JUNE 1//GOLD CLOSED UP $14.10 TO $1977.80//SILVER CLOSED UP $0.49 TO $23.90//PLATINUM CLOSED UP 8.80 TO $1009.90 WHILE PALLADIUM CLOSED UP $27.25 TO $1397.70//IMPORTANT GOLD POSTS: AMBROSE EVANS PRITCHARD//CHINA’S ECONOMY IF FALTERING AND 5 COMMODITIES WHICH PROVE THIS IS HAPPENING/THE IRISH ARE FORCING THE CULLING OF THE CATTLE TO MEET CLIMATE CHANGE: HOW STUPID CAN THEY BE?//RUSSIA CLAIMS THAT THE USA IS BEHIND THE CONFLICT BETWEEN SERBIA AND KOSOVO//PROBLEMS OCCUR AT THE BORDER OF IRAN AND AFGHANISTAN (TALIBAN)///COVID UPDATES//DR PAUL ALEXANDER/EWOL NEWS//SOUTH AFRICA SIDELINES ANOTHER RAIL DUE TO MASSIVE THEFTS OF EQUIPMENT//DEBT CEILING BILL PASSED //DAVID STOCKMAN TELLS THE TRUTH ON THE BILL//USA MFG PMI’S FALTER BADLY/SWAMP STORIES FOR YOU TONIGHT//

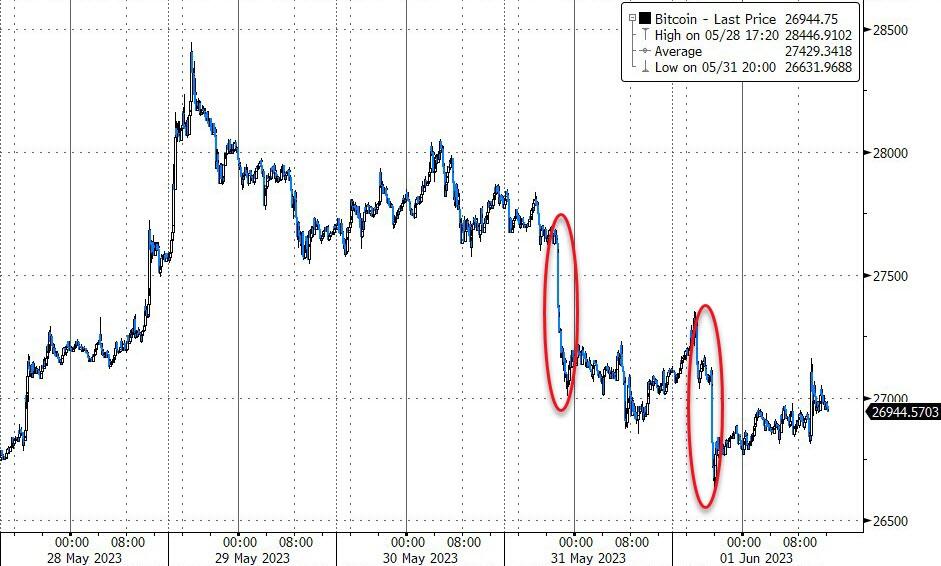

Bitcoin: afternoon price: $26,939 DOWN 126 dollars

Platinum price closing $1001.10 UP $19.85

Palladium price; $1370.45 UP$35.15

“Our system is so stinkin’ corrupt that we owe Sodom and Gomorrah an apology.” … Trader Dan Norcini in 2009

GO GATA!

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,660,61 DOWN 4.50 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1578,70 DOWN 1.21 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1838,15 UP 3.30 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

AMERICAS 161 134 167 C MAREX 6 190 H BMO CAPITAL 498 323 C HSBC 20 323 H HSBC 1503 357 C WEDBUSH 4 363 H WELLS FARGO SEC 147 435 H SCOTIA CAPITAL 844 624 H BOFA SECURITIES 5000 657 C MORGAN STANLEY 69 661 C JP MORGAN 15 2661 661 H JP MORGAN 219 685 C RJ OBRIEN 9 686 C STONEX FINANCIA 23 3 690 C ABN AMRO 88 45 709 C BARCLAYS 39 737 C ADVANTAGE 130 880 C CITIGROUP 1 880 H CITIGROUP 1389 905 C ADM 33 33

TOTAL: 6,537 6,537

JPMorgan stopped 3661/6537 contracts

FOR JUNE:

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2023. CONTRACT: 6537 NOTICES FOR 653,700 OZ or 20.3528 TONNES

total notices so far: 15,561 contracts for 1,556,100 oz (48.401 tonnes)

FOR JUNE:

SILVER NOTICES: 303 NOTICE(S) FILED FOR 1,515,000 OZ/

total number of notices filed so far this month : 362 for 1,810,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP UP $14.10

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

/NO CHANGES IN GOLD INVENTORY AT THE GLD:////

INVENTORY RESTS AT 939.56 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 49 CENTS AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV: : : INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 467.933 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A TINY SIZED 21 CONTRACTS TO 133,598 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS TINY SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR STRONG $0.37 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. TAS ISSUANCE WAS A HUGE SIZED 985 CONTRACTS. THESE WILL BE USED FOR MANIPULATION NEXT MONTH OR TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY: A HUGE 985 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.37). AND WERE UNSUCCESSFUL IN KNOCKING SOME SPEC LONGS AS WE HAD A FAIR GAIN ON OUR TWO EXCHANGES OF 274CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 0MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION. IT LOOKS LIKE IN THIS INITIAL WEEK IN THE DELIVERY CYCLE MORE MANIPULATION HAS BEEN SUMMONED BY OUR CROOKED BANKER LEADERS TO KEEP OUR PRECIOUS METALS IN CHECK.

WE MUST HAVE HAD:

A FAIR SIZED ISSUANCE OF EXCHANGE FOR PHYSICALS( 190 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.935 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S 30,000 OZ QUEUE JUMP// TOTAL FOR THE MONTH 3.965MILLION OZ ) // TINY SIZED COMEX OI LOSS/ SMALL SIZED EFP ISSUANCE/VI) HUGE NUMBER OF T.A.S. CONTRACT INITIATION (985 CONTRACTS)//ZERO T.A.S LIQUIDATION

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -removed 105CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTRACTS for 1 days, total 190 contracts: OR 0.95 MILLION OZ . (190 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 0.95 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 0.95 MILLION OZ//

RESULT: WE HAD A TINY SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 21 CONTRACTS DESPITE OUR STRONG RISE IN PRICE OF $0.37 IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 190 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.935 MILLION OZ FOLLOWED BY TODAY’S 30,000 OZ QUEUE JUMP//NEW TOTAL STANDING: 3.965 MILLION OZ////// .. WE HAVE A SMALL SIZED GAIN OF169 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE 985//ZERO FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED WEDNESDAY. THE NEW TAS ISSUANCE WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE.

