MAY 26/GOLD CLOSED UP $0.90 TO $1944.45//SILVER CLOSED UP $0.32 TO $23.25//PLATINUM CLOSED UP $0.55 DOLLARS TO $1026.50/PALLADIUM CLOSED UP $25.35 TO $1431.85//A MUST VIEW: ANDREW MAGUIRE INTERVIEWING PETER GRANDICH//NO DEAL YET ON THE DEBT CEILING//RUSSIA VS UKRAINE UPDATES/COVID UPDATES//DR PAUL ALEXANDER/VACCINE IMPACT/SLAY NEWS/EVOL NEWS//UPDATES ON DEBT CEILING FIASCO IN THE USA//FED’S FAVOURTE INDICATOR IN INFLATION , THE PCE DEFLATOR RED HOT//ANOTHER GREAT COMMENTARY FROM VICTOR DAVIS HANSON//SWAMP STORIES FOR YOU TONIGHT//

323 C HSBC 120 363 H WELLS FARGO SEC 10 657 C MORGAN STANLEY 2 661 C JP MORGAN 36 905 C ADM 13 991 H CME 83

TOTAL: 132 132 MONTH TO DATE: 2,690

JPMorgan stopped o/100 contracts

FOR MAY:

GOLD: NUMBER OF NOTICES FILED FOR MAY/2023. CONTRACT: 1 NOTICES FOR 100 OZ or 0.003110 TONNES

total notices so far: 6140 contracts for 614,000 oz (19.094 tonnes)

FOR MAY:

SILVER NOTICES: 132 NOTICE(S) FILED FOR 640,000 OZ/

total number of notices filed so far this month : 2690 for 13,450,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP UP $0.90

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

/NO CHANGES IN GOLD INVENTORY AT THE GLD:////

INVENTORY RESTS AT 941.29 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 44 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 3.306 MILLIO OZ OUT THE SLV//: ; : INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 468.300 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 519 CONTRACTS TO 136,177 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS STRONG SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.32 FALL IN SILVER PRICING AT THE COMEX ON THURSDAY. TAS ISSUANCE WAS A SMALLER SIZED 542 CONTRACTS. THESE WILL BE USED FOR MANIPULATION NEXT MONTH. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY: A SMALLER 542 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS) IF A CALENDAR SPREAD OCCURS. IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED THE COMPLAINT. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.32). BUT WERE UNSUCCESSFUL IN KNOCKING SOME SPEC LONGS AS WE HAD A HUGE GAIN ON OUR TWO EXCHANGES OF 1554CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 6.750MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION. WE WILL HAVE IN OUR FINAL WEEK IN THE DELIVERY CYCLE MORE MANIPULATION IN OUR PRECIOUS METALS DUE TO COMEX SPREADERS LIQUIDATION ACCOMPANYING OPTIONS EXPIRY ON BOTH THE COMEX AND LONDON’S LBMA ALONG WITH AN ADDED FEATURE OF TAS LIQUIDATION.

WE MUST HAVE HAD:

A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS( 1035 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.105 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 45,000 OZ (E.F.P. JUMP LOWERS THE AMOUNT OF SILVER STANDING)+0 MILLION OZ EXCHANGE FOR RISK ISSUED TODAY// TOTAL FOR THE MONTH 6.75MILLION OZ OF EXCHANGE FOR RISK (RAISES THE AMOUNT OF SILVER STANDING):THUS TOTAL OF 20.200 MILLION OZ OF SILVER STANDING FOR DELIVERY V) STRONG SIZED COMEX OI GAIN/ HUGE SIZED EFP ISSUANCE/VI) SMALLER NUMBER OF T.A.S. CONTRACT INITIATION (542 CONTRACTS)//CONSIDERABLE T.A.S LIQUIDATION MANIPULATING THE PRICE SOUTHBOUND THURSDAY.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -removed 81CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTRACTS for 20 days, total 12,810 contracts: OR 64.050 MILLION OZ . (640 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 64.050 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 64.050 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 581 CONTRACTS WITH OUR STRONG SIZED $0.32 LOSS IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1035 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAY OF 13.105 MILLION OZ//FIRST DAY NOTICE FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 45,000 OZ (DECREASES THE AMOUNT OF SILVER STANDING) +// + 0 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //TOTAL EXCHANGE FOR RISK MONTH= 6.75 MILLION//NEW TOTALS 13.450 MILLION OZ + 6.75 MILLION EXCH./RISK = 20.200 MILLION OZ STANDING FOR MAY// .. WE HAVE A HUGE SIZED GAIN OF 1554 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A SMALLER 542!!//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED THURSDAY. THE NEW TAS ISSUANCE WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE.

WE HAD 132 NOTICE(S) FILED TODAY FOR 640,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 10,886 CONTRACTS TO 469.026 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED – 2910 CONTRACTS

WE HAD A STRONG SIZED DECREASE IN COMEX OI ( 10,886 CONTRACTS) WITH OUR $19.70 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR MAY. AT 3.5085 TONNES ON FIRST DAY NOTICE // PLUS 100 OZ QUEUE. JUMP :(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)/+ /A SMALLER ISSUANCE OF 708 T.A.S. CONTRACTS/STRONG FRONT END OF TAS LIQUIDATION THURSDAY ////YET ALL OF..THIS HAPPENED WITH OUR $19.70 LOSS IN PRICEWITH RESPECT TO THURSDAY’S TRADING.WE HAD A GOOD SIZED LOSS OF 5073 OI CONTRACTS (15.779 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 5813 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 466,116

IN ESSENCE WE HAVE A GOOD SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5073 CONTRACTS WITH 10,886 CONTRACTS DECREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): 708 CONTRACTS) AND 5813 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 5073CONTRACTS OR 15.779TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5813 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (10,886) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 5073 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 3.5085 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 100 OZ // NEW STANDING: 19.094 TONNES+ 1.244 TONNES OF EXCHANGE FOR RISK//NEW TOTALS FOR GOLD STANDING FOR MAY: 20.338 TONNES // ///3) SOME LONG LIQUIDATION//4) STRONG SIZED COMEX OPEN INTEREST LOSS/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: SMALLER T.A.S. ISSUANCE: 708 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 68,701 CONTRACTS OR 6,870,100 OZ OR 213.68 TONNES IN 20 TRADING DAY(S) AND THUS AVERAGING: 3435 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAY(S) IN TONNES 213.68 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 213.68/3550 x 100% TONNES 6.00% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES ( MUCH SMALLER THAN LAST MONTH)

MAY: 213.68 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A STRONG SIZED 519 CONTRACTS OI TO 136,258 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 1035 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1035 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1035 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 519 CONTRACTS AND ADD TO THE 1035OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1554 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 7.770 MILLION OZ

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED UP 11.24 PTS OR 0.35% //Hang Seng CLOSED /The Nikkei closed UP 115.18 OR .37% //Australia’s all ordinaries CLOSED UP 0.24 % /Chinese yuan (ONSHORE) closed UP 7.0579 /OFFSHORE CHINESE YUAN DOWN TO 7.0685 /Oil DOWN TO 72.48 dollars per barrel for WTI and BRENT AT 76.87 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 10,998 CONTRACTS DOWN TO 466,116 WITH OUR LOSS IN PRICE OF $19.70 ON THURSDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF MAY… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 5813 EFP CONTRACTS WERE ISSUED: : JUNE 5813 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5813 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 5073 CONTRACTS IN THAT 5813LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 10,886 COMEX CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $19.70. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE),THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE TODAY WAS A MUCH SMALLER 708 CONTRACTS. DURING THIS WEEK THEY SOLD THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE).

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (20.338) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $19.70) //// AND WERE UNSUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD OUR FAIR SIZED LOSS OF 2164 CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE TAS LIQUIDATION. AND NOW FOR THE FIRST TIME TAS LIQUIDATION IS EXTENDING PAST MID MONTH. THE TAS ISSUED THURSDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 6.727PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY. (3.5085 TONNES) followed by today’s 100 oz queue jump //NEW STANDING 19.094 TONNES+1.244 exchange for risk(prior)// new total 20.338 tonnes ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $19.70

WE HAD – REMOVED 2910 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 5073 CONTRACTS OR 507,300 OZ OR 15.779 TONNES.

Total monthly oz gold served (contracts) so far this month

6140 notices 614,000 OZ 19.0974 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 1 contracts having LOST 99 contracts. We had 100 contracts filed

on THURSDAY, so we GAINED 1 contracts or an additional 100 oz will stand for gold in this non active delivery month of May

June LOST A HUGE 42,498 contracts DOWN to 69,612 contracts. We should have a strong delivery month for June (around 70 tonnes). We have 2 more reading days before first day notice.

July added 114 contracts to stand at 2917 contracts.

