MAY 30/GOLD PRICE UP $14.55 TO $1959.00//SILVER DOWN 9 CENTS TO $23.25//PLATINUM DOWN $5.45 TO $1925.85//PALLADIUM IS UP 30 CENTS TO$1406.50//MUST READS: MATHEW PIEPENBERG AND PETER SCHIFF//IN CHINA HUGE NUMBER OF SHADOW BANKING DEFAULTS//UKRAINE VS RUSSIA UPDATES//GOOD COMMENTARY FROM COL MACGREGOR//TURKISH LIRA COLLAPSES ON THE NEWS OF ERDOGAN’S ELECTION VICTORY///SERBIA AND KOSOVO UNDERGO HUGE BATTLES AT THEIR BORDER//COVID UPDATES/VACCINE IMPACT/DR PAUL ALEXANDER/SLAY NEWS/EVOL NEWS/UPDATES ON THE DEBT CEILING FIASCO//STATE FARM HALTS HOME INSURANCE IN CALIFORNIA AS THEY ARE SUFFERING HUGE LOSSES WITH FIRES ETC//SWAMP STORIES FOR YOU TONIGHT//

GOLD: NUMBER OF NOTICES FILED FOR MAY/2023. CONTRACT: 0 NOTICES FOR 0 OZ or 0.003110 TONNES

total notices so far: 6140 contracts for 614,000 oz (19.094 tonnes)

FOR MAY:

SILVER NOTICES: 4 NOTICE(S) FILED FOR 200,000 OZ/

total number of notices filed so far this month : 2694 for 13,470,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP UP $14.55

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

/NO CHANGES IN GOLD INVENTORY AT THE GLD:////

INVENTORY RESTS AT 941.29 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 9 CENTS AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV ///: ; : INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 468.300 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1025 CONTRACTS TO 135,152 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR VERY STRONG $0.44 RISE IN SILVER PRICING AT THE COMEX ON FRIDAY. TAS ISSUANCE WAS A TOUCH SMALLER SIZED 517 CONTRACTS. THESE WILL BE USED FOR MANIPULATION NEXT MONTH. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON FRIDAY: A LITTLE SMALLER 517 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS) IF A CALENDAR SPREAD OCCURS. IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED THE COMPLAINT. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.44). BUT WERE UNSUCCESSFUL IN KNOCKING SOME SPEC LONGS AS WE HAD A HUGE LOSS ON OUR TWO EXCHANGES OF 731CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 6.750MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION. WE WILL HAVE IN OUR FINAL WEEK IN THE DELIVERY CYCLE MORE MANIPULATION IN OUR PRECIOUS METALS DUE TO COMEX SPREADERS LIQUIDATION ACCOMPANYING OPTIONS EXPIRY ON BOTH THE COMEX AND LONDON’S LBMA ALONG WITH AN ADDED FEATURE OF TAS LIQUIDATION.

WE MUST HAVE HAD:

A FAIR SIZED ISSUANCE OF EXCHANGE FOR PHYSICALS( 245 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.105 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP OF 140,000 OZ (QUEUE. JUMP RAISES THE AMOUNT OF SILVER STANDING)+0 MILLION OZ EXCHANGE FOR RISK ISSUED TODAY// TOTAL FOR THE MONTH 6.75MILLION OZ OF EXCHANGE FOR RISK (RAISES THE AMOUNT OF SILVER STANDING):THUS TOTAL OF 20.340 MILLION OZ OF SILVER STANDING FOR DELIVERY V) STRONG SIZED COMEX OI LOSS/ FAIR SIZED EFP ISSUANCE/VI) SMALLER NUMBER OF T.A.S. CONTRACT INITIATION (517 CONTRACTS)//CONSIDERABLE T.A.S LIQUIDATION MANIPULATING THE PRICE SOUTHBOUND FRIDAY.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -removed 49CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTRACTS for 21 days, total 13,055 contracts: OR 65.275 MILLION OZ . (621 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 65.275 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 65.275 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 976 CONTRACTS DESPITE OUR STRONG SIZED $0.44 GAIN

IN SILVER PRICING AT THE COMEX//FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 245 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAY OF 13.105 MILLION OZ//FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 140,000 OZ (INCREASES THE AMOUNT OF SILVER STANDING) +// + 0 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //TOTAL EXCHANGE FOR RISK MONTH= 6.75 MILLION//NEW TOTALS 13.590 MILLION OZ + 6.75 MILLION EXCH./RISK = 20.340 MILLION OZ STANDING FOR MAY// .. WE HAVE A HUGE SIZED LOSS OF 731 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A SMALLER 517//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED FRIDAY. THE NEW TAS ISSUANCE WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE.

WE HAD 4 NOTICE(S) FILED TODAY FOR 20,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A VERY STRONG SIZED 12,768 CONTRACTS TO 453,348 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED – 296 CONTRACTS

WE HAD A VERY STRONG SIZED DECREASE IN COMEX OI ( 12,768 CONTRACTS) DESPITE OUR $0.90 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR MAY. AT 3.5085 TONNES ON FIRST DAY NOTICE // PLUS 0 OZ QUEUE. JUMP :(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)/+ /A LARGER ISSUANCE OF 1016 T.A.S. CONTRACTS/STRONG FRONT END OF TAS LIQUIDATION FRIDAY ////YET ALL OF..THIS HAPPENED WITH ONLY A $0.90 GAIN IN PRICEWITH RESPECT TO FRIDAY’S TRADING.WE HAD A STRONG SIZED LOSS OF 10,074 OI CONTRACTS (31.33 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2694 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 453,348

IN ESSENCE WE HAVE A GOOD SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,074 CONTRACTS WITH 12,768 CONTRACTS DECREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): 1016 CONTRACTS) AND 2694 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 10,074CONTRACTS OR 31.33TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2694 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (12,768) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 10,074 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 3.5085 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 0 OZ // NEW STANDING: 19.094 TONNES+ 1.244 TONNES OF EXCHANGE FOR RISK//NEW TOTALS FOR GOLD STANDING FOR MAY: 20.338 TONNES // ///3) SOME LONG LIQUIDATION//4) VERY STRONG SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: LARGER T.A.S. ISSUANCE: 1016 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 71,385 CONTRACTS OR 7,138,500 OZ OR 222.03 TONNES IN 21 TRADING DAY(S) AND THUS AVERAGING: 3399 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21 TRADING DAY(S) IN TONNES 222.03 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 222.03/3550 x 100% TONNES 6.25% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES ( MUCH SMALLER THAN LAST MONTH)

