by harveyorgan · in Uncategorized · Leave a comment·Edit

by harveyorgan · in Uncategorized · Leave a comment·Editi

GOLD PRICE CLOSED: UP $5.70 TO $1963.70

SILVER PRICE CLOSED: UP $0.37 AT $23.51

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1959.20

Silver ACCESS CLOSE: 23.19

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

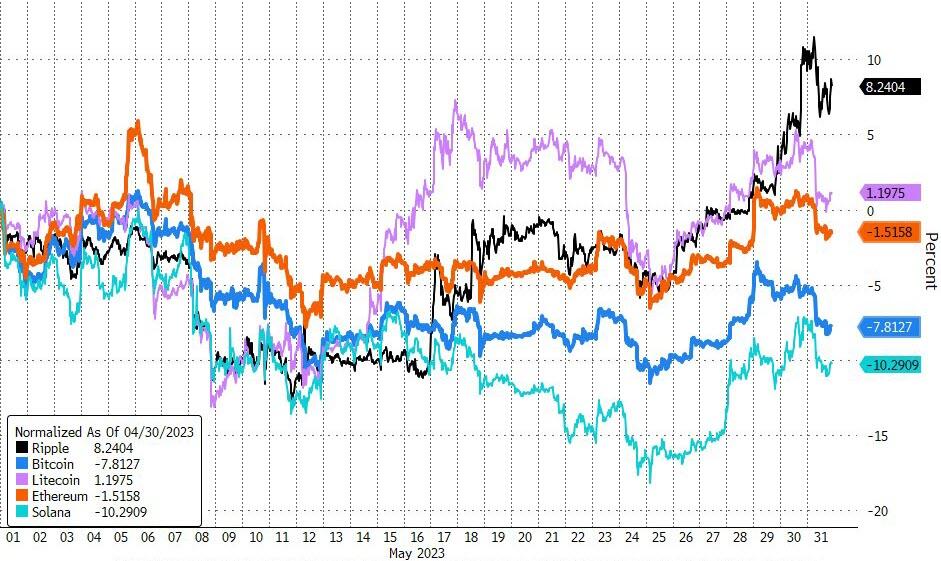

Bitcoin morning price:, $27,112 DOWN 726 Dollars

Bitcoin: afternoon price: $27,073 DOWN 7656 dollars

Platinum price closing $1001.10 DOWN $19.85

Palladium price; $1370/45 DOWN $35.15

“Our system is so stinkin’ corrupt that we owe Sodom and Gomorrah an apology.” … Trader Dan Norcini in 2009

GO GATA!

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,665,00 UP 1.50 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1577,85 DOWN 1.0 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1835,80 UP 10.30 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JUNE 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,958.000000000 USD

INTENT DATE: 05/30/2023 DELIVERY DATE: 06/01/2023

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 599

104 C MIZUHO 910

132 C SG AMERICAS 161

167 C MAREX 6

190 H BMO CAPITAL 1280

323 C HSBC 150

323 H HSBC 1651

332 H STANDARD CHARTE 2462

357 C WEDBUSH 5

363 H WELLS FARGO SEC 118

435 H SCOTIA CAPITAL 981

657 C MORGAN STANLEY 3643

661 C JP MORGAN 3529

661 H JP MORGAN 243

685 C RJ OBRIEN 11

686 C STONEX FINANCIA 76 23

690 C ABN AMRO 88

709 C BARCLAYS 56

732 H RBC CAP MARKETS 350

737 C ADVANTAGE 2 130

880 C CITIGROUP 1

880 H CITIGROUP 1535

905 C ADM 1 37

TOTAL: 9,024 9,024

MONTH TO DATE: 9,024

JPMorgan stopped 3772/9024 contracts

FOR JUNE:

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2023. CONTRACT: 9024 NOTICES FOR 902,400 OZ or 28.068 TONNES

total notices so far: 9024 contracts for 902,400 oz (28.068 tonnes)

FOR JUNE:

SILVER NOTICES: 24 NOTICE(S) FILED FOR 120,000 OZ/

total number of notices filed so far this month : 24 for 120,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP UP $5.70

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:////A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD/

INVENTORY RESTS AT 939.56 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 37 CENTS AT THE SLV//

SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 367,000 OZ FROM THE SLV ///: ; : INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 467.933 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1533 CONTRACTS TO 133,619 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR TINY $0.09 FALL IN SILVER PRICING AT THE COMEX ON TUESDAY. TAS ISSUANCE WAS A HUGE SIZED 984 CONTRACTS. THESE WILL BE USED FOR MANIPULATION NEXT MONTH OR TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY: A HUGE 984 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS) IF A CALENDAR SPREAD OCCURS.THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE.IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED THE COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.09). AND WERE SUCCESSFUL IN KNOCKING SOME SPEC LONGS AS WE HAD A HUGE LOSS ON OUR TWO EXCHANGES OF 1359 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 0 MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION. IT LOOKS LIKE IN THIS FINAL WEEK IN THE DELIVERY CYCLE MORE MANIPULATION IN OUR PRECIOUS METALS DUE TO COMEX SPREADERS LIQUIDATION OCCURRED ACCOMPANYING OPTIONS EXPIRY ON BOTH THE COMEX AND LONDON’S LBMA ALONG WITH AN ADDED FEATURE OF TAS LIQUIDATION.

WE MUST HAVE HAD:

A FAIR SIZED ISSUANCE OF EXCHANGE FOR PHYSICALS( 174 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.935 MILLION OZ(FIRST DAY NOTICE) TOTAL FOR THE MONTH 3.935 MILLION OZ ) // HUGE SIZED COMEX OI LOSS/ SMALL SIZED EFP ISSUANCE/VI) HUGE NUMBER OF T.A.S. CONTRACT INITIATION (984 CONTRACTS)//SOME T.A.S LIQUIDATION MANIPULATING THE PRICE SOUTHBOUND TUESDAY.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -removed 107 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTRACTS for 22 days, total 13,224 contracts: OR 66.120 MILLION OZ . (601 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 66.120 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1533 CONTRACTS DESPITE OUR TINY FALL IN PRICE OF $0.09 IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 174 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.935 MILLION OZ//// .. WE HAVE A HUGE SIZED LOSS OF 1359 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE 984//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED TUESDAY. THE NEW TAS ISSUANCE WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE.