AUGUST GAINED 31,219 contracts UP to 336,431 contracts

We had 1 contract filed for today representing 100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2023. contract month,

we take the total number of notices filed so far for the month (6,140 x 100 oz ), to which we add the difference between the open interest for the front month of MAY (1 CONTRACT) minus the number of notices served upon today 1 x 100 oz per contract equals 614,000 OZ OR 19.094 TONNES the number of TONNES standing in this NON- active month of May. And now we must add 1.244 tonnes of gold delivery through our 400 contract exchange for risk//new total 20.338 tonnes of gold.

thus the INITIAL standings for gold for the MAYcontract month: No of notices filed so far (6,140 x 100 oz) x xxx OI for the front month minus the number of notices served upon today (1)x 100 oz} which equals 614,000 oz standing OR 19.094 TONNES + 1.244 (exchange for risk) = 20.338 tonnes

TOTAL COMEX GOLD STANDING: 20.338 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,871,329.417 OZ

TOTAL REGISTERED GOLD: 11,999,869.189 (373,24 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,871,460.228 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,295,140 OZ (REG GOLD- PLEDGED GOLD) 320.222 tonnes//

END

SILVER/COMEX

MAY 26//2023// THE MAY 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

54,679/200 oz Asahi

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

592,520.400 oz Brinks

No of oz served today (contracts)

132 CONTRACT(S) (640,000 OZ)

No of oz to be served (notices)

0 contracts (nil oz)

Total monthly oz silver served (contracts)

2690 Contracts (13,450,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 1 dealer deposit

i)Dealer deposits: 1

Into Brinks 592,520.400 oz

total dealer deposit:592,520.400 oz

total dealer deposits: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We had 0 customer deposits

Total deposits: nil oz

JPMorgan has a total silver weight: 141.313 million oz/272.132 million =51.83% of comex .//dropping fast

Comex withdrawals 1

customer withdrawals: 1

i) Out of Asihi: 54,679.280 oz

total withdrawals: 54,679.280 oz

adjustments:

Adjustments; 2 dealer to customer

i) Out of HSBC: 299,213.500 pz

ii) Out of Manfra: 607,621.500 oz

TOTAL REGISTERED SILVER: 28.881 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 272.143 million oz

CALCULATION OF SILVER OZ STANDING FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2023 OI: 132 CONTRACTS HAVING LOST 13 CONTRACT(S). WE HAD 4 CONTRACTS FILED ON THURSDAY, SO WE LOST 9 CONTRACTS OR AN ADDITIONAL 45,000 OZ WILL STAND FOR DELIVERY ON THIS SIDE OF THE POND AS THEY WERE EFP’d to LONDON WHERE THEY WILL UNDERGO THE DELIVERY PROCESS OVER THERE AS THERE SEEMS TO BE NO SILVER OVER HERE.

JUNE HAD A 1 CONTRACT loss TO 1114

JULY HAD A 756 CONTRACT LOSS TO 106,540 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 132 for 640,000 oz

Comex volumes// est. volume today 59,370 good/

Comex volume: confirmed yesterday: 67,726

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 2690 x 5,000 oz = 13,450,000 oz

to which we add the difference between the open interest for the front month of MAY(132) and the number of notices served upon today 132 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2023 contract month: 2690 (notices served so far) x 5000 oz + OI for the front month of May (132) – number of notices served upon today (132 )x 500 oz of silver standing for the MAY contract month equates to 13.450 million oz + THE CRIMINAL 0 MILLION OZ EXCHANGE FOR RISK TODAY//NEW TOTAL EXCHANGE FOR RISK: 6.750//NEW TOTAL 20.200 MILLION OZ//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MAY 26/WITH GOLD UP $.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 941.29 TONNES

MAY 25/WITH GOLD DOWN $19.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 24/WITH GOLD DOWN $9.50 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 941.29 TONNES

MAY 23/WITH GOLD $2.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 942.74 TONNES

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

MAY 9/WITH GOLD UP $9.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTER DEPOSIT OF 5.88 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 937.64 TONNES

MAY 8/WITH GOLD UP $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 931.77 TONNES

MAY 5/WITH GOLD DOWN $30.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AS DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

MAY 4/WITH GOLD UP $19.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.30 TONNES

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

GLD INVENTORY: 941.29 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 26/WITH SILVER UP $0.44 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.306 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 25.WITH SILVER DOWN $0.32 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 471.606 MILLION OZ//

MAY 24/WITH SILVER DOWN $.35 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 23/WITH SILVER DOWN 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

MAY 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A TINY DEPOSIT OF .08 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 465.682 MILLION OZ//

MAY 8/WITH SILVER DOWN 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.602 MILLION OZ//

MAY 5/WITH SILVER DOWN 31 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 466.876 MILLION OZ//

MAY 4/WITH SILVER UP 53 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF .174 MILLION OZ INTO SLV.//INVENTORY RESTS AT 467.174 MILLION OZ//

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

3,Chris Powell of GATA provides to us very important physical commentaries

UAE plus other countries are cashing in big time importing Russian gold due to the stupid sanctions. Some refiners have stopped using Russian gold and this set up the UAE with its 75 tonnes of gold in 2021 as the central hub. You can be assured that the 2022 number of gold imports to the uAE will be higher than 2021.

India will be using them to buy gold to purchase Russian oil

Submitted by admin on Thu, 2023-05-25 09:09Section: Daily Dispatches

By Peter Hobson Reuters Thursday, May 25, 2023

LONDON — the United Arab Emirates has become a key trade hub for Russian gold since Western sanctions over Ukraine cut Russia’s more traditional export routes, Russian customs records show.

The records, which contain details of nearly a thousand gold shipments in the year since the Ukraine war started, show the Gulf state imported 75.7 tonnes of Russian gold worth $4.3 billion — up from just 1.3 tonnes during 2021

China and Turkey were the next biggest destinations, importing about 20 tonnes each between Feb. 24, 2022 and March 3, 2023. With the UAE, the three countries accounted for 99.8% of the Russian gold exports in the customs data for this period.

In the days after the Ukraine conflict started, many multinational banks, logistics providers and precious metal refiners stopped handling Russian gold, which had typically been shipped to London, a gold trading and storage hub. …

New ‘In Gold We Trust Report’ explains again why gold should be going up

Submitted by admin on Fri, 2023-05-26 11:18Section: Daily Dispatches

11:19a ET Friday, May 26, 2023

Dear Friend of GATA and Gold:

The annual “In Gold We Trust” report from Ronald-Peter Stoeferle and Mark J. Valek of Incrementum AG in Liechtenstein has just been published and as usual it provides a thousand reasons why gold should be soaring in price but no explanation of why it isn’t. Apparently that job is too sensitive, risking the ire of governments, major banks, establishment news organizations, and fearful mining companies, and so must be left to GATA:

All the same, there’s a lot of interesting stuff in the report’s 417 pages. This year’s edition is titled “Showdown” and it can be found in PDF format here:

It’s time to prepare both financially and mentally. Feat. Peter Grandich

In this week’s episode of Live from the Vault, Andrew Maguire is joined by renowned author Peter Grandich who offers a holistic approach to anchoring oneself to personal responsibility and financial decision-making in a world of debt reliance.

The precious metals experts examine whether the possible US debt default could ever be paid back in the end-of-the-dollar scenario and contemplate the changing behaviours of modern society in contrast to traditional norms and values.

END

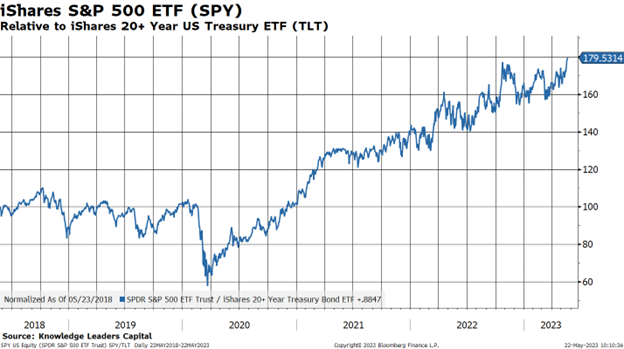

5.IMPORTANT COMMENTARIES ON COMMODITIES: COPPER//CHINESE BONDS VS STOCKS VS USA

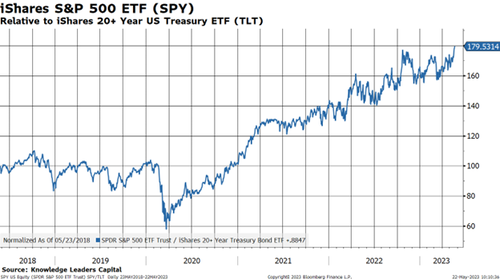

One metric I look at fairly often for various countries is the relationship between the performance of stocks vs. bonds. The idea is straightforward enough: when stocks are outperforming bonds, it tends to be associated with a growing economy. When bonds are outperforming stocks, it is a tell that there is some sort of negative dynamic going on.

Why do I bring this up? In the US, stocks—represented by the SPY ETF—have just made a new high relative to the TLT ETF (which represents long-term US Treasury bonds). This would suggest that despite all the angst over inflation, the debt ceiling, and other issues, investors seem to taking a positive perspective.

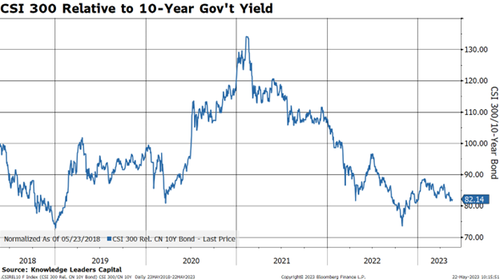

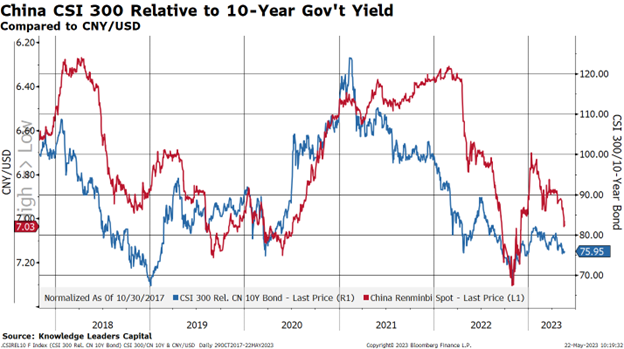

This contrasts with China. In China, stocks have underperformed government bonds by about 50% since the beginning of 2021. This suggests there could be something rotten going on underneath the surface of the Chinese economy. Debt issues, housing issues, demographic issues, and geopolitical issues all could be weighing on sentiment toward Chinese equities and growth.

