JUNE 15 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1818.30 UP $6.50

SILVER: $21.42 UP $0.44

ACCESS MARKET: GOLD $1833.90

SILVER: $21.69

Bitcoin morning price: $20,561 DOWN 1652

Bitcoin: afternoon price: $21669 DOWN 544

Platinum price: closing UP $13.60 to $934.75

Palladium price; closing UP $15.30 at $1859.30

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE:EXCHANGE:

COMEX

no. of contracts issued by JPMorgan: 180/204

EXCHANGE: COMEX

CONTRACT: JUNE 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,809.500000000 USD

INTENT DATE: 06/14/2022 DELIVERY DATE: 06/16/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 200 1

323 C HSBC 4

363 H WELLS FARGO SEC 3

435 H SCOTIA CAPITAL 1

624 H BOFA SECURITIES 5

657 C MORGAN STANLEY 4

661 C JP MORGAN 180

700 C UBS 3

709 H BARCLAYS 1

732 C RBC CAP MARKETS 2

800 C MAREX SPEC 3

905 C ADM 1

TOTAL: 204 204

MONTH TO DATE: 22,811

_____________________________________________________________________________________

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT 204 NOTICE(S) FOR 20,400 Oz//0.6345 TONNES)

total notices so far: 22,811 contracts for 2,281,100 oz (70.951 tonnes)

SILVER NOTICES:

19 NOTICE(S) FILED 95,000 OZ/

total number of notices filed so far this month 1691 : for 8,455,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $6.50

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD//

INVENTORY RESTS AT 1063.74 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 44 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV://NO CHANGES IN SILVER INVENTORY AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 544.399 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 3305 CONTRACTS TO 151,979 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUGE LOSS IN OI WAS ACCOMPLISHED WITH OUR $0.32 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.32) AND WERE SUCCESSFUL IN KNOCKING OFF SOME SILVER LONGS.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 7.635 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 20 CONTRACTS OR 100,000 OZ//NEW STANDING: 8,770,000 / // V) GIGANTIC SIZED COMEX OI LOSS/(SPECULATOR COVERING)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS :-1038

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTACTS for 11 days, total 9162, contracts: 45.810 million oz OR 4.16 MILLION OZ PER DAY. (833 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 45.810 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 45.810 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3305 WITH OUR HUGE $0.32 LOSS IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 1150 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S 100,000 QUEUE JUMP //NEW STANDING: 8,770,000 OZ // .. WE HAD A STRONG SIZED LOSS OF 1116 OI CONTRACTS ON THE TWO EXCHANGES FOR 5.580 MILLION OZ WITH THE LOSS IN PRICE.

WE HAD 19 NOTICES FILED TODAY FOR 95,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR 2411 CONTRACTS TO 497,456 AND FURTHER NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -2727 CONTRACTS.

.

THE SMALL GAIN IN COMEX OI CAME DESPITE OUR HUGE FALL IN PRICE OF $18.80//COMEX GOLD TRADING/TUESDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERING

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 69.26 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY’S 20,400 OZ QUEUE JUMP //NEW STANDING: 74.696 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $18.80 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 3085 OI CONTRACTS 9.595 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5496 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 500,183

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3085, WITH 2411 CONTRACTS DECREASED AT THE COMEX AND 5496 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3085 CONTRACTS OR 9.595 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5496) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2411,): TOTAL GAIN IN THE TWO EXCHANGES 3085 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING AND SOME ADDITION TO SPECULATOR SHORTS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE. AT 69.26 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 20,400 OZ//NEW STANDING: 74.696 TONNES / 3) ZERO LONG LIQUIDATION//SOME SPECULATOR SHORT COVERING//SOME SPECULATOR SHORT ADDITIONS //.,4) SMALL SIZED COMEX OI GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

47,535 CONTRACTS OR 4,753,500 OZ OR 147.85 TONNES 11 TRADING DAY(S) AND THUS AVERAGING: 4321 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAY(S) IN TONNES: 147.85 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 147.85/3550 x 100% TONNES 3.69% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 147.85 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A HUGE SIZED 3305 CONTRACT OI TO 151,979 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1150 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1150 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3305 CONTRACTS AND ADD TO THE 1150 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF 2155 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 10.275 MILLION OZ

OCCURRED WITH OUR LOSS IN PRICE OF $0.32 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 16.50 PTS OR 0.50% //Hang Sang CLOSED UP 240.22 PTS OR 1.14% /The Nikkei closed DOWN 303.70 OR 1.14% //Australia’s all ordinaires CLOSED DOWN 1.39% /Chinese yuan (ONSHORE) closed UP 6.7053 /Oil DOWN TO 117.53 dollars per barrel for WTI and UP TO 120.29 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7053 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7154: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER/

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2411 CONTRACTS TO 497,456 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR HUGE LOSS OF $18.80 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (5496 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 5496 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :5496 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5496 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3085 CONTRACTS IN THAT 5496 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI LOSS OF 2411 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF GOLD $18.80.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (74.696),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.696 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $18.80) BUT WERE UNSUCCESSFUL IN KNOCKING OFF SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED A GOOD SIZED GAIN OF 18.077 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JUNE (74.696 TONNES)…

WE HAD 2727 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3085 CONTRACTS OR 308,500 OZ OR 9.575 TONNES

Estimated gold volume 91,432/// poor/

final gold volumes/yesterday 181,703 /poor

INITIAL STANDINGS FOR JUNE ’22 COMEX GOLD //JUNE 15

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 42,768.488 oz Manfra Brinks HSBC Int. Delaware. 529 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 204 notice(s) 20,400 OZ 0.6345 TONNES |

| No of oz to be served (notices) | 1204 contracts 18,400 oz 5.7322 TONNES |

| Total monthly oz gold served (contracts) so far this month | 22811 notices 2,281,100 OZ 70.951 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

0 customer deposits

total deposits: nil oz

4 customer withdrawals:

i) Out of Brinks 20,464.700 oz

ii) Out of HSBC: 8006.55 oz

iii) Out of Int. Delaware 321.51 oz 1 kilobar

iv) Out of Manfra: 16,975.728 oz (528 kilobars)

total withdrawal: 45,768.488 oz

ADJUSTMENTS: 2 dealer to customer

Brinks: 5497.819 oz

Int. Delaware 6,462.351 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 1408 contracts having LOST 350 contracts

We had 554 notices filed on TUESDAY so we GAINED 204 contracts or an additional 20,400 oz will stand for gold in this very active month of June

July has a LOSS OF 160 OI to stand at 1880

August has a loss of 5701 contracts DOWN to 413,535 contracts

We had 204 notice(s) filed today for 20400 oz FOR THE JUNE 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 204 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 180 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2021. contract month,

we take the total number of notices filed so far for the month (22,811) x 100 oz , to which we add the difference between the open interest for the front month of (JUNE 1408 CONTRACTS ) minus the number of notices served upon today 204 x 100 oz per contract equals 2,401,500 OZ OR 74.696 TONNES the number of TONNES standing in this active month of JUNE.

thus the INITIAL standings for gold for the JUNE contract month:

No of notices filed so far (22,811) x 100 oz+ (1408) OI for the front month minus the number of notices served upon today (204} x 100 oz} which equals 2,401,500 oz standing OR 74.696 TONNES in this active delivery month of JUNE.

TOTAL COMEX GOLD STANDING: 74,082 TONNES (A STRONG STANDING FOR A JUNE ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,419,784.828 oz 75.26 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 34,288,311.082 OZ

TOTAL ELIGIBLE GOLD: 16,775,361.357 OZ

TOTAL OF ALL REGISTERED GOLD: 17,512,948.725 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,093154.0 OZ (REG GOLD- PLEDGED GOLD)

END

JUNE 2022 CONTRACT MONTH//SILVER//JUNE 15

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 808,919.200 oz Brinks Delaware JPMorgan HSBC |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 602,231.700 oz CNT |

| No of oz served today (contracts) | 19CONTRACT(S)95,000 OZ) |

| No of oz to be served (notices) | 63 contracts (315,000 oz) |

| Total monthly oz silver served (contracts) | 1691 contracts 8,455,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposits

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposit into the customer account

i) Into CNT: 602,231.700 oz

total deposit: 602,231.700 oz

JPMorgan has a total silver weight: 170.237 million oz/336.708 million =50.57% of comex

Comex withdrawals: 4

i) Out of Brinks 195,455.000 oz

ii) Out of Delaware 929.900 oz

iii) Out of JPMorgan: 597,263.200 oz

iv) Out of HSBC: 15,271.100 oz

total withdrawal 808,919.200 oz

0 adjustments:

the silver comex is in stress!

TOTAL REGISTERED SILVER: 71.395 MILLION OZ

TOTAL REG + ELIG. 336.708 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE OI: 82 HAVING LOST 37 CONTRACTS.

WE HAD 57 NOTICES FILED ON TUESDAY SO WE GAINED 20 CONTRACTS OR AN ADDITIONAL 100,000 OZ WILL STAND IN THIS NON ACTIVE

DELIVERY MONTH OF JUNE

JULY HAD A LOSS OF 5060 CONTRACTS DOWN TO 65,791 CONTRACTS.

