May 25, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

May 25, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1846.90 UP $2.70 from Friday

SILVER: $21.89 UP $.20 FROM FRIDAY

ACCESS MARKET: GOLD $1853.60

SILVER: $22.06

Bitcoin morning price: $29,499 UP 495 up from Saturday

Bitcoin: afternoon price: $29,705 up $701.00

Platinum price: closing DOWN $1.65 to $949.20

Palladium price; closing UP $39.15 at $1998.30

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX 2/260

EXCHANGE: COMEX

CONTRACT: MAY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,865.100000000 USD

INTENT DATE: 05/24/2022 DELIVERY DATE: 05/26/2022

FIRM ORG FIRM NAME ISSUED STOPPED

661 C JP MORGAN 2

737 C ADVANTAGE 1

905 C ADM 1

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT 2 NOTICE(S) FOR 200 OZ (0.00622 TONNES)

total notices so far: 6431 contracts for 643100 oz (20.003 tonnes)

SILVER NOTICES:

58 NOTICE(S) FILED 290,000 OZ/

total number of notices filed so far this month 5524 : for 27,624,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $2.70

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A HUGE DEPOSIT OF 11.89 TONNES INTO THE GLD

INVENTORY RESTS AT 1068.07 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 20 CENTS

AT THE SLV// A BIG CHANGE IN SILVER INVENTORY AT THE SLV://A HUGE CHANGE IN SILVER INVENTORY

AT THE SLV.: A WITHDRAWAL OF 0.922 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 561.586 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A SMALL SIZED 590 CONTRACTS TO 146,456 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GOOD GAIN IN OI WAS ACCOMPLISHED DESPITE OUR $0.20 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.20) BUT ALSO UNSUCCESSFUL IN KNOCKING OFF ANY SILVER LONGS AS THEY REMAIN FIRM IN THEIR BELIEF OF A SILVER FAILURE AS WE HAD A NET GAIN OF 1239 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 30.170 MILLION OZ FOLLOWED BY TODAY’S 70,000 OZ E.F.P. JUMP //NEW STANDING 28,245,000 MILLION OZ/ // V) STRONG SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : XX

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTACTS for 17 days, total 20,247, contracts: 101.235 million oz OR 5.953 MILLION OZ PER DAY. (1191CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 101.236 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 101.236 MILLION OZ//INCREASING AGAIN

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 590 DESPITE OUR $0.34 GAIN IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 125 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAY. OF 30.170 MILLION OZ FOLLOWED BY TODAY;S 20,000 OZ E.F.P.. JUMP //NEW STANDING 28.245 MILLION OZ// .. WE HAD A FAIR SIZED LOSS OF 465 OI CONTRACTS ON THE TWO EXCHANGES FOR 2.325 MILLION OZ DESPITE THE GAIN IN PRICE.

WE HAD 58 NOTICE FILED TODAY FOR 290,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 9936 CONTRACTS TO 530.098 AND FURTHER FROM NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: –XX CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE STRONG SIZED LOSS IN COMEX OI CAME DESPITE OUR GAIN IN PRICE OF $17.80//COMEX GOLD TRADING/TUESDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR GIGANTIC SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //JUST SPECULATOR SHORT COVERING FROM OUR STUPID SPECULATORS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 5.353 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY”S QUEUE JUMP OF 1900 OZ//NEW STANDING 20.111 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $7.75 WITH RESPECT TO FRIDAY’S TRADING

WE HAD A FAIR SIZED LOSS OF 3437 OI CONTRACTS (10.69 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6499 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 542,509

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3437, WITH 9936 CONTRACTS DECREASED AT THE COMEX AND 13437 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 3437 CONTRACTS OR 10.69 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (16499) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (9936,): TOTAL LOSS IN THE TWO EXCHANGES 3437 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY. AT 5.353 TONNES FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 1900 OZ//NEW STANDING 20.11 /// 3) ZERO LONG LIQUIDATION//CONSIDERABLE SPECULATOR SHORT COVERING //.,4) FAIR SIZED COMEX OI. LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

75,378 CONTRACTS OR 7,537,800 OR 206.87 TONNES 17 TRADING DAY(S) AND THUS AVERAGING: 4434 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES: 234.45 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 206.87/3550 x 100% TONNES 5.80% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 234,45 TONNES INITIAL// INCREASING AGAIN

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A SMALL SIZED 590 CONTRACT OI TO 146.456 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 125 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 125 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 119 CONTRACTS AND ADD TO THE 125 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A FAIR SIZED GAIN OF465 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 2.325 MILLION OZ

OCCURRED DESPITE OUR GAIN IN PRICE OF $0.34 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

Government is not competent enough to suppress gold price accord to Rick Rule formerly of Sprott

(Rick Rule/Chris Powell)

Government isn’t competent enough to suppress gold price, Rick Rule tells Kitco

Submitted by admin on Wed, 2022-05-25 01:08Section: Daily Dispatches

1:22a ET Wednesday, May 25, 2022

Dear Friend of GATA and Gold:

Investment analyst Rick Rule, interviewed yesterday at the Vancouver Resource Investment Conference by Kitco News editor Michelle Makori, acknowledged that the gold futures market is “ripe for manipulation” but dismissed complaints that government has undertaken any schemes to suppress the price of the monetary metal.

“The idea that there is some vast conspiracy between government and central banks and the Trilateral Commission to suppress the price of gold when history has depressed the price of gold seems silly to me,” Rule said. “The government can’t deliver the mail, they can’t educate the kids, and they can preside over a 40-year manipulation of the gold price? I don’t reckon.”

If Makori had wanted to attempt journalism at this point, she might have asked Rule about a few of the documents of longstanding government gold price suppression policy that are compiled by GATA here:

Instead Makori let Rule get away with his demagoguery about the Trilateral Commission, which as far as GATA can tell has never been mentioned in regard to complaints about gold price suppression, even as Rule failed to mention the Bank for International Settlements, the gold broker and gold market intervenor for major central banks.

Neither did Makori challenge Rule for his non-sequitur — that since government is incompetent with certain things it must be incompetent with all things. That also is demagoguery, which Rule may have picked up years ago from market analyst Doug Casey, someone else who denies government gold price suppression policy but has never taken a moment to examine and address the documents or to put a critical question to governments and central banks.