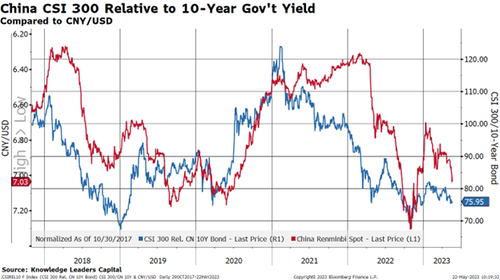

To further validate the theory that there is something rotten in China, I overlay the CNY/USD on the stock/bond chart. The CNY is weakening alongside this relationship of bonds outperforming stocks.

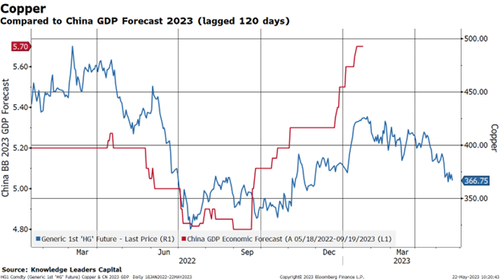

While last fall, the market began to discount the opening of China, now the dynamic seems to have changed. Copper did a good job signaling the upturn in Chinese GDP estimates for 2023.

With the Chinese reopening seeming to have less thrust than was anticipated, copper prices are falling again. This could telegraph a downturn in Chinese growth estimates.

end

5 B GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.0579

OFFSHORE YUAN: 7.0685

SHANGHAI CLOSED UP 11.24 PTS OR 0.35%

HANG SENG CLOSED

2. Nikkei closed UP 115.18 PTS OR 0.37%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 103.82 EURO FALLS TO 1.0727 DOWN 29 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.412 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 139.68 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP// OFF- SHORE:UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.5640***/Italian 10 Yr bond yield RISES to 4.392*** /SPAIN 10 YR BOND YIELD RISES TO 3.591…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 3.901

3j Gold at $1952.90 silver at: 23.17 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 2 /100 roubles/dollar; ROUBLE AT 80.03//

3m oil into the 72 dollar handle for WTI and 76 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 139.68 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .412% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9022 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9705 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.817 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 3.997 UP 1/2 BASIS PTS/

USA 2 YR BOND YIELD: 4.529 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 20.03…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.3800 UP 3 BASIS PTS (RATES RISING RAPIDLY)

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Rise On Optimism Of Imminent Debt Deal

FRIDAY, MAY 26, 2023 – 08:19 AM

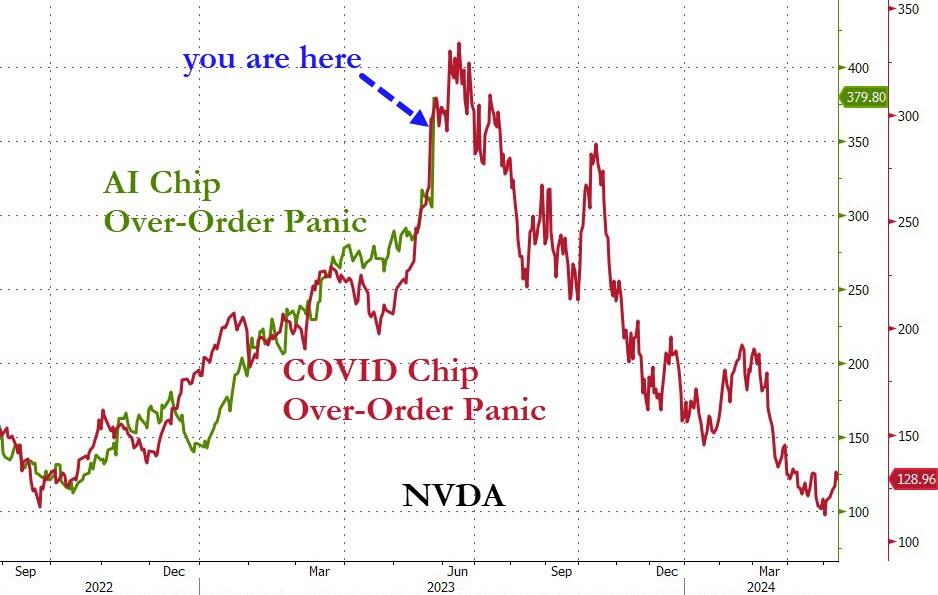

US equity futures are higher across the board, amid speculation that a debt deal is taking shape and may be announced as soon as today (whether or not a 0.2% spending cut “deal” is something to be proud about is a different matter) and also thanks to optimism around Nvidia and AI prospects. S&P futures are 0.2% higher, rising to 4,169 and undoing the drop from the previous two days, while Nasdaq futures are up 0.4% amid continued AI-bubble euphoria. Treasury yields are falling, most markedly at the short end, on debt ceiling optimism, while a measure of the dollar is weakening. Commodities are mostly higher led by base metals. Oil prices are set for a weekly gain, climbing higher today. Gold prices are edging higher but still set for their third weekly decline.

In premarket trading, Marvell Technology shares soared 17% after the chipmaker projected AI revenue in fiscal 2024 will “at least double” from a year ago. The company also reported first-quarter adjusted earnings per share that beat estimates and provided second-quarter guidance. Analysts had a positive reaction, increasing price targets on the stock. Meanwhile Nvidia shares were little-changed in US premarket trading, pausing following yesterday’s 24% surge after the chipmaker gave a bullish forecast thanks to surging demand amid an AI boom. Here are some other notable premarket movers:

Tilray Brands shares plunged 19% in premarket trading after the cannabis producer priced an offering of $150m of unsecured convertible senior notes.

Gap shares jump 11% in premarket trading after the apparel retailer produced better-than-expected earnings for the first quarter, compared to Wall Street forecasts for a sizable loss for the period. Analysts pointed toward the cost management of the company, with Jefferies saying lower expense on air freight contributed to the better margin and EPS.

Domo shares dropped 4.9% in postmarket trading after the application software company’s guidance for 2Q revenue missed the average analyst estimate, while analysts flagged the firm’s still-muted growth.

Workday shares gained 8.5% in extended trading, after the software company narrowed its subscription revenue forecast for the full year and named Zane Rowe as new chief financial officer. Analysts are positive on the report and forecast.