WE HAD 303 NOTICE(S) FILED TODAY FOR 1,515,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 4336 CONTRACTS TO 445,695 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED – 516 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 4336 CONTRACTS) DESPITE OUR $5.70 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JUNE. AT 70.79 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S MONSTROUS 8.2457 TONNE QUEUE JUMP: NEW TOTAL 62.469 TONNES STANDING SO FAR // + /A GIGANTIC ISSUANCE OF 2042 T.A.S. CONTRACTS/ZERO FRONT END OF TAS LIQUIDATION WEDNESDAY ////YET ALL OF..THIS HAPPENED WITH A $5.70 GAIN IN PRICEWITH RESPECT TO WEDNESDAY’S TRADING.WE HAD A FAIR SIZED LOSS OF 1961 OI CONTRACTS (6.099 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2375 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 445,179

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1961 CONTRACTS WITH 4,336 CONTRACTS DECREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): A HUGE 2042 CONTRACTS) AND 2375 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 1961CONTRACTS OR 6.099TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2375 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (4336) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 1961 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 70.79 TONNES FOLLOWED BY TODAY’S 265,100 OZ QUEUE JUMP I.E. 8.2457 TONNES: NEW STANDING REDUCES TO 62.479 TONNES// /3) ZERO LONG LIQUIDATION//4) GOOD SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: GIGANTIC T.A.S. ISSUANCE: 2045 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

TOTAL EFP CONTRACTS ISSUED: 2375 CONTRACTS OR 237,500 OZ OR 7.387 TONNES IN 1 TRADING DAY(S) AND THUS AVERAGING: 2375 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY(S) IN TONNES 7.387 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 7.387/3550 x 100% TONNES 0.208% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 7.387 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A TINY SIZED 21 CONTRACTS OI TO 133,598 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 190 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 190 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 190 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 21 CONTRACTS AND ADD TO THE 190OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 169 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 0.845 MILLION OZ

OCCURRED DESPITE OUR STRONG $0.37 GAIN IN PRICE …..

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING//WEDNESDAY NIGHT

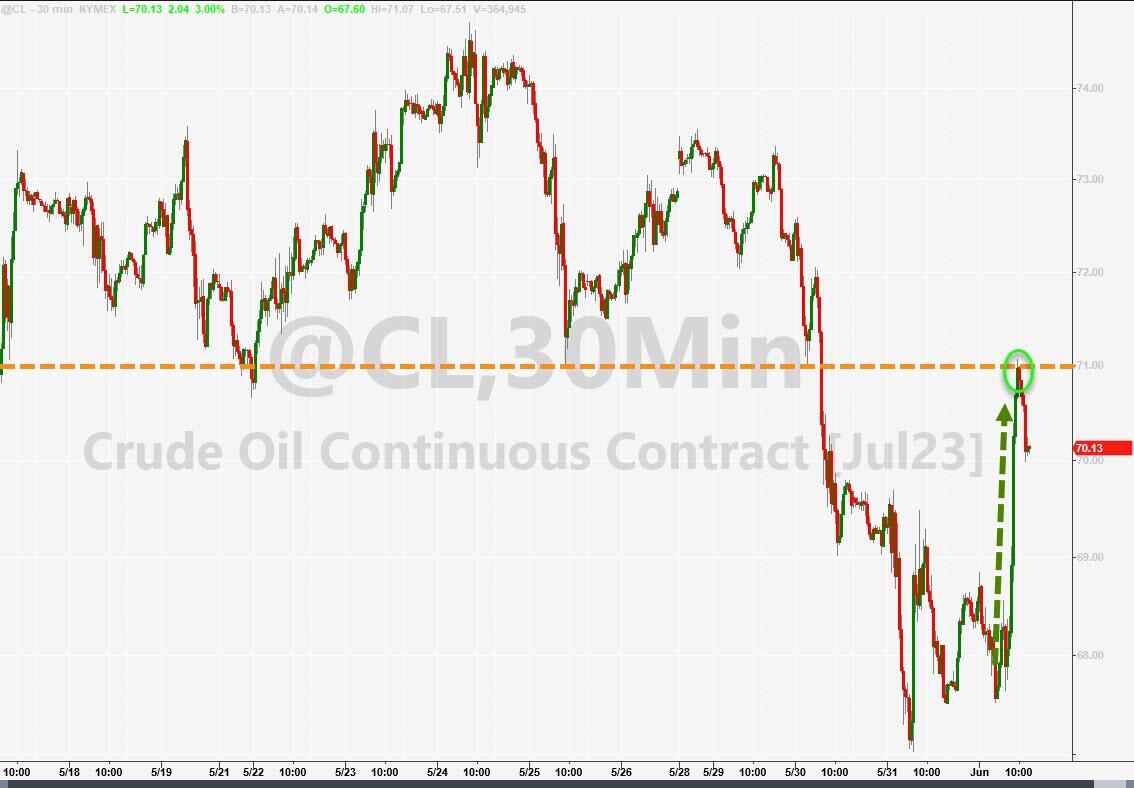

SHANGHAI CLOSED UP 0.07 PTS OR 0.00% //Hang Seng CLOSED DOWN 17.36 PTS OR 0.10% /The Nikkei closed UP 260.13 OR 0.84% //Australia’s all ordinaries CLOSED UP 0.24 % /Chinese yuan (ONSHORE) closed DOWN 7.1116 /OFFSHORE CHINESE YUAN DOWN TO 7.1289 /Oil UP TO 67.95 dollars per barrel for WTI and BRENT AT 72.66 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 4336 CONTRACTS DOWN TO 445,179 DESPITE OUR GAIN IN PRICE OF $5.70 ON WEDNESDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF MAY… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2375 EFP CONTRACTS WERE ISSUED: : AUGUST 2375 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2375 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1,961 CONTRACTS IN THAT 2,375LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED LOSS OF 4336 COMEX CONTRACTS..AND THIS FAIR SIZED LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR STRONG GAIN IN PRICE OF $5.70. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE TODAY WAS A HUGE 2042 CONTRACTS. DURING LAST WEEK THE BANKERS SOLD THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (62.506) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 62.506 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $5.70) //// AND WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD OUR FAIR SIZED LOSS OF 1961 CONTRACTS ON OUR TWO EXCHANGES. WE HAD ZERO/TINY TAS LIQUIDATION. . THE TAS ISSUED WEDNESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 6.099PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE. (70.790 TONNES) FOLLOWED BY TODAY’S HUGE 265,100 OZ EFP JUMP TO LONDON WHERE THIS 8.2457 TONNES OF GOLD WILL TAKE DELIVERY OVER IN LONDON // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $5.70

WE HAD – REMOVED 516 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 1,961 CONTRACTS OR 196,100 OZ OR 6.099 TONNES.

