next week beginning Monday April 20 through to Thursday,April 23, I will be out of the picture

for the 4 days. Thus I cannot do my normal report

I will provide the comex preliminary numbers and publish that as a work in progress. I will finalize the numbers late at night.

for you. HARVEY

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: APRIL 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,800.000000000 USD

INTENT DATE: 04/15/2026 DELIVERY DATE: 04/17/2026

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DEUTSCHE BANK AG 6

323 C HSBC 57

363 H WELLS FARGO SECURITI 61

365 C MAREX CAPITAL MARKET 1

555 C BNP PARIBAS SEC CORP 25

657 C MORGAN STANLEY 1

661 C JP MORGAN SECURITIES 11

737 C ADVANTAGE FUTURES 6

905 C ADM 2 2

TOTAL: 86 86

MONTH TO DATE: 18,296

MONTH TO DATE: 18,296

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2026: 86 CONTRACTs NOTICES FOR 8,600 OZ or 0.2678TONNES

total notices so far: 18,296 contracts FOR 1,829,600 OZ OR 56.908 TONNES

SILVER NOTICES: 480 NOTICE(S) FILED FOR 2.400 MILLION OZ /

total number of notices filed so far this month : 2713 CONTRACTS (NOTICES) for 13.565 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A STRONG QUEUE JUMP OF 42 CONTRACTS OR 0.210 MILLION OZ/NEW STANDING REDUCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 470 CONTRACT QUEUE JUMP WHERE 2.305 MILLION ADDITIONAL OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES HUGELY TO 13.705 MILLION OZ

SUMMARY OF OUR APRIL 2026 COMEX CONTRACT MONTH:

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 17.320 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 2.305 MILLION OZ QUEUE JUMP//NEW STANDING ADVANCES TO 13.705 MILLION OZ

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR FAIR 37 CONTRACT QUEUE JUMP FOR 3700 OZ//NEW STANDING ADVANCES TO 58.024 TONNES

MARCH:: SMALL INITIAL STANDING FOR GOLD FOR MARCH AT 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 46 CONTRACT QUEUE JUMP OF 4400 OZ OR 0.2320 TONNESAND THEN WE ADD BY OUR THREE EXCHANGE FOR RISK: 22.3818///NEW STANDING ADVANCES TO 67.6648 TONNES OF GOLD./

APRIL: INITIAL STANDING FOR GOLD; 52.600 TONNES FOLLOWED BY TODAY’S 1,500 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 57.552 TONNES.

STANDING FOR THE LAST 4 MONTHS JANUARY TO APRIL:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 3700 OZ QUEUE JUMP (0.1150 TONNES): NEW STANDING ADVANCES TO 58.024 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 45.597 TONNES// WILL BE VERY SMALL THIS MONTH

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONG

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE 814 CONTRACTS

EFP ISSUANCE 190 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 190 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 814 CONTRACTS AND ADD TO THE 190 E.FP. ISSUED

WE OBTAIN A STRONG SIZED LOSS OF 624 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN OF $0.01

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 3.120 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $0.01

2.ASIAN AFFAIRS APRIL 16 /2025

SHANGHAI CLOSED UP 28.41 PTS OR 0.70%

HANG SENG CLOSED UP 414,68 PTS OR 1.60%

Nikkei CLOSED UP 1441.26 PTS OR 2.48%

//Australia’s all ordinaries CLOSED DOWN 0.40%

//Chinese yuan (ONSHORE) CLOSED UP 6.8166

/ OFFSHORE CLOSED UP AT 6.8144 Oil UP TO 92.02 dollars per barrel for WTI and BRENT DOWN TO 95.50 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING 6.8166 (UP) OFFSHORE YUAN TRADING UP TO 6.8144 ONSHORE YUAN TRADING BELOW OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL 608 CONTRACTS DOWN TO AN OI OF 361,666 CONTRACTS (OI) , HAVING ADVANCED FROM OUR NEW LOW OI SET THIS MONTH AND SURPASSING THE PREVIOUS ALL TIME LOW IN OI OF 354,581 SET APRIL6/2026. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 354,581 WITH GOLD AT AN EXTREMELY HIGH $4700.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD NO T.A.S. LIQUIDATION DURING WEDNESDAY’S TRADING. IT SEEMS THAT THE SPECULATORS CONTINUED AGAIN TO GO MASSIVELY ON THE LONG SIDE WITH THE BANKERS TAKING THE SHORT SIDE, SUPPLYING THE NECESSARY PAPER, AS WELL AS COVERING THEIR SHORTFALL.

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE MASSIVE AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS APRIL CONTRACT MONTH!!

THE SMALL SIZED GAIN ON OUR TWO EXCHANGES OCCURRED WITH OUR LOSS IN PRICE IN GOLD. THE SPECS HAVE NOW GONE MASSIVELY ON THE LONG SIDE AGAIN WITH THE BANKERS BUYING UP ALL THEY COULD AND COVERING THEIR SHORTFALL IN GOLD.

WE THUS HAD A SMALL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 419 CONTRACTS (OR 1.303 TONNES) DESPITE OUR LOSS IN PRICE, AS WE WERE INFORMED OF A FAIR 1027 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE..

THEN WE WERE NOTIFIED TODAY OF A ZERO CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0.0 TONNES OF GOLD.

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 0 EXCHANGE FOR RISK FOR FAR.

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO APRIL:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 0 EXCHANGE FOR RISK SO FAR.

DETAILS ON OUR NEW APRIL COMEX CONTRACT MONTH//

IN TOTAL WE HAD A SMALL SIZED GAIN ON OUR TWO EXCHANGES OF 419 CONTRACTS WITH OUR LOSS IN PRICE ($24.15). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH APRIL/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A STRONG SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 2575 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING THIS WEEK WITH MUCH FAILURE DURING LONDON LBMA/OTC OPTION EXPIRY WEEK!! (APRIL FIRST DAY NOTICE)

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD.

FOR MARCH WE HAVE 3 EXCHANGE FOR RISK ISSUANCES SO FAR FOR 7196 CONTRACTS OR 719,600 OZ/22.3818 TONNES.. AS DELIVERIES OF GOLD THESE PAST SEVERAL MONTHS HAVE BEEN HUGE!!