AUGUST GAINED 11 CONTRACTS TO STAND AT 1003

SEPTEMBER HAD A GAIN OF 1678 CONTRACTS UP TO 68,040 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 19 for 95,000 oz

Comex volumes:39,935// est. volume today// poor

Comex volume: confirmed yesterday: 76,978 contracts ( good )

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1691 x 5,000 oz = 8,455,000 oz

to which we add the difference between the open interest for the front month of JUNE(82) and the number of notices served upon today 19 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE./2022 contract month: 1691 (notices served so far) x 5000 oz + OI for front month of JUNE (82) – number of notices served upon today (19) x 5000 oz of silver standing for the JUNE contract month equates 8,770,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 15/WITH GOLD UP $6.50/BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD////INVENTORY RESTS AT 1063.74 TONNES

JUNE 14/WITH GOLD DOWN $18.80/NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 13/WITH GOLD DOWN $41.55: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 10/WITH GOLD UP $21.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

MAY 18/WITH GOLD DOWN $2.55//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.07 TONNES FROM THE GLD///INVENTORY RESTS AT 1049.21 TONNES

MAY 17/WITH GOLD UP $5.40:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1053.28 TONNES

MAY 16/WITH GOLD UP $5.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD///INVENTORY RESTS AT 1055.89 TONNES

MAY 13/ WITH GOLD DOWN $16.25//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.8 TONNES FROM THE GLD.//INVENTORY RESTS AT 1060.82 TONNES

MAY 12/WITH GOLD DOWN $26.50: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD////INVENTORY RESTS AT 1066.62 TONNES

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

GLD INVENTORY: 1063.75 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 15/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 14/WITH SILVER DOWN 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 13/WITH SILVER DOWN 62 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 10.WITH SILVER UP 13 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 Z FROM THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

MAY 18/WITH SILVER UP $0.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL 1.892 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 17/WITH SILVER UP $.22 TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.508 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 16/WITH SILVER UP $.52 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.546 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.593 MILLION OZ//

MAY 13/WITH SILVER UP 31 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ/

MAY 12/WITH SILVER DOWN 88 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ//

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

INVENTORY TONIGHT RESTS AT 544.399 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg

END

3. Chris Powell of GATA provides to us very important physical commentaries

The BIS is getting out of the gold swap business as May showed a drop of 45 tonnes. They are down to 270. They must be compliant with BASEL iii by December.

(Robert Lambourne/GATA)

Robert Lambourne: BIS gold swaps fell substantially again in May

Submitted by admin on Tue, 2022-06-14 12:15Section: Daily Dispatches

By Robert Lambourne

Tuesday, June 14, 2022

Another substantial reduction in the gold swaps of the Bank for International Settlements is indicated by the bank’s statement of account for May:

In March the reduction in swaps was about 112 tonnes, bringing the swaps down from about 472 tonnes as of February 28 to about 360 tonnes at March 31. There was another reduction of 45 tonnes in April, bringing the swaps total down to 315 tonnes. In May the reduction was about 45 tonnes, bringing the bank’s total volume of swaps to 270 tonnes.

This is the lowest level of swaps for the bank since November 2019.

These totals compare to the relatively recent record high estimated at 552 tonnes as of February 28, 2021. The decline in swaps since January 31, 2022 is 231 tonnes or around 46%.

Once again it is evident that the BIS remains an active trader of significant volumes of gold swaps on a regular basis, and the recent data suggests that a downward trend in the bank’s swaps has begun. A continuation of this trend would indicate that an exit from the swaps is underway, potentially due “Basel III” regulations.

The BIS rarely comments publicly on its gold activities, but its first use of gold swaps was considered important enough to cause the bank to give some background information to the Financial Times for an article published July 29, 2010, coinciding with publication of the bank’s 2009-10 annual report.

The general manager of the BIS at the time, Jaime Caruana, said the gold swaps were “regular commercial activities” for the bank, and he confirmed that they were carried out with commercial banks and so did not involve central banks. It also seems highly likely that the BIS’ remaining swaps are still all made with commercial banks, because the BIS annual report has never disclosed a gold swap between the BIS and a major central bank.

The swap transactions potentially create a mismatch at the BIS, which may end up being long unallocated gold (the gold held in BIS sight accounts at major central banks) and short allocated gold (the gold required to be returned to swap counterparties). This possible mismatch has not been reported by the BIS.

The gold banking activities of the BIS have been a regular part of the services it offers to central banks since the establishment of the bank 90 years ago. The first annual report of the BIS explains these activities in some detail:

http://www.bis.org/publ/arpdf/archive/ar1931_en.pdf

A June 2008 presentation made by the BIS to potential central bank members at its headquarters in Basel, Switzerland, noted that the bank’s services to its members include secret interventions in the gold and foreign exchange markets:

https://www.gata.org/node/11012

The use of gold swaps to take gold held by commercial banks and then deposit it in gold sight accounts held in the name of the BIS at major central banks doesn’t appear ever to have been as large a part of the BIS’ gold banking business as it has been in recent years.

As of March 31, 2010, excluding gold owned by the BIS, there were 1,706 tonnes held in gold sight accounts at major central banks in the name of the BIS, of which 346 tonnes or 20% were sourced from gold swaps from commercial banks.

The BIS now operates a much smaller gold banking business, with an estimated 695 tonnes of gold deposited in gold sight accounts as of April 30. (This excludes 102 tonnes of the gold owned by the BIS itself.) The present-day role of gold swaps in this smaller business is proportionately far greater.

In May, excluding the 102 tonnes of gold owned by the BIS, some 39% of the gold held in sight accounts at major central banks on behalf of the BIS came from gold swaps instead of from other central banks. The proportion of this unallocated gold sourced via gold swaps is now declining as the use of gold swaps by the BIS has fallen.

If the BIS was adopting the level of disclosure made by publicly held companies, such as commercial banks, some explanation of these changes probably would have been required by the accounting regulators. This irony may not be lost on those dealing with regulatory activities at the BIS. Presumably the shrinkage of the BIS’ gold banking business shows that even central banks now prefer to hold their own gold or hold it in earmarked form — that is, as allocated gold.

A review of Table B below highlights recent BIS activity with gold swaps, and despite the recent declines, the latest position estimated from the BIS monthly statements remains large and the volume of trades is significant.

No explanation for this continuing use of swaps has been published by the BIS. Indeed, no comment on the bank’s use of gold swaps has been offered since 2010.

This gold is supplied to the BIS by bullion banks via the swaps. The gold is then deposited in BIS gold sight accounts (unallocated gold accounts) at major central banks such as the Federal Reserve.

The reasons for this activity have never been fully explained by the BIS and various conjectures have been made as to why the BIS is facilitating it. One conjecture is that the swaps are a mechanism for gold secretly supplied by central banks to cover shortfalls in the gold markets to be returned to the central banks. The use of the BIS to facilitate this trade suggests of a desire to conceal the rationale for the transactions.

The BIS’ use of gold swaps and other gold derivatives is still quite extensive despite the recent declines.

Table B below shows that the BIS continues to trade significant volumes of gold swaps regularly. As can be seen in Table A below, the BIS has used gold swaps extensively since its financial year 2009-10.

No use of swaps is reported in the bank’s annual reports for at least 10 years prior to the year ended March 2010.

The February 2021 estimate of the bank’s gold swaps (552 tonnes) is higher than any level of swaps reported by the BIS at its March year-end since March 2010. The swaps reported at March 2021 are at the highest year-end level reported, as is clear from Table A.

———————-

Table A — Swaps reported in BIS annual reports

March 2010: 346 tonnes.

March 2011: 409 tonnes.

March 2012: 355 tonnes.

March 2013: 404 tonnes.

March 2014: 236 tonnes.

March 2015: 47 tonnes.

March 2016: 0 tonnes.

March 2017: 438 tonnes.

March 2018: 361 tonnes.

March 2019: 175 tonnes

March 2020: 326 tonnes

March 2021: 490 tonnes

———————-

The table below reports the estimated swap levels since August 2018.

It can be seen that the BIS is actively involved in trading gold swaps and other gold derivatives with changes from month to month reported in excess of 100 tonnes in this period.

———————-

Table B – Swaps estimated by GATA from BIS monthly statements of account

Month ….. Swaps

& year … in tonnes

May-22 ….. /270

Apr-22 ….. /315

Mar-22 …. /360

Feb-22 …. /472

Jan-22 ….. /501

Dec-21…. /414

Nov-21…. /451

Oct-21…. /414

Sep-21 …. /438

Aug-21 …. /464

Jul-21 …. /502

Jun-21 …./471

May-21 …./517

Apr-21 …. /472

Mar-21…. /490±

Feb-21 …../552

Jan-21 …. /523

Dec-20 …. /545

Nov-20 …. /520

Oct-20 …. /519

Sep-20…../ 520

Aug-20…../ 484

Jul-20 ….. / 474

Jun-20 …. / 391

May-20 …. / 412

Apr-20 …. / 328

Mar-20 …. / 326*

Feb-20 …. / 326

Jan-20 …. / 320

Dec-19 …. / 313

Nov-19 …. / 250

Oct-19 …. / 186

Sep-19 …. / 128

Aug-19 …. / 162

Jul-19 ….. / 95

Jun-19 …. / 126

May-19 …. / 78

Apr-19 ….. / 88

Mar-19 …. / 175

Feb-19 …. / 303

Jan-19 …. / 247

Dec-18 …. / 275

Nov-18 …. / 308

Oct-18 …. / 372

Sep-18 …. / 238

Aug-18 …. / 370

± The estimate originally reported by GATA was 487 tonnes, but the BIS annual report states 490 tonnes, It is believed that slightly different gold prices account for the difference.

* The estimate originally reported by GATA was 332 tonnes, but the BIS annual report states 326 tonnes. It is believed that slightly different gold prices account for the difference.

GATA uses gold prices quoted by USAGold.com to estimate the level of gold swaps held by the BIS at month-ends.

—–

As noted already, the BIS in recent times has refused to explain its activities in the gold market, nor for whom the bank is acting:

https://www.gata.org/node/17793

Despite this reticence the BIS is almost certainly acting on behalf of central banks in taking out these swaps, as they are the BIS’ owners and control its Board of Directors.

This refusal to explain prompts some observers to believe that the BIS acts as an agent for central banks intervening surreptitiously in the gold and currency markets, providing those central banks with access to gold as well as protection from exposure of their interventions.

A recent report published by Bullion Star’s Ronan Manly on the Bank of Portugal’s use of its gold reserves reinforces this point as the Bank of Portugal confirms that 20 tonnes of its gold is stored with the BIS:

https://www.gata.org/node/21950

This disclosure seems a little economic with the truth as the BIS has no gold storage facilities of its own. Gold held by the BIS on behalf of central banks is either deposited into a BIS gold sight (unallocated) account or a BIS earmarked (allocated) gold account and deposited normally with one of the central banks based at a major gold trading center, such as the Federal Reserve in New York.

