June 3 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1847.60 DOWN $19.75

SILVER: $21.89 DOWN $.34

ACCESS MARKET: GOLD $1850.50

SILVER: $21.94

Bitcoin morning price: $29,768 DOWN291

Bitcoin: afternoon price: $29,548 down 511

Platinum price: closing DOWN $12.05 to $1013.50

Palladium price; closing DOWN $65.70 at $1984.80

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE: COMEX

JPMorgan issued

EXCHANGE: COMEX

CONTRACT: JUNE 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,866.500000000 USD

INTENT DATE: 06/02/2022 DELIVERY DATE: 06/06/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 80

118 H MACQUARIE FUT 116

323 C HSBC 162

323 H HSBC 552

332 H STANDARD CHARTE 74

363 H WELLS FARGO SEC 114

435 H SCOTIA CAPITAL 64

624 H BOFA SECURITIES 203

657 C MORGAN STANLEY 3

661 C JP MORGAN 4000 2386

686 C STONEX FINANCIA 26

690 C ABN AMRO 29

700 C UBS 103

709 H BARCLAYS 66

732 C RBC CAP MARKETS 11

800 C MAREX SPEC 6 15

880 C CITIGROUP 34

905 C ADM 42

TOTAL: 4,043 4,043

MONTH TO DATE: 14,705

EXCHANGE: COMEX

CONTRACT: MAY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,865.100000000 USD

INTENT DATE: 05/24/2022 DELIVERY DATE: 05/26/2022

FIRM ORG FIRM NAME ISSUED STOPPED

661 C JP MORGAN 2

737 C ADVANTAGE 1

905 C ADM 1

TOTAL: 2 2

MONTH TO DATE: 6,431

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT 4043 NOTICE(S) FOR 404,300 Oz//12.575 TONNES)

total notices so far: 14,705 contracts for 1,470,500 oz (45.738 tonnes)

SILVER NOTICES:

17 NOTICE(S) FILED 85,000 OZ/

total number of notices filed so far this month 1475 : for 7,375,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $19.75

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD/

INVENTORY RESTS AT 1066.04 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $.34 CENTS

AT THE SLV// A BIG CHANGE IN SILVER INVENTORY AT THE SLV://NO CHANGES IN SILVER IVWENTORY AT THE SLV.: A WITHDRAWAL OF 0.246 MILLION OZ FROMTHE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 553.626 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A TINY SIZED 197 CONTRACTS TO 146,737 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE TINY GAIN IN OI WAS ACCOMPLISHED DESPITE OUR VERY STRONG $0.57 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.57) BUT ALSO UNSUCCESSFUL IN KNOCKING OFF ANY SILVER LONGS AS THEY REMAIN FIRM IN THEIR BELIEF OF A SILVER FAILURE AS WE HAD A STRONG NET GAIN OF1245 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 7.635 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 21 CONTRACTS OR 105,000 OZ//NEW STANDING: 7,960,000 / // V) TINY SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -8

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTACTS for 3 days, total 4211, contracts: 21.055 million oz OR 7.015 MILLION OZ PER DAY. (1403CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 7.015 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 7.015 MILLION OZ

RESULT: WE HAD A TINY SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 97 DESPITE OUR STRONG $0.57 GAIN IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 1140 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S 105,000 QUEUE JUMP//NEW STANDING:7,960 // .. WE HAD A STRONG SIZED GAIN OF 1245 OI CONTRACTS ON THE TWO EXCHANGES FOR 6.225 MILLION OZ WITH THE GAIN IN PRICE.

WE HAD 17 NOTICES FILED TODAY FOR 85,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 5466 CONTRACTS TO 511,320 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – 204 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE GAIN IN COMEX OI CAME WITH OUR STRONG GAIN IN PRICE OF $22.50//COMEX GOLD TRADING/THURSDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //JUST SPECULATOR SHORT COVERING FROM OUR STUPID SPECULATORS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 69.26 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP//NEW STANDING: 69.063 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $22.50 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 7486 OI CONTRACTS 23.28 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2020 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 511,320

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7486, WITH 5466 CONTRACTS INCREASED AT THE COMEX AND 2020 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF7486 CONTRACTS OR 23.28 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2020) ACCOMPANYING THE GOOD SIZED GAIN IN COMEX OI (5466,): TOTAL GAIN IN THE TWO EXCHANGES 7486 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE. AT 69.26 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 0 OZ//NEW STANDING:69.063 TONNES / 3) ZERO LONG LIQUIDATION//CONSIDERABLE SPECULATOR SHORT COVERING //.,4) GOOD SIZED COMEX OI. GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

12,307 CONTRACTS OR 1,230,700 OZ OR 38.278 TONNES 3 TRADING DAY(S) AND THUS AVERAGING: 4102 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES: 38.278 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 38.278/3550 x 100% TONNES 1.07% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 38.278 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A TINY SIZED 97 CONTRACT OI TO 146,737 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1140 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1140 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 97 CONTRACTS AND ADD TO THE 1140 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 1237 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 6.185 MILLION OZ

OCCURRED WITH OUR GAIN IN PRICE OF $0.57 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED UP 13.30 PTS OR 0,42% //Hang Sang CLOSED DOWN 212.81 PTS OR 1.00% /The Nikkei closed UP 347.69 OR 1.27% //Australia’s all ordinaires CLOSED UP .97%% /Chinese yuan (ONSHORE) closed UP 6,60 /Oil UP TO 112.24dollars per barrel for WTI and UP TO 113.30 for Brent. Stocks in Europe OPENED MOSTLY GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.660 OFFSHORE YUAN CLOSEDUP ON THE DOLLAR AT 6.639: /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER/

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED 5466 CONTRACTS TO 511,320 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED WITH OUR GAIN OF $22.50 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2020 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ARE CAUGHT. THE COMMERCIALS WILL SLAUGHTER THESE GUYS WHEN THEY THINK THE TIME IS RIGHT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A fair SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2020 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :2020 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2020 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 7486 CONTRACTS IN THAT 2020 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI GAIN OF 5566 CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR SOLID GAIN IN PRICE OF GOLD $22.50.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (69.063),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 69.063 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $22.50) AND WERE UNSUCCESSFUL IN KNOCKING OFF SOME SPECULATOR LONGS/COMMERCIAL LONGS AS WELL AS SPECULATOR SHORTS//// WE HAVE REGISTERED A STRONG SIZED GAIN OF 23.28 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JUNE (69.063 TONNES)…

WE HAD 204 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 7486 CONTRACTS OR 758600 OZ OR 23.28 TONNES

Estimated gold volume 110,220/// poor

final gold volumes/yesterday 134,599 poor

INITIAL STANDINGS FOR JUNE ’22 COMEX GOLD //JUNE 3

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 450.11 oz Brinks 14 kilobars |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 4043 notice(s) 404,300 OZ 12.575 TONNES |

| No of oz to be served (notices) | 7499 contracts 749900 oz 23.32 TONNES |

| Total monthly oz gold served (contracts) so far this month | 14,705 notices 1470,500 OZ 45.738 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

dealer deposits 0

total dealer deposit 0 oz//

No dealer withdrawals

0 customer deposits

total deposits: nil oz

1 customer withdrawals:

i) Out of Brinks: 450.11 o (14 kilobars)

total withdrawal: 450,11 oz

ADJUSTMENTS: 4//all dealer to customer

i) dealer to customer: Brinks 2074.321 oz

ii)HSBC: 578.455 oz

iii) JPMorgan: 303.910 oz

iv) Manfra: 2806.891 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 11,542 contracts having LOST 1854 contracts

We had 1854 notices filed on THURSDAY so we GAINED 0 contracts

July has a GAIN OF 3 OI to stand at 2128

August has a GAIN of 5694 contracts UP to 434,414 contracts

We had 4043 notice(s) filed today for 404,300 oz FOR THE JUNE 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 4000 notices were issued from their client or customer account. The total of all issuance by all participants equate to 4043 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 2386 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2021. contract month,

we take the total number of notices filed so far for the month (14,705) x 100 oz , to which we add the difference between the open interest for the front month of (JUNE 11,542 CONTRACTS ) minus the number of notices served upon today 4043 x 100 oz per contract equals 2,220400 OZ OR 69.063 TONNES the number of TONNES standing in this active month of JUNE.

thus the INITIAL standings for gold for the JUNE contract month:

No of notices filed so far (14,705) x 100 oz+ (11,542) OI for the front month minus the number of notices served upon today (4043} x 100 oz} which equals 2,220,400 oz standing OR 69.063 TONNES in this active delivery month of JUNE.

TOTAL COMEX GOLD STANDING: 69.063 TONNES (A STRONG STANDING FOR A JUNE ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,210,073.763 oz

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 35,027,533.463 OZ

TOTAL ELIGIBLE GOLD: 17,023,653.974 OZ

TOTAL OF ALL REGISTERED GOLD: 18,003,879.519 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,793226.0 OZ (REG GOLD- PLEDGED GOLD)

END

JUNE 2022 CONTRACT MONTH//SILVER//JUNE 3

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 306,739.330 oz CNT Delaware Manfra HSBC |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 600,674.508 oz CNT Delaware |

| No of oz served today (contracts) | 217CONTRACT(S) 85,000 OZ) |

| No of oz to be served (notices) | 117 contracts (585,000 oz) |

| Total monthly oz silver served (contracts) | 1475 contracts 7,375,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) zero dealer deposits And now for the wild silver comex results

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 2 deposits into the customer account

ii) Into CNT: 599,734.320 oz

i) Into Delaware: 940.248 oz

total deposit: 600,674.508 oz

JPMorgan has a total silver weight: 171.637 million oz/336.605 million =50.98% of comex

Comex withdrawals: 4

i) Out of CNT 134,569.100 oz

ii) Out of Delaware 30,453.350 oz

iii) Out of HSBC 136,824.880 oz

iv) Out of Manfra: 4893.120 oz

total withdrawal 306,739.330 oz

1 adjustments: dealer to customer/HSBC 5277.230 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 72,453 MILLION OZ

TOTAL REG + ELIG. 336.605 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE OI: 134 HAVING GAINED 4 CONTRACTS.

WE HAD 17 NOTICES FILED ON THURSDAY SO WE GAINED 21 CONTRACTS OR AN ADDITIONAL 105,000 OZ WILL STAND IN THIS NON ACTIVE

DELIVERY MONTH OF JUNE

JULY HAD A LOSS OF 1324 CONTRACTS DOWN TO 104,614 CONTRACTS.

AUGUST GAINED 440 CONTRACTS TO STAND AT 459

SEPTEMBER HAD A GAIN OF 866 CONTRACTS UP TO 27,202 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 17 for 85,000 oz

Comex volumes:39,220// est. volume today// poor

Comex volume: confirmed yesterday: 40,937 contracts ( poor )

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1475 x 5,000 oz = 7,375,000 oz

to which we add the difference between the open interest for the front month of JUNE(134) and the number of notices served upon today 17 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE./2022 contract month: 1475 (notices served so far) x 5000 oz + OI for front month of JUNE (134) – number of notices served upon today (17) x 5000 oz of silver standing for the JUNE contract month equates 7,960,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

MAY 18/WITH GOLD DOWN $2.55//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.07 TONNES FROM THE GLD///INVENTORY RESTS AT 1049.21 TONNES

MAY 17/WITH GOLD UP $5.40:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1053.28 TONNES

MAY 16/WITH GOLD UP $5.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD///INVENTORY RESTS AT 1055.89 TONNES

MAY 13/ WITH GOLD DOWN $16.25//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.8 TONNES FROM THE GLD.//INVENTORY RESTS AT 1060.82 TONNES

MAY 12/WITH GOLD DOWN $26.50: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD////INVENTORY RESTS AT 1066.62 TONNES

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

GLD INVENTORY: 1066.04 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

MAY 18/WITH SILVER UP $0.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL 1.892 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 17/WITH SILVER UP $.22 TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.508 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 16/WITH SILVER UP $.52 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.546 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.593 MILLION OZ//

MAY 13/WITH SILVER UP 31 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ/

MAY 12/WITH SILVER DOWN 88 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ//

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

INVENTORY TONIGHT RESTS AT 563.626 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: Why Shouldn’t You Give Up On Gold And Silver?

THURSDAY, JUN 02, 2022 – 07:00 PM

A lot of investors wonder about the lack of movement in gold and silver, especially given rampant inflation. Why haven’t we seen a big rally in precious metals as many expected? Why shouldn’t you just give up on gold and silver?

Peter Schiff answers these questions in this video.

You bought gold and silver betting on inflation. You bet right. But you haven’t seen a big move up in metals – at least not yet.

All the people who said there was no inflation to worry about – they were wrong. Yet it’s very frustrating that even though we were right, we’re not getting rewarded for being right in the price of our gold and silver that should be much higher.”

But there are reasons why gold and silver haven’t rallied yet, as Peter lays out in the video. And he is certain they will rally, once the markets catch on to what’s really going on.

First, Peter reminds us that inflation isn’t new. It has been with us for more than a decade. When the Federal Reserve responded to the 2008 financial crisis with quantitative easing — that was inflation. But due to the way those early rounds of QE entered the economy, it primarily showed up in asset prices, not consumer prices.

A lot of asset prices went up, and when that happened, a lot of Americans who owned those assets felt richer. Therefore, they weren’t upset that the cost of living was also going up because their wealth was going up a lot faster, at least on paper.”

And of course, all along the government was understating the amount the cost of living was going up through a rigged CPI formula.

The policy response to COVID-19 kicked inflation into high gear. At the onset of the lockdowns, the Fed launched QE infinity.

While we cranked up the printing presses like never before, we basically ordered people to stop working. We told them to go home, and not produce goods and services, but just cash government checks. We wanted to replace the lost incomes with a printing press. So, people weren’t earning money anymore, but the Federal Reserve was printing money so people could buy things they were no longer producing.”

Peter called this the perfect storm of inflation.

But the question remains — why hasn’t the price of gold and silver responded to all of this inflation?

At times, it feels like the price of everything is going is going up – is going way up – except gold and silver, which doesn’t make sense, Gold and silver should be particularly sensitive not only to today’s inflation, but tomorrow’s inflation.”

By its very nature, the price of gold can discount the price of all the future inflation.

And that leads us to the first problem.

Even though we have a lot of inflation today, investors still think we won’t have inflation tomorrow.”

So, why aren’t investors worried about future inflation?

Because the Federal Reserve is promising to solve the problem. The conventional wisdom is that you don’t need to buy gold and silver to hedge against future inflation because there won’t be any. The Fed is on the job. Powell & Company will make it go away. They have the tools to get inflation back to 2%.

Rather than fearing inflation, they’re fearing the fight against inflation. Because how is the Fed going to fight inflation? It’s going to jack up interest rates. It’s going to have a tight monetary policy. In fact, it’s even going to start shrinking the balance sheet. It’s going to start taking money out of circulation — quantitative tightening. It’s going to reverse all of that inflation. It’s going to suck up that liquidity. And that is what is scaring investors out of buying gold and silver. They still have confidence in the Federal Reserve.”

Peter said that confidence is going to be lost.

He goes on to remind us of all the things the Fed has gotten wrong in the past – from “there is no problem in the housing market” in 2006 and 2007, to “inflation is transitory.” Now, Jerome Powell is saying it can slay inflation. And he’s confident he can do it because the economy is strong. The entire Fed policy is predicated on a strong economy.

