EXCHANGE: COMEX

CONTRACT: JUNE 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,475.800000000 USD

INTENT DATE: 06/04/2026 DELIVERY DATE: 06/08/2026

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DEUTSCHE BANK AG 5

190 H BMO CAPITAL MARKETS 1

323 C HSBC 80

435 H SCOTIA CAPITAL (USA) 78

555 C BNP PARIBAS SEC CORP 255

657 H MORGAN STANLEY 17

661 C JP MORGAN SECURITIES 8

709 C BARCLAYS 61

737 C ADVANTAGE FUTURES 1

905 C ADM 32

TOTAL: 269 269

MONTH TO DATE: 27,928

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2026: 269CONTRACTs NOTICES FOR 26,900 OZ or 0.836 TONNES

total notices so far: 27,928 contracts FOR 2,792,800 OZ OR 86.867 TONNES

SILVER NOTICES: 90 NOTICE(S) FILED FOR 0.450 MILLION OZ /

total number of notices filed so far this month : 2084 CONTRACTS (NOTICES) for 10.420 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A TINY QUEUE JUMP OF 1 CONTRACTS OR 0.005 MILLION OZ/NEW STANDING ADVANCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT QUEUE JUMP WHERE 5,000 OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES SLIGHTLY TO 16.565 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER 3 ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.730 MILLION OZ//

INITIAL STANDING FOR MAY: 31.495 MILLION OZ FOLLOWED BY ANOTHER 3 CONTRACT EXCHANGE FOR PHYSICAL JUMP TO LONDON FOR 0.015 MILLION OZ// AND THEN TO BOOT WE HAD OUR FIRST EXCHANGE FOR RISK ISSUANCE FOR 51 CONTRACTS OR 255,000 OZ MAY 21./STANDING BEFORE EXCHANGE FOR RISK: 32.070 MILLION OZ/NEW STANDING THUS REDUCES TO 32.325 MILLION OZ/.//(32.070 MILLION OZ NORMAL STANDING PLUS .255 MILLION OZ EXCHANGE FOR RISK = 32.325 MILLION OZ)

JUNE INITIAL STANDING FOR SILVER:10.935 MILLION OZ TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 480,000 OZ//NEW STANDING ADVANCES TO 11.635 MILLION OZ//

SUMMARY OF OUR JUNE 2026 COMEX CONTRACT MONTH:

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 44.44 MILLION OZ//FINAL.. SMALL THIS MONTH.

MAY 59.79 MILLION OZ

JUNE..14.280 MILION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUUE JUMP //NEW STANDING ADVANCES TO 16.565MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.730 MILLION OZ

MAY: INITIAL AMOUNT OF SILVER WILLING TO STAND; 31.495 MILLION OZ/ TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL JUMP OF 15,000 OZ//NEW STANDING REDUCES TO 32.070 MILLION OZ//(FOLLOWING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON DURING THIS MAY DELIVERY MONTH). THERE SEEMS TO BE A SCARCITY OF SILVER OVER AT THE COMEX). THEN WE ADD OUR FIRST EXCHANGE FOR RISK OF 51 CONTRACTS FOR 255,000 OZ//STANDING ADVANCES TO 32.325 MILLION OZ//

JUNE: INITIAL AMOUNT OF SILVER WILLING TO STAND: 10.935 MILLION OZ PLUS OUR NEXT QUEUE JUMP OF 480,000 OZ//NEW STANDING ADVANCES TO: 11.635 MILLION OZ

GOLD//OUTLINE

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 345 CONTRACT QUEUE JUMP FOR 34,500 OZ/ (1.073 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR 2ND EXCHANGE FOR RISK OF 1498 CONTRACTS FOR 149800 OZ OR 4.659 TONNES. THE NEW TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL IS 2239 CONTRACTS OR 223900 OZ OR 6.964 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS (70.762 TONNES) TO GIVE US WHAT WILL STAND IN APRIL (77.726 TONNES)

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 345 CONTRACTS OR 34500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCES FOR 24.635 TONNES/STANDING NOW ADVANCES TO 51.554 TONNES OF GOLD.

JUNE; INITIAL AMOUNT OF GOLD WILLING TO STAND; 64.496 TONNES.(CME CORRECTED) TO WHICH WE ADD OUR NEXT HUGE 1.878 TONNES OF A QUEUE JUMP/NEW STANDING ADVANCES TO 90.653 TONNES

STANDING FOR THE LAST 5 MONTHS JANUARY TO MAY:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR TWO EXCHANGE FOR RISK FOR 223,900 OZ OR 6.964 TONNES/NEW STANDING: 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND; 12.24 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 345 CONTRACTS/34,500 OZ// 1.073 TONNES/ THEN WE MUST ADD OUR EXCHANGE FOR RISK ISSUANCE: TOTAL EXCHANGE FOR RISK MAY// 5 OCCASIONS: 24.635 TONNES///NEW STANDING NOW ADVANCES TO 51.554 TONNES

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 1.878 TONNES//NEW STANDING ADVANCES TO 90.653 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 88.00 TONNES// WILL BE VERY SMALL THIS MONTH

MAY 118.430 TONNES

JUNE: 36.379 TONNES

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SOIS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A STRONG 420 CONTRACTS TO AN OI OF 103,653.

EFP ISSUANCE 260 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 260 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 420 CONTRACTS AND ADD TO THE 260 E.FP. ISSUED

WE OBTAIN A HUGE GAIN OF 680 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR GAIN OF $0.52

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 3.4000 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $0.52

2.ASIAN AFFAIRS JUNE 5 /2025

SHANGHAI CLOSED DOWN 30.04 PTS OR 0.74%

HANG SENG CLOSED DOWN 291.45 PTS OR 1.15%

Nikkei CLOSED DOWN 852.69 PTS OR 1.26%

//Australia’s all ordinaries CLOSED DOWN 0.91%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.7674

/ OFFSHORE CLOSED UP AT 6.7670 Oil DOWN TO 92.33 dollars per barrel for WTI and BRENT DOWN TO 94.65 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN// WITH YUAN TRADING UP (6.7674) OFFSHORE YUAN TRADING UP TO 6.7670 ONSHORE YUAN TRADING BELOW LEVEL OF OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL 193 CONTRACTS TO 328,219 RISING FROM ITS NEW ALL TIME LOW OF 326,052 OI SET JUNE 3, SURPASSING THE PREVIOUS ALL TIME LOW OF 345,705 SET (MAY 28) AND SURPASSING THE PREVIOUS ALL TIME LOW IN OI OF 353,490 SET MAY 27.. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 326,052 WITH GOLD AT AN EXTREMELY HIGH $4,450.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD HUGE T.A.S. LIQUIDATION DURING FRIDAY’S OP =EX TRADING (OTC/LONDON OPTIONS EXPIRY TRADING) AND JUNE 3!!. IT SEEMS THAT SOME OF THE SPECULATORS CONTINUED AGAIN TO GO MASSIVELY ON THE SHORT SIDE BUT WITH THE BANKERS NOW TAKING THE LONG SIDE,AND CENTRAL BANKS SUPPLYING THE NECESSARY PAPER, AS WELL AS COVERING THEIR SHORTFALL.

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE STRONG AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS MAY CONTRACT MONTH!!

THE FAIR SIZED GAIN ON OUR TWO EXCHANGES OCCURRED WITH OUR GAIN IN PRICE IN GOLD (UP $39.25).

