MAY 21/TRUMP RECEIVES FINAL DRAFT AND IT IS NOT WORTH THE PAPER IT IS PRINTED ON: GOLD HOWEVER CLOSED UP $7.60 TO $4541.40 WHILE SILSVER CLOSED UP $0.64 TO $76.59//PLATINUM CLOSED UP $18.00 TO $1973.00 WITH PALLADIUM UP $18.50 TO $1394.00//AN EXTREMELY IMPORTANT PODCAST TONIGHT FROM ANDREW MAGUIRE ON GOLD AND SILVER WITH EMPHASIS ON THE PETRO YUAN TO GOLD STRUCTURE//ALSO GOLD PODCAST COURTESY OF ITM TRADING//ASIAN REPORTS TONIGHT FROM SOUTH KOREA RE SAMSUNG AND CHINA ON RARE EARTHS//EUROPEAN REPORTS TONIGHT FROM THE UK AND GREECE//IN THE UK A ONE YR OLD CHILD HAS BEEN CRIMINALLY CHARGED/BOOKED WITH MISCHIEF//ISRAEL AND USA VS IRAN: FINAL DRAFT RECEIVED//MORE UPDATES ON THE CONFLICT//ISRAEL TBN/BIG UPDATE ON THE FOOLISHNESS OF THE TURKISH PRESIDENT ERODGAN ON HOW HE DEFENDS THE TURKISH LIRA; IT IS FALLING INTO OBLIVION//MAJOR UPDATES ON RUSSIA AS IT HOLDS MAJOR DRILLS WITH BELARUS; THE RUSSIAN ROUBLE SO FAR THIS YEAR IS THE STRONGEST CURRENCY GAIN/MAJOR UPDATES ON OIL//USA DATA RELEASES ON OUR PMI’S//BIG STORY ON THE HUGE SELLING OF USA TREASURIES FROM JAPAN AND CHINA//KING NEWS/SWAMP STORIES FOR YOU TONIGHT//

099 H DEUTSCHE BANK AG 119 118 C MACQUARIE FUTURES US 2 363 H WELLS FARGO SECURITI 361 555 C BNP PARIBAS SEC CORP 412 661 C JP MORGAN SECURITIES 198 220 686 H STONEX FINANCIAL INC 160 905 C ADM 37 3

TOTAL: 756 756 MONTH TO DATE: 6,310

MAY 21

MAY COMEX MONTH

JPMORGAN STOPPED: 230/756

GOLD: NUMBER OF NOTICES FILED FOR MAY/2026: 756 CONTRACTs NOTICES FOR 75,600 OZ or 2.3515 TONNES

total notices so far: 6310 contracts FOR 631,000 OZ OR 19.626 TONNES

FOR MAY 21

XXXXXXXXXXXXXXXXXX

SILVER NOTICES:37 NOTICE(S) FILED FOR .185 MILLION OZ /

total number of notices filed so far this month : 5681 CONTRACTS (NOTICES) for 28.405 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $7.60 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/// NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 1036.851 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.64 AT THE SLV: NO CHANGES IN SILVER INVENTORY AT THE SLV: //// : INVENTORY RESTS AT THE SLV AT 488.338 MILLION OZ//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 488.338 MILLION

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 188 CONTRACTS TO AN OI OF 100,939 STILL HIGHER FROM ITS NEW RECORD LOW OF 95,999 SET MAY 1. THE RECORD HIGH OI FOR SILVER IS 244,710, SET FEB 25/2020, AND THIS SMALL GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR GAIN OF $1.27 IN SILVER PRICING AT THE COMEX WITH RESPECT TO WEDNESDAY’S TRADING. ON THE FIRST OF MAY, WE REACHED OUR RECORD LOW OI OF 95,999 SURPASSING EVERY DAY NEW OI LOWS SET DURING THE LAST WEEK OF APRIL 2026.

NOW ON A NET BASIS OUR SPECULATORS HAVE REVERTED BACK TO GOING LONG. THE FRBNY ON A NET BASIS IS PROVIDING THE NECESSARY PAPER TO OUR LONGS ALONG WITH SOME BULLION BANKS AND THEN A HUGE NUMBERS OF LONGS ,OUR CENTRAL BANKERS, TAKE THE LONG SIDE AND TENDER FOR PHYSICAL AT 4 PM EACH NIGHT. BECAUSE OF THE HUGE SHORTFALL IN PHYSICAL SILVER IN LONDON THERE IS A LOTTERY TO SEE WHO GETS ANY OF THE PHYSICAL SILVER AVAILABLE THAT WHICH THEY ARE OBLIGATED TO DELIVER. THEY WAIT PATIENTLY FOR THEIR PHYSICAL METAL AND IF NOBODY GETS ANY THEY THEN COME BACK THE NEXT DAY AND SO ON. THIS IS IN LONDON, THE HOME OF PHYSICAL SILVER!!

WE ARE FINALLY MOVING TO A MUCH HIGHER BASE IN SILVER PRICING AT MAJOR SUPPORT LEVEL OF $70.00. SHORTLY WE WILL AGAIN ATTEMPT TO BREAK

WE HAVE A SMALL GAIN OF 188 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A ZERO SIZED SIZED 0 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE..(STRANGE) , WE HAD NO LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO WEDNESDAY TRADING// WE HAD A HUGE 795 CONTRACT T.A.S. ISSUANCE!! / THEY DESPERATELY AGAIN TODAY TRYING TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $100.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILRD ON WEDNESDAY WITH SILVER’S GAIN IN PRICE

THE PRICE STILL FINISHED ABOVE THE MAGIC NUMBER OF $70.00 SILVER SPOT PRICE BUT STILL BELOW THE $100.00 MARK CLOSING AT $75.95 UP $1.27. WE ARE NOW WITNESSING HAVING MANY HUGE T.A.S ISSUANCES // TODAY’S WAS A HUGE SIZED 795 T.A.S. CONTRACTS !!. THE CROOKS ARE BECOMING MORE DESPERATE TO STOP SILVER BREAKING ABOVE THE 100.00 DOLLAR MARK!! AND NOW THE HUGE SUPPORT LEVEL OF 70 DOLLARS!!.MAMMOTH SIZE T.A.S ISSUANCES ARE BECOMING THE NORM AT THE COMEX NOW!!

THERE IS NO NEXT LINE IN THE SAND ONCE THE 100.00 DOLLAR SILVER IS PIERCED AGAIN. WE HAD A ZERO SIZED 0 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE SIZED 795 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FUTURE TRADING//AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE.