Yes, the U.S. government has had trouble getting the U.S. Postal Service to be self-supporting, and yes, U.S. education long has been in decline. But government almost everywhere long has been extremely proficient at extracting wealth from the people over whom it rules and restricting their freedom. Government also can be pretty good at blowing things up, which Rule might begin to appreciate if he ever finds himself at the wrong end of a Stinger or Javelin missile.

Makori did note to Rule her interview three weeks ago with mining and entertainment entrepreneur Frank Giustra, who said he suspects that gold prices are manipulated by the Federal Reserve, to which Rule replied that he would be willing to debate Giustra on the issue.

In preparation for such a debate GATA would be happy to brief Giustra on the documents, and happier still to debate Rule directly.

If Makori ever wants to attempt journalism, GATA would be glad to brief her on the documents and help her frame some pointed questions for the Fed, Treasury Department, BIS. Bank of England, Commodity Futures Trading Commission, futures exchange operator CME Group, and a few bullion banks.

Of course that might be the last journalism Makori would ever attempt for Kitco News, but actual journalism often involves risk.

Makori’s interview with Rule is 29 minutes long with the conversation about gold beginning at the 18:27 mark. It can be found here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Gold and silver is still protecting our purchasing power: James Turk

(Turk/GATA)

Gold and silver still protect purchasing power, Turk tells Wall Street Silver

Submitted by admin on Sun, 2022-05-22 21:25Section: Daily Dispatches

9:27p ET Sunday, May 22, 2022

Dear Friend of GATA and Gold:

GoldMoney founder and GATA consultant James Turk, interviewed by Ivan Bayoukhi and Jim Lewis of Wall Street Silver, shows that despite their recent smashings in the futures market, gold and silver long have protected and still are protecting the purchasing power of their owners, especially in regard to the key measure of energy, the price of oil.

Turk’s interview is 14 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

BIS swamps fall by a third in two months; Is Basel 3 kicking in?

Robert Lamborn/GATA

Robert Lambourne: BIS gold swaps fall by a third in two months. Is ‘Basel 3’ kicking in?

Submitted by admin on Sat, 2022-05-21 11:46Section: Daily Dispatches

By Robert Lambourne

Saturday, May 21, 2022

The recently released March and April 2022 statements of account of the Bank for International Settlements —

— contain information suggesting a significant decrease in the bank’s gold swaps.

The March reduction was about 112 tonnes, bringing the swaps down from about 472 tonnes as of February 28 to about 360 tonnes at March 31. There was a reduction of about 45 tonnes in April, bringing the swaps down to 315 tonnes.

These totals compare to the relatively recent record high estimated at 552 tonnes as of February 28, 2021. April’s 315 tonnes is the lowest volume of gold swaps held by the BIS since December 2019.

Altogether the reductions in March and April brought the bank’s gold swaps down by slightly more than a third.

Once again it is evident that the BIS remains an active trader of significant volumes of gold swaps on a regular basis, and the recent data suggests that a downward trend in the bank’s swaps has begun. A continuation of this trend would be indicate that an exit from the swaps due to “Basel III” regulations is happening.

The BIS rarely comments publicly on its gold activities, but its first use of gold swaps was considered important enough to cause the bank to give some background information to the Financial Times for an article published July 29, 2010, coinciding with publication of the bank’s 2009-10 annual report.

The general manager of the BIS at the time, Jaime Caruana, said the gold swaps were “regular commercial activities” for the bank, and he confirmed that they were carried out with commercial banks and so did not involve central banks. It also seems highly likely that the BIS’ remaining swaps are still all made with commercial banks, because the BIS annual report has never disclosed a gold swap between the BIS and a major central bank.

The swap transactions potentially create a mismatch at the BIS, which may end up being long unallocated gold (the gold held in BIS sight accounts at major central banks) and short allocated gold (the gold required to be returned to swap counterparties). This possible mismatch has not been reported by the BIS.

The gold banking activities of the BIS have been a regular part of the services it offers to central banks since the establishment of the bank 90 years ago. The first annual report of the BIS explains these activities in some detail:

http://www.bis.org/publ/arpdf/archive/ar1931_en.pdf

A June 2008 presentation made by the BIS to potential central bank members at its headquarters in Basel, Switzerland, noted that the bank’s services to its members include secret interventions in the gold and foreign exchange markets:

https://www.gata.org/node/11012

The use of gold swaps to take gold held by commercial banks and then deposit it in gold sight accounts held in the name of the BIS at major central banks doesn’t appear ever to have been as large a part of the BIS’ gold banking business as it has been in recent years.

As of March 31, 2010, excluding gold owned by the BIS, there were 1,706 tonnes held in gold sight accounts at major central banks in the name of the BIS, of which 346 tonnes or 20% were sourced from gold swaps from commercial banks.

As can readily be seen, the BIS now operates a much smaller gold banking business, with 736 tonnes of gold deposited in gold sight accounts as of April 30. (This excludes 102 tonnes of the gold owned by the BIS itself.) The present-day role of gold swaps in this smaller business is proportionately far greater.

In April, excluding the 102 tonnes of gold owned by the BIS, some 43% of the gold held in sight accounts at major central banks on behalf of the BIS came from gold swaps rather than from other central banks.

If the BIS was adopting the level of disclosures made by publicly held companies, such as commercial banks, some explanation of these changes probably would have been required by the accounting regulators. This irony may not be lost on those dealing with regulatory activities at the BIS. Presumably the shrinkage of the BIS’ gold banking business shows that even central banks now prefer to hold their own gold or hold it in earmarked form — that is, as allocated gold.

A review of Table B below highlights recent BIS activity with gold swaps, and despite the recent declines, the latest position estimated from the BIS monthly statements remains large and the volume of trades is significant.

No explanation for this continuing high level of swaps has been published by the BIS. Indeed, no comment on the bank’s use of gold swaps has been offered since 2010.

This gold is supplied by bullion banks via the swaps to the BIS. The gold is then deposited in BIS gold sight accounts (unallocated gold accounts) at major central banks such as the Federal Reserve.

The reasons for this activity have never been fully explained by the BIS and various conjectures have been made as to why the BIS is facilitating it. One conjecture is that the swaps are a mechanism for gold secretly supplied by central banks to cover shortfalls in the gold markets to be returned to the central banks. The use of the BIS to facilitate this trade suggests of a desire to conceal the rationale for the transactions.

The BIS’ use of gold swaps and other gold derivatives remains extensive despite the recent declines.

