harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1852.25 UP $9.85

SILVER: $21.56 UP $.08

ACCESS MARKET: GOLD $1852.00

SILVER: $21.54

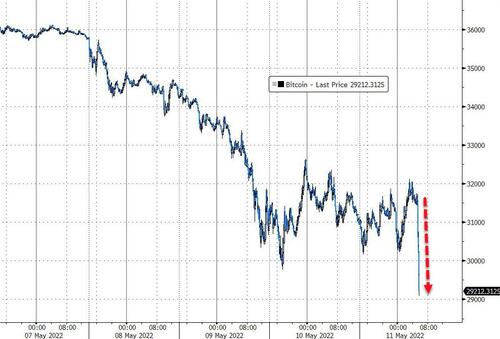

Bitcoin morning price: $31,614 UP 190

Bitcoin: afternoon price: $29,676 DOWN 1748

Platinum price: closing UP $26.80 to $999.70

Palladium price; closing DOWN $47.05 at $2029.90

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

comex notices percentage of JPMorgan notices filed: 1591/2173

EXCHANGE: COMEX

CONTRACT: MAY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,839.900000000 USD

INTENT DATE: 05/10/2022 DELIVERY DATE: 05/12/2022

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 3

657 C MORGAN STANLEY 2

657 H MORGAN STANLEY 544

661 C JP MORGAN 1591

709 C BARCLAYS 26

732 C RBC CAP MARKETS 3

737 C ADVANTAGE 4

880 H CITIGROUP 2171

905 C ADM 2

TOTAL: 2,173 2,173

MONTH TO DATE: 4,085

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT 2173 NOTICE(S) FOR 217,300 OZ (0.0 TONNES)

total notices so far: 4085 contracts for 408,500. oz (12.706 tonnes)

SILVER NOTICES:

875 NOTICE(S) FILED 4,375,000 OZ/

total number of notices filed so far this month 4737 : for 23,685,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $9.85

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD

INVENTORY RESTS AT 1068.65 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 8 CENTS

AT THE SLV// A BIG CHANGE IN SILVER INVENTORY AT THE SLV://A WITHDRAWAL OF 5.487 MILLION OZ INTO THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 570.439 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 1005 CONTRACTS TO 142,752 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GAIN IN OI WAS ACCOMPLISHED DESPITE OUR STRONG $0.40 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.40) BUT WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A HUMONGOUS GAIN OF 3153 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 30.170 MILLION OZ FOLLOWED BY TODAY’S 255,000 OZ E.F.P JUMP TO LONDON //NEW STANDING 27.845 MILLION OZ/ // V) STRONG SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : 212

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTACTS for 7 days, total 10,704, contracts: 53.520 million oz OR 7.645 MILLION OZ PER DAY. (1529CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 53.520 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 53.520 MILLION OZ//INCREASING AGAIN

RESULT: WE HAD A VERY STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1005 DESPITE OUR $0.40 LOSS IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1936 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAY. OF 30.170 MILLION OZ FOLLOWED BY TODAY;S 255,000 OZ E.F.P JUMP TO LONDON//NEW STANDING 27.845 MILLION OZ// .. WE HAD A HUMONGOUS SIZED GAIN OF 2941 OI CONTRACTS ON THE TWO EXCHANGES FOR 14.705 MILLION OZ DESPITE THE STRONG LOSS IN PRICE.

WE HAD 875 NOTICE FILED TODAY FOR 4,375,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIRY TALE SIZED 18,316 CONTRACTS TO 571,447 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: –3543 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE HUMONGOUS SIZED INCREASE IN COMEX OI CAME DESPITE OUR STRONG LOSS IN PRICE OF $16.90//COMEX GOLD TRADING/TUESDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 5.353 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY”S UNBELIEVABLE QUEUE JUMP OF 153,500 OZ//NEW STANDING 13.900 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $16.90 WITH RESPECT TO TUESDAY’S TRADING

WE HAD AN ATMOSPHERIC SIZED GAIN OF 27,726 OI CONTRACTS (95.89 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 8970 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 571,447.

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 27,286, WITH 18,316 CONTRACTS INCREASED AT THE COMEX AND 8970 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 27,286 CONTRACTS OR 84.97 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (8970) ACCOMPANYING THE GIGANTIC SIZED GAIN IN COMEX OI (18,316,): TOTAL GAIN IN THE TWO EXCHANGES 27,286 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY. AT 5.353 TONNES FOLLOWED BY TODAY’S GIGANTIC QUEUE JUMP OF 153,500 OZ//NEW STANDING 13.900 /// 3) ZERO LONG LIQUIDATION //.,4) ATMOSPHERIC SIZED COMEX OI. GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

29,905 CONTRACTS OR 2,990,500 OR 93.01 TONNES 7 TRADING DAY(S) AND THUS AVERAGING: 4272 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAY(S) IN TONNES: 93.01 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 93.01/3550 x 100% TONNES 2.62% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 93.01 TONNES INITIAL// INCREASING AGAIN

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A HUGE SIZED 1005 CONTRACT OI TO 142,752 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1936 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1936 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 560 CONTRACTS AND ADD TO THE 1936 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUMONGOUS SIZED GAIN OF 2941 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 14.705 MILLION OZ

OCCURRED DESPITE OUR LOSS IN PRICE OF $0.40 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 22,86 PTS OR 0.75% //Hang Sang CLOSED UP 190.88 PTS OR 0.97% /The Nikkei closed UP 46.54 OR 0.18% //Australia’s all ordinaires CLOSED UP 0.26% /Chinese yuan (ONSHORE) closed up 6,7179 /Oil UP TO 103.92 dollars per barrel for WTI and down TO 106.85 for Brent. Stocks in Europe OPENED ALL green // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7179 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7268: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER/

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A DOUBLY ATMOSPHERIC SIZED 18,316 CONTRACTS OR 1,831,600 OZ AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED DESPITE OUR LOSS OF $16.90 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2187 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF MAY.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 8970 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :8970 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 8970 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: AN UNBELIEVABLY SIZED TOTAL OF 27,286 CONTRACTS IN THAT 8970 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD AN ATMOSPHERIC SIZED COMEX OI GAIN OF 18,316 CONTRACTS..AND YET THIS GAIN OCCURRED DESPITE OUR LOSS IN PRICE OF GOLD $16.90.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (13.900),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 13.900 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $16.90) BUT WERE UNSUCCESSFUL IN FLEECING ANY LONGS// AS WE HAVE REGISTERED AN UNBELIEVABLY SIZED GAIN OF 95.89 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAY (13.900 TONNES)…

WE HAD 3543 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 27,726 CONTRACTS OR 2,778,600 OZ OR 84.87 TONNES

Estimated gold volume today: 285,824/// good

Confirmed volume yesterday:361,945 contracts good

INITIAL STANDINGS FOR MAY ’22 COMEX GOLD //MAY 11

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 76,020.400 oz Manfra Brinks Delaware JPMorgan includes10 kilobars and 150 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | 63,885.223 oz HSBC |

| No of oz served (contracts) today | 2173 notice(s) 217,300 OZ 6.75 TONNES |

| No of oz to be served (notices) | 384 contracts 38,400 oz 1.194 TONNES |

| Total monthly oz gold served (contracts) so far this month | 4085 notices 408,500 OZ 12.706 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit nil oz//

No dealer withdrawals

1 customer deposits

i) Into HSBC: 63,885.233 oz

4 customer withdrawals:

i) Out of Brinks: 56,330.330 oz

ii) Out of Manfra 14,545.910 oz

iii) Out of jPMorgan: 4822.650 oz (150 kilobars)

iv) Out of Delaware 321.510 oz (10 kilobars_

total withdrawal: 76,020/5– oz

ADJUSTMENTS: 1 Brinks//dealer to customer 100.01 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 2557 contracts having GAINED 1535 contracts

We had 0 notices filed on Monday, so we gained 1535 contracts or AN ADDITIONAL 153,500 oz will stand for delivery in this non active delivery month of May.

June saw a loss of 27,786 contracts down to 323,190 contracts

July has a gain of 3 OI to stand at 154

August has a gain of 42,926 contracts up to 190,070 contracts

We had 2173 notice(s) filed today for 217,300 oz FOR THE MAY 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 0 contract(s) of which 2173 notices were stopped (received) by j.P. Morgan dealer and 1591 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2021. contract month,

we take the total number of notices filed so far for the month (4085) x 100 oz , to which we add the difference between the open interest for the front month of (MAY 2557 CONTRACTS ) minus the number of notices served upon today 2173 x 100 oz per contract equals 446900 OZ OR 13.900 TONNES the number of TONNES standing in this non active month of MAY.

thus the INITIAL standings for gold for the MAY contract month:

No of notices filed so far (4085) x 100 oz+ (2557) OI for the front month minus the number of notices served upon today (2173} x 100 oz} which equals 446,900 oz standing OR 13.900 TONNES in this NON active delivery month of MAY.

TOTAL COMEX GOLD STANDING: 13.900 TONNES (A STRONG STANDING FOR A MAY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,026,795.134 oz

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 36,025,758.780 OZ

TOTAL ELIGIBLE GOLD: 18,195,107.026 OZ

TOTAL OF ALL REGISTERED GOLD: 17,830,651.712 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,803,856.0 OZ (REG GOLD- PLEDGED GOLD)

END

MAY 2022 CONTRACT MONTH//SILVER//MAY 11

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,186,964.100 oz Brinks CNT JPMorgan |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 1,170,303.526 oz CNT JPMorgan |

| No of oz served today (contracts) | 875CONTRACT(S)4,375,000 OZ) |

| No of oz to be served (notices) | 837 contracts (4,185,000 oz) |

| Total monthly oz silver served (contracts) | 4732 contracts 23,685,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposit into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 2 deposits into the customer account

i) Into CNT: 560,746.020 oz

ii) Into JPMorgan: 609,557.500 oz

total deposit: 1,170,303.526 oz

JPMorgan has a total silver weight: 177.201 million oz/336.966 million =52.56% of comex

Comex withdrawals: 3

i) Out of JPMorgan 581,487.080 oz

ii) Out of CNT:: 1032.000 oz

iii) Out of Brinks 604,445.020 oz

total withdrawal 1,186,964.100 oz

1 adjustments:

dealer to customer /JPMorgan 770,482.470 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 80.759 MILLION OZ

TOTAL REG + ELIG. 336.966 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY OI: 1712 HAVING LOST 293 CONTRACTS. WE HAD 242 NOTICES FILED ON MONDAY

SO WE LOST 51 CONTRACTS OR AN EFP JUMP OF 255,000

JUNE HAD A GAIN OF 5 TO STAND AT 1496

JULY HAD A GAIN OF 544 CONTRACTS UP TO 115,553 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 875 for 4,375,000 oz

Comex volumes: 76,415// est. volume today// good

Comex volume: confirmed yesterday: 84,462 contracts ( good )

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 4732 x 5,000 oz = 23,685,000 oz

to which we add the difference between the open interest for the front month of MAY(xxx) and the number of notices served upon today 875 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY./2021 contract month: 4732 (notices served so far) x 5000 oz + OI for front month of MAY (1712) – number of notices served upon today (875) x 5000 oz of silver standing for the MAY contract month equates 27,845,000 oz. .

We LOST 51 contracts or AN ADDITIONAL 255,000 will NOT stand for delivery at the comex as they were EFP’d to London

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

APRIL 8/WITH GOLD UP $7.70: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES INTO THE GLD//INVENTORY RESTS AT 1088.75 TONNES

APRIL 7/WITH GOLD UP $13.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1087.30 TONNES

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

GLD INVENTORY: 1068.65 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 8/WITH SILVER UP 11 CENTS :NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 7/WITH SILVER UP 27 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

INVENTORY TONIGHT RESTS AT 570.439 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2.LAWRIE WILLIAMS//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

LAWRIE WILLIAMS: China’s April gold demand confirms sharp economic downturn

The latest figures from China’s Shanghai Gold Exchange (SGE) for the April month’s gold withdrawals would seem to confirm a sharp downturn in that country’s key economic activity. This amidst some draconic measures to try and control new coronavirus outbreaks in some key industrial centres. Indeed the April gold withdrawal total at 83.74 tonnes is the lowest since July 2020 which was in the heart of the original Covid-19 outbreak in that nation.

What this may suggest is that the current coronavirus outbreak in China is more serious, and widespread, than the country’s government is telling us. Or perhaps because this time it is having a greater impact because it seems to be affecting the major centres of Shanghai and Beijing, which were largely spared at the height of the initial outbreak. Whatever the reason for the downturn, it is indeed likely to have an adverse impact on worldwide gold demand given that China has been the world’s largest gold consuming nation for some years now.

Of course the other effect is on global supply chain disruptions given the importance of Chinese products in global markets. It seems that hardly anything one buys in the West has not been made in China these days – particularly in the electronics sector. Already supply chain disruptions are a major contributor to global inflation.

There are also some reports suggesting that India, the world’s second largest gold consumer, may also be seeing a resurgence of coronavirus infection spread as new more infectious variants begin to dominate. Infection figures seem to be rising again in the U.S. too where virus-related deaths have already surpassed 1 million people and new infection rates are now also at worrying levels in Germany and France in Europe, with something of a return to higher infection figures in Italy, while other countries where things had seemed to be well under control, like Japan, South Korea, Australia, New Zealand even among others are seeing worrying infection numbers. The world is probably learning to live with the coronavirus, but the pandemic seems far from over and will continue to have an impact for the foreseeable future, if not for ever.

But back to China. We equate Chinese SGE gold withdrawals with overall demand levels – particularly with respect to gold imports and we have already noted a huge fall-off in Swiss gold exports to both China/Hong Kong and India, which has to be worrying for the gold mining sector. China is itself the world’s largest gold producer from its mines and as a byproduct from its big smelting and refining industry, so can probably meet the reduced demand level almost entirely from its own output.

World No. 2 producer (by some estimates) Russia, too, will be keen to sell gold to the Chinese markets if Western outlets are blocked due to economic sanctions, but may find there is no market for its excess output there. No doubt there are some countries which are not party to sanctions on Moscow, which will still buy Russian gold, particularly if it is offered at a discount. Thus we do see some disruptions in the gold markets ahead. Gold may therefore be in for a difficult few months, particularly if the fall- off in demand from China and India persists.

-END-

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

end

4.OTHER GOLD/SILVER COMMENTARIES

end

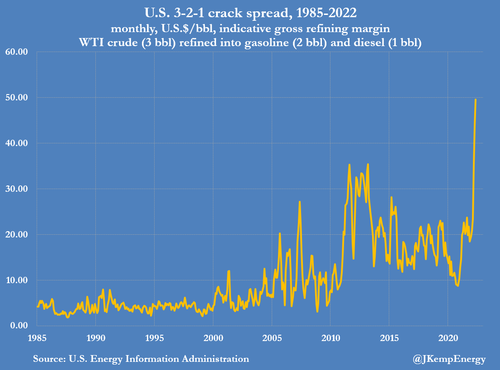

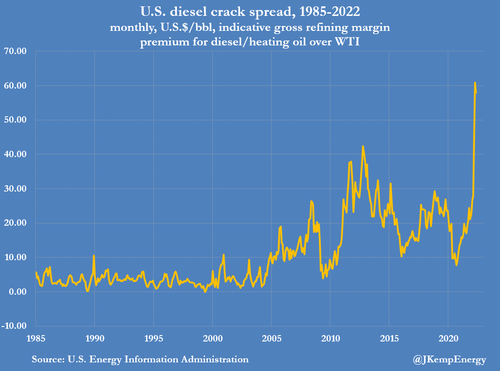

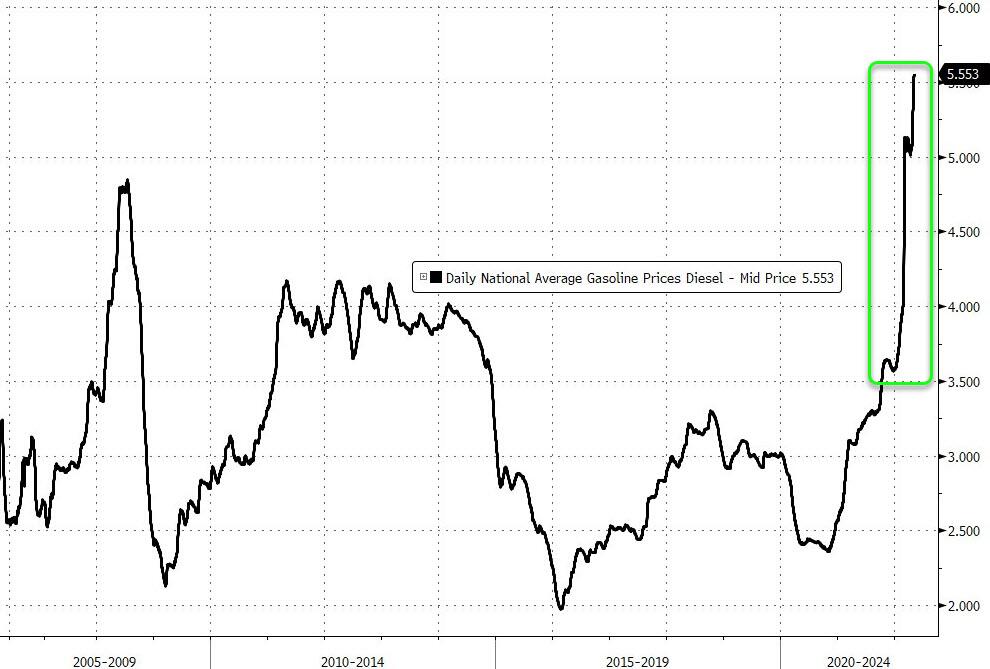

5.OTHER COMMODITIES //DIESEL

Widespread uSA diesel shortages. This sends the crack spreads to skyhigh prices

(zerohedge)

Widespread US Diesel Shortages Send Crack Spreads To Mindblowing Highs

WEDNESDAY, MAY 11, 2022 – 06:30 AM

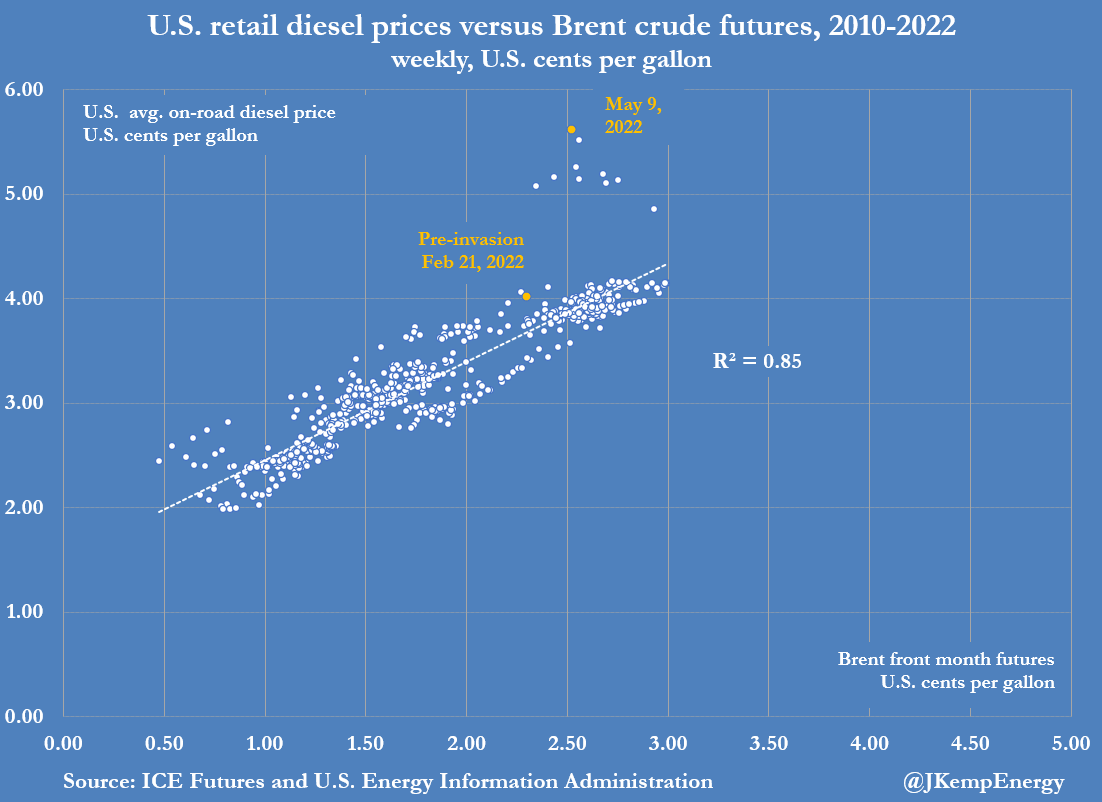

By John Kemp, senior market analyst

Global stocks of refined petroleum products have fallen to critically low levels as refineries prove unable to keep up with surging demand especially for the diesel-like fuels used in manufacturing and freight transportation. The result has been a surge in prices refiners receive for selling fuels compared with prices they pay for buying crude and other feedstocks, boosting their profitability significantly.

In the United States, refiners currently receive roughly an average of more than $150 per barrel from the sale of gasoline and diesel at wholesale prices, while paying only around $100 to purchase crude.

The indicative 3-2-1 margin of $50 per barrel is based on the assumption a refinery produces two barrels of gasoline and one barrel of diesel from refining three barrels of crude.

The margin is meant to be representative for an “average” refinery and is a gross figure out of which refiners have to pay for labor, electricity, gas, hydrogen, catalysts, pipeline transport and the cost of capital.

Net margins are narrower and refinery costs have been rising rapidly as result of widespread inflation ripping through the economy following the coronavirus pandemic. Nonetheless, even allowing for rising input costs, gross margins have more than doubled from $20 at the end of 2021, ensuring refiners have a strong financial incentive to maximize crude processing and fuel production.

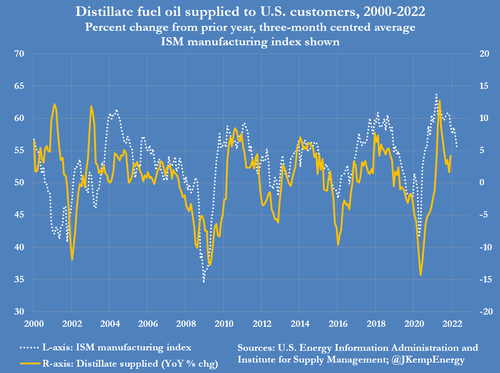

DISTILLATE FOCUS

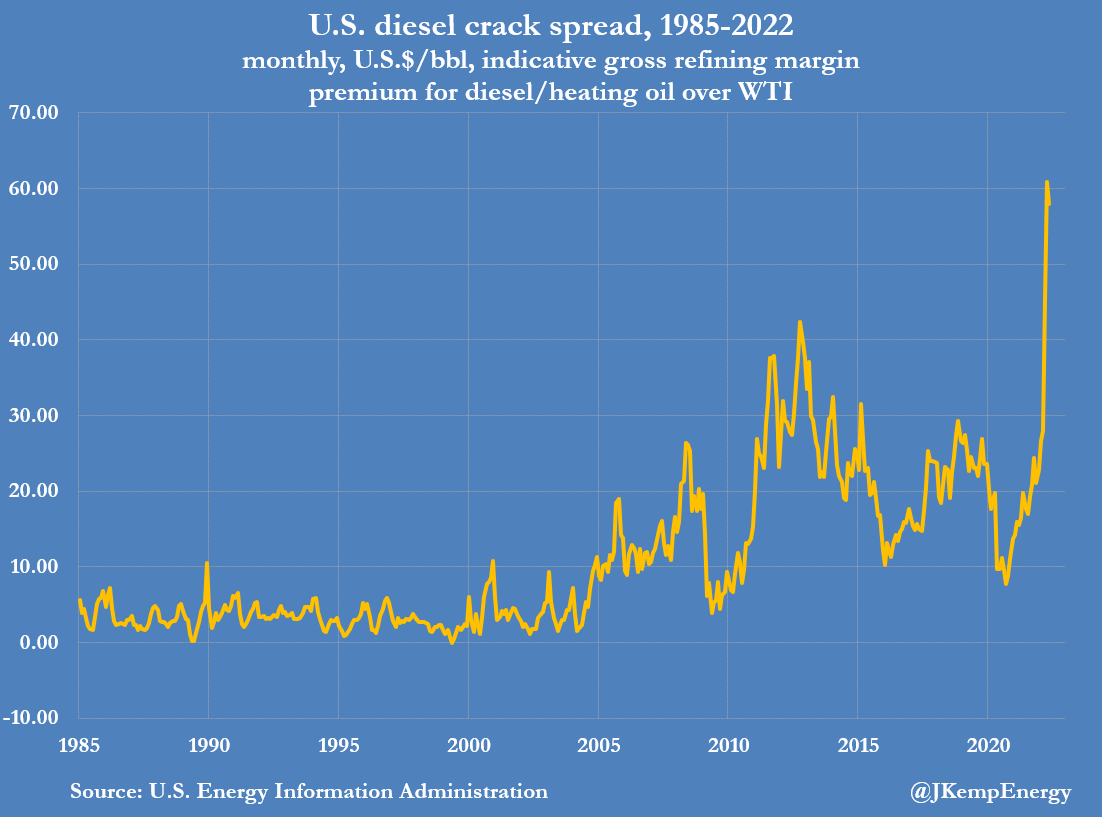

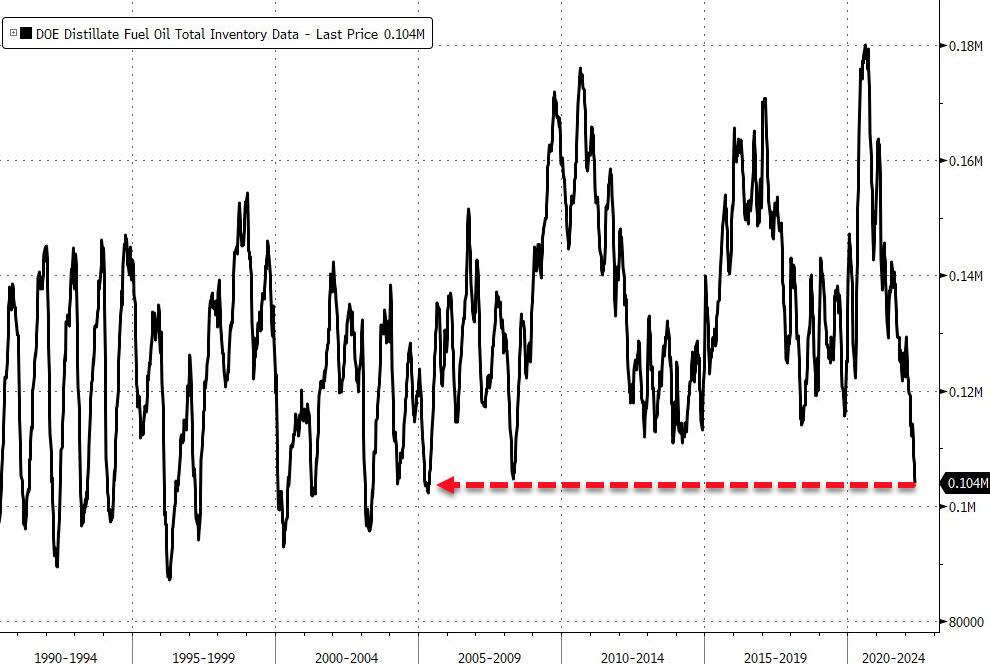

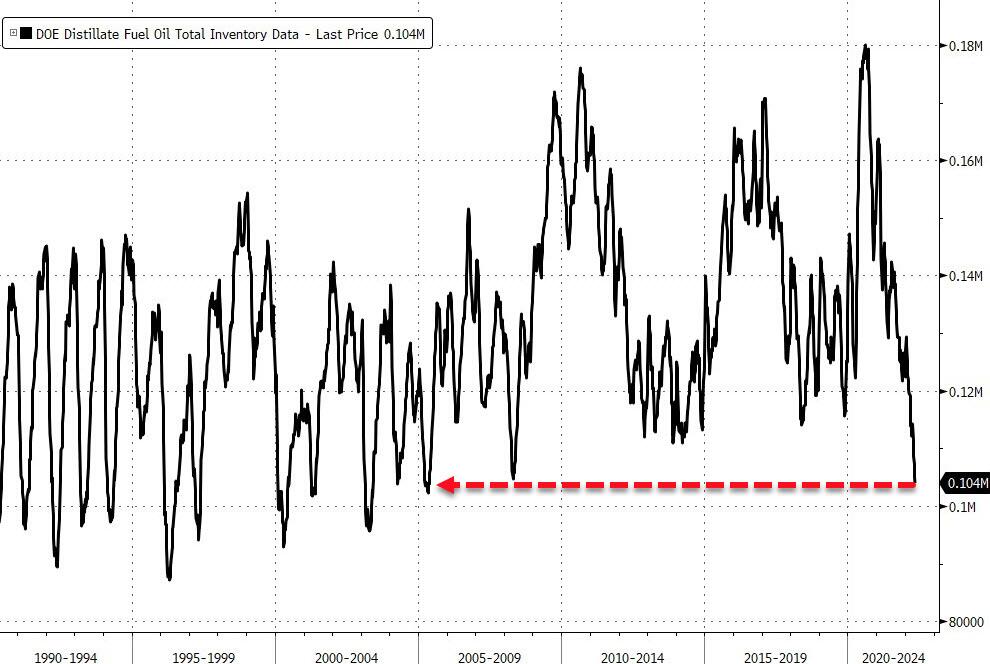

Gross margins are currently higher for making diesel (almost $60 per barrel) than for gasoline ($45 per barrel) reflecting the relative shortage of middle distillates.

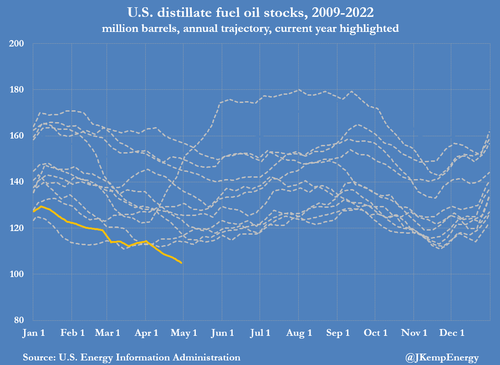

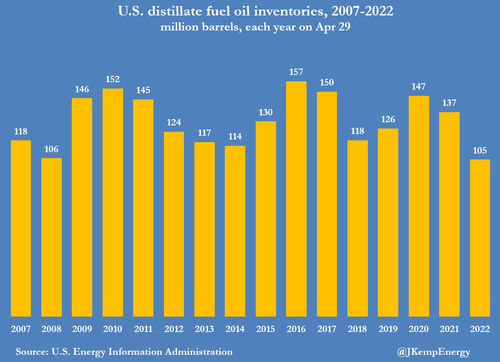

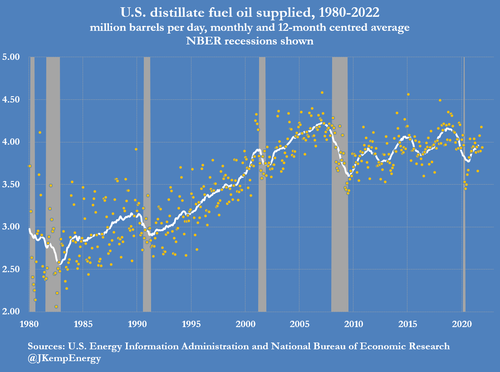

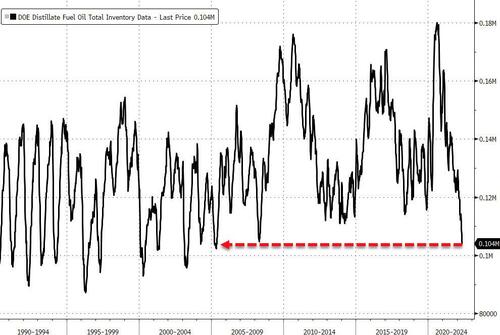

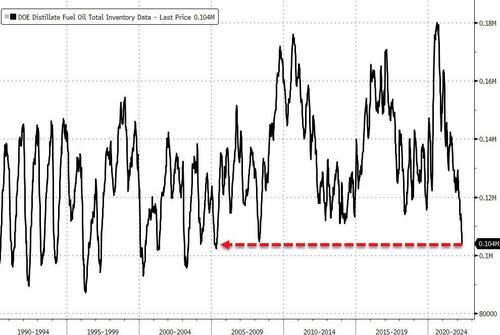

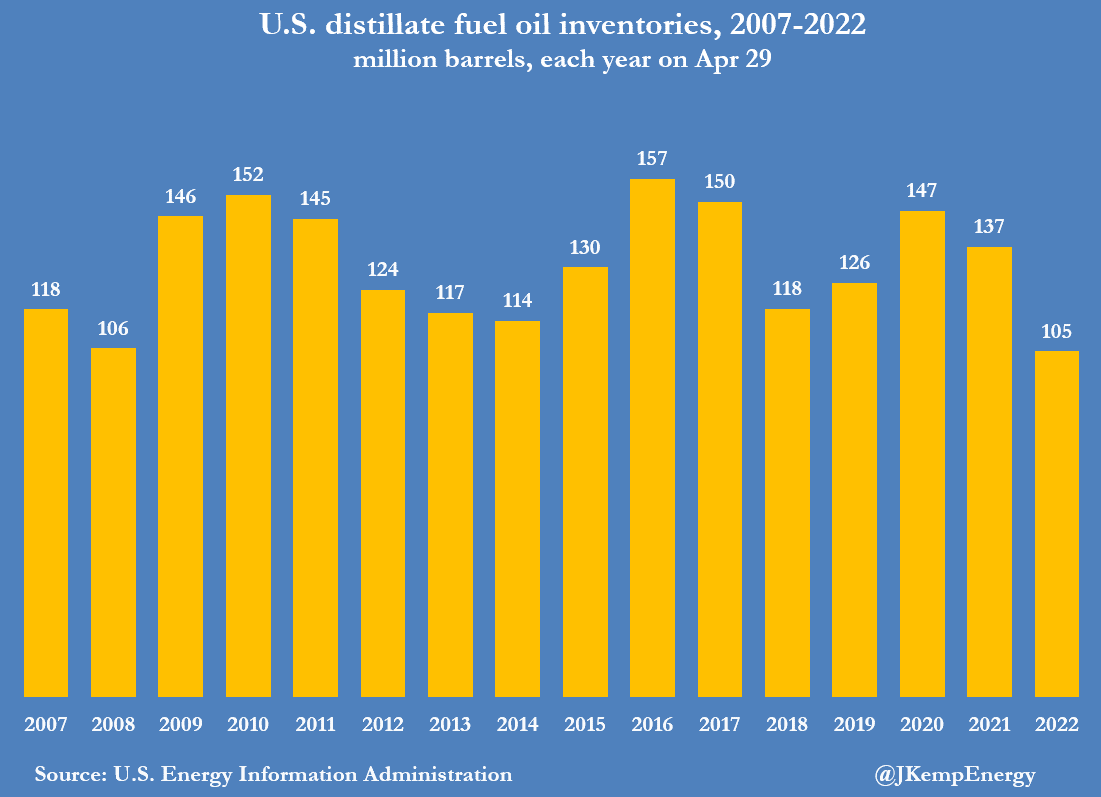

U.S. distillate fuel oil stocks are 31 million barrels (23%) below the pre-pandemic five-year average compared with a deficit of only 6 million barrels (3%) in gasoline.

The squeeze on fuel inventories and refinery capacity is compounding already high prices for crude caused by sanctions on Russia and output restraint by OPEC+ and U.S. shale producers. The resumption of international passenger aviation as quarantine restrictions are lifted is tightening the fuel market even further because jet fuel is broadly similar to diesel and gas oil.

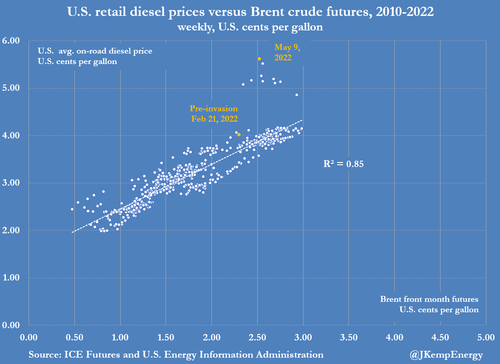

The effective wholesale price of diesel has climbed to over $160 per barrel while gasoline is trading at over $150, based on futures for delivery in New York Harbor.

Once distributors’ and retailers’ margins and taxes are included, the average price at the pump paid by motorists has climbed to $236 per barrel for diesel and $186 per barrel for gasoline.

The refining margins and fuel prices cited in this column are all for the United States but the same shortage of refining capacity and fuel inventories is boosting diesel prices in Europe, and dragging up gasoline prices with them.

SLOWDOWN AHEAD

There is scope for refiners to increase fuel production by postponing non-essential maintenance and running refineries flat out into the early autumn. And some room to adjust the output mix by switching from maximum gasoline to maximum diesel mode in downstream processing units.

But any increase in diesel production is unlikely to be able to reverse the depletion of inventories fully and return them to pre-pandemic levels. Prices will therefore have to continue rising until they begin to restrain consumption or the economy enters a cyclical downturn.

Consumers can reduce fuel use in the short term by consolidating freight loads (fewer voyages, flights and deliveries), reducing speeds (slower voyaging, flying and driving) and eliminating engine idling.

But the fuel savings are relatively modest and tend to degrade service levels, reduce capacity and increase capital costs.

By contrast, a slowdown in the business cycle delivers large simultaneous reductions in diesel use – absolutely or relative to trend – by freight firms, manufacturers, miners and construction firms. Business cycle slowdowns have therefore tended to be the main path by which the distillate market and other fuel markets have rebalanced in the past.

The adjustment process is probably underway in 2022. The cyclical slowdown and reduced fuel demand could occur in one, two or all three of the major consuming regions.

Parts of China’s economy appear to be in recession already as coronavirus lockdowns paralyse factories and transport systems and depress consumer spending.

Europe’s economy is on the verge of recession as Russia’s invasion of Ukraine, the sanctions imposed in response, soaring energy prices and rampant inflation disrupt manufacturing and depress household spending.

The only major economy with significant momentum is the United States, but there, too, the rate of expansion is slowing, which will likely result in slower growth in distillate consumption later in the year.

end

COMMODITIES IN GENERAL//DIESEL/OIL/INVENTORIES

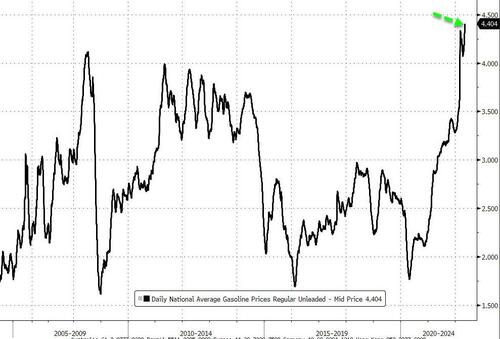

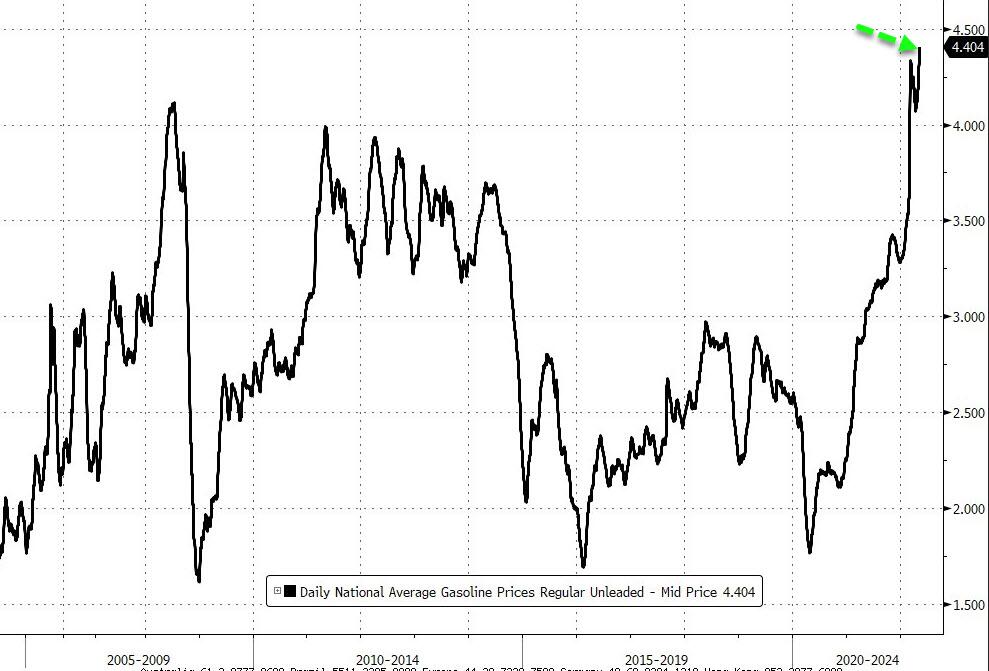

Tumbling Inventories Send US Gasoline, Diesel Prices To Fresh Record High

WEDNESDAY, MAY 11, 2022 – 02:05 PM

By Tsvetana Paraskova of OilPrice.com

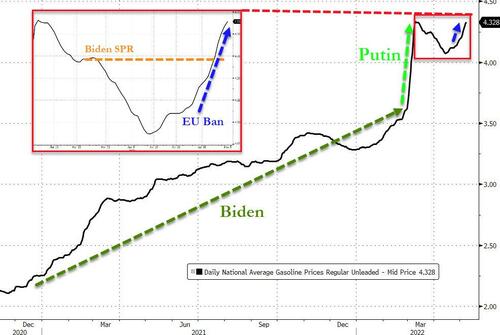

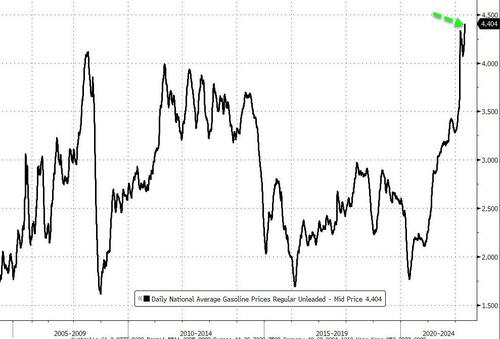

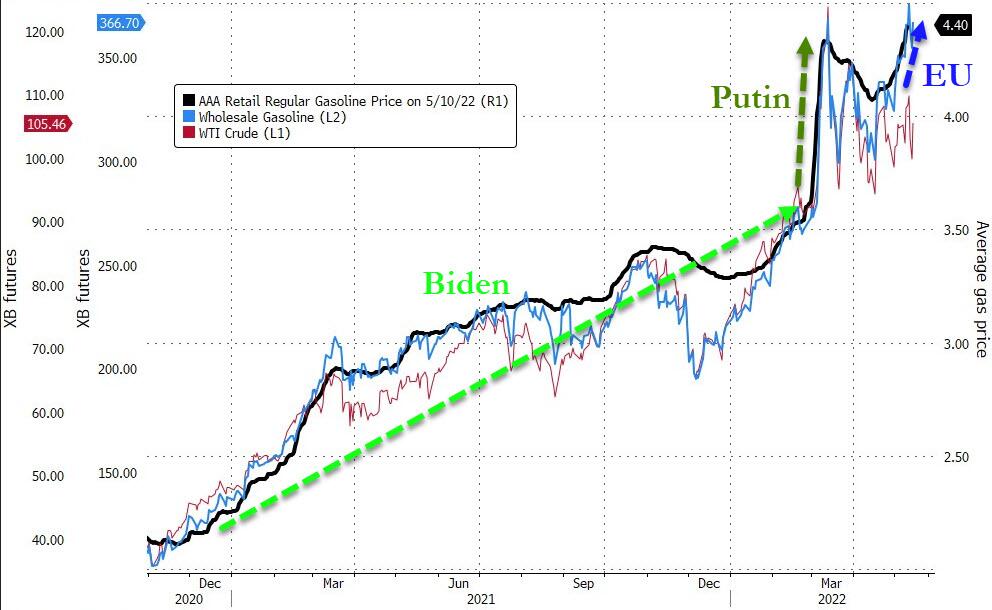

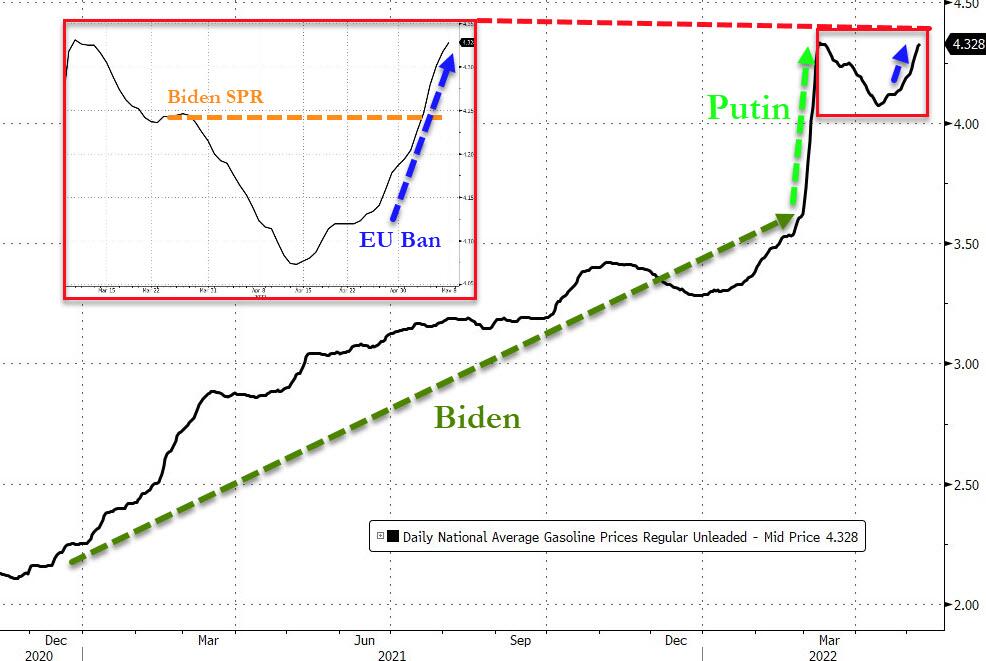

U.S. gasoline prices continued to rise, setting another all-time high on Wednesday at $4.404 per gallon average nationwide, data from AAA showed today.

That’s the highest recorded average price for gasoline in the United States, ever.

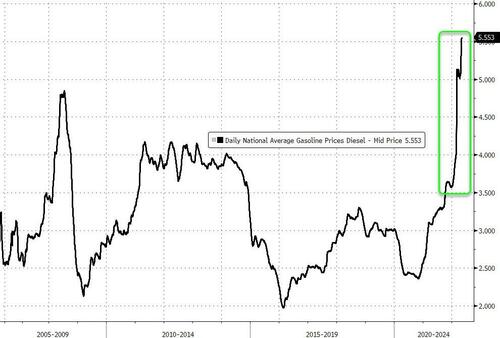

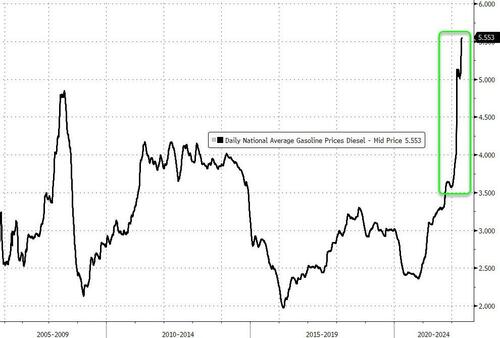

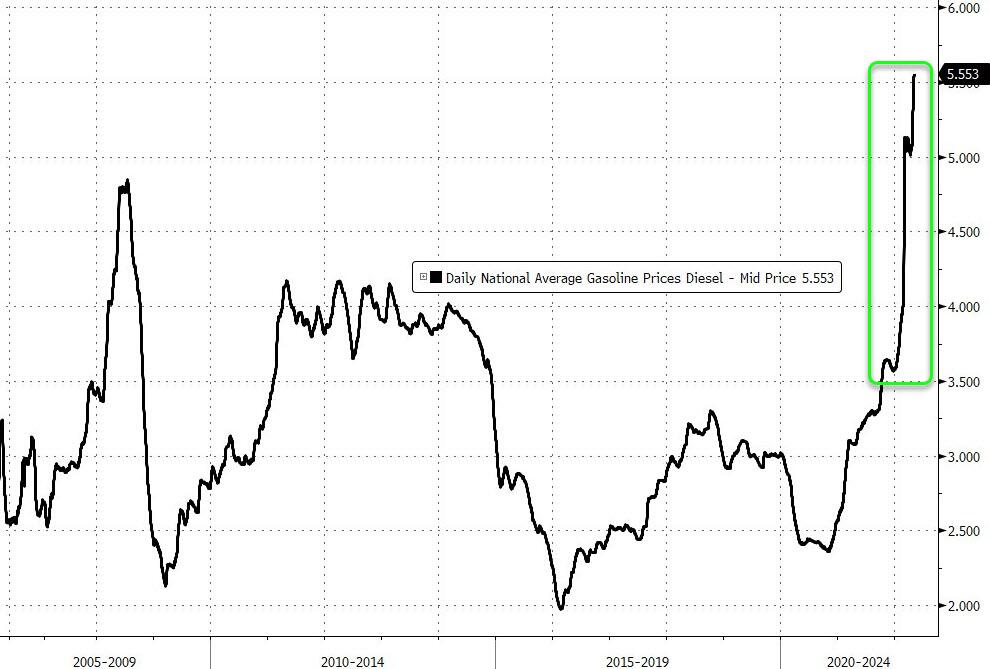

Diesel prices also hit a new high on Wednesday, reaching $5.553 a gallon. This is the highest average price ever recorded, too.

Average U.S. gasoline prices have reached new records every day this week, with Monday’s price at $4.328 per gallon. The gasoline price increased to $4.374 a gallon on Tuesday, to pass the $4.40 mark on Wednesday for the latest all-time high.

To compare, at this time last year, the national average U.S. gasoline price stood at $2.985 per gallon, per AAA data.

You will find more infographics at Statista

High international crude oil prices, with markets rattled by the Russian invasion of Ukraine and a post-COVID recovery in travel demand, have been pushing U.S. gasoline prices higher this year.

According to forecasts by fuel-savings app GasBuddy, U.S. gasoline prices will see the highest monthly average for 2022 in May. GasBuddy sees prices averaging $4.25/gal in May, but they could rise as high as $4.51/gal nationally, Patrick De Haan, head of petroleum analysis for GasBuddy, tweeted on Tuesday. Gasoline prices could hit $4.62/gal on some days in August this year, GasBuddy’s forecasts show. The yearly average for 2022 is predicted at $3.99 per gallon.

Meanwhile, the price of diesel has also soared to record highs amid very tight domestic inventories of middle distillates and a global shortage of supply. Diesel is used in every part of the industrial activity and supply chain, from goods transportation to manufacturing and agriculture; it fuels America’s economy. Diesel prices have soared to record highs in recent months, adding further upward pressure on U.S. inflation figures.

The exceptionally tight diesel market at home and abroad is unlikely to ease any time soon, considering the post-COVID demand from industry and for leisure and travel, as well as the reduced supply of diesel, other fuels, and crude oil from Russia following the invasion of Ukraine and the bans on Russian imports or self-sanctioning of buyers in the West to buy Russian energy goods.

On the East Coast, inventories are at their lowest ever, as the refinery capacity in the region has halved over the past decade to just 818,000 barrels per day now.

So, instead of focusing on boosting the production of gasoline in the summer driving season, this year U.S. refiners could be looking to raise diesel and jet fuel runs, as the global market of distillates is very tight following the Russian war in Ukraine and supports high refinery margins for those products.

U.S. inventories are “very, very tight, especially tight for diesel,” Gary Simmons, Executive Vice President and Chief Commercial Officer at Valero Energy, said on the Q1 earnings call at the end of April.

Valero Energy saw its highest-ever March refining margins this year, led by diesel, Simmons added.

The global diesel crunch is expected to worsen if the EU reaches some kind of a compromise on banning Russian crude and oil product imports. This will keep diesel prices elevated, impacting every economic activity in the U.S. and elsewhere, and ultimately hitting consumers.

Currently, diesel at New York harbor is trading at around $5 per gallon, which is well above $200 per barrel, Tom Kloza, head of global energy research at OPIS, told CNBC’s Pippa Stevens.

“These are numbers that are not just off the charts. They’re off the walls, out of the building, and maybe out of the solar system,” Kloza told CNBC.

END

Major Trucking Firms Prepare For “Imminent Diesel Shortage In Eastern Half Of US”

BY TYLER DURDEN

WEDNESDAY, MAY 11, 2022 – 03:07 PM

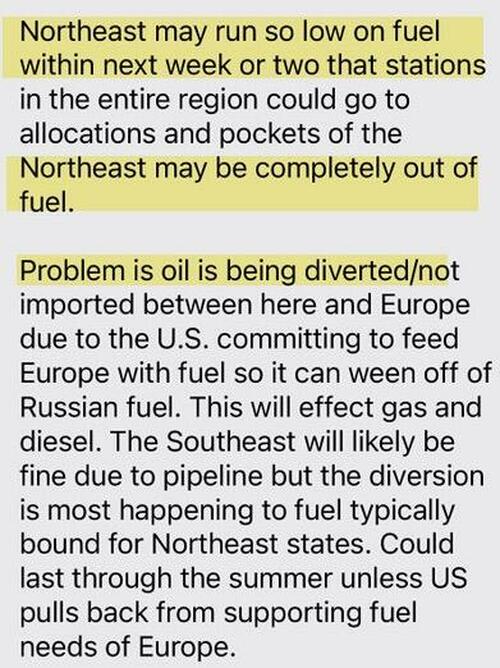

Major trucking fleets across the eastern half of the US are preparing for an “imminent” diesel shortage, according to logistics firm FreightWaves.

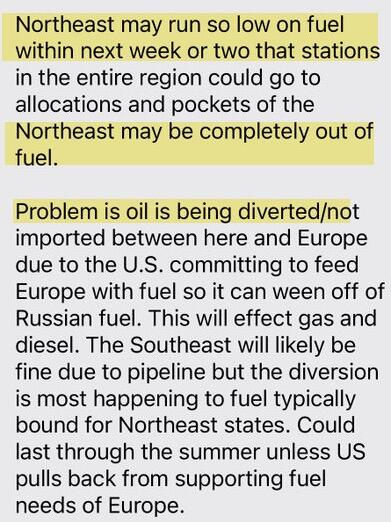

Founder and CEO of FreightWaves Craig Fuller said “3 very large fleets” are preparing for diesel pumps at fuel stations to run dry. Drivers of these fleets received notifications about fuel shortages that could materialize in the coming weeks across the Mid-Atlantic and Northeast regions.

Fuller tweeted several messages that drivers received from fleet operators. The notifications were alarming.

He also tweeted what appears to be an unnamed industry insider explaining the historic mess hitting Mid-Atlantic and Northeast markets is a combination of crude being diverted from the US to Europe and supply chains issues along the East Coast.

Diesel supply is short worldwide due to the invasion of Ukraine disrupting energy markets and resulting Western sanctions. The writing has been on the wall for months about developing shortages, as we discussed in:

- Global Diesel Shortage Raises Risk Of Even Greater Oil Price Spike

- “Gas Stations Will Run Dry”: Catastrophic Scenario For Diesel Emerging According To World’s Biggest Energy Traders

- D-Day Approaches: Crack Spread Soars As Diesel Market Braces For Historic Shock

- US East Coast Diesel Stockpiles Hit Record Low As Fuel Crisis Nears

- Widespread US Diesel Shortages Send Crack Spreads To Mindblowing Highs

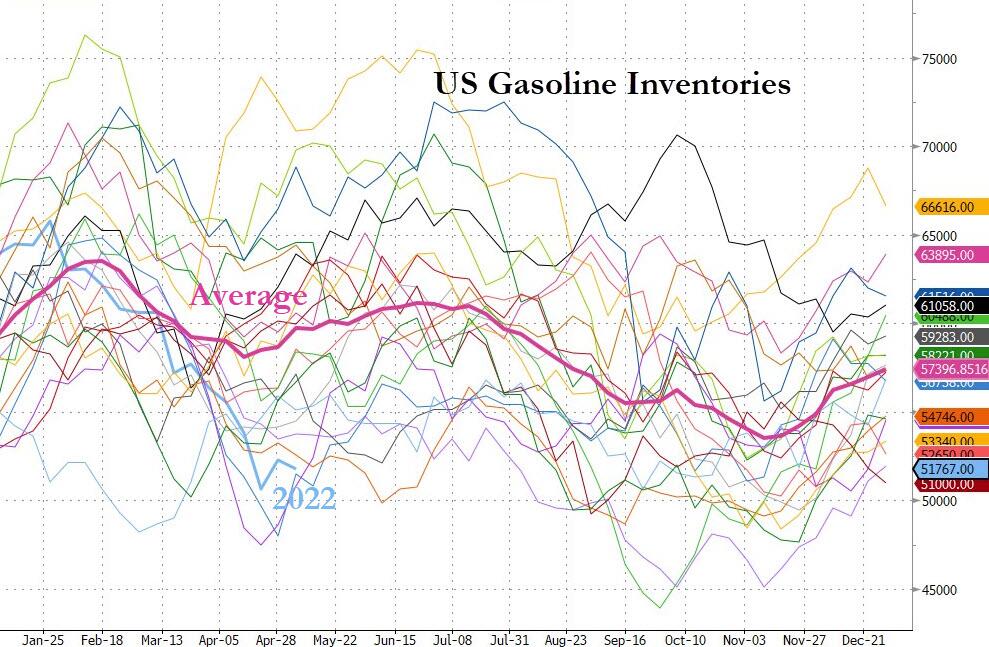

On Wednesday, DOE showed US diesel inventories are now 23% below the five-year average for this time of year, at their lowest since May 2005.

The situation isn’t improving as diesel prices at the pump soar to new highs.

Retail gas prices are also legging higher.

And who does President Biden blame this time for possible fuel shortages? Can’t keep blaming Putin for every problem.

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.7179

OFFSHORE YUAN: 6.7263

HANG SANG CLOSED UP 190.88 PTS OR 0.97%

2. Nikkei closed UP 46.54 OR 0.18%

3. Europe stocks ALL CLOSED ALL GREEN

USA dollar INDEX UP TO 103.62/Euro RISES TO 1.0547

3b Japan 10 YR bond yield: RISES TO. +.247/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 129.95/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN -SHORE CLOSED UP// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +1.044%/Italian 10 Yr bond yield FALLS to 3.06% /SPAIN 10 YR BOND YIELD FALLS TO 2.19%…

3i Greek 10 year bond yield FALLS TO 3.41

3j Gold at $1852.40 silver at: 21.77 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

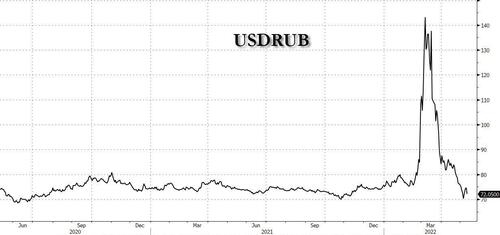

3k USA vs Russian rouble;// Russian rouble UP 1 3/8 roubles/dollar; ROUBLE AT 68.03

3m oil into the 103 dollar handle for WTI and 106 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 129.77 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9998– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0437well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.930 DOWN 6 BASIS PTS

USA 30 YR BOND YIELD: 3.085 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 15.34

Futures, Bonds Rise Ahead Of Critical CPI Print As Chinese Covid Fears Fade

WEDNESDAY, MAY 11, 2022 – 07:52 AM

US index futures and European stocks were set to extend their recovery from the longest streak of weekly declines since 2011 ahead of an inflation report that was expected to show prices cooled in April, while falling bond yields supported battered tech stocks; Asian equities also advanced, halting a seven-day slide, as new Covid cases tumbled in Shanghai with the local government saying there was basically no COVID community spread in 8 of 16 districts, and the Chinese covid scare appears set to fade.

S&P 500 futures were trading at session highs, up 1.2%, and Nasdaq 100 futures were up 1.4%, while Europe’s Stoxx 600 climbed for a second day. The dollar fell and Treasury yields slumped, with the 10Y trading a 2.91%, a 30 basis points slide in the past three days, providing further support for high duration tech names. US-listed Chinese stocks rallied in New York premarket trading after the Asian nation reported easing Covid cases. Tech stocks also climbed in Hong Kong and Europe on Wednesday.

In less than an hour, investors will be analyzing the latest US consumer price index reading, due out at 830am ET, which is expected to show price gains moderated in April, for clues on the Federal Reserve’s pace of monetary tightening (full preview here).

“A soft inflation read will come as a relief that the Fed doesn’t need to get much more aggressive to bring inflation back towards its 2% policy target,” said Swissquote Bank’s Ipek Ozkardeskaya. “If however, inflation hasn’t pulled lower as expected — and worse, if we see a higher figure than last month print — we would see another big wave of selloff.”

The “bar is low” for a surprise from the US data amid ebbing consumer sentiment, according to Brent Schutte, chief investment strategist at Northwestern Mutual Life Insurance Co. “Things are going to be just a bit better at the margin,” he said. “The Fed overall is going to tighten less. That will lead to a market that begins to find its feet and move higher in coming quarters as inflation does come off the boil.”

Technology shares have been leading the selloff as higher interest rates mean a bigger discount for the present value of future profits, hurting frothy growth stocks that have been among the past years’ best performers. Even though the Nasdaq 100 rose yesterday, it was trading near its November 2020 low and is down 24% this year.

In premarket trading, Coinbase shares plunged as much as 18% after posting revenue for the first quarter that fell short of estimates. Occidental Petroleum shares were up after adjusted earnings per share for the first quarter beat the average analyst estimate. US-listed Chinese stocks gained as declining Covid cases in Shanghai lifted hopes for a ease in lockdown measures, boosting risk appetite. Embark Technology shares jumped 31% in US premarket trading, after the self-driving truckmaker reported a smaller net loss per share for the first quarter, with KeyBanc saying the firm is seeing “steady progress.”

Here are the biggest premarket movers today:

- Occidental (OXY US) shares rise 1.7% in US premarket after adjusted earnings per share for the 1Q beat the average analyst estimate. The company demonstrated its ability to deleverage its balance sheet, analysts said

- Chinese stocks rose in premarket trading as declining Covid cases in Shanghai lift hopes for an ease in lockdown measures, boosting risk appetite. Alibaba (BABA US) was up 2.7%, JD.com (JD US) +2.5%, Pinduoduo (PDD US) +2.9% and Baidu (BIDU US) +3.6%.

- Embark Technology (EMBK US) shares jump as much as 31% in premarket, after the company reported a smaller net loss per share for the 1Q, with KeyBanc saying the firm is seeing “steady progress”

- Exicure (XCUR US) shares rise 48% in US premarket after the early-stage biotechnology company announced a $5m sale of common stock in a private placement at a premium to the last close

- Peloton (PTON US) shares up 3.3% premarket after closing at its lowest level since going public in September 2019. Analysts slash price targets as they expect the turnaround process to take time, but they maintained their recommendations on the stock

- Unity Software (U US) shares slump as much as 30% in U.S. premarket trading, after the 3D game-development company reported its 1Q results and gave a 2Q revenue forecast that was weaker than expected

- View (VIEW US) shares tumble 54% in premarket trading after the company delayed its 10-Q filing and said it expects to disclose substantial doubt about its ability to continue as a going concern

- Coinbase (COIN US) shares plunged as much as 18% in premarket after posting worse-than-expected revenue for the 1Q, with analysts pointing to drops in crypto prices impacting the firm’s earnings and outlook

- Roblox (RBLX US) shares were down 1.6% in premarket as its user growth in North America was slightly negative for the second straight quarter, KeyBanc analyst Tyler Parker says, adding that he continues to see significant growth internationally

Despite the gains, sentiment remains fragile as investors seek evidence that price pressures are peaking in the global economy. US data later Wednesday may show inflation moderated in April but stayed above 8%. Traders will use this information to weigh whether the Fed can continue with its half-point hikes as expected or will need to opt for a three-quarter-point increase (or reverse hiking once the US slides into recession). In other words, there’s a lot riding on the inflation figure, Esty Dwek, CIO at Flowbank SA, said in an interview with Bloomberg TV. Still, “the Fed is going to need to see a number of months of lower inflation before they start to even consider taking their foot of the pedal.”

In Europe, the Stoxx 600 Index was 1.2% higher, with consumer products and mining stocks leading the gains. The CAC outperforms, rising as much as 2% back to Monday’s best levels. Health care stocks underperformed as Roche Holding slumped as its cancer medicine billed as a potential blockbuster failed in a study on patients with the most common form of lung cancer. Here are some of the biggest European movers today:

- Compass shares gain as much as 12% after the catering company reported 1H results that beat estimates, increased its FY revenue forecast and announced a buyback.

- European tobacco stocks rise after Philip Morris offered to buysmokeless tobacco company Swedish Match in a $16b transaction. Swedish Match +9%, Imperial Brands +1.3%, BAT +1%

- European luxury stocks outperform as investors anticipate improving demand from easing virus cases in China.

- Kering +3.4%, Hermes +2.8%, Swatch +5.1%

- Pirelli gains as much as 3.6% in Milan trading after posting what Deutsche Bank called a “good” 1Q with a very strong price/mix.

- HomeServe rises as much as 14% amid a Bloomberg report that Brookfield Asset Management is near a $5 billion deal for the emergency household repairs provider.

- Roche falls as much as 7.2% on news that the Skyscraper-01 trial for the lung cancer drug tiragolumab missed co-primary endpoints.

- Bayer slides as much as 7.6% after the Biden administration recommended the US Supreme Court reject a California Roundup appeal.

- Alstom declines as much as 11% to erase gains made earlier in the session after full-year results.

- K+S falls as much as 7% after the potash producer’s 1Q free cash flow was hit by cash out on CO2 certificates, and negative factoring effect, Baader says.

Earlier in the session, Asian equities advanced, halting a seven-day slide, as new Covid cases fell in Shanghai and global appetite for risk improved. The MSCI Asia Pacific Index rallied 0.4% as tech giants Tencent and Alibaba climbed alongside consumer discretionary shares. China’s CSI 300 Index led gains in the region after Shanghai reported fewer daily infections Tuesday and zero cases found in the community. Shanghai Reports No Community Spread as Infections Halve Asia’s benchmark is set to end its longest losing streak since March 2020. The gauge has lost more than $2 trillion in value since a January peak, amid concerns over China’s Covid-Zero stance, inflation and U.S. interest rates. “Asia and EM equities are entering the late stages of a bear market that has traversed valuation, regulation, geopolitics and supply chain pressures,” Morgan Stanley strategists including Jonathan Garner wrote in a report. The firm prefers Japanese shares, due to their return ratios, and Southeast Asian stocks that benefit from higher inflation. Asia’s equity gauge reversed a 0.5% loss as investors awaited the release of U.S. consumer-price index data due later today. Benchmarks in the Philippines and Singapore were among the worst performers in the region.

India’s key equity gauges declined for a fourth day as quarterly earnings showed surging inflation eroding profit growth of top companies. The S&P BSE Sensex fell 0.5% to 54,088.39 in Mumbai to stretch its 4-day decline to 2.9%. The NSE Nifty 50 Index lost 0.5% on Wednesday. The key gauges have declined in all but one session this month. Fifteen of the 19 sector sub-indexes compiled by BSE Ltd. retreated, led by gauges of capital goods and information technology stocks. Of the 28 Nifty 50 companies that have announced results so far, 11 missed estimates and 17 matched. Cipla and Asian Paints were the latest to report profits below the consensus view after market hours on Tuesday.

“Lack of fresh positive cues is forcing investors to dump equities and switch to safer havens like gold,” according to Shrikant Chouhan, an analyst with Kotak Securities. He expects a sharp pullback in key indexes as they are already trading in oversold territory and sees 16,000 as a key support level for the Nifty 50 index. Infosys contributed the most to Sensex’s decline, decreasing by 1.7%. Out of 30 shares in the Sensex index, nine rose and 21 fell.

In FX, the Bloomberg Dollar Spot Index fell after trading near a recent two-year high as the greenback weakened against all of its Group-of-10 peers. Risk-sensitive Scandinavian and Antipodean currencies led gains as traders positioned ahead of the US inflation data. Treasuries rallied, sending yields up to 7bps lower. The euro traded in a narrow range around $1.055 and European bonds rallied, with the periphery outperforming the core. Australian and New Zealand dollars were bought to reduce short positions against the greenback. Australia’s consumer confidence index fell 5.6% from a month ago to 90.4, the lowest since Aug. 2020, according to a report.

In rates, Treasuries rallied for a second day ahead of today’s CPI print and 10Y TSY auction. Yields were richer by as much as 6bp in belly of curve which bull-steepened, and tightened the 2s5s30s fly by 4bp on the day to lowest levels since late March; 10-year yields around 2.925%, outperforming bunds and gilts by 3.5bp and 3bp. The front-end lags with 2-year yields richer by ~3bp on the day, flattening 2s5s, 2s10s spreads by ~3bp. The US auction cycle resumes with $36b 10-year at 1pm ET, following well-bid 3-year Tuesday. WI 10- year yield ~2.92% is above auction stops since late 2018 and ~20bp cheaper than April’s, which tailed the WI by 3bp. In Europe, the fixed income rally also extended with 5y Germany richening ~6bps. Peripheral and semi-core spreads narrow with 10y Bund/BTP near 195bps. Gilts bull-flatten slightly with 2s10s narrowing back near 50bps.

In commodities, Crude futures advanced; WTI rose over 3% and back on to a $102-handle. Base metals are mixed; LME nickel falls 2% while LME copper gains 1.3%. Spot gold rises roughly $13 to trade near $1,851/oz. Bitcoin rises above $31,000.

Bitcoin has stabilised somewhat above the USD 30k mark after the recent bout of stablecoin induced pressure.

Looking to the day ahead now, and the main highlight will be the aforementioned US CPI reading for April. Otherwise, central bank speakers include ECB President Lagarde, as well as the ECB’s Nagel, Vasle, Makhlouf, Knot, Centeno, Muller and Schnabel, and the Fed’s Bostic. Finally, earnings releases include Disney.

Market Snapshot

- S&P 500 futures up 1.2% to 4,047

- STOXX Europe 600 up 0.9% to 423.91

- MXAP up 0.2% to 160.15

- MXAPJ up 0.4% to 525.66

- Nikkei up 0.2% to 26,213.64

- Topix down 0.6% to 1,851.15

- Hang Seng Index up 1.0% to 19,824.57

- Shanghai Composite up 0.8% to 3,058.70

- Sensex down 0.7% to 54,011.37

- Australia S&P/ASX 200 up 0.2% to 7,064.68

- Kospi down 0.2% to 2,592.27

- German 10Y yield little changed at 0.98%

- Euro up 0.2% to $1.0555

- Brent Futures up 2.8% to $105.34/bbl

- Gold spot up 0.5% to $1,847.30

- U.S. Dollar Index down 0.28% to 103.62

Top Overnight News from Bloomberg

- ECB President Christine Lagarde said a first interest-rate increase in more than a decade may follow “weeks” after net bond-buying ends early next quarter, joining a growing crowd of policy makers signaling a move as soon as July

- ECB Governing Council member Joachim Nagel says the exit from very accommodative monetary policy should be “swift enough to affect the price path and to prevent second-round effects and a de- anchoring of inflation expectations”

- ECB Executive Board member Frank Elderson said policy makers can begin looking at raising interest rates from record lows in July, downplaying the risk of a euro-area recession as the war in Ukraine saps growth and fuels already record inflation

- The UK escalated its threats over the post-Brexit deal for Northern Ireland, saying the European Union’s latest proposals on trading arrangements won’t work and signaling it’s prepared to take unilateral steps unless a new agreement can be negotiated

- The EU’s executive arm is set to bolster renewables and energy savings goals as part of a 195 billion-euro ($205 billion) plan to end its dependency on Russian fossil fuels by 2027

- For many of Sweden’s highly indebted consumers, the Riksbank’s sudden interest-rate increase at the end of April marks the start of a new squeeze that officials have long fretted about

- Czech policy maker Ales Michl, a vocal opponent of the central bank’s aggressive campaign to increase interest rates, was appointed to take over as the bank’s governor as the country struggles to contain its worst inflation in almost three decades

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed following the choppy performance on Wall Street. ASX 200 was subdued and briefly fell below the 7,000 level with sentiment dampened by weak Consumer Confidence data. Nikkei 225 swung between gains and losses with the biggest movers driven by recent earnings releases. Hang Seng and Shanghai Comp were both initially lacklustre as property developer Sunac faces its grace period deadline for a dollar bond interest payment and with participants digesting the latest firmer than expected CPI and PPI data from China, although Chinese markets then strengthened amid speculation of policy easing in Q2 and positive signs from the COVID situation in Shanghai.

Top Asian News

- Why China Is Sticking With Its Covid Zero Strategy: QuickTake

- Gray Market Hints at Tepid Trading Debut for Biggest India IPO

- Malaysia Surprises With Rate Hike to Head Off Inflation

- Defense Official Says Curfew May Be Lifted: Sri Lanka Latest

European bourses are firmer across the board, Euro Stoxx 50 +1.4%, with the exception of the SMI -0.2% given the performance of heavyweight Roche, -6.5%. Stateside, futures are bolstered though with gains marginally more contained going into today’s inflation data, ES +1.0%. China April vehicles sales -47.6% YY (-11.7% in March), according to the Industry Association; January-April -12.1% YY (prev. +51.8%). On Tuesday, CPCA says China sold 1.062mln passenger cars were sold in April which was -35.7% Y/Y. China’s Auto Industry Association says the industry’s development situation is gradually improving, firms are seeing May and June as the window to make up for lost sales and production.

Top European News

- Lagarde Joins ECB Officials Signaling July as Liftoff for Rates

- Siemens Energy Slides Amid Mounting Losses at Wind-Turbine Unit

- Ukraine, Russia Gas Clash Raises Threat to Europe’s Supply

- Bayer Drops After Supreme Court Urged to Reject Roundup Appeal

FX

- Greenback grounded in advance of US CPI as Treasury yields recede and curve re-flattens, DXY slips further below 104.00 and sub-103.50 vs fresh 2022 peak at 104.190 on Monday.

- Aussie rebounds with iron ore and other commodities, shrugging off a drop in consumer confidence along the way; AUD/USD back on 0.7000 handle, albeit just and AUD/NZD around 1.1050 even though Kiwi relieved with full NZ reopening at the end of July and NZD/USD rebounds towards 0.6350 in response.

- Franc and Yen appreciate the less bearish bond climate, Euro underpinned as ECB President Lagarde joins others in guiding towards July rate hike; USD/CHF sub-0.9000, USD/JPY under 130.00 and EUR/USD circa 1.0575 at best.

- Loonie and Nokkie boosted by crude recovery, Swedish Crown supported by sharp rise in 1 year CPIF money market expectations; USD/CAD below 1.3000 and closer to hefty option expiry interest at 1.2950 (1.9bln vs 1.7bln at the round number).

- Yuan on firmer footing after stronger than forecast Chinese inflation data, but Czech Koruna floored as President confirms appointment of a known dove to govern CNB; USD/CNH around 6.7400, EUR/CZK near 25.4000.

Fixed Income

- Latest recovery leg in debt lifts Bunds, Gilts and 10 year T-note to new WTD peaks, at 153.61, 119.69 and 119-09+ respectively.

- Solid covers at 10 year German and 7 year UK auctions given recent yield retreat, but some metrics show signs of investor reticence.

- Min focus ahead, US CPI data, but also USD 36bln T-note leg of refunding.

Commodities

- WTI and Brent are bolstered in excess of USD 3.00/bbl in a paring of recent losses alongside a positive turn in China’s COVID situation.

- Currently, WTI Jun resides around USD 103/bbl (vs low USD 98.20/bbl) whilst Brent Jul trades around USD 105.50/bbl (vs low USD 101.30/bbl)

- US Energy Inventory Data (bbls): Crude +1.6mln (exp. -0.5mln), Gasoline +0.8mln (exp. -1.6mln), Distillates +0.7mln (exp. -1.3mln), Cushing +0.1mln.

- Libyan PM Bashagha announces the success of efforts to reopen the ports and oil fields in Libya, according to Sky News Arabia.

- Brazilian truck drivers are considering a strike from May 21st to stop a 9% rise in diesel prices by Petrobras, according to Estadão.

- Spot gold and silver are firmer and benefitting from the USD’s continuing pullback to fresh WTD lows, albeit, the yellow metal is steady around USD 1850/oz pre-inflation.

Central Banks

- ECB’s Lagarde says we have not yet precisely defined the notion of “some time”, but I have been very clear that this could mean a period of only a few weeks. After the first rate hike, the normalisation process will be gradual. Judging by the incoming data, my expectation is that the (asset purchase programme) should be concluded early in the third quarter. Click here for analysis

- ECB’s Muller says APP should end early July or a few weeks earlier; rate hike must not be far behind; appropriate for rates to be in positive territory by year-end, moves should be in 25bp increments. Rise in spreads is consistent with the changed ECB policy outlook; current policy is inappropriately easy, given high inflation.

- ECB’s Elderson says they can start considering normalisation of the policy rate in July.

- ECB’s Vasle says that inflation is becoming more broad-based and the policy response must follow the changed circumstances; supports further and faster action.

- Czech President Zeman has appointed Central Bank member Michl as the new governor, as expected; Czech President Zeman says does not wish to see a large decrease in interest rates but does not see a reason for additional increases.

- CBRT cuts its RRR for financing companies until May 13th, will be implemented at 0.00% until this point, according to the Official Gazette.

US Event Calendar

- 07:00: May MBA Mortgage Applications, prior 2.5%

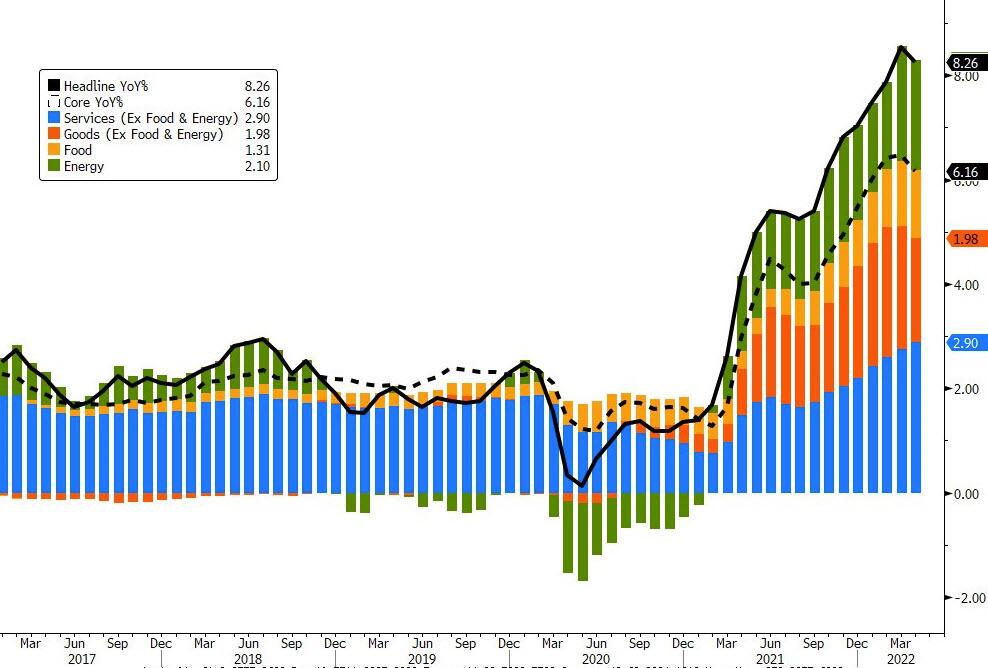

- 08:30: April CPI YoY, est. 8.1%, prior 8.5%

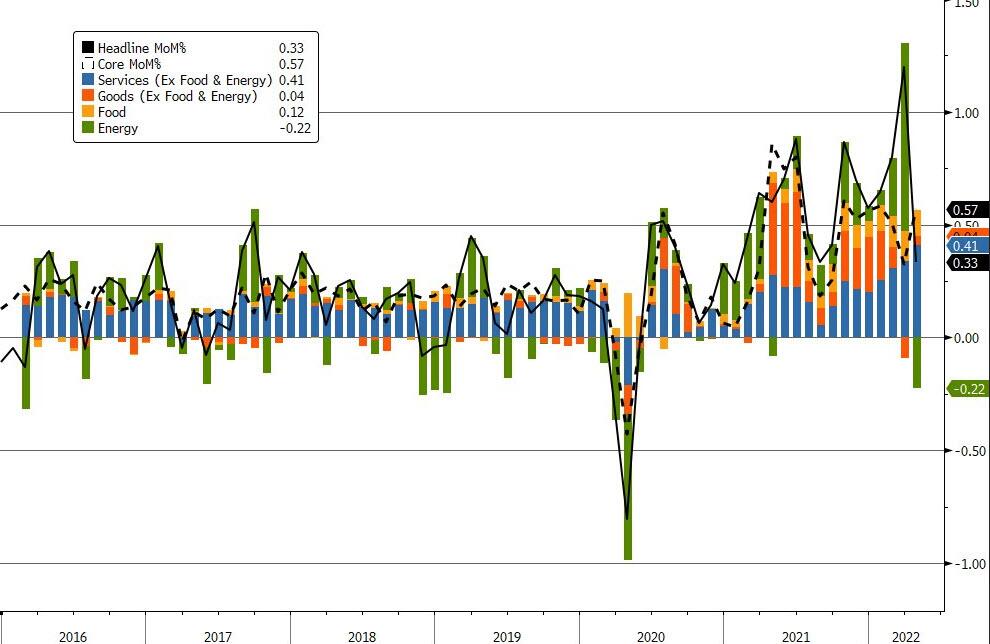

- April CPI MoM, est. 0.2%, prior 1.2%

- April CPI Ex Food and Energy YoY, est. 6.0%, prior 6.5%

- April CPI Ex Food and Energy MoM, est. 0.4%, prior 0.3%

- April Real Avg Hourly Earning YoY, prior -2.7%, revised -2.6%

- April Real Avg Weekly Earnings YoY, prior -3.6%, revised -3.5%

- 14:00: April Monthly Budget Statement, est. $220b, prior – $225.6b

DB’s Jim Reid concludes the overnight wrap

Markets have begun to stabilise over the last 24 hours following Monday’s rout, but there’s no doubt that risk appetite is still very subdued as worries about a potential recession gather pace. The S&P 500 eventually managed to post its first gain in 4 sessions (+0.24%) but only after spending half the day in the red. Today we get the all important US CPI report for April. This will be a very important one for markets and the Fed, since although policymakers have strongly signalled that they’re inclined to continue hiking by 50bps at the next couple of meetings, there is still 25/50/75bps to play for after those meetings. Today’s report will help shape the early read into this and has an ability to move markets in a large manner if diverging from consensus too far.

On that theme, we heard from an array of Fed speakers yesterday. The main takeaway was that +50bp hikes for the next few meetings is the preferred path, while at the margins the door was opened to consider larger hikes after that. For instance, Cleveland Fed President Mester (a voter this year) said that 75bps increases couldn’t be ruled out forever, and that the Fed could have to speed up in H2 if inflation didn’t ease, which coincided with the move into the red for US equities. Discussing another tool to help speed up that fight, she also noted the Fed could start selling asset holdings instead of letting them mature on their own which is currently the base case. Elsewhere Atlanta Fed President Bostic left the door open, saying that “everything is on the table”, but reinforced +50bp hikes were his preference for the next two or three meetings. Separately, New York Fed President Williams openly discussed the prospect that unemployment could rise as part of the Fed’s “soft landing”, saying that he “would not define a soft landing as unemployment staying at 3.6%”. He also mirrored the tone from Fed Chair Powell last week, who referred to a “softish” landing, which is certainly implying it might not be quite as smooth as they’d like in an ideal world, and speaks to the growing risks on the horizon.

Elsewhere on inflation, President Biden gave a speech on this hot topic, saying his administration is weighing whether to cut tariffs which have been in place since the Trump Presidency in order to help fight rising prices, but no decisions have been made.

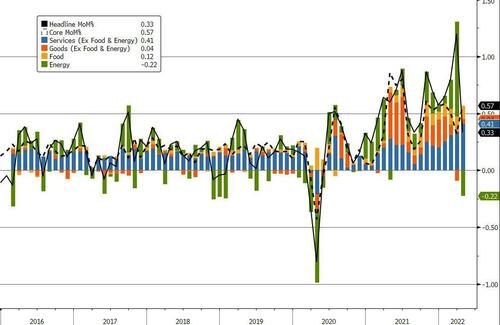

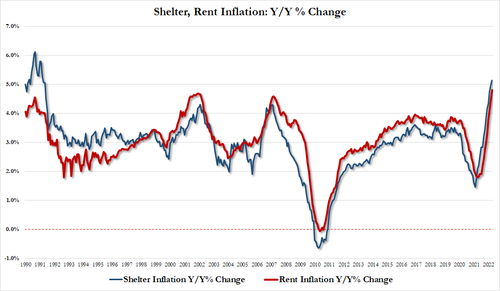

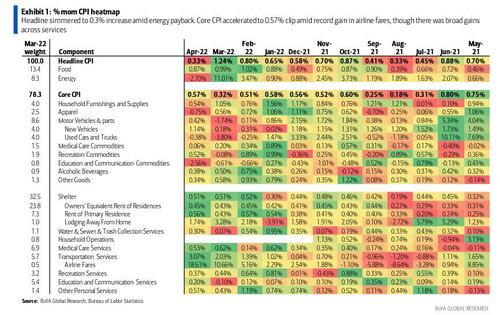

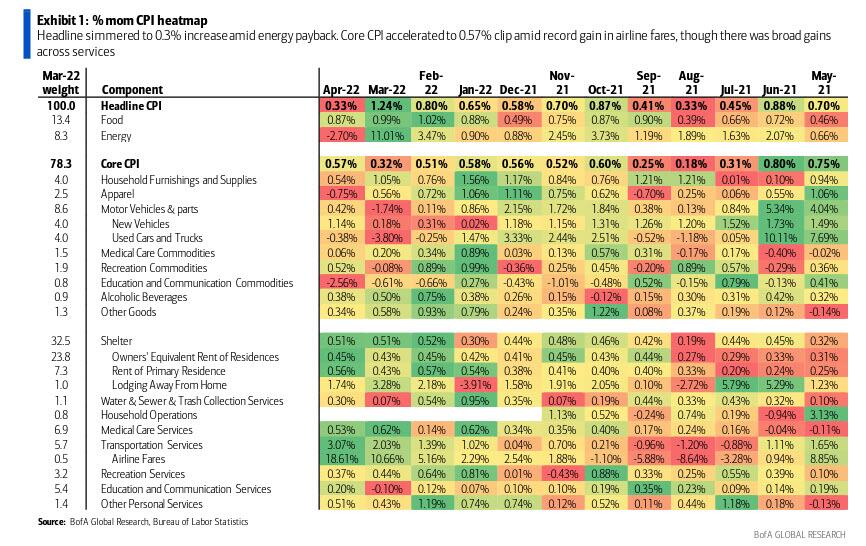

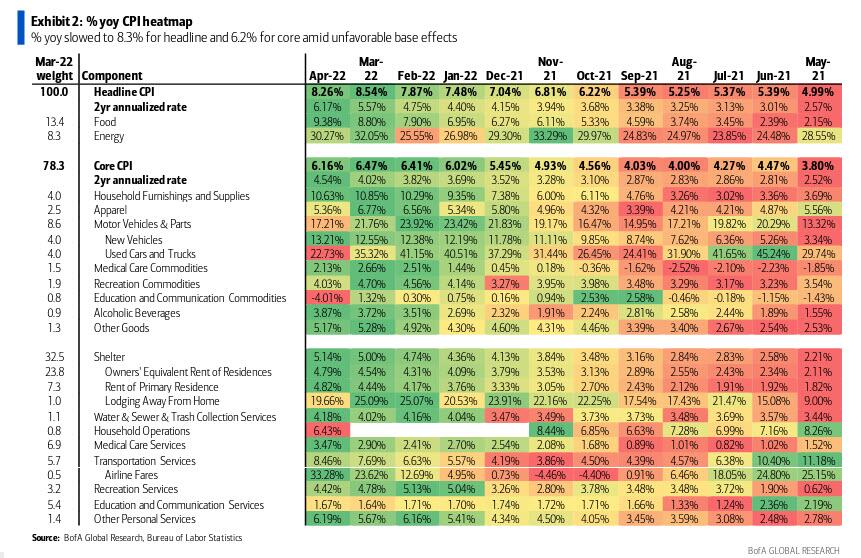

So against that backdrop, all attention will shift over to the US CPI report for April today. Back in March, the year-on-year measure rose to a 4-decade high of +8.5%, but our US economists write in their preview (link here) that’s likely to have been the peak in the year-on-year measure, with today’s reading marking the start of a gradual move lower over the coming months. They see the year-on-year measure coming in at +7.9% as base effects from last year’s surge in used car prices begin to roll off. Meanwhile they see the month-on-month measure at just +0.05% thanks to modest declines in gasoline prices after their near 20% run-up in March. It’ll be important to keep an eye on whether inflationary pressures remain broad-based, so the housing components like rent will be ones to watch.

As discussed at the top, US equities stabilised ahead of the print, with the S&P 500 gaining +0.24%, thus bringing its YTD decline to -16.05%. However, tech stocks outperformed thanks to a decline in yields, with the NASDAQ (+0.98%) and the FANG+ index (+1.42%) seeing bigger gains. And Europe also put in a stronger performance, with the STOXX 600 up +0.68% to end a run of 4 consecutive daily declines.

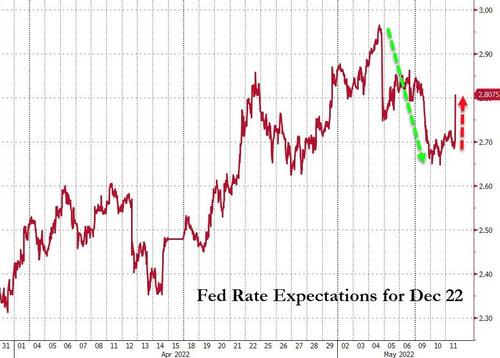

For sovereign bonds it was a different story for the most part, as the prospect of a recession brought down inflation expectations and led to a decline in yields across multiple countries. Yields on 10yr Treasuries were down -4.3bps on the day to 2.99%, whilst those on 10yr bunds (-9.5bps), OATs (-9.9bps) and BTPs (-15.0bps) all saw sizeable moves lower as well, in spite of Bundesbank President Nagel’s endorsement of a July rate hike from the ECB. The main exception were front-end Treasury yields, with the 2yr yield ticking up by +1.2bps in light of the renewed chatter around 75bp hikes this cycle and a slightly more risk on day. This shift was also reflected in Fed funds futures, where the rate priced in by the December meeting rose +3.5bps yesterday, paring back a small amount of the -15.5bps decline on Monday.

Overnight in Asia, major stock markets are mostly higher, with the Shanghai Composite (+1.63%) and the Hang Seng (+1.78%) racing ahead of the Nikkei (+0.44%) and the KOSPI (-0.05%). Chinese markets got a boost after Shanghai reported zero community cases and a halving of new infections. Optimism on covid powered stocks despite upside beats on both the CPI (2.1% vs 1.8% expected) and the PPI (8.0% vs 7.8% expected) overnight. Elsewhere, S&P 500 futures (+0.37%) are also in the green and the US 10y yield (-0.4bps) is edging lower.

Oil has been volatile over the last 24 hours. Brent crude came down a further -3.28% yesterday, which means that it had lost just under $10/bbl over the two days so far this week whilst WTI (-3.23%) slipped back beneath $100/bbl. However this morning the two contracts are back up +2.85% and +1.75% respectively. The EU are continuing to work on further sanctions, and French President Macron spoke about energy security yesterday with Hungarian PM Orban, whose government have been resistant to stronger energy sanctions on Russia.

Here in the UK, we had the State Opening of Parliament yesterday where the government outlined its legislative agenda. One potential area to watch out for is on the Brexit side, since there have been reports that legislation will be proposed that overrides parts of the Northern Ireland Protocol, which is the part of the Brexit deal that avoids a hard border between Northern Ireland and the Republic of Ireland, but instead puts an economic border in the Irish Sea between Great Britain and Northern Ireland. The government’s own explanatory notes to the Queen’s Speech yesterday said that “the Protocol needs to change”, but there was a distinctly lukewarm reaction from the EU to this prospect, with Commission Vice President Šefčovič saying in a statement that “Unilateral action by the UK would only make our work on possible solutions more difficult” and that “renegotiation is not an option”.

On the data side, Germany’s ZEW survey for May saw the expectations indicator unexpectedly rise to -34.3 (vs. -43.5 expected), up from its 2-year low in April. However, the current situation measure fell by more than expected to -36.5 (vs. -35.0 expected), reaching its lowest level in a year. Elsewhere, Italian industrial production was unchanged in March (vs. -1.5% expected).

To the day ahead now, and the main highlight will be the aforementioned US CPI reading for April. Otherwise, central bank speakers include ECB President Lagarde, as well as the ECB’s Nagel, Vasle, Makhlouf, Knot, Centeno, Muller and Schnabel, and the Fed’s Bostic. Finally, earnings releases include Disney.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 22,86 PTS OR 0.75% //Hang Sang CLOSED UP 190.88 PTS OR 0.97% /The Nikkei closed UP 46.54 OR 0.18% //Australia’s all ordinaires CLOSED UP 0.26% /Chinese yuan (ONSHORE) closed up 6,7179 /Oil UP TO 103.92 dollars per barrel for WTI and down TO 106.85 for Brent. Stocks in Europe OPENED ALL green // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7179 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7268: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER//

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

END

3B JAPAN

3c CHINA

COVID/SHANGHAI/LOCKDOWNS

Gordon Johnson: Tesla’s April Sales In China “Implode”, Fall 98% Sequentially, Despite Musk’s Comments To The Contrary

WEDNESDAY, MAY 11, 2022 – 11:50 AM

In Gordon Johnson’s latest note to clients, he reminds them that on Tesla’s April 21, 2022 conference call, Elon Musk said that Q2 production at Shanghai would be “roughly on par” with 1Q22, and “possible” to “be slightly higher”.

“Given TSLA has said it’s capacity constrained and sold out, this was also implicit sales guidance,” Johnson wrote.

In his note, Johnson takes exception with the media, who in his opinion seem to be making excuses for Tesla’s -98% sequential decline in April sales from China (versus a -41% decline in the overall BEV market for China).

However, the notion that these numbers were somehow “expected” stands at stark odds with what Elon Musk himself was saying leading into the end of April, Johnson says.

Johnson also claims that another shut down means that Elon Musk’s guidance for the quarter is likely incorrect:

“In addition to the above, when considering, as we warned weeks ago (due to parts shortages), TSLA’s Shanghai plant was shut down again (YES, YOU HEARD THAT RIGHT) – link – it seems nearly certain production (and, by default, sales) at the Shanghai plant will NOT be flat-to-up QoQ as E. Musk guided less than a month ago.