May 4, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

May 4, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1868.80 up $0.70

SILVER: $22.38 down $0.23

ACCESS MARKET: GOLD $1884.30

SILVER: $23.01

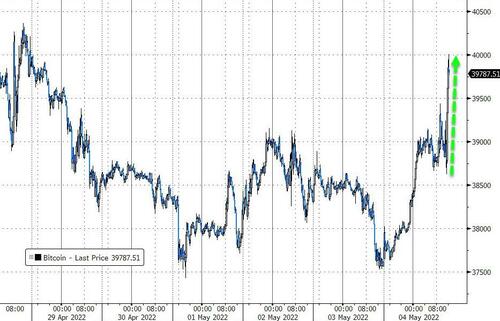

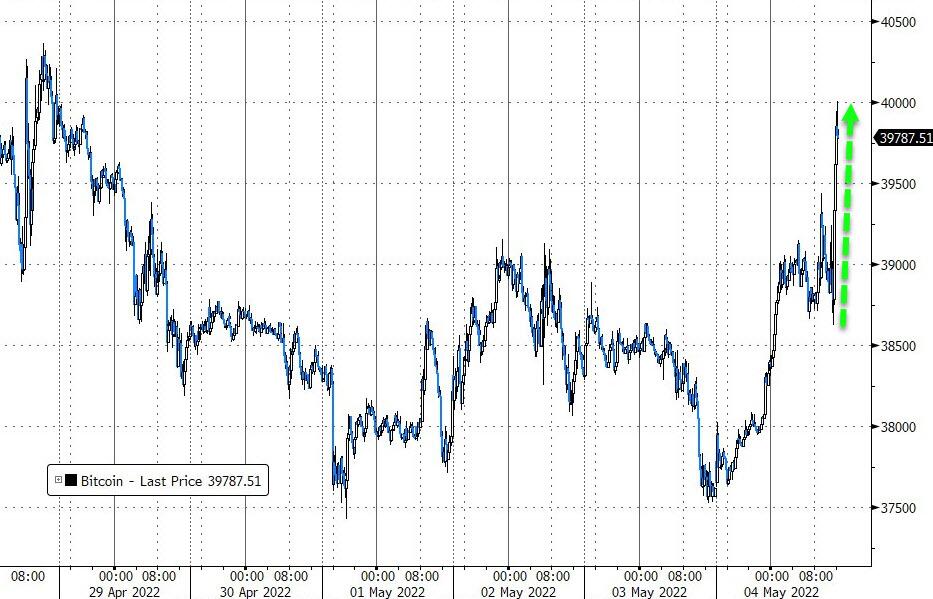

Bitcoin morning price: $39040 UP 707

Bitcoin: afternoon price: $39.848 UP 1515

Platinum price: closing UP $53.10 to $991.05

Palladium price; closing UP $36.40 at $2247.10

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices: 26/33

EXCHANGE: COMEX

CONTRACT: MAY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,868.800000000 USD

INTENT DATE: 05/03/2022 DELIVERY DATE: 05/05/2022

FIRM ORG FIRM NAME ISSUED STOPPED

657 C MORGAN STANLEY 3

657 H MORGAN STANLEY 5

661 C JP MORGAN 30 26

709 C BARCLAYS 2

TOTAL: 33 33

MONTH TO DATE: 1,483

TOTAL: 8 8

MONTH TO DATE: 1,450

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT 33 NOTICE(S) FOR 3300 OZ (0.1026 TONNES)

total notices so far: 1483 contracts for 148,300. oz (4.617 tonnes)

SILVER NOTICES:

69 NOTICE(S) FILED 345,000 OZ/

total number of notices filed so far this month 2828 : for 14,140,000 oz

END

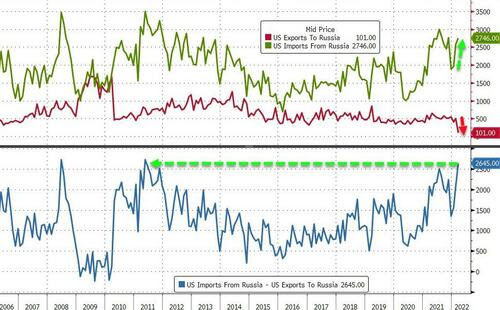

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD UP $0.70

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 TONNES FROM THE GLD.

INVENTORY RESTS AT 1089.04 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 27 CENTS

AT THE SLV// A SMALL CHANGE IN SILVER INVENTORY AT THE SLV://A DEPOSIT OF .851 MILLION OZ INTO THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 576.900 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 516 CONTRACTS TO 137,692 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GAIN IN OI WAS ACCOMPLISHED WITH OUR $0.04 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.04) AND WERE UNSUCCESSFUL IN KNOCKING OUT SOME SILVER LONGS AS WE HAD A STRONG GAIN OF 1086 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 30.170 MILLION OZ FOLLOWED BY TODAY’S 75,000 OZ EFP JUMP TO LONDON//NEW STANDING 28.430 MILLION OZ/ // V) FAIR SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : + 31

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTACTS for 3 days, total 4191, contracts: 20.955 million oz OR 6.966 MILLION OZ PER DAY. (1397CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 20.955 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 20.955 MILLION OZ//

RESULT: WE HAD A FAIR SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 516 WITH OUR $0.04 GAIN IN SILVER PRICING AT THE COMEX// TUESDAY., TODAY. THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE CONTRACTS: 570 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAY. OF 30.170 MILLION OZ FOLLOWED BY TODAY;S 75,000 OZ EFP TO LONDON//NEW STANDING 28.430 MILLION OZ// .. WE HAD A STRONG SIZED GAIN OF 1055 OI CONTRACTS ON THE TWO EXCHANGES FOR 5.275 MILLION OZ DESPITE THE SMALL GAIN IN PRICE.

WE HAD 69 NOTICES FILED TODAY FOR 345,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 275 CONTRACTS TO 560,441 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: –300 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE SMALL SIZED INCREASE IN COMEX OI CAME WITH OUR GAIN IN PRICE OF $6.05//COMEX GOLD TRADING/TUESDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 5.353 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY”S QUEUE JUMP OF 41,100 OZ//NEW STANDING 7,4650 TONNES

YET ALL OF..THIS HAPPENED DESPITE OUR GAIN IN PRICE OF $6,05 WITH RESPECT TO MONDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 2327 OI CONTRACTS (7.26 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2327 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 560,441.

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2327, WITH 275 CONTRACTS INCREASED AT THE COMEX AND 2062 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2637 CONTRACTS OR 8.202 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2062) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (275,): TOTAL GAIN IN THE TWO EXCHANGES 2327 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY. AT 5.353 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 41,100 OZ//NEW STANDING 7.4650 /// 3) ZERO LONG LIQUIDATION //.,4) SMALL SIZED COMEX OI. GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

8623 CONTRACTS OR 862300 OR 26.82 TONNES 3 TRADING DAY(S) AND THUS AVERAGING: 2974 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES: 26.82 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 26.82/3550 x 100% TONNES 0.760% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 26.82 TONNES INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A SMALL SIZED 516 CONTRACT OI TO 137,692 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 570 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 570 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 516 CONTRACTS AND ADD TO THE 570 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 1086 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE STRONG GAIN ON THE TWO EXCHANGES 5.430 MILLION OZ

OCCURRED DESPITE OUR TINY GAIN IN PRICE OF $0.04 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

.

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED //Hang Sang CLOSED DOWN 232.37 OR 1.10% /The Nikkei closed DOWN 29.37 OR .11% //Australia’s all ordinaires CLOSED DOWN 0.30% /Chinese yuan (ONSHORE) closed /Oil UP TO 103.36 dollars per barrel for WTI and UP TO 106.79 for Brent. Stocks in Europe OPENED ALL READ // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6064 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6587: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER/

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 275 CONTRACTS TO 560,441 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR GAIN OF $6.05 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2844 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF MAY.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2062 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :2062 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2062 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2327 CONTRACTS IN THAT 2062 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A TINY SIZED COMEX OI GAIN OF 275 CONTRACTS..AND THIS GAIN OCCURRED DESPITE OUR GAIN IN PRICE OF GOLD $6.05.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (7.4650),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 7.465 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $6.05) AND WERE UNSUCCESSFUL IN FLEECING QUITE ANY LONGS AS WE HAVE REGISTERED A STRONG SIZED GAIN OF 13.188 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAY (7.465 TONNES)…

WE HAD 300 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 2327 CONTRACTS OR 232,700 OZ OR 7.26TONNES

Estimated gold volume today: 71,634/// extremely poor

Confirmed volume yesterday:199,788 contracts poor

INITIAL STANDINGS FOR MAY ’22 COMEX GOLD //MAY 4

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 2,314.873 oz Int. Delaware Brinks 72 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 33 notice(s)3300 OZ 0.1026 TONNES |

| No of oz to be served (notices) | 917 contracts 91,700 oz 2.8522 TONNES |

| Total monthly oz gold served (contracts) so far this month | 1483 notices148,300 OZ 4.6127 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit nil oz//

No dealer withdrawals

0 customer deposits

2 customer withdrawals:

i) out of Brinks 289.360 oz 9 kilobar

ii) Int Delaware: 2025.513 oz 63 kilobars

total withdrawal: 2314.873 oz

ADJUSTMENTS: 1 dealer to customer

ii) Manfra: 9038.186 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 950 contracts having GAINED 403 contracts

We had 8 notices filed on Monday, so we gained 411 contracts or 41,100 oz will stand for delivery in this non active delivery month of May.

