by harveyorgan · in Uncategorized · Leave a comment·Editi

GOLD PRICE CLOSED: DOWN $19.70 TO $1943.55

SILVER PRICE CLOSED: DOWN $0.32 AT $22.81

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1940.75

Silver ACCESS CLOSE: 22.73

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $26,234 DOWN 5 Dollars

Bitcoin: afternoon price: $26,506 UP 267 dollars

Platinum price closing $1025.95 DOWN $25.90

Palladium price; $1406.50 DOWN $46.35

“Our system is so stinkin’ corrupt that we owe Sodom and Gomorrah an apology.” … Trader Dan Norcini in 2009

GO GATA!

END

Yesterday, we finished with option expiry for the comex and now we must endure some pain as we wait the conclusion of LBMA options expiry

May 31/2023.

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,644.00 DOWN 18.00 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1574.69 DOWN 9.61 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1809.07 DOWN 13.02 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: MAY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,962.800000000 USD

INTENT DATE: 05/24/2023 DELIVERY DATE: 05/26/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 23

363 H WELLS FARGO SEC 54

435 H SCOTIA CAPITAL 6

624 H BOFA SECURITIES 1

657 C MORGAN STANLEY 23

661 C JP MORGAN 21

726 C CUNNINGHAM COM 2

732 C RBC CAP MARKETS 1

737 C ADVANTAGE 3

880 H CITIGROUP 43

905 C ADM 23

TOTAL: 100 100

MONTH TO DATE: 6,139

JPMorgan stopped 21/100 contracts

FOR MAY:

GOLD: NUMBER OF NOTICES FILED FOR MAY/2023. CONTRACT: 100 NOTICES FOR 10000 OZ or 0.3110 TONNES

total notices so far: 6139 contracts for 613,900 oz (19.094 tonnes)

FOR MAY:

SILVER NOTICES: 4 NOTICE(S) FILED FOR 20,000 OZ/

total number of notices filed so far this month : 2558 for 12,790,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP DOWN $9.50..

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//WOW!!

/NO CHANGES IN GOLD INVENTORY AT THE GLD:////

INVENTORY RESTS AT 941.29 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 35 CENTS AT THE SLV//

SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 276,000 OZ INTO THE SLV//: ; : INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 471.606 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A TINY SIZED 82 CONTRACTS TO 135,658 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS TINY SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.35 FALL IN SILVER PRICING AT THE COMEX ON WEDNESDAY. TAS ISSUANCE WAS ANOTHER STRONG SIZED 719 CONTRACTS. THESE WILL BE USED FOR MANIPULATION NEXT MONTH. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY: A STRONG 719 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THEY VALUE 0 TO A POSITION LIMIT IF A CALENDAR SPREAD OCCURS. IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED THE COMPLAINT IN SIMILAR FASHION TO ALL OF THOSE DEMOCRATIC CRIMES COMMITTED WITH NO ATTENTION GIVEN BY ATTORNEY GENERALS.

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.35). AND WERE UNSUCCESSFUL IN KNOCKING SOME SPEC LONGS AS WE HAD A GOOD GAIN ON OUR TWO EXCHANGES OF 319 CONTRACTS WE HAD 500 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 2.5 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 6.750 MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION. WE WILL HAVE IN OUR FINAL WEEK IN THE DELIVERY CYCLE MORE MANIPULATION IN OUR PRECIOUS METALS DUE TO COMEX SPREADERS LIQUIDATION ACCOMPANYING OPTIONS EXPIRY ON BOTH THE COMEX AND LONDON’S LBMA ALONG WITH AN ADDED FEATURE OF TAS LIQUIDATION.

WE MUST HAVE HAD:

A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS( 250 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.105 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 5,000 OZ (E.F.P. JUMP LOWERS THE AMOUNT OF SILVER STANDING)+2.5 MILLION OZ EXCHANGE FOR RISK// TOTAL 6.75 MILLION OZ OF EXCHANGE FOR RISK FOR THE MONTH (RAISES THE AMOUNT OF SILVER STANDING):THUS TOTAL OF 20.245 MILLION OZ OF SILVER STANDING FOR DELIVERY V) SMALL SIZED COMEX OI LOSS/ SMALL SIZED EFP ISSUANCE/VI) HUGE NUMBER OF SHORT T.A.S. CONTRACT INITIATION (719 CONTRACTS)//CONSIDERABLE T.A.S LIQUIDATION MANIPULATING THE PRICE SOUTHBOUND.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -removed 151 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTRACTS for 19 days, total 11,775 contracts: OR 58.875 MILLION OZ . (619 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 58.875 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 58.875 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 82 CONTRACTS WITH OUR FAIR SIZED $0.35 LOSS IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 250 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAY OF 13.105 MILLION OZ//FIRST DAY NOTICE FOLLOWED BY TODAY’S E.F.P. JUMP OF 5,000 OZ (DECREASES THE AMOUNT OF SILVER STANDING) +// + 2.5 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //TOTAL EXCHANGE FOR RISK MONTH= 6.75 MILLION//NEW TOTALS 13.495 MILLION OZ + 6.75 MILLION = 20.245 MILLION OZ STANDING FOR MAY// .. WE HAVE A SMALL SIZED GAIN OF 168 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE 719!!//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED.

WE HAD 4 NOTICE(S) FILED TODAY FOR 20,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2074 CONTRACTS TO 477,002 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED 347 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 2078 CONTRACTS) WITH OUR $9.50 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR MAY. AT 3.5085 TONNES ON FIRST DAY NOTICE // PLUS 200 OZ E.F.P. JUMP TO LONDON :(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)/+ /A HUGE ISSUANCE OF 2554 T.A.S. CONTRACTS/STRONG FRONT END OF TAS LIQUIDATION ////YET ALL OF..THIS HAPPENED WITH OUR $9.50 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 1836 OI CONTRACTS (5.716 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3916 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 477,002

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1826 CONTRACTS WITH 2078 CONTRACTS DECREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): 2554 CONTRACTS) AND 3916 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1836 CONTRACTS OR 5.716 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3916 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2,076) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 1836 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 3.5085 TONNES FOLLOWED BY TODAY’S E.F.P. JUMP OF 200 OZ // NEW STANDING: 19.094 TONNES+ 1.244 TONNES OF EXCHANGE FOR RISK//NEW TOTALS FOR GOLD STANDING FOR MAY: 20.338 TONNES // ///3) ZERO LONG LIQUIDATION//4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: STRONG T.A.S. ISSUANCE: 2554 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 62,888 CONTRACTS OR 6,288,800 OZ OR 195.60 TONNES IN 19 TRADING DAY(S) AND THUS AVERAGING: 3309 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAY(S) IN TONNES 195.60 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 195.60/3550 x 100% TONNES 5.62% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES ( MUCH SMALLER THAN LAST MONTH)

MAY: 195.60 TONNES (HEADING FOR ANOTHER SMALL MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A TINY SIZED 82 CONTRACTS OI TO 135,658 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 250 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 250 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 250 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 82 CONTRACTS AND ADD TO THE 250 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A FAIR SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 168 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 0.84 MILLION OZ

