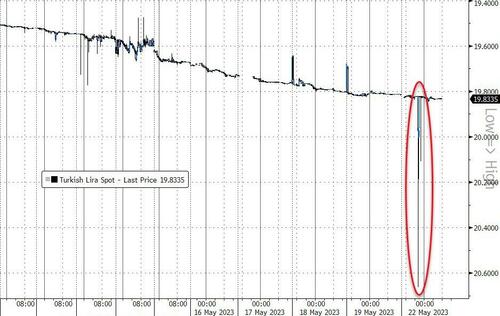

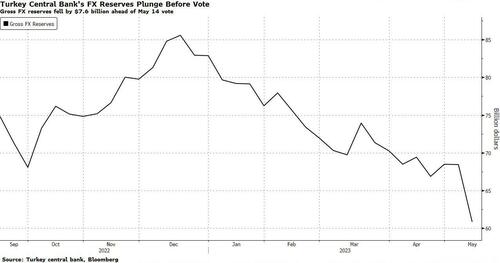

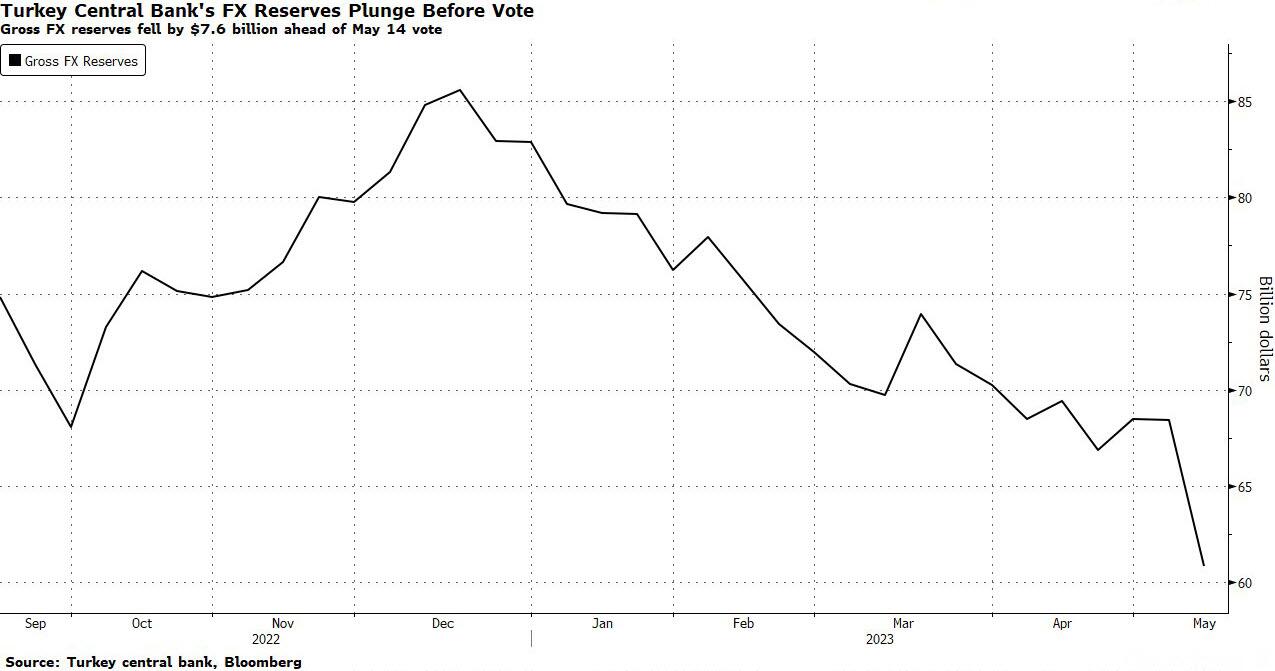

MAY 22/GOLD CLOSED DOWN $4,70 TO $1975.00//SILVER DOWN DOWN 19 CENTS TO $23.70. PLATINUM WAS THE ONLY GAINER AMONG OUR PRECIOUS METALS, BEING UP $1.15 TO $1072.35//PALLADIUM WAS DOWN A STORNG 425.55 TO $1490.05//ANDREW MAGUIRE A MUST VIEW/ALSO MATHEW PIEPENBERG A MUST READ//AS PER DEBT CEILING ANOTHER MEETING TODAY AT 4:15 BETWEEN BIDEN AND REPUBLICAN REPRESENTAIVES// COVID UPDATES// VACCINE IMPACT/DR PAUL ALEXANDER/SLAY NEWS/EVOL NEWS//UKRAINE VS RUSSIA; WAGNER GROUP CLAIMS THEY HAVE NOW 100% OF BAKHMUT//ANOTHER MUST READ: SEYMOUR HERSH//TURKISH LIRA FLASH CRASHES BEYOND 20 TO ONE AS FOREIGN EXCHANGE LEAVES TURKISH BANKS//THERE IS NOW ONLY 57 BILLION DOLLARS LEFT IN USA TREASURY//GOLDMAN SACHS WARNS ON USA COMMERCIAL REAL ESTATE//HUGE SHOPLIFTING PROBLEMS IN NEW YORK//ALSO NEW YORK CITY SUFFERING DUE TO MIGRANTS ENTERING HOTELS//SWAMP STORIES FOR YOU TONIGHT//

118 C MACQUARIE FUT 25 363 H WELLS FARGO SEC 100 435 H SCOTIA CAPITAL 5 657 C MORGAN STANLEY 2 661 C JP MORGAN 12 737 C ADVANTAGE 1 2 800 C MAREX SPEC 3 880 H CITIGROUP 45 905 C ADM 7

TOTAL: 101 101 MONTH TO DATE: 6,032

JPMorgan stopped 12/101 contracts

FOR MAY:

GOLD: NUMBER OF NOTICES FILED FOR MAY/2023. CONTRACT: 101 NOTICES FOR 10,100 OZ or 0.31415 TONNES

total notices so far: 603,200 contracts for 603,200 oz (18.762 tonnes)

FOR MAY:

SILVER NOTICES: 63 NOTICE(S) FILED FOR 315,000 OZ/

total number of notices filed so far this month : 2505 for 12,525,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP DOWN $4.70..

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//WOW!!

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:/// A MASSIVE DEPOSIT OF 5.83 TONNES OF GOLDINTO THE GLD DESPITE THELOSS IN PRICE.

INVENTORY RESTS AT 942.74 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 19 CENTS AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV: /; : INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 468.529 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 958 CONTRACTS TO 137,716 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS STRONG SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.38 RISE IN SILVER PRICING AT THE COMEX ON FRIDAY. TAS ISSUANCE WAS A STRONG 640 CONTRACTS. THESE WILL BE USED FOR MANIPULATION NEXT MONTH. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDER SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY: A STRONG 640 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS, IT FALLS ON DEAF EARS WITH OUR REGULATORS.

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.38). BUT WERE SUCCESSFUL IN KNOCKING SOME SPEC LONGS AS WE HAD A STRONG LOSS ON OUR TWO EXCHANGES OF 650 CONTRACTS ( MOST OF THIS LOSS OCCURED BEFORE THE ANNOUNCEMENT THAT REPUBLICANS LEFT THE NEGOTIATION TABLE ON DEBT CEILING). WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 4.250MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH (TAS), AND FINAL WEEK (COMEX SPREADERS).

WE MUST HAVE HAD:

A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS( 225 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.105 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP OF 310,000 OZ (QUEUE JUMP RAISES THE AMOUNT OF SILVER STANDING)+0 EXCHANGE FOR RISK// TOTAL 4.25MILLION OZ OF EXCHANGE FOR RISK FOR THE MONTH(RAISES THE AMOUNT OF SILVER STANDING):THUS TOTAL OF 17.560 MILLION OZ OF STANDING FOR DELIVERY V) STRONG SIZED COMEX OI LOSS/ SMALL SIZED EFP ISSUANCE/VI) LARGE NUMBER OF SHORT T.A.S. CONTRACT INITATION//ZERO T.A.S LIQUIDATION.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -removed 25CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTRACTS for 16 days, total 10,525 contracts: OR 52.625 MILLION OZ . (657 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 52.625 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 52.650 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 733 CONTRACTS DESPITE OUR $0.38 GAIN IN SILVER PRICING AT THE COMEX//FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 225 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAY OF 13.105 MILLION OZ//FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 310,000 OZ (INCREASES THE AMOUNT OF SILVER STANDING) +// + 0.0 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //TOTAL EXCHANGE FOR RISK MONTH= 4.25 MILLION//NEW TOTALS 13.310 MILLION OZ + 4.25 MILLION = 17.560 MILLION OZ// .. WE HAVE A STRONG SIZED LOSS OF 733 OI CONTRACTS ON THE TWO EXCHANGES AS SOME OF THE SHORT SIDE SPECS WERE CAUGHT FLAT FOOTED ON THE RISE IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG 640!!//ZERO TAS LIQUIDATED.