WE THUS HAD A FAIR SIZED GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 1198 CONTRACTS (OR 3.726 TONNES) WITH OUR GAIN IN PRICE, AS WE WERE INFORMED OF A FAIR CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE, EQUATING TO 1005 CONTRACTS.

THEN WE WERE NOTIFIED TODAY OF A 0 CONTRACT FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. ON FRIDAY, BY FAR WE HAD THE HIGHEST EVER EXCHANGE FOR RISK EVER ISSUED AT ONE TIME BEATING THE PREVIOUS SINGLE HIGHEST ISSUE BY ONE TONNE. THUS MAY 22 RECORDS THE HIGHEST EVER EXCHANGE FOR RISK AT 12.4416 TONNES. WE HAD OUR FIRST ISSUANCE FOR EXCHANGE FOR RISK IN THE MONTH OF MAY ON MAY 7, THEN OUR 2ND ISSUANCE FOR OUR MAY GOLD MONTH ON MAY 12. THE THIRD ON MAY 18 , THEN MAY 21 OUR 4TH ISSUANCE AND THEN FINALLY FRIAY, OUR 5TH ISSUANCE. THIS GOLD WILL BE ADDED TO OUR NORMAL MAY DELIVERIES TO GIVE US OUR FINAL AMOUNT OF GOLD WILLING TO STAND AT THE COMEX..

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH MAY

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 2 EXCHANGE FOR RISK SO FAR, I.E. 2239 CONTRACTS FOR 223,900 OZ OR 6.964 TONNES AND THIS TOTAL TONNES WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND IN APRIL

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS OR 792,000 OZ OR 24.635 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO MAY:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 2 EXCHANGE FOR RISK SO FAR FOR 223,900 OZ OR 6.964 TONNES. AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND FOR APRIL!!

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS, 792,000 OZ OR 24.635 TONNES OF GOLD. THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES IN MAY TO GIVE US WHAT WILL STAND IN MAY.

JUNE: ZERO SO FAR

DETAILS ON OUR NEW JUNE COMEX CONTRACT MONTH//

IN TOTAL WE HAD A FAIR GAIN ON OUR TWO EXCHANGES OF 1198 CONTRACTS WITH OUR GAIN IN PRICE ($39.25). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THEIR THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH MAY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A SMALL SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 497 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD. APRIL HAD 2 EXCHANGE FOR RISK ISSUANCES FOR 6.694 TONNES. AND NOW MAY WITH ITS 5TH ISSUANCE FOR 12.4436 TONNES///TOTAL EXCHANGE FOR RISK FOR MAY: 24.635 TONNES ISSUED MAY 6 ,MAY 12, MAY 18 MAY 21 AND NOW MAY 22..

WE MUST ALSO REMEMBER THAT THE FRBNY IS SHORT 134+ TONNES OF GOLD, THIS COMMENCED ON JAN 2 2023 AS THEY REFUSE TO COVER DESPITE THE BIS’S PLEA TO DO SO. WE WILL KNOW IN JUNE WHETHER THEY COVERED ANY OF THEIR SHORTFALL.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

1.APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.05 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP/ TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES TOTALLING 223,900 OZ OR 6.964 TONNES//STANDING ADVANCES TO 77.726 TONNES WHICH IS ABSOLUTELY HUGE

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT HUGE QUEUE JUMP OF 34,500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCE FOR 792,000 OZ OR 24.635 TONNES////NEW TOTALS STANDING FOR GOLD ADVANCES TO 51.554 TONNESS

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES TO WHICH WE ADD OUR NEXT HUGE QUEUE JUMP OF 1.878 TONNES//NEW STANDING ADVANCES TO 90.653 TONNES//

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING JUNE,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $39.25)

WE HAD LITTLE IF ANY, T.A.S. SPREADER LIQUIDATION THURSDAY // COMEX SESSION// WITH OUR GAIN IN PRICE , OUR LONG SPECULATORS STILL REMAIN RELENTLESS POURING INTO THE COMEX

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

THURSDAY NIGHT//FRIDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $39.25

WE HAD A FAIR 1140 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES: 3.736 TONNES

(GAIN IN COMEX 193 CONTRACTS AND GAIN IN EXCHANGE FOR PHYSICAL 1005 = 1198 CONTRACTS OR 3.736 TONNES)

MAY DELIVERY MONTH

JUNE 5

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 ENTRIES |

| Deposit to the Dealer Inventory in oz | 0 ENTRY oz |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER//gold ENTRY:0 xxxxxxxxxxxxxxxx |

| No of oz served (contracts) today | 269 CONTRACTS OR 26,900 OZ 0.836 TONNES OF GOLD |

| No of oz to be served (notices) | 1217 Contracts 121,700 OZ 3.785 TONNES |

| Total monthly oz gold served (contracts) so far this month | 27,928 notices 2,792,800 oz 86.867 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

DEPOSITS/CUSTOMER

ENTRY: 0

xxxxxxxxxxxxxxxxxx

comex withdrawal

0 ENTRIES

adjustments: 3// dealer: to customer

a) BRINKS 16,137.155 OZ

b) JPMORGAN: 14,457.938 OZ

c) Stonex: 6655.257 oz

total adjusted out of the dealer: 37,260.380 oz or1.15 tonnes

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF JUNE OI STANDS AT 1486 CONTRACTS HAVING A LOSS OF 1710 CONTRACTS.

WE HAD 2314 CONTRACTS SERVED ON THURSDAY, SO WE GAINED A MASSIVE 604 CONTRACTS OR 60,400 OZ. (1.878 TONNES) EXERCISED A QUEUE JUMP WHERE THEY WILL TAKE PHYSICAL GOLD ON THIS SIDE OF THE POND. THIS IS NO DOUBT CENTRAL BANKS STANDING FOR PHYSICAL GOLD.

JULY GAINED 10 CONTRACTS UP TO 2988 CONTRACTS.

AUGUST GAINED 1412 CONTRACTS UP TO AN OI OF 263,912

.

We had 269 contracts filed for today representing 26,900oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 9 notices issued from their client or customer account. The total of all issuance by all participants equate to 269 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 8 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JUNE. /2026. contract month, we take the total number of notices filed so far for the month (27,928) to which we add the difference between the open interest for the front month of JUNE(1486 CONTRACTS) minus the number of notices served upon today 269 x 100 oz per contract) equals 2,914,500 OZ OR (90.653Tonnes of gold)

THUS: INITIAL total number of gold ounces standing for JUNE. /2026. contract month, we take the total number of notices filed so far for the month (27,928) to which we add the difference between the open interest for the front month of JUNE( 1486 CONTRACTS) minus the number of notices served upon today 269 x 100 oz per contract) equals 2,914,500 OZ OR (90.653Tonnes of gold)

new total of gold standing in JUNE becomes 90.613 TONNES//

TOTAL COMEX GOLD STANDING FOR JUNE 90.613 TONNES TONNES WHICH IS NOW REALLY HUGE FOR THIS ACTIVE DELIVERY MONTH OF JUNE.

confirmed volume THURSDAY confirmed 119,545// extremely poor// many have left the arena

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,879,868.269 oz 58.47 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,879,868.269 tonnes oz 58.47 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 28,228,811.372oz

TOTAL REGISTERED GOLD 15,260,734.647 tonnes (474.672 tonnes)