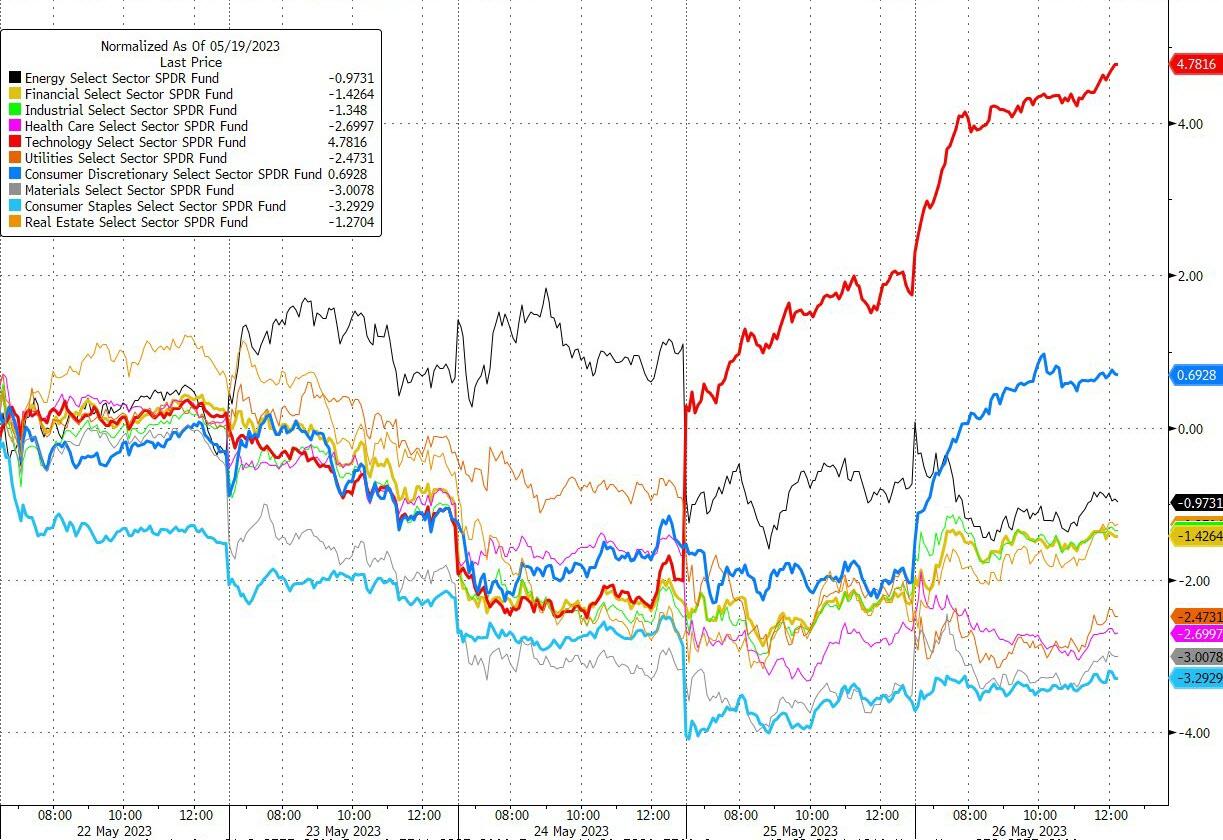

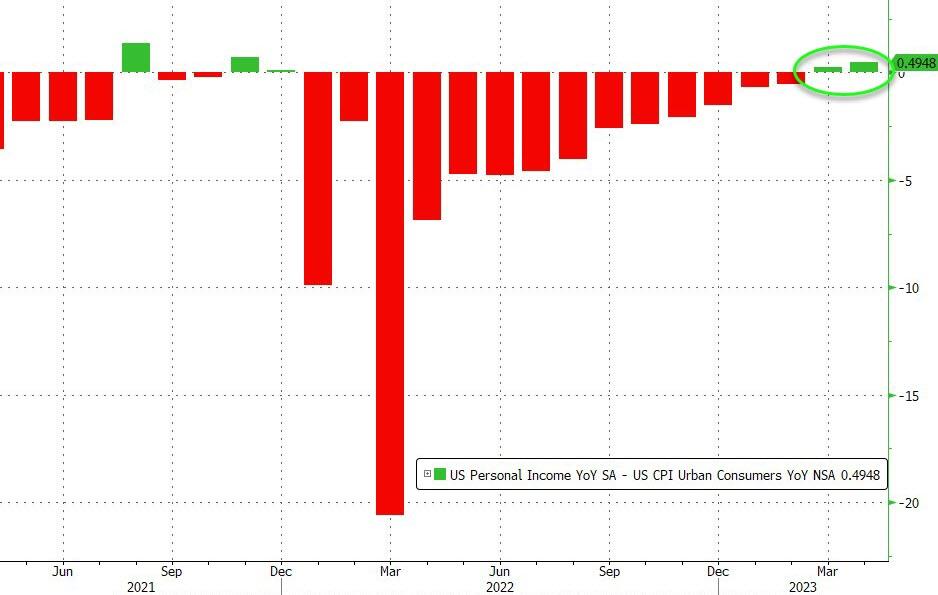

Yesterday, the Nasdaq rallied 2.5%, a 1.9-sigma move, as NVDA surged 24% amid forecast beat; XSD (Semiconductors ETF) added 4.5%. The NDX rally was driven by a narrow leadership as there are only 17 out of 100 companies outperformed the benchmark. On debt ceiling, headlines turned more optimistic as there seems to be a deal emerging, but gaps remains between the two parties. Today, macro focus will be the PCE and Durable Goods release. Optimism was also boosted by reports that a deal is emerging which could include a paltry $10bn spending cut. Today’s macro focus will be on PCE releases and Durable Goods Orders.

“We are in a very hesitant market,” said Ariane Hayate, a fund manager at Edmond de Rothschild Asset Management. The debt ceiling is “a factor that adds up nervousness, but the market isn’t expecting that no solution will be found.”

In Washington, Republican and White House negotiators have narrowed differences in talks over recent days and are moving closer to an agreement to raise the debt limit and cap federal spending for two years, according to people familiar with the matter. However, details agreed to are tentative and a final accord is still not in hand, the people said.

European stocks also rose with chipmakers including ASML Holding NV advancing for a second day. Glencore Plc advanced 2.5% after a report that Viterra unit is in talks to merge with Bunge Ltd., one of the world’s largest crop merchants. The Stoxx 600 was up 0.5% as European mining stocks rose and were among the biggest gainers on the Stoxx 600 regional benchmark as metal prices trim weekly decline, while the sector bounces on technical support and Rio Tinto gets a broker upgrade. Here are the most notable European movers:

Rio Tinto rallies as much as 4.3% in London after being upgraded to overweight from equal-weight at Morgan Stanley, which says weakness in the mining company’s shares has created an opportunity

European semiconductor equipment makers rise, extending Thursday’s blistering rally on hopes that adoption of chips used in artificial intelligence computing could accelerate the sector’s future growth

Faurecia gains as much as 5.7% and Valeo as much as 3.7% after Jefferies upgraded the firms to buy, saying auto suppliers are starting to benefit from a more supportive operating environment

Atos shares rise as much as 8.8% after the company got a favorable decision in litigation involving Syntel, now part of Atos, in the US, with Oddo calling the judgement “very favorable” at first sight

Coface jumps as much as 7.8% after reporting earnings that Deutsche Bank says could lead to mid-single-digit consensus upgrades as the French financial services company “continues to demonstrate its quality”

Asos shares rise as much as 8.9% after the UK online fast fashion retailer announced capital raising plans. The new debt financing and equity raise provide “much needed visibility on liquidity,” Citi analysts say

Casino shares slump as much as 11% after the debt-laden French retailer said a Paris court decided to open conciliation procedures amid talks with its creditors

Ninety One falls as much as 2.1% after being downgraded to underperform at Avior, which says the current market environment favors fixed-income instruments over stocks, putting equity performance at risk

Asian stocks traded mixed following the mild positive bias stateside where the tech sector surged on Nvidia’s blockbuster report and with sentiment underpinned by firm US data and progress in debt ceiling talks.

The Shanghai Comp. was subdued amid the closure of Hong Kong markets and Stock Connect trade but with the downside cushioned after the meeting between the US and China’s commerce chiefs where concerns were raised about recent actions taken against US companies in China, as well as US chip policy and export curbs

Japan’s Nikkei 225 outperformed and reclaimed the 31,000 level with the index lifted by recent currency weakness and mostly softer-than-expected Tokyo CPI, while tech stocks benefitted from the ripple effect which stemmed from the rally in US counterparts.

Australia’s ASX 200 was indecisive with price action rangebound and risk sentiment contained by disappointing Retail Sales data.

Indian stocks were the best performers among major Asian markets this week, even as investors awaited the outcome of ongoing negotiations to raise the US debt ceiling. The S&P BSE Sensex rose 1% to 62,501.69 in Mumbai, while the NSE Nifty 50 Index advanced by the same magnitude. The Sensex gained 1.3% this week, while the Nifty climbed 1.6%. The advance has mainly been supported by information technology, pharmaceuticals and consumer staple firms. Investors kept a close eye on US debt-ceiling talks. Republican and White House negotiators are making progress toward a deal to raise the debt limit. Strategists warn that any break down in negotiations could have serious implications for global economic growth.

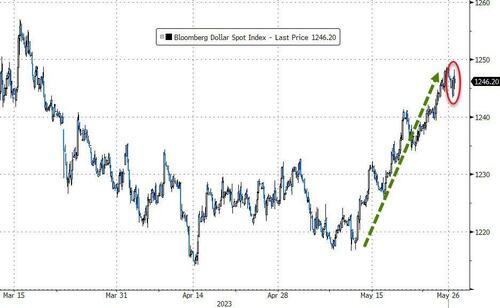

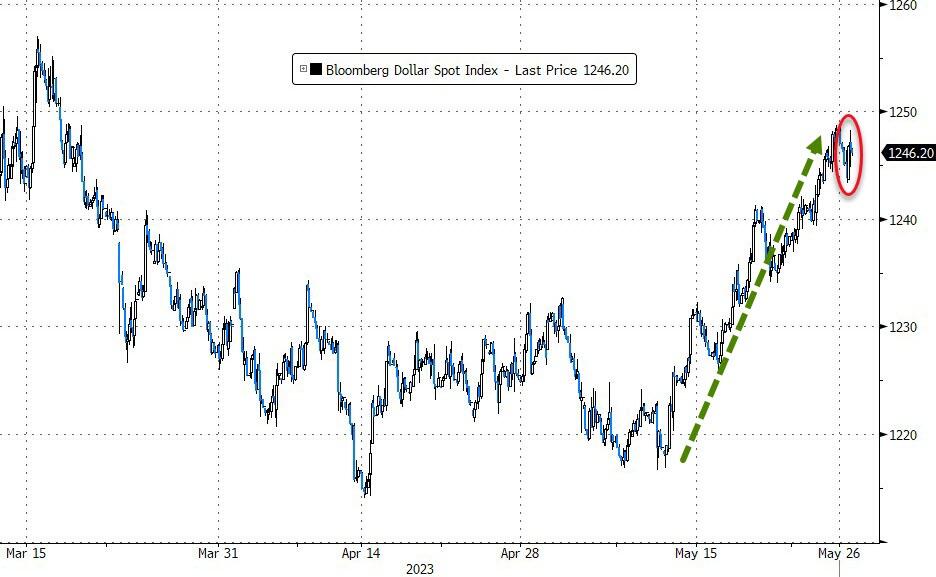

In FX, the Bloomberg Dollar Spot Index is also lower by 0.2%, snapping a four-day run of gains; it is on course to end the week in positive territory, posting its third straight week of gains. The Swedish krona is the best performer among the G-10’s. The Bloomberg Dollar Spot Index edged down 0.2%, USD/JPY slipped 0.3% on easing Treasury yields and as Japan’s 10-year breakeven inflation rate hit an eight-year high.