WE HAD 24 NOTICE(S) FILED TODAY FOR 120,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 3,833 CONTRACTS TO 449,515 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED – 492 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 3833 CONTRACTS) DESPITE OUR $14.05 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JUNE. AT 70.79 TONNES ON FIRST DAY NOTICE // + /A SMALLER ISSUANCE OF 863 T.A.S. CONTRACTS/ZERO FRONT END OF TAS LIQUIDATION TUESDAY ////YET ALL OF..THIS HAPPENED WITH A $14.05 GAIN IN PRICE WITH RESPECT TO TUESDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 873 OI CONTRACTS (2.715 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4706 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 450,007

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 873 CONTRACTS WITH 3,833 CONTRACTS DECREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): 863 CONTRACTS) AND 4706 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 873 CONTRACTS OR 2.715 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4706 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (3833) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 873 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 70.79 TONNES /3) ZERO LONG LIQUIDATION//4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: SMALLER T.A.S. ISSUANCE: 863 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 76,091 CONTRACTS OR 7,609,100 OZ OR 236.67 TONNES IN 22 TRADING DAY(S) AND THUS AVERAGING: 3399 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 22 TRADING DAY(S) IN TONNES 236.67 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 236.67/3550 x 100% TONNES 6.67% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 1533 CONTRACTS OI TO 133,619 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 174 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 174 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 174 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1533 CONTRACTS AND ADD TO THE 174 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1359 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 6.300 MILLION OZ

OCCURRED DESPITE OUR TINY $0.09 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED DOWN 19.65 PTS OR 0.61% //Hang Seng CLOSED DOWN 361.51 PTS OR 1.94% /The Nikkei closed DOWN 440.28 OR 1.41% //Australia’s all ordinaries CLOSED DOWN 1.54 % /Chinese yuan (ONSHORE) closed DOWN 7.1042 /OFFSHORE CHINESE YUAN DOWN TO 7.1235 /Oil DOWN TO 67.64 dollars per barrel for WTI and BRENT AT 71.97 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 3341 CONTRACTS DOWN TO 450,007 DESPITE OUR GAIN IN PRICE OF $14.05 ON TUESDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF MAY… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4706 EFP CONTRACTS WERE ISSUED: : JUNE 4706 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4706 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 1,365 CONTRACTS IN THAT 4706 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 3341 COMEX CONTRACTS..AND THIS SMALL SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR STRONG GAIN IN PRICE OF $14.05. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE TODAY WAS A LITTLE SMALLER AT 863 CONTRACTS. DURING LAST WEEK THEY SOLD THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (70.790) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 70.790 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $14.05) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR SMALL SIZED GAIN OF 873 CONTRACTS ON OUR TWO EXCHANGES. WE HAD ZERO TAS LIQUIDATION. . THE TAS ISSUED TUESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 4.245 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE. (70.790 TONNES) // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $14.05

WE HAD – REMOVED 492 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1,365 CONTRACTS OR 136,500 OZ OR 4.245 TONNES.

Estimated gold comex today 201,854// fair

final gold volumes/yesterday 311,144// good

//MAY 31/ FOR THE JUNE 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil . nil |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 5632.723 oz Delaware |

| No of oz served (contracts) today | 9024 notice(s) 902,400 OZ 28.068 TONNES |

| No of oz to be served (notices) | 13,734 contracts 1,373,400 oz 42.721 TONNES |

| Total monthly oz gold served (contracts) so far this month | 9024 notices 902,400 OZ 28.068 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

No dealer withdrawals

Customer deposits: 1

i) Into Delaware 5623.723 oz

total deposits: 5623.723 oz

Withdrawals: nil

Adjustments; one Brinks

dealer to customer 366,717.031 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 22,758 contracts having LOST 14,658 contracts.

Thus by definition, the initial amount of gold standing for delivery in this very active delivery month of June is as follows:

22,758 notices x 100 oz per notice

equals: 2,275,800 oz or 70.790 tonnes which is close to what I predicted would stand.

July gained 41 contracts to stand at 2891 contracts.

AUGUST gained 10,495 contracts UP to 366,320 contracts

We had 9024 contracts filed for today representing 902,400oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 9024 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 3772 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2023. contract month,

we take the total number of notices filed so far for the month (9024 x 100 oz ), to which we add the difference between the open interest for the front month of JUNE (22,758 CONTRACT) minus the number of notices served upon today 9024 x 100 oz per contract equals 2,275,800 OZ OR 70.790 TONNES the number of TONNES standing in this NON- active month of May.

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (9024 x 100 oz) x 22759 OI for the front month minus the number of notices served upon today (9024)x 100 oz} which equals 2,275,800 oz standing OR 70.790 TONNES

TOTAL COMEX GOLD STANDING: 70.79 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,704,729.632 OZ 53.02 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,870,917.752 OZ

TOTAL REGISTERED GOLD: 11,640,675.492 (362.07 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 11,230,242.260 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,525,513 OZ (REG GOLD- PLEDGED GOLD) 296.283 tonnes//

END

SILVER/COMEX

MAY 31//2023// THE JUNE 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 122,464.431 oz Manfra Loomis . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 519,881.100 oz Delaware JPM |

| No of oz served today (contracts) | 24 CONTRACT(S) (120,000 OZ) |

| No of oz to be served (notices) | 763 contracts (3,815,000 oz) |

| Total monthly oz silver served (contracts) | 24 Contracts (120,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposits

total dealer deposit: nil oz

total dealer deposits: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We had 2 customer deposits

i) Into Delaware: 5010.700 oz

ii) Into Loomis: 514,870.400 oz

Total deposits: 519,881.100 oz

JPMorgan has a total silver weight: 141.828 million oz/274.068 million =51.82% of comex .//dropping fast

Comex withdrawals 2

i) Out of Manfra 43,108.720 oz

iii) Out of Loomis: 80,108.720 oz

total withdrawals: 122,464.430 oz

adjustments: 4 all dealer to customer

i) CNT 533,338.970 oz

ii) HSBC 187,085.519 oz

iii) JPMorgan: 735,788.600 oz

iv)Manfra: 243,195.150 oz

total adjustment out of the dealer: 1.719 million oz

TOTAL REGISTERED SILVER: 28.161 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 274.068 million oz

DEALER SILVER DROPPING FAST.

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE /2023 OI: 787 CONTRACTS HAVING LOST 255 CONTRACT(S).