MAY: 222.03 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A STRONG SIZED 1025 CONTRACTS OI TO 135,152 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 245 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 245 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 245 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 10,074 CONTRACTS AND ADD TO THE 245OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 780 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 3.900 MILLION OZ

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED UP 2.77 PTS OR 0.09% //Hang Seng CLOSED UP 44.67 PTS OR .24% /The Nikkei closed DOWN 94.62 OR .30% //Australia’s all ordinaries CLOSED DOWN 0.11 % /Chinese yuan (ONSHORE) closed DOWN 7.0808 /OFFSHORE CHINESE YUAN DOWN TO 7.0904 /Oil DOWN TO 71.82 dollars per barrel for WTI and BRENT AT 75/96 / Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 12,472 CONTRACTS DOWN TO 453,644 DESPITE OUR GAIN IN PRICE OF $0.90 ON FRIDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF MAY… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2694 EFP CONTRACTS WERE ISSUED: : JUNE 2694 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2694 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 10,074 CONTRACTS IN THAT 2694LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A VERY STRONG SIZED LOSS OF 12,768 COMEX CONTRACTS..AND THIS STRONG SIZED LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR GAIN IN PRICE OF 90 CENTS. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE TODAY WAS A MUCH STRONGER 1016 CONTRACTS. DURING THIS PAST WEEK THEY SOLD THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE//(e.g. JUNE TAS 480 AND AUG TAS 524/ALL OTHER MONTHS NEGLIGIBLE). IT NOW LOOKS LIKE T.A.S. MANIPULATION WILL BE US UNTIL MONTH’S END.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (20.338) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $0.90) //// BUT WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD OUR STRONG SIZED LOSS OF 10,074 CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE TAS LIQUIDATION. AND NOW FOR THE FIRST TIME TAS LIQUIDATION IS EXTENDING PAST MID MONTH. THE TAS ISSUED FRIDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 30.413PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY. (3.5085 TONNES) //NEW STANDING 19.094 TONNES+1.244 exchange for risk(prior)// new total 20.338 tonnes ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $0.90

WE HAD – REMOVED 296 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 10,074 CONTRACTS OR 1,007,400 OZ OR 31.33 TONNES.

6044.388 oz Manfra (150 kilobars) Int Delaware (20 kb) HSBC (15 kilobars) Brinks (3 kilobars)

.

nil

Deposit to the Dealer Inventory in oz

Deposits to the Customer Inventory, in oz

nil

No of oz served (contracts) today

0 notice(s) 0 OZ 0.0 TONNES

No of oz to be served (notices)

0 contracts 0 oz 0.0 TONNES

Total monthly oz gold served (contracts) so far this month

6140 notices 614,000 OZ 19.0974 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

Withdrawals:

6044.388 oz

Manfra (150 kilobars) 4822.65 oz Int Delaware (20 kb) 643.02 oz HSBC (15 kilobars) 482.285 oz

Brinks (3 kilobars) 96.43 oz

Adjustments; one

dealer to customer Malca: 7523.334 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 0 contracts having LOST 1 contracts. We had 1 contracts filed

on FRIDAY, so we GAINED 0 contracts or an additional NIL oz will stand for gold in this non active delivery month of May

June LOST A HUGE 31,886 contracts DOWN to 37,726 contracts. We should have a strong delivery month for June (around 70 tonnes). We have 1 more reading

day before first day notice.

July lost 67 contracts to stand at 2850 contracts.

AUGUST gained 19,404 contracts UP to 355,835 contracts

We had 0 contracts filed for today representing 0 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2023. contract month,

we take the total number of notices filed so far for the month (6,140 x 100 oz ), to which we add the difference between the open interest for the front month of MAY (0 CONTRACT) minus the number of notices served upon today 0 x 100 oz per contract equals 614,000 OZ OR 19.094 TONNES the number of TONNES standing in this NON- active month of May. And now we must add 1.244 tonnes of gold delivery through our 400 contract exchange for risk//new total 20.338 tonnes of gold.

thus the FINAL standings for gold for the MAYcontract month: No of notices filed so far (6,140 x 100 oz) x xxx OI for the front month minus the number of notices served upon today (0)x 100 oz} which equals 614,000 oz standing OR 19.094 TONNES + 1.244 (exchange for risk) = 20.338 tonnes

TOTAL COMEX GOLD STANDING: 20.338 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,865,285.029 OZ

TOTAL REGISTERED GOLD: 12,007,392.523 (373,34 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,857,892.506 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,302,663 OZ (REG GOLD- PLEDGED GOLD) 320.455 tonnes//

END

SILVER/COMEX

MAY 30//2023// THE MAY 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

288,045.858 oz CNT Delaware Loomis

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

1.815.101/125 oz Delaware Loomis

No of oz served today (contracts)

4 CONTRACT(S) (20,000 OZ)

No of oz to be served (notices)

24 contracts (120,000 oz)

Total monthly oz silver served (contracts)

2694 Contracts (13,470,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposits

total dealer deposit: nil oz

total dealer deposits: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We had 2 customer deposits

i) Into Delaware: 15,045.285 oz

ii) Into Loomis: 1,800,055.840 oz

Total deposits: 1,815,101.125 oz

JPMorgan has a total silver weight: 141.313 million oz/273.670 million =51.53% of comex .//dropping fast

Comex withdrawals 3

i) Out of CNT: 17,226.780 oz

ii) Out of Delaware 69,834.922 oz

iii) Out of Loomis: 200,984.156 oz

total withdrawals: 288,045.858 oz

adjustments: 0

TOTAL REGISTERED SILVER: 29;881 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 273.670 million oz

CALCULATION OF SILVER OZ STANDING FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2023 OI: 28 CONTRACTS HAVING LOST 104 CONTRACT(S). WE HAD 132 CONTRACTS FILED ON THURSDAY, SO WE GAINED 28 CONTRACTS OR AN ADDITIONAL 140,000 OZ WILL STAND FOR DELIVERY ON THIS SIDE OF THE POND

JUNE HAD A 72 CONTRACT LOSS TO 1042

JULY HAD A 1643 CONTRACT LOSS TO 104,873 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 4 for 20,000 oz