In rates, Treasuries are richer across the curve with gains led by front-end, steepening spreads from Thursday’s close. US session focus includes a flood of economic data, headed by PCE deflator at 8:30am New York. US yields richer by up to 5bp across front-end of the curve with 2s10s, 5s30s spreads flatter by 1bp and 1.5bp on the day; 10- year yields around 3.78%, richer by 4bp on the day with bunds lagging by 1.5bp in the sector. The two-year Treasury yield slipped 4bps to 4.49%, pulling back from a two-month high around 4.55% hit the previous day. Markets are pricing in 23 basis points of Fed tightening in July, down 3 basis points from Thursday but still reflecting the likelihood of a 25 basis point hike in two months’ time; Boston Fed President Collins on Thursday said the central bank may have reached, or be approaching, the point at which it can pause interest-rate increases

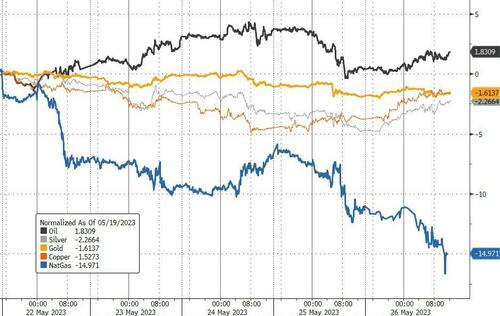

In commodities, crude futures advance with WTI rising 0.5% to trade near $72.20. Spot gold adds 0.6% to around $1,953. Bitcoin falls 0.2%

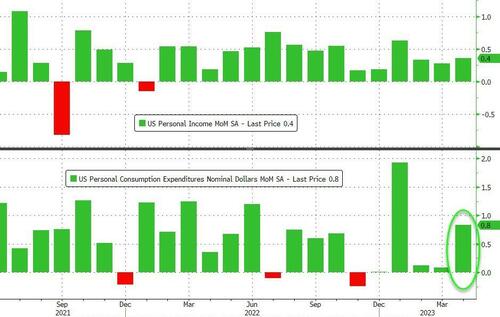

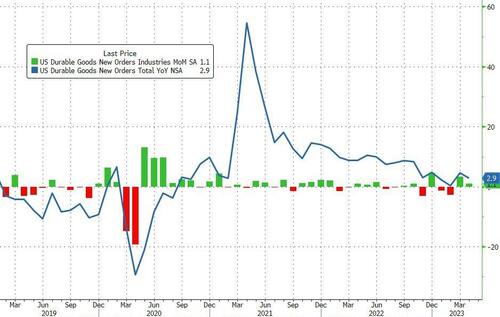

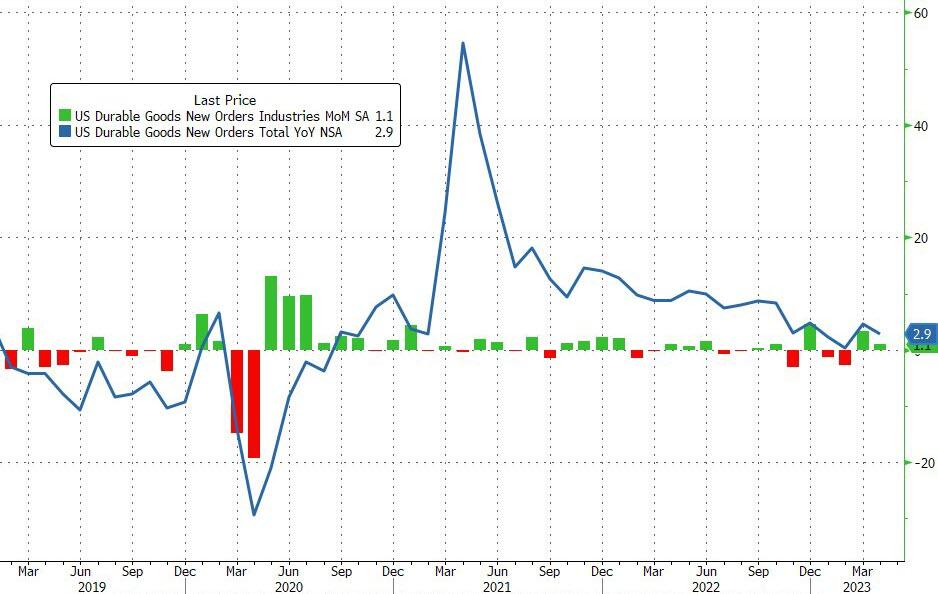

Looking to the day ahead now, and data releases from the US include PCE inflation for April, along with personal income and personal spending for April, preliminary durable goods orders for April, and the University of Michigan’s final consumer sentiment index for May. Meanwhile in Europe, there’s UK retail sales for April. Otherwise from central banks, we’ll hear from the ECB’s Lane and Vujcic.

Market Snapshot

S&P 500 futures down 0.3% to 4,170

MXAP up 0.5% to 159.93

MXAPJ up 0.7% to 506.87

Nikkei up 0.4% to 30,916.31

Topix little changed at 2,145.84

Hang Seng Index down 1.9% to 18,746.92

Shanghai Composite up 0.4% to 3,212.50

Sensex up 0.8% to 62,392.17

Australia S&P/ASX 200 up 0.2% to 7,154.76

Kospi up 0.2% to 2,558.81

STOXX Europe 600 up 0.3% to 457.36

German 10Y yield little changed at 2.52%

Euro little changed at $1.0729

Brent Futures little changed at $76.23/bbl

Gold spot up 0.6% to $1,953.26

U.S. Dollar Index down 0.15% to 104.09

Top Overnight News from Bloomberg

European stocks rose and Treasury yields ticked lower on signs that US negotiators are moving closer to striking a debt deal.

Republican and White House negotiators are nearing a deal to raise the debt limit and cap federal spending for two years, according to people familiar with the matter, as time grows short to avert a catastrophic US default

With investor attention on the US sovereign credit rating rising as the federal government gets ever closer to running out of cash, Moody’s Investors Service says that a mid-June payment of interest on Treasuries will be critical for maintaining the top, AAA grade.

Germany has been Europe’s economic engine for decades, pulling the region through one crisis after another. But that resilience is breaking down, and it spells danger for the whole continent.

In 2020, just after George Floyd’s murder in the US, one of the most senior Black professionals in the City of London, KPMG UK Partner and Vice-Chair Richard Iferenta, appealed to CEOs and chairpeople of the business community “to stamp out racism of all forms.” Three years later, he has yet to see the change and ambition he asked for.

Morgan Stanley is letting go of at least six managing directors, including some key China bankers, as part of broader job cuts in Asia where dealmaking has been stymied by growing China-US tensions and tepid economic growth.

Barclays Plc lost three senior investment bankers including John Miller, all of whom are joining Jefferies Financial Group Inc., according to people with knowledge of the matter.

A more detailed look at global markets courtesy of Newsquawk

European bourses began the session on the front foot but have since pulled back from best levels and now see a mixed picture, Euro Stoxx 50 -0.1%. Sectors in Europe are mixed (vs a mostly positive open). Basic Resources outperform as base metals claw back some recent losses, with Tech the next best performer as NVIDIA’s surge continues to reverberate globally. The downside meanwhile consists of Utilities, Telecoms, and Banks. US equity futures traded horizontally overnight but saw a slight uptick shortly after the cash open, in tandem with Europe, but have since pulled back; ES -0.1%.

Top European News

UK ministers look to reshape the pensions lifeboat fund to provide a boost to business, according to FT.

ECB’s Lane on “How quickly will inflation return to target?” – reiterates guidance from the 4th May ECB Meeting.

There is no sense of certainty in the terminal rate; uncertainty in models is high; some upside risks to wage growth.

ECB’s Vujcic says inflation momentum is still persistent and it is questionable that we will be able to get to 2% in the next two years.

Riksbank’s Breman says increasing asset sales is something we could think about if we see the crown continuing to weaken. Adds, increasing asset sales is something we should think about, doesn’t need to be next meeting.

APAC stocks traded mixed following the mild positive bias stateside where the tech sector surged on Nvidia’s blockbuster report and with sentiment underpinned by firm US data and progress in debt ceiling talks. ASX 200 was indecisive with price action rangebound and risk sentiment contained by disappointing Retail Sales data. Nikkei 225 outperformed and reclaimed the 31,000 level with the index lifted by recent currency weakness and mostly softer-than-expected Tokyo CPI, while tech stocks benefitted from the ripple effect which stemmed from the rally in US counterparts. Shanghai Comp. was subdued amid the closure of Hong Kong markets and Stock Connect trade but with the downside cushioned after the meeting between the US and China’s commerce chiefs where concerns were raised about recent actions taken against US companies in China, as well as US chip policy and export curbs

Top Asian News

US Commerce Secretary Raimondo met with Chinese Commerce Minister Wang in Washington and raised concerns about the recent spate of Chinese actions taken against US companies in China.

Furthermore, China’s MOFCOM said Wang and Raimondo agreed to keep communication on trade concerns and that China expressed concerns on US chip policy and export curbs, while the meeting was candid and constructive, according to Reuters.

China’s top server makers asked suppliers to suspend shipments of modules containing chips made by Micron (MU) following Beijing’s partial ban on Micron products, according to SCMP.

FX

The broader Dollar and index have pulled back from overnight highs. mostly amid the strength in G10 counterparts.

The non-US Dollars are firmer against the Dollar to varying degrees, AUD/USD outperforms as base metals rebound.

Sterling resides as one of today’s outperformers on the back of the stronger-than-expected Retail Sales data (+0. 5% M/M vs exp. 0.3%), coupled with hawkish commentary from BoE’s Haskel yesterday.

The SEK stands as the current G10 outperformer with strength seen amid hawkish commentary from Riksbank Deputy Governor Bremen.

PBoC set USD/CNY mid-point at 7.0760 vs exp. 7.0752 (prev. 7.0529)

Fixed Income

Core benchmarks are mixed with USTs bid as the risk tone slips while EGBs/Gilts are softer, but directionally infitting.

EGBs and Gilts were initially weighed on by strong UK Retail data which adds to the factors in-favour of further BoE tightening.

Though, market pricing for the BoE hasn’t altered significantly from the post-CPI pricing of 100bp of tightening by end-2023.

Stateside, yields are lower across the curve and towards troughs given the above benchmark pricing

Commodities

WTI and Brent futures are relatively flat on either side of the unchanged mark following the downside yesterday, which was due to a concoction of weak German GDP data and comments from Russia Deputy PM Novak.

Spot gold has firmed in the European morning as the DXY pulled back, while the yellow metal also found support near its 100 DMA (USD 1,934.86/oz) in APAC hours.

Base metals are firmer across the board following the losses seen throughout the majority of this week.