IN ESSENCE WE HAD A SMALL GAIN OF 188 CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $1.27. WE HAD HUGE GOVERNMENT (FRBY) COMEX CONTRACTS TRADING ALL WEEK AND A MAJOR PORTION WILL BE REMOVED BY DAYS END. (I RECORD THIS FOR YOU ON A DAILY BASIS). THE STICKY SPECULATOR LONGS STILL REMAIN STOIC

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE.

THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, THROUGHOUT MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT/THURSDAY MORNING: A HUGE SIZED 795 CONTRACTS. DESPITE MANY COMPLAINTS THAT THESE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED FRBNY BANKERS).

THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS AS ONE UNIT, BUT SELL THE SHORT SIDE FIRST AND THEN LIQUIDATE THE LONG SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS NOW ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1.1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

THUS:

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A TINY QUEUE JUMP OF 1 CONTRACTS OR 0.005 MILLION OZ/NEW STANDING ADVANCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT QUEUE JUMP WHERE 5,000 OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES SLIGHTLY TO 16.565 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER 3 ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.730 MILLION OZ//

INITIAL STANDING FOR MAY: 31.495 MILLION OZ FOLLOWED BY ANOTHER 86 CONTRACT EXCHANGE FOR PHYSICAL TRANSFER JUMP TO LONDONO FOR 0.430 MILLION OZ// AND THEN TO BOOT WE HAD OUR FIRST EXCHANGE FOR RISK ISSUANCE FOR 51 CONTRACTS OR 255,000 OZ/STANDING BEFORE EXCHANGE FOR RISK: 32.130 MILLION OZ/NEW STANDING THUS REDUCES TO 32.385 MILLION OZ/.//(32.130 MILLION OZ NORMAL STANDING PLUS .255 MILLION OZ EXCHANGE FOR RISK = 32.385 MILLION OZ)

SUMMARY OF OUR MAY 2026 COMEX CONTRACT MONTH:

WE HAD:

/ SMALL COMEX GAIN+// ZERO SIZED 0 EFP ISSUANCE CONTRACTS (/ VI) A HUGE NUMBER OF T.A.S. CONTRACT ISSUANCE 795 CONTRACTS

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:REMOVED 72 SILVER CONTRACT//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY.. ACCUMULATION

TOTAL CONTRACTS for 15 DAY(S), total 10,081 contracts: OR 50.405 MILLION OZ (672 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 50.405 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 44.44 MILLION OZ//FINAL.. SMALL THIS MONTH.

MAY 50.405 MILLION OZ

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 188 CONTRACTS WITH OUR GAIN IN PRICE OF $1.27 IN SILVER PRICING AT THE COMEX// WEDNESDAY,. THE CME NOTIFIED US THAT WE HAD A ZERO SIZED CONTRACT EFP ISSUANCE 0 CONTRACTS ISSUED FOR JULY, AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS).

INITIAL STANDING: 31.495 MILLION OZ NOW DECREASES WITH OUR NEXT EXCHANGE FOR PHYSICAL TRANSFER JUMP TO LONDON FOR 86 CONTRACTS OR 0.430 MILLION OZ//NEW STANDING IS THUS REDUCES TO 32.560 MILLION OZ/BUT WE THEN ADD OUR FIRST EXCHANGE FOR RISK OF 51 CONTRACTS FOR 255,000 OZ..TOTAL STANDING REDUCES TO 32.385 MILLION OZ//

LAST 14 MONTHS OF SILVER DELIVERIES

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUUE JUMP //NEW STANDING ADVANCES TO 16.565MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.730 MILLION OZ

MAY: INITIAL AMOUNT OF SILVER WILLING TO STAND; 31.495 MILLION OZ/ TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL TRANSFER JUMP OF 430,000 OZ//NEW STANDING REDUCES TO 32.130 MILLION OZ//(FOLLOWING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON DURING THIS MAY DELIVERY MONTH). THERE SEEMS TO BE A SCARCITY OF SILVER OVER AT THE COMEX). THEN WE ADD OUR FIRST EXCHANGE FOR RISK OF 51 CONTRACTS FOR 255,000 OZ//STANDING STILL REDUCES TO 32.385 MILLION OZ//

THE NEW TAS ISSUANCE FOR TODAY (795) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED NO DOUBT WITH FUTURE TRADING!

WE HAD 37 NOTICE(S) FILED TODAY FOR 0.185 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY BANKERS

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 4,659 OI CONTRACTS UP TO 374,666 OI ADVANCING FROM ITS ALL TIME LOW OF 354,581 OI AND CLOSER TO THE RECORD HIGH (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE HAVE NOW ADVANCED PAST THE PREVIOUS ALL TIME LOWS OF 357,136 SET APRIL 2/.2026. WE ARE STILL QUITE A WAY FROM OUR TWO DECADES OLD: 390,000 CONTRACTS LOW SET IN THE YEAR OF 2001 WITH TRADING FOR GOLD AT $260.00. THUS DURING EARLY APRIL WE HAD AN ALL TIME LOW OI IN COMEX (354,531) BUT WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE COMEX SHIP, NOBODY WANT TO PLAY IN THIS CROOKED CASINO!! (AND THIS CORRELATES WITH SILVER’S LOW OI OF 106.954 CONTRACTS WITH A MUCH HIGHER SILVER PRICE BASE)

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE 11,498 CONTRACTS //.

WE HAD A STRONG LOSS IN COMEX OI (4659 ONTRACTS) . THIS LOSS IN OI OCCURRED WITH OUR GAIN IN PRICE OF $26.30 //WEDNESDAY///.

LAST 13 MONTHS OF GOLD DELIVERIES: (MAY 2025 THROUGH TO /MAY 2026)

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

2 JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

3.JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES STANDING

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 278 CONTRACT QUEUE JUMP FOR 27800 OZ/ (0.8646 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR 2ND EXCHANGE FOR RISK OF 1498 CONTRACTS FOR 149800 OZ OR 4.659 TONNES. THE NEW TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL IS 2239 CONTRACTS OR 223900 OZ OR 6.964 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS (70.762 TONNES) TO GIVE US WHAT WILL STAND IN APRIL (77.726 TONNES)

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 961 CONTRACTS OR 96,100 OZ (3,082 TONNES) TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCES FOR 12.292 TONNES/STANDING NOW ADVANCES TO 33.896 TONNES OF GOLD.

