JUNE 9 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1850.45 DOWN $3.50

SILVER: $21.80 DOWN $.27

ACCESS MARKET: GOLD $1848.00

SILVER: $21.68

Bitcoin morning price: $30,370 UP 249

Bitcoin: afternoon price: $30,109 UP 12

GOLD; $1847.60

Platinum price: closing DOWN $32.40 to $978.90

Palladium price; closing DOWN $19.25 at $1932.65

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE:EXCHANGE:

COMEX

no. of contracts issued by JPMorgan: 1353/1845

CONTRACT: JUNE 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,851.900000000 USD

INTENT DATE: 06/08/2022 DELIVERY DATE: 06/10/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 333

104 C MIZUHO 600

118 C MACQUARIE FUT 25

118 H MACQUARIE FUT 112

323 C HSBC 50

323 H HSBC 173

332 H STANDARD CHARTE 22

363 H WELLS FARGO SEC 36

435 H SCOTIA CAPITAL 21

624 H BOFA SECURITIES 63

657 C MORGAN STANLEY 2

661 C JP MORGAN 600 1353

686 C STONEX FINANCIA 9

690 C ABN AMRO 8

700 C UBS 32

709 C BARCLAYS 192

709 H BARCLAYS 21

732 C RBC CAP MARKETS 15

800 C MAREX SPEC 4 11

905 C ADM 2 6

TOTAL: 1,845 1,845

MONTH TO DATE: 21,825

no. of contracts issued by JPMorgan:

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT 1845 NOTICE(S) FOR 184,500 Oz//5.738 TONNES)

total notices so far: 21,825 contracts for 218,500 oz (67.884 tonnes)

SILVER NOTICES:

23 NOTICE(S) FILED 115,000 OZ/

total number of notices filed so far this month 1588 : for 7,940,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $3.50

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD//

INVENTORY RESTS AT 1065.39 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 27 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV://A DEPOSIT OF 923,000 OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 545.229 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 1302 CONTRACTS TO 146,992 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE LOSS IN OI WAS ACCOMPLISHED DESPITE OUR SMALL $0.08 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.08) AND ALSO SUCCESSFUL IN KNOCKING OFF SOME SILVER LONGS AS THEY REMAIN FIRM IN THEIR BELIEF OF A SILVER FAILURE AS WE HAD A VERY STRONG GAIN OF 1283 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A ZERO ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 7.635 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 30 CONTRACTS OR 150,000 OZ//NEW STANDING: 8,260,000 / // V) STRONG SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -6

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTACTS for 7 days, total 5,511, contracts: 27.555 million oz OR 3.936 MILLION OZ PER DAY. (787 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 27.555 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 27.555 MILLION OZ

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1302 DESPITE OUR SMALL $0.08 LOSS IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A ZERO SIZED EFP ISSUANCE CONTRACTS: 0 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S 150,000 QUEUE JUMP //NEW STANDING:8,260,000 OZ // .. WE HAD A VERY STRONG SIZED LOSS OF 1296 OI CONTRACTS ON THE TWO EXCHANGES FOR 6.480 MILLION OZ WITH THE GAIN IN PRICE.

WE HAD 63 NOTICES FILED TODAY FOR 315,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 3492 CONTRACTS TO 497,622 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -XXX CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE GAIN IN COMEX OI CAME WITH OUR GAIN IN PRICE OF $4.75//COMEX GOLD TRADING/WEDNESDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //JUST SPECULATOR SHORT COVERING FROM OUR STUPID SPECULATORS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 69.26 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY’S HUGE 20,900 OZ QUEUE JUMP//NEW STANDING: 73.073 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $4.75 WITH RESPECT TO MONDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 5077 OI CONTRACTS 15.79 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1756 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 497,300

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5077, WITH 3492 CONTRACTS INCREASED AT THE COMEX AND 1756 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5077 CONTRACTS OR 15.79 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1756) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (3170,): TOTAL GAIN IN THE TWO EXCHANGES 5077 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE. AT 69.26 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 20,900 OZ//NEW STANDING: 73.073 TONNES / 3) ZERO LONG LIQUIDATION//CONSIDERABLE SPECULATOR SHORT COVERING //.,4) FAIR SIZED COMEX OI. GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

25,723 CONTRACTS OR 2,572,300 OZ OR 80.09 TONNES 7 TRADING DAY(S) AND THUS AVERAGING: 3675 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAY(S) IN TONNES: 68.59 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 80.09/3550 x 100% TONNES 2.25% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 80.09 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 1302 CONTRACT OI TO 146,992 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 0 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1302 CONTRACTS AND ADD TO THE 0 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF 1302 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 6.510 MILLION OZ

OCCURRED WITH OUR LOSS IN PRICE OF $0.08 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 24.84 PTS OR 0.76% //Hang Sang CLOSED DOWN 145.54 PTS OR 0.66% /The Nikkei closed UP 12.24 OR 0.04% //Australia’s all ordinaires CLOSED DOWN 1.45% /Chinese yuan (ONSHORE) closed UP 6.6764 /Oil UP TO 122.04dollars per barrel for WTI and UP TO 123.61 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6765 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6819: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER/

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 3,170 CONTRACTS TO 497,300 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED WITH OUR GAIN OF $4.75 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (1756 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ARE CAUGHT. THE COMMERCIALS WILL SLAUGHTER THESE GUYS WHEN THEY THINK THE TIME IS RIGHT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1756 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :1756 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1756 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 5077 CONTRACTS IN THAT 1756 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 3170 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR RISE IN PRICE OF GOLD $4.75.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (73.073),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 73.073 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE 4.75) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS/COMMERCIAL LONGS AS WELL AS SPECULATOR SHORTS//// WE HAVE REGISTERED A GOOD SIZED GAIN OF 16.323 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JUNE (73.073 TONNES)…

WE HAD 171 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 5077 CONTRACTS OR 507700 OZ OR 15.79 TONNES

Estimated gold volume 129,067/// poor

final gold volumes/yesterday 132,428 poor

INITIAL STANDINGS FOR JUNE ’22 COMEX GOLD //JUNE 9

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 80,981.068 oz Manfra Brinks JPMorgan 130 kilobars 2010 kilobars |

| Deposit to the Dealer Inventory in oz | 32,118.847OZ Brinks 999 kilobars |

| Deposits to the Customer Inventory, in oz | 32.151 oz Brinks one kilobar |

| No of oz served (contracts) today | 1845 notice(s)184,500 OZ5.738 TONNES |

| No of oz to be served (notices) | 1668 contracts 166,800 oz5.188 TONNES |

| Total monthly oz gold served (contracts) so far this month | 21,825 notices2,182,500 OZ67.884TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 1

Brinks: 32,118.847 oz 999 kilobars

No dealer withdrawals

1 customer deposits

i) Into Brinks 32.151 oz (1 kilobar)

total deposits: 32.151 oz

3 customer withdrawals:

i) Out of Brinks: 12,178,300

ii) Out of JPMorgan: 64,623.510 oz (2010 kilobars)

iii) Out of Manfra: 4179.258 oz (130 kilobars)

total withdrawal: 80,981.068 oz

ADJUSTMENTS: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 3513 contracts having LOST 771 contracts

We had 980 notices filed on WEDNESDAY so we GAINED A HUGE 209 contracts

July has a GAIN OF 89 OI to stand at 2302

August has a LOSS of 1335 contracts DOWN to 419,699 contracts

We had 980 notice(s) filed today for 98,000 oz FOR THE JUNE 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 600 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1845 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1363 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2021. contract month,

we take the total number of notices filed so far for the month (21,825) x 100 oz , to which we add the difference between the open interest for the front month of (JUNE 3513 CONTRACTS ) minus the number of notices served upon today 1845 x 100 oz per contract equals 2,349,300 OZ OR 73.073 TONNES the number of TONNES standing in this active month of JUNE.

thus the INITIAL standings for gold for the JUNE contract month:

No of notices filed so far (21,825) x 100 oz+ (3513) OI for the front month minus the number of notices served upon today (1845} x 100 oz} which equals 2,328,000 oz standing OR 73.073 TONNES in this active delivery month of JUNE.

