SEPT 15//GOLD ROSE BY $13.20 TO $1924.60// //SILVER ROSE BY 37 CENTS TO $23.09/PLATINUM CLOSED UP 19.45 TO $930.00 WHILE PALLADIUM CLOSED DOWN $0.60 TO $1250.50//IMPORTANT VIEW TO SEE ANDREW MAGUIRE INTERVIEWING JEFFREY SNIDER//AND ANOTHER IMPORTANT READ FROM ALASDAIR MACLEOD//GOLD DENOMINATED IN YEN REACHES ALL TIME HIGHS//UKRAINE VS RUSSIA UPDATES//COVID UPDATES//VACCINE UPDATES/DR PAUL ALEXANDER/SLAY NEWS/EVOL NEWS/NEWS ADDICTS//USA NEWS: UAW GOES ON STRIKE//SWAMP STORIES FOR YOU TONIGHT//

118 C MACQUARIE FUT 2 323 H HSBC 3 435 H SCOTIA CAPITAL 3 624 H BOFA SECURITIES 4 737 C ADVANTAGE 14 2

TOTAL: 14 14 MONTH TO DATE: 3,840

JPMorgan stopped 0/14 contracts.

FOR SEPT.:

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2023. CONTRACT: 14 NOTICES FOR 1400 OZ or 0.0126 TONNES

total notices so far: 3840 contracts for 384,000 oz (11.9440 tonnes)

FOR SEPT:

SILVER NOTICES: 13 NOTICE(S) FILED FOR 65,000 OZ/

total number of notices filed so far this month : 2604 for 13,020,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $13.20

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD//

INVENTORY RESTS AT 879,70 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 37 CENTS AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.055 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 439.681 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 990 CONTRACTS TO 127,586 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.16 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. TAS ISSUANCE WAS A SMALL SIZED 355 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 355 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.16). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A HUMONGOUS SIZED GAIN OF 3371 CONTRACTS ON BOTH EXCHANGES ALONG WITH CONSIDERABLE T.A.S.LIQUIDATION THROUGHOUT THE THURSDAY COMEX SESSION

WE MUST HAVE HAD:

A HUMONGOUS ISSUANCE OF EXCHANGE FOR PHYSICALS( 2110 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 14.420 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S SMALL QUEUE JUMP OF 15,000 OZ//NEW TOTAL 13.365 MILLION OZ + OUR CRIMINAL ISSUANCE OF 200 EXCHANGE FOR RISK CONTRACTS OR 1.0 MILLION OZ OF FUTURE SILVER STANDING FOR METAL//NEW TOTALS EXCHANGE FOR RISK: 3.0 MILLION OZ: NEW TOTALS SILVER STANDING: 16.365 MILLION OZ// /// / //HUGE SIZED COMEX OI GAIN/ HUMONGOUS SIZED EFP ISSUANCE/VI) SMALL SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 355CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -271 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 10 days, total 8054 contracts: OR 40.270 MILLION OZ (805 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 40.270 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 40.27 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 990 CONTRACTS DESPITE OUR LOSS IN PRICE OF $0.16 IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUMONGOUS EFP ISSUANCE CONTRACTS: 2110 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR SEPT OF 14.2 MILLION OZ FOLLOWED BY TODAY’S 15,000 OZ QUEUE JUMP .+ 1 MILLION OZ EXCHANGE FOR RISK//PRIOR TOTAL FOR EXCHANGE FOR RISK = 2.0 MILLION OZ/TOTAL EXCH. FOR RISK = 3.0 MILLION OZ////NEW TOTALS STANDING 16.365 MILLION OZ// /// WE HAVE A HUMONGOUS SIZED GAIN OF 3100 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A SMALL SIZED 355 CONTRACTS//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION. THE NEW TAS ISSUANCE THURSDAY NIGHT (355) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 13 NOTICE(S) FILED TODAY FOR 65,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1311 CONTRACTS TO 440.649 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: 413 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 898 CONTRACTS) WITH OUR $1.00 GAIN IN PRICE//THURSDAY. WE ALSO HAD A RATHER STRONG INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 12.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 1500 OZ QUEUE JUMP//NEW TOTAL STANDING 14.495 TONNES + /A FAIR (AND CRIMINAL) ISSUANCE OF 1084 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH OUR$1.00 GAIN IN PRICEWITH RESPECT TO THURSDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 2069 OI CONTRACTS (6.435 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3380CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 441,062

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2069 CONTRACTS WITH 1311 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 3380 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2069CONTRACTS OR 6.435 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 1084 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3380 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (1311) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 2492 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 12.656 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 1500 OZ/// 3) ZERO LONG LIQUIDATION WITH FAIR TAS LIQUIDATION DURING THE COMEX SESSION //4) SMALL SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 1084 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT :

TOTAL EFP CONTRACTS ISSUED: 23,269 CONTRACTS OR 2,326,900 OZ OR 72,37 TONNES IN 10TRADING DAY(S) AND THUS AVERAGING: 2327 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAY(S) IN TONNES 72.37 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 72.37/3550 x 100% TONNES 2.02% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 72.37 TONNES (SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 990 CONTRACTS OI TO 127,586 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A HUMONGOUS 2110 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 2110and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2110 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 990 CONTRACTS AND ADD TO THE 2110 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUMONGOUS SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 3100 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 16.855 MILLION OZ

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED DOWN 8,81 PTS OR 0.28% //Hang Seng CLOSED UP 134.97 PTS OR 0.75%/ /The Nikkei CLOSED UP 364.79 PTS OR 1.10% //Australia’s all ordinaries CLOSED UP 1.35 % /Chinese yuan (ONSHORE) closed UP AT 7.2772 /OFFSHORE CHINESE YUAN UP TO 7.2774 /Oil UP TO 90.34 dollars per barrel for WTI and BRENT UP AT 93.89 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1311CONTRACTS TO 440,649 DESPITE OUR GAIN IN PRICE OF $1.00 ON THURSDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3380 EFP CONTRACTS WERE ISSUED: : DEC 3380 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3380 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2069 CONTRACTS IN THAT 3380LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 1311 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $1.00//THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS A FAIR 1084 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: SEPT (14.495) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 14.495 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $1.00) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR GAIN OF 2069 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A CONSIDERABLE T.A.S. LIQUIDATION ON THE FRONT END OF THURSDAY’S TRADING. THE T.A.S. ISSUED ON THURSDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 7.720 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPT. (12.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 1500 OZ//NEW STANDING 14.495 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $1.00.

WE HAD – REMOVED 413 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 2069 CONTRACTS OR 206900 OZ OR 6.435 TONNES.