June saw a loss of 12,797 contracts down to 424,933 contracts

July has a gain of 117 OI to stand at 124

August has a gain of 11,647 contracts up to 83,401 contracts

We had 33 notice(s) filed today for 3300 oz FOR THE MAY 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 30 notices were issued from their client or customer account. The total of all issuance by all participants equate to 33 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 26 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2021. contract month,

we take the total number of notices filed so far for the month (1483) x 100 oz , to which we add the difference between the open interest for the front month of (MAY 950 CONTRACTS ) minus the number of notices served upon today 33 x 100 oz per contract equals 240,000 OZ OR 7.4650 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the MAY contract month:

No of notices filed so far (1483) x 100 oz+ (950) OI for the front month minus the number of notices served upon today (33} x 100 oz} which equals 240,000 oz standing OR 7.4650 TONNES in this NON active delivery month of MAY.

TOTAL COMEX GOLD STANDING: 7.4650 TONNES (A STRONG STANDING FOR A MAY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

263,958.054, oz JPM No 2 7.58 TONNES

1,063,208.634 oz pledged Brinks/27,96 TONNES

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

Loomis: 32,840.423 oz

total pledged gold: 1,941,626,135 oz (1115,92 TONNES)

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 35,969.513.602 OZ (1118.80 TONNES)

TOTAL ELIGIBLE GOLD: 18,238,460.914 OZ (567.29 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,731,052.688 OZ (548.39 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,789,426.0 OZ (REG GOLD- PLEDGED GOLD) 491.11tonnes

END

MAY 2022 CONTRACT MONTH//SILVER//MAY 4

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,905,908.760 oz Brinks CNT Delaware JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 579,586.700 oz JPMorgan |

| No of oz served today (contracts) | 69CONTRACT(S) 345,000 OZ) |

| No of oz to be served (notices) | 2858 contracts (14,290,000oz) |

| Total monthly oz silver served (contracts) | 2828 contracts 14,140,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposit into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

ii) Into JPMorgan: 579,586,700 oz

total deposit: 579,586.700 oz

JPMorgan has a total silver weight: 174.237 million oz/332.017 million =52.40% of comex

Comex withdrawals: 4

i) Out of Brinks 590,458.050 oz

ii) Out of CNT; 699,466.610 oz

iii) Out of Delaware 2927.000 oz

iv) Out of JPMorgan 613,057.100 oz

total withdrawal 1,905,908.760 oz

0 adjustments:

the silver comex is in stress!

TOTAL REGISTERED SILVER: 81.620 MILLION OZ

TOTAL REG + ELIG. 332.057 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY OI: 2927 HAVING LOST 1022 CONTRACTS. WE HAD 1007 NOTICES FILED ON TUESDAY

SO WE LOST 15 CONTRACTS THAT WE EFP’D TO LONDON (75,000 OZ) AS SILVER IS SCARCE OVER HERE.

JUNE HAD A LOSS OF 58 TO STAND AT 1794

JULY HAD A GAIN OF 1233 CONTRACTS UP TO 112,184 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 69 for 5,035,000 oz

Comex volumes: 19,204// est. volume today// extremely poor

Comex volume: confirmed yesterday: 46,540 contracts ( poor )

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 2828 x 5,000 oz = 14,140,000 oz

to which we add the difference between the open interest for the front month of MAY (2927) and the number of notices served upon today 69 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY./2021 contract month: 2828 (notices served so far) x 5000 oz + OI for front month of MAY (2927) – number of notices served upon today (69) x 5000 oz of silver standing for the MAY contract month equates 28,430,000 oz. .

We lost 15 contracts or 75,000 will not stand for delivery at the comex as these guys were EFP’d to London

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

APRIL 8/WITH GOLD UP $7.70: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES INTO THE GLD//INVENTORY RESTS AT 1088.75 TONNES

APRIL 7/WITH GOLD UP $13.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1087.30 TONNES

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

APRIL 4/WITH GOLD UP $.70//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1091.73 TONNES

APRIL 1///WITH GOLD DOWN $19.00 : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES INTO THE GLD///INVENTORY RESTS AT 1091.73 TONNES

MARCH 31/WITH GOLD UP $13.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD FROM MONDAY A WITHDRAWAL OF 1.71 TONNES FROM THE GLD:INVENTORY RESTS AT 1091.44

MARCH 28/WITH GOLD DOWN $14.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.18 TONNES

MARCH 25/WITH GOLD DOWN $7.60 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.52 TONNES INTO THE GLD///INVENTORY RESTS AT 1093.18 TONNES

MARCH 24/WITH GOLD UP $24.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1087.66 TONNES

MARCH 23/WITH GOLD UP $15.75//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1083.60 TONNES

MARCH 22/WITH GOLD DOWN $7.75: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES OF GOLD DEPOSITED INTO THE GLD//INVENTORY RESTS AT 1083.60 TONES

CLOSING INVENTORY FOR THE GLD//1089.04 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 8/WITH SILVER UP 11 CENTS :NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 7/WITH SILVER UP 27 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

APRIL 4/WITH SILVER DOWN 5 CENTS TO CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 6.326 MILLION OZ//INVENTORY REST AT 564.966 MILLION OZ//

APRIL 1/WITH SILVER DOWN 39 CENTS A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.302 MILLION OZ INTO THE SLV////INVENTORY REST AT 558.647 MILLION OZ//

MARCH 31/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.171 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 556.345 MILLION OZ

MARCH 28/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.847 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 554.167 MILLION OZ//

MARCH 25/WITH SILVER DOWN 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 24/WITH SILVER UP 54 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.092 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 23/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 22/WITH SILVER DOWN $0.29 TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

SLV FINAL INVENTORY FOR TODAY: 576.900 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Schiff: GDP Spin Is Orwellian Doublespeak

WEDNESDAY, MAY 04, 2022 – 06:30 AM

Despite all the talk about a “strong economy,” nobody was expecting a blistering hot GDP for the first quarter. The consensus was for around a 1% gain. As it turned out, it was even worse than expected. GDP shrank in Q1, contracting by 1.4%.

Despite the awful number, the mainstream spun it as a positive. Peter Schiff called it an outrageous positive spin on negative GDP and a great example of Orwellian doublespeak.

A New York Times headline proclaimed, “GDP Report Shows US Economy Shrank, Masking a Broader Recovery”

Basically, the NYT and others in the mainstream media are claiming the economy is really strong. You just can’t see that strength because it’s hidden behind this weak economy. Peter wondered out loud what in the hell they are talking about.

The first point to consider is that of negative GDP in one quarter means we’re halfway to a recession. A recession is defined as two consecutive quarters of contracting GDP.

Jerome Powell and the other central bankers at the Federal Reserve have hung their hats on the fact that the US has a super-strong economy. They claim the economy is strong enough to handle rate hikes and quantitative tightening without spinning into a deep recession. Peter asks the operative question.

If the economy is so strong, why is it contracting? How is a -1.4% GDP a strong economy?”

Peter said he can’t remember a time when the Fed hiked rates after a negative GDP quarter. Normally, a quarter like Q1 would have the Fed considering rate cuts in order to preemptively prevent a recession.

If we already have one negative quarter, and that’s with interest rates at 25 basis points, if the Fed really ratchets up interest rates in Q2, well, doesn’t it stand to reason that GDP in the second quarter will be even lower than GDP in the first quarter when the economy is going to have to contend with much higher interest rates? Of course! So, you would have to say the odds favor a recession.”

Normally when the Fed starts hiking rates, the economy is strong. You’re getting big GDP prints. When the economy is hot, the central bank typically tries to cool it off in order to head off inflation before it gets started.

Well, we don’t have a blazing hot economy. We really have an ice-cold economy. Just look at the GDP. Yet the Fed is just starting to raise rates anyway because we have inflation — not in a strong economy. We have inflation in a weak economy. We have stagflation.”

Peter said the Fed’s credibility is in a very precarious position. It’s pretty much ignoring this negative GDP print, claiming the economy is still strong.

What happens when we end up in a recession? What happens to the Fed’s credibility? Because, after all, they’ve got everything wrong. First, they said there’s no inflation. Then they said inflation is transitory. Then they admit they got that wrong. And now they see this negative GDP number, and basically, they say that’s transitory too.”

If Powell and Company were honest, they would say, “We’re going to hike rates to fight inflation and that’s going to cause a recession.” But they don’t want to admit that. They want to have it both ways. They want everybody to think they can put out the inflation fire without starting a fire in the economy.