Total monthly oz gold served (contracts) so far this month

15,561 notices 1,556,100 OZ 48.401 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

No dealer withdrawals

Customer deposits: 0

nil

total deposits: nil oz

Withdrawals: 2

i) Out of Brinks 33,536.100 oz

ii) Out of Int. Delaware 803.775 oz (25 kilobars)

total 34,339.875 oz

Adjustments; one Manfra

customer to dealer: 1929.06 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 11,092 contracts having LOST 11,666 contracts. We had 9024 contracts served upon yesterday so we lost 2642 contracts or a huge 264,200 oz were immediately E.F.P.’d to London where they will exercise contracts and take delivery of 8.2177 tonnes of gold over in London. The next front month after June is the non active delivery month of July. Here July gained 15 contracts to stand at 2906 contracts.

AUGUST gained 7298 contracts UP to 373.618 contracts

We had 6537 contracts filed for today representing 653,700oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 15 notices were issued from their client or customer account. The total of all issuance by all participants equate to 6,537 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 3661 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2023. contract month,

we take the total number of notices filed so far for the month (15,561 x 100 oz ), to which we add the difference between the open interest for the front month of JUNE (11,092 CONTRACT) minus the number of notices served upon today 6537 x 100 oz per contract equals 2,009,600 OZ OR 62.506 TONNES the number of TONNES standing in this NON- active month of May.

thus the INITIAL standings for gold for the JUNEcontract month: No of notices filed so far (15,561) x 100 oz + (11,092 OI for the front month minus the number of notices served upon today (6557)x 100 oz} which equals 2,009,600 oz standing OR 62.506 TONNES

TOTAL COMEX GOLD STANDING: 62.506 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,836,577.877 OZ

TOTAL REGISTERED GOLD: 11,642,604.552 (362.13 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 11,193,973.325 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,937875 OZ (REG GOLD- PLEDGED GOLD) 309.109 tonnes//

END

SILVER/COMEX

JUNE 1//2023// THE JUNE 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

1,882,086.114 oz Brinks CNT JPM Loomis

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

551,231/200 oz

JPM

No of oz served today (contracts)

303 CONTRACT(S) (1,515,000 OZ)

No of oz to be served (notices)

431 contracts (2,155,000 oz)

Total monthly oz silver served (contracts)

362 Contracts (1,810,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposits

total dealer deposit: nil oz

total dealer deposits: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We had 1 customer deposits

i) Into JPMorgan: 551,231.200 oz

Total deposits: 551,231.200 oz

JPMorgan has a total silver weight: 141.367 million oz/272.237 million =51.78% of comex .//dropping fast

Comex withdrawals 4

i) Out of Brinks 228,076.760 oz

iii) Out of Loomis: 600,387.130 oz

iii) out of JPMorgan: 1,011,611.610 oz

iv) Out of CNT 42,010.914 oz

total withdrawals: 122,464.430 oz

adjustments: 1 all dealer to customer

i) Brinks 4760.200 oz

TOTAL REGISTERED SILVER: 28.157 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 272.237 million oz

DEALER SILVER DROPPING FAST.

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE /2023 OI: 734 CONTRACTS HAVING LOST 53 CONTRACT(S).

WE HAD 59 NOTICES FILED YESTERDAY (CME CORRECTION) SO WE GAINED 6 CONTRACTS OR AN ADDITIONAL 30,000 OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF JUNE.

JULY HAD A 1490 CONTRACT LOSS TO 100,616 CONTRACTS

AUGUST GAINED ITS FIRST TWO CONTRACTS TO STAND AT 2

SEPT HAS A GAIN OF 1203 CONTRACTS UP TO 21,898

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 303 for 1,515,000 oz

Comex volumes// est. volume today 78,703 excellent/

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 362 x 5,000 oz = 1,810,000 oz

to which we add the difference between the open interest for the front month of JUNE(734) and the number of notices served upon today 303 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2023 contract month: 362 (notices served so far) x 5000 oz + OI for the front month of JUNE (734) – number of notices served upon today (303 )x 500 oz of silver standing for the JUNE contract month equates to 3.965 million oz +

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JUNE 1/WITH GOLD UP $14.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 939.56 TONNES

MAY 31/WITH GOLD UP $5.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 939.56 TONNES

MAY 30/WITH GOLD UP $14.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 26/WITH GOLD UP $.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 941.29 TONNES

MAY 25/WITH GOLD DOWN $19.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 24/WITH GOLD DOWN $9.50 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 941.29 TONNES

MAY 23/WITH GOLD $2.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 942.74 TONNES

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

MAY 9/WITH GOLD UP $9.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTER DEPOSIT OF 5.88 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 937.64 TONNES

MAY 8/WITH GOLD UP $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 931.77 TONNES

MAY 5/WITH GOLD DOWN $30.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AS DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

MAY 4/WITH GOLD UP $19.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.30 TONNES

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

GLD INVENTORY: 939.56 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 1/WITH SILVER UP 49 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.933 MILLION OZ

MAY 31/WITH SILVER UP 37 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 367,000 OZ FROM THE SLV////INVENTORY RESTS AT 467.933 MILLION OZ//

MAY 30/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 26/WITH SILVER UP $0.44 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.306 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 25.WITH SILVER DOWN $0.32 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 471.606 MILLION OZ//

MAY 24/WITH SILVER DOWN $.35 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 23/WITH SILVER DOWN 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

MAY 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A TINY DEPOSIT OF .08 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 465.682 MILLION OZ//

MAY 8/WITH SILVER DOWN 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.602 MILLION OZ//

MAY 5/WITH SILVER DOWN 31 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 466.876 MILLION OZ//

MAY 4/WITH SILVER UP 53 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF .174 MILLION OZ INTO SLV.//INVENTORY RESTS AT 467.174 MILLION OZ//

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

CLOSING INVENTORY 467.933 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

The Fed Blew Up Another Real Estate Bubble And It’s Losing Air

The rampant money creation and zero percent interest rates during the COVID pandemic on top of three rounds of quantitative easing and more than a decade of artificially low interest rates in the wake of the 2008 financial crisis created all kinds of distortions and malinvestments in the economy and the financial system. It was inevitable that something would break when the Federal Reserve tried to raise interest rates in order to fight the price inflation it caused with its loose monetary policy.

Easy money is the lifeblood of the US economy and financial system. The Fed started draining that lifeblood away when it stepped in to fight the price inflation it could no longer write off as transitory. There was no way the central bank wasn’t going to break something.

The first crack in the dam was the ongoing financial crisis kicked off by the failures of Silicon Valley Bank and Signature Bank. The Federal Reserve and the US government managed to plug that hole in the dam with a bank bailout. But there are plenty of other cracks in the dam.

For instance, the investment real estate market is under significant pressure due to rising interest rates. As a report by Yahoo Finance noted, “Big owners of property around the country were already under pressure from the Federal Reserve’s aggressive campaign to raise interest rates, which raised borrowing costs and lowered building values.”

It’s not unlike the housing bubble the Fed blew up in 2005 and 2006 but this time it’s concentrated on commercial real estate such as office buildings, multi-family housing complexes, and apartment buildings.

Jay Gajavell puts a human face on this problem.