TOTAL OF ALL ELIGIBLE GOLD 12,968,076.725 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,380,866 oz ((REG GOLD- PLEDGED GOLD)=

416.201 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

JUNE DELIVERY MONTH

JUNE 5

JUNE DELIVERY MONTH

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | one entry i) Delaware: 25,813.470 OZ oz total withdrawal: 25,813.470 oz |

| Deposits to the Dealer Inventory | 0 entries |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT DEPOSIT ENTRIES/CUSTOMER ACCOUNT 0 entries |

| No of oz served today (contracts) | 90 CONTRACT(S) (450,000 OZ) |

| No of oz to be served (notices) | 243 Contract (1.215 MILLIONoz) |

| Total monthly oz silver served (contracts) | 2084 contracts 10.426 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 entries

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

ENTRY:0

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

1 entry

adjustments dealer to customer Delaware’

one entry

i) Delaware: 25,813.470 OZ oz

total withdrawal: 25,813.470 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 84.808 MILLION OZ//.TOTAL REG + ELIGIBLE. 319.191 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE /2026 OI: 333 OPEN INTEREST CONTRACTS FOR A GAIN OF 19 CONTRACTS.

WE HAD 77 NOTICES SERVED ON THURSDAY SO WE GAINED A HUGE 96 CONTRACTS OR AN ADDITIONAL 480,000 OZ WILL STAND AS A QUEUE JUMP AT THE SILVER COMEX.

JULY SAW A LOSS OF 1041 CONTRACTS DOWN TO 68,286 CONTRACTS.

AUGUST SAW A GAIN OF 47 CONTRACTS UP TO 831…

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 90 or 450,000 oz

CONFIRMED volume THURSDAY; 40,409// poor volume

XXX

AND NOW JUNE. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 2084 X5,000 oz = 10.426 MILLION oz

to which we add the difference between the open interest for the front month of JUNE( 333) AND the number of notices served upon today (90 )x (5000 oz)

Thus the standings for silver for the JUNE 2026 contract month: (2084 )Notices served so far) x 5000 oz + OI for the front month of JUNE (333) minus number of notices served upon today (90)x 5000 oz equals silver standing for the JUNE..contract month equating to 11.635 MILLION OZ.+

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 84.808 million oz of registered silver

JPMorgan as a percentage of total silver: 140.287/319.191 million: 43.93

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42.

The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

JUNE 5 /2026/WITH GOLD DOWN $134;85 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1026.857 TONNES

JUNE 4 /2026/WITH GOLD UP $39.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.143 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1026.857 TONNES

JUNE 3 /2026/WITH GOLD DOWN $51.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.856 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1028.000 TONNES

JUNE 2 /2026/WITH GOLD UP $7.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.712 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1028.856 TONNES

JUNE 1 /2026/WITH GOLD DOWN $79.30 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1032.568 TONNES

MAY 29 /2026/WITH GOLD UP $59.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD ./ //:/INVENTORY RESTS AT 1032.568 TONNES

MAY 28 /2026/WITH GOLD UP $52.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 27 /2026/WITH GOLD DOWN $51.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 26 /2026/WITH GOLD DOWN $25.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.9988 TONNES OUT OF THE GLD ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 22 /2026/WITH GOLD DOWN $13.45 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

MAY 21 /2026/WITH GOLD UP $7.60 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

GLD INVENTORY: 1026.857 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

JUNE 5 WITH SILVER DOWN $4.86: NO CHANGES IN SILVER INVENTORY AT THE SLV /./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 4 WITH SILVER UP $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.432 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 3 WITH SILVER DOWN $2.55: NO CHANGES IN SILVER INVENTORY AT THE SLV >> /./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 2 WITH SILVER UP $0.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.2222 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 484.855 MILLION OZ

JUNE 1 WITH SILVER DOWN $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLVA WITHDRAWAL OF 1.9 MILLION OZ FORM THE SLV/./ // :INVENTORY RESTS AT 486.077 MILLION OZ

MAY 29 WITH SILVER DOWN $0.03: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 28 WITH SILVER UP $1.02: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 27 WITH SILVER DOWN $1.61: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.176 MILLION OZ OUT OF THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 26 WITH SILVER DOWN $0.14: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.131 OF 0.315 MILLION OZ INTO THE SLV/ // :INVENTORY RESTS AT 489.153 MILLION OZ

MAY 22 WITH SILVER DOWN $0.26: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.315 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 488.022 MILLION OZ

MAY 21 WITH SILVER UP $0.64: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

CLOSING INVENTORY 483.423 MILLION OZ OF SILVER

GOLD COMMENTARIES:

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD..

Summer doldrums

Over the last six months, gold and silver are barely changed. Investors are losing patience. It’s time to stand back and examine the big picture and ignore short-term sentiment.

| Alasdair MacleodJun 5 |

As our introductory chart shows, gold and silver are barely changed on the year. As a measure of investor sentiment, North American investors sold down 12 tonnes in gold ETFs in the last two weeks of May, according to The World Gold Council. Doubtless, this week they sold some more.

MacleodFinance Substack is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

This is one proxy for market sentiment. This indifference is also reflected in open interest on Comex, which has collapsed to the lowest levels for decades, even lower than at the end of the 2011—2016 bear market when sentiment was extremely negative, and from which the current bull market commenced:

Mood swings in markets always lead investors to buying tops and selling bottoms. Market makers know this and exploit investor sentiment ruthlessly. The time to kick an investor hard is when he is down. This is why very few people trade successfully and consistently.

In horse racing, the bookies make lots of money at the expense of the punters. It’s just the same in financial markets. This is why at MacleodFinance we discourage trading gold, insisting on stacking in the knowledge that the risk is in currencies and credit and not gold. Gold is legal money without counterparty risk, and has been remarkably stable in its purchasing power over long periods, as the next chart of the oil price in gold and US dollars demonstrates:

Currently, oil priced in gold is trading at a 40% discount to its stable post-war 1950—1972 Bretton Woods level, whereas in fiat dollars it has risen 25 times with great volatility along the way. This story is repeated for all commodities, reflecting the dollar’s loss of purchasing power, which is now accelerating, made increasingly obvious by the Iran war.

Would you rather have gold, which in times of currency stress is stable, or the fiat dollar with its inherent weaknesses? This is what the dollar is doing relative to gold:

If you had $1,000 in cash in the late-1960s, it would have lost $994 of its purchasing power by now. Furthermore, the rate of this loss is demonstrably accelerating.

The current gold/dollar exchange rate is irrelevant when fundamental factors are leading to a renewed loss of purchasing power for the dollar, misleadingly reported as price inflation. The Gulf war is bringing on the crisis, leading with certainly to an economic slump and rising prices. This is certain to reduce all G7 government revenues while at the same time increasing their spending commitments. From a debt-to-GDP starting point averaging about 120% on average, not only are bond yields set to rise significantly, but G7 government debt will simply become unfundable. Our next chart shows that the US long bond yield is on the verge of breaking higher, with disastrous consequences for financial assets and the dollar itself:

You would think that common sense will intervene and prevent this outcome. But that ignores a simple fact: economic outcomes are driven by politics, not sound economics and certainly not common sense.

Take Japan. Its prime minister thinks she can defend the yen by increasing spending in an attempt to strengthen the economy. In other words, she is having a Liz Truss moment but with a debt to GDP of 250%. And Japan depends almost entirely on imported oil and gas as well as fertilisers etc.