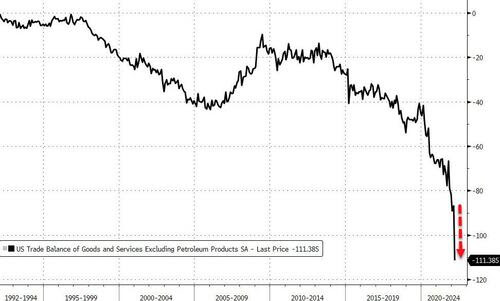

One of the factors pulling GDP down was the massive trade deficit. The March trade deficit in goods came in way above expectations and shattered the old record. And yet the dollar remains strong. Normally, a massive trade deficit would result in the dollar getting punished. But the US enjoys the privilege of issuing the world reserve currency. America imports goods and exports dollars.

Dollars are America’s greatest export. Except they’re worthless. We just print them. We create them out of thin air. They have no value. The stuff that we’re getting has real value. You need factories, machines, workers, land — all sorts of materials go into the production of finished goods that Americans are importing. And what are we giving our trading partners? Digits that we create out of thin air. Why do they do that? Beats the hell out of me. What is the world doing with all these dollars? What are they going to do with $125.3 billion they just earned?”

The more dollars the world has, the less they are worth. At some point, it has to collapse. At this point, the dollar is benefitting from being the cleanest dirty shirt in the laundry. There are problems in Japan and Europe. At some point, this bubble will pop.

But the mainstream spins big trade deficits as a sign of a strong economy. They reason that the voracious appetite for imports shows Americans have plenty of money to spend. Peter called this nonsense.

Strong economies produce stuff. They don’t simply consume stuff. If we really had a strong economy, we wouldn’t just be buying stuff. We would be making the stuff we’re buying. In fact, we would be making so much stuff that we’d have extra, and we’d be able to sell it to other people whose economies aren’t strong enough to make what we could make, and we would have a trade surplus.”

Peter called this “George Orwell doublespeak.”

This is everybody trying to convince the public that something bad is actually good.”

And that brings us back to the GDP report.

The mainstream spin is the economy is strong except for the pesky trade deficit. Trade deficits subtract from GDP. A record trade deficit means a record subtraction from GDP. But in the mainstream view, Americans are spending, spending, spending, and this signals economic strength. But Peter said you can’t just pretend that the trade deficit doesn’t exist. GDP measures the output of the domestic economy. That’s what the D stands for.

If you’re buying stuff that was made abroad, well, you’re not measuring the domestic economy. You’re measuring the foreign economy. We’re not supposed to be picking up the Japanese economy, or the Chinese economy, or the Korean economy, or any of these other economies. We’re focusing on the US economy. So, if we have a trade deficit, we have to minus that out.”

Ignoring the trade deficit destroys the whole concept of GDP.

You can’t take out the trade deficit and say, ‘This is a great economy. We have a broad-based recovery.’ We have a bubble. That’s what the trade deficit is showing. This isn’t real economic strength. This is a massive bubble. And when Powell is saying we have this great economy so we can raise rates, we have a lousy economy. The trade deficit proves it.”

END

2.LAWRIE WILLIAMS//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

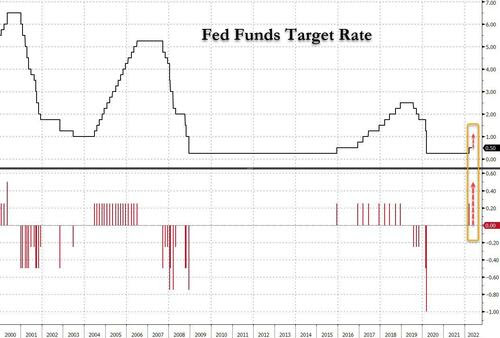

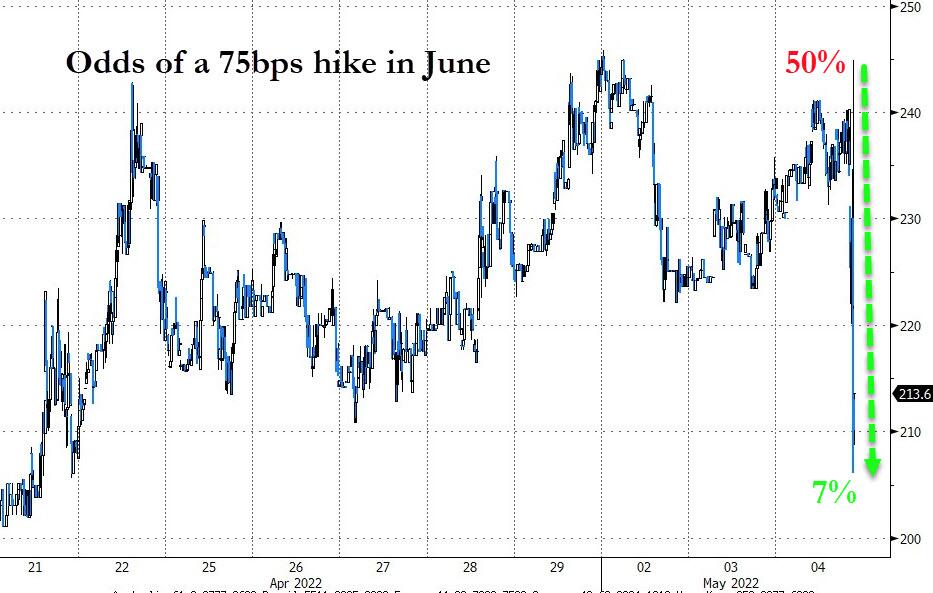

Craig Hemke on tomorrow’s Fed announcement of a 50% basis point rise in interest rates

(CraigHemke)

Craig Hemke at Sprott Money: Fed perception vs. Fed reality

Submitted by admin on Tue, 2022-05-03 20:46Section: Daily Dispatches

By Craig Hemke

TF Metals Report

via Sprott Money, Toronto

Tuesday, May 3, 2022

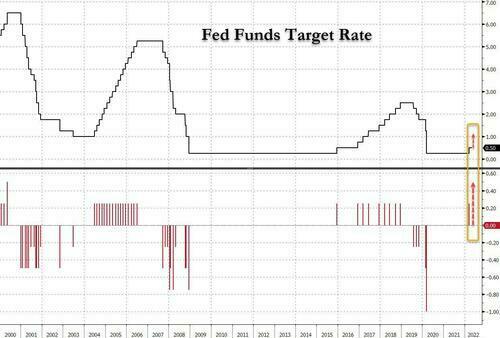

Wednesday brings the long-awaited conclusion of the May Federal Open Market Committee meeting. How will the statement read?

More importantly, how will Chief Goon Powell respond in his “press conference”?

But perhaps most important of all, does it even matter?

The fun and games begin with the 2 p.m.ET release of the FOMC “fed lines.” After that’s parsed and digested, Chief Goon Powell will appear via Zoom at 2:30 p.m. and pretend to host an unscripted “press conference.”

What he says and how he says it will drive bonds, for exchange, the S&P, and the precious metals through the remainder of the week and the balance of the month.

Let’s begin with perception. …

… For the remainder of the analysis:

https://www.sprottmoney.com/blog/Fed-Perception-vs-Fed-Reality-Craig-Hemke-May-3-2022

end

A 3% tax on using the uSA dollar on purchases is pushing Venezuelans back into bolivars

(Blomberg)

Maduro’s 3% dollar tax pushes Venezuelans back into bolivars

Submitted by admin on Tue, 2022-05-03 20:52Section: Daily Dispatches

By Nicolle Yapur

Bloomberg News

via Yahoo News, Sunnyvale, California

Tuesday, May 3, 2022

For years, the bolivar drifted toward irrelevancy as Venezuelans embraced the economic stability brought on by the widespread use of the U.S. dollar.

But the socialist regime, always reluctant to fully turn its economy over to the dollar, is now making a surprise bid to revive the local currency.

Emboldened by surging oil exports that are fueling economic growth and helping keep the foreign-exchange rate steady, the government is pushing Venezuelans to use the bolivar more by slapping a 3% tax on purchases made with dollars in shops, restaurants, and grocery stores.

One study done by a private firm indicates there was a slight shift away from the dollar in the days after the tax took effect. A separate report released today found the use of bolivars in Caracas rose sharply in April, the first full month after its introduction. …

… For the remainder of the report:

https://www.yahoo.com/now/venezuela-reins-dollarization-risky-bid-120000945.html

4.OTHER GOLD/SILVER COMMENTARIES

Russia is returning to the gold standard and China will follow

(QTR Fringe Finance)

Russia Is Returning To The Gold Standard: Is China Next?

TUESDAY, MAY 03, 2022 – 07:25 PM

Submitted by QTR’s Fringe Finance

No sooner was it that I wrote an article talking about how Russia was going to back the ruble with gold than “one of the Russia’s most powerful security/intelligence officers and a close ally of Putin” has admitted the country’s intentions to do just that.

And I’m predicting that no sooner will the gravity of this decision finally sink in with the West that China will follow closely in Russia’s footsteps and do the same.

Russia backing its currency with gold represents one of the most drastic changes to the foreign currency market in decades. As of 2022, precisely zero countries still adhere to a gold standard, though many countries still hold gold in reserve.

