MAY 11/2023 · by harveyorgan · in Uncategorized · Leave a comment·Editi

GOLD PRICE CLOSED: DOWN $15.15 TO $2015.15

SILVER PRICE CLOSED: DOWN $1.18 AT $24.23

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE $2014.50

Silver ACCESS CLOSE: 24.17

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

“America has been blessed never to have a native criminal class. Excepting Congress, of course.” … Mark Twain

GO GATA!

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $27,433 DOWN 265 Dollars

Bitcoin: afternoon price: $27,049 DOWN 649 dollars

Platinum price closing $1097.10 DOWN $15.85

Palladium price; $1558.40 DOWN $37.70

GO GATA!

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,718.21 UP 1.76 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1610.08 UP 2 01 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1845.57 DOWN 4.06 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: MAY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,030.500000000 USD

INTENT DATE: 05/10/2023 DELIVERY DATE: 05/12/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 53

132 C SG AMERICAS 234

363 H WELLS FARGO SEC 87

435 H SCOTIA CAPITAL 12

657 C MORGAN STANLEY 5

661 C JP MORGAN 34

709 C BARCLAYS 1

737 C ADVANTAGE 1 10

880 H CITIGROUP 1

905 C ADM 32

TOTAL: 235 235

MONTH TO DATE: 5,687

JPMorgan stopped 34/235 contracts

FOR MAY:

GOLD: NUMBER OF NOTICES FILED FOR MAY/2023. CONTRACT: 235 NOTICES FOR 235000 OZ or 0.7309 TONNES

total notices so far: 5687 contracts for 568,700 oz (17.6889 tonnes)

FOR MAY:

SILVER NOTICES: 10 NOTICE(S) FILED FOR 50,000 OZ/

total number of notices filed so far this month : 1972 for 9,860,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $15.15..THIS IS INTERESTING!!

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:///A DEPOSIT OF 4.04 TONNES INTO THE GLD//

INVENTORY RESTS AT 938.99 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN $1.18 AT THE SLV// ALSO INTERESTING

SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.480 MILLION OZ INTO THE SLV/: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 469.448 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 1351 CONTRACTS TO 146,796 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.23 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.23). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A MONSTROUS GAIN ON OUR TWO EXCHANGES OF 1644 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 4.250 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS( 293 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.105 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE. JUMP OF 25,000 OZ(QUEUE JUMP RAIDES THE AMOUNT OF SILVER STANDING)+0 EXCHANGE FOR RISK// TOTAL 4.25 MILLION OZ OF EXCHANGE FOR RISK FOR THE MONTH(RAISES THE AMOUNT OF SILVER STANDING):THUS TOTAL OF 17.305 MILLION OZ OF STANDING FOR DELIVERY V) HUGE SIZED COMEX OI GAIN/ SMALL SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –76 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTRACTS for 9 days, total 6565 contracts: OR 32.825 MILLION OZ . (663 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 32.825 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 32.825 MILLION OZ/INITIAL ( MUCH SMALLER THAN PREVIOUS MONTHS)

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1351 CONTRACTS DESPITE OUR $0.23 LOSS IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 293 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 13.105 MILLION OZ//FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 25,000 OZ (INCREASES THE AMOUNT OF SILVER STANDING) +// + 0.0 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //TOTAL EXCHANGE FOR RISK MONTH= 4.25 MILLION//NEW TOTALS 13.055 MILLION OZ + 4.25 MILLION = 17.305 MILLION OZ// .. WE HAVE A HUGE SIZED GAIN OF 1644 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 10 NOTICE(S) FILED TODAY FOR 50,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 4717 CONTRACTS TO 523,668 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: removed 1144 CONTRACTS

WE HAD A GOOD SIZED INCREASE IN COMEX OI ( 5861 CONTRACTS) DESPITE OUR $5.00 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR MAY. AT 3.5085 TONNES ON FIRST DAY NOTICE // PLUS 23,500 OZ QUEUE. JUMP :(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)////YET ALL OF..THIS HAPPENED WITH OUR $5.00 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING.WE HAD A STRONG SIZED GAIN OF 8580 OI CONTRACTS (26.68 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3863 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 524,812

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8580 CONTRACTS WITH 4717 CONTRACTS INCREASED AT THE COMEX AND 3863 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 8580 CONTRACTS OR 26.68 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3863 CONTRACTS) ACCOMPANYING THE GOOD SIZED GAIN IN COMEX OI (4717 //TOTAL GAIN IN THE TWO EXCHANGES 8580 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 3.5085 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 235,000 OZ // NEW STANDING: 18.081 TONNES // ///3) ZERO LONG LIQUIDATION//4) GOOD SIZED COMEX OPEN INTEREST GAIN/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 25,253 CONTRACTS OR 2,525,300 OZ OR 78.54 TONNES IN 9 TRADING DAY(S) AND THUS AVERAGING: 2805 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES 78.54 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 78.54/3550 x 100% TONNES 2.22% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES ( MUCH SMALLER THAN LAST MONTH)

MAY: 78.54 TONNES (HEADING FOR ANOTHER SMALLER MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS and sell the future TAS two months out. T they unload the front month so the price of gold/silver falls.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 1351 CONTRACTS OI TO 146,796 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 293 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 293 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 293 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1351 CONTRACTS AND ADD TO THE 293 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1644 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 8.220 MILLION OZ

OCCURRED DESPITE OUR $0.23 LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 9.60 PTS OR 0.29% //Hang Seng CLOSED DOWN 18.41 POINTS OR 0.09% /The Nikkei closed UP 4.54 OR 0.02% //Australia’s all ordinaries CLOSED DOWN 0.04 % /Chinese yuan (ONSHORE) closed DOWN 6.9377 /OFFSHORE CHINESE YUAN DOWN TO 6.9460 /Oil DOWN TO 72.48 dollars per barrel for WTI and BRENT AT 76.32 / Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED 4717 CONTRACTS UP TO 523,668 DESPITE OUR LOSS IN PRICE OF $5.00 ON WEDNESDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF MAY… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3863 EFP CONTRACTS WERE ISSUED: : JUNE 3863 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3863 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 8,580 CONTRACTS IN THAT 3863 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED GAIN OF 4717 COMEX CONTRACTS..AND THIS STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $5.00. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (18.075) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 18.075 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $5.00) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR STRONG SIZED GAIN OF 8580 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 26.58 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY. (3.5085 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 234,800 oz (0.7289 TONNES)//NEW STANDING 18.075 TONNES ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $5.00

WE HAD –REMOVED 1144 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 8580 CONTRACTS OR 858,000 OZ OR 26.68 TONNES.

Estimated gold comex today 323,972// strong//raid

final gold volumes/yesterday 323,278 strong//

//MAY 11/ MAY 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 12,088.776 OZ BRINKS 2 KILOBARS AND INT.DELAWARE 374 KILOBARS . |

| Deposit to the Dealer Inventory in oz | NIL |

| Deposits to the Customer Inventory, in oz | 54,656.700 oz JPMORGAN 1700 kilobars PHONY ENTRY |

| No of oz served (contracts) today | 235 notice(s) 23,500 OZ 0.7309 TONNES |

| No of oz to be served (notices) | 124 contracts 12400 oz 0.3856 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5687 notices 568,700 OZ 17.6889 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: NIL oz

customer withdrawals: 2

i) Out of BRINKS 64.302 (2 kilobars)

ii) Int. Delaware 12,024.474 oz (374 kilobars)

total withdrawals: 12,088.776 oz 376 kilobars

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 359 contracts having GAINED 117 contracts. We had 116 contracts filed

on WEDNESDAY, so we gained 233 contracts or an additional 23300 oz (0.7247 tonnes) will stand for gold in this non active delivery month of May.

June LOST 18,907 contracts DOWN to 294,982 contracts.

July added 95 contracts to stand at 1517 contracts.

AUGUST GAINED 22,433 contracts up to 175,115 contracts

We had 235 contracts filed for today representing 23500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 235 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 34 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2023. contract month,

we take the total number of notices filed so far for the month (5,687 x 100 oz ), to which we add the difference between the open interest for the front month of MAY 359 CONTRACTS) minus the number of notices served upon today 235 x 100 oz per contract equals 581,100 OZ OR 18.074 TONNES the number of TONNES standing in this NON- active month of May.

