May 27, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

May 27, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1853.95 UP $4.95

SILVER: $22.07 UP $.10

ACCESS MARKET: GOLD $1853.20

SILVER: $22.11

Bitcoin morning price: $28,914 DOWN 543

Bitcoin: afternoon price: $28,458 DOWN 999

Platinum price: closing UP $8.00 to $957.15

Palladium price; closing UP $52.00 at $2062.15

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE: COMEX

JPMorgan issued 11/19

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT 19 NOTICE(S) FOR 1900 OZ (0.05909 TONNES)

total notices so far: 6466 contracts for 646600 oz (20.111 tonnes)

SILVER NOTICES:

25 NOTICE(S) FILED 125,000 OZ/

total number of notices filed so far this month 5632 : for 28,166,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $4.95

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A HUGE DEPOSIT OF 1.74 TONNES INTO THE GLD

INVENTORY RESTS AT 1069.81 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 10 CENTS

AT THE SLV// A BIG CHANGE IN SILVER INVENTORY AT THE SLV://A HUGE CHANGE IN SILVER INVENTORY

AT THE SLV.: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 558.071 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GOOD SIZED 522 CONTRACTS TO 146,803 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GOOD GAIN IN OI WAS ACCOMPLISHED WITH OUR $0.08 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.08) AND ALSO UNSUCCESSFUL IN KNOCKING OFF ANY SILVER LONGS AS THEY REMAIN FIRM IN THEIR BELIEF OF A SILVER FAILURE AS WE HAD A STRONG NET GAIN OF 923 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 30.170 MILLION OZ FOLLOWED BY TODAY’S 305,000 OZ QUEUE JUMP //NEW STANDING 28,120,000 MILLION OZ/ // V) GOOD SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -1

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTACTS for 19 days, total 20,827, contracts: 104.135 million oz OR 5.473 MILLION OZ PER DAY. (1096CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 104.135 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 104.135 MILLION OZ//INCREASING AGAIN

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 522 WITH OUR $0.08 GAIN IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE CONTRACTS: 400 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAY. OF 30.170 MILLION OZ FOLLOWED BY TODAY;S 110,000 OZ QUEUE. JUMP //NEW STANDING 28.120 MILLION OZ// .. WE HAD A STRONG SIZED GAIN OF 922 OI CONTRACTS ON THE TWO EXCHANGES FOR 4.610 MILLION OZ WITH THE GAIN IN PRICE.

WE HAD 25 NOTICE FILED TODAY FOR 125,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2753 CONTRACTS TO 523,307 AND FURTHER FROM NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: –310 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE FAIR SIZED LOSS IN COMEX OI CAME DESPITE OUR GAIN IN PRICE OF $2.70//COMEX GOLD TRADING/THURSDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR GIGANTIC SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //JUST SPECULATOR SHORT COVERING FROM OUR STUPID SPECULATORS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 5.353 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY”S QUEUE JUMP OF 0 OZ//NEW STANDING 20.111 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $2.70 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A SMALL SIZED LOSS OF 1503 OI CONTRACTS 4,674 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 1250 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 523,307

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1503, WITH 2753 CONTRACTS DECREASED AT THE COMEX AND 1250 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF2853 CONTRACTS OR 8.811 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1250) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2753,): TOTAL LOSS IN THE TWO EXCHANGES 1503 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY. AT 5.353 TONNES FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 0 OZ//NEW STANDING 20.11 /// 3) ZERO LONG LIQUIDATION//CONSIDERABLE SPECULATOR SHORT COVERING //.,4) FAIR SIZED COMEX OI. LOSS 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

77,833 CONTRACTS OR 7,783,300 OR 242.09 TONNES 19 TRADING DAY(S) AND THUS AVERAGING: 4096 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAY(S) IN TONNES: 242.09 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 242.09/3550 x 100% TONNES 6.82% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 242,09 TONNES INITIAL// INCREASING AGAIN

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GOOD SIZED 522 CONTRACT OI TO 146,804 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 400 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 400 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 522 CONTRACTS AND ADD TO THE 400 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 922 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 4.610 MILLION OZ

OCCURRED WITH OUR GAIN IN PRICE OF $0.08 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

end

end

5. Other gold commentaries

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED UP 7.13 PTS OR 0.23% //Hang Sang CLOSED UP 581.16 PTS OR 2.89% /The Nikkei closed UP 176.84 OR 0.66% //Australia’s all ordinaires CLOSED UP 1.01% /Chinese yuan (ONSHORE) closed UP 6,7056 /Oil UP TO 113.57dollars per barrel for WTI and UP TO 117.16 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7056 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7240: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER/

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2753 CONTRACTS TO 523,307 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS FAIR COMEX DECREASE OCCURRED DESPITE OUR GAIN OF $2,10 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A SMALL SIZED EFP (1250 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ARE CAUGHT. THE COMMERCIALS WILL SLAUGHTER THESE GUYS WHEN THEY THINK THE TIME IS RIGHT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1250 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :1250 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1250 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 1503 CONTRACTS IN THAT 1250 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 2753 CONTRACTS..AND YET THIS STRONG LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF GOLD $2.70.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (20.11),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $2.70) BUT WERE SUCCESSFUL IN KNOCKING OFF SOME SPECULATOR LONGS/COMMERCIAL LONGS AS WELL AS SPECULATOR SHORTS//// WE HAVE REGISTERED A SMALL SIZED LOSS OF 4.674 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAY (20.11 TONNES)…

WE HAD 310 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 1503 CONTRACTS OR 150300 OZ OR 4.674 TONNES

Estimated gold volume 147,688/// poor

Confirmed volume yesterday:221,926 contracts fair

INITIAL STANDINGS FOR MAY ’22 COMEX GOLD //MAY 27

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | nil oz |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 19 notice(s) 1900 OZ 0.0599 TONNES |

| No of oz to be served (notices) | 0 contracts 00 oz 0.00 TONNES |

| Total monthly oz gold served (contracts) so far this month | 6466 64600 20.111TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit 0 oz//

No dealer withdrawals

0 customer deposits

total deposits: nil oz

0 customer withdrawals:

total withdrawal: nil oz

ADJUSTMENTS: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 19 contracts having LOST 16 contracts

We had 16 notices filed YESTERDAY, so we gained 0 contracts or AN ADDITIONAL NIL oz will stand for delivery in this non active delivery month of May.