APRIL: 0 SO FAR HAVE BEEN ISSUED

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

AND NOW APRIL 2026: INITIAL STANDING FOR GOLD: 52.600 TONNES FOLLOWED BY TODAY’S FAIR 3700 OZ (0.1150 TONNES) QUEUE JUMP. THUS STANDING FOR GOLD AT THE COMEX ADVANCES TO 58.024 TONNES.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING APRIL,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $24.15)

WE HAD ZERO T.A.S. SPREADER LIQUIDATION // COMEX SESSION// DESPITE OUR LOSS IN PRICE , OUR LONG SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI //

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

WEDNESDAY NIGHT//THURSDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 7 MONTHS:

STANDING FOR GOLD OCT THROUGH TO APRIL:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977TONNES

4. JANUARY:

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

10. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR LATEST QUEUE JUMP OF 0.0298 TONNES TO WHICH THIS IS ADDED TO ALL OTHER QUEUE JUMPS OF 41.2082 / NEW QUEUE JUMP ADVANCES TO: 41.233 TONNES//STANDING ADVANCES TO: 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES/NEW STANDING ADVANCES TO 157.879 TONNES

MARCH: INITIAL STANDING: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TO WHICH WE THEN ADD OUR THREE EXCHANGE FOR RISK FOR 22.3818 TONNES// GOLD STANDING ADVANCES TO: 67.6648 TONNES/

APRIL: INITIAL STANDING: A VERY STRONG 52.600 TONNES FOLLOWED BY TODAY’S FAIR 3700 OZ QUEUE JUMP (0.1150 TONNES). THUS STANDING FOR GOLD AT THE COMEX ADVANCES TO 58.024 TONNES

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $24.15

WE HAD A HUGE 2734 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES : 419 CONTRACTS OR 41,900 OZ OR 1.303TONNES

INITIAL GOLD COMEX

APRIL DELIVERY MONTH

APRIL 16 2026

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | ENTRIES; 2 2 entries a) Brinks 115,453.170 oz b) HSBC: 34,447.566 oz total withdrawal: 149.,900.736 in tonnes 4.66 |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 1 ENTRY i) Into Brinks: 20,000.00000 oz ???? total deposit: 20,000.000 oz xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 86 CONTRACTS OR 8600 OZ 0.2674 TONNES OF GOLD |

| No of oz to be served (notices) | 359 Contracts 35,900 OZ 1.117 TONNES |

| Total monthly oz gold served (contracts) so far this month | 18,296 notices 1,829,600 oz 56.908 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

DEPOSITS/CUSTOMER

1 ENTRY

i) Into Brinks: 20,000.00000 oz ????

total deposit: 20,000.000 oz

xxxxxxxxxxxxxxxxxx

comex withdrawals:

ENTRIES; 2

2 entries

a) Brinks 115,453.170 oz

b) HSBC: 34,447.566 oz

total withdrawal: 149.,900.736

in tonnes 4.66

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs

adjustments: / / 2

ADJUSTMENTS ://DEALER TO CUSTOMER

a) Loomis 96,453.000 oz

b) Manfra 3,396.558 oz

total removal from dealer account; 100,249.936 oz or 3.118 tonnes

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF APRIL OI STANDS AT 445 CONTRACTS HAVING A LOSS OF 81 CONTRACTS.

WE HAD 118 CONTRACTS SERVED UPON WEDNESDAY SO WE GAINED A FAIR SIZED QUEUE JUMP OF 37 CONTRACTS. THUS 3700 OZ OF ADDITIONAL GOLD WILL STAND ON THIS SIDE OF THE BORDER AND THIS EQUATES TO 0.1180 TONNES.

MAY LOST 9 CONTRACTS TO AN OI OF 3075

JUNE IS A HUGE DELIVERY MONTH AND HERE THE OI FELL BY 856 CONTRACTS DOWN TO AN OI OF 265,975

We had 86 contracts filed for today representing 8,600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 11 notices issued from their client or customer account. The total of all issuance by all participants equate to 86 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for APRIL. /2026. contract month, we take the total number of notices filed so far for the month (18,296) to which we add the difference between the open interest for the front month of APRIL (445 CONTRACTS) minus the number of notices served upon today 86 x 100 oz per contract) equals 1,865,500 OZ OR (58.024 Tonnes of gold)

THUS: INITIAL total number of gold ounces standing for APRIL. /2026. contract month, we take the total number of notices filed so far for the month (18,296) to which we add the difference between the open interest for the front month of APRIL ( 445 CONTRACTS) minus the number of notices served upon today 86 x 100 oz per contract) equals 1,865,500 OZ OR (58.024Tonnes of gold)

new total of gold standing in APRIL is 58.024 TONNES//

TOTAL COMEX GOLD STANDING FOR APRIL 58.024 TONNES TONNES WHICH IS NOW HUGE FOR THIS NORMALLY VERY ACTIVE ACTIVE DELIVERY MONTH OF APRIL.

confirmed volume WEDNESDAY confirmed 116,,943 poor

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,926,418.685 oz 59.91 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,926,418.685 tonnes oz 59.91 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 30,015,182.013 oz

TOTAL REGISTERED GOLD 15,777,724.632 or 490.753 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 14,237,459.381 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,851,306 oz ((REG GOLD- PLEDGED GOLD)=

430.833 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

APRIL DELIVERY MONTH

APRIL16

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 4 entries i) out of Brinks 620,385.490 oz ii) Out of CNT 188,742.910oz iii) Out of Delaware 3,000.000 oz ??? iv) Out of JPMorgan 653,684.400 oz total withdrawal: 1,465,812.810 oz |

| Deposits to the Dealer Inventory | 1 entries 1 entries i) Into Loomis: 59,974.000 oz ???? total deposit 59,974.000 oz ??? xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT zero |

| No of oz served today (contracts) | 480 CONTRACT(S) ( 2.400 MILLION OZ |

| No of oz to be served (notices) | 28 Contracts (0.140 MILLION oz) |

| Total monthly oz silver served (contracts) | 2713 contracts 13.565 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

1 entries

i) Into Loomis: 59,974.000 oz ????

total deposit 59,974.000 oz ???

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

nil

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

4 entries

i) out of Brinks 620,385.490 oz

ii) Out of CNT 188,742.910oz

iii) Out of Delaware 3,000.000 oz ???

iv) Out of JPMorgan 653,684.400 oz

total withdrawal: 1,465,812.810 oz

the comex is being drained of silver

the comex is being drained of silver

adjustments:

one adjustments customer to dealer: Manfra

a) Manfra 99,713.312 oz

WEDNESDAY volume: 55,389 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 77.120 MILLION OZ//.TOTAL REG + ELIGIBLE. 320.293 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL /2026 OI: 445 OPEN INTEREST CONTRACTS FOR A LOSS OF ONLY 106 CONTRACTS. WE HAD 576 CONTRACTS SERVED ON WEDNESDAY, SO WE GAINED 470 CONTRACTS OR 2.305 MILLION OZ UNDERWENT ANOTHER HUGE QUEUE JUMP FOR THE SECOND STRAIGHT DAY. STANDING THUS ADVANCES TO 13.705 MILLION OZ WHICH IS HUGE FOR THIS NORMALLY SMALL NON ACTIVE DELIVERY MONTH OF APRIL

MAY SAW A LOSS OF 1840 CONTRACTS DOWN TO 48,179 CONTRACTS.

