MAY 12/2023 · by harveyorgan · in Uncategorized · Leave a comment·Editi

GOLD PRICE CLOSED: DOWN $0.40 TO $2014.75

SILVER PRICE CLOSED: DOWN $0.26 AT $23.97

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE $2014.50

Silver ACCESS CLOSE: 24.17

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

“America has been blessed never to have a native criminal class. Excepting Congress, of course.” … Mark Twain

GO GATA!

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $26,339 DOWN 710 Dollars

Bitcoin: afternoon price: $26,165 DOWN 884 dollars

Platinum price closing $1061.25 DOWN $35.85

Palladium price; $1518.70 DOWN $39.70

GO GATA!

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,725.03 UP 7.00 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1614.92 UP 5.00 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1853.24 UP 8.20 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

CONTRACT: MAY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,014.700000000 USD

INTENT DATE: 05/11/2023 DELIVERY DATE: 05/15/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 35

323 C HSBC 80

363 H WELLS FARGO SEC 20

435 H SCOTIA CAPITAL 3

523 C INTERACTIVE BRO 3

661 C JP MORGAN 17

690 C ABN AMRO 5

709 C BARCLAYS 1

737 C ADVANTAGE 2 8

905 C ADM 8

TOTAL: 91 91

JPMorgan stopped 17/91 contracts

FOR MAY:

GOLD: NUMBER OF NOTICES FILED FOR MAY/2023. CONTRACT: 91 NOTICES FOR 9100 OZ or 0.2830 TONNES

total notices so far: 5778 contracts for 577,800 oz (17.6972 tonnes)

FOR MAY:

SILVER NOTICES: 169 NOTICE(S) FILED FOR 845,000 OZ/

total number of notices filed so far this month : 2141 for 10,705,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $0.40..THIS IS INTERESTING!!

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:///A DEPOSIT OF 2.89 TONNES INTO THE GLD//

INVENTORY RESTS AT 937.84 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN $.26 AT THE SLV// ALSO INTERESTING

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.123 MILLION OZ INTO THE SLV/: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 470.091 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 1429 CONTRACTS TO 148,225 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR HUGE $1.15 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $1.15). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A MONSTROUS GAIN ON OUR TWO EXCHANGES OF 3372 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 4.250 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS( 1864 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.105 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S E.F.P.. JUMP TO LONDON OF 145,000 OZ(EF.P. JUMP LOWERS THE AMOUNT OF SILVER STANDING)+0 EXCHANGE FOR RISK// TOTAL 4.25 MILLION OZ OF EXCHANGE FOR RISK FOR THE MONTH(RAISES THE AMOUNT OF SILVER STANDING):THUS TOTAL OF 17.160 MILLION OZ OF STANDING FOR DELIVERY V) HUGE SIZED COMEX OI GAIN/ HUGE SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –79 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTRACTS for 10 days, total 8429 contracts: OR 42.145 MILLION OZ . (842 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 42.145 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 42.145 MILLION OZ/INITIAL

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1429 CONTRACTS DESPITE OUR $1.15 LOSS IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1864 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 13.105 MILLION OZ//FIRST DAY NOTICE FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 145,000 OZ (DECREASES THE AMOUNT OF SILVER STANDING) +// + 0.0 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //TOTAL EXCHANGE FOR RISK MONTH= 4.25 MILLION//NEW TOTALS 12.910 MILLION OZ + 4.25 MILLION = 17.160 MILLION OZ// .. WE HAVE A HUGE SIZED GAIN OF 3293 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 169 NOTICE(S) FILED TODAY FOR 845,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 84 CONTRACTS TO 523,752 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: removed 581 CONTRACTS

WE HAD A SMALL SIZED INCREASE IN COMEX OI ( 84 CONTRACTS) DESPITE OUR $15.15 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR MAY. AT 3.5085 TONNES ON FIRST DAY NOTICE // PLUS 8400 OZ QUEUE. JUMP :(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)////YET ALL OF..THIS HAPPENED WITH OUR $15.15 LOSS IN PRICE WITH RESPECT TO THURSDAY’S TRADING.WE HAD A GOOD SIZED GAIN OF 3063 OI CONTRACTS (9.527 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 2975 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 523,752

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3063 CONTRACTS WITH 84 CONTRACTS INCREASED AT THE COMEX AND 2975 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3063 CONTRACTS OR 9.527 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3975 CONTRACTS) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (84 //TOTAL GAIN IN THE TWO EXCHANGES 3063 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 3.5085 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 8400 OZ // NEW STANDING: 18.336 TONNES // ///3) ZERO LONG LIQUIDATION//4) SMALL SIZED COMEX OPEN INTEREST GAIN/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 28,228 CONTRACTS OR 2,822,800 OZ OR 87.80 TONNES IN 10 TRADING DAY(S) AND THUS AVERAGING: 2822 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAY(S) IN TONNES 87.80 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 87.80/3550 x 100% TONNES 2.47% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES ( MUCH SMALLER THAN LAST MONTH)

MAY: 87.80 TONNES (HEADING FOR ANOTHER SMALLER MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS and sell the future TAS two months out. T they unload the front month so the price of gold/silver falls.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 1429 CONTRACTS OI TO 148,225 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 1864 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1864 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1864 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1429 CONTRACTS AND ADD TO THE 1864 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 3293 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 16.46 MILLION OZ

OCCURRED DESPITE OUR $1.15 LOSS IN PRICE??? ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED DOWN 37.19 PTS OR 1.12% //Hang Seng CLOSED DOWN 116.53 POINTS OR 0.59% /The Nikkei closed UP 261.53 OR 0.90% //Australia’s all ordinaries CLOSED UP 0.05 % /Chinese yuan (ONSHORE) closed DOWN 6.9514 /OFFSHORE CHINESE YUAN DOWN TO 6.9649 /Oil DOWN TO 71.18 dollars per barrel for WTI and BRENT AT 75.08 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 84 CONTRACTS UP TO 523,752 DESPITE OUR HUGE LOSS IN PRICE OF $15.15 ON THURSDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF MAY… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2975 EFP CONTRACTS WERE ISSUED: : JUNE 2975 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2975 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 3,063 CONTRACTS IN THAT 2975 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED GAIN OF 84 COMEX CONTRACTS..AND THIS GOOD SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR STRONG LOSS IN PRICE OF $15.15. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (18.336) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 18.336 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $15.15) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR GOOD SIZED GAIN OF 3063 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 9.527 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY. (3.5085 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 8400 oz (0.2612 TONNES)//NEW STANDING 18.336 TONNES ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $15.15

WE HAD –REMOVED 581 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3063 CONTRACTS OR 306300 OZ OR 9.527 TONNES.

Estimated gold comex today 228,458// fair

final gold volumes/yesterday 372,509 huge/yesterday’s raid//

//MAY 12/ MAY 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 192.906 OZ INT.DELAWARE 6 KILOBARS . |

| Deposit to the Dealer Inventory in oz | NIL |

| Deposits to the Customer Inventory, in oz | 10,165.388 oz Delaware |

| No of oz served (contracts) today | 91 notice(s) 9100 OZ 0.2830 TONNES |

| No of oz to be served (notices) | 117 contracts 11,700 oz 0.3639 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5778 notices 577,800 OZ 17.972 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i)Into Delaware: 10,165.388 oz

total deposits: 10,165.388 oz

customer withdrawals: 1

i) Out of Int. Delaware 192.906 oz (6 kilobars)

total withdrawals: 192.906 oz 6 kilobars

Adjustments; 1//customer to dealer/Manfra:

1639.701 oz (51 kilobars)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 208 contracts having LOST 151 contracts. We had 235 contracts filed

on THURSDAY, so we gained 84 contracts or an additional 8400 oz (0.2612 tonnes) will stand for gold in this non active delivery month of May.

June LOST 29,254 contracts DOWN to 265,728 contracts.

July added 30 contracts to stand at 1547 contracts.

AUGUST GAINED 28,008 contracts up to 203,115 contracts

We had 91 contracts filed for today representing 9100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 91 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 17 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2023. contract month,

we take the total number of notices filed so far for the month (5,778 x 100 oz ), to which we add the difference between the open interest for the front month of MAY 208 CONTRACTS) minus the number of notices served upon today 91 x 100 oz per contract equals 589,500 OZ OR 18.336 TONNES the number of TONNES standing in this NON- active month of May.

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (5,778 x 100 oz) 208 OI for the front month minus the number of notices served upon today (91)x 100 oz} which equals 589,500 oz standing OR 18.336 TONNES

TOTAL COMEX GOLD STANDING: 18.074 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,666,085.702 OZ 51.822 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,593,059.376 OZ

TOTAL REGISTERED GOLD: 12,401,306.774 (385,73 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,191,754.602 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,735,219 OZ (REG GOLD- PLEDGED GOLD) 333.91 tonnes//

END

SILVER/COMEX

MAY 12//2023// THE MAY 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,264,157.090 oz Brinks CNT Delaware JPMorgan . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 620,209.200 oz JPMorgan 599,378.800 oz Loomis |

| No of oz served today (contracts) | 169 CONTRACT(S) (845,000 OZ) |

| No of oz to be served (notices) | 441 contracts (2,205,000 oz) |

| Total monthly oz silver served (contracts) | 2141 Contracts (10,705,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i)Into Loomis: 599,378.800 oz

ii) Into JPMorgan: 620,209.200 oz

Total deposits: 1,219,588.000 oz

JPMorgan has a total silver weight: 139.024 million oz/270.359 million =51.42% of comex .//dropping fast

Comex withdrawals 4

i) Out of Delaware 5948,600 oz

ii) Out of jPMorgan: 584,559.800 oz

iii) Out of CNT: 515,928.550 oz

iv) Out of Brinks 157,720.140 oz

Total withdrawals; 1,264,157.090 oz

adjustments: 0

TOTAL REGISTERED SILVER: 29.958 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 270.359 million oz

we have now seen the movement of the registered silver comex into the 29 million column:

CALCULATION OF SILVER OZ STANDING FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2023 OI: 610 CONTRACTS HAVING LOST 39 CONTRACT(S). WE HAD 10 CONTRACTS FILED

ON WEDNESDAY, SO WE LOST 29 CONTRACTS OR AN ADDITIONAL 145,000 OZ WILL NOT STAND FOR DELIVERY ON THIS SIDE OF THE POND AS THE WERE EFP’d TO LONDON AS THERE IS NO SILVER OVER HERE FOR OUR CROOKS TO CLEAN..

JUNE HAD A 13 CONTRACT GAIN TO 1010

JULY HAD A 532 CONTRACT GAIN TO 124,714 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 169 for 845,000 oz

Comex volumes// est. volume today 71,449 strong

Comex volume: confirmed yesterday: 112,645 huge/yesterday’s raid

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 2141 x 5,000 oz = 10,705,000 oz

to which we add the difference between the open interest for the front month of MAY(610) and the number of notices served upon today 169 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2023 contract month: 2141 (notices served so far) x 5000 oz + OI for the front month of May (610) – number of notices served upon today (169 )x 500 oz of silver standing for the MAY contract month equates to 12.910 million oz + THE CRIMINAL 0 MILLION OZ EXCHANGE FOR RISK TODAY//NEW TOTAL EXCHANGE FOR RISK: 4.250//NEW TOTAL 17.160 MILLION OZ//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 437.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 434.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 434.95 TONNES

MAY 9/WITH GOLD UP $9.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTER DEPOSIT OF 5.88 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 437.64 TONNES

MAY 8/WITH GOLD UP $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 431.77 TONNES

MAY 5/WITH GOLD DOWN $30.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AS DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

MAY 4/WITH GOLD UP $19.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.30 TONNES

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

APRIL 10/WITH GOLD DOWN $21.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91 TONNES

APRIL 6//WITH GOLD DOWN $9.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91

APRIL 5//WITH GOLD UP 0 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04

APRIL 4/WITH GOLD UP $36.30 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

APRIL 3/WITH GOLD UP $14.20 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.02 TONNES

MARCH 31/WITH GOLD DOWN $10.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD////INVENTORY RESTS AT 928.02 TONNES

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

GLD INVENTORY: 937.84 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

MAY 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A TINY DEPOSIT OF .08 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 465.682 MILLION OZ//

MAY 8/WITH SILVER DOWN 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.602 MILLION OZ//

MAY 5/WITH SILVER DOWN 31 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 466.876 MILLION OZ//

MAY 4/WITH SILVER UP 53 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF .174 MILLION OZ INTO SLV.//INVENTORY RESTS AT 467.174 MILLION OZ//

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 10/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 6/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 4.643 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 468.585 MILLION OZ//

APRIL 5/WITH SILVER DOWN 4 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.942 MILLION OZ

APRIL 4/WITH GOLD UP $1.11 TODAY CRIMINAL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.47 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 463,942 MILLION OZ

APRIL 1/WITH SILVER DOWN 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.412

MARCH 31/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD/: A MASSIVE 4.779 MILLION OZ DEPOSITED INTO THE SLV///INVENTORY RESTS AT465.412 MILLION OZ

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

CLOSING INVENTORY 470.091 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

This is good news: investors bought 302 tonnes of gold bars/coins in Q1 and if we extropolate that for the year: around 1200 tonnes. Remember that the globe produces 2200 tonnes of gold ex China ex Russia (they never let their gold out)

(Schiff)

Physical Gold Investment Up 5% In First Quarter

THURSDAY, MAY 11, 2023 – 03:40 PM

Physical gold investment was up by 5% year-on-year in the first quarter.

Investors bought 302 tons of gold bars and gold coins in Q1 with a value of $18.4 billion. This was 14% above the 5-year average, according to the World Gold Council.

The surge in physical gold investment came even as gold prices reached record levels in many currencies.

According to the World Gold Council, persistently high inflation, geopolitical risks, and concern over contagion in the banking crisis fueled demand for gold.

Investors preferred gold in the form of coins in Q1. Demand for gold coins came in at 96.5 tons, a 14% annual increase. Bar demand was 181.9 tons, a 1% decline year-on-year.

Even with the jump in demand year-on-year, first-quarter gold buying did not match Q4’s record high. Higher gold prices encouraged some profit-taking and there were declines in demand in some markets, particularly India and Europe.

Physical Gold Demand By Region

The banking failure in March lit a fuse under US gold bar and gold coin investors. US bar and coin demand came in at 32 tons. It was the fourth-strongest quarter in the World Gold Council’s data series. Gold bar and coin demand jumped 40% from the fourth quarter of ’22 and charted a 4% year-on-year increase.

The US Mint reported rocketing coin sales of 288,000 ounces in March. It was the biggest monthly total since October 1998, when the Y2K safe-haven rush for gold was in full swing.

Q1 bar and coin investment also soared in China during the first quarter. Demand totaled 66 tons. That was a 34% jump year-on-year and a 7% rise quarter-on-quarter.

According to the World Gold Council, “Chinese New Year generated robust demand for gold investment, particularly given the local gold price strength, which outperformed relative to other domestic assets including stocks, bonds and commodities.”

The WGC also said gold buying by the Chinese central bank also drove local interest in the yellow metal.

China ranks as the largest gold market in the world.

In contrast, demand for physical gold in India came in at 34 tons, a 17% year-on-year decline. Record high and volatile local gold prices muted demand. According to the World Gold Council, “The speed and scale of the rise in the local gold price deterred fresh buying and instead encouraged profit-taking for many. Furthermore, the low margins on gold investment products, relative to jewelry, meant that retailers concentrated their promotional efforts on the latter.”

Demand was also muted in Europe. The 38 tons of physical gold purchased in Europe during Q1 was less than half the total recorded in q1 2022 and the lowest quarterly total since the beginning of the pandemic. A big drop in German demand drove overall European demand lower. According to the World Gold Council, “The main trigger for the collapse in investment appears to have been the shift back to positive real rates for the first time in nine years, due to easing inflation and higher nominal rates. The rising euro gold price in January also reportedly encouraged profit-taking, with the net result that demand was more or less zero during the month.”

All markets across the Middle East recorded growth in Q1 bar and coin demand. Regional investment hit 29 tons – a quarterly total that has been exceeded on only three previous occasions.

Also notable is that bar and coin investment in Turkey reached phenomenal levels in the first quarter, breaching 50 tons for the first time on record. Demand increased fivefold year-on-year and was 32% higher than in Q4.

ETFs

While investors rushed into physical gold, gold ETFs continued to see outflows in the first quarter. Globally, 29 tons of gold flowed out of gold-backed ETFs.

But there were signs of a reversal in the trend. For the first time in 10 months, gold flowed into ETFs in March with global gold ETFs recording net inflows of 32 tons.

Funds listed in North America saw gold inflows of 10 tons in Q1. European ETFs charted outflows of 40 tons. Asian funds reported modest outflows of less than 1 ton.

ETFs are backed by physical gold held by the issuer and are traded on the market like stocks. They allow investors to play gold without having to buy full ounces of gold at spot price. Since their purchase is just a number in a computer, they can trade their investment into another stock or cash pretty much whenever they want, even multiple times on the same day. Many speculative investors appreciate this liquidity.

There are good reasons to invest in ETFs, but they aren’t a substitute for owning physical metal. In an overall investment strategy, SchiffGold recommends buying gold bullion first.

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

3,Chris Powell of GATA provides to us very important physical commentaries

A must read: the dynamics of why the uSA dollar will be falling

(Alasdair Macleod)

Alasdair Macleod: The dynamics driving the dollar down

Submitted by admin on Fri, 2023-05-12 00:32Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, May 11, 2023

This article examines the currency imbalances between U.S. dollars and the other currencies and concludes that should foreign holders decide to reduce their dollar exposure, the consequences for the dollar’s value would be dramatic.

The dollar’s problems should be laid at the door of the wishful thinkers who think the state knows better than free markets. It is what has led to currency imbalances. Central banks attempting to manage economic outcomes by manipulating interest rates and “stimulating” economic activity have acted in defiance of Say’s Law, which defines the relationship between production and consumption, and the true role of a medium of exchange.

By dismissing this fundamental truth, the U.S. authorities have made a rod for their own backs. Their determination to replace gold as the highest form of money with the fiat dollar has led to extraordinary levels of dollar accumulation about to be unleashed onto unsuspecting markets. A break below 100.50 on the dollar’s trade weighted index will probably be the signal. It currently stands at 101.50. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/the-dynamics-driving-the-dollar-down?gmrefcode=gata

END

It is about time: AngloGold Ashanti is planning to redomicile in the UK after winding down its South African operations and will focus on other markets.

(London’s Financial Times)

AngloGold Ashanti to switch primary listing to New York

Submitted by admin on Fri, 2023-05-12 05:11Section: Daily Dispatches

By William Langley

Financial Times, London

Friday, May 12, 2023

https://www.ft.com/content/7704382c-a8fa-4ec8-9928-88a389449fe6

Miner AngloGold Ashanti has announced plans to transfer its primary listing to New York and redomicile in the UK after winding down its South African operations to focus on other markets.

Under a plan set out today the company, which has its primary listing in Johannesburg, will keep a secondary listing there and have another in Ghana.

AngloGold sold its last South African mine in 2020 to focus on operations elsewhere in the continent, as well as in Australia and the Americas. That move created speculation that the company could shift its listing to London, where shares in most of the world’s largest mining groups are traded.

The company said a US primary listing would boost access to “the world’s deepest pools of capital,” adding that an existing secondary listing on Wall Street already generated about two-thirds of daily liquidity in its shares.

The company expects the proposed changes to complete during the third quarter of this year.

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

Live from the Vault ANDREW MAGUIRE INTERVIEWING DAVID TICE

The gold window reopens! An opportunity among threats. Fea…

David Tice joins Andrew Maguire to discuss the latest geopolitical developments and their impact …

END

5.IMPORTANT COMMENTARIES ON COMMODITIES:

end

5 B GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS// FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.9518

OFFSHORE YUAN: 6.9644

SHANGHAI CLOSED DOWN 37.19 PTS OR 1.12%

HANG SENG CLOSED DOWN 116.53 PTS OR 0.59%

2. Nikkei closed UP 261.58 PTS OR 0.90%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 102.01 EURO FALLS TO 1.0895 DOWN 17 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.383 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 134.21 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.2625***/Italian 10 Yr bond yield FALLS to 4.155*** /SPAIN 10 YR BOND YIELD RISES TO 3.334…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 3.962

3j Gold at $2004.30 silver at: 23.82 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 50 /100 roubles/dollar; ROUBLE AT 77.74//

3m oil into the 71 dollar handle for WTI and 75 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 134.84 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .383% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8937 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9739 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.420 UP 2 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.773 UP 3 BASIS PTS/

USA 2 YR BOND YIELD: 3.9181 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.60…

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 3.79 UP 8 BASIS PTS

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Rise As Luxury Blowout Lifts European Markets; Dollar, Yields Higher

FRIDAY, MAY 12, 2023 – 08:15 AM

US equity futures advanced to end the week as traders remained fixated on the path of monetary policy while assessing stronger than expected corporate earnings as the season nears its end. Contracts on the S&P 500 rose 0.3% at 8:00 a.m. ET while those on the Nasdaq 100 advanced 0.2%. Swiss luxury-goods maker Richemont soared 7.8% to a record on “spectacular sales growth”, fueling a broad rally across European luxury stocks. Risk-on sentiment pushed Treasury yields higher. The Bloomberg dollar index was poised for its biggest weekly gain since March while oil prices declined again, set for their fourth weekly loss. Meanwhile, gold is also on course to end the week lower. Iron ore futures are falling sharply for a second day, but still on track for a weekly gain.

In premarket trading, Tesla rose 2% after the electric-car maker raised prices of its Model X and Model S cars in the US, the third change in less than a month, while Musk announced that Twitter would have a new CEO in 6 weeks.

- Amylyx Pharmaceuticals shares gain 7.5% after the drugmaker’s sales of its amyotrophic lateral sclerosis drug topped analyst estimates.

- ARS Pharmaceuticals surges 65% after saying an FDA panel voted to to support a favorable benefit-risk assessment for Neffy to treat severe allergic reaction.

- Blue Bird Corp. soars 31% after the company boosted its revenue and adjusted Ebitda forecast for the full year.

- Cidara Therapeutics rises 11% as Cantor Fitzgerald flagged multiple catalysts.

- Fox Corp. falls 1.8% as Wells Fargo cut the recommendation on the media company’s stock to equal-weight, saying there’s some strategic uncertainty ahead.

- IonQ drops 10% after the software company posted first-quarter results.

- Sarepta Therapeutics stock is halted for pending news, while the company’s drug candidate for Duchenne muscular dystrophy is set to face an FDA advisory committee meeting on Friday.

- SiriusPoint Ltd. falls 15% after Dan Loeb said he’s no longer exploring an acquisition of the company.

- CuriosityStream shares advanced in extended trading on Thursday, after the entertainment company reported its first-quarter results and gave an outlook.

S&P 500 futures traded higher after President Joe Biden and House Speaker Kevin McCarthy postponed a meeting on the debt ceiling that was planned for Friday. The delay reflects headway in staff-level discussions, Bloomberg reported citing people familiar with the talks, however a more realistic take came from Punchbowl which said that “the two sides haven’t narrowed down the policies they might want to include in a debt-limit or spending-cut package.”

“We believe that they will find a deal — we need to remember negotiations have only just started,” said Marie Jacot-Cardoen, chief executive officer of Edmond de Rothschild Asset Management France, on Bloomberg Television. “It is likely political antagonism will increase before deal is reached, but we believe a compromise will be found.”

US equities have been mainly trading in a very tight range all month after climbing over the past two amid concerns of a recession and uncertainty surrounding the path of interest rates. Earnings have been better than expected but did little to lift the S&P 500 after they rallied ahead of the season. Investors are also worried about the US debt-ceiling and stability of the banking industry, though efforts to repair ties between Washington and Beijing have been supportive.

“The breadth of the US equity market has fallen to multi-decade lows, masking the weaker performance and lower investor conviction in smaller constituents,” said Mark Haefele, chief investment officer of UBS Global Wealth Management. “This suggests crowding and vulnerability, as narrow equity market breadth historically happens in the later stages of a bull market.”

Meanwhile, BofA’s Michael Hartnett said a prolonged period of economic decline in the US will roil technology stocks at a time when they are attracting a weight of investor money. They expect a recession “to crack credit and tech” just as it did in 2008.

Elsewhere, investors remained focused on what major central banks will do next in their rate-hiking campaigns to quell inflation. US data Thursday showed initial jobless claims reached the highest since October 2021 while producer prices rose less than economists expected, suggesting Federal Reserve policy tightening may finally be having an effect.

“There’s a chink of light — inflation is beginning to show some signs of easing, boosting hopes the Fed’s rate hiking cycle is near an end and this means companies can start prioritizing growth, rather than servicing debt,” said Angeline Ong, a financial analyst at IG Group.

Luxury goods maker Richemont gained 7.8% to a record, fueling a broad rally across European luxury stocks. Europeans stocks are ahead and on course to finish the week in the green as investors welcome signs of easing strains between the US and China and tentative progress in the debt-ceiling negotiations. The Stoxx 600 is up 0.6% with consumer products, financial services and retailers the strongest-performing sectors while retail and autos fall. Here are the most notable European movers:

- Richemont shares rise as much as 5.6%, hitting a record high, after reporting forecast-beating sales growth and operating profit. Its jewelery division showed “spectacular sales growth,” driving significant improvement in profitability, Vontobel said. Other luxury stocks also gained, with LVMH rising 1.5%

- Scor shares rose as much as 11% after a strong set of results, with a significant net income beat driven by better performance in both L&H and P&C

- GSK shares rise as much as 1.7% after the UK pharma group £804 million sells a stake in Haleon, the consumer health- care division it spun off as a separate company last year. It also welcomed Zantac class action dismissal in British Columbia.

- Beazley shares rise as much as 6.5%, hitting the highest since March 31, after the British insurer’s quarterly results topped expectations for premium growth, while investment income also increased.

- THG shares drop as much as 23%, after the UK online retailer ended talks with Apollo about an indicative takeover proposal.

- Soitec shares tumble as much as 9.8%, after JPMorgan downgraded the stock to underweight from neutral and almost halved its price target, noting the wafer maker’s fiscal 2024 outlook was at risk of a slow recovery in demand for chips used in smartphones.

- Accor falls as much as 3.2% in Paris after an offering of 7m shares priced at €31.81 apiece by holder Qatar Holding via BofA Securities, according to terms seen by Bloomberg.

- Nordex shares drop as much as 5.6% after the German wind turbine maker reported results that analysts said were disappointing, noting a larger-than-expected loss driven by liquidated damages and extra catch-up costs from the delays in the winter.

Earlier in the session, Asian stocks headed for a fourth day of decline, as Chinese shares pulled back further after the nation’s weak inflation and borrowing data showed the economic recovery is waning, adding to growth concerns globally. The MSCI Asia Pacific dropped as much as 0.3% Friday, led lower by material and energy shares. Chinese and Hong Kong benchmarks led declines in the region as traders fret over the slew of worse-than-expected economic data, which underscores ongoing problems in the housing market and sluggish domestic demand after Covid reopening. Chinese tech stocks bucked the broader market’s trend after e-commerce firm JD.com reported better-than-expected results, and geopolitical concerns eased on the news of a meeting between Biden and Xi. US National Security Adviser Jake Sullivan also met with China’s top diplomat Wang Yi.

Meanwhile, Japanese shares outperformed the region as investors welcomed another wave of quarterly results from domestic companies. Companies including Honda and KDDI that announced buybacks along with earnings were among the biggest boosts. The Topix rose 0.6% to close at 2,096.39, while the Nikkei advanced 0.9% to 29,388.30. Keyence Corp. contributed the most to the Topix gain, increasing 2.7%. Out of 2,159 stocks in the index, 1,197 rose and 867 fell, while 95 were unchanged. In addition to the decline in U.S. long-term Treasury yields overnight, “the Japanese market is also benefiting from the sense of undervaluation of Japanese stocks,” said Ayako Sera, market strategist at Sumitomo Mitsui Trust Bank

The Asian stock benchmark was poised for a weekly drop amid weaker global growth and a resurgence of banking sector worries. Still, a cooling US job market and softening producer prices added confidence that the Federal Reserve may soon end its tightening campaign. “The Fed is easily positioned to hold rates at the June meeting and if we see further softening of labor conditions, that will continue to drive this market into pricing in easing before the end of the year,” said Ed Moya, senior market analyst at Oanda

Indian stocks closed the week as one of Asia’s best performers, aided by strong buying from overseas investors. Foreign investors bought net $1.1 billion of local equities this week through Thursday, NSDL data showed. The buying comes amid economic resilience and signs that the central bank will stay on hold as inflation moderates. For the week, the BSE-Sensex climbed 1.6% compared to MSCI Asia-Pacific index’s 0.4% loss. Sensex outperformed markets in China, Japan, Australia during the week. On Friday, the S&P BSE Sensex rose 0.2% to 62,027.90 in Mumbai, while the NSE Nifty 50 Index advanced 0.1% to 18,314.80.

Australian stocks edged higher sending the S&P/ASX 200 index up 0.1% to close at 7,256.70, boosted by banks and health shares. The benchmark gained 0.5% for the week, snapping three weeks of declines. Asian stocks were mixed and Treasuries held gains as investors weighed signs of cooling in the American jobs market and efforts to repair ties between Washington and Beijing.

Treasuries are lower with the US 10-year yield rising 2bps to 3.41% Bunds and Gilts have also declined with 10-year borrowing costs in Germany and the UK rising by 1bps and 2bps respectively.

In FX, the Bloomberg Dollar Spot Index is up 0.1% and was set to rise 0.5% this week, the most since the week ended March 10 even as traders weigh the likelihood of a Federal Reserve policy pivot following a soft US inflation report. The Kiwi dollar is the clear underperformer, falling 1% versus the greenback after New Zealand inflation expectations fell. “For the dollar, we are not quite at the tipping point where markets can plausibly expect that the Fed will weigh up steady versus rate cut,” said Sean Callow, senior currency strategist at Westpac Banking Corp. “That probably means ranges on BBDXY hold for now, even if we prefer selling rallies than buying dips”

- EUR/USD slips 0.1% to 1.0907; it is set to lose 1% this week, its worst performance in nearly two months after a broad rally in the dollar on Thursday knocked most G10 currencies and boosted the dollar

- GBP/USD edges up 0.2% to 1.2532; the pound brushes off a weaker-than-expected reading of UK GDP

- USD/JPY rises 0.2% to 134.76

- NZD/USD fell 1.1% to 0.6232, extending losses after the nation’s two-year inflation expectations eased to within the Reserve Bank’s target band

- AUD/USD dropped 0.2% to 0.6688, weighed in part by kiwi sales

In rates, treasuries drifted lower during the London session, after Fed’s Bowman said more hikes will be needed if inflation stays too high. Treasuries cheaper by up to 4bp across long-end of the curve with 2s10s spread steeper by ~2bp on the day; 10-year yields around 3.42%. Stronger S&P 500 futures also added to cheapening pressure on Treasury yields. Bunds were also lower after European Central Bank policymaker Luis de Guindos said more hikes may be possible. IG issuance slate empty so far; two names priced deals Thursday while at least three issuers were said to have stood down due to market conditions.

In commodities, crude futures decline with WTI falling 0.6% to trade near $70.45. Spot gold drops 0.4% to around $2,006.

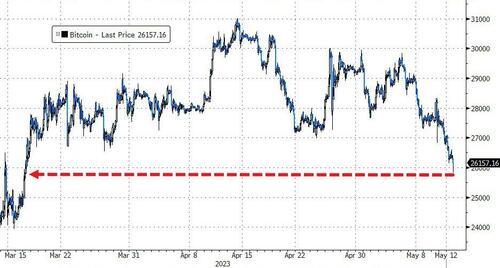

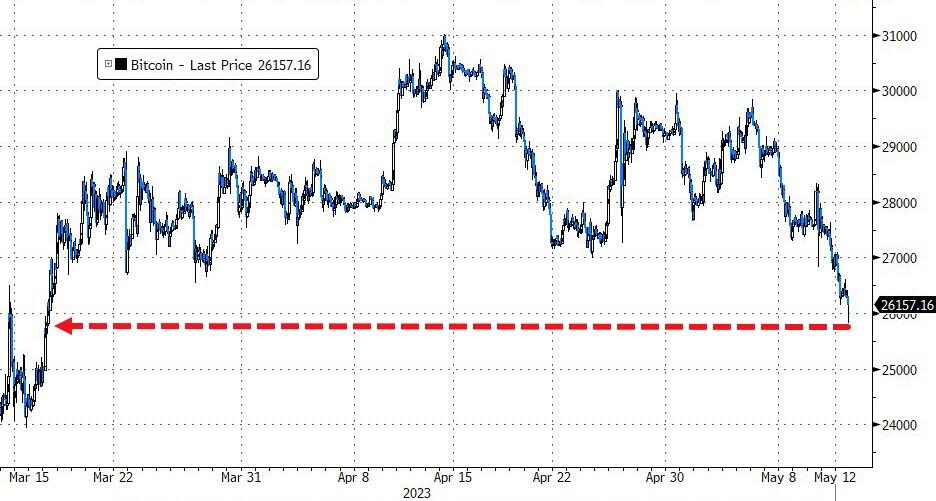

Bitcoin is softer on the session and nearing the USD 26k mark with newsflow generally light after a busy macro week ahead of a relatively busy US session. Action which keeps Bitcoin just above the earlier WTD trough.

To the day ahead now, and data releases include the UK GDP reading for Q1, along with the University of Michigan’s preliminary consumer sentiment index for May. Otherwise, central bank speakers include ECB Vice President de Guindos, BoE Chief Economist Pill and the Fed’s Daly, Bullard and Jefferson.

Market Snapshot

- S&P 500 futures up 0.4% to 4,160.00

- MXAP down 0.2% to 161.24

- MXAPJ down 0.6% to 511.37

- Nikkei up 0.9% to 29,388.30

- Topix up 0.6% to 2,096.39

- Hang Seng Index down 0.6% to 19,627.24

- Shanghai Composite down 1.1% to 3,272.36

- Sensex up 0.3% to 62,098.69

- Australia S&P/ASX 200 little changed at 7,256.65

- Kospi down 0.6% to 2,475.42

- STOXX Europe 600 up 0.6% to 466.41

- German 10Y yield little changed at 2.24%

- Euro little changed at $1.0911

- Brent Futures down 0.3% to $74.76/bbl

- Gold spot down 0.4% to $2,007.55

- U.S. Dollar Index little changed at 102.08

Top Overnight News from Bloomberg

- China will send a special envoy on a trip to Ukraine, Russia, Poland, France, and Germany as of Mon as the gov’t works to help foster a peace agreement. SCMP

- Turkish presidential candidate Ince drops out of the race, raising the odds of Erdogan being voted out of office this Sunday . FT

- The European Central Bank may have to continue raising borrowing costs beyond the summer, according to Governing Council member Joachim Nagel. BBG

- UK economic data for March is mixed, with soft GDP but better-than-anticipated industrial and manufacturing production. RTRS

- Janet Yellen reiterated the only good outcome in the debt standoff is for Congress to raise the ceiling. Global markets and US households and businesses need to see “we have a Congress that is committed to paying the bills. . . . That we’re not a deadbeat country,” she told Bloomberg at a G-7 meeting in Japan. BBG

- Fed’s Bowman warns the central bank should be prepared to continue hiking rates as employment and inflation are still too hot. WSJ

- If the U.S. defaults on its debt and is unable to pay all its bills this summer, the pain will fall squarely on the defense industry. National security is by far the largest category of discretionary federal spending, with budgets rising over the past two years to counter China’s military expansion and tackle the conflict in Ukraine. WSJ

- NBCUniversal’s head of advertising, Linda Yaccarino, is in talks to become the new CEO of Twitter, according to people familiar with the situation. WSJ

- Tesla raised prices of its vehicles in the US, the third change in less than a month, adding $1,000 to Model X and Model S base and plaid cars. It also recalled some 1.1 million cars in China — almost every EV it’s ever sold there — over a defect with their acceleration systems. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly lower amid a busy slate of earnings releases and after the subdued performance stateside where regional bank fears resurfaced and initial jobless claims disappointed. ASX 200 was lacklustre with the index constrained by weakness in the energy and mining-related sectors after the recent pressure in underlying commodity prices. Nikkei 225 outperformed and rose to its highest since November 2021 with price action largely driven by earnings results including various blue-chip stocks. Hang Seng and Shanghai Comp. were indecisive as talks between US National Security Adviser Sullivan and China’s top diplomat Wang Yi provided some encouragement towards a potential Biden-Xi call, although participants also digested weaker-than-expected Chinese loans and financing data.

Top Asian News

- Chinese Foreign Minister Qin Gang is to visit Australia in July for a reciprocal visit as ties between Australia and China ease, according to SCMP.

- EU Economic Commissioner Gentiloni said we cannot be too dependent on foreign powers and noted that decoupling would be a dangerous risk for the global economy, while he added that he is not talking about closing the trade with China but is instead talking about making supply chains more secure.

European bourses are firmer across the board, Euro Stoxx 50 +0.5%, with the Stoxx 600 set to end the week roughly where it commenced it. Sectors are primarily in the green with Consumer Products/Services outperforming post-Richemont’s (+5.0%) FY update while Real Estate/Autos lag. The APAC handover was a mixed one with sentiment inching higher since though with no clear driver/firm narrative behind this. Stateside, ES +0.2%, futures are bid but only modestly so as we await data and more Fed speak after Bowman’s early-doors commentary while Yellen provided familiar lines on the debt ceiling. Tesla (TSLA) to recall a total of 1,104,622 of imported Model S, Model X, Model 3 and domestic Model 3 and Model Y, according to Chinese market regulator. Elsewhere, WSJ said NBCUniversal’s head of advertising Linda Yaccarino was the candidate in talks to become the new CEO of Twitter.

Top European News

- Riksbank’s Thedeen says he is surprised as their rate increases have not “bitten” as he expected, the impact on the economy has not been that great, via SvD Näringsliv. “every time we have presented a new interest rate forecast; we have later revised it upwards… It is a sign that monetary policy may not have the desired effect as we have thought.” One explanation for why household consumption continues to be above expectations is their belief that rates will soon decrease rapidly. On QE, says he is somewhat “more sceptical” than perhaps some others have been, should be a “relatively high” threshold for implementing it.

- Northvolt investment within Germany reportedly to be circa. EUR 3-5bln with hundreds of millions expected in subsidies, via Reuters citing sources. *Follows earlier source reports in the FT and commentary from German officials who suggested that no details have been decided on yet.

FX

- Buck broadly underpinned as DXY fastens grip on 102.000 handle and Fed’s Bowman says recent CPI and NFP reports do not provide persistent evidence of disinflation.

- Kiwi undermined by much cooler NZ inflation expectations, NZD/USD sub-0.6250 from just above 0.6300, AUD/NZD cross tops 1.0700 vs 1.0640 low.

- Yen and Loonie soft against Greenback, but eyeing decent option expiry interest at 135.00 and 1.3500 for support.

- Pound retains 1.2500+ status despite monthly UK GDP contraction pre-BoE’s Pill and Euro treading water near 1.0900 irrespective of more hawkish ECB commentary.

- PBoC set USD/CNY mid-point at 6.9481 vs exp. 6.9472 (prev. 6.9101)

Fixed Income

- Bonds chop and churn after extending recovery gains to new w-t-d highs on Thursday.

- Bunds pivot 136.50 and 2.25% yield, Gilt veer towards base of 101.14-68 range and T-note hovers just under 116-00 within 116-07/115-28 confines ahead of more Central Bank speakers, US import/export prices and UoM sentiment

Commodities

- Crude benchmarks are flat after spending the morning slightly softer and only picking up incrementally most recently with no fresh driver behind the move at the time and action overall in familiar ranges.

- Iraqi oil minister says Iraq didn’t get a reply from Turkish Botas on the request to resume oil flow, expects Northern Oil exports to restart on Saturday with pumping of 500,000 barrels per day.

- Spot gold resides around this week’s lows, and just above the USD 2,000/oz level following yesterday’s advances in the Dollar index, whilst fresh macro new flows remain light; base metals mixed, overall.

- Turkish Defence Minister says parties to the Black Sea grain deal are approaching an agreement on an extension. Subsequently, Russian Kremlin says nothing new to report, for now, after Black Sea grain deal talks in Istanbul; potential conversation with Turkey’s Erdogan and Russia’s Putin won’t help achieve a deal.

Geopolitics

- China’s foreign ministry says China representative of Eurasian affairs to visit Ukraine, Poland, France, Germany and Russia from May 15th to promote peace.

- Israeli PM Netanyahu will hold a security consultation session shortly with senior security chiefs, according to Al Jazeera.

- From the EU-China strategy paper, WSJ’s Norman highlights that “EU-China relations will not develop if China does not push Russia to withdraw from Ukraine…”

US Event Calendar

- 08:30: April Import Price Index YoY, est. -4.8%, prior -4.6%; MoM, est. 0.3%, prior -0.6%

- April Export Price Index YoY, est. -5.5%, prior -4.8%; MoM, est. 0.2%, prior -0.3%

- 10:00: May U. of Mich. Expectations, est. 60.8, prior 60.5

- May U. of Mich. Sentiment, est. 63.0, prior 63.5

- May U. of Mich. Current Conditions, est. 67.5, prior 68.2

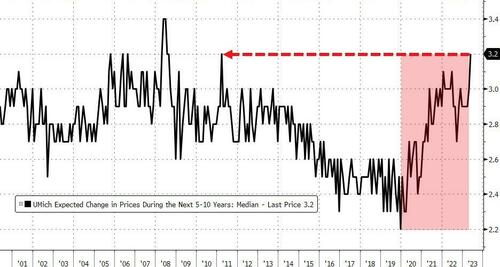

- May U. of Mich. 1 Yr Inflation, est. 4.4%, prior 4.6%

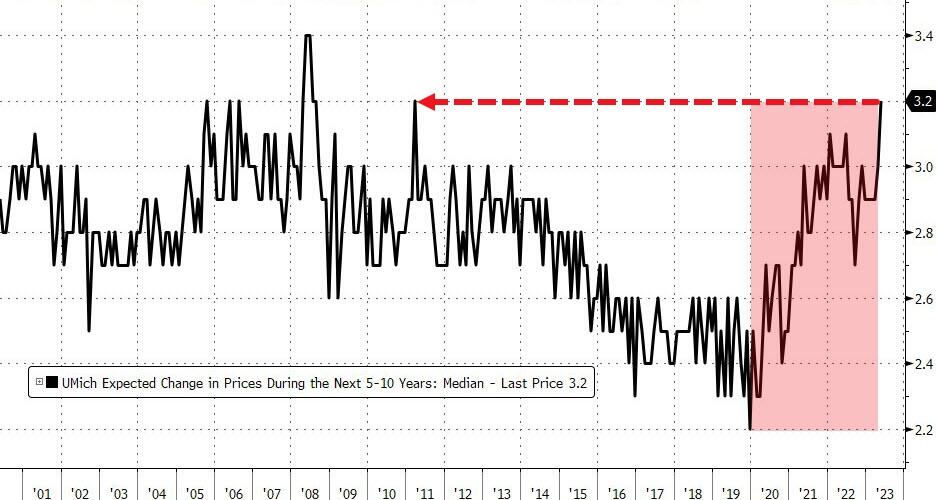

- May U. of Mich. 5-10 Yr Inflation, est. 2.9%, prior 3.0%

- 14:20: Fed’s Daly Gives Commencement Speech

- 19:45: Fed’s Bullard and Jefferson Take Part in Panel Discussion

DB’s Jim Reid concludes the overnight wrap

Today is an important one, since at lunchtime I have a slot to purchase tickets for the Paris Olympics in 2024. I honestly don’t know what will still be available by the time I’m allowed to log on, but last night my wife and I held a strategy meeting to decide what to aim for. First choice is the 100m final, followed by other nights of athletics. Other events were then suggested, but if they’re also taken we’re then into the danger zone where I’ve been instructed to use ‘common sense’ among the alternatives. I can only hope we’re still on speaking terms by this evening. Check back with me this time next year to find out my new favorite sport.

Markets failed to race away yesterday, as renewed fears of a slowdown led to a decent risk-off move, with investors growing concerned about weak data releases, the US debt ceiling, as well as the ongoing situation with regional banks. That meant the S&P 500 (-0.17%) lost ground, whilst sovereign bonds benefited from the flight to safety as speculation mounted about central bank rate cuts in response. These moves were evident across several asset classes, and the jitters also saw the US Dollar Index (+0.58%) record its best daily performance in six weeks.

Starting with the data, there was disappointment in the US from the weekly initial jobless claims, which came in at 264k (vs. 245k expected) in the week ending May 6. That’s their highest level since October 2021, and whilst we should add the usual caveats about not over-interpreting a single data point, it’s worth noting that claims have been on a broadly upward trend since late January. So that adds to the signs that the labour market has been softening in recent months, such as the decline in the number of job openings as well as the quits rate.

Alongside jobless claims, yesterday also saw the release of the US PPI release for April. That came in slightly beneath expectations, with headline PPI only up by a monthly +0.2% (vs. +0.3% expected), which took the annual measure down to +2.3% (vs. +2.5% expected). That added to the sense from the previous day’s CPI release that inflation might durably be heading lower, which could support a pivot towards rate cuts later in the year.

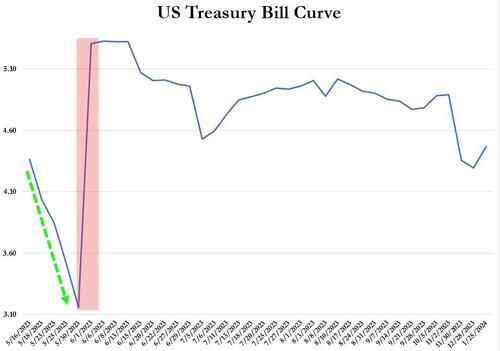

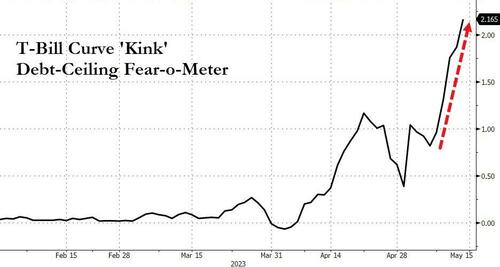

Those data releases supported a sovereign bond rally yesterday, with yields on 10yr Treasuries down -5.8bps to 3.375%. The 1m T-bill yield was just lower than unchanged at -0.08bps at 5.450%, but intraday the rate rose as high as 5.48% at one point and continues to see a good deal of intraday volatility. That maturity is exposed to potential debt ceiling default risk, which demonstrates how investors are positioning in case there are issues ahead. In terms of the latest on the debt ceiling, last night it was announced that President Biden and congressional leaders had postponed their planned meeting today until early next week. According to a Bloomberg report last night, the delay was due to conversations on government spending and energy permit reform gaining traction, so at first glance it signals that progress is being made. Our credit team put out a note yesterday (link here) that outlines the potential impact the debt ceiling can have on credit market and our spread forecast.

For equities, the generally downbeat newsflow meant that the major indices lost ground, with the S&P 500 ending the session -0.17% lower. The main outperformer were the megacap tech stocks, which benefited from the prospect of lower interest rates. In fact, the FANG+ index advanced another +0.90% to a fresh one-year high, which brings its YTD gains to a sizeable +44.52% already. On the other hand, banks continued to struggle and the KBW Banks Index fell a further -1.25%, closing less than 2% above its low from last week.

Here in the UK, the focus was on the Bank of England yesterday, who announced another 25bp hike that took Bank Rate up to a post-2008 high of 4.5%. Seven of the nine committee members voted for the move, and the minutes said that for those members, “there had been repeated surprises about the resilience of demand, while the labour market had remained tight.” There were also significant upward revisions to the BoE’s growth projections, and unlike in February they are no longer forecasting a recession. Nevertheless, growth was still expected to be weak by historic standards, at just ¼% in 2023, and then ¾% in 2024 and 2025. Looking forward, our UK economist writes in his recap note (link here) that another hike in June is more likely than not. That’s in line with current market expectations, and this morning investors are pricing in a 78% chance of a 25bp hike in June.

Staying on central banks, there was an interesting release yesterday as the ECB published their Consumer Expectations Survey for March. That showed inflation expectations were moving higher again after their recent decline, with the 1yr expectation up to +5.0%, and the 3yr expectation up to +2.9%. We also heard from Bundesbank President Nagel, who held the door open to the prospect that the ECB might still be hiking in September, by saying that “there’s nothing off the table” for that meeting. And President Lagarde herself reiterated that the ECB’s fight against inflation “is not over”. Despite of the hawkish tones from ECB officials however, European markets traded in line with the US for the most part, with yields on 10yr bunds (-6.3bps) coming down, and the STOXX 600 closing unchanged. See our German economists’ latest chartbook as well yesterday for more on the economic situation there (link here).

Overnight in Asia, equities have put in a mixed performance this morning amidst competing signals on the state of the global economy. On the one hand, the CSI (-0.59%), the Shanghai Composite (-0.39%), the KOSPI (-0.32%) and the Hang Seng (-0.13%) are trading lower. However, the Nikkei (+0.86%) has posted a decent advance that’s taken the index to its highest level since November 2021. One factor helping to support sentiment has been the meeting between US National Security Adviser Jake Sullivan and China’s top diplomat Wang Yi in Vienna. That was seen as a positive sign that the two sides were trying to ease tensions, and US-listed Chinese stocks on the NASDAQ Golden Dragon China Index (+3.82%) saw their biggest advance in three months yesterday. Looking forward, US equity futures are also in positive territory, with those on the S&P 500 (+0.20%) and NASDAQ 100 (+0.30%) pointing higher.

Since this is the last edition before the weekend, one thing to keep an eye on will be the Turkish election that’s taking place on Sunday. Our EM strategists have published a comprehensive preview of the election (link here), where they examine the process, along with what it could mean for the economy, markets, monetary policy and geopolitics. Yesterday saw some further developments in the contest, with presidential candidate Muharrem İnce withdrawing from the election.

Finally, another thing we’ve been watching out for is the prospect of an El Niño this year, which is a warming of sea surface temperatures in the eastern pacific, and is unfortunately correlated with a higher frequency of natural disasters like flooding. Yesterday saw the latest monthly update in the US National Weather Service’s forecast, which now sees a more than 90% chance of an El Niño occurring this winter, as well as a 54% chance of that it will be a strong El Niño (up from 41% last month). If there is an El Niño, then that could have important effects on food prices, as well as many emerging-market economies that would be most impacted by potential changes in weather patterns.

To the day ahead now, and data releases include the UK GDP reading for Q1, along with the University of Michigan’s preliminary consumer sentiment index for May. Otherwise, central bank speakers include ECB Vice President de Guindos, BoE Chief Economist Pill and the Fed’s Daly, Bullard and Jefferson.

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

Sentiment steady with drivers limited, DXY underpinned post-Bowman – Newsquawk US Market Open

FRIDAY, MAY 12, 2023 – 06:35 AM

- European bourses are firmer though the region is set to end the week where it began, US futures modestly bid.