SEPT 5/UNITED STATES WEAPONIZES THE DOLLAR AGAIN CAUSING OUR PRECIOUS METALS TO BE WHACKED AGAIN: GOLD CLOSED DOWN $13.50 TO $1940.70/SILVER CLOSED DOWN 69 CENTS TO $23,54/PLATINUM CLOSED DOWN $32.26 TO $933.35 WHILE PALLADIUM FINISHED THE DAY DOWN $10.00 TO $1220.60//GOOD COMMENTARY TODAY BY MATHEW PIEPENBERG//UKRAINE VS RUSSIA: HUNGARY BLOCKS THE LATEST EU ROUND OF MONEY TO UKRAINE//HUGE IMPORTS OF ELECTRICITY INTO GERMANY//NEW LNG AUSTRALIAN STRIKES THREATENS THE EU//COVID UPDATES/VACCINE UPDATES//DR PAUL ALEXANDER//SLAY NEWS/EVOL NEWS/NEWS ADDICTS//SWAMP STORIES FOR YOU TONIGHT//

118 C MACQUARIE FUT 76 132 C SG AMERICAS 5 323 H HSBC 32 363 H WELLS FARGO SEC 18 435 H SCOTIA CAPITAL 18 624 H BOFA SECURITIES 46 657 C MORGAN STANLEY 1 661 C JP MORGAN 20 2 686 C STONEX FINANCIA 1 690 C ABN AMRO 1 726 C CUNNINGHAM COM 2 737 C ADVANTAGE 26 10

TOTAL: 129 129 MONTH TO DATE: 3,544

JPMorgan stopped 2 /128 contracts.

FOR SEPT.:

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2023. CONTRACT: 128 NOTICES FOR 12,800 OZ or .3981 TONNES

total notices so far: 3544 contracts for 354,400 oz (11.0245 tonnes)

FOR SEPT:

SILVER NOTICES: 132 NOTICE(S) FILED FOR 660,000 OZ/

total number of notices filed so far this month : 2283 for 11,415,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $13.50

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/SMALL CHANGES IN GOLD INVENTORY AT THE GLD: / A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 890.97 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 69 CENTS AT THE SLV// SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.734 MILLION OZ OZ SILVER OUT OF THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 437.891 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG 768 SIZED 289 CONTRACTS TO 129,988 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS STRONG SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.20 LOSS IN SILVER PRICING AT THE COMEX ON FRIDAY. TAS ISSUANCE WAS A STRONG SIZED 629 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON FRIDAY NIGHT: 629 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.20). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER CONTRACTS AS WE HAD A SMALL SIZED LOSS OF 193 CONTRACTS ON BOTH EXCHANGES ALONG WITH HUGE T.A.S.LIQUIDATION THROUGHOUT THE COMEX SESSION.

WE MUST HAVE HAD:

A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 575 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 14.420 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 35,000 OZ//NEW TOTAL 12.385 MILLION OZ/// / //SMALL SIZED COMEX OI LOSS/ STRONG SIZED EFP ISSUANCE/VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE (629CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL 193 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTRACTS for 2 days, total 1345 contracts: OR 6.725 MILLION OZ (673 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 3.850 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 6.725 MILLION OZ

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 768 CONTRACTS WITH OUR LOSS IN PRICE OF $0.20 IN SILVER PRICING AT THE COMEX//FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG EFP ISSUANCE CONTRACTS: 575 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR SEPT OF 14.420 MILLION OZ FOLLOWED BY TODAY’S 35,000 OZ E.F.P. TO LONDON /// WE HAVE A SMALL LOSS OF 193 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG 629 CONTRACTS//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE FRIDAY COMEX SESSION . THE NEW TAS ISSUANCE FRIDAY NIGHT (629) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 132 NOTICE(S) FILED TODAY FOR 660,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2763 CONTRACTS TO 439,880 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: 766 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 1763 CONTRACTS) DESPITE OUR $1,00 GAIN IN PRICE//FRIDAY. WE ALSO HAD A RATHER STRONG INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 12.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 4300 OZ QUEUE JUMP//NEW TOTAL STANDING 13.530 TONNES + /A SMALL (AND CRIMINAL) ISSUANCE OF 868 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH OUR$1.00 GAIN IN PRICEWITH RESPECT TO FRIDAY’S TRADING.WE HAD A FAIR SIZED LOSS OF 1597 OI CONTRACTS (4.967 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1166CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 440,646

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 831 CONTRACTS WITH 1997 CONTRACTS DECREASED AT THE COMEX// AND A FAIR 1166 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 831CONTRACTS OR 2.584 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL 868 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1166 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2763) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 1597 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 12.656 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 4300 OZ/// 3) ZERO LONG LIQUIDATION WITH CONSIDERABLE TAS LIQUIDATION DURING THE COMEX SESSION //4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: SMALL T.A.S. ISSUANCE: 868 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT :

TOTAL EFP CONTRACTS ISSUED: 5865 CONTRACTS OR 586,500 OZ OR 18.242 TONNES IN 2TRADING DAY(S) AND THUS AVERAGING: 2932 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY(S) IN TONNES 18.242 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 18.242/3550 x 100% TONNES 0.507% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 18.242 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A STRONG SIZED 768 CONTRACTS OI TO 129,988 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A STRONG 575 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 575and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 575 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 289 CONTRACTS AND ADD TO THE 575 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 193 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 0.965 MILLION OZ

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED DOWN 22.69 PTS OR 0.69% //Hang Seng CLOSED DOWN 387.25 PTS OR 2.06% /The Nikkei CLOSED UP 97.55 PTS OR 0.30% //Australia’s all ordinaries CLOSED DOWN 0.12 % /Chinese yuan (ONSHORE) closed DOWN 7.3070 /OFFSHORE CHINESE YUAN DOWN TO 7.3080 /Oil UP TO 85.26 dollars per barrel for WTI and BRENT UP AT 88.36 / Stocks in Europe OPENED ALL MOSTLY RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2763CONTRACTS TO 439,880 WITH OUR GAIN IN PRICE OF $1,00 ON FRIDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1166 EFP CONTRACTS WERE ISSUED: : DEC 1166 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1166 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR TOTAL OF 1597 CONTRACTS IN THAT 1166LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 2763 COMEX CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR GAIN IN PRICE OF $1,00//FRIDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY NIGHT WAS A SMALL 831 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: SEPT (13.530) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 13.530 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $1.00) //// BUT WERE SUCCESSFUL IN KNOCKING A FEW SPECULATOR LONGS AS WE HAD A FAIR LOSS OF 1597 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE T.A.S. LIQUIDATION ON THE FRONT END OF FRIDAY’S TRADING. THE T.A.S. ISSUED ON FRIDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 4.967 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPT. (12.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 4300 OZ//NEW STANDING 13.530 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $1.00.