Comex volumes// est. volume today 81,262 excellent/

Comex volume: confirmed yesterday: 63,370 good

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 2694 x 5,000 oz = 13,470,000 oz

to which we add the difference between the open interest for the front month of MAY(28) and the number of notices served upon today 4 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2023 contract month: 2694 (notices served so far) x 5000 oz + OI for the front month of May (28) – number of notices served upon today (4 )x 500 oz of silver standing for the MAY contract month equates to 13.590 million oz + THE CRIMINAL 0 MILLION OZ EXCHANGE FOR RISK TODAY//NEW TOTAL EXCHANGE FOR RISK: 6.750//NEW TOTAL 20.340 MILLION OZ//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MAY 30/WITH GOLD UP $14.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 26/WITH GOLD UP $.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 941.29 TONNES

MAY 25/WITH GOLD DOWN $19.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 24/WITH GOLD DOWN $9.50 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 941.29 TONNES

MAY 23/WITH GOLD $2.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 942.74 TONNES

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

MAY 9/WITH GOLD UP $9.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTER DEPOSIT OF 5.88 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 937.64 TONNES

MAY 8/WITH GOLD UP $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 931.77 TONNES

MAY 5/WITH GOLD DOWN $30.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AS DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

MAY 4/WITH GOLD UP $19.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.30 TONNES

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

GLD INVENTORY: 941.29 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 30/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 26/WITH SILVER UP $0.44 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.306 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 25.WITH SILVER DOWN $0.32 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 471.606 MILLION OZ//

MAY 24/WITH SILVER DOWN $.35 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 23/WITH SILVER DOWN 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

MAY 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A TINY DEPOSIT OF .08 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 465.682 MILLION OZ//

MAY 8/WITH SILVER DOWN 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.602 MILLION OZ//

MAY 5/WITH SILVER DOWN 31 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 466.876 MILLION OZ//

MAY 4/WITH SILVER UP 53 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF .174 MILLION OZ INTO SLV.//INVENTORY RESTS AT 467.174 MILLION OZ//

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

CLOSING INVENTORY 471.300 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

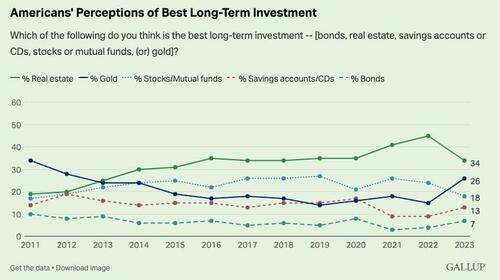

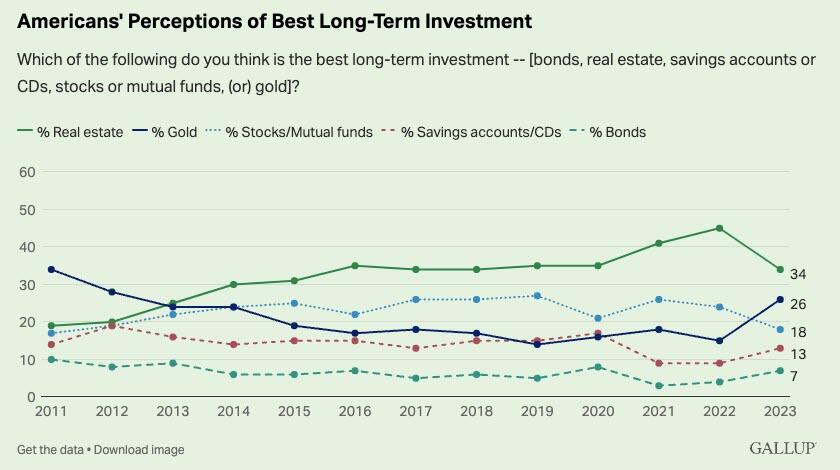

Americans Rank Gold As Second-Best Long-Term Investment

Americans consider gold the second-best long-term investment option, according to a recent Gallup poll. Gold beat out stocks, bonds and savings accounts.

The perception that gold is the best investment over the long term rose from 15% in 2022 to 26% in the 2023 poll, overtaking stocks at the number two spot.

Real estate has held the top spot since 2013 with 35% of Americans rating it the best long-term investment in the most recent poll. That was down sharply from last year’s record high of 45%.

Stocks held third place with 18%, followed by savings accounts/CDs (13%) and bonds (7%).

When cryptocurrency was included in the options, it got 4% of the votes. That was down from 8% in 2022.

On the contrary, the number of Americans naming gold as the best long-term investment almost doubled this year from last. This, despite interest rates climbing to a 16-year high in March.”

The Gallup poll dovetails with gold demand data. Demand hit an 11-year high in 2022, driven primarily by central bank gold buying and physical gold investment.

Gold bar and gold coin demand grew by 2% globally in 2022, building on strong demand in 2021. In total, global investors bought 1, 217 tons of gold bars and coins. The second half of the year was particularly strong for bar and coin buying, charting two successive quarters of demand of around 340 tons for the first time since 2013.

Investors in the West had a particularly strong appetite for gold and broke an annual record. Combined US and European purchases of gold bars and coins hit 427 tons. That exceeded the previous record of 416 tons set in 2011.

While institutional investors have sold gold on hot inflation news, thinking that means more rate hiking by the Federal Reserve, Street speculated that inflation pressure on US consumers may be driving demand as people seek an inflation hedge.

According to the Gallup poll, conviction in savings accounts/cash deposits as a good long-term investment increased only slightly this year, even with cash deposit rates reaching 5%. But these rates are still quite poor in real terms and anyone expecting persistent inflation may be tempted more by the long-term investment proposition of gold than that of savings accounts. Our research shows that gold’s potential to ‘protect against inflation/currency fluctuations’ is well recognized among gold investors.”

World Gold Council research shows Americans recognize gold’s “long-term value proposition and save haven attributes.” According to the WGC, around two-thirds of investors agree that “gold is a good safeguard against periods of political and economic uncertainty” and that “the price of gold increases over time.”

Below, we look at simple facts in the context of complex markets to underscore the dangerous direction of Fed-Speak and Fed policy.

Keep It Simple, Stupid

It’s true that, “the Devil is in the details.”

Anyone familiar with Wall Street in general, or market math in particular, for example, can wax poetic on acronym jargon, Greek math symbols, sigma moves in bond yields, chart contango or derivative market lingo.

Notwithstanding all those “details,” however, is a more fitting phrase for our times, namely: “Keep it simple, stupid.”

The Simple and the Stupid

The simple facts are clear to almost anyone who wishes to see them.

With US debt, for example, at greater than 120% of its GDP, Uncle Sam has a problem.

That is, he’s broke, and not just debt-ceiling broke, but I mean broke, broke.

It’s just THAT simple.

Consequently, no one wants his IOUs, confirmed by the simple/stupid fact that in 2014, foreign Central Banks stopped buying US Treasuries on net, something not seen in five decades.