THUS BY DEFINITION, THE INITIAL AMOUNT OF SILVER STANDING FOR DELIVERY IN JUNE IS AS FOLLOWS:

787 NOTICES X 5000 OZ PER NOTICE EQUALS:

3,935,000 OZ

JULY HAD A 2691 CONTRACT LOSS TO 102,186 CONTRACTS

SEPT HAS A GAIN OF 1479 CONTRACTS UP TO 20,683

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 24 for 120,000 oz

Comex volumes// est. volume today 78,180 excellent/

Comex volume: confirmed yesterday: 84,191 EXCELLENT

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 24 x 5,000 oz = 120,000 oz

to which we add the difference between the open interest for the front month of JUNE(787) and the number of notices served upon today 24 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2023 contract month: 24 (notices served so far) x 5000 oz + OI for the front month of JUNE (787) – number of notices served upon today (24 )x 500 oz of silver standing for the JUNE contract month equates to 3.935 million oz +

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MAY 31/WITH GOLD UP $5.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 939.56 TONNES

MAY 30/WITH GOLD UP $14.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 26/WITH GOLD UP $.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 941.29 TONNES

MAY 25/WITH GOLD DOWN $19.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 24/WITH GOLD DOWN $9.50 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 941.29 TONNES

MAY 23/WITH GOLD $2.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 942.74 TONNES

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

MAY 9/WITH GOLD UP $9.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTER DEPOSIT OF 5.88 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 937.64 TONNES

MAY 8/WITH GOLD UP $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 931.77 TONNES

MAY 5/WITH GOLD DOWN $30.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AS DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

MAY 4/WITH GOLD UP $19.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.30 TONNES

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

GLD INVENTORY: 939.56 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 31/WITH SILVER UP 37 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 367,000 OZ FROM THE SLV////INVENTORY RESTS AT 467.933 MILLION OZ//

MAY 30/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 26/WITH SILVER UP $0.44 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.306 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 25.WITH SILVER DOWN $0.32 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 471.606 MILLION OZ//

MAY 24/WITH SILVER DOWN $.35 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 23/WITH SILVER DOWN 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

MAY 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A TINY DEPOSIT OF .08 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 465.682 MILLION OZ//

MAY 8/WITH SILVER DOWN 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.602 MILLION OZ//

MAY 5/WITH SILVER DOWN 31 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 466.876 MILLION OZ//

MAY 4/WITH SILVER UP 53 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF .174 MILLION OZ INTO SLV.//INVENTORY RESTS AT 467.174 MILLION OZ//

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

CLOSING INVENTORY 467.933 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

Faced With New Round Of Demonetization Indians Turn To Gold

TUESDAY, MAY 30, 2023 – 07:00 PM

Authored by Michael Maharrey via SchiffGold.com,

The Indian central bank has announced another round of demonetization with a plan to withdraw 2,000-rupee notes from circulation.

The announcement led to a big jump in gold bullion sales.

The 2,000-rupee note will remain legal tender, but they will have to be deposited or exchanged for smaller denominations by Sept. 30.

The 2,000 rupee note ($24.19) is the largest currency denomination in India. According to Reuters, they make up about 10.8% of the currency in circulation.

T.V Somanathan, the top official at the Indian Finance Ministry, said confiscation of the 2,000 rupee notes wouldn’t cause any disruptions “either in normal life or in the economy.”

His assurances fall flat given history.

We’ve seen this play before. The Indian government announced a surprise demonetization policy in the fall of 2016 meant to drive so-called black money out of the shadows and declared that all of the 1,000 and 500-rupee notes then in circulation would no longer be valid. The suddenly worthless notes made up 86% of the currency in circulation in the country at the time. The move made virtually all of the cash in India valueless.

The government produced new 500 and 2,000-rupee notes to replace the old currency.

Now the government is pulling those 2,000-rupee notes out of circulation.

The government policy announced in 2016 was meant to force Indians to trade in the old notes for new ones. But there was a catch. The government placed limits on the amount of currency Indians could exchange, but no limits on bank deposits until the end of the year. The idea was to push Indians into putting their hoarded cash in the bank – thus bringing it “out of the shadows.” The demonetization policy resulted in severe cash shortages. As many as 90% of ATMs in some regions of the country completely ran out of currency.

With more time to exchange notes this time around, the latest round of demonetization is not expected to be as disruptive.

War on Cash

The Indian government’s move was part of the broader war on cash. The goal was to bring “black money” out of the shadows so it can be tracked and taxed. The vast majority of transactions in India are in cash. It is an overwhelmingly cash economy and virtually every Indian has currency stashed away in their home.

Transactions using black money mean no taxes are collected. Government estimates show that only 1% of the Indian population pays any taxes at all. By making the 1,000 and 500 rupee notes valueless, government officials hoped to force the black money into the light so they could get their cut.

Reserve Bank of India (RBI) justified eliminating the 2,000-rupee note, saying they are at the end of their useful life and citing evidence showing 2,000 rupee notes aren’t typically used in transactions. But the real motivation for this latest round of demonetization is likely the same as the first – to better track and tax transactions.

This war on cash isn’t isolated to India. The European Central Bank stopped producing and issuing 500-euro notes in 2018, and officials in the US have floated the idea of eliminating the $100 bill.

More recently, governments have experimented with central bank digital currency (CBDC) as a cash replacement.

There are also political motives for getting the 2,000-rupee notes out of circulation now.

The move comes ahead of elections in four Indian states and a national election next spring. According to Reuters, “Most of India’s political parties are believed to hoard cash in high denomination bills to fund election campaign expenses to get around tough spending limits imposed by the Election Commission.”

Forcing people to deposit the notes will also help boost bank deposits. Indian banks have struggled to maintain deposit levels large enough to support the country’s massive credit expansion.

Gold to the Rescue

When the government pulled 1,000 and 500-rupee notes out of circulation in 2016, Indians turned their “black money” into gold.

Tax officials attempting to track black money say gold jewelry sales spiked the night of Nov. 8, 2016, after the government announced the demonetization policy.

“Jewelers offered a platform to convert unreported cash into gold,” one official said.

To avoid reporting the transactions, sellers simply split single transactions into multiple sales in order to keep them below the Rs 2 lakh threshold that triggers reporting requirements in India.

After the RBI announced the elimination of 2,000-rupee notes earlier this month, local newspapers reported a similar rush to jewelry shops to exchange the notes for gold. The Hindustan Times reported a 10 to 20% increase in gold sales after the announcement.

People scrambled to buy gold and silver in bulk in bullion markets, leading to increase in prices, dealers in several states said.”

Gold was also a lifeline for Indians pummeled by the economic storm caused by the government response to the coronavirus pandemic.

Indians understand that gold tends to store value and that in the end gold is money. If they have gold, they know they will be able to get the goods and services they need – even in the event of an economic meltdown or a cash crunch.