Peter said, “That is completely wrong.” In fact, we may well already be in a recession.

I think that when the Fed ultimately has to admit – again – that it was wrong on the US economy and it overestimated the strength of the economy just like it underestimated inflation the Fed is going to lose its credibility.”

And when the Fed turns its attention to a tanking economy, inflation is going to get worse. Government deficits will explode again. The central bank will have to print even more money to monetize the debt. The balance sheet will explode.

And the cost of living is going to keep going up.

All of that inflation that started out in financial assets has now permanently migrated into consumer goods. … So, this is not a temporary situation. This is permanent. Inflation is going to get much, much worse. But the economy is going to get weaker. It’s stagflation.”

When the markets come to terms with this reality, everybody will come rushing into gold and silver.

In the meantime, it’s important not to give up on the gold and silver you already own. Furthermore, this is an opportunity to buy gold and buy silver while most investors remain clueless about what’s actually going on.

2. Lawrie Williams//Pam and Russ Martens/

LAWRIE WILLIAMS: China back as No. 1 importer of Swiss gold but at low level.

The Swiss Customs Administration has now released its gold import and export figures for April, and after a hiatus China is back as the leading importing nation, but at much lower level than it has tended to be in the past. That other usual contender for the No. 1 Swiss gold import position, India’s imports only came in at around half those for China in the April figures, so it is fair to say that gold bullion flows via Switzerland from West to East are still hugely curtailed. A country-by-country bar chart showing the principal recipients of the Swiss re-refined and exported gold bullion is set out below:

Indeed total gold flows in and out of Switzerland in April were much lower than average. Total gold imports only amounted to 83 tonnes and exports to 70.4 tonnes. In a normal month the totals in both directions probably average over 100 tonnes and, for example in March imports came to 181 tonnes and exports to 147 tonnes. For April just over 50% of the Swiss gold flowed to the Middle East and Asia. In some other months these directional flows have totalled 80% or more.

There were some major anomalies in the import sources for the Swiss gold confirming considerable turmoil in the global gold markets. The largest volume came from the United Arab Emirates, certainly not known as a gold producer, but very much at the centre of the Middle Eastern gold trade. It provided around a quarter of the gold flowing into the Swiss refineries at 20.6 tonnes during April which suggests a huge running down of built-up gold inventories and perhaps a degree of profit-taking around the peak in the gold price occurring in early April when the gold price topped out at over $1,980. If so that represented some pretty smart trading timing!

Hog Kong too provided an above average volume of gold to the Swiss refineries, presumably for similar reasons to the UAE supplies, although only 4.4 tonnes, but still a high volume for a nation which has no domestic gold production.

As usual, though, most of the balance of the Swiss refinery gold supplies came directly from mines in countries with no domestic gold refining capacity in the form of impure doré bullion, as well as gold scrap primarily from wealthier countries. Interestingly all 2.1 tonnes of gold from France appears to have been in the form of gold coins for remelting. The Swiss refineries tend to specialize in re-refining gold into the usually higher tenor product and smaller sized bars and wafers most in demand on international markets, particularly in the Far East. They process an amount equivalent to up to around half of the world’s new mined gold some months so provide an excellent window on the directions and volumes of global gold flows.

03 Jun 2022

END

3. Chris Powell of GATA provides to us very important physical commentaries

Your weekend reading material

(Alasdair Macleod/GATA)

Alasdair Macleod: Recession, prices, and the crackup boom

Submitted by admin on Thu, 2022-06-02 13:17Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, June 2, 2022

Initiated by monetarists, the debate between an outlook for inflation versus recession intensifies. We appear to be moving on from the stagflation story into outright fears of the consequences of monetary tightening and of interest rate overkill.

In common with statisticians in other jurisdictions, Britain’s Office for Budget Responsibility is still effectively saying that inflation of prices is transient, though the prospect of a return toward the 2% target has been deferred until 2024. Chancellor Sunak blithely accepts these figures to justify a one-off hit on oil producers, when, surely, with his financial expertise he must know the situation is likely to be very different from the OBR’s forecasts.

This article clarifies why an entirely different outcome is virtually certain. To explain why, the reasonings of monetarists and neo-Keynesians are discussed and the errors in their understanding of the causes of inflation is exposed.

Finally, we can see in plainer sight the evolving risk leading towards a systemic fiat currency crisis encompassing banks, central banks, and fiat currencies themselves. It involves understanding that inflation is not rising prices but a diminishing purchasing power for currency and bank deposits, and that the changes in the quantity of currency and credit discussed by monetarists are not the most important issue.

In a world awash with currency and bank deposits the real concern is the increasing desire of economic actors to reduce these balances in favour of an increase in their ownership of physical assets and goods. As the crisis unfolds, we can expect increasing numbers of the public to attempt to reduce their cash and bank deposits with catastrophic consequences for their currencies’ purchasing power.

That being so, we appear to be on a fast track towards a final crackup boom whereby the public attempts to reduce their holdings of currency and bank deposits, evidenced by selected non-financial asset and basic consumer items prices beginning to rise rapidly. …

… For the remainder of the analysis:

END

For your interest..

New ‘In Gold We Trust’ report shows why gold should be way up, not why it isn’t

Submitted by admin on Thu, 2022-06-02 11:13Section: Daily Dispatches

11:18a ET Thursday, June 2, 2022

Dear Friend of GATA and Gold:

The new annual “In Gold We Trust” report from financial house Incrementum’s Ronald-Peter Stoferle and Mark J. Valek has been published, containing a zillion reasons why gold should be going way up in price but not much if anything about why it hasn’t gotten there. For that information you’re probably still stuck with GATA. (As the White Queen told Alice: “Jam tomorrow and jam yesterday, but never jam today.”)

The report may be most interesting for the transcript of a long discussion among the report’s authors and GoldMoney research director Alasdair Macleod, who at least remarks that central banks are “sitting on the price of gold … because it’s a rival in this fiat paradigm.” Macleod, whose commentaries are often cited by GATA, believes that central banks eventually will be compelled to avert destruction of their currencies by returning them to some form of gold backing.

Incrementum’s new “In Gold We Trust” report is titled “Stagflation 2.0” and can be downloaded here:

https://www.incrementum.li/en/ingoldwetrust-report/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //PALM OIL+ OTHERS

END

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.660

OFFSHORE YUAN: 6.6390

HANG SANG CLOSED DOWN 212.81 PTS OR 1.00%

2. Nikkei closed UP 347,69% OR 1.27%

3. Europe stocks ALL CLOSED MOSTLY RED

USA dollar INDEX UP TO 102.21/Euro FALLS TO 1.0731

3b Japan 10 YR bond yield: FALLS TO. +.229/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 130.15/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: UP -SHORE CLOSED DOWN// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +1.258%/Italian 10 Yr bond yield RISES to 3.34% /SPAIN 10 YR BOND YIELD FALLS TO 2.40%…

3i Greek 10 year bond yield RISES TO 3.70

3j Gold at $1866.50 silver at: 22.44 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0.12 roubles/dollar; ROUBLE AT 61.52

3m oil into the 116 dollar handle for WTI and 117 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 130.15DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9606– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0305well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.920 UP 1 BASIS PTS