OCCURRED WITH OUR $0.35 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 3.49 PTS OR 0.11% //Hang Seng CLOSED DOWN 369.01 POINTS OR 1.93% /The Nikkei closed UP 118.45 OR 0.39% //Australia’s all ordinaries CLOSED DOWN 1.03 % /Chinese yuan (ONSHORE) closed DOWN 7.0699 /OFFSHORE CHINESE YUAN DOWN TO 7.0827 /Oil DOWN TO 72.86 dollars per barrel for WTI and BRENT AT 76.89 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2078 CONTRACTS DOWN TO 477,002 WITH OUR LOSS IN PRICE OF $9.50 ON WEDNESDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF MAY… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3916 EFP CONTRACTS WERE ISSUED: : JUNE 3916 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3916 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 1826 CONTRACTS IN THAT 3916 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 2078 COMEX CONTRACTS..AND THIS SMALL SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $9.50. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE),THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE TODAY WAS A GIGANTIC 2554 CONTRACTS. DURING THIS WEEK THEY SOLD THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE). FOR EXAMPLE WITH TONIGHT’S READING OF TAS, 100% OF ISSUANCE OF T.A.S. WAS JUNE AND AUGUST.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (20.338) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $9.50) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR SMALL SIZED GAIN OF 1836 CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE TAS LIQUIDATION. AND NOW FOR THE FIRST TIME TAS LIQUIDATION IS EXTENDING PAST MID MONTH.

WE HAVE GAINED A TOTAL OI OF 5.716 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY. (3.5085 TONNES) FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 200 oz//NEW STANDING 19.094 TONNES+1.244 exchange for risk(prior)// new total 20.345 tonnes ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $9/50

WE HAD +ADDED 347 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1826 CONTRACTS OR 182600 OZ OR 5.716 TONNES.

Estimated gold comex today 334,713// good//raid

final gold volumes/yesterday 312,691// good/raid

//MAY 25/ MAY 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | . nil |

| Deposit to the Dealer Inventory in oz | NIL |

| Deposits to the Customer Inventory, in oz | 231,133.539 oz Delaware Malca 7189 kilobars |

| No of oz served (contracts) today | 100 notice(s) 10,000 OZ 0.0000 TONNES |

| No of oz to be served (notices) | 0 contracts 0 oz 0.000 TONNES |

| Total monthly oz gold served (contracts) so far this month | 6139 notices 613,900 OZ 19.094 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 2

i) Into Delaware 5076.539 oz (189 kilobars)

ii) Into Malca: 225,057.000 oz (7000 kilobars)

total deposits: 231,133.539 oz 7139 kilobars

customer withdrawals: 0

i) Out of Brinks: 385.810 oz (12 kilobars)

total withdrawals: 385.810 oz

Adjustments; 1 dealer to customer/ JPMorgan

i) Out of JPMorgan: 117,769.110 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 100 contracts having LOST 2 contracts. We had 0 contracts filed

on WEDNESDAY, so we LOST 2 contracts or an additional 200 oz will not stand for gold in this non active delivery month of May as these guys were EFP.’d to London where they will try and take delivery over there.

June LOST A HUGE 28,289 contracts DOWN to 111,888 contracts. We have 3 more reading days before first day notice.

July added 180 contracts to stand at 2803 contracts.

AUGUST GAINED 24,663 contracts UP to 305,212 contracts

We had 100 contracts filed for today representing 10,000 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 100 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 21 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2023. contract month,

we take the total number of notices filed so far for the month (6,139 x 100 oz ), to which we add the difference between the open interest for the front month of MAY (100 CONTRACTS) minus the number of notices served upon today 100 x 100 oz per contract equals 613,900 OZ OR 19.094 TONNES the number of TONNES standing in this NON- active month of May. And now we must add 1.244 tonnes of gold delivery through our 400 contract exchange for risk//new total 20.338 tonnes of gold.

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (6,139 x 100 oz) x xxx OI for the front month minus the number of notices served upon today (100)x 100 oz} which equals 613,800 oz standing OR 19.094 TONNES + 1.244 (exchange for risk) = 20.338 tonnes

TOTAL COMEX GOLD STANDING: 20.338 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,696,563.034 OZ 52.77 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,843,438.663 OZ

TOTAL REGISTERED GOLD: 11,766,645.594 (365,99 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 11,076,793.069 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,070,082 OZ (REG GOLD- PLEDGED GOLD) 313.221 tonnes//

END

SILVER/COMEX

MAY 25//2023// THE MAY 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,087,462.838 oz CNT Brinks HSBC Delaware . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 532,257.716 oz HSBC JPM |

| No of oz served today (contracts) | 4 CONTRACT(S) (20,000 OZ) |

| No of oz to be served (notices) | 141 contracts (705,000 oz) |

| Total monthly oz silver served (contracts) | 2558 Contracts (12,790,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i) Into HSBC: 522,601.416 oz

ii) Into JPMorgan 9656.300

Total deposits: 169,641.100 oz

JPMorgan has a total silver weight: 141.373 million oz/271.605 million =51.91% of comex .//dropping fast

Comex withdrawals 4

i) out of CNT : 20,266.270 oz

ii) Out of Brinks: 68,577.970 oz

iii) Out of HSBC: 463,164.360 oz

iv) out of Delaware 535,454.288 oz

Total withdrawal: 1,087m462.838 oz

adjustments: 0/

TOTAL REGISTERED SILVER: 30.195 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 271.605 million oz

CALCULATION OF SILVER OZ STANDING FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2023 OI: 145 CONTRACTS HAVING LOST 26 CONTRACT(S). WE HAD 25 CONTRACTS FILED ON WEDNESDAY, SO WE LOST ONE CONTRACTS OR AN ADDITIONAL 5,000 OZ WILL NOT STAND FOR DELIVERY ON THIS SIDE OF THE POND AS THEY WERE E.F.P.’d TO LONDON

JUNE HAD A 9 CONTRACT LOSS TO 1115

JULY HAD A 2047 CONTRACT LOSS TO 107,296 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 4 for 20,000 oz

Comex volumes// est. volume today 63,152 good/raid

Comex volume: confirmed yesterday: 57,125 FAIR

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 2558 x 5,000 oz = 12,790,000 oz

to which we add the difference between the open interest for the front month of MAY(145) and the number of notices served upon today 4 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2023 contract month: 2558 (notices served so far) x 5000 oz + OI for the front month of May (145) – number of notices served upon today (4 )x 500 oz of silver standing for the MAY contract month equates to 13.495 million oz + THE CRIMINAL 0 MILLION OZ EXCHANGE FOR RISK TODAY//NEW TOTAL EXCHANGE FOR RISK: 6.750//NEW TOTAL 20.245 MILLION OZ//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MAY 25/WITH GOLD DOWN $19.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 24/WITH GOLD DOWN $9.50 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 941.29 TONNES

MAY 23/WITH GOLD $2.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 942.74 TONNES

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

MAY 9/WITH GOLD UP $9.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTER DEPOSIT OF 5.88 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 937.64 TONNES

MAY 8/WITH GOLD UP $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 931.77 TONNES

MAY 5/WITH GOLD DOWN $30.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AS DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

MAY 4/WITH GOLD UP $19.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.30 TONNES

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

GLD INVENTORY: 941.29 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 25.WITH SILVER DOWN $0.32 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 471.606 MILLION OZ//

MAY 24/WITH SILVER DOWN $.35 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 23/WITH SILVER DOWN 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

MAY 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A TINY DEPOSIT OF .08 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 465.682 MILLION OZ//

MAY 8/WITH SILVER DOWN 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.602 MILLION OZ//

MAY 5/WITH SILVER DOWN 31 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 466.876 MILLION OZ//

MAY 4/WITH SILVER UP 53 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF .174 MILLION OZ INTO SLV.//INVENTORY RESTS AT 467.174 MILLION OZ//

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

CLOSING INVENTORY 471.606 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

Citigroup Projects $30 Silver In The Next 6-12 Months

THURSDAY, MAY 25, 2023 – 07:20 AM

Citigroup projects silver could rise to $30 an ounce in the next six months to a year.

