chest-puffing while ignoring the math, history and science of sound national as well as well as global thinking.

(But then again, the entire woke fiasco of current US policy seems to be on a crusade to cancel such things as math, history and science; so, thinking contextually or globally is beyond their sound-bite-driven stump-speeches.)

Oil, however, still matters.

And when understood in the broader context of the macro-economic themes we’ve tracked for years–namely debt, currencies, inflation, gold, a cornered Fed and a weaponized USD–the current and future trends are already in motion.

And as for the endless debate as to global warming, butterfly-friendly energy policies and the simple reality of fossil fuels as a part of, rather than threat to, our planet, I’m certainly not here to answer or solve the same.

Certainly the Germans (and their solar powered ideas in a part of Europe with very little sun) are not getting it… In fact, they are getting much of their (nuclear) energy from France and are now forced to burn coal to get through the winter.

I am here, however, to lay down some objective facts and ask some blunt questions.

Oil Politics

Biden, it seems fairly clear to all, is not in charge of US policy.

That’s a scary fact. Even more scary, however, is determining who is in charge?

Again, not something I can answer.

But if he were in charge, we’d all be amused to ask how he expected Saudi Arabia to welcome him and his embarrassing pleas for Saudi production increases (to ostensibly ease inflated US fuel costs) after previously telling the world he considered Saudi Arabia a pariah state…

We all remember that embarrassing fist-pump with the Crown Prince.

Meanwhile, Saudi is now spending far more time with the Chinese and Iran…

We’d also love to hear the White House explain how it expects increased US shale production to reduce energy inflation when it has been simultaneously seeking to legislate oil off the American page.

Furthermore, it would be worth reminding Americans and politicians tired of inflated fuel prices that the vast majority of those inflated pump costs are due to US taxes per gallon, not Saudi production cuts.

But I digress.

Oil Math

At the current levels of US oil production and exploration, the US (according to its own Dallas Fed) will have to engage in annual energy price inflation levels of 8-10% just to keep the oil industry’s lights on at a breakeven price level.

Such conservative inflation figures for oil/fuel pricing, when seen in the context of over $31T in US Federal debt, basically means that Uncle Sam’s ability to cover his ever-increasing public debt burden will weaken by at least 8-10% per year at a moment in US history where Uncle Sam needs all the help, rather than weakness, he can get.

Fighting Inflation with Inflation, and Debt with Debt?

Needless to say, the only “solution” to these inflated debt burdens will be the monetary mouse-clicker at the Eccles Building, whose doom-loop (yet now ossified) “solution” to addressing inflated oil prices is the even more inflationary policy of printing more fake money to “fakely” cure an inflation crisis.

You really can’t make this stuff up.

Fed monetary policy, ever since patient-zero Greenspan sold his soul (and sound-money, gold-backed academic thesis) to Wall Street and Washington, boils down to this: We can solve a debt crisis with more debt, and an inflation crisis with more, well…inflation.

Does this seem like “sound monetary policy” to you?

Or, Just Export Your Inflation to the Rest of the World?

But as I’ve warned for years, Uncle Sam’s first instinct (as holder of the world reserve currency) whenever handed a hot-potato of self-inflicted inflation, is to hand it off to the rest of the world—i.e., to export his inflation to friends and foes alike.

Global energy importers in Europe, emerging markets, India, China, and Japan, for example, are facing what accountants call a balance of payments crisis, but what I’ll bluntly call by its real name: A currency crisis.

That is, under the current, but potentially dying petrodollar system, these countries will need more USDs to buy oil.

But that’s where the problem lies.

Why?

Simple: Those USDs are drying up (unless more are printed).

How Long Will Global Currencies (& Leaders) Remain Prisoner to the USD?

Regardless of whether you believe in the perpetual hegemony of the USD as a payment system or not, we can all agree that USD liquidity is drying up (whether it be from the milk-shake theory absorption in euro-dollar and derivative markets or from post-sanction de-dollarization).

Nations facing the double whammy of needing more USDs to pay for inflated oil prices and inflated USD-denominated debts around the globe are going to being crying “uncle!” rather than just “Uncle Sam.”

What can these nations do in the face of that bullying hot potato known as the USD? How can they service these increased USD payment (oil and debt) burdens?

How the US Creates a Global Currency Crisis

Well, short of turning their backs on the USD (not yet), the only current option other nations have is to devalue (i.e., inflate and debase) their own currencies at home, which is how Uncle Sam makes his problem just about everybody else’s problem…

As I often say, with friends like the US, who needs enemies?

Something, however, has to give.

How Physical Gold Offers Better Pricing than Fiat Dollars

This clearly broken system of the US exporting its inflation upon a world forced since the 1970’s to import oil under a broken and inflationary Greenback has a genuine potential to implode.

Already, countries like Ghana have realized that it’s better to trade oil in real gold rather than fake fiat dollars.

Long before the petrodollar became the mad king, for example, history recognized that physical gold was a far better instrument of payment to settle stable oil pricing.

See for yourself.

As more and more of the world recognizes the currency crisis slowly in play now, and then steadily in greater pain tomorrow, this “Balance of Payments” (i.e., currency) crisis can easily evolve into a “change of payments” reality in which gold re-emerges as a superior payment system for oil.

Think about that.

More Tailwinds for Gold

As of this writing, the physical oil markets are greater than 15X the size of the physical gold markets on an annualized (USD) production basis.

If the world turns slowly (then all at once?) toward settling oil in gold (partially or fully) to avoid a global currency crisis, gold will have to be repriced at levels significantly higher than current pricing.

Hmmm.

Something worth tracking, no?

Well, the Zeitgeist suggests that we are not the only ones tracking these trends…

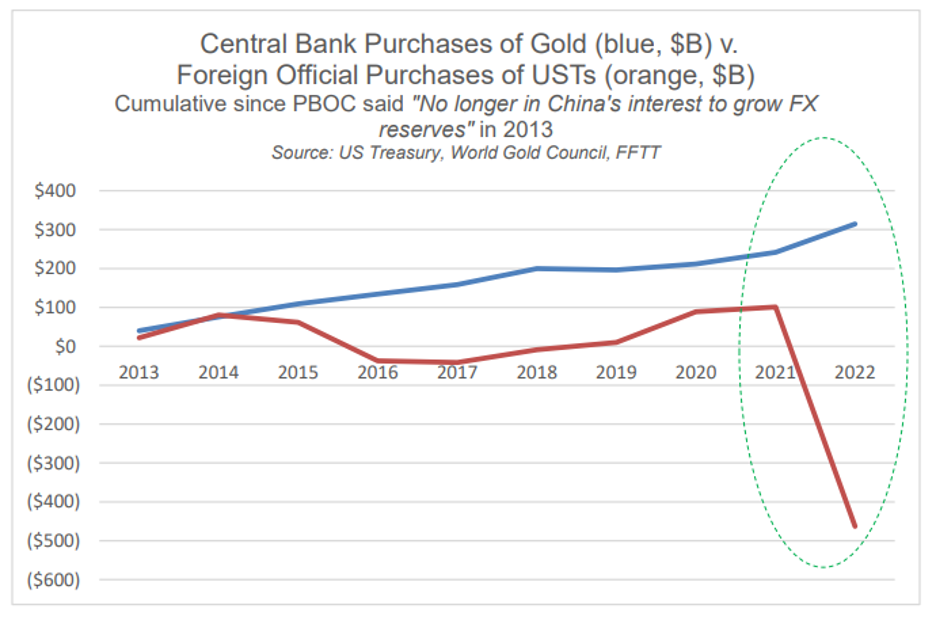

The Central Banks Are Catching On to (and Stacking) Gold

A recent pole of over 80 central banks holding greater than $7T in FX reserves indicated that 2 out of 3 polled strongly believe that central banks will be making more, not less, purchases of physical gold in 2023.

Again: Are you seeing a trend? Are you seeing the context? Are you seeing why?

As I’ve said countless times and will say countless times more: Debt matters.

Debt matters because debt, once it crosses the Rubicon of insanity and unsustainability, impacts everything we market jocks were supposed to have been taught in school and in the office—namely bonds, currencies, inflation and recessionary cycles follow debt cycles.

In short: It’s all tied together.

Once you understand debt, the policies, reactions, weaknesses, truths, lies, and cycles are far easier to see rather than just “predict.”

The increasing loss of faith in the world reserve currency and its embarrassing IOUs (i.e., USTs) is not merely the domain of “gold bugs” but the simple and historical consequence of the blunt math which always follows broken regimes, of which the US is and will be no exception.

The graph below, is thus worth repeating, as the world is clearly turning away from Uncle Sam’s drunken bar tabof debased dollars and IOUs toward something more finite in supply yet more infinite in duration.

Again: See the trend?

3,Chris Powell of GATA provides to us very important physical commentaries

Russia will only be happy with one currency: gold

(Reuters/GATA)

India and Russia suspend talks to settle trade in rupees

Submitted by admin on Thu, 2023-05-04 06:56Section: Daily Dispatches

But both nations seem to have a lot of a stronger currency, a shiny yellow metal. …

* * *

By Aftab Ahmed and Swati Bhat

Reuters

Thursday, May 4, 2023

India and Russia have suspended efforts to settle bilateral trade in rupees, after months of negotiations failed to convince Moscow to keep rupees in its coffers, two Indian government officials and a source with direct knowledge of the matter said.

This would be a major setback for Indian importers of cheap oil and coal from Russia who were awaiting a permanent rupee payment mechanism to help lower currency conversion costs.

With a high trade gap in favour of Russia, Moscow believes it will end up with an annual rupee surplus of over $40 billion if such a mechanism is worked out and feels rupee accumulation is “not desirable,” an Indian government official, who did not want to be named, told Reuters. …

… For the remainder of the report:

END

END

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

Newmont Merger Would Create The World’s Biggest Gold Miner

THURSDAY, MAY 04, 2023 – 01:15 PM

By Charles Kennedy of OilPrice

The board of Australia’s Newcrest Mining has recommended the latest takeover offer of bigger sector player Newmont, which last month valued the target company at $19.5 billion.

