by harveyorgan · in Uncategorized · Leave a comment·Editi

GOLD PRICE CLOSED: DOWN $24.40 TO $1953.40

SILVER PRICE CLOSED: DOWN $0.23 AT $23.67

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1948.50

Silver ACCESS CLOSE: 23.62

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $27,092 UP 153 Dollars

Bitcoin: afternoon price: $27,210 UP 271 dollars

Platinum price closing $1002.95 UP $1.85

Palladium price; $1409.15 UP $38.70

“Our system is so stinkin’ corrupt that we owe Sodom and Gomorrah an apology.” … Trader Dan Norcini in 2009

GO GATA!

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,615,61 DOWN 45.50 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1564.80 DOWN 13.34 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1819.67 DOWN 17 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

C 30

323 H HSBC 197

357 C WEDBUSH 1

435 H SCOTIA CAPITAL 247

624 C BOFA SECURITIES 373

657 C MORGAN STANLEY 16

661 C JP MORGAN 357

661 H JP MORGAN 29

685 C RJ OBRIEN 1

686 C STONEX FINANCIA 3

690 C ABN AMRO 45 4

709 C BARCLAYS 5

880 C CITIGROUP 71

880 H CITIGROUP 182

905 C ADM 8 4

TOTAL: 856 856

JPMorgan stopped 386/856 contracts

FOR JUNE:

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2023. CONTRACT: 856 NOTICES FOR 85,600 OZ or 2.6625 TONNES

total notices so far: 16,417 contracts for 1,641,700 oz (51.063 tonnes)

FOR JUNE:

SILVER NOTICES: 42 NOTICE(S) FILED FOR 210,000 OZ/

total number of notices filed so far this month : 404 for 2,020,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $24.40

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD://// A WITHDRAWAL OF 1.45 TONNES FROM THE GLD/

INVENTORY RESTS AT 938.11 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 23 CENTS AT THE SLV//

SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV/// INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 467.015 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 198 CONTRACTS TO 133,796 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS SMALL SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR STRONG $0.49 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. TAS ISSUANCE WAS A HUGE SIZED 952 CONTRACTS. THESE WILL BE USED FOR MANIPULATION THIS MONTH. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY: A HUGE 952 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.49). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A FAIR GAIN ON OUR TWO EXCHANGES OF 273 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 0 MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION.

WE MUST HAVE HAD:

A SMALL SIZED ISSUANCE OF EXCHANGE FOR PHYSICALS( 75 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.935 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S 210,000 OZ QUEUE JUMP// TOTAL STANDING FOR THE MONTH 4.175 MILLION OZ ) // SMALL SIZED COMEX OI GAIN/ SMALL SIZED EFP ISSUANCE/VI) HUGE NUMBER OF T.A.S. CONTRACT INITIATION (952 CONTRACTS)//ZERO T.A.S LIQUIDATION

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -removed 39 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTRACTS for 2 days, total 265 contracts: OR 1.325 MILLION OZ . (132 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 1.325 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 1.325 MILLION OZ//

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 198 CONTRACTS DESPITE OUR STRONG RISE IN PRICE OF $0.49 IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A TINY SIZED EFP ISSUANCE CONTRACTS: 75 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.935 MILLION OZ FOLLOWED BY TODAY’S 210,000 OZ QUEUE JUMP//NEW TOTAL STANDING: 4.175 MILLION OZ////// .. WE HAVE A SMALL SIZED GAIN OF 312 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE 952//ZERO FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED THURSDAY. THE NEW TAS ISSUANCE WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE.

WE HAD 42 NOTICE(S) FILED TODAY FOR 210,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1817 CONTRACTS TO 443,700 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED – 338 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 1479 CONTRACTS) DESPITE OUR $14.10 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JUNE. AT 70.79 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0 TONNE QUEUE JUMP//0 E.F.P.: NEW TOTAL 62.569 TONNES STANDING SO FAR // + /A SMALL ISSUANCE OF 456 T.A.S. CONTRACTS/ZERO FRONT END OF TAS LIQUIDATION THURSDAY ////YET ALL OF..THIS HAPPENED WITH A $14.10 GAIN IN PRICE WITH RESPECT TO THURSDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 1563 OI CONTRACTS (4.861 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3380 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 443,362

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1563 CONTRACTS WITH 1817 CONTRACTS DECREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): A SMALL 456 CONTRACTS) AND 3380 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1563 CONTRACTS OR 4.861TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3380 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (1817) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 1563 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 70.79 TONNES FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP//0 OZ E.F.P. JUMP // NEW STANDING REDUCES TO 62.569 TONNES// /3) ZERO LONG LIQUIDATION//4) SMALL SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: SMALL T.A.S. ISSUANCE: 456 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

TOTAL EFP CONTRACTS ISSUED: 5755 CONTRACTS OR 575,500 OZ OR 17.900 TONNES IN 2 TRADING DAY(S) AND THUS AVERAGING: 2878 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY(S) IN TONNES 17.900 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 17.900/3550 x 100% TONNES 0.508% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 17.900 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A SMALL SIZED 198 CONTRACTS OI TO 133,796 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 75 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 75 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 75 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 198 CONTRACTS AND ADD TO THE 75 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 273 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 1.365 MILLION OZ

OCCURRED DESPITE OUR STRONG $0.49 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED UP 25.43 PTS OR 0.79% //Hang Seng CLOSED UP 733.03 PTS OR 1.02% /The Nikkei closed UP 376.21 OR 1.21% //Australia’s all ordinaries CLOSED UP 0.56 % /Chinese yuan (ONSHORE) closed UP 7.0632 /OFFSHORE CHINESE YUAN UP TO 7.0802 /Oil UP TO 71,27 dollars per barrel for WTI and BRENT AT 73.91 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1817 CONTRACTS DOWN TO 443,362 DESPITE OUR GAIN IN PRICE OF $14.10 ON THURSDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3380 EFP CONTRACTS WERE ISSUED: : AUGUST 3380 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3380 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1,563 CONTRACTS IN THAT 3380 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 1817 COMEX CONTRACTS..AND THIS FAIR SIZED LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR STRONG GAIN IN PRICE OF $14.10. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE TODAY WAS A VERY SMALL 436 CONTRACTS. DURING LAST WEEK THE BANKERS SOLD THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE//WE SHOULD HAVE NO MANIPULATION FROM T.A.S THIS WEEK.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (62.559) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 62.569 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $14.10) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR FAIR SIZED GAIN OF 1563 CONTRACTS ON OUR TWO EXCHANGES. WE HAD ZERO TAS LIQUIDATION . THE TAS ISSUED THURSDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 4.861 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE. (70.709 TONNES) FOLLOWED BY TODAY’S 0 OZ EFP JUMP TO LONDON//0 OZ QUEUE JUMP..NEW STANDING REMAINS AT 62.569 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $14.10

WE HAD – REMOVED 338 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1,563 CONTRACTS OR 156,300 OZ OR 4.861 TONNES.