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (5,687 x 100 oz) 359 OI for the front month minus the number of notices served upon today (235)x 100 oz} which equals 581,100 oz standing OR 18.074 TONNES

TOTAL COMEX GOLD STANDING: 18.074 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,666,085.702 OZ 51.822 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,583,086.894 OZ

TOTAL REGISTERED GOLD: 12,399,365,073 (385,68 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,183,421.821 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,733,580 OZ (REG GOLD- PLEDGED GOLD) 333.86 tonnes//

END

SILVER/COMEX

MAY 11//2023// THE MAY 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,222,295.550 oz Delaware JPMorgan Loomis . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 603,217.700 oz Loomis |

| No of oz served today (contracts) | 10 CONTRACT(S) (50,000 OZ) |

| No of oz to be served (notices) | 639 contracts (3,195,000 oz) |

| Total monthly oz silver served (contracts) | 1972 Contracts (9,860,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i)Into Loomis: 603,217.700 oz

Total deposits: 603,217.700 oz

JPMorgan has a total silver weight: 138.988 million oz/270.403 million =51.40% of comex .//dropping fast

Comex withdrawals 3

i) Out of Delaware 3889.700 oz

ii) Out of jPMorgan: 618,280.280 oz

iii) Out of Loomis: 600,125.570 oz

Total withdrawals; 1,222,295.550 oz

adjustments: 7 all dealer to customer

Brinks 264,322.740 oz

CNT: 312,756.310 oz

Delaware 69,527.768 oz

HSBC 463,164.360 oz

Loomis 346,740.090 oz

Manfra 209,845.106 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 29.958 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 270.403 million oz

we have now seen the movement of the registered silver comex into the 29 million column:

CALCULATION OF SILVER OZ STANDING FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2023 OI: 649 CONTRACTS HAVING LOST 6 CONTRACT(S). WE HAD 11 CONTRACTS FILED

ON WEDNESDAY, SO WE GAINED 5 CONTRACTS OR AN ADDITIONAL 25,000 OZ WILL STAND FOR DELIVERY ON THIS SIDE OF THE POND.

JUNE HAD A 16 CONTRACT GAIN TO 997

JULY HAD A 1207 CONTRACT LOSS TO 124,182 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 10 for 50,000 oz

Comex volumes// est. volume today 104,555 huge/raid

Comex volume: confirmed yesterday: 81,704 strong

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 1972 x 5,000 oz = 9,860,000 oz

to which we add the difference between the open interest for the front month of MAY(649) and the number of notices served upon today 10 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2023 contract month: 1972 (notices served so far) x 5000 oz + OI for the front month of May (649) – number of notices served upon today (10 )x 500 oz of silver standing for the MAY contract month equates to 13.055 million oz + THE CRIMINAL 0 MILLION OZ EXCHANGE FOR RISK TODAY//NEW TOTAL EXCHANGE FOR RISK: 4.250//NEW TOTAL 17.305 MILLION OZ//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 434.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 434.95 TONNES

MAY 9/WITH GOLD UP $9.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTER DEPOSIT OF 5.88 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 437.64 TONNES

MAY 8/WITH GOLD UP $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 431.77 TONNES

MAY 5/WITH GOLD DOWN $30.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AS DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

MAY 4/WITH GOLD UP $19.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.30 TONNES

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

APRIL 10/WITH GOLD DOWN $21.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91 TONNES

APRIL 6//WITH GOLD DOWN $9.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91

APRIL 5//WITH GOLD UP 0 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04

APRIL 4/WITH GOLD UP $36.30 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

APRIL 3/WITH GOLD UP $14.20 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.02 TONNES

MARCH 31/WITH GOLD DOWN $10.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD////INVENTORY RESTS AT 928.02 TONNES

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

GLD INVENTORY: 934.95 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

MAY 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A TINY DEPOSIT OF .08 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 465.682 MILLION OZ//

MAY 8/WITH SILVER DOWN 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.602 MILLION OZ//

MAY 5/WITH SILVER DOWN 31 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 466.876 MILLION OZ//

MAY 4/WITH SILVER UP 53 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF .174 MILLION OZ INTO SLV.//INVENTORY RESTS AT 467.174 MILLION OZ//

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 10/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 6/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 4.643 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 468.585 MILLION OZ//

APRIL 5/WITH SILVER DOWN 4 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.942 MILLION OZ

APRIL 4/WITH GOLD UP $1.11 TODAY CRIMINAL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.47 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 463,942 MILLION OZ

APRIL 1/WITH SILVER DOWN 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.412

MARCH 31/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD/: A MASSIVE 4.779 MILLION OZ DEPOSITED INTO THE SLV///INVENTORY RESTS AT465.412 MILLION OZ

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

CLOSING INVENTORY 466.968 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

3,Chris Powell of GATA provides to us very important physical commentaries

Important: Craig Hemke outlines how the bullion banks re controlling the gold price using the trade at settlement mechanism

(zerohedge)

Craig Hemke at Sprott Money: Bullion bank trade-at-settlement abuse continues

Submitted by admin on Thu, 2023-05-11 04:51Section: Daily Dispatches

4:45p SGT Thursday, May 11, 2023

Dear Friend of GATA and Gold:

Craig Hemke of the TF Metals Report, writing at Sprott Money, today updates his readers about the continuing use by bullion banks of the “trade at settlement” mechanism for controlling the gold price.

Hemke’s analysis is headlined “Bullion Bank Trade-at-Settlement Abuse Continues” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/blog/Bullion-Bank-TAS-Abuse-Continues-May-10-2023

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Chris Powell: Chris Powell’s speech to the Mining Investment Asia Conference, Singapore

a must view….

Chris Powell: How might gold price suppression policy end?

Submitted by admin on Thu, 2023-05-11 05:32Section: Daily Dispatches

The slides accompanying this presentation can be viewed here:

* * *

SLIDE 1: TITLE

Remarks by Chris Powell, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

Mining Investment Asia Conference

Marriott Tang Plaza Hotel, Singapore

Thursday, May 11, 2023

For many years on behalf of the Gold Anti-Trust Action Committee I have spoken at this conference and others like it to detail the extensive official records and other evidence of manipulation of the gold market by central banks and particularly by the U.S. government. This manipulation has been undertaken to defend the U.S. dollar as the world reserve currency and to diminish all other currencies, gold especially.

Those records and the other evidence are compiled at GATA’s internet site. Because of their sensitivity they have been largely ignored but they have seldom been disputed. I would be delighted with any challenge to them, for at least a challenge would acknowledge them.

But today I want to concentrate on documents that show that central bank policy toward gold is changing profoundly — moving away from price suppression and toward renewed acceptance of gold’s superiority as money and its renewed value to central banks that possess it.

I’m talking about the monthly statements of account of the Bank for International Settlements, the central bank of the world’s central banks.

The BIS is crucial in analyzing the gold price because the bank acknowledges that it is a primary gold broker for its members. More than that, when the BIS doesn’t think that anyone outside the ranks of central banks is listening, the BIS acknowledges that it is the major mechanism by which central banks can control the gold price to protect their currencies against competition.

SLIDE 2: BIS PowerPoint presentation

For example, the BIS has actually advertised to prospective central bank members that its services to its members include secret interventions in the gold market. Here is a slide from a PowerPoint presentation the bank gave to prospective central bank members at BIS headquarters in Basel, Switzerland, in June 2008:

http://www.gata.org/node/11012

Indeed, according to its annual reports, the BIS functions largely as a gold banking and gold market intervention service for its member central banks:

http://www.gata.org/node/12717

SLIDE 3: BIS statement of account

GATA’s consultant about the BIS, Robert Lambourne, examines the bank’s monthly statement of accounts, since, if you look very closely at the statement, as Lambourne does, you’ll see that it includes entries for “gold and gold loans” and “gold deposits” and that these entries change each month. On the screen is a sample revealing page, taken from the BIS’ statement of account for January 2020:

In January 2022 Lambourne calculated that the BIS’ gold derivative positions remained near their longtime highs, standing at 501 tonnes.

SLIDE 4: BIS swaps chart

But after last January the BIS’ gold derivatives positions began falling sharply, going to zero in December last year as the “Basel 3” gold banking regulations promulgated by the BIS were taking effect. Those regulations made it almost impossible for the biggest banks trading in the gold market to trade gold without actually possessing it — sharply curtailing the sale of “paper gold,” the imaginary gold used primarily for price suppression.

As you can see from the chart on the screen, since last December the BIS’ gold derivatives position has rebounded to 136 tonnes, but that is just a fraction of what it was a year ago. (The data for March and April is not yet available.)

The sharp decline in BIS gold derivatives, as calculated by Lambourne in the chart, shows that a huge change in central bank policy toward gold is underway. That change likely involves an end to price suppression, or at least an end to the cooperation with price suppression by most central banks, and implies even an official upward revaluation of gold, since in recent years central banks on the whole have turned from gold sellers to very big gold buyers.

If you doubt this, please ask the BIS: What exactly has the BIS been doing in the gold market, for what objectives, and for whom? GATA put that question to the BIS in 2017 and the BIS promptly replied that it doesn’t answer such questions:

http://www.gata.org/node/17793

So you may fairly assume that any honest answers here would incriminate the BIS’ members and owners — central banks — in market-rigging policy that the BIS long has assisted and for which it has provided camouflage.

By rigging the currency markets, this policy has expropriated many countries largely for the benefit of the United States. It is a policy by which one country has controlled the valuation of all capital, labor, goods, and services in the world. It is a totalitarian and parasitic system.

How might this system end?

First it’s a question of world politics at the highest levels: Who wants to pull the plug on the dollar and begin a new system, and with what? This question is being addressed right now in Europe, Russia, China, Africa, and South America — almost everywhere in the world. Some countries are reducing or discontinuing their use of the U.S. dollar in trade. Some are considering starting new regional currencies.

The parasitic dollar system may end simply upon exhaustion of the relatively small gold supply that is needed to keep the futures and spot gold markets operating under U.S. control. Gold supply was exhausted in March 1968 when huge offtake forced the London Gold Pool to close. Lately there have been signs that gold supplies are critically tight in London and New York, the markets where price suppression is concentrated.

How much more gold from their reserves are the central banks suppressing the gold price prepared to lose? We don’t know. That is the most sensitive information. If you knew when the metal used for price suppression would run out, you could get rich.

The system may end when even one country decides to exchange substantial amounts of U.S. dollars and Treasury bonds for more gold — real metal — than is readily available. It may end when any country with a substantial foreign exchange surplus decides that it is hedged enough with gold that it can afford the severe devaluation of its dollar-denominated reserves.

Or the system may end as part of a plan by major central banks to avert the catastrophic debt-induced deflation that now threatens the world — a plan to inflate the debt away, essentially to default on it, by devaluing the major currencies against gold. This has happened before.

SLIDE 5: Peter Millar study

For example, a study in 2006 by the Scottish economist Peter Millar concluded that to avert a catastrophic debt deflation, central banks would need to raise the gold price by a factor of seven to 20 times in order to reliquefy themselves — to dramatically increase the value of their gold reserves as their currencies devalue along with the bonded debts of government and society generally:

SLIDE 6: Brodsky and Quaintance study / QB Asset Management

In May 2012 the U.S. economists Paul Brodsky and Lee Quaintance published a report speculating that central banks probably were already redistributing gold reserves among themselves in preparation for just such a currency devaluation and an upward revaluation of gold, even in preparation for gold’s return as formal backing for currencies.

http://www.gata.org/node/11373

This speculation is plausible, since, as I have noted, in recent years central banks have switched from being net gold sellers to net gold buyers. Just recently the Monetary Authority of Singapore has dramatically but quietly increased its gold reserves:

https://www.gata.org/node/22464

In February gold researcher Jan Nieuwenhuijs strengthened the speculation about gold revaluation, publishing evidence that European central banks have been working with the People’s Bank of China to match their gold reserves with their nations’ gross domestic product in preparation for some sort of new gold standard or gold price targeting system.

https://www.gata.org/node/22450

But the end of gold market rigging by central banks may also be a matter of education and publicity — a matter of whether governments that are not part of gold price suppression policy, along with investors around the world, will ever realize that as much as 90% of the world’s investment gold, supposedly being held in trust at investment banks, is, to put it politely, imaginary or at least oversubscribed.

If there is ever such a widespread realization and if delivery of the imaginary gold is ever demanded, the price of the metal may rise to multiples of its current price even as the holders of “paper gold” discover they have nothing.

*

While the prospect of much higher gold prices of course excites gold producers and investors, it raises its own questions.

Will governments let gold investors keep extraordinary gains, or will governments impose windfall profits taxes on them or even try to confiscate gold? Decades ago confiscation was undertaken in the United States and other countries.

In 2005 I had some interesting correspondence with the U.S. Treasury Department about gold confiscation. The chief counsel for the department’s Office of Foreign Assets Control told me that under the Trading With the Enemy Act of 1917 and the International Emergency Economic Powers Act of 1977, upon a proclamation of emergency by the president of the United States, the Treasury Department would have the power to seize or freeze any gold- or silver-related asset – and, for that matter, any other damned thing the Treasury Department wanted to seize:

https://www.gata.org/node/5606

If the gold price soars, will governments let mining companies keep taking metal out of the ground at current royalty rates? Will royalty rates be sharply raised? Will governments even let private companies keep mining gold at all?

If the gold market is rigged, why should anyone own gold?

You might want to own gold, first, if you think that the fraud being perpetrated by central banks — the longstanding naked short position in the monetary metal, a naked short position maintained in the London gold market via those BIS gold swaps and derivatives — will be exposed and collapse from its dishonesty, from exhaustion of the gold reserves of the most gold-suppressive governments, or because of defections from central bank ranks.

Second, you might want to own gold if you think that, as the economists Peter Millar, Paul Brodsky, and Lee Quaintance have speculated, central banks will change policy on gold and revalue it upward to devalue their currencies and government debts and to reliquefy themselves through a higher value for their gold reserves.

Third, you might want to own gold if you think that central banks, the biggest owners of gold, know something positive about it, as indicated by their recent purchases.

SLIDE 7: Wuermeling presentation

In March gold’s value as money received a powerful if strange endorsement from a member of the Executive Board of Germany’s central bank, the Bundesbank. The board member, Joachim Wuermeling, spoke at a press conference in Frankfurt presenting the Bundesbank’s annual report for 2022.

“Viewed over the long term,” Wuermeling said, “there is still a sustained marked increase in the revaluation reserve for gold. Compared with its starting balance at the launch of [European] monetary union [in 1999] — €21 billion — this revaluation reserve, with its current balance of €176.1 billion, is eight times as large as it was at the start of 1999.”

Here was a European central banker noting that gold has steadily outperformed the currency for which he shares responsibility — a central banker noting that gold is an outstanding hedge against inflation and currency devaluation. Central bankers are seldom so candid about the ancient form of money that still competes with their own:

https://www.gata.org/node/22457

But don’t underestimate the chance that, whatever you do to protect yourself financially, government will find a way to cheat you out of your foresight.

SLIDE 8: For more information

If you would like more information about GATA’s work, assistance locating any of the documents I’ve mentioned, or other information about gold-related issues, please e-mail me at CPowell@GATA.org. Please consider going to our internet site — http://gata.org/ — and subscribing to our free daily e-mail newsletter. We aim to keep our friends updated about developments in the monetary metals and the possibility that their markets may become free and transparent, as they should be.

Thanks for your kind attention.

* * *

END

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

END

5.IMPORTANT COMMENTARIES ON COMMODITIES: URANIUM

Seems that many countries will be going back to cheap and cleaner nuclear power. Uranium will be the big winner

(zerohedge)

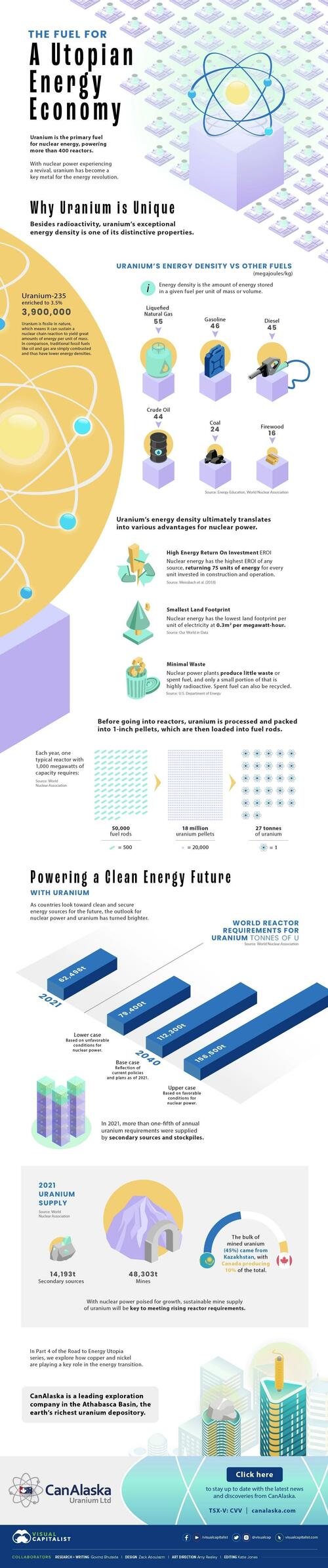

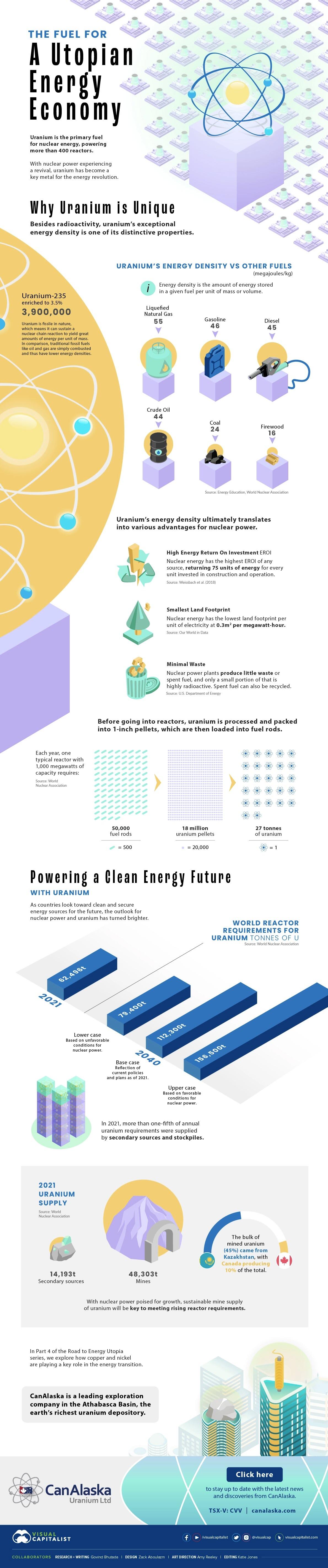

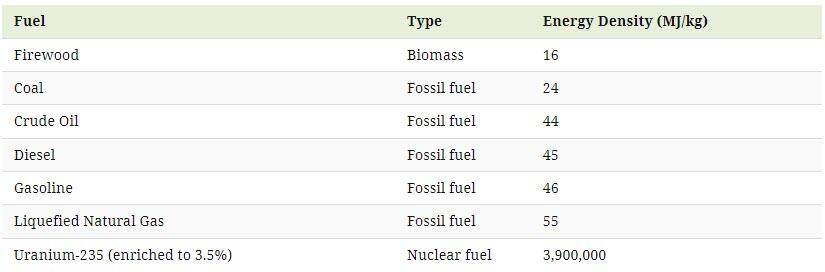

Is Uranium The Fuel For A Utopian Energy Economy?

WEDNESDAY, MAY 10, 2023 – 08:40 PM

Uranium is the primary fuel for nuclear energy, powering more than 400 reactors that make up 10% of the world’s annual electricity generation.

With countries turning back to nuclear power as a clean energy resource, uranium has become a strategically important metal for the future.

This infographic by Visual Capitalist’s Govind Bhutada and Zack Aboulazm, sponsored by CanAlaska Uranium. explores how uranium’s unique properties allow nuclear power to be clean and efficient, and highlights the outlook for its future.

Why Uranium is Unique

Nuclear power ultimately stems from the radioactivity of uranium atoms, which yield great amounts of energy when split by the process of fission.

Besides the radioactive nature of uranium, its energy density—the amount of energy it contains per unit of mass—is one of its exceptional properties, making it significantly more powerful than other energy fuels.

The table below compares the energy density of uranium to other fuels, expressed in megajoules of energy contained per kilogram of fuel:

Enriched uranium-235, the fuel used by commercial nuclear reactors, contains 3.9 million megajoules of energy per kilogram of weight, which is magnitudes larger than the energy density of traditional fossil fuels.

For this reason, a relatively small quantity of nuclear fuel can produce significant amounts of energy through fission, translating into various advantages for nuclear power:

High Energy Return on Investment (EROI)

Nuclear power has the highest EROI of any energy source, returning 75 units of energy for every unit of energy spent in construction and operation.

Low Land Footprint

Nuclear power plants have the smallest land footprint per unit of electricity at 0.3m2 per megawatt-hour.

Minimal Waste

Nuclear reactors produce little waste or spent fuel, and only a small portion of that is highly radioactive. Spent fuel can also be recycled.

Powering a Clean Energy Future with Uranium

The outlook for uranium has turned brighter with countries again embracing nuclear energy.

In 2021, global uranium requirements from reactors totaled 62,496 tonnes. By 2040, that figure could rise from 79,400 tonnes in the lower case to 156,500 tonnes in the upper case according to the World Nuclear Association, depending on how the conditions and policies for nuclear power shape up.

In 2021, mines provided about 77% of the uranium required for reactors, with 23% coming from secondary sources like stockpiles held by utilities and governments. Although maintaining these stockpiles is important for energy security, a sustainable mine supply of uranium will always be key to meeting rising reactor requirements.

end

5 B GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

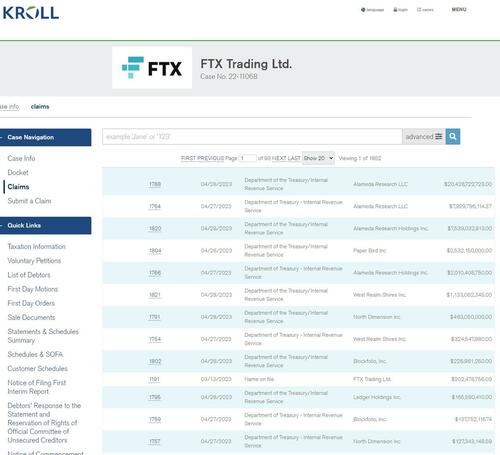

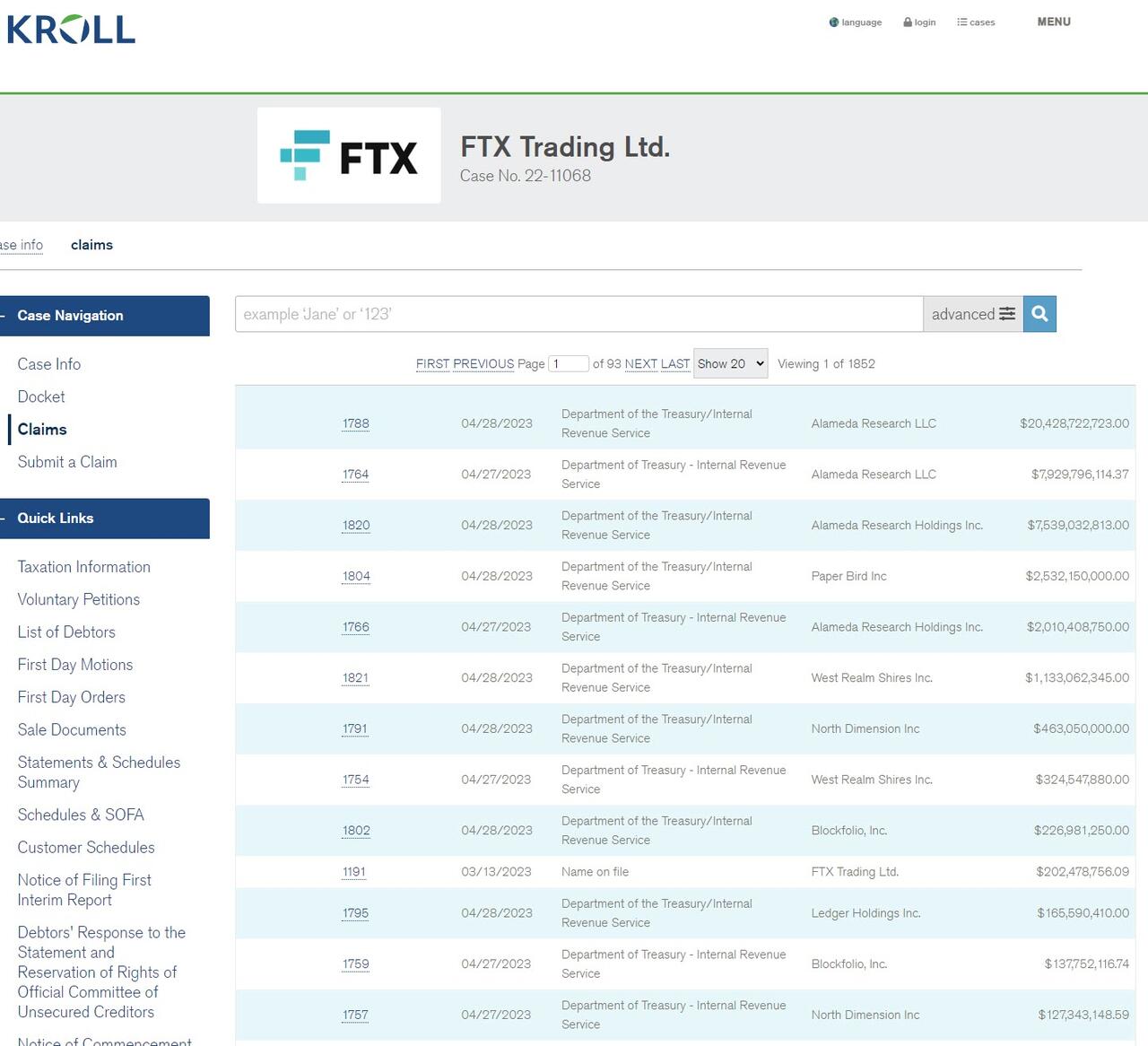

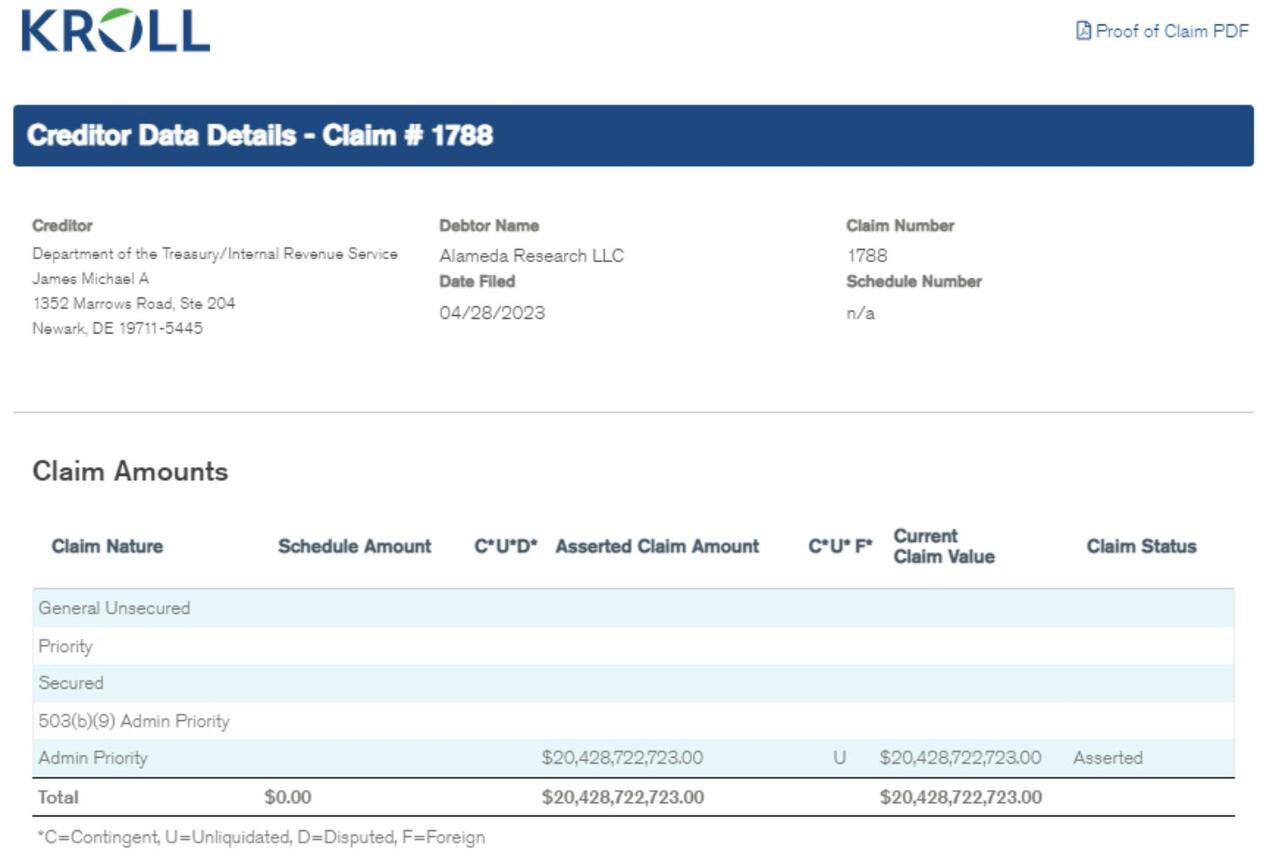

IRS Files $44 Billion Claims Against Bankrupt FTX; Court Filing Shows

THURSDAY, MAY 11, 2023 – 09:45 AM

The United States Department of Treasury and Internal Revenue Service (IRS) have filed 45 claims worth $44 billion against bankrupt cryptocurrency exchange FTX and its subsidiaries.

As CoinTelegraph’s Zhiyuan Sun reports, in what appears to be a tax bill for FTX’s sister company Alameda Research LLC that circulated online on May 10, the IRS assessed the firm $20.4 billion due in partnership taxes and payroll taxes.

The assessment appears to match the IRS claim found on the website of Kroll’s Restructuring Administration practice, FTX’s claims agent.

A further $7.9 billion claim is made by the IRS against Alameda Research LLC, while two claims — $7.5 billion and $2.0 billion — are made against Alameda Research Holdings.

The IRS filed the claims under “administrative priority,” enabling its claims to supersede that of unsecured creditors during bankruptcy proceedings.

While Alameda Research was headquartered in Hong Kong, its founders and key personnel, including Sam Bankman-Fried and Caroline Ellison, are U.S. nationals. Unlike most other countries, the U.S. uses a taxation-by-citizenship regime, meaning that U.S. nationals are liable for taxes on their worldwide income irrespective of their place of residence or how much time they spend in the U.S. each year. For partnership entities, taxes are not paid at the partnership level but are passed through their partners and taxed at the individual level.

In one single claim, the IRS assessed a balance of $20.4 billion against Alameda Research. Source: Kroll

In April, Coin telegraph reported that FTX had recovered $7.3 billion in assets and would consider rebooting the exchange next year. The announcement was made before the IRS’ claims, and at the time, FTX’s liabilities still outweighed its assets by an estimated $8.7 billion.