E.F.P. ISSUANCE/FOR OPENING MAY. GOLD CONTRACT

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 3025 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT A LOW OF 374,666 ADVANCING FROM OUR RECORD LOW OF 354,581 AND WE NOW WITNESSING A LOWER COMEX OI BUT WITH AN EXTREMELY HIGH

SILVER ALSO HAS AN ULTRA SMALL SIZED AND EXTREMELY LOW COMEX OI OF 100,939 CONTRACTS// RISING FROM PREVIOUS ALL TIME LOWS SET DURING THE MONTH OF APRIL AND MAY FIRST.

IN ESSENCE WE HAVE A FAIR LOSS IN TOTAL CONTRACTS IN COMEX GOLD ON THE TWO EXCHANGES OF 1634 CONTRACTS WITH 4659 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 3025 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON.

THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 1634 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A MUCH SMALLER SIZED BUT CRIMINAL 1382 CONTRACTS AND THESE ISSUANCES ARE GENERALLY USED TO INITIATE A RAID WHEN CALLED UPON. THE STRING OF 5 CONSECUTIVE HUGE ISSUANCES OF T.A.S. THUS ENDED LAST FRIDAY.

GOLD PRICE ON WEDNESDAY ROSE BY $26.30

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(3025 ) ACCOMPANYING THE STRONG LOSS IN COMEX OI OF 4659 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES 1634 CONTRACTS!! DESPITE THE LOSS IN PRICE.

WE HAVE 1) NOW REVERTED TO OUR NORMAL FORMAT OF BANKER (FRBNY) GOING ON THE SHORT SIDE AND SOME NEWBIE SPECULATORS GOING TO THE LONG SIDE BUT OTHER SPECS GOING ALSO TO THE SHORT SIDE LED BY THE NOSE BY HIGH FREQUENCY TRADERS AND SPREADERS..

STANDING FOR THE LAST 5 MONTHS JANUARY TO MAY:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR TWO EXCHANGE FOR RISK FOR 223,900 OZ OR 6.964 TONNES/NEW STANDING: 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND; 12.24 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 961 CONTRACTS/96,100 OZ// 3.082 TONNES/ THEN WE MUST ADD OUR EXCHANGE FOR RISK ISSUANCE: TOTAL EXCHANGE FOR RISK 4 OCCASIONS: 12.292 TONNES///NEW STANDING NOW ADVANCES TO 33.996 TONNES

3) HUGE T.A.S. LIQUIDATION IN THE COMEX SESSION AND SOME GOVT LIQUIDATION // WITH A HUGE GAIN OF EQUITY SHARES/MAY 20 HAVING 1)A $26.30 COMEX PRICE GAIN AND WE HAD 2) SPEC LONGS PILING HUGELY ON THE SHORT SIDE// +3. EASTERN CENTRAL BANKERS ALSO PILING INTO THE LONG SIDE. WE HAD A STRONG GAIN OF 9864 CONTRACTS ON OUR TWO EXCHANGES AND AS WELL A STRONG AMOUNT OF GOLD WILL STAND FOR DELIVERY IN MAY. (33.996 TONNES). //, CENTRAL BANKERS TENDERED FOR PHYSICAL WITH THEIR PURCHASES OF CONTRACTS../ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED FRIDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL

4)A STRONG SIZED COMEX OI GAIN 5) V) STRONG SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD(3025) AND 6. A FAIR T.A.S. ISSUANCE (1382) FOR RAID PURPOSES LIKE TODAY.!!!

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 26,153 CONTRACTS OR 2,615,300 OZ OR 81.347 TONNES IN 15 TRADING DAY(S) AND THUS AVERAGING: 1743 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN15 TRADING DAY(S) IN TONNES: 81.347 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2025, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 81.347 TONNES DIVIDED BY 3550 x 100% TONNES = 2.29% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2023 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2024: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES

2025: AND NOW 2026

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 88.00 TONNES// WILL BE VERY SMALL THIS MONTH

MAY 81.347 TONNES

SPREADERS:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A SMALL 188 CONTRACTS TO AN OI OF 100,961.

EFP ISSUANCE 0 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 0 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 188 CONTRACTS AND ADD TO THE 0 E.FP. ISSUED

WE OBTAIN A SMALL GAIN OF 188 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN OF $1.27

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 0.94 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $1.27

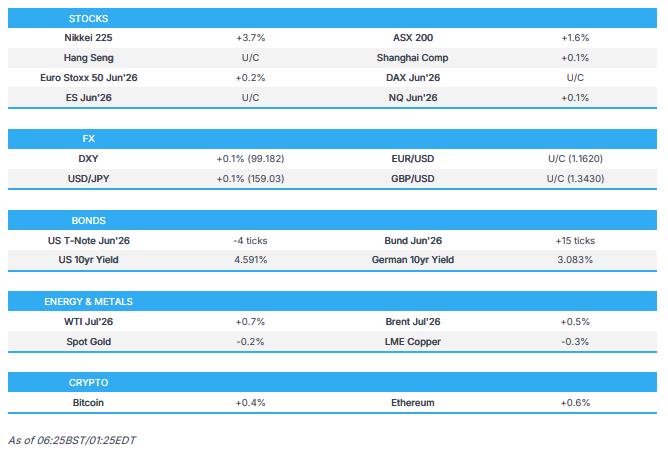

2.ASIAN AFFAIRS MAY 21 /2025

HANGHAI CLOSED DOWN 84.91 PTS OR 2.04%

HANG SENG CLOSED DOWN 264.60 PTS OR 1.03%

Nikkei CLOSED UP 1853.59 PTS OR 3.10%

//Australia’s all ordinaries CLOSED DOWN .22%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.8020

/ OFFSHORE CLOSED UP AT 6.8055 Oil UP TO 100.52 dollars per barrel for WTI and BRENT UP TO 107.28 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING UP (6.8020) OFFSHORE YUAN TRADING UP TO 6.8055 ONSHORE YUAN TRADING ABOVE OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG 4,659 CONTRACTS UP TO AN OI OF 374,666 CONTRACTS (OI) , HAVING ADVANCED FROM OUR NEW LOW OI SET LATE LAST MONTH AND SURPASSING THE PREVIOUS ALL TIME LOW IN OI OF 354,581 SET APRIL6/2026. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 354,581 WITH GOLD AT AN EXTREMELY HIGH $4,700.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD NO T.A.S. LIQUIDATION DURING WEDNESDAY’S TRADING. IT SEEMS THAT SOME OF THE SPECULATORS CONTINUED AGAIN TO GO MASSIVELY ON THE LONG SIDE BUT WITH THE BANKERS NOW TAKING THE LONG SIDE,AND CENTRAL BANKS SUPPLYING THE NECESSARY PAPER, AS WELL AS COVERING THEIR SHORTFALL. THERE ARE ALSO SOME SPECULATORS WHO CONTINUALLY GO TO THE SHORT SIDE AND AND OF COURSE THEY WILL BE ANNHILATED ON CENTRAL BANK COMMAND!!