TOTAL COMEX GOLD STANDING: 73.073 TONNES (A STRONG STANDING FOR A JUNE ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,331,163.529 oz 72.5 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 34,717,379.200 OZ

TOTAL ELIGIBLE GOLD: 16,753,348.887 OZ

TOTAL OF ALL REGISTERED GOLD: 17,964,030.333 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,632,867.0 OZ (REG GOLD- PLEDGED GOLD)

END

JUNE 2022 CONTRACT MONTH//SILVER//JUNE 9

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,258,913.021 oz Brinks CNT JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,733,315,931oz CNT Delaware HSBC JPMorgan |

| No of oz served today (contracts) | 23CONTRACT(S)115,000 OZ) |

| No of oz to be served (notices) | 64 contracts (320,000 oz) |

| Total monthly oz silver served (contracts) | 1588 contracts 7940,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) zero dealer deposits And now for the wild silver comex results

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 4 deposits into the customer account

i) Into CNT: 547,904.371 oz

ii) Into JPMorgan: 577,221.700

iii) Into Delaware: 20,514.360 oz

iv) Into HSBC: 587,625.500 oz

total deposit: 1,733,315.931 oz

JPMorgan has a total silver weight: 170.926 million oz/337.188 million =50.74% of comex

Comex withdrawals: 3

i) Out of Brinks 30,273.900 oz

ii) Out of JPMorgan: 1,138,692,800 oz

iii) Out of CNT 47,942.621 oz

total withdrawal 1,258,913.021 oz

0 adjustments:

the silver comex is in stress!

TOTAL REGISTERED SILVER: 72.742 MILLION OZ

TOTAL REG + ELIG. 337.188 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE OI: 87 HAVING LOST 33 CONTRACTS.

WE HAD 63 NOTICES FILED ON TUESDAY SO WE GAINED 30 CONTRACTS OR AN ADDITIONAL 150,000 OZ WILL STAND IN THIS NON ACTIVE

DELIVERY MONTH OF JUNE

JULY HAD A LOSS OF 7666 CONTRACTS DOWN TO 85,781 CONTRACTS.

AUGUST GAINED 77 CONTRACTS TO STAND AT 974

SEPTEMBER HAD A GAIN OF 5877 CONTRACTS UP TO 45,374 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 23 for 115,000 oz

Comex volumes:58,840// est. volume today// poor

Comex volume: confirmed yesterday: 72,441 contracts ( fair )

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1588 x 5,000 oz = 7,940,000 oz

to which we add the difference between the open interest for the front month of JUNE(87) and the number of notices served upon today 23 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE./2022 contract month: 1588 (notices served so far) x 5000 oz + OI for front month of JUNE (87) – number of notices served upon today (23) x 5000 oz of silver standing for the JUNE contract month equates 8,260,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

MAY 18/WITH GOLD DOWN $2.55//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.07 TONNES FROM THE GLD///INVENTORY RESTS AT 1049.21 TONNES

MAY 17/WITH GOLD UP $5.40:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1053.28 TONNES

MAY 16/WITH GOLD UP $5.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD///INVENTORY RESTS AT 1055.89 TONNES

MAY 13/ WITH GOLD DOWN $16.25//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.8 TONNES FROM THE GLD.//INVENTORY RESTS AT 1060.82 TONNES

MAY 12/WITH GOLD DOWN $26.50: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD////INVENTORY RESTS AT 1066.62 TONNES

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

GLD INVENTORY: 1065.39 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

MAY 18/WITH SILVER UP $0.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL 1.892 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 17/WITH SILVER UP $.22 TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.508 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 16/WITH SILVER UP $.52 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.546 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.593 MILLION OZ//

MAY 13/WITH SILVER UP 31 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ/

MAY 12/WITH SILVER DOWN 88 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ//

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

INVENTORY TONIGHT RESTS AT 545.229 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards

END

3. Chris Powell of GATA provides to us very important physical commentaries

For your interest….

Newmont sells 3,500 ounces of gold to Ghana’s central bank under local purchasing plan

Submitted by admin on Wed, 2022-06-08 11:26Section: Daily Dispatches

By Cooper Inveen and Sofia Christensen

Reuters

via Yahoo News, Sunnyvale, California

Tuesday, June 7, 2022

https://finance.yahoo.com/news/1-newmont-sells-3-500-181601073.html

ACCRA, Ghana — Newmont Mining’s Africa unit has sold 3,500 ounces of gold to the Bank of Ghana under a central bank domestic gold purchasing program launched in June 2021, the company said today.

The gold purchasing program aims to increase gold reserves and has spurred discussions with the Chamber or Mines about the Bank of Ghana’s intentions to purchase refined gold from mining companies in the country.

Newmont Africa said it was the first mining company to respond to the central bank’s initiative with a first sale of refined gold in May 2022.

Ghana’s central bank is seeking to raise the gold component of its reserves in a bid to strengthen the West African country’s local cedi currency without increasing inflation.

end

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //FERTILIZER OTHERS

END

END

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.6765

OFFSHORE YUAN: 6.6819

HANG SANG CLOSED DOWN 145.54 PTS OR 0.66%

2. Nikkei closed UP 12.24% OR 0.04%

3. Europe stocks ALL CLOSED ALL RED

USA dollar INDEX DOWN TO 102.32/Euro RISES TO 1.0734

3b Japan 10 YR bond yield: RISES TO. +.243/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 133.84/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN -SHORE CLOSED UP// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +1.441%/Italian 10 Yr bond yield RISES to 3.62% /SPAIN 10 YR BOND YIELD FALLS TO 2.59%…ALL BLOWING UP!!

3i Greek 10 year bond yield RISES TO 3.95

3j Gold at $1850.05 silver at: 21.96 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1.30 roubles/dollar; ROUBLE AT 58.11

3m oil into the 122 dollar handle for WTI and 123 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 133.84DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9771– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0486well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.033 UP 2 BASIS PTS

USA 30 YR BOND YIELD: 3.171 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.23

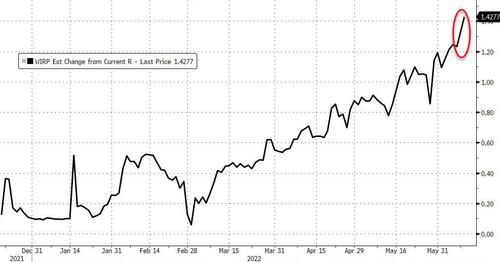

Futures Rise Ahead Of Hawkish ECB Meeting

THURSDAY, JUN 09, 2022 – 07:45 AM

US index futures turned positive on Thursday, even as European stock slipped ahead of the ECB decision at 745am ET, with Nasdaq 100 contracts outperforming as oil prices and bond yields stabilized and strategists at Goldman and JPMorgan gave more bullish comments on equities. Sentiment was boosted after Bloomberg reported that China’s crackdown on internet companies may be easing with a revival of the Ant Group IPO, which boosted the country’s US-traded stocks (the news was since refuted by China, but moments later Reuters re-reported what Bloomberg said). S&P 500 futures traded 22 points or 0.5% higher, and Nasdaq 100 futs were 0.4% higher. The dollar slid, and 10Y rates were flat at 3.02%.

Markets remain fixated on the risk that central banks intent on cooling inflation snuff out economic recoveries in the process. Money markets have priced in 36.5 basis points of tightening to the ECB’s rate by next month’s meeting, just short of a 50% chance of a half-a-percentage point increase, which would be the first since 2000.

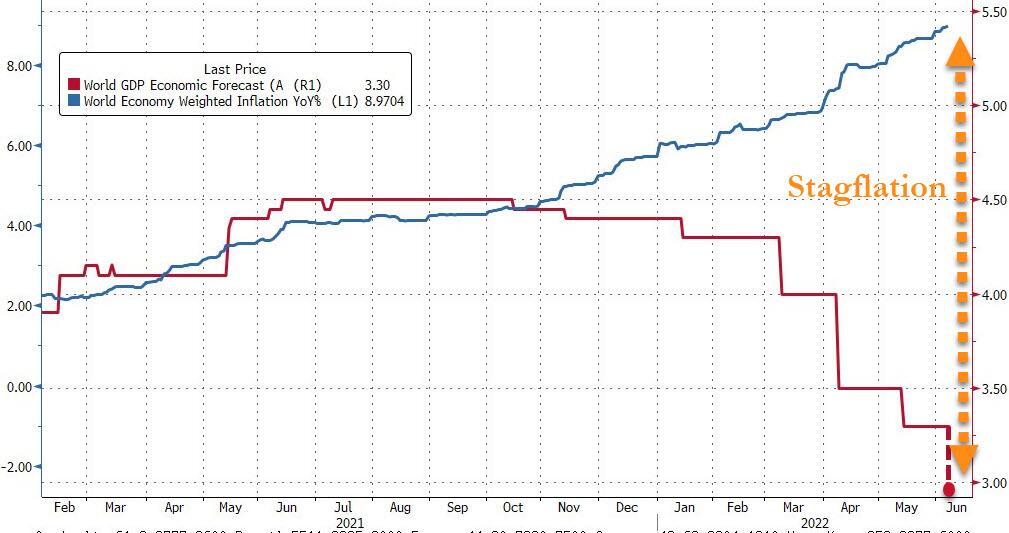

“To rein in surging prices the Fed has to increase rates, which can result in a recession,” Geir Lode, head of global equities at Federated Hermes, wrote in a note. “However, the pandemic-induced supply-chain shock and the Ukraine conflict are beyond the central bank’s control. In this environment we need to be lucky to avoid stagflation that could last for a long time.”