Doubtless, the Bank of Japan is furiously defending the currency against this madness, which is challenging all-time lows, while bond yields are soaring:

Last time this happened, which followed the oil crisis of October 1973, Japan’s CPI inflation rate soared to 25% by spring 1974, while the wholesale price index rose nearly 35%. The situation for Japan today certainly rhymes with 1973—1974. And being the largest source of foreign investment capital for the US and the rest of the world, the inevitable crisis Japan faces will affect us all, particularly the US government because Japan is the largest foreign holder of US treasuries.

In conclusion, current investor sentiment obscures the brutal facts facing the fiat currency world. Anyone who gets upset about losing money day-to-day by holding gold is suffering from extreme myopia and is prey to the real professionals such as central banks and market-makers who play on investor sentiment to get you to sell your gold to them.

Hold Fast!

3. CHRIS POWELL AND HIS GATA DISPATCHES

4.ANDREW MAGUIRE LIVE FROM THE VAULT 275 and 274

5. COMMODITY REPORT//GOLD

Russia’s Missing Gold Tonnes Suddenly Appear

by VBL

Friday, Jun 05, 2026 – 7:44

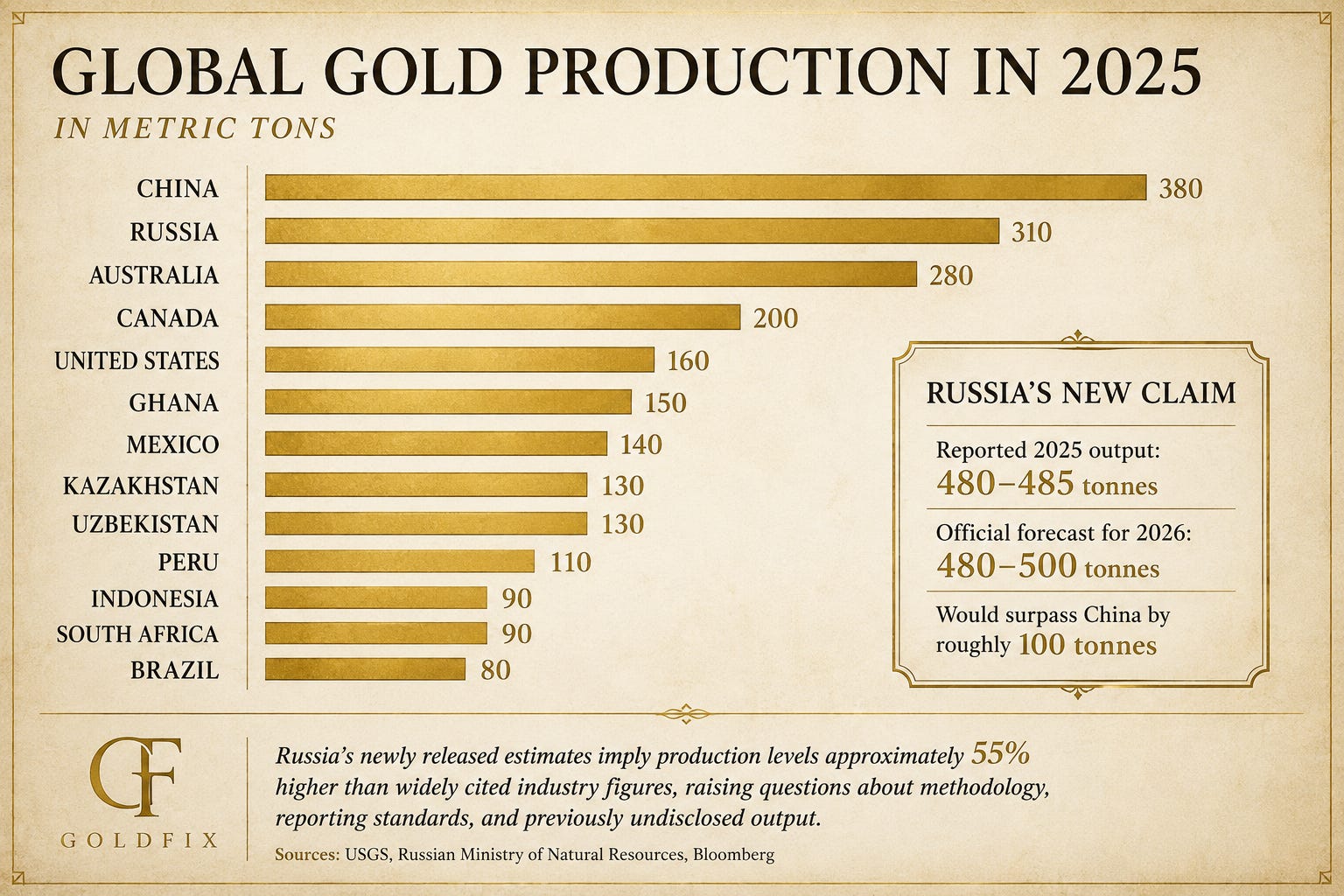

GFN – MOSCOW: Russia may have mined as much as 485 metric tons of gold in 2025 and could produce up to 500 tons in 2026, according to estimates released by the country’s Natural Resources Ministry, a figure that has surprised analysts and, if confirmed, would place Russia ahead of China as the world’s largest gold producer.

The estimates were disclosed by Natural Resources Minister Alexander Kozlov ahead of the St. Petersburg International Economic Forum. Russia has largely stopped publishing detailed gold production statistics since Western sanctions and bullion market restrictions were imposed following the Ukraine conflict.

According to Kozlov, preliminary calculations suggest Russian gold output reached between 480 and 485 tonnes in 2025, with production expected to range between 480 and 500 tonnes this year. The ministry confirmed the figures refer specifically to mined gold rather than broader production measures.

The numbers have drawn skepticism from mining analysts because publicly available estimates have been significantly lower. The World Gold Council previously estimated Russia mined roughly 330 tonnes in 2024, while independent industry consultants placed output closer to 345 tonnes. A jump toward 500 tonnes would imply an increase of roughly 40% to 50% in only a few years.

Analysts note that few major new mines have entered production recently, making the scale of the reported increase difficult to reconcile with existing industry data. However, the figures highlight the growing strategic importance of gold to Russia as sanctions continue to reshape global commodity markets.

“Gold production will amount to 480-485 tons.”

“The forecast for this year is 480-500 tons of gold.”

If the estimates are accurate, Russia would surpass both its previous production records and China’s reported output of approximately 381 tonnes, reinforcing its position as a dominant force in the global gold market.

Contributor posts published on Zero Hedge do not necessarily represent the views and opinions of Zero Hedge, and are not selected, edited or screened by Zero Hedge editors.