India weather office says El Nino seen emerging during monsoon season.

Geopolitics

Japan is to place additional sanctions against Russia in which it will freeze the assets of 78 groups and 17 individuals in Russia as part of new sanctions, according to a government bulletin. Furthermore, Chief Cabinet Secretary Matsuno said Japan is to ban providing construction and engineering services in Russia, while they condemned Russia’s plan to deploy tactical nuclear weapons to Belarus as it intensifies the situation around Ukraine, according to Reuters.

Regarding Sweden’s NATO accession, Sweden said Turkish President Erdogan’s demands are impossible to meet as Sweden has not received a list of relevant individuals from Turkey, according to a senior Swedish official cited by WSJ.

DB’s Jim Reid concludes the overnight wrap

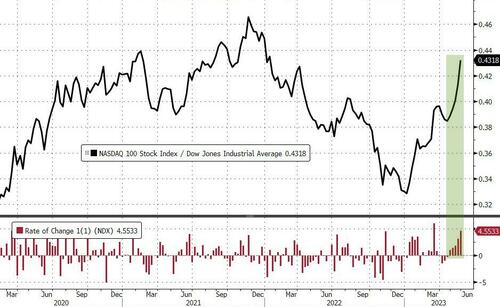

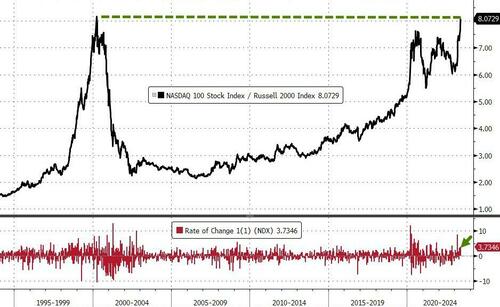

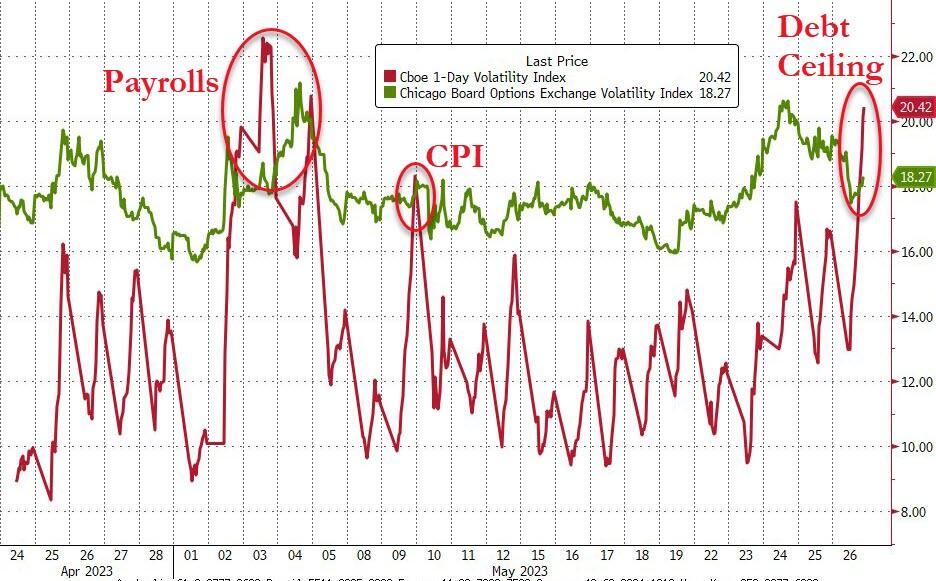

After some rough sessions earlier in the week, the newsflow has been a lot more positive for markets over the last 24 hours. First, there’s now some more optimism again around the debt ceiling, particularly after comments from Speaker McCarthy suggested that a deal was near, and that he would be staying in town over the long weekend to work on a deal. Second, tech stocks saw a big outperformance thanks to excitement surrounding AI, which followed Nvidia’s positive outlook from the previous day. And third, US economic data yesterday ran ahead of expectations, thus helping to ease fears about an imminent recession. But with all this newfound optimism, investors are once again dialling up their expectations for future rate hikes, and sovereign bonds saw a decent selloff in response. In the meantime, the gains for equities were actually very narrow and solely driven by the large tech stocks.

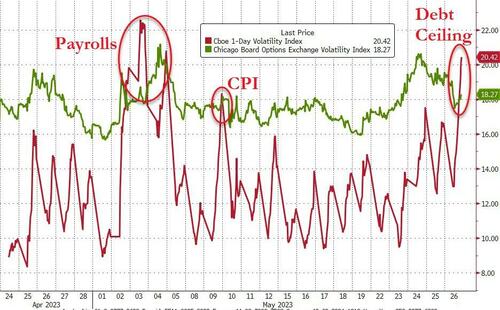

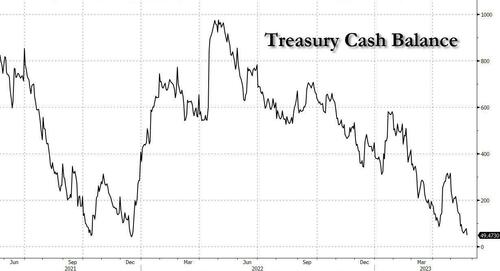

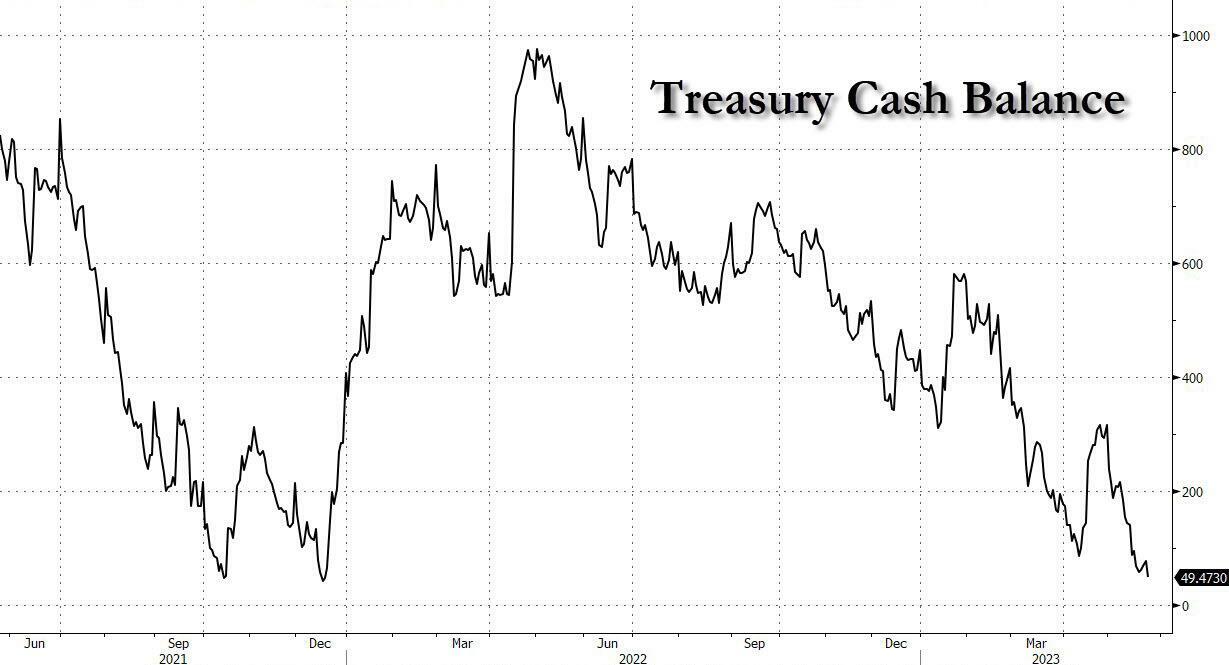

Starting with the debt ceiling, we still don’t have a deal yet, but the latest developments yesterday raised hopes that an agreement can be reached ahead of the deadline (whenever that actually is). Shortly after the US open, markets reacted to comments from Speaker McCarthy, who said “I thought we made some progress” in the discussions on Wednesday. Furthermore, he said “I don’t think everybody is going to be happy at the end of the day”, which was seen as laying the groundwork for any potential compromise, and hence positive for the likelihood of reaching a deal. Last night it was reported by Reuters that the two sides were just $70bn apart on discretionary spending levels, with the overall deal likely smaller in scope than what was first reported. While there was no deal when the sides went home, the tone from the top from Speaker McCarthy and President Biden is more encouraging than earlier this week. After the US close the Treasury disclosed their cash balances had fallen to $49.5bn, down from $76.5bn the day earlier and $140bn on May 12, so the clock is indeed ticking.

With that more positive backdrop to the talks, there were clear signs of market stress starting to ease again. For instance, the yield on the T-bill maturing on June 8 (so close to the potential X-date) came down by -32.4bps on the day to 6.48%, and it was a similar story for other bills around the X-date. Those moves were also in the opposite direction to the broader move toward higher yields yesterday, which further demonstrates how the debt limit was driving those moves. However, even with the growing optimism from yesterday, it’s worth noting that yields on bills around the X-date are trading with a 6 handle, which shows how investors are still wanting a premium to hold the Treasuries that might be affected by a potential default.