The new global monetary system is likely going to look like Russia, China, India, Saudi Arabia and other countries with commodity-backed, sound money on one side – and the west and our allies, with our “infinite” fiat, under the tutelage of rocket surgeon Neel Kashkari, on the other.

Despite the enormity of the situation, the news hasn’t really been digested by global markets yet. The FX market has been relatively calm, but for the ruble strengthening, and gold prices have crashed so far this week, with front month futures falling nearly $50/oz. on Monday, back down to about $1,860/oz.

Ruble vs. Euro chart from Zero Hedge

Today’s content is free, but if you enjoy it and have the means to support the blog, I’d be humbled by your subscription: Subscribe now

Aside from the FX market, the news also hasn’t been digested by US politicians or financial “thought leaders” yet.

However, there are underground rumblings starting to catch the ears of those who are actively listening. Ronan Manly wrote for BullionStar.com last week:

On Tuesday 26 April in an interview with newspaper Rossiyskaya Gazeta (RG), the Secretary of the Russian Federation’s Security Council, Nikolai Patrushev, said that Russian experts are working on a project to back the Russian ruble with gold and other commodities.

Manly was kind enough to translate the interview with RG, which stated Russia’s intentions to back the ruble with gold in crystal clear fashion:

RG Question: And what do we need to do to ensure the ruble’s sovereignty?

Nikolai Patrushev: “For any national financial system to be sovereignized, its means of payment must have intrinsic value and price stability, without being pegged to the dollar.

Now experts are working on a project proposed by the scientific community to create a two-circuit monetary and financial system.

In particular, it is proposed to determine the value of the ruble, which should be backed by both gold and a group of goods that are currency values, and to put the ruble exchange rate in line with the real purchasing power parity.”

Manly concludes, matter-of-factly:

So there you have it. The Russian Government is actively working on creating a gold and commodity backed Russian ruble with intrinsic value which is outside the orbit of the US dollar.

…

What we are seeing now is Nikolai Patrushev and the Kremlin confirming this simple equation of linking the Russian ruble to gold and commodities. In other words, the beginning of a multilateral gold and commodity backed monetary system, i.e. Bretton Woods III.

Just days ago I published an in-depth analysis by my friend Lawrence Lepard, about what Bretton Woods III might look like. For anyone concerned about the future of the monetary system, it is a must-read: Putin Knows The Monetary System Is A Credit Based Ponzi Scheme: Lawrence Lepard

Finally, to take Manly’s analysis one step further, I think China isn’t going to be far behind Russia in adopting a gold standard.

Going back to last summer, before the invasion of Ukraine happened and before inflation was an issue, I wrote an article arguing that it was the most common sense scenario for China to affix its new digital currency to gold.

That was before Russia decided they were ready to take a stand against the west’s monetary policies and before China became interested in buying distressed strategic oil assets from Russia while the rest of the globe tries to shut the country down economically.

Now, Russia and China are closer than they’ve ever been and arguably more unified in their interests of keeping the U.S., the west and NATO in check than they’ve ever been.

China has also kept one eye on Taiwan, as I noted in an article last month exploring whether or not President Xi is actively entertaining the idea of catalyzing World War III. For now, those concerns have taken a back seat to the country’s bizarre recent reaction to a Covid “outbreak” that it is fruitlessly trying to control.

Meanwhile, as Russia accepts payment for oil only in rubles or gold, “the digital yuan has already been piloted in various Chinese cities and was used in more than $8 billion worth of transactions in the second half of 2021,” CNN reported earlier this year. In other words, the rubber is starting to hit the road for China’s digital currency.

And, with everyone locked in their homes once again, it’s extremely convenient timing.

Is the picture becoming clear yet, or do I need to spell it out for you?

end

5.OTHER COMMODITIES //DIESEL

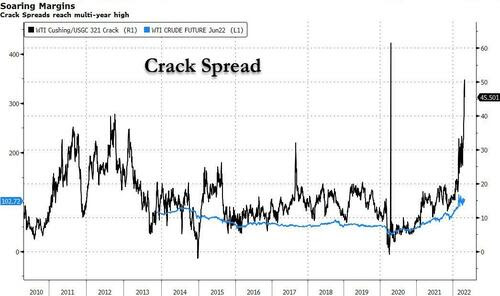

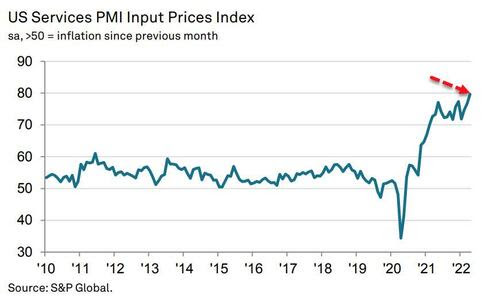

This is not good: the crack spread which are the distillates from oil are rising and becoming much more valuable than oi itself

(zerohedge)

D-Day Approaches: Crack Spread Soars As Diesel Market Braces For Historic Shock

TUESDAY, MAY 03, 2022 – 05:05 PM

While the market’s attention – and certainly that of the administration – has been focused on the surge in gas prices due to their vast political implications, the real action – and threat – is in diesel, as discussed extensively and most recently in “Why Every American Should Care That Diesel Prices Are Surging Across The Country“, and also in the following articles from the past 3 months.

- The Diesel Market Is Soaring, And Gasoline Prices Will Catch Up This Summer (May 1)

- Global Diesel Shortage To Push Oil Prices Much Higher (March 25)

- “Gas Stations Will Run Dry”: Catastrophic Scenario For Diesel Emerging (March 23)

- Global Diesel Shortage Raises Risk Of Even Greater Oil Price Spike (Mar 12)

- China Asks State-Owned Refiners To Halt Gasoline, Diesel Exports (Mar 10)

- U.S. Diesel Stocks Set To Fall Critically Low (Feb 18)

- Diesel Is The U.S. Economy’s Inflation Canary (Feb 8)

Well, with every passing day, D (for Diesel)-Day approaches, and as Bloomberg’s Natalia Kniazhevich observes today, the crack spread – or profit margins from products such as gasoline, diesel and jet fuel – reached the highest since the freak oil collapse of April 2020, confirming what we have been saying since January, namely that shortages in fuels like gasoline and diesel are greater than in crude oil.

Echoing what we have discussed on numerous occasions, the spread indicates that demand for refined products, mostly diesel, is so strong that refiners have only limited spare capacity to meet it.

There is a glimmer of hope: during the pandemic, lots of refinery units were shut down and there were few new additions to the market. Now that U.S. refiners have been steadily coming out of maintenance, as they begin ramping up for high-demand summer season, the tightness in the refined-product market may ease.

Of course, if demand destruction in diesel does not materialize soon, and remains at current high levels just as summer gasoline demand spikes, then all bets are off

end

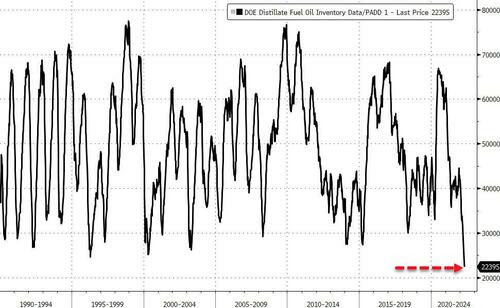

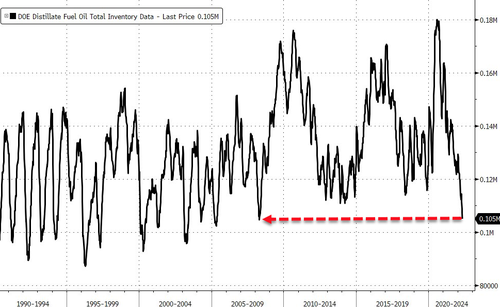

US East Coast Diesel Stockpiles Hit Record Low As Fuel Crisis Nears

WEDNESDAY, MAY 04, 2022 – 12:31 PM

We noted Tuesday evening, D (for Diesel)-Day quickly approaches, though it might already be here as U.S. East Coast distillate inventories plunge to a record low, according to new government data.

Weekly petroleum data from Energy Information Administration’s (EIA) Crude Oil Inventories show East Coast distillate inventories are at their lowest ever, dropping to just 22.4 million barrels.

Total U.S. distillate inventories have sunk to levels not seen since the last financial crisis.

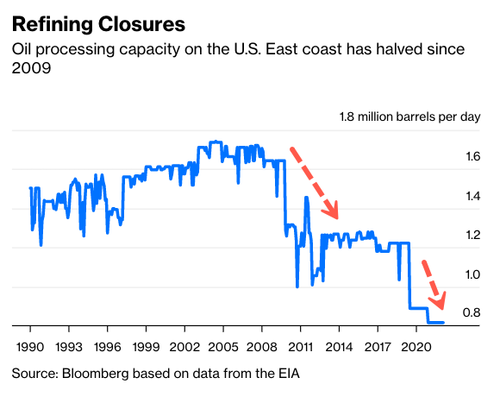

One of the reasons for the drop is East Coast refinery capacity has plunged over the last decade, “leaving the region vulnerable to squeezes,” according to Bloomberg’s Javier Blas.