Estimated gold volume today:// 200,914 fair

final gold volumes/yesterday 183,915// poor

//JUNE 2/ FOR THE JUNE 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil . nil |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 36,253.360 oz Brinks Delaware |

| No of oz served (contracts) today | 856 notice(s) 85,600 OZ 2.6625 TONNES |

| No of oz to be served (notices) | 3699 contracts 453.500 oz 11.505 TONNES |

| Total monthly oz gold served (contracts) so far this month | 16,417 notices 1,641,700 OZ 51.063 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

No dealer withdrawals

Customer deposits: 2

i) Into Brinks 32,009.144 oz

ii) Into Delaware 4244.216 oz

total deposits: 36,253.360 oz

Withdrawals: 0

total nil oz

Adjustments; none

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 4555 contracts having LOST 6537 contracts. We had 6537 contracts served upon yesterday so we lost 0 contracts or where neither zero oz were E.F.P.d to London nor were queue jumped..

The next front month after June is the non active delivery month of July. Here July lost 85 contracts to stand at 2821 contracts.

AUGUST gained 4308 contracts UP to 377,921 contracts

We had 856 contracts filed for today representing 85,600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 9 notices were issued from their client or customer account. The total of all issuance by all participants equate to 856 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 386 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2023. contract month,

we take the total number of notices filed so far for the month (16,417 x 100 oz ), to which we add the difference between the open interest for the front month of JUNE (4555 CONTRACT) minus the number of notices served upon today 856 x 100 oz per contract equals 2,011,600 OZ OR 62.569 TONNES the number of TONNES standing in this NON- active month of May.

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (16,417) x 100 oz + (455) [OI for the front month minus the number of notices served upon today (6557)x 100 oz} which equals 2,011600 oz standing OR 62.569 TONNES

TOTAL COMEX GOLD STANDING: 62.506 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,704,729.632 OZ 53.02 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,872,831.237 OZ

TOTAL REGISTERED GOLD: 11,642,604.552 (362.13 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 11,230,226.685 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,937875 OZ (REG GOLD- PLEDGED GOLD) 309.109 tonnes//

END

SILVER/COMEX

JUNE 2//2023// THE JUNE 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 00 oz . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 632,838.322 oz CNT Delaware |

| No of oz served today (contracts) | 42 CONTRACT(S) (210,000 OZ) |

| No of oz to be served (notices) | 431 contracts (2,155,000 oz) |

| Total monthly oz silver served (contracts) | 404 Contracts (2,020,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposits

total dealer deposit: nil oz

total dealer deposits: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We had 2 customer deposits

i) Into CNT: 602,621.060 oz

ii) Into Delaware 30,217.262

Total deposits: 632,838.322 oz

JPMorgan has a total silver weight: 141.307 million oz/273.370 million =51.57% of comex .//dropping fast

Comex withdrawals 0

total withdrawals: nil oz

adjustments: 1 all dealer to customer

i) Brinks 39,467.000 oz

TOTAL REGISTERED SILVER: 28.117 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 273.37 million oz

DEALER SILVER DROPPING FAST.

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE /2023 OI: 473 CONTRACTS HAVING LOST 261 CONTRACT(S).

WE HAD 303 NOTICES FILED YESTERDAY SO WE GAINED 42 CONTRACTS OR AN ADDITIONAL 210,000 OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF JUNE.

JULY HAD A 1918 CONTRACT LOSS TO 98,638 CONTRACTS

AUGUST REMAINS AT 2

SEPT HAS A GAIN OF 2393 CONTRACTS UP TO 24,281

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 42 for 210,000 oz

Comex volumes// est. volume today 60,902 fair/

Comex volume: confirmed yesterday: 82,220 EXCELLENT

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 404 x 5,000 oz = 2,020,000 oz

to which we add the difference between the open interest for the front month of JUNE(473) and the number of notices served upon today 42 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2023 contract month: 404 (notices served so far) x 5000 oz + OI for the front month of JUNE (473) – number of notices served upon today (42 )x 500 oz of silver standing for the JUNE contract month equates to 4.175 million oz +

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JUNE 2/WITH GOLD DOWN $24.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 938.11 TONNES

JUNE 1/WITH GOLD UP $14.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 939.56 TONNES

MAY 31/WITH GOLD UP $5.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 939.56 TONNES

MAY 30/WITH GOLD UP $14.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 26/WITH GOLD UP $.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 941.29 TONNES

MAY 25/WITH GOLD DOWN $19.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 24/WITH GOLD DOWN $9.50 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 941.29 TONNES

MAY 23/WITH GOLD $2.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 942.74 TONNES

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

MAY 9/WITH GOLD UP $9.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTER DEPOSIT OF 5.88 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 937.64 TONNES

MAY 8/WITH GOLD UP $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 931.77 TONNES

MAY 5/WITH GOLD DOWN $30.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AS DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

MAY 4/WITH GOLD UP $19.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.30 TONNES

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

GLD INVENTORY: 938.11 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 2/WITH SILVER DOWN 23 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV./INVENTORY RESTS AT 467.015 MILLION OZ/

JUNE 1/WITH SILVER UP 49 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.933 MILLION OZ

MAY 31/WITH SILVER UP 37 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 367,000 OZ FROM THE SLV////INVENTORY RESTS AT 467.933 MILLION OZ//