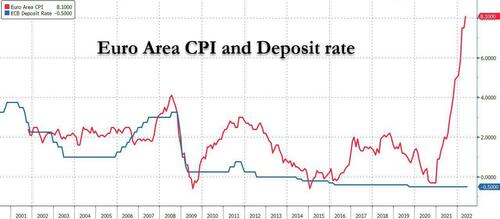

While the ECB isn’t expected to raise official borrowing costs, President Christine Lagarde signaled in a blog post last month that the central bank will end bond purchases this month, and hike once in July and again in September, lifting the deposit rate from minus 0.5% to zero. Some investors see a new tone reaching beyond the official line as central bankers succumb to huge pressure to rein in record inflation at more than four times their target of 2%. Peers at the Federal Reserve, Bank of Canada and Reserve Bank of Australia have hiked in 50-basis point increments this year.

“Chances are that the ECB will have a hawkish pivot today,” Carol Kong, a strategist at Commonwealth Bank of Australia, said on Bloomberg Television.

In US premarket trading, Alibaba Group was among the best performers – at least initially – as it pumped, dumped and then rose again after several conflicting reports that Chinese regulators are considering a potential revival of the initial public offering by Jack Ma’s Ant Group.

Tesla gained 3% after an upgrade to Buy from UBS and after the company said its deliveries of cars made in China doubled in May compared with April and as UBS recommended buying the stock. Bank stocks also traded higher in premarket trading as the US 10-year Treasury yield hovered just above 3%. In corporate news, Credit Suisse shares dropped after its CEO Thomas Gottstein said he wouldn’t comment on State Street’s reported interest in the Swiss bank. Here are all the notable premarket movers:

- Five Below (FIVE US) shares decline 7.3% in premarket trading after the company cut its full-year guidance, while analysts trimmed their targets for the stock, but were broadly positive on the firm’s longterm prospects.

- Spotify (SPOT US) shares could be in focus today as analysts were positive on the streaming giant’s forecast that its podcasting business will turn profitable as the company focuses on more non-music segments like audiobooks.

- Travel stocks could be active on Thursday following Expedia CEO Peter Kern’s bullish comments on summer travel. Keep an eye on Delta (DAL US), United (UAL US), Marriott (MAR US), Expedia (EXPE US), Airbnb (ABNB US) and Booking Holdings (BKNG US) among others

- Watch Oxford Industries (OXM US) shares after the company reported results, as Citi says that there is no sign of consumer weakness in any part of the branded apparel retailer’s business.

- Ollie’s Bargain (OLLI US) stock may be in focus as RBC Capital Markets upgraded the discount retailer to outperform, saying that despite another tough quarter, its fundamentals should improve in the back-half and beyond.

In Europe, equities slipped ahead of a European Central Bank decision that will put the region’s monetary policy on a path of tightening and help close the gap with global peers. Real-estate companies and retailers led the Stoxx Europe 600 Index 0.5% lower. EDF jumped the most in three months, after a newspaper report that the new French government is studying two options for the electricity giant’s nationalization, including a buyout offer. Here are the most notable European movers:

- EDF shares rise as much as 8.3% after Les Echos newspaper reported that nationalization is among priorities for new government after this month’s legislative elections alongside combating inflation and pension reform.

- Prosus gains as much as 7.4% in Amsterdam and Naspers gains as much as 6.8% in Johannesburg following a report that Chinese financial regulators are considering reviving the IPO of Jack Ma’s Ant Group.

- Tate & Lyle advances as much as 4.4% after the company reported FY22 results that beat estimates. The FY23 outlook suggests upgrades to consensus estimates, according to Jefferies.

- Beiersdorf rises as much as 7.8% after the company said in a Capital Markets Day presentation on its website that it targets above-market organic sales growth at its consumer unit in the medium term.

- Credit Suisse drops as much as 4.9% after State Street declined to comment on a report that it was looking to acquire the Swiss bank. Separately, Bloomberg reported that Credit Suisse is tapping the brakes on its China expansion.

- CMC Markets falls as much as 19% after cutting its dividend and saying it was boosting spending on new hires, product development and marketing as the firm seeks to diversify amid a fading retail trading boom.

- Wizz Air drops as much as 8.3%, extending Wednesday’s 9.5% decline after the company gave guidance for an operating loss for the first quarter, while analysts also noted their concern about pricing trends.

Asian stocks slipped as technology and financial firms declined and higher oil prices stoked concerns about inflation. The MSCI Asia Pacific Index fell 0.3%, trimming its gain this week. Chip stocks declined after a warning on demand from Intel Corp., with the Hang Seng Tech Index sliding more than 1%, a breather after its recent rally. Australian banks were among the biggest contributors to the regional benchmark’s loss. “We are seeing profit-taking moves after Chinese stocks rose a lot in recent sessions,” said Xue Hua Cui, a China equity analyst at Meritz Securities in Seoul. “There are also renewed concerns about the second-quarter corporate earnings.” Australia’s broad benchmark was among the biggest decliners in Asia Pacific as bank stocks slumped on concerns about valuations and macroeconomic risks. Shares in Singapore and Malaysia also fell. South Korean equities erased early-day losses to close nearly flat on options expiry, while Japanese peers also finished little changed amid the yen’s extended weakness. Read: Australian Bank Stocks Take $32 Billion Hit on Rate Concerns Stocks in much of the region held losses after data showed Chinese exports jumped more than expected in May, while a mini-lockdown weighed on market sentiment. Even with Thursday’s dip, the MSCI Asia Pacific Index remained on track for its fourth straight weekly gain, which would be its longest winning streak since early 2021

Japanese stocks traded in a narrow range as investors continued to worry about inflation and growth while the yen extended losses to a fresh 20-year low. The Topix Index was virtually unchanged at 1,969.05 as of the market close in Tokyo, while the Nikkei 225 was stable at 28,246.53. Out of 2,170 shares in the index, 937 rose and 1,105 fell, while 128 were unchanged.

In Australia, the S&P/ASX 200 index fell 1.4% to close at 7,019.70, its lowest level since May 12. Banks contributed the most to the benchmark’s slump on growing concerns that faster monetary policy tightening might increase housing-market risks and pressure valuations. Magellan was the top performer after saying co-founder Hamish Douglass will resume working with the business in a new consultancy role. In New Zealand, the S&P/NZX 50 index fell 0.5% to 11,211.31.

In India, stock gauges advanced for the first session in five, helped by a surge in Reliance Industries and energy companies on the improving outlook for refining margin and software exporters extending recovery. The S&P BSE Sensex rose 0.8% to 55,320.28 in Mumbai, while the NSE Nifty 50 Index gained 0.7%. Both indexes are still headed for weekly drops of about 0.8% and 0.6%, respectively, their first decline in four weeks. “With policy rate announcements now behind us, investors lapped up stocks that were in a downward spiral for quite some time,” Kotak Securities analyst Shrikant Chouhan said in a note. The market may witness select bouts, but volatility is expected to remain over the near-to-medium term, he added. Reliance Industries provided the biggest boost to the key gauges, increasing 2.7%. Out of 30 shares in the Sensex index, 21 rose and 9 fell

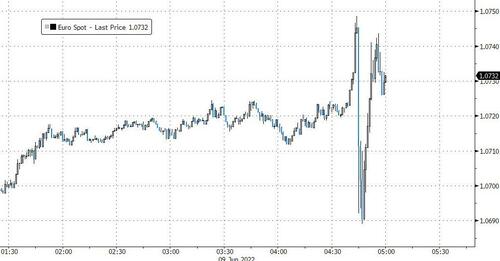

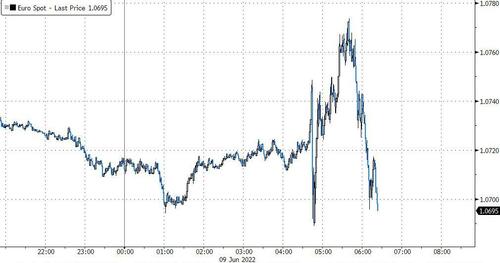

In FX, the Bloomberg Dollar Spot Index was little changed as the greenback traded mixed against its Group-of-10 peers. The euro fluctuated around $1.07. Bunds and Italian bonds swung between modest gains and losses. Options pricing in the euro and spot swings suggest not everyone is convinced that the euro will rally after the ECB meeting, which leaves ample room for an advance on a hawkish decision. The yen rebounded after touching a fresh two-decade low against the dollar and seven-year lows against the Australian dollar and the euro, as traders adjusted positions before the ECB. Speculators are gathering around the beleaguered yen and positioning is by no means extended, suggesting there’s still room for bears to pile in. The New Zealand dollar inched up and the nation’s 10-year yield hit a seven-year high after the RBNZ announced plans to offload QE bond holdings.