WE HAD – REMOVED 766 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET LOSS ON THE TWO EXCHANGES 1597 CONTRACTS OR 159,700 OZ OR 4,967 TONNES.

Estimated gold volume today:// 190,793 poor

final gold volumes/yesterday 169,880 awful//speculators have left the gold arena

Total monthly oz gold served (contracts) so far this month

3544 notices 354400 OZ 11.0245 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 0

total customer deposits: nil oz

we had 1 customer withdrawals

i) Out of Brinks: 1318.19o 41 KILOBARS

total withdrawals 1318.190 oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPTEMBER.

For the front month of SEPTEMBER we have an oi of 934 contracts having LOST 638 contracts. We had

681 contracts were served on FRIDAY, so we gained an additional 43 CONTRACTS or AN ADDITIONAL 4300 oz will stand for delivery in this non active

delivery month of Sept.

Oct lost 954 contracts to 28,106 contracts.

December LOST 1642 contracts down to 378,385 contracts.

We had 128 contracts filed for today representing 12,800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 20 notices were issued from their client or customer account. The total of all issuance by all participants equate to 128 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 2 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2023. contract month,

we take the total number of notices filed so far for the month (3544 x 100 oz ), to which we add the difference between the open interest for the front month of SEPT (934 CONTRACTS) minus the number of notices served upon today 128 x 100 oz per contract equals 435,000 OZ OR 13.530 TONNES the number of TONNES standing in this non active month of SEPT.

thus the INITIAL standings for gold for the SEPTcontract month: No of notices filed so far (3544) x 100 oz + (934) {OI for the front month} minus the number of notices served upon today (128) x 100 oz) which equals 435,000 oz standing OR 13.530 TONNES

TOTAL COMEX GOLD STANDING: 13.530 TONNES WHICH IS HUGE FOR AN INACTIVE DELIVERY MONTH.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,388,420.269 OZ

TOTAL REGISTERED GOLD 10 ,853.948.876 (337.60 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,534,471.393 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,843,355 OZ (REG GOLD- PLEDGED GOLD) 275.06 tonnes//dropping like a stone

END

SILVER/COMEX

SEPT 5

//2023// THE SEPT 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

530,308,190 oz Brinks CNT

.

Deposits to the Dealer Inventory

nil

Deposits to the Customer Inventory

601,725.160 oz CNT Delaware

No of oz served today (contracts)

132 CONTRACT(S) (660,000 OZ)

No of oz to be served (notices)

194 contracts (970,000 oz)

Total monthly oz silver served (contracts)

2283 Contracts (11,415,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposits customer account:

i) Into CNT 600,759.000 oz

ii) Into Delaware 966.16 oz

total customer deposits: 601,725.160 oz

JPMorgan has a total silver weight: 138.666 million oz/278.377.218 million = 50.00% of comex .//

Comex withdrawals 2

i) Out of Brinks 63,295.06 oz

ii) Out of CNT 467,013.130 oz

total 503,308.190 oz

adjustments: 0

TOTAL REGISTERED SILVER: 44.350 MILLION OZ//.TOTAL REG + ELIGIBLE. 278.377 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR August:

silver open interest data:

FRONT MONTH OF SEPT /2023 OI: 326 CONTRACTS HAVING LOST 295 CONTRACT(S). WE HAD 288

CONTRACTS SERVED ON FRIDAY. SO WE LOST AGAIN 7 CONTRACTS OR 35,000 OZ WERE IMMEDIATELY E.F.P’d TO LONDON AS THERE WAS NO METAL OVER HERE FOR THESE GUYS.

OCT GAINED 1 CONTRACTS TO STAND AT 1146.

NOVEMBER GAINED ITS FIRST 5 CONTRACTS TO STAND AT 5

DEC. LOST 744 CONTRACTS TO STAND AT 117,840 .

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 132 for 660,000 oz

Comex volumes// est. volume today 89,601 strong

Comex volume: confirmed yesterday 63,844. poor

To calculate the number of silver ounces that will stand for delivery in SEPT. we take the total number of notices filed for the month so far at 2283 x 5,000 oz = 11,415,000 oz

to which we add the difference between the open interest for the front month of SEPT (326) and the number of notices served upon today 132x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT/2023 contract month: 2283 (notices served so far) x 5000 oz + OI for the front month of SEPT (326) – number of notices served upon today (132 )x 500 oz of silver standing for the SEPT contract month equates to 12.385 million oz.

There are 44.350 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

SEPT 5/WITH GOLD DOWN $13.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.97 TONNES

SEPT 1/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 31/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 30/WITH GOLD UP $8.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.59 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.23 TONNES

AUGUST 29/WITH GOLD UP 17.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.6 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.64 TONNES

AUGUST 28/WITH GOLD UP $6.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / //INVENTORY RESTS AT 884.04 TONNES

AUGUST 25/WITH GOLD DOWN $6.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 884.04 TONNES

AUGUST 24/WITH GOLD UP $0.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //INVENTORY RESTS AT 884.91 TONNES

AUGUST 23/WITH GOLD UP $21.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 4.32 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 884.91 TONNES

AUGUST 22/WITH GOLD UP $2.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.87 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 889.23 TONNES

AUGUST 21/WITH GOLD UP $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.60 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 890.10 TONNES

AUGUST 18/WITH GOLD UP $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 6.92 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 887.50 TONNES

AUGUST 17/WITH GOLD DOWN $12.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 16/WITH GOLD DOWN $7.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 15/WITH GOLD DOWN $7,45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 895.87 TONNES

AUGUST 14/WITH GOLD DOWN $2.10 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.75 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 899.63 TONNES

AUGUST 11/WITH GOLD DOWN $2.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 903.31 TONNES

AUGUST 10/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 9/WITH GOLD DOWN $8.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 8/WITH GOLD DOWN $9.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES FORM THE GLD /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 7/WITH GOLD DOWN $5.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 906.00 TONNES

AUGUST 4/WITH GOLD UP $7.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.18 TONNES OF GOLD FROM THE GLD/// .///INVENTORY RESTS AT 906.00 TONNES