JUNE SAW A GAIN OF 75 CONTRACTS UP TO 741 OI CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 480 or 2.400 MILLION oz

CONFIRMED volume; ON WEDNESDAY; 55,389 fair

AND NOW APRIL. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 2713 X5,000 oz = 13.565 MILLION oz

to which we add the difference between the open interest for the front month of APRIL (508) AND the number of notices served upon today (480)x (5000 oz)

Thus the standings for silver for the APRIL 2026 contract month: (2713 )Notices served so far) x 5000 oz + OI for the front month of APRIL (508) minus number of notices served upon today (480 )x 5000 oz equals silver standing for the APRIL..contract month equating to 13.705 MILLION OZ.

NEW STANDING: 13.705 MILLION OZ WHICH IS HUGE FOR A GENERALLY LOUSY DELIVERY MONTH OF APRIL.

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 77.120 million oz of registered silver

JPMorgan as a percentage of total silver: 143.609/320.293million: 44.84%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

APRIL 16/2026/WITH GOLD DOWN $15.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.285 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1051.783 TONNES

APRIL 15/2026/WITH GOLD DOWN $24.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.289 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1049.478 TONNES

APRIL 14/2026/WITH GOLD UP $83.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.714 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1047.192 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 10/2026/WITH GOLD DOWN $11.90 TODAY/SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.724 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.42 TONNES

APRIL 9/2026/WITH GOLD UP $42.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.429 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.990 TONNES

APRIL 8/2026/WITH GOLD UP $88.95 TODAY/NO CHANGES IN GOLD AT THE GLD A//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 7/2026/WITH GOLD UP $5.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 3.429 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 6/2026/WITH GOLD UP $5.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/INVENTORY RESTS AT 1050.99 TONNES

APRIL 2/2026/WITH GOLD DOWN $132.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.714 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1050.99 TONNES

APRIL 1/2026/WITH GOLD UP $134.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 1.143 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1047.276 TONNES

MAR 31/2026/WITH GOLD UP $119.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.429 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1046.133 TONNES

MAR 30/2026/WITH GOLD UP $33.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.143 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1049.562

MAR 27/2026/WITH GOLD UP $103.55 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.285 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1052.705

MAR 26/2026/WITH GOLD DOWN $213.05 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.580 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1052.42

MAR 25/2026/WITH GOLD UP $155.30 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.300 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1053.000

MAR 24/2026/WITH GOLD DOWN $7.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4.286 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1052.705

MAR 23/2026/WITH GOLD DOWN $165.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 5.149 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1056.991

MAR 20/2026/WITH GOLD DOWN $39,55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4.855 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1062.135

MAR 19/2026/WITH GOLD DOWN $XXX TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 2.57 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1066.99

MAR 18/2026/WITH GOLD DOWN $111.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 1.144 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1069.564 TONNES

MAR 17/2026/WITH GOLD UP $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 0.857 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1070.708 TONNES

MAR 16/2026/WITH GOLD DOWN $60.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4/327 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1071/.565 TONNES

MAR 13/2026/WITH GOLD DOWN $61.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 1.428 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1075.852 TONNES

MAR 12/2026/WITH GOLD DOWN $49.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 3.715 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1077.28 TONNES

MAR 11/2026/WITH GOLD DOWN $70.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 2.858 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1073.565 TONNES

MAR 10/2026/WITH GOLD UP $137.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 2.614 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1070.707 TONNES

GLD INVENTORY: 1051..763 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

APRIL 16 WITH SILVER DOWN $1.00: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.132 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.477 MILLION OZ

APRIL 15 WITH SILVER UP $0.01: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.588 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.579 MILLION OZ

APRIL 14 WITH SILVER UP $3.99: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.633 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.991 MILLION OZ

APRIL 13 WITH SILVER DOWN 0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.589 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.624 MILLION OZ

APRIL 10 WITH SILVER DOWN 0.16: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.724 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 492.213 MILLION OZ

APRIL 9 WITH SILVER UP $0.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.173 MILLION OZ INTO THE SLV// // :INVENTORY RESTS AT 492.937 MILLION OZ

APRIL 8 WITH SILVER UP $3.50: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 7 WITH SILVER DOWN $0.89: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 6 WITH SILVER UP $0.41: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL WITHDRAWAL OF 0.224 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 2 WITH SILVER DOWN $3.57: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.091 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.988 MILLION OZ

APRIL 1 WITH SILVER UP $1.38: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE AND WITHDRAWAL OF 0.453 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 491.079 MILLION OZ

MAR 31 WITH SILVER UP $4.22: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE AND FRAUDULENT WITHDRAWAL OF 3.893 MILLION OZ FROM THE SLV // :INVENTORY RESTS AT 491.532 MILLION OZ

MAR 30 WITH SILVER UP $0.74: NO CHANGES IN SILVER INVENTORY AT THE SLV: // :INVENTORY RESTS AT 495.425 MILLION OZ

MAR 27 WITH SILVER UP $1.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 3.351 MILLION OZ FROM THE SLV// :INVENTORY RESTS AT 495.425 MILLION OZ

MAR 26 WITH SILVER DOWN $4.75: NO CHANGES IN SILVER INVENTORY AT THE SLV// :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 25 WITH SILVER UP $3.25: NO CHANGES IN SILVER INVENTORY AT THE SLV// :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 24 WITH SILVER DOWN $0.15: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT DEPOSIT OF 10.505 MILLION OZ INTO THE SLV :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 23 WITH SILVER UP $0.06: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// NO CHANGE IN INVENTORY/.. ./ :INVENTORY RESTS AT 488.271 MILLION OZ

MAR 20 WITH SILVER DOWN $1.92: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.490 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 488.271 MILLION OZ

MAR 19 WITH SILVER DOWN $6.22: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.9444 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 490.761 MILLION OZ

MAR 18 WITH SILVER DOWN $2.36: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 1.087 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 494.792 MILLION OZ.

MAR 17 WITH SILVER DOWN $0.89: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.351 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 493.705 MILLION OZ.