“The latest offer is one that the board would be prepared to recommend subject to successful due diligence during the period,” interim Newcrest chief executive Sherry Duhe said this week, as quoted by Bloomberg.

“This transaction would strengthen our position as the world’s leading gold company by joining two of the sector’s top senior gold producers and setting the new standard in safe, profitable and responsible mining,” Newmont’s chief executive TomPalmer said, as quoted by Reuters, after the announcement of the latest offer.

Newmont first made a non-binding offer for Newcrest in February, which valued the company at $16.9 billion, but Newcrest rejected that as too low. Then the gold miner tried again, sweetening the offer.

If a deal does materialize, it will bring Newmont’s gold output much higher—twice as high as the output of its rival, Barrick Gold, according to Reuters. It would also constitute the third-largest deal involving an Australian company as well as the third-largest M&A deal this year, the news outlet noted.

According to Bloomberg, the deal would also boost Newmont’s presence in copper: the basic metal, which is essential for the energy transition, makes up a quarter of Newcrest’s total output at present, but the company wants to boost that to 50% by 2030.

Copper is indispensable for wind and solar farm wiring and for EV engines. Yet supply of the metal is under threat because of insufficient new mining capacity coming on stream and falling ore grades.

Warnings of a looming copper shortage have been multiplying in recent months, but they have not yet made any forecasters budge on their expectations of an EV boom combined with a wind and solar boom.

END

5.IMPORTANT COMMENTARIES ON COMMODITIES:

end

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS// THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 6.9120

OFFSHORE YUAN: 6.9153

SHANGHAI CLOSED UP 27.18 PTS OR .82%

HANG SENG CLOSED UP 249,57 PTS OR 1.27%

2. Nikkei closed

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 100.95 EURO FALLS TO 1.1067 DOWN 2 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.415 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 134.42 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.268***/Italian 10 Yr bond yield RISES to 4.166*** /SPAIN 10 YR BOND YIELD RISES TO 3.356…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.087

3j Gold at $2041.95 silver at: 25.58 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 98 /100 roubles/dollar; ROUBLE AT 78.30//

3m oil into the 68 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 134.42 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .415% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8851 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9795 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.349 DOWN 5 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.703 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.816 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.49…