In the past 15 years, the number of refineries on the U.S. East coast has halved to just seven. The closures have reduced the region’s oil processing capacity to just 818,000 barrels per day, down from 1.64 million barrels per day in 2009. -Blas

Total U.S. refinery utilization capacity has plunged from 96% in February to 86% at the end of April. Also, the U.S. has halted energy imports from Russia.

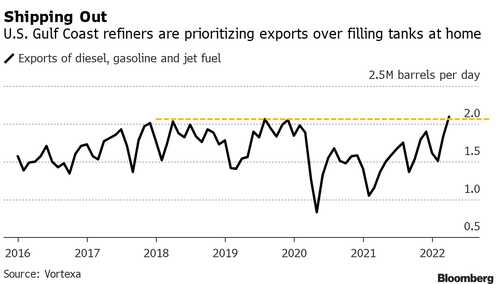

There’s also the issue Gulf Coast refiners’ are prioritizing exports to Europe rather than increasing domestic supply, sending the price of diesel to a record high.

Diesel is used in trucks, tractors, freight trains, and power generation. Soaring prices will only exacerbate inflationary pressures.

Blas said: “The diesel shortfall is nearing crisis levels.”

Reality is starting to sink in about the worst inflation in four decades. Truckers have told the Dirty Jobs jobs guy Mike Rowe that it now costs $1,000 to fill up their fuel tanks.

Rowe said truckers aren’t buying the Biden administration’s narrative that Russia is responsible for soaring fuel prices.

With the U.S.’ busy travel season less than a month away and diesel inventories on the East Coast at record lows with refinery capacity in the region struggling, this could only suggest a fuel crisis could be nearing.

COMMODITIES IN GENERAL//DIAMONDS

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.6085

OFFSHORE YUAN: 6.6587

HANG SANG CLOSED DOWN 230.37 OR 1.10%

2. Nikkei closed DOWN 29.37 PTS OR .11%

3. Europe stocks ALL CLOSED ALL RED

USA dollar INDEX DOWN TO 103.41/Euro RISES TO 1.0527

3b Japan 10 YR bond yield: RISES TO. +.224/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 129,93/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP -SHORE CLOSED DOWN// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.941%/Italian 10 Yr bond yield RISES to 2.85% /SPAIN 10 YR BOND YIELD RISES TO 2.00%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.91: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3i Greek 10 year bond yield RISES TO : 3.31

3j Gold at $1869.00 silver at: 22.681 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 3 roubles/dollar; ROUBLE AT 69.00

3m oil into the 106 dollar handle for WTI and 109 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 129.93 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9803– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0320well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

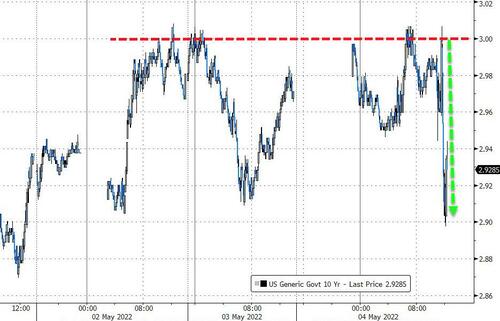

USA 10 YR BOND YIELD: 2.936 DOWN 0 BASIS PTS

USA 30 YR BOND YIELD: 2.995 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.81

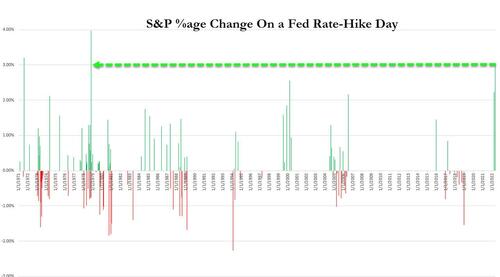

Futures Rise Ahead Of Biggest Fed Rate Hike Since The Dot Com Bubble Burst

WEDNESDAY, MAY 04, 2022 – 07:50 AM

May the 4th is here, and US futures are up slightly ahead of a key Federal Reserve meeting in which the Fed is widely expected to raise rates by 50bps, the biggest hike since the dot com bubble burst in May 2000, and to release plans for balance-sheet normalization; Chair Powell’s post-meeting press conference will provide guidance on potential for bigger rate hikes at subsequent meetings and policy makers’ assessment of the neutral rate. As DB’s Jim Reid puts it, “if you’re under 43, did 3 years at university and then joined financial markets then you won’t have worked in an era of 50bps Fed rate hikes. This will very likely change tonight as the Fed are a near certainty to raise rates by 50bps. In fact it’ll be the first time the Fed have hiked at consecutive meetings since 2006. So we enter a new era that won’t be familiar to many.”

In any case, investors have already priced in the Fed’s largest hike since 2000 – in fact, OIS contracts currently price in around 160bp of additional hikes over the next three policy meetings – and they will scrutinize Chair Jerome Powell’s speech for clues on the pace of future rate increases and balance-sheet reduction. Some traders are betting on an even larger 75 basis-point hike in June. As such, even though global financial conditions are already the tightest they have ever been (according to Goldman), S&P and Nasdaq futures are both up 0.5%, while 10-year yields drifts lower, having stalled again near 3% at the European open.

“Powell’s words about how aggressively the Fed will tame inflation are likely to shape market sentiment for the next couple of weeks at least,” said technical analyst Pierre Veyret at ActivTrades in London. Lyft tumbled 26% in premarket trading after the ride-hailing company’s second-quarter outlook disappointed Wall Street.

Global bonds have slumped under a wave of monetary tightening, with German 10-year yields around 1% and the U.K.’s near 2%, while US 10Y yields are circling 3%. Adding to the tightening outlook, European Central Bank Executive Board Member Isabel Schnabel said it’s time for policy makers to take action to tame inflation, and that an interest-rate hike might come as early as July. Meanwhile, Iceland’s central bank delivered its biggest hike since the 2008 financial crisis and India’s raised its key interest rate in a surprise move Wednesday.

“There is a difficult set up in general for risk assets” as valuations remain stretched despite a drop in equities, Kathryn Koch, chief investment officer for public markets equity at Goldman Sachs & Co., said on Bloomberg Television. She added that “some people think stagflation is a real risk.”

In premarket trading, Didi Global was 6% lower and Chinese technology shares slumped as the U.S. Securities and Exchange Commission is investigating the ride-hailing giant’s chaotic 2021 debut in New York. Advanced Micro Devices jumped 5.7% in premarket trading after the chipmaker gave a strong sales forecast for the current quarter. Starbucks gained 6.6% after the coffee chain reported higher-than-expected U.S. sales, outweighing the negative impact of high inflation and Chinese lockdowns. Here are some of the biggest U.S. movers today:

- Lyft (LYFT) shares slump 27% premarket after the ride-hailing company’s second-quarter outlook disappointed Wall Street, highlighting investors’ willingness to dump growth stocks at the first hint of trouble

- Uber (UBER) slipped as Lyft’s results hit the more diversified peer. Uber said it rescheduled the release of its 1Q financial results and its quarterly conference to Wednesday morning from the afternoon, after rival Lyft gave a weaker-than-expected outlook

- Airbnb (ABNB) jumps 4.5% premarket after its second-quarter revenue forecast beat estimates, with the company seeing “substantial demand” after more than two years of Covid-19 restrictions

- Livent (LHTM) shares surge 23% premarket, with KeyBanc highlighting an increase in the lithium product maker’s 2022 Ebitda guidance

- Match Group (MTCH) slips 6.7% premarket as analysts say the miss in the dating-app company’s guidance takes some of the shine off its revenue beat

- Didi Global (DIDI) led a drop in U.S.-listed Chinese internet stocks after news of an SEC investigation into the ride-hailing company’s 2021 debut in New York added to investor concerns around the sector

- Skyworks Solutions (SKWS) shares drop 2.5% premarket after the semiconductor device company gave a forecast that was below the average analyst estimate

- Herbalife (HLF) sinks 17% premarket after slashing its full-year forecast and setting second-quarter adjusted earnings per share outlook below the average analyst estimate

- Advanced Micro Devices (AMD) rises as much as 7.5% in premarket trading, with analysts positive on the demand the chipmaker is seeing from data centers

- Akamai (AKAM) falls as much as 14% after analysts noted that a slowdown in internet traffic and the loss of revenue due to the war in Ukraine hit the company’s first-quarter results and full-year guidance

JPMorgan CEO Jamie Dimon said in an interview Wednesday that the Fed should have moved quicker to raise rates as inflation hits the world economy. He said there was a 33% chance of the Federal Reserve’s actions leading to a soft landing for the U.S. economy and a third chance of a mild recession.

“The Fed remains very focused on bringing inflation down, however, any further hawkish pivots will likely be tempered to some extent by the desire to achieve a soft landing,” Blerina Uruci, U.S. economist at T. Rowe Price Group Inc., wrote in a note.

In Europe, declines for retailers and most other industry groups outweighed gains for energy, media and travel and leisure companies, pulling the Stoxx 600 Europe Index down 0.6%. The DAX outperforms, dropping 0.4%, Stoxx 600 lags, dropping 0.5%. Retailers, financial services and construction are the worst performing sectors. Here are the biggest European movers:

- Flutter Entertainment rises more than 6.9% its 1Q update matched broker expectations. Jefferies says a strong U.S. performance fuels confidence that a profitability “tipping point” is nearing.

- Kindred shares advance after its second-biggest shareholder, Corvex Management LP, said it believes Kindred’s board should evaluate strategic alternatives including a sale or merger.

- Fresenius SE shares rise as much as 4.2% on beating 1Q expectations. The beat was driven by the Kabi pharmaceutical division, which benefited from a positive FX impact, according to Jefferies.

- Siemens Healthineers rises after the German health care firm upgraded its earnings guidance. The beat was driven by a “strong performance” in its diagnostics division, Jefferies says.

- Stillfront shares rise as much as 10% after the Swedish video gaming group presented its latest earnings. Handelsbanken says the report provides good news, justifying some relief in the shares.

- Yara and K+S climb after the EU’s proposal to sanction the largest Belarus potash companies. Yara may see higher input prices but its market share may rise in wake of a ban, analysts note.

- Skanska falls as much as 12% after the construction group presented its latest earnings. The report was overall in-line, but construction margins were a weakness, Kepler Cheuvreux says.

Earlier in the session, Asian stocks declined for a third straight day, with the Federal Reserve’s upcoming policy decision and a U.S. regulatory probe into Didi Global weighing on sentiment. The MSCI Asia Pacific Index fell by as much as 0.5%, with Chinese internet giants Tencent and Alibaba the biggest drags. The sector declined on news that the U.S. regulators are investigating Didi’s 2021 trading debut in New York. India’s stock measures fell the most in the region as the domestic central bank hiked a key policy rate in an unscheduled decision. Benchmarks in Hong Kong and Vietnam also fell as some markets returned from holidays, while Japan and China remained closed. All eyes are now on the Fed’s interest-rate decision on Wednesday, with policy makers expected to hike by 50 basis points, the biggest increase since 2000.

“We have two forces of gravity working on Asian equities -the rising interest rates and the lockdowns and weaker growth in China,” Herald van der Linde, head of Asia Pacific equity strategy at HSBC, told Bloomberg Television. The MSCI Asia gauge has dropped more than 13% this year as rising borrowing costs, China’s Covid-19 lockdowns and rising inflation hurt prospects for corporate profits. Shanghai’s exit from a five-week lockdown that has snarled global supply chains is being delayed by infections persistently appearing in the community. “The most important decision Asian equity investors have to make throughout this year may be duration, how to position themselves if inflation is going to peak,” van der Linde added.

In rates, treasuries advanced, outperforming bunds and rising with stock futures, although price action remains subdued ahead of 2pm ET Fed policy decision. Intermediate sectors lead the advance, with yields richer by ~2bp in 5- to 10-year sectors, before Treasury’s quarterly refunding announcement at 8:30am. Yields little changed across 2-year sector, flattening 2s10s by ~1.5bp; 10-year at ~2.96% outperforms bunds and gilts by ~3.5bp. Dollar issuance slate empty so far; two borrowers priced $3.7b Tuesday taking weekly total past $8b as new-issue activity remains light; at least two borrowers stood down from announcing deals. Bund and gilt curves bear flatten. Euribor futures drop 7-8 ticks in red and green packs following comments from ECB’s Schnabel late Tuesday.

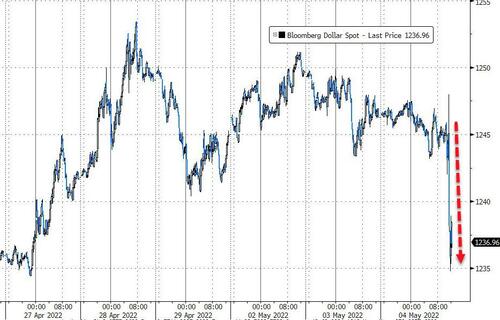

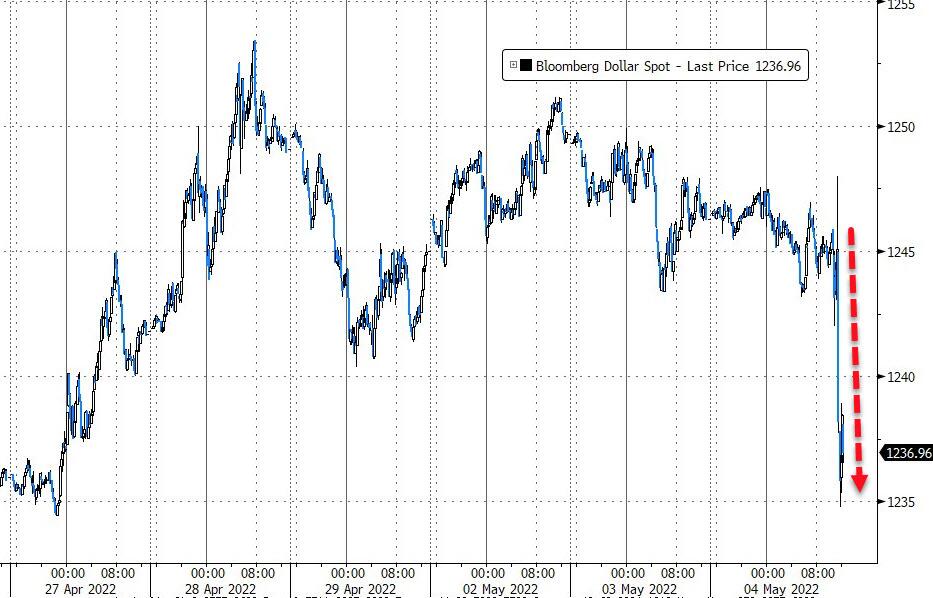

In FX, the Bloomberg Dollar Spot Index was little changed and the dollar was steady to slightly weaker against most of its Group- of-10 peers. Treasuries were steady, with the 10-year yield nudging 3%. The euro hovered around $1.0520 and European bonds fell. The pound rose past the key $1.25 level and gilts fell in line with euro-area peers, as traders braced for the FOMC rate decision later Wednesday and eyed Thursday’s Bank of England meeting. Data from the British Retail Consortium showed shop price inflation accelerated to 2.7% from a year ago in April, the most since 2011. Australia’s dollar advanced against all its Group-of-10 peers and the nation’s sovereign bonds extended losses as retail sales rising to a record high boosted bets for central bank tightening. Retail sales surged 1.6% in March to A$33.6b, more than triple economists’ forecast for a 0.5% increase.

Bitcoin is bid this morning, in contrast to the recent contained sessions, posting upside in excess of 3.0% on the session; albeit, yet to mount a test of the USD 40k mark.

In commodities, oil rallies after the European Union proposed to ban Russian crude oil over the next six months; however, sources indicate that Hungary and Slovakia will receive an extend phase-our period in order to appease their known opposition. WTI drifts 3.2% higher with gains capped near $105 so far. Spot gold steady at $1,868/Oz. Most base metals trade in the green

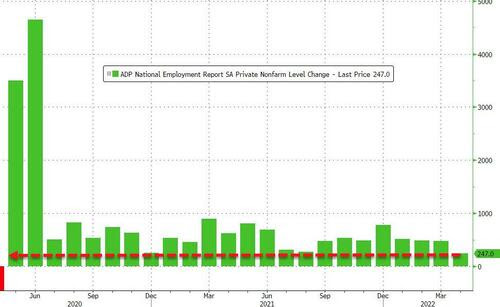

Looking at the day ahead, the main highlight will be the aforementioned Fed decision, along with Chair Powell’s subsequent press conference. On the data side, we’ll also get the final services and composite PMIs from around the world, UK mortgage approvals and Euro Area retail sales for March, and US data for the March trade balance, the ISM services index for April, and the ADP’s report of private payrolls for April. Finally, earnings releases include CVS Health, Booking Holdings, Regeneron, Uber, Marriott International and Moderna.

Market Snapshot

- S&P 500 futures up 0.3% to 4,180.00

- STOXX Europe 600 down 0.4% to 444.21

- MXAP down 0.3% to 167.37

- MXAPJ down 0.4% to 553.87

- Nikkei down 0.1% to 26,818.53

- Topix little changed at 1,898.35

- Hang Seng Index down 1.1% to 20,869.52

- Shanghai Composite up 2.4% to 3,047.06

- Sensex down 1.2% to 56,318.69

- Australia S&P/ASX 200 down 0.2% to 7,304.68

- Kospi down 0.1% to 2,677.57

- German 10Y yield little changed at 1.00%

- Euro little changed at $1.0527

- Brent Futures up 3.6% to $108.77/bbl

- Gold spot up 0.1% to $1,870.11

- U.S. Dollar Index little changed at 103.40

Top Overnight News from Bloomberg

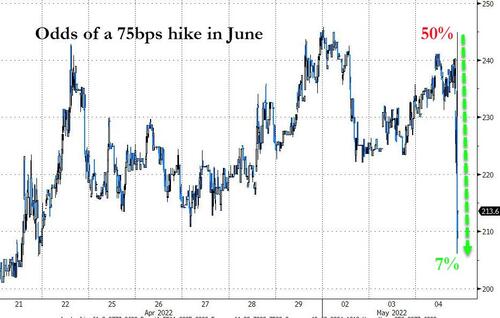

- A lot is riding on how Federal Reserve Chairman Jerome Powell parries a question he’ll surely be asked after Wednesday’s monetary policy decision: is a 75-basis-point rate hike in the cards at some stage?

- The negative-yielding bond is nearing extinction: there’s only 100 left in the world. That’s down from over 4,500 such securities last year in the Bloomberg Global Aggregate Negative Yielding Debt index, following a surge in yields as investors bet on imminent interest-rate hikes.

- The EU plans to ban Russian crude oil over the next six months and refined fuels by the end of the year as part of a sixth round of sanctions to increase pressure on Vladimir Putin over his invasion of Ukraine

- The ECB should consider raising interest rates as soon as July as inflation accelerates, ERR reported, citing Governing Council member Madis Muller

- North Korea launched what appeared to be a medium-range ballistic missile Wednesday, as Kim Jong Un ramps up his nuclear program ahead of U.S. President Joe Biden’s first visit to Seoul

- Iceland’s central bank delivered its biggest hike since the 2008 financial crisis to try to curb inflation and rein in Europe’s fastest house-price rally. The Monetary Policy Committee in Reykjavik lifted the seven-day term deposit rate by 100 basis points to 3.75%, accelerating tightening with its largest move yet since the pandemic. The increase was within the range of outcomes indicated by recent surveys of market participants

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were cautious amid holiday closures and as markets braced for the incoming FOMC. ASX 200 was rangebound as strength in financials was offset by tech and consumer sector losses. Hang Seng underperformed amid a tech rout and after a wider than expected contraction in Hong Kong’s advanced Q1 GDP, while China’s COVID-19 woes persisted with Beijing tightening its restrictions.

Top Asian News

- Hong Kong Plots Different Covid Path to Xi’s Zero Tolerance

- Beijing Shuts Metro Stations and Suspends Bus Routes

- Didi Leads Slump in U.S.-Listed Chinese Shares Amid SEC Probe

- Record India IPO Opens to Retail Amid Fickle Markets: ECM Watch

European bourses, Euro Stoxx 50 -0.3%, are modestly softer after another subdued but limited APAC handover amid ongoing regional closures. US futures remain in tight pre-FOMC ranges, with participants also awaiting ISM Services and ADP. In Europe, sectors are mostly lower with the exception. US President Biden’s administration is reportedly moving towards the imposition of human-rights related sanctions on Hikvision, according to FT sources; final decision has not been taken.

Top European News

- Hungary Voices Objection to EU Sanctions Plan on Russian Oil

- U.K. Mortgage Approvals Fall to 70.7k in March Vs. Est. 70k

- European Energy Prices Jump as EU Proposes Banning Russian Oil

- Boohoo Plunges as Online Clothing Retailer’s Growth Wilts

FX

- DXY anchored around 103.500 awaiting FOMC and Fed chair Powell for further guidance.

- Aussie gets retail therapy and hawkish RBA rate calls to consolidate gains made in wake of 25 bp hike; AUD/USD pivots 0.7100 and AUD/NZD 1.1050.

- Kiwi elevated following NZ labour data showing record low unemployment and strength in wages, NZD/USD tightens grip of 0.6400 handle and closer to half round number above.

- Loonie on a firmer footing ahead of Canadian trade as oil prices bounce, USD/CAD towards base of a broad 1.2850-00 range.

- Indian Rupee rallies after RBI lifts benchmark rate and reserve ratio at off-cycle policy meeting, former up 40 bp to 4.40% and latter +50 bp to 4.50%.

- Euro, Yen and Franc remain in close proximity of round and psychological numbers, circa 1.0500, 130.00 and 0.9800 respectively.

- RBI raises its key repo rate by 40bps to 4.4% in an off-cycle meeting; Also raises the cash reserve ratio by 50bps to 4.5%. Will retain accommodative policy stands but will remain focused on the withdrawal of accommodation.

Fixed Income

- Bonds attempt to nurse some losses before FOMC and a busy agenda in the run up, including ADP, Quarterly Refunding details and the services ISM.

- Bunds back from a 152.44 low to 153.00+, Gilts edging towards 118.00 from 117.55 and 10 year T-note fractionally above par within a 118-17+/06 range.

- German Green issuance well received as cover climbs from prior sale and retention dips, albeit with the average yield sharply higher.

Commodities

- WTI and Brent are bolstered amid the EU unveiling the sixth round of Russian sanctions, seeing a complete import ban on all Russian oil, benchmarks firmer by circa. USD 3.5/bbl

- However, sources indicate that Hungary and Slovakia will receive an extend phase-our period in order to appease their known opposition.

- US Energy Inventory Data (bbls): Crude -3.5mln (exp. -0.8mln), Gasoline -4.5mln (exp. -0.6mln), Distillate -4.5mln (exp. -1.3mln), Cushing +1.0mln.

- India is looking for Russian oil at under USD 70/bbl on a delivered basis in order to compensate for additional components incl. securing financing, via Bloomberg sources; adding, that India has purchased over 40mln/bbl of Russian crude since late-Feb.

- OPEC+ sees the 2022 surplus at 1.9mln, +600k BPD from the prior forecasts, according to the JTC report.

- Several OPEC+ officials expected the current oil pact to continue, according to Argus Media.

US Event Calendar

- 07:00: April MBA Mortgage Applications, prior -8.3%

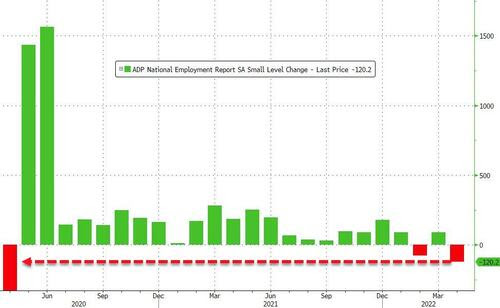

- 08:15: April ADP Employment Change, est. 382,000, prior 455,000

- 08:30: March Trade Balance, est. -$107.1b, prior -$89.2b

- 09:45: April S&P Global US Services PMI, est. 54.7, prior 54.7

- 09:45: April S&P Global US Composite PMI, est. 55.1, prior 55.1

- 10:00: April ISM Services Index, est. 58.5, prior 58.3

- 14:00: May Interest on Reserve Balances R, est. 0.90%, prior 0.40%

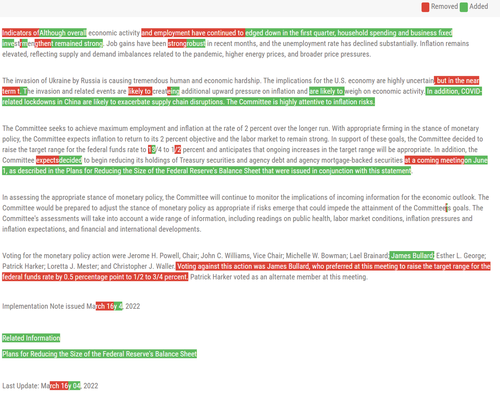

- 14:00: May FOMC Rate Decision; est. 0.75%, prior 0.25%

DB’s Jim Reid concludes the overnight wrap

I feel like I aged 20 years after the first half of the Champions League semi-final last night. Luckily the second half was less stressful and Liverpool are through to the final. I don’t think I got those 20 years back though.

Talking of age, if you’re under 43, did 3 years at university and then joined financial markets then you won’t have worked in an era of 50bps Fed rate hikes. This will very likely change tonight as the Fed are a near certainty to raise rates by 50bps. In fact it’ll be the first time the Fed have hiked at consecutive meetings since 2006. So we enter a new era that won’t be familiar to many.

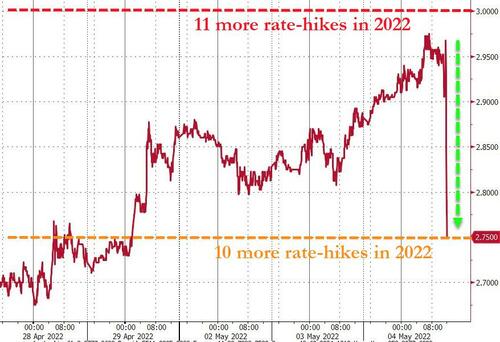

In terms of what to expect later, our US economists are also calling for a 50bps hike in their preview (link here), which follows the comment from Chair Powell before the blackout period that “50 basis points will be on the table” at this meeting. Looking forward, they further see Powell affirming market pricing that further 50bp hikes are ahead, and our US economists believe this will be the first of 3 consecutive 50bp moves, which will eventually take the Fed funds to a peak of 3.6% in mid-2023. We’re also expecting an announcement that balance sheet rundown will begin in June, with terminal cap sizes of $60bn for Treasuries and $35bn for MBS, with both to be phased in over 3 months. See Tim’s preview on QT (link here) for more info on that as well.

