EXCHANGE: COMEX

CONTRACT: MAY 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,539.800000000 USD

INTENT DATE: 05/21/2026 DELIVERY DATE: 05/26/2026

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DEUTSCHE BANK AG 26

363 H WELLS FARGO SECURITI 231

555 C BNP PARIBAS SEC CORP 177

661 C JP MORGAN SECURITIES 60

686 C STONEX FINANCIAL INC 11

905 C ADM 21

TOTAL: 263 263

MONTH TO DATE: 6,573

MONTH TO DATE: 6,573

GOLD: NUMBER OF NOTICES FILED FOR MAY/2026: 263 CONTRACTs NOTICES FOR 26,300 OZ or 0.8180 TONNES

total notices so far: 6573 contracts FOR 657,300 OZ OR 20.444 TONNES

SILVER NOTICES: 0 NOTICE(S) FILED FOR 0.000 MILLION OZ /

total number of notices filed so far this month : 5681 CONTRACTS (NOTICES) for 28.405 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A TINY QUEUE JUMP OF 1 CONTRACTS OR 0.005 MILLION OZ/NEW STANDING ADVANCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT QUEUE JUMP WHERE 5,000 OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES SLIGHTLY TO 16.565 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER 3 ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.730 MILLION OZ//

INITIAL STANDING FOR MAY: 31.495 MILLION OZ FOLLOWED BY A 5 CONTRACT QUEUE JUMP FOR 0.025 MILLION OZ// AND THEN TO BOOT WE HAD OUR FIRST EXCHANGE FOR RISK ISSUANCE FOR 51 CONTRACTS OR 255,000 OZ MAY 21./STANDING BEFORE EXCHANGE FOR RISK: 32.125 MILLION OZ/NEW STANDING THUS ADVANCES TO 32.380 MILLION OZ/.//(32.125 MILLION OZ NORMAL STANDING PLUS .255 MILLION OZ EXCHANGE FOR RISK = 32.380 MILLION OZ)

SUMMARY OF OUR MAY 2026 COMEX CONTRACT MONTH:

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 44.44 MILLION OZ//FINAL.. SMALL THIS MONTH.

MAY 51.405 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUUE JUMP //NEW STANDING ADVANCES TO 16.565MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.730 MILLION OZ

MAY: INITIAL AMOUNT OF SILVER WILLING TO STAND; 31.495 MILLION OZ/ TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 25,000 OZ//NEW STANDING ADVANCES TO 32.125 MILLION OZ//(FOLLOWING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON DURING THIS MAY DELIVERY MONTH). THERE SEEMS TO BE A SCARCITY OF SILVER OVER AT THE COMEX). THEN WE ADD OUR FIRST EXCHANGE FOR RISK OF 51 CONTRACTS FOR 255,000 OZ//STANDING ADVANCES TO 32.380 MILLION OZ//

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 278 CONTRACT QUEUE JUMP FOR 27800 OZ/ (0.8646 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR 2ND EXCHANGE FOR RISK OF 1498 CONTRACTS FOR 149800 OZ OR 4.659 TONNES. THE NEW TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL IS 2239 CONTRACTS OR 223900 OZ OR 6.964 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS (70.762 TONNES) TO GIVE US WHAT WILL STAND IN APRIL (77.726 TONNES)

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 418 CONTRACTS OR 41,800 OZ (1.300 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCES FOR 24.635 TONNES/STANDING NOW ADVANCES TO 47.540 TONNES OF GOLD.

STANDING FOR THE LAST 5 MONTHS JANUARY TO MAY:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR TWO EXCHANGE FOR RISK FOR 223,900 OZ OR 6.964 TONNES/NEW STANDING: 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND; 12.24 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 418 CONTRACTS/41800 OZ// 1.300 TONNES/ THEN WE MUST ADD OUR EXCHANGE FOR RISK ISSUANCE: TOTAL EXCHANGE FOR RISK 5 OCCASIONS: 24.635 TONNES///NEW STANDING NOW ADVANCES TO 47.540 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 88.00 TONNES// WILL BE VERY SMALL THIS MONTH

MAY 88.562 TONNES

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A STRONG 302 CONTRACTS TO AN OI OF 10,241.

EFP ISSUANCE 200 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 200 CONTRACTS and 200 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 302 CONTRACTS AND ADD TO THE 200 E.FP. ISSUED

WE OBTAIN A STRONG GAIN OF 502 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN OF $1.27

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 2.510 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $0.64

2.ASIAN AFFAIRS MAY 22 /2025

SHANGHAI CLOSED UP 36.04 PTS OR 0.39%

HANG SENG CLOSED UP 236.00 PTS OR 0.94%

Nikkei CLOSED UP 1690.80 PTS OR 2.74%

//Australia’s all ordinaries CLOSED UP .02%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.7970

/ OFFSHORE CLOSED UP AT 6.8002 Oil DOWN TO 98.06 dollars per barrel for WTI and BRENT UP TO 105.14 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING UP (6.7970) OFFSHORE YUAN TRADING UP TO 6.8002 ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG 4,059 CONTRACTS UP TO AN OI OF 370,607 CONTRACTS (OI) , HAVING ADVANCED FROM OUR NEW LOW OI SET LATE LAST MONTH AND SURPASSING THE PREVIOUS ALL TIME LOW IN OI OF 354,581 SET APRIL6/2026. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 354,581 WITH GOLD AT AN EXTREMELY HIGH $4,700.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD NO T.A.S. LIQUIDATION DURING THURSDAY’S TRADING. IT SEEMS THAT SOME OF THE SPECULATORS CONTINUED AGAIN TO GO MASSIVELY ON THE LONG SIDE BUT WITH THE BANKERS NOW TAKING THE LONG SIDE,AND CENTRAL BANKS SUPPLYING THE NECESSARY PAPER, AS WELL AS COVERING THEIR SHORTFALL. THERE ARE ALSO SOME SPECULATORS WHO CONTINUALLY GO TO THE SHORT SIDE AND AND OF COURSE THEY WILL BE ANNHILATED ON CENTRAL BANK COMMAND!!

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE STRONG AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS MAY CONTRACT MONTH!!

THE FAIR SIZED LOSS ON OUR TWO EXCHANGES OCCURRED WITH OUR GAIN IN PRICE IN GOLD (UP $26.30).

WE THUS HAD A FAIR SIZED LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 1739 CONTRACTS (OR 5.409 TONNES) WITH OUR GAIN IN PRICE, AS WE WERE INFORMED OF A FAIR SIZED CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE, EQUATING TO 2320 CONTRACTS.