MAR 16 WITH SILVER DOWN $0.57: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.536 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 497.056 MILLION OZ.

MAR 13 WITH SILVER DOWN $3.83: NO CHANGES IN SILVER INVENTORY AT THE SLV// . ./ :INVENTORY RESTS AT 499.592

MAR 12 WITH SILVER DOWN $0.51 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// ANOTHER MONSTER WITHDRAWAL OF 3.713 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 499.592 MILLION OZ

MAR 11 WITH SILVER DOWN $3.96 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// ANOTHER MONSTER WITHDRAWAL OF 1.812 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 503.305 MILLION OZ

MAR 10 WITH SILVER UP $5. HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 1.63 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 505.117 MILLION OZ

MAR 9 WITH SILVER DOWN $0.30 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 1.54 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 506.747 MILLION OZ

CLOSING INVENTORY 490.447 MILLION OZ OF SILVER..

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

MATHEW PIEPENBURG…

XXX

JOHN RUBINO

Interviews With KER, WBB, Coffee and a Mike, USAWatchdog

| John RubinoApr 16 |

You’re currently a free subscriber to John Rubino’s Substack. For the full experience, upgrade your subscription.

ALASDAIR MACLEOD

NO 268 DR STEPHEN LEEB…

4. ANDREW MAGUIRE/LIVE FROM THE VAULT NO 267

end.

5. COMMODITY REPORT//..COPPER

ASIAN AFFAIRS APRIL 16/2026

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 28.41 PTS OR 0.70%

HANG SENG CLOSED UP 414,68 PTS OR 1.60%

Nikkei CLOSED UP 1441.26 PTS OR 2.48%

//Australia’s all ordinaries CLOSED DOWN 0.40%

//Chinese yuan (ONSHORE) CLOSED UP 6.8166

/ OFFSHORE CLOSED UP AT 6.8144 Oil UP TO 92.02 dollars per barrel for WTI and BRENT DOWN TO 95.50 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING 6.8166 (UP) OFFSHORE YUAN TRADING UP TO 6.8144 ONSHORE YUAN TRADING BELOW OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 6.8166

OFFSHORE YUAN: UP TO 6.8144

1.HANG SANG CLOSED UP 414.68 PTS OR 1.40%

2. Nikkei closed UP 1441.26 PTS OR 2.48%

WEST TEXAS INTERMEDIATE OIL UP TO 92.02

BRENT; 95.50

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 97.86/// EURO FALLS TO 1.1799 DOWN 7 BASIS PTS

3b Japan 10 YR bond yield:LOWERS. +2.404 DOWN 1 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 158.82… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.611 UP 1 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: 6.8166( UP AND OFFSHORE: UP AT 6.8144

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +3.0124 Italian 10 Yr bond yield DOWN to 3.768// SPAIN 10 YR BOND YIELD DOWN TO 3.456%

3i Greek 10 year bond yield DOWN TO 3.745%

3j Gold at $4826.75 //Silver at: 80.19 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 59 100 roubles/75.41

3m oil (WTI) into the 92 dollar handle for WTI and 96 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 158.32 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.404% DOWN 1 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.613 UP 1 PTS..: USA/SF this 0.7814 as the Swiss Franc . Euro vs SF: 0.9221

USA 10 YR BOND YIELD: 4.271 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.891 DOWN 0 BASIS PTS/

USA 2 YR BOND YIELD: 3.749 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 44.77 UP 2 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD

10 YR UK BOND YIELD: 4.7860 DOWN 3 PTS

30 YR UK BOND YIELD: 5.467 DOWN 3 BASIS PTS

10 YR CANADA BOND YIELD: 3.474 UP 4 BASIS PTS

5 YR CANADA BOND YIELD: 3.086 UP 3 BASIS PTS.

1a New York Opening report

“The Roaring 2020s Are Back”: S&P Futures Hit New Record With Nasdaq Up 12 Straight Days On Iran Truce Optimism

Thursday, Apr 16, 2026 – 08:45 AM

Stock futures are edging higher on continued optimism about an extended truce in the Middle East, while Taiwan Semi’s solid results have sparked another leg higher in AI trade. As of 8:15 am ET, S&P 500 futures rose 0.1%, while Nasdaq 100 contracts +0.2%, and on pace for a 12th day of gains. The early hours of the session saw a sharp rally in technology stocks after TSMC’s upbeat revenue outlook highlighted the resilience of AI chip demand. In premarket trading, Mag 7 stocks were mostly higher led by MSFT +1.8% and TSLA +1.3%. On geopolitical headlines, the White House remains optimistic on the second round of talk (key Pakistani negotiator visits Tehran); Israel’s security cabinet met to discuss a possible ceasefire. Bond yields are 0-2bp lower with a modest gain in the dollar. Brent rose toward $96 a barrel as movements through the Strait of Hormuz remained all but paralyzed. Bonds rose, led by gains in Europe where central bank policymakers signaled they’re in no rush to raise interest rates. The dollar snapped an eight-day losing streak while gold rose above $4,800 an ounce. April’s strong stock rebound is being driven by a new kind of FOMO, according to Ed Yardeni, with Goldman saying that “despite the sharp market rebound, positioning has not fully caught up.” Still, while equities are “definitely pricing” the end of the war, we are “not there yet,” cautioned HSBC’s Patrick George while the IMF and World Bank are also worried that markets are underestimating the war’s economic damage. Today’s US economic data calendar includes April New York Fed services business activity, Philadelphia Fed business outlook, weekly jobless claims (8:30am) and March industrial production (9:15am). Fed speaker slate includes Williams (8:35am) and Miran (10:35am)

In premarket trading, Mag 7 stocks are mixed: Microsoft +1.3%, Tesla +0.7%, Meta Platforms +0.5%, Nvidia -0.4%, Alphabet -0.2%, Apple +0.8%, Amazon -0.1%

- Nuclear and uranium companies are set to extend this week’s rally after the White House released rules for establishing a National Initiative for American Space Nuclear Power. Oklo (OKLO) +7%, NuScale Power (SMR) +10%.

- Quantum computing shares are on track to extend gains for a third consecutive session after Nvidia unveiled a suite of new open-source AI models aimed at accelerating progress within quantum computing.

- Allbirds (BIRD) tumbles 21% as the newly minted AI stock takes a breather after soaring more than 580% on Thursday.

- Hims & Hers (HIMS) rises 9%, with shares on track to extend the previous day’s 14% rally, after Health Secretary Robert F. Kennedy Jr. said the FDA is seeking to remove 12 peptides from Category 2 restrictions.