Estimated gold volume today:// 191,632 poor

final gold volumes/yesterday 216,600 poor//speculators have left the gold arena

Total monthly oz gold served (contracts) so far this month

3840 notices 384000 OZ 11.9444 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 0

total customer deposits: nil oz

we had 1 customer withdrawal

i) Out of Brinks: 3279.400 oz (102 kilobars)

total withdrawals 3279.400 oz

Adjustments; 3: all dealer to customer i) Asahi: 8583.231 oz

ii) Brinks: 1739.711 oz

iii) Manfra: 38,098.935 oz

total 48,421.877o

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPTEMBER.

For the front month of SEPTEMBER we have an oi of 834 contracts having GAINED 12 contracts. We had

4 contracts were served on THURSDAY, so we gained an additional 15 CONTRACTS or AN ADDITIONAL 1500 oz will stand for delivery in this non active delivery month of Sept.

Oct LOST 311 contracts to 25,437 contracts.

NOV GAINED 1 CONTRACTS to stand at 20

December LOST 2436 contracts DOWN to 376,555 contracts.

We had 14 contracts filed for today representing 1400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 14 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2023. contract month,

we take the total number of notices filed so far for the month (3840 x 100 oz ), to which we add the difference between the open interest for the front month of SEPT (834 CONTRACTS) minus the number of notices served upon today 14 x 100 oz per contract equals 466,000 OZ OR 14.495 TONNES the number of TONNES standing in this non active month of SEPT.

thus the INITIAL standings for gold for the SEPTcontract month: No of notices filed so far (3840) x 100 oz + (834) {OI for the front month} minus the number of notices served upon today (14) x 100 oz) which equals 466,000 oz standing OR 14.495 TONNES

TOTAL COMEX GOLD STANDING: 14.495 TONNES WHICH IS HUGE FOR AN INACTIVE DELIVERY MONTH.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 20,878,273.020 OZ

TOTAL REGISTERED GOLD 10,801,765.332 (335,98 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,076,507.688 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,747,673 OZ (REG GOLD- PLEDGED GOLD) 272.08 tonnes//dropping like a stone

END

SILVER/COMEX

SEPT 15

//2023// THE SEPT 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

849,053.410 oz ASAHI Brinks

.

Deposits to the Dealer Inventory

nil

Deposits to the Customer Inventory

nil

No of oz served today (contracts)

13 CONTRACT(S) (65,000 OZ)

No of oz to be served (notices)

69 contracts (345,000 oz)

Total monthly oz silver served (contracts)

2604 Contracts (13,020,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 deposit customer account:

total customer deposit nil oz

JPMorgan has a total silver weight: 136.901 million oz/272.781 million or 50.18%

Comex withdrawals 2

i) Out of ASAHI: 265,450.900 oz

ii) Out of Brinks: 583,602.510 oz

total: 849,053.410 o

adjustments:

TOTAL REGISTERED SILVER: 42.405 MILLION OZ//.TOTAL REG + ELIGIBLE. 272.781 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR August:

silver open interest data:

FRONT MONTH OF SEPT /2023 OI: 82 CONTRACTS HAVING GAINED 2 CONTRACT(S). WE HAD 1

CONTRACT SERVED ON THURSDAY. SO WE GAINED 3 CONTRACTS OR 15,000 OZ WILL STAND FOR SILVER AT THE COMEX..

OCT GAINED 43 CONTRACTS TO STAND AT 1143.

NOVEMBER GAINED 25 CONTRACTS TO STAND AT 134

DEC. GAINED 711 CONTRACTS TO STAND AT 115,186 .

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 13 for 65,000 oz

Comex volumes// est. volume today 64,659 fair

Comex volume: confirmed yesterday 87,858 good

To calculate the number of silver ounces that will stand for delivery in SEPT. we take the total number of notices filed for the month so far at 2604 x 5,000 oz = 13,020,000 oz

to which we add the difference between the open interest for the front month of SEPT (82) and the number of notices served upon today 13 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT/2023 contract month: 2604 (notices served so far) x 5000 oz + OI for the front month of SEPT (82) – number of notices served upon today (13 )x 500 oz of silver standing for the SEPT contract month equates to 13.3650 million oz. + OUR 1.0 MILLION EXCHANGE FOR RISK..NEW TOTALS EXCHANGE FOR RISK: 3.0 MILLION OZ//NEW TOTAL STANDING FOR SILVER: 16.3650 MILLION OZ//

There are 42.145 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

SEPT 15/WITH GOLD UP $13.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD : A WITHDRAWAL OF 1.055 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 879.70 TONNES

SEPT 14/WITH GOLD UP $1.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD : A WITHDRAWAL OF 4.63 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 882.01 TONNES

SEPT 13/WITH GOLD DOWN $2.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 12/WITH GOLD DOWN $11.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 11/WITH GOLD UP $4.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 8/WITH GOLD UP $0.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 7/WITH GOLD DOWN $0.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.22 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.69 TONNES

SEPT 6/WITH GOLD DOWN $8.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.81 TONNES

SEPT 5/WITH GOLD DOWN $13.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.97 TONNES

SEPT 1/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 31/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 30/WITH GOLD UP $8.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.59 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.23 TONNES

AUGUST 29/WITH GOLD UP 17.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.6 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.64 TONNES

AUGUST 28/WITH GOLD UP $6.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / //INVENTORY RESTS AT 884.04 TONNES

AUGUST 25/WITH GOLD DOWN $6.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 884.04 TONNES

AUGUST 24/WITH GOLD UP $0.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //INVENTORY RESTS AT 884.91 TONNES

AUGUST 23/WITH GOLD UP $21.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 4.32 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 884.91 TONNES

AUGUST 22/WITH GOLD UP $2.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.87 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 889.23 TONNES

AUGUST 21/WITH GOLD UP $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.60 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 890.10 TONNES

AUGUST 18/WITH GOLD UP $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 6.92 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 887.50 TONNES

AUGUST 17/WITH GOLD DOWN $12.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 16/WITH GOLD DOWN $7.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 15/WITH GOLD DOWN $7,45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 895.87 TONNES

AUGUST 14/WITH GOLD DOWN $2.10 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.75 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 899.63 TONNES

AUGUST 11/WITH GOLD DOWN $2.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 903.31 TONNES

AUGUST 10/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 9/WITH GOLD DOWN $8.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 8/WITH GOLD DOWN $9.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES FORM THE GLD /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 7/WITH GOLD DOWN $5.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 906.00 TONNES

AUGUST 4/WITH GOLD UP $7.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.18 TONNES OF GOLD FROM THE GLD/// .///INVENTORY RESTS AT 906.00 TONNES

AUGUST 3/WITH GOLD DOWN $5.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 2/WITH GOLD DOWN $3.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.75 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 1/WITH GOLD DOWN $28.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

GLD INVENTORY: 879.681 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 15/WITH SILVER UP 37 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.31 MILLION OZ FROM THE SLV. : // /.////INVENTORY RESTS AT 439.681 MILLION OZ