Since Manly shows that the Bank of Portugal is focused on earning income from its gold, it seems highly likely that this gold is held in a BIS sight account, though its ultimate location is unclear.

It is possible that the swaps provide a mechanism for bullion banks to return gold originally lent to them by central banks to cover bullion bank shortfalls of gold. Some commentators have suggested that a portion of the gold held by exchange-traded funds and managed by bullion banks is sourced directly from central banks.

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults with GATA about the involvement of the Bank for International Settlements in the gold market.

* * *

end

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //LITHIUM

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.7093

OFFSHORE YUAN: 6.7154

HANG SANG CLOSED UP 240.22 PTS OR 1.14%

2. Nikkei closed DOWN 303.70% OR 1.14%

3. Europe stocks ALL CLOSED ALL GREEN

USA dollar INDEX UP TO 104.61/Euro RISES TO 1.0484

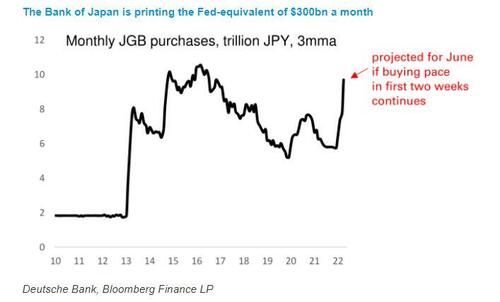

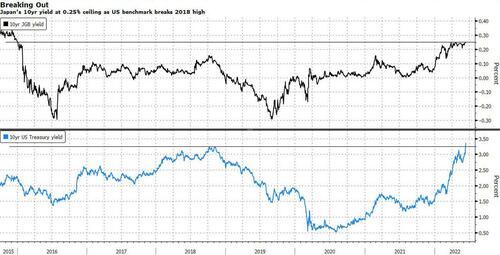

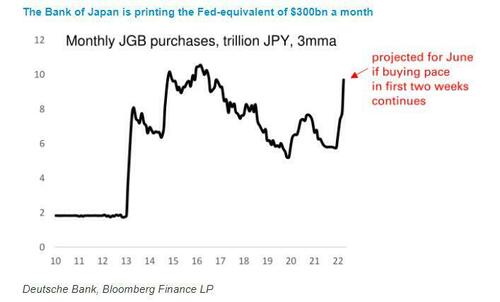

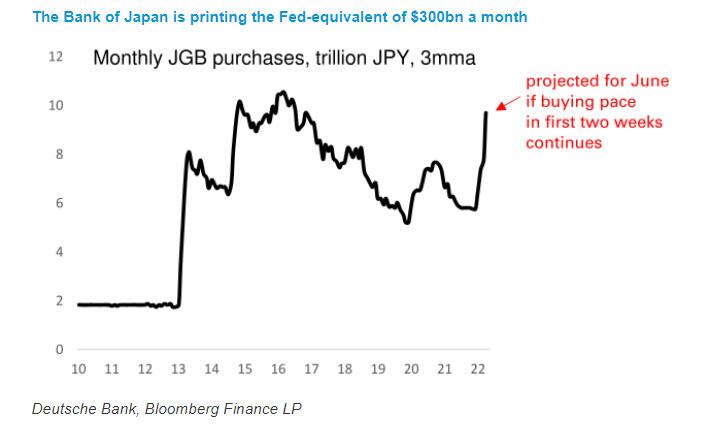

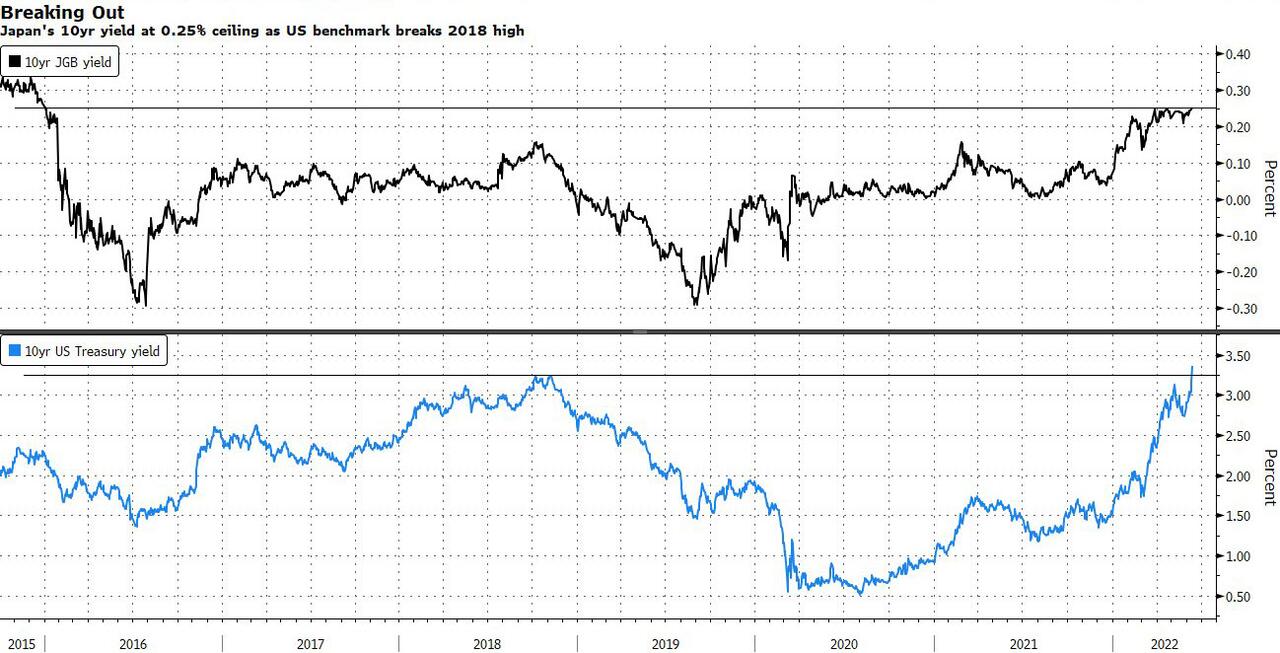

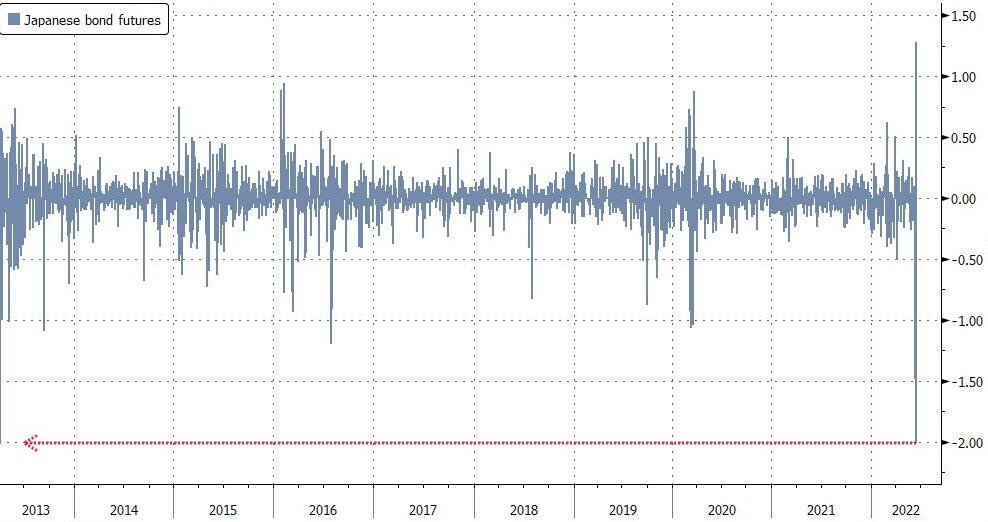

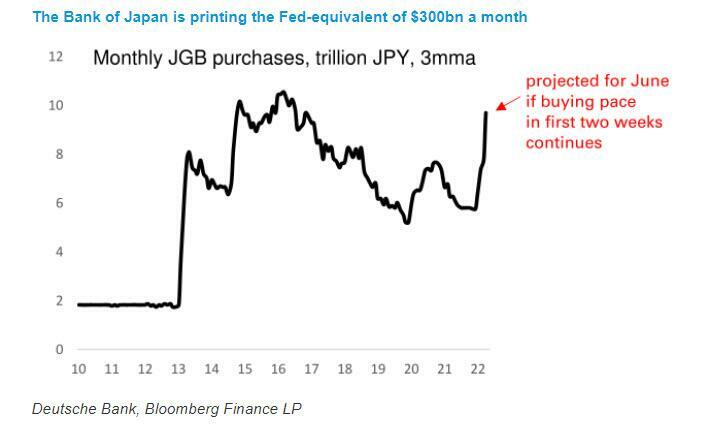

3b Japan 10 YR bond yield: FALLS TO. +.227/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 134.49/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN -SHORE CLOSED UP// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

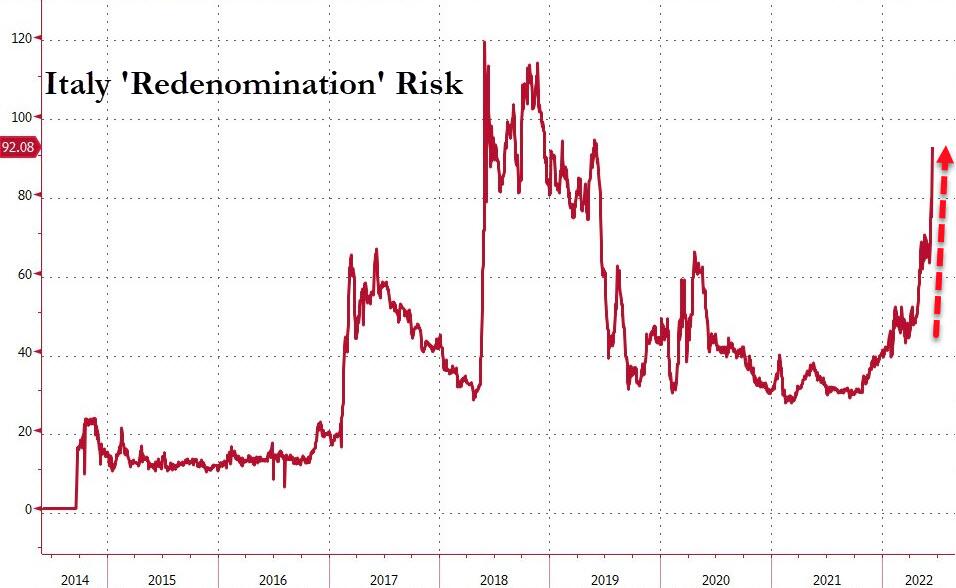

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.649%/Italian 10 Yr bond yield FALLS to 3.91% /SPAIN 10 YR BOND YIELD FALLS TO 2.92%…ALL BLOWING UP!!