USA 30 YR BOND YIELD: 3.087 UP 1 BASIS PTS

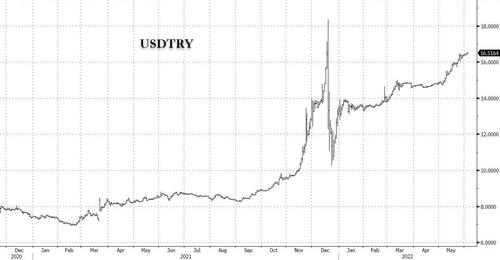

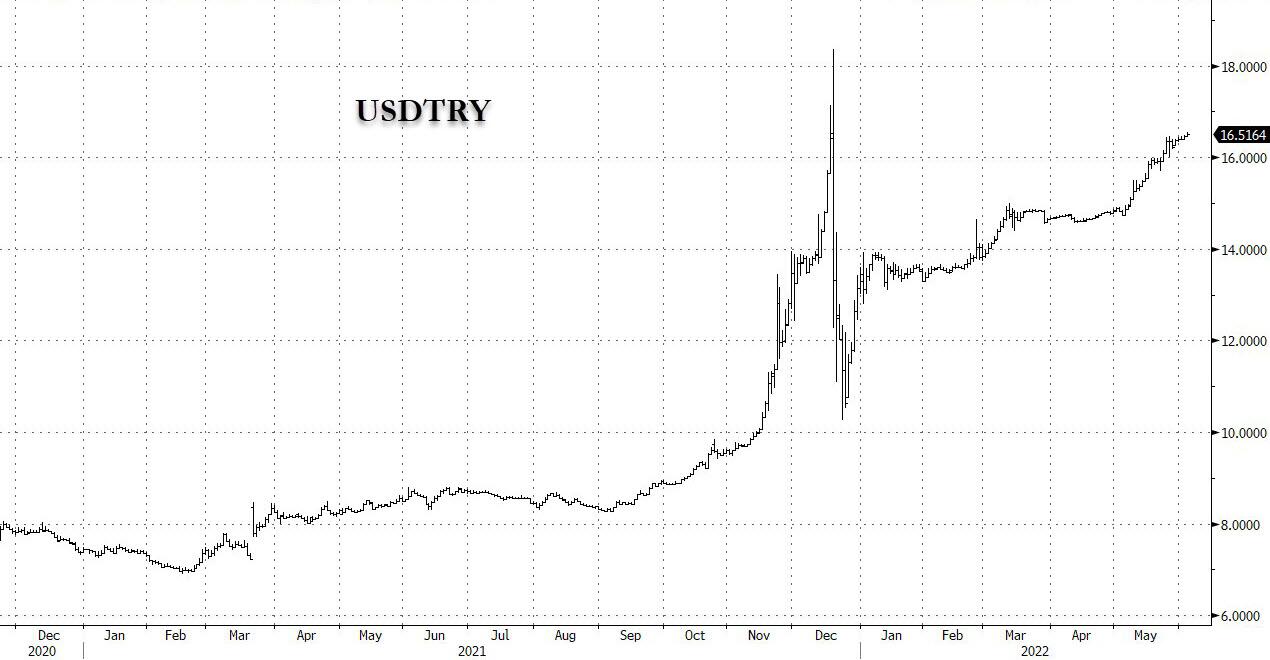

USA DOLLAR VS TURKISH LIRA: 16.51

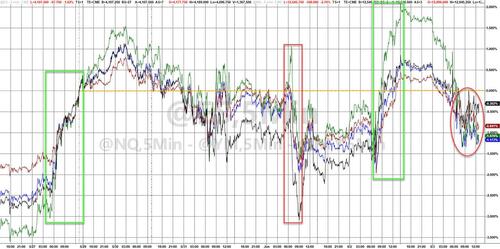

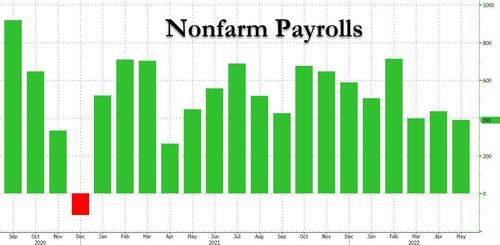

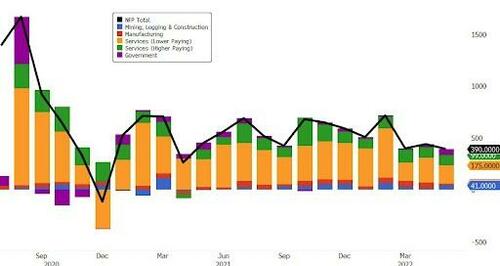

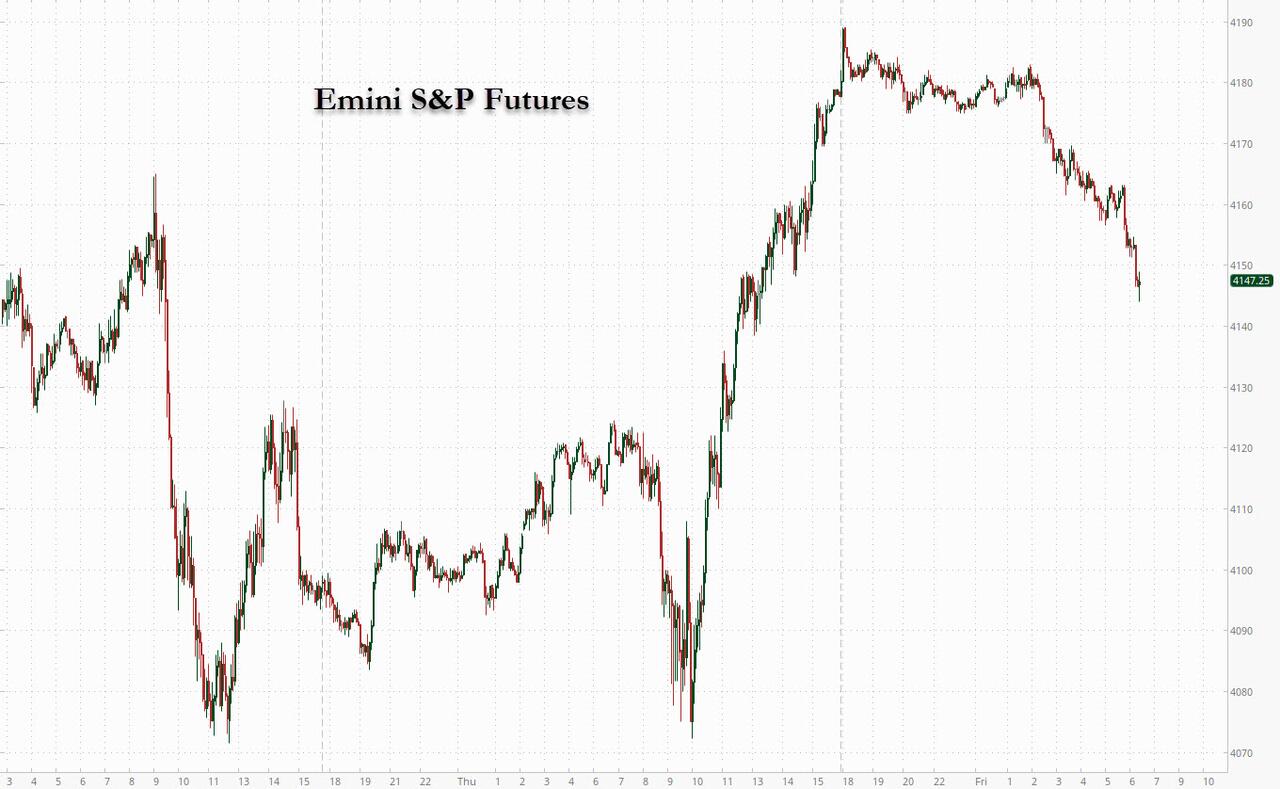

Futures Dump Ahead Of Payrolls Despite Musk’s “Super Bad Feeling”