While the Fed might have already begun their hiking cycle 7 weeks ago now, the sense that they’re behind the curve has only grown over that time. For example, the latest inflation data from March showed CPI hitting a 40-year high of +8.5%, meaning that the Fed Funds rate was beneath -8% in real terms that month, which is lower than at any point during the 1970s. Meanwhile the labour market has continued to tighten as well, with unemployment at a post-pandemic low of 3.6% in March, and data out yesterday showed that the number of job openings hit a record high of 11.55m (vs. 11.2m expected) as well. That means the number of vacancies per unemployed worker stood at a record high of 1.94 in March, which speaks to the labour shortages present across numerous sectors at the minute.

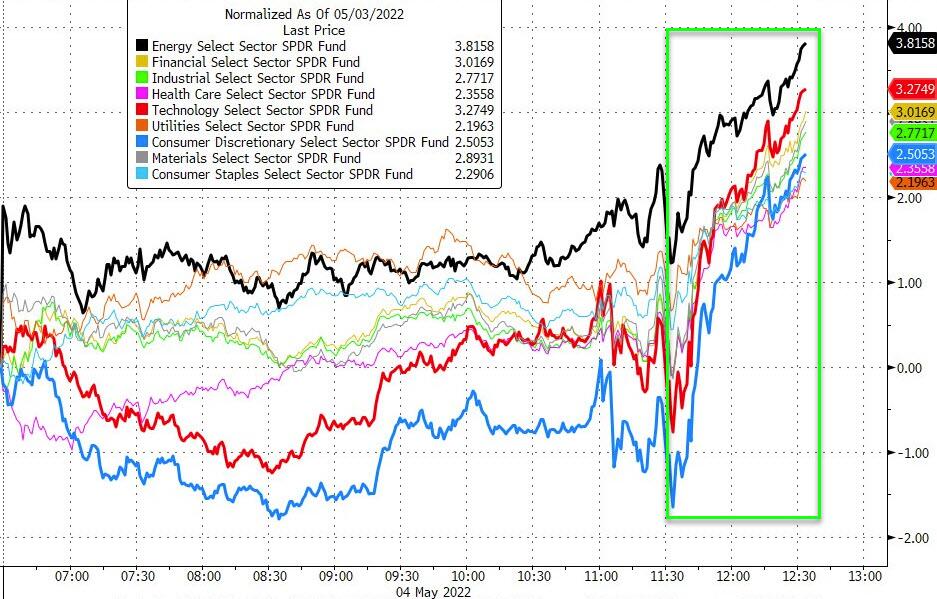

Ahead of the decision later on, the S&P 500 surrendered an intraday gain of more than +1% to finish the day +0.48% higher, in another New York afternoon turnaround. Energy (+2.87%) and financials (+1.26%) did most of the work keeping the index afloat after dipping its toes in the red late in the day, while only two sectors ultimately finished lower, staples (-0.24%) and discretionary (-0.29%). A sizable 35 S&P 500 companies reported earnings before the close, but there weren’t any standout results to drive an index-wide response. Indeed, the mega-cap FANG+ index only slightly underperformed the broader index at +0.11%. In Europe the STOXX 600 was up +0.53%, closing before the New York reversal. In line with the turnaround, overall volatility remained elevated, with the VIX index (-3.09pts) closing just below the 30 mark.

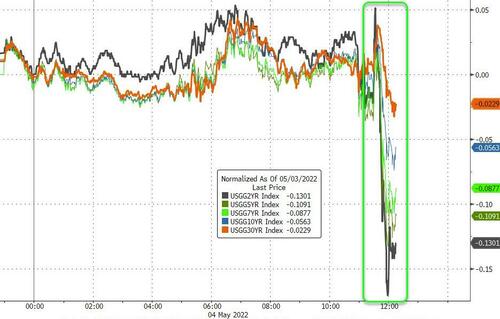

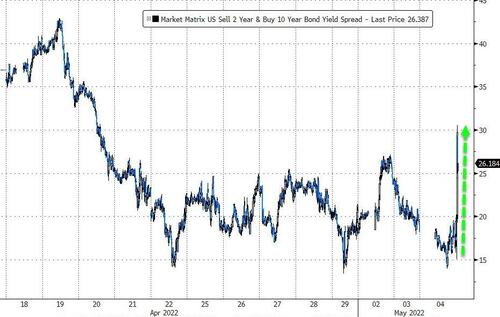

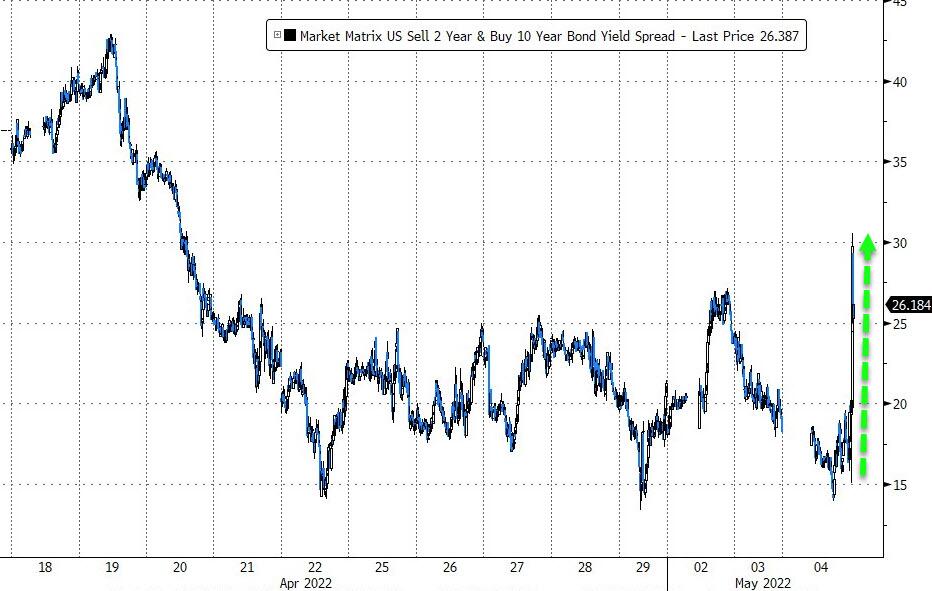

Ahead of today’s FOMC decision US Treasuries continued their recent back-and-forth price action. The 10yr yield ended ever so slightly lower at -0.1bps. That masks continued rates volatility, however, with the 10yr as much as -8bps lower intraday after having moved above 3% in the previous session for the first time since 2018. The back-and-forth was matched by real yields, as 10yr real yields were as many as -11bps lower before closing down just -0.1bps, comfortably in positive territory for only the second day since March 2020 at 0.14%. The curve flattened as short-end rates moved higher, with 2yr yields gaining +5.1bps, after most tenors were lower earlier in the session.

In Europe, yields on 10yr bunds moved above 1% in trading for the first time since 2015 shortly after the open. Yields did then swing lower, but subsequently recovered to be down just -0.2bps at 0.961%. However, bunds were one of the stronger-performing European sovereigns yesterday, and the spread of both Italian (+2.2bps) and Spanish (+1.1bps) 10yr yields over bunds widened to fresh post-Covid highs in both cases, at 191bps and 106bps respectively.

Asian equity markets are mixed in a holiday thinned session ahead of the Fed’s key rate decision later. The Hang Seng (-0.90%) is trading in negative territory as a decline in Chinese listed tech stocks is weighing on sentiment. Elsewhere, the Kospi (-0.15%) and S&P/ASX 200 (-0.08%) are fractionally lower. Meanwhile, markets in Japan and mainland China are closed today for holidays. Oil prices are slightly higher amid rising prospects of an EU embargo of Russian crude oil. As I type, Brent and WTI futures are c.+1% up to trade at $106.09/bbl and $103.53/bbl respectively.

Early morning data showed that Australia’s retail sales rose for the third consecutive month, advancing +1.6% m/m in March and going past market estimates for a + 0.5% gain. It followed a +1.8% rise in February.

Looking at yesterday’s other data releases, US factory orders grew by a stronger-than-expected +2.2% in March (vs. +1.2% expected). And over in Europe, German unemployment fell be -13k in April (vs. -15k expected), whilst the Euro Area unemployment rate in March fell to 6.8%, which is the lowest since the single currency’s formation. Finally, Euro Area PPI in March soared to 36.8% (vs. 36.3% expected), which is also a record since the single currency’s formation.

To the day ahead now, and the main highlight will be the aforementioned Fed decision, along with Chair Powell’s subsequent press conference. On the data side, we’ll also get the final services and composite PMIs from around the world, UK mortgage approvals and Euro Area retail sales for March, and US data for the March trade balance, the ISM services index for April, and the ADP’s report of private payrolls for April. Finally, earnings releases include CVS Health, Booking Holdings, Regeneron, Uber, Marriott International and Moderna.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT