May 26, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

May 26, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1849.00 UP $2.10

SILVER: $21.97 UP $.08

ACCESS MARKET: GOLD $1850.30

SILVER: $22.02

Bitcoin morning price: $29,020 DOWN 685

Bitcoin: afternoon price: $29,457 DOWN 248

Platinum price: closing UP $4.00 to $949.20

Palladium price; closing UP $11.95 at $2010.25

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE: COMEX

JPMorgan issued 11/16

CONTRACT: MAY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,846.200000000 USD

INTENT DATE: 05/25/2022 DELIVERY DATE: 05/27/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 16

661 C JP MORGAN 11

737 C ADVANTAGE 3

905 C ADM 2

TOTAL: 16 16

MONTH TO DATE: 6,447

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT 16 NOTICE(S) FOR 1600 OZ (0.00497 TONNES)

total notices so far: 6447 contracts for 644700 oz (20.052 tonnes)

SILVER NOTICES:

83 NOTICE(S) FILED 415,000 OZ/

total number of notices filed so far this month 5607 : for 28,035,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $2.10

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A HUGE DEPOSIT OF 1.74 TONNES INTO THE GLD

INVENTORY RESTS AT 1069.81 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 8 CENTS

AT THE SLV// A BIG CHANGE IN SILVER INVENTORY AT THE SLV://A HUGE CHANGE IN SILVER INVENTORY

AT THE SLV.: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 558.071 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A SMALL SIZED 175 CONTRACTS TO 146,276 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE SMALL LOSS IN OI WAS ACCOMPLISHED DESPITE OUR $0.20 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.20) BUT ALSO UNSUCCESSFUL IN KNOCKING OFF ANY SILVER LONGS AS THEY REMAIN FIRM IN THEIR BELIEF OF A SILVER FAILURE AS WE HAD A NET GAIN OF 0 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 30.170 MILLION OZ FOLLOWED BY TODAY’S 305,000 OZ QUEUE JUMP //NEW STANDING 28,050,000 MILLION OZ/ // V) SMALL SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : + 5

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTACTS for 18 days, total 20,427, contracts: 102.135 million oz OR 5.666 MILLION OZ PER DAY. (1134CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 102.135 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 102.135 MILLION OZ//INCREASING AGAIN

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 175 DESPITE OUR $0.20 GAIN IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 180 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAY. OF 30.170 MILLION OZ FOLLOWED BY TODAY;S 0 OZ QUEUE. JUMP //NEW STANDING 28.050 MILLION OZ// .. WE HAD A 0 SIZED GAIN OF 5 OI CONTRACTS ON THE TWO EXCHANGES FOR 0.15 MILLION OZ DESPITE THE GAIN IN PRICE.

WE HAD 83 NOTICE FILED TODAY FOR 415,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 4038 CONTRACTS TO 526,060 AND FURTHER FROM NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: –1881 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE FAIR SIZED LOSS IN COMEX OI CAME DESPITE OUR GAIN IN PRICE OF $2.70//COMEX GOLD TRADING/WEDNESDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR GIGANTIC SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //JUST SPECULATOR SHORT COVERING FROM OUR STUPID SPECULATORS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 5.353 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY”S QUEUE JUMP OF 0 OZ//NEW STANDING 20.111 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $2.70 WITH RESPECT TO WEDNEDAY’S TRADING

WE HAD A FAIR SIZED LOSS OF 2853 OI CONTRACTS (8,811 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 1205 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 526,060

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2853, WITH 4053 CONTRACTS DECREASED AT THE COMEX AND 1205 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF2853 CONTRACTS OR 8.811 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1205) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (4038,): TOTAL LOSS IN THE TWO EXCHANGES 2853 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY. AT 5.353 TONNES FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 0 OZ//NEW STANDING 20.11 /// 3) ZERO LONG LIQUIDATION//CONSIDERABLE SPECULATOR SHORT COVERING //.,4) FAIR SIZED COMEX OI. LOSS 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

76,583 CONTRACTS OR 7,658,300 OR 238.20 TONNES 18 TRADING DAY(S) AND THUS AVERAGING: 4255 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAY(S) IN TONNES: 238.20 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 238.20/3550 x 100% TONNES 6.70% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 238,20 TONNES INITIAL// INCREASING AGAIN

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A SMALL SIZED 175 CONTRACT OI TO 146.281 AND FURTHER FORM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 180 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 180 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 175 CONTRACTS AND ADD TO THE 180 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A MINISCULE SIZED GAIN OF5 OR .150 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 0 MILLION OZ

OCCURRED DESPITE OUR GAIN IN PRICE OF $0.20 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

end

end

5. Other gold commentaries

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED UP 15.65 PTS OR 0.50% //Hang Sang CLOSED UP 55.07 PTS OR 0.27% /The Nikkei closed DOWN 72.96 OR 0.27% //Australia’s all ordinaires CLOSED DOWN 0.71% /Chinese yuan (ONSHORE) closed DOWN 6,7360 /Oil DOWN TO 111.01dollars per barrel for WTI and UP TO 114.41 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.73604 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7604: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER/

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 4038 CONTRACTS TO 526,060 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX DECREASE OCCURRED DESPITE OUR GAIN OF $2,70 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A SMALL SIZED EFP (1205 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ARE CAUGHT. THE COMMERCIALS WILL SLAUGHTER THESE GUYS WHEN THEY THINK THE TIME IS RIGHT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF MAY.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1205 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :1205 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1205 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2853 CONTRACTS IN THAT 1205 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 4038 CONTRACTS..AND YET THIS STRONG LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF GOLD $2.70.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (20.11),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $2.70) BUT WERE SUCCESSFUL IN KNOCKING OFF SOME SPECULATOR LONGS/COMMERCIAL LONGS AS WELL AS SPECULATOR SHORTS//// WE HAVE REGISTERED A FAIR SIZED LOSS OF 8.8811 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAY (20.11 TONNES)…

WE HAD 1881 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 2853 CONTRACTS OR 285300 OZ OR 8,811 TONNES

Estimated gold volume 204,595/// fair

Confirmed volume yesterday:288,065 contracts good

INITIAL STANDINGS FOR MAY ’22 COMEX GOLD //MAY 26

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 15,951.297 oz Int Delaware JPMorgan Manfra 400 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 16 notice(s)1600 OZ 0.00497 TONNES |

| No of oz to be served (notices) | 19 contracts 1900 oz 0.5909 TONNES |

| Total monthly oz gold served (contracts) so far this month | 6447 notices 644,700 OZ 20.052 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit 0 oz//

No dealer withdrawals

0 customer deposits

total deposits: nil oz

3 customer withdrawals:

i) Out of JPMorgan: 4822.650 oz (150 kilobars)

ii) Out of Int.Delaware: 8037.750 oz (250 kilobars)

iii) Out of Manfra: 2930.147 0z

total withdrawal: 15,951.297 oz

ADJUSTMENTS:

) Brinks dealer to customer 12,178.3057

and Manfra 1,450.337 0z

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 35 contracts having LOST ONLY 2 contracts

We had 2 notices filed YESTERDAY, so we gained 0 contracts or AN ADDITIONAL NIL oz will stand for delivery in this non active delivery month of May.