END

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

SHANGHAI CLOSED DOWN 30.04 PTS OR 0.74%

HANG SENG CLOSED DOWN 291.45 PTS OR 1.15%

Nikkei CLOSED DOWN 852.69 PTS OR 1.26%

//Australia’s all ordinaries CLOSED DOWN 0.91%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.7674

/ OFFSHORE CLOSED UP AT 6.7670 Oil DOWN TO 92.33 dollars per barrel for WTI and BRENT DOWN TO 94.65 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN// WITH YUAN TRADING UP (6.7674) OFFSHORE YUAN TRADING UP TO 6.7670 ONSHORE YUAN TRADING BELOW LEVEL OF OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP 6.7677

OFFSHORE YUAN: UP TO 6.7670

1.HANG SANG CLOSED DOWN 291.44 PTS OR 1.15%

2. Nikkei closed DOWN 852.69 PTS OR 1.26%

WEST TEXAS INTERMEDIATE OIL DOWN TO 92.33

BRENT; 94.65

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 99.19/// EURO RISES TO 1.1639 UP 27 BASIS PTS

3b Japan 10 YR bond yield:RISES TO. +2.658 DOWN 1 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 159.92… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.894 UP 1 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP( 6.7677 AND OFFSHORE: DOWN AT 6.7670

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and BRENT DOWN this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +3.0231// Italian 10 Yr bond yield DOWN to 3.771// SPAIN 10 YR BOND YIELD DOWN TO 3.448%

3i Greek 10 year bond yield DOWN TO 3.691%

3j Gold at $4464.60 //Silver at: 72.70 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 35/ 100 roubles/73.84

3m oil (WTI) into the 92 dollar handle for WTI and 94 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 159.87 // 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.658% DOWN 1 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.894 UP 1 PTS..: USA/SF this 0.7878 as the Swiss Franc . Euro vs SF: 0.9176

USA 10 YR BOND YIELD: 4.463 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.974 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.037 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 46.09 UP 12 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD AND USA DOLLAR RESERVES.

10 YR UK BOND YIELD: 4.8910 DOWN 3 PTS

30 YR UK BOND YIELD: 5.581 DOWN 3 BASIS PTS

10 YR CANADA BOND YIELD: 3.437 UP 1 BASIS PTS

5 YR CANADA BOND YIELD: 3.093 UP 1 BASIS PTS.

Futures Drop On Souring Chipmaker Sentiment, Kospi Plunge

Friday, Jun 05, 2026 – 08:27 AM

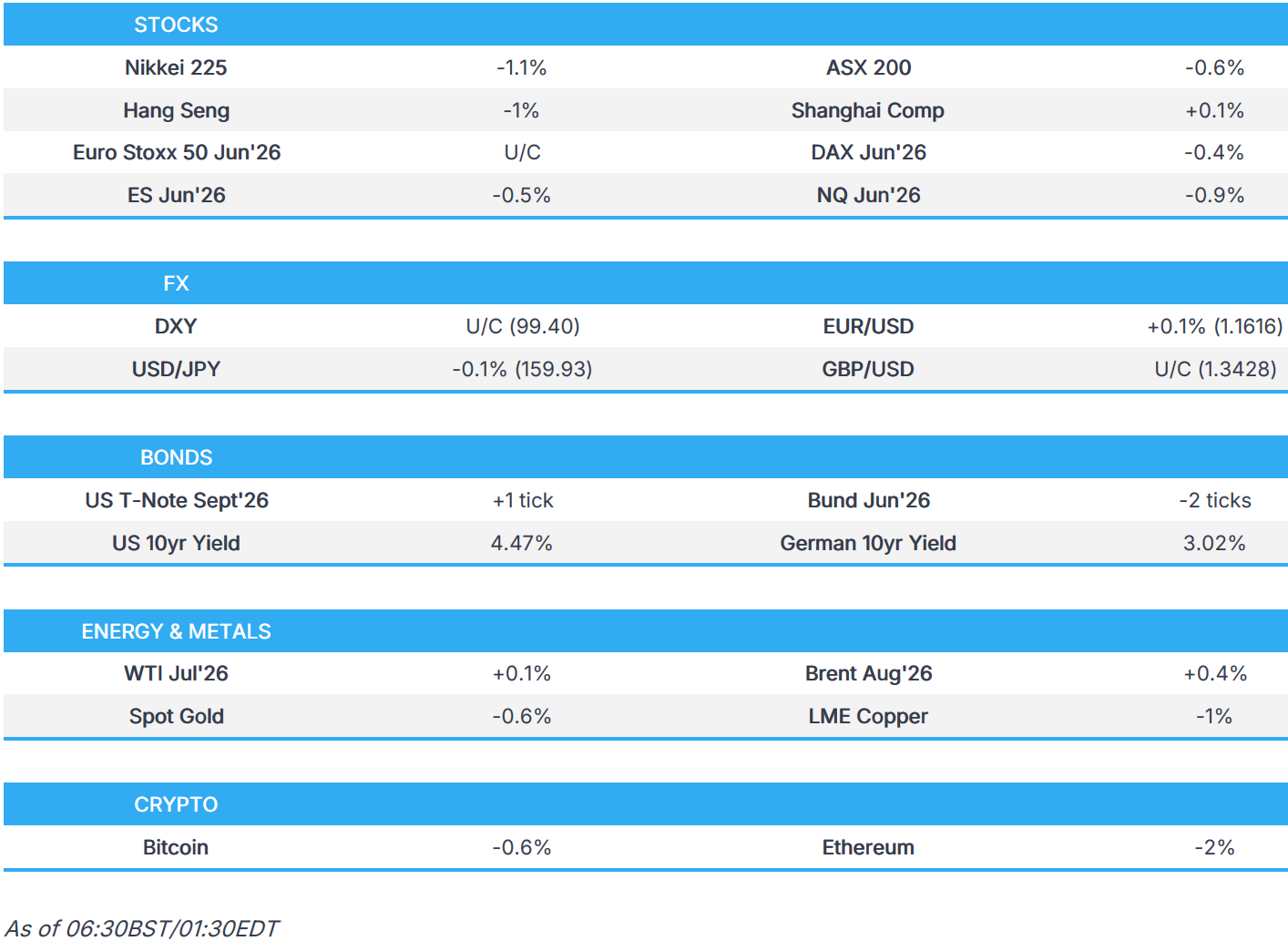

Futures are lower amid fresh underperformance of tech. If the premarket weakness persists, the S&P 500 is set to break a historic weekly run of gains as the AI trade takes another leg lower this time driven by the cartoonish Kospi index, with investors also expecting payrolls data to affirm that interest rates will stay higher for longer (full payrolls preview here). As of 8:00am ET, S&P futures are down 0.5% while Nasdaq futures slide 1% as chipmakers fall and big tech stocks are lower too, following on from a slump in South Korea’s Kospi. All Mag 7 names are all lower in premarket trading except for MSFT (+0.4%); NVDA fell -1.3%, a continuation of yesterday’s underperformance post AVGO earnings. On news flow, headlines were mostly muted this morning; after yesterday’s non-tech led rebound, we saw more negative sentiment this morning with all three indices lower during the pre-market session. Bond yields are flat to lower, the 10Y yield trading unchanged at 4.47% lower; the USD is also lower. WTI crude fell -0.2% to $92.86; both base and precious metals are lower while the bitcoin mauling shows no signs of ending. Today, the key focus is NFP; see our full preview here.

In premarket trading, Mag 7 stocks are mostly lower (Nvidia -1.3%, Microsoft +0.4%, Tesla +0.1%, Apple -0.1%, Alphabet -0.4%, Amazon -0.2%, Meta -0.2%, Nvidia -1.3%)

- Argan (AGX) rises 11% after the power-plant construction company reported first-quarter revenue above what analysts expected.

- Chipotle (CMG) is up about 2% after JPMorgan upgraded to overweight, citing a “rare valuation opportunity” for the stock.

- Cooper Cos (COO) gains 6% after the lens maker posted second quarter sales and profit that topped estimates.

- Docusign Inc. (DOCU) is down 4% after the company provided an in-line forecast for second quarter revenue. Analysts notes that its still a wait-and-see story as the company ramps Intelligent Agreement Management, its AI-powered platform for contracts.

- G-III Apparel Group (GIII) rises 8% after the clothing company boosted its adjusted earnings per share guidance for the full year.

- Guidewire (GWRE) is down 12% after the midpoint of the software company’s subscription and support revenue forecast for the fourth quarter fell short of the average analyst estimate.

- Lululemon Athletica Inc. (LULU) slides 10% after the company lowered its annual forecast due to deteriorating performance in North America.

- Merlin Inc. (MRLN) soars 29% after the defense technology company announced the successful completion of the critical design review for its C-130J autonomy program with the US Special Operations Command.

- Samsara (IOT) slips 2% after the GPS fleet tracking company posted first-quarter results.

- ServiceTitan (TTAN) jumps 15% after the software solutions firm reported revenue for the first quarter that beat the average analyst estimate.

Stocks are pulling back for a second day after Broadcom’s outlook for chip sales fell short of high expectations, raising questions over whether the rally in the AI trade had run too hard. The lack of progress toward a deal in the Middle East has also stoked worries that oil prices will remain elevated for some time.

“Following a period of upward revisions to earnings expectations across the sector, investors are taking a more selective approach to new information and guidance updates,” said Tomás García-Purriños, senior asset allocation strategist at Santander Asset Management. “We would view the recent weakness primarily as profit-taking and consolidation after a strong run.”

The chase for tech stocks took a further knock after S&P Dow Jones Indices said it would keep its eligibility criteria for benchmarks such as the S&P 500, rejecting proposals that would’ve allowed mega-caps to gain entry more quickly after going public. The decision means companies such as SpaceX, Anthropic PBC and OpenAI would have to wait at least a year for inclusion in the US benchmark after their debut. Fast inclusion in the S&P 500 would’ve led to about $14 billion in forced passive buying for SpaceX.

Friday’s jobs data will likely show a solid increase in payroll numbers, up 88K (if down from 115K in April), suggesting the strong March and April reports reflected underlying momentum rather than just a rebound from earlier weakness, according to Bloomberg Economics. Our preview can be found here. The report may not offer strong direction for stock markets, as a focus on signs of price pressures is keeping investors to expect a rate hike as soon as December. Goldman noted that the implied move of 47 basis points is much lower than the average realized move over the past year, and the lowest since Dec 24.

“Employment figures should not move the needle unless there is a major surprise,” said Roberto Scholtes, head of strategy at Singular Bank. “Instead, the key variables to watch are 10- and 30-year Treasury yields, which are hovering around the 4.5% and 5% ‘pain threshold’ levels.”

Europe’s Stoxx 600 is brushing broader losses off and edging higher, as losses for tech stocks and miners are offset by gains for consumer names.Here are the biggest movers Friday:

- Raspberry Pi shares rise as much as 14%, extending their run and hitting a new all-time high after the British maker of small, low-cost computers said earnings this year will be well ahead of expectations, pointing to robust demand

- Evoke shares rise as much as 17% yet trade about 10% below the value of a recommended all-stock offer from Bally’s Intralot. Berenberg analysts expect the deal to get done on the current terms

- CMC Markets shares rise as much as 7.3%, extending strong gains since the online trading platform guided to a stronger-than-expected FY27 performance on Thursday, as Jefferies upgrades to buy from hold

- Infineon shares slide 5.7% after being downgraded by analysts at MP Capital Markets because the recent strength in the semiconductor stock leaves “limited upside” on the table

- Bodycote shares fall as much as 11%, most since March 2025, after Apollo Management Holdings said it does not intend to make a firm offer, ending discussions that began with a conditional proposal announced on May 22

- Wacker Chemie falls as much as 6%, the most since April 29, after Citi cut its recommendation to sell, saying momentum in upstream chemicals may be moderating, leading to a less compelling risk/reward for Wacker Chemie and Clariant

Asian equities slid for a second day, dragged down by losses in technology hardware shares as enthusiasm for the artificial intelligence trade cools. The MSCI Asia Pacific Index fell as much as 2.3% before paring some of its declines. Heavyweight chipmakers Samsung and SK Hynix were the biggest drags. South Korea’s Kospi led losses around the region, tumbling over 5%. For the week, the regional measure was down about 1.3%. Stocks in Indonesia extended this week’s slump, heading for the lowest close since November 2020. Global tech stocks fell after a weaker-than-expected outlook from US chipmaker Broadcom, indicating investors are nervous about sustainability of the AI rally. Meanwhile a lack of progress in talks between the US and Iran threatened to keep oil prices elevated, raising inflation concerns.

In FX, The Bloomberg Dollar Spot Index is down 0.2%, while the euro is holding its gain despite a downward revision to first-quarter GDP growth, entirely due to a contraction in Ireland. EUR/USD rose 0.2% to 1.1637. USD/JPY inched 0.1% lower to 159.86: Japan Finance Minister Satsuki Katayama reiterated that the government stands ready to respond appropriately to currency moves at any time. USD/CAD fell 0.2% to 1.3880:Friday’s data will include change in nonfarm payrolls, unemployment rate for the US and unemployment rate, net change in employment for Canada as well

In rates, treasuries are mixed ahead of the May jobs report at 8:30am New York time, with oil prices little changed as traders await signs of progress in US-Iran peace talks.US yields remain within a basis point of Thursday’s closing levels with the 10-year near 4.47%. Gilts in the sector outperform slightly while bunds lag by around 1bp. US curve spreads are marginally steeper on the day. WTI crude oil futures down 0.2% underpin Treasuries, while Nasdaq 100 futures are off nearly 1% as tech stocks falter.

Ahead of May jobs report, Fed-dated OIS contracts price in around 17bp of tightening by year-end and fully price in a 25bp hike by the March FOMC meeting. Into the data, Thursday’s activity in Treasury options was active and mixed in direction, while SOFR options flows largely consisted of position liquidation and adjustment, as traders looked reduce risk.

In commodities, Brent edged lower to around $94.80 a barrel.

Cryptocurrencies are under sustained selling pressure, heading for a sixth straight day of losses. Sentiment is hurt by Middle East tensions, expectations of higher U.S. rates, ETF outflows, and Strategy’s reported bitcoin sales for the first time since 2022. Bitcoin falls 2% to $62,292, Ether drops 5.8% to $1,669, and Solana declines 4.1% to $66.20, all near multi-month or multi-year lows.

Today’s US economic data calendar includes May jobs report (8:30am) and April consumer credit (3pm). Fed speaker slate empty for the session. External communications blackout commences Saturday ahead of the June 17 policy announcement

Market Snapshot

Top Overnight News

- US and Iran Show Little Progress in Talks After Week of Clashes: BBG

- Iran has informed Pakistan of its acceptance of transferring part of its uranium to a third country that agrees to it. However, Al Arabiya followed up by stating that the US still refuses Iran’s request to release its frozen funds.

- Senate passes $70 billion ICE funding; fails to ban Trump’s ‘anti-weaponization’ fund: RTRS

- Senate blocks debate on FISA surveillance law days before program ‘goes dark: RTRS

- Anthropic Calls for AI Pause Button to Let Humans Take Stock: BBG

- Apple’s Plan for AI Dominance Rests on Fixing Its Much‑Maligned Chatbot: WSJ

- Point72 Weighs Paying Other Hedge Funds to See Their Trade Ideas: BBG

- Morgan Stanley Sees SpaceX’s Revenue Reaching $3.4 Trillion in 2040: WSJ

- Trump’s trade adviser Navarro said the Fed shouldn’t raise rates into supply shock inflation.

- US officials held preliminary discussions with major AI companies about the potential for the government to acquire some shares in their firms, according to people familiar with the matter cited by NOTUS.

- Banks Curb China Trips, Delay Events After Cross-Border Scrutiny: BBG

- The Anything-Goes Era in Private‑Credit Lending Is Coming to an End: WSJ

- Americans on GLP-1s Are Overwhelming Retailers With Their Nonstop Returns: WSJ

- A weekly flow data shows USD 39bln into bonds (a record inflow), USD 122bln into cash, USD 23.1bln into stocks, USD 2bln out of crypto (biggest since November 2025), USD 3.1bln out of gold (biggest in 10 weeks).

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly lower with the region subdued by recent tech-related pressure, and despite the predominantly positive handover from Wall St, where healthcare helped boost the Dow to a record high. ASX 200 declined as the losses in the mining, materials and resources sectors overshadowed the outperformance in health care. Nikkei 225 retreated amid tech selling but with the index off today’s worst levels after bouncing off a floor beneath the 66,000 level, while data was mostly encouraging as Household Spending and Labour Cash Earnings topped forecasts, which effectively supports the argument for a BoJ rate hike this month. Hang Seng and Shanghai Comp were mixed with Hong Kong pressured after the recent efforts to tighten cross-border capital outflows, including banks suspending opening Hong Kong bank accounts for mainland clients that could be used for overseas investments, while the mainland is marginally positive after the PBoC resumed open market operations.

Top Asian News

- Japanese PM Takaichi said there are pros and cons to a weak yen, while she added that investment strategy will help maintain trust in the yen and that her economic policy is aimed at boosting Japan’s economic capability, not at FX manipulation.

- Japanese Finance Minister Katayama said the direction on sales tax cut hasn’t been decided, adds government will not rely on debt to finance the food sales tax cut.

European bourses (STOXX 600 +0.2) start the last trading session of the week mixed, with the breadth of performance narrow. Global tech continues to sell off, after Broadcom’s AI chip revenue fell short of expectations, weighing on indices that are heavily weighted with tech names (AEX -0.1%, EuroStoxx 50 -0.1%). Sectors point to a neutral bias. Retail (+1.5%) and Media (+1.5%) outperform, while Technology (-1.6%) and Basic Resources (-1.8%) are the clear laggards.

Top European News

- UK MP/PM candidate Burnham has spoken on options for increasing infrastructure spending without breaching the fiscal rules, FT reported citing sources.

- Andy Burnham says he would run in a Labour leadership contest and, if prime minister, urgently tackle social care, taxation and devolution while avoiding a snap election or immediate Brexit rerun, according to the Guardian.

- UK PM spokesperson said Starmer will not walk away from PM job, in response to Andy Burnham’s bid for the leadership, while Burnham confirmed he’ll stand to replace PM Starmer as Labour leader, as he stated that Wes Streeting seems to have launched a leadership contest, which he would seek to join.

- Norway’s Stryke labour union said companies have agreed wage deal for oil workers and that they will not go and strike.

FX

- G10s are all firmer against the Buck, where DXY -0.2% as it respects recent ranges into the US Jobs report. Franc leads, EUR +0.2% and GBP +0.2% also performing well.

- In a quiet morning session, the Buck has trundled lower from a 99.40 peak to a trough just above 99.20. Today sees the release of May US Jobs data, expected to tick lower to 85k from 115k in April. Recent labour market proxies align with expectations of a cooling in the labour market, as initial jobless claims rose to 225k from 212k, above the top end of the forecast range, while Challenger layoffs rose to 97.006k from 83.387k. Aside from macro data, focus remains on geopolitics, where headlines overnight suggested Washington demanded Tehran deliver its response before the end of the week or be hit with strikes. MUFG notes EUR/USD is vulnerable to a stronger employment print citing the OIS curve in Europe, which they believe is now well priced or even overpriced for what the ECB will deliver. Markets currently assign 14bps of tightening by year-end for the Fed.

- EUR performs well on the back of the weaker Buck. The likely catalysts today for the single currency will be the US Jobs report, which is expected to cool on a monthly basis. ING, which has an above consensus expectation (100k vs consensus 85k), contends the US print will support the Buck, and potentially enough to price a 25bp hike from the Fed by year-end, widening rate differentials. EUR/USD +0.2% firmed throughout the morning after rising from the 1.16 mark.

- CHF continues to mark gains against the Euro and Buck in wake of May inflation data. EUR/CHF U/C, USD/CHF -0.2%. Antipodeans firmer, but to a lesser extent than cyclicals as metals are lower across the board and amid the general equity risk tone.

Central Banks

- RBI keeps Repurchase Rate unchanged at 5.25%, as expected, via unanimous decision, while policy stance kept at neutral. RBI Governor Malhotra said the central bank would take steps, if needed, to rein in speculative activity in the FX market.

Fixed Income

- Global fixed benchmarks are slightly firmer this morning alongside some mild pressure in the energy complex. Markets remain on tenterhooks, awaiting the key NFP report and mixed geopolitical updates: 1) Trump said talks with Iran are going well, 2) reports suggest Washington has demanded Iran deliver a response before the end of the week, 3) Hezbollah rejected the US-backed ceasefire between Lebanon and Israel. (Please see the commodities section for details.)

- USTs (+9 ticks) are firmer and trade within a narrow 19-18 to 109-23 range. Tentative action as markets await the US NFP report later today; in brief, the US economy is expected to add 85k nonfarm payrolls in May, vs 115k added in April. The unemployment rate is seen unchanged at 4.3%. Traders will be watching closely for signs of labour market deterioration, given that FOMC officials view employment risks as tilted to the downside, though Fed officials are seemingly more concerned about the inflation side of its mandate, amid the labour market stability.

- US yields are lower across the curve, with some mild underperformance in the belly. The 10yr (4.46%) resides just shy of the key 4.50% mark; a dovish NFP report could see the yield test near-term support at 4.45%, and then a cluster of highs at around the 4.42%. Of course, a hawkish report would see a potential test of 4.50%, and a breach above that mark will bring in near-term highs at 4.53%.

- Bunds (U/C) and Gilts (+17 ticks) also trade incrementally firmer. There has been a lack of pertinent newsflow for either region; UK Halifax House Price Index showed that prices edged a little lower in May due to the Middle East war. Elsewhere, the BoE DMP report was released, which saw 1yr ahead inflation expectations rise, whilst the 3yr was left unchanged. Focus will shift to BoE speak via Dhingra and Bailey this afternoon. Bunds currently hold within a 125.54 to 125.69 range; Gilts hold within a 87.77 to 88.05 range.

Commodities

- In US-Iran news, the biggest setback this week regarding US and Iran talks (in spite of the flare-ups) came in Lebanon, where Hezbollah publicly rejected the latest US-backed Israel-Lebanon ceasefire framework, saying it required Hezbollah concessions without an Israeli withdrawal, and vowed to continue resistance while Israeli forces remain in Lebanese territory. An Israel-Hezbollah ceasefire remains a key Iranian demand for broader peace talks. Washington reportedly demanded Tehran respond by the end of the week and warned of either an agreement or military action. More recently, Al Hadath reported that Iran has informed Pakistan of its acceptance of transferring part of its uranium to a third country that agrees to it, which resulted in fleeting downside in energy benchmarks.