3i Greek 10 year bond yield FALLS TO 4.31//

3j Gold at $1832.16 silver at: 21.56 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 1/8 roubles/dollar; ROUBLE AT 56.74

3m oil into the 117 dollar handle for WTI and 120 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 134.49DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9992– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0466well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.381 DOWN 10 BASIS PTS

USA 30 YR BOND YIELD: 3.377 DOWN 6 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.29

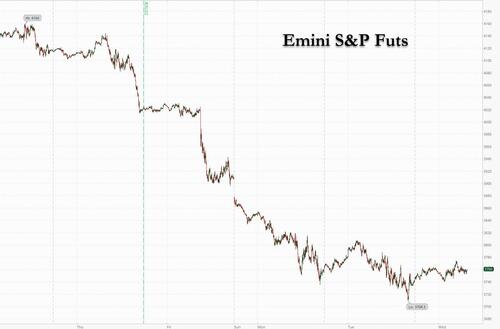

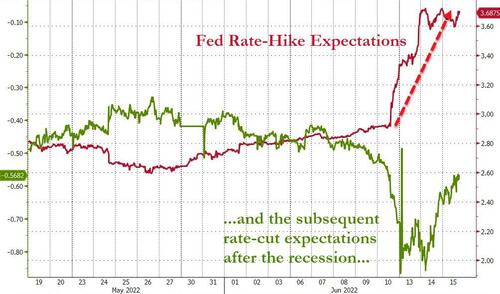

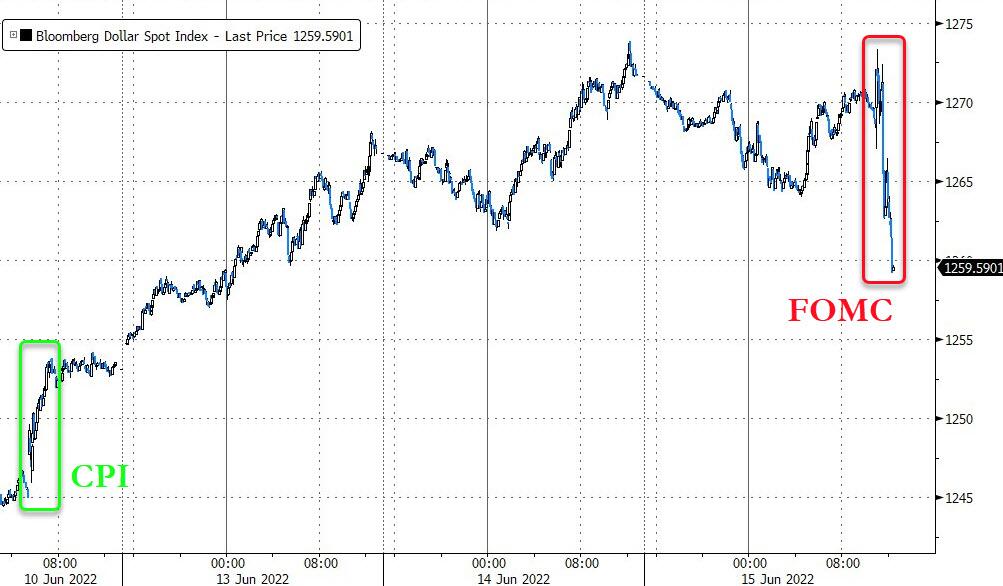

Futures Rise As ECB Panics And Fed Looms

WEDNESDAY, JUN 15, 2022 – 07:53 AM

After five days of non-stop losses, US index futures finally bounced modestly along with stocks in Europe as the ECB announced it would hold an emergency meeting to undo the damage done by its meeting from last week, and ahead of the Fed which today will hike by 75bps, the most since 1994, and will then scramble to undo the damage from pushing the US into a recession in coming days and weeks.

Contracts on the S&P 500 and Nasdaq 100 posted modest gains, rising 0.8% and 1% respectively, ahead of the Fed, with markets fully pricing in the biggest rate hike since 1994 amid worries about the outlook for the economy. Europe’s Stoxx Europe 600 index jumped more than 1%, snapping a six-day losing streak, while the euro strengthened and the region’s bonds advanced as the European Central Bank’s Governing Council started an emergency meeting. Treasury yields dipped and the dollar retreated from a two-year high.

In premarket trading, major technology and internet stocks are higher in premarket trading along with US stock futures ahead of Wednesday’s Federal Reserve announcement, with investors expecting a 75 basis-point increase in rates. Bank stocks were also higher in premarket trading. Here are some other notable premarket movers:

- Spotify (SPOT US) shares gain 2.2% in premarket trading as Wells Fargo upgraded the stock to equal-weight, saying the music streaming firm’s recent investor day laid out a more profitable company than the brokerage has modeled historically.

- Chinese tech stocks are mostly higher in US premarket trading, with education shares continuing their winning streak since peer Koolearn’s livestreaming hit went viral. Alibaba (BABA US) +1.9%, Baidu (BIDU US) +3.6%, Pinduoduo (PDD US) +2.3%, New Oriental Education (EDU US) +8.4%, TAL Education (TAL US) +4.5%.

- iQIYI (IQ US) shares decline 3.9% in US premarket trading as Baidu is in talks to sell its majority stake in the streaming service in a deal that could value all of iQIYI at $7 billion, Reuters reported, citing people with knowledge of the matter.

- Cryptocurrency-related stocks fell in premarket trading on Wednesday as Bitcoin and Ethereum tumbled. MicroStrategy (MSTR US) -7.6%, Marathon Digital Holdings (MARA US) -7.6%, Riot Blockchain (RIOT US) -7%, Coinbase (COIN US) -6.6%.

- Apple (AAPL US) and other consumer computer-hardware stocks may be in focus today as Morgan Stanley cut its price targets for such shares due to risks related to a potential slowdown in consumer spending.

- Moderna’s (MRNA US) shares rose 1.2% in US after-hours trading on Tuesday, while analysts said that the unanimous verdict from an FDA panel, which supported the biotech firm’s Covid vaccine for children, came as no surprise.

- Qualcomm (QCOM US) stocks could be in focus after the company won a European Union court bid to topple a 997 million-euro antitrust fine for allegedly pressuring Apple to only buy its 4G chips.

Fears of stagflation have driven stocks into a bear market and triggered a stunning selloff in bonds in recent days. Uncertainty is elevated heading into the Fed decision: increments of 50 basis points, 75 basis points and even 100 basis points have all been chewed over by commentators. Parts of the US yield curve remain inverted, signaling concerns that restrictive monetary policy will lead to an economic downturn.

Today’s main event is of course the Fed decision which is expected to include a 75bp rate hike, with latest forecasts released at the same time. Swaps market is currently pricing in around 70bp of rate hikes for the meeting with a combined 202bp of additional hikes priced for the June, July and September meetings. From the forecasts, focus will be on revisions to the Fed’s long-term rate; swaps market is currently pricing a rate peak at around 3.90% by the middle of next year (full preview here).

“Markets are poised for aggressive rate hikes, but what of US economic growth?” said Nema Ramkhelawan-Bhana, an economist at Rand Merchant Bank in Johannesburg. “It might not be in recessionary territory just yet, but the landing is not going to be as soft as the Fed predicates. Anything less than 75 basis points or at least a strong willingness to make more significant adjustments will likely turn the market on its head, eroding total returns of global bonds and equities even further.”

European equities trade well but off session highs. FTSE MIB outperforms, rallying as much as 3.3% before stalling. Stoxx 600 rises as much as 1.2% with travel, banks and insurance names doing much of the heavy lifting, while the euro strengthened and the region’s bonds advanced as the European Central Bank’s Governing Council started an emergency meeting. While new stimulus may not be on the agenda, officials will discuss a crisis strategy and the reinvestment of bond purchases conducted under the now-halted pandemic emergency program, Bloomberg reported. Here are the biggest European movers:

Rate-sensitive sectors such as financials and technology gained in Europe as the ECB holds an ad hoc meeting to discuss market conditions and the Fed concludes its two-day policy meeting. Finecobank shares rise as much as 8.4%, Intesa Sanpaolo +7.5%, Assicurazioni Generali +5.3%.

- Europe auto stocks are among outperforming sectors in the wider equity gauge, led by French part suppliers Faurecia and Valeo, and carmaker Renault. Faurecia shares gain as much as 8.7%, Valeo +6.5%, Renault +5.6%

- Whitbread shares rise as much as 6.4% after the hotel operator reported quarterly sales, with Barclays noting the company’s “upbeat tone.”

- Gerresheimer shares rise as much as 17% after a Bloomberg report that the German maker of packaging for drugs and cosmetics rejected an informal takeover approach from Bain Capital in recent weeks.