One beneficiary of a hawkish pivot by the ECB would be the euro. The common currency has been bogged down by concerns over euro-area growth while a resurgent dollar and hawkish Fed pushed it to a five-year low against the US currency last month. The euro traded little changed against the dollar at $1.07.

“If we do see Christine Lagarde leaning toward a 50 basis-points hike in July, that’s going to be very supportive of the euro-dollar,” Kong said.

In rates, Treasuries are narrowly mixed with the yield flatter ahead of ECB rate decision at 7:45am ET and 30-year bond reopening, the last of this week’s coupon auctions. 2-year TSY yields rose to 2.80%, highest level since May 4 YTD high. 10-year little changed at 3.02%, underperforming bunds while gilts trail. US front-end cheapening flattens 2s10s by ~1bp on the day toward lowest level since May 25; as previewed before, the ECB is expected to announce imminent end to large-scale asset purchases, opening the door for interest-rate hikes at the July meeting; swaps price in around 30bp of rate- hike premium. Looking at today’s auction we have a $19BN 30-year bond reopening which follows Wednesday’s mediocre 10-year, which tailed by 1.2bp. WI 30-year yield at ~3.16% is above auction stops since 2018 and ~16bp cheaper than May’s, which stopped 0.9bp through.

German bonds and the euro are steady ahead of the ECB’s meeting later Thursday, where traders will look for clues on whether the bank will raise rates by 25bps or 50bps in July. Money markets don’t expect a hike today, and currently bet on 36bps next month, and about 132bps by the end of the year. Peripheral spreads tighten to Germany. Both gilt and Treasury curves flatten.

In commodities, WTI trades within Wednesday’s range around the $122 level. Most base metals trade in the red; LME nickel falls 2.9%, underperforming peers. Spot gold falls roughly $3 to trade near $1,850/oz

To the day ahead now, and the main highlight will be the aforementioned ECB decision and President Lagarde’s subsequent press conference. We’ll also hear from Bank of Canada Governor Macklem, and data releases today include the US weekly initial jobless claims.

Market Snapshot

- S&P 500 futures up 0.4% to 4,130.75

- STOXX Europe 600 down 0.7% to 437.16

- MXAP down 0.4% to 168.75

- MXAPJ down 0.6% to 557.70

- Nikkei little changed at 28,246.53

- Topix little changed at 1,969.05

- Hang Seng Index down 0.7% to 21,869.05

- Shanghai Composite down 0.8% to 3,238.95

- Sensex up 0.2% to 54,988.33

- Australia S&P/ASX 200 down 1.4% to 7,019.75

- Kospi little changed at 2,625.44

- Brent Futures down 0.4% to $123.07/bbl

- Gold spot down 0.3% to $1,848.12

- U.S. Dollar Index little changed at 102.62

- German 10Y yield little changed at 1.35%

- Euro down 0.1% to $1.0701

Top overnight News from Bloomberg

- The ECB is set to announce an imminent end to large-scale asset purchases, paving the way for the first increase in interest rates in more than a decade next month

- Traders are betting the BOE will deliver a historic half-point interest-rate hike by September to wrest control of inflation running at the fastest pace in four decades

- Judging by the latest comments, the yen’s exchange rate still has some way to go before Japan’s finance ministry would consider intervention to prop up the currency via actual purchase operations, something it has avoided for more than two decades. With the US more likely to be against any moves to weaken the dollar, Japan faces the problem that actual intervention may not be effective

- Japan’s Prime Minister Fumio Kishida appears to be counting on the Bank of Japan to keep borrowing costs near rock-bottom levels as his government paves the way for continued spending even after a record-breaking pandemic splurge and with the yen languishing at two-decade lows

- Riksbank Deputy Governor Anna Breman said all options are on the table for the June policy meeting as speculation grows over whether the Swedish central bank needs to speed up its interest rate increases

- China’s exports rebounded in May as Covid-related bottlenecks on production and logistics clear up, but a slowdown looms this year as global consumer demand for goods cools, weakening trade’s ability to act as a driver for economic growth

A more detailed look at global markets courtesy of newsquawk

Asia-Pac stocks were subdued following a weak handover from the US and with sentiment cautious. ASX 200 was pressured by underperformance in the top-weighted financials sector and weakness in property-related stocks also suffering amid expectations of aggressive RBA rate hikes which increases banks’ funding costs and could threaten the quality of their loan portfolios. Nikkei 225 kept afloat as participants contemplated the ramifications of further currency depreciation. Hang Seng and Shanghai Comp. were lacklustre despite the mostly better than expected Chinese trade data as some COVID concerns resurfaced in Shanghai with the city locking down the Minhang district on Saturday morning for mass COVID testing.

Asia headlines

- Shanghai will lockdown the Minhang district on Saturday morning for mass COVID-19 testing, according to Bloomberg; additionally, Beijing’s Chaoyang district is to close all entertainment venues from 14:00 local time (07:00BST) for COVID containment.

- US Treasury Secretary Yellen said China is guilty of unfair trade practices but some tariffs on Chinese goods do not serve US strategic interests and the Biden administration is looking to reconfigure tariffs in a way that would be more strategic, according to Bloomberg.

- Japan is planning to expand its prefectural travel subsidies across the entire country, according to Yomiuri.

- RBNZ outlined plans to sell New Zealand government bonds from July 2022 in which it intends to offload NZD 5bln per fiscal year in order of maturity date until its LSAP holdings are reduced to zero, according to Reuters.

Equities are, overall, struggling for clear direction in relatively cautious trade going into ECB; Euro Stoxx 50 -0.5%. Bourses, and US futures, were lifted amid further constructive China tech developments, this time for Ant Group; albeit, we have drifted modestly off best since, ES +0.3%. China is said to be mulling reviving Jack Ma’s Ant IPO, with reports framing it as an easing in crackdowns from China, according to Bloomberg sources. *Click here for analysis/reaction. China PCA Retail Passenger Vehicle Sales (May): -17.3% YY; Tesla (TSLA) 32.2k (prev. 33.5k YY). Walgreens Boots Alliance’s (WBA) Boots has received a non-binding bid from Apollo Global Management and Reliance Industries, according to FT sources.

European headlines

- Hawkish Lagarde Is Not Fully Priced In the Euro: ECB Cheat Sheet

- Traders Bet BOE Will Join Peers in Historic Half-Point Rate Hike

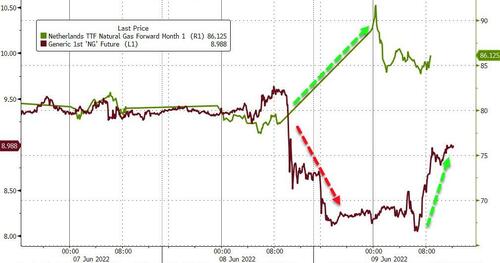

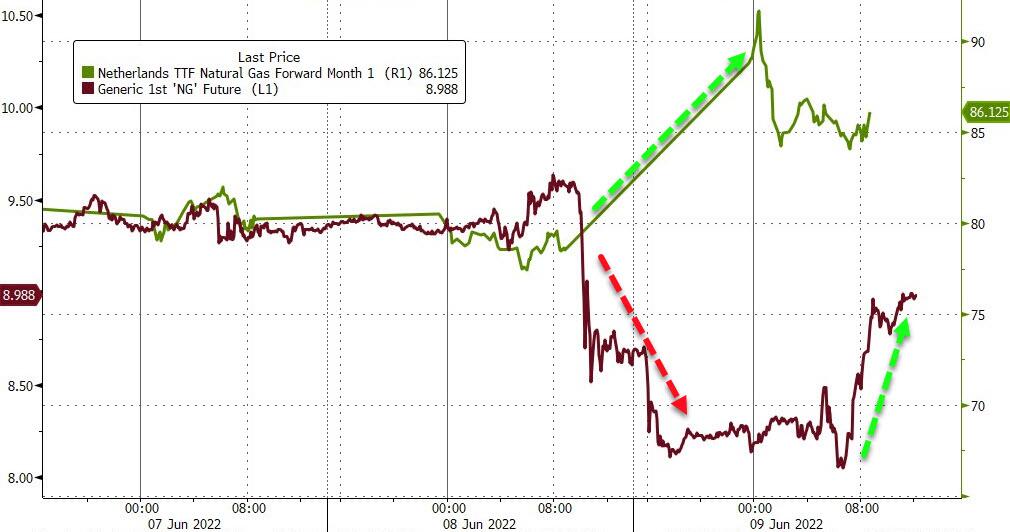

- European Gas Soars as Fire in US Compounds Russia Supply Concern

- Italy’s Eni to List Renewable Unit Plenitude in Milan

- FirstGroup Rejects £1.2 Billion Takeover Bid From I Squared

FX

- Yen finally finds some friends amidst less hostile yield environment and supportive risk backdrop; USD/JPY retreats just over 100 pips around 134.00 and EUR/JPY almost 150 pips from 144.00+ peak.