June saw a loss of 30,127 contracts down to 37,092 contracts//June standing will be very strong

July has a GAIN OF 429 OI to stand at 1695

August has a gain of 26,121 contracts up to 421,917 contracts

We had 19 notice(s) filed today for 1900 oz FOR THE MAY 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 19 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 11 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2021. contract month,

we take the total number of notices filed so far for the month (6466) x 100 oz , to which we add the difference between the open interest for the front month of (MAY 19 CONTRACTS ) minus the number of notices served upon today 19 x 100 oz per contract equals 6,666,000 OZ OR 20.11 TONNES the number of TONNES standing in this non active month of MAY.

thus the INITIAL standings for gold for the MAY contract month:

No of notices filed so far (6466) x 100 oz+ (19) OI for the front month minus the number of notices served upon today (19} x 100 oz} which equals 646,600 oz standing OR 20.111 TONNES in this NON active delivery month of MAY.

TOTAL COMEX GOLD STANDING: 20.111 TONNES (A STRONG STANDING FOR A MAY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,130,325.976 oz

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 35,520,541.296 OZ

TOTAL ELIGIBLE GOLD: 17,398,567.733 OZ

TOTAL OF ALL REGISTERED GOLD: 18,121,973.563 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,991.648.0 OZ (REG GOLD- PLEDGED GOLD)

END

MAY 2022 CONTRACT MONTH//SILVER//MAY 27

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 604,551.640 oz Brinks JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,219,304.600 oz Malca |

| No of oz served today (contracts) | 25CONTRACT(S)125,000 OZ) |

| No of oz to be served (notices) | 0 contracts (0 oz) |

| Total monthly oz silver served (contracts) | 5632 contracts 28,160,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) zero dealer deposits And now for the wild silver comex results

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

i) Into Malca: 1,219.304.600 oz

total deposit: 1,219,304.600 oz

JPMorgan has a total silver weight: 174.032 million oz/336.359 million =51.72% of comex

Comex withdrawals: 2

i) Out of Brinks 99,663.640 oz

ii) Out of JPMorgan: 504,888.000 oz

total withdrawal 604,551.640 oz

4 adjustments: dealer to customer:

a) Brinks: 459,966.580 oz

b) Int. Delaware: 155,035.105 oz

c) JPMorgan: 3,380,556.640 oz

d) Malca: 551,742.632 iz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 75.474 MILLION OZ

TOTAL REG + ELIG. 336.359 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY OI: 25 HAVING LOST 61 CONTRACTS. WE HAD 83 NOTICES FILED ON YESTERDAY

SO WE GAINED 22 CONTRACTS OR A QUEUE JUMP OF 110,000 OZ

JUNE HAD A LOSS OF 21 TO STAND AT 1558

JULY HAD A LOSS OF 904 CONTRACTS DOWN TO 109,486 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 25 for 125,000 oz

Comex volumes: 39,807// est. volume today// poor

Comex volume: confirmed yesterday: 33,463 contracts ( poor )

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 5632 x 5,000 oz = 28,160,000 oz

to which we add the difference between the open interest for the front month of MAY(25) and the number of notices served upon today 25 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY./2022 contract month: 5632 (notices served so far) x 5000 oz + OI for front month of MAY (25) – number of notices served upon today (25) x 5000 oz of silver standing for the MAY contract month equates 28,160,000 oz. .

We GAINED 22 contracts or AN ADDITIONAL 110,000 OZ will stand for delivery at the comex

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

MAY 18/WITH GOLD DOWN $2.55//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.07 TONNES FROM THE GLD///INVENTORY RESTS AT 1049.21 TONNES

MAY 17/WITH GOLD UP $5.40:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1053.28 TONNES

MAY 16/WITH GOLD UP $5.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD///INVENTORY RESTS AT 1055.89 TONNES

MAY 13/ WITH GOLD DOWN $16.25//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.8 TONNES FROM THE GLD.//INVENTORY RESTS AT 1060.82 TONNES

MAY 12/WITH GOLD DOWN $26.50: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD////INVENTORY RESTS AT 1066.62 TONNES

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

GLD INVENTORY: 1069/81 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

MAY 18/WITH SILVER UP $0.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL 1.892 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 17/WITH SILVER UP $.22 TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.508 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 16/WITH SILVER UP $.52 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.546 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.593 MILLION OZ//

MAY 13/WITH SILVER UP 31 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ/

MAY 12/WITH SILVER DOWN 88 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ//

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

INVENTORY TONIGHT RESTS AT 558.071 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/

END

3. Chris Powell of GATA provides to us very important physical commentaries

end

4.OTHER GOLD/SILVER COMMENTARIES

Bill is interviewed by Andrew Maguire at Live from the Vault.

Attachments area

Ep 75: Live From The Vault – Why The Western Economy Can’t Survive. Feat. Bill Holter

end

5.OTHER COMMODITIES //PALM OIL+ OTHERS

END

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.7056

OFFSHORE YUAN: 6.7240

HANG SANG CLOSED UP 581.16 PTS OR 2.89%

2. Nikkei closed UP 176.84 OR 0.66%

3. Europe stocks ALL CLOSED ALL GREEEN

USA dollar INDEX DOWN TO 101.83/Euro FALLS TO 1.0708

3b Japan 10 YR bond yield: FALLS TO. +.225/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 126.92/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN -SHORE CLOSED UP// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +0.859%/Italian 10 Yr bond yield FALLS to 2.75% /SPAIN 10 YR BOND YIELD FALLS TO 1.90%…

3i Greek 10 year bond yield FALLS TO 3.47

3j Gold at $1857.85 silver at: 22.28 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0.41 roubles/dollar; ROUBLE AT 65.67

3m oil into the 114 dollar handle for WTI and 117 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 126.92DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9588– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0268well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.725 DOWN 3 BASIS PTS

USA 30 YR BOND YIELD: 2.952 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 16.39

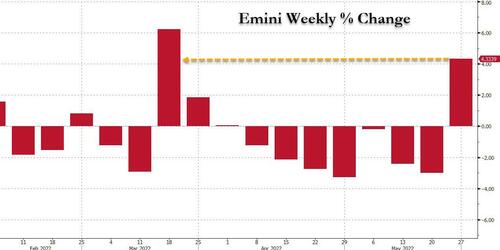

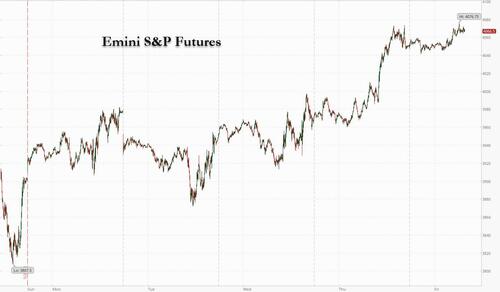

Futures Rise As Dip Buyers Emerge To Cap Best Week Since Mid-March

FRIDAY, MAY 27, 2022 – 07:54 AM

Unless stocks crater today, and the S&P tumbles by 4.3%, the streak of seven consecutive weekly declines in the S&P is about to end…

… as US stock futures rose again on Friday, their third consecutive gain, setting up the underlying indexes for the first strong weekly finish since late March on signs consumers remain resilient despite inflationary pressures, as upbeat earnings from Alibaba and Baidu eased some fears on the economic impact of China’s Covid lockdowns, and as investors (mostly retail) have staged a cautious return to the market hoping that the selloff earlier this month left valuations at bargain levels. Nasdaq 100 contracts rose 0.5% by 7:15 a.m. in New York, while S&P 500 futures were up 0.4%. Still, even after the recent rout, upside may be limited as the S&P 500’s 12-month fwd P/E ratio is now near its 10-year average.