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE STRONG AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS MAY CONTRACT MONTH!!

THE STRONG SIZED GAIN ON OUR TWO EXCHANGES OCCURRED WITH OUR GAIN IN PRICE IN GOLD (UP $26.30).

WE THUS HAD A FAIR SIZED LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 1634 CONTRACTS (OR 5.082 TONNES) WITH OUR GAIN IN PRICE, AS WE WERE INFORMED OF A STRONG CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE, EQUATING TO 3025 CONTRACTS.

THEN WE WERE NOTIFIED TODAY OF A 166 CONTRACT FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 16,600 OZ OR 0.536 TONNES OF GOLD. A FEW DAYS AGO BY FAR WE HAD THE HIGHEST EVER EXCHANGE FOR RISK EVER ISSUED AT ONE TIME. WE HAD OUR FIRST ISSUANCE FOR EXCHANGE FOR RISK IN THE MONTH OF MAY ON MAY 7, THEN OUR 2ND ISSUANCE FOR OUR MAY GOLD MONTH ON MAY 12. THE THIRD ON MAY 18 AND NOW TODAY MAY 21 OUR 4TH ISSUANCE. THIS GOLD WILL BE ADDED TO OUR NORMAL MAY DELIVERIES TO GIVE US OUR FINAL AMOUNT OF GOLD WILLING TO STAND AT THE COMEX..

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH MAY

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 2 EXCHANGE FOR RISK SO FAR, I.E. 2239 CONTRACTS FOR 223,900 OZ OR 6.964 TONNES AND THIS TOTAL TONNES WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND IN APRIL

MAY: FOUR ISSUANCES SO FAR FOR 3,920 CONTRACTS OR 392,000 OZ OR 12.192 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO MAY:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 2 EXCHANGE FOR RISK SO FAR FOR 223,900 OZ OR 6.964 TONNES. AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND FOR APRIL!!

MAY: FOUR ISSUANCES SO FAR FOR 3920 CONTRACTS, 392,000 OZ OR 12.292 TONNES OF GOLD. THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES IN MAY TO GIVE US WHAT WILL STAND IN MAY.

DETAILS ON OUR NEW MAY COMEX CONTRACT MONTH//

IN TOTAL WE HAD A FAIR LOSS ON OUR TWO EXCHANGES OF 1634 CONTRACTS DESPITE OUR GAIN IN PRICE ($26.30). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THEIR THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH MAY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS FINALLY A FAIR SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 1382 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD. APRIL HAD 2 EXCHANGE FOR RISK ISSUANCES FOR 6.694 TONNES. AND NOW MAY WITH ITS 3RD ISSUANCE FOR 11.676 TONNES///TOTAL EXCHANGE FOR RISK FOR MAY: 12.292 TONNES ISSUED MAY 6 ,MAY 12, MAY 18 AND NOW MAY 21.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

1.APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.05 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP/ TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES TOTALLING 223,900 OZ OR 6.964 TONNES//STANDING ADVANCES TO 77.726 TONNES WHICH IS ABSOLUTELY HUGE

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT HUGE QUEUE JUMP OF 96,100 OZ (3.082 TONNES) TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE FOR 392,000 OZ OR 12.292 TONNES////NEW TOTALS STANDING FOR GOLD ADVANCES TO 33.896 TONNESS

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING MAY,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $26.30)

WE HAD ZERO T.A.S. SPREADER LIQUIDATION WEDNESDAY // COMEX SESSION// WITH OUR GAIN IN PRICE , OUR LONG SPECULATORS STILL REMAIN RELENTLESS POURING INTO THE COMEX

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

WEDNESDAY NIGHT//THURSDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR GAIN IN PRICE TO THE TUNE OF $26.30

WE HAD A HUGE 11,498 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET LOSS ON THE TWO EXCHANGES : 1634 CONTRACTS OR 163,400 OZ OR 5.082 TONNES

Total monthly oz gold served (contracts) so far this month

6310 notices 631000 oz 19.626 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0

0 ENTRY

DEPOSITS/CUSTOMER

0 ENTRY

xxxxxxxxxxxxxxxxxx

comex withdrawals:

ENTRIES; 1

i) BRINKS 31,941.499 oz 1149 kilobars)

TOTAL WITHDRAWAL: 31,941.499 OZ (1.149 TONNES)

adjustments: 5// ONE //CUSTOMER TO DEALER; OTHER 4 DEALER TO CUSTOMER

a) Asahi customer to dealer: 35,685.181 oz

b) Brinks: dealer to customer: 11,786.181 oz

c) Malca dealer to customer: 13,406.967 oz

d) Manfra: 6414.477 oz dealer to customer

e) Stonex: 6384.212 oz dealer to customer

Net 2,706.696 oz out of the dealer into the customer accts.

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF MAY OI STANDS AT 1392 CONTRACTS HAVING A LOSS OF 103 CONTRACTS.

WE HAD 858 CONTRACTS SERVED ON WEDNESDAY SO WE GAINED A HUGE 961 CONTRACTS OR 96,100 OZ (3.082 TONNES) UNDERWENT A HUGE QUEUE JUMP WHERE THEY WILL TAKE DELIVERY ON THIS SIDE OF THE POND. THIS QUEUE JUMP IS CENTRAL BANK CLAMORING FOR PHYSICAL GOLD.

.

JUNE IS A HUGE DELIVERY MONTH AND HERE THE OI FELL BY 19,485 CONTRACTS DOWN TO AN OI OF 166,466. JUNE BECOMES THE NEW FRONT MONTH AND WE SHOULD HAVE A STRONG AMOUNT OF GOLD STANDING FOR DELIVERY.

JULY LOST 10 CONTRACTS DOWN TO AN OI OF 1677.

We had 756 contracts filed for today representing 75,600oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 756 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 220 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAY. /2026. contract month, we take the total number of notices filed so far for the month (6,310) to which we add the difference between the open interest for the front month of MAY (1392 CONTRACTS) minus the number of notices served upon today 756 x 100 oz per contract) equals 694,600 OZ OR (21.604 Tonnes of gold) to which we add our FOUR exchange for risk issuance for 392,200 oz or 12.292 tonnes//new standing for gold/May again advances to 33.896 tonnes.