- DXY remains anchored around 102.500 ahead of Friday’s US CPI data and as Euro pivots 1.0700 pre-ECB; EUR/USD flanked by decent option expiries as well from 1.0750-55 to 1.0605-00 on the downside.

- Kiwi underpinned after RBNZ outlines schedule for balance sheet rundown; NZD/USD hovers near 0.6450, AUD/NZD sub-1.1150 with AUD/USD capped into 0.7200.

- Rand continues bull run with extra incentive from wider than forecast SA current account surplus, USD/ZAR straddling 15.2500.

- Lira rout resumes following fleeting respite on prospect of capital controls raised by S&P, USD/TRY above 17.2200.

- Yuan retains bulk of Chinese trade data related gains even though parts of Beijing and Shanghai reimpose restrictive Covid measures; USD/CNH closer to 6.6700 than 6.7100, USD/CNY settles sub-6.7000 vs circa 6.7000 high.

Fixed Income

- Bunds choppy and lagging Eurozone periphery within 149.17-148.52 range pre-ECB, as focus falls on fragmentation along with rate and QE guidance

- Gilts underperforming between 114.86-42 parameters as BoE tightening expectations rise and drag Sonia strip down

- US Treasuries flat-lining ahead of jobless claims and long bond supply, with 10 year T-note just above par inside tight 118-07/117-26+ band

Commodities

- WTI and Brent are steady after giving up overnight gains with participants cautious and cognizant of China’s fluid COVID situation.

- Currently, the benchmarks are sub-USD 122/bbl and USD 123.50/bbl respectively, vs highs of 122.72 and 124.34.

- Magnitude 5.6 earthquake hits the Antofagasta region in Chile, according to EMSC.

- Spot gold is sub-USD1850/oz, having slipped below its falling 10-DMA but holding above the overlapping 200- & 21-DMAs at USD 1842/oz.

Central Banks

- Riksbank’s Breman says she will support doing what is required to attain the inflation target, including more hikes than are currently in the path; adding, to control inflation back to target, need to act now. Does not exclude a 50bps hike at the next meeting.

- Hungarian Finance Minister says the Hungary has issued FX bonds totalling USD 3bln and EUR 750mln; follows the NBH maintaining its one-week deposit rate at 6.75%.

US Event Calendar

- 08:30: May Continuing Claims, est. 1.3m, prior 1.31m

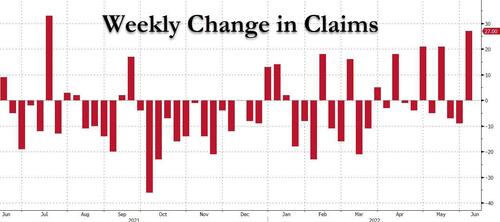

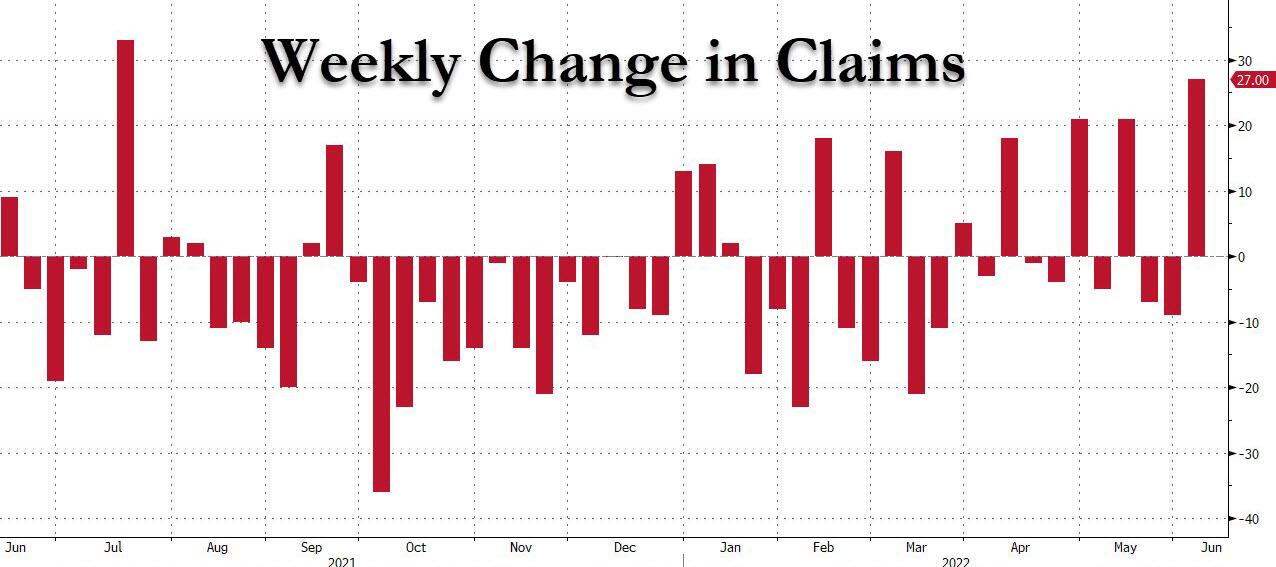

- 08:30: June Initial Jobless Claims, est. 206,000, prior 200,000

- 12:00: 1Q US Household Change in Net Wor, prior $5.3t

DB’s Jim Reid concludes the overnight wrap

I kicked off Day 1 of our annual European LevFin conference in London yesterday and we had a record attendance of over 1100 issuers and investors. It was the first in-person version since 2019 and if this conference is anything to go by, people still like the personal contacts that such an event brings. I also had a dinner at the event last night so I’m a bit shattered this morning so bear with me. This conference has been going now for 26 years at DB and the headline acts at the post conference entertainment have in the past included, The Killers, Duran Duran, Cheryl Crow, Dire Straits, The Corrs, The Sugababes, Stevie Wonder and Bon Jovi. Last night’s entertainment was a pub quiz. How times have changed.

If you think the above means Zoom is dead then think again, as I’ll be doing a Zoom webinar next Wednesday (June 15th) at 2pm on my annual Default Study (“The End of the ultra-low default world?”), published earlier this week, that I presented at the conference. Please click here to register, and here to see the report itself.

The day before this (June 14th), also at 2pm London time, a selection of our heads of trading and research desks will do a call on the near-term macro outlook across rates, FX, EM, equities and credit. Please click here to register.

As I recover from the heckling of telling High Yield investors that defaults are coming, we arrive at the business end of the week with a big 36 hours ahead with the ECB meeting today, and US CPI tomorrow, looming large! And then don’t forget the FOMC, BoE and BoJ meetings next week. Markets approach this busy period on the nervous side with rates and equities selling off over the last 24 hours, and that’s still the case in much of Asia in this morning’s trading.

Starting with Europe, sovereign bond yields hit fresh highs yesterday as investors have come to view a potential 50bp hike at some point this year as an increasingly likely possibility. In fact by the close of trade yesterday, overnight index swaps were pricing in 132bps worth of ECB hikes by the December meeting, which is the highest to date and more than double the 63bps of hikes expected after their last meeting in mid-April. So if they don’t hike until July as is widely expected, that implies at least one 50bp move is being fully priced in by year-end.

In their preview last week (link here), our European economists agreed with this assessment that a 50bp hike is likely soon, and their view is that one of the two hikes in Q3 will be a 50bp hike, with September being more likely than July. After that, they then see the ECB reverting to continuous back-to-back 25bp hikes until they reach a terminal deposit rate of 2% in mid-summer 2023, although there’s a risk of a second 50bp hike before policy rates reach neutral. In terms of today’s decision however, they expect the ECB to confirm that APP net purchases will cease at the end of June, and that their new staff forecasts will show inflation at 2.0% in 2024, thus satisfying the liftoff criteria. When it comes to new guidance, their view is that the three conditions for policy rate liftoff are likely to be replaced by new guidance on the speed and extent of the hiking cycle. And finally on TLTRO, they expect the end of the TLTRO discount to be confirmed and the ECB to pledge a smooth transmission of monetary tightening through the banking system.