With silver currently in the $23.50 range, this represents a possible 27.66% return.

We think recent price weakness offers a strong dip-buying opportunity, reiterating our call for $30/oz silver over the next 6-12 months as US growth rolls over, even if emerging markets growth stagnates.”

Silver is currently in a dip. The white metal is down almost 7% this month after cumulative gains of 20% over the past two months. Silver was above $26 at one point. But the dip appears to be temporary.

Citigroup analysts aren’t buying the Federal Reserve’s hawkish posturing. They think interest rates will fall in the near future as a recession takes hold.

We expect silver would rally in anticipation of the fall in US interest rates and real yields that will likely accompany an anticipated rollover in US growth in Q4’22 or early 2024. This should weigh on the dollar, with Citi economists expecting US rates and the dollar to weaken further.”

Citigroup analysts said these dynamics should underpin demand for ETF silver.

Weaker competition for investment capital from other asset classes should also support silver pricing as markets increasingly price US recession risks.”

They also expect a potential increase in demand for silver in China.

Our economists expect China to continue to gradually recover and any associated rebound in EM [emerging market] growth sentiment could be an incremental tailwind for silver. … We expect China demand could recover in 2H 23 following further easing measures by the PBoC.”

There are other bullish signs for silver the Citigroup analysis didn’t mention.

The silver-gold ratio still indicates silver is on sale.

The current silver-gold ratio is just over 83-1. That means it takes over 83 ounces of silver to buy an ounce of gold. To put that into perspective, the average in the modern era has been between 40:1 and 50:1. Historically, the ratio has always returned to that mean. And when it does, it does it with a vengeance. The ratio fell to 30-1 in 2011 and below 20-1 in 1979.

Historically, when the spread gets this wide, silver doesn’t just outperform gold, it goes on a massive run in a short period of time. Since January 2000, this has happened four times. As this chart shows, the snapback is swift and strong.

The supply-demand dynamics also look good for silver.

Silver demand set a record in every category last year, including industrial demand. Industrial offtake accounts for about half of the global demand, and that is only expected to increase in the years ahead as the push toward “green energy” continues.

Silver is an important component in solar panels. According to a study by scientists at the University of New South Wales, solar manufacturers will likely require over 20% of the current annual silver supply by 2027. And by 2050, solar panel production will use approximately 85–98% of the current global silver reserves.

On the other side of the equation, supply was flat last year and it’s expected to be flat again in 2023.

Record global silver demand and a lack of supply upside contributed to last year’s 237.7 million ounce market deficit. It was the second consecutive annual deficit in a row. The Silver Institute called it “possibly the most significant deficit on record.” It also noted that “the combined shortfalls of the previous two years comfortably offset the cumulative surpluses of the last 11 years.”

Based on the supply and demand fundamentals and Citigroup’s analysis, this may be the perfect time to buy silver.

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

John Rubino..part i

Very important..

Next Gen Money, Part 1: Texas Re-Imagines The Dollar

THURSDAY, MAY 25, 2023 – 11:05 AM

Authored by John Rubino via Substack,

Digital currency might be a good thing in the right hands…

With all the (completely justified) angst surrounding central bank digital currencies (CBDCs), it’s easy to forget that the concept of digital money isn’t the problem. It’s just a tool like any other and can be used for good or evil, depending on who’s wielding it.

Obviously, if a CBDC is managed by some combination of the Federal Reserve, the military-industrial complex, the intelligence community, and Big Pharma, that currency will be a mechanism of state control and should be avoided at all costs. But if it’s backed by gold or silver and run transparently by people who respect their citizens’ privacy and agency, then it’s potentially part of a brighter monetary future.

This brings us to Texas Senate Bill 2334, which calls for the introduction of a state-run digital currency, backed by gold and/or silver, accepted as legal tender within the state and available to people living anywhere in the world.

Texas is a logical first mover since in the 2010s it opened a state gold depository where citizens could safely store their bullion. Think of it as Texas’ Fort Knox. This depository gives the state a physical starting point for establishing a gold-backed currency.

From the Epoch Times:

Texas Lawmakers Consider Creating Gold-Based Digital Currency for Use by Anyone Anywhere

Texas could become the first state in the nation to issue its own digital currency based on gold and silver.

The Texas Senate could vote on Senate Bill 2334 this week. A similar bill in the Texas House, House Bill 4903, did not advance.

If the Texas digital currency proposal becomes law, money could be spent with a debit card by people anywhere in the world, not just within Texas.

Under the proposed law, the Texas comptroller would create a digital currency based on gold or silver and would be given the authority to mint pure gold or silver coins based on weight.

The coins and the digital currency would be considered legal tender to pay debts and would be “readily transferable … to another person,” according to the bill.

Under the plan, the digital money debit card could be used anywhere debit cards are accepted. People outside of Texas could create accounts and use the system wherever they live in the world as long as it’s legal.

The state comptroller, or a trustee hired to oversee the program, would purchase and hold enough gold or silver to cover the units of digital currency set aside for each account holder.

How a gold standard works

To make sure we’re all on the same conceptual page, a gold standard is a monetary system in which the circulating currency is backed by gold stored in a government vault. Gold and currency are convertible into each other at the discretion of their owners, which prevents the government from creating too much currency. And that’s it. No half-wit Ivy League economists rewarding their future hedge fund employers with artificially-low interest rates. No reporters asking repetitive softball questions of the aforementioned economists, and no money managers building careers on predicting what irrational thing the Fed will do next.

The central bank becomes not much more than a bank teller window, exchanging gold for cash and cash for gold. Money becomes part of the environment, a stable thing that no one worries about, rather than a tool the authorities use to manipulate markets. The rich lose the ability to game the system by buying politicians and Fed governors, so economic inequality is less of an issue. In short, the good effects of a gold standard far outweigh the bad.

Some other possible effects of Texas starting its own gold-backed currency:

- The Texas Gold Depository might become a gold/silver storage alternative to vaults in Singapore or Switzerland. For the average American, Texas would seem a lot less exotic and intimidating as a place to store physical precious metals.

- The resulting capital inflows would, other things being equal, benefit the Texas economy.

- It would serve as a proof-of-concept experiment demonstrating how a state-sponsored gold-backed digital currency would work, possibly inspiring competitors around the world.

- It would increase demand for gold and silver, giving people another way to vote with their bank accounts for a return to a gold/silver standard. The result might be a positive feedback loop in which rising demand for gold-backed currencies pushes up the price of gold, making the currencies even more attractive, and so on, until gold and silver approach their intrinsic values of $10,000 and $500 an ounce, respectively.

It’s way too early for predictions, but the best-case scenarios for state-based gold-backed digital currencies are exciting. In any event, it’s nice to be able to report some positive monetary news for a change.

end

Crooks!

New Evidence Emerges that the Investigation of the Fed’s Trading Scandal by the Inspector General Has Been a Coverup from the Beginning

By Pam Martens and Russ Martens: May 25, 2023

Unlike his three immediate predecessors who chaired the Federal Reserve (Janet Yellen, Ben Bernanke and Alan Greenspan), who all had doctoral degrees in economics, the current Fed Chairman, Jerome Powell, has a law degree from Georgetown University.

