JUNE 6 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1841.75 DOWN $5.85

SILVER: $22.09 UP $.20

ACCESS MARKET: GOLD $1842.20

SILVER: $22.09

Bitcoin morning price: $31,417 UP 1869

Bitcoin: afternoon price: $31,317 UP 1769

GOLD; $1847.60

Platinum price: closing UP $16.35 to $1029.85

Palladium price; closing UP $20.20 at $2005,19

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE: COMEXEXCHANGE: COMEX

CONTRACT: JUNE 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,845.400000000 USD

INTENT DATE: 06/03/2022 DELIVERY DATE: 06/07/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 13

118 H MACQUARIE FUT 18

323 C HSBC 25

323 H HSBC 84

332 H STANDARD CHARTE 12

363 H WELLS FARGO SEC 18

435 H SCOTIA CAPITAL 9

624 H BOFA SECURITIES 31

661 C JP MORGAN 600 363

686 C STONEX FINANCIA 4

690 C ABN AMRO 4

700 C UBS 16

709 H BARCLAYS 9

732 C RBC CAP MARKETS 1

800 C MAREX SPEC 15 3

905 C ADM 5

TOTAL: 615 615

MONTH TO DATE: 15,320

JPMorgan issued 363/615

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT 615 NOTICE(S) FOR 61,500 Oz//1.9129 TONNES)

total notices so far: 15,320 contracts for 1,532,000 oz (47.6516 tonnes)

SILVER NOTICES:

27 NOTICE(S) FILED 135,000 OZ/

total number of notices filed so far this month 1502 : for 7,510,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $5.85

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 1066.04 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $.20 CENTS

AT THE SLV// A BIG CHANGE IN SILVER INVENTORY AT THE SLV://NO CHANGES IN SILVER IVWENTORY AT THE SLV.: A HUGE WITHDRAWAL OF 6.459 MILLION OZ FROMTHE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 547.167 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GOOD SIZED 641 CONTRACTS TO 146,193 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE LOSS IN OI WAS ACCOMPLISHED WITH OUR VERY STRONG $0.34 LOSS IN SILVER PRICING AT THE COMEX ON FRIDAY( ASSISTED BY THE CRIMINAL TAS/SPREADER LIQUIDATION). OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.34) AND ALSO SUCCESSFUL IN KNOCKING OFF SOME SILVER LONGS AS THEY REMAIN FIRM IN THEIR BELIEF OF A SILVER FAILURE AS WE HAD A TINY NET LOSS OF194 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 7.635 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 29 CONTRACTS OR 145,000 OZ//NEW STANDING: 8,145,000 / // V) GOOD SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -97

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTACTS for 4 days, total 4561, contracts: 22.805 million oz OR 5.7 MILLION OZ PER DAY. (1140CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 5.7 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 5.7 MILLION OZ

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 641 WITH OUR STRONG $0.34 LOSS IN SILVER PRICING AT THE COMEX// FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE CONTRACTS: 350 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S 145,000 QUEUE JUMP//NEW STANDING:8.145 // .. WE HAD A SMALL SIZED LOSS OF 291 OI CONTRACTS ON THE TWO EXCHANGES FOR 1.4550 MILLION OZ WITH THE LOSS IN PRICE.

WE HAD 27 NOTICES FILED TODAY FOR 135,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 12,278 CONTRACTS TO 498,442 AND FURTHER FROM NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -62 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE LOSS IN COMEX OI CAME WITH OUR STRONG LOSS IN PRICE OF $19.75//COMEX GOLD TRADING/FRIDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //JUST SPECULATOR SHORT COVERING FROM OUR STUPID SPECULATORS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 69.26 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP//NEW STANDING: 69.063 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $19.75 WITH RESPECT TO FRIDAY’S TRADING

WE HAD A STRONG SIZED LOSS OF 10,287 OI CONTRACTS 31.986 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1991 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 498,442

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,287, WITH 12,278 CONTRACTS DECREASED AT THE COMEX AND 1991 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 10,287 CONTRACTS OR 31.986 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1991) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (12,278,): TOTAL LOSS IN THE TWO EXCHANGES 10,287 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE. AT 69.26 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 0 OZ//NEW STANDING:69.063 TONNES / 3) MINOR LONG LIQUIDATION ( MOSTLY TAS)//CONSIDERABLE SPECULATOR SHORT COVERING //.,4) STRONG SIZED COMEX OI. LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

14,298 CONTRACTS OR 1,429,800 OZ OR 44.47 TONNES 4 TRADING DAY(S) AND THUS AVERAGING: 3575 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAY(S) IN TONNES: 44.47 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 44.47/3550 x 100% TONNES 1.26% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 44.47 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GOOD SIZED 641 CONTRACT OI TO 146,096 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 350 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 350 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 641 CONTRACTS AND ADD TO THE 350 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED LOSS OF 291 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 1.455 MILLION OZ

OCCURRED WITH OUR LOSS IN PRICE OF $0.34 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

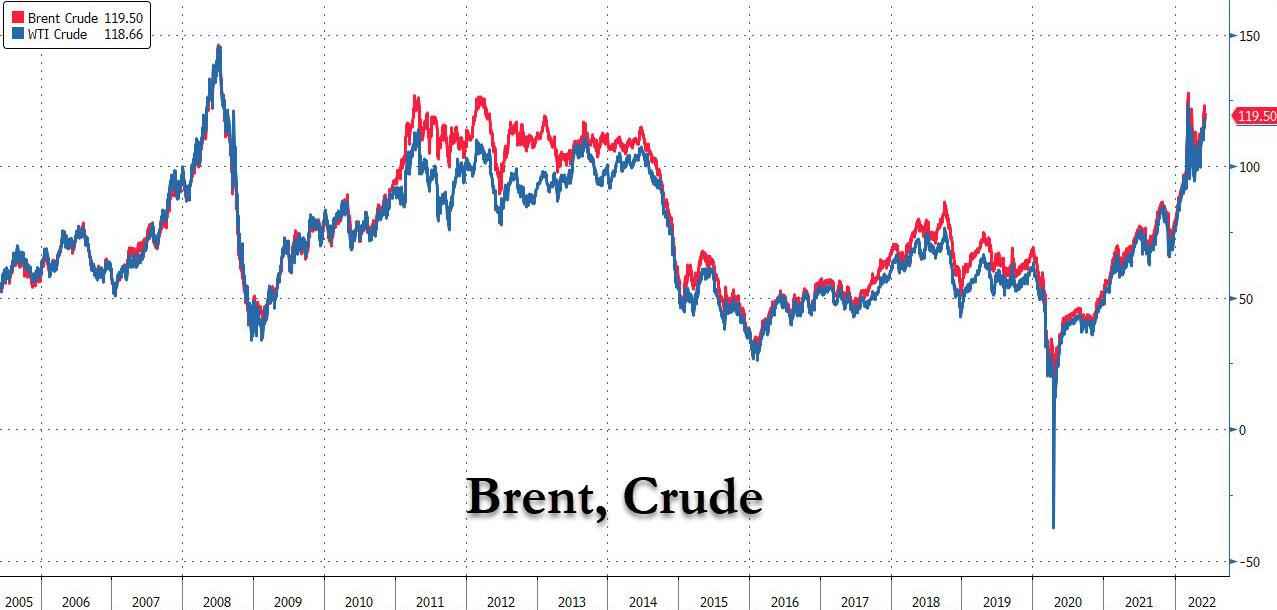

SHANGHAI CLOSED UP 40.91 PTS OR 1.28% //Hang Sang CLOSED UP 571.79 PTS OR 2.71% /The Nikkei closed UP 154.32 OR 0.56% //Australia’s all ordinaires CLOSED DOWN .54%% /Chinese yuan (ONSHORE) closed UP 6,6401 /Oil UP TO 119.30dollars per barrel for WTI and UP TO 120.08 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6401 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6389: /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER/

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 12,278 CONTRACTS TO 498,442 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR LOSS OF $19.75 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE NOW DOUBT HAD OUR SPREADER //TAS OPERATION IN FULL SWING ON FRIDAY. WE ALSO HAD A FAIR SIZED EFP (1991 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ARE CAUGHT. THE COMMERCIALS WILL SLAUGHTER THESE GUYS WHEN THEY THINK THE TIME IS RIGHT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A fair SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1991 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :1991 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1991 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 10,287 CONTRACTS IN THAT 1991 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 12,278 CONTRACTS..AND THIS STRONG LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR FALL IN PRICE OF GOLD $19.75.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (69.063),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 69.063 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $19.75) AND WERE SUCCESSFUL IN KNOCKING OFF SOME SPECULATOR LONGS/COMMERCIAL LONGS AS WELL AS SPECULATOR SHORTS//// WE HAVE REGISTERED A STRONG SIZED LOSS OF 31.986 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JUNE (69.063 TONNES)…

WE HAD 62 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 10,287 CONTRACTS OR 1,028,700 OZ OR 31.986 TONNES

Estimated gold volume 95,980/// poor

final gold volumes/yesterday 120,675 poor

INITIAL STANDINGS FOR JUNE ’22 COMEX GOLD //JUNE 6

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 32.151 oz BRINKS1 kilobar |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 615 notice(s) 61,500 OZ 1.9129 TONNES |

| No of oz to be served (notices) | 6884 contracts 688,400 oz 21.412 TONNES |

| Total monthly oz gold served (contracts) so far this month | 15,320 notices 1,532,000 OZ 47.6516 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

dealer deposits 0

total dealer deposit 0 oz//

No dealer withdrawals

0 customer deposits

total deposits: nil oz

1 customer withdrawals:

i) Out of Brinks: 32.151 (1 kilobars)

total withdrawal: 32.151 oz

ADJUSTMENTS: 1 dealer to customer//manfra/

20,166.668 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 7499 contracts having LOST 4043 contracts

We had 4043 notices filed on FRIDAY so we GAINED 0 contracts

July has a LOSS OF 56 OI to stand at 2072

August has a LOSS of 9524 contracts DOWN to 424,894 contracts

We had 4043 notice(s) filed today for 404,300 oz FOR THE JUNE 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 600 notices were issued from their client or customer account. The total of all issuance by all participants equate to 615 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 363 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2021. contract month,

we take the total number of notices filed so far for the month (15,320) x 100 oz , to which we add the difference between the open interest for the front month of (JUNE 7499 CONTRACTS ) minus the number of notices served upon today 615 x 100 oz per contract equals 2,220400 OZ OR 69.063 TONNES the number of TONNES standing in this active month of JUNE.

thus the INITIAL standings for gold for the JUNE contract month:

No of notices filed so far (15,320) x 100 oz+ (7499) OI for the front month minus the number of notices served upon today (615} x 100 oz} which equals 2,220,400 oz standing OR 69.063 TONNES in this active delivery month of JUNE.