SEPT 14/WITH SILVER DOWN 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: : // /.////INVENTORY RESTS AT 440.736 MILLION OZ

SEPT 13/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1,009 MILLION OZ INTO THE SLV//: // /.////INVENTORY RESTS AT 440.736 MILLION OZ

SEPT 12/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.209 MILLION OZ INTO TEH SLV//: // /.////INVENTORY RESTS AT 439.727 MILLION OZ

SEPT 11/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.209 MILLION OZ INTO TEH SLV//: // /.////INVENTORY RESTS AT 439.727 MILLION OZ

SEPT 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 7/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 6/WITH SILVER DOWN 36 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.373 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 5/WITH SILVER DOWN 69 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 734,000 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 437.891 MILLION OZ

SEPT 1/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 440.00 MILLION OZ

AUGUST 31/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 438.625 MILLION OZ

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.834 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 443.210 MILLION OZ

AUGUST 29/WITH SILVER UP 49 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 183,000 OF SILVER INTO THE THE SLV// /.////INVENTORY RESTS AT 445.044 MILLION OZ

AUGUST 28/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.281 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 444.861 MILLION OZ

AUGUST 25/WITH SILVER UP ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.751 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 446.145 MILLION OZ

AUGUST 24/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.651 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 448.896 MILLION OZ

AUGUST 23/WITH SILVER UP 94 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 826,000 OZ FROM THE SLV// /.////INVENTORY RESTS AT 450.547 MILLION OZ

AUGUST 22/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: /.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 21/WITH SILVER UP 59 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 917,0000 OZ FROM THE SLV//.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 18/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 17/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 16/WITH SILVER DOWN 13 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 15/WITH SILVER DOWN 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 14/WITH SILVER DOWN 3 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.459 MILLION OZ INTOTHE SLV/: //////INVENTORY RESTS AT 452.565 MILLION OZ

AUGUST 11/WITH SILVER DOWN 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.926 MILLION OZ INTOTHE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 452.106 MILLION OZ

AUGUST 10/WITH SILVER UP 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 9/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 8/WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 7/WITH SILVER DOWN 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 4/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.294 MILLION OZ FROM THE SLV// OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 3/WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 189,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.281 MILLION OZ

AUGUST 2/WITH SILVER DOWN 43 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 275,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.471 MILLION OZ

AUGUST 1/WITH SILVER DOWN 61 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

3,Chris Powell of GATA provides to us very important physical commentaries

Alasdair Macleod: Currency wars vs. gold standards

Your weekend reading material:

Submitted by admin on Thu, 2023-09-14 11:57Section: Daily Dispatches

By Alasdair Macleod Head of Research, GoldMoney, Toronto via Schiff Gold, White Plains, New York Thursday, September 14, 1012

Russia and the Saudis are driving up oil and diesel prices. But these moves are likely to undermine the rouble more than they undermine the dollar, euro, and other major currencies.

Therefore, higher energy prices will rebound on the Russians this winter: If they shiver in Germany, they will freeze in Russia. If the dollar is king of the fiats, the rouble is just a lowly serf.

There is little doubt that Russian President Vladimir Putin and his advisers are aware of this problem. Plan A was to introduce a new gold-backed BRICS currency, which might be expected to weaken the dollar and euro relative to the rouble.

Plan B was more drastic: to back the rouble itself with gold. This is the financial equivalent of dropping a hydrogen bomb on the dollar and the global fiat currency system upon which it is based.

As well as demonstrating why there is no option for Russia but to back her currency with gold, this article shows why it is perfectly possible for Russia to do so during wartime and explains how it can be done.

It is, as a matter of fact, very easy for Russia to reintroduce a gold standard for the rouble, but the consequences for the global fiat currency system are nothing short of lethal. …

Japanese gold denominated in Yen is exploding in price reaching all time highs

(zerohedge)

Japanese Panic Buy Gold As Yen Implodes And Inflation Soars

THURSDAY, SEP 14, 2023 – 05:20 PM

A gold-buying frenzy in hyperinflating banana-republic basket cases such as Venezuela, Zimbabwe, Argentina or Turkey makes sense; one can also imagine Indians and Chinese liquidating rushing to buy the precious metal, as they periodically do (for other, not less relevant, reasons). But Japan?

That’s right: the otherwise quiet (and rapidly aging) population of Japan has found a new infatuation with gold, and it has the relentless money-printing juggernaut that is the BOJ to thank for it.

The retail gold price in Japan — the main reference price for the metal in the country — tracks global spot prices, which have been pushed up by the coronavirus pandemic, the war in Ukraine, the debt ceiling crisis in the US and global tensions between the east and west. But most of all, it reflects the dramatic collapse in the value of the yen, which recently passed ¥147 against the dollar, a level that last year triggered verbal market intervention by the Japanese authorities but this year has been widely ignored by a central bank which realizes that intervention at this point is futile and would only precipitate Japanese hyperinflation and systemic collapse.

And since Japan’s inflation, which recently surpassed that of the US, will keep rising…

… as the weak yen will only get weaker – occasional desperation intervention aside – as long as there was no signal from the Bank of Japan that it is ready to tighten its ultra-loose policy which won’t happen for a long time (and when it does, it will spark a collapse in the JGB bond market forcing the trapped BOJ to immediately reverse once again) demand for gold in Japan will only keep rising.

Economists cited by the FT, said the move in retail gold prices, which extends an 18-month rally at gold stores around Japan, was part of a rapid shift in household attitudes to risk as years of deflation have given way to rising consumer prices.

Imagine a world where the biggest source of demand for gold in Asia is not India but Japan, and where demand will only rise as the yen (inevitably) falls as it gets closer to its inevitable and catastrophic end. Well, we are pretty much there now.

Jesper Koll, an economist and adviser to the Japan Catalyst Fund, an investment fund, said the primary driver for the buying by Japanese households was an urgent search for inflation protection after years without strong incentive to move assets out of cash.

“The fact that gold is a non-yen asset helps, but the trigger is inflation,” said Koll, and since inflation in Japan is only going to rise, so will demand for gold.

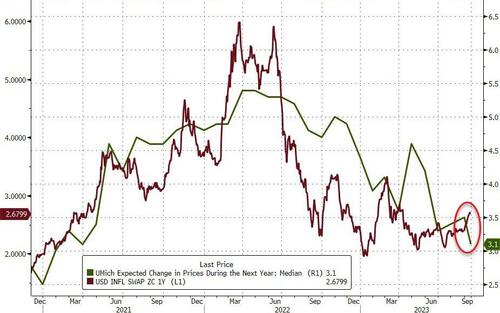

Japanese households emerged from the pandemic with a record of more than ¥2 quadrillion in accumulated assets or around four times the country’s annual gross domestic product. About half of that was held in cash and deposits — a balance closely eyed by Japan’s securities houses, which are trying to convince customers that inflation is here to stay and they now need to switch their savings into other financial products. The problem is that core CPI in Japan reached 3.1% last month.

