MAY 19//DEMOCRATS WALK AWAY FROM THE DEBT CEILING DEBATE AND THAT CAUSES OUR PRECIOUS METALS TO ZOOM POST T.A.S. MANIPULATION: GOLD CLOSED UP $22.20 TO $1979.70//SILVER CLOSED UP 38 CENTS TO $23.89//PLATINUM CLOSED UP $18.15 TO $1071.20//PALLADIUM CLOSED UP $52.00 TO $1515.80//AS PER GOLD AND SILVER, THE VIDEO OF ANDREW MAGUIRE DISCUSSING THE FED’S PREDICIMENT IS A MUST VIEW//ALSO ALASDAIR MACLEOD’S ESSENTIAL READING THIS WEEKEND//COVID UPDATES//DR PAUL ALEXANDER/DR PANDA/VACCINE IMPACT//SLAY NEWS/EVOL NEWS//UKRAINE VS RUSSIA VS USA UPDATES HIGHLIGHTED BY THE USA TO ALLOW F 16’S TO BE SENT TO UKRAINE////UK’S ROYAL MAIL LOSES ONE BILLION POUNDS THIS YEAR!!//USA DATA: 90 MILLION AMERICANS STRUGGLE PAYING THEIR BILLS//REPORT ON THE USA CRE CRISIS//FOOTLOCKER WARNS//SWAMP STORIES FOR YOU TONIGHT..

118 C MACQUARIE FUT 7 363 H WELLS FARGO SEC 5 661 C JP MORGAN 3 737 C ADVANTAGE 1 1 800 C MAREX SPEC 1 880 H CITIGROUP 6 905 C ADM 2

TOTAL: 13 13

JPMorgan stopped 3/13 contracts

FOR MAY:

GOLD: NUMBER OF NOTICES FILED FOR MAY/2023. CONTRACT: 13 NOTICES FOR 1300 OZ or 0.0404 TONNES

total notices so far: 5931 contracts for 593,100 oz (18.4479 tonnes)

FOR MAY:

SILVER NOTICES: 29 NOTICE(S) FILED FOR 145,000 OZ/

total number of notices filed so far this month : 2442 for 12,210,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $22.20..

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/NO CHANGES IN GOLD INVENTORY AT THE GLD:///

INVENTORY RESTS AT 936.96 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 38 CENTS AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV: /; : INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 468.529 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A FAIR SIZED 630 CONTRACTS TO 138,674 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS FAIR SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.23 FALL IN SILVER PRICING AT THE COMEX ON THURSDAY. THIS AGAIN HAS ALL THE HALLMARKS OF TRADE AT SETTLEMENT (TAS) MANIPULATION WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS IN FULL FORCE DURING MID CYCLE IN THE DELIVERY MONTH. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY: A STRONG 503 CONTRACTS. THE CROOKS LIQUIDATED MOST LIKELY THE REMAINDER OF THE SHORT END OF THE SPREAD TRADE MANIPULATING THE PRICE OF SILVER SOUTHBOUND.

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.23). AND WERE SUCCESSFUL IN KNOCKING SOME SPEC LONGS AS WE HAD A SMALL LOSS ON OUR TWO EXCHANGES OF 269 CONTRACTS ( MOST OF THIS LOSS WITH HIGH PROBABILITY WAS DUE TO TAS LIQUIDATION). WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 4.250MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH (TAS), AND FINAL WEEK (COMEX SPREADERS).

WE MUST HAVE HAD:

A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS( 361 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.105 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP OF 65,000 OZ (QUEUE JUMP RAISES THE AMOUNT OF SILVER STANDING)+0 EXCHANGE FOR RISK// TOTAL 4.25MILLION OZ OF EXCHANGE FOR RISK FOR THE MONTH(RAISES THE AMOUNT OF SILVER STANDING):THUS TOTAL OF 17.250 MILLION OZ OF STANDING FOR DELIVERY V) FAIR SIZED COMEX OI LOSS/ FAIR SIZED EFP ISSUANCE/VI) LARGE NUMBER OF SHORT T.A.S. CONTRACT LIQUIDATION MANIPULATING THE PRICE DOWN.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -removed 149CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTRACTS for 15 days, total 10,300 contracts: OR 51.500 MILLION OZ . (687 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 51.500 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 51.50 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

RESULT: WE HAD A FAIR SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 630CONTRACTS WITH OUR $0.23 LOSS IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE CONTRACTS: 361 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAY OF 13.105 MILLION OZ//FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 65,000 OZ (INCREASES THE AMOUNT OF SILVER STANDING) +// + 0.0 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //TOTAL EXCHANGE FOR RISK MONTH= 4.25 MILLION//NEW TOTALS 13.000 MILLION OZ + 4.25 MILLION = 17.250 MILLION OZ// .. WE HAVE A SMALL SIZED LOSS OF120 OI CONTRACTS ON THE TWO EXCHANGES AS WE HAD FINALIZATION OF TAS LIQUIDATION. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG 503!!

WE HAD 29 NOTICE(S) FILED TODAY FOR 145,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A VERY STRONG SIZED 11,345 CONTRACTS TO 488,839 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -928 CONTRACTS

WE HAD A VERY STRONG SIZED DECREASE IN COMEX OI ( 11,345 CONTRACTS) WITH OUR $23.80 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR MAY. AT 3.5085 TONNES ON FIRST DAY NOTICE // PLUS 700 OZ QUEUE JUMP :(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)/+ /A HUGE ISSUANCE OF 1870 T.A.S. CONTRACTS//CONSIDERABLE (AND DEFINITELY FINAL) LIQUIDATION OF TAS TODAY////YET ALL OF..THIS HAPPENED WITH OUR HUGE $23.80 LOSS IN PRICEWITH RESPECT TO THURSDAY’S TRADING.WE HAD A GOOD SIZED LOSS OF 7349 OI CONTRACTS (22.85 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3996 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 487,911

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7349 CONTRACTS WITH 11,345 CONTRACTS DECREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): 1870 CONTRACTS) AND 3996 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 7349CONTRACTS OR 22.85TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3996 CONTRACTS) ACCOMPANYING THE LARGE SIZED LOSS IN COMEX OI (11,345) //TOTAL LOSS IN THE TWO EXCHANGES 7,349 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 3.5085 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 700 OZ // NEW STANDING: 18.790 TONNES // ///3) SOME LONG LIQUIDATION//4) STRONG SIZED COMEX OPEN INTEREST LOSS/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: T.A.S. ISSUANCE: 1870 CONTRACTS (AFTER WHICH THEY FINALIZED LIQUIDATION OF THE REMAINDER OF MAY’S T.A.S. CONTRACTS.)

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 46,444 CONTRACTS OR 4,644,400 OZ OR 144.46 TONNES IN 15 TRADING DAY(S) AND THUS AVERAGING: 3093 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAY(S) IN TONNES 144.46 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 144.46/3550 x 100% TONNES 4.08% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES ( MUCH SMALLER THAN LAST MONTH)

MAY: 144.46 TONNES (HEADING FOR ANOTHER SMALLER MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A STRONG SIZED 630 CONTRACTS OI TO 138,674 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 361 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 361 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 361 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 630CONTRACTS AND ADD TO THE 361OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 269 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 1.345 MILLION OZ

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED DOWN 13.78 PTS OR 0.42% //Hang Seng CLOSED DOWN 276.68 POINTS OR 1.40% /The Nikkei closed UP 234.42 OR 0.77% //Australia’s all ordinaries CLOSED UP 0.60 % /Chinese yuan (ONSHORE) closed UP 7.0137 /OFFSHORE CHINESE YUAN UP TO 7.0267 /Oil UP TO 72.77 dollars per barrel for WTI and BRENT AT 76.78 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 11,345 CONTRACTS DOWN TO 488,674 WITH OUR LOSS IN PRICE OF $23.80 ON THURSDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF MAY… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3996 EFP CONTRACTS WERE ISSUED: : JUNE 3996 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3996 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 7,349 CONTRACTS IN THAT 3996LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 11,345COMEX CONTRACTS..AND THIS GOOD SIZED LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $23.80. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE),THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE THIS MORNING WAS A STRONG 1870 CONTRACTS. THE SHORT SIDE WAS LIQUIDATED TUESDAY, WEDNESDAY, THURSDAY AND AGAIN TODAY WHICH OF COURSE MANIPULATED THE PRICE OF GOLD SOUTHBOUND. (THE LONG SIDE OF THE EQUATION WILL BE LIQUIDATED TWO MONTHS HENCE)

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (18.790) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 18.790 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $23.80) //// AND WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD OUR GOOD SIZED LOSS OF 7349 CONTRACTS ON OUR TWO EXCHANGES BUT I SUSPECT THAT MOST OF THAT LOSS WAS DUE TO FINALIZATION OF LIQUIDATION WITH RESPECT TO THE TAS CONTRACTS.