AUGUST 3/WITH GOLD DOWN $5.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 2/WITH GOLD DOWN $3.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.75 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 1/WITH GOLD DOWN $28.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 31/WITH GOLD UP $9.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 28/WITH GOLD UP $14.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 915,82 TONNES

JULY 27/WITH GOLD DOWN $21.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 917.26 TONNES

JULY 26/WITH GOLD UP $6.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 25/WITH GOLD UP $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 24/WITH GOLD DOWN $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.20 TONNES OF GOLD INTO THE GLD//: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

GLD INVENTORY: 890.97 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 5/WITH SILVER DOWN 69 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 734,000 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 437.891 MILLION OZ

SEPT 1/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 440.00 MILLION OZ

AUGUST 31/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 438.625 MILLION OZ

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.834 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 443.210 MILLION OZ

AUGUST 29/WITH SILVER UP 49 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 183,000 OF SILVER INTO THE THE SLV// /.////INVENTORY RESTS AT 445.044 MILLION OZ

AUGUST 28/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.281 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 444.861 MILLION OZ

AUGUST 25/WITH SILVER UP ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.751 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 446.145 MILLION OZ

AUGUST 24/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.651 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 448.896 MILLION OZ

AUGUST 23/WITH SILVER UP 94 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 826,000 OZ FROM THE SLV// /.////INVENTORY RESTS AT 450.547 MILLION OZ

AUGUST 22/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: /.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 21/WITH SILVER UP 59 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 917,0000 OZ FROM THE SLV//.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 18/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 17/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 16/WITH SILVER DOWN 13 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 15/WITH SILVER DOWN 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 14/WITH SILVER DOWN 3 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.459 MILLION OZ INTOTHE SLV/: //////INVENTORY RESTS AT 452.565 MILLION OZ

AUGUST 11/WITH SILVER DOWN 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.926 MILLION OZ INTOTHE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 452.106 MILLION OZ

AUGUST 10/WITH SILVER UP 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 9/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 8/WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 7/WITH SILVER DOWN 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 4/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.294 MILLION OZ FROM THE SLV// OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 3/WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 189,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.281 MILLION OZ

AUGUST 2/WITH SILVER DOWN 43 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 275,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.471 MILLION OZ

AUGUST 1/WITH SILVER DOWN 61 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 31/WITH SILVER UP 45 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 28/WITH SILVER UP 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.930 MILLION OZ

JULY 27/WITH SILVER DOWN 59 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ

JULY 26/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 25/WITH SILVER UP 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 826,000 OZ FROM THE SLV..////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 24/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

Rising GDP plus Rising Yields equals A MAJOR Sign of “Uh-Oh”

Matthew Piepenburg September 3, 2023

Have you heard the good news?

The Atlanta Fed GDPNow estimates a 5.9% growth in real GDP for Q3 2023. In nominal terms, we can even boast of an 8.9% surge.

What fantastic news! Growth! Productivity!

This must mean we can all breath a collective sigh of relief as Powell continues his valiant war against inflation as GDP rises, right?

I can almost hear the champagne bottles popping from the Eccles Building to the Bezos-owned Washington Post.

The financial wizards have saved us once again, right?

Wrong.

Oh, so, so, so, so WRONG.

Why?

Debt-Driven Growth is Not Growth, but a Slow Death Trap

As usual, the answer lies in math, history and, of course, THE BOND MARKET.

For years and years, I have tried to make one point (and indicator) almost reflexively clear, namely: The Bond Market Is the Thing.

This is because the bond market reflects debt forces, the most cancerous of all market killers once they metastasize from the acceptable to the fantastical, and the cheap to the unaffordable.

Today, we stare upon the greatest national and global debt bubble in history.

And the cost of that debt is getting higher, not lower.

This should be the key theme of every conversation, but instead, our citizens are arguing over gender neutral bathrooms and exciting politicos (opportunists) scurrying for power like donkeys fighting for hay.

In particular, they just need to consider and understand yields on Uncle Sam’s IOU (with particular emphasis on his 10-Year UST), which tells us the market’s measurement of the cost of debt.

And given that debt is the sole (rotten) wind beneath the wings of the post-08 American dream, when those yields rise like approaching shark fins, we all need to pause and think deeply, realistically and, hence differently from the consensus pablum which currently passes for financial reporting.

The Open Secret Hiding in Plain Sight (Ignored Shark Fins…)

As Luke Gromen has been warning for quite some time, and as my partner, Egon von Greyerz, has been arguing/expecting for even longer, we are now seeing rising yields on the 10Y UST while inflation rates (intentionally misreported) continue to fall—temporarily.

Folks, this is worth understanding. It’s not hard to do. But it’s critical.

That is, we need to understand how scary it is to see GDP rising alongside 10Y Treasury yields.

So, let’s dig in.

Debt-Based Growth is the Oxymoron of, Well…Morons

GDP is rising because government deficit spending (on everything from yet another preventable yet losing war in the Ukraine to stimmy checks for migrants [“asylum seekers”?] pouring through Texas) is rising well beyond sustainable levels.

Near-term, spending always leads to growth. But when that spending is done on a maxed-out national credit card, the short-term growth (i.e., GDPNow forecasts above) come at a comical, yet serious price.

Stated otherwise, spending, even deficit spending, has quick benefits; the debt consequences, and economic pains, however, take longer to show their economic (moronic) effects.

But when they do, the sickening results are as mathematical as they are historical.

A Tale of the Drunk and Stupid

If one, for example, were to hand a college frat boy his rich uncle’s credit card and permit him unlimited credit, that frat boy would undoubtedly throw the kind of seductive campus parties which would ensure his popularity along side many, many weekends of extravagant bacchanalia and a campus filled with smiling, drunk undergrads.

Soon, the frat house would construct its own elaborate bar, with weekly transports of unlimited beer kegs, a billiards room adorned with flat-screen TVs and 24-hour ESPN.

Others, even from universities miles way, would embark upon a joyous pilgrimage, crowding their Friday-night gatherings with shouts of awe and cries for more vodka shots.

The fun would seemingly never end.

Until, that is, the credit card bill came and the rich Uncle was tapped out.

At that point, the frat house’s growth story devolves into a comical escapade of the drunk and the stupid, which effectively describes the profiles and policies of our so-called financial elite.

The DC Frat House

When GDP spikes on the tailwind of deficit spending, the Fed starts to suffer from the beer-goggle effect of blindness to reality.

It then feels even more pressure (or drunken confidence) to raise short-term interest rates, which also sends the USD higher in the near-term but just about everything else (i.e., stocks, bonds, real estate and tax receipts) lower.