With all that in mind, European yields moved higher through the day, with those on 10yr bunds (+6.2bps) and OATs (+7.0bps) both rising to their highest levels since 2014. The selloff was more pronounced among peripheral debt, with yields on 10yr Italian (+8.8bps) and Spanish (+8.2bps) debt seeing even larger rises, although the spread of both over bunds was still tighter than their recent peak last week. There are signs of growing nervousness elsewhere too, with EURUSD overnight implied volatility at its highest level right now since the US presidential election in November 2020. Meanwhile, those at the more hawkish end of the Governing Council received further support yesterday from data revisions, with Euro Area growth in Q1 revised up to show a +0.6% expansion (vs. +0.3% previously).

This investor concern about rate hikes and persistent inflation was bad news for equities, first in Europe where the STOXX 600 (-0.57%) fell for a second day running and then extending to a late sell-off across the Atlantic, where the S&P 500 fell -1.08%, with only energy (+0.15%) managing to end the day in the green. This brings the index to +0.18% for the week, as it enters yet another late week showdown to see if it can manage to stay in positive territory. The decline came as 10yr Treasuries eclipsed the 3% mark again, closing up +4.8bps at 3.02%, and we’re up another +1.5 bps higher this morning at 3.036%. The impact of tighter monetary policy extended beyond risk assets and showed some signs of being felt in the real economy, too, with the number of mortgage applications in the US falling to a 22-year low in the week ending June 3.

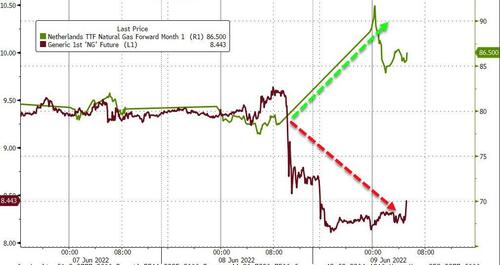

These inflationary worries for investors and central banks were aggravated further by a fresh rise in commodity prices. Oil prices saw further gains, and Brent Crude (+2.50%) moved back above $123/bbl again, inching ever closer to their post-invasion peak levels despite news of OPEC supply expansion and US reserve releases. That trend has continued this morning, with Brent crude up a further +0.33% at $123.98/bbl. WTI (+2.26%) moved above $122/bbl as well, so not far from its peak closing level following the invasion of $123.70/bbl. US natural gas prices displayed a lot of volatility, hitting a post-2008 high intraday before crashing into the close to finish down -6.39% following reports of a fire at a terminal used for exporting, keeping supplies stateside. European natural gas futures fell for a 6th consecutive session to hit another post-Ukraine invasion low of €78.41/MWh.

Those losses on Wall Street have carried over into Asia overnight as that rally in oil prices has ramped up worries about inflation and the outlook for interest rates. The Hang Seng (-0.24%), the Shanghai Composite (-0.49%) and the CSI 300 (-0.64%) are all in negative territory, as is the Kospi (-0.31%), although the Nikkei (+0.26%) is up as the weaker Yen has raised hopes for an earnings improvement. Indeed yesterday, the Yen fell a further -1.22% against the US Dollar to close at a 20-year low of 134.25 Yen per dollar, having at one point traded at an intraday low of 134.47. Bear in mind that its intraday low so far in the 21st century was at 135.15 back in January 2002, so we’re not far off reaching levels unseen since the 1990s, although this morning it’s strengthened a touch to 134.06. Outside of Asia, stock futures in the US and Europe are pointing to additional losses today with contracts on the S&P 500 (-0.10%), NASDAQ 100 (-0.11%) and DAX (-0.44%) edging lower.

Finally on the data front, China’s May exports advanced +16.9% y/y, beating analyst estimates for a +8.0% rise and faster than the +3.9% increase in April. At the same time, the nation’s trade surplus grew to $78.76 bn in May, (vs. $57.7 bn expected) and compared to a $51.12 bn surplus in April. Separately, German industrial production grew by a weaker-than-expected +0.7% in April (vs. +1.2% expected), which comes on the back of an unexpected contraction in factory orders the previous day.

To the day ahead now, and the main highlight will be the aforementioned ECB decision and President Lagarde’s subsequent press conference. We’ll also hear from Bank of Canada Governor Macklem, and data releases today include the US weekly initial jobless claims.

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 24.84 PTS OR 0.76% //Hang Sang CLOSED DOWN 145.54 PTS OR 0.66% /The Nikkei closed UP 12.24 OR 0.04% //Australia’s all ordinaires CLOSED DOWN 1.45% /Chinese yuan (ONSHORE) closed UP 6.6764 /Oil UP TO 122.04dollars per barrel for WTI and UP TO 123.61 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6765 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6819: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER/

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

end

3c CHINA

4/EUROPEAN AFFAIRS//UK AFFAIRS/

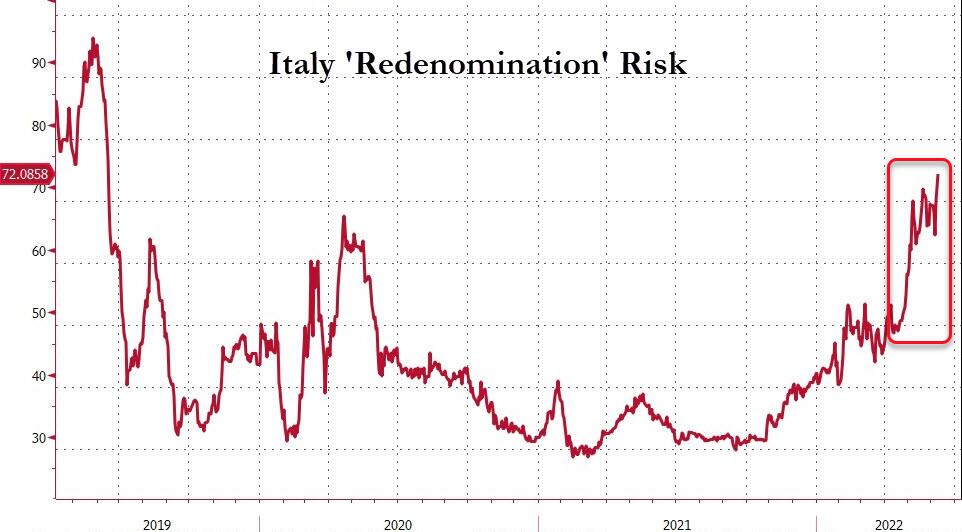

Yields skyrocket throughout Europe as Lagarde announces rate hikes. EU is undergoing defragmentation amid a stagflation forecast

(zerohedge)

ECB’s Lagarde Threads Needle Of Rate-Hikes Amid EU Defragmentation & Stagflation Forecast

THURSDAY, JUN 09, 2022 – 08:23 AM

Following The ECB’s statement, traders have moved rate-hike expectations up to around 150bps by December 2022…

All eyes will now be on what Lagarde says at the press conference as she tries to thread a needle of a fragmenting European bond market, ending bond-buying, and hiking rates into her own stagflationary forecast (lower growth and higher inflation). As Bloomberg Economics’ Geoff King points out:

“The most closely scrutinized part of the press conference will be any comments made by Lagarde on the likelihood of a 50 bp interest rate increase instead of a 25 bp move. She has published a roadmap for her preferred course of action and it’s consistent with 25 bp increases in July and September. We don’t expect her message to differ, but she’s changed tack before after inflation surpassed expectations.”

Markets were pricing in the 25 bp increase in July (and about a 40% chance of a 50bp move), and pricing in 25bps hikes for September and December as well as one each quarter thereafter until the main refinancing rate hits 1.5% (the estimate of neutral).

Watch live here (due to start at 0830ET)

* * *

Amid increasingly fragmented European bond markets, The ECB – as expected and well telegraphed for months – officially ended its bond-purchasing scheme and signaled lift-off on its interest rates, after eight years of NIRP (currently at -50bps).

European sovereign bond spreads are breaking out as the post-QE era begins…

Source: Bloomberg

Interestingly, given the surge in Italian yields/spreads, speaking just hours before the decision today, Lagarde’s predecessor Mario Draghi sounded a note of caution on tightening too fast.

Europe’s ‘inflation problem’ – which began long before Putin invaded Ukraine – have forced Lagarde into this corner, despite drastically slowing growth (as stagflationary threats leave central planners in a box).

Source: Bloomberg

The statement confirms that the ECB’s net buying under its asset-purchase program will conclude this month. That paves the way for Lagarde to hike rates next month, in effect keeping its long-standing promise that an end to its asset purchases will precede an increase in the benchmark deposit rate.

QE Ends July 1:

The Governing Council decided to end net asset purchases under its asset purchase programme (APP) as of 1 July 2022. The Governing Council intends to continue reinvesting, in full, the principal payments from maturing securities purchased under the APP for an extended period of time past the date when it starts raising the key ECB interest rates and, in any case, for as long as necessary to maintain ample liquidity conditions and an appropriate monetary policy stance.

No hint at QT:

“The Governing Council intends to continue reinvesting, in full, the principal payments from maturing securities purchased under the APP for an extended period of time”

Forward Guidance of a 25bps hike in July:

Accordingly, and in line with the Governing Council’s policy sequencing, the Governing Council intends to raise the key ECB interest rates by 25 basis points at its July monetary policy meeting. In the meantime, the Governing Council decided to leave the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility unchanged at 0.00%, 0.25% and -0.50% respectively.

On Fragmentation (via Bloomberg):

There’s no substantive change to the part of the statement relating to what the ECB could do to counter an unwarranted widening of spreads as it pares back stimulus. It amounts to a repeat of the point that “under stressed conditions, flexibility will remain an element of monetary policy.” The key question is whether an anti-fragmentation tool – which Bloomberg reported the ECB has worked on – should be explicit or implicit. It will be interesting to see how Lagarde responds to questions on this.

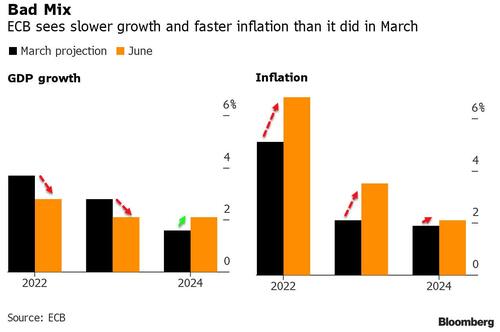

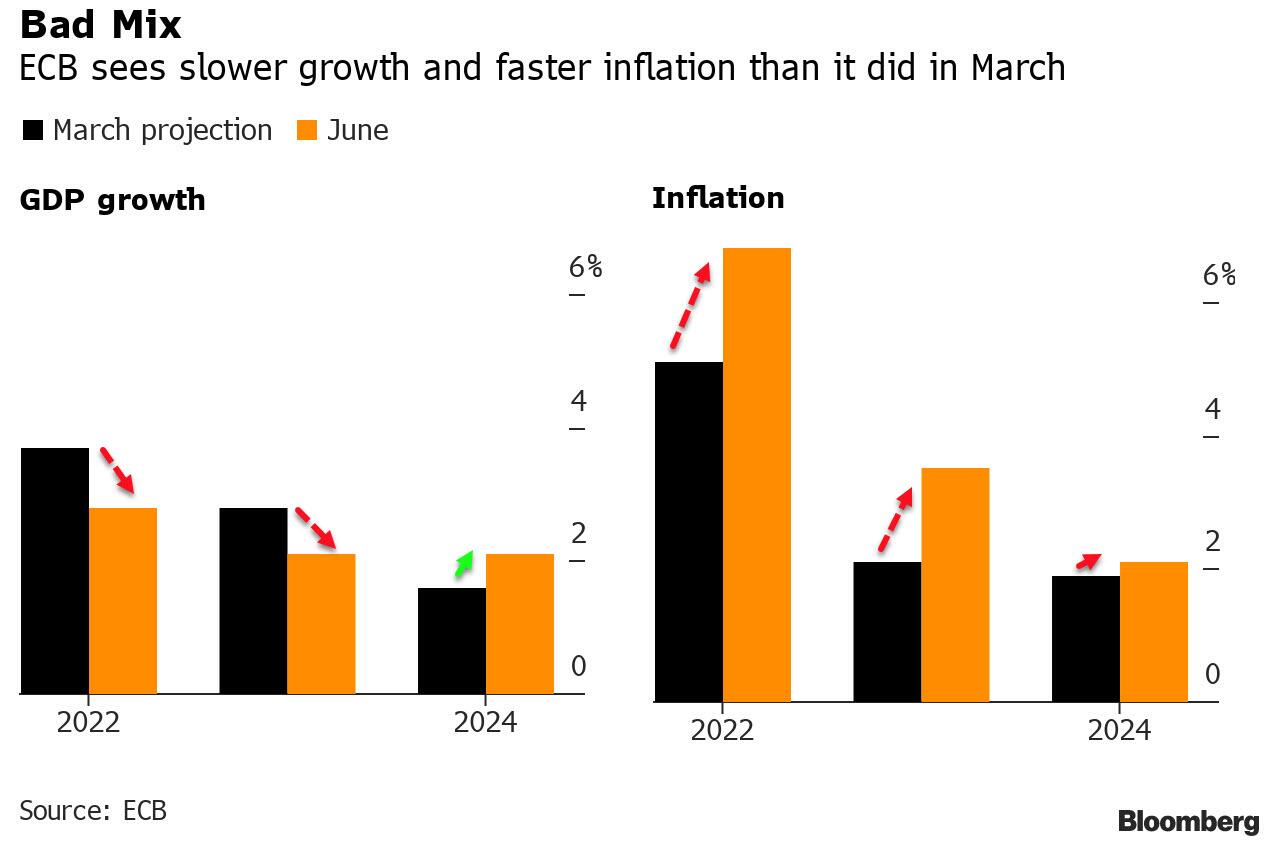

Additionally The ECB revised its inflation forecast notably higher and growth forecasts significantly lower (via Newsquawk)

Eurosystem staff have revised their baseline inflation projections up significantly.

These projections indicate that inflation will remain undesirably elevated for some time.

However, moderating energy costs, the easing of supply disruptions related to the pandemic and the normalisation of monetary policy are expected to lead to a decline in inflation.

The new staff projections foresee annual inflation at 6.8% in 2022. before it is projected to decline to 3.5% in 2023 and 2.1% in 2024 – higher than in the March projections.

This means that headline inflation at the end of the projection horizon is projected to be slightly above the Governing Council’s target.

Inflation excluding energy and food is projected to average 3.3% in 2022. 2.8% in 2023 and 2 3% in 2024 – also above the March projections.

ECB cuts its 2022 growth forecast to 2.8% from 3.7% and 2023 to 2.1% from 2.8%. For 2024, it’s an upward revision to 2.1% from 1.6%.

The euro spiked ahead of the ECB decision then tumbled after only to immediately bounce back…

Read the full ECB Statement below:

High inflation is a major challenge for all of us. The Governing Council will make sure that inflation returns to its 2% target over the medium term.

In May inflation again rose significantly, mainly because of surging energy and food prices, including due to the impact of the war. But inflation pressures have broadened and intensified, with prices for many goods and services increasing strongly. Eurosystem staff have revised their baseline inflation projections up significantly. These projections indicate that inflation will remain undesirably elevated for some time. However, moderating energy costs, the easing of supply disruptions related to the pandemic and the normalisation of monetary policy are expected to lead to a decline in inflation. The new staff projections foresee annual inflation at 6.8% in 2022, before it is projected to decline to 3.5% in 2023 and 2.1% in 2024 – higher than in the March projections. This means that headline inflation at the end of the projection horizon is projected to be slightly above the Governing Council’s target. Inflation excluding energy and food is projected to average 3.3% in 2022, 2.8% in 2023 and 2.3% in 2024 – also above the March projections.

Russia’s unjustified aggression towards Ukraine continues to weigh on the economy in Europe and beyond. It is disrupting trade, is leading to shortages of materials, and is contributing to high energy and commodity prices. These factors will continue to weigh on confidence and dampen growth, especially in the near term. However, the conditions are in place for the economy to continue to grow on account of the ongoing reopening of the economy, a strong labour market, fiscal support and savings built up during the pandemic. Once current headwinds abate, economic activity is expected to pick up again. This outlook is broadly reflected in the Eurosystem staff projections, which foresee annual real GDP growth at 2.8% in 2022, 2.1% in 2023 and 2.1% in 2024. Compared with the March projections, the outlook has been revised down significantly for 2022 and 2023, while for 2024 it has been revised up.

On the basis of its updated assessment, the Governing Council decided to take further steps in normalising its monetary policy. Throughout this process, the Governing Council will maintain optionality, data-dependence, gradualism and flexibility in the conduct of monetary policy.

Asset purchase programme (APP) and pandemic emergency purchase programme (PEPP)

The Governing Council decided to end net asset purchases under its asset purchase programme (APP) as of 1 July 2022. The Governing Council intends to continue reinvesting, in full, the principal payments from maturing securities purchased under the APP for an extended period of time past the date when it starts raising the key ECB interest rates and, in any case, for as long as necessary to maintain ample liquidity conditions and an appropriate monetary policy stance.