END

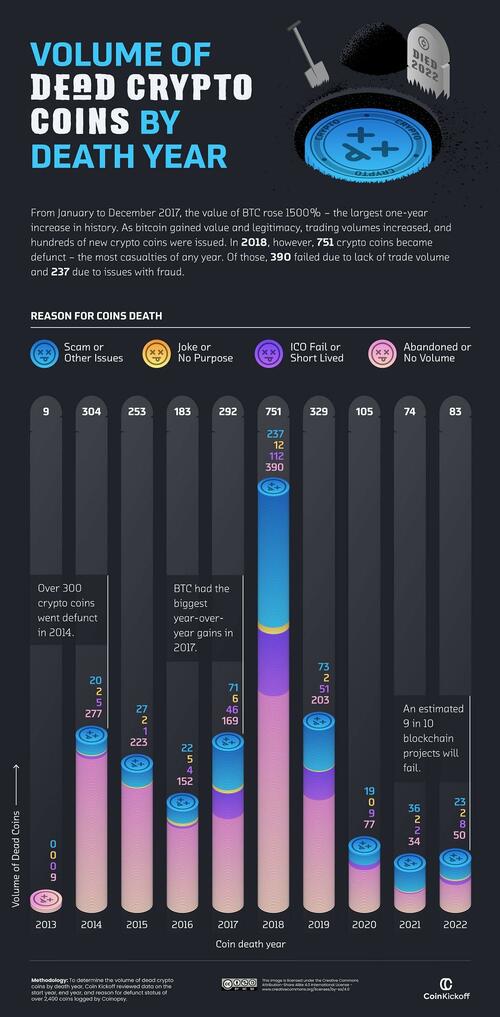

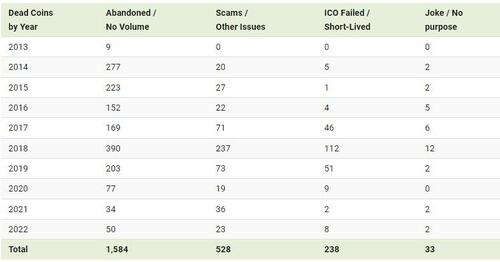

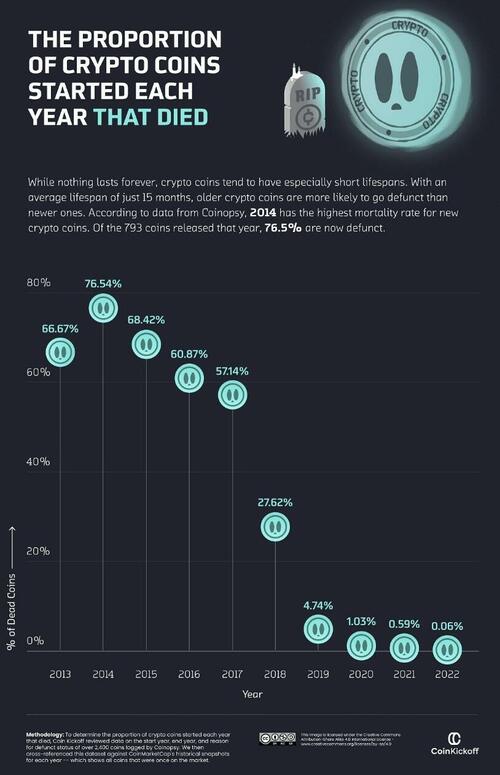

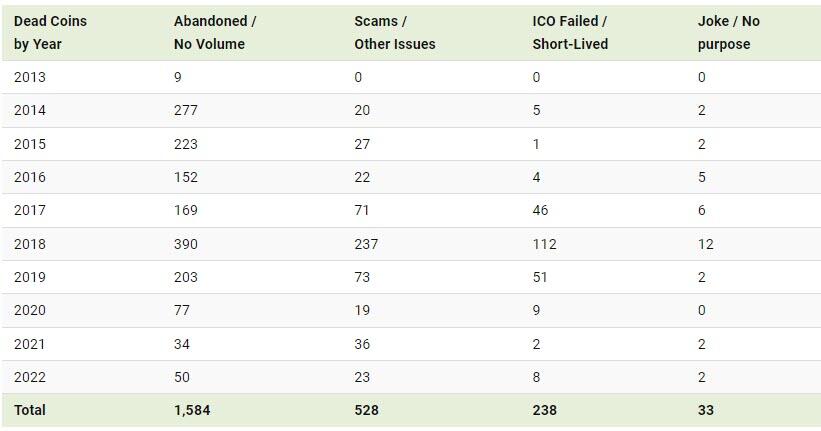

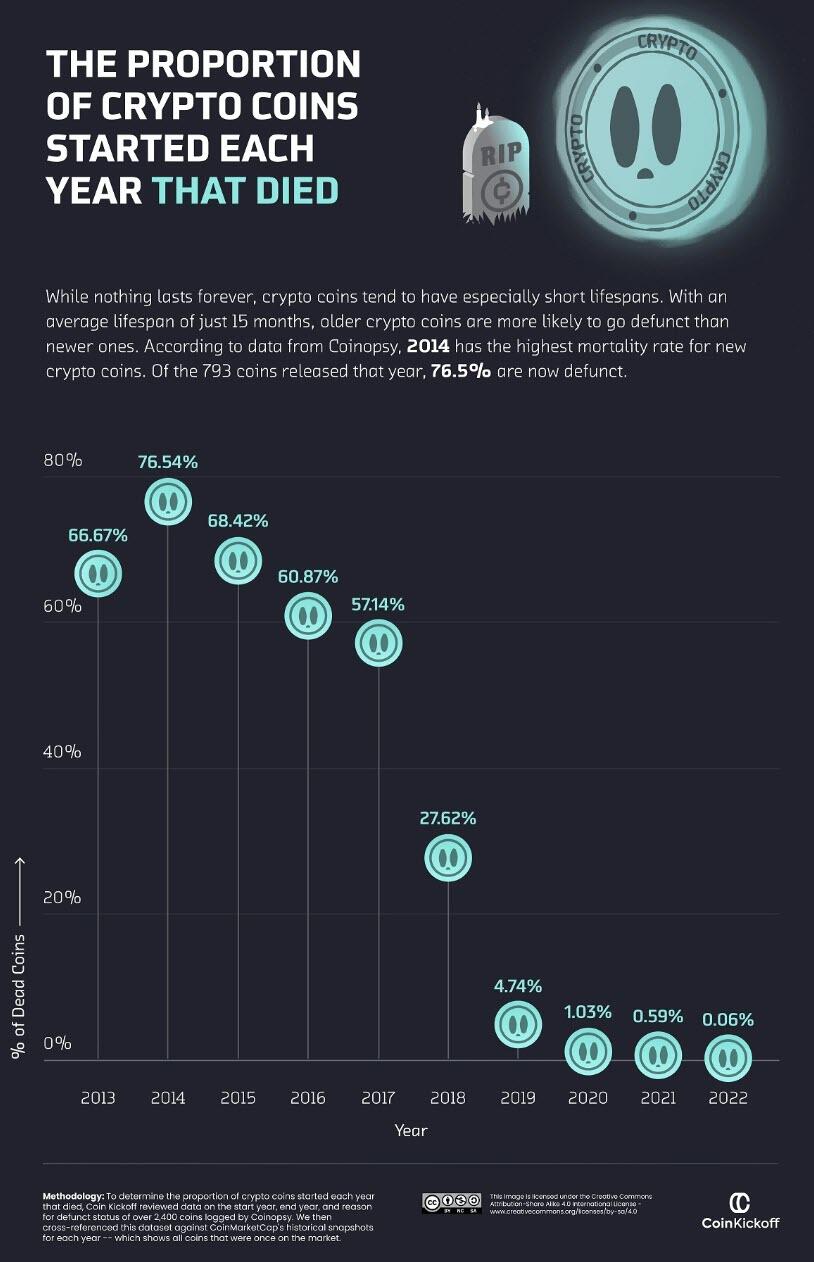

Visualizing The Number Of Failed Crypto Coins, By Year (2013-2022)

WEDNESDAY, MAY 10, 2023 – 10:00 PM

Ever since the first major crypto boom in 2011, tens of thousands of cryptocurrency coins have been released to market.

And while some cryptocurrencies performed well, others have ceased to trade or have ended up as failed or abandoned projects.

As Visual Capitalist’s Aran Ali and Pallavi Rao detail below, these graphics from CoinKickoff break down the number of failed crypto coins by the year they died, and the year they started. The data covers a decade of coin busts from 2013 through 2022.

Methodology

What is the marker of a “dead” crypto coin?

This analysis reviewed data from failed crypto coins listed on Coinopsy and cross-referenced against CoinMarketCap to verify previous market activity. The reason for each coin death was also tabulated, including:

- Failed Initial Coin Offerings (ICOs)

- Abandonment with less than $1,000 in trade volume over a three-month period

- Scams or coins that were meant as a joke

Dead Crypto Coins from 2013 to 2022

While many familiar crypto coins—Litecoin, Dogecoin, and Ethereum—are still on the market today, there were at least 2,383 crypto coins that bit the dust between 2013 and 2022.

Here’s a breakdown of how many crypto coins died each year by reason:

Abandoned coins with flatlining trading volume accounted for 1,584 or 66.5% of analyzed crypto failures over the last decade. Comparatively, 22% ended up being scam coins, and 10% failed to launch after an ICO.

As for individual years, 2018 saw the largest total of annual casualties in the crypto market, with 751 dead crypto coins. More than half of them were abandoned by investors, but 237 coins were revealed as scams or embroiled in other controversies, such as BitConnect which turned out to be a Ponzi scheme.

Why was 2018 such a big year for crypto failures?

This is largely because the year prior saw Bitcoin prices climb above $1,000 for the first time with an eventual peak near $19,000. As a result, speculation ran hot, new crypto issuances boomed, and many investors and firms got bullish on the market for the first time.

How Many Newly Launched Coins Died?

Of the hundreds of coins that launched in 2017, more than half were considered defunct by the end of 2022.

Indeed, a lot of earlier-launched coins have since died. The majority of coins launched between 2013 and 2017 have already become “dead coins” by the end of 2022.

Part of this is because the cryptocurrency field itself was still being figured out. Many coins were launched in a time of experimentation and innovation, but also of volatility and uncertainty.

However, the trend began to shift in 2018. Only 27.62% of coins launched in that year have bit the dust so far, and the failure rates in 2019 and 2020 fell further to only 4.74% and 1.03% of launched coins, respectively.

This suggests that the crypto industry has become more mature and stable, with newer projects establishing themselves more securely and investors becoming wiser to potential scams.

How will this trend evolve into 2023 and beyond?

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS// THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.9377

OFFSHORE YUAN: 6.9460

SHANGHAI CLOSED DOWN 9.60 PTS OR 0.29%

HANG SENG CLOSED DOWN 18.41 PTS OR 0.09%

2. Nikkei closed UP 4.54 PTS OR 0.02%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 101.59 EURO FALLS TO 1.0934 DOWN 49 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.387 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 134.21 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.245***/Italian 10 Yr bond yield FALLS to 4.165*** /SPAIN 10 YR BOND YIELD RISES TO 3.333…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.023

3j Gold at $2037.40 silver at: 25.03 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 59 /100 roubles/dollar; ROUBLE AT 76.65//

3m oil into the 72 dollar handle for WTI and 76 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 134/21 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .387% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8928 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9763 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

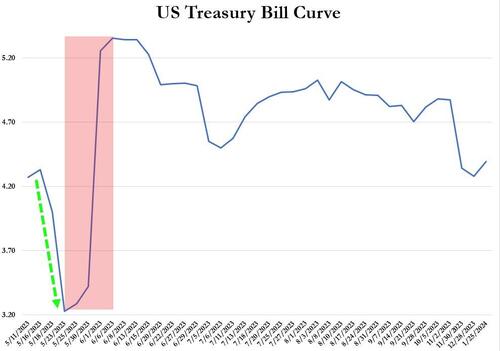

USA 10 YR BOND YIELD: 3.408 DOWN 3 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.776 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.8848 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.56…

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 3.8300 UP 3 BASIS PTS

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Slide As Bank Selloff Returns With Pacwest Tumble

THURSDAY, MAY 11, 2023 – 08:21 AM

US equity futures pared an earlier advance and dropped to session lows driven by a fresh plunge in Pacwest shares after the bank warned the bank run was back (or rather, had never gone away as we warned last weekend) as a renewed sharp deposit outflow from the bank spooked investors, even as European stocks rose as more investors said the Fed is likely to pause interest-rate hikes on the back of cooling inflation data. Contracts on the S&P 500 dropped to session lows, down -0.1% after rising 0.2% earlier; the Nasdaq was flat.