GREAT BRITAIN/10 YEAR YIELD: UP 4 BASIS PTS AT 3.739

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

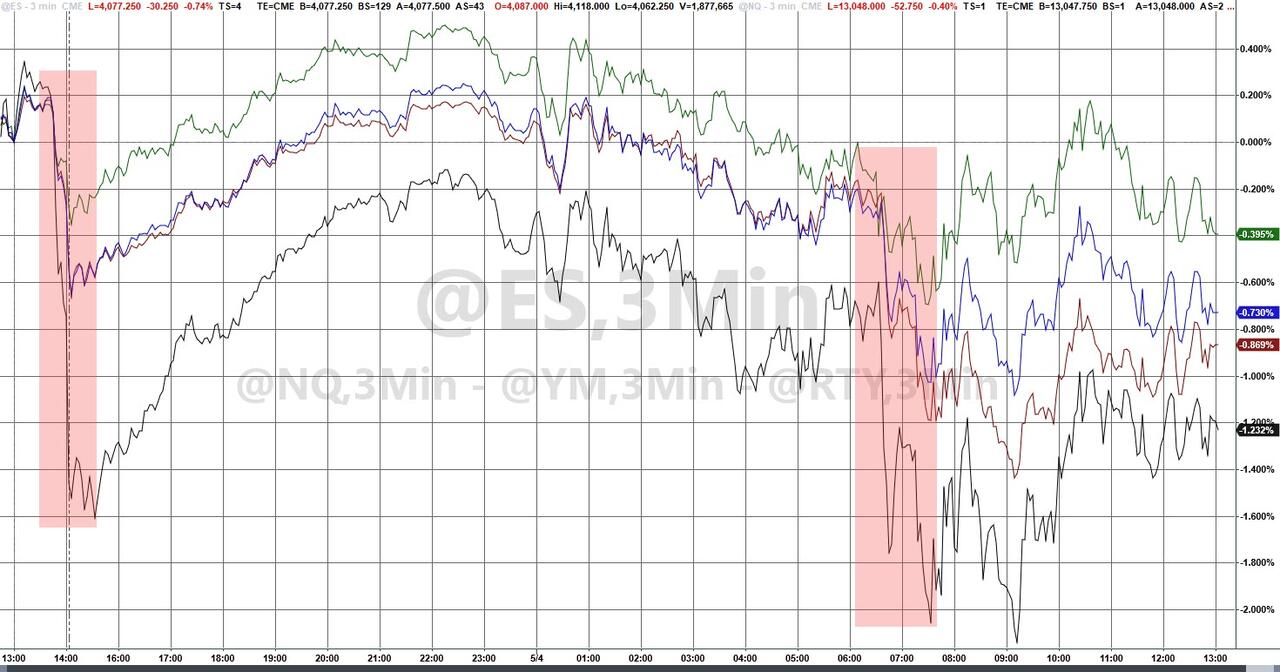

Futures Slide As Fed Pauses Rate Hikes, Regional Banks Resume Plunge

THURSDAY, MAY 04, 2023 – 08:03 AM

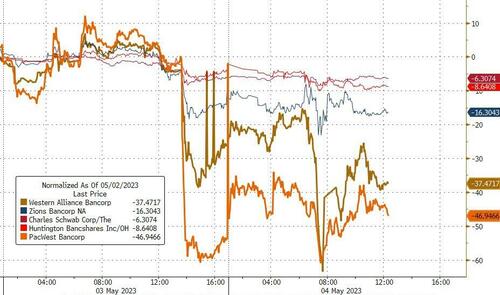

US stocks were set to open lower, reversing a modest gain earlier and extending a three-day selloff as investors weighed the possibility of more bank failures against a pause in rate hikes by the Federal Reserve as growth slows. Contracts on the S&P 500 were down 0.3% as of 7:45 a.m. ET while Nasdaq 100 futures were flat. The benchmark S&P 500 had slid on Wednesday, marking its longest losing streak in nearly two months even as the Fed signaled a possible pause in its most aggressive tightening campaign in decades. Sentiment was routed as US regional banks tumbled further even after PacWest said its deposits rose since March and confirmed a Bloomberg report that it’s talking with potential investors in a bid to calm markets. The stock slumped as much as 45% premarket. And Western Alliance was down 23%, though it claimed it hasn’t seen unusual deposit flows.

Treasury yields kneejerked higher but have also since reversed as worries over the impending debt-ceiling deadline weigh. A measure of the dollar is weakening as traders hike recession bets, and gold has steadied after jumping to just shy of record highs on news that the Fed may pause tightening. Iron ore is declining, while copper gains as concerns mount around global supply. Oil rose, recovering after a sudden dip early in the session on Thursday as Chinese traders returned after a break.

In premarket trading, PacWest Bancorp shares slumped as much as 46% with other regional lenders also plunging, after the Los Angeles-based bank confirmed that it is weighing strategic options. Western Alliance shares fell as much as 24%, headed for a fifth straight day of declines, as confidence in regional lenders remains shaky. The Arizona-based lender sought to reassure the market with an update on deposits after US markets closed, saying that it hasn’t seen unusual deposit flows following the sale of First Republic Bank. First Horizon stock was thrashed after TD terminated its planned $13.4 billion acquisition of the Memphis-based bank, citing uncertainty over a regulatory approval timeline. TD will fork out $200 million in cash to get out of the deal. TripAdvisor also dropped after the online travel company reported first-quarter adjusted earnings per share that missed consensus estimates. On the other end, Arconic surged 28% after a report that private equity firm Apollo Global Management was nearing a deal to buy the industrial-parts manufacturer. Here are all the notable premarket movers:

- Qualcomm falls as much as ~6.7% in premarket trading, after the chipmaker gave a third-quarter forecast that was weaker than expected. Analysts say the guidance shows that weakness in the smartphone market will persist until September.

- TripAdvisor shares drop 8.2% in premarket trading after the online travel company reported first-quarter adjusted earnings per share that missed consensus. Analysts flagged the performance of the company’s Viator business, which they said was the main driver behind the miss on adjusted Ebitda.

- Upwork shares drop as much as 14% in US premarket trading, set to hit a three-year low, after the online recruitment company cut its full-year revenue forecast. Analysts lowered their price targets on the stock, seeing an impact on spending from a tough macroeconomic backdrop, though some brokers were positive on the steps the company is taking to progress toward profitability.

- Etsy shares gained in extended trading, after the online retailer reported first- quarter results that beat expectations and gave an outlook that Bloomberg Intelligence sees as encouraging.

- Zillow Group advanced in extended trading, after the online real estate company gave a revenue outlook for the current period that at the midpoint of the forecast range topped the average analyst estimate. Analysts are positive on the report, and highlight the company’s Premier Agent offering as notably strong.

US stocks slumped to start the month of May as glum economic data has fueled concerns about a possible recession. The Fed on Wednesday hiked rates as expected, while pausing the tightening process even as Chair Jerome Powell said his forecast was for modest growth and not a recession, and said he disagrees with the staff’s bearish consensus. But he reiterated that the process of getting inflation down had a long way to go.

Susannah Streeter, head of money and markets at Hargreaves Lansdown, said hopes that a rate cut might come before the end of the year faded after the Fed’s statement. “It’s clear inflation is still not coming down as fast as policymakers hoped,” she said. “It looks like the hiking cycle is now at an end, but the door to another rise is still slightly ajar and that’s still causing nervousness given that rates are already at the highest level for 16 years.”

“The tightening in credit conditions will put some significant downward pressure on the economy,” Michelle Girard, head of US for NatWest Markets, said on Bloomberg Television. “You will see the Fed in a position to move policy to a less restrictive stance sooner than what the Fed chairman today was suggesting.”

Meanwhile, strategists at UBS Global Wealth Management said even a pause in hikes by the Fed may not necessarily spur a rally in equities as those expectations should now be baked in. In past cycles, the S&P 500 typically didn’t bottom until after the Fed started to cut rates, the team led by Mark Haefele wrote in a note.