TOTAL COMEX GOLD STANDING: 69.063 TONNES (A STRONG STANDING FOR A JUNE ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,210,073.763 oz

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 35,027,501.338 OZ

TOTAL ELIGIBLE GOLD: 17,043,783.837 OZ

TOTAL OF ALL REGISTERED GOLD: 17,983717.501 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,793226.0 OZ (REG GOLD- PLEDGED GOLD)

END

JUNE 2022 CONTRACT MONTH//SILVER//JUNE 6

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 805,334/501 oz CNT Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,093,826.344 oz CNT |

| No of oz served today (contracts) | 27CONTRACT(S) 135,000 OZ) |

| No of oz to be served (notices) | 119 contracts (595,000 oz) |

| Total monthly oz silver served (contracts) | 1502 contracts 7,510,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) zero dealer deposits And now for the wild silver comex results

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

i) Into CNT: 1,093,826.344 oz

total deposit: 1,093,826.344 oz

JPMorgan has a total silver weight: 171.637 million oz/336.894 million =50.95% of comex

Comex withdrawals: 2

i) Out of CNT 205,198.600 oz

ii) Out of Manfra: 600,135.901 oz

total withdrawal 805,334.501 oz

0 adjustments:

the silver comex is in stress!

TOTAL REGISTERED SILVER: 72,453 MILLION OZ

TOTAL REG + ELIG. 336.894 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE OI: 146 HAVING GAINED 12 CONTRACTS.

WE HAD 17 NOTICES FILED ON FRIDAY SO WE GAINED 29 CONTRACTS OR AN ADDITIONAL 145,000 OZ WILL STAND IN THIS NON ACTIVE

DELIVERY MONTH OF JUNE

JULY HAD A LOSS OF 1401 CONTRACTS DOWN TO 103,213 CONTRACTS.

AUGUST GAINED 151 CONTRACTS TO STAND AT 619

SEPTEMBER HAD A GAIN OF 718 CONTRACTS UP TO 27,920 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 27 for 135,000 oz

Comex volumes:54,484// est. volume today// poor

Comex volume: confirmed yesterday: 41,578 contracts ( poor )

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1510 x 5,000 oz = 7,510,000 oz

to which we add the difference between the open interest for the front month of JUNE(146) and the number of notices served upon today 27 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE./2022 contract month: 1510 (notices served so far) x 5000 oz + OI for front month of JUNE (146) – number of notices served upon today (27) x 5000 oz of silver standing for the JUNE contract month equates 8,145,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

MAY 18/WITH GOLD DOWN $2.55//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.07 TONNES FROM THE GLD///INVENTORY RESTS AT 1049.21 TONNES

MAY 17/WITH GOLD UP $5.40:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1053.28 TONNES

MAY 16/WITH GOLD UP $5.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD///INVENTORY RESTS AT 1055.89 TONNES

MAY 13/ WITH GOLD DOWN $16.25//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.8 TONNES FROM THE GLD.//INVENTORY RESTS AT 1060.82 TONNES

MAY 12/WITH GOLD DOWN $26.50: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD////INVENTORY RESTS AT 1066.62 TONNES

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

GLD INVENTORY: 1066.04 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

MAY 18/WITH SILVER UP $0.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL 1.892 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 17/WITH SILVER UP $.22 TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.508 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 16/WITH SILVER UP $.52 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.546 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.593 MILLION OZ//

MAY 13/WITH SILVER UP 31 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ/

MAY 12/WITH SILVER DOWN 88 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ//

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

INVENTORY TONIGHT RESTS AT 547.167 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/

END

3. Chris Powell of GATA provides to us very important physical commentaries

end

4.OTHER GOLD/SILVER COMMENTARIES

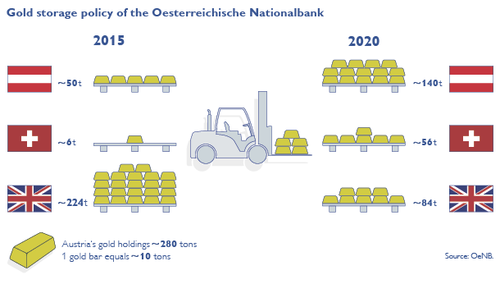

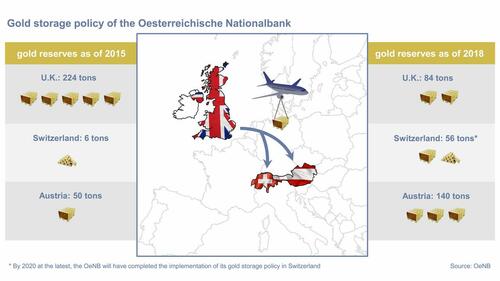

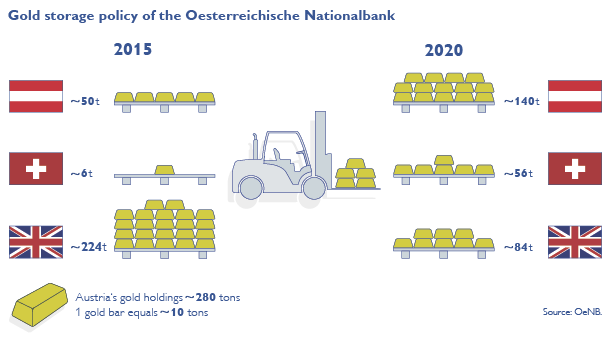

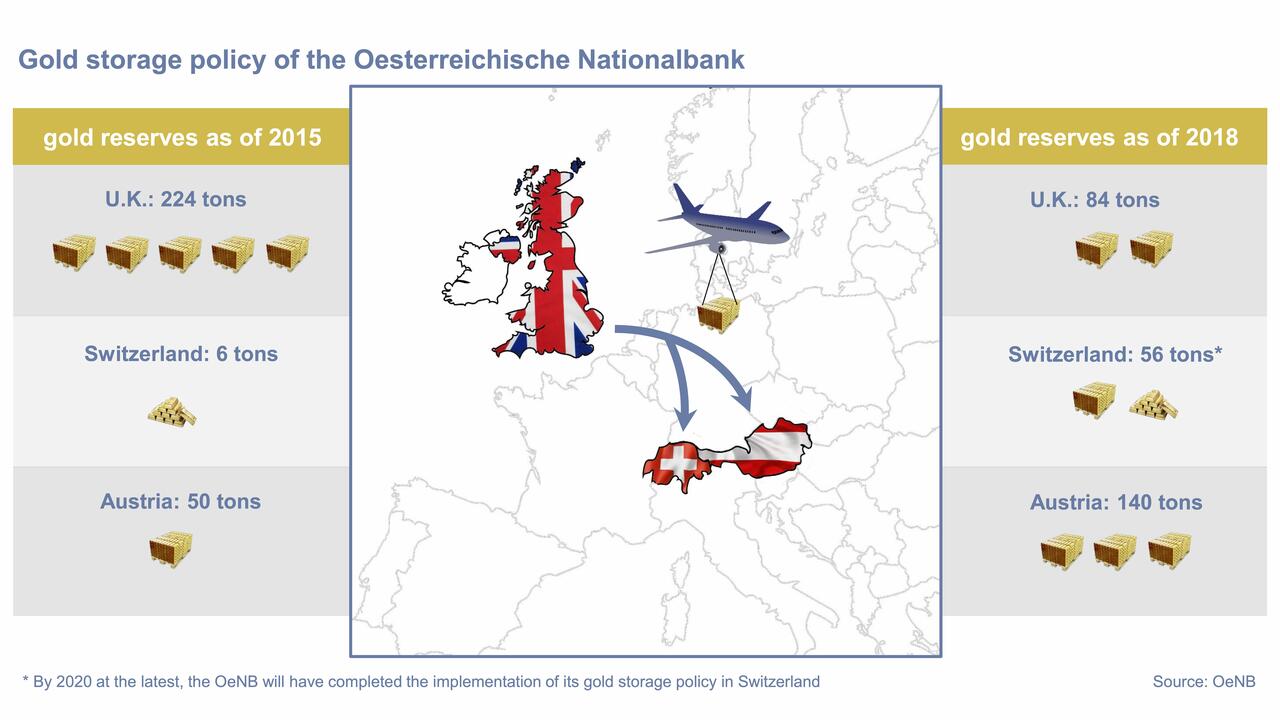

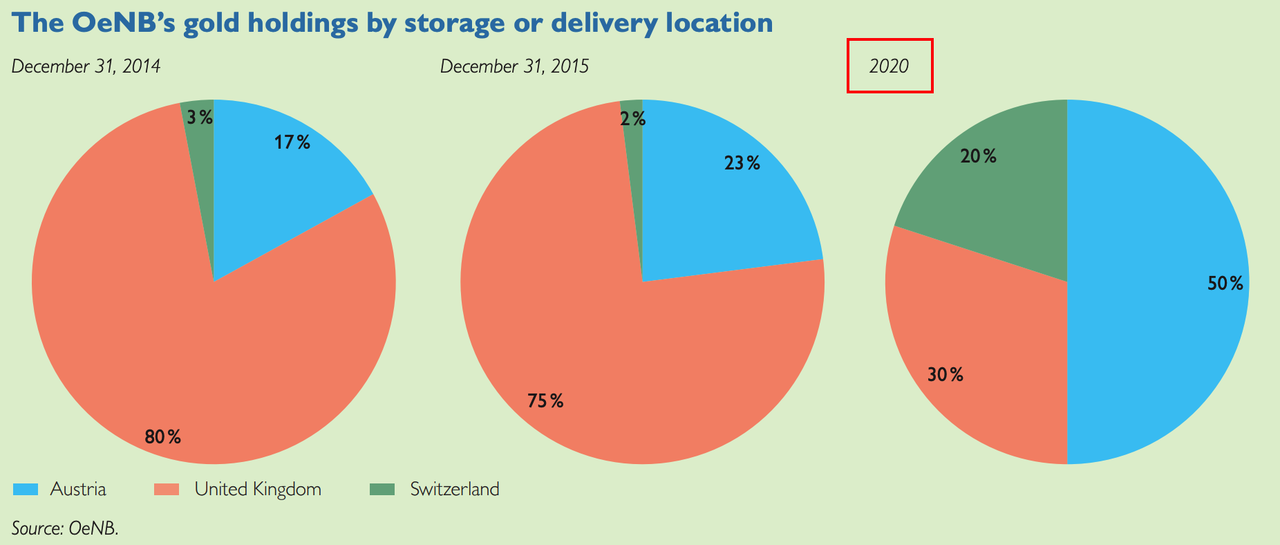

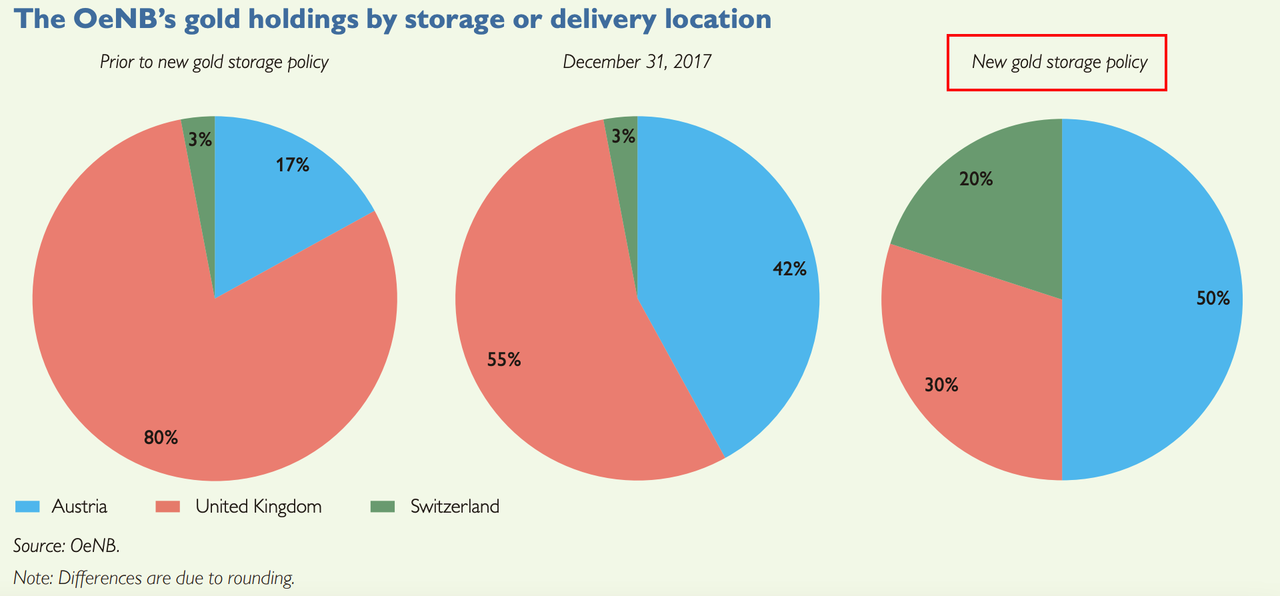

Austrian Monetary Gold Transfer From London To Switzerland, Planned In 2015, Still Hasn’t Arrived

SUNDAY, JUN 05, 2022 – 11:30 AM

By Jan Nieuwenhuijs of Gainesville Coins

A plan conceived by the Austrian central bank in 2015 to move 50 tonnes of their monetary gold from London to Switzerland has not been realized seven years later. Here is an introduction to what could possibly have happened.

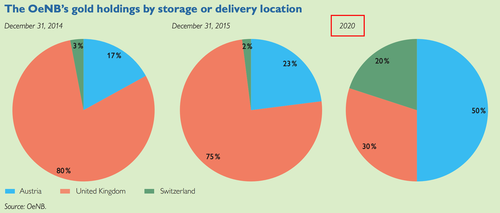

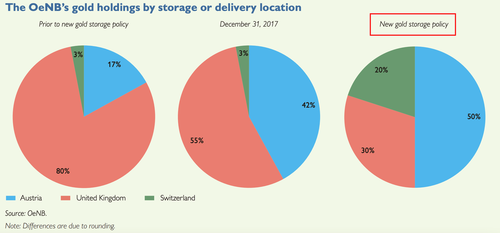

Since 2007 the Austrian central bank (Oesterreichische Nationalbank, hereafter “OeNB”) owns a few kilograms short of 280 tonnes of gold. In a report released by the Austrian “court of audits” (Rechnungshof, RH) from February 2015 it stated Austria was holding too much of its metal (82%) in London at the Bank of England (BOE). The court of audits concluded that all contracts between OeNB and its external depositories, but mainly the one in England, contained deficiencies and auditing measures were lacking.

Soon after the Austrian central bank announced a new storage concept. Contracts with external depositories would be reviewed and amended, 90 tonnes stored at BOE would be repatriated, and 50 tonnes would be transferred from London to Switzerland. Within five years (by 2020) the new storage concept should have been completed.

In 2018 OeNB announced to have repatriated 90 tonnes from London—ahead of schedule. Up to fifty percent of OeNB’s gold was brought home, divided between OeNB’s own vaults (90 tonnes) and the vaults of the Austrian Mint (50 tonnes). The transfer of gold from London to Switzerland, however, wasn’t done yet.

From January 2020 up until January 2022 there was a graph on OeNB’s website suggesting all metal that was supposed to be located in Switzerland had arrived, though in the fine print it read: “By 2020 at the latest, the OeNB will have completed the implementation of its gold storage policy in Switzerland.”

It’s very likely that up until today none of the gold that was planned to be transferred from London to Switzerland has arrived. Somewhere after January 2022, the graph above disappeared from OeNB’s website. Now the webpage reads:

The relocation [from London to Switzerland] has been postponed until organizational and logistical obstacles have been resolved.

In an email OeNB wrote me:

We can confirm that the relocation has been postponed. However, we are not allowed to disclose any details in order to comply with contractual obligations to keep business secrets of external partners involved.

For a fact OeNB knew the transfer would be delayed long before 2022. In OeNB’s Annual Report 2015 the original plan is shown: 90 tonnes would be repatriated from BOE and 50 tonnes would be transferred from the U.K. to Switzerland by 2020 (to store 50% in Austria, 30% in the U.K., and 20% in Switzerland). The same deadline was disclosed in the OeNB’s Annual Report 2016.

The original plan was first adapted in OeNB’s Annual Report 2017. The deadline was dropped and replaced by: “New gold storage policy.” Meanwhile zero gold had arrived in Switzerland by then. Still 3% was stored in Switzerland, the same as prior to the new gold storage concept.

Based on the publication dates of the reports OeNB must have concluded the shipment towards Switzerland would be postponed in between May 2017 and May 2018. Repatriating gold from London went as scheduled.

What could possibly have happened in between May 2017 and May 2018 that made OeNB have to wait for more than six years to move its gold from London to Switzerland?

Due to the complexity of this investigation, I have decided to publish my analysis in multiple parts—at least three as I see it now. In forthcoming articles, we will zoom in on the role of BOE, the Bank for International Settlements (BIS), and the vaults of the Swiss central bank—where the gold was supposed to be by now

end

5.OTHER COMMODITIES //DIESEL+ OTHERS

Diesel Once Again Racing Higher Than Prices For Crude Oil, Gasoline

SUNDAY, JUN 05, 2022 – 03:30 PM

By John Kingston of FreightWaves

Diesel prices have wrapped up four days of trading in which they are finishing far higher than they were at the start of the business week and have moved up faster than crude and gasoline prices.

It’s a worrisome trend for consumers because it signals that once again, diesel is moving at a pace more bullish than that of the petroleum market as a whole. That it already has done so in recent months is evident in the gasoline-diesel spread seen on price signs outside of retail outlets, and it has a complex set of causes.

Ultra low sulfur diesel for July delivery settled on the CME commodity exchange Friday at $4.2803 a gallon. That marked a gain of 7.19 cents per gallon on the day for an increase of 1.71%. It traded as high as $4.3250.

For the week — which was just four trading days, given the Memorial Day holiday — July ULSD rose 9.6%, posting a gain of 37.5 cents per gallon.

By contrast, the gain in WTI over the four days (from the May 27 settlement through the settlement at the end of this week) was 3.3% for West Texas Intermediate crude, barely any overall movement for global crude benchmark Brent, and 8.6% for RBOB, an unfinished gasoline blendstock that is a trading proxy for gasoline.

Those sorts of numbers suggest that increasingly, the issue in the market is not just the loss of Russian crude supplies but a loss of refining capacity worldwide that is coming home to roost, aggravated by the effective loss of some Russian refining capacity and its output as a result of formal and informal sanctions.

It is most evident in one of the most basic numbers traders watch: the 3:2:1. It’s a rough estimate of refining margins, arrived at by taking the price of either Brent or WTI and multiplying it by 3, and then subtracting that number from the sum of taking two barrels of gasoline and one barrel of ULSD.

The 3:2:1 for both Brent and WTI spent most of the week in the range of $55 to $60 per barrel, depending on how it was calculated. (Even a simple number like this can be the focus of differences in methodology.) At the start of 2021, it was closer to $20 a barrel, a figure that was far more in line with historic norms. A 3:2:1 in the upper $50s is leaving traders searching for new words to describe how unprecedented that is.

That sort of blowout can be expected in a world in which the International Energy Agency estimated earlier this year that global refining capacity had a net decline of 730,000 barrels per day in 2021. While that is less than 1% of the global oil market, in a tight supply/demand balance, the impact of such a decline can be enormous.

A $55, 3:2:1 will lead refiners to process as much as they can. And that is evident in the weekly Energy Information Administration data on U.S. refining operations — mostly.

U.S. refineries operated at 92.6% of capacity in the week ended May 27. While that is a healthy number, it actually was down slightly from the 93.6% from the prior week. And it isn’t that much higher than the average for the final full week of May, which is 91.8% over the last five years of data points, excluding pandemic-impacted 2020.

But the numbers on ULSD production nationwide are disappointing. Total output the last two weeks through May 27 was 4.875 and 4.818 million barrels per day, respectively. Those are the highest in a year, but the bad news for diesel consumers is that it’s still less than the output for the final week of May for the three years before the pandemic. Even with enormous margins, U.S. refiners are making less diesel than they were for this time of the year between 2017 and 2019.

On the U.S. East Coast, refiners have rushed to take advantage of the strong margins in that region. Refiners there over the last two weeks have operated at 97% and 98.2%, respectively, in an industry in which it is virtually impossible to run at 100% for any sustained period of time. Something inevitably breaks down. But the East Coast operating rates are against a base of refining capacity that has lost several hundred thousand barrels per day in the past several years.

The East Coast has been of particular interest to the diesel market given its soaring value relative to the Gulf Coast, which is the major refining center and a key export point for the U.S. and the world.

Weekly inventory figures dropped once again for the week ended May 27. They were at 18.8 million barrels, down from 20.4 million barrels just two weeks ago. And when it was at 20.4 million, it was already well below the roughly 38 million barrels at the start of the year in the East Coast area known as PADD 1, an EIA-designated area.

Despite those tight inventories, the spot market spread between the East Coast price and that in the Gulf Coast reacted counterintuitively.

Through much of May, as East Coast diesel inventories declined steadily during the year, that spread blew out to as much as 70 cents per gallon, according to data provided to FreightWaves by benchmark gateway General Index.

But on Friday, General Index estimated the spread at 7 cts/g, after it declined steadily through the week. It closed last week at 11.5 cents, went to 10.8 cents for Monday and Tuesday and then dropped to 5 cents Thursday before the slight widening Friday.

That odd movement may be a signal that the squeeze seen in the East is no longer the outlier and tight inventories through the country mean the East Coast just got there first. For example, the spread between the Gulf Coast and Chicago ULSD markets stood at roughly 20 cents by Thursday, with Chicago running that much of a premium to the Gulf Coast. That spread also tends to be a few cents during normal periods, much like the East Coast/Gulf Coast spread.

END

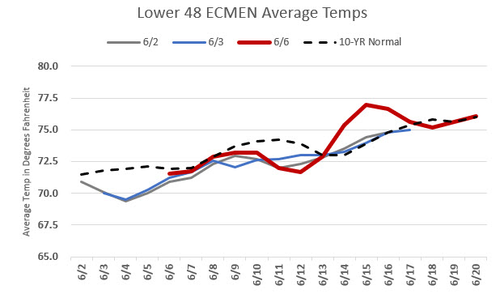

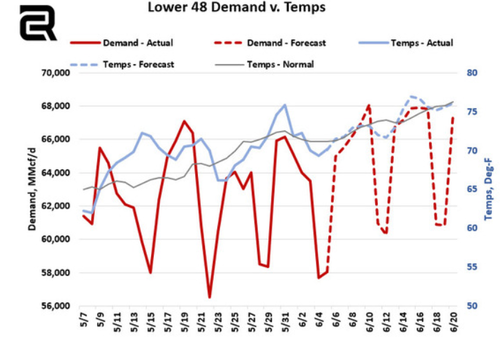

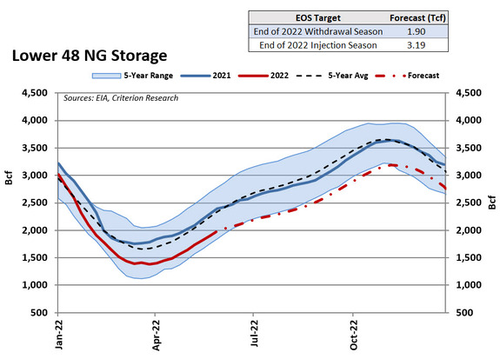

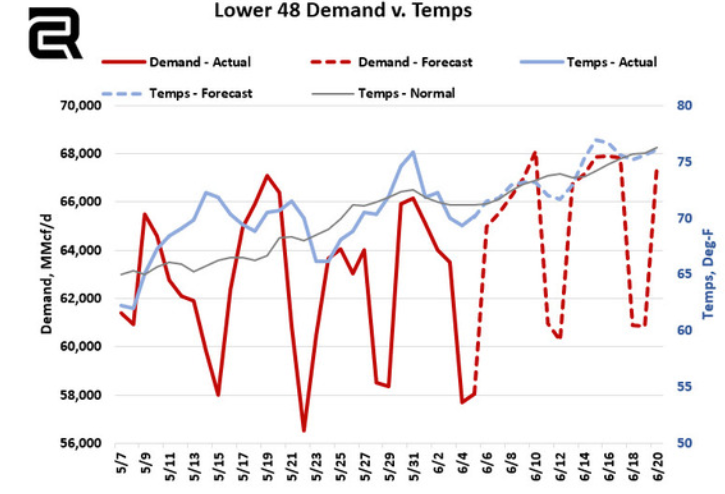

Perfect Storm Of Factors Sends US Natural Gas Prices Soaring

MONDAY, JUN 06, 2022 – 03:25 PM

U.S. natural gas fundamentals remain bullish as above-normal temperatures drive cooling demand and dwindling supplies that would’ve been used for the next winter season cause market tightness, sending futures for July delivery soaring 9.5% to $9.340/mmbtu as of 1315 ET.

Houston-based energy firm Criterion Research sheds more color on the natgas fundamentals driving prices higher. They report a combination of factors, including above-average temperatures in the Lower U.S. 48, natgas demand, slumping natgas production, and below-average national stockpiles, which have driven July contracts above $9.

The Lower 48’s weather outlook has come in warmer this morning, with the latest models showing a warmer than average forecast for mid-June (versus the ten-year average.)

The week ending 6/17 should bring impressive natural gas demand numbers of 65.5 Bcf/d, marking the highest we’ve seen this summer.

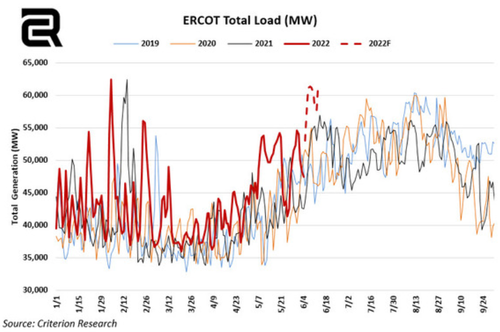

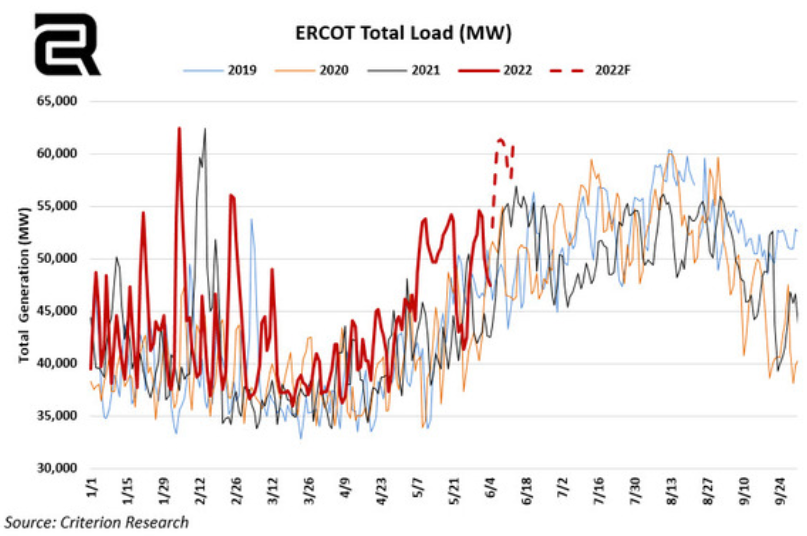

The warmer trend can especially be seen in states such as Texas, where ERCOT is forecasting record-high summer generation.

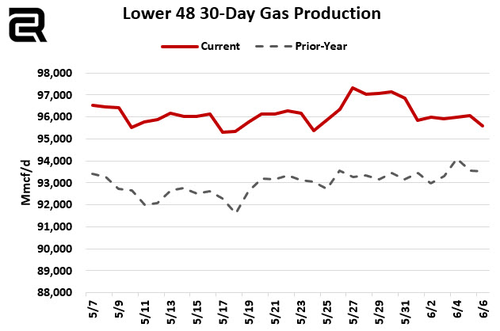

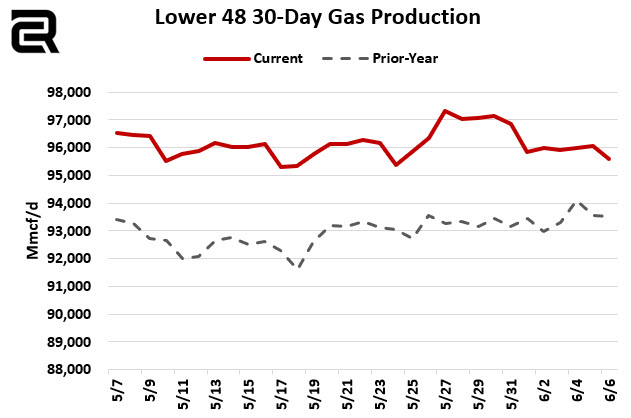

While the demand side of the equation comes in strong, U.S. natural gas production has been struggling since the start of June. Volumes quickly fell after June 1 and have remained off of the May highs.

Although general production growth is widely expected through year-end by most energy analyses, the speed at which that production comes online is the main concern. Higher production rates will be needed to fill national storage inventories before the winter, especially if summer temperatures continue to come in above-average.

At Criterion, the latest iteration of our long-term supply & demand forecast, we have adjusted our Fall EOS target to a lower 3.19 Tcf, which marked a drop from the last forecast for a 3.25 Tcf level.

The current situation may remain uber bullish and could push natgas prices even higher as summer begins and driving season is underway, which puts upward pressure on energy markets.

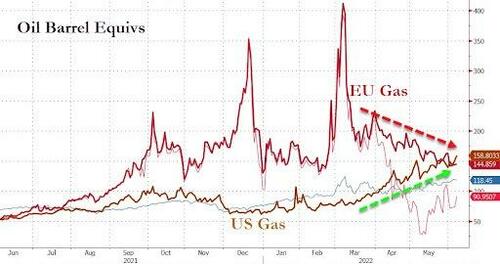

Higher U.S. demand versus Europe has compressed the E.U.-U.S. natgas spread (1mo ahead vs. futs).

And in fact, US natgas futures are now trading at a premium to Day-Ahead EU NatGas prices.

Soaring natgas prices will only mean the cost of power will rise. We outlined the cities where power bills will skyrocket this summer as threats of rolling blackouts increase.

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings MONDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.6401

OFFSHORE YUAN: 6.6389

HANG SANG CLOSED DOWN 212.81 PTS OR 1.00%

2. Nikkei closed UP 154.32% OR 0.56%

3. Europe stocks ALL CLOSED ALL GREEN

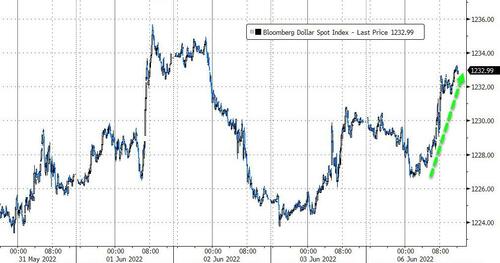

USA dollar INDEX DOWN TO 102.00/Euro RISES TO 1.0727

3b Japan 10 YR bond yield: RISES TO. +.238/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 130.65/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP -SHORE CLOSED DOWN// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +1.258%/Italian 10 Yr bond yield RISES to 3.34% /SPAIN 10 YR BOND YIELD FALLS TO 2.40%…

3i Greek 10 year bond yield RISES TO 3.89

3j Gold at $1853.90 silver at: 22.33 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0.11 roubles/dollar; ROUBLE AT 60.83

3m oil into the 119 dollar handle for WTI and 120 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 130.65DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9617– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0318well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

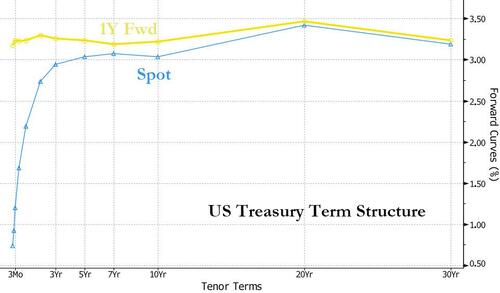

USA 10 YR BOND YIELD: 2.953 DOWN 0 BASIS PTS

USA 30 YR BOND YIELD: 3.108 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 16.59

Futures Jump, Tech Stocks Rally As Beijing Eases Covid Restrictions

MONDAY, JUN 06, 2022 – 07:51 AM

Global markets and US equity futures pushed sharply higher to start the new week (at least until some Fed speakers opens their mouth and threatens a 100bps emergency rate hike) as Beijing’s latest move to ease Covid restrictions injected a note of optimism into markets rattled by inflation and rate-hike concerns. Nasdaq 100 futures climbed 1.4% at 7:15 a.m. in New York after the underlying index erased more than $400 billion in market value on Friday amid renewed concerns about tightening monetary policy, as Beijing rolled back Covid-19 restrictions, boosting global risk appetite after reporting zero local covid cases on Monday while also finding no community cases for three straight days…

… while a Wall Street Journal report that China is preparing to conclude its probe on Didi Global boosted sentiment further, with Didi shares surging 50% and sending the Hang Seng Tech index soaring. S&P 500 futures also climbed, rising about 1% and trading near session highs. Treasuries and the dollar slipped.