Given his legal education, one might have expected that when Fed Chair Powell became aware of the largest trading scandal in the Fed’s history in September of 2021, he would have done his legal due diligence to determine where to refer the matter for investigation.

While multiple Wall Street watchdogs called for Powell to refer the investigation to the U.S. Department of Justice and the Securities and Exchange Commission – which conduct all legitimate insider trading investigations involving publicly-traded stocks — the Fed instead referred the investigation on October 4, 2021 to the Federal Reserve Board’s own Inspector General, who is appointed by the Chair of the Fed, reports to the Fed Board (including the Chair) and can be fired by a two-thirds vote of the Fed Board.

The Fed Inspector General to whom the investigation was referred is Mark Bialek, who was appointed to the position by Fed Chair Ben Bernanke in 2011, just four days after an explosive audit of the Fed’s emergency bailout programs during and after the 2008 financial crisis was released by the Government Accountability Office (GAO). That audit showed that the Fed had secretly sluiced more than $16 trillion in cumulative loans to the mega banks on Wall Street and their foreign derivative counterparties from December 2007 to at least July of 2010. A statement from Senator Bernie Sanders’ office at the time included the following:

“The Fed outsourced virtually all of the operations of their emergency lending programs to private contractors like JP Morgan Chase, Morgan Stanley, and Wells Fargo. The same firms also received trillions of dollars in Fed loans at near-zero interest rates. Altogether some two-thirds of the contracts that the Fed awarded to manage its emergency lending programs were no-bid contracts. Morgan Stanley was given the largest no-bid contract worth $108.4 million to help manage the Fed bailout of AIG.”

Not to put too fine a point on it, but JPMorgan also played a key role in causing the financial crisis.

The bank holding companies of JPMorgan Chase, Morgan Stanley and Wells Fargo are supervised by the Federal Reserve, as is every other Wall Street mega bank holding company. At the same time, these mega banks are sitting on committees at the New York Fed to determine “best practices” for their industry. See our report: New York Fed’s Answer to Cartels Rigging Markets – Form Another Cartel.

Equally Orwellian, the Federal Reserve Board outsources the role of bank examiners to its regional Fed Banks, which – wait for it – are, literally, owned by the banks being examined, and who get to elect two-thirds of the Board of Directors of their respective regional Fed Bank. See our report: These Are the Banks that Own the New York Fed and Its Money Button.

This Kafkaesque situation resulted in one such bank examiner at the New York Fed, Carmen Segarra, rushing to the Spy Store in lower Manhattan for a tiny microphone to record the bizarre goings on at the New York Fed when she attempted to write a negative bank examination of Goldman Sachs.

On July 11, 2022, Bialek publicly released a letter clearing Fed Chair Powell and former Vice Chair Richard Clarida of violating any “laws, rules, regulations, or policies” for their part in the trading scandal. Bialek’s statement further indicated that “The investigation of senior Reserve Bank officials is ongoing.”

The senior Reserve Bank officials that Bialek is referring to include Robert Kaplan, former Dallas Fed President, and Eric Rosengren, former Boston Fed President. Both stepped down in September 2021 when news of the trading scandal first broke. See our reports: Robert Kaplan Was Trading Like a Hedge Fund Kingpin for Five Years while President of the Dallas Fed; a Dozen Legal Safeguards Failed to Stop Him and Was Boston Fed President Rosengren Trading with Citigroup’s Money?

Powell has repeatedly refused to answer press questions on the matter, stating that the investigation was in the hands of the Inspector General. For example, the following exchange occurred at Powell’s press conference on January 26, 2022, following an FOMC meeting, when Bloomberg News reporter Craig Torres raised the issue:

Torres: “Chair Powell, I have a quick administrative question. You know, Robert Kaplan’s disclosure of his securities transactions: In a couple of months, Chair Powell, or maybe sooner, you and I will file our tax returns. And we’ll list transactions and all kinds of things. And next to those transactions we’ll put dates. And Bloomberg asked for the dates of Mr. Kaplan’s transactions. The Dallas Fed is not giving us the dates. And I don’t see why this is a matter for the Inspector General or anybody else. I mean, why can’t he give us the dates? Will you help us get the dates of those transactions? Thanks.”

Powell: “I know you’ve been all over this issue with my colleagues, Craig, on the issue of information. We don’t have that information at the Board. And, you know, I had — I asked the Inspector General to do an investigation, and that is out of my hands. I’m playing no role in it. I seek to play no role in it. And I don’t — I really — I can’t help you here today on this issue. And I’m sorry I can’t.”

The financial disclosure form that Kaplan and every other Federal Reserve Bank President is required to file clearly indicates that the filer is required to give the month, day and year of each purchase and each sale of a stock or other trading instrument. The form even provides an example of how it wants the date shown, e.g., 2/1/93.

Kaplan was a former CPA with Peat Marwick Mitchell and 22-year veteran of the trading powerhouse Goldman Sachs, where he rose to the rank of Vice Chairman. Kaplan knew, or should have known, that he was evading the prescribed rules of the Federal Reserve system when he substituted the word “multiple” for the specific dates of his trades. Kaplan didn’t do this just on his financial disclosure form for 2020, when the Fed was making unprecedented market interventions during the first year of the pandemic, Kaplan did this on every financial disclosure form that he filed annually from 2015 through 2020. (See Kaplan’s 2015 through 2020 financial disclosure forms here.) And in each of those years Kaplan was, astonishingly, trading in S&P 500 futures contracts, an instrument used typically by hedge funds and other speculators to make highly leveraged bets on the direction of the market.

Every other Fed Bank President and every member of the Fed Board of Governors’ financial disclosure forms for 2020 that we reviewed listed the specific dates of each purchase and each sale of a trading instrument. But Kaplan did not list the dates of his trades for six running years.

Kaplan’s financial disclosure forms suggest that Kaplan maintained a trading relationship with Goldman Sachs, since he lists proprietary products created by “GS,” short for Goldman Sachs.

Wall Street On Parade previously reached out via email to a total of five Goldman Sachs press contacts, inquiring as to whether Kaplan was conducting his “over $1 million” S&P 500 trades and/or his individual stock trades at their firm. (Goldman Sachs’ sophisticated compliance officers should have refused such trades, and certainly in 2020 when Kaplan was a voting member of the FOMC and the Fed was taking unpresented market moving actions throughout the year in response to the pandemic.)

Goldman Sachs declined to answer our questions. The Dallas Fed refused to tell us if Kaplan was using S&P 500 futures to short the market — a bet that the market would go down.

Bialek has been silent on his investigation of Kaplan and Rosengren for more than 19 months now – other than to say that his investigation continues.

New evidence has now emerged that Bialek’s Office of the Inspector General never had the statutory authority to investigate the trading of Fed regional bank presidents in the first place.

Two days ago we sent the following email inquiry to the press office for the Federal Reserve Board’s Inspector General and a similar one to the Federal Reserve Board’s press office. We wrote:

The most recent 2021 Fed Annual Report (as well as previous ones) refer to the reach of the Inspector General of the Fed’s Board of Governors as follows:

“In addition, the OIG conducts audits, evaluations, investigations, and other reviews relating to the Board’s programs and operations as well as to Board functions delegated to the Reserve Banks. Certain aspects of Federal Reserve operations are also subject to review by the Government Accountability Office.”