THEN WE WERE NOTIFIED TODAY OF A MASSIVE 4000 CONTRACT FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 400,000 OZ OR 12.4416 TONNES OF GOLD. A FEW DAYS AGO BY FAR WE HAD THE HIGHEST EVER EXCHANGE FOR RISK EVER ISSUED AT ONE TIME AND YET THIS ONE BEATS IT BY A FULL TONNE. THUS MAY 22 RECORDS THE HIGHEST EVER EXCHANGE FOR RISK FOR 12.4416 TONNES. WE HAD OUR FIRST ISSUANCE FOR EXCHANGE FOR RISK IN THE MONTH OF MAY ON MAY 7, THEN OUR 2ND ISSUANCE FOR OUR MAY GOLD MONTH ON MAY 12. THE THIRD ON MAY 18 , THEN MAY 21 OUR 4TH ISSUANCE AND THEN FINALLY TODAY, OUR 5TH ISSUANCE. THIS GOLD WILL BE ADDED TO OUR NORMAL MAY DELIVERIES TO GIVE US OUR FINAL AMOUNT OF GOLD WILLING TO STAND AT THE COMEX..

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH MAY

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 2 EXCHANGE FOR RISK SO FAR, I.E. 2239 CONTRACTS FOR 223,900 OZ OR 6.964 TONNES AND THIS TOTAL TONNES WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND IN APRIL

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS OR 792,000 OZ OR 24.635 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO MAY:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 2 EXCHANGE FOR RISK SO FAR FOR 223,900 OZ OR 6.964 TONNES. AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND FOR APRIL!!

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS, 792,000 OZ OR 24.635 TONNES OF GOLD. THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES IN MAY TO GIVE US WHAT WILL STAND IN MAY.

DETAILS ON OUR NEW MAY COMEX CONTRACT MONTH//

IN TOTAL WE HAD A FAIR LOSS ON OUR TWO EXCHANGES OF 1730 CONTRACTS WITH OUR GAIN IN PRICE ($26.30). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THEIR THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH MAY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS FINALLY A FAIR SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 1300 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD. APRIL HAD 2 EXCHANGE FOR RISK ISSUANCES FOR 6.694 TONNES. AND NOW MAY WITH ITS 5TH ISSUANCE FOR 12.4436 TONNES///TOTAL EXCHANGE FOR RISK FOR MAY: 24.635 TONNES ISSUED MAY 6 ,MAY 12, MAY 18 MAY 21 AND NOW MAY 22..

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

1.APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.05 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP/ TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES TOTALLING 223,900 OZ OR 6.964 TONNES//STANDING ADVANCES TO 77.726 TONNES WHICH IS ABSOLUTELY HUGE

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT HUGE QUEUE JUMP OF 41,800 OZ (1.300 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCE FOR 792,000 OZ OR 24.635 TONNES////NEW TOTALS STANDING FOR GOLD ADVANCES TO 47.540 TONNESS

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING MAY,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $7.60)

WE HAD ZERO T.A.S. SPREADER LIQUIDATION THURSDAY // COMEX SESSION// WITH OUR GAIN IN PRICE , OUR LONG SPECULATORS STILL REMAIN RELENTLESS POURING INTO THE COMEX

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

THURSDAY NIGHT//FRIDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $26.30

WE HAD A HUGE 9,733 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET LOSS ON THE TWO EXCHANGES : 1739 CONTRACTS OR 173,900 OZ OR 5.409 TONNES

MAY DELIVERY MONTH

MAY 22

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | ENTRIES; 0 |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 1 ENTRY i) Into JPMorgan enhanced: 10,062.825 oz or 25 London good delivery bars. gold never comes into the comex//just an entry xxxxxxxxxxxxxxxx |

| No of oz served (contracts) today | 263 CONTRACTS OR 26,300 OZ 0.8180 TONNES OF GOLD |

| No of oz to be served (notices) | 791 Contracts 79,100 OZ 2.460 TONNES |

| Total monthly oz gold served (contracts) so far this month | 6373 notices 637,300 oz 20.444 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRY

DEPOSITS/CUSTOMER

1 ENTRY

i) Into JPMorgan enhanced:

10,062.825 oz

or 25 London good delivery bars.

gold never comes into the comex//just an entry

xxxxxxxxxxxxxxxxxx

comex withdrawals:

ENTRIES; 0

adjustments: 4

All dealer to customer

a) Asahi 5,467.327 oz

b) Brinks: 58,562.037 oz

c) Manfra: 2,617.980 oz

d) Customer to dealer JPMorgan 14,567.935 oz

e) stonex: addition of 259.539 into registered

stonex addition 29.039 oz into eligible/stonex

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF MAY OI STANDS AT 1054 CONTRACTS HAVING A LOSS OF 338 CONTRACTS.

WE HAD 756 CONTRACTS SERVED ON THURSDAY SO WE GAINED A HUGE 418 CONTRACTS OR 41,800 OZ (1.300 TONNES) UNDERWENT A HUGE QUEUE JUMP WHERE THEY WILL TAKE DELIVERY ON THIS SIDE OF THE POND. THIS QUEUE JUMP IS CENTRAL BANK CLAMORING FOR PHYSICAL GOLD EXACTLY AS ANDREW MAGUIRE TOLD US IN HIS LATEST PODCAST. ALL OF THIS GOLD IS ENDING UP IN SHANGHAI GOLD EXCHANGE: SGE.

.

JUNE IS A HUGE DELIVERY MONTH AND HERE THE OI FELL BY 31,155 CONTRACTS DOWN TO AN OI OF 135,311. JUNE BECOMES THE NEW FRONT MONTH AND WE SHOULD HAVE A STRONG AMOUNT OF GOLD STANDING FOR DELIVERY.

JULY LOST 36 CONTRACTS DOWN TO AN OI OF 1641.

We had 263 contracts filed for today representing 26,300oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 263 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 60 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAY. /2026. contract month, we take the total number of notices filed so far for the month (6,573) to which we add the difference between the open interest for the front month of MAY 1054 CONTRACTS) minus the number of notices served upon today 263 x 100 oz per contract) equals 736,400 OZ OR (22.905 Tonnes of gold) to which we add our FIVE exchange for risk issuance for 792,000 oz or 24.635 tonnes//new standing for gold/May again advances to 47.540 tonnes which is a monstrous delivery for a non active delivery month.