THUS: INITIAL total number of gold ounces standing for MAY. /2026. contract month, we take the total number of notices filed so far for the month (6,310) to which we add the difference between the open interest for the front month of MAY( xxx CONTRACTS) minus the number of notices served upon today 756 x 100 oz per contract) equals 694,600 OZ OR (21.604 Tonnes of gold) plus we must add our FOUR exchange for risk issuances of 392,200 oz or 12.292 tonnes/new standing advances to 33.896 tonness

new total of gold standing in MAY ADVANCES TO 33.896 TONNES//

TOTAL COMEX GOLD STANDING FOR MAY 33.896 TONNES TONNES WHICH IS NOW STRONG FOR THIS NORMALLY NON ACTIVE DELIVERY MONTH OF MAY.

confirmed volume WEDNESDAY confirmed 209,926// fair// many have left the arena

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,911,131.257 oz 59.44 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,911,131.257 tonnes oz 59.44 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 28,660,544.627oz

TOTAL REGISTERED GOLD 15,720,995.771 488.988 tonnes

TOTAL OF ALL ELIGIBLE GOLD 12,939,548.856 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,809,864 oz ((REG GOLD- PLEDGED GOLD)=

429.54 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

MAY DELIVERY MONTH

MAY 21

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

2 entries

i) Out of Loomis: 607,009.030 oz ii Out of CNT: 600,713.800 oz

total withdrawal: 1,207,722.830 oz

Deposits to the Dealer Inventory

0 entries

Deposits to the Customer Inventory

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

0 ENTRIES

No of oz served today (contracts)

37 CONTRACT(S) (0.185 MILLION OZ

No of oz to be served (notices)

868 Contracts (4.340 MILLION oz)

Total monthly oz silver served (contracts)

5,681 contracts 28.405 MILLION oz

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

DEPOSITS INTO DEALER ACCOUNTS

0 entries

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

2 entries

i) Out of Loomis: 607,009.030 oz ii Out of CNT: 600,713.800 oz

total withdrawal: 1,207,722.830 oz

adjustments 1 customer to dealer

a) Manfra; 19,940.417 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 81.689 MILLION OZ//.TOTAL REG + ELIGIBLE. 314.647 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2026 OI: 782 OPEN INTEREST CONTRACTS FOR A LOSS OF 102 CONTRACTS. WE HAD 16 CONTRACTS SERVED UPON ON WEDNESDAY SO WE LOST86 CONTRACT OR 0.430 MILLION OZ UNDERWENT AN EXCHANGE FOR PHYSICAL TRANSFER TO LONDON WHERE THEY WILL TAKE DELIVERY OVER ON THAT SIDE OF THE POND. IT SHOWS THAT THERE IS NO REAL PHYSICAL SILVER OVER HERE TO BE DELIVERED UPON.

JUNE SAW A LOSS OF 11 CONTRACTS DOWN TO 2889 OI CONTRACTS

JULY SAW A LOSS OF 56 CONTRACTS DOWN TO 72,414 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 37 or 0.185 MILLION oz

CONFIRMED volume WEDNESDAY; 45,025 fair

XXX

AND NOW MAY. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 5681 X5,000 oz = 28.405 MILLION oz

to which we add the difference between the open interest for the front month of MAY (782) AND the number of notices served upon today (37 )x (5000 oz)

Thus the standings for silver for the MAY 2026 contract month: (5,681 )Notices served so far) x 5000 oz + OI for the front month of MAY (782) minus number of notices served upon today (37)x 5000 oz equals silver standing for the MAY..contract month equating to 32.130 MILLION OZ.+TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.255 MILLION OZ//

NEW STANDING REDUCES T0: 32.385 MILLION OZ WHICH IS STILL PRETTY GOOD FOR THIS ACTIVE DELIVERY MONTH OF MAY.

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 81.689 million oz of registered silver

JPMorgan as a percentage of total silver: 140.287/314.649 million: 44.58

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42.

The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

MAY 21 /2026/WITH GOLD UP $7.60 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

MAY 20 /2026/WITH GOLD UP $26.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.999 TONNES OF GOLD OUT OF THE GLD./ //:/INVENTORY RESTS AT 1036.851 TONNES

MAY 19 /2026/WITH GOLD DOWN $46.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.57 TONNES OF GOLD INTO THE GLD./ //:/INVENTORY RESTS AT 1038.85 TONNES

MAY 18 /2026/WITH GOLD DOWN $4.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 15 /2026/WITH GOLD DOWN $118.70 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 14 /2026/WITH GOLD DOWN $20.95 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 13 /2026/WITH GOLD UP $18.75 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 12 /2026/WITH GOLD DOWN $38.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.285 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 11 /2026/WITH GOLD DOWN $2.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.515 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1033.995 TONNES

MAY 8 /2026/WITH GOLD UP $22.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.283 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1033.480TONNES

MAY 7 /2026/WITH GOLD UP $15.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.853 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1033.197TONNES

MAY 6 /2026/WITH GOLD UP $124.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.718 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1034.05TONNES

MAY 5 /2026/WITH GOLD UP $33.75 TODAY/NO CHANGES IN GOLD AT THE GLD:// //:/INVENTORY RESTS AT 1035.768 TONNES

MAY 4 /2026/WITH GOLD DOWN $106.65 TODAY/NO CHANGES IN GOLD AT THE GLD:// //:/INVENTORY RESTS AT 1035.768 TONNES

MAY 1 /2026/WITH GOLD UP $13.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.427 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1035.768 TONNES

APRIL 30/2026/WITH GOLD UP $19.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 5.142 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1039.195 TONNES

APRIL 29/2026/WITH GOLD DOWN $45.70 TODAY/NO CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1044.337 TONNES

APRIL 28/2026/WITH GOLD DOWN $85.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1044.337 TONNES

APRIL 27/2026/WITH GOLD DOWN $41.10 TODAY/NO CHANGES IN GOLD AT THE GLD: // //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 24/2026/WITH GOLD UP $13.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 23/2026/WITH GOLD DOWN 28.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.000 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1050.91 TONNES

APRIL 22/2026/WITH GOLD UP 26.40 TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 21/2026/WITH GOLD DOWN 11.90TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 17/2026/WITH GOLD UP $71.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 1.15 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 16/2026/WITH GOLD DOWN $15.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.285 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1051.783 TONNES

APRIL 15/2026/WITH GOLD DOWN $24.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.289 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1049.478 TONNES

APRIL 14/2026/WITH GOLD UP $83.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.714 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1047.192 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 10/2026/WITH GOLD DOWN $11.90 TODAY/SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.724 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.42 TONNES

APRIL 9/2026/WITH GOLD UP $42.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.429 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.990 TONNES

APRIL 8/2026/WITH GOLD UP $88.95 TODAY/NO CHANGES IN GOLD AT THE GLD A//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 7/2026/WITH GOLD UP $5.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 3.429 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 6/2026/WITH GOLD UP $5.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/INVENTORY RESTS AT 1050.99 TONNES

APRIL 2/2026/WITH GOLD DOWN $132.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.714 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1050.99 TONNES

GLD INVENTORY: 1036.851 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

MAY 21 WITH SILVER UP $0.64: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

MAY 20 WITH SILVER UP $1.27: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

MAY 19 WITH SILVER DOWN $2.39: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.086 MILLION OZ OUT OF THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

MAY 18 WITH SILVER DOWN $0.09: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 489.424 MILLION OZ

MAY 15 WITH SILVER DOWN $7.06: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.9000 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 489.424 MILLION OZ

MAY 14 WITH SILVER DOWN $3,79: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.448 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 487.524 MILLION OZ

MAY 13 WITH SILVER UP $3,62: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.086 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 486.087 MILLION OZ

MAY 12 WITH SILVER DOWN $0.48: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.176 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 484.990 MILLION OZ

MAY 11 WITH SILVER UP $5.10: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.995 MILLION OZ OF SILVER PUT OF THE SLV// / // :INVENTORY RESTS AT 483.814 MILLION OZ

MAY 8 WITH SILVER UP $1.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.689 MILLION OZ OF SILVER INTO THE SLV// / // :INVENTORY RESTS AT 484.809 MILLION OZ

MAY 7 WITH SILVER UP $2.26: NO CHANGES IN SILVER INVENTORY AT THE SLV: / // :INVENTORY RESTS AT 484.130 MILLION OZ

MAY 6 WITH SILVER UP $3.75: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.724 MILLION OZ INTO THE SLV/ // :INVENTORY RESTS AT 484.130 MILLION OZ

MAY 5 WITH SILVER UP $0.21: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.734 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 483.604 MILLION OZ

MAY 4 WITH SILVER DOWN $3.05: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.734 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 483.604 MILLION OZ

MAY 1 WITH SILVER UP $2.38: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.905 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 484.338 MILLION OZ

APRIL 30 WITH SILVER UP $2.03: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.991 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 485.243MILLION OZ

APRIL 29 WITH SILVER DOWN $1.95: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 28 WITH SILVER DOWN $2.05: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 27 WITH SILVER DOWN $1.39: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 24 WITH SILVER UP 0.92: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.54 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 487,23MILLION OZ

APRIL 23WITH SILVER DOWN $2.35: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.489 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 488,773MILLION OZ

APRIL 22 WITH SILVER UP 1.43: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262MILLION OZ

aPRIL 21 WITH SILVER DOWN 3.71: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262 MILLION OZ

APRIL 17 WITH SILVER UP $3.09: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.453 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.900 MILLION OZ

APRIL 16 WITH SILVER DOWN $1.00: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.132 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.477 MILLION OZ

APRIL 15 WITH SILVER UP $0.01: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.588 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.579 MILLION OZ

APRIL 14 WITH SILVER UP $3.99: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.633 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.991 MILLION OZ

APRIL 13 WITH SILVER DOWN 0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.589 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.624 MILLION OZ

APRIL 10 WITH SILVER DOWN 0.16: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.724 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 492.213 MILLION OZ

APRIL 9 WITH SILVER UP $0.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.173 MILLION OZ INTO THE SLV// // :INVENTORY RESTS AT 492.937 MILLION OZ

APRIL 8 WITH SILVER UP $3.50: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 7 WITH SILVER DOWN $0.89: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 6 WITH SILVER UP $0.41: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL WITHDRAWAL OF 0.224 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 2 WITH SILVER DOWN $3.57: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.091 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.988 MILLION OZ

CLOSING INVENTORY 488.338 MILLION OZ OF SILVER

GOLD COMMENTARIES:

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD

4.ANDREW MAGUIRE LIVE FROM THE VAULT 273 and 272

MUST VIEWl ANDREW’S NEWEST PODCAST

Ted Oakley//272

5. COMMODITY REPORT/GOLD

A 1973 Repeat: Gold to Soar Amidst Oil Embargo, Inflation Says Analyst

by ITM Trading

Wednesday, May 20, 2026 – 15:03

Markets may be sleepwalking into a 1970s-style inflation shock. Gold analyst John Doody warns that escalating tensions around the Strait of Hormuz could trigger an oil embargo scenario eerily similar to the crises that sent gold soaring from $35 to $850 an ounce decades ago. With deficits exploding, central banks de-dollarizing, and a Fed chair allegedly unwilling to aggressively hike rates, Doody sees inflation reaccelerating toward 6% or higher. His message: gold remains the ultimate refuge as geopolitical instability collides with fiscal recklessness. Meanwhile, silver remains “gold on steroids,” while mining M&A activity signals insiders are positioning for much higher metals prices.

END

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

SHANGHAI CLOSED DOWN 84.91 PTS OR 2.04%

HANG SENG CLOSED DOWN 264.60 PTS OR 1.03%

Nikkei CLOSED UP 1853.59 PTS OR 3.10%

//Australia’s all ordinaries CLOSED DOWN .22%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.8020

/ OFFSHORE CLOSED UP AT 6.8055 Oil UP TO 100.52 dollars per barrel for WTI and BRENT UP TO 107.28 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING UP (6.8020) OFFSHORE YUAN TRADING UP TO 6.8055 ONSHORE YUAN TRADING ABOVE OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP 6.8020

OFFSHORE YUAN: UP TO 6.8055

1.HANG SANG CLOSED DOWN 264.60 PTS OR 1.03%

2. Nikkei closed UP 1853.59 PTS OR 3.10%

WEST TEXAS INTERMEDIATE OIL UP TO 100.52

BRENT; 107.28

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 99.23/// EURO FALLS TO 1.1605 DOWN 19 BASIS PTS

3b Japan 10 YR bond yield:FALLS TO. +2.758 DOWN 1 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 159.13… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 4.030 DOWN 3 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP( 6.8020 AND OFFSHORE: UP AT 6.8055

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +3.1162// Italian 10 Yr bond yield DOWN to 3.888// SPAIN 10 YR BOND YIELD DOWN TO 3.560%