“The ECB meeting is expected to be a more complex one compared to that of the Federal Reserve,” said Erick Muller, director of product and investment strategy at Muzinich & Co. “If no one doubts the ECB will raise rates again at this week meeting, the magnitude of the rise and the tone of the communication are difficult to forecast.”

European stocks are on the back foot as investors count down to a rate decision from the European Central Bank later today. The Stoxx 600 is down 0.7% with media, real estate and autos the worst-performing sectors. Energy names have outperformed, led higher by Shell who maintained the pace of share buybacks after quarterly profit topped estimates. Here are the most notable European movers:

- Shell rises as much as 3.5%, the most since April 3, after the oil major’s quarterly profit beat expectations, with strong performances across divisions and particularly its gas business, analysts say

- Equinor rises as much as 4.4% after reporting 1Q profits that beat estimates. Analysts say the firm exceeded expectations across all key divisions as higher production offset lower oil and gas prices

- Hargreaves Lansdown shares rise as much as 4.5% after the investment platform’s net new business flows in its fiscal 3Q topped expectations, offsetting a small deterioration in asset retention

- Next shares rise as much as 2.7%, best performer in the Stoxx 600 Retail Index, after the UK clothing and furnishings seller’s 1Q sales beat estimates despite the cold weather

- Scout24 rises as much as 4.4% after digital marketplace operator reported better-than-expected revenue and Ebitda in 1Q thanks to strong growth in its core business as well as cost cuts

- Novo Nordisk falls as much as 6.5% after its blockbuster obesity drug Wegovy missed estimates due to supply woes. Analysts say their 1Q update, while beating expectations, otherwise held few surprises

- Airbus shares fell as much as 3.2% as analysts said the quarterly update indicates continued supply-chain challenges at the planemaker, which may weigh further on its delivery numbers for the year

- Zalando shares drop as much as 7.7% to the lowest since March after the online fast fashion retailer reported 1Q earnings, with Citigroup analysts noting caution around elevated inventory levels

- Leonardo falls as much as 7.5% and are the lead decliners on the FTSE MIB index after the Italian defense company reported what analysts called disappointing first-quarter results at the Ebita level

- Rheinmetall shares fall 3.8% after the German defense company’s first quarter operating profit misses estimates due to rising costs. Stifel says results were expected to be weak but “came in weaker”

- Virgin Money shares drop as much as 11%, the most since November 2020, as analysts flagged higher costs and impairments for the UK lender, which offset a small net interest income beat

- Casino shares plunge as much as 17% after the debt- laden French supermarket operator reported 1Q sales that missed the average analyst estimate

Earlier in the session, Asian stocks climbed as the dollar weakened on bets the Federal Reserve will pause interest-rate hikes, while Chinese shares ended flat as traders returned from the Golden Week holiday. The MSCI Asia Pacific Index advanced as much as 0.6%. The Fed hinted the latest hike could be the last one in its policy decision Wednesday, although pushed back against market expectations of rate cuts this year. Utilities and energy shares led broad-based gains. Onshore China stocks pared losses to close little changed as trading resumed following the Golden Week holidays. Concerns remain about the pace of China’s economic rebound despite strong holiday spending figures, as data showed factory activity struggled in April. Benchmarks in Hong Kong led gains in the region after falling in the previous session.

Expectations of lower US interest rates and a weaker dollar are boosting bets of outperformance for Asian equities as borrowing costs decline and US equities are weighed down by recession risks. The MSCI Asia Pacific Index is up about 3.6% this year, lagging the S&P 500. “While a lot of people are focused on the dollar smile theory, saying risk off is good for the dollar, when the epicenter is the US that’s not necessarily the case,” Steve Brice, group chief investment officer at Standard Chartered Wealth Management, told Bloomberg Television. “If you look at the growth differentials between the developed world and Asia, and also the dollar outlook, it paints a picture of Asian equity outperformance.”

In FX, the Bloomberg Dollar Index is flat having pared an earlier drop. The Swiss franc is the weakest among the G-10 currencies while the Norwegian krone sits atop the intraday rankings after the Norges Bank hiked 25bps and signaled more tightening ahead.

In rates, US yields have recouped some of Wednesday’s post-Fed losses with two-year borrowing costs initially rising 6bps to 3.86% but then sliding back to 3.81%. Treasuries are slightly cheaper across the curve along with European bond markets ahead of ECB rate decision at 8:15am New York time. US stock futures had opening gap lower as regional lenders continued to slump but have pared losses. US yields are higher by less than 2bp across the curve with spreads narrowly mixed after steepening sharply after Wednesday’s Fed rate increase and pause signal; 10-year yields around 3.34% outperforms bunds and gilts by ~1bp.

In commodities, crude futures advance with WTI rising 0.9% to trade near $69.20 after whipsawing at the open. Spot gold is down 0.2% around $2,035.

Bitcoin is essentially unchanged, pivoting the USD 29k mark in parameters that are even thinner than those seen at this time yesterday.

To the day ahead now, and the main highlight will be the ECB’s policy decision and President Lagarde’s press conference. We’ll also get the final services and composite PMIs from Europe for April, Euro Area PPI for March, and from the US there’s the weekly initial jobless claims, the March trade balance, and nonfarm productivity in Q1. Otherwise, earnings releases include Apple. And local elections will be taking place in the UK.