Among notable moves in premarket trading, Gap Inc. shares sank as much as 17% as analysts after analysts said that the retailer’s guidance cut was worse than expected, prompting brokers to lower their targets and downgrade the stock given a worsening macroeconomic environment could trigger further bad news. China’s Uber, Didi Chuxing, jumped after a Bloomberg News report that state-owned automaker China FAW Group is considering acquiring a significant stake in the ride-hailing company. Zscaler Inc. rose after the security software company reported results above expectations. Here are some other notable premarket movers:

- Gap (GPS US) shares dropped as much as 17% in US premarket trading with analysts saying that the retailer’s guidance cut was more than expected, prompting brokers to lower their targets and downgrade the stock given a worsening macroeconomic environment could trigger further bad news.

- Costco (COST US) shares dropped 2.1% in US after-hours trading on Thursday. While Costco’s margins disappointed analysts, brokers were generally positive on how the wholesale retailer is navigating an environment with rising inflation by controlling expenses.

- Zscaler (ZS US) shares rose 2% in extended trading on Thursday, after the security software company reported third- quarter results that beat expectations and raised its full-year forecast. Analysts lauded strength in multi-product deals.

- Marvell Technology (MRVL US) shares climbed 3.4% in US postmarket trading after results. Analysts highlighted that the semiconductor maker is seeing strength across key markets, in particular across data center and carrier infrastructure.

- 23andMe Holding Co. (ME US) dropped 8.3% in postmarket trading Thursday. It is in a “tough spot,” Citi says in note after the consumer genetics firm gave a fiscal 2023 revenue forecast that missed expectations.

- Workday (WDAY US) shares fell 9% in extended trading on Thursday, after the software company reported adjusted first-quarter earnings that missed expectations. Analysts noted that software deals were pushed out of the quarter and cut their price targets as they factored in the increased global uncertainty.

The latest round of retail earnings have restored some confidence in consumer demand, lifting appetite for risk assets, while speculation is growing that the Federal Reserve will pause its rate hikes later this year as inflation shows signs of peaking. Still, Citigroup strategists on Friday cut their recommendation on US stocks to neutral on the risk of a recession, joining an increasing number of banks in warning of a growth slowdown.

The path for the Federal Reserve to successfully bring inflation down while keeping the rate of economic growth above zero is narrow, according to Mark Haefele, chief investment officer at UBS Global Wealth Management. “If Fed policymakers underestimate the strength of the US economy, we face an extended period of above-target inflation. If they overestimate it, we face a recession. And we can’t know with great conviction which path we’re on,” he wrote in a note.

Global stock funds saw their biggest inflows in 10 weeks, led by US stocks, according to EPFR data, as cheaper valuations lured buyers after a steep selloff on recession fears. The selloff made valuations attractive and enticed investors back into a market still shadowed by worries about inflation and higher interest rates, China’s downbeat economic outlook and the war in Ukraine.

“We may see a little bit more stability here because we have repriced the stocks so much already,” Anastasia Amoroso, iCapital chief investment strategist, said on Bloomberg Television. “In the next three to six months it’s still going to be a constrained market environment.”

Meanwhile, China-US tensions are once again being played out after direct comments from Secretary of State Antony Blinken aimed at Chinese President Xi Jinping. And in a fresh challenge to Beijing, the US and Taiwan are planning to announce negotiations to deepen economic ties.

And elseshwere, as the Russins war in Ukraine approaches 100 days, the US may announce a new package of aid for Kyiv as soon as next week that would include long-range rocket systems and other advanced weapons. Boris Johnson urged further military support for Ukraine, including sending it more offensive weapons such as Multiple Launch Rocket Systems that can strike targets from much further away. Russia’s efforts to avoid its first foreign default in a century are back in focus on Friday, when investors are supposed to receive about $100 million in interest on Russian debt.

Turning back to markets, consumer and technology sectors led gains in Europe’s Stoxx 600 which rose 0.9%, and was headed for its best weekly advance since mid-March, while utilities and energy shared lagged after the UK government announced windfall tax plans on oil and gas companies on Thursday. BP Plc said it will look again at its plans in the country. Here are some of the more notable movers in Europe:

- Cantargia gains as much as 23%, the largest intraday rise since December, after releasing three research updates late Thursday. The interim readout for the company’s nadunolimab (CAN04), used in combination with gemcitabine and nab-paclitaxel as a first line treatment of PDAC, a type of pancreatic cancer, was the most interesting of the data releases, according Kempen.

- FirstGroup shares jump as much as 9.8%, extending the gains from yesterday’s confirmation that the public transport operator received an unsolicited takeover approach from I Squared.

- Richemont shares rise as much as 8.3%, heading for their best weekly advance since November, pushing the Swiss Market Index higher as dip buyers returned more broadly this week.

- European miners advance for a third day, outperforming all other sectors on the Stoxx 600 on Friday as iron ore futures climb and metals posted broad gains.

- Hapag-Lloyd falls as much as 7.1% after Citi cut the recommendation to neutral from buy due to valuation versus peers. In note on European shipping, broker says it expects the supply and demand dynamics to remain favorable in the near term.

- Rieter Holding falls as much as 5.4% as Baader Helvea downgrades its recommendation to reduce from add after the manufacturer of chemical fiber systems said that it’s seeing a challenging first half.

Earlier in the session, Asian stocks also advanced as upbeat earnings from Alibaba and Baidu eased some fears on the economic impact of China’s Covid lockdowns and fueled risk-on sentiment. The MSCI Asia Pacific Index rose 1.6%, poised for its first gain in four sessions, led by consumer discretionary and technology shares. Most markets in the region were up, led by Hong Kong. Alibaba and Baidu both delivered better-than-expected quarterly sales growth, providing investors with some relief after Tencent’s recent lackluster report and amid concerns over China’s virus measure and regulatory crackdowns. The Hang Seng Tech Index, which tracks the nation’s tech giants listed in Hong Kong, surged 3.8%. Asian equities have gained about 0.7% this week, set for a back-to-back weekly advance as dip buyers emerged. The regional MSCI benchmark is still down about 14% this year amid ongoing market concerns over global inflation and higher US interest rates, China’s economic outlook and the war in Ukraine.