FRIDAY, JUN 03, 2022 – 07:57 AM

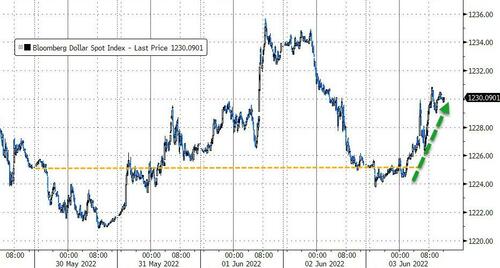

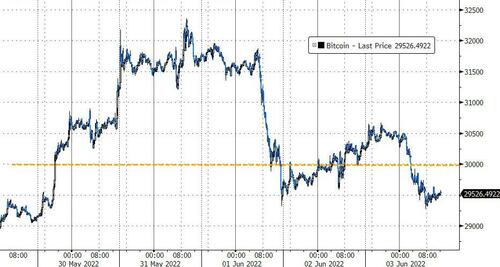

Tech stocks led US index futures slumped on the last day of the week, after a report about looming job cuts at Tesla deepened concerns about economic growth, and confirming what we wrote a week ago in “We Could See A Million Layoffs Or More” – Here Comes The Job Market Shock. Futures were lower as dismal trading volumes accentuating every sell order, and further reduced by UK holidays marking the Queen’s Jubilee. And speaking of the job market, in less than an hour we get the May payrolls print, where Wall Street consensus expects the a +320k number vs. +428k in April, although the whisper number is currently lower than survey at +301k, and as we noted last night, the odds of a negative print are non-trivial. Of course, should we get a subzero print, watch stocks explode higher as the Fed’s tightening plans are for all intents and purposes crushed. The Bloomberg dollar index steadied after overnight losses, Treasury yields held at around 2.91%, bitcoin resumed its slide and gold rose.

Anyway, back to markets, where S&P futures dropped 0.7%, down 30 points to 4,145 and Nasdaq 100 futures fell 1.1% trading at session lows…

… with Tesla, one of the biggest members of the tech-heavy index with a 4% weight, sliding 5% in premarket trading after Elon Musk said he had a “super bad feeling” about the economy and the electric carmaker needed to cut staff by about 10% and pause hiring. Other electric-vehicle stocks dropped in New York premarket trading following the Tesla report, with Nikola Corp. and Rivian Automotive Inc. lower. Elsewhere, Lululemon Athletica Inc. climbed after the athletic-wear retailer’s results surpassed analyst’s expectations and software company Okta Inc. rallied after its earnings.

“It’s very prudent by Tesla to reduce the staff,” Peter Garnry, head of equity strategy at Saxo Bank A/S, said on Bloomberg Television. “This market is not rewarding high revenue growth at all costs. You’re being rewarded from improvement in return on investor capital and free cash flow generation.” Here are other notable premarket movers:

- Okta (OKTA US) shares are up 16% in premarket trading after the software company reported first-quarter results ahead of expectations and raised its full-year forecast. Piper Sandler notes revenue acceleration and strength across key growth metrics, adding that it has increased “confidence in the story going forward.” BMO highlights “impressive” revenue that beat estimates.

- StoneCo (STNE US) soars 20% in premarket trading after its quarterly revenue more than doubled, but analysts expect the rally could be short-lived amid concerns about higher interest rates.

- RH (RH US) shares slipped 0.3% after the home-furnishing retailer warned of further slowdown in demand since Russia’s invasion of Ukraine and cited expectations for challenges for “several quarters” ahead.

- CrowdStrike (CRWD US) drops 2.5% after the security software company reported first-quarter results that were seen as mixed.

- PagSeguro (PAGS US) jumped after Brazilian fintech peer StoneCo reported quarterly adjusted net income that topped analysts’ expectations.

- Asana (ASAN US) dropped after the software company forecast an adjusted loss per share for the second quarter of 38c to 39c.

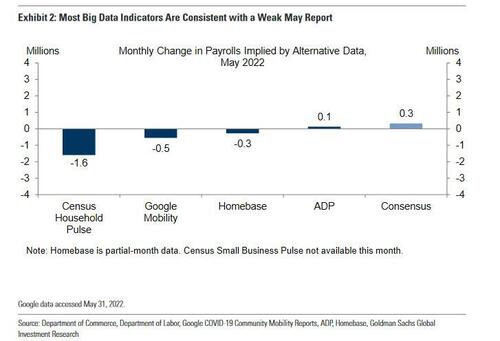

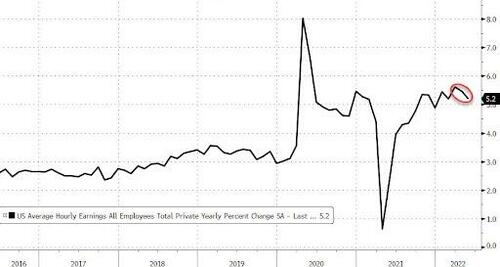

Investors remain on edge as some fear the pace of US monetary tightening could throw the world’s largest economy into a recession. Friday’s May labor report is likely to show the smallest gain in jobs since April 2021 alongside a down shift in average hourly earnings growth, Bloomberg Economics said.

“Investors remain nervous, trying to collect more information about earnings prospects on one side and economic data on the other,” said Cedric Ozazman, head of investment solutions at Mirabaud & Cie SA in Geneva. “The jobs report will be crucial as any bad news will reignite speculation about a pause in the Fed monetary tightening cycle during the last quarter of the year.” Of course, that means that “any bad economic news might be actually good for risky assets, as they will probably remove some pressure on interest rates,” Ozazman said.

On the other hand, Fed Vice Chair Lael Brainard said it was hard to see a case for a September pause in rate hikes and that increases of 50 basis points in June and July seemed reasonable.

In Europe, gains for real-estate and consumer companies outweighed declines in the cars and banking sectors, with the Stoxx Europe 600 Index rising 0.1%, erasing earlier gains. Here are the most notable European movers today:

- Rheinmetall gains as much as 3.9% after Warburg raised its rating on the stock to buy, noting comments by CEO indicating stronger-than-anticipated mid-term revenue potential, with peer Leonardo rising as much as 3.6%.

- Ringkjoebing Landbobank, or Rilba, rise as much as 8.4%. after the Danish lender boosted its FY pretax profit guidance. Handelsbanken notes a “positive development” in lending.

- Leonteq shares jump as much as 18% after the Swiss technology and service provider announced it expects to generate significant revenue growth on the back of strong net trading results.

- Avance Gas and BW LPG gain as Fearnley Securities calls the sector a “long-term value play,” increasing their target prices for the LPG firms it covers despite a strong year-to-date share rally.

- Lotos shares gain as much as 7.9% after Orlen offered a premium of about 9% with its all-stock deal to buy Lotos in a planned merger of Polish state-controlled refiners.

- PGS rise as much as 23% as Kepler Cheuvreux resumes coverage of the shares with a buy recommendation, seeing a more supportive macroeconomic environment and better liquidity.

- Aperam rises while Acerinox falls as Morgan Stanley says in a note that potentially combining their businesses would bring top-line and cost synergies via improved pricing power.

- Faurecia falls as much as 6.6% after the French automotive part maker launches EU705m rights issue as part of refinancing of Hella acquisition.

Asian stocks rose, poised for a third straight week of gains as investors awaited US non-farm payrolls for clues on the trajectory of interest rates. The MSCI Asia Pacific Index advanced as much as 0.7%, led by energy and material firms, with BHP Group and Reliance Industries among the biggest contributors. Gauges in Japan and Australia were the region’s best performers, while markets in China, Hong Kong and Taiwan were shut for a holiday. Investors are turning their attention to Friday’s data on non-farm payrolls following the release of weak private payrolls figures overnight. This comes as Federal Reserve Vice Chair Lael Brainard said expectations for half-percentage-point increases in interest rates this month and next were reasonable.

“The wide underperformance in job gains took the spotlight and the hopes that the Fed may take on a more cautious and gradual approach in tightening toward the latter part of the year may lead to some unwinding of hawkish expectations,” Jun Rong Yeap, a market strategist at IG Asia, wrote in a note. Asia’s benchmark index has climbed more than 7% from a trough in mid-May as the reopening of Shanghai supports stocks in China and Hong Kong. Still, the outlook for the region remains uncertain amid prospects of aggressive US monetary tightening, soaring inflation and China’s ongoing Covid-Zero stance.