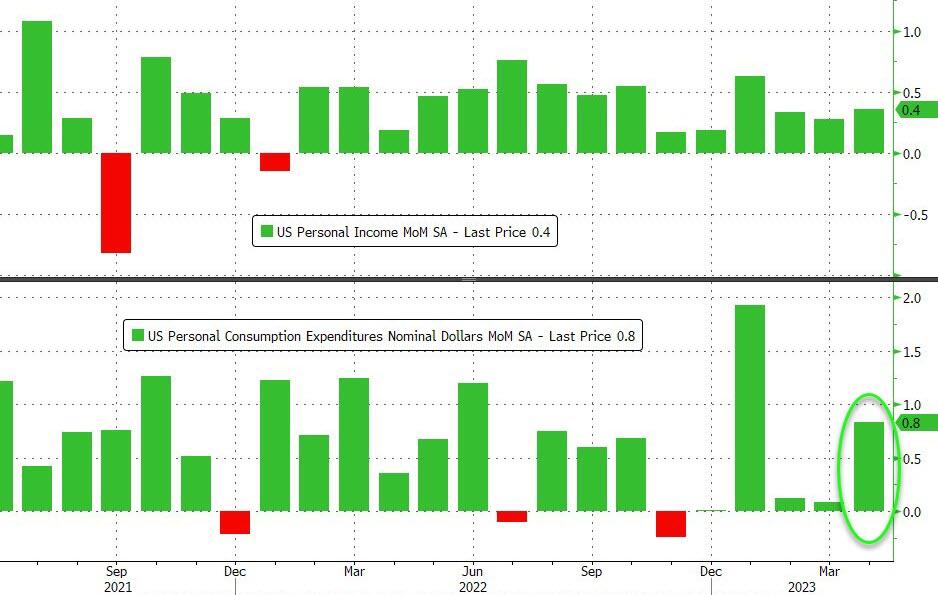

Just as better news was coming through on the debt ceiling, we also had a decent round of releases on the US economy that further supported risk appetite. One was the weekly initial jobless claims, which came in at 229k over the week ending May 20 (vs. 245k expected), and we also heard that the state of Massachusetts had downwardly revised three months of data due to fraudulent applications. Alongside that, it turned out that growth in Q1 was stronger than initially thought, having been revised up to a +1.3% annualised rate (vs. 1.1% previously), whilst core PCE inflation was revised up to +5.0% (vs. +4.9% previously).

With all that positive news coming through, it means that markets are putting increasing weight on the prospect of another rate hike from the Federal Reserve. By the close, futures had raised the chances of a June hike up to 54%, which is the first time since SVB’s collapse back in March, so it’s a prospect that investors are taking more and more seriously. At the same time, there’s been growing speculation that the Fed might skip a hike in June and move again in July, which means that if you look at the chances that we’ve had a hike by July, they’re now up to a very strong 94% probability. That’s a big shift from where we were after the Fed’s last meeting at the start of the month, when the consensus view was that they were done hiking, and the next move was more likely to be a cut than a hike.

As markets priced in more rate hikes, sovereign bonds sold off across the board once again. In the US, yields on 10yr Treasuries (+7.6bps) hit a post-SVB high of 3.817%, having now risen for 9 of the last 10 sessions. And the 10yr real yield (+7.9bps) closed above 1.5% for the first time since the SVB turmoil as well. In Europe yields were set to close lower than they did before a late comment from ECB board member Knot (a noted hawk) who said that rate hikes were needed over the next two months, that he was “open-minded” about September, and finally that the market pricing of rates cuts is “overly optimistic”. This resulted in yields on 10yr bunds (+5.0bps), OATs (+5.0bps) and BTPs (+5.9bps) all moving higher after being close to finishing just higher than unchanged. Overnight swap pricing is still nearly fully pricing in the next two hikes (97% for June and 80% for July ), while the chance of a rate cut in February of next year is now the lowest it has been in 3 weeks.

But it was gilts that saw the biggest declines once again, with the 10yr yield (+16.0bps) closing at 4.37%, which isn’t far off its closing high just after the September mini-budget, when it reached 4.50%. That comes as our UK economist has updated his call for the BoE, where he now thinks we’ll get another three 25bp hikes that take us up to a terminal rate of 5.25%. See his latest call here.

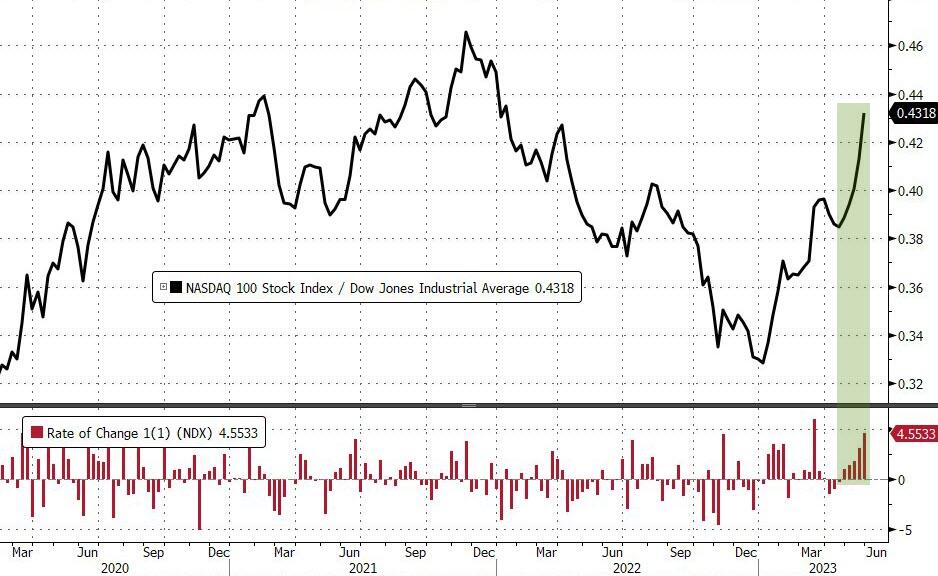

For equities, there were several factors at play yesterday, and the S&P 500 (+0.88%) ultimately ended the day in positive territory. But it’s worth stressing that this was down to incredible strength among tech stocks, with only just over 40% of the index actually ending the day in positive territory. In fact, on an industry basis, semiconductors were up +11.0% and software was up +3.6%, with transports the next best at +1.2%. 15 of the 24 other industries were lower on the day. So clearly tech outperformance was the big story with the NASDAQ recovering +1.71% after declining over the last couple of days. Nvidia (+24.37%) was one of the biggest outperformers, and was single-handedly responsible for most of the NASDAQ’s gains. In addition, the company’s strength meant that the FANG+ Index (+2.51%) extended its YTD gains to +55.19%. Elsewhere, the Philadelphia Stock Exchange Semiconductor Index was up +6.81%, and individual companies like Advanced Micro Devices surged +11.13%. Marvell kept the semi’s ball rolling after hours by reporting better-than-expected results and forecasting AI-related revenues to at least double for this fiscal year. Their stock was +16.74% higher after the close.

Overnight in Asia, the Nikkei 225 (+0.62%) and the Kospi (+0.17%) are advancing just as the Shanghai Composite (-0.14%) lags. Some of the gains continue to be driven by AI sentiment – IT is the best-performing sector in the Topix and companies like TSMC (+4.05%) and SK Hynix (+5.51%) are rallying further on Marvell’s earnings. In terms of economic data in the region, the Tokyo CPI slowed to 3.2% from 3.5% YoY, coming in below estimates of 3.4%. The yen has strengthened +0.23% against the dollar. In terms of US assets, Marvell’s $42bn market cap has done little to lift Nasdaq futures (-0.18%), with the S&P 500 (-0.18%) contracts also falling. Meanwhile, Treasury yields are down by at least 1bps across most of the curve.

In Germany, there was another round of weak data yesterday, as their Q1 GDP number was revised to show a -0.3% contraction, rather than a flat reading as initially thought. Given that the economy saw a -0.5% contraction in Q4, that means there were two consecutive contractions that meet the technical definition of a recession. So assuming the data isn’t revised further in future, it turns out there was a winter recession amidst the energy shock, despite hopes the country might have just about managed to avoid one.

To the day ahead now, and data releases from the US include PCE inflation for April, along with personal income and personal spending for April, preliminary durable goods orders for April, and the University of Michigan’s final consumer sentiment index for May. Meanwhile in Europe, there’s UK retail sales for April. Otherwise from central banks, we’ll hear from the ECB’s Lane and Vujcic.

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

APAC mixed with focus on debt ceiling talks; UK Retail Sales & US PCE ahead – Newsquawk Europe Market Open

FRIDAY, MAY 26, 2023 – 01:33 AM

APAC stocks traded mixed following the mild positive bias stateside where the tech sector surged on Nvidia’s blockbuster report

Nikkei 225 outperformed, US equity futures were rangebound, and European equity futures are indicative of a flat open

US President Biden and House Speaker McCarthy are said to be near a deal that would raise the debt ceiling for two years and cap spending

US House Speaker McCarthy said there was no agreement on Thursday and he will stay at the Capitol to continue to work this weekend

Looking ahead, highlights include UK Retail Sales, US PCE Price Index, Durable Goods, Speeches from ECB’s Lane, Enria & RBNZ’s Orr, Supply from the UK

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

US TRADE

EQUITIES

US stocks finished somewhat mixed albeit with a positive bias as a debt limit solution appears increasingly likely and with the advances led by a surge in the tech sector after Nvidia (NVDA) ballooned its market cap by around 25% to approach near the USD 1tln club. In addition, the data releases were stronger than expected, which coupled with the increased optimism on the debt ceiling, put the onus back on the Fed and saw money market pricing edge towards a hike at the next FOMC meeting in June.