“The risk of a bull trap cannot be dismissed,” Vishnu Varathan, the head of economics and strategy at Mizuho Bank, wrote in a note. “Bear markets are famous for the pockets of relief rallies,” and increasing strains on liquidity in the coming quarters “may not pass without pain.”

Japan’s stocks likewise advanced as the nation prepared to reopen to foreign tourists and China’s tech shares jumped. The Topix rose 0.5% to 1,887.30 as of the 3pm close in Tokyo, while the Nikkei 225 advanced 0.7% to 26,781.68. Tokyo Electron Ltd. contributed the most to the Topix’s gain, increasing 3.2%. Out of 2,171 shares in the index, 1,480 rose and 615 fell, while 76 were unchanged

In Australia, the S&P/ASX 200 index rose 1.1% to close at 7,182.70, the highest level since May 6, led by energy and consumer discretionary shares. Woodside Energy Group was among the biggest gainers as US crude and gasoline stockpiles showed signs of continuing decline ahead of the summer driving season. Appen was the top decliner after saying that Telus revoked its indicative proposal for a takeover. In New Zealand, the S&P/NZX 50 index fell 0.3% to 11,065.15

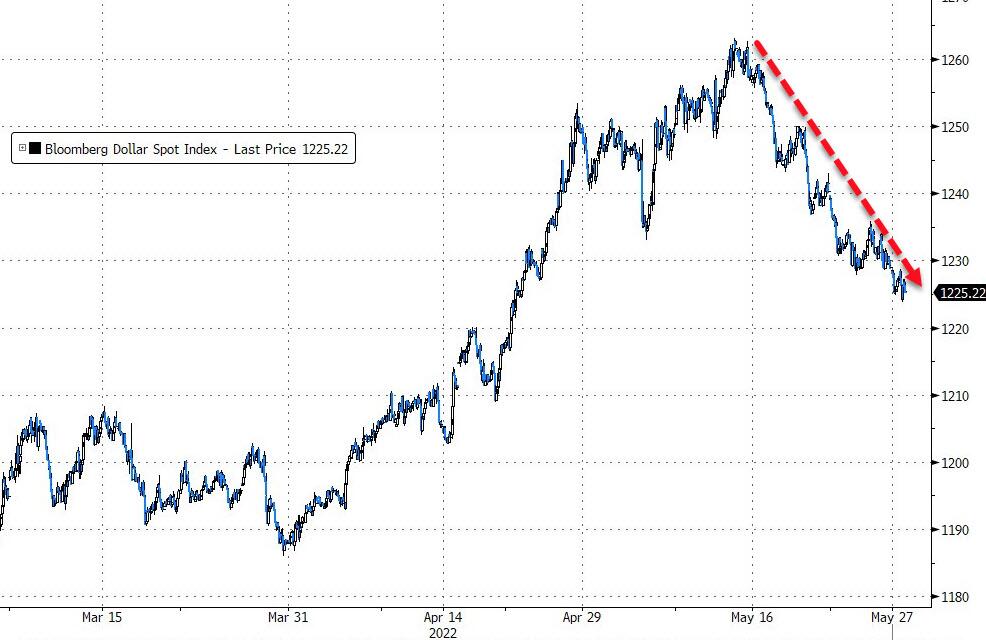

In FX, the Bloomberg Dollar Spot Index slumped as the dollar was steady to weaker against all of its Group-of-10 peers. Treasuries were steady across the curve. The euro inched up to touch a fresh one- month high of 1.0765 before paring. The bund yield curve bull- flattened slightly, drawing the 10-year yield away from 1%. Risk- sensitive Antipodean and Scandinavian currencies led gains. The Australian dollar climbed as a decent retail sales print brightened the outlook and a drop in the greenback triggered buy-stops. Benchmark bonds slipped. Australian retail sales rose 0.9% m/m in April vs estimate +1% and prior +1.6%. The pound ticked higher, touching its highest level in a month against the dollar, while gilts advanced. Chancellor of the Exchequer Rishi Sunak said that his package of support for the UK economy will have a “minimal” impact on inflation. The yen advanced for a second day as lower Treasury yields weighed on the dollar. Japanese bonds rise after being sold off on Thursday

In rates, Treasuries were steady, following gains in European markets where bull-flattening was observed across bunds and gilts. Yields were richer by 1bp-3bp across the curve, the 10-year yield dropped by ~2bp to 2.72%, underperforming bunds by 1.5bp, gilts by ~3bp. IG dollar issuance slate still blank in what has so far been the slowest week of the year for new deals; next week’s calendar is expected to total $25b- $30b. Focal points for US session include several economic data releases including April personal income/spending with PCE deflator. Sifma recommended 2pm close of trading for dollar-denominated fixed income ahead of US holiday weekend.

In commodities, WTI drifts 0.7% higher to trade below $115. Spot gold rises roughly $7 to trade at $1,858/oz. Most base metals are in the green; LME nickel rises 6.6%, outperforming peers.

Looking to the day ahead, and data releases include US personal income and personal spending for April, as well as the preliminary wholesale inventories for that month, and the final University of Michigan consumer sentiment index for May. In the Euro Area, there’s also the M3 money supply for April. Otherwise, central bank speakers include ECB Chief Economist Lane.

Market Snapshot

- S&P 500 futures up 0.3% to 4,068.25

- STOXX Europe 600 up 0.7% to 440.64

- MXAP up 1.6% to 165.89

- MXAPJ up 2.1% to 542.44

- Nikkei up 0.7% to 26,781.68

- Topix up 0.5% to 1,887.30

- Hang Seng Index up 2.9% to 20,697.36

- Shanghai Composite up 0.2% to 3,130.24

- Sensex up 1.2% to 54,919.92

- Australia S&P/ASX 200 up 1.1% to 7,182.71

- Kospi up 1.0% to 2,638.05

- German 10Y yield little changed at 0.99%

- Euro up 0.1% to $1.0737

- Brent Futures up 0.4% to $117.91/bbl

- Gold spot up 0.5% to $1,859.48

- U.S. Dollar Index down 0.16% to 101.67

Top Overnight News from Bloomberg

- The path for Russia to keep sidestepping its first foreign default in a century is turning more onerous as another coupon comes due on the warring nation’s debt. Investors are supposed to receive about $100 million of interest on Russian foreign debt in their accounts by Friday, payments President Vladimir Putin’s government says it has already made

- China’s oil trading giant Unipec has significantly increased the number of hired tankers to ship a key crude from eastern Russia

- A central bank legal proposal envisages Russian eurobond issuers placing “substitute” bonds in order to ensure debt payments come through to local investors, Interfax reported

- The US and Taiwan are planning to announce negotiations to deepen economic ties, people familiar with the matter said, in a fresh challenge to Beijing, which has cautioned Washington on its relationship with the island.