Japanese stocks gain ahead of US labor report and as OPEC+ agreed to increase its oil production rates. Markets are closed in Hong Kong and China. The Topix index rose 0.4% to 1,933.14 as of market close in Tokyo, while the Nikkei 225 advanced 1.3% to 27,761.57. Sony Group Corp. contributed the most to the Topix Index gain, increasing 1.9%. Out of 2,170 shares in the index, 1,135 rose and 940 fell, while 95 were unchanged. “Inflation concerns are receding as labor market tensions are seen to be weakening from the US economic indicators and Beige Book,” said Nobuhiko Kuramochi, a market strategist at Mizuho Securities

Australian stocks rebounded, with the S&P/ASX 200 index rising 0.9% to close at 7,238.80, recouping Thursday’s 0.8% loss in a rally led by miners. Champion Iron gained on higher iron ore prices. Healius was the worst performer after flagging more difficult conditions in 2H. In New Zealand, the S&P/NZX 50 index rose 0.6% to 11,417.34. The gauge added 3.2% since Monday, posting its best week since Feb.

In FX, a Bloomberg dollar gauge steadied after yesterday’s loss and the euro traded around $1.0750. A day after pricing in a 50 basis-point rate hike by the ECB by the end of the year, traders are now betting that the move will happen by October itself. Australia’s swap spreads widened to the most in almost six years on speculation that the Reserve Bank will become more hawkish next week.

In rates, Treasuries are mostly unchanged across the curve with losses led by front-end, flattening spreads with 2s10s and 5s30s both tighter by over 1bp. 10-year TSY yields around 2.92%, flat on the day; bunds lag by additional 2bp in the sector. European bonds drifted at the open after yields rose to multi-year highs Thursday. US IG dollar issuance slate empty so far; four borrowers priced $3BNBThursday, pushing weekly volume up to $30b and high end of $25b to $30b forecast. Bloomberg notes that there has been some speculation that a jumbo Oracle deal (around $20BN) could come as early as next week which may see some rate lock selling flows weigh over Friday’s session.

In commodities, oil headed for a sixth weekly advance after a keenly anticipated OPEC+ meeting delivered only a modest increase in output that failed to assuage concerns over a widening supply deficit. Gas traders are rushing to secure LNG tankers ahead of winter with ship rates surging as sanctions on Russia reshape global energy flows, according to FT. NHC notes of a disturbance producing tropical-storm-force winds; with a new Tropical Storm warning issued for Florida, Cuba, and North-western Bahamas; additional strengthening possible late Saturday and Sunday. Spot gold is steady and comfortably above USD 1,850/oz pre-NFP, whilst base metals futures see the closure of Chinese and UK exchanges amid domestic holidays.

To the day ahead, where nonfarm payrolls will be the main event. We expect headline nonfarm payrolls to (+325k forecast vs. +428k previously) to slightly outperform private sector hiring (+300k vs. +406k). If our forecast is close to the mark, it should have the effect of lowering the unemployment rate by a tenth to 3.5%. With respect to other details of the report, average hourly earnings (+0.3% vs. +0.3%) will likely be a key focus for Fed policymakers. US ISM and PMI services readings are due, along with PMI composites. Service and composite PMIs are also due across Europe along with industrial production for France.

Market Snapshot

- S&P 500 futures down 0.6% to 4,148.00

- STOXX Europe 600 up 0.2%

- MXAP up 0.4% to 168.75

- MXAPJ up 0.4% to 555.45

- Nikkei up 1.3% to 27,761.57

- Topix up 0.4% to 1,933.14

- Hang Seng Index down 1.0% to 21,082.13

- Shanghai Composite up 0.4% to 3,195.46

- Sensex up 0.6% to 56,166.51

- Australia S&P/ASX 200 up 0.9% to 7,238.75

- Kospi up 0.4% to 2,670.65

- German 10Y yield up 1bp to 1.25%

- Euro up 0.1% to $1.0761

- Brent futures down 0.5% to $117.03/bbl

- Gold spot down 0.1% to $1,866.02

- U.S. Dollar Index down 0.1% to 101.69

Top Overnight News from Bloomberg

- Turkey is planning to restrict purchases by domestic investors of new lira bonds sold by multinational lenders, the latest effort to curb short selling of the local currency by limiting the supply of liquidity in the offshore market

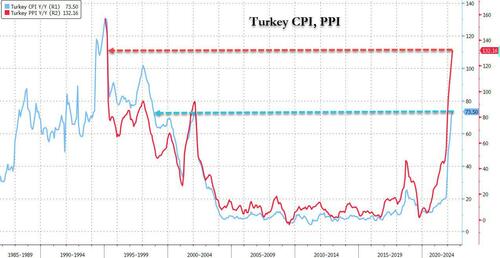

- Turkey’s inflation soared in May to the fastest since 1998 as it came under more pressure from the rising cost of food and energy, while ultra- loose monetary policy contributed to currency weakness

- New Australian Prime Minister Anthony Albanese has made a submission to the country’s labor watchdog, proposing to lift minimum wages by more than the inflation rate in a bid to fulfill one of his key election promises

- The Japanese government will maintain its 2013 joint policy statement with the Bank of Japan and basically stick with the current macro economic policy, Prime Minister Fumio Kishida says Friday

- The yen is likely to come under more pressure as Japanese life insurers slash the proportion of the dollar-denominated investments they hedge to the lowest in more than a decade. The companies hedged just 43.3% of the 42.8 trillion yen ($330 billion) of their dollar assets at the end of March, down from 45.8% six months earlier. The figure was as high as 62.8% in September 2016

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks took impetus from the gains in the US but with advances capped in holiday-thinned conditions. ASX 200 was led higher by tech with the sector inspired following the outperformance of the Nasdaq stateside and with mining-related stocks underpinned by the recent gains across commodity prices. Nikkei 225 benefitted from recent currency weakness and with index heavyweight Fast Retailing among the biggest gainers after a double-digit percentage jump in its same-store sales. KOSPI is firmer but lagged behind regional counterparts after CPI data climbed to its highest in nearly 14 years and added to the pressure for the BoK to continue with its hiking cycle

Top Asian News

- Deputy USTR Bianchi said all options are on the table regarding tariff decisions on Chinese imports and that the USTR is seeking strategic realignment with China and a tariff structure that makes sense, while she added the USTR is to focus the China trade relationship on US concerns about Chinese non-market practices and economic coercion, according to Reuters.

- South Korean Finance Ministry said they are taking the inflation situation very seriously, while the BoK noted that demand-side inflation pressure is likely to build and that inflation is to be above 5% in June and July, according to Reuters.

- India Cumulative Monsoon Rainfall 35% Below Normal as of June 3

- India Reports Biggest Jump in Covid Cases in Almost Three Months

- Toshiba Director Opposes Board Nominees From Elliott, Farallon

- Meituan 1Q Beat Raises Optimism on Stock, Business: Street Wrap

European cash bourses are trimming the Wall Street-induced gains seen at the open (Euro Stoxx 50 +0.2%; Stoxx 600 +0.2%) – with volumes also low as British and Chinese traders observe domestic holidays. European sectors are mostly higher with the breadth of the market narrow. US equity futures post modest losses across the contracts, with the NQ (-0.7%) straddling behind peers, ES -0.4%. The modest downside coincided with Reuters reports that Tesla (-3.7% pre-market) CEO Musk, via an email, said they need to make roughly a 10% staff reduction and he has a “super bad feeling about the economy”.