WE HAD 63 NOTICE(S) FILED TODAY FOR 315,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAR SIZED 1,214 CONTRACTS TO 486,848 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -151 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 1,214 CONTRACTS) DESPITE OUR $22.20 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR MAY. AT 3.5085 TONNES ON FIRST DAY NOTICE // PLUS 9700 OZ QUEUE JUMP :(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)/+ /A SMALLER ISSUANCE OF 812 T.A.S. CONTRACTS//NO TAS LIQUIDATION////YET ALL OF..THIS HAPPENED WITH OUR HUGE $22.20 GAIN IN PRICEWITH RESPECT TO FRIDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 2856 OI CONTRACTS (883 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4070 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 486,848

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3007 CONTRACTS WITH 1,063 CONTRACTS INCREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): 812 CONTRACTS) AND 4070 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3007CONTRACTS OR 9.353TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4070 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (1,214) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 2856 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 3.5085 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 9700 OZ // NEW STANDING: 19.0917 TONNES // ///3) ZERO LONG LIQUIDATION//4) SMALL SIZED COMEX OPEN INTEREST LOSS/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: T.A.S. ISSUANCE: 812 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 50,514 CONTRACTS OR 5,051,400 OZ OR 157.119 TONNES IN 16 TRADING DAY(S) AND THUS AVERAGING: 3157 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES 157.119 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 157.119/3550 x 100% TONNES 4.42% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES ( MUCH SMALLER THAN LAST MONTH)

MAY: 157.119 TONNES (HEADING FOR ANOTHER SMALLER MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A STRONG SIZED 958 CONTRACTS OI TO 137,716 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 225 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 225 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 225 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 958 CONTRACTS AND ADD TO THE 225OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 733 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 3.290 MILLION OZ

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

MONDAY MORNING//SUNDAY NIGHT

SHANGHAI CLOSED UP 12.93 PTS OR 0.39% //Hang Seng CLOSED UP 278/47 POINTS OR 0.90% /The Nikkei closed UP 227.60 OR 1.17% //Australia’s all ordinaries CLOSED DOWN 0.28 % /Chinese yuan (ONSHORE) closed DOWN 7.0293 /OFFSHORE CHINESE YUAN DOWN TO 7.0418 /Oil DOWN TO 71.62 dollars per barrel for WTI and BRENT AT 75.72 / Stocks in Europe OPENED ALL MOSTLY RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1214 CONTRACTS DOWN TO 486,697 DESPITE OUR GAIN IN PRICE OF $22.20 ON FRIDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF MAY… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4070 EFP CONTRACTS WERE ISSUED: : JUNE 4070 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4070 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2856 CONTRACTS IN THAT 4070LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 1,214 COMEX CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR STRONG GAIN IN PRICE OF $22.20. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE),THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE THIS MORNING WAS A SMALLER 812 CONTRACTS. DURING THIS WEEK THEY SOLD THE LONG SIDE OF THE SPREAD WHICH OF COURSE MANIPULATED THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDER SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (19.0717) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.0917 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $22.20) //// AND WERE UNSUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD OUR FAIR SIZED GAIN OF 2856 CONTRACTS ON OUR TWO EXCHANGES. WE HAD NO TAS LIQUIDATION.

WE HAVE GAINED A TOTAL OI OF 9.353PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY. (3.5085 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 9700 oz (0.3017 TONNES)//NEW STANDING 19.0917 TONNES ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $22.20

WE HAD +REMOVED XXX CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3007 CONTRACTS OR 30700 OZ OR 9.353 TONNES.

Total monthly oz gold served (contracts) so far this month

6032 notices 603,200 OZ 18.762 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: NIL oz

customer withdrawals: 0

total withdrawals: nil oz

Adjustments; 1//dealer to customer

out of Brinks: 46,220.901 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 207 contracts having GAINED 84 contracts. We had 13 contracts filed

on FRIDAY, so we GAINED A HUGE 97 contracts or an additional 9700 oz (0.3017 tonnes) will stand for gold in this non active delivery month of May

June LOST A SMALLER 9339 contracts DOWN to 177,474 contracts.

July added 359 contracts to stand at 2247 contracts.

AUGUST GAINED 8120 contracts UP to 251,996 contracts

We had 101 contracts filed for today representing 10,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 101 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 12 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2023. contract month,

we take the total number of notices filed so far for the month (6,032 x 100 oz ), to which we add the difference between the open interest for the front month of MAY (207 CONTRACTS) minus the number of notices served upon today 101 x 100 oz per contract equals 613,800 OZ OR 19.0917 TONNES the number of TONNES standing in this NON- active month of May.

thus the INITIAL standings for gold for the MAYcontract month: No of notices filed so far (6,032 x 100 oz) x 207 OI for the front month minus the number of notices served upon today (101)x 100 oz} which equals 613,800 oz standing OR 19.0917 TONNES

TOTAL COMEX GOLD STANDING: 19.0917 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,580,639.231 OZ

TOTAL REGISTERED GOLD: 12,356,261.338 (384.331 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,224,378.008 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,659,678 OZ (REG GOLD- PLEDGED GOLD) 331.56 tonnes//

END

SILVER/COMEX

MAY 22//2023// THE MAY 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

408,195.128 oz Brinks Delaware HSBC’ JPMorgan

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

610,239.306 oz JPMorgan CNT

No of oz served today (contracts)

63 CONTRACT(S) (315,000 OZ)

No of oz to be served (notices)

157 contracts (785,000 oz)

Total monthly oz silver served (contracts)

2505 Contracts (12,525,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposits: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i) Into JPMorgan: 600,206,200 oz

ii) Into CNT: 10,033.106 oz

Total deposits: 598,898.300 oz

JPMorgan has a total silver weight: 142.178 million oz/274.397 million =51.88% of comex .//dropping fast

Comex withdrawals 4

i) Out of Brinks: 2983.14 oz

ii) Out of Delaware 48,306.790 oz

iii) Out of HSBC: 10,165.108 oz

iv) Out of JPMorgan: 346,740.090 oz

Total withdrawal: 408,195.128 oz

adjustments: 1//dealer to customer Brinks

i) Out of Brinks 54,679.220 oz

TOTAL REGISTERED SILVER: 30.978 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 274.397 million oz

CALCULATION OF SILVER OZ STANDING FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2023 OI: 220 CONTRACTS HAVING GAINED 33 CONTRACT(S). WE HAD 29 CONTRACTS FILED ON FRIDAY, SO WE GAINED 62 CONTRACTS OR AN ADDITIONAL 310,000 OZ WILL STAND FOR DELIVERY ON THIS SIDE OF THE POND

JUNE HAD A 21 CONTRACT GAIN TO 1139

JULY HAD A 1284 CONTRACT LOSS TO 112,391 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 63 for 315,000 oz

Comex volumes// est. volume today 38,625 fair

Comex volume: confirmed yesterday: 58,786 fair

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 2505 x 5,000 oz = 12,525,000 oz

to which we add the difference between the open interest for the front month of MAY(220) and the number of notices served upon today 63 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2023 contract month: 2505 (notices served so far) x 5000 oz + OI for the front month of May (220) – number of notices served upon today (63 )x 500 oz of silver standing for the MAY contract month equates to 13.310 million oz + THE CRIMINAL 0 MILLION OZ EXCHANGE FOR RISK TODAY//NEW TOTAL EXCHANGE FOR RISK: 4.250//NEW TOTAL 17.560 MILLION OZ//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

MAY 9/WITH GOLD UP $9.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTER DEPOSIT OF 5.88 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 937.64 TONNES

MAY 8/WITH GOLD UP $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 931.77 TONNES

MAY 5/WITH GOLD DOWN $30.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AS DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

MAY 4/WITH GOLD UP $19.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.30 TONNES

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

GLD INVENTORY: 942.74 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

MAY 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A TINY DEPOSIT OF .08 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 465.682 MILLION OZ//

MAY 8/WITH SILVER DOWN 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.602 MILLION OZ//

MAY 5/WITH SILVER DOWN 31 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 466.876 MILLION OZ//

MAY 4/WITH SILVER UP 53 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF .174 MILLION OZ INTO SLV.//INVENTORY RESTS AT 467.174 MILLION OZ//

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

De-Dollarization is a real, all too real trend, though it is both fascinating and disturbing to see what is otherwise so obvious being deliberately down-played, excused or ignored from the top down.

But then again, the laundry list of ignored facts and open lies from the top down to hide hard truths in everything from inflation data to recessionary debt traps is nothing new.

Instead, such propaganda replacing blunt transparency is the new normal (and classic trick) for all historical endings to debt-soaked (and failing) nations/systems and their fork-tongued (i.e., guilty) policy makers.

Slow & Steady

De-Dollarization, of course, is a gradual rather than over-night process.

Its origins stem from 1) years of exporting USD inflation overseas (to the painful detriment of friend and foe alike) and 2) the insanely stupid decision to weaponize the world reserve currency (i.e., USD) subsequent to a border war between two local tyrants in the Ukraine.

Whether or not you buy into the Western “media’s” narrative which categorizes Putin as Hitler 2.0 and Zelensky as a modern George Washington, the weaponization of the USD (and freezing of FX reserves) has made an already dollar-tired globe even more distrusting of Uncle Sam’s currency and IOUs.

This trend is confirmed by the profound dumping of USTs throughout 2022 and the undeniable trend among the BRICS (and the 36 other nations) to deliberately seek bilateral trade agreements and settlements outside of the USD.

Furthermore, with Saudi talking to China and Iran, and with China talking to Mexico, Russia and just about everyone else, it’s fairly clear that a move away from the once sacred petrodollar (Pakistan now seeking Russian oil in Yuan) is no longer just the fantasy of conveniently eliminated folks like Saddam Hussein or Muammar Gaddafi…

As I discussed here and here, the petrodollar is under threat, which means longer-term demand for the USD is equally so.

But the USD Still Has Legs—For Now…

That said, there’s also no denying that the USD is still very strong, very important and very much in demand.

After all, and despite welching in 1971 on its 1944 promise to be gold-backed, the USD is still the world reserve currency.

With over 40% of global debt instruments denominated in Greenbacks and over 60% of the reservoir of global currencies composed of USDs, this reserve status (and hence forced demand) aint going anywhere too soon.

Furthermore, and as I have written and agreed, the so-called “milk-shake theory” is not altogether wrong.

That is, demand for USDs (and USTs) within the tangled and levered web of US derivative and Euro Dollar markets is baked into a system which will take years (not days) to unravel, monetize or replace, and this sure as heck won’t be orderly, global nor overnight.

Then Comes Change, Pain and Open Denial

But let’s get real: The days of the USD as a trusted payment system or hegemonic power broker are unwinding right before our very eyes.

And the best way to see the truth of this reality is to catalogue the ever-expanding list of lies from the big boys and their complicit, media ja-sagenders (“yes-sayers”) desperately trying to deny the same.