- Profits at Chinese industrial firms shrank last month for the first time in two years as Covid outbreaks and lockdowns disrupted factory production, transport logistics and sales

- “The process of increasing interest rates should be gradual,” ECB Governing Council member Pablo Hernandez de Cos comments in op- ed in Expansion. “The aim is to avoid abrupt movements, which could be particularly damaging in a context of high uncertainty such as the current one”

- The RBA is poised for its first review in a generation as new Treasurer Jim Chalmers makes good on a pledge to ensure the nation’s monetary and fiscal regimes are fit for purpose

- The UK signed its first trade agreement with a US state, amid warnings that Prime Minister Boris Johnson’s stance on Brexit is hindering progress on a broader deal with Joe Biden’s administration

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks took impetus from the risk-on mood on Wall St where all major indices were lifted amid month-end flows and encouraging retailer earnings. ASX 200 was led higher by outperformance in the commodity and resources industries, while consumer stocks were mixed after Retail Sales printed in line with expectations, albeit at a slowdown from the prior month. Nikkei 225 traded positively but with upside capped by a mixed currency and weakness in energy and power names after increases in international prices and with the government looking to address the tight energy market. Hang Seng and Shanghai Comp were firmer with notable outperformance in Hong Kong amid a euphoric tech sector after earnings from Alibaba and Baidu topped estimates which also inspired the NASDAQ Golden Dragon China Index during the prior US session, while advances in the mainland were moderated by the contraction in April Industrial Profits and after Premier Li’s unpublished comments from Wednesday’s emergency meeting came to light in which he warned of dire consequences for the economy.

Top Asian News

- China’s State Council will seek specific implementation rules by May 31st regarding necessary measures at all levels of government and will dispatch inspection teams to all 31 provinces, municipalities and autonomous regions to oversee the rollout amid an urgent need for national economic mobilisation, according to SGH Macro Advisors.

- US is seeking to hold economic discussions with Taiwan in the latest test with China, while supply chains and agriculture are said to be among the topics, according to Bloomberg. Furthermore, reports noted that bilateral economic talks will be announced in the upcoming weeks.

- Evergrande (3333 HK) is reportedly considering repaying offshore bondholders in instalments, according to Reuters sources; discussing giving the option of converting part of debt into equity of property management and EV units.

- China’s Health Official says some areas along the Jilin border report local infections without a clear source, close attention should be paid to the risk of importing the virus; COVID infections show a trend of gradual spread from border to inland areas, via Reuters

European bourses are firmer, Euro Stoxx 50 +0.9%, drawing impetus from APAC strength into month-end with catalysts thin thus far. Stateside, futures are supported across the board with familiar themes in play pre-PCE Price Index for insight into the ‘peak’ inflation narrative; ES +0.3%. Note, the FTSE 100 Unch. is the mornings underperformer amid pressure in energy names after Chancellor Sunak’s windfall tax announcement on Thursday. DiDi (DIDI) has reportedly drawn interest from FAW Group, regarding a stake purchase, according to Bloomberg. +7.5% in the pre-market

Top European News

- UK Oil Windfall Tax Prompts BP to Review Investment Plans; UK Energy Stocks Extend Windfall Declines as Retailers Gain

- Richemont Leads Swiss Stocks Higher as Dip Buyers Return

- Hapag-Lloyd Drops; Cut to Neutral at Citi on Valuation

- Big Dividend Payers May Be Next After UK Windfall Tax on Energy

FX

- Greenback grinds higher ahead of PCE inflation metrics with month end rebalancing flows providing impetus, DXY bounces from fresh WTD base just under 101.500 to 101.800.

- Kiwi and Aussie propped by bounce in commodities and Loonie protected by further gains in crude; NZD/USD tests Fib retracement at 0.7129, AUD/USD eyes 0.7150 and USD/CAD probes 1.2750.

- Big option expiries in the mix and potentially supportive for the Dollar into long US holiday weekend, +1bln rolling off at NY cut not far from spot in EUR/USD, USD/JPY, AUD/USD and USD/CAD.

- Rand firmer as Gold touches Usd 1860/oz after 200 DMA breach, USD/ZAR below 15.7000.

Fixed Income

- Debt futures on a firmer footing ahead of US PCE price metrics, but some way below weekly peaks.

- Bunds sub-154.00, Gilts under 119.00 and 10 year T-note below 121-00.

- Curves a tad flatter following hot reception for 7 year US issuance.

Commodities

- Crude benchmarks are underpinned, but off best levels, by broader sentiment and initial USD weakness going into a long US weekend with Memorial Day touted as the driving seasons commencement.

- WTI July and Brent August, at best, were in proximity to USD 115/bbl vs troughs of USD 113.61/bbl and USD 113.77/bbl respectively.

- US Treasury is reportedly expected to renew Chevron’s (CVX) license to operate in Venezuela as soon as Friday, according to Reuters citing sources.

- China’s State Planner has approved a coal mine in the Shanxi area to bolster annual output to 12mln tonnes per annum from 8mln; investment of CNY 5.35bln, via Reuters.

- Spot gold is steady and holding onto the bulk of overnight upside after breaching the 21-DMA at USD 1850.80/oz; USD 1860.19/oz peak, thus far.