Table B below shows that the BIS continues to trade significant volumes of gold swaps regularly. As can be seen in Table A below, the BIS has used gold swaps extensively since its financial year 2009-10.

No use of swaps is reported in the bank’s annual reports for at least 10 years prior to the year ended March 2010.

The February 2021 estimate of the bank’s gold swaps (552 tonnes) is higher than any level of swaps reported by the BIS at its March year-end since March 2010. The swaps reported at March 2021 are at the highest year-end level reported, as is clear from Table A.

Table A — Swaps reported in BIS annual reports

March 2010: 346 tonnes.

March 2011: 409 tonnes.

March 2012: 355 tonnes.

March 2013: 404 tonnes.

March 2014: 236 tonnes.

March 2015: 47 tonnes.

March 2016: 0 tonnes.

March 2017: 438 tonnes.

March 2018: 361 tonnes.

March 2019: 175 tonnes

March 2020: 326 tonnes

March 2021: 490 tonnes

—–

The table below reports the estimated swap levels since August 2018. It can be seen that the BIS is actively involved in trading gold swaps and other gold derivatives with changes from month to month reported in excess of 100 tonnes in this period.

Table B – Swaps estimated by GATA from BIS monthly statements of account

Month ….. Swaps

& year … in tonnes

Apr-22 ….. /315

Mar-22 …. /360

Feb-22 …. /472

Jan-22 ….. /501

Dec-21…. /414

Nov-21…. /451

Oct-21…. /414

Sep-21 …. /438

Aug-21 …. /464

Jul-21 …. /502

Jun-21 …./471

May-21 …./517

Apr-21 …. /472

Mar-21…. /490±

Feb-21 …../552

Jan-21 …. /523

Dec-20 …. /545

Nov-20 …. /520

Oct-20 …. /519

Sep-20…../ 520

Aug-20…../ 484

Jul-20 ….. / 474

Jun-20 …. / 391

May-20 …. / 412

Apr-20 …. / 328

Mar-20 …. / 326*

Feb-20 …. / 326

Jan-20 …. / 320

Dec-19 …. / 313

Nov-19 …. / 250

Oct-19 …. / 186

Sep-19 …. / 128

Aug-19 …. / 162

Jul-19 ….. / 95

Jun-19 …. / 126

May-19 …. / 78

Apr-19 ….. / 88

Mar-19 …. / 175

Feb-19 …. / 303

Jan-19 …. / 247

Dec-18 …. / 275

Nov-18 …. / 308

Oct-18 …. / 372

Sep-18 …. / 238

Aug-18 …. / 370

± The estimate originally reported by GATA was 487 tonnes, but the BIS annual report states 490 tonnes, It is believed that slightly different gold prices account for the difference.

* The estimate originally reported by GATA was 332 tonnes, but the BIS annual report states 326 tonnes. It is believed that slightly different gold prices account for the difference.

GATA uses gold prices quoted by USAGold.com to estimate the level of gold swaps held by the BIS at month-ends.

—–

As noted already, the BIS in recent times has refused to explain its activities in the gold market, nor for whom the bank is acting:

https://www.gata.org/node/17793

Despite this reticence the BIS is almost certainly acting on behalf of central banks in taking out these swaps, as they are the BIS’ owners and control its Board of Directors.

This refusal to explain prompts some observers to believe that the BIS acts as an agent for central banks intervening surreptitiously in the gold and currency markets, providing those central banks with access to gold as well as protection from exposure of their interventions.

A recent report published by Bullion Star’s Ronan Manly on the Bank of Portugal’s use of its gold reserves reinforces this point as the Bank of Portugal confirms that 20 tonnes of its gold is stored with the BIS:

https://www.gata.org/node/21950

This disclosure seems a little economic with the truth as the BIS has no gold storage facilities of its own. Gold held by the BIS on behalf of central banks is either deposited into a BIS gold sight (unallocated) account or a BIS earmarked (allocated) gold account and deposited normally with one of the central banks based at a major gold trading center, such as the Federal Reserve in New York.

Since Manly shows that the Bank of Portugal is focused on earning income from its gold, it seems highly likely that this gold is held in a BIS sight account, though its ultimate location is unclear.

It is possible that the swaps provide a mechanism for bullion banks to return gold originally lent to them by central banks to cover bullion bank shortfalls of gold. Some commentators have suggested that a portion of the gold held by exchange-traded funds and managed by bullion banks is sourced directly from central banks.

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults with GATA about the involvement of the Bank for International Settlements in the gold market.

* * *

end

Rubel rises to 2015 level against euro and dollar as the EU prepares to pay for gas in roubles.

Ruble rises to 2015 level against euro as EU prepares to pay for gas

Submitted by admin on Fri, 2022-05-20 12:29Section: Daily Dispatches

Wonderful sanctions you got there, Boys and Girls.

* * *

From Reuters

Friday, May 20, 2022

The Russian ruble today rallied to its strongest levels against the euro and dollar since June 2015 and March 2018 respectively, which analysts attributed to EU countries preparing to pay Russia for gas and to capital controls imposed by Moscow.

Russia said Thursday that half of gas giant Gazprom’s 54 clients have opened accounts at Gazprombank, as European companies approach imminent deadlines to pay for their gas supplies.

Opening such accounts became possible after EU executives allowed member states to keep buying Russian gas without breaching the slew of sanctions they have collectively imposed on Russia over what Moscow calls its “special military operation” in Ukraine that started on Feb. 24. …

… For the remainder of the report:

https://www.reuters.com/markets/europe/russian-rouble-rallies-past-60-vs-dollar-2022-05-20/

end

5. Other gold commentaries

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 36.54 PTS OR 1.19% //Hang Sang CLOSED UP 59.19 PTS OR 0.26% /The Nikkei closed DOWN 76.34 OR 0.26% //Australia’s all ordinaires CLOSED UP 0.25% /Chinese yuan (ONSHORE) closed DOWN 6,6954 /Oil UP TO 111.09dollars per barrel for WTI and UP TO 114.62 for Brent. Stocks in Europe OPENED ALL MIXED // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6954 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6708: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER/