3i Greek 10 year bond yield DOWN TO 3.785%

3j Gold at $4515.85 //Silver at: 74.87 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 43/ 100 roubles/71.01

3m oil (WTI) into the 100 dollar handle for WTI and 107 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 159.13 // 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.758% DOWN 1 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 4.030 DOWN 3 PTS..: USA/SF this 0.7879 as the Swiss Franc . Euro vs SF: 0.9144

USA 10 YR BOND YIELD: 4.621 UP 8 BASIS PTS…

USA 30 YR BOND YIELD: 5.143 UP 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.096 UP 6 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 45.62 UP 2 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD

10 YR UK BOND YIELD: 4.9920 DOWN 1 PTS

30 YR UK BOND YIELD: 5.670 UP 1 BASIS PTS

10 YR CANADA BOND YIELD: 3.620 UP 3 BASIS PTS

5 YR CANADA BOND YIELD: 3.271 UP 3 BASIS PTS.

1a New York Opening report

Futures Slump, Ignoring Korean Euphoria, After Iran Rejects Trump Enriched Uranium Demands

Thursday, May 21, 2026 – 07:38 AM

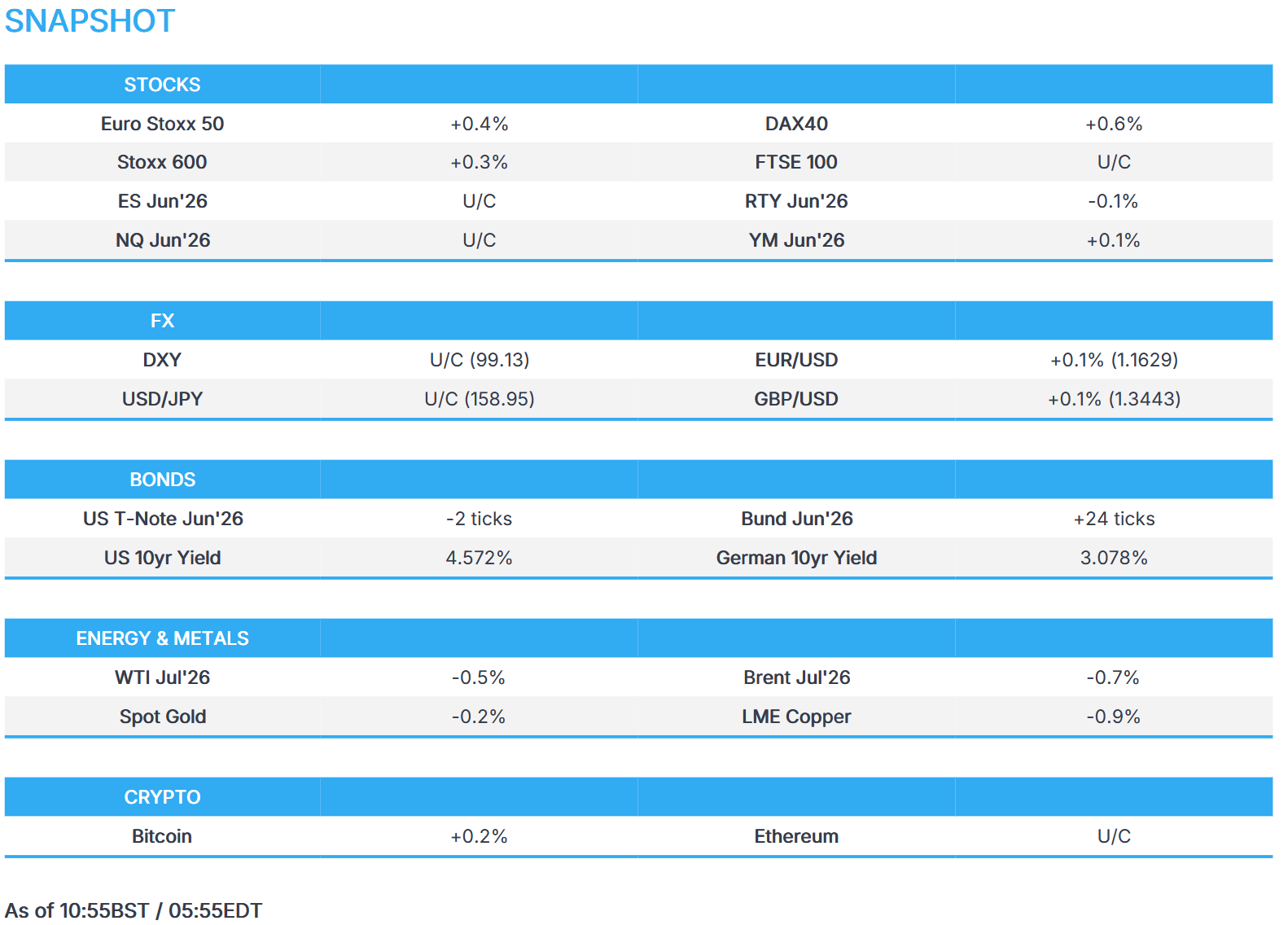

A steady rebound in US equities driven by peak insanity in Korea (where the two chip stocks that account for most of the market surged and sent the Kospi soaring more than 8% overnight) faded after a report that Iran’s Supreme Leader issued a directive that the country’s near-weapons-grade uranium must remain in the country,rejecting Trump’s key ceasefire demand, while oil and bond yields jumped as traders waited in mounting futility to see whether hopes of a peace deal in the Middle East would translate into tangible progress. As of 7:15am ET, S&P 500 futures fell 0.4% and Nasdaq futures slid 0.3% after otherwise very strong Nvidia’s earnings failed to ignite further strong gains in the artificial intelligence trade. Treasuries fell as Brent reversed earlier losses to climb 2% above $107 after Tehran’s response disappointed those hoping for de-escalation. JPMorgan CEO Jamie Dimon did not help, warning that interest rates may climb much further from current levels. Long-dated bonds around the world have tested multiyear highs in recent days on concern about an oil-driven spike in inflation and amid worries over government spending.

Yesterday’s Nvidia earnings proved to be a dud: Nvidia shares were unchanged (crushing both put and call buyers as the implied vol collapse) in US premarket trading after the AI chipmaker reported Q1 results and gave a forecast amid increased investor skepticism. While analysts were broadly positive, some also questioned the sustainability of growth, especially amid higher competition. Intuit sank 13% after the software company said it plans to reduce its workforce by about 17%. The shares of space exploration and satellite internet companies were broadly steady after Elon Musk’s SpaceX filed publicly for an initial public offering. Tesla advanced 1.6%, while other Mag 7 stocks were mixed (Amazon +0.6%, Alphabet +0.3%, Meta -0.2%, Apple -0.3%, Microsoft -0.3%).