As concerns the pandemic emergency purchase programme (PEPP), the Governing Council intends to reinvest the principal payments from maturing securities purchased under the programme until at least the end of 2024. In any case, the future roll-off of the PEPP portfolio will be managed to avoid interference with the appropriate monetary policy stance.

In the event of renewed market fragmentation related to the pandemic, PEPP reinvestments can be adjusted flexibly across time, asset classes and jurisdictions at any time. This could include purchasing bonds issued by the Hellenic Republic over and above rollovers of redemptions in order to avoid an interruption of purchases in that jurisdiction, which could impair the transmission of monetary policy to the Greek economy while it is still recovering from the fallout from the pandemic. Net purchases under the PEPP could also be resumed, if necessary, to counter negative shocks related to the pandemic.

Key ECB interest rates

The Governing Council undertook a careful review of the conditions which, according to its forward guidance, should be satisfied before it starts raising the key ECB interest rates. As a result of this assessment, the Governing Council concluded that those conditions have been satisfied.

Accordingly, and in line with the Governing Council’s policy sequencing, the Governing Council intends to raise the key ECB interest rates by 25 basis points at its July monetary policy meeting. In the meantime, the Governing Council decided to leave the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility unchanged at 0.00%, 0.25% and -0.50% respectively.

Looking further ahead, the Governing Council expects to raise the key ECB interest rates again in September. The calibration of this rate increase will depend on the updated medium-term inflation outlook. If the medium-term inflation outlook persists or deteriorates, a larger increment will be appropriate at the September meeting.

Beyond September, based on its current assessment, the Governing Council anticipates that a gradual but sustained path of further increases in interest rates will be appropriate. In line with the Governing Council’s commitment to its 2% medium-term target, the pace at which the Governing Council adjusts its monetary policy will depend on the incoming data and how it assesses inflation to develop in the medium term.

Refinancing operations

The Governing Council will continue to monitor bank funding conditions and ensure that the maturing of operations under the third series of targeted longer-term refinancing operations (TLTRO III) does not hamper the smooth transmission of its monetary policy. The Governing Council will also regularly assess how targeted lending operations are contributing to its monetary policy stance. As announced previously, the special conditions applicable under TLTRO III will end on 23 June 2022.

***

The Governing Council stands ready to adjust all of its instruments, incorporating flexibility if warranted, to ensure that inflation stabilises at its 2% target over the medium term. The pandemic has shown that, under stressed conditions, flexibility in the design and conduct of asset purchases has helped to counter the impaired transmission of monetary policy and made the Governing Council’s efforts to achieve its goal more effective. Within the ECB’s mandate, under stressed conditions, flexibility will remain an element of monetary policy whenever threats to monetary policy transmission jeopardise the attainment of price stability

end

Euro Weakens, Fragmentation Fears Rise As Hawkish Lagarde Promises Bond Bailout

THURSDAY, JUN 09, 2022 – 09:36 AM

- End of QE? Check!

- Interest-rate hikes? Check!

- Peripheral spread-narrowing tools? Check!

ECB President Christine Lagarde started with the pre-approved hawkish comments, blaming Putin for both weaker growth forecasts and higher inflation outlooks, promising to end the bond-buying and start hiking rates in July.

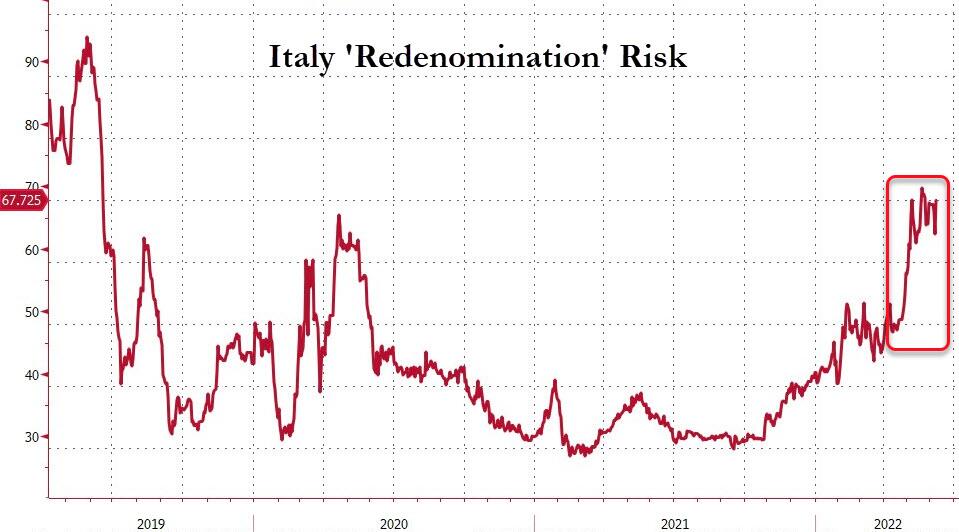

But then, the question of ‘fragmentation’ loomed (the fact that peripheral bond yields/spreads are decoupling – in a bad way – from the core, since she stopped buying everything), and the ECB boss appeared to fold like cheap lawn chair.

Lagarde says it is necessary to ensure monetary policy is transmitted through the whole area:

“we need to make sure there is no fragmentation.”

She notes there are existing instruments with the reinvestment capacity under the PEPP.

“And if it is necessary, as we have amply demonstrated in the past, we will deploy either existing or new instruments that will be made available.”

Lagarde states that “within our mandate we are committed to preventing fragmentation risks within the euro area.”

So some kind of asset purchase scheme for peripherals? The vagueness is intentional as it appears Lagarde is trying to pull off a Draghi ‘Whatever it takes’ moment while keeping her foot on the hawkish pedal.

As The IIF’s Robin Brooks pointed out:

If the ECB says to markets: “we will defend Italy’s spread,” markets will for sure test that statement.

So – in effect – what the ECB did today is to raise the odds of markets trying to force its hand.

All this is avoidable. Don’t hike. The Euro zone is going into recession…

The Euro reacted to this ‘dovish’ stance immediately, erasing its gains and heading to the lows of the day…

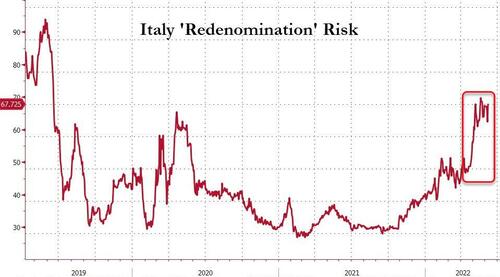

European bond spreads were mixed interestingly with Italian spread compressing (Lagarde will save us) while Spain and Portugal widened…

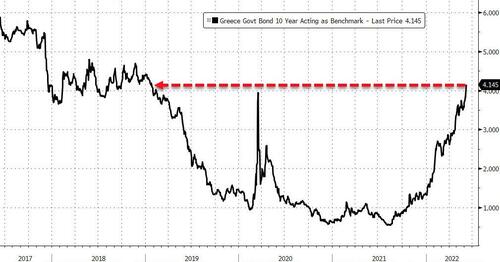

Greek yields are blowing out again…

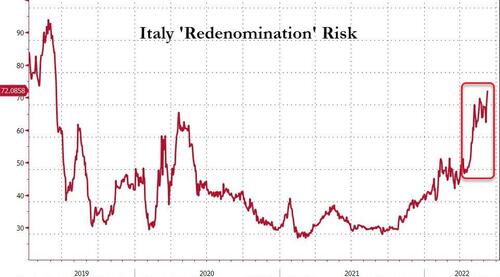

The reason this is worrisome is clear – markets are once again pricing in non-negligible possibility of ‘Italeave’…

So which is it Christine? More money printing for the PIIGS and nothing for the core? Or a real effort to battle inflation?

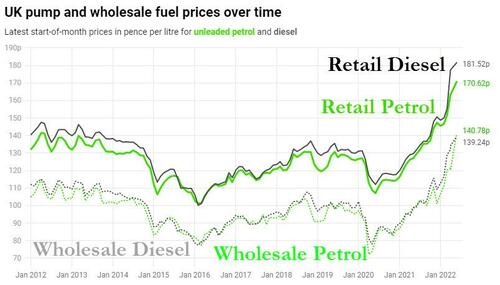

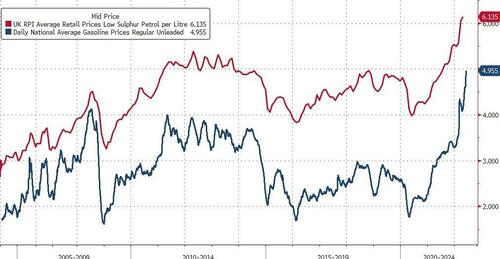

UK

Record UK gasoline prices…biggest surge in 17 years