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 9936 CONTRACTS TO 530,098 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX DECREASE OCCURRED DESPITE OUR GAIN OF $7.75 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A SMALL SIZED EFP (1307 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ARE CAUGHT. THE COMMERCIALS WILL SLAUGHTER THESE GUYS WHEN THEY THINK THE TIME IS RIGHT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF MAY.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 6439 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :6439 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 6439 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3437 CONTRACTS IN THAT 6439 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 9936 CONTRACTS..AND YET THIS STRONG LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF GOLD $7.75.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (20.11),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $17.90) BUT WERE SUCCESSFUL IN KNOCKING OFF SOME SPECULATOR LONGS/COMMERCIAL LONGS AS WELL AS SPECULATOR SHORTS//// WE HAVE REGISTERED A GOOD SIZED LOSS OF 14/86 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAY (20.11 TONNES)…

WE HAD XX CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 3437 CONTRACTS OR 477,900 OZ OR 10.69 TONNES

Estimated gold volume 125,244/// poor

Confirmed volume yesterday:257,307 contracts fair

INITIAL STANDINGS FOR MAY ’22 COMEX GOLD //MAY 25

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 32,115.000 oz JPMORGAN1000 KILOBARS |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | 2066.39 OZ BRINKS |

| No of oz served (contracts) today | 2 notice(s)200 OZ 0.000622 TONNES |

| No of oz to be served (notices) | 35 contracts 3500 oz 0.1088 TONNES |

| Total monthly oz gold served (contracts) so far this month | 6431 notices643,100 OZ 20.003 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit 0 oz//

No dealer withdrawals

1 customer deposits

i) Into Brinks: 2066.39 oz

total deposits: 2066.39 oz

1 customer withdrawals:

i) Out of JPMorgan: 32115.00 oz (1000 kilobars)

total withdrawal: 32115.000 oz

ADJUSTMENTS:

a) JPMorgan 250,266.617 oz customer to dealer

b) Brinks dealer to customer 73,593.642

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 37 contracts having LOST ONLY 402 contracts

We had 421 notices filed YESTERDAY, so we gained 19 contracts or AN ADDITIONAL 1900 oz will stand for delivery in this non active delivery month of May.

June saw a loss of 40,935 contracts down to 184,466 contracts

July has a GAIN OF 606 OI to stand at 1099

August has a gain of 30,512 contracts up to 349,852 contracts

We had 32 notice(s) filed today for 3200 oz FOR THE MAY 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 2 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 2 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2021. contract month,

we take the total number of notices filed so far for the month (6431) x 100 oz , to which we add the difference between the open interest for the front month of (MAY 37 CONTRACTS ) minus the number of notices served upon today 2 x 100 oz per contract equals 6,666,000 OZ OR 20.11 TONNES the number of TONNES standing in this non active month of MAY.

thus the INITIAL standings for gold for the MAY contract month:

No of notices filed so far (6431) x 100 oz+ (xx) OI for the front month minus the number of notices served upon today (2} x 100 oz} which equals 646,600 oz standing OR 20.111 TONNES in this NON active delivery month of MAY.

TOTAL COMEX GOLD STANDING: 20.11 TONNES (A STRONG STANDING FOR A MAY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,060,078.634 oz

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 35,596,492.593 OZ

TOTAL ELIGIBLE GOLD: 18,135.608.203 OZ

TOTAL OF ALL REGISTERED GOLD: 17,640,890.390 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,550,812.0 OZ (REG GOLD- PLEDGED GOLD)

END

MAY 2022 CONTRACT MONTH//SILVER//MAY 25

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 124,139.264 oz CNT |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 6915.605 oz Delaware |

| No of oz served today (contracts) | 58CONTRACT(S) 290,000 OZ) |

| No of oz to be served (notices) | 125 contracts (2,045,000 oz) |

| Total monthly oz silver served (contracts) | 5524 contracts 27,620,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) zero dealer deposits And now for the wild silver comex results

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

i) Into Delaware: 6915.605 oz

total deposit: 6915.605 oz

JPMorgan has a total silver weight: 175.84 million oz/337.779 million =52.16% of comex

Comex withdrawals: 1

i) Out of Brinks 9520.210 oz

ii) Out of CNT: 124,139.264. oz

total withdrawal 124,139.264 oz

2 adjustments: customer to dealer JPMorgan: 205,266.617 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 80.031 MILLION OZ

TOTAL REG + ELIG. 336.970 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY OI: 483 HAVING LOST 295 CONTRACTS. WE HAD 291 NOTICES FILED ON YESTERDAY

SO WE LOST 4 CONTRACTS OR A E.F.P. JUMP TO LONDON OF 20,000 OZ

JUNE HAD A GAIN OF 4 TO STAND AT 1569

JULY HAD A LOSS OF 1769 CONTRACTS UP TO 112,140 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 58 for 290,000 oz

Comex volumes: 14,796// est. volume today// poor

Comex volume: confirmed yesterday: 40,517 contracts ( fair )

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 5524 x 5,000 oz = 27,624,000 oz

to which we add the difference between the open interest for the front month of MAY(x83) and the number of notices served upon today 58 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY./2022 contract month: 5524 (notices served so far) x 5000 oz + OI for front month of MAY (83) – number of notices served upon today (58) x 5000 oz of silver standing for the MAY contract month equates 28,245,000 oz. .

We LOST 4 contracts or AN ADDITIONAL 20,000 OZ will NOT stand for delivery at the comex

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MAY 24/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

MAY 18/WITH GOLD DOWN $2.55//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.07 TONNES FROM THE GLD///INVENTORY RESTS AT 1049.21 TONNES

MAY 17/WITH GOLD UP $5.40:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1053.28 TONNES

MAY 16/WITH GOLD UP $5.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD///INVENTORY RESTS AT 1055.89 TONNES

MAY 13/ WITH GOLD DOWN $16.25//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.8 TONNES FROM THE GLD.//INVENTORY RESTS AT 1060.82 TONNES

MAY 12/WITH GOLD DOWN $26.50: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD////INVENTORY RESTS AT 1066.62 TONNES

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

GLD INVENTORY: 1068.07 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 24/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

MAY 18/WITH SILVER UP $0.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL 1.892 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 17/WITH SILVER UP $.22 TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.508 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 16/WITH SILVER UP $.52 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.546 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.593 MILLION OZ//

MAY 13/WITH SILVER UP 31 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ/

MAY 12/WITH SILVER DOWN 88 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ//

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

INVENTORY TONIGHT RESTS AT 561.486 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