THUS: INITIAL total number of gold ounces standing for MAY. /2026. contract month, we take the total number of notices filed so far for the month (6,573) to which we add the difference between the open interest for the front month of MAY( 1054 CONTRACTS) minus the number of notices served upon today 263 x 100 oz per contract) equals 736,400 OZ OR (22.905 Tonnes of gold) plus we must add our Five exchange for risk issuances of 792000 oz or 24.635 tonnes/new standing advances to 46.540 tonness

new total of gold standing in MAY ADVANCES TO 47.540 TONNES//

TOTAL COMEX GOLD STANDING FOR MAY 47.540 TONNES TONNES WHICH IS NOW HUGE FOR THIS NORMALLY NON ACTIVE DELIVERY MONTH OF MAY.

confirmed volume THURSDAY confirmed 225,680// fair// many have left the arena

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,925,502.739 oz 59.89 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,925,502.739 tonnes oz 59.89 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 28,670,896.030oz

TOTAL REGISTERED GOLD 15,669,075.906 487.374 tonnes

TOTAL OF ALL ELIGIBLE GOLD 13,001,820.124 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,743,573 oz ((REG GOLD- PLEDGED GOLD)=

427.48 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

MAY DELIVERY MONTH

MAY 22

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2 entries i) Out of Brinks: 1,200,607.240 oz ii Out of Manfra: 199,365.670 oz total withdrawal: 1,399,972.910oz |

| Deposits to the Dealer Inventory | 0 entries |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT DEPOSIT ENTRIES/CUSTOMER ACCOUNT 1 ENTRIES i) Into Asahi: 605,421.670 oz total deposit: 605,421.670 oz |

| No of oz served today (contracts) | 0 CONTRACT(S) (0.000 MILLION OZ |

| No of oz to be served (notices) | 744 Contracts (3.720 MILLION oz) |

| Total monthly oz silver served (contracts) | 5,681 contracts 28.405 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 entries

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1 ENTRIES

i) Into Asahi: 605,421.670 oz

total deposit: 605,421.670 oz

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

2 entries

i) Out of Brinks: 1,200,607.240 oz

ii Out of Manfra: 199,365.670 oz

total withdrawal: 1,399,972.910oz

adjustments 1 customer to dealer

a) Manfra; 19,940.417 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 81.689 MILLION OZ//.TOTAL REG + ELIGIBLE. 313.855 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2026 OI: 744 OPEN INTEREST CONTRACTS FOR A LOSS OF 32 CONTRACTS. WE HAD 37 CONTRACTS SERVED UPON ON THURSDAY SO WE GAINED 5 CONTRACTS OR 0.025 MILLION OZ UNDERWENT A QUEUE JUMP WHERE THEY WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND.

JUNE SAW A LOSS OF 44 CONTRACTS DOWN TO 2845 OI CONTRACTS

JULY SAW A LOSS OF241 CONTRACTS DOWN TO 72,173 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 or 0.0 MILLION oz

CONFIRMED volume THURSDAY; 40,402 poor

XXX

AND NOW MAY. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 5681 X5,000 oz = 28.405 MILLION oz

to which we add the difference between the open interest for the front month of MAY (744) AND the number of notices served upon today (0 )x (5000 oz)

Thus the standings for silver for the MAY 2026 contract month: (5,681 )Notices served so far) x 5000 oz + OI for the front month of MAY (744) minus number of notices served upon today (0)x 5000 oz equals silver standing for the MAY..contract month equating to 32.125 MILLION OZ.+TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.255 MILLION OZ//

NEW STANDING ADVANCES T0: 32.380 MILLION OZ WHICH IS STILL PRETTY GOOD FOR THIS ACTIVE DELIVERY MONTH OF MAY.

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 81.689 million oz of registered silver

JPMorgan as a percentage of total silver: 140.287/313.855 million: 44.61

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42.

The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

MAY 22 /2026/WITH GOLD DOWN $13.45 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

MAY 21 /2026/WITH GOLD UP $7.60 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

MAY 20 /2026/WITH GOLD UP $26.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.999 TONNES OF GOLD OUT OF THE GLD./ //:/INVENTORY RESTS AT 1036.851 TONNES

MAY 19 /2026/WITH GOLD DOWN $46.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.57 TONNES OF GOLD INTO THE GLD./ //:/INVENTORY RESTS AT 1038.85 TONNES

MAY 18 /2026/WITH GOLD DOWN $4.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 15 /2026/WITH GOLD DOWN $118.70 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 14 /2026/WITH GOLD DOWN $20.95 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 13 /2026/WITH GOLD UP $18.75 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 12 /2026/WITH GOLD DOWN $38.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.285 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 11 /2026/WITH GOLD DOWN $2.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.515 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1033.995 TONNES

MAY 8 /2026/WITH GOLD UP $22.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.283 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1033.480TONNES

MAY 7 /2026/WITH GOLD UP $15.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.853 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1033.197TONNES

MAY 6 /2026/WITH GOLD UP $124.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.718 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1034.05TONNES

MAY 5 /2026/WITH GOLD UP $33.75 TODAY/NO CHANGES IN GOLD AT THE GLD:// //:/INVENTORY RESTS AT 1035.768 TONNES

MAY 4 /2026/WITH GOLD DOWN $106.65 TODAY/NO CHANGES IN GOLD AT THE GLD:// //:/INVENTORY RESTS AT 1035.768 TONNES

MAY 1 /2026/WITH GOLD UP $13.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.427 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1035.768 TONNES

APRIL 30/2026/WITH GOLD UP $19.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 5.142 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1039.195 TONNES

APRIL 29/2026/WITH GOLD DOWN $45.70 TODAY/NO CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1044.337 TONNES

APRIL 28/2026/WITH GOLD DOWN $85.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1044.337 TONNES

APRIL 27/2026/WITH GOLD DOWN $41.10 TODAY/NO CHANGES IN GOLD AT THE GLD: // //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 24/2026/WITH GOLD UP $13.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 23/2026/WITH GOLD DOWN 28.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.000 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1050.91 TONNES

APRIL 22/2026/WITH GOLD UP 26.40 TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 21/2026/WITH GOLD DOWN 11.90TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 17/2026/WITH GOLD UP $71.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 1.15 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 16/2026/WITH GOLD DOWN $15.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.285 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1051.783 TONNES

APRIL 15/2026/WITH GOLD DOWN $24.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.289 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1049.478 TONNES

APRIL 14/2026/WITH GOLD UP $83.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.714 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1047.192 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 10/2026/WITH GOLD DOWN $11.90 TODAY/SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.724 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.42 TONNES

APRIL 9/2026/WITH GOLD UP $42.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.429 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.990 TONNES

APRIL 8/2026/WITH GOLD UP $88.95 TODAY/NO CHANGES IN GOLD AT THE GLD A//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 7/2026/WITH GOLD UP $5.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 3.429 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 6/2026/WITH GOLD UP $5.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/INVENTORY RESTS AT 1050.99 TONNES