Gold is not just a luxury in India. Even poor people buy gold in the Asian nation. According to an ICE 360 survey in 2018, one in every two households in India purchased gold within the last five years. Overall, 87% of households in the country own some amount of the yellow metal. Even households at the lowest income levels in India own some gold. According to the survey, more than 75% of families in the bottom 10% had managed to buy gold.

It’s no surprise that when faced with the possibility of another disruption to the cash system, Indians have turned to gold.

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

3,Chris Powell of GATA provides to us very important physical commentaries

4, OTHER IMPORTANT GOLD COMMENTARIES/VIDEOS

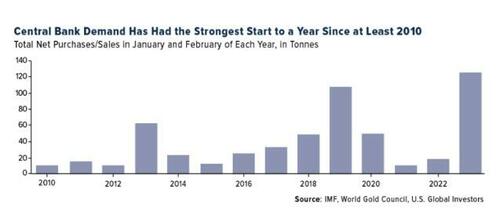

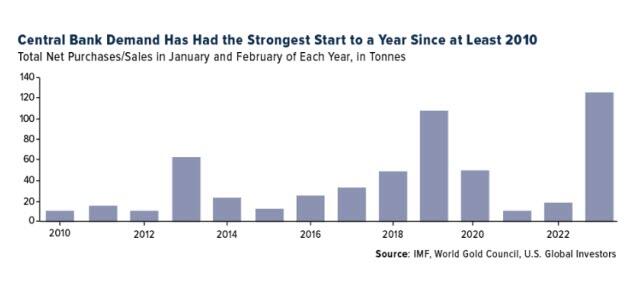

Mish Shedlock on Central banks are buying gold at record pace

(Mish Shedlock)

Central Banks Are Buying Gold At Record Pace, What Does That Mean For Inflation?

WEDNESDAY, MAY 31, 2023 – 07:20 AM

Authored by Mike Shedlock via MishTalk.com,

A reader wanted to know if central bank buying gold at a record pace adds to inflation. Let’s crunch the numbers then look at the true meaning of the buying spree…

Warren B. Mosler noted central bank are buying gold at a record pace and that adds to global inflation.

A second reader asked if I agreed.

Inflation Meaning

Q. What does central bank buying of gold mean for inflation?

A: Not much, per se, especially in the amount of purchases.

The Math

A metric ton of gold is 2204.62 pounds. There are 14.5833 troy ounces to a pound. That means there are 32,150.7 troy ounces per metric ton.

As of 11:45 PM on 2023-05-29, gold is $1952 per troy ounce.

One metric ton is worth 2022.62 * 14.5833 * $1952 per ounce = $62,701,106. Multiply that by 120 tons (lead chart) and you get $7,524,132,720.

With monstrous US deficits, and US debt approaching $32 trillion, $7.5 billion is not enough to matter in and of itself.

Stagflation Right Now, But What’s Ahead?

On April 28, I noted forces for inflation and deflation.

For discussion, please see Worst of Both Worlds, Stagflation Right Now, But What’s Ahead?

Understanding the Real Point

Buying gold has no direct impact on inflation. However, it’s important to note that the record pace is a result of US measures to weaponize the dollar.

Weaponizing the US dollar refers to actions by the US to confiscate Russia’s dollar reserves in response to the war in Ukraine.

Regardless of how one feels about the war or Putin, this was an unprecedented and illegal action by the US.

No Man’s Land

Weaponization of the US dollar will matter at some point, but it is difficult to say when because dollar avoidance itself is very difficult (see the first of two links below).

Weaponizing the Dollar

- March 18, 2022: What Does China Do With a Dollar That’s No Longer Risk Free? Buy Gold?

- May 13, 2023: Dollar Weaponization Expands – FDIC Message to Foreign Depositors Is Don’t Trust the US

The second point pertains to US actions regarding failed US banks in 2023 that further weaponized the dollar.

Weaponizing the dollar is a serious mistake, and it’s a Rubicon that cannot be undone.

So far, however, we are witnessing symbolic actions that eventually spell a currency crisis, but we are all guessing when that is.

* * *

Like these reports? I hope so, and if you do, please Subscribe to MishTalk Email Alerts.

END

5.IMPORTANT COMMENTARIES ON COMMODITIES:

END

5 B GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.1082

OFFSHORE YUAN: 7.1235

SHANGHAI CLOSED DOWN 19.65 PTS OR 0.61%

HANG SENG CLOSED DOWN 361.51 PTS OR 1.94%

2. Nikkei closed DOWN 440.28 PTS OR 1.41%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 104.47 EURO FALLS TO 1.0681 DOWN 51 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.430 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 139.86 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN// OFF- SHORE:DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.2595***/Italian 10 Yr bond yield FALLS to 4.071*** /SPAIN 10 YR BOND YIELD FALLS TO 3.306…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 3.72

3j Gold at $1961.50 silver at: 23.32 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 1 /100 roubles/dollar; ROUBLE AT 81.13//

3m oil into the 67 dollar handle for WTI and 71 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 139.86 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .412% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9100 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9721 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.654 DOWN 5 BASIS PTS…

USA 30 YR BOND YIELD: 3.852 DOWN 6 BASIS PTS/

USA 2 YR BOND YIELD: 4.423 DOWN 6 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 20.71…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.218 DOWN 3 BASIS PTS (RATES RISING RAPIDLY)

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Slump On Dismal Chinese PMIs, Rates Slide As European Inflation Stalls

WEDNESDAY, MAY 31, 2023 – 08:09 AM

US equity futures are lower and flirting with 4,200 after another round of very ugly economic data out of China (where both mfg and service PMI missed) which dragged Asian markets lower (the HSEI entered a bear market) and slammed European stocks, while traders closely watched the debt ceiling situation after late last night the House Rule Committee advanced the bill which will now be submitted to a full vote in the House later today. That vote may not come until after market hours (~7pm) so headline risk remains.

At 7:30am ET, S&P futures were down 0.4% at 4,200 while Nasdaq futures dropped 0.2% as NVDA dipped back under $400 and exited the trillion dollar market cap club just as fast as it entered. Treasury yields slumped, dropping to 3.64%, down about 4bps, led by European rates as inflation came in weaker than expected in France and German states, prompting traders to trim bets on the path of future ECB rate hikes. The Bloomberg dollar index gained for the first time in four days whie oil extended losses with WTI crude oil futures dropping more than 2.5% after Tuesday’s 4.4% drop; bitcoin got hammered in overnight trading as usual.