- Nordic and European forestry and paper mill companies’ shares rebound, breaking sharp declines triggered after brokers cut their respective outlooks for the sector in the past week. Smurfit Kappa stock rises as much as 5.3%, BillerudKorsnas +4.8%, Huhtamaki +5.6%

- H&M shares drop as much as 6.4% with uncertainty about the margin outlook and ongoing cost pressures overshadowing the apparel retailer’s 2Q sales beat.

- Getinge shares fall as much as 18% after the medical technology firm lowered guidance, projecting flat organic sales growth for the year. Nordea and JPMorgan downgraded their recommendations.

- Elia Group shares fell as much as 12% after the electricity transmission company laid out plans for a rights offering.

- Autoneum shares drop as much as 5.2% after the car- parts maker warned on profits. Vontobel analyst Arben Hasanaj noted the firm’s difficulty in passing on higher costs, along with further likely delays in car production recovery.

- Voltalia slumps as much as 9.1% after Oddo downgrades to neutral in note as it questions what level of growth is possible after 2023.

“The ECB is between rock and a hard place, like most other central banks,” said Marija Veitmane, a senior strategist at State Street Global Markets. “Inflation is very high and shows little signs of quickly declining, while the economy is increasingly fragile, particularly with the war in Europe and ever-rising energy costs. So anything the ECB can announce to reduce systemic risk is very welcome.”

Earlier in the session, Asian stocks posted modest declines as sentiment improved from earlier in the week, with Chinese shares rising after domestic economic data showed pockets of recovery. The MSCI Asia Pacific Index was down 0.4% as of 6:07 p.m. in Singapore, as losses in regional tech hardware shares offset advances in China’s internet giants. South Korea and the Philippines led declines, while Japanese stocks fell ahead of a central bank policy meeting this week. Gains in China and Hong Kong helped offset losses elsewhere as data showed the country’s industrial production unexpectedly increased in May. Meanwhile the nation’s central bank kept a key policy rate unchanged, avoiding further policy divergence as the Federal Reserve tightens.

“A more accommodative policy and fiscal environment together with stronger corporate fundamentals should be positive for Chinese equity assets,” said Jessica Tea, an investment specialist at BNP Paribas Asset Management. The MSCI Asia gauge dropped almost 4% over the previous two sessions as inflation data from the US fueled bets of a 75-basis-point rate hike by the Fed at Wednesday’s meeting. Still, the index has outperformed a measure of global peers this year, with the latter now in a bear market.

Japanese stocks dropped ahead of a Federal Reserve rate decision. A Bank of Japan review on Friday is also on the radar. The Topix Index fell 1.2% to close at 1,855.93 while the Nikkei gauge declined 1.1% to 26,326.16. Keyence Corp. contributed the most to the Topix Index’s decline, decreasing 3.9%. Out of 2,170 shares in the index, 288 rose and 1,829 fell, while 53 were unchanged. “The sharp decline in JGBs is also contributing to the drop in stock prices as uncertainty mounts ahead of the BOJ meeting,” said Hajime Sakai, chief fund manager at Mito Securities Co

Indian stocks fell after swinging between gains and losses for the most part of the session, as concerns over higher inflation and likely tighter monetary policy measures weighed on sentiment. The S&P BSE Sensex slipped 0.3% to close at 52,541.39 in Mumbai to its lowest level since July 28. The NSE Nifty 50 Index also slipped by a similar magnitude. Reliance Industries Ltd. posted its longest run of losses in more than a month and was the biggest drag on the Sensex, which had 17 of 30 member stocks trading lower. Ten of the 19 sector sub-indexes compiled by BSE Ltd fell, led by a gauge of power stocks. Retail inflation in India held above the central bank’s target in May, while wholesale prices accelerated for a third-straight month as input costs continue to rise, hurting company earnings. “Commodity prices continue to remain elevated and despite passing on the costs to consumers, India Inc. is still facing margin pressures,” Mitul Shah, head of research at Reliance Securities wrote in a note.

Australia’s S&P/ASX 200 index fell 1.3% to close at 6,601.00, the fourth straight day of declines. All sectors finished lower, with mining stocks and banks the biggest drags on the index. During early trade, Australia’s industrial relations umpire raised the minimum wage by 5.2% from July 1, a larger-than-expected increase, affirming speculation of faster tightening by the central bank. Meanwhile, in New Zealand, the S&P/NZX 50 index was little changed at 10,635.92., after entering a bear market Tuesday. The gauge has shed more than 20% from its January 2021 peak.

In FX, the Bloomberg Dollar Spot Index fell as the greenback weakened against all of its Group-of-10 peers apart from the Canadian dollar. Risk-sensitive Scandinavian currencies and the Aussie dollar lead gains. The euro rose by as much as 0.9% to 1.0508, and the yield on 10-year Italian bonds fell as much as 30bps after the ECB announced the Governing Council would hold an ad-hoc meeting on Wednesday “to discuss current market conditions.” ECB officials will be invited to sign off on the reinvestment of bond purchases conducted under the now-halted pandemic emergency program, a crisis response that they flagged in their decision last week, according to people familiar with the matter. Three-month euribor fixes higher by the most in more than two years, climbing to the highest since April 2020 as funding rates seek to mirror ECB rate hike expectations. Japanese bond futures drop most since 2013 as traders ramp up bets BOJ will give in to tweak policy. Australian bonds slumped with three-year yields posting steepest two-day climb since 1994. The Aussie extended an advance after the Fair Work Commission said the minimum wage will be increased by 5.2%. Earlier, the RBA said it “will do what’s necessary” to bring inflation back down to its 2-3% target as Goldman sees three more half-point hikes.

In rates, Treasuries pared a recent drop, with yields falling up to 8bps led by shorter maturities amid a TSY rally in Asia and early European sessions, leaving yields richer by as much as 12.5bp across front-end leading into US session. Markets are pricing in 73bps worth of hikes from the Fed today. US 10-year yields around 3.36%, richer by 10bp on the day while front-end outperformance steepens 2s10s, 5s30s spreads by 3bp and 6.5bp respectively. Curve steepens as long-end lags front-end rally and some rate hike premium eases out the swaps market ahead of 2pm ET Fed policy decision. European bonds rallied after ECB announces emergency meeting to discuss market conditions, with French and UK outperforming along with Italy and other peripherals.

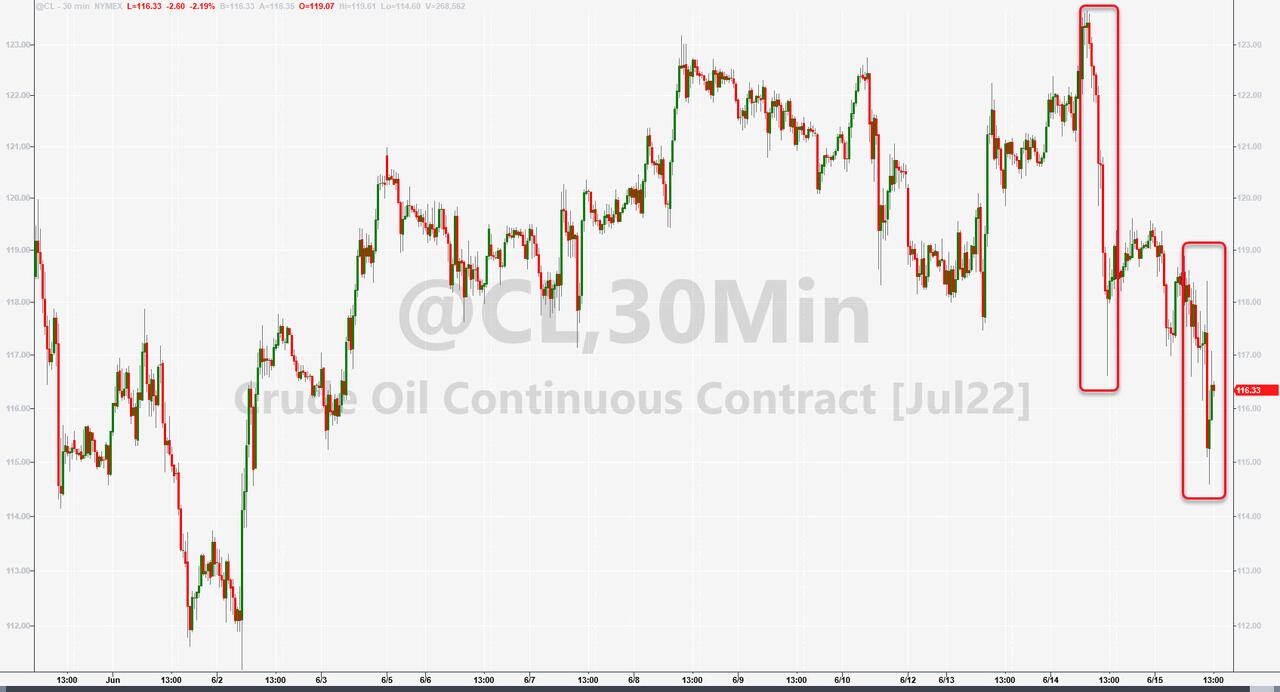

In commodities, crude futures drop back toward the lows for the week. WTI falls 1.2% near $117.50. Most base metals trade in the green; LME tin rises 2.3%, outperforming peers. Spot gold rises roughly $16 to trade near $1,825/oz

Looking to the day ahead, the main highlight will likely be the aforementioned FOMC decision and Chair Powell’s subsequent press conference. There’s also an array of ECB speakers, including President Lagarde, as well as the ECB’s Holzmann, Nagel, Centeno, Muller, De Cos, Panetta and Knot. Otherwise, data releases include Euro Area industrial production for April, US retail sales for May, the NAHB housing market index for June and the Empire State manufacturing survey for June.