- PepsiCo Inc. (PEP) gains 1% after quarterly revenue and earnings beat expectations as the maker of Doritos and Lay’s sees improvement in salty snacks volume following recent price cuts.

- PPG Industries (PPG) rises 3% after the supplier of paints and coatings posted preliminary first quarter adjusted earnings per share that topped expectations.

- QuidelOrtho Corp. (QDEL) sinks 17% after the health care services provider posted disappointing preliminary first-quarter revenue as US flu-like illness visits fell by about 30% from the year-earlier period.

- Travelers (TRV) slips 1.4% after the insurance company posted first quarter results where net premiums written declined 1.7% from the year-ago period.

- U.S. Bancorp (USB) rises about 1% after first-quarter profit beat estimates, as Chief Executive Officer Gunjan Kedia rounds out her first year leading the largest regional bank and boosting its stock.

- Voyager Technologies (VOYG) gains 6% after the defense and space company signed an order with NASA for the seventh Private Astronaut Mission to the International Space Station.

Elsewhere in AI, Nvidia’s Jensen Huang said the US should seek greater cooperation with China on AI research. Politicians are also weighing in on the global AI race, with House Republicans calling for US sanctions against Chinese entities that improperly extract results from leading US AI models to develop their own competing systems. Today’s Big Take focuses on Anthropic’s race to assess the dangers of Mythos.

Stock markets have rebounded as signs of easing tensions in the Middle East, combined with a fresh burst of AI optimism and corporate earnings, pushed investors to abandon their cautious views. Sentiment was boosted by lack of bad Iran news again: this time, the US and Iran are said to be considering a two-week ceasefire extension to allow more time to negotiate a peace deal; the next meeting between US / Iran may take place later this week with chatter from Pakistani media that Trump is said to be in attendance. April’s strong stock rebound is being driven by a new kind of FOMO, the fear of missing out on peace, according to Ed Yardeni, who said that for stocks, the V-shaped recovery this month makes it feel “like the Roaring 2020s are back.” Still, while equities are “definitely pricing” the end of the war, we are “not there yet,” cautioned HSBC’s Patrick George. The IMF and World Bank are also worried that markets are underestimating the war’s economic damage.

In the latest developments in the conflict, Pakistan stepped up efforts to help the US and Iran prolong a ceasefire that’s set to expire next week.

“Investors have become conditioned to buy every dip,” said Michael Bell, head of market strategy at RBC BlueBay Asset Management. “The outlook is binary, either Hormuz reopens soon or it doesn’t. With equity markets already assuming Hormuz will reopen soon, the upside is perhaps limited.”

The AI narrative is back in focus after TSMC raised its outlook for 2026, forecasting revenue growth of more than 30% and saying that capex is likely to lean toward the upper end of its forecast ($56 billion). Elon Musk’s Terafab project, which aims to reshape the chipmaking landscape dominated by TSMC, is reaching out to chip industry suppliers and asking them to move at ‘light speed’ on his project.

“TSMC describing AI demand as ‘extremely robust,’ pushing capex to the upper end of a $52-56 billion range, and signaling that the next three years of investment will significantly exceed the last three; that is not the language of a cycle nearing its peak,” said Amanda Lyons, information technology sector lead and head of research at Energy Group Capital.

While the S&P 500 hit a new record on Wednesday, valuation ratios are still well below the levels seen in late 2025, indicating that earnings forecasts are moving up faster than stock prices. The current 12-month forward blended PE multiple for the S&P 500 of about 21 times compares to a peak of 23 times in November. The rally is also without breadth, with more decliners than advances as the gauge passed 7,000.

Another concerning fact about the latest record high: it was reach with more decliners than advancers, suggesting the leadership of this meltup is becoming dangerously narrow.

Lack of breadth however hasn’t stopped the Nasdaq from going from oversold to overbought in 2 weeks.

Technology stocks have been snapped up in recent weeks after lagging the market for much of the year, putting the Nasdaq 100 on course for its longest winning streak since 2017 if the gauge extends gains on Thursday.

Claudia Panseri of UBS Wealth Management said her exposure to artificial intelligence stocks is focused on the US and China and is “more selective” than two years ago. “We also prefer companies which are still investing using cash, rather than companies issuing bonds,” Panseri told Bloomberg TV.

Some stocks face a volatile option expiry into Friday, with $3.3 trillion notional of options open interest expiring across US indexes, ETFs and single stocks. Investors are “scrambling” for the “under-owned right tail” according to Nomura’s cross asset desk strategist Charlie McElligott.

Meanwhile, the latest private credit headlines have a more reassuring tone, with Goldman Sachs’ global head of alternatives for wealth saying she expects private credit firms to keep drawing capital despite recent redemption episodes. That follows Blue Owl shares posting their biggest two-day gain since November 2022, and reassurances from US banks that their exposure to private credit is manageable.

Technology stocks fueled gains in Europe where the Stoxx 600 rose 0.4%. Technology and retail shares are leading gains, while telecoms and food beverage stocks are the biggest laggards. Optimism surrounding the sector got a boost after Taiwan Semiconductor Manufacturing Co. raised its revenue outlook for 2026. Here are the biggest movers Thursday:

- Entain shares rise as much as 6.6% after its first-quarter online gaming revenue grew faster than expected, offsetting weaker retail and adverse sports results, according to analysts

- Tesco shares rise as much as 3.5% after the UK’s largest supermarket chain delivered annual earnings ahead of expectations

- Mitie Group rises as much as 4.5%, touching a record high, after the support services provider delivered a trading update

- Barry Callebaut shares drop as much as 17%, hitting the lowest level since November, after the Swiss chocolate maker reported first-half earnings that missed estimates and lowered guidance for the year

- Kering shares fall as much as 4.6% after the French owner of Gucci outlined financial ambitions at its capital markets day that analysts deemed cautious

- EasyJet shares fall as much as 8.7%, the most since June 2022, as the low-cost airline forecasts a 1H26 headline pretax loss of between £540 million ($733 million) and £560 million

- Heidelberger Druckmaschinen shares drop as much as 9.2%, pulling back from a two-month high, after the printing press maker issued a profit warning

Earlier in the session, Asian tech stocks also climbed to a record high, while Taiwan’s total market cap topped $4.1 trillion to overtake the UK. Asian markets rose, with a key regional benchmark on course for a third-straight day of gains, on optimism over corporate earnings and a potential US-Iran ceasefire extension. The MSCI Asia Pacific Index advanced as much as 1.5%, with Samsung Electronics and Alibaba among the biggest boosts. Technology stocks led gains, with a sector gauge climbing to a new record high. South Korea’s Kospi, Japan’s Nikkei 225 and Hong Kong’s Hang Seng Tech Index rose more than 2% each, while Taiwan’s total market cap climbed above $4.1 trillion to overtake the UK. Investors are renewing their interest in the artificial intelligence theme with support from resilient earnings at Asian tech hardware makers. At the same time, an outlook for an eventual end to the Middle East conflict and tamer energy prices is gaining traction. Among key moves, EV battery maker CATL climbed more than 10% in Hong Kong after better-than-expected earnings. Meanwhile, chip giant TSMC raised its revenue outlook for 2026, an upbeat forecast that underscores the resilience of AI chip demand.