Top European News

- SAS Woes Mount With Reports on Risks From Chinese Debt, Strikes

- Allianz Takes $430 Million Profit Hit in Retreat from Russia

- Aperam Says in Talks With Acerinox on Potential Combination

- Yara Takes Next Step on Path to Clean Ammonia Unit IPO

- Eurozone May Composite PMI 54.8 vs Flash Reading 54.9

- CRH to Buy Barrette Outdoor Living of US for $1.9 Billion

FX

- Greenback cagey and rangy pre-NFP with DXY holding between 102.000-101.500.

- Euro eyes more decent option expiry interest around 1.0750 – 1.1bln rolling off between 1.0755-45 to be precise.

- Yen relying on Fib retracement (130.17) for support as Treasury yields remain firm and risk sentiment buoyed, USD/JPY towards upper end of 130.08-129.69 range.

- Sterling somewhat sidelined as UK gears up for Jubilee Day festivities, Cable contained within 1.2589-69 confines, EUR/GBP tight around 0.8550.

- Lira extends losses as acceleration in Turkish PPI outweighs sub-forecast, but still firmer CPI, USD/TRY tops 16.5100.

- Yuan breaches more technical resistance levels as correction continues, USD/CNH sub-6.6200 at one stage overnight.

- Russian Foreign Ministry does not plan to conduct market forex operations this year as per its early decision to temporarily suspend budget rules, according to Reuters

Fixed Income

- Debt on the defensive after a few dead cat bounces ahead of US jobs data.

- Bunds unable to defend 150.00 or 1.25% in cash, Treasuries more contained and curve flat awaiting NFP amidst a busy pm docket.

- T-note just under par between 118-30/24 parameters.

Commodities

- Bitcoin is little changed on the session, holding above USD 30k, in-fitting with the broader contained tone as we await the afternoon’s US data docket following particularly thin APAC and European sessions owing to CWTI and Brent futures have been waning off best levels following the overnight consolidation seen in the aftermath of the OPEC+ confab.

- Gas traders are rushing to secure LNG tankers ahead of winter with ship rates surging as sanctions on Russia reshape global energy flows, according to FT.

- NHC notes of a disturbance producing tropical-storm-force winds; with a new Tropical Storm warning issued for Florida, Cuba, and North-western Bahamas; additional strengthening possible late Saturday and Sunday.

- Norway’s Industri Energy Labour Union says 573 members at oil/gas platforms would go on strike on June 12th, if wage negotiations fail; such action would impact nine installations; would not initially impact output, via Reuters.

- Spot gold is steady and comfortably above USD 1,850/oz pre-NFP, whilst base metals futures see the closure of Chinese and UK exchanges amid domestic holidays.hina and UK market holidays, respectively.

US event calendar

- 08:30: May Change in Private Payrolls, est. 302,000, prior 406,000

- May Change in Nonfarm Payrolls, est. 320,000, prior 428,000

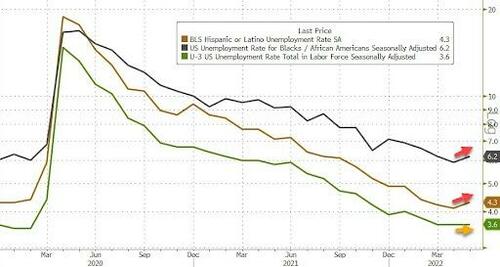

- May Unemployment Rate, est. 3.5%, prior 3.6%

- May Labor Force Participation Rate, est. 62.3%, prior 62.2%

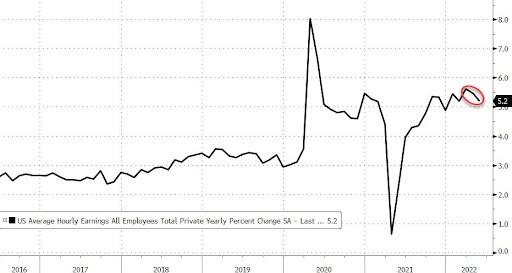

- May Average Hourly Earnings MoM, est. 0.4%, prior 0.3%; YoY, est. 5.2%, prior 5.5%;

- May Average Weekly Hours All Emplo, est. 34.6, prior 34.6

- 09:45: May S&P Global US Composite PMI, est. 53.8, prior 53.8

- 09:45: May S&P Global US Services PMI, est. 53.5, prior 53.5

- 10:00: May ISM Services Index, est. 56.5, prior 57.1

DB’s Jim Reid concludes the overnight wrap

Yesterday’s US employment data painted a mixed picture ahead of today’s official employment situation report. OPEC+ agreed to increase production targets but oil prices still managed to climb. Vice Chair Brainard and President Mester provided guidance ahead of the Fed’s blackout period, reinforcing expectations for the near-term path of policy. Sovereign bond markets were quiescent in ahead of jobs data today, which created fertile ground for equity markets to rally.

After a steady news leak about expanded production, OPEC+ agreed to increase production to +648k b/day, above the recent +400k b/day. Nevertheless, brent crude futures gained +1.14% over the session, as it was not clear whether all members had the capacity to increase production to the putative headline figures, if the totals merely represented production brought forward in time, or if the market expected larger increases after the week of rumors. After the production increase, the New York Times reported that President Biden plans to visit the crown prince in Saudi Arabia after much speculation.

Fed Vice Chair Brainard provided lucid guidance in the waning days before the Fed’s June communication blackout. She first put a pin on the intermeeting period by endorsing +50bp hikes for June and July, in a robust show of Committee consensus. As we mentioned yesterday, what the Fed will do in September is the next ‘live’ policy decision; Brainard weighed in, downplaying the chance of a pause given the current data outlook, instead dimensioning the decision between 25bp or 50bp hikes depending on the pace of inflation in the interregnum. President Mester later took things a step further, noting the pace of rate hikes could be accelerated if inflation readings merited, and that rates would probably need to get above neutral. Further, for those looking for evidence of a Fed put, Brainard noted that financial conditions are not yet at a concerning level.

On the other side of the Fed’s mandate, ADP employment payrolls surprised to the downside, adding just +128k jobs versus expectations of +300k while the prior month was also revised lower. Small businesses, construction, and leisure hospitality sectors were sources of weakness. The series does not always have a strong signal for the nonfarm payrolls out later in the week, so it’s not clear if the miss is noise or signal of a labor market naturally slowing as ADP payrolls are now above their pre-pandemic levels.

Initial and continuing jobless claims, meanwhile, reinforced data elsewhere this week that shows the labor market is currently very robust. Initial jobless claims slowed to +200k, below expectations of +210k, while continuing claims hit their lowest level since 1969. Elsewhere in data, Eurozone PPI printed at +1.2% versus +2.0% expectations.

European sovereign yields underperformed, with 2yr bunds selling off +7.6bps ahead of next week’s ECB meeting, while 10yr yields gained +5.0bps. 10yr BTP spreads widened another +4.6bps to +206bps above bund equivalents. Treasury yields were much more subdued, with 10yr yields barely budging (+0.2bps). 10yr Treasury yields are about +1bp higher this morning. The relative calm in sovereign yields helped drive equity indices higher on both sides of the Atlantic. The STOXX 600 gained +0.57% while the Dax (+1.01%) and CAC (+1.27%) outperformed. US stocks performed even better, with the S&P 500 climbing +1.84% with every sector but energy in the green, and a solid shift from cyclical sectors. The small cap Russell 200 climbed +2.31% while the tech-heavy NASDAQ gained +2.69%. The S&P 500 is now +0.45% on the holiday shortened week, as it looks to make it back-to-back weekly gains for the first time in two months.

Asian equity markets are trading higher this morning amid thin holiday trading riding a strong Wall Street close . The Nikkei (+1.14%), Kospi (+0.38%) are in positive territory while markets in mainland China, Hong Kong are closed for a holiday.

Outside of Asia, US stock futures are fluctuating with contracts on the S&P 500 (+0.04%) and NASDAQ 100 (+0.07%) are little changed.

To the day ahead, where nonfarm payrolls will be the main event. We expect headline nonfarm payrolls to (+325k forecast vs. +428k previously) to slightly outperform private sector hiring (+300k vs. +406k). If our forecast is close to the mark, it should have the effect of lowering the unemployment rate by a tenth to 3.5%. With respect to other details of the report, average hourly earnings (+0.3% vs. +0.3%) will likely be a key focus for Fed policymakers. US ISM and PMI services readings are due, along with PMI composites. Service and composite PMIs are also due across Europe along with industrial production for France.

end

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED UP 13.30 PTS OR 0,42% //Hang Sang CLOSED DOWN 212.81 PTS OR 1.00% /The Nikkei closed UP 347.69 OR 1.27% //Australia’s all ordinaires CLOSED UP .97%% /Chinese yuan (ONSHORE) closed UP 6,60 /Oil UP TO 112.24dollars per barrel for WTI and UP TO 113.30 for Brent. Stocks in Europe OPENED MOSTLY GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.660 OFFSHORE YUAN CLOSEDUP ON THE DOLLAR AT 6.639: /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER/

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA/

3B JAPAN

end

3c CHINA

4/EUROPEAN AFFAIRS//UK AFFAIRS/

Europe’s ban of Russian energy will only cause trouble on the inflation front down the road

(zerohedge)

Europe’s Ban On Russian Energy Will Only Trigger More Inflation Pain In The West

FRIDAY, JUN 03, 2022 – 02:45 AM

Europe’s extreme dependency on Russian energy products from oil to natural gas is made clear recently from the manner in which they have approached sanctions – with incrementalism, slowly sinking back into the bushes.

The latest agreement among member nations on export bans targeting Russia is largely oil focused, not natural gas focused, with the union demanding an immediate 70% decrease in Russian oil transferred BY SHIP. Oil transferred by pipeline will continue to flow into the EU for now. The ban is intended to expand to 90% of all shipborne Russian oil by the end of this year. Natural gas imports from Russia will also continue.

While some European nations are more dependent on Russian energy than others, overall 40% of the EU’s needs are supplied by the country’s industry. It is not surprising that they are seeking an incremental approach to sanctions, they simply would not be able to survive another winter if they were to go cold turkey and block Russian imports completely. Of course, this does not mean that Russia has to operate on Europe’s timetable.

Russia is already reducing exports of natural gas to multiple EU countries, with Denmark, Netherlands and Germany being the latest to see losses. The EU’s ban was oil and ship focused because they cannot find an alternative source for natural gas that would resolve shortages if they banned everything. Germany in particular would be destroyed by the loss of natural gas supplies from Russia with its 42% dependency.

The solutions offered by governments and in the mainstream media neglect certain realities. Namely, they claim that output can be increased or diverted to Europe to fill the gap. Joe Biden has suggested that the US is a “net exporter” of oil (this advantage has swiftly declined since he entered the White House according to the IEA) and that the US could help alleviate European demand. The IEA and OPEC members like Saudi Arabia have offered to increase market availability and output of oil if Russian exports are hit with sanctions.

The problem is that increased production is a fantasy stifled by the realities of labor shortages, increased drilling costs due to inflation and shortages in raw materials caused by supply chain disruptions. There is little chance that production capacity will ever be able to match EU demands, according to experts in the drilling industry.

So what does this mean?

It means that in order for Europe to fulfill its energy needs while banning its primary import source, the union will have to leach existing supplies from the global market. In other words, supplies will be greatly reduced in the West and prices are about to spike exponentially in order to feed the EU.

Despite all of this economic bluster, Russia has shown considerable resilience to sanctions on oil as both China and India have increased purchases in tandem with Europe’s bans. The wider implication of this being that Europe and the West will be facing reduced global oil supplies and paying a premium while countries like China and India will be enjoying increased supplies and lower prices from Russia. The East grows stronger while the West gets weaker

end

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

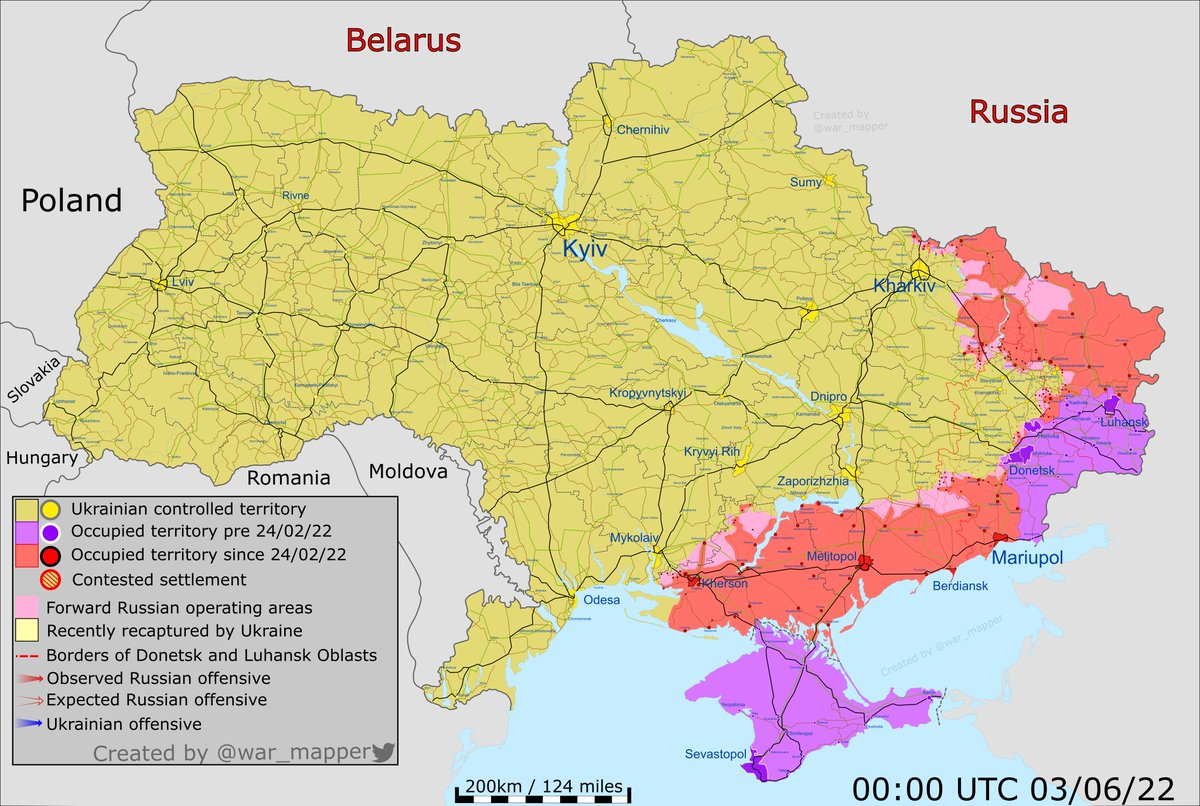

As Invasion Enters 100th Day, Russia Now Holds 20% Of Ukraine: Zelensky

FRIDAY, JUN 03, 2022 – 08:25 AM

As the Russian invasion has entered its 100th day, Ukrainian President Volodymyr Zelensky has confirmed that Russian forces are now in control of 20% of Ukraine’s territory.

“As of today, about 20% of our territory is under the control of the occupiers, almost 125 thousand square kilometers. This is much larger than the area of all the Benelux countries combined,” he said in a virtual address before Luxembourg lawmakers.

“All combat-ready Russian military formations are involved in this aggression,” he told MPs, describing that the front line extends for over 1,000km (or 621 miles).

This as it now appears Russia is poised to also seize the key city of Severodonetsk in the Donbas amid continuing fierce street-to-street fighting. If subdued, this would put the Russian army in control over all of Luhansk province.