Market Snapshot

- S&P 500 futures up 0.8% to 3,768.50

- STOXX Europe 600 up 1.2% to 412.15

- MXAP down 0.4% to 159.27

- MXAPJ little changed at 529.71

- Nikkei down 1.1% to 26,326.16

- Topix down 1.2% to 1,855.93

- Hang Seng Index up 1.1% to 21,308.21

- Shanghai Composite up 0.5% to 3,305.41

- Sensex up 0.2% to 52,797.58

- Australia S&P/ASX 200 down 1.3% to 6,601.03

- Kospi down 1.8% to 2,447.38

- Brent Futures down 0.2% to $120.90/bbl

- Gold spot up 0.6% to $1,818.80

- U.S. Dollar Index down 0.56% to 104.93

- German 10Y yield little changed at 1.77%

- Euro up 0.6% to $1.0479

- Brent Futures down 0.2% to $120.90/bbl

Top Overnight News from Bloomberg

- Federal Reserve Chair Jerome Powell, who’s carefully telegraphed interest rate hikes over four years, looks likely to abandon gradualism and move more forcefully to stamp out inflation along with growing concerns that it will persist

- The European Central Bank’s Governing Council is ready to step in if it considers moves in government bond markets to be unjustified, according to Belgium’s Pierre Wunsch, as the ECB prepared for an emergency meeting on recent euro-zone bond turbulence

- The European Union is restarting infringement proceedings against the UK and will launch two new legal actions after London proposed legislation to override part of the Brexit withdrawal agreement, according to an EU official

- The first batch of a Chinese offshore yuan sovereign bond sale saw the strongest demand in nearly two years, defying a recent stream of outflows at a time when the global debt market is showing deepening levels of stress

- Even after central banks recognized they got their inflation calls wrong last year, they’ve continued to flub their policy guidance, threatening greater damage to their credibility, roiling markets and undermining the pandemic recovery

A more detailed look at markets courtesy of Newsquawk

Asia-Pac stocks traded mixed amid cautiousness heading into the FOMC with markets pricing in a more than 90% chance of a 75bps rate hike, while the region also digested better-than-expected Chinese activity data. ASX 200 was led lower by energy, resources and tech, despite a 5.2% national minimum wage increase. Nikkei 225 failed to benefit from strong Machinery Orders data amid the ongoing currency-related jitters. Hang Seng and Shanghai Comp. were positive with encouragement from the latest activity data that showed surprise growth in Industrial Production and a narrower than feared contraction in Retail Sales, while attention was also on the PBoC which rolled over CNY 200bln through its 1-year MLF with the rate unchanged.

Top Asian News

- PBoC injected CNY 200bln via 1-year MLF vs. CNY 200bln maturing with the rate kept at 2.85%, as expected.

- China’s stats bureau said the main indicators show marginal improvement and the economy shows good recovery momentum, but added that the economic recovery still faces many difficulties and challenges. Furthermore, it said policies to stabilise economic growth gained traction and it expects economic performance to improve further in June due to policy support, but noted recovery is still at an initial stage and main indicators are at low levels, according to Reuters.

- Hong Kong reports 1047 new COVID cases. Appears to be the first time since early April that cases have surpassed the 1k mark.

European equities are firmer across the board ahead of the impromptu ECB meeting, Euro Stoxx 50 +1.0%; unsurprisingly, periphery-nation indexes are outperforming, FTSE MIB +3.0%, given upside in banking names. As such, the Banking sector outperforms with most of its peers also in the green, though the Energy sector lags amid benchmark pricing. Stateside, futures are firmer across the board deriving impetus from European performance, but with overall action somewhat more contained ahead of the Fed and uncertainty around 75bp, ES +0.3%. Baidu (BIDU) is in discussions with potential suitors to offload its 53% stake in video-streaming name Iqiyi, according to Reuters sources. +3.8% in the pre-market.

Top European News

- UK PM Johnson is reportedly determined to reverse Chancellor Sunak’s planned GBP 15bln tax raid on business as he tries to firm up support following last week’s confidence vote, according to The Times.

- UK PM Johnson is understood to have told his cabinet to ‘de-escalate’ the Northern Ireland Protocol stand-off with the EU, according to The Telegraph.

- UK exports to the EU during H1 of last year fell by 15.6% amid Brexit frictions, according to a study by Aston University cited by FT.

- Swiss SECO Forecasts (summer): Inflation: 2022 2.5% (prev. 1.9%), 2023 1.4% (prev. 0.7%). GDP: 2022 2.8% (prev. 3.0%), 1.6% (prev. 1.7%)

Central Banks

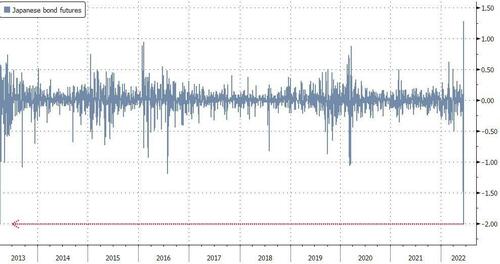

- BoJ offers an additional emergency bond buying operation; to buy unlimited amounts of 10yr JGBs on June 16th & 17th at 0.25%.

- Fall in JGB futures has triggered a circuit breaker at the Tokyo stock exchange, via Japan Exchange Group.

- Japan’s Securities Dealer Association’s Morita says the JPY may have weakened too much, via Reuters.

- 8/9 members (vs. 3/9 at the May meeting) of the Times’ shadow MPC believe that the BoE should raise rates by 50bps at its policy meeting tomorrow, according to the Times.

FX

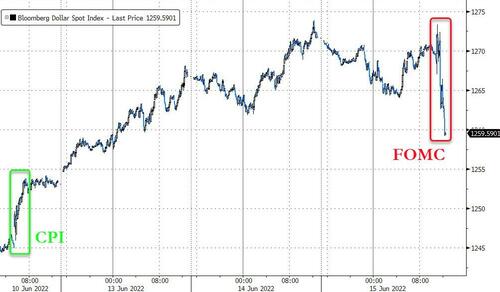

- Buck backs off from best levels into FOMC and US data awaiting confirmation of the hawkish hype or half point hike signalled pre-hot CPI; DXY slips from 105.650 peak on Tuesday into 105.380-104.700 range.

- Aussie rebounds on risk grounds and more aggressive RBA tightening calls, AUD/USD reclaims 0.6900+ status.

- Yen takes note of latest verbal intervention and Hong Kong Dollar supported by more physical HKMA buying to keep it pegged; USD/JPY sub-134.50 vs 135.50+ overnight.

- Euro extends recovery rally as ECB holds ad hoc meeting to discuss fragmenting debt markets and Wunsch contends that gradualism does not rule out larger than 25 bp moves; EUR/USD pops over 1.0500 from just below 1.0400 yesterday.

- Yuan gleans impetus from better than expected or feared Chinese industrial production and retail sales, USD/CNH nearer 6.7200 than 6.7600, USD/CNY close to 6.7100 and not far from 21 DMA at 6.6965 today.

Fixed Income

- Decent bear market retracement in debt approaching the FOMC.

- Bunds up to 143.79 at best vs new 143.25 cycle low, Gilts towards top of 112.48-111.88 band and 10 year T-note closer to 115-06 than 114-10.

- BTPs markedly outperform after near 3 full point bounce from Tuesday close in anticipation of an anti-fragmentation tool from the ECB as GC meets for crisis talks.

Commodities

- Currently, WTI and Brent are lower by circa. USD 1.00bbl but reside within comparably narrow ranges of around USD 2.00bbl vs, for instance, yesterday’s USD +6.00/bbl parameters.

- Curtailed amid COVID updates from China and Hong Kong alongside Biden’s reported push for an explanation from producers over why supply isn’t increasing.

- US President Biden has demanded an explanation from oil companies over why they are refraining from putting additional gasoline on the market and wants concrete ideas as to how they can increase supplied, according to a letter seen by Reuters.

- US Energy Inventory Data (bbls): Crude +0.7mln (exp. -1.3mln), Cushing -1.1mln, Gasoline -2.2mln (exp. +1.1mln), Distillates +0.2mln (exp. +0.3mln)

- US DoE announced contract awards and issued the fourth emergency sale of crude oil from SPR (as previously announced), in which contracts were awarded to nine including Chevron (CVX), Exxon (XOM) and Marathon Petroleum (MPC).

- Kazakhstan has capped wheat exports at 550k tonnes and wheat flour at 370k tonnes until September 30th, according to the Agriculture Ministry, via Reuters.

- Spot gold derives impetus from the USD’s retreat and is now back above USD 1820/oz but still shy of yesterday’s USD 1831/oz best and the subsequent 200-, 10- & 21-DMAs ahead at USD 1842, 1843 & 1845 respectively.

US Event Calendar

- 07:00: June MBA Mortgage Applications +6.6%, prior -6.5%

- 08:30: May Import Price Index YoY, est. 11.9%, prior 12.0%; MoM, est. 1.1%, prior 0%

- May Export Price Index YoY, prior 18.0%; MoM, est. 1.3%, prior 0.6%

- 08:30: May Retail Sales Advance MoM, est. 0.1%, prior 0.9%

- May Retail Sales Ex Auto MoM, est. 0.7%, prior 0.6%

- May Retail Sales Control Group, est. 0.3%, prior 1.0%

- 08:30: June Empire Manufacturing, est. 2.2, prior -11.6

- 10:00: April Business Inventories, est. 1.2%, prior 2.0%

- 10:00: June NAHB Housing Market Index, est. 67, prior 69

- 14:00: June FOMC Rate Decision

- 16:00: April Total Net TIC Flows, prior $149.2b

DB’s Jim Reid concludes the overnight wrap

In these crazy days for markets, I’m willing to stake my reputation that I’ve done something in the last 24 hours that no-one else reading this did. Yes, after a business trip to Europe yesterday, I watched the original Top Gun on my iPad on the plane ride home for the very first time, some 36 years after it came out. My wife wants to watch the sequel, so I thought I ought to see what all the fuss was about. She’s seen it around 20 times and always asks what I was doing in my teenage years that’s made me miss all the films of her youth. The truth is I was either studying or playing cricket or golf. Not much else. My review is that it was a decent film, but Mavericks’ courting technique doesn’t really age very well.