Gajavell is a Texas real estate investor. According to the Wall Street Journal, his company owned $500 million-plus worth of Sunbelt apartment buildings with more than 7,000 units. He ranked as one of the biggest landlords in Houston.

Gajavelli is what is known as a syndicator. He built his real estate empire using funding from numerous small investors who wanted to get into the real estate game without all the work.

The plan was to buy apartment buildings, upgrade units, raise rents, and sell the buildings for a profit in as little as three years. But as the WSJ described it, these investors were “highly vulnerable to interest-rate increases over the past year that crushed the business model they and thousands of others in similar deals across the US had hoped would make them wealthy.”

The Wall Street Journal described the situation as a “looming investment-property disaster.”

In fact, rising interest rates have already caught up with Gajavelli. In April, his company lost four rental complexes with more than 3,000 units through foreclosure.

The Wall Street Journal explained what did Gajavelli in.

His company had taken out commercial real-estate loans that carried floating interest rates and were adjusted each month. Those types of loans in 2021 offered initial rates as low as 3.5%. Everything changed when the Federal Reserve began raising rates last year, driving up monthly loan payments. Inflation contributed to higher expenses, and Applesway couldn’t raise rents fast enough to keep pace. After bills went unpaid, company properties went into foreclosure.”

It would be one thing if this was an isolated incident, but it isn’t. There are thousands of real estate entrepreneurs like Gajavelli, and many are in a similar situation.

A law passed by Congress in 2012 helped spark the boom in real estate syndication, making it easier to market real estate investments online. According to a Wall Street Journal analysis of Securities and Exchange Commission filings, real estate syndicators reported raising at least $115 billion from investors between 2020 and 2022.

In the wake of the pandemic, there was a major real estate boom spurred by zero percent interest rates and billions of dollars in stimulus money that further incentivized people to invest in real estate.

As housing prices exploded, rents skyrocketed as well. One property manager described it as a mania.

Now the bubble is deflating, as the WSJ describes.

Many syndicators are racing to either raise funds or sell properties before tipping into foreclosure. Most hold balloon-payment loans that require repayment when they come due this year or next. Those syndicators face large payouts at a time when getting new, more affordable property loans will be difficult. Even firms with multibillion-dollar portfolios have used syndication to buy apartment buildings that no longer make enough money to cover debt payments, bond documents show.”

While the Wall Street Journal does a great job of explaining the nuts and bolts of the syndication scheme and mentions the role of rising interest rates in popping the bubble, it completely ignores the Federal Reserve’s role in blowing up the bubble to begin with.

As I pointed out earlier, the Fed created this problem long before when it held rates artificially low for so long. It incentivized all of this borrowing and risk-taking. Everybody just assumed rates would stay low forever so they levered up and took on more and more risk.

Gajavelli probably wouldn’t have been able to build his real estate empire without Fed’s easy money policies.

Unfortunately for Gajavelli and many like him, what the Fed giveth, the Fed taketh away.

This describes the impact of Fed monetary policy on one sector. Bubbles and malinvestments are certainly present in many other sectors of the economy as well. The question is where will the next hole open up in the dam?

3,Chris Powell of GATA provides to us very important physical commentaries

the sad state of affairs with respect to the huge debt of the USA

(Ambrose Evans Pritchard/GATA)

Ambrose Evans-Pritchard: America’s Faustian pact with runaway debt is coming due

Submitted by admin on Tue, 2023-05-30 10:25Section: Daily Dispatches

By Ambrose Evans-Pritchard The Telegraph, London Tuesday, May 30, 2023

The Republicans have capitulated on the U.S. debt ceiling. This averts the risk of abrupt fiscal tightening in a slowing economy that has yet to digest the most aggressive monetary squeeze in over 40 years.

The putative accord between the White House and Congress does not even try to address the larger threat to America’s economic model and hegemonic status.

The Congressional Budget Office says the U.S. is on course for fiscal deficits of 7% of GDP as far as the eye can see.

Sacred entitlements remain untouchable. Middle-class welfare – ie. consumption – will continue to eat up an ever-greater share of the budget. It is this, that is leading to slow fiscal ruin.

The gross debt-to-GDP ratio was 62% in 2007 (IMF data). It will be 122% this year, and 138% by 2028, with no sign of reaching a plateau. By then it will have overtaken Italy.

It is a sobering thought that the US is racking up as much debt-to-GDP accumulation over 20 years as it did over two world wars and the Great Depression combined.

You can blame it on the Lehman crisis and Covid, overlaid with Trump’s unfunded tax cuts and Biden’s unfunded multi-trillion fiscal spree, but behind that lies a structural rot across most of the federal budget.

China’s fiscal deterioration has been just as bad. The difference is that China funds its own borrowing (for now) from high internal savings. Foreigners have some $25 trillion of net debt claims on the US government and US corporations.

America’s net international investment position has gone from near balance a generation ago to minus 62% of GDP. Part of that is the distortion of the strong dollar. A big chunk is not. America is selling the family silver to live. (So is Britain.)

“It is alarming to us, and should be to other investors, too. What is even more alarming is the lack of concern on the part of the U.S. policymakers,” said Stephen Jen from Eurizon SLJ, who advises Asian sovereign wealth funds.

“Foreign investors should not be blamed for starting to wonder if the US Treasuries and the dollar are still safe. We believe the U.S. debt problem will have consequences for the markets in the not-too-distant future,” he said. …

USAGold’s ‘News & Views’ letter summarizes top 10 financial posts for May

Submitted by admin on Tue, 2023-05-30 11:23Section: Daily Dispatches

11:24a ET Tuesday, May 30, 2023

Dear Friend of GATA and Gold:

USAGold’s top 10 reports and essays about the financial markets and the monetary metals in May are summarized today in the coin and bullion dealer’s monthly ‘News & Views’ letter here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

END

The farce on the debt ceiling brought to you by Craig Hemke

(Craig Hemke/Sprottt)

Craig Hemke at Sprott Money: The debt schlemieling

Submitted by admin on Tue, 2023-05-30 16:10Section: Daily Dispatches

By Craig Hemke Sprott Money, Toronto Tuesday, May 30, 2023

Another deal to extend the debt limit of the U.S. government appears to have been reached. If that’s a surprise to you, then I guess you haven’t been paying attention over the years.

The farce of the “debt ceiling” is simple political theater and nothing more. For decades cynical politicians have used the imagined “catastrophe of default” as a tool to stoke division and score political points, usually just before major elections.

Both sides of The Uniparty will ultimately claim victory, allowing their partisans to rejoice while the public at large gets fleeced. …

More and more nations strive to ditch the USA dollar, realizing that it is killing their financial well being

(Business Daily Africa/Nairobi/GATA)

Kenya’s president revives push by African nations to ditch the dollar

Submitted by admin on Wed, 2023-05-31 12:06Section: Daily Dispatches

By Constant Munda Business Daily Africa, Nairobi Tuesday, May 30, 2023

President William Ruto has asked African leaders to take first steps toward ditching the globally-bullish U.S. dollar by signing up to a pan-African payments system to facilitate trade within the continent.