MAY 30/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 26/WITH SILVER UP $0.44 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.306 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 25.WITH SILVER DOWN $0.32 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 471.606 MILLION OZ//

MAY 24/WITH SILVER DOWN $.35 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 23/WITH SILVER DOWN 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

MAY 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A TINY DEPOSIT OF .08 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 465.682 MILLION OZ//

MAY 8/WITH SILVER DOWN 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.602 MILLION OZ//

MAY 5/WITH SILVER DOWN 31 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 466.876 MILLION OZ//

MAY 4/WITH SILVER UP 53 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF .174 MILLION OZ INTO SLV.//INVENTORY RESTS AT 467.174 MILLION OZ//

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

CLOSING INVENTORY 467.015 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

This is huge!! The bank may not be able to cover all of its deposits

(zerohedge)

Disgraced Silvergate Bank Hints It May Not Be Able to Cover All of Its Deposits; Fed Slaps It with a Cease and Desist Consent Order

By Pam Martens and Russ Martens: June 2, 2023 ~

Last week, on Tuesday, May 23, the Federal Reserve and California Department of Financial Protection and Innovation (the state banking regulator) hit the collapsed federally- insured bank, Silvergate Bank, and its parent, Silvergate Capital Corporation, with an enforcement action called a “Cease and Desist Consent Order.” The action was not announced to the public until yesterday.

A Consent Order is meant to function along the lines of a legal settlement, with the bank agreeing to the detailed terms of the Consent Order and waiving its right to judicial review. The individual signing the Consent Order on behalf of the bank was its controversial CEO, Alan Lane, who had allowed his federally-insured bank to get in bed with Sam Bankman-Fried’s house of frauds, including the FTX crypto exchange and Bankman-Fried’s hedge fund, Alameda Research. Lane also had allowed his deposit base to become heavily involved with other crypto-related companies.

When details of the Bankman-Fried relationship with Silvergate Bank came out in the news, a run on deposits commenced. On January 5, Silvergate reported in a filing with the Securities and Exchange Commission (SEC) that its “total deposits from digital asset customers declined to $3.8 billion” as of December 31, 2022 (down from the previously reported $11.9 billion on September 30, 2022.) That’s a 68 percent drop in deposits in one quarter.

The primary regulator of Silvergate Bank was, embarrassingly, the Federal Reserve, which had farmed out the examinations of the bank to the San Francisco Fed. The San Francisco Fed was also the primary supervisor for Silicon Valley Bank, which failed on March 10 and was put into FDIC receivership. (See our report: Silicon Valley Bank Was a Wall Street IPO Pipeline in Drag as a Federally- Insured Bank; FHLB of San Francisco Was Quietly Bailing It Out.)

Silvergate announced on March 8 that it was going to voluntarily wind down and liquidate itself. That announcement included this statement on its deposits: “The Bank’s wind down and liquidation plan includes full repayment of all deposits.” (We thought to ourselves at the time, do federal bank regulators really want to trust a bank with this dubious history to make its depositors whole?)

By March 29, Wall Street On Parade had serious questions about how Silvergate’s wind down and liquidation were proceeding. We wrote:

Silvergate Capital, the parent of Silvergate Bank – which has lost 90 percent of its share price year-to-date and announced it is winding down and liquidating — is still running a website that is putting a rosy glow on the bank’s operations. For example, under the heading of “Banking for the future,” the Silvergate website shares this:

“Silvergate Bank has served entrepreneurs in unique and niche industries for over 20 years. Recognizing digital currency’s potential during the sector’s infancy, we built strong relationships with pioneers who were turned away by traditional banks. This solidified our position as industry- leading partners and innovators which remains true today.”

On the date that we accessed the above statement on the public website of Silvergate Bank, it was a collapsing institution, its depositors in the digital currency field had mostly fled, and the bank was under an investigation by the U.S. Department of Justice. Adding to its troubles, Silvergate’s March 1 filing with the Securities and Exchange Commission indicated that record-keeping at the bank was in such shambles that it couldn’t even file its annual report for the full year of 2022 (Form 10-K) on time and it required more time to “record journal entries.”

Silvergate also noted in the SEC filing that “its independent registered public accounting firm” will require more time “to complete certain audit procedures, including review of adjustments not yet recorded and the evaluation of the effectiveness of the Company’s internal control over financial reporting.”

Last week, on May 22, Silvergate made another filing with the SEC, indicating that it has fired its independent public accounting firm, Crowe LLP, and won’t be filing any annual report for the year ended December 31, 2022 – ever. (Seriously, is this any way to garner public confidence in the U.S. banking system?)

But the most troubling SEC filing by Silvergate arrived on May 11, which likely freaked out the Fed and the Federal Deposit Insurance Corporation (FDIC) that insures deposits in U.S. banks. The filing included this statement, raising doubts about Silvergate Bank’s ability to make its depositors whole:

“As of May 9, 2023, the Company had cash and cash equivalents in excess of the amounts required to fully repay all remaining deposit liabilities of the Bank. However, the Company has potential contingent liabilities related to, among other things, the regulatory and other inquiries and investigations that are pending with respect to the Company and the Bank, the various litigation with respect to the Company (including private litigation) and other expenses to be incurred in connection with operating the Bank through the Bank Liquidation (including expenses necessary for the operation of the Company and/or the Bank, employee benefits and compensation and fees and expenses of professionals retained by the Company in connection with the Bank Liquidation) and is unable to quantify such amounts at this time.”

You are likely thinking, who (in their right mind) would still be maintaining deposits in this bank. It turns out that Silvergate was involved with brokered CDs and there may be folks out there who bought a federally-insured Certificate of Deposit from their brokerage firm and haven’t yet figured out that their CD is with this deeply-troubled, liquidating bank.

A notice on Silvergate’s website yesterday has this Q&A:

“Who do I contact if I have questions about my Certificate of Deposit (Brokered CD)?”

“Please contact your Broker. Brokered CDs will remain active until the maturity date, at which time they will be remitted according to the agreement.”