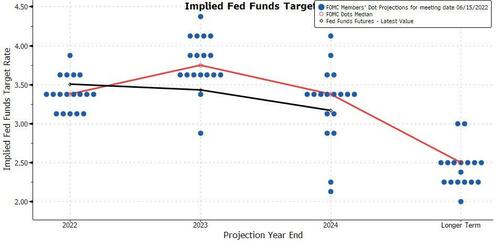

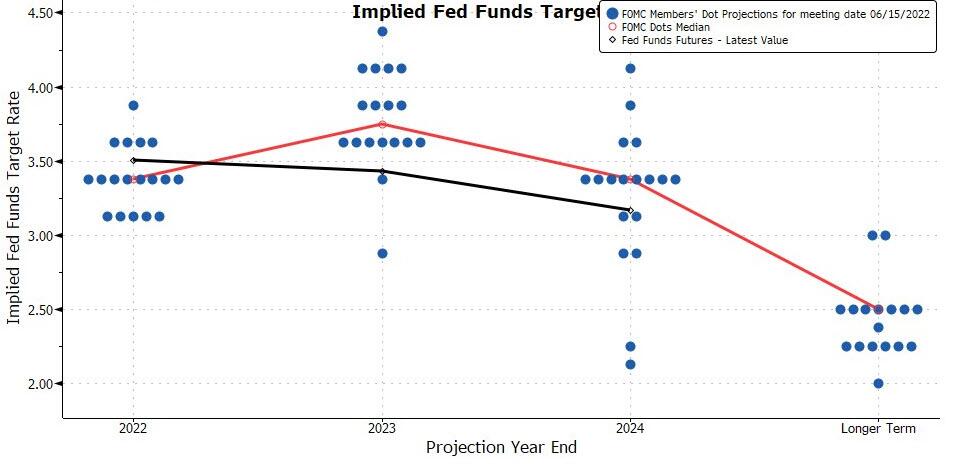

I’m not sure Maverick and Goose would have been able to get out of the tight spot that the Fed are in at the moment very easily. After the astonishing price action over the previous 2 business days, markets have settled somewhat over the last 24 hours, but overall have continued to struggle as they await today’s all-important Federal Reserve decision. Up until the CPI report last Friday, that decision seemed like a lock in favour of a second consecutive 50bp hike, not because that was the right move, but because the Fed had firmly guided us to such an outcome. The CPI report raised doubts as to whether they could hold that line over the summer, but the WSJ article on Monday night broke the levee as a 75bps move tonight is now suddenly pretty much consensus. Our economics team agrees and have now updated their previously street leading view to have a +75bp hike tonight followed by another +75bp increase in July. The team believes fed funds will reach 3.5% by the end of the year, and hit a terminal rate of 4.1% in Q1 2023, sooner than they thought before the WSJ story. See their full updated call, available here.

As we hit this big day, markets now fully price in a 75bps hike today. Indeed, 76.3bps is priced, so that actually incorporates a small risk of 100bps, something former New York Fed President Bill Dudley was openly considering yesterday, which may have contributed to the sentiment that drove the next leg of the selloff in the New York afternoon. A total of 289bps worth of rate hikes by year-end is now priced. So quite the turnaround from a few weeks back when some were even floating the strange idea of a “pause” in September. Clearly the 75bp call is mostly based on a WSJ article so we can’t be certain but you would have thought the Fed would have tried to leak out a rebuttal if that wasn’t what they wanted to guide the market towards. We will see.

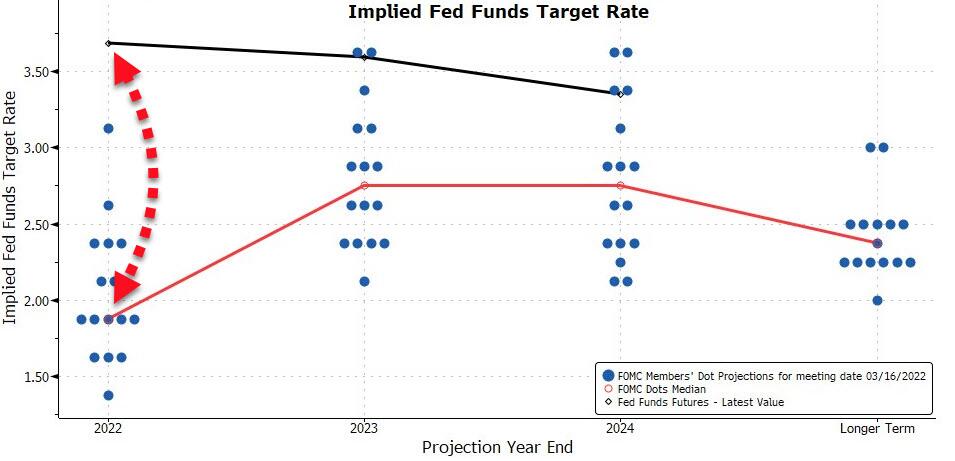

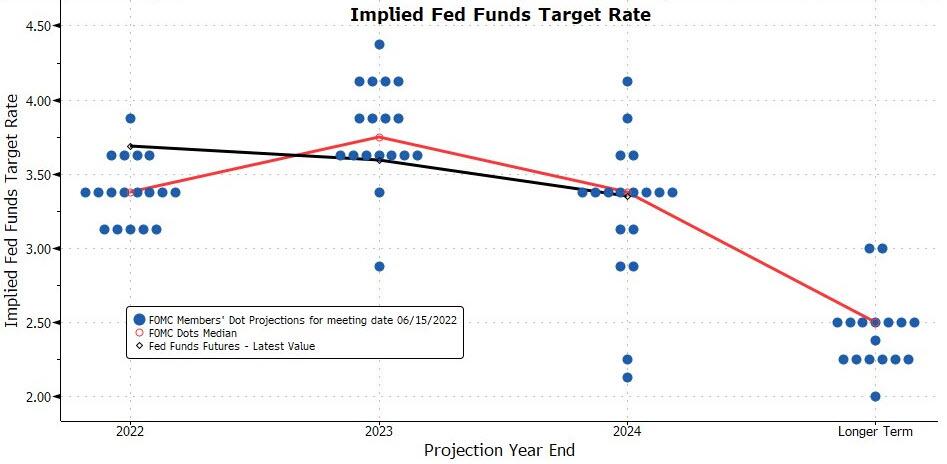

Whilst the size of any rate hike will be the focal point, today also brings the latest dot plot from the FOMC and offers an insight into the potential pace of rate hikes over the months ahead. Our US economists expect that to undergo substantial revisions, with the median dot likely rising to 3.5% and 3.8% for 2022 and 2023 respectively. Meanwhile on the economic projections, they think they’ll also show further movements towards a “softish landing”, with growth revised lower throughout the forecast, albeit stopping short of anticipating a recession.

Ahead of all that, US equities slipped to fresh lows yesterday with the S&P 500 (-0.37%) falling to its lowest closing level since January 2021. Tech stocks outperformed, in contrast to the recent trend, with the NASDAQ (+0.18%) and the FANG+ Index (+1.97%) bouncing off of recent lows. Small-caps fared less well today and the Russell 2000 (-0.39%) fell to its lowest closing level since November 2020. Over in Europe, equities similarly fell to fresh lows and the STOXX 600 (-1.26%) likewise fell to levels unseen since March 2021.

Rates sold off by a smaller magnitude than the previous two sessions (low bar to clear), but an initial rally gave way to a selloff in the European afternoon that continued to gather pace into the New York close. Yields on 10yr Treasuries were up +11.3bps to a fresh post-2011 high of 3.47%, supported by a further rise in the 10yr real yield (+13.7bps) that took it up to a 3-year high of 0.82 The 2s10s curve just about clambered out of inversion territory where it’d closed on Monday, steepening by +3.8bps to end the day at just 3.6bps. But even the Fed’s preferred yield curve measure of the near-term forward spread fell to its flattest level in 3 months, even if it’s still well out of inversion territory for now. This spread will likely collapse in the months ahead. As we go to press, yields on 10yr USTs (-4.63 bps) are moving lower to 3.42% with 2yrs -5.6bps.

Today’s focus may be on the Fed, but over at the ECB we had Isabel Schnabel of the Executive Board give a significant speech last night about policy fragmentation. Recall, one of the key takeaways from last week’s ECB meeting was the apparent lack of progress on anti-fragmentation tools, shining a spotlight on Schnabel’s remarks last night. As our European economists emphasised last week, Schnabel argued that any tool would be reactionary, that is in response to more spread widening. She did not offer new details of any potential tool last night, instead echoing President Lagarde that PEPP purchase flexibility would be used to ensure smooth policy transmission in the interim. However, Schnabel also re-emphasised the ECB’s commitment to ensure smooth policy transmission. That Schnabel, a relative hawk on the committee and one that has expressed trepidation about a new facility in the past, so willingly supported the idea of doing what was needed to support policy implementation was an important shift for the ECB. The language Schnabel used last night may support the notion that the spread widening seen to date may already be approaching levels inconsistent with smooth policy transmission. It may not take much more pressure for the ECB to act but we are still in the dark on how they will.

Earlier in the day, Dutch central bank governor Knot made some incredibly hawkish comments, saying that if “conditions remain the same as today, we will have to raise rates by more than 0.25 points” in September, and that “our options are not necessarily limited” to a 50bps move, so openly floating the potential to move by even more, which hasn’t been something discussed by the ECB to date.

European sovereign bonds sold off significantly against that backdrop, with fresh multi-year highs seen for yields on 10yr bunds (+11.9bps), OATs (+13.7bps) and BTPs (+14.9bps). Peripheral spreads hit new post-Covid highs too, with the gap between Italian and German 10yr yields widening to 241bps. And there were some significant milestones on the credit side as well, with iTraxx Crossover widening +10.4bps to a fresh 10 year high of 544bps outside of 2-months around peak covid, and in North America we saw the CDX IG spread move above 100bps in trading for the first time since April 2020, before settling back at 99.0bps.