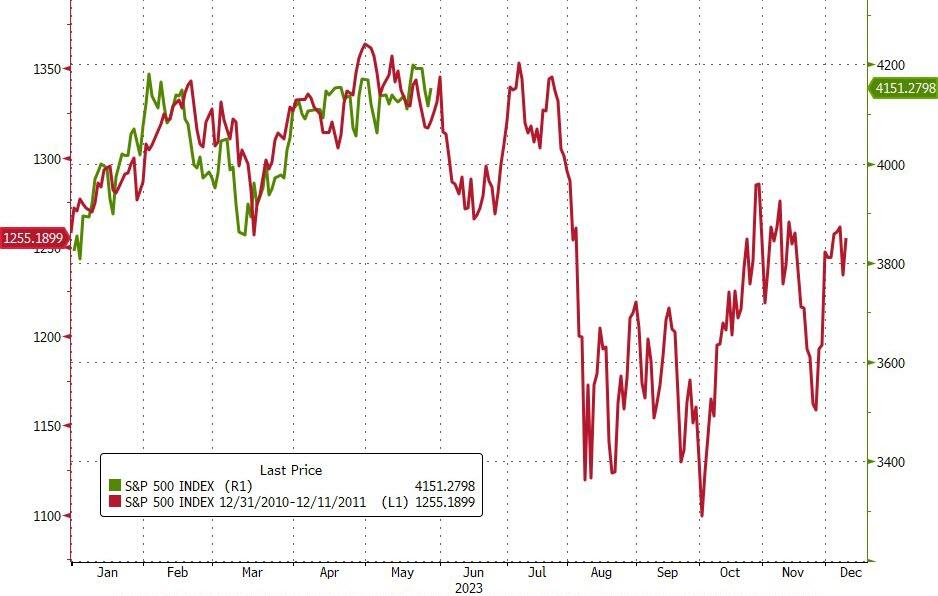

SPX +0.88% at 4,151, NDX +2.46% at 13,938, DJIA -0.11% at 32,764, RUT -0.70% at 1,754.

Fed Discount Window borrowing at USD 4.2bln on May 24th vs USD 9bln W/W, while Other Credit was at USD 192.6bln vs USD 208.5bln WW and BTFP lending was at 91.9bln vs 87bln W/W, according to Reuters.

US President Biden said he had several productive conversations on the debt ceiling with House Speaker McCarthy and it is time for Congress to act now, while Biden put forward a proposal to freeze spending for two years and said negotiations are about budget outlines. Biden added that he has a very different view to McCarthy of who should bear the burden of additional efforts to get the fiscal house in order and he will not agree to huge cuts on teachers, police, border patrol agents or increase wait times for social security claims and he believes they’ll come to an agreement.

US President Biden and House Speaker McCarthy are said to be near a deal that would raise the debt ceiling for two years and cap spending on most items other than military and veterans, while President Biden and Democrats are considering scaling back the boost in IRS funding as part of a budget deal, according to a US official cited by Reuters.

White House Communications Director said they are getting closer to a deal on the debt ceiling, while the White House earlier said President Biden’s team had productive debt ceiling talks and discussions continue.

White House and Republican debt limit proposals differ now by less than USD 70bln on discretionary spending, while the contours of a US debt limit deal are taking shape and the focus is primarily on the top-line number. Furthermore, negotiators are likely to agree on a slimmed-down agreement with just a few key numbers, according to Reuters sources.

US House Speaker McCarthy said there was no agreement on Thursday and he will stay at the Capitol to continue to work this weekend, while he added it is not easy and they will continue working until they get it done, according to Reuters.

US GOP Rep. Graves said work requirements are a sticking point in talks with the White House, according to Reuters.

US GOP Rep. McHenry said there is alignment on what they need to work on with the debt ceiling, while he responded that he doesn’t think so and they are not quite in that zone yet when asked if a deal could have been made yesterday, but noted the work they are doing centres on a shorter and shorter array of issues.

US GOP Rep. McHenry, in a letter to Treasury Secretary Yellen, said the Biden admin’s outbound investment proposal requires rigorous scrutiny by the Treasury and thorough oversight by Congress, while it is unclear that investment restrictions would be more effective than export controls or sanctions in regulating foreign investment.

US Treasury is preparing to change how the US processes federal agencies’ payments if the debt ceiling is breached whereby agencies would submit payments to the Treasury no sooner than the day before they are due and if the Treasury can’t make a full day’s payments, it would likely delay until it has enough cash, according to WSJ sources.

US regulator vowed to take a tough line on problem banks with the Office of the Comptroller of the Currency to consider taking corrective action against persistently weak banks including forcing them to exit certain businesses, according to WSJ.

APAC TRADE

EQUITIES

APAC stocks traded mixed following the mild positive bias stateside where the tech sector surged on Nvidia’s blockbuster report and with sentiment underpinned by firm US data and progress in debt ceiling talks.

ASX 200 was indecisive with price action rangebound and risk sentiment contained by disappointing Retail Sales data.

Nikkei 225 outperformed and reclaimed the 31,000 level with the index lifted by recent currency weakness and mostly softer-than-expected Tokyo CPI, while tech stocks benefitted from the ripple effect which stemmed from the rally in US counterparts.

Shanghai Comp. was subdued amid the closure of Hong Kong markets and Stock Connect trade but with the downside cushioned after the meeting between the US and China’s commerce chiefs where concerns were raised about recent actions taken against US companies in China, as well as US chip policy and export curbs.

US equity futures were rangebound as participants await further development in the debt ceiling negotiations and ahead of the Fed’s preferred inflation measure scheduled for release later today.

European equity futures are indicative of a flat open with the Euro Stoxx 50 flat after the cash market closed up by 0.1% yesterday.

FX

DXY marginally softened overnight but held on to most of its recent gains after printing a two-and-a-half-month high above 104.00 following a clean sweep of forecast-beating data releases which contributed to a shift in pricing towards a 25bps Fed hike next month.

EUR/USD attempted to nurse some of its losses but with the rebound limited after yesterday’s weak German data.

GBP/USD was off the prior day’s lows although lacked any meaningful strength and largely ignored comments from BoE’s Haskel who noted that further UK rate rises cannot be ruled out.

USD/JPY slightly pulled back after its brief incursion above 140.00 which coincided with moves in US yields.

Antipodeans were rangebound amid the mixed risk appetite and after flat Australian Retail Sales.

China’s major state-owned banks were seen selling dollars in the onshore spot FX market.

PBoC set USD/CNY mid-point at 7.0760 vs exp. 7.0752 (prev. 7.0529)

FIXED INCOME

10yr UST futures languished near yesterday’s lows after having bear-flattened to their most inverted since mid-March as strong data and debt ceiling progress placed the onus back on the Fed.

Bund futures were subdued after the recent sell-off and hawkish comments from ECB’s Knot but with a floor around 133.00.

10yr JGB futures were pressured on spillover selling from global peers and amid the lack of additional BoJ purchases which instead offered to purchase commercial paper from May 31st, although losses were stemmed after mostly softer-than-expected Tokyo CPI data.

COMMODITIES

Crude futures were lacklustre after yesterday’s slide owing to the headwinds from a firm dollar and comments from Russia’s Novak who initially downplayed prospects of an OPEC+ output cut but has since stated that the group could make a decision at the June meeting.

Russian Deputy PM Novak said Russia and OPEC+ partners will decide on what is best for the oil market, while he added that OPEC+ can make a decision at the June meeting if necessary and that Russia will participate in OPEC+ talks.

Iraqi Oil Ministry said discussions with Saudi companies including Aramco about gas and oil investments have not reached a final agreement.

Spot gold marginally recovered as the greenback took a breather from its recent advances.

Copper futures notched mild gains in the aftermath of the firm US data and debt ceiling progress.

CRYPTO

Bitcoin traded indecisively overnight in which price action oscillated around the USD 26,500 level.

NOTABLE ASIA-PAC HEADLINES

US Commerce Secretary Raimondo met with Chinese Commerce Minister Wang in Washington and raised concerns about the recent spate of Chinese actions taken against US companies in China. Furthermore, China’s MOFCOM said Wang and Raimondo agreed to keep communication on trade concerns and that China expressed concerns on US chip policy and export curbs, while the meeting was candid and constructive, according to Reuters.

US official Ratner said China has not answered the US request for a defence ministers meeting.

US State Department said it is aware of recent activity by a Chinese-sponsored cyber actor to develop a presence in networks across US critical infrastructure and such attacks could include against oil and gas pipelines and rail systems.

China’s top server makers asked suppliers to suspend shipments of modules containing chips made by Micron (MU) following Beijing’s partial ban on Micron products, according to SCMP.

DATA RECAP

Tokyo CPI YY (May) 3.2% vs. Exp. 3.9% (Prev. 3.5%)

Tokyo CPI Ex. Fresh Food YY (May) 3.2% vs. Exp. 3.3% (Prev. 3.5%)

Tokyo CPI Ex. Fresh Food & Energy YY (May) 3.9% vs. Exp. 3.9% (Prev. 3.8%)

Australian Retail Sales MM Final * (Apr) 0.0% vs. Exp. 0.2% (Prev. 0.4%)

GEOPOLITICS

White House said it has seen reports of the Russian-Belarus nuclear weapon arrangement and will continue to monitor.

US issued new Russia-related sanctions related to the Russian Wagner Group, according to Treasury’s website.

Japan is to place additional sanctions against Russia in which it will freeze the assets of 78 groups and 17 individuals in Russia as part of new sanctions, according to a government bulletin. Furthermore, Chief Cabinet Secretary Matsuno said Japan is to ban providing construction and engineering services in Russia, while they condemned Russia’s plan to deploy tactical nuclear weapons to Belarus as it intensifies the situation around Ukraine, according to Reuters.

Russian Defence Ministry said it deployed a fighter jet to prevent two US Air Force bombers from violating Russian state borders, according to TASS.

UK/EU

UK ministers look to reshape the pensions lifeboat fund to provide a boost to business, according to FT.