Aevex Corp. (AVEX) is up 8.5% after the drone maker reported first-quarter earnings. The company also announced that it was awarded $15.6 million in contracts by the US Air Force.

Applied Digital (APLD) jumps 11% after the company signed a 15-year lease valued at about $7.5 billion with a US investment-grade hyperscaler for its Polaris Forge 3 campus.

Elf Beauty Inc. (ELF) is up 9.9% after the cosmetics company beat the average analyst estimate on major profit and revenue estimates. Meanwhile, the company forecast adjusted earnings per share for 2027 that fell short of expectations.

Intuit (INTU) sinks 13% after the tax-preparation software company reported third-quarter results that were seen as disappointing for its TurboTax business. It also said it is cutting about 17% of its staff, confirming an earlier Reuters report.

Nebius (NBIS) is up 8.4% after partnering with Bloom Energy to deploy fuel-cell technology to power its AI infrastructure build-out in the US. Bloom rises 2.6%.

In other corporate news, Samsung reached a tentative last-minute deal with its union, averting a potentially crippling strike scheduled to start on Thursday at the world’s biggest memory firm.

Virtually all overnight gains in the S&P faded just after 6am when Reuters blasted the following two headlines which poured cold water on expectations of a quick deescalation in the Iran war

*IRAN SUPREME LEADER SAYS URANIUM MUST STAY IN IRAN: REUTERS

*IRAN SUPREME LEADER ISSUES DIRECTIVE ON URANIUM: REUTERS

Almost overshadowed by headlines related to AI-disrupter Anthropic and SpaceX, Nvidia’s results produced the expected high growth. Nvidia’s revenue growth shows that the momentum of the debt-fueled AI data-center buildout is accelerating. While analysts are broadly positive, some also questioned the sustainability of growth, especially amid higher competition. Some also pointed to the company’s compute revenue miss as an early warning sign, especially with Nvidia changing the way it reports revenue so it masks this weakness going forward. Nvidia’s price reaction was expected to be more muted compared to the last few years – call open interest has been drifting lower. While this suggests a cooling in the speculative chase that previously defined the popular AI trade, it isn’t dimming the price action of peripheral beneficiaries – a windfall for Asian chip makers.

“Investors remain relentless in pursuit of supernormal returns offered by AI,” said Emmanuel Valavanis, an equity sales specialist at Forte Securities, noting how narrow the market has become given a “laser beam focus on AI, the biggest tech infrastructure build-out of 21st century.”

Shortly after the Nvidia results, SpaceX filed publicly for what stands to be the largest-ever IPO, revealing billions in losses and a super-voting share plan allowing Elon Musk to keep the company under his control. SpaceX had a net loss of $4.28 billion on revenue of $4.69 billion for the first quarter, compared with a net loss of $528 million on revenue of about $4 billion a year earlier, the filing shows.

While this will surely change, for now SpaceX is now a cash incinerating machine, with nearly $25BN in cash burn in the last 12 months.

“We believe that our current space efforts will catalyze transformative breakthroughs that could reshape terrestrial industries and lead to the emergence of new trillion-dollar markets on the Moon, Mars, and beyond.” Space Exploration said in its Form S-1.

Elsewhere Jamie Dimon said interest rates may climb much higher from current levels, while his firm will likely hire more AI specialists and fewer traditional bankers as the adoption of the technology accelerate.

The muted tone in US markets contrasted with buoyant optimism in Asia, where a key tech gauge jumped the most in six weeks.

Overnight Asia saw stock market fireworks with Korea’s LG Electronics and Hyundai Mobis both surging in Seoul after Nvidia CEO Jensen Huang touted new opportunities offered by robots and automated vehicles. SoftBank Group Corp. jumped 20% as two companies backed by the Japanese investor – OpenAI and SB Energy Corp. – were said to be preparing for initial public offerings. Regional chipmakers tracked Wednesday’s gains in US peers.

“The rally in Asia has been supported by very strong momentum in technology, particularly around the current reality of AI demand,” said Francisco Simón, European head of strategy at Santander Asset Management. “Looking ahead, investors also continue to see structural growth potential linked to the future evolution of AI, including companies that may emerge as leaders.”

European shares edged higher after early declines as investors digested earnings reports and purchasing managers’ index data from across the region. The Stoxx 600 rose 0.4%, British defense technology firm QinetiQ was among the top gainers after posting strong results and announcing a new share buyback programme, while Ubisoft slumped on weak bookings. Here are the biggest movers Thursday:

QinetiQ shares jumped as much as 11%, the biggest daily rise in over a year, after earnings showed a profit beat and a buyback initiative.

Investec rallied as much as 5.3% in London to its highest intraday level since April after the specialist lender reported net income for the full year that beat the average analyst estimate.

Generali shares rose as much as 2.9%, the best performer on the Stoxx 600 Insurance Index, after the Italian insurer reported what analysts say are strong 1Q earnings.

CSG shares rose as much as 5.9% after Oddo BHF upgraded the defense company to outperform from neutral, saying there is potential for significant re-rating after a short attack sent the stock plunging earlier this month.

Naturgy Energy Group shares gained as much as 3.4%, trading at their highest level since 2022, after receiving upgrades from Morgan Stanley and BNP Paribas.

Alfen rose as much as 25% after a Jefferies upgrade gives it a sole buy rating, with the energy-equipment company seen favorably positioned to capitalize on the energy transition theme, with double-digit growth in all end-markets.

Greece’s Public Power rose as much as 6% to a record high after it concluded a share capital increase on Wednesday.

Hexagon shares fell as much as 18% on Thursday, their first day of trading excluding rights to the company’s upcoming spin off of its subsidiary Octave.

Ubisoft shares slumped as much as 19% on Thursday after the video game maker guided to a high single-digit percentage drop in net bookings for the coming fiscal year, well below expectations.

Convatec shares dropped as much as 5.6%, worst performer in the Stoxx 600 Health Care Index on Thursday morning, after the medical products and equipment manufacturer provided an update for the first four months of 2026.

MaaT Pharma shares plunge as much as 61%, the most on record, after the French biotech company said its experimental therapy Xervyteg for acute graft-versus-host disease is likely to be turned down by the European Medicines Agency.

Autotrader falls as much as 4.8%, most since Feb. 3, after a soft earnings report which analysts said will weaken confidence in the online vehicle marketplace. The stock has lost about a fifth of its value this year.