“Inflation in Japan is at a crossroads,” said Tomohiro Ota, senior Japan economist at Goldman Sachs, noting that although consumer prices keep going up, some of the increase is down to temporary government subsidies while consumption growth has stalled since March. Goldman Sachs predicts that Japan’s currency will hit ¥155 against the dollar in the next six months.

Eiichiro Kato, a general manager for Tanaka Kikinzoku’s Precious Metals Retail Department, said that gold had become particularly attractive to customers concerned about the yen’s fall to multi-decade lows and their assets being denominated in yen.

Of course, it’s not just Japanese savers who are rushing to the safety of gold: a year of record gold purchases by central banks in a world where the dollar is now weaponized against enemies of Ukraine the Biden administration, has made it clear that demand for gold will only rise.

“We do not see many factors that would cause the dollar-denominated price to fall significantly, and we think that the yen-denominated price could rise further if the yen continues to weaken,” said Kato.

However, Hideo Kumano, chief economist at Dai-Ichi Research Institute, warned against reading too much into the rise in Japan’s gold price due to the small size of the market.

“It could prove to be an outlier and the country’s elderly population might not change their behaviour and start to consume, even if inflation does remain high,” he said. On the other hand, with deflation now dead and buried (at least until the next global depression) the odds that Japan’s notoriously thrifty population will continue to save at a time when its currency is collapsing are nil, especially since the BOJ itself has given up trying to contain the surge in yen-denominated gold…

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2772

OFFSHORE YUAN: UP TO 7.2774

SHANGHAI CLOSED DOWN 8.81 PTS OR 0.28%

HANG SENG CLOSED UP 134.97PTS OR 0.75%

2. Nikkei closed UP 364.79 OR 1.10%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 104.93 EURO RISES TO 1.0657 UP 22 BASIS PT

3b Japan 10 YR bond yield: RISES TO. +.703 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.83/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ON SHORE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.6515***/Italian 10 Yr bond yield DOWN to 4.410*** /SPAIN 10 YR BOND YIELD DOWN TO 3.713…**

3i Greek 10 year bond yield RISES TO 4.004

3j Gold at $1916.50 silver at: 23.02 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 45 /100 roubles/dollar; ROUBLE AT 96.89//

3m oil into the 90 dollar handle for WTI and 93 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.83// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.703% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8967 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9557well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.326 UP 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.407 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 5.032 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.98…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 1 BASIS PTS AT 4.3865

end

2.a Overnight: Newsquawk and Zero hedge:

USA EARLY MORNING REPORT

Futures Flat On Record $3.4 Trillion Triple-Witching Day As UAW Strike Begins

FRIDAY, SEP 15, 2023 – 08:49 AM

US equity futures traded flat to start today’s massive triple-witching option expiration, as the UAW labor union went on strike, while Arm Holdings shares rallied as much as 10% before turning red. As of 8:15am, S&P futures were flat while Nasdaq 100 futures dropped 0.1%; in Europe and Asia, stocks jumped on the back of better-than-expected economic data in China, which fueled hopes stimulus measures are paying off. Brent crude traded near $94 per barrel, at new YTD high, up 0.4% after rising 1.9% Thursday, putting additional upward pressure on Treasury yields while the dollar edged lower versus most major peers. Gold rose and bitcoin dropped.

In premarket trading, GM and Ford shares dropped about 2% before the official US open. The UAW started an unprecedented a strike, setting the stage for a protracted showdown and shutting down about half of US auto production.Unmute

Adobe fell over 2% after the software company gave an outlook that analysts see as conservative even as it reported third-quarter results that beat expectations. Arm Holdings rose as much as 10% after its IPO, before reversing all gains and turning red. Here are some other notable premarket movers:

Canopy Growth shares jump 10%, putting it on track to extend gains for a second session, after the cannabis company ceased funding for BioSteel Sports Nutrition on Thursday.

Celsius Holdings rises 0.7% is initiated outperform at Cowen, which says the growing appeal of the energy-drink maker’s differentiated product line-up is helping the firm continue to build US market share.

DoorDash 1.9% after MoffettNathanson downgrades shares to market perform from outperform, saying the resumption of student-loan payments introduces bookings risk to food-delivery businesses.

Iovance jumps 16% after the FDA extended its target action date for its treatment for advanced melanoma, lifileucel, saying that there are no major review issues.

Lindsay drops 12% as it is cut to hold from buy at Stifel, citing a challenging near-term outlook and lack of positive catalysts for the irrigation company.

Nikola climbs 11%, putting the electric-vehicle maker on track to extend Thursday’s 32% advance and end the week higher.

GM and Ford fell as the United Auto Workers started strikes at the companies’ plants.

Unity Software Inc. shares are up 4% after BofA upgraded the graphic tools provider to buy from neutral.

Markets were braced for Friday’s triple witching event, which at $3.4 trillion will be the biggest September options expiration in history…

… and which may trigger violent market swings, volume spikes and volatility as a huge number of pins centered around 4,500 matures and “unclenches” the gamma gravity which has kept the market from making large moves. Attention is also turning to the Federal Reserve’s meeting next week, with traders betting at the US will keep interest rates on hold and avoid a sharp economic slowdown.

Meanwhile, expectations that the ECB is done raising rates hammered the euro: the currency headed toward its ninth straight week of losses, the longest run on record. President Christine. Lagarde reiterated on Friday that the ECB isn’t discussing cuts in interest rates. She told reporters after a meeting of the Eurogroup that the level of borrowing costs and the length of time they stay elevated “will matter significantly,” without elaborating.

Equity funds saw the biggest weekly inflow in 18 months amid growing investor confidence the US economy is headed for a soft landing. Global stocks attracted $25.3 billion in the week to Sept. 13, the most since March 2022, according to EPFR data. “It looks like ‘happy hour’ for the market,” said Guillermo Hernandez Sampere, head of trading at asset manager MPPM. “To confirm the bull case, high cash piles must find their way into markets, and next week the Fed could send signals to initiate such action.”

European equities rallied after better-than-expected economic data in China fueled hopes stimulus measures are paying off. Euro Stoxx 50 climbs 1%. CAC 40 outperforms peers, adding 1.5%, boosted by exposure to luxury companies. Consumer products, autos and travel are the strongest performing sectors.

Earlier in the session, Asia stocks also rallied after Chinese industrial production and retail sales statistics beat estimates. The Chinese data showed the economy picking up steam in August as a summer travel boom and a heftier stimulus push boosted consumer spending and factory output. Here are the most notable European movers:

European luxury shares rise after Chinese industrial production and retail sales data beat estimates, easing fears consumers in the world’s second-largest economy would no longer be able to fuel growth for the sector.