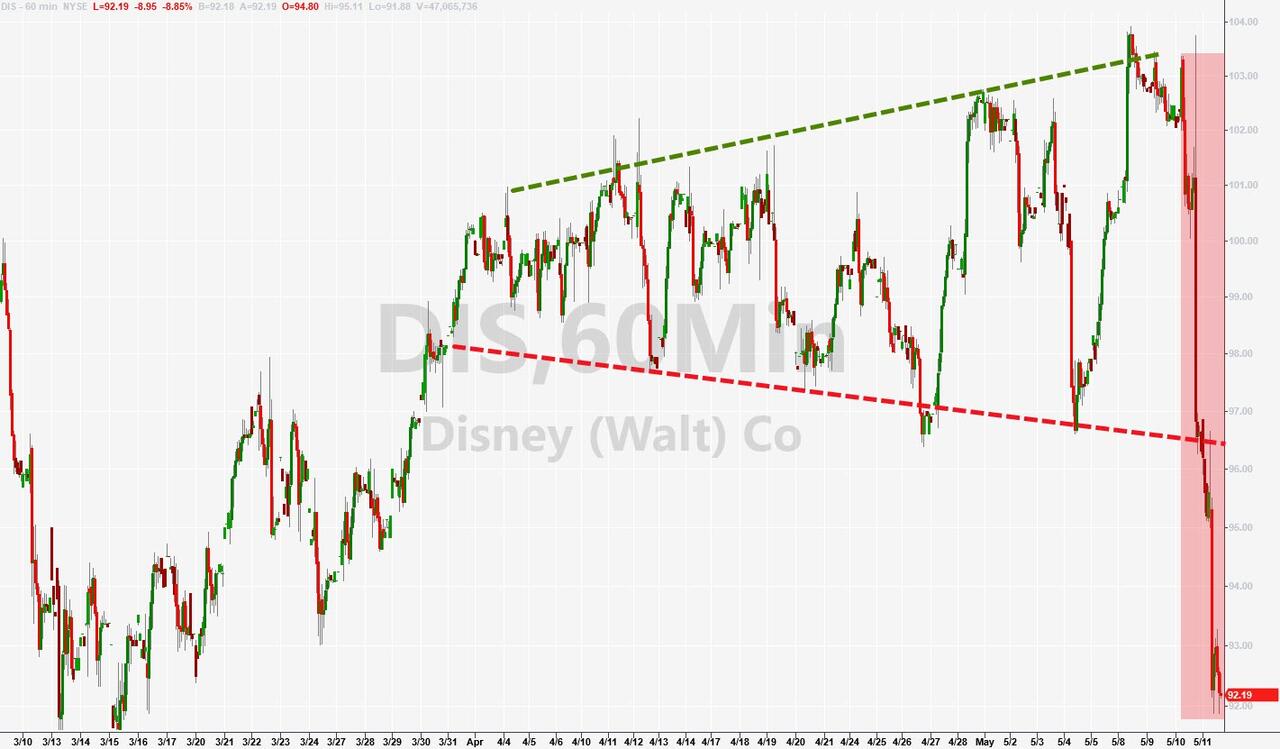

In US premarket trading,PacWest Bancorp plunged as much as 26% after it said deposits declined about 9.5% during the week ended May 5, with a majority of that decline occurring on May 4 and May 5 after the news reports on the afternoon of May 3. Walt Disney dropped after revealing a surprise drop in subscribers and predicting a wider loss for its streaming service this quarter. Robinhood rose following better-than-expected results from the trading platform. Beyond Meat fell after analysts said its earnings outlook is clouded by uncertainty around demand ahead of the key summer months and the company announced a $200MM ATM stock offering. Here are the other notable premarket movers:

- Google unveiled its latest artificial intelligence tools and launched new hardware at its annual developer conference. Analysts were optimistic about the speed with which Google was incorporating AI into its products and services. Shares of parent Alphabet are set to extend gains, rising as much as 1.8% in premarket trading on Thursday.

- Alcoa rises 1% in US premarket trading after Credit Suisse upgrades the stock to outperform from neutral, and makes it a top pick, citing expectations of recovering aluminum prices.

- Sonos shares drop 24% in US premarket trading after the wireless speaker maker cut its revenue guidance. Analysts said macro weakness is weighing more broadly, though also question whether this is particularly acute for the audio segment.

- Purple Innovation jumps 18% in US premarket trading after the mattress, bedding and cushioning firm reported net revenue for the first quarter that beat the average analyst estimate, amid anticipation over the launch of new products. .

- Roblox shares rise 3% in US premarket trading after the video-game firm’s comments on operating leverage helped buoy sentiment and offset an earnings miss in the first-quarter, analysts said. The stock was also upgraded by Roth MKM.

- Twilio drops 1.9% in premarket trading, following a 13% slump in the stock on Wednesday. Goldman Sachs cuts its ratings on Twilio, Bentley Systems and RingCentral to neutral and TechTarget to sell to reflect updated views on the technology companies following first-quarter earnings.

- Unity Software shares gain 8.9% in US premarket trading after the graphic-tools provider’s quarterly sales topped expectations and analysts said its outlook, following completion of its combination with IronSource, remains robust.

- Allegro MicroSystems rises 1.9% in US premarket trading after forecast net sales for the first quarter beat the average analyst estimate.

The pound trimmed its losses slightly after the Bank of England raised rates to the highest level since 2008 and said further increases may be needed if inflationary pressures persist. The BOE also made the biggest upgrade to UK growth projections since it gained independence in 1997.

After gaining in April, US stocks have traded range-bound so far this month as worries about the turmoil in regional banks and a potential recession outweigh corporate earnings that were better than investors feared. Sentiment has picked up in recent days after the Fed signaled that a pause in rate hikes might be on the cards, but market participants warned equity markets could see more volatility.

“While inflation is trending in the right direction, we still see potential for disappointment among equity investors on the pace of Fed easing in the remainder of this year,” Mark Haefele, chief investment officer at UBS Global Wealth Management, wrote in a note.

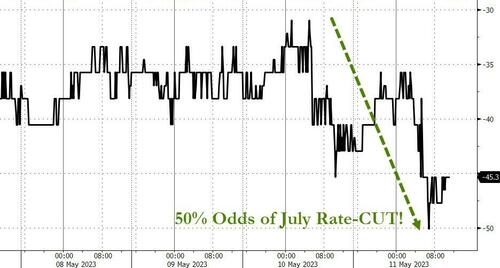

Investor attention now turns to US initial jobless claims and producer prices data due later, which will provide the latest snapshot of the state of the economy. Figures out Wednesday showed signs of moderating US inflation after a year’s worth of Fed rate hikes and recent credit stress. However, overall prices are still rising at a brisk pace and the job market remains robust.

“It’s definitely optimistic to think about a rate cut, but not so optimistic to think about a rate pause,” Sunaina Sinha Haldea, global head of private capital advisory at Raymond James, said on Bloomberg Television. “The print gives the Fed what it needs to contemplate a pause.”