In addition, in written testimony for the May 17 Senate Banking hearing, an academic scholar on Fed history, Peter Conti-Brown wrote this:

“Congress did create Inspectors General in 1978 to provide some of this oversight. The inspector general for the Federal Reserve, however, is appointed by consultation between the Fed and the CFPB, which shares a single individual inspector general. To be more precise still, this inspector general oversees only the Fed’s Board of Governors, not the Federal Reserve System.” [Bold emphasis added for this article.]

In addition, I found nothing in the Inspector General Act of 1978 (as amended) that gives the Fed Board’s OIG the authority to investigate the privately-owned Fed regional bank presidents’ trading activities.

So my question is, under what statutory authority is the Fed Board’s OIG investigating the trading activities of former Fed Bank presidents?

My deadline is tomorrow, May 24, at 6 p.m. ET.

Best regards,

Pam Martens

Editor, Wall Street On Parade

The press office for the Federal Reserve Board told us our question belonged at the press office for the Inspector General. The press office for the Inspector General cited to Bialek’s July 11, 2022 statement, while ignoring our direct question of: “under what statutory authority is the Fed Board’s OIG investigating the trading activities of former Fed Bank presidents?”

Bialek appeared as a witness at the May 17 Senate Banking Subcommittee on Economic Policy hearing last week. Senator Elizabeth Warren, Chair of the Subcommittee, showed her exasperation with Bialek’s stonewalling, stating as follows:

“You have had a year and a half. You did not call out the trades that we can see. Let us just put it this way, this is not strong oversight. In fact, it is not even competent oversight. It looks like, to anyone in the public, that you gave your boss a free pass, and that’s just not gonna cut it here. And even today, a year and a half later, the Fed continues to stonewall Congress, stonewall the public, on the underlying information about these trades. This is not acceptable. This is why we are pushing for an independent IG.”

Senator Warren has bipartisan support in the Senate to tinker around the edges of the Fed in hopes of reforming it. That includes barring executives from Wall Street mega banks from serving on regional Fed Reserve Bank’s Boards of Directors and making the Fed’s Inspector General a presidentially appointed/Senate-confirmed position.

The American people understand that tinkering is not going to reform what Senator Warren herself calls a “culture of corruption” at the Fed. This culture has become too deeply ingrained over 110 years to be cured by tinkering at the edges.

The place to start with reform is to strip the Fed of any supervisory role of these Wall Street mega banks; strip the Fed of any ability to make trillions of dollars in secret loans to these Wall Street mega banks and their trading casinos; and separate the federally-insured banks from the Wall Street trading casinos by restoring the Glass-Steagall Act, which protected the U.S. from this kind of insanity from 1933 to its repeal in 1999.

end

3,Chris Powell of GATA provides to us very important physical commentaries

UAE plus other countries are cashing in big time importing Russian gold due to the stupid sanctions. Some refiners have stopped using Russian gold and this set up the UAE with its 75 tonnes of gold in 2021 as the central hub. You can be assured that the 2022 number of gold imports to the uAE will be higher than 2021.

India will be using them to buy gold to purchase Russian oil

(Peter Hobson/Reuters)

UAE cashes in with Russian gold as sanctions bite

Submitted by admin on Thu, 2023-05-25 09:09Section: Daily Dispatches

By Peter Hobson

Reuters

Thursday, May 25, 2023

LONDON — the United Arab Emirates has become a key trade hub for Russian gold since Western sanctions over Ukraine cut Russia’s more traditional export routes, Russian customs records show.

The records, which contain details of nearly a thousand gold shipments in the year since the Ukraine war started, show the Gulf state imported 75.7 tonnes of Russian gold worth $4.3 billion — up from just 1.3 tonnes during 2021

China and Turkey were the next biggest destinations, importing about 20 tonnes each between Feb. 24, 2022 and March 3, 2023. With the UAE, the three countries accounted for 99.8% of the Russian gold exports in the customs data for this period.

In the days after the Ukraine conflict started, many multinational banks, logistics providers and precious metal refiners stopped handling Russian gold, which had typically been shipped to London, a gold trading and storage hub. …

… For the remainder of the report:

https://www.reuters.com/markets/russia-with-gold-uae-cashes-sanctions-bite-2023-05-25/

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/…

END

5.IMPORTANT COMMENTARIES ON COMMODITIES: BASE METAL GIANT NORILSK/Nickel Palladium

How sanctions have backfired again as Norlisk shipped most of its base metals and palladium to Asia

(ZEROHEDGE)

“Redrawing Global Trade Map”: Top Russian Miner Now Receives Half Of Its Revenue In Asia

WEDNESDAY, MAY 24, 2023 – 11:50 PM

The US and its G7 partners have slapped more than 300 economic sanctions on Russia since the invasion of Ukraine over a year ago. Initially, Washington and Brussels pitched the idea of sanctions as a strategy to paralyze Moscow. However, Western sanctions have backfired as Russian companies are redrawing commodity flows from the West to Asia.

The latest example of global supply chains being rejiggered comes from Russia’s biggest miner MMC Norilsk Nickel PJSC. Bloomberg said the miner recorded 45% of revenue from Asia for the first quarter of 2023. Traditionally, its revenue from Europe is the largest but plunged to 24%. Asia’s revenue share has increased from 27% in 2021 to 31% in 2022 to 45% in 2023.

Nornickel controls about 7% of global nickel output and 40% of palladium. The US and UK have imposed sanctions on Norilsk Nickel’s top shareholder and president, Vladimir Potanin. But no sanctions have been placed on the miner. However, the company faces challenges such as shipping, insurance, and logistics in getting products to Western countries, which is one of the main reasons the miner has easily found new customers in Asia.

Nornickel sought to increase sales to China this year, in some cases offering metals for yuan, people familiar with the matter said in March. Those prices are set in Shanghai, a sign of how the conflict is redrawing the global trade map for commodities and handing greater power to China, they said. –Bloomberg

Western sanctions have pushed Russia and China closer:

Chinese President Xi Jinping concluded his Russian visit on Wednesday without much progress on peace in Ukraine. China, however, has pushed for deeper trade and investment links with its northern neighbor using its own currency. That suggests the path of least resistance for yuan internationalization now runs through Moscow instead of London or Singapore. — Bloomberg Markets Live reporter George Lei wrote in March.

Lei also noted the share of yuan in Russia’s export payments has surged:

The share of yuan in Russian export payments surged 32-fold in 2022 to 16% by year-end, according to the Bank of Russia. Its use in Russian imports also jumped to 23% from 4%. Yuan savings accounted for 11% of Russia’s total FX deposits as of January, compared with practically zero when the war broke out. The Chinese currency has also overtaken the dollar and euro as the most traded FX on the Moscow Exchange.

Western sanctions severely limited Russia’s access to dollars and euros, forcing Russian companies to seek new business opportunities in Asia.