In premarket trading, Nvidia dropped back below $400 and is no longer in the $1TN market cap club after soaring 31% over the past three sessions on optimism surrounding artificial intelligence, a trend that contributed to a blowout revenue forecast for the chipmaker last week. Cryptocurrency-exposed stocks also fell in US premarket trading Wednesday as Bitcoin snapped its longest streak since March. The largest cryptocurrency slid along with US equity futures as China’s economic woes reverberated beyond the country’s domestic markets. Here are some other notable premarket movers:

- HP Inc shares drop as much as 4.9% in US premarket trading on Wednesday, after the computer hardware firm reported lower-than- expected second-quarter revenue, highlighting the weakness in PC demand. However, the report suggests that the PC market may have bottomed, Bloomberg Intelligence writes.

- Hewlett Packard Enterprise shares fall as much as 8.4% in premarket trading on Wednesday, after second-quarter revenue and the current-quarter forecast from the information technology services company missed expectations. Analysts note that weakness in the company’s server business offset momentum at its Intelligent Edge unit.

- Ambarella shares drop 18% in US premarket trading after sales guidance from the maker of semiconductor devices fell short of expectations, prompting a downgrade from KeyBanc.

- Avis Budget rises 3.2% in premarket trading after Deutsche Bank upgrades the car rental firm to buy from hold, with its call “primarily valuation- centric.”.

- Chevron Corp. has no sell ratings left after JPMorgan Chase & Co. upgraded the US oil major, saying it is well positioned for a potential downturn.

- LL Flooring Holdings shares surge as much as 25% in premarket trading after founder Tom Sullivan makes another attempt to buy the home-improvement retailer.

- Twilio shares advance as much as 5.1% in premarket trading after The Information reported that activist investor Legion Partners had met with the communication software company’s board of directors and managers to suggest changes to the board.

- Faraday Future shares rise 6% in premarket trading on Wednesday, after the electric-vehicle maker launches an “AI-powered” variant of its FF 91 EV.

- Box’s fiscal 1Q results were solid, the margin outlook continues to improve and opportunities around AI are starting to come into focus for the software firm, analysts said. This is partially offset by a tougher macro picture, which appears to have got incrementally worse over the course of the quarter, they said. Box shares rose 3.4% in after-hours trading.

- Sportsman’s Warehouse dropped 7.8% in extended trading after the sporting-goods retailer’s projections for fiscal second-quarter net sales and adjusted EPS fell short of the average analyst estimates at the midpoint of the ranges.

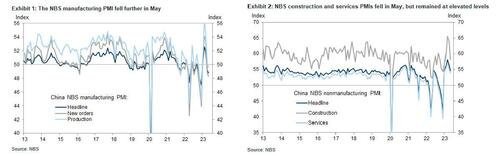

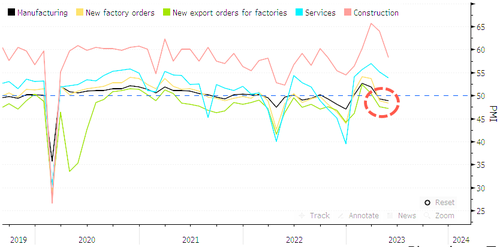

A major cause for the soggy trading sentiment overnight, was China’s NBS manufacturing PMI which fell to a lower-than-expected 48.8 in May from 49.2 in April, below expectations of 49.5, with output sub-index falling the most followed by new orders sub-index. The NBS non-manufacturing PMI moderated to 54.5 in May from 56.4 in April, and also below the 55.2 median estimate, showing ongoing recovery in both the construction and services sectors but at a slower pace. Some more details:

- The China NBS purchasing managers’ indexes (PMIs) survey suggested manufacturing activity contracted in May. The NBS manufacturing PMI headline index fell to 48.8 in May from 49.2 in April. Among five major sub-indexes, the output sub-index fell to 49.6 from 50.2, the new orders sub-index decreased to 48.3 from 48.8 and the employment sub-index declined to 48.4 from 48.8. The suppliers’ delivery times sub-index edged up to 50.5 in May from 50.3 in April, suggesting faster supplier deliveries. The NBS commented that the drop in the May PMI reading was linked to insufficient demand (especially in chemical fibers, non-metallic mineral products and ferrous metal processing industries).

- The official non-manufacturing PMI (comprised of the services and construction sectors) moderated to 54.5 in May (vs. 56.4 in April), which was still solid but lower than market expectations, suggesting continued recovery in construction and services sectors but at a slower sequential pace. The services PMI slowed to 53.8 (vs. 55.1 in April). According to the survey, the PMIs of service industries such as airlines, ship and road transport services and telecommunication were above 60 while the PMI in property sector was below 50 in May. The construction PMI moderated to 58.2 in May (vs.63.9 in April) but remained elevated. The NBS noted that construction enterprises were optimistic about the outlook of construction sector.

China’s soft manufacturing data added to concerns about the outlook for global economic growth at a time when central banks are still in tightening mode. Meanwhile, weak price data from Europe on Wednesday prompted traders to curb bets on European Central Bank rate hikes, though worries remain about the region’s prospects as demand from its largest trading partner falters. Hawkish comments from Federal Reserve officials added mix of factors traders have to consider.

“We’re facing quite a lot of headwinds: firstly, the China growth story, clearly that’s been a major disappointment. On top of that, there’s a risk of a US recession, and for the euro region, there’s a likelihood that they’re facing stagnation,” Jane Foley, head of FX strategy at Rabobank, said on Bloomberg TV. “So you’ve got a pretty disappointing outlook for growth, not an environment where you really want to be piling en masse into high-risk assets, and therefore the dollar is likely to do well.” Meanwhile, Fedspeak remains hawkish with bonds pricing in a 66% chance for a hike at the June meeting.