The Air Is Coming Out Of The Housing Bubble

WEDNESDAY, MAY 25, 2022 – 09:25 AM

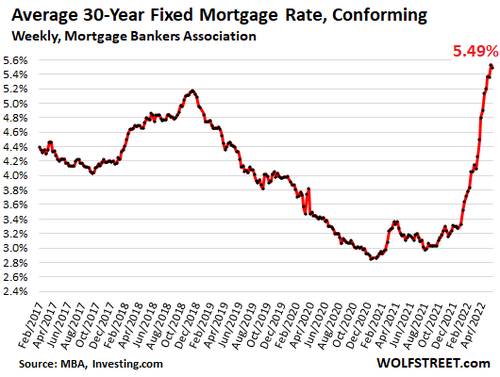

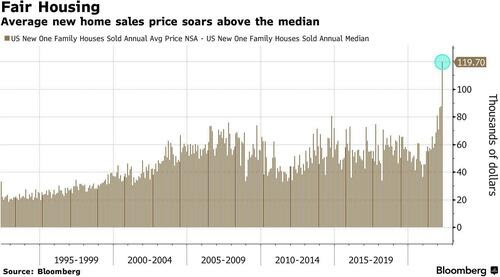

The Fed has barely started raising interest rates but the air is already seeping out of the housing bubble.

New single-family home sales plunged by 16.6% from March and were down 26.9% year on year. New home sales dropped to the lowest level since the lockdown in April 2020.

New home sales are often viewed as a leading indicator of the state of the overall housing market.

The unsold inventory of new homes spiked by 34,000, a historic month-to-month leap. There were 440,000 unsold new homes (seasonally adjusted), the highest level since May 2008 in the midst of the housing bust. Both, the month-to-month and year-over-year increases in unsold new homes were the largest leaps ever recorded, both in numbers of unsold houses and in percentage terms.

The biggest drop in new home sales occurred in the under-$400k price range, indicating that high prices and rising mortgage rates are squeezing middle-class Americans out of the housing market.

WolfStreet broke down the current dynamics in housing.

Homebuyers struggle with spiking mortgage rates which make the high home prices that much more difficult to deal with. And with each increase in mortgage rates, and with each increase in home prices, entire layers of potential buyers abandon the market, and sales volume plunges.”

The Mortgage Bankers Association (MBA) data for April 2022 shows mortgage applications for new home purchases decreased 10.6% compared to a year ago. Compared to March 2022, applications decreased by 14%.

The Federal Reserve blew up this housing bubble when it artificially suppressed interest rates and bought billions of dollars in mortgage-backed securities. Now the central bank has pricked the bubble by allowing rates to rise ever-so-slightly.

What the Fed giveth, the Fed taketh away.

Mortgage rates began to fall in late 2018 as the economy tanked and the Federal Reserve ended its post-2008 rate hike cycle. Rates continued to fall as the Fed pivoted back to quantitative easing and then dropped through the floor with the rate cuts and QE infinity in response to the coronavirus. The big spike in mortgage rates we’re seeing today started as the Fed began talking up monetary tightening to tackle raging inflation.

Tight housing inventory has kept home prices up even as sales have dropped, but as more and more people are squeezed out of the market, prices will likely begin to fall. While we may not see the kind of crash we saw in 2008, a housing market bust will reverberate through the economy as rising housing prices squeeze Americans already struggling to make ends meet.

And as Peter Schiff pointed out in a tweet, falling prices will wipe out home equity for millions of homeowners.

But lower house prices will offer little relief to new buyers, as rising mortgage rates, utilities, taxes, maintenance, and insurance offset the drop.”

Peter Schiff: The Fed Girds For Battle

2.LAWRIE WILLIAMS//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

LAWRIE WILLIAMS: ‘In Gold we Trust’ 2022 released – $4,800 gold by 2030 prediction still intact

Keen gold analysts will be pleased to know that the latest edition of Incrementum AG’s hugely comprehensive ‘In Gold we Trust’ annual treatise has been released and is available for free download in various forms and languages as follows:

English:

In Gold We Trust report – English?(390?pages)

Compact Version – English (26?pages)

https://www.incrementum.li/en/ingoldwetrust- report/

German:

In Gold We Trust-Report – Deutsch (420?Seiten)

Compact Version – Deutsch (26?Seiten)

Spanish:

Compact Version – Spanish (26 Pages)

For the follower of the gold sector this is probably the most comprehensive report on gold freely available to the general public and is packed full of statistics, graphics, tabulations and opinion relevant to all aspects of gold supply and demand together with price projections. It has now been published annually since Ronald-Peter Stöferle prepared its first edition, originally for Austria’s Erste Bank, some 16 years ago and has been one of the most followed annual treatises on the global gold market ever since.

This latest issue, inter alia, takes a detailed view on what the seemingly inexorable move of the global economy into a period of stagflation means for us all, and its likely effects on the equities markets, U.S. Fed policy and the future price of gold. Back in 2020, the report’s authors were predicting a gold price reaching around $4,800 by the end of the current decade, and this view has not changed. In order to achieve this they see the yellow metal’s price reaching around $2,200 in the current year – a very similar level to that of our own latest price forecast of a month or so ago.

So what is stagflation and how does it contribute to this kind of rising gold price scenario? Briefly it was a term coined in the UK back in the early 1970s during a period of stagnant economic growth coupled with high inflation, in turn brought about by high energy prices. Does that look familiar as being representative of the current economic environment. We have even gone on record as suggesting that this time around it may even be the precursor of recession, an even worse economic scenario, although in the past stagflation has seldom been followed by recession but ….currently who knows?

Certainly in the U.S. in particular, and in a pattern which is being followed by the Bank of England and, most likely, also by the European Central Bank, there is a strong programme already being initiated of Quantitative Tightening and strong interest rate rises to try and bring inflation under control, which could well have a recessionary impact without necessarily reducing the inflationary pressures that significantly. There is, though, the strong opinion held by a number of commentators and economists, and by the authors of the ‘In Gold we Trust’ report too, that the Fed will not follow through to the year-end with its more hawkish rate rise programme and will be forced into an about-turn later in the year in the face of a severe collapse in equity prices. This will be brought about as the markets take into consideration the likely effects on businesses of higher interest rates coupled with a downturn in general economic activity due to the ongoing ravages of inflation.

If this is indeed the case then there would be a likely recovery in both equities and precious metals towards the year end due to what may well be a short-lived period of economic optimism. This could represent the proverbial calm before the economic storm which we fear may await with the onset of a severe recession which would devastate equity prices – particularly for those which have been verging on illiquidity for some time. Gold may well do rather better, though, as the ultimate safe haven as the ‘In Gold we Trust’ authors expect, although their predicted path to a higher gold price is more slow and steady than the rapid rise predicted for many years now by some of the out and out gold bulls.