In FX, the Bloomberg Dollar Spot Index is up 0.2% and on course to snap an eight-day losing streak. The kiwi is the laggard among the G-10’s, falling 0.4% against the greenback. The pound falls 0.2% having derived little support from stronger-than-expected UK GDP data.

In rates, treasuries are slightly richer across the curve with gains led by the front-end and belly, supported by a wider bull steepening move seen across European bonds with oil prices steady. US yields lower by up to 2bp across front-end and belly with 2s10s, 5s30s spreads steeper by around 0.5bp and 1.2bp on the day. US 10-year trades around 4.265%, richer by 1.5bp on the day with bunds and gilts outperforming by 1.5bp and 1bp in the sector. In Europe, both UK and German 2-year yields outperform, richer by over 5bp on an outright basis, follows UK manufacturing data printing lower-than-expected. The US session includes weekly claims and a couple of Fed speakers.

In commodities, brent crude futures climb 1.6% to around $96.40 a barrel. European government bonds gain, led by the short-end as traders pare bets on interest rate hikes by the Bank of England and European Central Bank this year. UK and German 2-year yields fall 4 bps each. Precious metals advance, although are off their best levels.

Today’s US economic data calendar includes April New York Fed services business activity, Philadelphia Fed business outlook, weekly jobless claims (8:30am) and March industrial production (9:15am). Fed speaker slate includes Williams (8:35am) and Miran (10:35am)

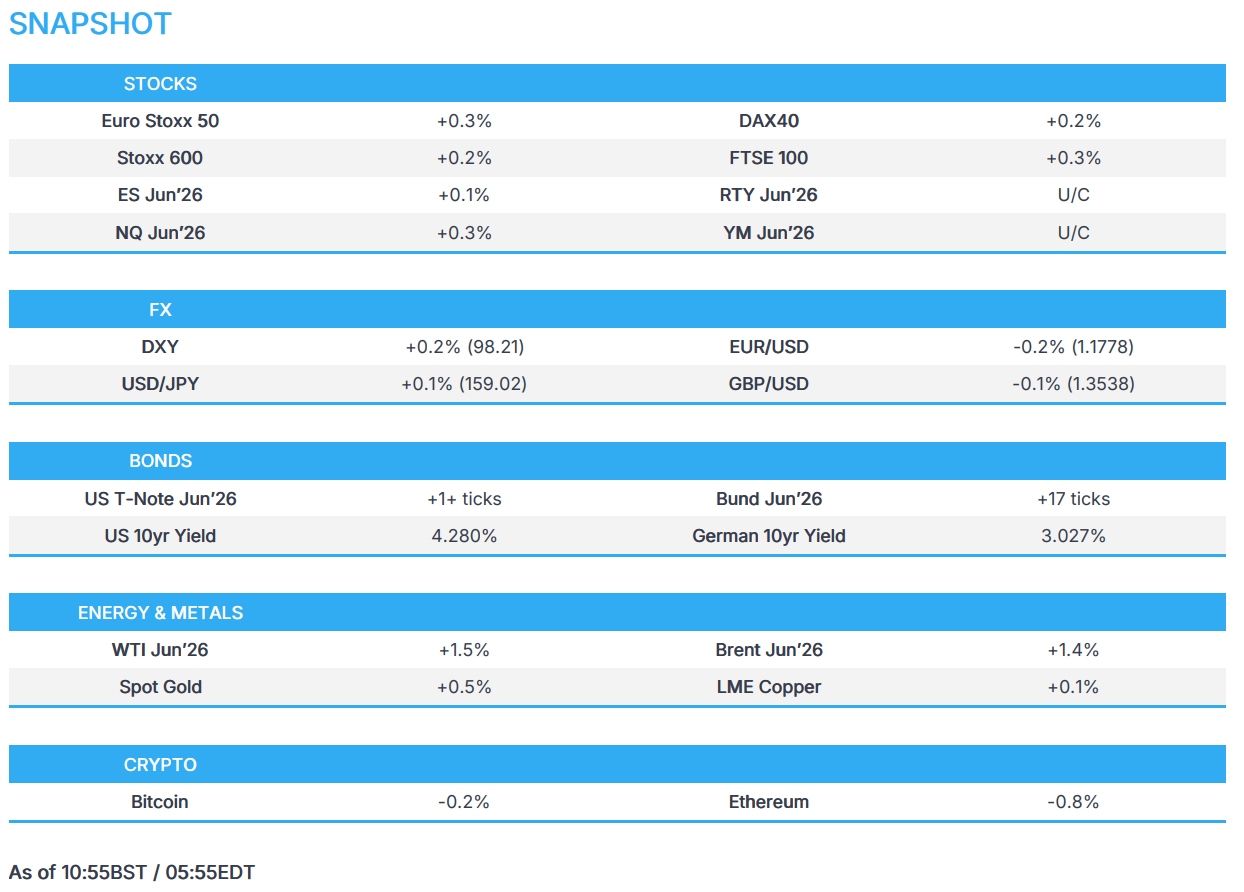

Market Snapshot

- S&P 500 mini +0.1%

- Nasdaq 100 mini +0.3%

- Russell 2000 mini little changed

- Stoxx Europe 600 little changed

- DAX little changed

- CAC 40 +0.3%

- 10-year Treasury yield little changed at 4.28%

- VIX little changed at 18.14

- Bloomberg Dollar Index little changed at 1193.41

- euro -0.2% at $1.178

- WTI crude +1.7% at $92.84/barrel

Top Overnight News

- Pakistan is stepping up efforts to ensure the US and Iran prolong a ceasefire that’s set to end next week, allowing more time for the warring sides to negotiate a lasting peace deal. The US and Iran are considering a two-week ceasefire extension, according to a person familiar with the matter, with neither side desiring to restart fighting. BBG

- The Trump administration wants automakers and other American manufacturers to play a larger role in weapons production, reminiscent of a practice used during World War II: WSJ