Among other notable movers in premarket trading, Apple rose 1.6%, Tesla jumped 3.9% after tumbling over 9% by the close on Friday, while cryptocurrency-tied stocks jumped with Bitcoin. Here are some other notable premarket movers:

- Amazon.com (AMZN US) shares rose as much as 2% following a 20-for-1 stock split.

- Didi Global Inc. (DIDI US) soared after a report that Chinese regulators are about to conclude a probe into the company and restore its apps to mobile stores as soon as this week.

- Cryptocurrency-tied stocks climb with Bitcoin, which rose beyond the $30,000 level after languishing at the weekend. Riot Blockchain (RIOT US) +7.1%; Coinbase (COIN US) +6.6%.

- Crowdstrike (CRWD US) shares rise as much as 3.9% following an upgrade to overweight from equal- weight at Morgan Stanley, with the broker saying that the cyber security firm offers “durable” growth and free cash flow at a discount.

- ON Semi (ON US) shares rise as much as 8.2%. The sensor maker will be added to the S&P 500 Index this month, S&P Dow Jones Indices said late

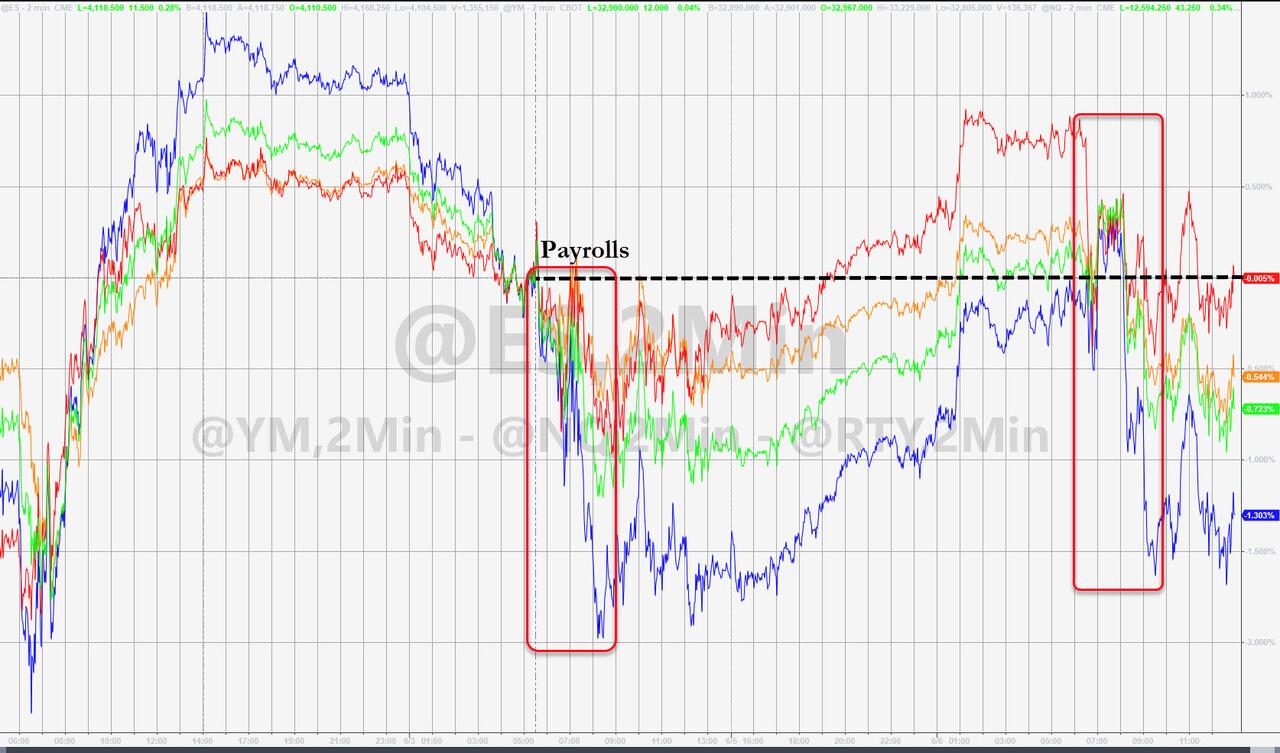

US stocks slumped in last week’s final session after strong hiring data cleared the way for the Federal Reserve to remain aggressive in its fight against inflation by raising rates, and after repeat warnings by Fed presidents that the central bank was willing to keep hiking. This week, focus will be on the latest US CPI print to assess how much further the Fed will tighten policy.

Inflation is likely to “stall by the end of this year unless the energy or oil prices double again, but a lot of it is already priced in,” Shanti Kelemen, chief investment officer at M&G Wealth, said on Bloomberg Television. While the economy is likely to slow, “I don’t think the US will flip into a recession this year. I think there is still too much of a tailwind from spending and economic activity.”

Goldman economists said the Fed may be able to pull off its aggressive rate-hike plan without tipping the country into recession. The easing of Chinese lockdowns will help abate supply-chain pressures, said Diana Mousina, a senior economist at AMP Capital.

“Positive news around Chinese economic activity and cheaper equity valuations could offer value from a long-term investment perspective, but volatility will remain high in the short-term,” Mousina said in a note.

On the other hand, Morgan Stanley’s permagloomish Michael Wilson warned that weakening corporate profit forecasts will provide the latest headwind to US stocks, which are likely to fall further before bottoming during the second-quarter earnings season.

In Europe, the Stoxx 600 was up 0.9% with technology and mining stocks leading gains. Basic resources led an advance in the Stoxx Europe 600 index as copper rose to its highest since April, with sentiment across industrial metals bolstered by China’s gradual reopening. The technology sector also outperformed, following a gain for Asian peers and amid a recovery in Nasdaq 100 futures in the US. The Stoxx 600 Tech index was up as much as 2.1%; Stoxx 600 benchmark up 0.9%. Tencent-shareholder Prosus was among the biggest contributors to the gain amid a rise for Hong Kong’s Hang Seng tech index, driven by Didi Global and Meituan; Tencent shares rose 2.4% while Semiconductor-equipment giant ASML was the biggest contributor to the gain; other chip stocks ASMI, Infineon and STMicro all higher too. Just Eat Takeaway also higher following a report that Grubhub co-founder Matt Maloney had worked with private equity investor General Atlantic to buy back the food delivery company he sold to the Dutch firm last year. Here are some of the other notable European movers today:

- Just Eat Takeaway.com shares rise as much as 12% in the wake of a report saying Grubhub co-founder Matt Maloney had worked with private equity investor General Atlantic to buy back the food delivery company he sold to the Dutch firm last year for $7.3b.

- Semiconductor-equipment giant ASML climbs as much as 3.1% as European tech stocks outperform the broader benchmark, following a gain for Asian peers and amid a recovery in Nasdaq 100 futures.

- LVMH gains as much as 1.7% with luxury stocks active as Beijing continues to roll back Covid-19 restrictions in a bid to return to normality. Kering and Hermes both climb as much as 1.9%.

- Melrose rises as much as 4.7% after the firm said it has entered into an agreement to sell Ergotron to funds managed by Sterling for a total of ~$650m, payable in cash on completion.

- Serica Energy jumps as much as 12%, the most since March 30, after the oil and gas company published a corporate update and said it expects to benefit from investment incentives packaged with the UK’s windfall tax.

- Airbus rises as much as 2.8% after Jefferies reinstated the stock as top pick in European aerospace & defense, replacing BAE Systems, as short-term production challenges should not overshadow the potential to double Ebit by 2025.

- EDF drops as much as 3.3% after HSBC analyst Adam Dickens downgraded to reduce from hold, citing “corroded confidence”

- Accell falls as much as 4.8%, the most intraday since December, after KKR’s tender offer for the bicycle maker failed to meet the 80% acceptance threshold.

Meanwhile, the European Central Bank is set to announce an end to bond purchases this week and formally begin the countdown to an increase in borrowing costs in July, joining global peers tightening monetary policy in the face of hot inflation. The ECB is planniing to strengthen its support of vulnerable euro-area debt markets if they are hit by a selloff, Financial Times reported. Italian and Spanish bonds gained.

Earlier in the session, Asian stocks climbed, supported by a rally in Chinese tech shares and positive sentiment following Beijing’s economic reopening. The MSCI Asia Pacific index rose 0.6% as Hong Kong-listed internet names jumped after a report that authorities are wrapping up their probe into Didi Global. Hong Kong and Chinese shares were among the top gainers in the region, also helped by Beijing moving closer to returning to normal as it rolled back Covid-19 restrictions. “As policymakers continue to deliver on support pledges, the worst is likely behind us,” said Marvin Chen, strategist at Bloomberg Intelligence. “We are seeing the beginning of a recovery into the second half of the year as the growth outlook bottoms out.”

Japanese shares were higher, with transportation and restaurant stocks gaining after the Nikkei reported the government is considering restarting the “Go To” domestic travel subsidy campaign as soon as this month. Japanese equities erased early losses and rose with Chinese stocks as a loosening of Covid-19 restrictions in Beijing increased bets that economic activity will pick up. The Topix rose 0.3% to 1,939.11 as of market close Tokyo time, while the Nikkei advanced 0.6% to 27,915.89. Daiichi Sankyo Co. contributed the most to the Topix gain, increasing 3.7%.