This means the risk of a market implosion in a setting of rising GDP increases exponentially, which is precisely what we saw near the end of 2018 when Powell tried to tighten the Fed’s balance sheet and raise rates at the same time.

Net result?

Markets tanked by Christmas, and as the new year rolled in, the Fed was bailing out the repo markets to the tune of hundreds of billions/week and printing inflationary money quicker than Nolan Ryan’s fastball.

Ignored Patterns, Ignorant Polices

But this otherwise ignored pattern, like a fast-ball, is pretty easy to track. The more the Fed hikes rates, the fatter and more expensive are Uncle Sam’s deficits as GDP rises on drunken (deficit) spending.

This leads to a mathematical case of “fiscal dominance,” which even the St. Louis Fed confessed in June (and of which I recently explained here)—namely, the ironic scenario in which the war on inflation (fought with rising rates) actually causes more inflation.

Why?

Because rising rates don’t just stimulate a GDP frat party (as per above), but they make America’s debt costs (interest expenses) skyrocket into the trillion/year category, which can then only be paid by a Fed mouse-clicker, which is the inevitable inflationary consequence of Powell’s deflationary “higher-for-longer” policy.

Stated otherwise, Powell, like Robert E. Lee, Napoleon, Paulus, Westmorland and Zelensky, is fighting a losing war.

Or for you film buffs who recall Maverick “writing checks [his] body can’t cash,” America is issuing IOUs its Treasury Dept. can’t pay—unless, of course, it prints a lot more fake/fiat money.

And those IOUs (i.e., USTs) are rising at a sickening rate, which means bond prices (which move inversely to supply) will fall and yields (which move inversely to price) will rise.

Read that last sentence again. It’s our bond market (and nightmare) in a nutshell.

And when yields on US 10Y USTs rise, the interest expense on Uncle Sam’s $33T bar tab becomes a bayonet wound to the economy and the market.

Horribly, Horrible Bad News

Thus, when we see GPD growth rising at the same time UST supplies (and hence yields) are climbing at a rate not seen in 55 years, this is not good news—it’s horribly, horribly bad news.

Not only are rates rising along side GDP, but our deficits are growing even deeper and hence this vicious circle of debt just gets deadlier and darker.

And this means the need to cover those deficits by printing trillions out of thin air becomes clearer and clearer, which means inflation is no longer a debate, but as fatally foreseeable as Pickett’s failed charge at Gettysburg.

We Need a Bigger Boat

In the coming months, or early into 2024, Egon and I foresee rising US sovereign bond yields and rising rates which will be near-term deflationary for risk assets and disturbing for Main Street economies no longer able to re-finance their way out of a national debt trap.

At some point thereafter, the cost of those debts will demand a monetary response (money printing to the moon) which will be, by definition, inflationary for regular Joes and no help to mean-reverting markets.

In short: We not only see inflation ahead, but stagflation to boot.

In such a setting, the USD, like the stern of the Titanic, will go from rising, and then temporarily pausing, to sinking fast to the bottom.

Again, the bond market is the thing.

Those yields matter. They are the approaching shark fins racing toward our shores which no one wishes to see.

3,Chris Powell of GATA provides to us very important physical commentaries

Important view…

‘Live from the Vault’ reviews huge threat to government’s money monopoly: Valaurum bills

Submitted by admin on Fri, 2023-09-01 21:52Section: Daily Dispatches

9:53p ET Friday, September 1, 2023

Dear Friend of GATA and Gold:

On this week’s episode of Kinesis Money’s “Live from the Vault” program, London metals trader Andrew Maguire interviews Adam Trexler, founder of Valaurum, the company issuing polymer-coated, gold-containing bills in assorted denominations that put the monetary metal back in circulation in a supremely practical way for people of ordinary means.

Such bills may be the most formidable threat to government’s monopoly on money, and thus they are potentially a powerful weapon of individual freedom.

The interview is bit less than an hour long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

Brazil Displaces US As Corn-Exporter King As Trade Winds Shift

FRIDAY, SEP 01, 2023 – 10:40 PM

It appears that a new world order is emerging, with BRICS and the Shanghai Cooperation Organization offering trade alternatives to the hegemonic West. The latest example of a multi-polar world is the US being displaced by BRICS country Brazil as the world’s top corn supplier.

The US held the crown for fifty years as the world’s top corn exporter. A new Blomberg report, citing data from the US Department of Agriculture (USDA), shows the five-decade reign is over:

In the 2023 harvest year, the US will account for about 23% of global corn exports, well below Brazil’s nearly 32%, US Department of Agriculture data show. Brazil is seen holding onto its lead in the 2024 planting year that begins Sept. 1, too. Only once in data going back to the Kennedy administration did America drop out of first place before: for a single year in 2013 following a devastating drought. The US corn-exporting industry has never before spent two back-to-back years in second place — until now.

It’s not corn. Brazil has also displaced American farmers in both soybean and wheat exports. Bloomberg explained more:

Losing its lead in corn exports may feel familiar to American farmers, who in the last decade have also relinquished the top spot in both soybean and wheat exports. Soy was the first to go, with Brazil definitively taking the lead in 2013. The next year, the US lost its wheat dominance, too, with the European Union, then Russia, beginning to elbow out American farmers in the global market.

The export ag market share slide is troubling news for the domestic industry that exported $200 billion in farm products in 2022. Sliding dominance may suggest that farmer incomes may slide in the years ahead.

Stephen Nicholson, global grains and oilseeds sector strategist with Rabobank, an agricultural lender, told Reuters:

“When we look at US corn demand long term, we wonder where new demand is coming from.

“Brazil is likely taking a bigger share of the global market, ethanol has likely peaked and animal protein is likely not going to grow fast enough.”

The reason for the shift is a rejiggering of China’s ag trade away from the US to Brazil. China signed a deal with Brazil last year to increase gain purchases.

“Brazil has the ability to ramp that planting area up to meet Chinese demand in a way that the United States doesn’t,” said Matthew Roberts, senior grain analyst with consultancy Terrain.

Plus, the Chinese are steering clear of US trade because lawmakers on Capitol Hill have been in a frenzy to weaponize the dollar and trade against Beijing.

“The US reminds me of the frog being slowly boiled,” Ann Berg, an independent consultant and veteran trader who started her career at Louis Dreyfus Co. in 1974, told Bloomberg.

Berg said, “It’s lost its dominance, but it took 40 years.”