At first, for example, the centralized economists were blaming de-dollarization and CNY energy transactions on the Russian sanctions.

Gee. Go figure?

Thereafter, the economists said de-dollarization is just the result of Emerging Market (EM) countries momentarily running out of (in fact they’re intentionally dumping) USD reserves.

Western “experts” are trying to convince themselves and the rest of the world that EM nations will implode unless they eventually acquire more USTs and USDs to buy energy.

What these experts are failing to see (or say), however, is that many of those countries are already beginning to buy that energy outside of the USD…

Folks, de-dollarization in global commodity markets is happening already, and will accelerate rather than fade away into some fantasy image of how the “West was Won,” for as argued elsewhere, the West is already losing.

Facts Are Stubborn Things

As for the list of nations, both big and small, de-dollarizing right before our watering eyes, just consider, well…China, Russia, India, Pakistan, Ghana, Bolivia…

Even the world’s largest hardwood pulp producer, Suzano SA, is in talks with China to trade its commodity in CNY.

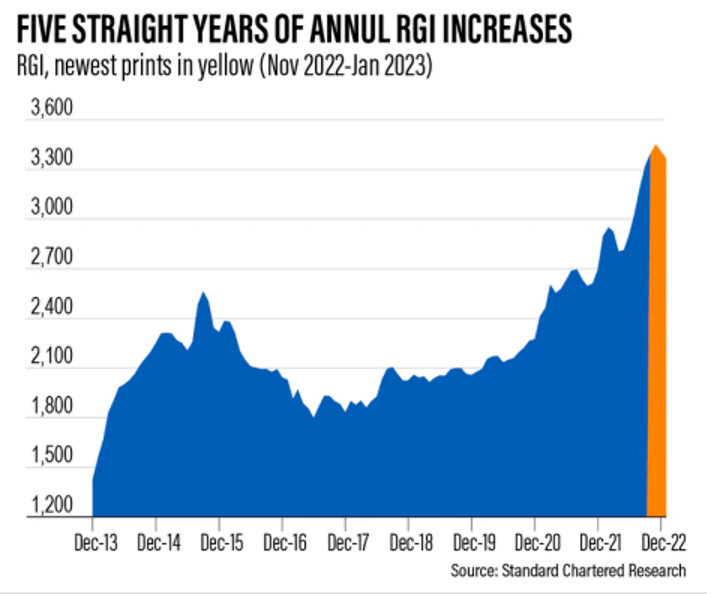

This transition from a weaponized USD to an expanding CNY is not just the sensationalism of fiat-haters but the hard math of real events and data, which the following chart of the Renminbi Globalization Index (up 26% in 2022) makes all too clear…

The undeniable trend and rise (which is not the same as “hegemony”) of the CNY is certainly not good news for the fiat-all-too-fiat USD, who is less and less the prettiest girl at the dance.

As trust/demand in the USD falls, so too does its purchasing power, which may explain why China, at the very same time its trade power increases, is simultaneously growing its gold reserves in anticipation for what it knows is coming but what the West still refuses to see, namely: The slow-drip neutering of Uncle Sam’s fiat currency.

See the trend folks?

We Told You So

See why picking a currency-for-energy war against Russia (the world’s biggest commodity exporter and a nuclear power in bed with China, the world’s biggest factory owner and a nuclear power) may have been a bad idea?

As we warned literally from day-1 of the sanctions, this was obviously not the same as picking a sanction fight with say, Iran or Venezuela…

Nope. This scale of this was far more dangerous, and the avoidable casualties still piling up in the West’s proxy war (on Ukrainian soil/rubble) are not just soldiers and civilians, but Greenbacks too.

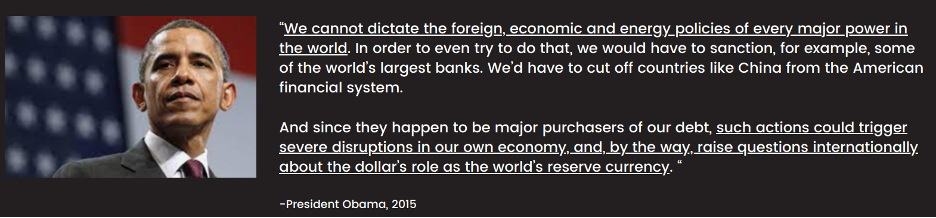

This was foreseeable.

Even Obama foresaw it in 2015:

Clearly, Biden’s handlers, however, didn’t see it in 2022.

They wanted to play war rather than sound economics, and the end result will be a loss of both.

As for the USD: Volatility Before Debasement

As for the fate and price of the USD near-term and long-term, the move will be volatile rather than in a straight line north or south.

The USD can still go higher, much higher, as fewer Greenbacks overseas still face large debt payments.

Ultimately, however, Uncle Sam’s own twin deficits and schoolyard of children masquerading as House Members/”leaders” will deficit spend the USA into a debt spiral whose only “cure” is more mouse-clicked and debased dollars along side more unloved and over-issued USTs (IOUs).

Thereafter, the up and down moves of the USD will eventually just sink, Titanic-like, in one direction as ever-more USD’s collide with a growing debt iceberg.

As argued so many times, but worth repeating: The last bubble to die in a debt-soaked regime is always the currency. Even the increasingly unloved world reserve currency will be no exception to the laws of over-supply and decreasing demand.

We have always warned that Powell’s rate hikes (too much, too fast, too late) would be too expensive for Uncle Sam, and would thus break things here and abroad—from repo markets, gilt markets and Treasury markets to a US fiscal implosion and dying regional banks.

Next to implode are the labor markets.

Six decades of data confirm that rising rates always break things.

But when you place such rising rates into the context of the greatest debt crisis in US (as well as global) history, the “breaking” gets really ugly.

Until the Fed supplies more inflationary liquidity (fiat-fantasy money), the dual forces of a hawkish Powell and a de-dollarizing yet milk-shake world means the USD could rise and squeeze out the dollar short traders nearer term.

Anything but “Softish”

Ultimately, however, and after enough smaller banks have been murdered (more will die) and after the UST market has suffered all it can suffer, too much will break at once, and it won’t be soft, or even “softish.”

This is not fable but fact. The only “tool” the centralizers will have left is more synthetic, fiat (and inflationary) liquidity on demand.

This trend is simple: Uncle Sam is broke and his only solution is a money printer.

In short, a counterfeit answer to a real cancer.

Don’t believe me?

Just ask the US Treasury Dept.

More Ignored Math from DC

The latest TBAC (Treasury Borrowing Advisory Committee) confirms the US has already deficit spent $2.060T in fiscal 1H23, the interest expense alone of which is 101% of tax receipts.

This effectively puts the USA into a red-zone of imbalance reminiscent of the COVID crisis, only this time they don’t have COVID to blame for a debt addiction that was in play long before Fauci stained our screens or Powell printed more money post-March-of-2020 than was produced in the entire compounded history of our nation.

The TBAC report further indicated that projected US Federal deficits for 2023 to 2025 have risen by 30-50% in just the last 90 days…

And folks, the only way to pay for this embarrassing bar tab in DC is either more open QE (mouse-clicked trillions) and/or a much, much, much weaker USD to inflate away this debt as we head simultaneously into the mother of all recessions.

Such a crisis, of course, could be preceded by temporary (relative, rather than inherent) spikes in the USD until more UST supply/liquidity weakens the Greenback and sends gold higher, regardless of the USD’s relative strength and then subsequent weakness.

Meanwhile the Propaganda from On-High Continues

As I’ve said in interview after interview, you know things are getting really bad when comforting words and de-contextualized data increasingly replace simple (but scary) math.

At $95+T in public, household and corporate debt, the US has irreversibly passed the Rubicon of any easy solutions.

As Egon von Greyerz makes abundantly clear week after week, the US in general and the Fed in particular have irrevocably cornered themselves.

Stated otherwise: The USA is screwed.

DC has to chose between saving its “system” (of insider/TBTF banks, self-interested politicos–from the Maoist “woke” to the neocon “dark” and Wall Street Socialism) or destroying its currency.

Needless to say, it’s ultimately the currency that will fall on the sword for this now openly corrupt and pathetic “system.”

But again, rather than confess their own sins, the message is always “be calm and carry on.”

The Latest Fantasy Chart

Take, for example, the latest puff-tweet regarding Bloomberg’s “US Economic Surprise Index” which paints an oh-so rosy picture of the US economy rising at the fastest pace in over a year.

But as far smarter folks than me (i.e., Luke Gromen) will remind, this so-called data is ignoring a few contextual elephants in the room…

Context Helps

First, the above “good news” ignores a US debt/GDP ratio of 125%, a deficits/GDP ratio of 8% and government spending at 25% of GDP.

Secondly, US Government Outlays (i.e., deficit spending) has been growing at 30% for five of the last seven months.

Spending rates like this have only occurred twice in the last four decades, namely: 1) during the height of the COVID hysteria and 2) during the height of the 2008 GFC.

So, despite the “good news” in puff-charts above, the pundits are ignoring the fact that Uncle Sam (and his mis-fit children in the House of [lobbied] “Representatives”) are spending as if the USA is already in the eye of a financial storm.

And yet we haven’t even seen the recession officially hit or labor and risk markets tank, YET.

Imagine the spending when things get officially far worse than today—and they will; it’s now mathematical.

Out of Sight, Out of (Our) Mind

Sadly, however, very few investors are seeing the bigger picture and the wandering elephants.

In the interim: 1) the military industrial complex will create more profits and jobs here and more casualties overseas; and 2) deficit spending will keep unemployment in check (for now) and GDP “stable” until 3) its deficits (and debts) cancerously metastasize within a nation frog-boiling in debt and fractured by manufactured identity politics over transgender beer ads and slavery reparations from the 1860’s.

Such “woke” trends are ironic, given the fact that middleclass Americans of all colors, sexualities, “privileges” or political bends are already unknowing slaves/serfs in a modern feudalismof fake capitalism fighting against the bogus (yet SJW) “equity” euphemism of a woke (but hidden) re-distribution of social “shares” smacking of modern yet genuine Marxism.

Slowly, Then All at Once

And amidst all this distraction, division and in-fighting, the reality of rising rates colliding into historically unprecedented debt levels will just crush all stripes of Americans in the same manner Hemingway described poverty: “Slowly, then all at once.”

As Egon has often told me: Be careful what you wish for or already know.

Gold will inevitably go higher as the rest of the nation/world slides into its foreseeable debt trap and fiat end-game.

This may be obviously good for gold; but it will be at the expense of so much else, as the disorder ahead is neither fun nor pretty.

And it’s only just beginning…

end

WALL STREET ON PARADE

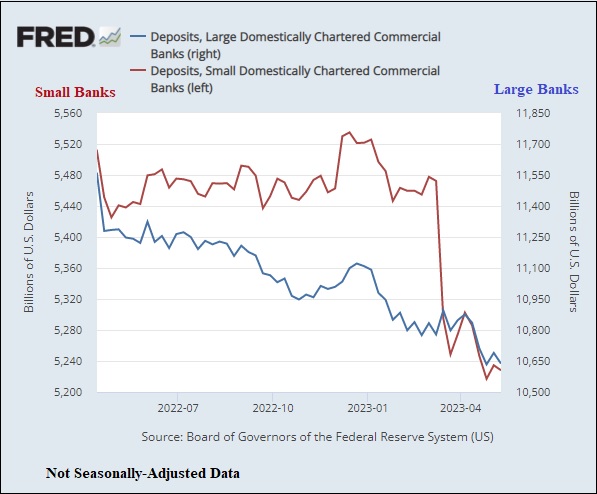

PAM AND RUSS MARTENS: A MUST READ!! ACTUALLY BY DEC 22/IT WAS THE LARGEST BANKS THAT SAW A SHEDDING OF DEPOSITS!

Pretty much everything the average American has read about the banking crisis is wrong. And there is at least a prima facie case that could be made that Big Media is responsible for that misinformation.

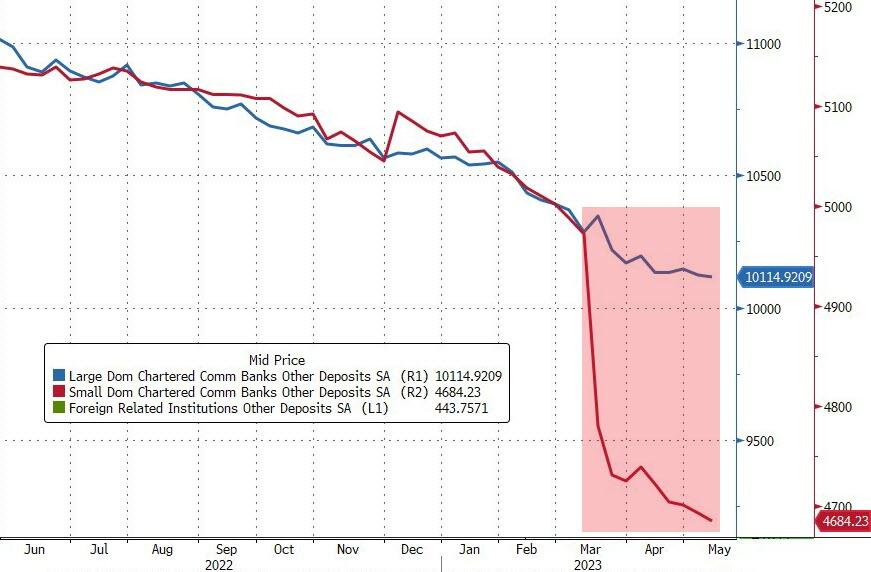

Let’s start with the dozens of mainstream media reports that small banks were bleeding deposits and these deposits were flooding into the biggest banks in the U.S. as a safe haven. Those reports gave the distinct impression that the mega banks on Wall Street are viewed by Americans as a safe place to stash money, never mind that they blew up the U.S. financial system in 2008 and still have more than $200 trillion in derivatives lurking in the shadows.

According to FRED data compiled by the St. Louis Fed (see chart above), bank deposits at the 25 largest U.S.-chartered commercial banks peaked at $11.556 trillion on April 13, 2022, then went into a persistent downtrend that erased $457 billion of deposits by December 12, 2022. Meanwhile, the more than 4,000 small U.S. banks, on the other hand, produced a $25 billion gain in deposits in the same time span.

It was not until all of those news articles appeared in March and April of this year, saying that small banks were losing deposits, that the small banks actually saw a sharp drop in their deposits.

On April 28, the Bloomberg columnist, John Authers, wrote a column that was syndicated to the Washington Post. Authers included this misleading information about the four largest U.S. banks: JPMorgan Chase, Bank of America, Wells Fargo and Citigroup’s Citibank.

“This summary from the Canadian firm Palos Management explains neatly why the bigger banks are still OK:

“The first quarter’s performance of the big four was consistent with a broad consensus that the big banks have capitalized on massive depositor inflows, clearly related to the well-documented liquidity stresses facing their smaller, regionally based brethren. This should come as no surprise. The panic-fueled depositor exodus from the smaller banks to the larger ‘too big to fail’ banks is simply a rational decision. Protection of capital rules.”

“The deposit losses at JPMorgan Chase, Bank of America and Wells Fargo are more than twice what the 4,000 small banks lost in total during the same period. Their combined loss in deposits was just $210 billion…

“Bank of America and Wells Fargo not only lost those large deposit sums on a year-over-year basis, but both banks saw deposits fall during the past five quarters, including the quarter ending March 31, 2023 when headlines were declaring that they were seeing big inflows of deposits as a result of the banking crisis. JPMorgan Chase lost deposits in each of the quarters in 2022 and then saw a small increase in deposits in the first quarter of this year – likely from all of those misleading headlines. (This information is easily obtained from the financial statements the firms file publicly with the SEC.)”

Over this past weekend, the Wall Street Journal ran a big article on how the banking crisis has “only made JPMorgan stronger.” (Paywall.) Reporter David Benoit writes as follows about JPMorgan Chase’s purchase of the collapsed bank, First Republic:

“Yet JPMorgan’s show of strength, for many, exposed a weakness in the U.S. financial system. The bank and its largest rivals have become so big, their reach so extensive, that the government would almost surely step in to prevent their failure. That implicit guarantee encourages people and businesses to move their money to them in times of stress creating a feedback loop that makes big banks bigger at the expense of their smaller peers.”

The only feedback loop we’re seeing is the echo chamber of the mainstream business press.

What is not in dispute about JPMorgan Chase’s grab of First Republic Bank is the following: JPMorgan Chase was first called First Republic’s “rescuer” by the media. Then JPMorgan Chase became First Republic’s “advisor” to find strategic options for its survival. Then JPMorgan Chase put at least 800 of its employees to work on doing due diligence in order to buy First Republic for itself and get a sweetheart deal from the FDIC. The sweetheart terms of the deal include the FDIC eating 80 percent of any losses on single-family residential mortgages for 7 years and 80 percent of any losses on commercial loans, including commercial real estate, for five years. The FDIC also, bizarrely, handed JPMorgan Chase a $50 billion, five-year fixed-rate loan at an undisclosed interest rate.