The 390-page report obviously covers far more than its coverage of inflation. stagflation and its gold price projections. Other analysis looks deeper at the causes of the current inflationary pressures, with the Russia/Ukraine war having a huge impact, thereby putting global monetary policy strongly on the defensive in its attempts to counter inflation without driving the whole world into recession – probably without success.

Markets are transitioning almost overnight from ‘bubble’ to crash with the reality of the strength of the U.S. anti- inflation measures threatening to provoke an equity market crash. So far huge equity falls have been tempered by perhaps less significant recoveries with the overall trend downwards and it seems unlikely to the report’s authors and contributors that moves by central banks to bring their respective economies under control can be achieved without some serious casualties developing.

In effect all this adverse economic projection is due to the virtual inevitability of continuing inflationary pressures ahead.. There is, in effect, a new ‘Cold War’ in the making in Europe – and perhaps in the Far East too if China seizes the opportunity to initiate one as well – and an overall move towards ‘de-globalization’. The world is entering an enormous de-carbonization cost phase too in response to global warming fears, with a wage-price spiral likely developing as a consequence. There may well be several such global inflationary phases to come.

These scenarios envisage changes to conventional investment strategies which may no longer apply. Commodities may benefit the most – history tells us that this may be the case and the ultimate safe haven asset, gold, could benefit strongest of all – particularly if rumours of a gold-backed reserve currency being developed by Russia and China turn out to be accurate.

END

3. Chris Powell of GATA provides to us very important physical commentaries

end

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //PALM OIL+ OTHERS

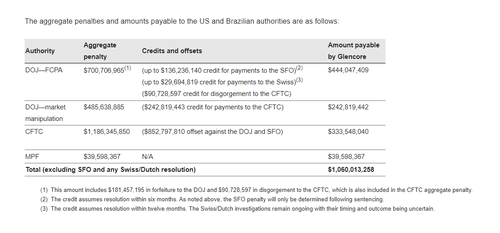

Glenclore pleads bleads guilty to decade of bribery and market manipulation….pays a $1.5 million penalty

(zerohedge

Glencore Pleads Guilty To Decade Of Bribery And Market Manipulation, Will Pay $1.5 BIllion Penalty

TUESDAY, MAY 24, 2022 – 09:05 PM

Swiss commodity trading giant Glencore agreed to plead guilty to multiple counts of bribery and market manipulation and pay penalties of up to $1.5BN to settle US, UK and Brazilian probes that have hung over the commodities giant for years.

The settlements will help remove question marks that have long overshadowed the trader’s (shady) business, profiled extensively in the gripping book The World For Sale. But the charges and admissions of guilt paint a damning, globe-spanning picture of how far the company, founded by U.S. fugitive Marc Rich, has been willing to go in pursuit of profit.

According to Bloomberg, Glencore units agreed to plead guilty to a list of charges that range from bribery and corruption in South America and Africa, to price manipulation in US fuel-oil markets.

The UK’s Serious Fraud Office on Tuesday charged the group’s subsidiary Glencore Energy UK with seven cases of profit-driven bribery and corruption in connection to oil operations in Cameroon, Equatorial Guinea, Ivory Coast, Nigeria and South Sudan. In a statement, the SFO said that its case was that “Glencore agents and employees paid bribes worth over $25mn for preferential access to oil, with approval by the company”.

In the US, Glencore pleaded guilty in two separate criminal cases and agreed to pay approximately $1.1bn in criminal fines and forfeiture. One case involved what prosecutors described as a decade-long bribery scheme, and in the second, Glencore’s US commodities trading arm pleaded guilty to engaging in an eight-year scheme to manipulate US fuel oil price benchmarks.

Glencore said it would pay about $1.5bn in overall penalties, including the $1.1bn to US authorities, $40mn to Brazilian prosecutors and an amount due to the UK to be finalised at a sentencing hearing. The company made a $1.5bn provision for the settlement in February, and said in an update on Tuesday that it does not expect the total fines to “differ materially” from what it has set aside.

Merrick Garland, US attorney-general, called it the US Department of Justice’s “largest criminal enforcement action to date for commodity price manipulation conspiracy in oil markets”.

“Bribery was built in to the corporate culture,” Manhattan US Attorney Damian Williams said at a press conference. “The tone from the top was clear: whatever it takes.” Glencore paid more than $100 million in bribes to government officials in Brazil, Nigeria, the Democratic Republic of the Congo and Venezuela, he said.

Glencore is the largest among a handful of independent commodity merchants that dominate global trading of oil, fuel, metals, minerals and food. The company and its rivals, most of which are privately held, have traditionally operated outside of the view of regulators and been willing to go to countries and do deals that others shy away from. In recent months, Glencore has fallen under the microscope for continuing to conduct Russian oil trade despite blanket western sanctions.

Glencore first said it was being investigated by the US in 2018 and details of the corruption in Africa began to emerge last year as a former Glencore trader pleaded guilty in the US to participating in an international scheme to bribe officials in Nigeria to win favorable treatment from the state-owned oil company.

The commodity trader and miner said in February it expected to resolve the UK, US and Brazilian investigations this year and set aside $1.5 billion. However, it still faces investigations in Switzerland and the Netherlands.

In an order Tuesday, the Commodity Futures Trading Commission describes how Glencore traders would use codes like “newspapers” or “chocolates” to refer to corrupt payments. The corruption and manipulation took place from at least 2007 through at least 2018, the CFTC said.

The investigations overshadowed the last years at the helm for former Chief Executive Officer Ivan Glasenberg, who built the company in its current form and remains a top shareholder. Glasenberg handed over the leadership last year to his handpicked successor, Gary Nagle, as part of a wider generational transition.

The company, which shifts millions of tonnes of metals, minerals and oil across the globe, also faces probes by Swiss and Dutch authorities, the timing and result of which remain uncertain.

Last July, a former Glencore oil trader pleaded guilty in New York over his role in a scheme to bribe government officials in Nigeria in return for lucrative oil contracts. The allegations in the original US DoJ investigation, which date as far back as 2007, happened during Glasenberg’s 19-year reign at the top of the company.

And while two Glencore traders have pleaded guilty as part of the US cases, the company’s top executives have so far escaped punishment.