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.3070

OFFSHORE YUAN: DOWN TO 7.3080

SHANGHAI CLOSED DOWN 22.69 PTS OR 0.71%

HANG SENG CLOSED DOWN 387.25 PTS OR 2.06%

2. Nikkei closed UP 97.55 OR 0.30%

3. Europe stocks SO FAR: ALL MOSTLY RED

USA dollar INDEX UP TO 104.66 EURO FALLS TO 1.0731 DOWN 60 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.647 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.31/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ON SHORE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.6055***/Italian 10 Yr bond yield UP to 4.325*** /SPAIN 10 YR BOND YIELD RISES TO 3.641…**

3i Greek 10 year bond yield RISES TO 3.908

3j Gold at $1930.75 silver at: 23.50 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 67 /100 roubles/dollar; ROUBLE AT 97.55//

3m oil into the 85 dollar handle for WTI and 88 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 146.35// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.647% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8892 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9543well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.230 UP 6 BASIS PTS…

USA 30 YR BOND YIELD: 4.336 UP 5 BASIS PTS/

USA 2 YR BOND YIELD: 4.924 UP 6 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.79…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 12 BASIS PTS AT 4.5430

end

2.a Overnight: Newsquawk and Zero hedge:

USA EARLY MORNING REPORT

Futures Slide, Dollar Surges As China Services Unexpectedly Slump

TUESDAY, SEP 05, 2023 – 08:13 AM

Futures are lower, tracking European bourses and Asian markets, but well off session lows as a brief burst of China-linked optimism promptly following a Monday surge in property stocks and hopes of a Chine recovery turned to bust, as China reported the slowest service sector monthly growth so far this according to the August PMI survey, adding to a series of disappointing data. As of 7:50am ET, S&P futures were down 0.1% to 4,517 reversing the 0.2% gain during the Monday Labor Day holiday session; Nasdaq 100 futures dropped 0.4%. The US currency gained as much as 0.5% against its Group-of-10 peers, touching the highest level since March, sending commodities, gold and bitcoin lower. 10Y Yields are up to 4.22% and once again approaching the key resistance level of 4.25%, pressured not just by oil trading near 2023 highs but also in anticipation of a surge in corporate bond sales this week. Also, UK and euro-zone yields rose Monday and are extending that move. Today’s macro data focus is Durable Goods/Cap Goods plus Factory Orders. Later in the week we receive ISM-Srvcs and Jobless Claims.

In premarket trading, NextGen Healthcare jumped 8% after Bloomberg News reported that Thoma Bravo is in advanced talks to buy the health-records software company. US-listed Chinese stocks dropped following their best weekly performance since July, as August data pointed to a slowdown in China’s services sector. Alibaba -1%, Baidu -1.7%. Blackstone and Airbnb rose after the S&P Dow Jones Indices said the stocks will join the S&P 500 index prior to the opening of trading on Sept. 18. Manchester United fell as much as 9.2% amid ongoing speculation over a possible deal for the Premier League team. Here are some other notable premarket movers:

Associated Banc-Corp (ASB US) shares rise as much as 0.6% after Baird upgraded the Midwest bank to outperform from neutral, saying that the shares offer attractive risk-reward following recent underperformance.

Oracle (ORCL US) gains 1.5% after Barclays upgrades to overweight from equal-weight in note, calling the infrastructure software company a “multi-year growth story.”

General Mills Inc. (GIS) slips 0.4% after BNP Paribas Exane analyst Max Gumport cut the recommendation on the packaged-foods company to neutral from outperform, citing a slowdown in premium dog-food demand.

Lowe’s (LOW) recommendation was raised to outperform from market perform at Bernstein, with the broker noting that there are multiple positive catalysts including: margin expansion and improving return on invested capital. Stock edges higher, up 1%.

NetApp Inc. shares are up 1.8% after Susquehanna Financial upgraded the data storage company to positive from neutral.

Olin Corp is upgraded to overweight from sector weight at KeyBanc Capital Markets, which says the stock’s valuation appears attractive after shares tumbled following news that CEO Scott Sutton will step down. Shares in the manufacturer of chemical products and ammunition rise 2%.

Oracle gains 1.7% after Barclays upgrades to overweight from equal-weight in note, calling the infrastructure software company a “multi-year growth story.”

Viatris gains 2% after the firm said the US FDA has tentatively approved a drug cocktail for children with HIV-1.

Overnight, China’s services sector saw the slowest growth this year in August, an industry survey showed, adding to evidence the economic recovery is losing traction and damping earlier optimism over government stimulus.

Similarly in Europe, the composite purchasing managers’ index undershot expectations, posting a contraction for a third straight month.

As we enter Sept, JPM’s market intel team writes that there is much discussion on seasonality; while Sept’s average return is negative, its median return is ~0%. When SPX is update double-digits into Sept, then Sept tends to be positive, too. We may also see a surge of capital markets activity over the next couple weeks.

The European Central Bank, which meets next week, faces a quandary over interest rates, given recession fears and above-target inflation. “There is real concern for the euro-area picture, with survey data suggesting the economy is sliding into recession,” said Sarah Hewin, head of Europe and Americas research at Standard Chartered. “It raises questions over how aggressive the ECB can be going forward.”

By contrast, recent data shows the US economy is holding up well and rate cuts may not come any time soon, even though many economists say the Federal Reserve has come to the end of its 18-month long policy-tightening campaign. Goldman Sachs now sees just a 15% probability of a US recession in the coming year, down five percentage points from their previous estimate.

Europe’s Stoxx 600 traded flat, after paring a drop of as much as 0.8% with luxury goods among the worst performers. Here are the most notable European movers:

Partners Group rises as much as 8.4% and is the biggest gainer in the Stoxx 600 after the Swiss investment manager delivered performance fees that analysts describe as a material beat

BKW climbs as much as 4.4% after the Swiss energy company reported operating profit for the first half-year that beat estimates, with analysts highlighting positive momentum in the energy division

Johnson Service Group rises as much as 5.5% in 7th straight day of gains, hitting highest since March 22, as RBC highlights good first-half momentum for the UK textile rental and laundry firm

Alten rises as much as 2.8% after Stifel initiates coverage with a buy rating, saying the engineering and technology consulting firm is set for long-term earnings growth

European food retail stocks fall after JPMorgan downgrades the sector, citing an “unattractive risk reward” given the current sentiment as well as valuations

Commerzbank drops as much as 5.2%, the most in a month, after Barclays downgrades to underweight from equal-weight based on “significant” downside risk to estimates

Roche falls as much as 2.2%, slipping to its lowest since January 2019, after Berenberg cut its recommendation for the Swiss pharma giant to hold on a lack of share-price catalysts