In short, the US, and its sacred bonds, just aren’t what they used to be.

To fill this gap, that creature from Jekyll Island otherwise known as the Federal Reserve, which is neither Federal nor a reserve, has to mouse-click money to pay the deficit spending of short-sighted and opportunistic administrations (left and right) year after year after year.

Uncle Fed, along with its TBTF nephews, have thus become the largest marginal financiers of US deficits for the last 8 years.

In short, the Fed and big banks are literally drinking Uncle Sam’s debt-laced Kool aide.

The Fed’s money printer has thus become central to keeping credit markets alive despite the equal fact (paradox) that its rate hikes are simultaneously gutting bonds, banks and small businesses to fight inflation despite the stubborn fact that such inflation is still here.

Like all debt-soaked and failing regimes, the Fed secretly wants inflation to outpace rates (i.e., it wants “negative real rates”) in order to inflate away some of that aforementioned and embarrassing debt.

Thus, the Fed will seek inflation while simultaneously mis/under-reporting CPI inflation by at least 50%. I’ve described this as “having your cake and eating it too.”

All that said, inflation, which was supposed to be transitory, is clearly sticky (as we warned from the beginning), and even its under-reported 6% range has the experts in a tizzy of comical proportions.

Neel Kashkari, for example, is thinking the US may need to get rates to at least 6% to “beat” inflation. James Bullard is asking for more rate hikes too.

But what these “go higher, longer” folks are failing to mention is that rate hikes make Uncle Sam’s bar tab (i.e., debt) even more expensive, a fact which deepens rather than alleviates the US deficit nightmare.

The War on Inflation is a Policy that Actually Adds to Inflation

Ironically, however, few (including Kashkari, Bullard, Powell or just about any economic midget in the House of Representatives) are recognizing the additional paradox that greater deficits only add to (rather than “combat”) the inflation problem, as deficit spending (an economy on debt respirator) keeps artificial demand (and hence) prices rising rather than falling.

Furthermore, these deficits will ultimately be paid for with more fiat fake money created out of thin air at the Eccles building, a policy which is inherently (and by definition): INFLATIONARY.

In short, and as even Warren B. Mosler recently tweeted, “the Fed is chasing its own tail.”

Inflation, in other words, is not only here to stay, the Fed’s “anti-inflationary” rate hike policies are actually making it worse.

Even party-line economists are forecasting higher core inflation this year:

The Real Solution to Inflation? Scorched Earth.

In fact, the only way to truly dis-inflate the inflation problem is to raise rates high enough to destroy the bond market and the economy.

Afterall, major recessions/depressions do “beat” inflation—along with just about everything and everyone else.

The current Fed’s answer to combatting the inflation problem is in many ways the equivalent of combatting a kitchen rodent problem by placing dynamite in the sink.

Meanwhile, the Rate Hikes Keep Blowing Things Up

Buried beneath the headlines of one failing bank (and tax-payer-funded depositor bailout) after the next, is the equally dark picture of US small businesses, all of which rely on loans to stay afloat.

But according to the U.S. Small Business Association, loan rates for the “little guys” have reached double digit levels.

Needless to say, such debt costs don’t just hurt small enterprises, they destroy them.

This credit crunch is only just beginning, as small enterprises borrow less in the face of rising rates.

Real estate, of course, is just another sector for which the “war on inflation” rate hikes are creating collateral damage.

Homeowners enjoying the fixed low rates of days past are naturally remiss to sell current homes only to face the pain of buying a newer one at much higher mortgage rates.

This means the re-sale inventory for older homes is shrinking, which means the market (as well as price) for new construction homes is spiking—serving as yet another and ironic example of how the Fed’s alleged war on inflation is actually adding to price inflation…

In short, Fed rate hikes can make inflation rise, and equally tragic, is that Fed rate cuts can also make inflation rise, as cheaper money only means greater velocity of the same, which, alas, is inflationary…

See the Paradox?

And that, folks, is the paradox, conundrum, corner or trap in which our central planners have placed us and themselves.

As I’ve warned countless times, we must eventually pick our poison: It’s either a depression or an inflation crisis.

Ultimately, Powell’s rate hikes, having already murdered bonds, stocks and banks, will also murder the economy.

Save the System or the Currency?

At that inevitable moment when the financial and social rubble of a national and then global recession is too impossible to ignore, the central planners will have to take a long and hard look at the glowing red buttons on their money printers and decide which is worthing saving: The “system” or the currency?

The answer is simple. They’ll push the red button while swallowing the blue pill.

Ultimately, and not too far off in our horizon, the central planners will “save” the system (bonds and TBTF banks) by mouse-clicking trillions of more USDs.

This simply means that the deflationary recession ahead will be followed by a hyper-inflationary “solution.”

Again, and worth repeating, history confirms in debt crisis after debt crisis, and failed regime after failed regime, that the last bubble to “pop” is always the currency.

A Long History of Stupid

In my ever-growing data base of things Fed-Chairs have said that turned out to be completely and utterly, well…100% WRONG, one of my favorites was Ben Bernanke’s 2010 assertion that QE would be “temporary” and with “no consequence” to the USD.

According to this false idol, QE was safe because the Fed was merely paying out dollars to purchase Treasuries is an even swap of contractually even values.

What Bernanke failed to foresee or consider, however, is that such an elegant “swap” is anything but elegant when the Fed is marred by an operating loss in which its Treasuries are tanking in value.

That is, the “swap” is now a swindle.

As deficits rise, the TBTF banks will require more mouse-clicked (i.e., inflationary) dollars to meet Uncle Sam’s interest expense promise to the banks (“Interest on Excess Reserves”).

In the early days of standard QE operations, at least the Fed’s printed money was “balanced” by its purchased USTs which the TBTF banks then removed from the market and parked “safely” at the Fed.

But today, given the operating losses in play, the Fed’s raw money printing will be like like raw sewage with nowhere to go but straight into the economy with an inflationary odor.

Bad Options, Fluffy Words

Again, the cornered Fed’s options are simple/stupid: It can continue to hawkishly raise rates higher for longer and send the economy into a depression and the markets into a spiral while declaring victory over inflation, or it can print trillions more fiat dollars to prop the system and neuter/debase the dollar.

And for this wonderful set of options, Bernanke won a Nobel Prize?

The ironies do abound…

But as a famous French moralist once said, the highest offices are rarely, if ever, held by the highest minds.

Gold, of course, is not something the Fed (nor anyone else) can print or mouse-click, and gold’s ultimate role as a currency-insurer is not a matter of debate, but a matter of cycles, history and simple/stupid common sense. (See below).

Markets Are Prepping

In the interim, the markets are slowly catching on to the fact that protecting purchasing power is now more of a priority than looking for safety in grossly and un-naturally inflated “fixed income” or “risk-free-return” bonds.

Why?

Because those bonds are now (thanks to Uncle Fed) empirically and mathematically nothing more than “no-income” and “return-free-risk.”

Meanwhile, hedge funds are building their net short positions in S&P futures at levels not seen since 2007 for the simple reason that they foresee a Powell-induced market implosion off the American bow.

Once that foreseeable implosion occurs, get ready for the Fed’s only pathetic tools left: Lower rates and trillions of instant liquidity—the kind that kills a currency.

In Gold We Trust

The case for gold as insurance against such a backdrop of debt, financial fragility and openly dying currencies is, well: Simple stupid and plain to see.

Few on this round earth see the simple among the complex better than our advisor and friend, Ronni Stoeferle, whose most recent In Gold We Trust Report has just been released.

Co-produced with his Incrementum AG colleague, Mark Valek, this annual report has become the seminal report in the precious metal space.

The 2023 edition is replete with not only the most sobering and clear data points and contextual common sense, but also a litany of entertaining quotations from Churchill and the Austrian School to The Grateful Dead and Anchorman …

Ronni and Mark unpack the consequences of a Fed that has raised rates too high, too fast and too late, which is, again a fact plain to see:

Needless to say, hiking rates into an economic setting already historically “debt fragile” tends to break things (from USTs to regional banks) and portends far more pain ahead, as both history and math also plainly confirm:

In a debt-soaked world fully addicted to years of instant liquidity from a central bank near you, Powell’s sudden (but again too late, too much) hiking policies will not “softly” restrain market exuberance nor contain inflation without unleashing the mother of all recessions.

Instead, the subsequent and sudden negative growth of money supply will only hasten a recession as opposed to a “softish” landing:

As the foregoing report warns, the looming approach of this recession is already (and further) confirmed by such basic indicators as the Conference Board of Leading Indicators, an inverted yield curve and the alarming spread between 10Y and 2Y yields.

Self-Inflicted Geopolitical Risks

The report further examines the geopolitical shifts of which we have been warning(and writing) since March of 2022, when Western sanctions against Russia unleashed a watershed trend by the BRICS and other nations to seek settlement payments outside of the weaponized USD.

One would be unwise to ignore the significance of this shift or underestimate the growing power of these BRICS (and BRICS “plus”) alliances, as their combined share of global GDP is rising not falling…

As interest in (and trust for) the now weaponized USD as a payment system declines alongside a weakening faith in Uncle Sam’s IOUs, the world, and its central banks (especially out East) are turning away from USTs and turning toward physical gold.

Again, I give credit to the In Gold We Trust Report:

See a trend?

See why?

It’s fairly simple, and for this we can thank the fairly stupid policies of the Fed in particular and the declining faith in their prowess in general:

Myths Are Stubborn Things

Many, of course, find it hard to imagine that a Federal Reserve based in DC and within the land of the Great American dream (and world reserve currency) could be anything but wise, efficient and stabilizing, despite an embarrassingFed track record that is empirically unwise, inefficient and consistently destabilizing…

Myths are hard to break, despite the fact the myth of MMT and QE on demand has been a failed experiment and is sending the US, as well as the global, economy toward a reckoning of historical proportions.

But the messaging of “Keep calm and carry on” from Powell is calming in spirit despite the fact that it hides terrifying math and historically confirmed consequences for the fiat money by which investors still wrongly measure their wealth.

But as Brian Fantana of Anchorman would tell us, trust the central planners.

“They’ve done studies, you know. 60% of the time it works every time.”

As for us, we trust the kind of data Ronni and Mark have gathered and that barbarous relic of gold far more than calming words and debased, fiat currencies.

As history reminds, when currencies die within a backdrop of unsustainable debt, gold in fact does work—and every time.

end

3,Chris Powell of GATA provides to us very important physical commentaries

3 reasons why China doesn’t want yuan to replace dollar as world’s reserve currency

Submitted by admin on Mon, 2023-05-29 08:45Section: Daily Dispatches

By Huileng Tan Insider, New York Sunday, May 28, 2023

The Chinese currency is having its moment in the sun as a potential challenger to the U.S. dollar-dominated global payments system. As it looks to broaden the use of its currency internationally, China has forged deals with countries including Russia. And while the currency isn’t the only greenback challenger, it is the most high-profile contender, against the backdrop of US-China tensions and Beijing’s alliance with Russia amid the war.

However, it would be difficult for any asset or currency to unseat the U.S. dollar. As it is, even the use of the euro is a far second to the greenback.

And more importantly, Beijing wouldn’t even want the yuan to be the major reserve currency for the world, an expert on China’s economy told Insider.

Here are three reasons why even China isn’t that keen on de-dollarizing the world economy. …

Most Central banks are buying gold including broke Iraq which just bought 2.5 tonnes of gold

(Bloomberg)

Iraq boosts gold reserves by 2% in a day as it undertakes gradual buildup

Submitted by admin on Mon, 2023-05-29 08:38Section: Daily Dispatches

By Khalid Al Ansary Bloomberg News Monday, May 29, 2023

Iraq’s central bank boosted its gold reserves by about 2% in a single day last week as part of what it calls a gradual plan to stock up on the precious metal that’s seen as a traditional haven in times of economic distress.

Iraq bought 2.5 tons of bullion on Thursday to bring its reserves to 132.73 tons, Mazin Sabah, director general of the central bank’s investments department, said in an interview in Baghdad. The strategy is to acquire more gold in the second half of the year, Sabah said.

“Our plan is to buy small quantities over multiple times, not a big quantity in one go,” Sabah said.

Central banks around the world are expanding their holdings of bullion amid escalating geopolitical and economic risks. Iraq, OPEC’s second-biggest oil producer, resumed gold purchases in 2022 after a four-year hiatus, under a program to diversify its roughly $100 billion in foreign assets.

Iraq’s central bank bought 34 tons of gold last June, a one-time increase of 35% in its holdings. It stores bullion with the Bank of England and the Bank of France. …

One metric I look at fairly often for various countries is the relationship between the performance of stocks vs. bonds. The idea is straightforward enough: when stocks are outperforming bonds, it tends to be associated with a growing economy. When bonds are outperforming stocks, it is a tell that there is some sort of negative dynamic going on.

Why do I bring this up? In the US, stocks—represented by the SPY ETF—have just made a new high relative to the TLT ETF (which represents long-term US Treasury bonds). This would suggest that despite all the angst over inflation, the debt ceiling, and other issues, investors seem to taking a positive perspective.

This contrasts with China. In China, stocks have underperformed government bonds by about 50% since the beginning of 2021. This suggests there could be something rotten going on underneath the surface of the Chinese economy. Debt issues, housing issues, demographic issues, and geopolitical issues all could be weighing on sentiment toward Chinese equities and growth.

To further validate the theory that there is something rotten in China, I overlay the CNY/USD on the stock/bond chart. The CNY is weakening alongside this relationship of bonds outperforming stocks.

While last fall, the market began to discount the opening of China, now the dynamic seems to have changed. Copper did a good job signaling the upturn in Chinese GDP estimates for 2023.

With the Chinese reopening seeming to have less thrust than was anticipated, copper prices are falling again. This could telegraph a downturn in Chinese growth estimates.

end

Why? protecting commodities like Lithium and silver

The ostensible goal of the operation is to provide “support and assistance to the Special Operations of the Joint Command of the Armed Forces and National Police of Peru,” including in regions recently engulfed in violence.

Unbeknown, it seems, to most people in Peru and the US (considering the paucity of media coverage in both countries), US military personnel will soon be landing in Peru. The plenary session of Peru’s Congress last Thursday (May 18) authorised the entry of US troops onto Peruvian soil with the ostensible purpose of carrying out “cooperation activities” with Peru’s armed forces and national police. Passed with 70 votes in favour, 33 against and four abstentions, resolution 4766 stipulates that the troops are welcome to stay any time between June 1 and December 31, 2023.

The number of US soldiers involved has not been officially disclosed, at least as far as I can tell, though a recent statement by Mexico’s President Andrés Manuel Lopéz Obrador, who is currently person non grata in Peru, suggests it could be around 700. The cooperation and training activities will take place across a wide swathe of territory including Lima, Callao, Loreto, San Martín, Huánuco, Ucayali, Pasco, Junín, Huancavelica, Iquitos, Pucusana, Apurímac, Cusco and Ayacucho.

The last three regions, in the south of Peru, together with Arequipa and Puno, were the epicentre of huge political protests, strikes and road blocks from December to February after Peru’s elected President Pedro Castillo was toppled, imprisoned and replaced by his vice-president Dina Boluarte. The protesters’ demands included:

The release of Castillo

New elections

A national referendum on forming a Constitutional Assembly to replace Peru’s current constitution, which was imposed by former dictator Alberto Fujimori following his self-imposed coup of 1992

Brutal Crackdown on Protests

Needless to say, none of these demands have been met. Instead, Peru’s security forces, including 140,000 mobilised soldiers, unleashed a brutal crackdown that culminated in the deaths of approximately 70 people. A report released by international human rights organization Amnesty International in February drew the following assessment:

“Since the beginning of the massive protests in different areas of the country in December 2022, the Army and National Police of Peru (PNP) have unlawfully fired lethal weapons and used other less lethal weapons indiscriminately against the population, especially against Indigenous people and campesinos (rural farmworkers) during the repression of protests, constituting widespread attacks.”

As soon as possibly next week, an indeterminate number of US military personnel could be joining the fracas. According to the news website La Lupa, the purported goal of their visit is to provide “support and assistance to the Special Operations of the Joint Command of the Armed Forces and National Police of Peru” during two periods spanning a total of seven months: from June 1 to September 30, and from October 1 to December 30, 2023.

The secretary of the Commission for National Defence, Internal Order, Alternative Development and the Fight Against Drugs, Alfredo Azurín, was at pains to stress that there are no plans for the US to set up a military base in Peru and that the entry of US forces “will not affect national sovereignty.” Some opposition congressmen and women begged to differ, arguing that the entry of foreign forces does indeed pose a threat to national sovereignty. They also lambasted the government for passing the resolution without prior debate or consultation with the indigenous communities.

The de facto Boluarte government and Congress are treating the arrival of US troops as a perfectly routine event. And it is true that the US military has long held a presence in Peru. For example, in 2017, U.S. personnel took part in military exercises held jointly with Colombia, Peru and Brazil in the “triple borderland” of the Amazon region. Also, the US Navy operates a biosafety-level 3 biomedical research laboratory close to Lima as well as two other (biosafety-level 2) laboratories in Puerto Maldonado.

But the timing of the operation raising serious questions. After all, Peru is currently under the control of an unelected government that is heavily supported by Washington but overwhelmingly rejected by the Peruvian people. The crackdown on protests in the south of the Peru by the country’s security forces — the same security forces that US military personnel will soon be joining — has led to dozens of deaths. Peru’s Congress is refusing to call new elections in total defiance of public opinion. Just a few days ago, the country’s Supreme Court issued a ruling that some legal scholars have interpreted as essentially criminalising political protest.

As Peru’s civilian institutions fight among themselves, Peru’s armed forces — the last remaining “backbone” in the country, according to Mexican geopolitical analyst Alfredo Jalife — has taken firm control. And lest we forget, Peru is home to some of the very same minerals that the US military has identified as strategically important to US national security interests, including lithium. Also, as I noted in my June 22, 2021 piece, Is Another Military Coup Brewing in Peru, After Historic Electoral Victory for Leftist Candidate?, while Peru’s largest trading partner is China, its political institutions — like those of Colombia and Chile — remain tethered to US policy interests:

Together with Chile, it’s the only country in South America that was invited to join the Trans-Pacific Partnership, which was later renamed the Comprehensive and Progressive Agreement for Trans-Pacific Partnership after Donald Trump withdrew US participation.

Given as much, the rumours of another coup in Peru should hardly come as a surprise. Nor should the Biden administration’s recent appointment of a CIA veteran as US ambassador to Peru, as recently reported by Vijay Prashad and José Carlos Llerena Robles:

Her name is Lisa Kenna, a former adviser to former US Secretary of State Mike Pompeo, a nine-year veteran at the Central Intelligence Agency (CIA), and a US secretary of state official in Iraq. Just before the election, Ambassador Kenna released a video, in which she spoke of the close ties between the United States and Peru and of the need for a peaceful transition from one president to another.

It seems more than likely that Kenna played a direct role in the not-so-peaceful transition from President Castillo to de facto President Boluarte, having met with Peru’s then-Defence Minister Gustavo Bobbio Rosas on December 6, the day before Pedro Castillo was ousted, to tackle “issues of bilateral interest”.

On a Knife’s Edge

After decades of stumbling from crisis to crisis and government to government, Peru rests on a knife’s edge. When Castillo, a virtual nobody from an Andean backwater who had played an important role in the teachers’ strikes of 2017, rode to power on a crest of popular anger at Peru’s hyper-corrupt establishment parties in June 2021, Peru’s legions of poor and marginalised hoped that positive changes would follow. But it was not to be.

Castillo was always an outsider in Lima and was out of his depth from day one. He had zero control over Congress and failed miserably to overcome rabid right-wing opposition to his government. Even in his first year in office he faced two impeachment attempts. As Manolo De Los Santos wrote in People’s Dispatch, Peru’s largely Lima-based political and business elite could never accept that a former schoolteacher and farmer from the high Andean plains could become president.

On December 7, they finally got what they wanted: Castillo’s impeachment. Just hours before a third impeachment hearing, he declared on national television that he was dissolving Congress and launching an “exceptional emergency government” and the convening of a Constituent Assembly. It was a preemptive act of total desperation from a man who held no sway with the military or judiciary, had zero control over Congress, and had even lost the support of his own party. Hours later, he was impeached, arrested by his own security detail and taken to jail, where he remains to this day.

Castillo may be out of the picture but political instability continues to reign in Peru. The de facto Boluarte government and Congress are broadly despised by the Peruvian people. According to the latest poll by the Institute of Peruvian Studies (IEP), 78% of Peruvians disapprove of Boluarte’s presidency while only 15% approve. Congress is even less popular, with a public disapproval rate of 91%. Forty-one percent believe that the protests will increase while 26% believe they will remain the same. In the meantime, Peru’s Congress continues to block general elections.

Peru’s “Strategic” Resources

As regular readers know, EU and US interest in Latin America is rising rapidly as the race for lithium, copper, cobalt and other elements essential for the so-called “clean” energy transition heats up. It is a race that China has been winning pretty handily up until now.

Peru is not only one of China’s biggest trade partners in Latin America; it is home to the only port in Latin America that is managed entirely by Chinese capital. And while Peru may not form part of the Lithium Triangle (Bolivia, Argentina and Chile), it does boast significant deposits of the white metal. By one estimate, it is home to the sixth largest deposits of hard-rock lithium in the world. It is also the world’s second largest producer of copper, zinc and silver, three metals that are also expected to play a major role in supporting renewable energy technologies.

In other words, there is a huge amount at stake in how Peru evolves politically as well as the economic and geopolitical alliances it forms. Also, its direct neighbour to the north, Ecuador, is undergoing a major political crisis that is likely to spell the end of the US-aligned Guillermo Lasso government and a handover of power to Rafael Correa’s party and its allies.

And the US government and military have made no secret of their interest in the mineral deposits that countries like Peru hold in their subsoil. In an address to the Washington-based Atlantic Council on Jan 19, Gen. Laura Richardson, head of the U.S. Southern Command, spoke gushingly of Latin America’s rich deposits of “rare earth elements,” “the lithium triangle — Argentina, Bolivia, Chile,” the “largest oil reserves [and] light, sweet crude discovered off Guyana,” Venezuela’s “oil, copper, gold” and the fact that Latin America is home to “31% of the world’s fresh water in this region.”

She also detailed how Washington, together with US Southern Command, is actively negotiating the sale of lithium in the lithium triangle to US companies through its web of embassies, with the goal of “box[ing] out” US adversaries (i.e. China and Russia), concluding with the ominous words: “This region matters. It has a lot to do with national security. And we need to step up our game.”

Which begs the question: is this the first step of the US government and military’s stepping-up-the-game process?

The former president of Bolivia Evo Morales, who knows a thing or two about US interventions in the region, having been on the sharp end of a US-backed right-wing coup in 2019, certainly seems to think so. A few days ago, he tweeted the following message:

The Peruvian Congress’ authorisation for the entry and stationing of US troops for 7 months confirms that Peru is governed from Washington, under the tutelage of the Southern Command.

The Peruvian people are subject to powerful foreign interests mediated by illegitimate powers lacking popular representation.

The greatest challenge for working people and indigenous peoples is to recover their self-determination, their sovereignty and their natural resources.

With this authorization from the Peruvian right, we warn that the criminalization of protest and the occupation of US military forces will consolidate a repressive state that will affect sovereignty and regional peace in Latin America.

Mexico’s President Andrés Manuel Lopéz Obrador, who refuses to acknowledge Boluarte (whom he calls the “great usurper”) as Peru’s president and has recently faced threats of direct US military intervention in Mexico’s drug wars from US Republican lawmakers, had a message for the US government this week: “[Sending soldiers to Peru] merely maintains an interventionist policy that does not help at all in building fraternal bonds among the peoples of the American continent.”

Unfortunately, the US government does not seem interested, if indeed it ever has been, in building fraternal bonds with the peoples of the American continent. Instead, it is set on upgrading the Monroe Doctrine for the 21st century. Its strategic rivals this time around are not Western European nations, which are now little more than US vassals (as a recent paper by the European Council of Foreign Relations, titled “The Art of Vassalisation”, all but admitted), but rather China and Russia.

END

5 B GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.0808

OFFSHORE YUAN: 7.0904

SHANGHAI CLOSED UP 2.77 PTS OR 0.09%

HANG SENG CLOSED UP 44.67 PTS OR .24%

2. Nikkei closed DOWN 94.67 PTS OR 0.24%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 104.01 EURO RISES TO 1.0739 UP 32 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.412 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 139.75 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN// OFF- SHORE:DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.3705***/Italian 10 Yr bond yield FALLS to 4.192*** /SPAIN 10 YR BOND YIELD FALLS TO 3.421…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 3.81

3j Gold at $1960.50 silver at: 23.30 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 7 /100 roubles/dollar; ROUBLE AT 80.76//

3m oil into the 71 dollar handle for WTI and 75 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 139.75 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .412% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9019 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9690 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.722 DOWN 9 BASIS PTS…

USA 30 YR BOND YIELD: 3.892 DOWN 9 BASIS PTS/

USA 2 YR BOND YIELD: 4.525 DOWN 6 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 20.394…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.3465 UP 2 BASIS PTS (RATES RISING RAPIDLY)

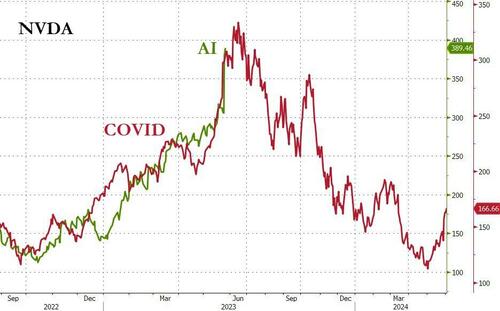

US stock futures levitated on Tuesday as euphoria over AI fueled a rally in chipmakers and tech stocks, while hopes that Congress will pass a debt accord to head off a default boosted risk sentiment, and sent the dollar and yields lower even as many warned that prospects of the debt ceiling deal – which we explained does not even cut real spending for one year – getting the necessary votes in Congress are “not that great right now.” Contracts on the S&P 500 rose 0.6%, hitting a YTD high of 4238, while the Nasdaq was up 1.1%. Treasuries are continuing to rebound, with yields falling the most in the middle of the curve, as traders anticipate a deal over the debt ceiling. A measure of the dollar is weakening slightly, erasing earlier gains. Oil prices are dropping today while gold and bitcoin advance.

In premarket trading, Nvidia’s market value topped $1 trillion as it climbed more than 3% after CEO Jensen Huang unveiled several AI-related products and services. Other AI-related stocks also gained, including Advanced Micro Devices, Intel, Qualcomm and Meta Platforms; C3.ai rose +7%, while SoundHound AI bounce +5.9%.

Stocks linked to cryptocurrencies also rallied in premarket trading after Bitcoin climbed amid a boost to investor sentiment from a provisional deal on raising the US debt limit. Bit Digital +12%; Riot Platforms +6%. here are some other notable premarket movers:

Shares connected to the Chinese education sector jump after Chinese President Xi Jinping called on top officials to boost a “high- quality” education system that strengthens China’s development. New Oriental Education gains 2.7% in US premarket trading and peer TAL Education +2.6%.

Ford shares rise 2.7% in US premarket trading as it is raised to buy from hold at Jefferies with the broker confident that the US carmaker can address a “deficit of execution” that has weighed on the shares in recent years.

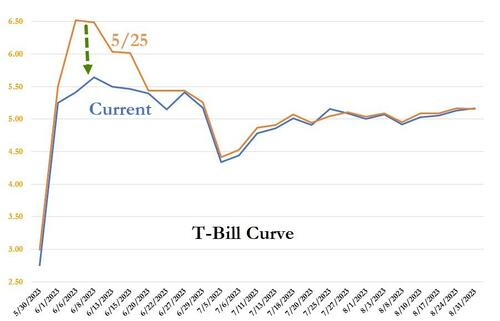

Meanwhile, Treasury yields dropped across the curve as White House and Republican congressional leaders stepped up lobbying in support of a debt-ceiling deal. Yields on short-dated bills – the most at risk of a default extended declines from recent highs. A gauge of the dollar declined for a third day.

The clock is ticking as backers of the agreement have only a week to get it through Congress before a possible June 5 default – the so-called X Day. President Joe Biden has been personally calling lawmakers to support the bill, with a vote by the House likely Wednesday, before it goes to the Senate.

“Maybe the rally has a bit further to go but it’s more buy-on-rumor, sell-on-the-news,” said Cesar Perez Ruiz, chief investment officer of Pictet Wealth Management. “As from now, we will go back to looking at economy, inflation, plus the drain of liquidity as the Treasury General Account will need to be refilled.”

European stocks fluctuated, with the Stoxx 600 gaining 0.1%; technology, utilities and real estate are the best performing sectors. Nestle SA and Unilever Plc fell after both announced the appointment of new chief financial officers, underscoring a changing of the guard at consumer-goods companies as inflation pressures the industry. Euro-area government bonds got a boost from data showing inflation in Spain slowed more than expected in May.

Meanwhile, investors remain deeply pessimistic about China against a backdrop of disappointing economic data. The Hang Seng China Enterprises Index neared a bear market and the offshore yuan weakened past 7.1 per dollar for the first time since November. Oil declined amid concern about faltering demand. Other Asian markets were mixed and choppy:

ASX 200 was lacklustre amid losses in real estate and financials, while weak Building Approvals added to the glum mood.

Nikkei 225 was choppy but remained above the 31,000 level after BoJ Governor Ueda reiterated a dovish message.

India stocks gained for a fourth straight day, inching closer to their record high levels amid continued purchases from foreign investors. The S&P BSE Sensex rose 0.2% to 62,969.13 in Mumbai, while the NSE Nifty 50 Index advanced 0.2% to 18,633.85. The MSCI Asia Pacific index closed 0.2% higher after initially falling as much as 0.4%. Gains in shares of lenders and some technology firms also boosted the benchmark.

In FX, the Bloomberg Dollar Spot Index is down 0.1%. The Japanese yen has been choppy as investors react to headlines related to a meeting of finance officials while the pound has emerged as the best performer among the G-10’s. The Turkish lira and South African Rand led declines in emerging market currencies on Tuesday while Nigeria’s dollar bonds rallied after President Bola Tinubu’s new road map on economic reforms.

Lira dropped as much as 1.5% to 20.4254, extending its decline to a sixth day. Investors are awaiting President Recep Tayyip Erdogan’s announcement of a new cabinet, which is expected at the end of the week. Ahead of that, Erdogan met Mehmet Simsek, a market-friendly former finance minister, in the capital Ankara on Monday. With wagers for a return toward more orthodox policy on the rise, Turkey’s banking stocks rose as much as 9.6%.

The rand weakened as much as 1% to an all-time low of 19.8672. The currency is the worst performer Tuesday among its EM peers after the lira. Local bonds are also under pressure on Tuesday as markets digest news that attendees at the BRICs summit will have immunity from arrest; That may fan tension over South Africa’s stance toward Russia

In rates, cash treasuries rose on return from a long holiday weekend, with cash yields richer by 5bp to 7bp across the curve vs Friday’s close; US 10-year yields around 3.70%, richer by ~10bp vs Friday’s close amid hopes that debt ceiling turmoil has been resolved; belly of the curve outperforms slightly, dropping 2s5s30s fly by 3bp on the day; Germany and UK 10-year sectors lag by 3bp and 7.5bp vs Treasuries; bund futures rally after data showed Spanish inflation slowed more than expected in May. German 10-year yields are down 4bps while US 10-year borrowing costs drop 7bps.

In commodities, crude futures decline with WTI falling 1.8% to trade near $71.30. Spot gold is up 0.2% around $1,947. Bitcoin rises 0.6%.

Bitcoin is supported but remains capped by the USD 28k mark and has been in comparably narrow ranges vs broader market action.