Games Workshop shares jump as much as 11% after the table-top games maker said that recent trading was ahead of its expectations, with Jefferies saying that the quarter has been “outstanding” and Peel Hunt noting robust growth. Both brokers highlighted a successful launch for the company’s ‘Warhammer 40,000 Leviathan’ boxed set.

MorphoSys shares gain as much as 9.5% to the highest since January 2022 after Goldman Sachs upgraded its recommendation on the German biotech firm to neutral from sell ahead of results from a late-stage study.

Vitrolife shares rise as much 8.8% after Handelsbanken raised its short-term recommendation to buy from hold, citing the stock’s steep decline.

Pharming shares gain as much as 6.2% after Kempen upgraded the stock to buy from neutral, saying the Dutch biopharmaceutical company is “in growth mode” as it expands the sales opportunity for its Joenja drug.

H&M shares drop as much as 5.8%, the most since March, after the Swedish clothing retailer reported 3Q sales that missed estimates. The “flattish” net sales in local currencies suggest limited pricing power and a lack of traction with shoppers on product ranges, according to Bernstein.

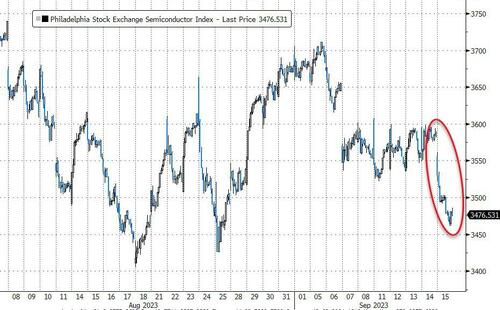

ASML and other European chip-equipment stocks fall on Friday after Reuters reported that TSMC asked its major suppliers to delay shipment of high-end chipmaking equipment.

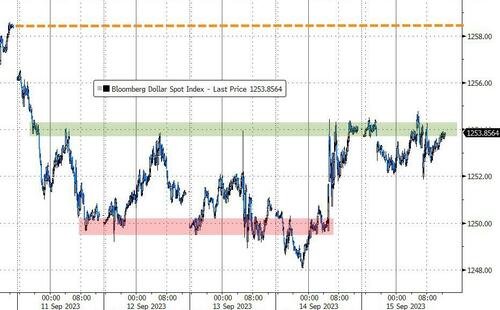

In FX, the Bloomberg dollar spot index is near flat. Yen and Canadian dollar are the weakest performers among G-10 peers.

In rates, Treasuries grind lower in early US session with futures near lows of the day, following wider losses in core European rates that pare most of Thursday’s post-ECB gains. Parallel yield shift across the curve leaves curve spreads little changed. US session has heavy economic data slate, headed by industrial production. US yields are cheaper by 3bp to 4bp across the curve with 10-year around 4.32%, cheaper by ~3.5bp on the day, outperforming bunds and gilts by 2.5bp and 3bp in the sector; both UK and German curves cheaper by 4bp to 6bp on the day. Dollar IG issuance slate empty so far with muted activity expected; three names priced $2.1b Thursday, taking weekly total above $34bn.

In commodities, crude futures advance. WTI drifts 0.3% higher to trade near $90.44. Spot gold rises roughly $7 to trade near $1,918/oz.

Bitcoin is a touch firmer on the session, holding around the USD 26.5k mark with newsflow light to end a busy week ahead of a particularly busy week for Central Bank activity.

To the day ahead now, and US data releases include industrial production and capacity utilisation for August, the Empire State manufacturing survey for September, and the University of Michigan’s preliminary consumer sentiment index for September. Otherwise, central bank speakers include ECB President Lagarde and the ECB’s Villeroy.

Market Snapshot

S&P 500 futures little changed at 4,509.00

STOXX Europe 600 up 0.8% to 464.76

MXAP up 0.6% to 164.01

MXAPJ up 0.7% to 509.24

Nikkei up 1.1% to 33,533.09

Topix up 0.9% to 2,428.38

Hang Seng Index up 0.7% to 18,182.89

Shanghai Composite down 0.3% to 3,117.74

Sensex up 0.4% to 67,761.76

Australia S&P/ASX 200 up 1.3% to 7,279.03

Kospi up 1.1% to 2,601.28

German 10Y yield little changed at 2.65%

Euro up 0.2% to $1.0665

Brent Futures up 0.5% to $94.17/bbl

Gold spot up 0.4% to $1,917.57

U.S. Dollar Index down 0.18% to 105.21

Top Overnight News

China economic data came in strong for Aug, with retail sales +4.6% Y/Y (up from +2.5% in Jul and ahead of the Street’s +3% forecast) and industrial production +4.5% (up from +3.7% in Jul and ahead of the Street’s +3.9% forecast). BBG

China injects more liquidity via its medium-term lending facility (the net injection was CNY191B), the second easing measure in as many days (after the RRR cut yesterday morning). BBG

Republican lawmakers are pressing the Biden administration to completely cut off Huawei Technologies Co. and Semiconductor Manufacturing International Corp. from their American suppliers after Huawei launched a new phone using highly advanced technology the US has been trying to keep out of China’s hands. BBG

The US government believes Chinese defense minister Li Shangfu has been placed under investigation in the latest sign of turmoil among elite members of Beijing’s military and foreign policy establishment. FT

BOJ officials see a discrepancy between what Governor Kazuo Ueda said in a recent interview and how traders interpreted the remarks, according to people familiar with the matter. Most of what Ueda said in the Yomiuri newspaper interview published Saturday was consistent with his routine remarks of late. Taken in total, his comments indicate little change in the view among officials that they’ll need to weigh both upside and downside risks in deciding whether to adjust policies. BBG

Italian and Portuguese politicians lashed out at the ECB’s latest rate hike, with the Italian Deputy PM Matteo Salvini accusing Christine Lagarde of “living on Mars.” Elsewhere, ECB officials Madis Muller and Luis de Guindos said current levels are probably sufficient to return inflation to the 2% target, reducing chances of further rate increases. BBG

House Republicans begin working on a 30-day continuing resolution to avoid a shutdown at the end of the month (the proposal will receive pushback from the Dem-controlled Senate, but it could form the basis for negotiations). The Hill

AAPL is relying on aggressive carrier subsidies to drive iPhone sales following a relatively underwhelming iPhone 15 debut. WSJ

Ford and GM shares fell premarket as 12,700 auto workers went on strike at targeted plants; Stellantis was little changed in Paris. Sites affected include a Ford factory in Michigan that makes the Bronco SUV, a GM facility in Missouri and a plant in Ohio that builds the Jeep Wrangler. It’s the first time the UAW has taken action against the Big Three legacy Detroit carmakers simultaneously. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks gained after global risk was fuelled by the upside in Europe and the US, while sentiment was also bolstered by better-than-expected Chinese activity data. ASX 200 was boosted with miners leading the advances seen across all sectors following the reserve ratio cut in China which is expected to release over CNY 500bln of liquidity for Australia’s largest trading partner and with recent comments from RBA watcher McCrann that there will likely be no more rate hikes. Nikkei 225 extended its gains amid notable outperformance in power companies and with SoftBank boosted after shares in its Arm unit climbed 25% in its US debut. Hang Seng and Shanghai Comp were both initially underpinned by the encouraging Chinese activity data in which Industrial Production and Retail Sales both topped forecasts, while attention was also on the PBoC which recently cut the RRR by 25bps but maintained its 1-year MLF rate at 2.50%, although Shanghai Comp later faded into the red.