APRIL 2/2026/WITH GOLD DOWN $132.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.714 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1050.99 TONNES

GLD INVENTORY: 1036.851 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

MAY 22 WITH SILVER DOWN $0.26: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.315 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 488.022 MILLION OZ

MAY 21 WITH SILVER UP $0.64: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

MAY 20 WITH SILVER UP $1.27: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

MAY 19 WITH SILVER DOWN $2.39: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.086 MILLION OZ OUT OF THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

MAY 18 WITH SILVER DOWN $0.09: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 489.424 MILLION OZ

MAY 15 WITH SILVER DOWN $7.06: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.9000 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 489.424 MILLION OZ

MAY 14 WITH SILVER DOWN $3,79: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.448 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 487.524 MILLION OZ

MAY 13 WITH SILVER UP $3,62: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.086 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 486.087 MILLION OZ

MAY 12 WITH SILVER DOWN $0.48: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.176 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 484.990 MILLION OZ

MAY 11 WITH SILVER UP $5.10: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.995 MILLION OZ OF SILVER PUT OF THE SLV// / // :INVENTORY RESTS AT 483.814 MILLION OZ

MAY 8 WITH SILVER UP $1.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.689 MILLION OZ OF SILVER INTO THE SLV// / // :INVENTORY RESTS AT 484.809 MILLION OZ

MAY 7 WITH SILVER UP $2.26: NO CHANGES IN SILVER INVENTORY AT THE SLV: / // :INVENTORY RESTS AT 484.130 MILLION OZ

MAY 6 WITH SILVER UP $3.75: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.724 MILLION OZ INTO THE SLV/ // :INVENTORY RESTS AT 484.130 MILLION OZ

MAY 5 WITH SILVER UP $0.21: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.734 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 483.604 MILLION OZ

MAY 4 WITH SILVER DOWN $3.05: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.734 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 483.604 MILLION OZ

MAY 1 WITH SILVER UP $2.38: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.905 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 484.338 MILLION OZ

APRIL 30 WITH SILVER UP $2.03: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.991 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 485.243MILLION OZ

APRIL 29 WITH SILVER DOWN $1.95: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 28 WITH SILVER DOWN $2.05: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 27 WITH SILVER DOWN $1.39: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 24 WITH SILVER UP 0.92: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.54 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 487,23MILLION OZ

APRIL 23WITH SILVER DOWN $2.35: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.489 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 488,773MILLION OZ

APRIL 22 WITH SILVER UP 1.43: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262MILLION OZ

aPRIL 21 WITH SILVER DOWN 3.71: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262 MILLION OZ

APRIL 17 WITH SILVER UP $3.09: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.453 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.900 MILLION OZ

APRIL 16 WITH SILVER DOWN $1.00: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.132 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.477 MILLION OZ

APRIL 15 WITH SILVER UP $0.01: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.588 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.579 MILLION OZ

APRIL 14 WITH SILVER UP $3.99: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.633 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.991 MILLION OZ

APRIL 13 WITH SILVER DOWN 0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.589 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.624 MILLION OZ

APRIL 10 WITH SILVER DOWN 0.16: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.724 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 492.213 MILLION OZ

APRIL 9 WITH SILVER UP $0.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.173 MILLION OZ INTO THE SLV// // :INVENTORY RESTS AT 492.937 MILLION OZ

APRIL 8 WITH SILVER UP $3.50: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 7 WITH SILVER DOWN $0.89: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 6 WITH SILVER UP $0.41: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL WITHDRAWAL OF 0.224 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 2 WITH SILVER DOWN $3.57: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.091 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.988 MILLION OZ

CLOSING INVENTORY 488.022 MILLION OZ OF SILVER

GOLD COMMENTARIES:

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD

US$ — Slowly then rapidly

Foreigners increasingly distrust the dollar, which is why central banks, the ultimate insiders are selling them for gold. The decline in the $ has not been noticed by Americans — yet.

| Alasdair MacleodMay 22∙Paid |

The chart above prices the dollar, which is only imaginary money, in real money which is gold. In 1968, when the exchange rate was $35 for an ounce of gold, if you bought $1,000 by selling 28.57 ounces of gold that $1,000 would be worth only 0.22 ounces today. The loss is represented by the double-headed arrow in the chart above. The pace at which the dollar’s value is slipping is now accelerating, even plotted on a log scale.

Of course, the relationship is almost always presented the other way round, showing gold having risen from $35 to $4,540 giving the illusion that gold is rising and the dollar is constant. The illusion continues to fool investors and commentators in G7 capital markets, but it no longer fools other foreign holders of the dollar, principally the Chinese. This is why gold and silver are being drained out of London and New York. Central banks and sovereign wealth funds along with increasing members of Asia’s private sector actors are dumping their excess dollars and other G7 currencies, encashing them for real money without counterparty risk.

Slowly and then suddenly is what Hemmingway said about bankruptcy. National bankruptcies are no different. But the way they are reflected in national bankruptcies is different, being exposed by loss of faith in the currency and the growing realisation that it is only imaginary money.

That is ahead of us, how far is difficult to tell. This week, gold and silver were on pause, with gold at $4520 down a mere $20 from last Friday, and silver at $75.75 is unchanged on the week. Silver’s volumes on Comex declined, suggesting that its sideways move is corrective of a positive trend, while gold’s volume improved over the week suggesting increasing resistance to further price rises. Looked at in the round, silver is suffering from lack of liquidity, while there’s plenty still in paper gold. But it is hardly relevant given the almost total absence of interest from US and London. This is reflected in the lowest levels of open interest on Comex for some time:

Very low open interest confirms oversold conditions when there are very few sellers left and buyers are uninterested. Furthermore, with stands-for-delivery and exchanges-for-physical, Comex vaults are being drained of bullion:

It turns out that gold is now one of the US’s top exports, not what was intended by the US Government’s rebalancing of the trade position. The other side of these exports is selling of the dollar, which is reflected in the dollar falling priced in yuan, China being the principal seller of dollars for gold and silver:

Slowly then suddenly: When Western capital markets run out of physical gold and silver to export to China and other Asian buyers, the price effect is likely to be dramatic. Investors in G7 capital markets will initially think it’s crazy, particularly with bond yields rising to long-term highs in all their currencies. Only later they will realise that it is not gold and silver rising, but their currencies entering a debt-driven collapse. And North Americans willingly exporting their gold hold an allocation estimated at only 0.2% in their $160 trillion portfolios. Their exposure to the collapse of their dollars is virtually total.

3. CHRIS POWELL AND HIS GATA DISPATCHES

Gold will replace the dollar in oil trade, Maguire tells LFTV

Submitted by admin on Thu, 2026-05-21 12:54 Section: Daily Dispatches

12:52p ET Thursday, May 21, 2026

Dear Friend of GATA and Gold:

Gold is likely to replace the U.S. dollar as the trade settlement currency for oil, London metals trader Andrew Maguire tells this week’s edition of Kinesis Money’s “Live from the Vault” program.

This replacement, Maguire explains, will be accomplished through the Chinese yuan, which is freely convertible to gold at the Shanghai exchange. China, Maguire notes, already operates an international bank clearing system.

The program is 54 minutes long and can be viewed at Kinesis Money’s channel at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Money Metals CEO deplores superficiality of treatment of Fort Knox gold issue

Submitted by admin on Wed, 2026-05-20 23:24 Section: Daily Dispatches

11:28p ET Wednesday, May 20, 2026

Dear Friend of GATA and Gold:

In an interview today with Chris Marcus of Arcadia Economics, Money Metals Exchange CEO Stefan Gleason deplores the superficiality with which the issue of auditing the U.S. gold reserve at Fort Knox continues to be treated by the Trump administration and financial news organizations.

The audits claimed to have been done by the U.S. government, Gleason says, have not really been audits at all but just a review of paperwork that itself has been improperly altered from time to time.

In any case, Gleason says, much of the U.S. gold reserve is impure metal, not acceptable for trade under current “good delivery” standards, and thus could not be fully mobilized in a financial emergency. U.S. Treasury officials, Gleason says, don’t seem to understand this basic issue.

Then, Gleason notes, there is the question of whether the U.S. gold reserve has been encumbered in any way by swaps, leases, or other transactions undertaken for surreptitious intervention in markets. That is, that there is gold in Fort Knox is only part of the issue; the other part is: Does anyone besides the U.S. government have a claim on it?

Gleason also recalls a conversation he had some years ago with former Federal Reserve Governor Kevin Warsh, who has just reappointed to the Fed board as chairman, in which Warsh backhandedly acknowledged that the Fed had intervened surreptitiously in the gold market.

The interview is 27 minutes long and can be viewed at the Arcadia Economics channel at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Hong Kong targets July launch for new gold-clearing system

Submitted by admin on Wed, 2026-05-20 10:33 Section: Daily Dispatches

By Yihui Xie

Bloomberg News

Tuesday, May 19, 2026

Hong Kong plans to launch a new gold-clearing system by July, advancing the city’s ambitions to become a global hub for bullion trading.

The government-owned mechanism will mirror the financial infrastructure used in London, the world’s largest bullion market, and allow participants to settle trades through unallocated accounts, people familiar with the matter said, requesting anonymity as they are not authorized to speak to the media.

Unallocated accounts allow for faster and more scalable trading, which is important for liquidity. They permit customers to hold a claim against the clearer on a quantity of gold without the need to own specific, numbered bars. Most precious metals traded in London are cleared in this way.

Hong Kong has invited a number of China-friendly central banks to participate in the clearing system as part of a push to promote itself as a trading, financing, and storage hub. The special administrative region has also signed a cooperation pact with the Shanghai Gold Exchange and plans to expand gold-storage capacity to 2,000 tons within three years. …

… For the remainder of the report:

END

Japan, China lead foreign govt. retreat from U.S. Treasurys as Iran war stokes currency fears

Submitted by admin on Wed, 2026-05-20 08:57 Section: Daily Dispatches

By Anniek Bao

CNBC, New York

Tuesday, May 19, 2026

Foreign governments cut U.S. Treasurys in March as the Middle East war forced central banks to liquidate dollar reserves, defending local currencies against an energy shock that sent exchange rates tumbling.

China reduced its holdings to $652.3 billion, down roughly 6% from February to the lowest level since September 2008, according to U.S. Treasury data released late Monday stateside.

Japan, the single largest foreign holder of U.S. government debt, shed approximately $47 billion to $1.191 trillion. Overall foreign holdings fell to $9.25 trillion in March from $9.49 trillion in February.

The selloff came as the outbreak of the U.S.-Iran conflict and a subsequent surge in crude oil prices sent the yen and other Asian currencies tumbling. Regional economies reliant on Gulf oil imports, including Japan, faced the largest energy shock in decades, prompting policymakers to sell part of their dollar-denominated assets to fund currency intervention.

“Given increased financial volatility since the start of the war in the Gulf, and resultant pressure on exchange rates, especially in Asia, it is not a surprise that U.S. Treasury holdings by central banks have fallen,” said Frederic Neumann, chief Asia economist at HSBC.

“Exchange market intervention to support local currencies will have led some central banks to sell a share of their U.S. Treasury holdings.” …

… For the remainder of the report:

4.ANDREW MAGUIRE LIVE FROM THE VAULT 273 and 272

MUST VIEWl ANDREW’S NEWEST PODCAST

Ted Oakley//272

5. COMMODITY REPORT/GOLD

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 36.04 PTS OR 0.39%

HANG SENG CLOSED UP 236.00 PTS OR 0.94%

Nikkei CLOSED UP 1690.80 PTS OR 2.74%

//Australia’s all ordinaries CLOSED UP .02%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.7970

/ OFFSHORE CLOSED UP AT 6.8002 Oil DOWN TO 98.06 dollars per barrel for WTI and BRENT UP TO 105.14 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING UP (6.7970) OFFSHORE YUAN TRADING UP TO 6.8002 ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP 6.7970

OFFSHORE YUAN: UP TO 6.8002

1.HANG SANG CLOSED UP 236.00 PTS OR 0.94%

2. Nikkei closed UP 1690.50 PTS OR 2.74%

WEST TEXAS INTERMEDIATE OIL DOWN TO 98.06

BRENT; 105.14

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 99.24/// EURO FALLS TO 1.1608 DOWN 9 BASIS PTS

3b Japan 10 YR bond yield:FALLS TO. +2.754 DOWN 1/2 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 159.12… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.998 DOWN 3 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP( 6.7990 AND OFFSHORE: UP AT 6.8002

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and BRENT DOWN this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +3.0637// Italian 10 Yr bond yield DOWN to 3.810// SPAIN 10 YR BOND YIELD DOWN TO 3.475%

3i Greek 10 year bond yield DOWN TO 3.722%

3j Gold at $4527/00 //Silver at: 76.25 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 16/ 100 roubles/71.36

3m oil (WTI) into the 98 dollar handle for WTI and 105 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 159.12 // 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.754% DOWN 1/2 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.998 DOWN 3 PTS..: USA/SF this 0.7867 as the Swiss Franc . Euro vs SF: 0.9136

USA 10 YR BOND YIELD: 4.573 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 5.092 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.085 UP 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 45.74 UP 12 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD AND USA DOLLAR RESERVES.