- Crude futures are off their worst levels with little in terms of notable geopolitical headlines this morning. Following Hezbollah’s rejection yesterday, Israeli army issued evacuation warnings for 9 villages in southern Lebanon. Note, this morning, there were reports of a marine drone exploding in Romania, although the Romanian defence ministry later clarified that this was a Romanian army drone. WTI Jul resides in a USD 91.50-USD 93.54/bbl range while Brent Aug sits in a USD 93.64-95.90/bbl range. Dutch TTF trades higher by around 1%, just north of the EUR 49/MWh level.

- Spot gold has rebounded after finding support at its 200 DMA for a second day in a row (200 DMA at USD 4428/oz today). The yellow metal still trades with modest intraday losses and within a USD 4429-4482/oz range, within yesterday’s 4424-4515/oz parameter. Traders look ahead to the US NFP later today for impetus (full preview available on Newsquawk).

- Base metals are lower across the board but to varying degrees after trickling lower in APAC alongside the mostly downbeat overnight risk sentiment. 3M LME copper resides in a USD 13,711.70-13,893.30/t range at the time of writing.

- Petroleum Development Oman said operations at the Mina Al Fahal port are proceeding normally after oil loadings were suspended following an explosion due to an alleged drone attack.

Trade/Tariffs

- US President Trump said automakers sought no tariff changes in their meeting and that talks focused mostly on car repair.

- China International Trade Council says it opposes proposed US tariffs and criticised the plan for 12.5% tariffs on Chinese goods.

Geopolitics: Middle East

- Iran has informed Pakistan of its acceptance of transferring part of its uranium to a third country that agrees to it, Al-Hadath reported. However, Al Arabiya followed up by stating that the US still refuses Iran’s request to release its frozen funds.

- US President Trump said they do not need help from European countries regarding Hormuz and noted that Iran talks are going well, while he reiterated that almost all of Iran’s leadership has been wiped out and that Iran has no navy or air force. Trump said if Iran killed US troops, it would restart the war quickly, and the Israel-Lebanon conflict is interconnected with Iran. Trump also stated he thinks progress has been made on Lebanon, and he would be honoured to meet Iran’s Supreme Leader if a deal is made.

- Iranian Foreign Minister Araghchi said they have many documents and evidence that show Kuwaiti skies have been used regularly against Iran. Araghchi also commented that Iran and Oman will regulate the management of the Strait of Hormuz based on international law standards, while they will exchange views and ideas about the management of the Strait with the Persian Gulf countries, but ultimately the decision will be made between Iran and Oman.

- Iran’s Supreme Leader advisor Rezaei said US President Trump wants to pressure Iran to accept his conditions and keep Iran in a vague state, while he added that the current draft has ambiguities that have to be clarified. Rezaei also said that Iran will stand firmly with Hezbollah in Lebanon and that Iran will have no hesitation in defending its interests and security.

- Pakistan’s interior minister was reported to return to Tehran to push negotiations.

- Israeli army issued evacuation warnings for 9 villages in southern Lebanon, Sky News Arabia reported.

- Hezbollah claimed drone and missile attacks on Israeli bases, while it also stated that six Merkav tanks were destroyed in Lebanon, according to Fars.

- US House rejected a war powers resolution on Lebanon in a 92 vs 324 vote.

Geopolitics: Ukraine

- US House voted 226 to 195 to approve the Ukraine aid package and Russia sanctions bill after more than a dozen GOP lawmakers voted against party lines.

Geopolitics: Other

- US sanctioned Cuba’s President Miguel Diaz-Canel, while President Trump said sanctions are not meant to accelerate a collapse, and stated they will handle Cuba after they take care of Iran.

- Marine drone explosion has been reported in Romanian Black Sea Port of Constanta-Digi 24. Romania’s Defence Ministry later said that the Romanian Army maritime drone found at Constanța civilian port self-detonated, causing no casualties, and was not linked to recent Black Sea exercises.

US Event Calendar

- 8:30 am: May Change in Nonfarm Payrolls, est. 88k, prior 115k

- 8:30 am: May Change in Manufact. Payrolls, est. 2k, prior -2k

- 8:30 am: May Unemployment Rate, est. 4.3%, prior 4.3%

DB’s Jim Reid concludes the overnight wrap

As we hit another payrolls Friday in the US, Asian markets are seeing some decent sized tech losses in what seems to be a hangover from Wednesday night’s Broadcom results where forecasts weren’t as elevated as some of the more optimistic predictions hoped. The KOSPI is down -5.02% with the Nikkei -1.27% lower. The latter is also influenced by the increasing view that the Bank of Japan will have to raise rates over the coming year. The meeting on the 16th of this month now sees a 96% probability of a hike according to futures. In our World Outlook our economist forecast a hike a quarter over the next year. This is more hawkish than the consensus.

The Hang Seng (-0.84%) is also trading lower on tech losses with the ASX -0.63%. S&P 500 (-0.59%) and NASDAQ 100 (-1.07%) futures are also weak for this time of the day. Bucking the trend is the Shanghai Composite (+0.43%). European stock futures are only down just over a tenth of a percent given their low tech weighting.

Early morning data revealed that Japan’s real wages rose by +1.9% in April (compared to +1.7% anticipated) y/y, contributing to a smaller-than-expected decline in household spending. Average nominal wages, or total cash earnings, increased by +3.5% year-on-year (against +3.1% expected). This figure represents the fastest wage growth since December 2024, following a revised increase of +3.1% in March. The April data marks the first instance in over 34 years where wage growth has surpassed 3% for three consecutive months. In a separate report, Japan’s household spending decreased by -0.5% year-on-year in April, a less severe decline than the expected drop of -1.5%, following a -2.9% decrease in the previous month. This decline has extended the trend of falling consumer spending to five consecutive months.

Before these overnight moves, markets stabilised yesterday amidst growing hopes for some sort of US-Iran deal. So Brent crude oil prices (-2.84%) fell back to $95.03/bbl, reversing course after three consecutive gains, which in turn helped to ease fears about a stagflationary shock. As a result, markets followed the usual pattern of the last three months, where lower oil prices meant bond yields also fell back, with investors pricing in a more dovish path for central banks too. Meanwhile, equities recovered, including the S&P 500 (+0.41%), although it wasn’t all good news for risk assets yesterday, with Bitcoin (-2.06%) falling to its lowest level since early February, at $63,575.

In terms of the latest from the Middle East, there wasn’t much in the way of fresh news. However, oil prices saw a clear move lower after Trump issued a post criticising the vote in the House of Representatives against the Iran conflict. That was because Trump’s post said the vote was “right in the middle of my final negotiations to end the War”. So that suggested talks were still happening and a deal might be near. Oil prices did rebound a bit during the US session as Lebanon’s Hezbollah militia rejected the US-brokered ceasefire, but overall this didn’t derail the more optimistic mood following the ceasefire announcement by Israel and the Lebanese government the previous evening.

And investors also priced out the chance of a longer conflict, with the 6-month Brent future (-2.15%) also falling to $85.04/bbl. So that helped to ease concerns about inflation, with the 1yr US inflation swap (-9.2bps) falling to 3.09%, whilst the 1yr Euro inflation swap (-5.5bps) fell to 2.99%.