Top Asian News

PBoC announced CNY 591bln (CNY 400bln maturing) through 1-year MLF with the rate maintained at 2.50%.

China reportedly told brokers to cut FX trading to shore up a weak yuan, according to Bloomberg.

PBoC injected CNY 105bln via 7-day reverse repos with the rate kept at 1.80% and CNY 34bln via 14-day reverse repos with the rate at 1.95% (prev. 2.15%).

China’s NBS said the economy saw accelerated demand but domestic demand remains insufficient and the foundation of the economic recovery needs to be consolidated. Furthermore, the stats bureau stated the domestic economy is recovering but still faces difficulties and that China should focus on expanding domestic demand.

US senior House Republicans urged the US Commerce Department to toughen export controls against Huawei and SMIC citing the new advanced smartphone from Huawei.

Sino-Ocean Group (3377 HK) announced the suspension of trading of offshore USD securities and said the group has been in talks with creditors, while it noted that the optimal path forward is holistic restructuring and payments under all of its offshore debts will be suspended until holistic restructuring and/or extension are implemented.

JP Morgan upgrades China’s 2023 GDP growth forecast to 5.0% (prev. 4.8%); Goldman Sachs maintains China’s Q3 GDP growth forecast 4.9% YY while acknowledging elevated uncertainties surrounding the property sector.

BoJ is said to see continued upside risks to the price outlook and discrepancy between recent comments by Governor Ueda and how traders interpreted the comments, according to Bloomberg citing sources.

European bourses are in the green, Euro Stoxx 50 +0.9%, as sentiment picks up following constructive Chinese data and after yesterday’s ECB announcement, despite subsequent sources. Sectors are mostly in the green with Consumer Products & Services the major outperformer, given Luxury names; with sectors exposed to China also underpinned. At the other end of the spectrum, Chip names are pressured following a Reuters source piece that TSMC told vendors to delay chip equipment delivery, citing nervousness about consumer demand. Stateside, futures are flat/mixed after the modest rally on Thursday, ES +0.1%; Arm gave the NQ +0.1% a helping hand and continues to climb in the pre-market. US auto names are pressured in pre-market trade as strike action commences; Ford (F) -1.7%.

Top European News

Several of the ECB’s more hawkish rate-setters believe that rates could rise again in December, in the scenario of hot wages and inflation, via FT citing sources. Three individuals involved in the September meeting said if EZ inflation were above forecast the door remains open to a hike in December, when the next set of projections are provided. One respondent said a “very negative surprise” on inflation would be needed for an October move.

ECB’s de Guindos says both headline and core CPI will continue to ease, any future cuts will depend on multiple factors, via Cope radio.

ECB’s Muller says no additional hikes expected in the coming months, though higher inflation could merit a further hike.

ECB’s President Lagarde says ECB will return to 2% inflation target, will set rates at restrictive level as long as needed for it.

ECB’s Kazaks says this week’s rate decision was not a ‘dovish hike’; does not preclude future decisions

ECB TLTRO.III September early repayment figure (EUR): 34.2bln (prev. 29.5bln).

Bank of England/Ipsos Inflation Attitudes Survey – August 2023: Median expectations of the rate of inflation over the coming year were 3.6%, up from 3.5% in May 2023.

FX

DXY idles above 105.000 after Thursday’s near 100 tick bounce on a combination of Euro losses and strong US data releases.

Yen retreats amidst a rebound in UST yields towards YTD lows vs. USD circa 147.87 after hitting resistance ahead of 147.00.

Yuan rebounds as Chinese activity data beats consensus and PBoC cuts 14-day reverse repo to provide more stimulus.

USD/CNY and USD/CNH probe 7.2500 and 7.2600 respectively.

Aussie extends gains vs Buck to 0.6470+ as iron ore soars.

Sterling and Euro recover as Gilts and EGBs retreat further than Treasuries

Cable back above 200 DMA after bounce from 1.2400, EUR/USD off multiple lows within 1.0635-69 range.

PBoC set USD/CNY mid-point at 7.1786 vs exp. 7.2849 (prev. 7.1874)

Fixed Income

Bonds in freefall following deeper reversal from post-ECB highs through levels prevalent prior to the ‘dovish’ hike.

Bunds towards base of 131.27-130.43 range, Gilts nearer 95.39 than 96.08 and T-note hovering close to 109-15+ having peaked at 109-28+.

Multiple factors weighing on debt including better-than-forecast Chinese data, ongoing strength in crude prices and hawkish ECB/BoJ sources.

Commodities

WTI and Brent futures are firmer intraday but off best levels, with overnight gains fuelled by the broader constructive tone and better-than-expected Chinese activity data.

Spot gold held onto the USD 1,900/oz handle yesterday despite the gains in the DXY, with the yellow metal climbing north of USD 1,915/oz in APAC trade, and briefly topped its 21 DMA (1,918.55/oz) as it eyes its 200 DMA at USD 1,921.93/oz.

Metals are relatively mixed and off best levels after seeing some upside on the aforementioned Chinese data, with 3M LME copper briefly rising above USD 8,500/t before waning alongside the mainland Chinese stock market.

Qatar set November-loading Al-Shaheen crude term price at about USD 2.73/bbl above Dubai quotes.

Turkish Energy Minister says a survey of the Iraq-Turkey oil pipeline is complete with a report expected soon; the pipeline will soon be technically operational.

Geopolitics

Russia seeks to expand its naval presence in the Mediterranean in which it wants access for its warships to a Mediterranean port in Libya, according to WSJ.

US Event Calendar

08:30: Sept. Empire Manufacturing +1.9, est. -10.0, prior -19.0

08:30: Aug. Import Price Index YoY, est. -2.8%, prior -4.4%

Aug. Import Price Index MoM, est. 0.3%, prior 0.4%

Aug. Export Price Index YoY, est. -6.8%, prior -7.9%

Aug. Export Price Index MoM, est. 0.4%, prior 0.7%

09:15: Aug. Industrial Production MoM, est. 0.1%, prior 1.0%

Aug. Manufacturing (SIC) Production, est. 0.1%, prior 0.5%

Aug. Capacity Utilization, est. 79.3%, prior 79.3%

10:00: Sept. U. of Mich. Sentiment, est. 69.0, prior 69.5

Sept. U. of Mich. Current Conditions, est. 74.8, prior 75.7

Sept. U. of Mich. Expectations, est. 65.0, prior 65.5

Sept. U. of Mich. 1 Yr Inflation, est. 3.5%, prior 3.5%

Sept. U. of Mich. 5-10 Yr Inflation, est. 3.0%, prior 3.0%

DB’s Jim Reid concludes the overnight wrap

If you thought patrolling a laser quest party for my twins was hard work two weeks ago, tomorrow we have a private party for Maisie’s 8th birthday at the local swimming pool. So I’ll be doing my best David Hasselhoff impression and operating as a lifeguard. Problem is Maisie is already 10x the swimmer I am so I’m hoping my skills won’t be required.

Markets haven’t required much saving over the last 24 hours, with risk assets posting a strong advance overcoming several potential pitfalls. Among others, we had a 25bp rate hike from the ECB, which was mostly expected by markets but went against the consensus of economists who were forecasting a pause. Then we had another relatively strong round of US data, which kept the idea of a further Fed hike firmly on the table. And if that wasn’t enough, oil prices hit another YTD high as Brent Crude surpassed $93/bbl (+1.98%), which raised the prospect of even more inflationary pressures still in the pipeline. We’re up above $94 in Asia. Countering this, China cut its RRR rate yesterday and their monthly data dump this morning was better than expected. Just when you thought it was safe to go back into the water watch out for triple witching today which brings huge volumes of derivative contracts simultaneously expiring across the board.

We’ll start with the ECB, who after much speculation announced a 25bp rate hike yesterday, which took their deposit rate up to 4%. That’s the highest level for the deposit rate since the ECB’s creation, exceeding the previous peak back in 2000. And having now delivered 450bps of rate hikes over the last 15 months, it also marks the fastest pace of tightening they’ve ever done as well. Indeed, even if you go back before the ECB’s formation and look at previous tightening episodes from the German Bundesbank, they’ve now delivered as much tightening in the space of 15 months as the Bundesbank did from the start of our data in 1948.

President Lagarde said that a “solid majority” were in favour of the decision to hike rates (which sounds less convincing than the “large” or “overwhelming” majorities seen in the recent past). The Governing Council’s statement said they thought rates were now at levels that if “maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to the target.” The statement also said that “future decisions will ensure that the key ECB interest rates will be set at sufficiently restrictive levels for as long as necessary.”

In its forecasts, the ECB raised the inflation projections for this year to +5.6% (vs. 5.4% in June), and for 2024 to +3.2% (vs. +3.0% in June), although this was largely due to energy prices with the core inflation projection a touch lower for 2024 and 2025. So the recent oil price rise may have played a sizeable part in the rationale for yesterday’s hike. The growth forecast was revised down as the ECB pushed out its expected recovery from H2-23 to H1-24, with 2024 growth downgraded half a point to +1.0% as a result.

Obviously the question for markets is whether that’s it for the ECB’s tightening cycle, though President Lagarde said “we can’t say” that. Our European economists see a mild hawkish bias persisting, but with a long pause being the baseline. In their view, it would take a substantial surprise relative to ECB expectations to deliver another hike, with duration of restrictive policy now the more relevant policy dimension. See their full ECB reaction note here.

Looking forward, markets are now pricing a 45% likelihood of another hike from the ECB by year-end. So as with the Fed, investors are clearly still alive to the prospect of further hikes. But in spite of that, we actually saw a big reduction in bond yields over the day, with 10yr bunds (-5.8bps) and OATs (-6.9bps) seeing their strongest rally in two weeks, possibly because the market thinks the ECB is getting ahead of the inflation curve or that they are over hiking and taking the economy to a recession and will have to cut sooner. The strong equity performance (see below) might argue against the latter interpretation! Italy’s BTPs (-10.7bps) outperformed, also helped by President Lagarde’s comments noting the importance of PEPP flexibility, suggesting a high hurdle for early exit from PEPP reinvestments that are part of the ECB’s anti-fragmentation toolkit. The euro itself also weakened noticeably, ending the day -0.86% lower against the US Dollar at $1.065, which is the second lowest close (and the largest daily decline) since March.

The stronger dollar narrative was also buoyed by greater optimism about the state of the US economy, with a fresh round of data that added to hopes of a soft landing. First up, the retail sales numbers for August grew by +0.6% (vs. +0.1% expected), and the measure excluding autos and gas was also up +0.2% (vs. -0.1% expected). Within the details of the print, retail control (which enters goods spending in GDP) was actually a touch below consensus when accounting for revisions. But this is still tracking at a strong 5% annualised in Q3, according to our US economists. Secondly, the weekly initial jobless claims came in at 220k (vs. 225k expected) over the week ending September 9, which takes the 4-week moving average down to its lowest level since late February.

Treasury yields saw choppy price action around the US releases and the ECB meeting but a risk-on mood prevailed, with yields moving higher across the curve. The 10yr yield was up +3.8bps to 4.29%, while the 2yr rose back above 5% (+4.3bp to 5.01%). Those moves were given further momentum by the latest PPI data for August, which also showed that inflation was a bit stronger than thought, with the headline measure at a monthly +0.7% (vs. +0.4% expected). So that was certainly consistent with the prospect that the Fed could yet deliver another hike by the end of the year, and futures are still pricing in a 43% likelihood they’ll do so. This was a slight decline from 47% the day before, but with end-24 Fed funds pricing (+7.7bp) closing at a new high of 4.50%.

For equities, this was all great news, and the economic optimism led to a strong rally on both sides of the Atlantic. In the US, the S&P 500 posted both the strongest (+0.84%) and the broadest advance so far this month, with 429 of its constituents and each of the 24 industry groups positive on the day. Bank stocks (+1.79%) were among the strongest performers in the S&P 500, while small cap stocks also outperformed with the Russell 2000 up +1.40%. Over in Europe, the gains were even stronger, and the STOXX 600 surged +1.52% to a one-month high, whilst the FTSE 100 (+1.95%) had its best daily performance since last November.

The other big story in the background has been the ongoing rise in commodity prices, and oil in particular. Yesterday saw Brent Crude close above $93/bbl for the first time so far in 2023 (+1.98% to $93.70), having traded above $94/bbl late it the day. It has moved higher overnight, trading at $94.50/bbl as I type. The ongoing oil price rally is likely to lead to further pressure on gasoline prices. Separately, another potential risk for commodities (including food prices) is the current El Nino event, and yesterday we got the latest forecasts from the US Climate Prediction Center. They said there was now a 73% likelihood that this current El Nino develops into a strong one over Q4, which would be the first time we’ve had a strong one since the 2014-16 event.