Market Wrap

- S&P 500 futures down 0.3% at 4,093.5

- STOXX Europe 600 down 0.4% to 460.71

- MXAP up 0.5% to 161.32

- MXAPJ up 0.6% to 514.21

- Nikkei up 0.1% to 29,157.95

- Topix down 0.1% to 2,075.53

- Hang Seng Index up 1.3% to 19,948.73

- Shanghai Composite up 0.8% to 3,350.46

- Sensex up 0.5% to 61,505.99

- Australia S&P/ASX 200 little changed at 7,193.11

- Kospi little changed at 2,500.94

- German 10Y yield little changed at 2.27%

- Euro down 0.2% to $1.1045

- Brent Futures up 1.2% to $73.23/bbl

- Gold spot down 0.2% to $2,033.95

- U.S. Dollar Index little changed at 101.37

Top Overnight News

- Chinese tourist spending during one of the country’s most important national holidays has exceeded pre-pandemic levels for the first time, authorities said, in a sign of economic momentum after China ended its coronavirus containment policies. FT

- China’s Caixin manufacturing PMI fell short of expectations in April, dipping into contraction territory at 49.5 (vs. the Street consensus of 50 and down from 50 in March). RTRS

- China’s fight against a weaponized dollar puts the yuan front and center. Its use in contracts for everything from oil to nickel is gathering speed and its share of global trade finance has tripled since the end of 2019. The US remains the world’s clear financial hegemon, but these moves help China play a bigger role in the international financial system. BBG

- The ECB is set to slow the pace of rate hikes, matching the Fed’s 25-bp move yesterday and taking the key rate to 3.25%, after its preferred inflation measure eased for the first time in 10 months. BBG

- Regional banks remain in focus after PACW announced post-close they are weighing strategic options (deposits rose since March). FHN -40% pre mkt after TD scrapped its planned $13.4 billion acquisition of the Memphis-based bank, citing uncertainty over a regulatory approval timeline. TD will pay $200 million in cash to First Horizon. FT

- Leaders on both sides of the aisle in Washington insist they won’t enact a short-term debt ceiling fix to allow more time for negotiations on a larger fiscal package. Politico

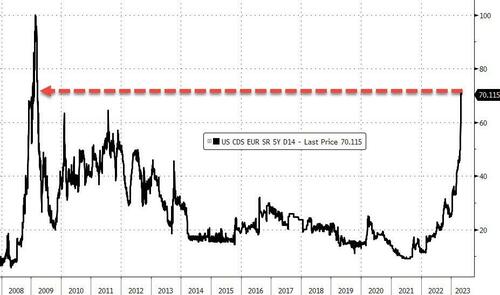

- Bill Isaac, a former regulator credited with stabilizing the US banking system during the 1980s crisis has hit out at the decision to sell First Republic to JPMorgan Chase as he warned of “more problems” to come for regional lenders. “We are kidding ourselves if we think there are only four problem banks in the country,” Isaac said. “We have not gotten that smart. It’s been so long since we had a lot of problems, that I can’t help but think that there are going to be more problems.” FT

- Apple’s sales may have dropped for a second quarter when it reports postmarket, though share buybacks may hold up. Analysts see revenue down 5% year on year, though Bloomberg Intelligence expects higher-end iPhone sales to help the gross margin as Mac sales underwhelm. In other earnings, Peloton is up before the bell, while Lyft and Carvana report later. BBG

- Biden’s Fed picks. He’s chosen current Governor Philip Jefferson for a promotion to vice chair and will nominate economist Adriana Kugler to an open board slot, people familiar said. The selections may be announced tomorrow. Jefferson voted to raise rates by 25 bps yesterday. Kugler is currently the World Bank’s executive director for the US. BBG

- Almost half of US adults say they’re worried about the safety of their deposits in banks and other financial institutions — levels of concern as high or higher than during the 2008 financial crisis….(BBG)

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed in the aftermath of the FOMC meeting where the Fed delivered a widely expected 25bps rate hike and paved the way for a pause, although Fed Chair Powell pushed back against cutting rates this year and alluded to banks tightening lending standards and slowing the pace of lending. ASX 200 was lacklustre amid weakness in its top-weighted financial sector after big four bank NAB’s H1 profit missed analysts’ estimates, although losses were cushioned by resilience in mining names and improved trade data. KOSPI was subdued as participants digested mixed earnings results, while Nikkei 225 remain closed. Hang Seng and Shanghai Comp. were firmer as mainland participants returned from the golden week break with Chinese markets shrugging off the surprise contraction in Caixin Manufacturing PMI and the PBoC’s significant liquidity drain, as well as the HKMA’s 25bps rate hike in lockstep with the Fed.

Top Asian News

- PBoC injected CNY 33bln via 7-day reverse repos with the rate at 2.00% for a CNY 529bln net drain.

- HKMA raised its base rate by 25bps to 5.50%, as expected.

- Chinese airlines will be allowed to expand their flights to the US, according to FT.

European equities, Euro Stoxx 50 -0.7%, trade mostly lower following the post-FOMC selling pressure in US indices. Equity sectors in Europe are mostly lower in what has been a busy morning for corporates. To the downside, Media and Auto names lag while Energy names are the clear outperformer in what has been a tough week for the sector amid declines in underlying crude prices, with upside also spurred by Shell’s +1.8% update. US equity futures have spent the morning slightly better than flat in an attempted recovery following the Fed rate decision and further jitters on the regional banking front, with PACW’s shares plunging over 50% in after hours trade. PacWest (PACW) has reportedly been approached by several potential partners and investors, according to Bloomberg.. -35% in the pre-market.

Top European News

- UK March Mortgage Approvals Unexpectedly Rise to 5-Month High

- UK April Composite PMI 54.9 vs Flash Reading 53.9

- Norway Hikes by Quarter-Point Again as Krone Woes Fester

- European Gas Prices Ease as IEA Sees Weaker Demand This Year

- Bud Light Brewer AB InBev Beats Forecasts on Strong Pricing

- Casino Plunges After 1Q Net Sales Misses Estimates

- European Stocks Retreat as Investors Await ECB After Fed Hike

FX

- DXY defends 101.000 in post-FOMC aftermath, as EUR/USD rejects 1.1100 in the run-up to the ECB amidst mixed EZ PMIs and a raft of hefty option expiries.

- Kiwi retains momentum above 0.6200 vs Buck and around 1.0700 vs Aussie as NZ building consents rebound firmly, AUD/USD underpinned within a 0.6699-41 band after export-led wider than forecast trade surplus.

- Pound perky near new YTD peak vs Buck just under 1.2600 with impetus from upgraded UK services and composite PMIs.

- PBoC set USD/CNY mid-point at 6.9054 vs exp. 6.9061 (prev. 6.9240)

- Norges Bank Key Policy Rate: 3.25% vs. Exp. 3.25% (Prev. 3.0%); policy rate will most likely be raised further in June. If NOK remains weaker than projected or pressures in the economy persist, a higher policy rate than envisaged earlier may be needed.

- Brazil Central Bank maintained the Selic rate at 13.75%, as expected. BCB said it will assess if the strategy of maintaining the Selic rate for a long period will be sufficient to ensure the convergence of inflation to the target and will persist in its strategy until consolidating disinflation and anchoring expectations around its targets.

Fixed Income

- Treasuries retain their bull-steepening trajectory post-Fed and ahead of several US data points, with T-notes holding above 116-00.

- Bunds probe 136.00 from 136.66 a peak as ECB looms and hawkish guidance is seen accompanying a 25 bp hike.

- Gilts teeter towards base of 101.37-93 range after upwardly revised UK services and composite PMIs.

Commodities

- WTI and Brent futures are firmer following the recent hefty losses in the complex. WTI June and Brent July slumped to lows of USD 63.64/bbl and USD 71.28/bbl respectively overnight as futures reopened amid banking sector woes.

- Spot gold shot higher by some USD 40/oz overnight, very briefly to a fresh all-time high on some charts, north of USD 2,080/oz. The yellow metal then immediately pulled back to levels under USD 2,050/oz and trades lower intraday in the European morning.

- Base metals are mostly firmer, underpinned by the return of the markets largest purchaser China from a five-day holiday.

- Shell (SHEL LN) CEO says they are getting close to Chinese levels of oil demand last seen in 2019; sees strong rebound in gas demand in China’s services sectors, but less in the industrial sectors.

Geopolitics

- An oil refinery in Krasnodar Krai, southern Russia caught fire after a drone attack, according to TASS.

- The governor of the Russian Voronezh region announces that the air defenses shot down a drone over the city, according to Sky News Arabia citing Tass.

- Russian Foreign Ministry says “Moscow will quickly deal with Kiev’s terrorist and subversive activities”, via Al Jazeera.

- Indian and Russia suspend negotiations to settle bilateral trade in Rupees, Russia reportedly not willing to amass INR as trade gap remains large, via Reuters citing sources.

- Russia’s Kremlin says we know decisions about such terrorist acts are taking in Washington and not Kyiv; Washington is definitely behind the attack, Kremlin is well aware of this; Russia has multiple response options, response will be thought-out.

US Event Calendar

- 07:30: April Challenger Job Cuts 175.9% YoY, prior 319.4%

- 08:30: April Initial Jobless Claims, est. 240,000, prior 230,000

- April Continuing Claims, est. 1.87m, prior 1.86m

- 08:30: March Trade Balance, est. -$63.1b, prior -$70.5b

- 08:30: 1Q Unit Labor Costs, est. 5.5%, prior 3.2%

- 08:30: 1Q Nonfarm Productivity, est. -2.0%, prior 1.7%

DB’s Jim Reid concludes the overnight wrap

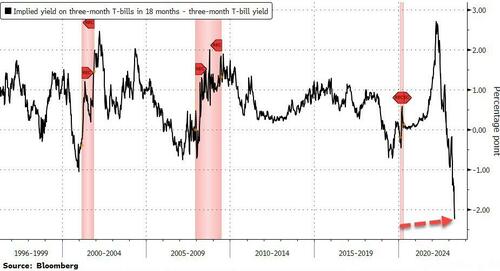

With the combination of a Fed that is now fully data dependent and further woes in the US regional banking sector before and after the closing bell, a decent survey question today might be, “when will the Fed next raise rates?”. I’d imagine the bid-offer would be somewhere between next month and only in 10 years’ time. Monetary policy clearly operates with a lag and the current US regional banking woes might be near the early stages of the fallout from this tighter policy rather than the end of it. That is a big worry. Before we recap the latest regional banking woes, let’s take a look at the Fed.