WE HAVE LOST A TOTAL OI OF 22.85PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY. (3.5085 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 700 oz (0.0217 TONNES)//NEW STANDING 18.790 TONNES ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $23.80

WE HAD +REMOVED 928 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 7349 CONTRACTS OR 734,900 OZ OR 22.85 TONNES.

Total monthly oz gold served (contracts) so far this month

5931 notices 593,100 OZ 18.4479 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: NIL oz

customer withdrawals: 4

i) Out of Brinks 292.920 oz

ii) Out of JPMorgan 5632.723 oz

iii) Out of Manfra: 6076.539 oz (189 kilobars)

total withdrawals: 12,002.182 oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 123 contracts having LOST 38 contracts. We had 45 contracts filed

on THURSDAY, so we GAINED 7 contracts or an additional 700 oz (0.02177 tonnes) will stand for gold in this non active delivery month of May

June LOST A HUGE 17,582 contracts DOWN to 186,811 contracts. (FROM WHICH A CONSIDERABLE AMOUNT WAS DUE TO TAS FINAL LIQUIDATION)

July added 26 contracts to stand at 1890 contracts.

AUGUST GAINED 5449 contracts UP to 243,876 contracts

We had 13 contracts filed for today representing 1300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 9 notices were issued from their client or customer account. The total of all issuance by all participants equate to 13 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 3 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2023. contract month,

we take the total number of notices filed so far for the month (5,931 x 100 oz ), to which we add the difference between the open interest for the front month of MAY (123 CONTRACTS) minus the number of notices served upon today 13 x 100 oz per contract equals 604,100 OZ OR 18.790 TONNES the number of TONNES standing in this NON- active month of May.

thus the INITIAL standings for gold for the MAYcontract month: No of notices filed so far (5,931 x 100 oz) x 123 OI for the front month minus the number of notices served upon today (13)x 100 oz} which equals 603,400 oz standing OR 18.768 TONNES

TOTAL COMEX GOLD STANDING: 18.790 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,580,639.231 OZ

TOTAL REGISTERED GOLD: 12,396,482.120 (385,58 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,196,159.289 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,699,919 OZ (REG GOLD- PLEDGED GOLD) 332.81 tonnes//

END

SILVER/COMEX

MAY 19//2023// THE MAY 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

524,506.399 oz Brinks CNT Manfra

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

598,898.300 oz JPMorgan

No of oz served today (contracts)

29 CONTRACT(S) (145,000 OZ)

No of oz to be served (notices)

158 contracts (790,000 oz)

Total monthly oz silver served (contracts)

2442 Contracts (12,210,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposits: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) Into JPMorgan: 598,898.300 oz

Total deposits: 598,898.300 oz

JPMorgan has a total silver weight: 141.925 million oz/274.195 million =51.71% of comex .//dropping fast

Comex withdrawals 3

i) Out of Brinks: 1904.900 oz

ii) Out of CNT: 312,756.310 oz

iii) Out of Manfra 209,845.189 oz

Total withdrawal: 524,506.399 oz

adjustments: 0

TOTAL REGISTERED SILVER: 30.933 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 274.195 million oz

CALCULATION OF SILVER OZ STANDING FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2023 OI: 187 CONTRACTS HAVING LOST 237 CONTRACT(S). WE HAD 250 CONTRACTS FILED ON THURSDAY, SO WE GAINED 13 CONTRACTS OR AN ADDITIONAL 65,000 OZ WILL STAND FOR DELIVERY ON THIS SIDE OF THE POND

JUNE HAD A 45 CONTRACT GAIN TO 1118

JULY HAD A 880 CONTRACT LOSS TO 113,675 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 29 for 145,000 oz

Comex volumes// est. volume today 55,075 fair

Comex volume: confirmed yesterday: 50,049 fair

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 2442 x 5,000 oz = 12,210,000 oz

to which we add the difference between the open interest for the front month of MAY(187) and the number of notices served upon today 29 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2023 contract month: 2442 (notices served so far) x 5000 oz + OI for the front month of May (187) – number of notices served upon today (29 )x 500 oz of silver standing for the MAY contract month equates to 13.000 million oz + THE CRIMINAL 0 MILLION OZ EXCHANGE FOR RISK TODAY//NEW TOTAL EXCHANGE FOR RISK: 4.250//NEW TOTAL 17.250 MILLION OZ//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

MAY 9/WITH GOLD UP $9.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTER DEPOSIT OF 5.88 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 937.64 TONNES

MAY 8/WITH GOLD UP $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 931.77 TONNES

MAY 5/WITH GOLD DOWN $30.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AS DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

MAY 4/WITH GOLD UP $19.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.30 TONNES

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

GLD INVENTORY: 936.96 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

MAY 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A TINY DEPOSIT OF .08 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 465.682 MILLION OZ//

MAY 8/WITH SILVER DOWN 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.602 MILLION OZ//

MAY 5/WITH SILVER DOWN 31 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 466.876 MILLION OZ//

MAY 4/WITH SILVER UP 53 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF .174 MILLION OZ INTO SLV.//INVENTORY RESTS AT 467.174 MILLION OZ//

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

3,Chris Powell of GATA provides to us very important physical commentaries

Alasdair Macleod: Now we’re all working for the state

Your weekend reading material:

Alasdair Macleod….

Submitted by admin on Thu, 2023-05-18 13:09Section: Daily Dispatches

By Alasdair Macleod GoldMoney, Toronto Thursday, May 18, 2023

A consequence of increasing economic intervention by the state is that we are now expected to breed more taxpayers in future and draw down on our state pensions for less time. Our productivity must be improved as well, thereby maximising our state’s tax revenues.

With respect to the democratic process, is this really what we have signed up for? It is hardly surprising that we are losing individual freedom. We are now working for the state, instead of the state working for us.

This role inversion is the logical outcome of turning our backs on free markets and ceding a role to the state in the management of our personal and economic affairs. And it is further justified by statistical analysis that supports the role of the state, but on examination turns out to be thoroughly misleading.

In this article, I comment on the economics of population growth as discussed by mainstream economists, show how we are being badly misled by productivity statistics, and by the true value of GDP which is to enable the state to estimate future tax revenue.

But the states’ habitual predation on their private sectors is coming to an end, because it will become impossible to finance. The end of the long-term trend of falling interest rates will see to that. …

In this week’s Live from the Vault, Andrew Maguire brings us up to date on the escalating battle between physical and paper gold, the current price dip, and how the trapped Federal Reserve might be able to get out of its predicament. …

END

5.IMPORTANT COMMENTARIES ON COMMODITIES: DIAMONDS

Slowdown in diamonds and other luxury goods throughout the world

(zerohedge)

World’s Top Polishing Diamond Hub Warns “Difficult Year” Ahead On Weak US, China Demand

FRIDAY, MAY 19, 2023 – 02:45 AM

Another sign of a possible consumer downturn is unfolding in India, recognized as the world’s top polishing gem hub. The country is bracing for a challenging year as diamond demand from key markets in North America and Asia is expected to soften.

For the fiscal year ending in March, India reported a 10% drop in cut and polished diamond exports to $22 billion, driven primarily by inconsistent Russian rough-diamond supplies and waning demand in the US and China, according to Bloomberg, citing a new report from Gem & Jewellery Export Promotion Council.

On Wednesday, Vipul Shah, chairman of the state-backed industry group, spoke with Bloomberg TV about the souring diamond demand in top global markets:

“It is going to be a difficult year,” Shah said. Elevated inflationary pressures in the US, China’s slower-than-expected recovery after pandemic restrictions lifted, and volatile gold prices will make it “tough and challenging” for Indian diamond merchants, he noted.

“Supply is also one of the constraints,” while factories in the key hub of Surat, Gujarat state, have been slow in building inventories, with working shifts staggered in light of the weak demand, Shah said.

India, which considers Moscow a close political and trade partner, imports oil, weapons, and commodities from Russia despite the threat of sanctions due to the war in Ukraine. Shah’s group is in talks with the Indian government to resolve a payment issue with regard to procuring rough-gem supplies from Russia, he said. Still, the industry’s biggest challenge was waiting for “the US economy to pick up, consumer demand to pick up,” Shah said. –Bloomberg

Another sign that consumers in the world’s largest economy might be under pressure is a report last month from French luxury group LVMH which pointed out a “bit of a slowdown” in luxury spending in the first quarter.

The luxury spending slowdown comes as the seemingly invincible US consumer starts to break, first at the low end (as we explained two months ago in “First Signs Of A Notable Low-Income Slowdown“) and now at the top.

Now according to the most recent debit and credit card data published by the Bank of America Institute, the recent higher-income job market slowdown is also starting to impact spending. Yes: the upper-income cohort is finally starting to crack too.

And what are some of the first things consumers dial back spending as macroeconomic headwinds mount? Well, it’s jewelry and other forms of luxury spending.

END

end

5 B GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS// FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.0137

OFFSHORE YUAN: 7.0267

SHANGHAI CLOSED DOWN 13.78 PTS OR 0.42%

HANG SENG CLOSED DOWN 276.68 PTS OR 1.40%

2. Nikkei closed UP 234.62 PTS OR 0.77%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 103.16 EURO RISES TO 1.0798 UP 23 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.401 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 138.42 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.480***/Italian 10 Yr bond yield RISES to 4.357*** /SPAIN 10 YR BOND YIELD RISES TO 3.538…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 40.034

3j Gold at $1963.50 silver at: 23.58 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 15 /100 roubles/dollar; ROUBLE AT 80.07//

3m oil into the 72 dollar handle for WTI and 76 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 138.43 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .401% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9002 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9743 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.666 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 3.906 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.2637 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.81…

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.006 UP 11 BASIS PTS

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Rise After Breaking Out To New 2023 Highs Ahead Of Powell Speech

FRIDAY, MAY 19, 2023 – 08:06 AM

After breaking out to new 2023 highs, US equity futures are up small (on “debt talk progress” even though there has been zero actual debt talk progress) ahead of Powell’s speech today, trading in a narrow 10 points. As of 730am ET, S&P futures are up 0.2% to 4,220 while Nasdaq futures are up 0.1%. European stocks are up 0.8%m near session highs with Germany’s DAX set for a record close for the first time since January 2022 while the Nikkei 225 closed at a 33-year peak, as momentum carried over from Wall Street. Bond yields reversed earlier losses and hit session highs around 3.65% while dollars are weaker. Pre-market, megacap tech, where we just saw the biggest call buying since 2014, continues to drive higher amid yesterday’s rally. Commodities are mixed: oil is set to close its best week since mid-April while base metals are lagging. Macro calendar is quiet today with the major focus on Powell’s speech at a panel at 11am ET (Fed) where former chair Ben Bernanke will also be present. Keep an eye on the key 4200 level today.

In premarket trading, Applied Materials shares edged lower, down 1.7% trading, after the semiconductor-capital equipment company said sales will drop in the third quarter as the memory- chip slump weighs on its business. However, analysts noted that strength in its IoT, Communications, Automotive, Power and Sensors (ICAPS) business might offset some of the weakness in the memory segment. Here are some other notable premarket movers:

PacWest shares rose 3.8% in premarket trading Friday, set for a third day of gains amid an ongoing relief rally for US regional banks. PacWest has already gained 28% this week, and is set for the best weekly gain since June 2020.

Farfetch shares surge as much as 21% in premarket trading, poised for their biggest jump since November, after the specialty online retailer’s first-quarter results beat expectations on back of growing sales volumes in the US and China. Analysts expect further improvement in 2H, as business in China ramps up and FX headwinds ease.

As discussed extensively in recent days, much of the recent optimism appears to be some unfounded hope that a debt ceiling deal will get done ahead of a market freakout just because algos believe the jawboning from politicians. In a call early Friday from Japan, President Joe Biden told his negotiating team that he’s confident Congress will act in time to avoid a default (he won’t), according to a White House official. House Speaker Kevin McCarthy and Senate Majority Leader Chuck Schumer are making plans for votes in the coming days on a bipartisan deal (there won’t be a deal).

“Growing optimism for a resolution to the debt ceiling negotiations has lifted sentiment, although the mood was slightly tempered by question marks over the Federal Reserve’s next move on interest rates,” said Richard Hunter, head of markets at Interactive Investor.

Meanwhile, treasuries recouped some losses from a selloff on mounting doubts the Federal Reserve will pause its credit tightening campaign next month.

European stocks rally for a second day with the German DAX on course for a record close as the mood around the US debt ceiling negotiations continues to improve. The Stoxx 600 is up 0.8%, its largest gain in two weeks, with financial services, miners and tech the strongest-performing sectors. Here are some of the most notable European movers:

Allegro gain as much as 5.7% after Poland’s largest e-commerce platform said it would increase merchants’ co-financing of delivery costs and introduce commissions on pay buy-now-pay- later

Smiths Group rises as much as 1.9% after an earnings update from the UK engineer. Jefferies (buy) says the top-line guidance upgrade will likely be well-received by investors

1&1 shares jump as Deutsche Bank raises the German telecom operator to buy from hold, seeing room for the stock to go higher whether or not it opts to abandon its 5G network buildout

SBB shares fall as much as 7.7% to the lowest in more than five years, after Goldman Sachs halved its price target on the beleaguered Swedish landlord and reiterated its sell recommendation

Novartis shares fall as much as 2% after JPMorgan opened a negative catalyst watch on the Swiss pharma group ahead of the company’s presentation of data from its NATALEE breast cancer trial

Burberry shares fall as much as 3.2%, extending Thursday’s 5.2% drop that followed the publication of the British luxury- goods company’s FY results. Berenberg says the guidance was “not enough”

C&C slumps as much as 18% after the cider maker issued a profit warning, citing “significant challenges” in relation to implementing a complex system upgrade in two of its UK businesses

CEZ falls as much as 5.8% after the Czech government took legislative steps that would allow the it to overhaul the power utility without minority investors’ consent

Earlier in the session, Asian stocks were mostly higher following the tech-led gains on Wall Street, although Chinese markets lagged and were the outlier to Friday’s risk-on mood amid disappointment from Alibaba’s revenue miss. The Hang Seng Tech Index slumped as much as 2.4% as Alibaba Group Holding Ltd dropped in the wake of disappointing sales. India stocks snapped a three-day losing streak as banks and Adani Group stocks surged late in the session. The S&P BSE Sensex rose 0.5% to 61,729.68 in Mumbai, while the NSE Nifty 50 Index advanced 0.4% to 18,203.40. The MSCI Asia-Pacific index climbed 0.3% for the day. Adani Group stocks rallied led by flagship Adani Enterprises’ 3.5% surge after a Supreme Court-appointed panel in a report said it found no conclusive evidence to suggest a stock price manipulation in the group’s stocks. Infosys contributed the most to the Sensex’s gain, increasing 1.8%. Out of 30 shares in the Sensex index, 22 rose and 8 fell.

In FX, the Bloomberg Dollar Spot Index is down 0.2% having lost ground versus all its G-10 rivals. The New Zealand dollar is the best performer followed by the Norwegian krone.

In rates, treasuries initially rose for the first time this week with the US 10-year yield dropping 2bps to 3.62% before the entire move reversed and yields resumed their grind higher; the 10Y was last trading at 3.66% with bunds and gilts are little changed.

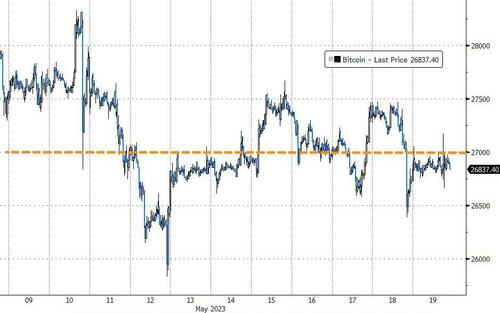

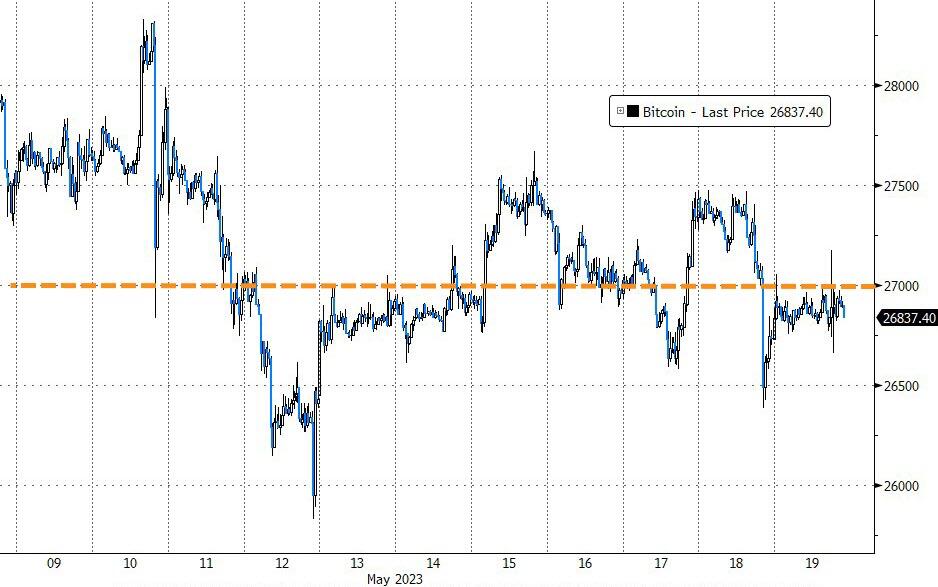

In commodities, crude futures advance with WTI rising 0.8% to trade near $72.40. Spot gold adds 0.4% to $1,965. Bitcoin gains 0.5%

Bitcoin is modestly firmer and despite eclipsing the USD 27k mark as the USD comes under Yuan-driven pressure this morning, BTC thus far has been unable to hold onto the level and is now holding just below it.

To the day ahead now, and the highlights will include remarks from Fed Chair Powell and ECB President Lagarde. Other central bank speakers include the Fed’s Williams and Bowman, the ECB’s Schnabel and De Cos, along with the BoE’s Haskel. Data releases include German PPI for April. Finally, G7 leaders are currently meeting in Japan.

Market Snapshot

S&P 500 futures up 0.2% to 4,219.50

MXAP up 0.3% to 162.24

MXAPJ up 0.2% to 513.46

Nikkei up 0.8% to 30,808.35

Topix up 0.2% to 2,161.69

Hang Seng Index down 1.4% to 19,450.57

Shanghai Composite down 0.4% to 3,283.54

Sensex up 0.2% to 61,577.36

Australia S&P/ASX 200 up 0.6% to 7,279.52

Kospi up 0.9% to 2,537.79

STOXX Europe 600 up 0.6% to 468.70

German 10Y yield little changed at 2.45%

Euro up 0.2% to $1.0788

Brent Futures up 0.6% to $76.31/bbl

Gold spot up 0.5% to $1,967.13

U.S. Dollar Index down 0.23% to 103.35

Top Overnight News

Europe’s largest asset manager, Amundi, is shifting assets to China from the US as it feels the former market has become too cheap to ignore and has superior economic prospects. FT

China’s crackdown on overseas firms has made clear that leader Xi Jinping values security over economic growth. To eradicate any doubt, according to people familiar with the matter, he has put state-security czar Chen Yixin in charge. The campaign, which has included raids on Chinese offices of U.S. due-diligence firms and questioning of staff at the Bain consulting firm, is sending shock waves across global businesses. WSJ

BOJ Governor Kazuo Ueda said on Friday the central bank will patiently maintain its ultra-loose monetary policy given “very high” uncertainty over the economic outlook. RTRS

The European Central Bank is stepping up scrutiny of lenders’ liquidity reserves and may communicate stricter requirements to individual firms later this year, according to people with knowledge of the matter. BBG

G7 countries are preparing new sanctions against Russia, covering ships, aircraft, individuals and diamonds, officials say, as they seek to increase economic pressure on the Kremlin’s war machine. FT

Germany’s PPI cools by more than anticipated in April, coming in at +4.1% Y/Y (down from +6.7% in Mar and below the Street’s +4.3% forecast). RTRS

House Speaker Kevin McCarthy and Senate Majority Leader Chuck Schumer are making plans for votes in the coming days on a bipartisan deal to avert a catastrophic US debt default. McCarthy said that negotiators on the federal debt limit may reach an agreement in principle as soon as this weekend, lining up a vote in his chamber. BBG

The White House is willing to make concessions on work requirements for certain federal aid programs, a breakthrough that could lead to an imminent debt ceiling deal. Politico

“Skip” is the new “pause.” Jerome Powell may shine some light on the murky rate path as the FOMC looks increasingly split on whether to pause next month or keep on hiking. A compromise would be a skip, where they put off an increase in June but return to it in July. Powell takes part in a panel discussion at a Fed conference today and there’ll be a Q&A. John Williams also speaks there. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly higher following the tech-led gains on Wall St where the Nasdaq outperformed and the S&P 500 printed a 9-month high on debt ceiling optimism and firm data, although Chinese markets lagged amid disappointment from Alibaba’s revenue miss. ASX 200 was lifted with the tech sector front-running the gains as it took inspiration from its US counterpart and with the top-weighted financial industry trailing closely behind. Nikkei 225 surged at the open to print its highest since August 1990 although pared some of the gains after losing steam on its approach to the 31,000 level and as participants digested the latest CPI figures which were mostly in line with expectations but showed a faster pace of acceleration. Hang Seng and Shanghai Comp. were mixed with the Hong Kong benchmark pressured as tech giants suffered following Alibaba’s earnings which beat on the bottom line but missed on revenue, while frictions lingered after the US and Taiwan reached an initial agreement on a ’21st Century’ trade pact and with China concerned about recent signs of negative China-related developments at the G7.

Top Asian News

Chinese President Xi said China proposed to establish meeting and dialogue mechanisms in cooperation between China and Central Asian countries in which the mechanisms will cover agriculture, transportation, emergency management, education and political party affairs, while Xi added that China will roll out more trade facilitation measures and upgrade bilateral investment agreements with Central Asian countries.

China’s Commerce Minister is to meet with US Commerce Secretary Raimondo and US Trade Representative Tai next week, according to Politico.

China’s Taiwan Affairs Office said it will allow travel agencies to resume group tours for Taiwan residents to the mainland from today, according to Reuters.

USTR office said US and Taiwan reached an initial agreement on a ’21st Century’ trade pact which covers customs and trade facilitation, good regulatory practices, services regulations, anti-corruption measures and SMEs. USTR added that further US-Taiwan negotiations will commence on additional trade areas including agriculture, digital trade, labour, environment and SOEs, according to Reuters.

China’s Major state-owned banks are reportedly seen swapping Yuan for Dollars in the onshore FX forwards market, according to currency traders cited by Reuters; One source said state banks have started heavily trading buy/sell 1yr tenor since Thursday. Subsequently, China is to curb speculations on Yuan rates when necessary, according to PBoC.

BoJ’s Ueda says the domestic economy is picking up, driver of the economic recovery is likely to shift from pent up demand to rising income/expenditure. Adds, it is appropriate to take time to decide on adjustments to monetary easing toward a future exit. “While there is an opposite risk that inflation will remain above 2 percent if a change in policy falls behind the curve, the cost of waiting for underlying inflation to rise until it can be judged that 2 percent inflation has fully taken hold is not as large as the cost of making hasty policy changes. In this sense, it is appropriate to take time to decide on adjustments to monetary easing toward a future exit.”

European bourses are in the green, Euro Stoxx 50 +0.8%, and are set to see the week out with upside of a similar magnitude. Thus far, fresh macro drivers have been limited the focus firmly on the Central Bank docket which features Lagarde & Schnabel from the ECB. Stateside, futures are flat/slightly firmer following as the debt ceiling sees tentative progress and participants switch their near-term focus to Fed speak/next week’s data; firstly, Fed’s Powell, Williams & Bowman are due today. Deere & Co (DE) Q1 2023 (USD): EPS 9.65 (exp. 8.59), Revenue 17.39bln (exp. 14.83bln). +2.5% in pre-market trade. Samsung Electronics (005930 KS) will not be swapping out default search engine on its smartphones from Google (GOOGL) to Microsoft’s (MSFT) Bing, via WSJ citing sources.

Top European News

UK plans GBP 1bln of semiconductor investment in a new strategy that aims to strengthen the domestic industry and chip supply chains, according to the government.

ECB is reportedly to increase scrutiny of bank liquidity and could lift requirements, via Bloomberg; could communicate such requirements later this year. Scrutiny into liquidity following on from US bank and Credit Suisse (CSGN SW) failures.

ECB’s Lagarde says we are heading towards more delicate policy decisions going forward; will be courageous to take the decisions needed to bring inflation back to the target.

Geopolitics

Ukrainian President Zelensky is to travel to Japan to attend the G7 Summit in person, according to Bloomberg.

US senior administration official said all G7 members are preparing to implement new Russian sanctions and export controls with the sanctions aimed at closing evasion loopholes and will target war inputs, energy reliance and access to financial systems. US is to target Russia with roughly 300 sanctions on individuals, entities, vessels and aircraft across Europe, the Middle East, and Asia. US sanctions will also target financial facilitators, Russia’s future energy and extraction capabilities, as well as others supporting Russia’s war, while G7 countries remain committed to upholding the price cap on Russian oil, according to Reuters.

US President Biden’s administration signalled to European allies in recent weeks that the US would allow them to export F-16 fighter jets to Ukraine, while Ukraine was said to have used a Patriot to shoot down at least one Russian fighter jet in recent weeks, according to CNN’s Bertrand.

EU”s President of the European Council Michel said they will restrict the sale of Russian diamonds and call on China to pressure Russia to stop military aggression, while he said stable and constructive cooperation with China is in their interests and that they need to engage with China on global challenges.

Commodities

Crude is firmer on the session and back towards yesterday’s best levels in what has been a choppy session for the complex despite a lack of specific drivers ahead of a busy US agenda and with attention on the G7.

Currently, WTI and Brent are posting upside of over USD 0.50/bbl in circa. USD 1.00/bbl parameters.

As the USD comes under pressure, metals are experiencing relatively broad based upside; specifically, spot gold is bid but remains shy of the week’s USD 2022/oz best with LME Copper similarly sub-8.3k.

Saudi’s Energy Minister said coordination with OPEC+ countries is a cornerstone of the efforts to enhance the stability of oil markets and maintain their balance, according to the state news agency.

Fixed Income

Bonds fade from best levels in dead cat fashion awaiting final Central Bank speakers of the week headlined by Fed Chair Powell and ECB President Lagarde.

Bunds back below par between 134.33-133.76 parameters, Gilts slipping to new intraday lows towards 98.50 vs 99.21 at best and T-note rooted towards base of 113-30/114-05 range.

Permanent TSB (SAB SM) says it has not seen a slowdown in demand for mortgages due to higher rates, not seeing stress in mortgage book. Note, this headline is potentially a factor behind the recent increase in benchmark pressure, which is seemingly being led by Gilts

FX

Buck backs off from fresh multi-week peaks awaiting potentially pivotal remarks from Fed Chair Powell, DXY back under 103.500 towards 103.21 trough after forming a virtual 103.620-630 double top.

Yen claws back losses vs Dollar from 138.72 to 137.98 amidst reports of pre-weekend long liquidation.

Yuan regains poise from deeper sub-7.0000 lows as Chinese state banks step in to curb the slide.

Kiwi bounces firmly on 0.6200 handle after NZ trade balances swings from deficit into surplus.

Aussie, Euro and Sterling all take advantage of Greenback retreat within 0.6617-63, 1.0761-1.0804 and 1.2393-1.2435 respective ranges.

PBoC set USD/CNY mid-point at 7.0356 vs exp. 7.0392 (prev. 6.9967)

US Event Calendar

Nothing scheduled

Central Bank Speakers

08:45: Fed’s Williams Speaks at Monetary Policy Conference

09:00: Fed’s Bowman Takes Part in Discussion at Bankers Convention

11:00: Fed Chair Powell, Former Chair Bernanke Speak on Policy Panel

DB’s Jim Reid concludes the overnight wrap

Earlier this week Henry and I published a chartbook entitled “A Time Capsule for the Future”. It imagines how those in the distant future might look at what the macro signals were telling us now in May 2023. The presentation is here and yesterday we hosted a webinar with around 500 people on, the replay of which will go out this morning to this list. I’ll also add the link to my CoTD later.

Talking of 500 people, tomorrow that number will be at a social event my wife has organised at our kid’s school. We’re having a 3 movie outdoor cinema afternoon/early evening shindig. Fortunately the weather looks clear. Our house currently has more popcorn in it than your local multiplex. Infact as I type this at 5am I can smell it which is a bit off putting. So if you’re running short in the weeks ahead you know where to come.

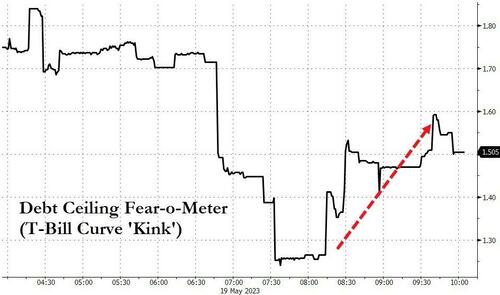

The movie of choice for markets in recent times has of course been the debt ceiling where events seem to be unfolding much quicker than anticipated. It was quite easy last week to suggest that the debt ceiling was having minimal negative impact on markets (outside of short-dated T-bills) but this week’s more positive sentiment on the topic has moved bond markets a lot and sent the S&P 500 and Nasdaq to highest levels since late-August, indicating that maybe more risk was priced in than we thought.

The latest driver were comments from Republican Speaker McCarthy, who said “I can see now where a deal can come together”, and that the negotiators were in a “much better place”. Furthermore, he even said he expected the House to consider a deal next week, with an “agreement in principle” possible this weekend. There was some hesitation from Financial Services Chairman McHenry in the afternoon that injected a degree of volatility into markets, but given McCarthy’s tone he seems to think he has enough GOP votes even with some dissenters. Clearly we’ll have to see how this develops and the content of what’s actually agreed, but this is a world away from where we were a week-and-a-half ago, when the two sides came out of their initial meeting with no public progress at all, and the route to a deal was much harder to envisage.

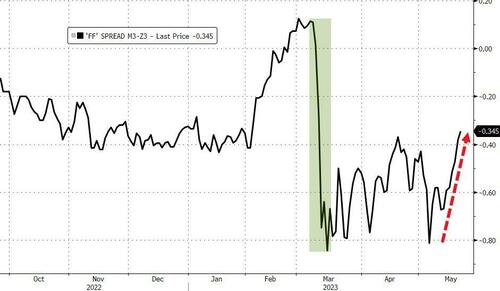

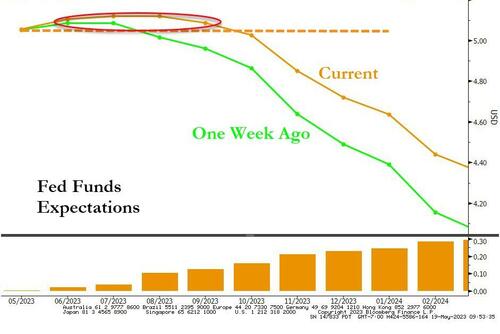

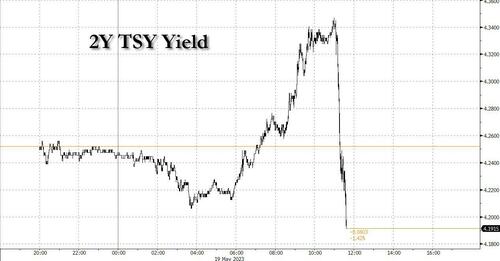

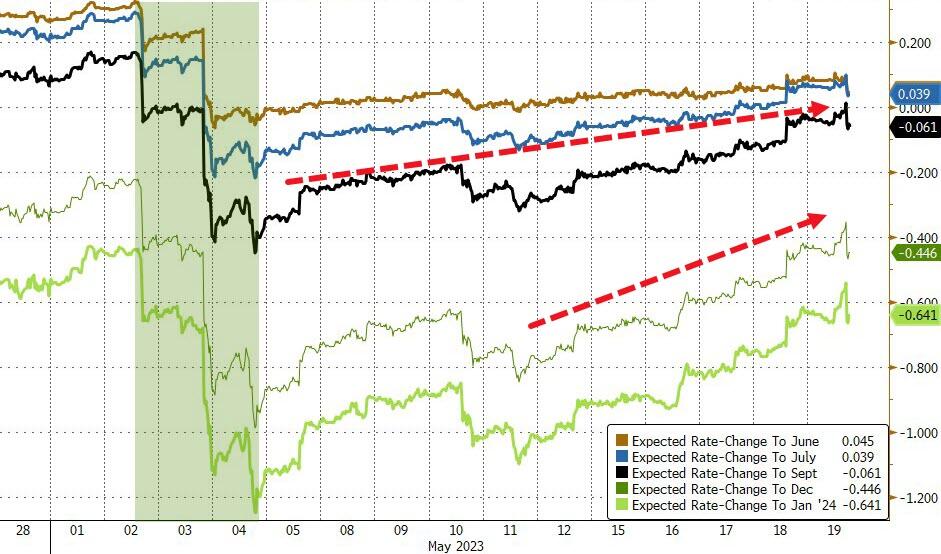

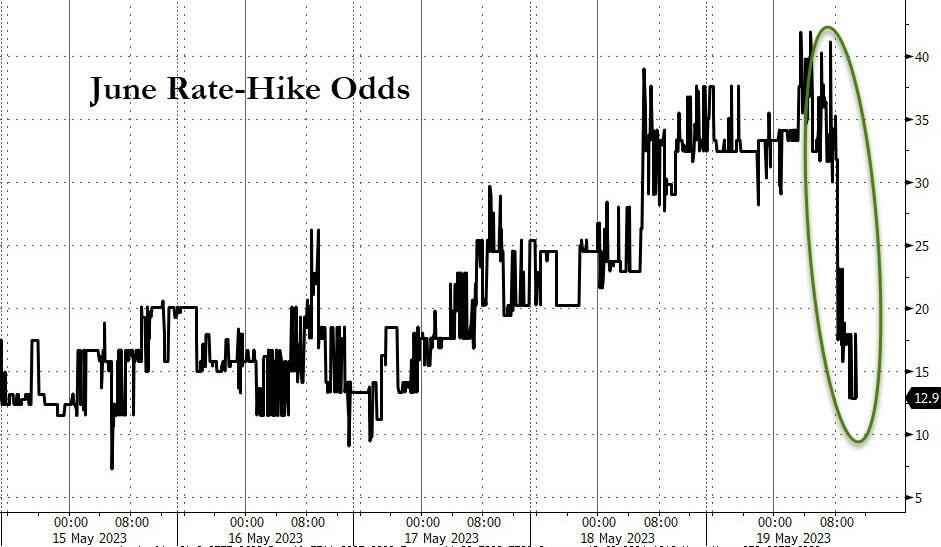

The other big story yesterday was a significant bond selloff that was sparked by hawkish comments from Dallas Fed President Logan (voter). In particular, she said that “we haven’t yet made the progress we need to make” on inflation, and that “we aren’t there yet” in terms of it being appropriate to pause rate hikes. That caused a big reaction in markets, and led investors to dial up their expectations of another rate hike at the next meeting in June. Then later in the session, an FT interview with St Louis Fed President Bullard (non-voter) came out, who said that the situation “may warrant taking out some insurance by raising rates somewhat more to make sure that we really do get inflation under control”. On the more dovish side, Governor Jefferson (voter) said that “a year is not a long enough period for demand to feel the full effect of higher interest rates”. But the more hawkish comments got the attention, and by the close fed funds futures were pricing the chances of a June hike at 37.6%, having briefly gone as high as 41% on an intraday basis. So for the first time since SVB’s collapse, it’s clear that markets are now considering the prospect of a June hike as a serious possibility rather than just some tail risk.

In many respects, those two stories above are interlinked. After all, if we do get a resolution on the debt ceiling by early June, clearly that would make it easier for the Fed to proceed with a hike at their meeting on June 14. And with greater optimism on the debt ceiling and those hawkish remarks from Fed officials, US Treasuries sold off across the curve. For instance, the 10yr yield (+8.2bps) rose for a 5th consecutive session to a post-SVB high of 3.646%. Meanwhile, at the very front end, the pricing of further rate hikes meant that the 3m yield (+0.7bps) closed at a fresh post-2001 high of 5.225%. 2yr yields rose +9.8bps and are now +44bps above where they were intra-day last Thursday and +59bps above the lows from the prior Thursday, which was just after the last FOMC meeting .

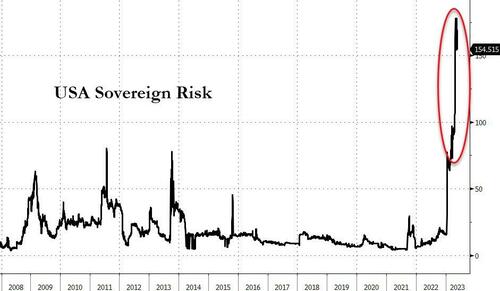

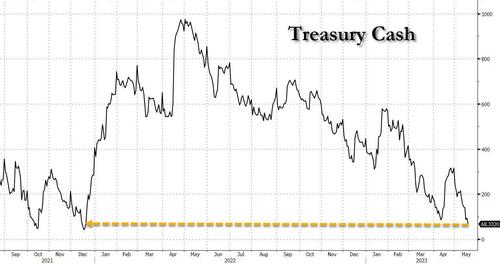

US 1M Treasury yields (x-date sensitive) were down -4.7bps yesterday to 5.299%, that is their lowest closing level since May 5. The 1M yield is now down -23.2ps since its highest closing levels on Monday, having peaked intraday then at 5.577%, which is the all-time high for the security since they were first issued in late-2001. The spread of the 1M treasury yield remains 14bps higher than the 1M OIS overnight swap rate (which controls for the fed funds rate) after peaking at 44.5bps back on Monday as well, which is higher than we saw during the 2011 (5.3bps) or 2013 (23.8bps) debt ceiling episodes.

That risk-on tone from the perceived debt ceiling progress, and the moves to price in a June hike were given further support from various data releases. One was the weekly initial jobless claims from the US, which came in at 242k (vs. 251k expected) in the week ending May 13. On top of that, the Philadelphia Fed’s business outlook for May saw a noticeable rebound to -10.4 (vs. -20.0 expected), after coming in at its lowest of this cycle so far in April. So there was some encouragement for those hoping that a recession might be avoided. That said, there was also further evidence for the pessimists on offer, since the Conference Board’s Leading Index fell a further -0.6% in April, bringing its year-on-year decline to -8.0% now. And for what it’s worth, on the 6 previous occasions since 1960 when it had fallen by such a large amount, the economy was already in recession by that point.

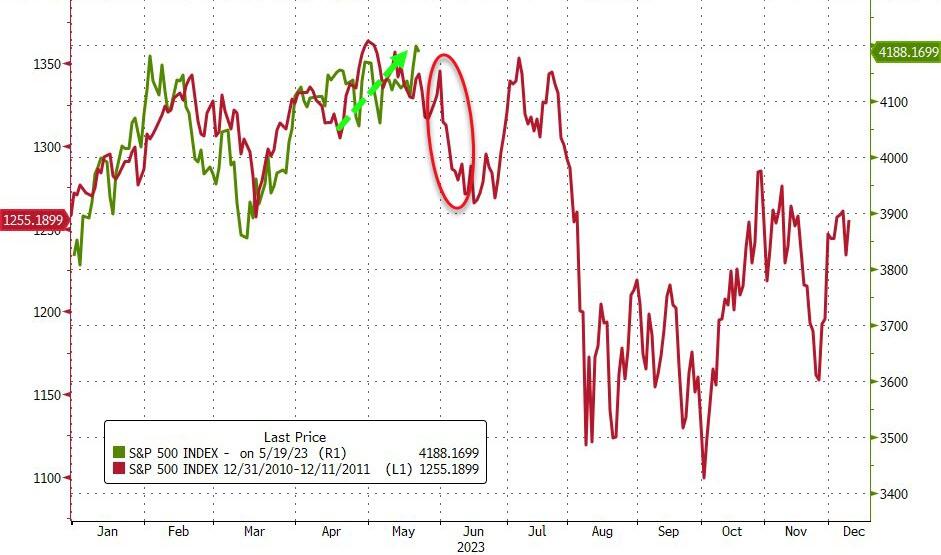

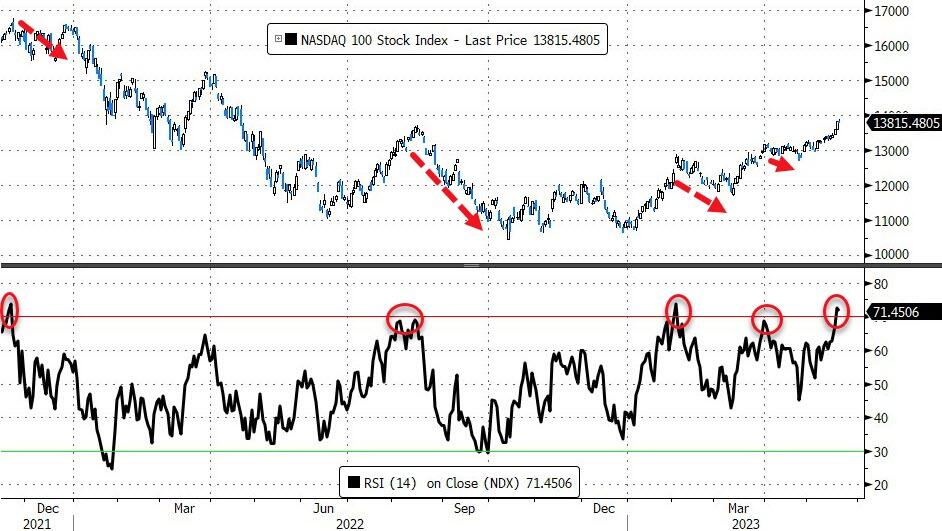

For now at least, markets were focusing on the positives, which enabled equities to advance on both sides of the Atlantic. For instance, the S&P 500 (+0.94%) advanced for a second day, and to a nearly 9-month high, running with a particularly strong close that can be partially attributed to today’s option expiry. Cyclical and tech stocks powered the advance with the NASDAQ (+1.51%) continuing its outperformance, and for the first time this year it now has a YTD performance of +20% (+21.2%), which is one of the biggest of any major index (admittedly after a -33% decline in 2022). And if you just look at the 10 megacap tech stocks in the FANG+ index, the performance is even more notable, with the index up +3.45% yesterday to bring its YTD gains to +53.21%.

Asian equity markets continue to build on the global rally with the Nikkei (+1.04%) leading gains across the region, extending its winning streak to 7 consecutive day and maintaining its’ highest levels since 1990. Meanwhile, the KOSPI (+0.79%), the CSI (+0.21%) and the Shanghai Composite (+0.13%) are also trading up. Elsewhere, the Hang Seng (-1.01%) is bucking the regional trend this morning after weaker results from Alibaba. Outside of Asia, US stock futures are indicating a decent start with those tied to the S&P 500 (+0.18%) and NASDAQ 100 (+0.28%) printing mild gains.

Data from Japan showed that consumer price inflation accelerated to +3.5% y/y in April, matching market expectations against last month’s +3.2% increase. Additionally, core consumer inflation (+3.4% y/y) rose in-line with market expectations in April (v/s +3.2% in March) and stayed well above the central bank’s 2% target, thus renewing thoughts over if and when the Bank of Japan (BOJ) will make adjustments to their YCC policy.

Back in Europe, there was also growing optimism after natural gas prices closed beneath €30/MWh for the first time since June 2021, which has led to growing optimism about the economic picture as we head deeper into the year. That helped support risk assets across the continent, with the STOXX 600 up +0.39%, having also gotten a boost from the positive debt ceiling news as well. For sovereign bonds, the selloff was even bigger than the US though, with yields on 10yr bunds (+11.0bps), OATs (+11.9bps) and BTPs (+13.0bps) all seeing a significant increase.

Here in the UK, gilt yields actually hit some of their highest levels since Liz Truss was PM yesterday, after BoE Deputy Governor Ramsden said that they might accelerate their QT programme. He said that “There’s the potential for us to go up a little bit. I don’t see us going down given the experience of the first year.” However, Governor Bailey also said that “I do not envisage the balance sheet returning to what it was before the financial crisis”. Against that backdrop, yields on 10yr gilts were up +12.0bps to 3.957%, marking their highest level since late-October.

To the day ahead now, and the highlights will include remarks from Fed Chair Powell and ECB President Lagarde. Other central bank speakers include the Fed’s Williams and Bowman, the ECB’s Schnabel and De Cos, along with the BoE’s Haskel. Data releases include German PPI for April. Finally, G7 leaders are currently meeting in Japan.

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

Generally constructive tone ahead of key Fed speak – Newsquawk US Market Open

FRIDAY, MAY 19, 2023 – 06:33 AM

European bourses/US futures are firmer with fresh drivers limited and the focus firmly on Fed speak

Debt ceiling reports indicate steady progress is being made, a view echoed by White House officials; Biden to leave G7 dinner early

USD retreats from multi-weak peaks amid a Yuan revival to the benefit of G10s pre-Powell

EGBs have seen two-way action but are holding off early German PPI-induced lows, USTs comparably more contained

Commodities are benefitting from the USD’s downside with Crude towards Thursday’s best while XAU remains shy of USD 2k/oz

Looking ahead, highlights include Speeches from ECB’s Lagarde & Schnabel, Fed’s Powell, Williams & Bowman. Moody’s on Italy and S&P on S. Africa

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

European bourses are in the green, Euro Stoxx 50 +0.8%, and are set to see the week out with upside of a similar magnitude.

Thus far, fresh macro drivers have been limited the focus firmly on the Central Bank docket which features Lagarde & Schnabel from the ECB.

Stateside, futures are flat/slightly firmer following as the debt ceiling sees tentative progress and participants switch their near-term focus to Fed speak/next week’s data; firstly, Fed’s Powell, Williams & Bowman are due today.

Deere & Co (DE) Q1 2023 (USD): EPS 9.65 (exp. 8.59), Revenue 17.39bln (exp. 14.83bln). +2.5% in pre-market trade

Samsung Electronics (005930 KS) will not be swapping out default search engine on its smartphones from Google (GOOGL) to Microsoft’s (MSFT) Bing, via WSJ citing sources.

Click here and here for a recap of the main European updates.

Buck backs off from fresh multi-week peaks awaiting potentially pivotal remarks from Fed Chair Powell, DXY back under 103.500 towards 103.21 trough after forming a virtual 103.620-630 double top.

Yen claws back losses vs Dollar from 138.72 to 137.98 amidst reports of pre-weekend long liquidation.

Yuan regains poise from deeper sub-7.0000 lows as Chinese state banks step in to curb the slide.

Kiwi bounces firmly on 0.6200 handle after NZ trade balances swings from deficit into surplus.

Aussie, Euro and Sterling all take advantage of Greenback retreat within 0.6617-63, 1.0761-1.0804 and 1.2393-1.2435 respective ranges.

PBoC set USD/CNY mid-point at 7.0356 vs exp. 7.0392 (prev. 6.9967)

Click here for the notable FX expiries for today’s NY cut.

FIXED INCOME

Bonds fade from best levels in dead cat fashion awaiting final Central Bank speakers of the week headlined by Fed Chair Powell and ECB President Lagarde.

Bunds back below par between 134.33-133.76 parameters, Gilts slipping to new intraday lows towards 98.50 vs 99.21 at best and T-note rooted towards base of 113-30/114-05 range.

Permanent TSB (SAB SM) says it has not seen a slowdown in demand for mortgages due to higher rates, not seeing stress in mortgage book. Note, this headline is potentially a factor behind the recent increase in benchmark pressure, which is seemingly being led by Gilts

Crude is firmer on the session and back towards yesterday’s best levels in what has been a choppy session for the complex despite a lack of specific drivers ahead of a busy US agenda and with attention on the G7.

Currently, WTI and Brent are posting upside of over USD 0.50/bbl in circa. USD 1.00/bbl parameters.

As the USD comes under pressure, metals are experiencing relatively broad based upside; specifically, spot gold is bid but remains shy of the week’s USD 2022/oz best with LME Copper similarly sub-8.3k.

Saudi’s Energy Minister said coordination with OPEC+ countries is a cornerstone of the efforts to enhance the stability of oil markets and maintain their balance, according to the state news agency.

UK plans GBP 1bln of semiconductor investment in a new strategy that aims to strengthen the domestic industry and chip supply chains, according to the government.

ECB is reportedly to increase scrutiny of bank liquidity and could lift requirements, via Bloomberg; could communicate such requirements later this year. Scrutiny into liquidity following on from US bank and Credit Suisse (CSGN SW) failures.

ECB’s Lagarde says we are heading towards more delicate policy decisions going forward; will be courageous to take the decisions needed to bring inflation back to the target.

DATA RECAP

UK GfK Consumer Confidence (May) -27 vs. Exp. -27 (Prev. -30)

German Producer Prices MM (Apr) 0.3% vs. Exp. -0.5% (Prev. -2.6%, Rev. -1.4%); YY (Apr) 4.1% vs. Exp. 4.0% (Prev. 7.5%, Rev. 6.7%)

NOTABLE US HEADLINES

Fed Discount Window loans were at USD 9.05bln in the week ended May 17th which was down from the USD 9.32bln level during the prior week, while BTFP lending was USD 87bln vs prev. USD 83.1bln W/W and the Fed’s Other Credit was at USD 208.5bln vs prev. USD 212.5bln W/W.

White House officials said US President Biden held a call with the debt ceiling negotiation team and his negotiating team said that steady progress is being made in talks, while President Biden is confident that Congress will take action to avoid a US default, according to Reuters.

US debt-ceiling negotiations are reportedly moving slowly and quite deliberately, sources tell Punchbowl. “It’s still possible the two sides reach a deal by Sunday or Monday, but legislative text is unlikely to be ready by then.”. A White House official said “steady progress is being made.”; Biden administration is aiming for a debt-hike extension into 2025 during talks with House GOP negotiators, according to multiple sources involved in the discussions.

Spokesperson says US President Biden is planning to leave G7 leaders dinner early.

Ukrainian President Zelensky is to travel to Japan to attend the G7 Summit in person, according to Bloomberg.

US senior administration official said all G7 members are preparing to implement new Russian sanctions and export controls with the sanctions aimed at closing evasion loopholes and will target war inputs, energy reliance and access to financial systems. US is to target Russia with roughly 300 sanctions on individuals, entities, vessels and aircraft across Europe, the Middle East, and Asia. US sanctions will also target financial facilitators, Russia’s future energy and extraction capabilities, as well as others supporting Russia’s war, while G7 countries remain committed to upholding the price cap on Russian oil, according to Reuters.

US President Biden’s administration signalled to European allies in recent weeks that the US would allow them to export F-16 fighter jets to Ukraine, while Ukraine was said to have used a Patriot to shoot down at least one Russian fighter jet in recent weeks, according to CNN’s Bertrand.

EU”s President of the European Council Michel said they will restrict the sale of Russian diamonds and call on China to pressure Russia to stop military aggression, while he said stable and constructive cooperation with China is in their interests and that they need to engage with China on global challenges.

CRYPTO

Bitcoin is modestly firmer and despite eclipsing the USD 27k mark as the USD comes under Yuan-driven pressure this morning, BTC thus far has been unable to hold onto the level and is now holding just below it.

APAC TRADE

APAC stocks were mostly higher following the tech-led gains on Wall St where the Nasdaq outperformed and the S&P 500 printed a 9-month high on debt ceiling optimism and firm data, although Chinese markets lagged amid disappointment from Alibaba’s revenue miss.

ASX 200 was lifted with the tech sector front-running the gains as it took inspiration from its US counterpart and with the top-weighted financial industry trailing closely behind.

Nikkei 225 surged at the open to print its highest since August 1990 although pared some of the gains after losing steam on its approach to the 31,000 level and as participants digested the latest CPI figures which were mostly in line with expectations but showed a faster pace of acceleration.

Hang Seng and Shanghai Comp. were mixed with the Hong Kong benchmark pressured as tech giants suffered following Alibaba’s earnings which beat on the bottom line but missed on revenue, while frictions lingered after the US and Taiwan reached an initial agreement on a ’21st Century’ trade pact and with China concerned about recent signs of negative China-related developments at the G7.

NOTABLE ASIA-PAC HEADLINES

Chinese President Xi said China proposed to establish meeting and dialogue mechanisms in cooperation between China and Central Asian countries in which the mechanisms will cover agriculture, transportation, emergency management, education and political party affairs, while Xi added that China will roll out more trade facilitation measures and upgrade bilateral investment agreements with Central Asian countries.

China’s Commerce Minister is to meet with US Commerce Secretary Raimondo and US Trade Representative Tai next week, according to Politico.

China’s Taiwan Affairs Office said it will allow travel agencies to resume group tours for Taiwan residents to the mainland from today, according to Reuters.

USTR office said US and Taiwan reached an initial agreement on a ’21st Century’ trade pact which covers customs and trade facilitation, good regulatory practices, services regulations, anti-corruption measures and SMEs. USTR added that further US-Taiwan negotiations will commence on additional trade areas including agriculture, digital trade, labour, environment and SOEs, according to Reuters.

China’s Major state-owned banks are reportedly seen swapping Yuan for Dollars in the onshore FX forwards market, according to currency traders cited by Reuters; One source said state banks have started heavily trading buy/sell 1yr tenor since Thursday. Subsequently, China is to curb speculations on Yuan rates when necessary, according to PBoC.

BoJ’s Ueda says the domestic economy is picking up, driver of the economic recovery is likely to shift from pent up demand to rising income/expenditure. Adds, it is appropriate to take time to decide on adjustments to monetary easing toward a future exit. “While there is an opposite risk that inflation will remain above 2 percent if a change in policy falls behind the curve, the cost of waiting for underlying inflation to rise until it can be judged that 2 percent inflation has fully taken hold is not as large as the cost of making hasty policy changes. In this sense, it is appropriate to take time to decide on adjustments to monetary easing toward a future exit.”. Click here for more detail.

DATA RECAP

Japanese National CPI YY (Apr) 3.5% vs. Exp. 3.5% (Prev. 3.2%); Ex. Fresh Food YY (Apr) 3.4% vs. Exp. 3.4% (Prev. 3.1%)

Japanese National CPI Ex. Fresh Food & Energy YY (Apr) 4.1% vs. Exp. 4.2% (Prev. 3.8%)

New Zealand Trade Balance (Apr) 427M (Prev. -1273.0M, Rev. -1586M)

ASIAN AND AUSTRALIAN CLOSINGS//EUROPE OPENING TRADING:

FRIDAY MORNING/THURSDAY NIGHT