Overnight in Asia risk on continues alongside a batch of China’s economic data for August that came in better than anticipated. The Hang Seng (+1.58%) is leading gains even if mainland Chinese markets are a bit more subdued, with the CSI (+0.07%) and the Shanghai Composite (+0.27%) only edging up. Elsewhere, the Nikkei (+1.34%) and the KOSPI (+1.30%) are sharply higher. S&P 500 (+0.20%) and NASDAQ 100 (+0.23%) futures are moving higher.

Coming back to China, industrial output as well as retail sales picked up in August indicating that the recent flurry of support measures may be slowly starting to have an effect. Industrial production advanced +4.5% y/y in August (v/s +3.9% expected), faster than the +3.7% increase in July while retail sales grew by +4.6% y/y in August beating market expectations for a +3.0% gain as against a rise of +2.5% in July. However, Fixed asset investment grew by 3.2% y/y in August on a year-to-date basis missing market expectations for a +3.3% increase, and slower than last month’s +3.4% uptick.

Additionally, the Chinese central bank further ramped up stimulus by adding a net 191 billion yuan into the financial system via a one-year policy loan, a day after announcing another cut (+25 bps) to lenders’ reserve requirements. According to some estimates, this measure is expected to free up as much as 500 billion yuan. The central bank kept the medium-term lending facility (MLF) borrowing cost unchanged at 2.5%, after a surprise 15bps cut last month. The Chinese yuan has risen by +0.31%, trading at 7.57 against the dollar following the August data releases while yields on the 10yr government bonds moved higher by +2.3bps to 2.65% as we go to print.

To the day ahead now, and US data releases include industrial production and capacity utilisation for August, the Empire State manufacturing survey for September, and the University of Michigan’s preliminary consumer sentiment index for September. Otherwise, central bank speakers include ECB President Lagarde and the ECB’s Villeroy.

END

2 B) NOW NEWSQUAWK (EUROPE/REPORT)/

Sentiment improves after Chinese data, DXY over 105.00, Yuan rebound & JPY pressured – Newsquawk US Market Open

FRIDAY, SEP 15, 2023 – 06:47 AM

European bourses are in the green as sentiment improves after constructive Chinese data

Though, US futures are more contained with specifics light into Quad Witching

DXY idles above 105.00, JPY pressured as yields lift despite sources while Yuan rebounds on mentioned data

Fixed benchmarks under pressure in a marked reversal of post-ECB highs with multiple factors weighing

Crude benchmarks firmer intraday, though shy of best, metals more mixed

Looking ahead, highlights include US UoM Sentiment, NY Fed Manufacturing, Import & Export Prices. CBR’s Nabiullina, Quad Witching.

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

European bourses are in the green, Euro Stoxx 50 +0.9%, as sentiment picks up following constructive Chinese data and after yesterday’s ECB announcement, despite subsequent sources.

Sectors are mostly in the green with Consumer Products & Services the major outperformer, given Luxury names; with sectors exposed to China also underpinned.

At the other end of the spectrum, Chip names are pressured following a Reuters source piece that TSMC told vendors to delay chip equipment delivery, citing nervousness about consumer demand.

Stateside, futures are flat/mixed after the modest rally on Thursday, ES +0.1%; Arm gave the NQ +0.1% a helping hand and continues to climb in the pre-market.

US auto names are pressured in pre-market trade as strike action commences; Ford (F) -1.7%.

WTI and Brent futures are firmer intraday but off best levels, with overnight gains fuelled by the broader constructive tone and better-than-expected Chinese activity data.

Spot gold held onto the USD 1,900/oz handle yesterday despite the gains in the DXY, with the yellow metal climbing north of USD 1,915/oz in APAC trade, and briefly topped its 21 DMA (1,918.55/oz) as it eyes its 200 DMA at USD 1,921.93/oz.

Metals are relatively mixed and off best levels after seeing some upside on the aforementioned Chinese data, with 3M LME copper briefly rising above USD 8,500/t before waning alongside the mainland Chinese stock market.

Qatar set November-loading Al-Shaheen crude term price at about USD 2.73/bbl above Dubai quotes.

Turkish Energy Minister says a survey of the Iraq-Turkey oil pipeline is complete with a report expected soon; the pipeline will soon be technically operational.

UAW President announced workers’ strikes at the Stellantis (STLA) Toledo Jeep plant, Ford’s (F) Bronco assembly plant in Michigan and GM’s (GM) Wentzville mid-size truck plant from midnight, while Ford said the UAW made a counterproposal but showed little movement from initial demands.

Several of the ECB’s more hawkish rate-setters believe that rates could rise again in December, in the scenario of hot wages and inflation, via FT citing sources. Three individuals involved in the September meeting said if EZ inflation were above forecast the door remains open to a hike in December, when the next set of projections are provided. One respondent said a “very negative surprise” on inflation would be needed for an October move.

ECB’s de Guindos says both headline and core CPI will continue to ease, any future cuts will depend on multiple factors, via Cope radio.

ECB’s Muller says no additional hikes expected in the coming months, though higher inflation could merit a further hike.

ECB’s President Lagarde says ECB will return to 2% inflation target, will set rates at restrictive level as long as needed for it.

ECB’s Kazaks says this week’s rate decision was not a ‘dovish hike’; does not preclude future decisions

ECB TLTRO.III September early repayment figure (EUR): 34.2bln (prev. 29.5bln).

Bank of England/Ipsos Inflation Attitudes Survey – August 2023: Median expectations of the rate of inflation over the coming year were 3.6%, up from 3.5% in May 2023.

NOTABLE EUROPEAN DATA

EU Wages In Euro Zone (Q2 2023) 4.6% (Prev. 4.6%); Labour Costs YY (Q2 2023) 4.5% (Prev. 5.0%)

CBR hikes by 100bps as expected to 13.00%; sees its key rate in the 9.6-9.7% range (prev. view 7.9-8.3%)).

GEOPOLITICS

Russia seeks to expand its naval presence in the Mediterranean in which it wants access for its warships to a Mediterranean port in Libya, according to WSJ.

CRYPTO

Bitcoin is a touch firmer on the session, holding around the USD 26.5k mark with newsflow light to end a busy week ahead of a particularly busy week for Central Bank activity.

APAC TRADE

APAC stocks gained after global risk was fuelled by the upside in Europe and the US, while sentiment was also bolstered by better-than-expected Chinese activity data.

ASX 200 was boosted with miners leading the advances seen across all sectors following the reserve ratio cut in China which is expected to release over CNY 500bln of liquidity for Australia’s largest trading partner and with recent comments from RBA watcher McCrann that there will likely be no more rate hikes.