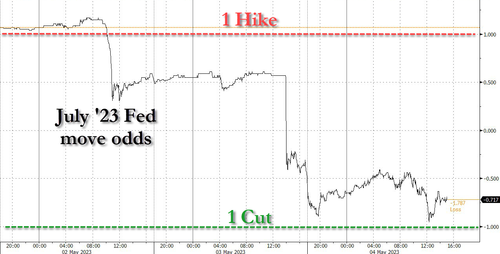

They delivered the expected 25bps hike last night with the upper bound of the target policy rate now 5.25%, the highest level it has been since 2007. The Fed also maintained their monthly pace of shrinking the balance sheet by $60bn for Treasuries and $35bn for MBS. It was a unanimous decision but the Fed dropped the phrase “some additional policy firming may be appropriate.” Fed Chair Powell called the removal of the phrase “meaningful”. The Fed pointed to inflation, labour-market strength, and credit conditions as factors they will be watching to decide future policy decisions. By doing away with forward guidance and transitioning to a more “data-dependent approach”, as Chair Powell said, the Fed opened the door to pausing rate hikes next meeting.

At the press conference, Chair Powell once again addressed the recent strains in the banking system following regulators seizing First Republic on Monday. He noted that the conditions in the banking sector “broadly improved” since early March and that the financial stability tools are not at odds with the monetary policy tools. Chair Powell noted that the banking system is “sound and resilient” but that the issues in the sector are further tightening lending conditions for small businesses and households. On credit conditions, Chair Powell – who received the Senior Loan Officer Survey data ahead of the meeting – said that “these tighter credit conditions are likely to weigh on economic activity, hiring and inflation.”

He also noted that the survey results are consistent with what policy makers have said and other data points have showed recently – namely that lending has grown in aggregate but the pace has slowed since 2H’22. When discussing a possible recession, Chair Powell acknowledged that a mild recession is possible as the Fed’s staff forecast shows, but that “the case of avoiding a recession is in (his) view more likely than that of having a recession.” On this he pointed to the excess demand in the labour market which seems to be cooling without a surge of unemployment seen in previous periods. Lastly on a question about the current market pricing of rate cuts in 2023, Chair Powell cautioned that the FOMC is not expecting inflation to come down that quickly and that rate cuts would not be appropriate, hence why it is not in their forecast. Fed futures are now pricing in a -11.5% chance of a rate cut in June and 82.7bps of cuts by year-end. However, before the after-market weakness in regional banks fed futures closed yesterday with a smaller chance of a cut next meeting (5%). See Matt Luzzetti’s review of the FOMC here. He continues to believe that the Fed is now done but that the first cut won’t come until Q1 2024.

Before the FOMC decision, US 2 year Treasury yields were down -2.9bps with 10 year yields down around -4.5bps. The S&P 500 was up +0.33%, with the USD index down -0.5%. As the statement came out, the dollar sold off initially whilst yields and equities rose. However there was a reversal during the last hour or so of US trading with equities selling off -1.4% from just after Powell started his presser to see the S&P 500 finish -0.70% lower on the day. US 10 year yields continued to fall after a brief rate selloff with yields finishing near their lows of the day down -8.8bps at 3.335%, as 2 year yields fell -15.6bps to 3.805. That’s the lowest the 2yr and 10yr yield has been in nearly a month and down an impressive -36bps and -27bps from their intra-day peaks on Monday just before the close.

Expanding on the equity moves, 20 of 24 industry sectors were lower on the day led by further weakness in cyclicals and banks. The KBW bank index was -1.89% lower as every member ended the day lower, as regionals were under pressure yet again. PacWest Bancorp, which was down -42% over the last 5 sessions and trading at its lowest share price since March 2009, announced after the US close that it has been approached by several partners and investors. The stock was down -52.49% in after-market trading. The news and weakness of the California-based lender caused fellow regional banks Western Alliance Bancorp to fall -22.42% after-hours and Zion Bank to decline -9.09%.

With the Fed now out of the way, attention will turn to the ECB today as they make their own policy decision. In terms of what to expect, both the consensus and DB view is that they’ll slow down their rate hikes to a 25bp pace, which would take the deposit rate up to 3.25%. However, as our European economists write in their preview (link here), it’s a close call between that and 50bps, since underlying inflation remains high and a rapid return to target is far from proven. So irrespective of how much they hike by, their view is that the underlying and conditional message will be that the tightening cycle isn’t over yet. Moreover, to stop financial conditions from overreacting to a slower hike, they expect the ECB to announce faster QT, with an increase in the roll-off of APP reinvestments from €15bn per month to €20bn per month from Q3.