Credit Agricole falls as much as 3.8% after Goldman Sachs downgraded the stock to sell from neutral as it turned “more cautious” on the French lender’s earnings expectations

Sectra falls as much as 14% after the Swedish medical imaging and cybersecurity firm reported first-quarter earnings which included a year-on-year fall for operating margins and profit

EnQuest shares drop as much as 17% in their worst day since April 2020, after the oil producer swung to a 1H loss from a profit a year earlier due to the impact of the UK energy windfall tax

Earlier in the session, Asian stocks fell, with the key regional benchmark on track to snap a six-day winning streak, as a property-led rally in Chinese equities fizzled amid disappointing economic data. The MSCI Asia Pacific Index fell as much as 0.8%, dragged by weakness in the financial sector. China equities declined, retreating after Monday’s strong gains as a gauge of services activity printed well below estimates. China led the rally in Asian stocks on Monday after authorities rolled out more stimulus for the embattled property sector. The decline on Tuesday shows investor sentiment toward Chinese shares remains fragile, casting a pall on the outlook for regional equities. Even after its latest rally, the Asian benchmark is trailing key gauges of peers in the US and Europe this year.

Hang Seng and Shanghai Comp were pressured after Chinese Caixin Services PMI data missed forecasts and with the property sector dampened by default fears with about a third of 50 major private builders said to face around $1.5bln dollars of payments this month, while Country Garden narrowly averted a default and paid USD-denominated coupons hours before the end of the grace period.

South Korea stocks traded lower, where inflation accelerated much faster than estimated in August, keeping the door open to a rate hike. Shares also dropped in Australia, where the central bank is expected to keep rates unchanged for a third-straight month in a meeting later Tuesday. Vietnamese equities were the only notable gainers following a national holiday.

Australia’s ASX 200 was lower amid underperformance in the commodity-related sectors and as participants braced for the conclusion of RBA Governor Lowe’s final policy meeting in which the central bank kept rates unchanged as expected.

Nikkei 225 stalled on its approach to the 33,000 level and with headwinds from disappointing household spending data which suffered its worst drop since February 2021.

“It’s the typical post-party reality check that’s cooling down China’s rally today, as the services PMI notably missed expectations, suggesting further economic downtrend ahead,” said Hebe Chen, an analyst at IG Markets Ltd. “Meanwhile, investors are cautiously awaiting the RBA’s meeting decision, which is poised to raise the curtain for a new round of central bank talks.”

In FX, the US dollar rose to the strongest since July against the euro and the pound. Against the yen, it’s approaching the highest since November, and BOJ intervention is looking increasingly inevitable. The Bloomberg Dollar Index jumped 0.4% to 1250.81, its highest since mid-March as China data pointed to sputtering economic recovery. The US currency posted the biggest gains against the Australian dollar, down 1.3%. Australia’s central bank kept its key interest rate unchanged and maintained a tightening bias. “With RBA already acknowledging that the economy is already experiencing below-trend growth, surely any further tightening should crimp on growth momentum further down the road,” said Fiona Lim, senior FX strategist at Malayan Banking Bhd. in Singapore. “AUD could still remain under pressure.” EUR/USD fell 0.5% to $1.0747 as data showed consumer inflation expectations rose in July even as demand for services cooled

In rates, treasuries were lower with US 10-year yields rising 4bps to 4.22%. US yields are higher by 3bp-54bp across the curve led by intermediate tenors, leaving curve spreads narrowly mixed, and extending a slide that began Friday in anticipation of a surge in corporate bond sales this week. At least six US high-grade corporate bond issuers have slated offerings for Tuesday; sales are expected to total about $120b this month, a seasonally heavy month that normally sees issuance concentrated in the week or so after US Labor Day. Treasury coupon supply is on hiatus until Sept. 11, when cycle including new 3-year and 10- and 30-year reopenings is slated to begin. Also, UK and euro-zone yields rose Monday and are extending that move. Bunds are also in the red with little reaction shown to a downward revision to euro-area service PMI.

In commodities, crude futures decline, with WTI falling 0.2%. Spot gold drops 0.6%.

Bitcoin is under modest pressure, -0.2%, as the USD continues to climb higher and the overall tone remains a subdued one after the APAC handover. Currently, BTC resides at the mid-point of USD 25.55-25.83k parameters.

To the day ahead now, and data releases include the global services and composite PMIs for August, along with Euro Area PPI for July and US factory orders for July. From central banks, we’ll get the ECB’s Consumer Expectations Survey, and hear from the ECB’s Schnabel and Visco.

Market Snapshot

S&P 500 futures down 0.1% to 4,515

MXAP down 0.8% to 163.12

MXAPJ down 1.1% to 509.51

Nikkei up 0.3% to 33,036.76

Topix up 0.2% to 2,377.85

Hang Seng Index down 2.1% to 18,456.91

Shanghai Composite down 0.7% to 3,154.37

Sensex little changed at 65,687.26

Australia S&P/ASX 200 little changed at 7,314.28

Kospi little changed at 2,582.18

STOXX Europe 600 down 0.6% to 455.24

German 10Y yield little changed at 2.59%

Euro down 0.5% to $1.0746

Brent Futures down 0.8% to $88.30/bbl

Gold spot down 0.5% to $1,933.17

U.S. Dollar Index up 0.35% to 104.61

Top overnight news from Bloomberg

Home sales in two of China’s biggest cities soared in the past two days following mortgage relaxations, an early sign that government efforts to cushion a record housing slowdown are helping. Existing-home sales for Beijing and Shanghai doubled over the weekend from the previous one, according to CGS-CIMB Securities. “We were surprised by the strong pick up in Beijing and Shanghai, despite the challenging economy,” said Raymond Cheng, head of China property at CIMB. BBG

Chinese property developer Country Garden made payments on two dollar bonds within their grace periods on Tuesday, ending a month-long saga that had become the focal point of global investors’ concerns about China’s struggling property sector. FT

China’s Caixin services PMI for Aug was very soft, coming in at 51.8, down from 54.1 in Jul and below the Street’s 53.5 forecast. RTRS

North Korean leader Kim Jong-un plans to travel to Russia this month for a meeting with Putin at which the two will discuss Pyongyang ramping its weapons supplies to Moscow. NYT

Ukraine president Zelensky said he was replacing the minister of defense, confirming recent media speculation, in what is the biggest shakeup since Russia launched its invasion. NYT