Glasenberg and his top lieutenants took the company public in 2011 in what was then one of the largest ever flotations in London. It partly used the funds to transform the company from a pure commodity trader into a mining company through a merger with Xstrata in 2013 and a series of acquisitions.

But the company has struggled to shake off a reputation for sometimes questionable activity that many investors saw as embedded in its DNA, stretching back to its time as a privately held trading house, the FT notes.

“We acknowledge the misconduct identified in these investigations and have cooperated with the authorities,” CEO Nagle said in a statement. “This type of behavior has no place in Glencore, and the board, management team and I are very clear about the culture that we want and our commitment to be a responsible and ethical operator wherever we work.”

While the expected total payment is among the largest anti-corruption fines on record, it’s a pittance amount for Glencore. The company is expected to earn more than $17 billion this year, according to analysts’ consensus, meaning that it would make back the $1.5 billion in less than 5 weeks, according to Bloomberg.

“Glencore shouldn’t be allowed to gloss over what these charges reveal,” said Alexandra Gillies, an adviser at the Natural Resource Governance Institute. “These are some of the poorest countries in the world, countries where citizens have suffered the terrible costs of corruption for many years.”

Some more details from Bloomberg:

Glencore expects to pay about $1 billion to U.S. authorities after accounting for credits and offsets payable to other jurisdictions and agencies, and about $40 million to Brazil, the company said. The payment to the UK will only be finalized after a hearing next month but Glencore said it doesn’t expect the amount will result in the total penalties differing materially from the $1.5 billion previously disclosed.

Earlier Tuesday, Shaun Teichner, the general counsel for the company, told a federal judge in New York that Glencore International AG knowingly and willingly entered into a conspiracy to violate the Foreign Corrupt Practices Act by making payments to corrupt government officials.

“It’s a good day for them to finally get this done because it’s been hanging over them for a while,” said Ben Davis, a mining analyst at Liberum Capital. “It at least allows them to start to move forward.”

The bottom line, however, is that today’s settlement once again reveals that there are those who can pay their way out of legal trouble, and those who go to jail. Glencore, and its executives, are among the former: as Bloomberg’s Javier Blas notes, “not a single senior executive faces jail time. Other than Enron’s executives, the US last jailed a top oil trader in 2007-08 when it sent to prison David Chalmers and Oscar Wyatt, the CEOs of Bayoil and Coastal after the Iraq’s Oil-for-Food scandal.”

END

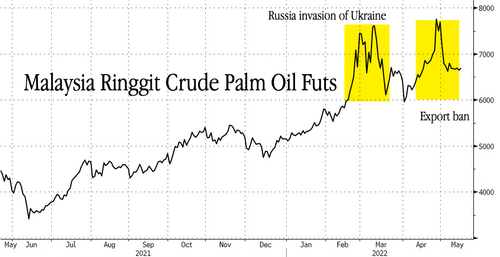

Indonesia lifts palm oil export ban

(zerohedge)

Indonesia Lifts Palm Oil Export Ban As Supply Improves

FRIDAY, MAY 20, 2022 – 10:00 PM

After nearly a month, Indonesia will lift an export ban on palm oil starting Monday, which could ease tight edible oil markets worldwide and reduce some of the pressure on soaring food prices.

“Based on the current supply and price of cooking oil and considering that there are 17 million workers in the palm oil industry, both working farmers and other supporting staff, I have decided that the export of cooking oil will reopen on Monday, May 23,” President Joko Widodo said in a statement on Thursday.

Indonesia is the world’s biggest shipper of edible oils, accounting for nearly 60% of global palm oil production. Palm oil is used in everything from food manufacturing to beauty products to biofuel. The export ban was the most significant act of crop protectionism globally following Russia’s invasion of Ukraine that choked the world off of edible oil supplies from the Black Sea region. Sending prices sky-high.

Widodo decided in late April to impose the export ban because domestic prices were rising and stockpiles were shrinking. The ban authorized shipments of palm oil to be rerouted into domestic supplies. The president expects domestic prices to ease in the coming weeks.

“Consumers can breathe a sigh of relief now,” Gnanasekar Thiagarajan, head of trading and hedging strategies at Kaleesuwari Intercontinental, told Bloomberg.

Presidential ratings for the Widodo have slid to a six-year low due to Indonesians’ growing discontent with soaring food prices.

Bloomberg notes the ban was lifted after hundreds of farmers protested the government, “saying their incomes have suffered because prices of their fresh fruit bunches plunged.”

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.6953

OFFSHORE YUAN: 6.70800

HANG SANG CLOSED UP 59.19 PTS OR 0.29%

2. Nikkei closed DOWN 76.34 OR 0.26%

3. Europe stocks ALL CLOSED ALL MIXED

USA dollar INDEX DOWN TO 102.43/Euro FALLS TO 1.0648

3b Japan 10 YR bond yield: FALLS TO. +.212/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 126.99/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN -SHORE CLOSED UP// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +0.859%/Italian 10 Yr bond yield FALLS to 2.75% /SPAIN 10 YR BOND YIELD FALLS TO 1.90%…

3i Greek 10 year bond yield RISES TO 3.58

3j Gold at $1855.60 silver at: 21.80 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 1.000 roubles/dollar; ROUBLE AT 57.78

3m oil into the 111 dollar handle for WTI and 114 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 126.96 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.620– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.027well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 27368 DOWN 2 BASIS PTS

USA 30 YR BOND YIELD: 2.950 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 16.32

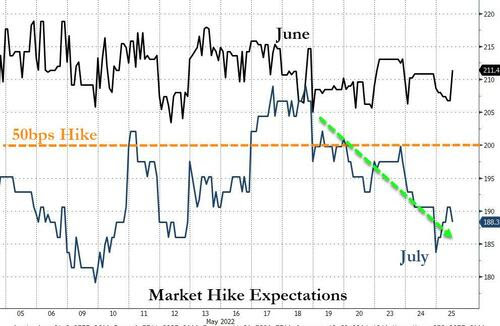

Futures Slide Before Fed Minutes, Dollar Jumps As China Lockdown Fears Return

WEDNESDAY, MAY 25, 2022 – 08:00 AM

Another day, another failure by markets to hold on to even the smallest overnight gains: US futures erased earlier profits and dipped as traders prepared for potential volatility surrounding the release of the Federal Reserve’s minutes which may provide insight into the central bank’s tightening path, while fears over Chinese lockdowns returned as Beijing recorded more Covid cases and the nearby port city of Tianjin locked down a city-center district. Contracts on the Nasdaq 100 and the S&P 500 were each down 0.5% at 7:30 a.m. in New York after gaining as much as 1% earlier, signaling an extension to Tuesday’s slide that followed a profit warning from Snap.