European stocks erase much of their earlier gains after the Bank of England hiked rates by a quarter point and after the latest negative Pacwest news hit. The Stoxx 600 gains 0.1% with consumer products, travel and healthcare the strongest performing sectors. Here are the notable European movers:

- Genmab gains as much as 6.9%, with analysts saying the Danish biotech’s latest quarterly earnings show it remains on track to meet its guidance, with good performance for its key products

- ING rises as much as 4% after posting estimate-beating 1Q net income and announcing a share buyback of up to €1.5 billion, with RBC analysts calling it a “strong” set of results

- Diploma climbs as much as 6.4% as Jefferies upgrades to buy, citing the UK equipment-parts supplier’s capacity to deploy its recent equity raise on further M&A

- Knorr-Bremse gains as much as 3.9% after 1Q results, with analysts noting record order numbers at the braking-systems manufacturer, driven by a strong performance in the trucks unit

- Deutsche Telekom rises as much as 1.9%, the biggest one-day advance in a month, as the German carrier’s 1Q revenue growth in European markets beat analyst estimates

- Grainger advances as much as 3.5%, the most intraday since February, after the UK property developer’s results beat expectations, with analysts noting the resilience of its underlying markets

- Suse plunges as much as 23% after missing analyst expectations for the second quarter and lowering its full-year guidance, citing the impact of ongoing economic uncertainty on customers’ decision making

- Bayer falls as much as 7.9% as analysts say the German company’s pharmaceuticals division weighed on the first quarter amid weakness in key drug Xarelto

- Rolls-Royce drops as much as 4.4% after it reaffirmed its forecast for the full year as analysts cite ongoing supply-chain issues as a drag, with Bernstein seeing significant uncertainty ahead

- Coloplast falls as much as 9% after the Danish ostomy and continence care firm reported its latest earnings and updated its FY23 forecasts, with Citi describing the results as “underwhelming”

- Verbund dips as much as 2.3% after the Austrian utility narrowed its full-year guidance and analysts flagged the potential further impact from new windfall tax plans in the country

Earlier in the session, Asian stocks fell as traders weighed inflation numbers from the world’s two largest economies as well as global corporate earnings. The MSCI Asia Pacific Index declined as much as 0.4%, as all but two sectors fell. TSMC and Tencent dragged on the gauge, while Li Auto was among the biggest boosts after robust results. The regional benchmark erased an early gain after China reportedslower-than-expected inflation amid weak consumer demand. That damped sentiment after the US consumer-price print overnight showed signs of cooling and boosted hopes for a pause in Federal Reserve rate hikes.

“Investors breathed a sigh of relief” on the US CPI data but the China data “points to an uneven economic recovery,” said Eli Lee, head of investment strategy at Bank of Singapore. He added that the key issue going forward will be the ongoing debt-ceiling talks in the US. Hong Kong’s Hang Seng Index and China’s CSI 300 gauge ended the day lower after the inflation report. Stocks also fell in South Korea, Singapore, Taiwan and Australia

Japanese equities were mixed as investors examined a wave of domestic company results. The Topix fell 0.1% to close at 2,083.09, while the Nikkei was little changed at 29,126.72. Toyota Motor contributed the most to the Topix decline, decreasing 0.8%. Out of 2,159 stocks in the index, 884 rose and 1,170 fell, while 105 were unchanged. Panasonic and Fujifilm were among stocks that climbed after better-than-expected earnings and outlooks, while Sumitomo Metal and Kao fell after disappointing investors. “Yesterday and today are basically the peak of the earnings season,” said Hitoshi Asaoka, a strategist at Asset Management One. “Japan is more focused on earnings right now rather than overseas macro or US CPI data.”

Austarlian stocks edged lower: the S&P/ASX 200 index fell 0.1% to close at 7,251.90, notching its third straight day of declines. Miners and health shares contributed the most to the benchmark’s retreat. Lithium producers were among the top performers after Allkem agreed to merge with US rival Livent. In New Zealand, the S&P/NZX 50 index fell 0.8% to 11,887.76

In FX, the Bloomberg Dollar Spot Index has gained 0.3% with the greenback rising versus all its G-10 rivals. The Australian dollar is the weakest, falling 0.6%, while the pound is down 0.3% after the BOE having erased a modest gain.

In rates, treasuries were near session highs US trading gets under way Thursday amid weakness in US equity index futures, after a brief setback following Bank of England policy statement. Yields across curve are richer by 3bp-4bp, new 10-year around 3.40% vs Wednesday’s 3.448% auction stop. Gilts pared gains following Bank of England rate decision to hike 25bp (in line with estimate) in a 7-2 vote, while statement was slightly hawkish. German two-year yields are up 1bps at 2.59% having pared an earlier drop after an ECB survey revealed a notable rise in consumer inflation expectations. The US treasury auction cycle concludes with $21b 30-year bond sale at 1pm; 10-year sale produced mixed demand metrics. WI 30- year at 3.765% is ~10bp cheaper than April’s, which stopped on the screws. IG issuance slate includes BNG Bank 5Y SOFR and is expected to be modest; four names priced $3.1b Wednesday with at least one borrower electing to stand down.

In commodities, crude futures advance with WTI rising 0.9% to trade near $73.20. Spot gold falls 0.3% to around $2,024.

Bitcoin is softer and has moved marginally below the USD 27.5k mark in relatively narrow sub-500 parameters as we await the afternoon’s key events with broader market action generally lacking catalysts at this point in time.

To the day ahead now, and the main highlight will be the Bank of England’s latest policy decision. From central banks, we’ll also hear from Fed Governor Waller, ECB Vice President de Guindos, as well as the ECB’s Schnabel and de Cos. Otherwise, US data releases include the April PPI reading and the weekly initial jobless claims.

Market Snapshot

- S&P 500 futures up 0.3% to 4,165.50

- STOXX Europe 600 up 0.5% to 465.82

- MXAP down 0.3% to 161.46

- MXAPJ down 0.3% to 514.13

- Nikkei little changed at 29,126.72

- Topix down 0.1% to 2,083.09

- Hang Seng Index little changed at 19,743.79

- Shanghai Composite down 0.3% to 3,309.55

- Sensex little changed at 61,979.09

- Australia S&P/ASX 200 little changed at 7,251.92

- Kospi down 0.2% to 2,491.00

- German 10Y yield little changed at 2.29%

- Euro down 0.5% to $1.0929

- Brent Futures up 0.9% to $77.07/bbl

- Gold spot down 0.4% to $2,022.94

- U.S. Dollar Index up 0.40% to 101.88

Top Overnight News from Bloomberg

- China’s inflation sinks far below expectations, with the Apr CPI coming in +0.1% (vs. the Street +0.3% and down from +0.7% in March) and Apr PPI at -3.6% (vs. the Street -3.3% and down from -2.5% in March). WSJ

- China’s April M2 money supply growth falls short of the Street consensus at +12.4% (down from +12.7% in March and below the Street +12.5%) while new yuan loans were just CNY718B (about half the Street’s CNY1.4T forecast). WSJ

- China’s soft inflation & bank lending data, coupled with reports of plans by banks to cut deposit rates, fuels expectations of easier monetary policy from the PBOC. RTRS

- SoftBank has warned that the war in Ukraine and the US-China dispute continue to pose the biggest market risk after annual investment losses from its Vision Funds hit a record ¥5.3tn ($39bn). FT

- ECB’s consumer survey shows a sharp jump in inflation expectations (the median rate of perceived inflation over the previous 12 months increased to 9.9% in March 2023, from 8.7% in February), a finding that will keep pressure on Lagarde to proceed with further tightening. ECB

- US Treasury secretary Janet Yellen has warned of a global downturn and “dreadful consequences” that would undermine its economic leadership if Congress does not raise the federal debt limit. FT

- Donald Trump urged Republican lawmakers to let the US default on its debts unless Democrats capitulate to demands for “massive” spending cuts, a significant intervention by the former president as Washington contends with a looming fiscal crisis. FT

- Blackstone reaffirmed it’s in talks with regional lenders. Its president, Jon Gray, told the FT discussions center around the banks making loans that Blackstone would funnel to insurers, which would hold the debt to maturity. The insurers would pay Blackstone for directing the assets their way. FT / BBG

- PacWest filed its 10Q this morning and provided details on deposit flows during the month of May. The company said the recent “exploring options” media report from back on May 3 created fears among its customer base about the safety of their deposits. “During the week ended May 5, 2023, our deposits declined approximately 9.5%, with a majority of that decline occurring on May 4th and May 5th after the news reports on the afternoon of May 3rd. These recent events, and the ongoing news coverage of these events, has increased certain risks and uncertainties related to our business and future prospects”. RTRS

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed after the indecisive performance stateside where stock markets whipsawed and treasuries rallied in the absence of any hawkish surprises from the US CPI report, while the regional bourses also reflected on softer-than-expected Chinese inflation data. ASX 200 was marginally lower as weakness in utilities and the commodity-related sectors overshadowed the outperformance in tech and after consumer inflation expectations ticked higher. Nikkei 225 was indecisive with the biggest movers in the index largely influenced by earnings releases, while the BoJ’s Summary of Opinions from the April meeting did little to shift the dial. Hang Seng and Shanghai Comp. were choppy after the latest Chinese inflation supported the idea of a slow economic rebound as consumer prices grew at the slowest pace of increase since February 2021 and with factory gate prices at a deeper deflation.

Top Asian News

- China reportedly told the US that there is little chance of their defence chiefs meeting, according to FT.

- Chinese Foreign Minister Qin is to meet with his French counterpart and said that China wants to mutually open up markets with France and create a more resilient supply chain, while he added that China’s determination to promote high-quality development and a high level of opening up is unswerving.