10 YR UK BOND YIELD: 4.9680 DOWN 2 PTS

30 YR UK BOND YIELD: 5.638 DOWN 3 BASIS PTS

10 YR CANADA BOND YIELD: 3.552 DOWN 3 BASIS PTS

5 YR CANADA BOND YIELD: 3.199 DOWN 3 BASIS PTS.

1a New York Opening report

US Stock Futures Rise, Set For 8th Consecutive Week Of Gains

Friday, May 22, 2026 – 08:07 AM

US equity futures are higher into the long weekend, with the S&P 500 gaining for an 8th consecutive week higher, its longest streak of weekly wins since 2023 with sustained momentum in popular thematics, thanks to a liquidity boost, supportive macro readings, solid earnings and hopes that the US and Iran are moving closer to a peace deal, not to mention unrelenting enthusiasm for artificial intelligence which is fueling a historic gamma squeeze.

As of 7:30am ET, S&P futures are 0.2% higher, cutting overnight gains of 0.5% by more than half, and Nasdaq future gain 0.1% with most Mag 7 banes higher pre market led by GOOG/L (+0.4%) and NVDA (+0.3%). Bond yields are 1-2bp lower led by the belly of the curve; the 10-year yield is down two basis points to 4.55%; the softer-than-expected Japan CPI drove 30Y JGB yield 3.6bp lower (now back below 4%), which supported global bond markets. The USD is higher, while commodities are mixed: WTI crude added $2.10 to $98.50 this morning; precious metals are lower; Brent rebounded 2.6% to above $105 a barrel, but remained lower for the week. Ags are higher. Economic data slate includes May final University of Michigan sentiment (10am) and Kansas City Fed services activity (11am). Fed speaker slate includes only Waller at 10am

In premarket trading, Mag 7 stocks are mixed (Alphabet +0.06%, Nvidia +0.2%, Apple +0.07%, Tesla +0.05, Amazon -0.2%, Microsoft +0.1%, Meta -0.2%)

- US-listed Chinese stocks decline after China’s securities regulator announced plans to penalize three cross-border brokerages, adding to investor concerns around Beijing’s stance toward internet firms. Among large-cap Chinese internet firms, Alibaba (BABA) -4% and Baidu (BIDU) -3%.

- Booz Allen Hamilton (BAH) rises 5% after the defense contractor forecast adjusted Ebitda for 2027 that beat the average analyst estimate.

- Deckers Outdoor (DECK) gains 2% after the parent company of both Ugg and Hoka reported revenue for the fourth quarter that beat the average analyst estimate.

- Estee Lauder Cos. (EL) climbs 10% after the collapse of a proposed combination with Puig Brands SA that would have created one of the world’s largest fragrance and skincare companies.

- IBM (IBM) rises 2%, GlobalFoundries (GFS) gains 3% and smaller quantum computing firms climb, putting them on track to build on Thursday’s rally that came after the US government awarded $2 billion to IBM and several other companies as part of an investment push to develop quantum wafer facilities.

- IMAX Corp. (IMAX) gains 15% after the Wall Street Journal reported the large-screen theater company is exploring a sale and has approached entertainment companies as potential buyers.

- Ross Stores (ROST) rises 4% after the off-price retailer boosted its comparable sales forecast for the full year.

- Sweetgreen (SG) gains 6% after JPMorgan raised its recommendation on the restaurant chain to overweight from neutral on new products and an improving balance sheet.

- Take-Two Interactive Software (TTWO) rises 2% after the video-game company reported fourth-quarter results that beat expectations and confirmed a Nov. 19 release date for Grand Theft Auto VI.

- Workday (WDAY) jumps 7% after the software company reported first-quarter results that beat expectations and gave an outlook that is seen as positive.

- Zoom Communications (ZM) rises 7% after the company raised its full-year forecast for both adjusted earnings and revenue. It also reported first-quarter results that beat expectations.

In other news, SpaceX delayed a critical test of its massive Starship rocket just seconds before launch after a pin holding the tower arm in place failed to retract. Polymarket has appointed a representative in Japan and is preparing to lobby for the authorization of prediction markets in the country.

Markets are heading into the weekend on a quieter note, shaking off worries that severe disruptions to energy flows from the Middle East could stoke inflation. Signs that neither Iran nor the US is looking to widen their conflict and growing appetite for a broader group of AI beneficiaries have kept volatility subdued despite conflicting reports around peace talks. A drop in the VIX to the lowest since early February is helping the mood, as are some chunky numbers on announced corporate equity purchases. These have already exceeded $1 trillion for 2026 across new stock buybacks and cash takeovers, according to EPFR data.

Those looking for signs of economic resilience can point to the “US exceptionalism” that strategists at Evercore ISI saw in Thursday’s S&P PMI data. They lauded the contributions from domestic energy production, AI capex and wealth creation. Exceptional, too, is the performance by tech and AI since the start of the Iran War. A basket of stocks exposed to the Anthropic AI ecosystem has surged 56% since the start of March while the equal-weighted S&P 500 is flat.

On the subject of AI, Bloomberg notes that talks between the EU and Anthropic over testing banks and companies for digital vulnerabilities have stalled. Lenovo jumped to 26-year highs in Hong Kong trading after AI-related sales surged 84% year-on-year. DeepSeek’s senior management is said to have told potential investors in its ongoing 70 billion yuan ($10 billion) funding round that the startup will prioritize groundbreaking AI research over short-term commercialization.

“We’ve got the biggest capital spending boom since the financial crisis,” said Guy Miller, chief market strategist at Zurich Insurance.“That’s leading to record corporate profitability; we are in this virtuous circle where it’s generating profitability for other suppliers, other companies too.”

“The market is fully aware that headlines will remain volatile, and while oil needs to react for practical reasons, equities have probably moved on,” said Geoff Yu, senior macro strategist at BNY. “The lack of an agreement does not imply re-escalation, so the focus for now will stay with earnings and data.”

In politics, Alberta’s Premier said she’ll call a referendum on whether the energy-rich province should stay in Canada or start a legal process that could eventually lead to its independence. China imposed new export controls on some key chemical ingredients shipped to the US, Mexico and Canada, in a further sign of cooperation with Washington on curbing drug trafficking.

Away from stocks, treasuries gain for a third straight day after yields earlier this week tested multiyear highs. Investors said US authorities remain highly attentive to borrowing costs and that current levels will sharpen the White House’s resolve to find a resolution in the Middle East.

“The administration is well-focused on the bond market, even more than equities in my view, so they won’t allow the curve to steepen much further,” said Andrea Gabellone, head of global equities at KBC Securities.