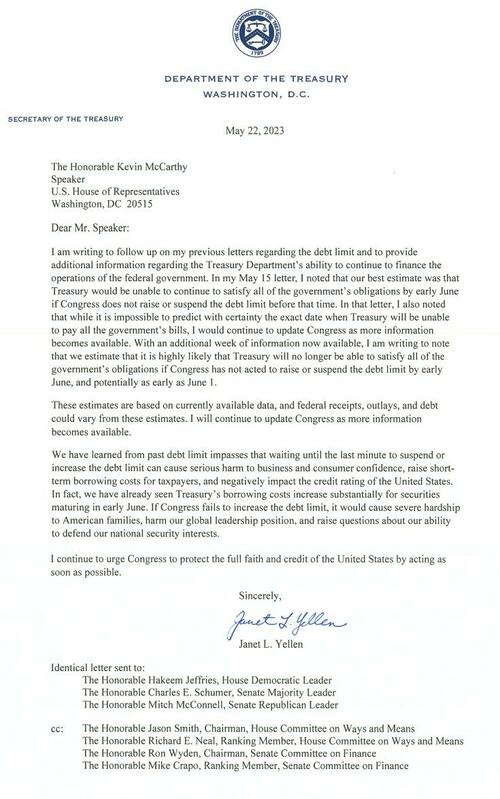

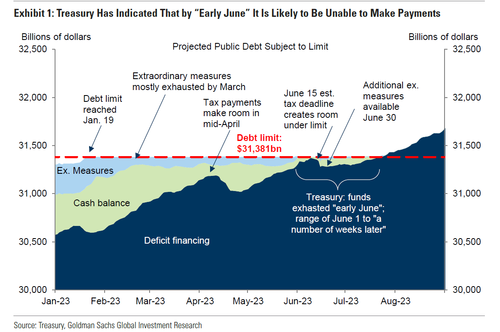

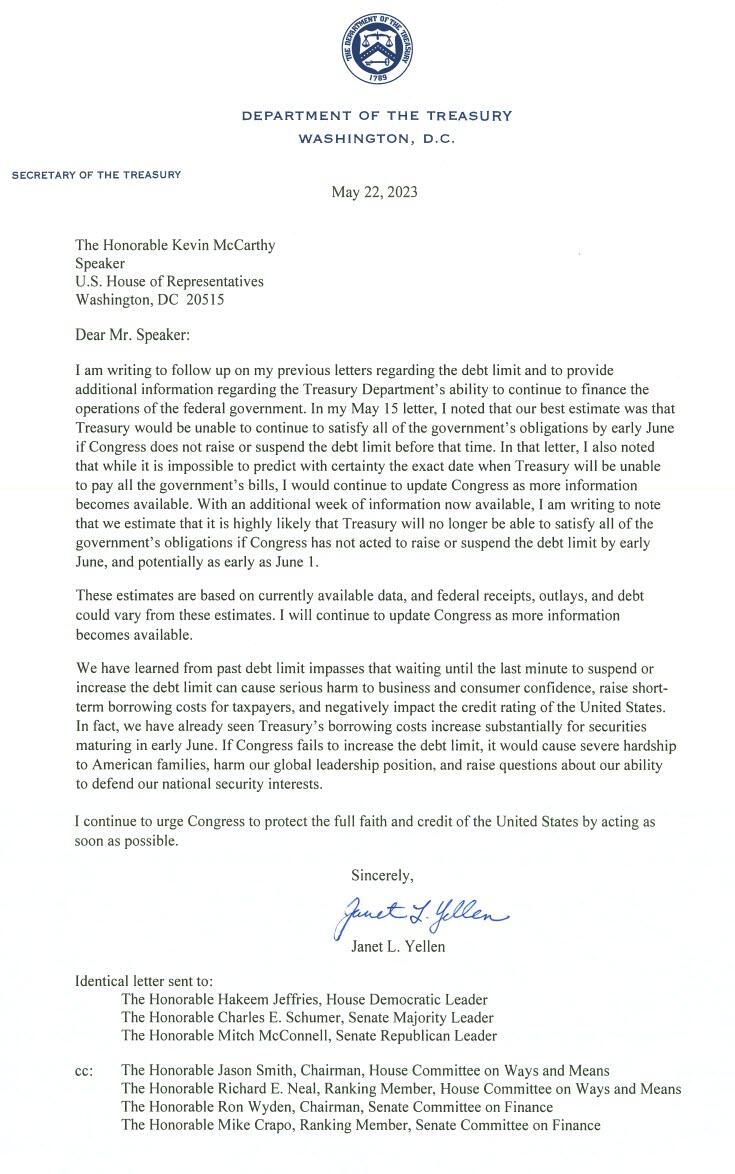

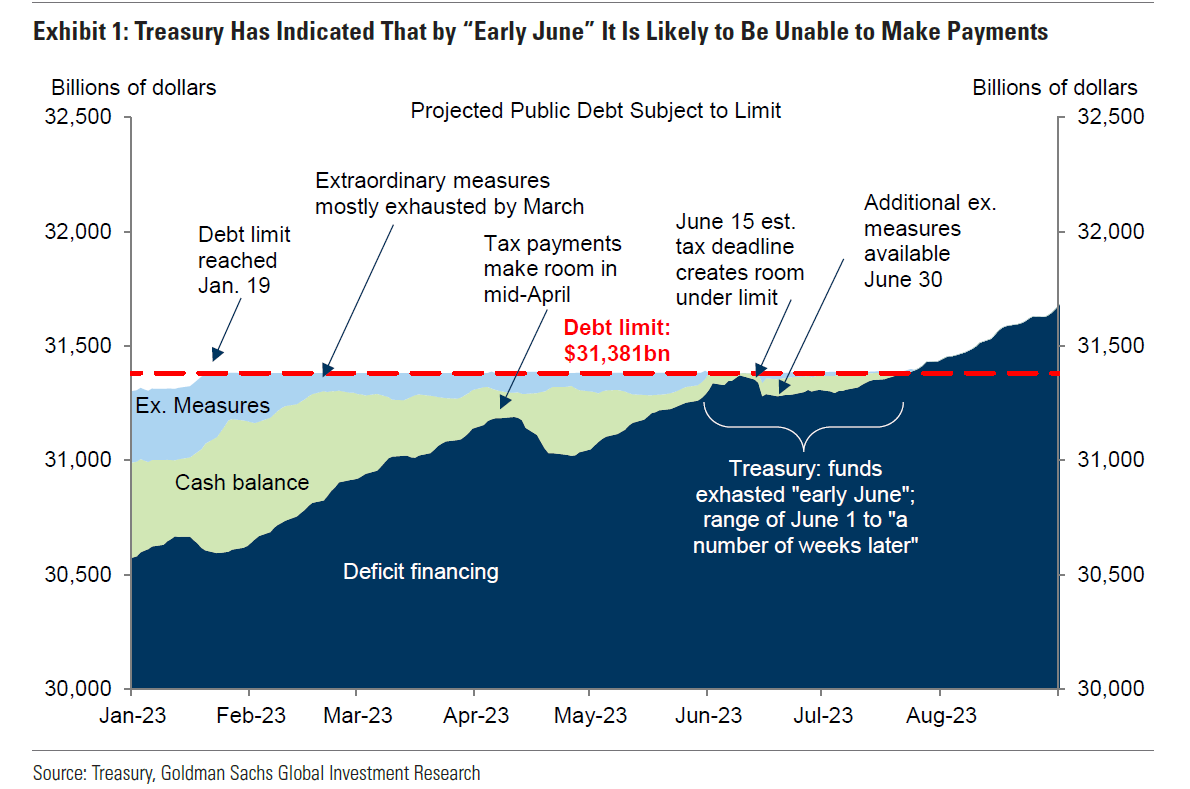

The X-DATE is the day the US Treasury goes broke, writes Jim Rickards in The Daily Reckoning.

It’s not the same as the debt ceiling but it is a consequence of the failure of Congress to raise the debt ceiling.

Right now, the Treasury is at the debt ceiling. That means it has no legal authority to issue net new debt. It can issue new debt if old debt is maturing. That keeps the total debt unchanged; you’re just rolling over maturing debt into new debt without increasing the total debt.

The problem is that the US is running $2 trillion per year deficits. It’s not enough to just roll over existing debt. You have to issue new debt to finance the deficits and that’s where the debt ceiling bites.

How is the US Treasury paying its bills today without new debt? They’re playing shell games, playing fast and loose.

There is some net cash flow from tax collections in the April time frame although that’s being rapidly depleted by tax refunds. There are some other tax collections including excise taxes.

The Treasury has some slush funds including the Exchange Stabilization Fund (ESF), currently over $100 billion. The ESF was created in 1934 using the profits from FDR’s confiscation of gold at $20 per ounce and subsequent revaluation to $35 per ounce.

It has been used numerous times including in the 1994 Mexican bailout that Congress refused to authorize (ESF use has no congressional oversight).

Recently part of the ESF was used to bail out Silicon Valley Bank. But eventually even the cash flow and the slush funds run out of juice. Then the Treasury goes broke. That’s the X-Date.

Treasury Secretary Janet Yellen recently estimated the X- Date is June 1. Yellen knows little about monetary or fiscal policy and her June 1 date was probably a political ploy to put pressure on Republicans to raise the debt ceiling without conditions, as favored by the White House.

We shouldn’t rely on Yellen’s estimates; she’s not very competent at this. That’s being generous. She’s over her skis. All the same, there is an X-Date and it’s coming sooner rather than later.

Most investors are ignoring this development and are assuming that Congress will strike a deal with the White House, raise the debt ceiling and make the X-Date go away (for now). Well, all I can say is don’t be so sure.

J.P.Morgan has actually convened a war room that will soon be meeting three times per day to deal with the fallout of the X-Date and the possibility of the US missing principal and interest payments on US government securities or possibly skimping on Social Security payments or other entitlements.

They’re obviously taking the X-Date seriously, even if investors aren’t.

Whether the X-Date arrives or not, investors should at least be prepared for the market turmoil that will arise as the impasse between Congress and the White House comes down to the wire.

These are all short-term concerns. They’re important, but let’s zoom out toward the bigger fiscal challenges facing our nation.

Those who focus on the US national debt (and I’m one of them) keep wondering how long this debt levitation act can go on. The US debt-to-GDP ratio is basically at the highest level in history (124%), with the exception of the immediate aftermath of the Second World War. At least in 1945, the US had won the war and our economy dominated world output and production. Today, we have the debt – but without the global dominance we had in 1945.

The US has always been willing to increase debt to fight and win a war, but the debt was promptly scaled down and contained once the war was over. Today, there is no war comparable to the great wars of American history, and yet the debt keeps growing.

Debt has been increased and decreased on a regular basis over the long period of American history. But never until today was there a view that the deficit didn’t matter, and that it could be increased indefinitely.

Consider that it took the United States 193 years to accumulate its first trillion Dollars of federal debt. Amazingly, it routinely adds that much debt these days. These historic debt-management efforts have been bipartisan.

Republicans Harding and Coolidge reduced the debt; the Democrat Andrew Jackson actually eliminated the debt in 1836. Today there is bipartisan profligacy. Neither party today has the will to restore fiscal responsibility.

One party outright rejects financial responsibility altogether, the other party simply pays lip service to it. That’s why you can expect more of the same.

Although I was laughed at, I predicted that Trump would win the 2016 election. I was less sanguine about his prospects in the 2020 election, for a variety of reasons. And looking ahead? If Trump receives the 2024 Republican nomination, which I believe he will, he will face the same obstacles, only stronger.

The Deep State, the administrative state, whatever you want to call it, along with powerful factions within his own party, are moving heaven and earth to prevent Trump from getting the 2024 Republican nomination.

Regardless, we need to recognize that Trump is not some kind of fiscal conservative. He isn’t. And he wasn’t. He wasn’t a Paul Ryan Republican, whatever you think of Paul Ryan.

Regardless, today, in 2023, it doesn’t matter. Why not? Because the United States is going broke.

I don’t say that to be hyperbolic. I’m not looking to scare people. It’s just an honest assessment, based on the numbers.

Right now, the United States is over $31 trillion in debt. Now, a $31 trillion debt would be fine if we had a $50 or $60 trillion economy. The debt-to-GDP ratio in that example would be manageable.

But we don’t have a $50 or $60 trillion economy. We have about a $23 trillion economy, which means our debt is much, much bigger than our economy.

This is a question that I’ve asked before, but I need to ask it again: When is the debt-to-GDP ratio too high? When does a country reach the point that it either turns things around – or ends up like Japan?