(zerohedge)

end

5 B GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.0699

OFFSHORE YUAN: 7.0827

SHANGHAI CLOSED DOWN 3.49 PTS OR 0.11%

HANG SENG CLOSED DOWN 369.01 PTS OR 1.93%

2. Nikkei closed UP 118.45 PTS OR 0.39%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 104.01 EURO FALLS TO 1.0727 DOWN 29 BASIS PTS

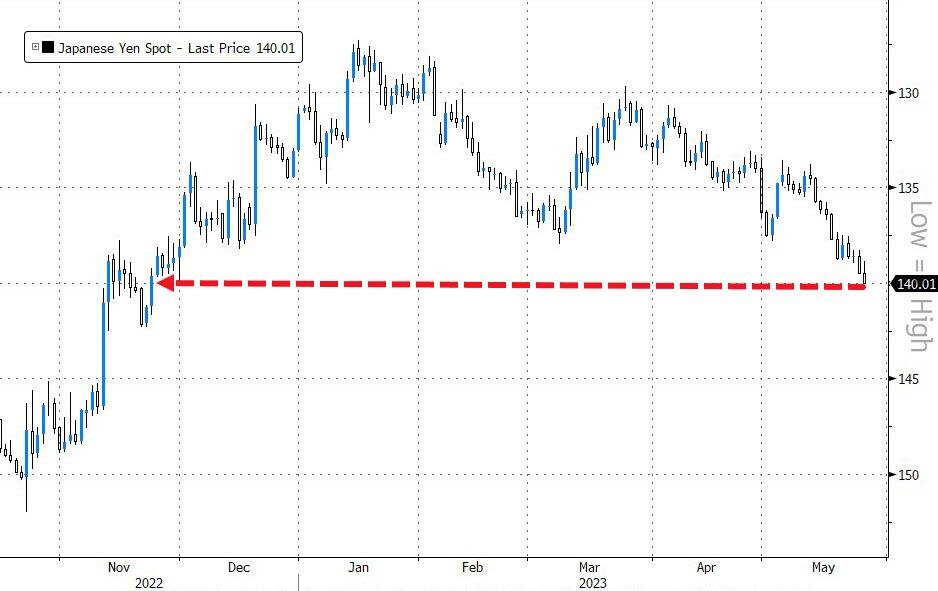

3b Japan 10 YR bond yield: RISES TO. +.429 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 139.61 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.4690***/Italian 10 Yr bond yield RISES to 4.312*** /SPAIN 10 YR BOND YIELD RISES TO 3.532…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 3.852

3j Gold at $1962.15 silver at: 23.07 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 1 /100 roubles/dollar; ROUBLE AT 80.16//

3m oil into the 72 dollar handle for WTI and 76 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 139.61 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .429% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9052 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9710 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

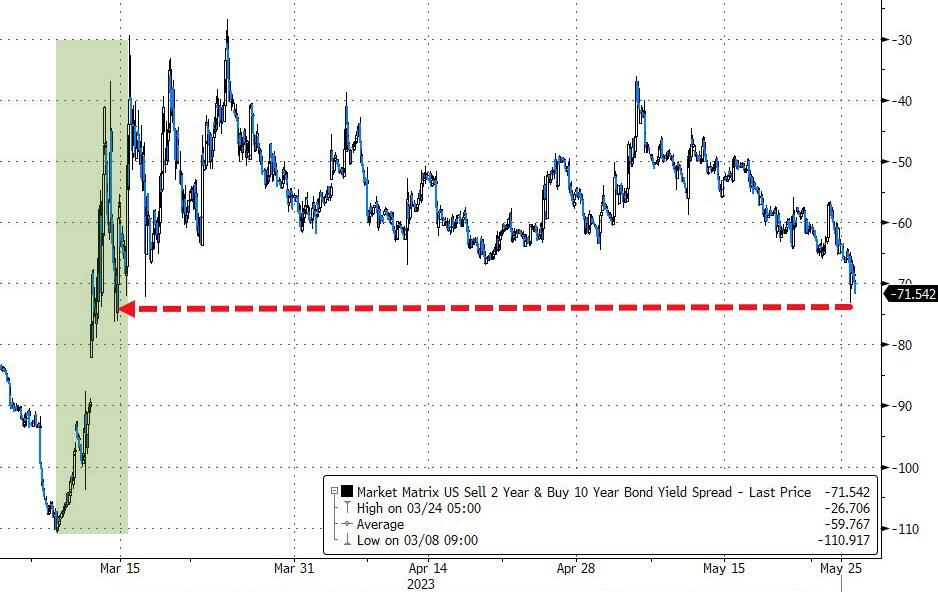

USA 10 YR BOND YIELD: 3.759 UP 4 BASIS PTS…

USA 30 YR BOND YIELD: 3.998 UP 4 BASIS PTS/

USA 2 YR BOND YIELD: 4.441 UP 7 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.93…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.3444 UP 13 BASIS PTS (RATES RISING RAPIDLY)