The world’s most powerful financial watchdog has warned of “further challenges and shocks” in the months ahead, as high interest rates undermine economic recoveries and threaten key sectors including real estate. In his regular update to G20 leaders ahead of their summit in New Delhi this week, Klaas Knot, chair of the Basel-based Financial Stability Board, said: “The global economic recovery is losing momentum and the effects of the rise in interest rates in major economies are increasingly being felt.” FT

The US deficit is climbing, but not for reasons that are inflationary – things like higher interest expense, reduced Fed earnings, and lower non-withheld tax revenue (due to smaller capital gains) are pushing deficits higher. WSJ

Trump’s lead grows more dominant – he’s now the choice of ~60% of GOP primary voters, up 11 points from the prior survey in April. Biden’s age a growing political liability – 73% of voters think Biden is too old for a second term vs. 47% who feel the same about Trump (and Trump has an 11-point advantage on record of accomplishments as president) WSJ

Private equity giant Blackstone Inc. is the latest addition to the S&P 500 Index, the first alternative asset manager to join the equity gauge. Airbnb Inc. is added as well. The New York-based Blackstone and Airbnb will replace Lincoln National Corp. and Newell Brands Inc. prior to the start of trading on Sept. 18, S&P Dow Jones Indices said. BBG

The continued positive inflation and labor market news has led GIR to cut our estimated 12-month US recession probability further to 15%, down 5pp from our prior estimate and equal to the unconditional average recession probability of 15% calculated from the fact that a recession has occurred roughly once every seven years since WW2

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly subdued after the holiday lull stateside and as the region digested disappointing data releases including the weaker-than-expected Chinese Caixin Services PMI. ASX 200 was lower amid underperformance in the commodity-related sectors and as participants braced for the conclusion of RBA Governor Lowe’s final policy meeting in which the central bank kept rates unchanged as expected. Nikkei 225 stalled on its approach to the 33,000 level and with headwinds from disappointing household spending data which suffered its worst drop since February 2021. Hang Seng and Shanghai Comp were pressured after Chinese Caixin Services PMI data missed forecasts and with the property sector dampened by default fears with about a third of 50 major private builders said to face around USD 1.5bln dollars of payments this month, while Country Garden narrowly averted a default and paid USD-denominated coupons hours before the end of the grace period.

Top Asian News

China’s MIIT released a plan to develop the electronics industry and will guide capital to the industry, while it will support qualified enterprises to make good use of financing tools such as domestic and overseas listings and bond issuances, according to Bloomberg and Reuters.

China’s Foreign Minister Wang said following the recent meeting with his Italian counterpart that China and Italy should adhere to the right way of getting along in terms of mutual respect, trust, openness and cooperation, while he added that both countries should strive for bilateral relations to be at the forefront of China-EU relations. Furthermore, Wang said they should jointly safeguard a free and open multilateral trading system, maintain a stable global supply chain and provide a fair business environment for each other’s enterprises.

A debt crisis reportedly threatens to engulf Chinese developers with about two-thirds of 50 major private builders defaulters and with the 16 survivors facing USD 1.5bln of bond payments this month, according to Bloomberg.

Country Garden Holdings (2007 HK) paid USD-denominated coupons that were due last month before the end of the grace period which was set to expire by September 6th, according to Bloomberg and Reuters.

RBA kept the Cash Rate Target unchanged at 4.10%, as expected, while it reiterated that some further tightening of monetary policy may be required and the Board remains resolute in its determination to return inflation to the target.. RBA higher interest rates are working to establish a more sustainable balance between supply and demand in the economy and will continue to do so but noted inflation is still too high and will remain so for some time yet. Furthermore, the RBA said the pause will provide further time to assess the impact of the increase in interest rates to date and the economic outlook but noted increased uncertainty around the outlook for the Chinese economy due to ongoing stresses in the property market and that the outlook for household consumption also remains uncertain

China is reportedly to launch a new state-backed fund that aims to raise USD 40bln in order to boost the chip industry, via Reuters citing sources. The new fund will focus on areas incl. equipment for chip manufacturing. Fund has received approval from Chinese authorities in recent months. Finance Ministry intends to contribute CNY 60bln to it.

European bourses are in the red, Euro Stoxx 50 -0.2%, but have been gradually making their way higher after a subdued open given the downbeat APAC handover. A handover that was negatively affected by soft Chinese Caixin PMI data. Since action has been influenced by Final PMIs though the metrics provided little to lift the overall tone with the recovery off lows occurring gradually and without a specific fundamental driver. Sectors are mixed after beginning the morning firmly in the red. Personal Care, Drug & Household names alongside Consumer Products/Services continue to lag given broker activity and data while Financial Services, Energy, Insurance and Banking are now modestly firmer on the session; the latter components perhaps benefitting from yield support. Stateside, futures have been directionally in-fitting with the above though magnitudes have been more contained thus far. ES -0.2% has lifted off of lows with the NQ -0.3% following suit but to a slightly lesser extend given yield upside. Action which comes ahead of Final PMIs and a handful of other data points.

Top European News

ECB’s Lane (conducted on August 31st): I would underline the fact that there has been some easing in goods inflation and services inflation, which is a welcome development. “expect to see this famous core inflation come down throughout the autumn.”; “… it would be a mistake to extrapolate the high inflation we’ve seen into a longer-term projection.”. Click here for the full release.

Spanish Catalan Leader Puigdemont says all judicial cases that are targeting Catalan separatism must be dropped as a condition for discussions on the PMs investiture

FX

A firm start to the session for the Dollar index, fuelled by risk aversion and an overnight uptick in yields, and with US cash yields back online following its long Labor Day weekend.

The Yen is one of the focal points in today’s session as it approaches YTD lows against the Dollar, while the overnight session saw a particularly weak 10-year JGB auction.

The Antipodeans sit as G10 underperformers as the fallout from the softer Chinese Services PMI takes its toll, while the RBA’s policy decision saw no fireworks.

The European majors succumb to the Dollar but to a lesser extent than their Antipodean counterparts. The morning saw the final PMIs in the EZ downgraded, with the broader theme being slower growth and rising input prices.

PBoC set USD/CNY mid-point at 7.1783 vs exp. 7.2703 (prev. 7.1786)

World Bank is reportedly in talks to double its Turkey exposure to USD 35bln, according to Bloomberg sources; the World Bank is reportedly working on USD 18bln in new funding over the next three years which will focus mostly on the private sector.

Fixed Income

Core benchmarks are under modest pressure with action occurring around the EZ/regional and UK PMIs but for the most part this has been shortlived as we await the return of US players from the long weekend.