In Europe, the Stoxx Europe 600 index headed for its lowest close since March, with China-exposed luxury-goods makers LVMH and Richemont among the biggest laggards, while Swedish landlord SBB plunged to an all-time low after its CEO said his holding company had deferred interest payments on a loan. Software and telecommunications stocks advanced, led by Capgemini SE after the Paris-based firm said it expanded a partnership with Google Cloud in data analytics and artificial intelligence. Here are some other notable European movers:

- B&M gains as much as 6.6% after the UK retailer reported FY results that met market expectations. The results are encouraging, given the current macroeconomic environment, Shore Capital said

- JD Wetherspoon shares jump as much as 6.3%, with Mitchells & Butlers up as much as 3.2%, after HSBC said the UK pub and restaurant sector still looks cheap despite a recent rally

- Huuuge gains as much as 6.1% after the Warsaw-listed mobile games developer announced a $150m share buyback priced at a premium to Tuesday’s close following a first-quarter earnings beat

- LVMH shares fall drop as much as 2.3% on Wednesday, as concerns over China’s economy pummeled luxury stocks exposed to the world’s second economy, with Kering and Hermes both falling 2.7%

- Entain shares decline as much as 3.8% after the UK-based gambling company said an HMRC investigation will likely lead to a “substantial financial penalty”

- SBB shares fall as much as 11%, reaching both all-time intraday lows and on track for their worst close on record, after the embattled landlord’s CEO said his holding company has deferred interest payments

- Impax Asset Management shares sink as much as 11%, hitting the lowest since January, with analysts flagging a hit to profits from hiring by the ESG fund manager

- Heineken shares fall as much as 3% after Femsa’s offering to sell more of its shares in the Dutch brewer at a ~4% discount to Tuesday’s close

The euro slumped to a two-month through against the dollar after French inflation eased more than anticipated, reaching its lowest level in a year. Data from Germany’s states also signaled inflation may be falling more quickly than expected in the region’s biggest economy, prompting traders to trim bets on future European Central Bank interest-rate increases. European bonds rallied, with the German 10-year yield down about 9 basis points.

“There’s a fairly consistent line with the euro-area CPI numbers: it is coming down,” Paul Donovan, chief economist at UBS Global Wealth Management, said on Bloomberg TV. “This whole idea of stickiness, of inflation sticking around, is really being blown out of the water. Interestingly, we’re also getting this confirmed in the regional data in the US.”

Earlier in the session, Asian equities fell, led by shares listed in Hong Kong, as weaker-than-expected manufacturing data showed the Chinese economy continues to struggle. The MSCI Asia Pacific Index dropped as much as 1.4%, set for its biggest decline since March 14, with a gauge of Chinese stocks in Hong Kong as well as the city’s benchmark index headed for bear markets. Data Wednesday showed China’s manufacturing activity contracted for a second month in May, offering the latest proof that the post-Covid recovery is stalling. Broad weakness also pulled Korean stocks lower, after they briefly headed for a bull market amid foreign demand for the nation’s chipmakers.

“Cyclically, the recovery in China is on a much weaker footing,” Timothy Moe, chief Asia Pacific equity strategist at Goldman Sachs, told Bloomberg Television. For Korea, investors are looking past the earnings trough expected this year to a rebound in the chip sector in 2024, he said. Declines were broad-based, with gauges in Japan, Australia and Thailand also falling. An energy sub-gauge dropped the most as crude prices fell. The broader MSCI Asia gauge is down about 7% from a peak in January as China’s faltering economic recovery and worries about a recession in the US damp sentiment.

- The Hang Seng and Shanghai Comp. declined with Hong Kong dragged lower by notable weakness in the local blue-chip tech stocks and following disappointing Manufacturing and Non-Manufacturing PMI data in which the former printed at a second consecutive month in contraction territory and its weakest reading YTD.

- Japan’s Nikkei 225 was pressured by data releases in which Industrial Production printed a surprise contraction and Retail Sales missed forecasts, with early jitters also from North Korea’s failed satellite launch.

- Australia’s ASX 200 was led lower by underperformance in the commodity-related sectors with energy the worst hit after oil prices slumped by more than 4% yesterday and with the mood not helped by firmer-than-expected monthly CPI.

- Indian stocks posted their sharpest drop in two weeks on Wednesday as most Asian markets declined after China reported weaker-than-expected manufacturing data. The S&P BSE Sensex fell 0.6% to 62,622.24 as of 03:45 p.m. in Mumbai, while the NSE Nifty 50 Index declined 0.5%. The drop was their biggest decline since May 17. Reliance Industries contributed the most to the Sensex’s decline, decreasing 1.8%. Out of 30 shares in the Sensex index, 11 rose, while 19 fell.

In FX, the Bloomberg Dollar Spot Index rises 0.3% with the largest gains for the greenback seen against the Norwegian krone and kiwi. EUR/USD fell as much as 0.7% to 1.0662, the lowest since March 20, as euro-area bond yields dropped; German two- and five-year bond yields fell as much as 10 basis points before paring the move; 10-year yield is down 9bps to 2.25%.

- The Norwegian krone underperformed its Group-of-10 peers for a second day, down 0.8% versus the dollar and 0.2% against the euro

- The Australian and New Zealand dollars fell after a contraction in China’s manufacturing activity, which brought weak long stops onto the radar, according to an Asia- based FX trader

In rates, treasuries extended this week’s gains, with yields richer by ~4bp across the curve, led by bunds: the German 10-year yields are down 9bps after regional prints point to soft German CPI due at 8am New York time, while French inflation slowed more than expected. US session includes four Fed speakers and JOLTS job openings. Treasury gains are led by belly of the curve, tightening 2s5s30s fly by 1.5bp on the day after almost 6bp of tightening Tuesday; 10-year yields around 3.65% with bunds outperforming and trading 5bp richer in the sector. IG issuance slate includes Hong Kong 3Y/5Y/10Y; five deals priced $11.3b Tuesday, with final order books said to be more than four times covered. US economic data slate includes May MNI Chicago PMI (9:45am), April JOLTS job openings (10am) and May Dallas Fed services activity (10:30am)

In commodities, crude futures decline with WTI falling 1.2% to trade below $69. Spot gold is little changed around $1,958. Bitcoin drops 2.4%, sliding below $27,000.

Looking to the day ahead now, and data releases include the May CPI releases from Germany, France and Italy, along with German unemployment for May. In the US there’s also the JOLTS job openings for April, as well as the MNI Chicago PMI for May. From central banks, we’ll hear from the Fed’s Collins, Bowman, Harker and Jefferson, the ECB’s Villeroy and Visco, and the BoE’s Mann. In addition, the Fed will release their Beige Book, and the ECB will release their Financial Stability Review.

Market Snapshot

- S&P 500 futures down 0.3% to 4,203.50

- MXAP down 1.3% to 158.39

- MXAPJ down 1.3% to 501.13

- Nikkei down 1.4% to 30,887.88

- Topix down 1.3% to 2,130.63

- Hang Seng Index down 1.9% to 18,234.27

- Shanghai Composite down 0.6% to 3,204.56

- Sensex down 0.7% to 62,521.87

- Australia S&P/ASX 200 down 1.6% to 7,091.31

- Kospi down 0.3% to 2,577.12

- STOXX Europe 600 down 0.3% to 455.30

- German 10Y yield little changed at 2.26%

- Euro down 0.6% to $1.0670

- Brent Futures down 0.6% to $73.08/bbl

- Gold spot down 0.1% to $1,958.09

- U.S. Dollar Index up 0.36% to 104.54

Top Overnight News from Bloomberg

- China’s economic recovery weakened in May as manufacturing activity continued to slump, prompting investors to dump stocks and call for more stimulus measures to boost growth

- The debt- limit deal struck by President Joe Biden and Speaker Kevin McCarthy is heading toward a vote Wednesday in the House of Representatives after clearing a crucial procedural hurdle with just days remaining to avoid a US default

- French inflation eased to its lowest level in a year, though Italy overshot analyst expectations, underlining the challenge for the European Central Bank as it nears the end of its unprecedented campaign of interest-rate hikes.

- Japan’s biggest life insurers have ramped up their use of longer-dated currency hedges to a record to escape sky-high costs, suggesting they’re buying more riskier securities that benefit from protection.

A more detailed look at global markets corutesy of Newsquawk

APAC stocks were mostly lower following the mixed handover from Wall St where sentiment was clouded as hardliners voiced opposition to the debt ceiling bill, while risk appetite was subdued overnight as participants digested a slew of data releases heading into month-end including disappointing Chinese official PMIs. ASX 200 was led lower by underperformance in the commodity-related sectors with energy the worst hit after oil prices slumped by more than 4% yesterday and with the mood not helped by firmer-than-expected monthly CPI. Nikkei 225 was pressured by data releases in which Industrial Production printed a surprise contraction and Retail Sales missed forecasts, with early jitters also from North Korea’s failed satellite launch. Hang Seng and Shanghai Comp. declined with Hong Kong dragged lower by notable weakness in the local blue-chip tech stocks and following disappointing Manufacturing and Non-Manufacturing PMI data in which the former printed at a second consecutive month in contraction territory and its weakest reading YTD.

Top Asian News

- US imposed sanctions on Chinese and Mexican entities to combat the opioid crisis, according to FT.

- China’s NBS said the economic activity level in China declined slightly in May which indicates the need to strengthen the foundation for recovery and development, according to Reuters.

- Japan’s METI said the decline in semiconductors and flat panel manufacturing equipment were the main contributors pushing down Japan’s industrial output in April and noted that official business sentiment remains bearish as overseas economies continue to weaken.

- RBA Governor Lowe said they are in data-dependent mode and there is not a single variable that drives their decisions, while he added that monetary policy is in a restrictive environment and that they are on a narrow path with success not guaranteed

European bourses are mostly in the red, Euro Stoxx 50 -0.4%, following the soft APAC handover and despite the generally softer inflation data from European nations thus far. Sectors are lower across the board, with Luxury names lagging after the weak Chinese PMI figures. Stateside, futures are all in the red though only modestly so, ES -0.1%, with the NQ in-line with broader action today and NVIDIA pulling back a touch from its recent upside, -1.5% in the pre-market.

Top European News

- Netherlands Senate approved a wide-ranging reform of the Dutch pension system, according to Reuters.

- ECB’s Muller says core inflation shows no signs of slowing yet, very likely that the ECB will hike by 25bp more than once; probably too optimistic to see ECB rate cut in early 2024.

- ECB’s de Guindos says we have to adjust liquidity requirements to modern world; inflation data today and yesterday was positive; victory over inflation is not there but the trajectory is correct; markets are absorbing QT smoothly and positively.

- ECB’s Visco says longer-term inflation expectations remain in line with the definition of price stability; now that rates are in restrictive territory, must proceed with the correct degree of graduality.

- ECB Financial Stability Review: says financial stability outlook remains fragile.

- Spain’s People’s Party (PP) leader says they will reduce public debt if they win the snap election and will reduce electric bill for small consumers and certain companies.

FX

- Yuan’s post-PMI pain revives Greenback fortunes with hawkish Fed’s Mester also boosting the Buck; USD/CNY and USD/CNH top 7.1100 and 7.1300 respectively, while DXY sets new w-t-d peak at 104.630.

- Aussie retreats through 0.6500 irrespective of stronger than forecast CPI, but AUD/NZD remains elevated on RBA rate hike expectations.

- Euro undermined by mostly weaker than expected EZ inflation data, as EUR/USD eyes Fib support just above 1.0650.

- Franc hit by feeble Swiss retail sales and Pound weighed down by decline in Lloyds UK business barometer; USD/CNF above 0.9100 and Cable probing 1.2350

- Yen treading water near 140.00 amidst softer Treasury yields and debt ceiling deal jitters.

- PBoC set USD/CNY mid-point at 7.0821 vs exp. 7.0764 (prev. 7.0818)

Fixed Income

- Debt elevated approaching month end with added impetus via weak Chinese PMIs and mostly cooler than forecast EZ inflation data.

- Bunds, Gilts and T-note all hovering just below best levels between 136.39-135.31, 96.97-37 and 114-14+/00 bounds.

- 2029 German supply reasonably well sponsored with collapse in crude and other commodities supporting the disinflation narrative.

- Germany sells EUR 2.504bln vs exp. EUR 3.00bln 2.10% 2029 Bund: b/c 2.30x (prev. 2.50x), average yield 2.23% (prev. 2.22%) & retention 16.53% (prev. 15.00%).

Commodities

- Crude benchmarks continue to slip following Tuesday’s marked pressure and subdued settlement. Renewed pressure comes after soft Chinese data, broader risk-aversion and ahead of the June 4th OPEC+.

- Currently, WTI Jul and Brent Aug are towards the lower end of respective USD 68.60-69.69/bbl and USD 72.68-73.95/bbl parameters.

- Base metals are dented following the mentioned Chinese data while spot gold is proving relatively resilient to the firmer USD and is only incrementally softer, given the broader underlying tone and its haven status.

- Iraqi cabinet approved USD 417mln for the construction of a third offshore export pipeline.

- Norway Police are responding to report of a gas leak at Equinor’s (EQNR NO) Melkoeya LNG facility.

- Hungary asked the EU to extend import restrictions on grains from Ukraine for five eastern-European states until at least end-2023.

- EU Executive VP Dombrovskis says the EU-US steel and raw material deals are both making progress.

Geopolitics

- A fire broke out at an oil refinery in Russia which was likely due to a falling drone, according to RIA citing the local Governor; subsequently, drone crashed on Ilsky oil refinery in Russia’s south, no damages to infrastructure and no casualties, according to RIA citing local taskforce

- South Korean military said North Korea fired a space satellite, while Japan’s Defence Ministry said North Korea fired what could be a ballistic missile and Japan’s government issued a shelter-in-place order for residents in Okinawa, according to Reuters. Japan’s government later stated that the missile did not fly into Japanese territory and it lifted the evacuation warning, while South Korea said a previous warning by Seoul city was an error. Furthermore, North Korea said an accident occurred during its satellite launch and that it will verify grave defects, as well as conduct a second launch soon, while South Korea’s military said the North Korean projectile was more likely to be a space vehicle rather than a missile.

- US, Japan and South Korea strongly condemned North Korea’s launch, while South Korea said the launch was a serious provocation and a grave violation of UN resolutions, according to Reuters.

- US military said a Chinese fighter pilot performed an unnecessary aggressive manoeuvre during an intercept of a US jet over the South China Sea on May 26th, in which it flew directly in front of the nose of a US air force jet, according to a statement.

- US President Biden’s senior Middle East adviser discussed with Oman a possible outreach to Iran on the nuclear program earlier this month, according to sources cited by Axios.

US Event Calendar

- 07:00: May MBA Mortgage Applications -3.7%, prior -4.6%

- 09:45: May MNI Chicago PMI, est. 47.2, prior 48.6

- 10:00: April JOLTs Job Openings, est. 9.4m, prior 9.59m

- 10:30: May Dallas Fed Services Activity, prior -14.4

- 14:00: Federal Reserve Releases Beige Book

DB’s Jim Reid concludes the overnight wrap

The AI hype continued to help push the NASDAQ (+0.32%) to another YTD high yesterday, even if the mood was more subdued elsewhere. For instance, a sizeable majority (296/502) of the S&P 500 (unchanged) actually fell on the day, with the index only treading water thanks to tech. Nvidia climbed +2.99% to a market cap of $991bn, tantalisingly close to the trillion mark which it’s crossed intraday. Otherwise, the weak economic backdrop meant commodity aggregates fell to their lowest levels in nearly two years. And on top of that, sovereign bonds staged a big rally as concern about the outlook resurfaced as the debt ceiling distortions started to wane. So despite some of the headline gains, the last 24 hours have seen several warning lights under the surface, including multiple recession indicators that are flashing with growing alarm. The highlight today might be German, French and Italian CPI after Spain’s surprise fall yesterday (see below).

As a minimum this will be the highlight until the debt ceiling votes comes through. We’re expecting that the House of Representatives to be voting on the deal agreed by President Biden and Speaker McCarthy tonight. That deal is formally called the Fiscal Responsibility Act, and yesterday saw it pass through the House Rules Committee despite the opposition of two Republican members and all Democrats to pass 7-6, meaning it can now be voted on by the full chamber today.

In terms of the prospects for today, investors seem relatively relaxed that this is going to pass. There has been reports overnight that over 150 GOP members would vote to approve the bill, with the balance needed to pass the House coming from Democrats. So things seem on track. Indeed, one of the good news stories from yesterday was that T-bill yields around the X-date fell back to more normal levels again, with the bill expiring June 8th seeing yields fall -75bps to 5.05, after having briefly traded with a 7 handle last week. Also the 1M US Treasury yield is trading at the same level of swaps for the first time since early May, and at the same time 5yr CDS spreads for the US dropped back to their lowest level since March, which shows how fears of default have continued to ebb over recent days. Bear in mind that this deal has the backing of the Biden Administration as well as the Republican leadership in the House and Senate, even if a minority of members have already said they’ll vote against it.

Of course, the event that’s still scars a lot of people is what happened with the first TARP vote in September 2008, which for younger readers was the $700bn bailout package proposed by the Bush Administration at the height of the GFC. Much like today’s deal, it also had the support of leaders in both parties, but it was rejected in the House on its first vote by a 228-205 margin, sparking what was then the biggest one-day decline in the S&P 500 (-8.79%) since Black Monday in 1987. Now clearly we’re not at the height of a once-in-a-generation financial crisis today, but markets have been taken by surprise on these votes before, even if all might look OK for the time being.

Against that backdrop, there was a big rally among sovereign bonds yesterday, with yields on 10yr Treasuries falling -10.8bps to 3.69% (3.68% in Asia). And similarly in Europe, yields on 10yr bunds (-9.2bps), OATs (-9.8bps) and BTPs (-12.6bps) all moved notably lower for a second day. One factor supporting that was good news on the inflation side, since the Spanish CPI print for May came in at just +2.9% using the EU-harmonised measure (vs. +3.3% expected), which was the slowest it’s been since July 2021. Now of course that’s just one country, but it often attracts outsize interest since it’s one of the first to report inflation each month, so is seen as a potential leading indicator for what will happen elsewhere. We will find out more from the EU big-3 CPI prints today. Another supportive factor was that the relentless commodity decline of recent months showed no signs of abating, leaving Bloomberg’s Commodity Spot Index (-1.75%) at its lowest closing level in just over 22 months.

But on top of that, we also had another batch of weak economic data over the last 24 hours, which helped raise concern about the outlook heading into H2. For instance in the US, the Dallas Fed’s manufacturing index fell to -29.1 (vs. -18.0 expected), which is a new low for this cycle. And over in Europe, the European Commission’s economic sentiment indicator for May fell to a 6-month low of 96.5 (vs. 98.8 expected). All that came as various recession indicators continued to worsen, with the 2s10s Treasury yield curve (-4.5bps) closing at a post-SVB low of -76.8bps.

For equities, as we discussed at the top, tech led the way with the FANG+ Index (+1.54%) up to a new YTD high that now leaves its gains for 2023 at a massive +62.68%. It was a similar story for the NASDAQ (+0.32%), which also hit a new YTD high of +24.37%. However, elsewhere the story was mostly one of declines, with the equal-weighted S&P 500 -0.20%. Europe’s STOXX 600 shed -0.92%.

Asian equity markets are trading sharply lower this morning as disappointing factory activity in China is denting sentiment across the region. As I type, the Hang Seng (-2.33%) is leading losses, tumbling to a new low for 2023 while the mainland Chinese markets are also sliding with the CSI (-1.09%) and the Shanghai Composite (-0.73%) trading in the red as the economic recovery in the world’s second biggest economy is losing steam (more below). Elsewhere, the Nikkei (-1.12%) is also trading lower with the KOSPI (-0.20%) reversing earlier gains. Outside of Asia, US equity futures are slightly negative with those on the S&P 500 (-0.23%) and NASDAQ 100 (-0.13%) edging lower.