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

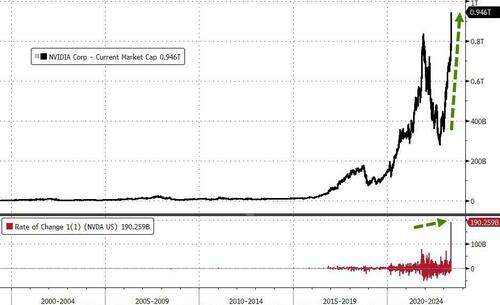

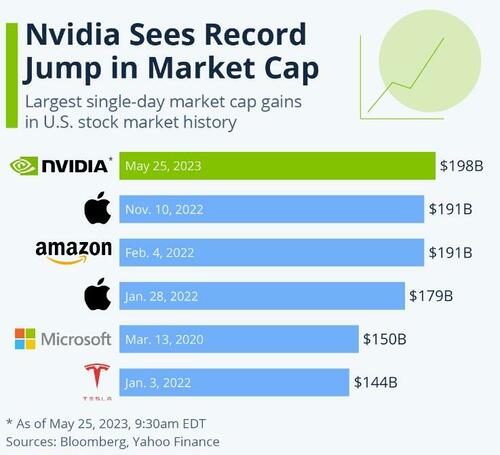

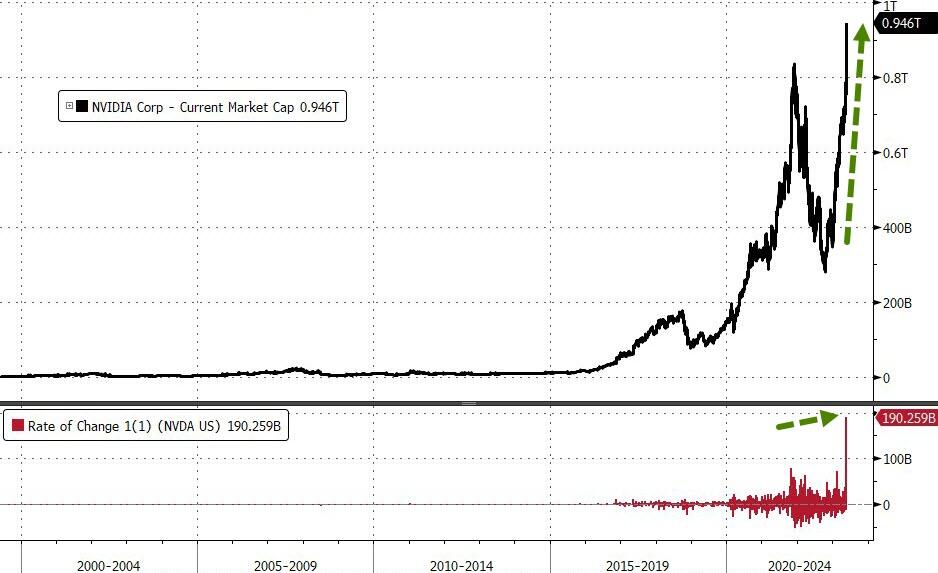

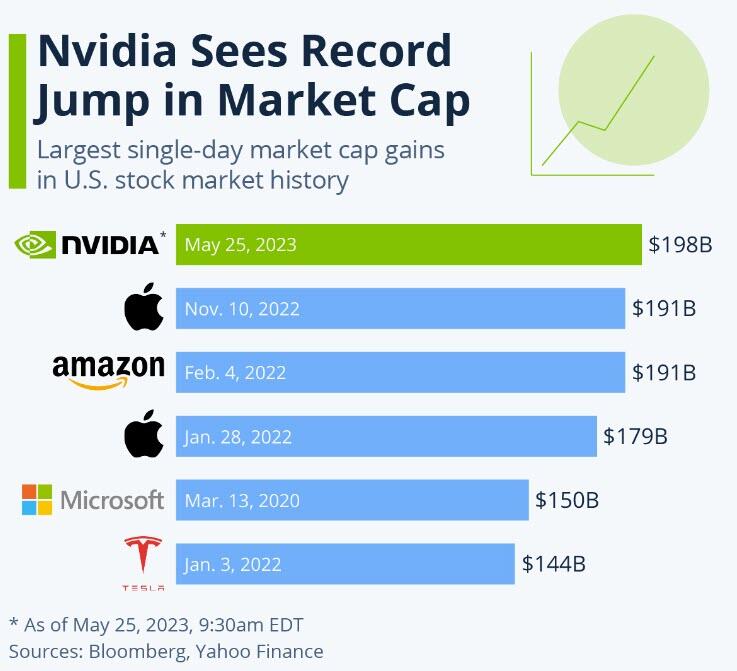

US Futures Jump Led By Record-Breaking Surge In Nvidia

THURSDAY, MAY 25, 2023 – 08:11 AM

US equity futures are higher led by tech names after blowout earnings reported by Nvidia – which as Goldman reminds us “is now #5 weight in the S&P and the poster child for “AI” Euphoria + momentum” – whose stock is up almost 30% premarket and rapidly approaching $1 trillion in market cap. S&P futures were up 0.6% to 4,151 with Nasdaq 100 futures up a whopping 2% led higher by NVDA and semi stocks. Bond yields are slightly higher, while USD is stronger. Commodities are mostly lower as WTI fell 1.5% reversing all of yesterday’s gains after Russia played down the likelihood of OPEC+ cutting production further.

In premarket trading, Tech stocks are surging boosted by NVDA which reported after the bell yesterday with forecast beat; stocks is up almost 30% after close. For some context, NVDA added > $200bn in market cap overnight post earnings and as Goldman notes, “this might be the best TMT earnings print we’ve seen since that June qtr 2020 print from Zoom (ZM), when they beat revs by ~62%.” In any case, it’s another sign that investors are willing to pile into promising tech stocks, despite the growing worries about China’s economy and a potentially catastrophic US debt default.

“If you look at tech it continues to reinvent itself over and over,” Larry Adam, chief investment officer at Raymond James, said in an interview on Bloomberg Television. “I continue to like the big tech names.”

Here are some other notable premarket movers:

- American Eagle Outfitters (AEO) shares tumble 21% after the apparel retailer’s forecast for the full-year disappointed analysts.

- Carnival Corp. (CCL) rises 2.5% after Citi upgrades to buy from hold, citing in note continued good momentum for the cruise sector.

- Desktop Metal (DM) shares trade 9.1% higher after Stratasys agreed to buy the 3D printer company in an all-stock transaction valued at around $1.8 billion. Stratasys shares are up 3.8%, reversing an earlier drop.

- Dish Network Corp. (DISH) shares are down 3.4% after Citi downgraded the satellite television company to neutral from buy.

- Dorian LPG (LPG) upgraded to outperform from inline at Evercore ISI based on valuation, following the propane gas shipper’s fourth-quarter results. Shares are up 1.1%

- Dycom Industries (DY) rises 1.5% as Wells Fargo raises to overweight from equal-weight after the engineering services company “massively” beat first-quarter expectations.

- Leidos (LDOS) rises 1.7% after Wells Fargo upgrades to overweight from equal-weight, saying the engineering company’s valuation includes too much fear around short-term uncertainty, while not taking into account upside for 2024 sales, margin and cash flow.

- Nutanix (NTNX) shares are up 17% after the infrastructure-software company boosted its revenue guidance for the full year. The outlook beat the average analyst estimate. The company also said its audit committee completed an investigation of third-party software usage.

- Nvidia Corp.’s (NVDA) blowout sales forecast puts a fresh emphasis on the latest game in town: identifying artificial intelligence losers. Shares are up 28%.

- Snowflake (SNOW) shares fall 13% after the cloud-software company cut its product revenue guidance for the full year.

In other overnight news, Fitch put US’s AAA rating on negative watch amid debt ceiling concerns, and this morning DBRS echoed the move when it “Placed United States Ratings Under Review With Negative Implications.” McCarthy signaled some progress being made on the negotiation, but representatives are not required to stay in DC over the holiday weekend. Meanwhile, JPM sees the odds of passing x-date without an increase in the ceiling index is now around 25% and rising.

Elsewhere, Treasury-bill yields slated to mature early next month surged above 7% on Wednesday, with the rate on the June 1 and June 6 maturities increasing by more than a percentage point. Those securities are seen as most at risk of non-payment if the government exhausts its borrowing capacity. On Thursday morning, Bills maturing on June 1 traded just around 7%.

“Nvidia was last night’s good surprise,” said Gilles Guibout, head of European equity strategies at Axa Investment Managers. “But more broadly, there are few reasons for the market to keep rising: interest rates are not going down, global economic growth isn’t rebounding, full-year earnings are seen flat and stock valuations are already at a decent level.”

European markets were propped up by chipmakers after sales guidance from Nvidia smashed expectations – shares in the US semiconductor maker are up ~28% in the premarket. The Stoxx 600 is up 0.1% after touching a seven-week low on Wednesday. Here are some of the most notable European movers:

- ASML leads a rally in shares of European semiconductor equipment makers after US chipmaker Nvidia gave a sales forecast that blew past estimates, boosted by burgeoning AI demand

- GN Store Nord gains as much as 10%, the most in a month, after a DKK2.75 billion rights issue removes a “significant overhang” for the Danish hearing-aid and audio equipment firm, Citi says

- Tate & Lyle rises as much as 2.6% after the ingredients company reported FY23 results and forecast revenue growth of 4%-6% for the current fiscal year. The profit beat was impressive, Citi says

- Elekta shares gain as much as 4.8% after the Swedish medical technology firm beat expectations on sales and Ebit, with Handelsbanken noting the company’s free cash flows are at a record high

- D’Ieteren rises as much as 3.3% after the automotive retailer reiterates its pretax profit guidance for the full year. Analysts flag this was maintained despite costs associated with recent refinancing

- QinetiQ rises as much as 2.2%, snapping three days of declines, after the British technology and research firm delivered full-year results that Barclays says beat consensus on all metrics

- ALSO gains as much as 2.4% after Stifel initiated coverage of the Swiss IT and consumer electronics wholesaler with buy, saying its cloud marketplace business is an underestimated value driver

- Allegro shares fall as much as 6.7%, their biggest decline in more than four months, after Poland’s biggest e-commerce platform guided for slower gross merchandise value growth in 2Q

- Johnson Matthey shares decline as much as 3.8%, to the lowest since October, after the UK-based chemicals company published below-consensus guidance for this year and next