In Europe, the Stoxx 600 rose for a fifth straight day, climbing 0.5% as the region’s semiconductor-linked stocks such as ST Microelectronics, ASML Holding and Infineon led gains.Here are the biggest movers Friday:

- Deutsche Post shares gain as much as 4.5% after being upgraded at Deutsche Bank, with analysts calling an end to the earnings downgrade cycle and saying recent fears over AI disruption and competition are overdone

- Softcat shares rise as much as 12%, hitting a six-month high, after the IT services firm lifted its annual underlying operating profit guidance. Analysts said a pull-forward in orders helped and expect consensus estimates to increase

- Brembo shares jump as much as 9.3% after the breaking systems maker announced the creation of a joint venture with Ningbo Huaxiang in China

- Games Workshop shares rise as much as 3.6% after the Warhammer owner said it expects full-year core revenue and pretax profit to be higher than the previous year

- Siemens Healthineers shares climb as much as 1.5% as Barclays analysts note the German medical equipment maker’s upbeat commentary on inflation at its European Leadership conference this week

- Puig shares slide as much as 15% at open, the most on record since its 2024 IPO, after the Spanish beauty firm’s merger talks with Estee Lauder collapsed

- Julius Baer shares dropped 10% following earnings update that analysts say was disappointing, with weak inflows. Shares had gained 9% YTD through Thursday

- Genuit Group shares drop as much as 6.1% after the developer of plastic piping systems warned its annual underlying operating profit will be toward the lower end of analyst expectations

- Amplifon drops as much as 3% after the Italian company sold shares to fund its acquisition of GN Store Nord’s hearing-aid business, announced in March

- Alerion Clean Power shares drop as much as 11% after the Italian renewable energy company’s board approved a €135.6 million capital increase, excluding pre-emptive rights, for up to 10% of its share capital

Earlier, Asian equities extended their advance, supported by sustained optimism in artificial intelligence and signs of progress in US-Iran talks. The MSCI Asia Pacific Index climbed as much as 1%, putting it on track to recover losses from the previous week. Japan and Taiwan led broad advances in the region. Interest in AI stocks remained firm amid stellar results from companies. Lenovo Group was the best performer on the Asian benchmark after reporting strong growth in AI-related earnings. In Japan, tech shares led gains, while the Kosdaq gauge extended gains in South korea to a second day, driven by a new government-backed fund for tech firms. Japanese equities rose, “supported by lower interest rates and expectations for an end to the Iran conflict,” BofA Securities analysts including Masashi Akutsu wrote in a note. “From a medium-term perspective, we maintain a preference for AI-related names and a bullish stance on Japanese equities.” Here Are the Most Notable Movers

- China’s hottest AI stocks may be among candidates for inclusion in Hong Kong stock gauges, opening access to trading links that may trigger billions of dollars in inflows.

- Zhipu shares surge as much as 23% in Hong Kong to a record, with analysts citing the Chinese AI company as a potential candidate for inclusion in the Hang Seng Tech Index.

- Lenovo Group Ltd. shares jumped to the highest in 26 years on Friday after reporting strong growth in AI-related earnings that offset difficulties from rising component prices.

- SoftBank Group shares surged for a second day, rising as much 13.9%, after the ADRs of its unit ARM Holdings rallied in the wake of earning results from AI chip leader Nvidia, which Jefferies sees as positive for ARM.

- Tongcheng Travel’s shares drop as much as 6.6%, after Citigroup cut its price target for the Chinese online travel agent, citing concerns over the greater-than-expected impact of oil price hikes on domestic Travel.

- Shares of NetEase rise as much as 5.8% in Hong Kong after the Chinese video games company reported better-than-expected results, thanks to strong game revenue growth and record-high margins after cost-cutting efforts.

- Lenovo’s shares rally as much as 11% in Hong Kong to their highest since March 2000, after the Chinese computer hardware maker reported fourth quarter revenue that beat estimates.

- Xiaomi’s Hong Kong-listed shares jump as much as 1.6% after the company introduced a performance version of its popular YU7 SUV, which Citigroup estimates could achieve monthly sales above 10,000 units.

- Shares of Guzman y Gomez surge as much as 21% after the Australian burrito restaurant chain exits the US market, a move that analysts say will improve future earnings.

- Tuas shares slide as much as 10% after the Australian telecommunications firm confirmed that the sale and purchase agreement for its subsidiary Simba to acquire M1 has been terminated.

The Bloomberg Dollar Spot Index is up by 0.2% after closing +0.1% in a choppy Thursday session, Antipodeans lag amid the risk environment and shifting tightening bets. Conflicting reports from the Gulf whipsawed the Buck on Thursday. Traders circulated fabricated reports that a final US-Iran draft had been reached, attributing the report to Al Arabiya, though this was later denied by the outlet. Despite this, progress in talks appears evident, while gaps remain on key issues, uranium and Hormuz. Energy benchmarks have rebounded, and as such, DXY is a touch firmer. The index resides well above significant DMAs, and within recent ranges – today supported by 99.20.

- AUD is the worst G10 performer as domestic banks push back on RBA calls. Recent soft PMI, and labour market data which showed a surprise contraction in headline employment change, and an uptick in the unemployment rate prompted NAB and Westpac to push calls for tightening back to August, which both previously expected the first hike expected in June. AUD/USD resides within Thursday’s ranges, remaining below 0.72 and supported by 0.71.

- GBP is unchanged against the Buck, and a touch firmer against the EUR. Retail Sales missed estimates, with the ONS noting that the poor figure was driven lower by fuel purchases. The PSNB figure also rose from April’s print and overshot the OBR’s forecast.

- EUR/GBP lower by 0.1% and within Thursday’s broad ranges. Support around 0.8640. GBP/USD little changed, within recent ranges

In rates, Treasuries gained for a third straight day after yields earlier this week tested multiyear highs. US yields are 1bp-1.5bp richer across the curve with intermediates outperforming, flattening 2s10s spread by almost 1bp; 10-year near 4.56% trails bunds and gilts in the sector by about 2.5bp. SIFMA has recommended a 2pm New York time close of trading for USD-denominated cash bonds ahead of US Memorial Day holiday Monday. IG dollar issuance slate empty so far. One offering was priced on Thursday, bringing weekly total to about 80% vs dealers’ $40 billion forecast. Focal points of holiday-shortened US session include University of Michigan sentiment data and speech by Fed’s Waller on the economic outlook.

In commodities, WTI crude futures are up around 2%, snapping a three-day decline, following latest Iran comments on uranium and the Strait of Hormuz.

Economic data slate includes May final University of Michigan sentiment (10am) and Kansas City Fed services activity (11am). Fed speaker slate includes only Waller at 10am

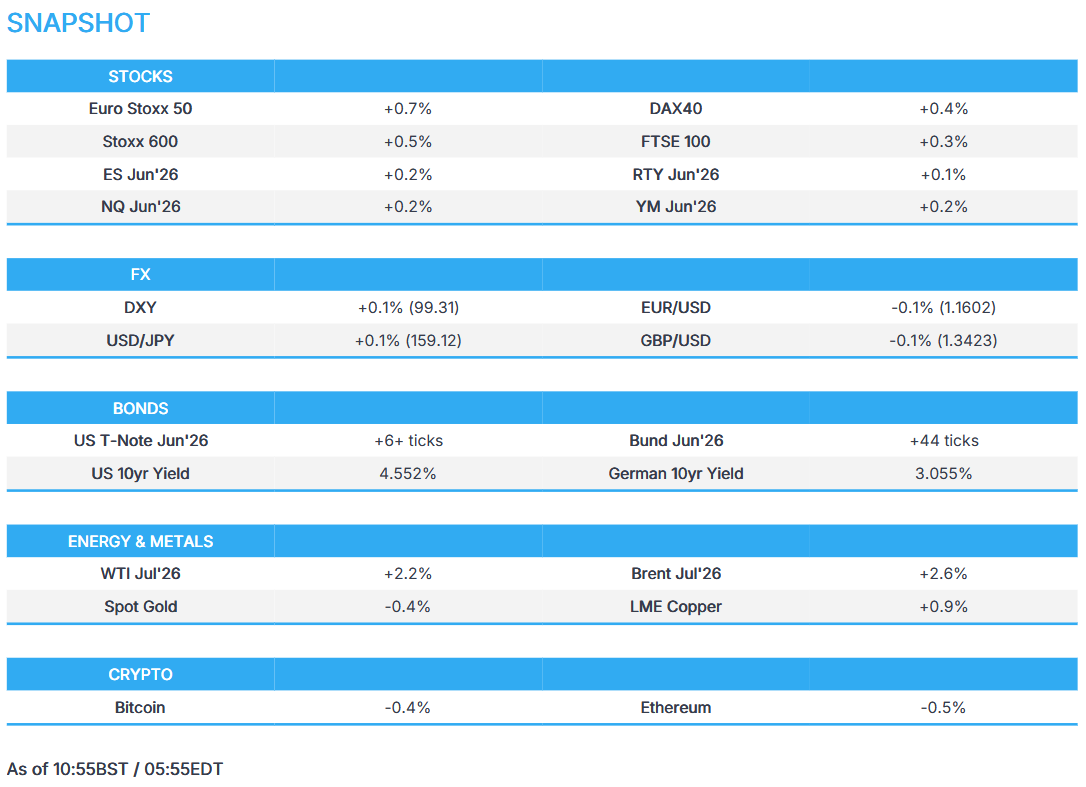

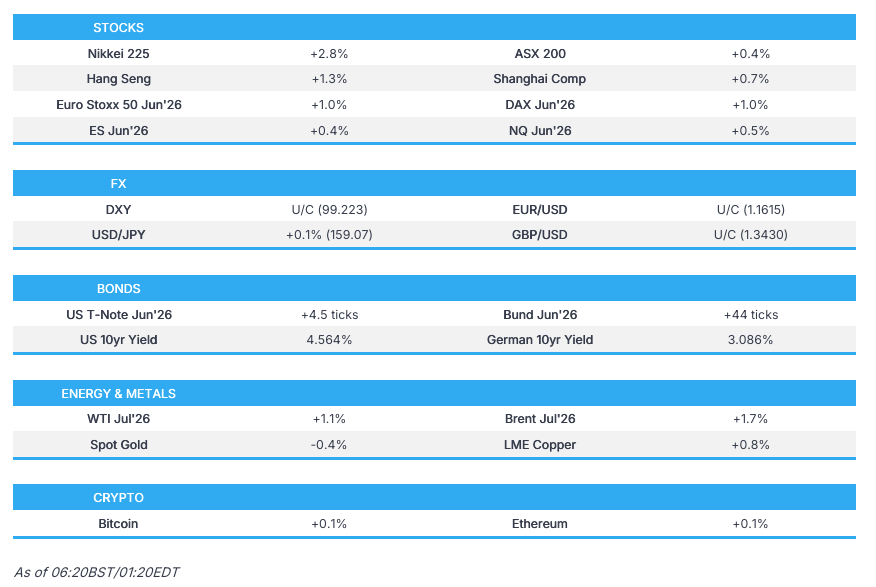

Market Snapshot

Top overnight News

- Oil rose as an Iran peace deal remained elusive. Iran’s recent attack on UAE’s nuclear power plant is seen as a “warning shot.” BBG

- Arabiya and Al Hadath exclusively report the text of the anticipated US-Iran agreement in case of its approval. The agreement includes: an immediate, comprehensive, and unconditional ceasefire on all fronts, a halt to military operations, ensuring freedom of navigation in the Arabian Gulf, the Strait of Hormuz, and the Sea of Oman and establishing a joint mechanism for monitoring and resolving disputes.

- Trump said the US will send 5,000 more troops to Poland in a policy U-turn. Separately, Ukraine and its allies are growing confident Russia’s invasion is running out of steam. BBG

- China has launched an unprecedented campaign against illegal cross-border trading, threatening severe penalties against popular brokers and ordering existing non-compliant accounts to be liquidated within two years. BBG

- China imposed new export controls on some key chemical ingredients shipped to the US, Mexico and Canada, in a further sign of cooperation with Washington on curbing drug trafficking. The targeted substances are primary building blocks used to manufacture illicit fentanyl. BBG

- China’s stock exchanges are scrutinizing recent stock rallies that have been fueled by artificial intelligence optimism, asking some listed companies and funds to give more details about their approach to the technology. Regulators have sent inquiries to managers of exchange-traded funds and other funds with heavy exposure to AI-related sectors, asking them to disclose their valuation methodologies and justify the assets they hold. BBG

- Japan’s key inflation gauge rose at the slowest pace in four years as the government continued to help ease the cost of living, creating difficult optics for the Bank of Japan to raise interest rates soon. Japan’s core consumer price index, which excludes fresh food, rose 1.4% in April from a year earlier. BBG

- The IMF approved the latest review of Argentina’s $20 billion debt deal to unlock about $1 billion, a vote of confidence in Javier Milei despite the country missing a program target. BBG

- UK government borrowing hit the highest level for any April in six years, as pressure on public finances mounts from the Iran war and domestic political instability. BBG