Silvergate Bank is being sued by multiple litigants over its involvement with Sam Bankman-Fried’s companies. There are going to be heavy litigation expenses. The most recent lawsuit comes from the Texas-based Word of God church.

According to the lawsuit, Word of God church lost $25 million of the deposits it placed with Bankman-Fried’s FTX, which it says were mishandled by Silvergate Bank. The lawsuit shares this:

“Silvergate Bank and Silvergate Capital Corporation (jointly, ‘Silvergate’), and their CEO, Alan Lane, are being sued for their role in the fraudulent scheme. Silvergate maintained both FTX and Alameda’s bank accounts and thus, had unparalleled knowledge of the rampant fraud and corporate malfeasance. Rather than flag, report, or investigate the suspicious activity, as required by federal banking regulations, Silvergate substantially assisted FTX by allowing FTX’s continued use of its services and processing new customer deposits and transfers. Silvergate further bolstered the legitimacy of FTX by consistently touting its enhanced due diligence processes, designed to weed out customers such as FTX engaging in fraud or other financial crimes…

“Plaintiff was one of millions of investors who fell victim to this scheme, losing $25,000,000 that it had deposited in an FTX bank account maintained by Silvergate just two months before the fraud was uncovered by the public….”

Given this background, it becomes clearer why the Fed felt it needed to get a Cease and Desist Consent Order signed by the CEO of Silvergate Bank. Among other things, the order requires the bank to:

Within 10 days, “submit a plan acceptable to the Supervisors that provides for the implementation of the Bank’s voluntary decision to self-liquidate and the orderly wind down of its operations”;

“The Self-Liquidation Plan shall be designed to protect the Bank’s depositors and the Deposit Insurance Fund to the fullest extent possible”;

“monetize and recover on its loans, securities, and other assets in a manner that prioritizes and protects depositors’ funds”;

“ensure that the books and records of the Bank are adequately maintained” – (that horse has, apparently, already left the barn);

“Effective immediately, the Company and the Bank shall preserve their respective cash assets and shall not dissipate those assets, including with respect to executive compensation and severance payments, without prior written approval from the Supervisors….”

On August 1 of last year, we penned this headline: Brace Yourself for Federally-Insured Bank Failures Caused by Crypto. We specifically discussed the problems at Silvergate Bank and Signature Bank. Silvergate Bank announced on March 8 its intention to liquidate; Signature Bank failed on March 12 and was put into FDIC receivership.

If we saw the dangers of letting crypto get anywhere near a federally-insured bank in August, why did federal banking regulators continue to allow these toxic combinations?

3,Chris Powell of GATA provides to us very important physical commentaries

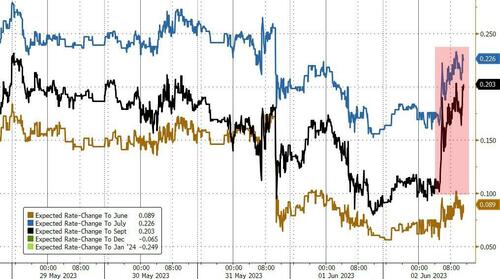

Seems that the Fed is signaling a pause in rate hikes

(Bloomberg News/GATA)

Fed signal for pause in rate hikes takes pressure off hot jobs report

Submitted by admin on Thu, 2023-06-01 10:02Section: Daily Dispatches

By Steve Matthews

Bloomberg News

Thursday, June 1, 2023

Federal Reserve officials are signaling that they plan to keep interest rates steady in June while retaining the option to hike further in coming months, steering market expectations ahead of a key employment report.

Governor Philip Jefferson, a centrist who is nominated to be vice chair and who often echoes Chair Jerome Powell’s views, said Wednesday that skipping an increase would give policymakers time to assess data but not preclude future tightening

That view undercuts the importance of the monthly jobs report, due Friday, which has often been viewed by Wall Street as a key data point swaying policy. After Jefferson spoke, investor bets for a hike at the June 13-14 Federal Open Market Committee plunged to about 35% Wednesday from nearly 60% a day earlier.

“I definitely think this was a signal” and “likely completely in sync with Chair Powell’s views,” said Rubeela Farooqi, chief U.S. economist at High Frequency Economics. “Just the response of market pricing makes it clear that the message is getting through.” …

… For the remainder of the report:

END

This is a must read over the weekend

Alasdair Macleod…

Alasdair Macleod: Sterling crisis ahead!

Submitted by admin on Thu, 2023-06-01 21:21Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, June 1, 2023

This article points to the factors driving sterling gilt yields higher. They are likely to lead to a sterling crisis as foreign selling gathers pace of gilts acquired since 2018.

Before interest rates began to rise, foreign buyers had enjoyed higher gilt prices which more than offset losses on sterling. That is no longer the case

Instead, there is growing disaffection with the Bank of England’s performance and perhaps a realisation that a general election in only 18 months’ time introduces political risk.

This article explains the consequences of denying Say’s law, otherwise known as the law of the markets, and by pursuing interest rate policies that have been disproved as a means of controlling inflation. Furthermore, it will be increasing shortages of bank credit that drive interest rates and bond yields higher, not central bank policies.

These are factors that affect all currencies allied to the dollar. The difference between the dollar and sterling is not so much to be found in broad policy dissimilarities but the lower levels of foreign confidence in sterling as a currency in uncertain times. …

… For the remainder of the report:

https://www.goldmoney.com/research/sterling-crisis-ahead?gmrefcode=gata

END

In 3 months, the city state of Singapore bought 69 tonnes of gold. They are heading for a huge 280 tonnes this year. Remarkable for a state of 4 million people

(Ronan Manly)

Ronan Manly: Singapore’s central bank is big — and secretive — gold buyer

Submitted by admin on Fri, 2023-06-02 09:29Section: Daily Dispatches

By Ronan Manly

Bullion Star, Singapore

Friday, June 2, 2023

Last year a major theme in the global gold market was the record gold buying by central banks across the world, with the World Gold Council and its data gatherers (Metals Focus) calculating that central banks had cumulatively purchased a net 1,136 tonnes of monetary gold during 2022.

At the outset of 2023, this led the World Gold Council to predict that:

“Looking ahead, we see little reason to doubt that central banks will remain positive towards gold and continue to be net purchasers in 2023.”

This indeed has proven to be the case, for after Q1 2023 drew to a close, the World Gold Council estimated that in the first quarter of 2023, the world’s central banks had again been net buyers of gold to the tune of a combined 228 tonnes. This is the strongest first quarter of central bank gold buying on record.

And the central bank leading the pack in this gold accumulation has been none other than BullionStar’s neighbour, the Monetary Authority of Singapore (MAS), whose headquarters are literally a short 2-kilometer stroll from Bullion Star’s shop and showroom in Singapore’s central business district.

For in the space of three months between January and March 2023, Singapore’s central bank has quietly bought an incredible 68.7 tonnes of gold, making Singapore the world’s leading sovereign gold buyer for the first quarter of 2023, even ahead of China. …

… For the remainder of the analysis:

end

The world continues its backlash against a weaponized USA dollar

(Bloomberg/GATA)

Backlash against weaponized dollar is growing across the world

Submitted by admin on Fri, 2023-06-02 09:15Section: Daily Dispatches

Michelle Jamrisko and Ruth Carson

Bloomberg News

via Yahoo News, Sunnyvale, California

Friday, June 2, 2023

All around the world, a backlash is brewing against the hegemony of the US dollar.

Brazil and China recently struck a deal to settle trade in their local currencies, seeking to bypass the greenback in the process. India and Malaysia in April signed an accord to ramp up usage of the rupee in cross-border business. Even perennial US ally France is starting to complete transactions in yuan.

Currency experts are leery of sounding like the Cassandras who have, embarrassingly, predicted the dollar’s imminent demise on any number of occasions over the past century. And yet in observing this sudden wave of agreements aimed at sidestepping the dollar, they detect the sort of meaningful action, however small and gradual, that was typically missing in the past.

For many global leaders, their rationales for taking these measures are strikingly similar. The greenback, they say, is being weaponized, used to push America’s foreign-policy priorities — and punish those that oppose them. …

… For the remainder of the report:

https://finance.yahoo.com/news/putin-war-ignites-backlash-against-040100975.html

end

END

4, OTHER IMPORTANT GOLD COMMENTARIES/

ANDREW MAGUIRE/LIVE FROM THE VAULT/125

https://kinesis.money/live-from-the-vault/chinas-gold-rush/

Episode 125

1 day ago

China’s gold rush – Xi prepares for “Worst case scenarios”

In this week’s episode of Live from the Vault, Andrew Maguire discusses the latest market catalysts that are capable of triggering a global gold reevaluation event, as a result of the ongoing paper versus physical gold showdown.

The precious metals expert delves into the underreported decision of the People’s Bank of China to start preparing its 1.4 billion citizens for opting out of the dollar and into gold, explaining how this will impact gold’s supply, demand and price.

END

5.IMPORTANT COMMENTARIES ON COMMODITIES:

END

5 B GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.0632

OFFSHORE YUAN: 7.0801

SHANGHAI CLOSED UP 25.43 PTS OR 0.79%

HANG SENG CLOSED UP 733.03 PTS OR 1.02%

2. Nikkei closed UP 733,03 PTS OR 1.02%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 103.50 EURO RISES TO 1.0763 UP 3 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.409 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 138.95 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN// OFF- SHORE:DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.2815***/Italian 10 Yr bond yield FALLS to 3.981*** /SPAIN 10 YR BOND YIELD FALLS TO 3.304…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 3.65

3j Gold at $1979.00 silver at: 23.87 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 16 /100 roubles/dollar; ROUBLE AT 80.91//

3m oil into the 71 dollar handle for WTI and 73 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 138.95 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .409% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9062 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9754 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.612 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 3.832 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.341 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 20.89…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.1600 UP 4 BASIS PTS (RATES RISING RAPIDLY)

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Jump After Senate Passes Debt Deal, China Plans New Stimulus Package

FRIDAY, JUN 02, 2023 – 07:57 AM

US Futures extended yesterday’s rally after the Senate passed a bill late on Thursday to raise the debt ceiling and prevent a US default, with risk-on sentiment getting a boost following the sharpest rally in Chinese stocks for three months amid Bloomberg reports that China is mulling a new stimulus package to support the property market after existing policies failed to sustain a rebound in the ailing sector.

At 7:45am, S&P futures rose 0.5% to 4249, while the Nasdaq rose by 0.6% and was set for a sixth straight weekly advance. Europe’s Stoxx Europe 600 index followed Asian benchmarks higher, with luxury-goods makers LVMH and Richemont among the leading gainers after the China stimulus report. Treasury yields were little changed, diverging from higher rates in Europe and the UK. Oil and bitcoin both gained more than 1%, while gold was little changed after three days of gains.

In premarket trading, US-listed Chinese stocks extended a rally after Bloomberg News reported that regulators are considering a new basket of measures to boost the property market. Broadcom shares fell as the chipmaker remains mired in a broader slowdown. While the company talked up the potential boost from artificial intelligence, it wasn’t enough to sustain recent gains for the stock, which jumped nearly 30% last month. Dell Technologies also fell after the personal-computer maker gave a lukewarm sales outlook indicating that a recovery may take a bit longer than expected as it continues to struggle to sell PCs, particularly to consumers. Here are some other notable premarket movers:

- Lululemon shares surged after the athletic- apparel brand reported first-quarter net revenue that beat estimates. Analysts say the results were better than feared, highlighting the brand’s strong guest metrics as well as growth in China.

- MongoDB shares soared, with analysts positive on the database software company after it reported first-quarter results that beat expectations and raised its full-year forecast. Citi says the outlook “could signal a faster recovery in the consumption trends of the business, potentially driven by GenAI tailwinds.”

- SentinelOne shares slumped after the software company cut its year revenue guidance. “Macroeconomic pressures continue to impact deal sizes, sales cycles, and pipeline conversion rates,” the company wrote in a letter to shareholders.

Tech giants are still driving most of the stock market’s advance, with Apple nearing a record and Nvidia. climbing more than 5% Thursday; both were set for more gains today. The sector attracted record inflows last week, Bank of America said. Aside from the obsession for anything AI-related that drove megacaps up 17% in May, the industry also got a boost from wagers the Fed will stop raising interest rates.

Late on Thursday, the Senate voted 63-36 to pass the US debt ceiling bill, which sends it to President Biden’s desk. Biden said he wants to thank Senate leaders Schumer and McConnell for quickly passing the debt ceiling bill and noted that the bipartisan agreement is a big win for the economy, while he looks forward to signing the bill ASAP and directly addressing Americans on Friday. The White House announced that President Biden is to deliver an address on averting a default and the bipartisan budget agreement according to Reuters.

Today, all eyes will be on the NFP print at 8:30am (see our preview here). Consensus expects NFP to print 195k with the whisper number higher at 225k (vs. 253k prior) and the Unemp rate to rise to 3.5%, vs. 3.4% prior; focus also on average hourly earnings data which is expected to rise 0.3% MoM. Traders are betting that the jobs report will show enough moderation in the pace of hiring to allow the Fed to pause its tightening cycle, helping sustain the rally. Dovish comments from Fed officials supported this view: Fed Bank of Philadelphia President Patrick Harker said “we should at least skip this meeting in terms of an increase,” and his St. Louis counterpart James Bullard said interest rates may already be sufficiently restrictive to bring down inflation.

“The more pertinent Fed speakers have suggested a June pause is more likely and I don’t think non-farms payrolls should change that view meaningfully,” said James Athey, investment director at Abrdn. “Therefore I think the risks are skewed to a dovish disappointment this afternoon.”

According to Goldman trading desk, a print sub 100k likely hits the tape by ~100bps and a print north of 375k hits the tape by 25 – 50bps.

In Europe, the Stoxx Europe 600 index was up 1% and on course for back-to-back gains for the first time in two weeks, following Asian benchmarks higher, with luxury-goods makers LVMH and Richemont among the leading gainers after Bloomberg reported that China is considering new stimulus measures. Miners and energy companies climbed as crude oil and industrial metals rebounded. Among individual movers in Europe, sportswear makers Puma SE and Adidas AG rose more than 4% each after Lululemon Athletica Inc.’s robust results. Dechra Pharmaceuticals Plc jumped after EQT AB made a firm offer for the UK veterinary drugmaker. Embattled Swedish landlord SBB soared as it attracted interest from investors including Brookfield Asset Management. Here are some other notable movers.

- Addnode shares gain as much as 11% after the Swedish IT services group announced it would acquire US firm Team D3 for up to $59m. Handelsbanken says the price tag looks “almost worryingly attractive”

- Diageo shares underperformed its peers Friday, with analysts seeing the UK alcoholic beverage maker’s capital markets day as failing to dispel uncertainty about its outlook, with Citi noting a lack of clarity

The MSCI Asia-Pacific Index jumped as much as 2.1% Friday, poised for its biggest weekly advance since late January as Chinese tech stocks fuel big gains in Hong Kong benchmarks. Biggest contributors to gauge’s climb are Tencent and Alibaba, which jump more than 5% each. Hang Seng Tech Index spikes as much as 5.7%; other Hang Seng benchmarks rally at least 4% Shares in Japan, Australia, China advanced while South Korea’s Kospi index was headed for bull market territory following a gain of more than 20% from a low in September. Hong Kong’s Hang Seng index rose more than 3%, pulling the benchmark back from the brink of a bear market following concerns about Chinese growth.

The bullish sentiment emerged amid reports that China is working on a new basket of measures to support the property market after existing policies failed to sustain a rebound in the ailing sector, Bloomberg reported Friday. The yuan extended gains and crude oil rose along with industrial metals. An index of emerging-market stocks soared the most since January.

In FX, the Bloomberg Dollar Spot Index eased for a second day as traders are betting that the monthly US jobs report will show enough moderation in the pace of hiring to allow the Fed to pause its tightening cycle. Money markets now assign a three-in- four chance of a 25 basis-point hike next month. Supporting that view, Fed Bank of Philadelphia President Patrick Harker said “we should at least skip this meeting in terms of an increase,” and his St. Louis counterpart James Bullard said interest rates may already be sufficiently restrictive to bring down inflation. Dollar weakness also gained traction after a report that China is working on a new basket of measures to support its property market.

- TheAussie rose as much as 1% against the dollar after industrial relations umpire boosted the national minimum wage by 5.75%, a decision that increased the chances of an interest-rate increase as soon as next week

- Short-covering against the yen topped out around 139.00 option strikes, according to traders

- The pound was up 0.1% to $1.2533, set for a sixth day of gains for the first time since December; currency is up 1.5% this week, the biggest advance this year

In rates, treasuries were slightly cheaper across the curve as S&P 500 futures gain; Treasury yields cheaper by 0.5bp to 2bp across the curve with 2s10s, 5s30s spreads steeper by 1bp and 0.5bp as front-end slightly outperforms; 10-year yields around 3.61% with bunds, gilts cheaper by 3bp and 1bp in the sector. US session focus switches to data, with the May jobs report scheduled for 8:30am New York.

In commodities, crude futures advance with WTI rising 1.9% to trade near $71.45. Spot gold is little changed around $1,980. Bitcoin rises 1%

Looking to the day ahead now, and the main highlight will be the US jobs report for May. Otherwise, data releases include French industrial production for April. And from central banks, we’ll hear from the ECB’s Vasle.

Market Snapshot

- S&P 500 futures up 0.4% to 4,244.25

- MXAP up 2.0% to 162.70

- MXAPJ up 2.2% to 513.59

- Nikkei up 1.2% to 31,524.22

- Topix up 1.6% to 2,182.70

- Hang Seng Index up 4.0% to 18,949.94

- Shanghai Composite up 0.8% to 3,230.07

- Sensex up 0.4% to 62,663.00

- Australia S&P/ASX 200 up 0.5% to 7,145.14

- Kospi up 1.3% to 2,601.36

- STOXX Europe 600 up 0.7% to 458.52

- German 10Y yield little changed at 2.28%

- Euro little changed at $1.0771

- Brent Futures up 0.7% to $74.80/bbl

- Gold spot down 0.0% to $1,977.49

- U.S. Dollar Index down 0.10% to 103.46

Top Overnight News

- China is working on a new basket of measures to support the property market after existing policies failed to sustain a rebound in the ailing sector, according to people familiar with the matter. BBG

- South Korea’s CPI cools to 19-month low, coming in at +3.3% Y/Y in May (down from +3.7% in April and below the Street’s +3.4% forecast). RTRS

- Australia’s industrial relations umpire raised the national minimum wage by 5.75% in an effort to support low-paid workers, a decision that boosted the chances of an interest-rate increase as soon as next week. BBG

- The UN food price index for May fell 2.6% M/M and is now off 22.1% from the all-time high hit in March of 2022. UN

- The Senate passed wide-ranging legislation Thursday that suspends the $31.4 trillion debt ceiling while cutting federal spending, backing a bipartisan deal struck by President Biden and House Speaker Kevin McCarthy to avert an unprecedented U.S. default. WSJ

- Consensus for payrolls this AM is +195k headline print (vs +253k prior, GIR +175k), AHE MoM .3% (vs .5% prior, GIR +.25%) & U/E 3.5% (vs 3.4% prior, GIR 3.4%). We are finally back in a good employment data is good for stocks set up with goldilocks zone for headline print at +175k to +250k (anything in here should keep today’s rally going). A print sub 100k likely hits the tape by ~100bps and a print north of 375k hits the tape by 25 – 50bps. GS GBM

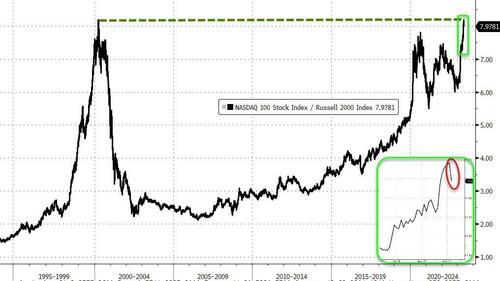

- The buzz around AI has investors pouring a record amount of money into tech stocks, with the Nasdaq 100 Index now at an all-time high relative to the Russell 2000 small-cap index. A “baby bubble” in AI was the dominant market theme in May, with tech funds attracting a high of $8.5 billion in the week through May 31, he said, citing EPFR Global data. BBG

- Brookfield is said to be among investors in early stage talks to evaluate SBB’s real estate portfolio (European real estate rallying sharply in sympathy). RTRS

- Broadcom said sales tied to AI will double this year but will be overshadowed by a wider slowdown. Chip revenue from companies building out their AI capabilities may grow to $1 billion per quarter. Broadcom’s total revenue is expected to rise less than 5% this quarter, its slowest in years. The shares dipped. BBG

- The average rate on the standard 30-year fixed mortgage rose to 6.79%, according to a survey of lenders released Thursday by mortgage-finance giant Freddie Mac. That is the highest level since this past fall, when mortgage rates briefly topped 7% for the first time in two decades. The near-quarter percentage point increase from a week ago was the largest jump since October. Mortgage rates remain sharply above their roughly 5% level a year ago. That and elevated home prices have kept many potential home buyers on the sidelines. WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded higher as the region took impetus from Wall St where the S&P 500 and Nasdaq climbed to 9-month highs amid debt ceiling optimism, falling labour costs and dovish Fed commentary. ASX 200 was positive with the index led higher by the mining sector and after the Australian Fair Work Commission raised the minimum wage by 5.75%, although gains were capped by weakness in financials and after recent upward revisions to banks’ forecasts on the RBA’s peak rate. Nikkei 225 was underpinned amid comments from BoJ Governor Ueda who stuck to the dovish script, with SoftBank among the biggest gainers following a buy rating from Jefferies and as the Co. benefits from the recent AI tech bid in the build-up to the ARM IPO. Hang Seng and Shanghai Comp. conformed to the broad upbeat mood with Hong Kong significantly outperforming amid a rally in property and tech.

Top Asian News

- China is reportedly mulling a property-market support package to bolster the economy, according to Bloomberg sources. Regulators are said to be considering reducing the down payment in some non-core neighbourhoods of major cities, alongside lowering agent commissions on transactions, and further relaxing restrictions for residential purchases under the guidance of the State Council, according to sources. China is working on a new basket of measures to support the property market after existing policies failed to sustain a rebound.

- US President Biden said the US does not seek conflict in competition with China and the countries should work together where they can.

- BoJ Governor Ueda said premature tightening could hurt companies even in good health and may weaken the economy’s potential, while he said patiently maintaining easy policy would heighten Japan’s potential growth in the long run. Ueda also stated it is not time yet to debate a specific exit strategy including the possible sale of the BoJ’s holdings of J-REITs and the BoJ will maintain massive monetary easing as it will take more time to achieve the price target, according to Reuters.

Top European News

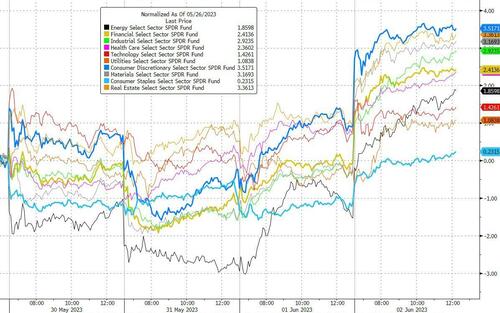

- European equities trade on the front foot following the Senate passage of the debt ceiling bill. Despite the positivity during today’s session, the negativity earlier in the week means that the Stoxx 600 is on track to close the week out with losses of around 0.8%.

- Equity sectors in Europe are higher across the board (ex-healthcare) with Real Estate names top of the leaderboard followed by Basic Resources and Consumer Products & Services. Luxury names also benefit from gains in the sector overnight.

- US equity futures see gains but to a lesser magnitude compared to European peers ahead of the US jobs report.

Debt Ceiling news

- US Senate voted 63-36 to pass the US debt ceiling bill, which sends it to President Biden’s desk.

- US President Biden said he wants to thank Senate leaders Schumer and McConnell for quickly passing the debt ceiling bill and noted that the bipartisan agreement is a big win for the economy, while he looks forward to signing the bill ASAP and directly addressing Americans on Friday. Furthermore, the White House announced that President Biden is to deliver an address on averting a default and the bipartisan budget agreement at 19:00EDT/00:00BST, according to Reuters.

FX

- DXY oscillates in a tight range on either side of 103.50 ahead of the US jobs report, whilst the debt ceiling bill makes its way to President Biden after passing through the Senate.

- Yuan is firmer on reports China is reportedly mulling a property-market support package to bolster the economy as existing policies failed to sustain a rebound.

- Yen saw its revival thwarted by firmer US Treasury yields whilst also taking on board more dovish comments from the BoJ governor,

- Euro and Sterling are flat against the Dollar around 1.0770 and 1.2530 respectively in a quiet morning.

- Aussie outperforms amid a rebound in base metal prices ahead of the RBA policy announcement next week.

- PBoC set USD/CNY mid-point at 7.0939 vs exp. 7.0958 (prev. 7.0965)

Fixed Income

- Debt futures are observing caution in the run-up to NFP that crowns a holiday-shortened week.

- Bunds are losing further traction from 136.00 following an opening 136.36 Eurex print.

- Gilts trades around 97.00 and T-note is closer to 114-19+ overnight trough than 114-24+ peak

Commodities

- WTI and Brent front-month futures are on a firmer footing as the complex holds onto yesterday’s data-driven upside with further tailwinds seen following reports China is looking to further boost its property sector.

- Spot gold is flat around the USD 1,975/oz mark after meeting resistance at its 21 DMA (1,983.77/oz) overnight, with eyes on the US jobs report.

- Base metals are firmer across the board, bolstered by the risk appetite coupled with stimulus hopes from China.

Geopolitics

- South Korea and the US issued a joint cybersecurity advisory against North Korean hacking group Kimsuky and stated that North Korea is engineering cyberattack campaigns targeting think tanks, academia and news outlets, while South Korea issued new independent sanctions on the North Korean hacking group, according to the South Korean Foreign Ministry cited by Reuters.

- North Korea denounced the US Secretary-General over condemning its satellite launch and said it will continue to exercise its sovereign rights including the military spy satellite launch, according to KCNA.

- UN spokesman is concerned about the continuous slowdown in implementing the Black Sea grain initiative and noted that a slowdown was observed particularly in April and May.

- White House National Security Adviser Sullivan hosted Israel’s National Security Advisor and Minister of Strategic Affairs, while the officials continued discussions on enhanced coordination to prevent Iran from acquiring a nuclear weapon, according to Reuters.

- Chinese Eurasian Affairs Envoy said ‘fruitful’ talks on Ukraine may be difficult, according to Reuters.

US Event Calendar

- 08:30: May Change in Nonfarm Payrolls, est. 195,000, prior 253,000

- 08:30: May Change in Private Payrolls, est. 165,000, prior 230,000

- 08:30: May Change in Manufact. Payrolls, est. 5,000, prior 11,000

- 08:30: May Unemployment Rate, est. 3.5%, prior 3.4%

- 08:30: May Labor Force Participation Rate, est. 62.6%, prior 62.6%

- 08:30: May Average Weekly Hours All Emplo, est. 34.4, prior 34.4

- 08:30: May Average Hourly Earnings YoY, est. 4.4%, prior 4.4%

- 08:30: May Average Hourly Earnings MoM, est. 0.3%, prior 0.5%

DB’s Jim Reid concludes the overnight wrap

Markets recovered their poise over the last 24 hours, with the S&P 500 (+0.99%) closing at a 9-month high. That’s been driven by several factors, including the passage of the debt ceiling deal through Congress, the prospect that the Fed might finally pause their rate hikes at the next meeting, along with further signs that inflation is still falling. All this meant that June kicked off with a decent cross-asset rally, and sovereign bonds and commodities also moved higher after a fairly rough performance back in May.

The next test for markets will come with today’s US jobs report, which is one of the last big data releases ahead of the Fed’s next decision on June 14. For what it’s worth, markets have been consistently taken by surprise by the jobs report over recent months, and the last 13 in a row have all seen the initial release for nonfarm payrolls beat the Bloomberg consensus forecast on the day. In terms of what to expect, our US economists are looking for a +200k increase in payrolls (vs. +195k consensus), so slightly above consensus once again. In turn, that would see the unemployment rate tick up a tenth to 3.5%, having come in at a 53-year low of 3.39% last month if you look to two decimal places. See more from our US economists here.

Ahead of that jobs report, yesterday brought a collection of robust data releases on the US labour market. First, the ADP’s report of private payrolls rose by +278k in May (vs. +170k expected), which was above every economist’s forecast on Bloomberg. Second, the weekly initial jobless claims came in at 232k over the week ending May 27 (vs. 235k expected), which took the 4-week moving average down to an 11-week low of 229.5k. And third, although the latest ISM manufacturing reading remained in contractionary territory at 46.9 (vs. 47.0 expected), the employment component ticked up to a 9-month high of 51.4. This good news wasn’t just confined to the US either, since the Euro Area unemployment rate fell to its lowest since the formation of the single currency in April, at 6.5%.

Alongside those positive signals on the labour market, markets also received some good news on inflation too. In the Euro Area, the flash CPI estimate for May fell to a 15-month low of +6.1% (vs. +6.3% expected), and core inflation was down for a second month running to +5.3% (vs. +5.5% expected). And in the US, the prices paid component of the manufacturing ISM was far beneath expectations at 44.2 (vs. 52.3 expected).

Markets then got some further momentum by fresh support for the Fed pausing their cycle of rate hikes at the next meeting. That came from Philadelphia Fed President Harker, who said that “we should at least skip this (June) meeting in terms of an increase” and that “we are close to the point where we can hold rates in place”. As a result, investors further dialled back the chances of a June rate hike, which were down to 23% by yesterday’s close, having been as high as 69% at the close last Friday. We did hear from St Louis Fed President Bullard as well, one of the hawks on the committee, who published an updated analysis suggesting that policy rates are “now at the low end of what is arguably sufficiently restrictive”.