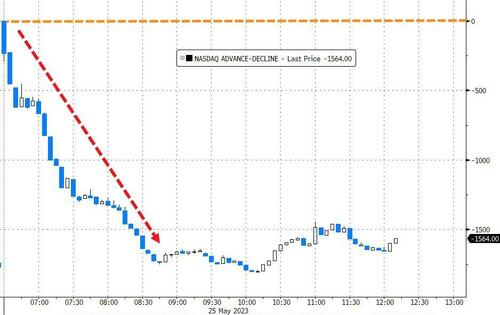

Earlier in the session, Asian stocks were mostly lower with the region cautious after the losses on Wall Street due to debt ceiling fears. The MSCI Asia-Pacific index closed 0.8% lower for the day as sentiment around Chinese markets continued to worsen. The Hang Seng Index shed 1.9% on the day and the yuan broke through the closely-watched 7-per-dollar level. The key worry for investors is that China’s economy is losing momentum and there are persistent financial troubles in the real estate industry. Recent data suggest gross domestic product growth this year will be closer to the government’s target of about 5%, contrary to expectations of a large overshoot formed earlier in the year. The Hang Seng was pressured with underperformance in Hong Kong after the benchmark index slipped beneath the 19,000 level.

- Japan’s Nikkei 225 was kept afloat but with the upside capped in the absence of any major positive drivers.

- Australia’s ASX 200 weakened as the commodity-related sectors led the broad declines across nearly all industries and with sentiment also dampened as households are set to pay hundreds of dollars more each year after the energy regulator approved an increase of up to 25% in electricity bills.

- Korea’s KOSPI was subdued after the BoK rate decision in which the central bank kept rates unchanged as expected, although 6 out of the 7 board members saw the need to keep the door open for one more rate hike.

- Indian stocks recovered late in the day to end higher and outperform most of their Asian peers even as broad sentiment remains cautious amid ongoing concerns of a possible debt default by the US. The S&P BSE Sensex rose 0.2% to 61,872.62 in Mumbai, while the NSE Nifty 50 Index advanced 0.2% to 18,321.15. Stocks of consumer staple, energy and communication services firms, part of the benchmarks, led the recovery as the May futures contract expired.

In FX, the Bloomberg dollar index climbed for a fourth day, boosted by rising US yields and more-averse trading conditions after Fitch Ratings on Wednesday said it may downgrade the US’s AAA credit rating; the kiwi is the weakest of the G-10 currencies. The USD/JPY was little changed at 139.49, holding near 139.70 hit in earlier trade, its highest since late November.

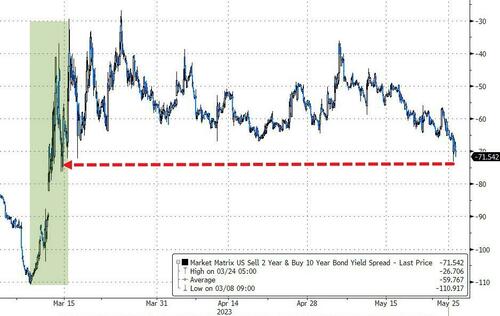

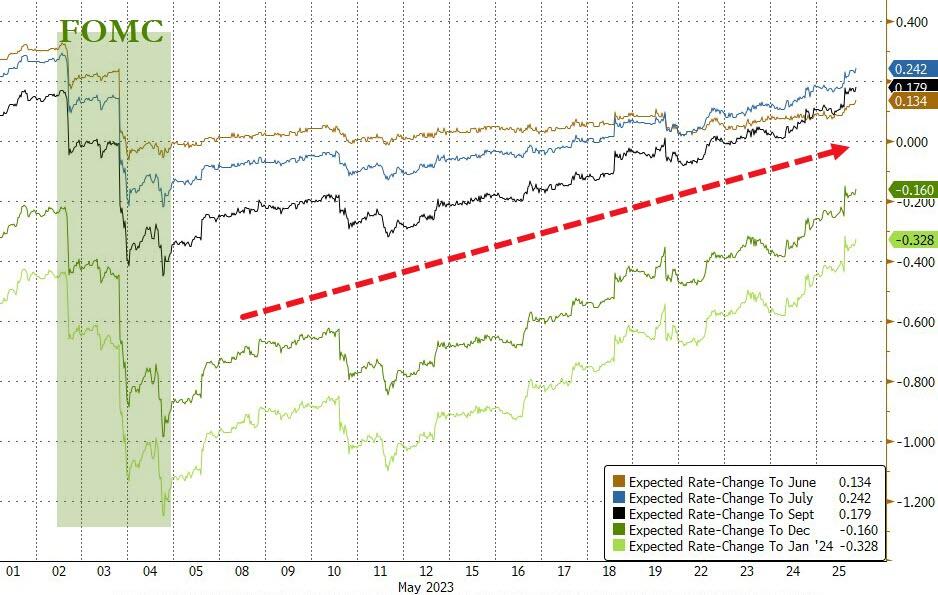

In rates, treasuries are lower with the US 10-year yield rising 1bps to 3.76% ahead of GDP and claims data. The yield on two-year Treasuries rose 4 basis points to 4.42%, its highest since March; traders are pricing in a nearly 50% chance that the Fed will raise rates by 25 basis points next month; 10-year yields sit around 3.76%, with gilts trading cheaper by 10bp in the sector as rate-hike premium increases further in sterling swaps. A late Wednesday announcement that Fitch placed US credit on “rating watch negative” elicited limited market reaction. The US auction cycle concludes with $35b 7-year note sale at 1pm, following strong demand for 2- and 5-year sales. WI yield around 3.790% is ~25bp cheaper than last month’s, which tailed by 1.3bp.

Meanwhile, UK government bonds led losses in Europe. Traders added to bets the Bank of England will keep raising interest rates after an unexpectedly strong reading of UK inflation Wednesday. Money markets are now pricing more than 100 basis points of additional tightening by December.

In commodities, WTI declined 1.3% to trade near $73.40 on Thursday after the dollar strengthened and Russia played down the likelihood of OPEC+ cutting production further. Billionaire mining investor Robert Friedland says the copper market weakness is temporary. Southwestern Energy is among the most active resources stocks in premarket trading, falling 4.6%.

Bitcoin is lower but holding above the $26k mark despite briefly dropping below in early trade, with the USD capping upside and broader marks still focused on the debt ceiling as we near the US long weekend.

To the day ahead now, and data releases from the US include the weekly initial jobless claims, the second estimate of Q1 GDP, pending home sales for April, and the Kansas City Fed’s manufacturing index for May. Central bank speakers include the Fed’s Barkin and Collins, ECB Vice President de Guindos and the ECB’s Nagel, Villeroy, Centeno and De Cos, along with the BoE’s Haskel.

Market Snapshot

- S&P 500 futures up 0.5% to 4,144.75

- MXAP down 0.8% to 159.34

- MXAPJ down 0.9% to 503.86

- Nikkei up 0.4% to 30,801.13

- Topix down 0.3% to 2,146.15

- Hang Seng Index down 1.9% to 18,746.92

- Shanghai Composite down 0.1% to 3,201.26

- Sensex down 0.4% to 61,526.09

- Australia S&P/ASX 200 down 1.0% to 7,138.16

- Kospi down 0.5% to 2,554.69

- STOXX Europe 600 down 0.1% to 457.06

- German 10Y yield little changed at 2.47%