- Energy Secretary Chris Wright and Interior Secretary Doug Burgum will urge the heads of top U.S. oil and gas companies in a call Thursday to increase drilling in a bid to lower oil prices. Politico

- China’s economy picked up speed early in 2026, riding an export surge before the Iran war sent energy costs soaring and put global demand – vital to Beijing’s growth ambitions – at risk. The 5.0% year-on-year pace in the first quarter sits at the top of China’s full-year target range of 4.5%-5.0%, highlighting a resilience that sets it apart from much of Asia, helped by ample strategic oil reserves and a diversified energy mix. RTRS

- Australian employment rose by 17,900 in March, missing expectations and driven entirely by full-time roles, while the jobless rate held at 4.3%. BBG

- The UK economy grew 0.5% in February, beating estimates to post its strongest monthly reading since January 2024. Activity was boosted by the services sector, though the data predate the Iran war. BBG

- Policymakers at the European Central Bank are leaning toward keeping interest rates unchanged this month, postponing their verdict on whether the fallout of the Iran war warrants a response. BBG

- Senator Thom Tillis is blocking Trump’s Fed chair nominee, Kevin Warsh, until the Justice Department drops an investigation into Powell. And the stalemate is leaving him in limbo with no clear off-ramp in sight. Politico

- Anthropic’s Mythos is so skilled at hacking that access is tightly controlled. The system’s ability to autonomously find and exploit vulnerabilities is forcing banks and governments to rethink cybersecurity. BBG

- Foreign holdings of Treasuries soared to a record $9.49 trillion in February. Canada led with a $50.5 billion increase, while Japan remained the largest holder. BBG

Iran Conflict

- The Trump admin’s goal is to bring both sides to the brink of an overarching deal to end the conflict that can then be pushed over the finish line in a second face-to-face meeting, according to ABC, citing officials. The officials acknowledge that technical talks to hammer out the fine details and implementation of the arrangement will likely take longer to complete, perhaps eventually necessitating an extension of the initial ceasefire, but that pushing back the truce’s expiration date isn’t a top priority for the administration at the moment.

- US President Trump told guests Monday night he wants to bring the war in Iran to a swift end; said only way to get Iran back to negotiating table was to increase the pressure, according to WSJ citing officials at the dinner.

- US President Trump posted “Trying to get a little breathing room between Israel and Lebanon. It has been a long time since the two leaders have spoken, like 34 years. It will happen tomorrow. Nice!”.

- Pakistani Army Chief is heading to the US on Friday as part of mediation efforts between the US and Iran, Al Jazeera reported citing a Pakistani security source.

- Pakistan’s Foreign Ministry said the US and Iran are willing to hold talks and the process is continuing but no date decided for next round of US-Iran talks.

- A military advisor to the Islamic Revolution Leader said Iranian Armed Forces’ launchers are ready to hit American warships and sink all of them, Press TV reported.

- A senior Iranian official said the fate of Iran’s highly enriched uranium and the duration of its nuclear restrictions remain unresolved, adding that fundamental disagreements persist over nuclear issues. Iranian official said there are greater hopes for extending the ceasefire and holding a second round of talks after the trip, adding that the Pakistani army chief’s visit to Iran helped reduce differences in some areas.

- Iranian officials will meet with Pakistan’s army chief on Thursday in Tehran and will discuss US proposals, according to TASS.

- Iran and the Pakistani mediator will discuss details of the messages exchanged between Tehran and Washington tomorrow, Thursday; via Al Jazeera citing Iranian TV.

- Journalist Abas Aslani posted source said Iran-US talks are far less positive [than reported] due to contradictory US stances & Israeli spoiler efforts, media push hyping success of talks is a PR manoeuvre to calm markets and shield Trump from pressure.

- Iran’s ambassador to Pakistan said Islamabad is the sole venue for Iran–US talks.

- Diplomatic sources suggest that “Washington is pressing forcefully to cool down the Lebanese front”, via Kan’s Kais; “Second round of negotiations between Israel and Lebanon will take place in Washington soon”. “Second round of negotiations between Israel and Lebanon will take place in Washington soon, and that the current contacts are focused on achieving a temporary ceasefire that will lay the groundwork for ending the war.”

- Two Israeli officials said the meeting of the political security cabinet ended without a decision on a ceasefire in Lebanon, according to Axios’s Ravid.

- Israeli media citing informed sources state that a ceasefire in Lebanon will not happen soon despite Trump’s statements.

- Israeli army has not received any instructions so far to prepare for a ceasefire in Lebanon, via Al Arabiya citing local reported.

- Lebanese officials say a ceasefire between Israel and Lebanon is expected ‘soon’, according to FT.

- The next meeting between Israel and Lebanon is expected to be held early next week, via Sky news Arabia citing Israel Hayom.

- Iran’s Interior Minister has ordered border governors to neutralise the threat of a naval blockade by strengthening and developing border trade by increasing imports of basic goods and exports of goods, utilising all national and regional capacities.

- Iranian politician affiliated with Resistance Front of Islamic Iran, Mohsen Rezaei said they will not leave the Strait of Hormuz until the full realisation of Iran’s rights, adds that this time, Iran has set preconditions.

- Iranian Parliament Speaker Ghalifbaf said US should withdraw from ‘Israel first’ mistake and must comply with agreement, also said resistance and Iran are one soul both in war and ceasefire.

- Hezbollah fires long-range missiles at Tel Aviv, according to Defapress.

- Iranian military affiliated outlet Defapress claims that four ships broke the US naval blockade over the past 24 hours, citing satellite data.

- Israeli warplanes carried out a strike on the town of Shihabiya in southern Lebanon.

- US Central Command said US blockade has turned back 10 vessels in the Strait of Hormuz today.

- China’s Foreign Minister Wang Yi stressed to Iran that the Strait of Hormuz needs to reopen and stressed freedom of navigation in Hormuz, while he said Hormuz reopening is a unanimous call from the international community.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly gained following the positive lead from Wall Street, where the S&P 500 and Nasdaq printed fresh all-time highs, amid tech strength and peace talk optimism. ASX 200 bucked the trend and gave back initial gains, and more, as notable outperformance in tech was offset by losses in energy, resources, materials, financials and miners. Nikkei 225 rallied to a fresh record high after reclaiming the 59,000 status amid the hopes for a Middle East resolution and with the index led by the momentum in tech stocks. Hang Seng and Shanghai Comp were higher with further upside seen as the dust settled following the mixed Chinese GDP and activity data, in which GDP growth for Q1 missed expectations, but GDP Y/Y topped forecasts and printed at the high-end of China’s official 2026 GDP growth target. Meanwhile, Industrial Production data for March was better-than-expected, but Retail Sales disappointed.

Top Asian News

- Japan’s top FX diplomat Mimura said told US Treasury Secretary Bessent will upgrade FX developments as needed, and both sides agreed to coordinate closely on FX.

- Japanese Finance Minister Katayama said regarding exchange rates, agreed to further intensify communication with US Treasury Secretary Bessent.

- Japanese Finance Minister Katayama said many central bankers are adopting a wait-and-see stance, as raising interest rates could have a negative impact on the economy, adds it is impossible to predict when the current situation ends and spillover effects.

- Senior Japanese Financial Regulator official said Japan sees private credit as potential pillar in new strategy to meet corporate funding demand driven by M&A surge, according to reported.

- China NBS said the economy had a good start in Q1, but the external situation is becoming more complex, adds China is to expand domestic demand and optimise supply. China will implement proactive macro policies. Expects a complex, volatile external environment. China will consolidate economic recovery foundation. Sees mixed signs of strong supply and weak demand.

- Deutsche Bank upgrades China’s 2026 real GDP growth to 4.9% (prev. 4.5%).

- Barclays raises China 2026 GDP growth view to 4.6% (prev. saw 4.0%).

European bourses (STOXX 600 +0.2%) are broadly gaining, albeit only modestly. The CAC 40 is the outperformer, rebounding from Wednesday’s luxury-driven selloff. The FTSE 100 is also slightly higher this morning, after UK GDP came in far stronger than expected in February (0.5% vs exp. 0.1%). Sectors point to a positive bias. Top of the pile lies Technology, supported by strong TSMC earnings, which has lifted peers such ASML. Telecoms is the underperformer, with a downgrade for Telia weighing on the broader sector.

Top European News

- EU Inflation Rate MoM Final (Mar) M/M 1.3% vs. Exp. 1.2% (Prev. 0.6%, Low. 1.2%, High. 1.2%).

- EU Inflation Rate YoY Final (Mar) Y/Y 2.6% vs. Exp. 2.5% (Prev. 1.9%, Low. 2.5%, High. 2.6%).

- EU Core Inflation Rate YoY Final (Mar) Y/Y 2.3% vs. Exp. 2.3% (Prev. 2.4%).

- UK Balance of Trade (Feb) -0.720B vs. Exp. -3.6B (Prev. 3.922B).

- UK Goods Trade Balance (Feb) -18.79B vs. Exp. -20.2B (Prev. -14.45B, Low. -20.5B, High. -14B).

- UK GDP YoY (Feb) Y/Y 1.0% vs. Exp. 1.0% (Prev. 0.8%).

- UK GDP MoM (Feb) M/M 0.5% vs. Exp. 0.1% (Prev. 0%, Low. 0.0%, High. 0.3%).

Trade/Tariffs

- UK Europe Minister Nick Thomas-Symonds is expected to offer an update on the state of play in negotiations; EU Trade Chief Sefcovic, and European Parliament President Roberta Metsola, will also provide keynotes, reported Politico.

- USTR Greer said US-China Board of Investment is to be a government forum, adds there’s no situation where there’s no trade between US and China, also said the Trump admin wants to be pragmatic regarding China.

FX

- DXY edged higher throughout the entirety of the European session following punchy Iran rhetoric. The index marked a session high of 98.21, rising from its earlier trough of 97.83 made in Asia. (Full Middle East analysis on the headline feed) As it stands, both US and Iran continue communication, but there is no confirmation yet on second-round talks or a ceasefire extension – not to mention Lebanon, which remains a key point. Aside from geopolitics, POLITICO reported this morning, “a growing chorus of Republicans, eager to install Warsh, are joining the call for the administration to end the probe” into Fed Chair Powell. This comes ahead of Warsh’s hearing next week. The session ahead sees remarks from Fed’s Williams (voter), who will speak at a Federal Home Loan Bank of New York event, while Miran (voter, dovish dissenter) will speak on the global outlook.

- GBP knee-jerked higher on a stronger-than-expected UK GDP report from February, but now trades with very mild losses given the Dollar strength this morning. In brief, on a monthly basis, GDP rose 0.5%, while yearly saw an increase of 0.1%. This set of metrics did not encapsulate the US-Iran war and as such, MPC members will likely refer to the second-round effects of the energy shock before opting to adjust rates. Cable continues to trade towards recent highs and is essentially at pre-war levels. The pair attempted to breach 1.36, a rally which faltered at 1.3594.

- Antipodeans trade mixed. While Aussie is a touch firmer against a resilient USD following jobs data – Kiwi sits at the bottom of the pile as bets for RBNZ tightening pare a touch with markets implying 77bps of easing by year end (prev. c. 83bps). NZD/USD began falling in Asia, though losses extended throughout the European morning to trade at session lows of 0.5893, the move likely to face support @ 0.5892.

- JPY had a choppy overnight session with USD/JPY marking a session low of 158.27 after successful jawboning from Finance Minister Katayama; she told G7 members that Japan was watching FX with a high sense of urgency. She also reiterated close communication with the US Treasury. This, as is typically the case with the Japanese Finance Ministry, indicates officials are uncomfortable with the extent of JPY weakness, with JPY nearing the key 160 mark. Since these comments, JPY pared the entirety of the strength Katayama gave to the haven, pressured by the gains in the USD.

Central Banks

- ECB officials are said to be leaning towards an April rate hold.

- ECB’s Schnabel said that the memory of high inflation remains fresh, and inflation expectations could be more fragile. Can afford to take time to analyse the Iran shock. We are in a relatively favourable position because we were successful in bringing down inflation to 2% before the war started, have monetary policy stance that is broadly neutral. To carefully consider data that may indicate inflation becoming entrenched or having second-round effects.

- ECB’s Demarco said policymakers must be patient on rate decisions, but warns an adverse scenario could materialise; adverse scenario could require two rate hikes; longer-term inflation expectations anchored.

- ECB’s Muller said rate move at April meeting still cannot be ruled out, adds may not have all the data this month to determine if interest rates will have to be raised to tame an inflation surge and June meeting will offer greater body of information. No hard evidence of second-round effects of inflation.

- Goldman Sachs expects the ECB to deliver 25bp rate hikes in June and September 2026 (prev. saw hikes in April and June). Analysts expect energy prices to remain persistently high through 2026, significant pass-through into inflation is likely in coming months and ECB’s communication has remained largely hawkish on the path ahead.

Fixed Income