In premarket trading, Nordstrom jumped 10% after raising its forecast for earnings and revenue for the coming year suggesting that the luxury consumer is doing quite fine even as most of the middle class has tapped out; analysts highlighted the department store’s exposure to higher-end customers.Meanwhile, Wendy’s surged 12% after shareholder Trian Fund Management, billionaire Nelson Peltz’ investment vehicle, said it will explore a transaction that could give it control of the fast-food chain. Here are the most notable premarket movers in the US:

- Urban Outfitters (URBN US) shares rose as much as 5.7% in premarket trading after Nordstrom’s annual forecasts provided some relief for the beaten down retail sector. Shares rallied even as Urban Outfitters reported lower-than-expected profit and sales for the 1Q.

- Best Buy (BBY US) shares could be in focus as Citi cuts its price target on electronics retailer to a new Street-low of $65 from $80, saying that there continues to be “significant risk” to 2H estimates.

- Dick’s Sporting Goods (DKS US) sinks as much as 20% premarket after the retailer cut its year adjusted earnings per share and comparable sales guidance for the full year. Peers including Big 5 Sporting Goods, Hibbett and Foot Locker also fell after the DKS earnings release

- 2U Inc. (TWOU US) shares drop as much as 4.3% in US premarket trading after Piper Sandler downgraded the online educational services provider to underweight from neutral, with broker flagging growing regulatory risk.

- Verrica Pharma (VRCA US) shares slump as much as 61% in US premarket trading after the drug developer received an FDA Complete Response Letter for its VP-102 molluscum treatment.

- Shopify’s (SHOP US) U.S.-listed shares fell 0.7% in premarket trading after a second prominent shareholder advisory firm ISS joined its peer Glass Lewis to oppose the Canadian company’s plan to give CEO Tobi Lutke a special “founder share” that will preserve his voting power.

- Cazoo (CZOO US) shares declined 3.3% in premarket trading as Goldman Sachs initiated coverage of the stock with a neutral recommendation, saying the company is well positioned to capture the significant growth in online used car sales.

- CME Group (CME US Equity) may be in focus as its stock was upgraded to outperform from market perform at Oppenheimer on attractive valuation and an “appealing” dividend policy.

US stocks have slumped this year, with the S&P 500 flirting with a bear market on Friday, as investors fear that the Fed’s active monetary tightening will plunge the economy into a recession: as Bloomberg notes, amid surging inflation, lackluster earnings and bleak company guidance have added to market concerns. The tech sector has been particularly in focus amid higher rates, which mean a bigger discount for the present value of future profits. The Nasdaq 100 index has tumbled to the lowest since November 2020 and its 12-month forward price-to-earnings ratio of 19.7 is the lowest since the start of the pandemic and below its 10-year average.

“The consumer in the US is still showing really good signs of strength,” said Michael Metcalfe, global head of macro strategy at State Street Global Markets. “Even if there is a slowdown it’s going to be quite mild,” he said in an interview with Bloomberg Television.

Meanwhile, Barclays Plc strategists including Emmanuel Cau see scope for stocks to fall further if outflows from mutual funds pick up, unless recession fears are alleviated. Retail investors have also not yet fully capitulated and “still look to be buying dips in old favorites in tech/growth,” the strategists said.

“Our central scenario remains that a recession can be avoided and that geopolitical risks will moderate over the course of the year, allowing equities to move higher,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. “But recent market falls have underlined the importance of being selective and considering strategies that mitigate volatility.”

The Fed raised interest rates by 50 basis points earlier this month — to a target range of 0.75% to 1% — and Chair Jerome Powell has signaled it was on track to make similar-sized moves at its meetings in June and July. Investors are now awaiting the release of the May 3-4 meeting minutes later on Wednesday to evaluate the future path of rate hikes. However, in recent days, traders have dialed back the expected pace of Fed interest-rate increases over worse-than-expected economic data and the selloff in equities. Sales of new US homes fell more in April than economists forecast, and the Richmond Fed’s measure of business activity dropped to a two-year low. The yield on the 10-year Treasury slipped for a second day to 2.73%.

“Given the risks to growth and our view that positive real rates will be unmanageable for any significant length of time, we expect the Fed to deliver less tightening in 2022 overall than it and markets currently expect,” Salman Ahmed, global head of macro and strategic asset allocation at Fidelity International, wrote in a note.

In Europe, stocks pared an earlier advance but hold in the green while the dollar rallies. The Stoxx 600 gave back most of the morning’s gains with autos, financial services and travel weighing while miners and utilities outperformed. The euro slid as comments by European Central Bank officials indicated policy normalization will be gradual. The ECB is in the midst of a debate over how aggressive it should act to rein in inflation. Here are some of the most notable European movers today:

SSE shares rise as much as 6.3% after strong guidance and amid reports that electricity generators are likely to escape windfall taxes being considered by the U.K. government.

- Air France-KLM jumps as much as 13% in Paris after falling 21% on Tuesday as the airline kicked off a EU2.26 billion rights offering.

- Mining and energy stocks outperform the broader market in Europe as iron ore rebounded, while oil rose after a report that showed a decline in US gasoline stockpiles. Rio Tinto gains as much as 2.3%, Anglo American +2.6%, TotalEnergies +2.8%, Equinor +3.7%

- Elekta rises as much as 9.3% after releasing a 4Q earnings report that beat analysts’ expectations.

- Torm climbs as much as 12% after Pareto initiates coverage at buy and says the company may pay out dividends equal to 40% of its market value over the next 3 years.

- Mercell rises as much as 104% to NOK6.13/share after recommending a NOK6.3/share offer from Spring Cayman Bidco.

- Luxury stocks traded lower amid rekindled Covid-19 worries in China as Beijing continued to report new infections while nearby Tianjin locked down its city center. LVMH declines as much as 1.4%, Burberry -2.6% and Hermes -1.7%

- Sodexo falls as much as 5.7% after the French caterer decided not to open up the capital of its benefits & rewards unit to a partner following a review of the business.

- Ocado slumps as much as 8% after its grocery joint venture with Marks & Spencer slashed its forecast for FY22 sales growth to low single digits, rather than around 10% guided previously.