Dr. Ruto has urged his peers in Africa to mobilise central and commercial banks to join the Pan-African Payments and Settlement System, (PAPSS) which was launched in January 2022.

The system for intra-African trade was developed by the African Export-Import Bank (Afreximbank) and African Continental Free Trade Area (AfCFTA) Secretariat. The initiative was backed by the African Union and African central banks.

“We are all struggling to make payments for goods and services from one country to another because of differences in currencies. And in the middle of all these, we are all subjected to a dollar environment,” Dr. Ruto told a forum of government and private-sector officials attending a forum on AfCFTA in Nairobi on Monday.

“There has been a mechanism where all our traders can trade in the local currency and we leave it to the Afreximbank to settle all the payments. We do not have to look for dollars. Our businessmen will concentrate on moving goods and services, and leave the arduous task of currencies to Afreximbank.” …

Will gold rescue Zimbabwe from the ashes of economic despair and usher in a new economic era?

Since Zimbabwe declared independence from the former Republic of Rhodesia in 1980, the southern African country has been ravaged by inflation and overall economic turmoil. Over the past 40 years, the annual inflation rate has only touched single-digit territory twice: 1980 (7 percent) and 1988 (7 percent).

Excessive money printing, fiscal mismanagement, economic sanctions, and currency instability have been the root causes of its perpetual financial crisis, resulting in political and social upheaval.

In 2008, Zimbabwe was given the unfortunate record of the highest inflation rate in the world, touching 250 million percent. This forced then-President Robert Mugabe and his government to abandon the Zimbabwe dollar and begin relying on nine foreign currencies, particularly the U.S. dollar and the South African rand. In 2019, Harare introduced a new Zimbabwean currency, but it did not take long for the revival of hyperinflation, with the inflation rate surpassing 600 percent by March 2020.

After numerous trials and errors on the monetary policy front, the Reserve Bank of Zimbabwe (RBZ) experimented with something old and something new: a gold-backed digital currency.

“Pursuant to the resolution of the Monetary Policy Committee (the MPC) on 28 March 2023 to complement the issuance of physical gold coins with gold-backed digital products, the Bank wishes to advise that it will be issuing gold-backed digital tokens with effect from 8 May 2023,” said RBZ Governor John Mangudya in a statement. “The gold-backed tokens will be fully backed by physical gold held by the Bank.”

Central bank officials say this money will be supported by 140 kilograms (4,900 ounces) of gold.

The two-phase implementation began with the RBNZ selling digital tokens to investors for a minimum price of $10 for individuals and $5,000 for businesses and other entities. The transition will then allow consumers to purchase the digital currency from banks and use the tokens to conduct “person-to-person and person-to-business transactions and settlements” by using “e-gold wallets or e-gold cards” held by these financial institutions. Consumers can also rely on virtual tokens to save their money.

The announcement came months after the government allowed gold coins to be used as legal tender, but the decision did not appeal to struggling families because they were too expensive.

Gold bars at Korea Gold Exchange in Seoul, South Korea, on Aug. 6, 2020. (Kim Hong-Ji/Reuters)

A Lack of Trust

But while this policy pursuit might sound like music to the ears of sound money advocates, a chorus of critics contend that this will not achieve the desirable outcome of currency stability.

Some economists have expressed doubt about the efficacy of this project, asserting that this is not a traditional gold standard because the tokens are not convertible to gold bars and coins.

A notable drawback is a paucity of trust in the institutions and officials managing the precious metal, says Aaron Rafferty, CEO of the financial technology firm Standard DAO.

“The critical factor here isn’t gold itself, but rather a reliable, trusted institution to maintain the gold reserves and handle redemption requests,” Rafferty told The Epoch Times. “Any nation considering such a policy will need robust systems to manage these requirements.”

Richard Gardner, the CEO of financial technology company Modulus, says the better option is to re-adopt the greenback.

“There is an easy solution here, and it doesn’t involve a digital currency,” he told The Epoch Times. “Instead, the country should simply take its medicine: re-adopt the US dollar. Not only will this move not be the start of an avalanche effect of similar global efforts, it will almost certainly be a failure.”

The International Monetary Fund (IMF) has cautioned against the campaign, warning of the financial stability, governance, operational, and legal risks.

Currency Experiments

Across the global economy, a growing number of countries are experimenting with digital currencies backed by central banks. Some have already launched these virtual currencies, while others are in the trial phase.

Last year, Nigeria released the eNaira, the country’s central bank digital currency (CBDC). However, nearly a year later, the adoption rate has been abysmal, with about 99 percent of digital wallets unused.

“The take-up of the eNaira by households and merchants has been slow,” the IMF said in a recent report assessing the eNaira.

“As indicated by the levels of wallet downloads and transactions, the public adoption of the eNaira thus far has been disappointingly low.”

The Bahamas and Jamaica have released their digital currencies. China, Japan, and Russia are testing the digitization efforts of their currencies. The United States, UK, and the European Union are still in the research phases of their CBDCs.

But Zimbabwe’s endeavor is unique because it is backed by the yellow metal, meaning it is not a digital version of physical fiat currency.

At a time when more central banks are stockpiling gold, experts have speculated that more nations could integrate the commodity with their currencies.

Gold: The New Money

Could Zimbabwe be facilitating a new era of gold-backed money?

At the very least, the development of a gold-supported digital currency comes at a time when there has been a substantial increase in demand for the metal.

In the first quarter, central bank demand for gold reached 228.4 tons, up 176 percent from the same time a year ago, according to the World Gold Council (WGC). This was also higher than the previous first-quarter record established in 2013.

Singapore (69 tons), China (58 tons), Turkey (30 tons), and India (7 tons) were the largest buyers of the metal commodity. Selling was modest, led by Kazakhstan (negative 20 tons), Uzbekistan (negative 15 tons), and Cambodia (negative 10 tons).

“Our broad expectation for central bank demand in 2023 has, so far, been borne out,” the WGC said in its report this month.

“Central bank buying remains robust, with little to indicate that this will change in the short term. As such, we maintain our belief that purchases will continue to outweigh sales as we move into Q2.”

WGC data also confirmed in January that 2022 was a record year for central bank gold demand, soaring more than 1,100 tons worth approximately $70 billion.

Moreover, emerging market countries are poised to surpass their developed market counterparts in gold reserves by 2050 “should they maintain the current pace of acquisition,” noted In Gold We Trust.

Central banks acquire gold for a variety of reasons, including the diversification of reserves, hedging against inflation and currency risks, and bolstering the credibility and confidence of these institutions. But during geopolitical turmoil and a bloc of nations altering the world order, some officials have signaled that gold could play an integral role, particularly as they reduce their exposure to foreign currencies, like the greenback.

Ahead of the annual BRICS Summit in August in South Africa, officials have hinted that the annual meeting will focus on the creation of a new currency that could rival the U.S. dollar or euro, effectively bolstering the global de-dollarization campaign.

Russian President Vladimir Putin told BRICS Business Forum participants last year that the bloc (Brazil, Russia, India, China, and South Africa) is reviewing the creation of a new international reserve currency based on the basket of currencies of our countries.”

Russian President Vladimir Putin takes part in the XIV BRICS summit in virtual format via a video call, in Moscow, on June 23, 2022. (Mikhail Metzel/Sputnik/AFP via Getty Images)

State Duma (the Russian legislative assembly) deputy chairman Alexander Babakov purported in March at the St. Petersburg International Economic Forum event in New Delhi, India, that a currency could be pegged to gold or “other groups of products, rare-earth elements, or soil.”

While a currency supported by commodities is not universally endorsed, it has been championed by several leading economic figures.

Stephen Moore, a bestselling author and economic adviser to former President Donald Trump’s 2016 campaign, believes monetary policy could be based on general commodity prices, such as cotton, copper, crude oil, and wheat.

“However, I do not advocate a return to the gold standard today,” the former Fed nominee wrote in a 2019 op-ed.

In a June 2018 paper for the Cato Journal, economist Judy Shelton, who was nominated to the Fed by Trump, wrote, “We make America great again by making America’s money great again.”

She proposed linking the greenback to gold or another commodity instead of just trusting Washington.

“In proposing a new international monetary system linked in some way to gold, America has an opportunity to secure continued prominence in global monetary affairs while also promoting genuine free trade based on a solid monetary foundation,” Shelton wrote.

“Gold has historically provided a common denominator for measuring value; widely accepted at all income levels of society, it is universally acknowledged as a monetary surrogate with intrinsic value.”

At a time when the U.S. government is facing astronomical levels of debt—a $32 trillion national debt and trillion-dollar budget deficits—sound money proponents aver that gold could help restore fiscal discipline.

According to former Fed Chair Alan Greenspan, gold limits the amount the government can borrow because it cannot be printed.

“But government bonds are not backed by tangible wealth, only by the government’s promise to pay out of future tax revenues,” Greenspan wrote in a 1966 essay entitled “Gold and Economic Freedom.”

However, critics charge that commodity-backed currencies would pose trouble for governments because they would prevent officials from responding to changes in economic conditions and leave currencies vulnerable to commodity price fluctuations. A dramatic shift might also distort the allocation of resources and cause transactional difficulties for everyday purchases.

A New Monetary Regime

As the international de-dollarization initiative accelerates and more economies attempt to shift away from dollar dependence, there is an expectation that a new monetary regime could be forming. Experts have noted that if the BRICS or individual countries do successfully topple the dollar hegemony, it might not happen for many years. With global debt exceeding $300 trillion, could the world economy afford to dismantle the fiat empire?

END

5.IMPORTANT COMMENTARIES ON COMMODITIES:

END

5 B GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.11116

OFFSHORE YUAN: 7.1289

SHANGHAI CLOSED UP 0.07 PTS OR 0.00%

HANG SENG CLOSED DOWN 17.36 PTS OR 0.10%

2. Nikkei closed UP 260.13 PTS OR 0.84%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 104.14 EURO RISES TO 1.0696 UP 3 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.413 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 139.55 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN// OFF- SHORE:DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.2815***/Italian 10 Yr bond yield RISES to 4.067*** /SPAIN 10 YR BOND YIELD RISES TO 3.325…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 3.735

3j Gold at $1965.00 silver at: 23.45 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 16 /100 roubles/dollar; ROUBLE AT 80.98//

3m oil into the 67 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 139.55 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .413% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9103 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9736 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.647 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 3.847 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.455 UP 7 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 20.80…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.1905 UP 1 BASIS PTS (RATES RISING RAPIDLY)

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Rise After House Passes Debt Deal, Europe Boosted By Weaker Inflation

THURSDAY, JUN 01, 2023 – 08:03 AM

US futures edged higher after the House passed a deal to avert a US default (with more Democrats voting for the “McCarthy” deal than Republicans) and Fed officials hinted at a pause in interest-rate hikes. Globally, the Caixin China PMIs beat expectations (not to be confused with the catastrophic official PMI print) and Euro Area CPI printed dovishly, aiding a global risk-on tone. As of 7:45am ET, S&P 500 futures added 0.2% and were again trading right around 4,200 ironclad resistance, while Nasdaq 100 contracts were 0.1% higher. The Dollar slumped to a three day low as the euro rallied after data showed underlying inflation in the euro zone dipped by more than expected in May, though that may not stop the European Central Bank from raising rates. Treasury yields edged higher, mirroring moves in Europe and the UK. Gold and Bitcoin fell, while oil climbed for the first time in three days. Today’s macro data focus includes ADP, Jobless Claims, ISM-Mfg, and Construction Spending. As the market moves past the debt ceiling, the focus shifts to the Fed and the macro narrative.

In premarket trading, a rally in companies exposed to the development of artificial intelligence-related products continued to cool in US premarket trading. Software maker C3.ai Inc. plunged as much as 22% after a disappointing sales outlook. Nvidia, whose meteoric rise had fueled the rally, was steady after losing some ground on Wednesday. Among other individual movers, Salesforce Inc. slumped abut 6% after it gave a lackluster outlook for future sales. Advance Auto Parts Inc. extended a decline after cutting earnings and sales guidance. Here are some other notable premarket movers:

Alteryx rises 5.6% in premarket trading as BofA moves to buy from neutral in note, citing three reasons supporting its upgrade for the software company.

Chewy shares jump 16% in US premarket trading as analysts said the online pet supplies retailer topped expectations across the board, with a beat on its key customer metric the highlight.

Lucid shares drop 8% in US premarket trading, after the electric-vehicle maker said it’s raising about $3 billion in a common stock offering, with the majority of the money coming from its Saudi owners. The fundraising reduces expectations for Lucid to go private anytime soon, Bloomberg Intelligence notes.

Nordstrom shares rallied as much as 7.8% in premarket trading, after the department-store chain reported better-than-expected quarterly revenue and profit. Analysts were optimistic about the improvements at the retailer’s off-price Rack stores.

Okta shares fall as much as 19% in premarket trading on Thursday, after the application software company reported its first- quarter results and analysts noted weakness in the outlook for current remaining-performance obligations (cRPO) as a concern.

Salesforce shares fall as much as 6% in premarket trading, after the software company reported its first-quarter results and gave a forecast showing the company isn’t growing as fast as it used to. Analysts noted, in particular, the slowdown in contracted sales.

Veeva Systems quarterly results beat expectations, with the application software firm’s billings a beat. Notably, analysts said it appears to be navigating well through the macro weakness which had impacted its peers. Veeva shares rose 7.1% in after-hours trading.

Passage of the debt-ceiling deal struck by House Speaker Kevin McCarthy and President Joe Biden means the bill will be sent to the Senate where it will be promptly signed well before the June 5 default deadline. The signs of optimism were helped along by comments from Fed officials who backed the possibility of holding rates unchanged the next meeting, and some encouraging economic data out of China.

“Finally, some good news is driving today’s optimism,” said Ludovica Scotto di Perta, a structured-product specialist at Swissquote Bank SA. “US raising the debt ceiling and sentiment that the Fed will pause are boosting risk appetite. It might only be temporary but we will take anything at this point.”

“A June swoon may be in the cards as the S&P 500 struggles to clear key resistance at 4,200,” said Adam Turnquist, chief technical strategist at LPL Financial. “While a deal in Washington could be a catalyst for a breakout, overbought conditions in the technology sector and mega-cap space — the primary drivers of this year’s market advance — could make this a high hurdle for the market to clear on a near-term basis, especially without broader participation.”

Meanwhile, hopes for a Fed pause were partly pared back after Wednesday’s JOLTS jobs report for April showed more than 10 million openings, the highest in three months and above consensus estimates. But Fed Governor Philip Jefferson said the central bank is inclined to keep interest rates steady in June to assess the economic outlook. His remarks were echoed by Philadelphia Fed President Patrick Harker, who said, “I think we can take a bit of a skip for a meeting.”

Attention turns next to US jobless claims data due later Thursday, before Friday’s nonfarm payrolls.

European stocks rose amid a wider risk-on sentiment after the House passed debt limit deal, and were on course to snap a three-day losing streak after US lawmakers took a step closer to averting a default. The Stoxx 600 is up 0.7% with media, banks and carmakers among the leading performers as data showed euro-area inflation slowed more than analysts’ estimates in May. Adnoc Logistics & Services, the maritime logistics unit of Abu Dhabi’s main energy company, soared as much as 52% on its debut after a hugely oversubscribed initial public offering. Airbus SE gained after Reuters reported a rise in aircraft deliveries. Here are the most notable European movers:

Neste shares gain as much as 4.4% after being raised to buy from neutral at UBS, with the broker more optimistic on the outlook for renewable fuel products beyond the key Swedish market

Recordati gains as much as 5% and leads gains on Italy’s FTSE MIB benchmark, after Equita added the Italian drugmaker to its best picks selection, citing better-than-expected 1Q results

Johnson Matthey rises as much as 2.1% after Bloomberg reported the British industrial conglomerate is planning the sale of its medical device components business

Wolters Kluwer rises as much as 4.1%, after BNP Paribas Exane raises its recommendation to outperform, seeing professional information providers such as Wolter Kluweras potential AI winners

Lonza gains 1.6%, after the drug-ingredient supplier announced its acquisition of early stage biotech Synaffix. Morgan Stanley welcomes the move, saying it gains access to ADC technology

ITM Power rises as much as 4.4%, after the clean-fuel firm said it is making good progress against its 12-month plan, with net cash set to be ahead of guidance and the adjusted Ebitda loss within

Remy Cointreau trades flat, having initially jumped as much as 6%, after the French distiller reported FY current operating income that beat estimates

Dr. Martens slumps 14% at the open after the bootmaker’s FY profit missed expectations. Morgan Stanley analysts called the sales forecast “ambitious,” while RBC sees double-digit downgrades ahead

Auto Trader shares slip as much as 2.5%, with analysts predicting limited changes to consensus estimates following results and guidance that largely matched expectations

Pennon shares fall as much as 2.3% as worries over the ongoing Ofwat investigation into sewage pollution overshadow the utility’s EPS beat, with Jefferies flagging lack of detail in the guidance

Earlier in the session, most Asian benchmarks rose, though gains in Chinese stocks faded as investors studied mixed readings on the country’s manufacturing activity. Caixin manufacturing data for May showed an expansion, exceeding forecasts for a small contraction. The numbers followed official figures Wednesday that showed a further contraction in activity.

Hang Seng and Shanghai Comp. shrugged off the early indecision and were boosted after the Chinese Caixin Manufacturing PMI data partially atoned for yesterday’s weak official PMI readings.

Japan’s Nikkei 225 was marginally supported by data releases including business capex which grew at its fastest pace since Q3 2016 and with Japanese firms logging their largest recurring profits for Q1.

Australia’s ASX 200 was choppy in early trade but ultimately gained after stronger-than-expected capital expenditure and the improvement in Chinese Caixin PMI.

Key stock gauges in India fell for a second day, led by losses in financial services and communication companies. The S&P BSE Sensex fell 0.3% to 62,428.54 in Mumbai, while the NSE Nifty 50 Index declined 0.3% to 18,487.75. The MSCI Asia-Pacific index climbed 0.4% for the day. Nifty Financial Services and Nifty Bank index were the worst performing sectoral indexes falling 0.6% and 0.8%, respectively. Out of 30 shares in the Sensex index, 18 rose, while 12 fell.

In FX, the Bloomberg Dollar Spot Index is flat while the Swiss franc has outperformed its G-10 peers slightly. The Norwegian krone is the worst performer, falling 0.8% versus the greenback. Crude futures decline with WTI falling 0.3% to trade near $67.90. Spot gold falls 0.2% to around $1,958. Bitcoin drops 0.7%. The euro rallied against the dollar after data showed underlying inflation in the euro zone dipped by more than expected in May, though that may not stop the European Central Bank from raising rates. European Central Bank Governing Council member Olli Rehn said the bank won’t contemplate lowering borrowing costs before core consumer-price growth slows in a continuous manner.

In rates, treasuries are lower with US 10-year yields rising 3bps, while two-year borrowing costs climb 4bps as stock futures partly bounce from Wednesday’s drop. 2s10s, 5s30s spreads are flatter by 1bp and 1.8bp on the day while 10-year yields are around 3.67%, cheaper by 2.5bp and lagging bunds and gilts by 0.5bp and 1.5bp in the sector. Bunds and gilts are also in the red with the former showing little reaction to data showing a larger than expected slowdown in euro-area inflation. US session focus turns to data, including ADP employment, jobless claims and ISM manufacturing. Fed’s Harker also due to speak after urging a June pause Wednesday.

In commodities, WTI futures lower by 0.75% on the day. Industrial metals climbed from six-month lows, led by copper and nickel. China’s sluggish economy has been a key driver of weakness demand for raw materials.

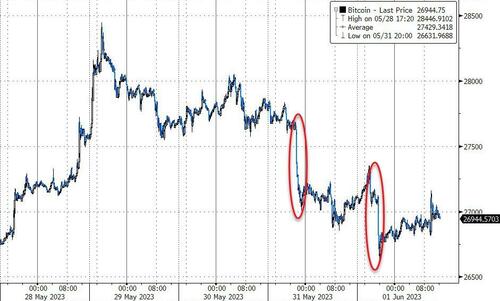

Bitcoin is softer on the session, though only incrementally so, and remains in close proximity to the USD 27k mark which itself is towards the mid-point of sub-1k parameters.

To the day ahead now, and the data highlights include the flash CPI release from the Euro Area for May, as well as the unemployment rate for April. Otherwise in the US, there’s the ISM manufacturing release for May, the ADP’s report of private payrolls for May, and the weekly initial jobless claims. In addition, there’s the global manufacturing PMIs for May, along with April data on German retail sales and UK mortgage approvals. From central banks, we’ll hear from ECB President Lagarde, the ECB’s Knot and Villeroy, as well as the Fed’s Harker. The ECB will also be releasing the account of their May meeting.

Market Snapshot

S&P 500 futures up 0.2% to 4,197.25

MXAP up 0.3% to 158.90

MXAPJ little changed at 501.17

Nikkei up 0.8% to 31,148.01

Topix up 0.9% to 2,149.29

Hang Seng Index little changed at 18,216.91

Shanghai Composite little changed at 3,204.64

Sensex little changed at 62,620.45

Australia S&P/ASX 200 up 0.3% to 7,110.81

Kospi down 0.3% to 2,569.17

STOXX Europe 600 up 0.9% to 455.89

German 10Y yield little changed at 2.30%

Euro down 0.1% to $1.0675

Brent Futures up 0.3% to $72.81/bbl

Gold spot down 0.4% to $1,955.07

U.S. Dollar Index little changed at 104.39

Top Overnight News

China’s Caixin manufacturing PMI for May came in at 50.9, up from 49.5 in April and ahead of the Street’s 49.5 forecast. RTRS

China has only modestly expanded its energy ties w/Russia, suggesting Xi is cautious about embracing Moscow as Putin becomes a larger int’l pariah. SCMP

The ECB has gone through most of its monetary policy tightening to bring inflation back to its medium-term target of 2%, though the cycle is not quite over yet, ECB Vice-President Luis de Guindos said on Thursday. RTRS

The head of UK chip designer Arm met Chinese officials in Beijing on Monday as the group sought to resolve issues over its plan to sell shares in New York. While Arm has tried to wash its hands of its problematic Chinese joint venture, Beijing has so far refused to process paperwork confirming the transfer of its stake to owner SoftBank. FT

A rare ECB warning about the bond market risk of a Bank of Japan policy change comes at a time when Japanese outflows from the region are already at record levels. Investors from the Asian nation offloaded 5.4 trillion yen ($38.7 billion) of European bonds in 2022, the most according to Bloomberg-compiled data going back to 2005. While Japanese funds have been net buyers so far this year, they’ve spent a mere 81 billion yen on purchases — the lowest amount for a first quarter in six years. BBG

Eurozone CPI for May undershot the Street, coming in at +6.1% Y/Y on the headline (down from +7% in April and below the Street’s +6.3% forecast) and +5.3% core (down from +5.6% in April and below the Street’s +5.5% forecast). BBG

The debt ceiling bill passed the House by an overwhelming amount Wed night (the final vote was 314-117, including 149-71 for Republicans and 165-46 for Democrats). NYT

Federal Reserve officials signaled they are increasingly likely to hold interest rates steady at their June meeting before preparing to raise them again later this summer.

WSJ

US crude stockpiles rebounded 5.2 million barrels last week after a big drop in the prior period, the API is said to have reported. Stocks at Cushing rose for a sixth week. More oil: OPEC+ faces a divided market when it meets this weekend. The group has never cut within three months of similar action. BBG

Overseas sales of U.S. oil and refined products have surged. Exports of crude have jumped twelve-fold since December 2015, when Washington nixed crude-export restrictions…(WSJ)

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly positive after the US House passed the debt ceiling bill to avert a default which now moves to the Senate and with sentiment helped by the surprise expansion in Chinese Caixin Manufacturing PMI. ASX 200 was choppy in early trade but ultimately gained after stronger-than-expected capital expenditure and the improvement in Chinese Caixin PMI. Nikkei 225 was marginally supported by data releases including business capex which grew at its fastest pace since Q3 2016 and with Japanese firms logging their largest recurring profits for Q1. Hang Seng and Shanghai Comp. shrugged off the early indecision and were boosted after the Chinese Caixin Manufacturing PMI data partially atoned for yesterday’s weak official PMI readings.

Top Asian News

US official said fewer US companies are applying to export sensitive tech to China amid growing government scrutiny of the flow of goods to the country, especially those with potential military applications, according to WSJ.

Taiwan’s government said it expects to sign the first deal under the new trade talks framework with the US on Thursday, according to Reuters.

European bourses are firmer across the board, Euro Stoxx 50 +1.0%, as sentiment continues to improve after the US House vote and strong Chinese Caixin PMI. Note, limited sustained reaction was seen following the EZ Flash PMIs given they very much chime with the skew from the regional metrics released in recent sessions. Sectors are predominantly firmer with Energy outperforming after recent marked pressure while Real Estate names lag across the region. Stateside, futures are essentially flat as we await the debt ceiling’s progression into the Senate and particularly the prospect of amendments sending it back to the House, ES +0.2%. Nvidia (NVDA) CEO is to meet TSMC (2330 TT/TSM) and Foxconn (2354 TT) executives on Friday; adds that TSMC has immense capacity and incredible agility.

Top European News

ECB’s Lagarde says today inflation is too high and is set to remain so for too long; we will keep moving forward – determined and undeterred – until we see inflation returning to our 2% medium-term target in a timely manner. Speech published after the EZ CPI print.

ECB’s Rehn says core inflation must slow for the ECB to consider easing. Monetary policy journey has not concluded yet. Remarks made before the EZ CPI print

ECB’s de Guindos says recent data on inflation are positive, still far from the inflation target. Still someway to go on rates Remarks made before the EZ CPI print

ECB’s Knot says there is a need to reconsider which banks should be considered systemic, time to reconsider liquidity buffers after the SVB collapse.

BoE Monthly Decision Maker Panel data – May 2023: 1-year ahead CPI inflation expectations ticked up to 5.9%, up from 5.6% in April.

FX

Buck bases after downside in wake of Fed’s Harker and Jefferson backing June FOMC rate skip, DXY sits tight within 104.150-500 confines ahead of more NFP proxies, final US manufacturing PMI and ISM.

Yen retreats towards 140.00 vs Dollar as UST-JGB differentials widen.

Euro capped just shy of 1.0700 and raft of upside option expiries against the Greenback amidst mixed EZ data and manufacturing PMIs.

Aussie underpinned around 0.6500 vs Buck after stronger than expected Capex, but Yuan remains week sub-7.1000 on US-China angst rather than 50+ Caixin Chinese PMI.

PBoC set USD/CNY mid-point at 7.0965 vs exp. 7.0964 (prev. 7.0821)

Fixed Income

Bonds retreat after pre-month end squeeze awaiting Senate debt ceiling passage, a busy June 1st US agenda and NFP on Friday.

Bunds, Gilts and T-note are all underwater within 136.17-135.60, 96.74-34 and 114-16/01 respective ranges.

French OATs and Spanish Bonos soft in the wake of multi-tranche issuance.

Commodities