June saw a loss of 51,247 contracts down to 67,219 contracts

July has a GAIN OF 167 OI to stand at 1266

August has a gain of 45,844 contracts up to 395,796 contracts

We had 16 notice(s) filed today for 1600 oz FOR THE MAY 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 16 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 11 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2021. contract month,

we take the total number of notices filed so far for the month (6447) x 100 oz , to which we add the difference between the open interest for the front month of (MAY 35 CONTRACTS ) minus the number of notices served upon today 16 x 100 oz per contract equals 6,666,000 OZ OR 20.11 TONNES the number of TONNES standing in this non active month of MAY.

thus the INITIAL standings for gold for the MAY contract month:

No of notices filed so far (6447) x 100 oz+ (35) OI for the front month minus the number of notices served upon today (16} x 100 oz} which equals 646,600 oz standing OR 20.111 TONNES in this NON active delivery month of MAY.

TOTAL COMEX GOLD STANDING: 20.11 TONNES (A STRONG STANDING FOR A MAY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,060,078.634 oz

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 35,520,541.296 OZ

TOTAL ELIGIBLE GOLD: 17,398,567.733 OZ

TOTAL OF ALL REGISTERED GOLD: 18,121,973.563 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 16,061.895.0 OZ (REG GOLD- PLEDGED GOLD)

END

MAY 2022 CONTRACT MONTH//SILVER//MAY 26

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,688270.9 oz Brinks CNT Delaware JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 464,667.700 oz CNT |

| No of oz served today (contracts) | 83CONTRACT(S)415,000 OZ) |

| No of oz to be served (notices) | 3 contracts (15,000 oz) |

| Total monthly oz silver served (contracts) | 5607 contracts 28,035,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) zero dealer deposits And now for the wild silver comex results

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

i) Into CNTL 464.667.700 oz

total deposit: 464,667.700 oz

JPMorgan has a total silver weight: 174.533 million oz/335.786 million =52.08% of comex

Comex withdrawals: 4

i) Out of Brinks 566,802.770 oz

ii) Out of CNT: 99,891.200 . oz

iii) Out of Delaware 1863.500 oz

iv) Out of JPMorgan: 1021.572 oz

total withdrawal 1,688,270.900 oz

1 adjustments: customer to dealer HSBc: 9852.980 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 80.021 MILLION OZ

TOTAL REG + ELIG. 335/746 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY OI: 86 HAVING GAINED 3 CONTRACTS. WE HAD 58 NOTICES FILED ON YESTERDAY

SO WE GAINED 61 CONTRACTS OR A QUEUE JUMP OF 305,000 OZ

JUNE HAD A GAIN OF 11 TO STAND AT 1579

JULY HAD A LOSS OF 1750 CONTRACTS UDOWN TO 110,390 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 83 for 415,000 oz

Comex volumes: 30,638// est. volume today// poor

Comex volume: confirmed yesterday: 36,229 contracts ( poor )

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 5607 x 5,000 oz = 28,035,000 oz

to which we add the difference between the open interest for the front month of MAY(86) and the number of notices served upon today 83 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY./2022 contract month: 5607 (notices served so far) x 5000 oz + OI for front month of MAY (86) – number of notices served upon today (83) x 5000 oz of silver standing for the MAY contract month equates 28,050,000 oz. .

We GAINED 61 contracts or AN ADDITIONAL 305,000 OZ will stand for delivery at the comex

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

MAY 18/WITH GOLD DOWN $2.55//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.07 TONNES FROM THE GLD///INVENTORY RESTS AT 1049.21 TONNES

MAY 17/WITH GOLD UP $5.40:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1053.28 TONNES

MAY 16/WITH GOLD UP $5.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD///INVENTORY RESTS AT 1055.89 TONNES

MAY 13/ WITH GOLD DOWN $16.25//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.8 TONNES FROM THE GLD.//INVENTORY RESTS AT 1060.82 TONNES

MAY 12/WITH GOLD DOWN $26.50: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD////INVENTORY RESTS AT 1066.62 TONNES

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

GLD INVENTORY: 1069/81 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

MAY 18/WITH SILVER UP $0.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL 1.892 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 17/WITH SILVER UP $.22 TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.508 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 16/WITH SILVER UP $.52 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.546 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.593 MILLION OZ//

MAY 13/WITH SILVER UP 31 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ/

MAY 12/WITH SILVER DOWN 88 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ//

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

INVENTORY TONIGHT RESTS AT 558.071 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: It’s Not Putin, Or The Pandemic…It’s The Fed!

THURSDAY, MAY 26, 2022 – 01:00 PM

There is all kinds of spin out there when it comes to inflation. Peter Schiff recently appeared on News Nation to talk about the economy. He explained that the spin misses the mark. The real source of inflation isn’t the pandemic or Putin. It’s the Federal Reserve.

Peter said he thinks the Q1 GDP contraction will turn out to be the first quarter of this new recession.

This is going to be a very deep recession. It’s going to last for a long time. And it could be the worst recession anyone has experienced.”

Peter said inflation will make this recession particularly problematic.

Inflation is high and it’s going higher. So, you’re going to have the combination of a very weak economy in recession and high inflation getting worse. And inflation is going to complicate the severity of the recession and make it that much more difficult for average Americans to endure it.”

The host mentioned that Treasury Secretary Janet Yellen recently conceded that the economy will likely face more shocks and challenges in the future.

But she continues to insist the economy is strong overall. Peter said Yellen has a very poor understanding of the economy.

She had a poor understanding as Fed chairman, and before that, she had a poor understanding when she was a member of the FMOC. She was clueless about the financial crisis that was looming right around the horizon. And of course, she was jumping on the bandwagon more recently of inflation being ‘transitory’ when it clearly was not. So, she doesn’t really know very much about the economy. She’s just there to talk up the economy no matter how bad it looks. She’s going to put positive spin on it. But it’s a disaster.”

Peter pointed out the record trade deficit for April and reiterated the economy is a disaster.

The host pushed back a bit, saying there are some signs that the economy is OK. He pointed out that airlines have never been busier. Hotels are booked for the summer. That would seem to indicate consumers think things have the potential to be OK.

Peter conceded that some people still have hope. But it’s a false hope.

The Fed is printing a lot of money and the value of that money is going down. It’s going to crash eventually. It’s not about the consumer. It’s about the producer. And I just said we have the worst trade deficit in our history because our economy is not productive. What we’re doing is printing a lot of money and we’re spending that money to buy things that are made in other countries. So, it’s the rest of the world that’s being productive, not America. We’re being profligate. We’re just spending the money that the Federal Reserve prints out of thin air. But that’s inflation. That’s the source of the inflation. It’s not Putin. It’s not the pandemic. It’s the Federal Reserve. It’s the US government running record budget deficits being monetized by a Federal Reserve that’s printing all this money. The money is losing value. Prices are going up. The government is being dishonest about how much because the CPI grossly understates the degree a which prices are rising. Prices are rising at more than double the rate the government claims.”

2.LAWRIE WILLIAMS//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

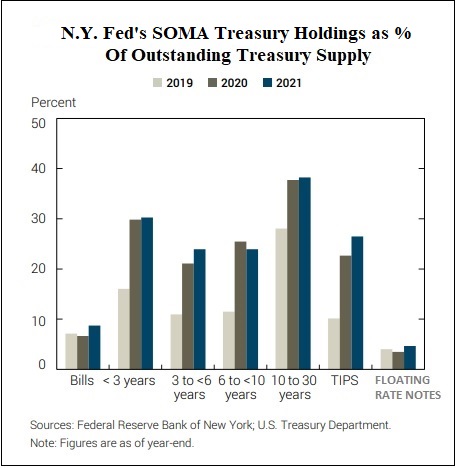

New York Fed Stuns with New Report: At Year End Its Trading Desk Owned 38 Percent of All 10-30 Year U.S. Treasuries

Pam and Russ Martens….

New York Fed Stuns with New Report: At Year End Its Trading Desk Owned 38 Percent of All 10-30 Year U.S. Treasuries

By Pam Martens and Russ Martens: May 26, 2022

On Tuesday, the New York Fed’s trading desk released its annual report showing what it was up to in 2021. The New York Fed is the only one of the Federal Reserve’s 12 regional Fed banks to have a trading desk operation with speed dials to Wall Street’s trading houses, so we’re always interested in reading the “official” version of what’s been happening there.

The report is a deeply sanitized version of the facts on the ground. (For example, there is nothing in the report to indicate that the New York Fed has established a second trading floor near the futures exchange in Chicago.)

However, there is one paragraph in the newly-released report that took our breath away. It reveals that the New York Fed’s trading operation (officially called the System Open Market Account or SOMA) currently owns 38 percent of all outstanding U.S. Treasury Securities with 10 to 30 years remaining until maturity. (See the last two paragraphs on page 33 of the report.)

There are multiple reasons that this detail takes our breath away. First of all, the U.S. Treasury market is massive – at $22.6 trillion as of year-end 2021. That any one entity controls a big chunk of the market is deeply concerning. (The same report showed that the New York Fed’s trading desk owned 25 percent of all maturities of outstanding Treasury debt.)

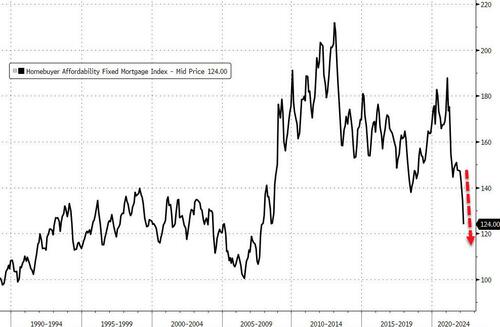

The New York Fed’s trading desk owning 38 percent of the 10-30 year Treasuries is also deeply alarming because it is that maturity range that has a dramatic impact on the interest rate of the 30-year fixed-rate residential mortgage, the most popular mortgage among first-time homebuyers historically. It means that the New York Fed’s gobbling up of these 10-year U.S. Treasury Notes and 30-year U.S. Treasury Bonds, to the tune of 38 percent of the market, has created artificial demand for these instruments that would not otherwise exist. That, in turn, means that mortgage rates have been artificially held lower – much lower – than they would otherwise have been.

Even more alarming, it means that the recent announcements by the Fed that it will be reducing its purchases of Treasury securities and shrinking its balance sheet by reducing the amount of principal payments that are rolled over into new Treasury securities, is going to have a dramatic impact on residential mortgage rates.

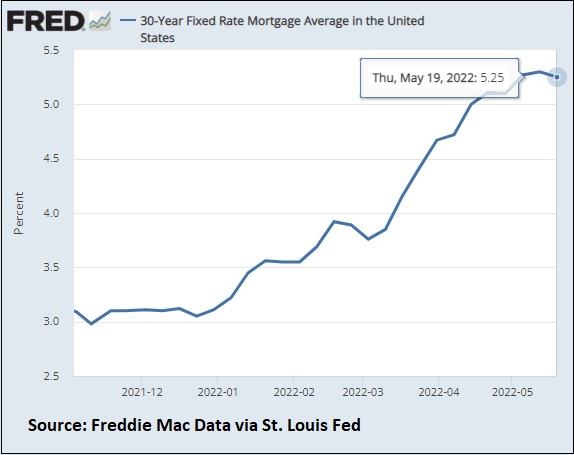

The chart below shows how the 30-year fixed rate mortgage has risen since the Fed made its first announcement of QE tapering on November 3, 2021 and subsequent tapering announcements. The 30-year fixed rate mortgage has spiked from an average of 3 percent to 5.25 percent as of May 19 of this year – an increase of 75 percent. The dramatic spike in the rate over a period of just seven months has priced many first-time home buyers out of the market.

The Fed calls its purchases of Treasuries and other debt instruments “Quantitative Easing” or QE. The Fed embarked on three rounds of QE between 2008 and 2012 in an effort to stimulate the economy and get it back on a sound footing after Wall Street crashed the economy with its derivatives and subprime debt bombs in 2008.

When the repo market blew up in the fall of 2019, the New York Fed cranked up its QE operations again and ramped them up further when the pandemic hit in 2020. In June of 2020, the Fed began purchasing a total of $120 billion in debt securities each month, a larger amount than during the 2008 financial crisis.

The Fed’s balance sheet has grown from $924 billion on December 26, 2007 – prior to the financial crash of 2008 – to $8.99 trillion as of last Wednesday.

-END-

END

3. Chris Powell of GATA provides to us very important physical commentaries

end

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //PALM OIL+ OTHERS

END

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7360

OFFSHORE YUAN: 6.7604

HANG SANG CLOSED DOWN 55.07 PTS OR 0.27%

2. Nikkei closed DOWN 72.96 OR 0.27%

3. Europe stocks ALL CLOSED ALL GREEEN

USA dollar INDEX DOWN TO 102.06/Euro FALLS TO 1.0647

3b Japan 10 YR bond yield: RISES TO. +.229/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 127.09/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN -SHORE CLOSED DOWN// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +0.859%/Italian 10 Yr bond yield FALLS to 2.75% /SPAIN 10 YR BOND YIELD FALLS TO 1.90%…

3i Greek 10 year bond yield FALLS TO 3.53

3j Gold at $1843.40 silver at: 21.81 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 4.66 roubles/dollar; ROUBLE AT 63.37

3m oil into the 111 dollar handle for WTI and 114 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 127.90DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.620– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.027well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.734 DOWN 1 BASIS PTS

USA 30 YR BOND YIELD: 2.980 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 16.42

S&P Futures Jump Above 4,000 As Fed Fears Fade

THURSDAY, MAY 26, 2022 – 07:50 AM

After yesterday’s post-FOMC ramp which sent stocks higher after the Fed’s Minutes were less hawkish than feared and also hinted at a timeline for the Fed’s upcoming pause (and easing), US index futures initially swung between gains and losses on Thursday as investors weighed the “good news” from the Fed against downbeat remarks on the Chinese economy from premier Li who warned that China would struggle to post a positive GDP print this quarter coupled with Apple’s conservative outlook. Eventually, however, bullish sentiment prevailed and even with Tech stocks underperforming following yesterday’s disappointing earnings from Nvidia, e-mini futures rose to session highs as of 715am, and traded up 0.6% above 4,000 for the first time since May 18, while Nasdaq 100 futures were up 0.2% after earlier dropping as much as 0.8%. The tech-heavy index is down 27% this year. Treasury yields and the dollar slipped. Fed policy makers indicated their aggressive set of moves could leave them with flexibility to shift gears later if needed.

Investors took some comfort from the Fed minutes that didn’t show an even more aggressive path being mapped to tackle elevated prices, though central banks remain steadfast in their resolve to douse inflation. Still, volatility has spiked as the risk of a US recession, the impact from China’s lockdowns and the war in Ukraine simmer.

While the Fed minutes “provided investors with a temporary relief, today’s mixed price action on stocks mostly shows that major bearish leverages linger,” said Pierre Veyret, a technical analyst at ActivTrades in London. “The war in eastern Europe and concerns about the Chinese economy still add stress to market sentiment,” he wrote in a report. “Investors will want to see evidence of improvements regarding the pressure coming from rising prices.”

“We expect key market drivers to continue to be centered around inflation and how central banks react; global growth concerns and how China gets to grip with its zero-Covid policy; and the geopolitical conflict between Russia and Ukraine,” said Fraser Lundie, head of fixed income for public markets at Federated Hermes Limited. “Positive news flow on any of these market drivers could sharply improve risk sentiment; however, there is a broad range of scenarios that could play out in the meantime.”

In premarket trading, shares in Apple dropped 1.4% after a report said that the tech giant is planning to keep iPhone production flat in 2022, disappointing expectations for a ~10% increase. The company also said it was raising salaries in the US by 10% or more as it faces a tight labor market and unionization efforts. In other premarket moves, Nvidia dropped 5.3% as the biggest US chipmaker by market value gave a disappointing sales forecast. Software company Snowflake slumped 14%, while meme stock GameStop Corp. fell 2.9%. Among gainers, Twitter Inc. jumped 5.2% after billionaire Elon Musk dropped plans to partially fund his purchase of the company with a margin loan tied to his Tesla stake and increased the size of the deal’s equity component to $33.5 billion. Other notable premarket movers include:

- Shares of Alibaba and Baidu rise following results, sending other US-listed Chinese stocks higher in US premarket trading. Alibaba shares shot up as much as 4.5% after reporting fourth- quarter revenue and earnings that beat analyst expectations.

- Lululemon’s (LULU US) stock gains 2.4% in premarket trading as Morgan Stanley raised its recommendation to overweight, suggesting that the business can be more resilient through headwinds than what the market is expecting.

- Macy’s (M US) shares gain 15% in premarket trading after Co. increases its adjusted earnings per share guidance for the full fiscal year

- Williams-Sonoma (WSM US) shares jumped as much as 9.6% in premarket trading after 1Q sales beat estimates. The retailer was helped by its exposure to more affluent customers, but analysts cautioned that it may be difficult to maintain the sales momentum amid macroeconomic challenges.

- Nutanix (NTNX US) shares shed about a third of their value in US premarket trading as analysts slashed their price targets on the cloud platform provider after its forecast disappointed.

- US airline stocks rise in premarket trading on Thursday, after Southwest and JetBlue provided upbeat outlooks for the second-quarter. LUV up 1.5% premarket, after raising its second-quarter operating revenue growth forecast. JBLU up 2% after saying it expects second-quarter revenue at or above high end of previous guidance.

- Cryptocurrency-tied stocks fall in premarket trading as Bitcoin snaps two days of gains. Coinbase -2.6%; Marathon Digital -2.3%; Riot Blockchain -1.2%. Bitcoin drops 1.9% at 6:11 am in New York, trading at $29,209.88.

It’s time to buy the dip in stocks after a steep global selloff in equity markets, according to Citi strategists. Meanwhile, Fidelity International Chief Executive Officer Anne Richards said the risk of a recession has increased and markets are likely to remain volatile, the latest dire warning on the outlook at the World Economic Forum.

“If inflation gets tame enough over summer, there may not be continued raising of rates,” Carol Pepper, Pepper International chief executive officer, said on Bloomberg TV, adding that investors should look to buy tech stocks after the selloff. “Stagflation, I just don’t think that’s going to happen anymore. I think we are going to be in a situation where inflation will start tapering down and then we will start going into a more normalized market.”

In Europe, the Stoxx Europe 600 Index rose 0.3%, pare some of their earlier gains but remain in the green, led by gains for retail, consumer and energy stocks. IBEX outperforms, adding 0.6%, FTSE MIB is flat but underperforms peers. Retailers, energy and consumer products are the strongest-performing sectors, with energy shares outperforming for the second day as oil climbed amid data that showed a further decrease in US crude and gasoline stockpiles. Here are the most notable European movers:

- Auto Trader rises as much as 3.5% after its full-year results beat consensus expectations on both top- and bottom-lines.

- Galp climbs as much as 4.1% as RBC upgrades to outperform, saying the stock might catch up with the rest of the sector after “materially” underperforming peers in recent years.

- Rightmove rises as much as 1.5% after Shore upgrades to hold from sell, saying the stock has reached an “appropriate” level following a 27% decline this year.

- FirstGroup soars as much as 16% after the bus and train operator said it received a takeover approach from I Squared Capital Advisors and is currently evaluating the offer.

- United Utilities declines as much as 8.9% as company reports a fall in adjusted pretax profit. Jefferies says full-year guidance implies a materially-below consensus adjusted net income view.

- Johnson Matthey falls as much as 7.5% after the company reported results and said it expects operating performance in the current fiscal year to be in the lower half of the consensus range.

- BT drops as much as 5.7% after the telecom operator said the UK will review French telecom tycoon Patrick Drahi’s increased stake in the company under the National Security and Investment Act.

- JD Sports drops as much as 12% as the departure of Peter Cowgill as executive chairman is disappointing, according to Shore Capital.

Earlier in the session, Asian stocks were mixed as traders assessed China’s emergency meeting on the economy and Federal Reserve minutes that struck a less hawkish note than markets had expected. The MSCI Asia Pacific Index was little changed after fluctuating between gains and losses of about 0.6% as technology stocks slid. South Korean stocks dipped after the central bank raised interest rates by 25 basis points as expected. Chinese shares eked out a small advance after a nationwide emergency meeting on Wednesday offered little in terms of additional stimulus. The benchmark CSI 300 Index headed for a weekly drop of more than 2%, despite authorities’ vows to support an economy hit by Covid-19 lockdowns. Investors took some comfort from Fed minutes in which policy makers indicated their aggressive set of moves could leave them with flexibility to shift gears later if needed. Still, Asia’s benchmark headed for a weekly loss amid concerns over China’s lockdowns and the possibility of a US recession.

“The coming months are ripe for a re-pricing of assets across the board with a further shake-down in risk assets as term and credit premia start to feature prominently,” Vishnu Varathan, the head of economics and strategy at Mizuho Bank, wrote in a research note.

Japanese stocks closed mixed after minutes from the Federal Reserve’s latest policy meeting reassured investors while Premier Li Keqiang made downbeat comments on China’s economy. The Topix rose 0.1% to close at 1,877.58, while the Nikkei declined 0.3% to 26,604.84. Toyota Motor Corp. contributed the most to the Topix gain, increasing 1.9%. Out of 2,171 shares in the index, 1,171 rose and 898 fell, while 102 were unchanged.

In Australia, the S&P/ASX 200 index fell 0.7% to close at 7,105.90 as all sectors tumbled except for technology. Miners contributed the most to the benchmark’s decline. Whitehaven slumped after peer New Hope cut its coal output targets. Appen soared after confirming a takeover approach from Telus and said it’s in talks to improve the terms of the proposal. Appen shares were placed in a trading halt later in the session. In New Zealand, the S&P/NZX 50 index fell 0.6% to 11,102.84.

India’s key stock indexes snapped three sessions of decline to post their first advance this week on recovery in banking and metals shares. The S&P BSE Sensex rose 0.9% to 54,252.53 in Mumbai, while the NSE Nifty 50 Index advanced by a similar measure. Both benchmarks posted their biggest single-day gain since May 20 as monthly derivative contracts expired today. All but one of the 19 sector sub-indexes compiled by BSE Ltd. gained. HDFC Bank and ICICI Bank provided the biggest boosts to the two indexes, rising 3% and 2.2%, respectively. Of the 30 shares in the Sensex, 24 rose and 6 fell. As the quarterly earnings season winds up, among the 45 Nifty companies that have so far reported results, 18 have trailed estimates and 27 met or exceeded expectations. Aluminum firm Hindalco Industries is scheduled to post its numbers later today.

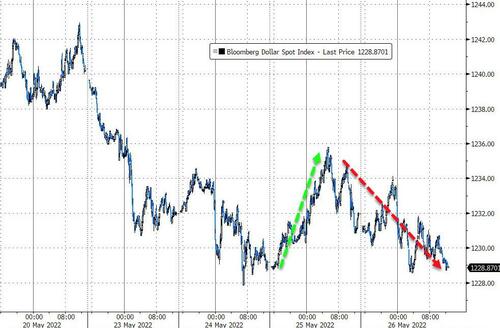

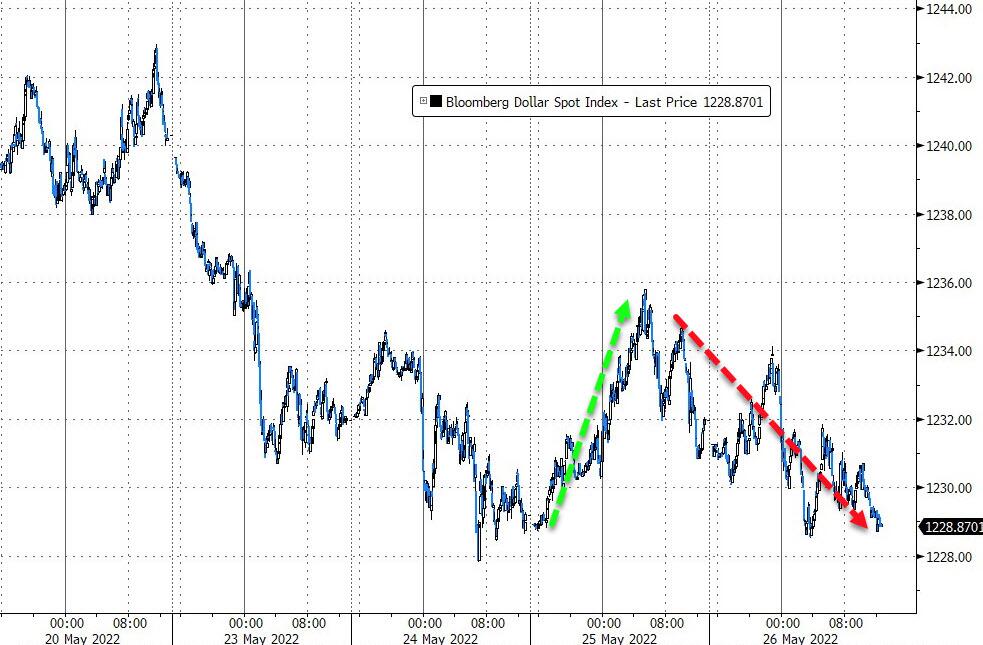

In FX, the Bloomberg Dollar fell 0.3%, edging back toward the lowest level since April 26 touched Tuesday. The yen jumped to an intraday high after the head of the Bank of Japan said policymakers could manage an exit from their decades-long monetary policy, and that U.S. rate rises would not necessarily keep the yen weak. Commodity currencies including the Australian dollar fell as China’s Premier Li Keqiang offered a bleak outlook on domestic growth. The Chinese economy is in some respects faring worse than in 2020 when the pandemic started, he said.

Central banks were busy overnight:

- Russia’s central bank delivered its third interest-rate reduction in just over a month and said borrowing costs can fall further still, as it looks to stem a rally in the ruble and unwinds the financial defenses in place since the invasion of Ukraine.

- The Bank of Korea raised its key interest rate on Thursday as newly installed Governor Rhee Chang-yong demonstrated his intention to tackle inflation at his first policy meeting since taking the helm. New Zealand’s central bank has also shown its commitment this week to combat surging prices.

In rates, Treasuries bull-steepen amid similar price action in bunds and many other European markets and gains for US equity index futures. Yields richer by ~3bp across front-end of the curve, steepening 2s10 by ~2bp, 5s30s by ~3bp; 10-year yields rose 2bps to 2.76%, keeps pace with bund while outperforming gilts. 2- and 5-year yields reached lowest levels in more than a month, remain below 50-DMAs. US auction cycle concludes with 7-year note sale, while economic data includes 1Q GDP revision. Bund, Treasury and gilt curves all bull-steepen. Peripheral spreads tighten to Germany with 10y BTP/Bund narrowing 5.1bps to 194.6bps.

The US weekly auction calendar ends with a $42BN 7-year auction today which follows 2- and 5-year sales that produced mixed demand metrics, however both have richened from auction levels. WI 7-year yield at ~2.735% is ~17bp richer than April’s, which tailed by 1.7bp. IG dollar issuance slate includes Bank of Nova Scotia 3Y covered SOFR; issuance so far this week remains short of $20b forecast, is expected to remain subdued until after US Memorial Day.

In commodities, WTI trades within Wednesday’s range, adding 0.6% to around $111. Spot gold falls roughly $7 to trade around $1,846/oz. Cryptocurrencies decline, Bitcoin drops 2.5% to below $29,000.

Looking at the day ahead now, and data releases from the US include the second estimate of Q1 GDP, the weekly initial jobless claims, pending home sales for April, and the Kansas City Fed’s manufacturing index for May. Meanwhile in Italy, there’s the consumer confidence index for May. From central banks, we’ll hear from Fed Vice Chair Brainard, the ECB’s Centeno and de Cos, and also get decisions from the Central Bank of Russia and the Central Bank of Turkey. Finally, earnings releases include Costco and Royal Bank of Canada.

Market Snapshot

- S&P 500 futures little changed at 3,974.25

- STOXX Europe 600 up 0.2% to 435.16

- MXAP little changed at 163.17

- MXAPJ down 0.3% to 529.83

- Nikkei down 0.3% to 26,604.84

- Topix little changed at 1,877.58

- Hang Seng Index down 0.3% to 20,116.20

- Shanghai Composite up 0.5% to 3,123.11

- Sensex up 0.4% to 53,975.57

- Australia S&P/ASX 200 down 0.7% to 7,105.88

- Kospi down 0.2% to 2,612.45

- German 10Y yield little changed at 0.90%

- Euro little changed at $1.0679

- Brent Futures up 0.5% to $114.55/bbl

- Gold spot down 0.3% to $1,847.94

- U.S. Dollar Index little changed at 102.11

Top Overnight News from Bloomberg

- Federal Reserve officials agreed at their gathering this month that they need to raise interest rates in half-point steps at their next two meetings, continuing an aggressive set of moves that would leave them with flexibility to shift gears later if needed.

- Russia’s central bank delivered its third interest-rate reduction in just over a month and said borrowing costs can fall further still, halting a rally in the ruble as it unwinds the financial defenses in place since the invasion of Ukraine.

- China’s trade-weighted yuan fell below 100 for the first time in seven months as Premier Li Keqiang’s bearish comments added to concerns that the economy may miss its growth target by a wide margin this year.

- Bank of Japan Governor Haruhiko Kuroda said interest rate increases by the Federal Reserve won’t necessarily cause the yen to weaken, saying various factors affect the currency market.

A more detailed breakdown of global markets courtesy of Newsquawk

Asia-Pac stocks were indecisive as risk appetite waned despite the positive handover from Wall St where the major indices extended on gains post-FOMC minutes after the risk event passed and contained no hawkish surprises. ASX 200 failed to hold on to opening gains as weakness in mining names, consumer stocks and defensives overshadowed the advances in tech and financials, while capex data was mixed with the headline private capital expenditure at a surprise contraction for Q1. Nikkei 225 faded early gains but downside was stemmed with Japan set to reopen to tourists on June 6th. Hang Seng and Shanghai Comp were mixed with early pressure after Premier Li warned the economy was worse in some aspects than in 2020 when the pandemic began, although he stated that China will unveil detailed implementation rules for a pro-growth policy package before the end of the month, while the PBoC issued a notice to promote credit lending to small firms and the MoF announced cash subsidies to Chinese airlines.

Top Asian News

- PBoC issued a notice to promote credit lending to small firms and is to boost financial institutions’ confidence to lend to small firms, according to Reuters.

- BoK raised its base rate by 25bps to 1.75%, as expected, via unanimous decision. BoK raised its 2022 inflation forecast to 4.5% from 3.1% and raised its 2023 forecast to 2.9% from 2.0%, while it sees GDP growth of 2.7% this year and 2.4% next year. BoK said consumer price inflation is to remain high in the 5% range for some time and sees it as warranted to conduct monetary policy with more focus on inflation, according to Reuters.

- Morgan Stanley has lowered China’s 2022 GDP estimate to 3.2% from 4.2%.

- CSPC Drops After Earnings, Covid Impact to Weigh: Street Wrap

- China Builder Greenland’s Near-Term Bonds Set for Record Drops

- Debt Is Top Priority for Diokno as New Philippine Finance Chief

European bourses are firmer across the board, Euro Stoxx 50 +0.7%, but remain within initial ranges in what has been a relatively contained session with much of northern-Europe away. Stateside, US futures are relatively contained, ES +0.2%, with newsflow thin and on familiar themes following yesterday’s minutes and before PCE on Friday. Apple (AAPL) is reportedly planning on having a 220mln (exp. ~240mln) iPhone production target for 2022, via Bloomberg. -1.4% in the pre-market. Baidu Inc (BIDU) Q1 2022 (CNY): non-GAAP EPS 11.22 (exp. 5.39), Revenue 28.4bln (exp. 27.82bln). +4.5% in the pre-market. UK CMA is assessing whether Google’s (GOOG) practises in parts of advertisement technology may distort competition.

Top European News

- UK Chancellor Sunak’s package today is likely to top GBP 30bln, according to sources via The Times; Chancellor will confirm that the package will be funded in part by windfall tax on oil & gas firms likely to come into effect in the autumn. Subsequently, UK Gov’t sources are downplaying the idea that the overall support package is worth GBP 30bln, via Times’ Swinford; told it is a very big intervention.

- UK car production declined 11.3% Y/Y to 60,554 units in April, according to the SMMT.

- British Bus Firm FirstGroup Gets Takeover Bid from I Squared

- Citi Strategists Say Buy the Dip in Stocks on ‘Healthy’ Returns

- The Reasons to Worry Just Keep Piling Up for Davos Executives

- UK Unveils Plan to Boost Aviation Industry, Passenger Rights

- Pakistan Mulls Gas Import Deal With Countries Including Russia

FX

- Dollar drifts post FOMC minutes that reaffirm guidance for 50bp hikes in June and July, but nothing more aggressive, DXY slips into lower range around 102.00 vs 102.450 midweek peak.

- Yen outperforms after BoJ Governor Kuroda outlines exit strategy via a combination of tightening and balance sheet reduction, when the time comes; USD/JPY closer to 126.50 than 127.50 where 1.13bln option expiries start and end at 127.60.

- Rest of G10, bar Swedish Crown rangebound ahead of US data, with Loonie looking for independent direction via Canadian retail sales, USD/CAD inside 1.2850-00; Cable surpassing 1.2600 following reports that the cost of living package from UK Chancellor Sunak could top GBP 30bln.

- Lira hits new YTD low before CBRT and Rouble weaker following top end of range 300bp cut from CBR.

- Yuan halts retreat from recovery peaks ahead of key technical level, 6.7800 for USD/CNH.

Fixed Income

- Debt wanes after early rebound on Ascension Day lifted Bunds beyond technical resistance levels to 154.74 vs 153.57 low.

- Gilts fall from grace between 119.17-118.19 parameters amidst concerns that a large UK cost of living support package could leave funding shortfall.

- US Treasuries remain firm, but off peaks for the 10 year T-note at 120-31 ahead of GDP, IJC, Pending Home Sales and 7 year supply.

Commodities

- Crude benchmarks inch higher in relatively quiet newsflow as familiar themes dominate; though reports that EU officials are considering splitting the oil embargo has drawn attention.

- Currently WTI and Brent lie in proximity to USD 111/bbl and USD 115/bbl respectively; within USD 1.50/bbl ranges.

- Russian Deputy PM Novak expects 2022 oil output 480-500mln/T (prev. 524mln/T YY), via Ria.

- Spot gold is similarly contained around the USD 1850/oz mark, though its parameters are modestly more pronounced at circa. USD 13/oz

Central Banks

- CBR (May, Emergency Meeting): Key Rate 11.00% (exp. ~11.00/12.00%, prev. 14.00%); holds open the prospect of further reductions at upcoming meetings.

- BoJ’s Kuroda says, when exiting easy policy, they will likely combine rate hike and balance sheet reduction through specific means, timing to be dependent on developments at that point; FOMC rate hike may not necessarily result in a weaker JPY or outflows of funds from Japan if it affects US stock prices, via Reuters.

US Event Calendar

- 08:30: 1Q PCE Core QoQ, est. 5.2%, prior 5.2%

- 08:30: 1Q Personal Consumption, est. 2.8%, prior 2.7%

- 08:30: May Continuing Claims, est. 1.31m, prior 1.32m

- 08:30: 1Q GDP Price Index, est. 8.0%, prior 8.0%

- 08:30: May Initial Jobless Claims, est. 215,000, prior 218,000

- 08:30: 1Q GDP Annualized QoQ, est. -1.3%, prior -1.4%

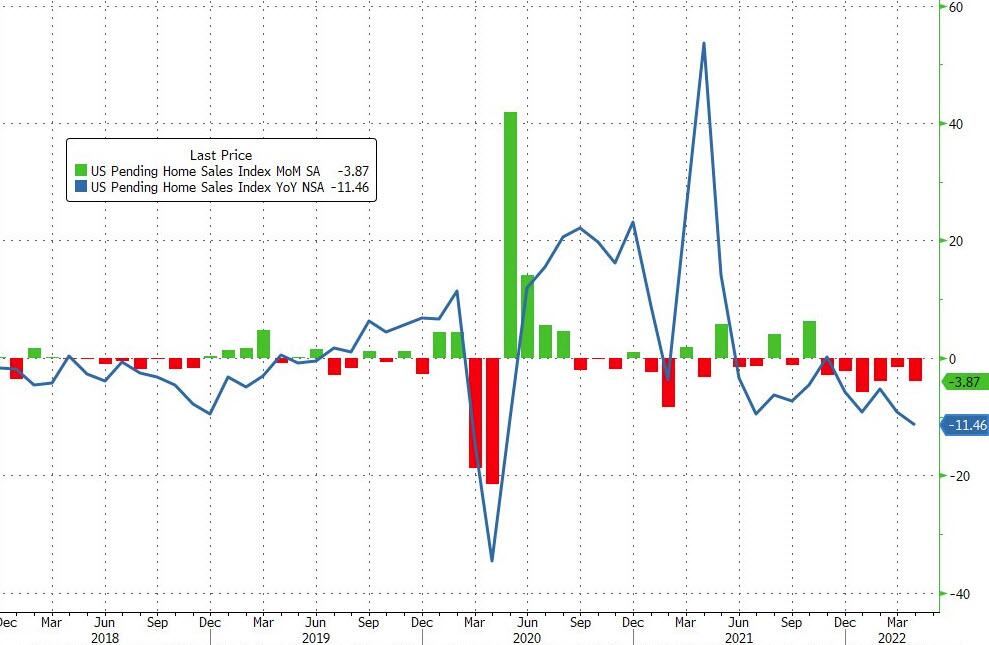

- 10:00: April Pending Home Sales YoY, est. -8.0%, prior -8.9%

- 10:00: April Pending Home Sales (MoM), est. -2.0%, prior -1.2%

- 11:00: May Kansas City Fed Manf. Activity, est. 18, prior 25

DB’s Jim Reid concludes the overnight wrap

A reminder that our latest monthly survey is now live, where we try to ask questions that aren’t easy to derive from market pricing. This time we ask if you think the Fed would be willing to push the economy into recession in order to get inflation back to target. We also ask whether you think there are still bubbles in markets and whether equities have bottomed out yet. And there’s another on which is the best asset class to hedge against inflation. The more people that fill it in the more useful so all help from readers is very welcome. The link is here.

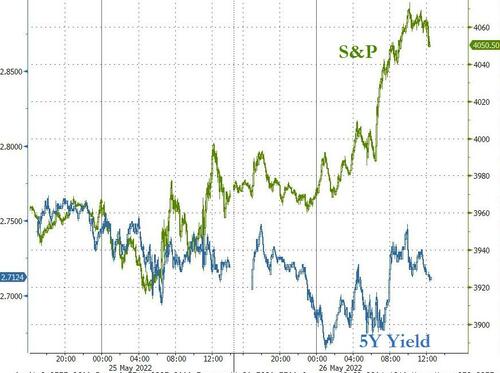

For markets it’s been a relatively quiet session over the last 24 hours compared to the recent bout of cross-asset volatility. The main event was the release of the May FOMC minutes, which had the potential to upend that calm given the amount of policy parameters currently being debated by the Fed. But in reality they came and went without much fanfare, and failed to inject much life into afternoon markets or the debate around the near-term path of policy. As far as what they did say, they confirmed the line from the meeting itself that the FOMC is ready to move the policy to a neutral position to fight the current inflationary scourge, with agreement that 50bp hikes were appropriate at the next couple of meetings. That rapid move to neutral would leave the Fed well-positioned to judge the outlook and appropriate next steps for policy by the end of the year, and markets were relieved by the lack of further hawkishness, with the S&P 500 extending its modest gains following the release to end the day up +0.95%.

As the Chair said at the meeting, and has been echoed by other Fed officials since, the minutes noted that the hawkish shift in Fed communications have already had a noticeable effect on financial conditions, with Fed staff pointing out that “conditions had tightened by historically large amounts since the beginning of the year.” Meanwhile on QT, which the Fed outlined their plans for at the May meeting, the minutes expressed some trepidation about market liquidity and potential “unanticipated effects on financial market conditions” as a result, but did not offer potential remedies.

With the minutes not living up to hawkish fears alongside growing concerns about a potential recession, investors continued to dial back the likelihood of more aggressive tightening, with Fed funds futures moving the rate priced in by the December meeting to 2.64%, which is the lowest in nearly a month and down from its peak of 2.88% on May 3. So we’ve taken out nearly a full 25bp hike by now, which is the biggest reversal in monetary policy expectations this year since Russia’s invasion of Ukraine began. That decline came ahead of the minutes and also saw markets pare back the chances of two consecutive +50bp hikes, with the amount of hikes priced over the next two meetings falling under 100bps for only the second time since the May FOMC. Yields on 10yr Treasuries held fairly steady, only coming down -0.5bps to 2.745%.

Ahead of the Fed minutes, markets had already been on track to record a steady performance, and the S&P 500 (+0.95%) extended its existing gains in the US afternoon. That now brings the index’s gains for the week as a whole to +1.98%, so leaving it on track to end a run of 7 consecutive weekly declines, assuming it can hold onto that over the next 48 hours, and futures this morning are only down -0.13%. That said, we’ve seen plenty of volatility in recent weeks, and after 3 days so far this is the first week in over two months where the S&P hasn’t seen a fall of more than -1% in a single session, so let’s see what today and tomorrow bring. In terms of the specific moves yesterday, it was a fairly broad advance, but consumer discretionary stocks (+2.78%) and other cyclical industries led the way, with defensives instead seeing a much more muted performance. Tech stocks outperformed, and the NASDAQ (+1.51%) came off its 18-month low, as did the FANG+ index (+1.99%).

Over in Europe, equities also recorded a decent advance, with the STOXX 600 gaining +0.63%, whilst bonds continued to rally as well, with yields on 10yr bunds (-1.5bps) OATs (-1.5bps) and BTPs (-2.7bps) all moving lower. These gains for sovereign bonds have come as investors have grown increasingly relaxed about inflation in recent weeks, with the 10yr German breakeven falling a further -4.2bps to 2.23% yesterday, its lowest level since early March and down from a peak of 2.98% at the start of May. Bear in mind that the speed of the decline in the German 10yr breakeven over the last 3-4 weeks has been faster than that seen during the initial wave of the Covid pandemic, so a big shift in inflation expectations for the decade ahead in a short space of time that’s reversed the bulk of the move higher following Russia’s invasion of Ukraine. Nor is that simply concentrated over the next few years, since the 5y5y forward inflation swaps for the Euro Area looking at inflation over the five years starting in five years’ time has come down from aa peak of 2.49% earlier this month to 2.07% by the close last night, so almost back to the ECB’s target. To be fair there’s been a similar move lower in US breakevens too, and this morning the 10yr US breakeven is down to a 3-month low of 2.56%.

That decline in inflation expectations has come as investors have ratcheted up their expectations about future ECB tightening. Yesterday, the amount of tightening priced in by the July meeting ticked up a further +0.2bps to 32.7bps, its highest to date, and implying some chance that they’ll move by more than just 25bps. We heard from a number of additional speakers too over the last 24 hours, including Vice President de Guindos who said in a Bloomberg interview that the schedule for rate hikes outlined by President Lagarde was “very sensible”, and that the question of larger hikes would “depend on the outlook”.

Overnight in Asia, equities are fluctuating this morning after China’s Premier Li Keqiang struck a downbeat note on the economy yesterday. Indeed, he said that the difficulties facing the Chinese economy “to a certain extent are greater than when the epidemic hit us severely in 2020”. As a reminder, our own economist’s forecasts for GDP growth this year are at +3.3%, which if realised would be the slowest in 46 years apart from 2020 when Covid first took off. Against that backdrop, there’s been a fairly muted performance, and whilst the Shanghai Composite (+0.65%) and the CSI 300 (+0.60%) have pared back initial losses to move higher on the day, the Hang Seng (-0.13%) has lost ground and the Nikkei (+0.07%) is only just in positive territory. We’ve also seen the Kospi (-0.08%) give up its initial gains overnight after the Bank of Korea moved to hike interest rates once again, with a 25bp rise in their policy rate to 1.75%, in line with expectations. That came as they raised their inflation forecasts, now expecting CPI this year at 4.5%, up from 3.1% previously. At the same time they also slashed their growth forecast to 2.7%, down from 3.0% previously.

There wasn’t much in the way of data yesterday, though we did get the preliminary reading for US durable goods orders in April. They grew by +0.4% (vs. +0.6% expected), although the previous month was revised down to +0.6% (vs. +1.1% previously). Core capital goods orders were also up +0.3% (vs. +0.5% expected).

To the day ahead now, and data releases from the US include the second estimate of Q1 GDP, the weekly initial jobless claims, pending home sales for April, and the Kansas City Fed’s manufacturing index for May. Meanwhile in Italy, there’s the consumer confidence index for May. From central banks, we’ll hear from Fed Vice Chair Brainard, the ECB’s Centeno and de Cos, and also get decisions from the Central Bank of Russia and the Central Bank of Turkey. Finally, earnings releases include Costco and Royal Bank of Canada.

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED UP 15.65 PTS OR 0.50% //Hang Sang CLOSED UP 55.07 PTS OR 0.27% /The Nikkei closed DOWN 72.96 OR 0.27% //Australia’s all ordinaires CLOSED DOWN 0.71% /Chinese yuan (ONSHORE) closed DOWN 6,7360 /Oil DOWN TO 111.01dollars per barrel for WTI and UP TO 114.41 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.73604 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7604: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER/

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA/

3B JAPAN

end

3c CHINA

/ECONOMY

China builds the world’s first artificial intelligence powered drone carrier for maritime operations

(zerohedge)

China Builds World’s First AI-Powered Drone Carrier For Maritime Operations

WEDNESDAY, MAY 25, 2022 – 11:20 PM

The latest observation of how China aims to use artificial intelligence to conquer the Pacific is the launching of the world’s first autonomous drone carrier.

According to the South China Morning Post, the intelligent, unmanned 88-meter drone carrier named Zhu Hai Yun will bring revolutionary changes to ocean surveillance, deploying a swarm of aerial, sea, and or submersible drones.

The Zhu Hai Yun is powered by an artificial intelligence system called the Intelligent Mobile Ocean Stereo Observing System (IMOSOS). The vessel can navigate autonomously in open water and or be controlled remotely while releasing various types of drones.

“The intelligent, unmanned ship is a beautiful, new ‘marine species’ that will bring revolutionary changes for ocean observation,” Chen Dake, director of the laboratory responsible for the ship, was quoted as saying by the Science and Technology Daily in 2021 when the shipbuilding began.

The ship was built by Guangzhou of the Huangpu Wenchong Shipyard, a subsidiary of China’s top shipbuilding company, the China State Shipbuilding Corporation. Sea trials will happen in the second half of the year.

Aside from these civilian uses, the drone carrier could be used for military operations.

Suppose the autonomous drone carrier is transferred to the People’s Liberation Army Navy (PLAN). In that case, it could be used as a surveillance craft to patrol the country’s militarized islands in the South China Sea.

China’s primary strategy is to defeat the US by expanding its artificial intelligence military capabilities. So this could be the beginning of the world’s second-largest superpower building out a fleet of intelligent drone carriers to patrol highly contested waters.

Meanwhile, the US Navy has piloted drone ships in the Pacific, though only equipped for anti-submarine warfare.

END

APPLE/CHINA

Apple’ iphone production to remain flat as supply chain woes wount

(zerohedge)

Apple’s iPhone Production To Remain Flat As Supply Chain Woes Mount

THURSDAY, MAY 26, 2022 – 06:55 AM

Apple shares are lower premarket following a new report that iPhone production will be flat this year, according to Bloomberg, citing people familiar with its projections.

Market forecasts, including ones from IDC Research and Bloomberg Intelligence analysts, had predicted total production figures for the year at around 240 million units. However, sources say output could be 8.3% lower, at about 220 million.

One of the world’s biggest companies, Apple, isn’t immune to the continuing effects of supply chain disturbances stoked by China’s zero COVID policy, disrupting factories in the Shanghai area since late March. Last month, the tech behemoth warned it would recognize a $4 billion to $8 billion range hit in the current quarter because of the disruptions.

Nikkei Asia reported Wednesday that at least one of Apple’s new iPhone 14 models could experience delays in mass production because of the disorder in Shanghai.

A supply chain analyst with the Taiwan Institute for Economic Research, Chiu Shih-fang, told Nikkei: “China has not yet returned to normal” despite strict zero-COVID policies easing in the greater Shanghai area. The analyst noted, “It would take at least one to two more months for the supply chain to recover.”

Here’s a glimpse into Apple’s supply chain.

Apple’s overreliance on Shanghai factories for the final assembly of its iPhones shows tremendous weakness in its supply chains to mitigate disruptions (and inability to shift production elsewhere).

It’s just not Apple. The overall smartphone industry is in turbulent times. Strategy Analytics expects global smartphone shipments to decline 2% in 2022, and TrendForce downgraded the full-year production forecast earlier this month.

Apple shares have been hammered into a bear market since the end of March. As of 0630ET, premarket trading is down 1.5%.

On the demand side, Apple is betting its more affluent customer base will fuel new sales, according to the people. They added there’s less competition in the global smartphone market now that some Western governments have banned rival Huawei Technologies Co. and other Chinese phone makers.

Apple also faces high inflation in a low-growth economy. It released a statement Wednesday about increasing wages for workers by 10%. Today’s news of the possibility of lower production of its top-selling product could cut into margins.

end

4/EUROPEAN AFFAIRS//UK AFFAIRS/

end

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

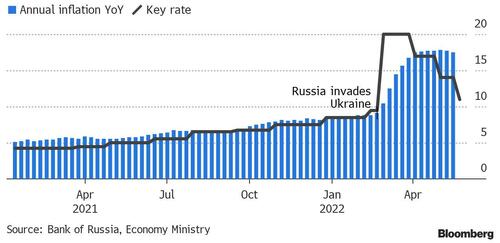

Inflation easing in Russia as controls keep the rouble strong:

Reuters/special thanks to Doug C for sending this to us;