Foreign investors are returning to emerging Asian equities after several weeks of outflows, data compiled by Bloomberg show. Weekly inflows for Asian stock markets excluding Japan and China climbed to almost $2.7 billion last week, the most since February. Asian stocks have been outperforming their US counterparts over the past few weeks, with the MSCI regional benchmark up 5.7% since May 13, more than double the gains in the S&P 500. Stock markets in South Korea, New Zealand and Malaysia were closed on Monday

Stocks in India dropped amid concerns over inflation as the Reserve Bank of India’s interest rate setting panel starts a three-day policy meeting. The S&P BSE Sensex fell 0.2% to 55,675.32 in Mumbai, while the NSE Nifty 50 Index declined 0.1%. Ten of the 19 sector sub-gauges managed by BSE Ltd. slid, led by an index of realty companies. Makers of consumer discretionary goods were also among the worst performers. “The market has been exercising caution ahead of the credit policy announcement this week, and hence investors trimmed their position in rate-sensitive sectors such as realty,” according to Kotak Securities analyst Shrikant Chouhan. The yield on the benchmark 10-year government bond rose to its highest level since 2019 on Monday amid a surge in crude prices and ahead of the RBI’s rate decision on Wednesday. Reliance Industries contributed the most to the Sensex’s decline, decreasing 0.5%. Out of 30 shares in the Sensex index, 9 rose and 21 fell.

In Australia, the S&P/ASX 200 index fell 0.5% to close at 7,206.30 after a strong US jobs report reinforced bets for aggressive Fed tightening. The RBA is also expected to lift rates on Tuesday, with the key debate centering on the size of the move. Read: Australia Set for Back-to-Back Rate Hikes Amid Split on Size Magellan was the worst performer after its funds under management for May declined 5.2% m/m. Tabcorp climbed after settling legal proceedings with Racing Queensland. In New Zealand, the market was closed for a holiday

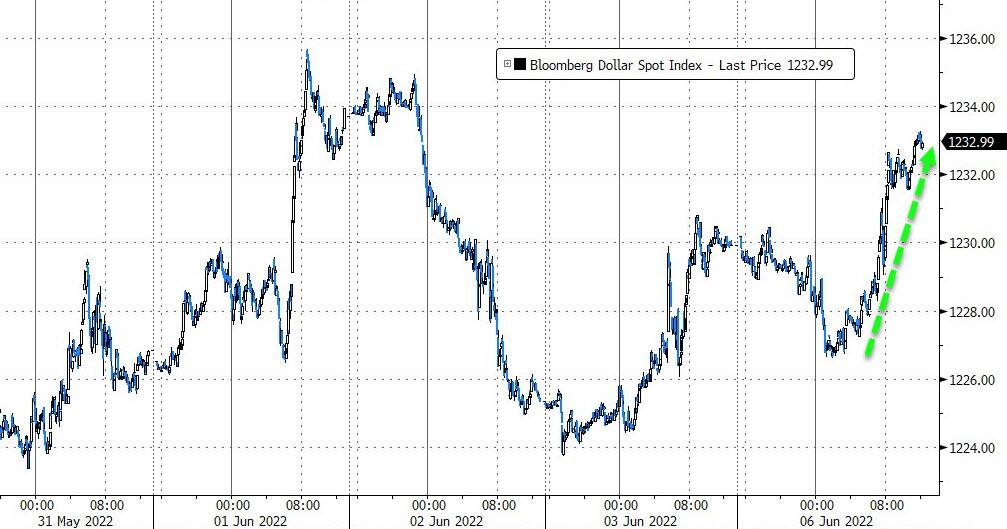

In FX, the dollar fell against its Group-of-10 peers as hopes for a recovery in China’s economy damped demand for the haven currency. The Bloomberg Dollar Spot Index fell 0.3% after posting a weekly gain on Friday. China’s equity index jumped after Beijing rolled back Covid-19 restrictions and received a further boost after a report that a ban on Didi adding new users may be lifted. “Further lifting of restrictions in Beijing helped Chinese equities, which spilled over into Europe with risk more ‘on’ than ‘off’,” Societe Generale strategist Kit Juckes wrote in a note to clients. “The dollar is once again on the back foot.” USD/JPY dropped 0.1% to 130.73. It touched 130.99 earlier, inching closer to the 131.35 reached last month, which was the highest since April 2002. “Dollar-yen is being sold for profit-taking because we don’t have enough catalysts to break 131.35,” said Juntaro Morimoto, a currency analyst at Sony Financial Group Inc. in Tokyo. But, should US inflation data due this week be higher than estimated, it will see dollar-yen break 131.35.

In rates, Treasuries, though off session lows, remained under pressure as S&P 500 futures recover a portion of Friday’s loss. 10-year TSY yields rose 1bp to 2.95%, extending the streak of advances to five days, the longest in eight weeks; UK 10-year yield underperformed, jumping 6bps to 2.21% after domestic markets were closed Thursday and Friday for a holiday. US auctions resume this week beginning Tuesday, while May CPI report Friday is the main economic event. IG dollar issuance slate includes Tokyo Metropolitan Govt 3Y SOFR; this week’s issuance slate expected to be at least $25b. Three- month dollar Libor +3.90bp to 1.66500%. Bund, Treasury and gilt curves all bear-flatten, gilts underperform by about 2bps at the 10-year mark. Peripheral spreads tighten to Germany.

In commodities, WTI crude futures hover below $120 after Saudis raised oil prices for Asia more than expected. Spot gold is little changed at $1,851/oz. Spot silver gains 1.5% near $22. Most base metals trade in the green; LME nickel rises 5.4%, outperforming peers. LME tin lags, dropping 0.7%.

There is no major economic data on the US calendar.

Market Snapshot

- S&P 500 futures up 1.1% to 4,152.50

- STOXX Europe 600 up 0.9% to 443.90

- MXAP up 0.6% to 169.12

- MXAPJ up 0.8% to 558.02

- Nikkei up 0.6% to 27,915.89

- Topix up 0.3% to 1,939.11

- Hang Seng Index up 2.7% to 21,653.90

- Shanghai Composite up 1.3% to 3,236.37

- Sensex little changed at 55,772.44

- Australia S&P/ASX 200 down 0.4% to 7,206.28

- Kospi up 0.4% to 2,670.65

- German 10Y yield little changed at 1.29%

- Euro up 0.2% to $1.0742

- Brent Futures up 0.5% to $120.28/bbl

- Gold spot up 0.0% to $1,851.93

- U.S. Dollar Index down 0.22% to 101.92

Top Overnight News from Bloomberg

- Boris Johnson will face a leadership vote in his ruling Conservative Party on Monday following a series of scandals, including becoming the first sitting prime minister found to have broken the law.

- Chinese regulators are concluding probes into Didi and two other US-listed tech firms, preparing as early as this week to lift a ban on their adding new users, the Wall Street Journal reported, citing people familiar with the matter.

- The European Central Bank is set to strengthen commitment to support vulnerable euro-area debt markets if they are hit by a selloff, the Financial Times reported, citing unidentified people involved in the discussions.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mixed following last Friday’s post-NFP losses on Wall St and ahead of this week’s global risk events – including central bank meetings and US inflation data, while participants also digested the latest Chinese Caixin PMI figures and the North Korean missile launches. ASX 200 was pressured by weakness in tech and mining, with sentiment not helped by frictions with China. Nikkei 225 pared early losses but with upside limited by geopolitical concerns after North Korean provocations. Hang Seng and Shanghai Comp. were encouraged by the easing of COVID restrictions in Beijing, while the Chinese Caixin Services and Composite PMI data improved from the prior month but remained in contraction. Sony Group (6758 JT) said its planned EV JV with Honda Motor (7267 JT) may hold a public share offering, according to Nikkei.

Top Asian News

- China’s Beijing will continue to roll back its COVID-19 restrictions on Monday including allowing indoor dining and public transport to resume in most districts aside from Fengtai and some parts of Changping, according to Reuters and Bloomberg. Furthermore, a China health official called for more targeted COVID control efforts and warned against arbitrary restrictions for COVID, while an official also said that Jilin and Liaoning should stop the spread of COVID at the border.

- Australia accused China of intercepting a surveillance plane and said that a Chinese military jet conducted a dangerous manoeuvre during routine surveillance by an Australian plane over international waters on May 26th, according to FT.

- BoJ Governor Kuroda said Japan is absolutely not in a situation that warrants tightening monetary policy and the BoJ’s biggest priority is to support Japan’s economy by continuing with powerful monetary easing, while he added Japan does not face a trade-off between economic and price stability, so can continue to stimulate demand with monetary policy, according to Reuters.

European bourses are firmer on the session, Euro Stoxx 50 +1.3%, with newsflow thin and participants reacting to China’s incremental COVID/data developments during reduced trade for Pentecost. Stateside, futures are bid to a similar extent in a paring of the post-NFP pressure on Friday, ES +1.0%, with no Tier 1 events for the region scheduled today and attention very much on inflation data due later. Chinese regulators intend to conclude the DiDi (DIDI) cybersecurity probe, and remove the ban on new users, via WSJ citing sources; could occur as soon as this week. DIDI +50% in pre-market trade

Top European News

- Most of the ECB governing council members are expect to back proposals to create a bond-purchase programme to buy stressed government debt, such as Italy, according to sources cited by the FT.

- Confidence vote in UK PM Johnson to occur between 18:00-20:00BST today, results to be immediately counted, announcement time TBC.

- London’s Heathrow Airport ordered carriers to limit ticket sales for flights until July 3rd to maintain safety amid understaffing and overcrowding, according to The Times.

- French Finance Minister Le Maire expects positive economic growth this year although will revise economic forecasts in July, according to Reuters.

- EU Commissioner Gentiloni said he aims to propose reform for the EU stability pact after summer which could envisage a specific debt/GDP target for each country, while he added that Italy should show commitment to keeping public debt under control and needs to avoid increasing current spending in a permanent way, according to Reuters.

FX

- Pound perky on return from long Platinum Jubilee holiday weekend as UK yields gap up in catch up trade and Sterling awaits fate of PM; Cable above 1.2550 to probe 10 DMA, EUR/GBP tests 0.8550 from the high 0.8500 area.

- Dollar eases off post-NFP peaks as broad risk sentiment improves and DXY loses 102.000+ status.

- Kiwi lofty as NZ celebrates Queen’s birthday and Aussie lags ahead of RBA awaiting a hike, but unsure what size; NZD/AUD above 0.6525, AUD/USD sub-0.7125 and AUD/NZD cross closer to 1.1050 than 1.1100.

- Euro firmer amidst further declines in EGBs, bar Italian BTPs, eyeing ECB policy meeting and potential news on a tool to curb bond spreads, EUR/USD nearer 1.0750 than 1.0700.

- Loonie underpinned by rise in WTI after crude price increases from Saudi Arabia, but Lira extends losses irrespective of CBRT lifting collateral requirements for inflation linked securities and Government bonds; USD/CAD under 1.2600, USD/TRY not far from 16.6000.

Fixed income

- Gilts hit hard in catch-up trade, but contain losses to 10 ticks under 115.00 awaiting the outcome of no confidence vote in PM Johnson

- Bunds underperform BTPs ahead of ECB on Thursday amidst reports that a new bond-buying scheme to cap borrowing costs may be forthcoming; 10 year German bond down to 149.59 at worst, Italian peer up to 123.15 at best

- US Treasuries relatively flat in post-NFP aftermath and ahead of low-key Monday agenda comprising just employment trends

Commodities

- Crude benchmarks are bid by just shy of USD 1.00/bbl; though, overall action is contained amid limited developments and two-way factors influencing throughout the morning.

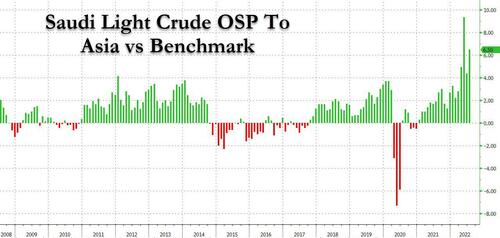

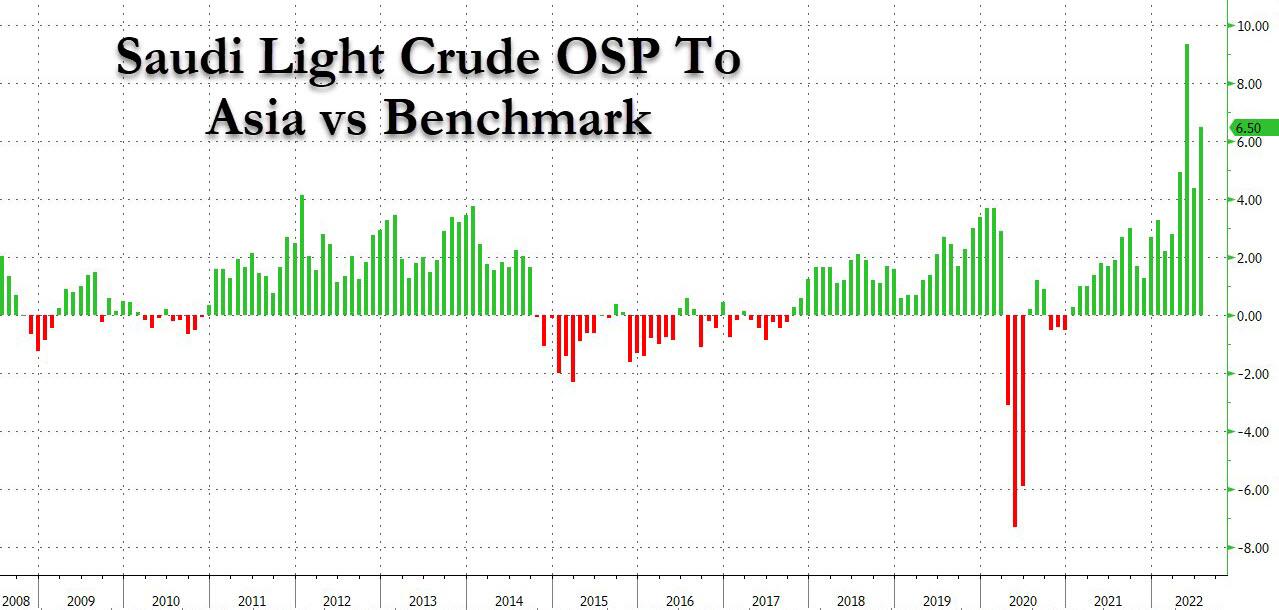

- Saudi Aramco increased its prices to Asia for July with the light crude premium raised to USD 6.50/bbl from USD 4.40/bbl vs Oman/Dubai, while it raised the premium to North West Europe to USD 4.30/bbl from USD 2.10/bbl vs ICE Brent but maintained premiums to the US unchanged from the prior month.

- Oman announced new oil discoveries that will increase output by 50k-100k bpd in the next 2-3 years, while it noted that its crude reserves stand at 5.2bln bbls and gas reserves are at around 24tln cubic feet, according to the state news agency citing the energy and minerals minister.

- Libya’s El Sharara oil field resumed production at around 180k bpd after having been shut by protests for more than six weeks, according to Argus.

- French Finance Minister Le Maire said that France is in discussions with the UAE to replace Russian oil supplies, according to Reuters.

- US will permit Italy’s Eni and Spain’s Repsol to begin shipping oil from Venezuela to Europe as early as next month to replace Russian crude, according to Reuters citing sources familiar with the matter.

- Austria released strategic fuel reserves to cover for loss of production at a key refinery due to a mechanical incident, according to Reuters.

- Indonesia will adjust its palm oil export levy with the regulations that will outline the changes expected soon, according to a senior official in the economy ministry cited by Reuters.

- Turkish presidential spokesman Kalin said deliveries of Ukrainian grain via the Black Sea and through the area of the strait could begin in the near future, according to TASS citing an interview with Anadolu news agency.

US Event Calendar

- Nothing major scheduled

DB’s Jim Reid concludes the overnight wrap

Later this morning, I will be publishing the 24th Annual Default Study entitled “The end of the ultra-low default world?”. Please keep an eye out for it but I won’t let you miss it in the EMR and CoTD over the next few days!

For those in the UK, I hope you had a good four-day weekend. We went to two big parties and my digestive system and liver need a rest. Well, until my upcoming birthday this weekend!. One of the parties had a converted VW campervan with 5 or 6 self-service drinks taps on the outside of which one was filled with ice cold Prosecco. Thankfully the Queen doesn’t have a 70-year Jubilee very often!

The fun and games in markets this week are heavily back ended as an ECB meeting on Thursday is followed by US CPI on Friday. The rest of the week is scattered with production and trade balance data, while Chinese aggregate financing data is expected at some point. The Fed are now on their pre-FOMC blackout so the attention will be firmly on the ECB this week.

So let’s preview the two main events. For the ECB, our European economists believe the ECB will confirm that APP net purchases will cease at the end of the month, paving the way for policy rate lift-off at the July meeting. Our economists believe the ECB will have to hike rates by 50 basis points at either the July or September meeting, with the risks skewed toward the latter, to accelerate the policy hiking cycle in light of growing inflationary pressures. Our economists also believe that hiking cycle will ultimately reach a 2 percent terminal rate next summer, some 50 basis points into restrictive territory. As prelude, next week watch for the staff’s forecast to upgrade inflation to 2 percent in 2024, satisfying the criteria for lift-off. With all three lift-off conditions met, expect the statement language to upgrade rate guidance for the path of the hiking cycle. Meanwhile, the June meeting should also bring about the expiration of the TLTRO discount.

There are two interesting things for the ECB to consider at the extreme end of the spectrum at the moment. Firstly German wages seem to be going higher. In a note on Friday, DB’s Stefan Schneider (link here) updated earlier work on domestic wage pressures by highlighting that on Thursday night, the 700k professional cleaners in the country achieved a 10.9% pay rise. In addition, with the nationwide minimum wage legalisation voted through on Friday, the lowest paid in this group will get a +12.6% rise from October.

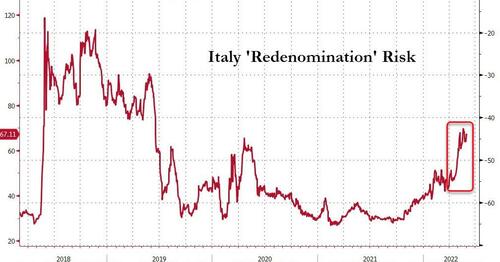

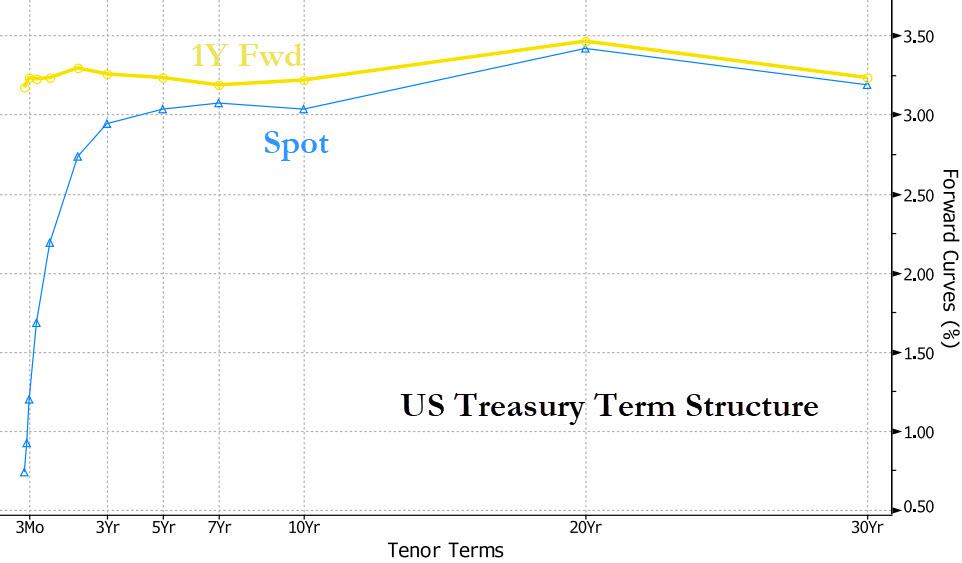

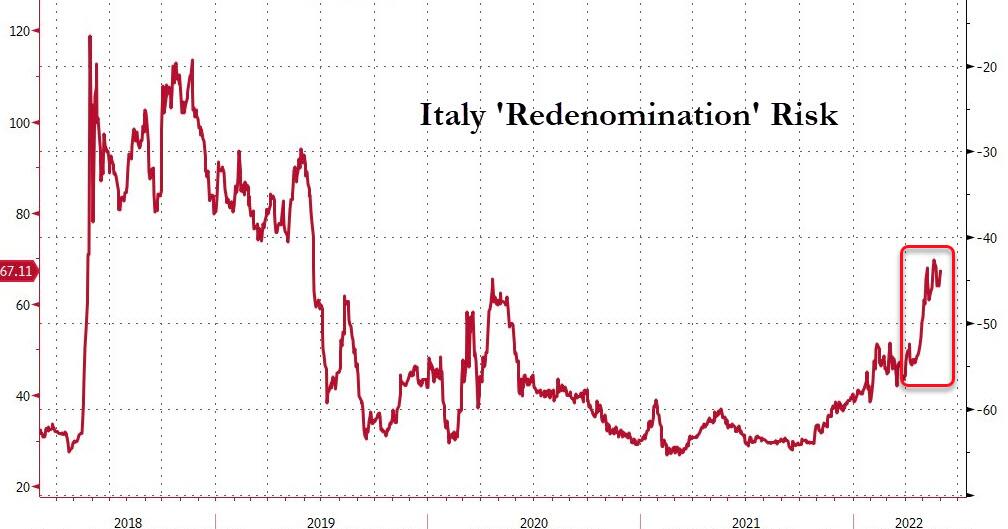

At the other end of the spectrum 10yr Italian BTPs hit 3.40% on Friday, up from 1.12% at the start of the year and as low as 2.85% intra-day the preceding Friday. We’re confident that the ECB will create tools to deal with Italy’s funding issues, but it is more likely to be reactive than proactive to ensure legal barriers to intervene are not crossed. However, the nightmare scenario we’ve all been hypothetically thinking about for years, if not decades, is here. Runaway German inflation at the same time as soaring Italian yields. The good news is that this should bring a lot more targeted intervention and a better-balanced policy response than in the last decade where negative rates and blanket QE was a one size fits all policy. High inflation will force the ECB to hike rates while managing the fall out on a more bespoke basis. It won’t be easy, but it will likely be better balanced.

Following on from the ECB, the next day brings the US CPI data. Month-over-month CPI is expected to accelerate to 0.7% from last month’s 0.3% reading. The core measure stripping out food and energy is expected to print at 0.5%. Those figures would translate to 8.3% and 5.9% for the year-over-year measures, respectively (from 8.3% and 6.2% last month). The Fed policy path for the next two meetings appears to be locked in to 50 basis point hikes, but Fed officials have highlighted the importance of inflation readings to determine the path of policy thereafter. There is a growing consensus that month-over-month inflation readings will have to decelerate in order to slow hikes to 25 basis points come September. Some Fed officials are still considering ramping the pace up to 75 basis points if inflation doesn’t improve. None appear to be considering zero policy action in September. Elsewhere, data will highlight production figures and the impact of the nascent tightening of financial conditions, with PMI, PPI, and industrial production figures due from a number of jurisdictions.

Asian equity markets have overcame initial weakness this morning and are moving higher as I type. Across the region, the Hang Seng (+1.14%) is leading gains due to a rally in Chinese listed tech stocks. Additionally, the Shanghai Composite (+1.01%) and CSI (+1.06%) are also trading up after markets resumed trading following a holiday on Friday. The easing of Covid-19 restrictions in Beijing is helping to offset a miss in China’s Caixin Services PMI for May. It came in at 41.4 (vs. 46.0 expected), up from 36.2 last month. Elsewhere, the Nikkei (+0.30%) is also up while markets in South Korea are closed for a holiday.

Outside of Asia, US stock futures have been steadily climbing in the last couple of hours before finishing this with contracts on the S&P 500 (+0.55%) and NASDAQ 100 (+0.65%) both in the green. US Treasuries are ever so slightly higher in yield.

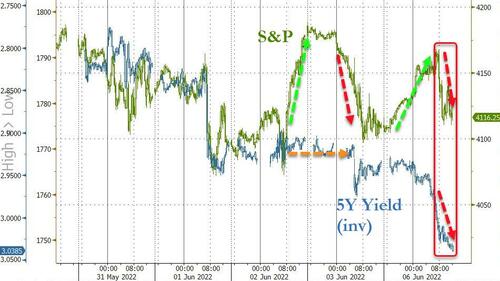

Recapping last week now and a renewed sense that global central banks would have to tighten policy more than was priced in given historic inflation drove yields higher and equity markets lower over the past week. This reversed a few weeks where market hike pricing had reversed.

This move was driven by a series of inflationary data but also came right from the source, as Fed and ECB speakers sounded a hawkish tone ahead of their respective meetings in June. Elsewhere, OPEC+ met and agreed to expand daily production, which was followed by reports that President Biden would visit the Crown Prince in Saudi Arabia.

Peeling back the covers. A series of ECB speakers openly considered the merits of +50bp hikes in light of growing inflation prints, as core Euro Area CPI rose to a record high, while German inflation hit figures not seen since the 1950s. In turn, 2yr bund yields climbed +30.9bps (+3.0bps Friday), and the week ended with +122bps of tightening priced in through 2022, the highest to date and implies some hikes of at least +50bps. A reminder that our Europe economists updated their ECB call to at least one +50bp hike in either July or September; full preview of that call and next week’s ECB meeting here.

Yields farther out the curve increased as well, including 10yr bunds (+31.0bps, +3.6bps Friday), OATs (+32.3bps, +4.2bps Friday), and gilts (+23.8bps, +5.4bps Friday) on their holiday-shortened week. Italian BTP 10yr spreads ended the week at their widest spread since the onset of Covid at 212bps. The tighter expected policy weighed on risk sentiment, sending the STOXX 600 -0.87% lower over the week (-0.26% Friday).

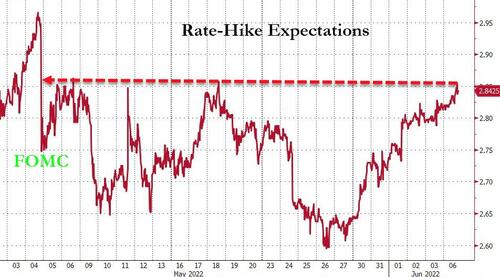

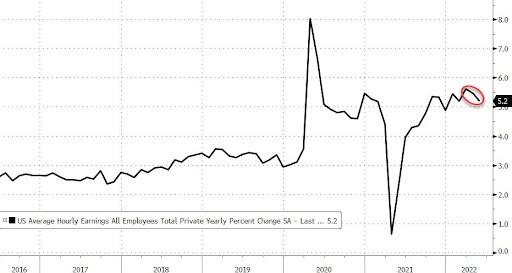

It was a similar story in the US, where a march of Fed officials, led by Vice Chair Brainard herself, again signed on for +50bp hikes at the next two meetings, and crucially, ruling out anything less than a +25bp hike in September. It appeared there was growing consensus on the Committee to size the September hike between +25bp and +50bps based on how month-over-month inflation evolves between now and then, with clear evidence of deceleration needed to slow the pace of hikes. The May CPI data will come this Friday but last week had a series of labour market prints that showed the employment picture remained white hot, capped on Friday with nonfarm payrolls increasing +390k and above expectations of +318k. Meanwhile, average hourly earnings maintained its +0.3% month-over-month pace.

Treasury yields thus sold off over the week, with 2yr yields gaining +17.9bps (+2.5bps Friday) and 10yr yields up +20.1bps (+3.1bps Friday). The implied fed funds rate by the end of 2022 ended the week at 2.82%, its highest in two weeks, while the probability of a +50bp September hike ended the week at 66.3%, its highest in a month. The S&P 500 tumbled -1.20% (-1.63% Friday), meaning its run of weekly gains will end at a streak of one. Tech and mega-cap stocks fared better, with the NASDAQ losing -0.98% (-2.47% Friday) and the FANG+ fell -0.30% (-3.76% Friday).

Elsewhere OPEC+ agreed to increase their production to +648k bls/day, after a steady flow of reports leaked that the cartel was considering such a move. Nevertheless, futures prices increased around +1.5% (+3.10% Friday) over the week, as it was not clear whether every member had the spare capacity to increase production to the new putative target, while easing Covid restrictions in China helped increase perceived demand. The OPEC+ announcement was closely followed by reports that President Biden would visit the Crown Prince in Saudi Arabia.

end

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED UP 40.91 PTS OR 1.28% //Hang Sang CLOSED UP 571.79 PTS OR 2.71% /The Nikkei closed UP 154.32 OR 0.56% //Australia’s all ordinaires CLOSED DOWN .54%% /Chinese yuan (ONSHORE) closed UP 6,6401 /Oil UP TO 119.30dollars per barrel for WTI and UP TO 120.08 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6401 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6389: /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER/

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA/

3B JAPAN

end

3c CHINA

4/EUROPEAN AFFAIRS//UK AFFAIRS/

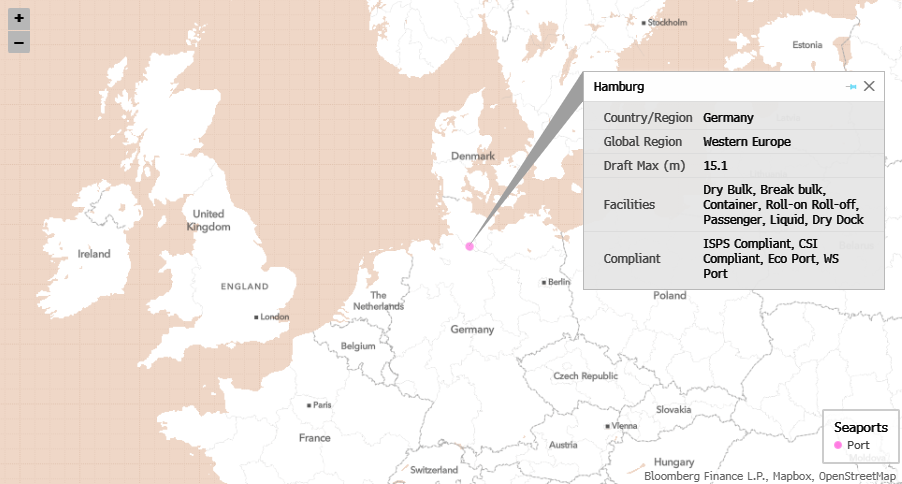

this could be very dangerous for Germany: a potential dockworker strike

(zerohedge)

Potential Dockworker Strike Could Unleash “Super Meltdown” At German Port Of Hamburg

SATURDAY, JUN 04, 2022 – 07:35 AM

Dozens of container ships are piling up outside Germany’s largest seaport by volume, known as the Port of Hamburg. It’s the third busiest port in Europe and the 15th largest globally and could be plunged into chaos next week as dockworkers may strike.

German newspaper Die Welt reports congestion at Hamburg is worsening, and container ships have to wait two weeks before entering the port.

“The waiting times are unsatisfactory,” a spokesman for shipping company Hapag-Lloyd said, referring to Hamburg.

Hamburger Hafen und Logistik AG (HHLA), a top European port and transport logistics company, said the reason for increasing congestion is a slowdown in the processing of containers, especially imports from the Far East not being transported fast enough by truck and train.

Besides congestion, Kiel Institute for Economic Research estimates that around 2% of the global container load is stuck at the port. There are also mounting concerns dockworkers could be ready to strike.

“There could be additional problems from next Tuesday. Many reckon that dockers could then go on strike in order to increase the pressure on the ongoing wage negotiations. The next round of negotiations is scheduled for June 10, but the peace obligation has already expired,” Die Welt said.

According to the Verdi services union, the strike could begin next Tuesday. The last time strikes hit Hamburg was in the late 1970s, a period when the world suffered from disastrous stagflation, similar to the economic climate today.

A shipowner told the German newspaper Hamburger Abendblatt: “If it comes to that, we’ll have a super meltdown in Hamburg.”

The timing of the proposed strike by dockworkers comes as consumer prices in Europe’s largest economy surged 8.7% YoY last month (the highest since the start of the monthly statistics in 1963).

The squeeze for households is far from over as consumers pay record prices for fuel and food and power bills. Inflation is only getting worse for households as the country could be on the verge of a recession.

end

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS/

Russia limits the export of noble gases like Neon

(zerohedge)

Russia Hits Hobbled Chip Market, Limiting Export Of Noble Gases

FRIDAY, JUN 03, 2022 – 08:00 PM