As I’ve explained in previous articles, economists Ken Rogoff and Carmen Reinhart carried out a long historical survey going back 800 years, looking at individual countries, or empires in some cases, that have gone broke or defaulted on their debt.

They put the danger zone at a debt-to-GDP ratio of 90%. Once it reaches 90%, they found, a turning point arrives. At that point, a Dollar of debt yields less than a Dollar of output. Debt becomes an actual drag on growth. Again the current US debt-to-GDP ratio is about 124%.

We are deep into the red zone, that is. And we’re only going deeper. The US has a 124% debt-to-GDP ratio, trillion- Dollar deficits are on the way, more spending is on the way.

We’re getting more and more like Japan, with its lost decades. We’re heading for a sovereign debt crisis in one form or another. That’s not an opinion; it’s based on the numbers.

Many nations around the world are actively seeking payment alternatives to the Dollar, which has only been accelerated by the unprecedented sanctions against Russia.

The process is well underway, which has of course been accelerated by the drastic US-led sanctions against Russia.

The world wants a change. I keep thinking about the saying widely attributed to Lenin: “There are decades where nothing happens; and there are weeks where decades happen.”

These days, it seems like decades are happening in days.

3,Chris Powell of GATA provides to us very important physical commentaries

India to withdraw 2,000-rupee notes from circulation

Submitted by admin on Sat, 2023-05-20 09:18Section: Daily Dispatches

By Ira Dugal and Aftab Ahmed Reuters Saturday, May 20, 2023

MUMBAI — India will start withdrawing its highest value currency notes from circulation, the central bank said on Friday, in a move that economists said could boost bank deposits at a time of high credit growth.

The withdrawal of 2,000-rupee ($24.5) notes — which the finance ministry’s top official, T.V Somanathan, said would not cause disruption “either in normal life or in the economy” – also comes ahead of elections in four large states at the end of the year and a national ballot in spring 2024.

Most of India’s political parties are believed to hoard cash in high denomination bills to fund election campaign expenses to get around tough spending limits imposed by the Election Commission.

Announcing the withdrawal, the Reserve Bank of India (RBI) said evidence showed the denomination was not being commonly used for transactions.

The notes will remain legal tender, it added, but people will be asked to deposit and exchange them for smaller denominations by Sept. 30.

“The stock of banknotes in other denominations continues to be adequate to meet the currency requirement of the public,” the RBI added in a statement.

The 2,000 rupee note was introduced in 2016 after the Narendra Modi-led government abruptly withdrew 500 and 1000 rupee denominations in an effort to remove forgeries from circulation.

There is little evidence that plan succeeded, but the move did create a systemic shortage of cash by taking away 86% of the economy’s currency in circulation by value overnight.

The government began issuing new 500 rupee notes days later, and added the 2,000 to replenish currency in circulation at a faster pace. …

By Andy Verity British Broadcasting Corp., London Monday, May 22, 2023

UK and US regulators were told of a state-led drive to “rig” interest rates in the 2008 financial crisis, but covered it up, evidence indicates.

Documents suggest lenders sharply dropped their interest-rate estimates after pressure from central banks.

Evidence was not shown to juries at the time when bankers were jailed for smaller-scale interest-rate “rigging.”

Regulators said they had followed disclosure rules, declined to comment or in one case rebutted the claims.

Some evidence has previously emerged of Bank of England and UK government involvement in manipulation of interest rates. But the evidence indicating that it was part of a broader, international drive not just by the UK but by central banks across the Western world to push key interest rates down in October 2008 has never been published before.

The evidence indicates that in October 2008 central banks including the Bank of England, the Banque de France, the European Central Bank, Banca d’Italia, Banco de Espana, and the Federal Reserve Bank of New York intervened on a large scale in the setting of Libor and Euribor.

At the height of the 2008 financial crisis, when bank lending had almost ground to a halt, central banks around the world urged calm. But my investigation reveals evidence that, behind the scenes, they were pulling levers to restore calm artificially — measures that would later be ruled to be against the law in the UK. …

Submitted by admin on Sat, 2023-05-20 09:00 Section: Daily Dispatches

9a ET Saturday, May 20, 2023

Dear Friend of GATA and Gold:

London metals trader Andrew Maguire, speaking with Shane Morand on this week’s “Live from the Vault” program from Kinesis Money, says central banks, excepting the Federal Reserve, are positioning themselves for an upward revaluation of gold, that the price for physical gold in China is already substantially higher than the nominal price in the West, and that suppression of gold prices on the New York Commodities Exchange is being exploited to drain gold out of London.

Rehypothecated Gold HELL! Live From The Vault Ep:123

In this week’s Live from the Vault, Andrew Maguire brings us up to date on the escalating battle between physical and paper gold, the current price dip, and how the trapped Federal Reserve might be able to get out of its predicament. …

END

5.IMPORTANT COMMENTARIES ON COMMODITIES:

END

end

5 B GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS// FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.0293

OFFSHORE YUAN: 7.0418

SHANGHAI CLOSED UP 12.93 PTS OR 0.39%

HANG SENG CLOSED UP 227.66 PTS OR 1.17%

2. Nikkei closed UP 278.47 PTS OR 0.90%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 103.04 EURO RISES TO 1.0815 UP 22 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.382 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 138.27 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.430***/Italian 10 Yr bond yield FALLS to 4.274*** /SPAIN 10 YR BOND YIELD FALLS TO 3.471…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 3.364

3j Gold at $1973.40 silver at: 23.76 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 3 /100 roubles/dollar; ROUBLE AT 80.03//

3m oil into the 71 dollar handle for WTI and 75 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 138.27 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .382% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8961 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9689 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.675 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 3.933 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.2493 DOWN 4 BASIS PTS

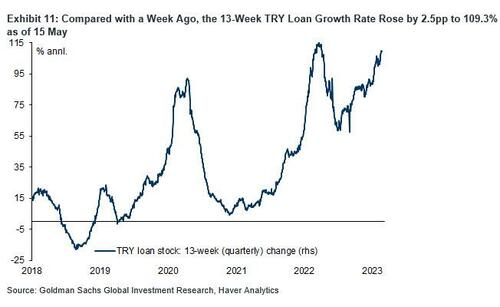

USA DOLLAR VS TURKISH LIRA: 19.83…

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.0525 UP 6 BASIS PTS

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Flat As Fractured Debt Ceiling Discussions Resume

MONDAY, MAY 22, 2023 – 08:18 AM

US futures are flat as we start a new week and inch closer to the debt ceiling x-date: as a reminder, according to Janet Yellen the US could be in default in just 10 days. At 8:00am ET , S&P futures were up 0.1%, near session highs, after trading in a narrow range overnight; the tech-heavy Nasdaq was pressured by losses on semiconductor stocks after China said products from Micron Technology had failed a cybersecurity review. Micron shares dropped more than 5% in New York premarket trading, dragging down other chipmakers, including Nvidia and Qualcomm. Asian markets are higher, while European stocks trade near session lows. Bond yields are higher, rebounding from session lows, while the USD is slightly in the green with commodities also erasing earlier losses. MegaCap Tech names are up slightly pre-market. McCarthy and Biden spoke on Sunday and will resume negotiations today. Fed’s Kashkari, a Fed dove turned hawk (and soon to turn dove again) is now open to holding rates steady in June; OIS now sees more than 80% odds of a pause at the June mtg. Biden expected ties with China to improve very shortly and considers lifting sanctions on Chinese Defense Minister.

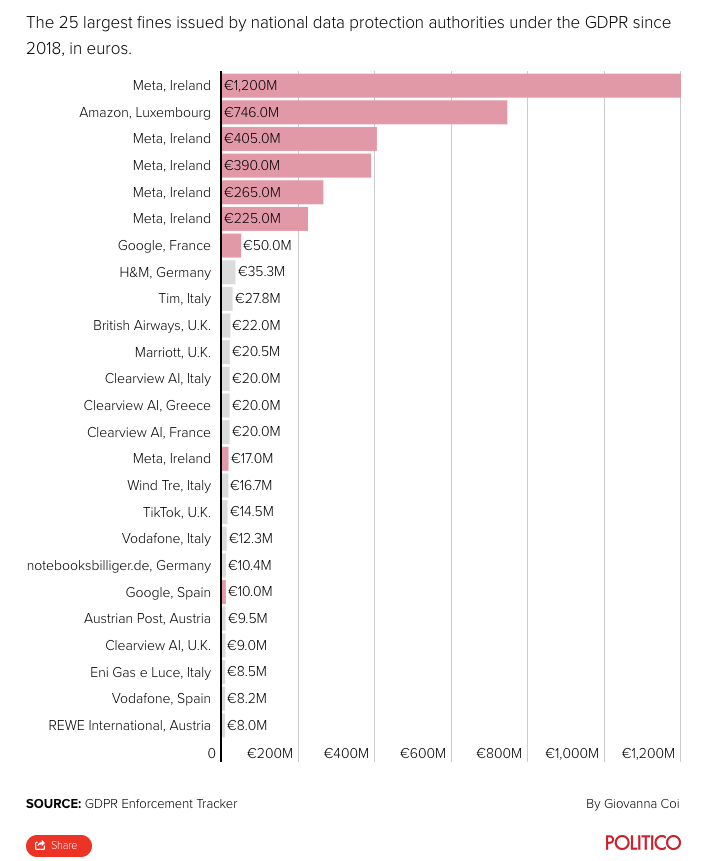

In premarket trading, Micron dropped 4.3%, leading fellow US semiconductor stocks, lower, after China said that the memory- chipmaker’s products have failed to pass a cybersecurity review in the country and banned it as a supplier. Meta Platforms fell more than 1.5%, after being hit with a record €1.2 billion ($1.3 billion) European Union privacy fine. Apple slipped 1% as Loop Capital downgrades to hold, saying it sees a revenue downside risk. WeWork gained 4.8% as the beleaguered real estate company recouped some of the declines from last week’s four-session losing streak; for context it is trading at 22 cents a share. Here are some other notable premarket movers:

Avrobio soars 63% on plans to sell its cystinosis gene therapy program for $87.5 million in cash.

DraftKings gains 3.1% after UBS upgrades its rating to buy based on stronger revenue growth and greater flow through to Ebitda.

Foot Locker is down 2.3% as Citi downgraded its rating to neutral following the athletic retailer’s significant guidance cut on Friday.

Intercept Pharmaceuticals shares tumble 15% after the company’s obeticholic acid failed to win the support of a panel of FDA advisers.

Meta Platforms shares are down 1% as the company was hit by a record $1.3 billion European Union privacy fine and given a deadline to stop shipping users’ data to the US after regulators.

Nike slips 2.1% after Williams Trading cuts the recommendation on the sportswear company to sell on the expectation that the US business will remain challenged through at least the first half of fiscal 2024.

PacWest Bancorp one of the regional US lenders that was engulfed in turmoil earlier this month, rises 4% after agreeing to sell a $2.6 billion portfolio of 74 real estate construction loans as part of its plan to shore up liquidity.

Revolve Group (RVLV) declines 2.5% after TD Cowen downgrades its recommendation on the e- commerce retailer, saying the company’s growth has cooled and that it sees limited near-term catalysts.

VectivBio rises 39% after agreeing to be purchased by Ironwood for $17/share in an all-cash transaction.

Zions Bancorp gains 2% as Hovde Group initiated coverage with an outperform, saying “misplaced fears” drove a discounted valuation.

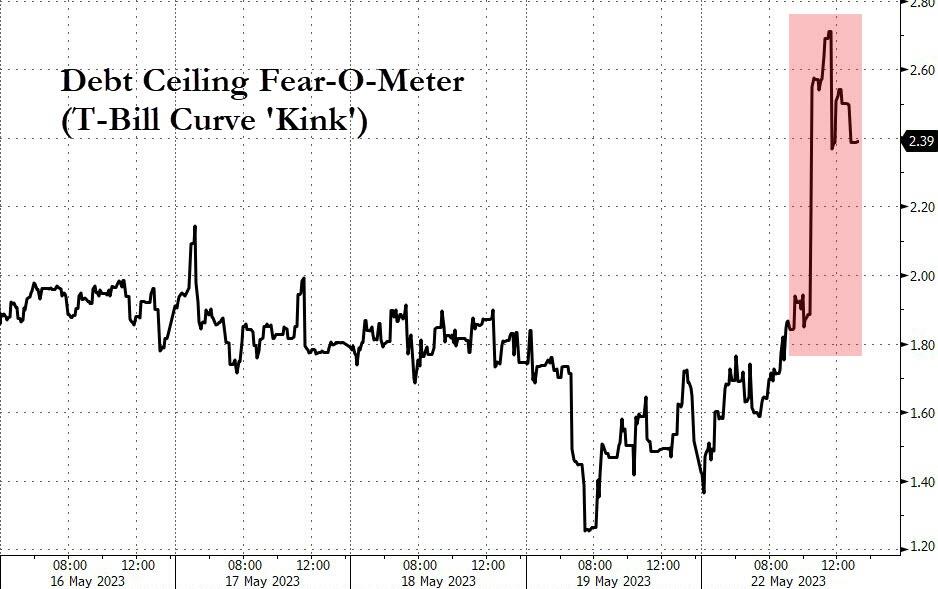

The question for investors is whether US politicians will be able to reach a deal to raise the debt limit before the government runs out of money. Stocks gave up gains late on Friday after Republicans temporarily walked out. The urgency of the situation was underscored on Sunday by Treasury Secretary Janet Yellen, who said the chances are “quite low” that the US can pay all its bills by mid-June.

“There is a lot of showmanship around the debt ceiling,” said Sarah Hewin, senior economist at Standard Chartered Plc in London. “The closer we get to June 1 without a resolution, the greater the risk of an accident so there is a lot of potential for markets to get concerned.”

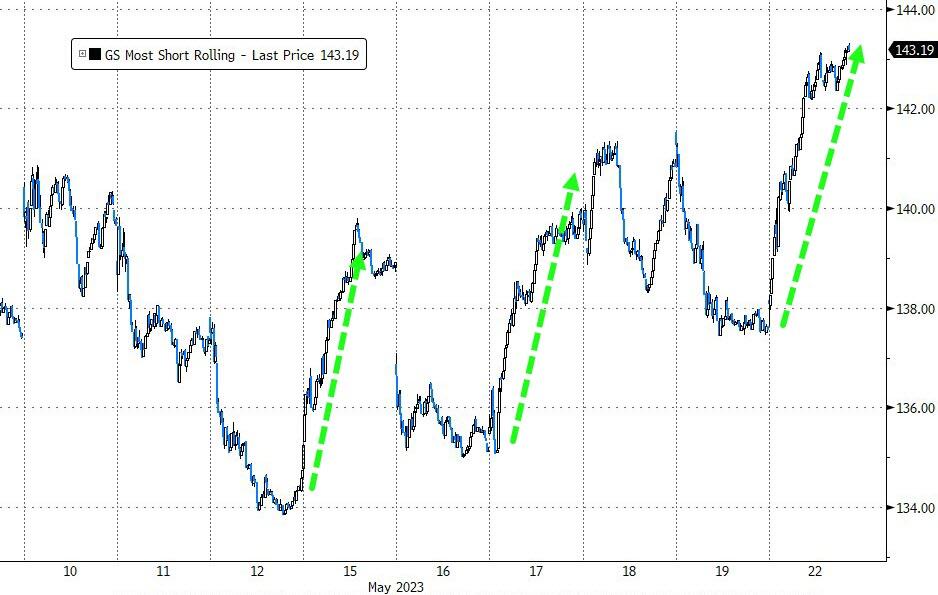

The debt-ceiling risks as well as concern for the US economy have induced investors to boost bearish positions on the S&P 500 to the highest since 2007.

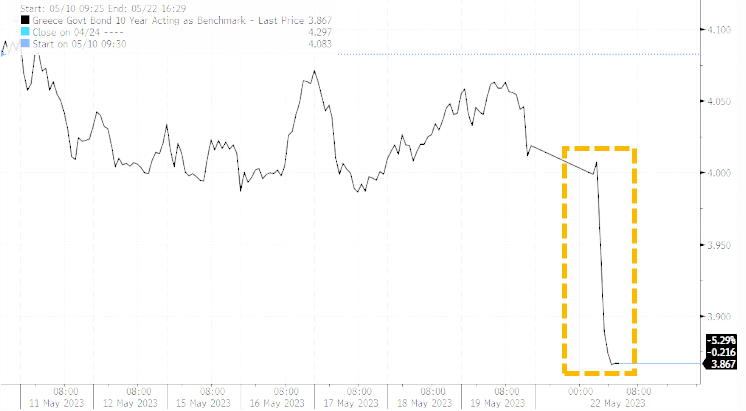

European stocks are lower as investors remain hesitant amid the ongoing US debt-ceiling negotiations. The Stoxx 600 is down 0.3%, trading near session lows with telecommunication and utilities the best-performing sectors. Greek markets were a bright spot after Sunday’s national election resulted in a strong showing for Prime Minister Kyriakos Mitsotakis, signaling that investment-friendly policies will continue. Here are the most notable European movers:

Ryanair shares rise as much as 2.5% after it reported a beat on net income in its FY results, driven by the low-cost airline’s better-than-expected pricing in 4Q, up around 26% versus 2019, says Citi. Analysts also welcome the confident outlook.

Dassault Systemes shares gain as much as 3.6% to the highest level since September. Stifel says in a note that strong software sales at Siemens, which reported earnings last week, bode well for Dassault Systemes.

Man Group shares rise as much as 2%, touching the highest since May 2, after BNP Paribas Exane raised the hedge fund manager to neutral from underperform on a more balanced risk-reward.

Begbies Traynor shares rise as much as 2.3% after the restructuring advisory firm releases a pre-close statement which Canaccord says indicates a strong finish to the year.

Polymetal shares slump as much as 37% after the London- listed gold miner’s Russian unit was sanctioned by the US. Top Russian gold miner Polyus PJSC and Polymetal JSC, Polymetal International’s Russian unit, were targeted.

Dechra shares fall as much as 8.7%, the most since February, after the UK pharmaceuticals firm said it has experienced a “more volatile and challenging” trading environment during the January to April period than previously predicted.

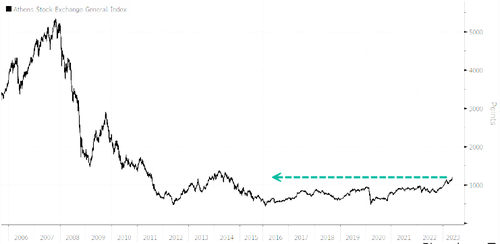

The benchmark Athens Stock Exchange General Index jumped to its highest level in almost a decade. The premium investors demand to hold Greek 10-year debt compared with super-safe bonds of Germany, fell to the lowest in more than a year while the cost of insuring exposure to Greek debt fell sharply, according to data from S&P Markit.

The MSCI Asia-Pacific Index closed higher by 0.7% for the day. A sub-gauge for technology stocks gained 2.2%, its biggest jump since March 31, tracking similar gains in peers in Asia and the US. Metal stocks surged after US President Joe Biden hinted at improving ties with China, which lifted outlook for the sector. Investors are keen to see however on how China’s economy is faring after its knee-jerk rebound following the removal of Covid curbs. Iron ore futures dropped for the third day in a row on signs of disappointing steel demand from the construction sector, while the most recent batch of industrial and retail sales data was unexpectedly soft.

Hang Seng and Shanghai Comp. traded higher albeit with the mainland choppy after mixed commentary from the G7 and frictions related to China’s ban on Micron from key infrastructure, while the PBoC provided no surprises and kept its benchmark lending rates unchanged with the 1-year and 5-year LPRs kept at 3.65% and 4.30%, respectively.

Nikkei 225 was indecisive as the momentum from its recent rally to 33-year highs initially waned and with the mood also clouded by the surprise contraction in Machinery Orders, although the index later caught a second wind and broke above the 31,000 level.

Indian stocks rose after a rally in technology and base metal firms helped key stock gauges end higher for the second successive day on Monday. The S&P BSE Sensex rose 0.4% to 61,963.68 in Mumbai, while the NSE Nifty 50 Index advanced 0.6% to 18,314.40. Shares of Adani Group soared, extending their gains from Friday, after the SEBI told a Supreme Court-appointed panel that it found no conclusive evidence of stock price manipulation in the conglomerate’s stocks. Flagship Adani Enterprises jumped 18.9% and the market value of the entire group swelled by $9.7 billion. Infosys Ltd. contributed the most to the index gain, increasing 1.9%.

ASX 200 was subdued amid weakness in financials although losses were cushioned amid the improving trade environment between Australia and its largest trading partner as evidenced by an 89% rise in coal exports to China.

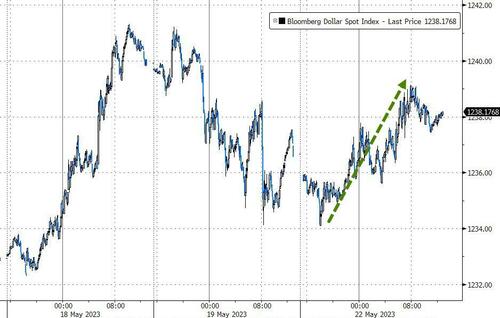

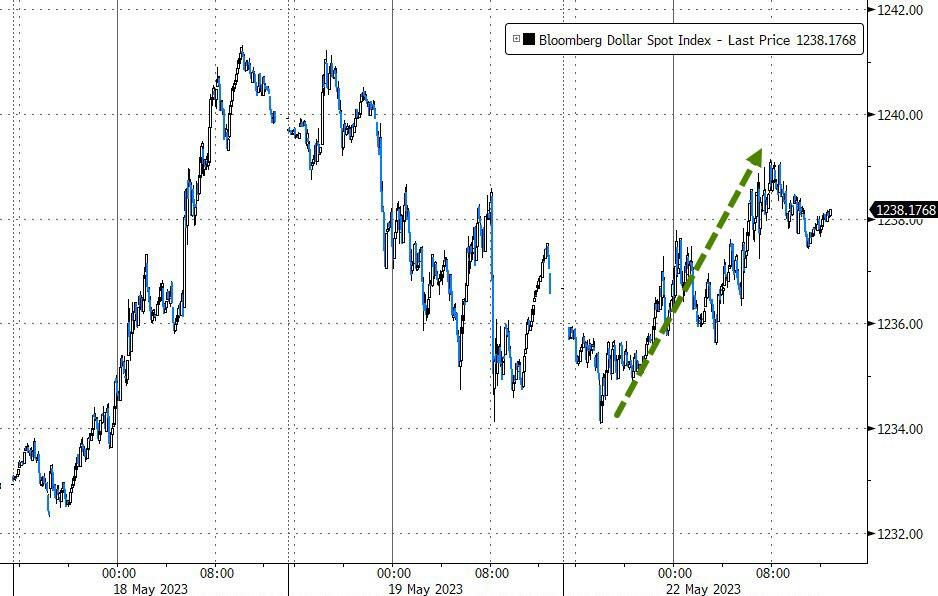

In FX, the Bloomberg Dollar Spot Index is down 0.1% while the Swiss franc is the clear outperformer among the G-10s, rising 0.5% versus the greenback. The Aussie dollar is the weakest.

Money markets bet on 5bps of Fed tightening in June but add to easing wagers beyond after Minneapolis Fed President Neel Kashkari said in an interview with Dow Jones that he may support holding interest rates at current levels in June. His comments echoed remarks from Fed Chair Jerome Powell that gave a clear signal he is inclined to pause interest-rate increases next month. “Cracks may be showing in the FOMC’s rate hike path, and markets are pricing the new information in,” said Mingze Wu, an FX trader at StoneX Group.

In rates, treasuries are flat with the US 10-year yield unchanged at 3.67%, with yields rising modestly from session lows of 3.65%; 2s10s, 5s30s spreads are steeper by ~1bp. Bunds and gilts are also in the green. Sentiment continues to take cues from debt-ceiling negotiations, with President Joe Biden and Republican House Speaker Kevin McCarthy planning to meet Monday. On Sunday, Secretary Janet Yellen said the chances are “quite low” that the US can pay all its bills by mid-June. IG issuance slate includes NWB 5Y SOFR; expectations are for $15b to $20b in new bond sales this week, concentrated on Monday. Treasury auctions this week include 2-, 5- and 7-year sales over Tuesday, Wednesday and Thursday. Three-month dollar Libor -1.80bp at 5.37471%.

In commodities, crude futures are little changed with WTI trading near $71.55. Spot gold rises 0.1% to around $1,980

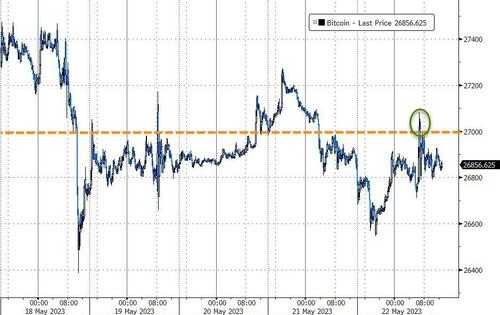

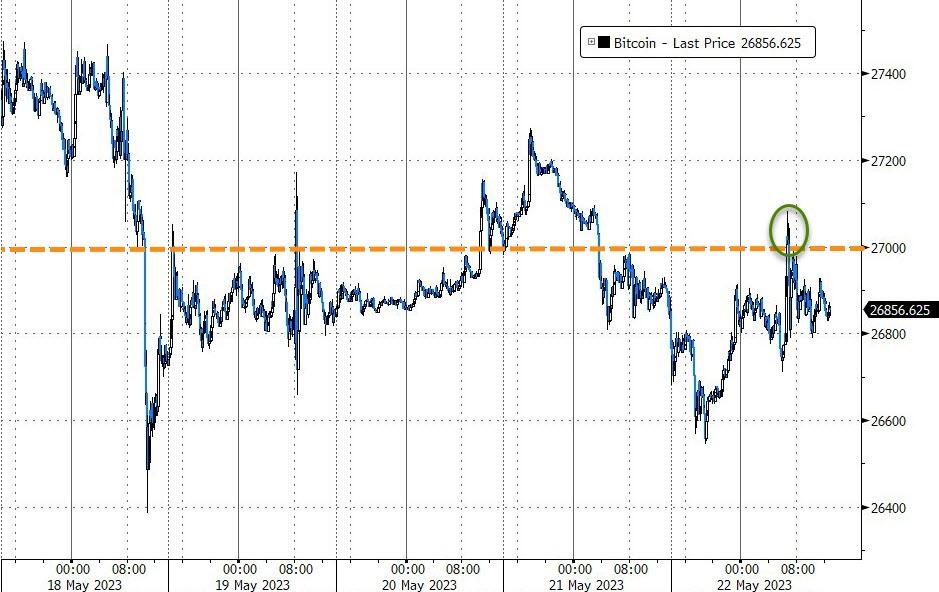

Bitcoin is essentially unchanged trading around $27K, as specifics remain somewhat light and the broader markets focus on a number of moving parts but primarily the US debt ceiling, with Biden and McCarthy to speak today at some point.

There is nothing on today’s economic calendar, later this week we get the latest FOMC minutes release, revisions to 2Q GDP and the PCE deflator.

Market Snapshot

S&P 500 futures little changed at 4,205.00

MXAP up 0.7% to 163.16

MXAPJ up 0.5% to 515.79

Nikkei up 0.9% to 31,086.82

Topix up 0.7% to 2,175.90

Hang Seng Index up 1.2% to 19,678.17

Shanghai Composite up 0.4% to 3,296.47

Sensex up 0.3% to 61,926.65

Australia S&P/ASX 200 down 0.2% to 7,263.25

Kospi up 0.8% to 2,557.08

STOXX Europe 600 up 0.2% to 469.60

German 10Y yield little changed at 2.41%

Euro little changed at $1.0802

Brent Futures little changed at $75.52/bbl

Gold spot down 0.0% to $1,976.92

U.S. Dollar Index little changed at 103.23

Top Overnight News

China said it uncovered “relatively serious” cybersecurity risks in Micron products sold in the country, and warned makers of key infrastructure to avoid using the company’s memory chips. BBG

The EU has said the bloc will push ahead with plans to jointly buy hydrogen and critical raw materials after its first attempt at aggregated gas purchases was oversubscribed. FT

China left its 5 and 1-year Loan Prime Rates unchanged, a move that was widely expected. RTRS

Ukrainian President Volodymyr Zelenskiy suggested his country was losing control of Bakhmut after months of fierce fighting but downplayed Russian claims it now fully occupied the eastern city. BBG

G-7 leaders struggled to win over swing nations being courted by China and Russia at a weekend summit in Japan. A surprise visit from Volodymyr Zelenskiy gave him a chance to appeal to those who’ve been neutral on the war. He met with India’s Narendra Modi and Indonesia’s Joko Widodo, but a meeting with Brazil’s Lula da Silva fell through. BBG

Treasury Secretary Janet Yellen said the US is unlikely to reach mid-June and still be able to pay its bills, underscoring the urgency of the White House reaching a deal with Republicans to raise the debt limit. BBG

Auto inventory levels are back on the rise following years of shortages thanks to normalizing supply chain conditions and improved production. WSJ

Fed now seen cutting rates in Q1:24 instead of Q4:23 according to an updated survey from the National Association for Business Economics (NABE). RTRS