In Asia markets are mixed with the Hang Seng (+1.44%) trading up boosted by technology stocks following the Nasdaq’s overnight gain. Likewise, stocks in mainland China are also higher in early trade with the Shanghai Composite (+1.41%) and CSI (+1.57%) edging higher as the economy showed a slightly better than expected recovery in May (see below). However, the Nikkei (-0.73%) and the Kospi (-1.54%) are trading lower, extending earlier session losses. Outside of Asia, US equity futures are reversing losses this morning with contracts on the S&P 500 (+0.38%) and NASDAQ 100 (+0.59%) trading up.

Early this morning, data released showed that China’s industrial production unexpectedly rebounded +0.7% y/y in May (v/s -0.9% expected), against a drop of -2.9% in April, whilst retail sales slid -6.7% in the period, less than -7.1% projected decline and slightly better than April’s -11.1% plunge. Meanwhile, Fixed-asset investment grew +6.2% in the first 5 months of the year (v/s +6.0% expected). Elsewhere, Japan’s core machinery orders strongly beat at +10.8% m/m in April, its fastest pace in 18 months (v/s -1.3% market consensus and +7.1% in March).

Yesterday we also heard that the Bank of Japan had bought a record ¥2.2tn in government notes through its fixed-rate operation as they seek to defend their yield curve target and keep 10-year JGB yields beneath their stated limit of 0.25%. This has continued to put pressure on the Yen however, which fell to a closing level of 135.47 per dollar yesterday, thus moving beneath its 2002 closing low of 134.71 and leaving it at levels unseen since 1998. We’re at just above 135 this morning after a small rally back. Speaking of currencies under pressure, Bitcoin fell to a 17-month low of $21,966 yesterday, having been trading around $30,000 just prior to the CPI release on Friday. This morning it’s at $21,100.

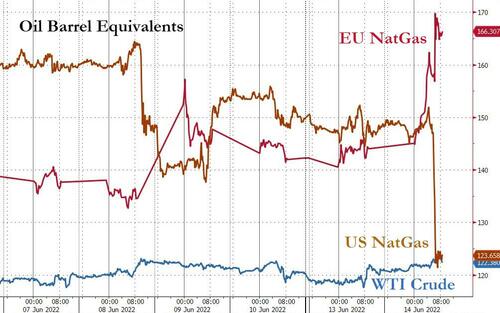

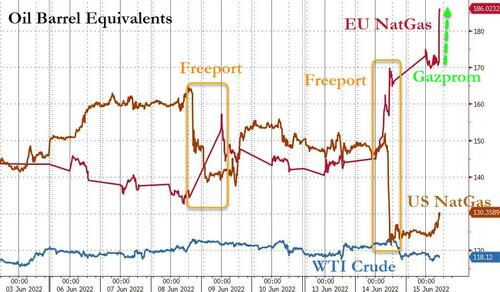

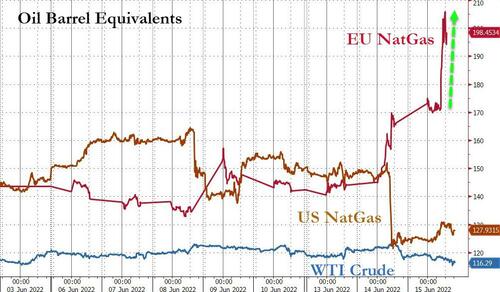

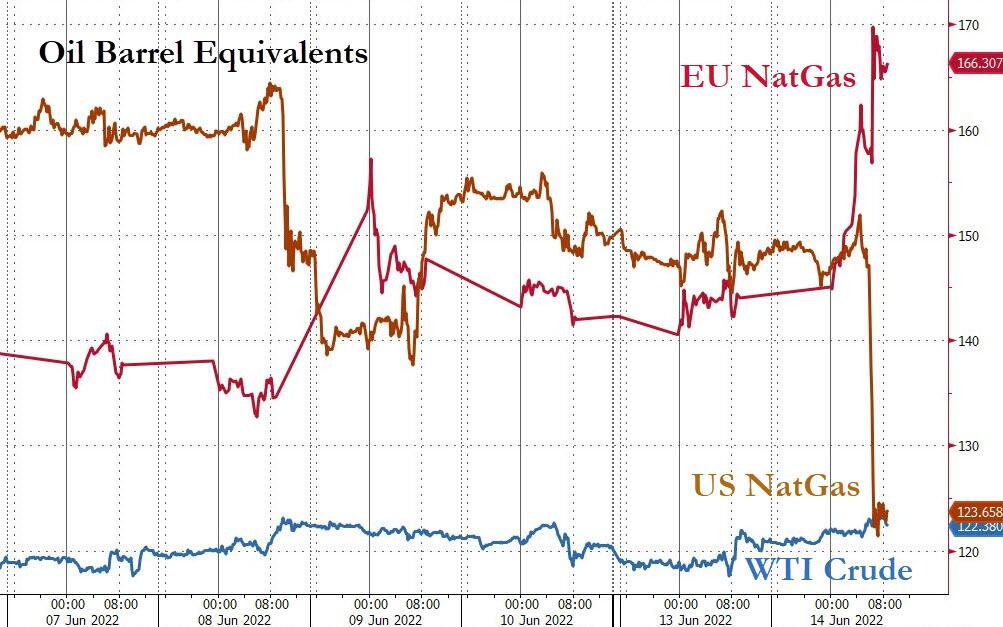

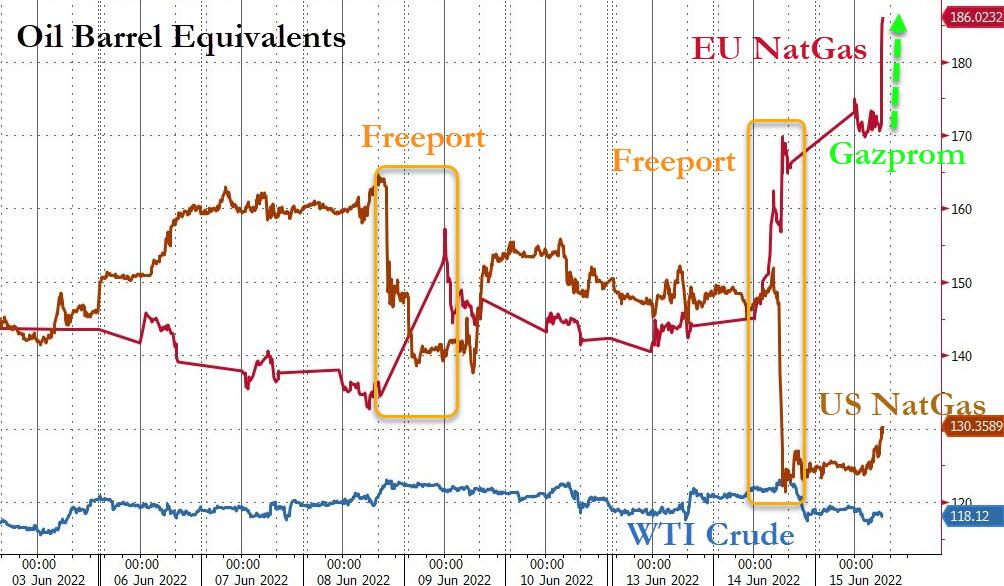

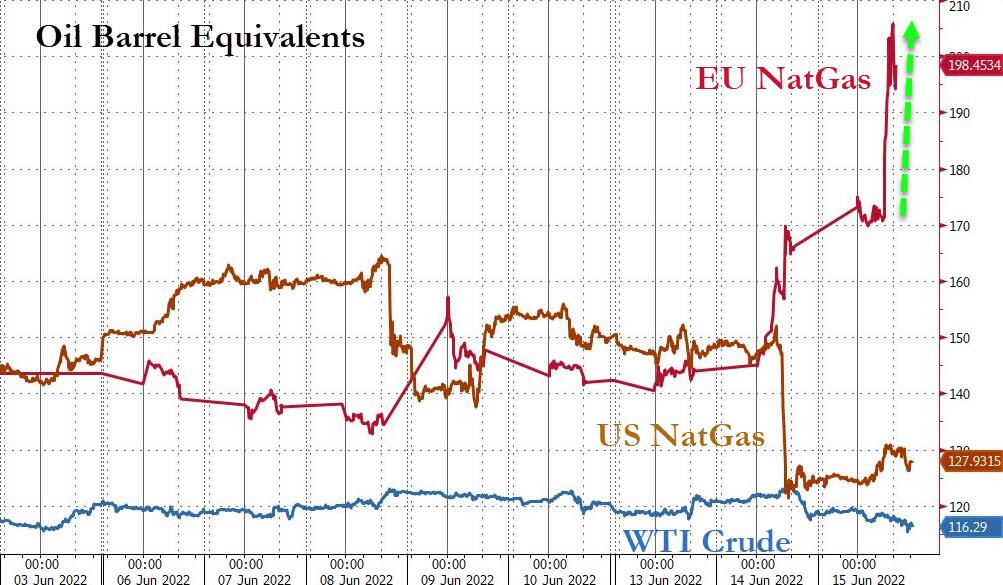

Elsewhere, brent crude and WTI futures reversed mid-day gains of near 2% to close -0.90% and -1.65% lower, respectively, following reports that the Biden Administration may pose a surtax on oil company profit margins, as another sign Biden is looking high and low for potential actions to curb oil gains into this year’s mid-terms. The big moves were seen in natural gas however, where US futures were down -16.5% and European futures were up +16.12% after the operator Freeport LNG said that they aiming for a partial resumption of operations at one of their Texas export terminals in 90 days, and that full operations wouldn’t return until late 2022. That’s a longer delay than was expected, and by keeping gas in the US led to that decline in US futures and the rise in European ones.