Bunds are softer to the tune of 15 ticks and reside towards the mid-point of 131.61-131.98 boundaries. A high which printed in proximity to the morning’s Spanish Services PMI while the low was re-tested on the Final EZ figure.

Gilts have been slightly more contained given their more outsized action on Monday while USTs are broadly in-line with EGBs ahead of data points. As it stands, yields are firmer across the curve with action slightly more pronounced at the long end and the curve incrementally bear-steepening as a result.

Commodities

WTI and Brent front-month futures are softer intraday amid the broader risk aversion emanating from the Chinese Services PMIs overnight.

Dutch TTF kicked off the session firmer but then fell into losses, with news overnight suggesting Offshore Alliance members at Chevron’s Gorgon Facility, Wheatstone Platform and Wheatstone Downstream gas processing facilities in northwest Western Australia have notified the company that they intend to stop work for 2 weeks commencing September 14.

Metals are seeing broader pressure from the firmer Dollar whilst industrial metals see deeper losses vs precious metals amid the demand dent emanating from China.

Australia’s Offshore Alliance served Chevron (CVX) with further notice of protected industrial action which will commence after the first 7 days of the protected industrial action kicks off on September 7th, while the Australian union said it plans a full strike at Chevron’s Wheatstone and Gorgon LNG facilities in Australia for two weeks from September 14th if its demands are not met, according to Reuters.

Goldman Sachs said it still sees a potentially more aggressive OPEC+ price target as a key moderately bullish risk to its 12-month ahead Brent crude forecast of USD 93/bbl and it no longer expects Saudi to announce a partial unwind of its 1mln bpd production cut, according to Reuters.

Ukraine does not expect its grain export situation to change after the talks between Russian President Putin and Turkish President Erdogan, according to Reuters sources.

Chevron (CVX), on industrial action, says it has continuity plans and plans to be a reliable supplier. Elsewhere, says if the winter is a normal one, then it could be a difficult time for some European nations.

Geopolitics

The Russian Defence Ministry said it shot down a drone over Russia’s Kaluga region,** according to Reuters.

North Korean leader Kim plans to travel to Russia this month and meet Russian President Putin to discuss the possibility of supplying weapons for the war in Ukraine, according to NYT citing US and allied sources. In response, the Russian Kremlin says it has “nothing to say”.

US Event Calendar

10:00: July Factory Orders, est. -2.5%, prior 2.3%

July Factory Orders Ex Trans, est. 0.1%, prior 0.2%

10:00: July Durable Goods Orders, prior -5.2%

Durables-Less Transportation, prior 0.5%

Cap Goods Orders Nondef Ex Air, prior 0.1%

Cap Goods Ship Nondef Ex Air, prior -0.2%

DB’s Jim Reid concludes the overnight wrap

The last 24 hours have been fairly quiet for markets given the US holiday, but the overall tone was slightly negative after what was earlier a very good handover from a strong China market on Monday. However this faded as the day progressed with losses for bonds and equities in Europe, just as oil prices hit a new high for 2023. The recent run-up in oil prices is already setting us up for some hotter August CPI prints, so any further gains there are going to be a fresh hurdle for central banks in their quest to get inflation back to target.

That concern was evident among sovereign bonds, which sold off mainly thanks to higher inflation expectations. For instance, the 10yr bund yield was up +3.1bps on the day to 2.57%, of which +2.5bps was a result of higher inflation expectations. Yields moved higher in other countries as well, with those on 10yr OATs (+2.8bps), BTPs (+5.4bps) and gilts (+3.5bps) all rising.

Unsurprisingly, that rise in inflation expectations led to a bit more speculation about whether the ECB might deliver another hike next week. Currently, overnight index swaps still consider that an unlikely prospect and are pricing in a 25.7% chance, but that’s up from 23% the previous day, so clearly investors aren’t entirely discounting the prospects of another move.

When it comes to that meeting, ECB President Lagarde provided no clues on what the ECB might do in a speech yesterday. That focused on communication and monetary policy, although Lagarde did say “actions speak louder than words” and referenced the 425bps of hikes that the ECB had already delivered. If they were to pause, that would end a run of 9 consecutive rate hikes, so it could be a big moment. However, markets think there’s also a decent probability they might do a “skip” like the Fed did in June, since they’re also pricing in a 50% chance of a hike by the time of the December meeting.

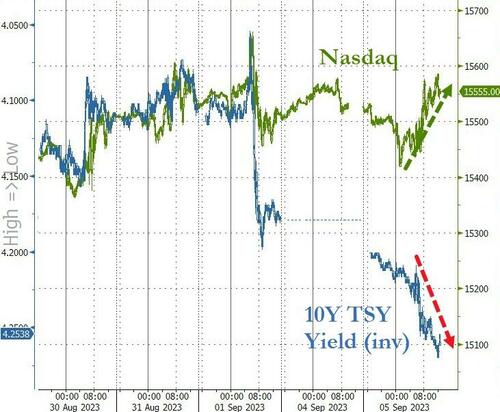

This backdrop saw European equities lose ground throughout the session, despite a fairly strong performance at the open. Indeed, the STOXX 600 was initially up +0.88%, with China related stocks in the ascendency. These gains were pared back with the index ending the day -0.04% lower. It was a similar story across the continent, with modest losses for the FTSE 100 (-0.16%), the CAC 40 (-0.24%) and the DAX (-0.10%) as well. US markets were closed yesterday, but S&P 500 (-0.17%) and NASDAQ 100 (-0.11%) futures have edged lower overnight. 10yr USTs yields (+3.15bps) have edged up trading at 4.21% as trading has resumed.

The other big development yesterday came from oil prices, which hit a new closing high for 2023. The latest moves saw Brent crude up +0.51% yesterday to $89.0/bbl, whilst WTI is up +0.47% this morning trading at $85.95/bbl as we go to press. The last time Brent traded above $90/bbl was last November, and even a temporary uplift could prove challenging for policymakers and markets, since inflation is still running above target. So any pivot away from restrictive policy is going to be hard so long as it remains there, and it’s going to heighten the dilemmas they might face if we do end up with a noticeable downturn in growth.

Asian equity markets are lower this morning reversing some of yesterday’s gains. Chinese equities are leading losses with the Hang Seng (-1.55%) the biggest underperformer followed by the Shanghai composite (-0.63%) and the CSI (-0.57%). The Nikkei (-0.21%) and the KOSPI (-0.12%) are also slightly lower as I type.