US Event Calendar

- 08:30: April Advance Goods Trade Balance, est. -$114.8b, prior -$125.3b, revised -$127.1b

- 08:30: April Retail Inventories MoM, est. 2.0%, prior 2.0%

- April Wholesale Inventories MoM, est. 2.0%, prior 2.3%

- 08:30: April Personal Income, est. 0.5%, prior 0.5%; April Personal Spending, est. 0.8%, prior 1.1%

- 08:30: April PCE Deflator MoM, est. 0.2%, prior 0.9%; PCE Deflator YoY, est. 6.2%, prior 6.6%

- April PCE Core Deflator MoM, est. 0.3%, prior 0.3%; PCE Core Deflator YoY, est. 4.9%, prior 5.2%

- April Real Personal Spending, est. 0.7%, prior 0.2%

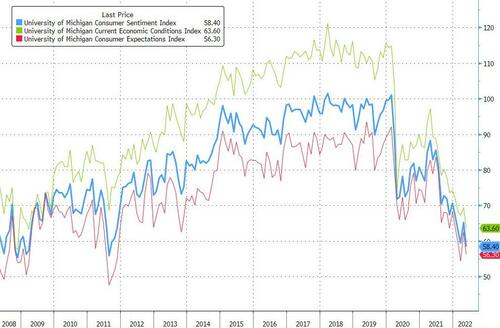

- 10:00: May U. of Mich. Current Conditions, est. 63.6, prior 63.6; Expectations, est. 56.3, prior 56.3; Sentiment, est. 59.1, prior 59.1

- 10:00: May U. of Mich. 1 Yr Inflation, est. 5.4%, prior 5.4%; 5-10 Yr Inflation, prior 3.0%

DB’s Jim Reid concludes the overnight wrap

A reminder that it’s your last chance to answer our latest monthly survey, where we try to ask questions that aren’t easy to derive from market pricing. This time we ask if you think the Fed would be willing to push the economy into recession in order to get inflation back to target. We also ask whether you think there are still bubbles in markets and whether equities have bottomed out yet. And there’s another on which is the best asset class to hedge against inflation. The more people that fill it in the more useful so all help from readers is very welcome. The link is here.

I did have tickets available for tomorrow night’s Champions League final but there is a big 36 hole golf tournament at my club so I decided that at my age you never know when your body will fail next so playing sport now pips watching it live. So I’ll be playing golf all day, trying to rescue my marriage for an hour when I get home, and then blaring out the final on the TV at home with a couple of glasses of wine for good measure. I can’t honestly think of a better day. However I may come last and Liverpool may lose so let’s see what happens!

The market comeback this week is on a par with some of Madrid’s remarkable ones this year and indeed it’s been another strong performance over the last 24 hours, with better-than-expected outlooks from US retailers helping to bolster sentiment, coupled with growing hopes that the Fed won’t take policy much into restrictive territory, if at all. Those developments helped the S&P 500 to post a +1.99% advance yesterday, bringing its gains for the week to +4.01%, and means we should finally be on the verge of ending a run of 7 consecutive weekly losses. Obviously it’s not impossible things could end up in negative territory given recent volatility, and it was only last week the index posted a one-day decline of more than -4%, but it would still take a massive slump today to get an 8th consecutive week in the red for only the third time since the Great Depression.

That advance grew stronger as the day went on, with S&P futures having actually been negative when we went to press yesterday. But sentiment was aided by a number of positive earnings developments, with Macy’s (+19.31%) boosting its adjusted EPS guidance before the US open, whilst the discount retailers Dollar Tree (+21.87%) and Dollar General (+13.72%) both surged as well thanks to decent reports of their own. That helped consumer discretionary (+4.78%) to be the top performing sector in the S&P, and in fact Dollar Tree was the top performing company in the entire index. Cyclicals were the outperformers, but defensives also shared in the advance that saw around 90% of the index’s members move higher on the day.

As well as that news on the retail side, risk appetite has been further supported by growing speculation that the Fed won’t be as aggressive in hiking rates as had been speculated just a few weeks ago. I’m not sure I agree with that conclusion but if you look at the futures-implied rate by the December 2022 meeting of 2.64%, that is some way down from its peak of 2.88% back on May 3rd, and in fact means that markets have now taken out just shy of one 25bp hike from the rate implied by year end, which makes a change from that pretty consistent move higher we’ve seen over recent months.

Yesterday also brought fresh signs that this re-pricing is beginning to filter its way through to the real economy, with data from Freddie Mac showing that the average rate for a 30-year mortgage fell to 5.10% last week, down from 5.25% the week before. For reference that’s the biggest weekly decline since April 2020, and comes on the back of recent housing data that’s underwhelmed against the backdrop of higher rates. There was another report fitting that pattern yesterday too, with pending home sales for April dropping by a larger than expected -3.9% (vs. -2.1% expected). But as with the retail outlooks, the more timely data was much more positive, with the weekly initial jobless claims falling to 210k (vs. 215k expected) in the week ending May 21, whilst the Kansas City Fed’s manufacturing index for May came in at 23 (vs. 15 expected).

Treasuries swung back and forth against this backdrop, but ultimately the more bullish outlook led to a small steepening in the curve, with the 2yr yield down -1.6bps as 10yr yields were essentially flat at 2.75%. In a change from recent weeks, breakevens marched higher despite the little changed headline, with the 10yr breakeven up +7.0bps to come off its two-month low the previous day. But to be fair, that came amidst a big surge in oil prices after US data showed gasoline stockpiles fell to their lowest seasonal level since 2014, with Brent Crude (+2.96%) up to a 2-month high of $117.40/bbl, whilst WTI (+3.41%) rose to $114.09/bbl.

European markets followed a pretty similar pattern to the US, with the STOXX 600 advancing +0.78% on the day. However, utilities (-1.12%) were the worst-performing after the UK government moved to impose a temporary windfall tax on oil and gas firms’ profits at a rate of 25%. That came as part of a wider package of measures to help with the cost of living, adding up to £15bn in total. They included a one-off payment of £650 to 8mn households in receipt of state benefits, with separate payments of £300 to pensioner households and £150 to those receiving disability benefits. There was also a doubling in the energy bills discount from £200 to £400, whilst the requirement to pay it back over five years has been removed as well. See Sanjay Raja’s blog on it here and where he also compares the measures to similar ones seen in the big 4 EuroArea economies.

With more fiscal spending in the pipeline, UK gilts underperformed their counterparts elsewhere in Europe, with 10yr yields ending the day up +5.9bps. Those on bunds (+4.6bps) and OATs (+3.2bps) also rose too, but the broader risk-on tone led to a tightening in peripheral spreads, with the gap between 10yr BTPs over bunds falling -10.4bps yesterday to 189bps. There was a similar pattern on the credit side, with iTraxx crossover coming down -23.9bps to 439bps, which was its biggest daily decline in nearly 2 months.

Asian equity markets are joining in the rally this morning with the Hang Seng rising +2.93% as Chinese listed tech stocks are witnessing big gains after Alibaba (+12.21%) posted better than expected Q4 earnings yesterday. Mainland Chinese stocks are also trading higher with the Shanghai Composite (+0.52%) and CSI (+0.63%) up. Elsewhere, the Nikkei (+0.63%) and Kospi (+0.89%) are also in the green. Outside of Asia, futures contracts on the S&P 500 (-0.11%) and NASDAQ 100 (-0.14%) are seeing mild losses.

Data released earlier showed that Tokyo’s core CPI rose +1.9% y/y in May versus +2.0% expected. Core core was +0.9% y/y as expected with nothing here at the moment to change the BoJ’s stance. Elsewhere, China’s industrial profits (-8.5% y/y) shrank at the fastest pace in two years in April, swinging from a +12.2% gain in March.

On the geopolitical front, we heard from US Secretary of State Blinken yesterday, who gave a significant speech on the Biden Administration’s China policy. Blinken zoomed out to give a view of the forest from the trees, noting that the Russia-Ukraine conflict was not as strategically important as America’s relationship with China over the long-run. He offered a three pillar strategy for managing the relationship with China that involved investing in US competitiveness, aligning strategy with allies to enhance effectiveness, and to compete with China across economic, military, and technological frontiers. He noted the countries’ two different political systems need not impair connection between its peoples, or inhibit dialogue.

Staying on the US-China front but switching gears, a bi-partisan group of US senators sent a letter to President Biden urging him to keep tariffs on China, to improve the US’s negotiating position in future deals, pouring cold water on the prospects for tariff relief to provide a temporary salve to raging price pressures.

To the day ahead, and data releases include US personal income and personal spending for April, as well as the preliminary wholesale inventories for that month, and the final University of Michigan consumer sentiment index for May. In the Euro Area, there’s also the M3 money supply for April. Otherwise, central bank speakers include ECB Chief Economist Lane.

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED UP 7.13 PTS OR 0.23% //Hang Sang CLOSED UP 581.16 PTS OR 2.89% /The Nikkei closed UP 176.84 OR 0.66% //Australia’s all ordinaires CLOSED UP 1.01% /Chinese yuan (ONSHORE) closed UP 6,7056 /Oil UP TO 113.57dollars per barrel for WTI and UP TO 117.16 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7056 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7240: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER/

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA/

3B JAPAN

end

3c CHINA

/ECONOMY

We are now witnessing an open feud between Xi and Li over Xi’s COVID response and that is paralyzing China

(zerohedge)

China Paralyzed As Feud Erupts Between Xi And Li Over Covid Response

THURSDAY, MAY 26, 2022 – 11:00 PM

For the past several months there had been rumors that a quiet feud had erupted within Beijing’s top echelons, the result of disagreement within the communist party whether Xi Jinping’s “zero covid” policy was the proper solution for the country of 1.4 billion and which two and a half years ago unleashed the coronavirus plague on the world. Well, now it’s official because as Bloomberg reported this morning, China finds itself gripped by “discord” at the very top level, with president Xi and premier Li on opposite sides of the the “zero covid” ring.

As Bloomberg notes, shortly after Premier Li Keqiang held the previously discussed “rare” video call with thousands of Chinese officials across the nation to warn of an even worse economic crisis than two years ago, and calling on them to better balance Covid controls and economic growth, those same government officials charged with implementing policy at the ground level found themselves stumped and unsure whether they should still listen to: supreme leader Xi – who continues to emphasize the need for officials to push for zero Covid-19 cases – or Li, who continuously urges them to bolster the economy and hit preordained growth targets.

This apparent dilemma has led to paralysis within a nation normally hailed for speedy implementation of orders from above, Bloomberg reports, citing eight unnamed senior local government officials.

While analysts saw Li’s impromptu meeting as an attempt to strengthen consensus on the urgency to revive the economy, four senior officials said it did little to change their view that controlling the Covid outbreak still took priority: “One said that from a personal career perspective, a cadre’s hard work means nothing if they fail to contain an outbreak, while the upside for kicking off economic projects was limited.”

For a glaring example of just how deep the schism within China’s core runs, one should look at who did not attend Li’s mammoth meeting – which brought together cadres right down to the county level, featuring officials from nearly all government departments including propaganda, environment, and utilities, according to notices on county-level government websites – the top-ranking Communist Party official for many cities was absent because they had to focus on ensuring Covid control, said a BBG source, adding that it signaled that pandemic work still trumped the economy. Attendance for party heads wasn’t mandatory.

Which is bad news for Li who is tasked with restoring the economy… without actually being allowed to do anything:

“He is being put in the impossible position of trying to rescue the economy without being able to adjust the one policy — zero-Covid — that is causing the most economic damage,” McArver said, referring to Li.

For Li, who will depart the post of China’s second in command next March, the stakes couldn’t be higher: the Chinese Communist Party prepares to hold a twice-a-decade leadership conclave later this year, where Xi is expected to win a landmark third term, yet where rumor also has it some of his challengers are sharpening their knives if covid is still uncontained and if the economy remains a complete mess. The top party ranks will also be reshuffled, clearing the way for other cadres to move up the ladder if they can avoid any missteps, particularly in handling Covid outbreaks.

The paralysis is reflected in market sentiment. On Wednesday, the benchmark CSI 300 Index remained flat after sliding as much as 1.1% while shares in Hong Kong declined as investors have lost hope that – besides constant jawboning – China will be unable to implement a major stimulus.

Which is a problem because as Li warned on Wednesday, when he delivered his starkest warnings about the economy’s weak performance, Beijing is facing another economic crisis with “difficulties in some aspects, to a certain extent, are greater than when the epidemic hit us severely in 2020.” He said China must avoid a contraction in the second quarter, adding that the nation would pay a huge price with a long road to recovery if the economy can’t keep expanding at a certain rate.

It is unclear if Xi had heard the message.

Meanwhile, as reported earlier this month, the latest official data also showed a contraction in industrial output for the first time since 2020 and a jump in the surveyed jobless rate to 6.1% in April, close to a record. High-frequency data for May showed the economy remained in a deep slump, according to Bloomberg’s aggregate index of eight indicators.

Xi hasn’t directly addressed the depths of China’s economic struggle in recent weeks, though his more generic comments have received prominent treatment in state-run newspapers. “China’s resolve to open up at a high standard will not change and the door of China will open still wider to the world,” Xi said at a recent trade council anniversary meeting, in a typical comment.

Li, by contrast, has emerged as a more candid figure. At the same trade council event in Beijing earlier this month Joerg Wuttke, president of the European Union Chamber of Commerce in China, said the premier “woke up” when some delegates shared their frustrations over China’s Covid policy.

“Li came over afterward and asked us how we were doing and how was business,” Wuttke said, adding that he was surprised by the move. “It was a very positive gesture. His actual crossing the street, showing up and saying ‘let’s chat’ was impressive.”

Meanwhile, as it scrambles to address these two contradictory mandates, China prepares to unleash the latest bubble: according to Bloomberg, bank managers at several state-owned lenders have been told they will be held accountable for failing to meet loan issuance targets. They have struggled to implement orders to introduce more liquidity, as companies that meet requirements are reluctant to borrow given the uncertain outlook of economy, according to banking business heads and executives.

In other words, with little actual loan demand, China has no other option than to flood markets with said loans, which will then promptly find their way into speculative activity – such as equities and housing, both of which will soon be on the receiving end of trillions more in liquidity. In fact, as we noted last night, it appears that China’s housing bubble is already making a comeback.

END

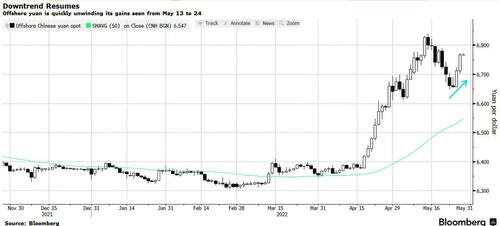

Initially the yuan fell against the dollar but has since risen:

(zerohedge)

Yuan, Dollar Divergence Heralds More Losses Ahead

THURSDAY, MAY 26, 2022 – 08:20 PM

by George Lei, Bloomberg Markets Live Commentator and analyst

The Chinese yuan is on track for the first weekly slide in more than two months, despite a much lower dollar and good news on the trade front. That’s a tell-tale sign of how pessimistic market sentiment is and may only reinforce expectations that yuan’s downtrend is here to stay.

The Chinese currency has lost 1% so far this week in offshore trading and 0.7% onshore. While the drop itself doesn’t seem very remarkable, the context is key: the yuan couldn’t hold on to its Monday rally amid news of possible US tariff removals. It also failed to benefit from a 1.3% weekly decline in the dollar index.

The last time a weaker greenback couldn’t help at all was in March: the dollar index lost 0.9% in the week ending March 18, while the onshore yuan dropped 0.34% and its offshore counterpart declined 0.14%. Since then, the Chinese currency has weakened more than 5.5%. Only the Turkish lira, Argentine peso and Hungarian forint lost more among 24 emerging-market peers tracked by Bloomberg.

Following a brief rebound from May 13 to 24, the offshore yuan is sliding once again and is now poised to revisit 6.80 support. A breach may open up path toward year-to-date low at 6.8380, last seen on May 13, when the dollar index found its recent top. Further losses could send the currency toward 6.90, a level last seen in August 2020.

The discord between China’s top leaders over whether to prioritize Covid control or economic growth is paralyzing the implementation of policy responses, according to eight senior local government officials and financial bureaucrats. It may also amplify the negative sentiment toward broader Chinese assets and weigh heavily on the yuan, independent of what the dollar does.

On Thursday, China’s trade-weighted yuan fell below 100 for the first time in seven month, according to a Bloomberg replica of the CFETS RMB index that tracks the exchange rate against 24 peers. Fidelity International and Credit Agricole CIB both predicted more downside for the trade-weighted gauge, with the dollar-yuan pair possibly testing 7 level in the coming months.

“China and the US are moving in different directions and I don’t see PBOC stand in the way of depreciation,” said David Loevinger, Los Angeles-based managing director at TCW Group Inc. and a former China specialist at the US Treasury. He said the big selloff is over and the next 6- to 12-month view is a gradually weaker yuan.

END

4/EUROPEAN AFFAIRS//UK AFFAIRS/

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

UKRAINE/RUSSIA//WASHINGTON POST

This is stunning: the Washington Post now admits what we have been telling you throughout that Ukraine is experiencing collapsing morale issues on the front lines and are losing

(zerohedge)

In Stunning Shift, WaPo Admits Catastrophic-Conditions, Collapsing-Morale Of Ukraine Front-Line Forces

FRIDAY, MAY 27, 2022 – 07:24 AM

With Russia’s war in Ukraine now in its fourth month, mainstream media consumers have been treated to seemingly endless headlines and analysis of Russia’s extensive military losses. At the same time Ukrainian forces have tended to be lionized and their battlefield prowess romanticized, with essentially zero public information so far being given which details up-to-date Ukrainian force casualties, set-backs, and equipment losses.

But for the first time The Washington Post is out with a surprisingly dire and negative assessment of how US-backed and equipped Ukrainian forces are actually fairing. Gone is the rosy idealizing lens through which each and every encounter with the Russians is typically portrayed. WaPo correspondent and author of the new report Sudarsan Raghavan underscores of the true situation that “Ukrainian leaders project an image of military invulnerability against Russia. But commanders offer a more realistic portrait of the war, where outgunned volunteers describe being abandoned by their military brass and facing certain death at the front.”

As many careful and less idealistic observers suspected the whole time, a steady stream of both wartime propaganda and one-sided social media feeds where it seems the only tanks being blown up are Russian ones has served to present a very skewed portrayal of the battlefield to the Western public. While it’s perhaps easier to get sucked into this pro-Ukraine bias based on the innumerable so-called open source intelligence self-anointed ‘experts’ on Twitter, this is less so if one wades into Telegram, where a flood of uncensored videos from both sides gives a truer picture, as the fresh report seems to also suggest.

The Washington Post report belatedly admits the avalanche of propaganda based in a pro-Kiev, pro-West narrative from the outset: “Videos of assaults on Russian tanks or positions are posted daily on social media. Artists are creating patriotic posters, billboards and T-shirts. The postal service even released stamps commemorating the sinking of a Russian warship in the Black Sea.”

The report then pivots to the reality of an undertrained, poorly commanded and equipped, rag-tag force of mostly volunteers in the East who find themselves increasingly surrounded by the numerically superior Russian military which has penetrated almost the entire Donbas region. “Ukraine, like Russia, has provided scant information about deaths, injuries or losses of military equipment. But after three months of war, this company of 120 men is down to 54 because of deaths, injuries and desertions,” the report reads as it follows one particular battalion.

The report’s sources speak out despite threat of being court-martialed amid a heavily controlled information flow:

“War breaks people down,” said Serhiy Haidai, head of the regional war administration in Luhansk province, acknowledging many volunteers were not properly trained because Ukrainian authorities did not expect Russia to invade. But he maintained that all soldiers are taken care of: “They have enough medical supplies and food. The only thing is there are people that aren’t ready to fight.”

The report references a video widely circulating online this week wherein a group the size of a platoon declares they simply can’t fight for lack of weaponry, ammunition, food and proper command support:

“We are being sent to certain death,” said a volunteer, reading from a prepared script, adding that a similar video was filmed by members of the 115th Brigade 1st Battalion. “We are not alone like this, we are many.”

Ukraine’s military rebutted the volunteers’ claims in their own video posted online, saying the “deserters” had everything they needed to fight: “They thought they came for a vacation,” one service member said. “That’s why they left their positions.”

In the wake of the video, the Ukrainian troops featured are being accused of ‘desertion’: