2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1836.45 UP $0.15

SILVER: $21.48 DOWN 14 CENTS

ACCESS MARKET: GOLD $1837.70

SILVER: $21.40

Bitcoin morning price: $20,448 DOWN 689

Bitcoin: afternoon price: $20,051 DOWN 1086

Platinum price: closing DOWN $11.15 to $931.65

Palladium price; closing DOWN $13.50 at $1867.45

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE:EXCHANGE: 0

COMEX 0

no. of contracts issued by JPMorgan: xxx/55

_____________________________________________________________________________________

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT 55 NOTICE(S) FOR 5500 Oz//0 TONNES)

total notices so far: 23,796 contracts for 2,379,600 oz (74.0155 tonnes)

SILVER NOTICES:

6 NOTICE(S) FILED 30,000 OZ/

total number of notices filed so far this month 1787 : for 8,935,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $.15

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD//

INVENTORY RESTS AT 1073.80 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 14 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV://BIG CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 3.506 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 547.166 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A VERY STRONG SIZED 1768 CONTRACTS TO 145,356 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN OI WAS ACCOMPLISHED DESPITE OUR TINY $0.09 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.09) AND WERE SUCCESSFUL IN KNOCKING OFF SOME SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 7.635 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 6 CONTRACTS OR 30,000 OZ//NEW STANDING: 9,140,000 / // V) STRONG SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -236

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTACTS for 15 days, total 11,642, contracts: 58.210 million oz OR 3.866 MILLION OZ PER DAY. (776 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 58.21 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 58.21 MILLION OZ

RESULT: WE HAD A VERY STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1768 DESPITE OUR TINY $0.09 GAIN IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 640 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S 30,000 QUEUE JUMP //NEW STANDING: 9,140,000 OZ // .. WE HAD A VERY STRONG SIZED GAIN OF 2644 OI CONTRACTS ON THE TWO EXCHANGES FOR 13.220 MILLION OZ WITH THE GAIN IN PRICE.

WE HAD 6 NOTICES FILED TODAY FOR 30,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2466 CONTRACTS TO 500,276 AND FURTHER NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -171 CONTRACTS.

.

THE FAIR GAIN IN COMEX OI CAME DESPITE OUR SMALL FALL IN PRICE OF $2.00//COMEX GOLD TRADING/TUESDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERING

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 69.26 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY’S 3900 OZ E.F.P JUMP TO LONDON //NEW STANDING: 74.911TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $2.00 WITH RESPECT TO FRIDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 3222 OI CONTRACTS 10.02 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 746 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 500,276

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3222, WITH 2461 CONTRACTS INCREASED AT THE COMEX AND 761 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3222 CONTRACTS OR 10.02 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (761) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (2461,): TOTAL GAIN IN THE TWO EXCHANGES 3222 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING AND SOME ADDITION TO SPECULATOR SHORTS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE. AT 69.26 TONNES FOLLOWED BY TODAY’S E.F.P JUMP OF 3900 OZ//NEW STANDING: 74/9611 TONNES / 3) ZERO LONG LIQUIDATION//SOME SPECULATOR SHORT COVERING//SOME SPECULATOR SHORT ADDITIONS //.,4) FAIR SIZED COMEX OI GAIN 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

54.393 CONTRACTS OR 5,439,300 OZ OR 169.18 TONNES 15 TRADING DAY(S) AND THUS AVERAGING: 3626 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAY(S) IN TONNES: 169.18 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 169.18/3550 x 100% TONNES 4.76% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 169.18 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A VERY STRONG SIZED 1768 CONTRACT OI TO 145,356 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 640 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 640 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1768 CONTRACTS AND ADD TO THE 640 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A VERY STRONG SIZED GAIN OF 2408 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 12.04 MILLION OZ

OCCURRED WITH OUR RISE IN PRICE OF $0.09 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 39.52 PTS OR 1.20% //Hang Sang CLOSED DOWN 551.25 PTS OR 2.56% /The Nikkei closed DOWN 96.76 OR 0.57% //Australia’s all ordinaires CLOSED DOWN 0.28% /Chinese yuan (ONSHORE) closed DOWN 6.7144 /Oil DOWN TO 104.55 dollars per barrel for WTI and DOWN TO 110.12 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7144 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7185: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 2461 CONTRACTS TO 500,276 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR LOSS OF $2.00 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A SMALL SIZED EFP (743 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 743 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :743 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 743 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 3222 CONTRACTS IN THAT 743 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 2461 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR FALL IN PRICE OF GOLD $2.00.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JUNE (74.911),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.911 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $2.00) AND WERE UNSUCCESSFUL IN KNOCKING OFF SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED A FAIR SIZED GAIN OF 3302 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JUNE (74.911 TONNES)…

WE HAD 2768 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3222 CONTRACTS OR 3222 OZ OR 10.02 TONNES

Estimated gold volume 82,105/// poor/

final gold volumes/yesterday 188,107 /poor

INITIAL STANDINGS FOR JUNE ’22 COMEX GOLD //JUNE 22

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 140,671.700 oz Brinks Int Delaware Malca Manfra 4266 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 55 notice(s) 5500 OZ .1717 TONNES |

| No of oz to be served (notices) | 304 contracts 30400 oz 0.9455 TONNES |

| Total monthly oz gold served (contracts) so far this month | 23,796 notices 2,379,600 OZ 74.012 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

0 customer deposits

total deposits: nil oz

4 customer withdrawals:

i) Out of Brinks 514.470 oz 16 kilobars

ii) Out of Manfra 1297.111 oz

iii) Out of Malca: 138,213.149 oz (4230 kilobars)

iv)Int Delaware 643.02 oz 20 kilobars

total withdrawal: 140,671.700 oz

ADJUSTMENTS: 7/dealer to customer/

Brinks, 10,528.121 oz

HSBC 3691.834

Int Delaware: 1639.650

JPMorgan 16,982.719 oz

Loomis: 867.077 oz

Malca 18,330.377 oz

Manfra: 19,234.420 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 359 contracts having lost 39 contracts

We had 0 notices filed on FRIDAY so we LOST 39 contracts or an additional 3900 oz will stand for gold in this very active month of June

July has a LOSS OF 27 OI to stand at 1601

August has a GAIN of 815 contracts UP to 413,632 contracts

We had 55 notice(s) filed today for NIL 550oz FOR THE JUNE 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 55 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2021. contract month,

we take the total number of notices filed so far for the month (23,796) x 100 oz , to which we add the difference between the open interest for the front month of (JUNE 359 CONTRACTS ) minus the number of notices served upon today 55 x 100 oz per contract equals 2,410,000 OZ OR 75.082 TONNES the number of TONNES standing in this active month of JUNE.

thus the INITIAL standings for gold for the JUNE contract month:

No of notices filed so far (23,689) x 100 oz+ (359) OI for the front month minus the number of notices served upon today (55} x 100 oz} which equals 2,410,000 oz standing OR 74.911 TONNES in this active delivery month of JUNE.

TOTAL COMEX GOLD STANDING: 74.911 TONNES (A STRONG STANDING FOR A JUNE ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,419,784.828 oz 75.26 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 33,507,434.664 OZ

TOTAL ELIGIBLE GOLD: 16,231,369.943 OZ

TOTAL OF ALL REGISTERED GOLD: 17,276,064.721 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 14,921,555.0 OZ (REG GOLD- PLEDGED GOLD)

END

SILVER/COMEX/JUNE 22

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,347,016.200 oz CNT Delaware Int Delaware JPMorgan Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1234,405.289 oz CNT Delaware JPMorgan |

| No of oz served today (contracts) | 6CONTRACT(S)30,000 OZ) |

| No of oz to be served (notices) | 19 contracts (95,000 oz) |

| Total monthly oz silver served (contracts) | 1809 contracts 9,045,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 3 deposit into the customer account

i) Into CNT 619,387.430 oz

ii) Into Delaware: 2044.759

iii) Into JPMorgan 612,973.100 oz

total deposit: 0 oz

JPMorgan has a total silver weight: 169,658 million oz/337.263 million =50.27% of comex

Comex withdrawals: 5

CNT 84,737.500 oz

Delaware 1056.600 oz

Int Delaware 58,516.300 oz

JPMorgan 600,331.800 oz

Manfra 602,374.000

total withdrawal 1,347,016.200 oz

adjustments: 3 dealer to customer

Brinks 35,230.510 oz

Int Delaware 167,586.840 oz

JPMorgan 69,481.240 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 71.388 MILLION OZ

TOTAL REG + ELIG. 337.375 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE OI: 25 HAVING LOST 9 CONTRACTS.

WE HAD 16 NOTICES FILED ON TUESDAY SO WE GAINED 7 CONTRACTS OR AN ADDITIONAL 35,000 OZ WILL STAND IN THIS NON ACTIVE

DELIVERY MONTH OF JUNE

JULY HAD A LOSS OF 3055 CONTRACTS DOWN TO 45,422 CONTRACTS.

AUGUST GAINED 34 CONTRACTS TO STAND AT 1016

SEPTEMBER HAD A GAIN OF 4365 CONTRACTS UP TO 81,375CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 6 for 30,000 oz

Comex volumes:35,247// est. volume today// poor

Comex volume: confirmed yesterday: 87,824 contracts ( good )

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1809 x 5,000 oz = 9,045,000 oz

to which we add the difference between the open interest for the front month of JUNE(25) and the number of notices served upon today 6 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE./2022 contract month: 1809 (notices served so far) x 5000 oz + OI for front month of JUNE (25) – number of notices served upon today (6) x 5000 oz of silver standing for the JUNE contract month equates 9,140,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

JUNE 21/WITH GOLD DOWN $2.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1075.54 TONES

JUNE 17/WITH GOLD DOWN $11.25: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.60 TONNES INTO THE GLD.///INVENTORY RESTS AT 1075.54 TONNES

JUNE 16/WITH GOLD UP $28.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.74 TONNES

JUNE 15/WITH GOLD UP $6.50/BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD////INVENTORY RESTS AT 1063.74 TONNES

JUNE 14/WITH GOLD DOWN $18.80/NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 13/WITH GOLD DOWN $41.55: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 10/WITH GOLD UP $21.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

GLD INVENTORY: 1073.80 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

JUNE 21/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.506 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 547.166 MILLION OZ//

JUNE 17/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 739,000 OZ FROM THE SLV./:INVENTORY RESTS AT 543.660 MILLION OZ/

JUNE 16/WITH SILVER UP 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 15/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 14/WITH SILVER DOWN 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 13/WITH SILVER DOWN 62 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 10.WITH SILVER UP 13 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 Z FROM THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

CLOSING INVENTORY 547.166 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg

LAWRIE WILLIAMS: Markets mixed to positive post FOMC – so far.

With U.S. markets closed on Monday for the new Juneteenth Federal holiday, to celebrate the emancipation and supposed freedom from oppression of racial minorities in the U.S., it has been difficult to yet judge the ongoing reaction from the decisions taken at last week’s FOMC meeting. To recap, up until the Friday prior, markets had been anticipating a 50 basis point Federal Funds interest rate rise in the Fed’s latest attempt to bring down inflation. Then came the release that day of the latest Consumer Price Index (CPI) data from the Bureau of Labor Statistics (BLS) which came in at a well-above-expectations 8.6% year-on-year, which many feel understates the real level.

Immediately the BLS figure was released, consensus expectations for the likely interest rate rise to be imposed at the forthcoming FOMC meeting a few days later moved up from 50 basis points to 75 basis points – some had even suggested 100 basis points. In the event the 75 basis point rise was the actual result as announced on the 15th at the end of the FOMC meeting.

One might have expected something of a stock market meltdown at such an announcement, and maybe a boost to precious metals prices, but this was not to be. Indeed, almost the reverse happened, perhaps boosted by Fed chair Jerome Powell’s subsequent presentation which served to play down some of the worst analyses. Indeed some of the anticipated fallout will have already been in the pipeline ahead of the meeting’s outcome.

Over the past couple of days since the U.S. holiday weekend, , on initial trade, stocks and bitcoin seemed to be moving higher on a surge of optimism – wholly unjustified in our opinion – while gold continued to weaken a little, although was quite volatile in its path. There has, though, been a bit of a turnaround in European trade this morning, with gold recovering and European stocks and bitcoin dipping again, but it remains to be seen whether this trend will follow through into the key U.S. markets today. We think it should as the true ramifications of the Fed’s moves sink in, but markets are fickle and prone to optimistic manipulation. Investors tend to believe what they want to believe.

There was little in Powell’s summary statement, in our opinion at least, that really promised much in the way of optimism. The Fed has an abysmal track record on predicting future inflation levels and one suspects that Powell’s suggestion that future 75 basis point increases would be unlikely should be taken with the proverbial pinch of salt. If the next CPI data release, due out on July 13th, to be followed by an FOMC meeting on the 26th and 27th, comes out at around, or higher than, June’s 8.6% year on year increase, then we would put the higher rate rise level as the more likely despite Powell’s apparent tentative insistence to the contrary.

Unless there is a swift, and seemingly at this time, unlikely, end to the Russia/Ukraine conflict, we suspect inflation will remain elevated, and possibly rise further, as the key elements in its rise – energy and food prices – are hugely impacted by the war and thus totally outside any Fed moves to try and control them. We had pointed this out ahead of the June release when we had predicted an inflation rise, contrary to mainstream and Fed optimism, and in our view the situation has not changed for the better since then. We are likely stuck with high headline inflation levels for many months yet to come.

True the year-on-year figures may start to fall from around October as it was from October last year that the big headline inflation levels started to be recorded. This will, no doubt, be seized upon by the optimists as showing that the Fed measures are beginning to take effect, but with headline inflation still likely to be excessive that will be small comfort to the consumer. Prices will remain high and whichever domestic currency you trade with will be unable to purchase what it used to. Such is inflation. It lowers the purchasing power of your cash and savings, and at the current rate these are going down fast!

Powell is predicting a ‘softish’ landing from the Fed’s moves. He has lost much of any economic forecasting credibility he may have had with his insistence for many months that any inflationary trends would be ’transitory’ and his ‘soft landing’ predictions may well be just as far off the mark. In our view the U.S., and much of the rest of the world, is heading for a recession, and a steep one at that. There is probably little the Fed, or other central banks can do to ward one off. There is a strong raft of opinion that thinks the only option that lies ahead is for the Fed, and other central banks, to return to Quantitative Easing to re-stimulate their respective economies before too long, but this has to be a recipe for ever increasing inflation – in the worst case scenario perhaps hyper- inflation and the end of the economic world as we know it.

Gold may be one of the only protectors under these circumstances, although one obviously hopes it doesn’t come to this, but it is as well to be prepared. So far though gold has not performed as expected but has shown signs of weakness in the face of rampant inflation, deteriorating economics and weaker equities, whereas we might have expected it to have performed rather better under such circumstances. But we still remain confident that its attributes in a recession-headed economy will at least lead to its role as a wealth protector come to the fore. We are not so confident on the other precious metals, though, as they are all much more dependent for their demand on growth in the global economy, which we feel may be in for a hiatus period.

22 Jun 2022

-END-

END

3. Chris Powell of GATA provides to us very important physical commentaries

Craig Hemke at Sprott Money: The ‘washed-out’ silver futures market

Submitted by admin on Tue, 2022-06-21 21:00 Section: Daily Dispatches

By Craig Hemke

TF Metals Report

via Sprott Money, Toronto

Tuesday, June 21, 2022

Recent data from the U.S. Commodity Futures Trading Commission suggests that Comex silver positioning is the most favorable since June 2019.

While this does not preclude more downside, it certainly suggests that any further price drops will be shallow.

So what we’re talking about here is the CFTC’s weekly commitment-of-traders reports that are surveyed at the Comex close each Tuesday and then reported 74 hours later, after the Comex close the following Friday. This data is therefore not made timely, nor is it suitable for trading.

However, once you track the data for years as I have, you begin to notice discernible trends that can help you spot potential price highs and lows. …

… For the remainder of the analysis:

https://www.sprottmoney.com/blog/The-Washed-Out-Silver-CoT-Craig-Hemke-June-21-2022

end

Chris Powell is certainly correct on this one:

(ChrisPowell/GATA)

After 15 years in mining he still says central banks leave gold alone

Submitted by admin on Tue, 2022-06-21 21:36Section: Daily Dispatches

9:48p ET Tuesday, June 21, 2022

Dear Friend of GATA and Gold:

Maybe it’s only what to expect from a stock-touting service, but today’s commentary by Alastair Ford, senior equities reporter for Proactive Investor in London, is disappointing all the same insofar as it comes from someone claiming 15 years of experience in the mining sector.

Ford was trying to say something nice about gold: That “given U.S. dollar strength, gold has considerably outperformed, which is another way of saying that over the past few months it has been broadly flat against a rising dollar.”

But then as a reason for gold’s respectable performance, Ford added:

“There’s no hot money in gold, and there are no central bankers monkeying with supply.”

Good grief!

“Central bankers monkeying with supply” has been the main influence on the gold price for decades now.

Has Ford never heard of the London Gold Pool, the International Monetary Fund’s gold sales, the surreptitious trading undertaken every month for its central bank members by the Bank for International Settlements, the bank’s actually advertising its secret interventions in the gold market, the Bank of England’s gold sales that were ridiculed as “Brown’s Bottom,” the March 1999 secret staff report of the International Monetary Fund explaining that central bank gold reserve accounting had to be camouflaged to conceal interventions, Federal Reserve Chairman Alan Greenspan’s admission in testimony to Congress in July 1998 that “central banks stand ready to lease gold in increasing quantities should the price rise,” and the incriminating public statements by a half dozen other central bankers?

GATA has summarized this documentation and more here —

— even as we’re sure we don’t know even half the substance of longstanding Western government gold price suppression policy.

Of course it’s easier to tout gold mining shares, as Proactive Investor does, if you don’t tell gold investors what they are up against. But telling them that central banks will not get in the way of their investments is aggressively dishonest and it hampers the exposure needed to liberate the gold market and realize full value from gold investments.

Ford’s commentary is headlined as erroneously as it could be — “Gold Proves Its Worth, Once Again, as the Only Asset Safe from the Meddling of Central Bankers” — and its posted at Proactive Investor here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //LITHIUM

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7144

OFFSHORE YUAN: 6.7185

HANG SANG CLOSED DOWN551.25 PTS OR 2.33%

2. Nikkei closed DOWN 96.76% OR 0.37%

3. Europe stocks ALL CLOSED ALL RED

USA dollar INDEX DOWN TO 104.25/Euro FALLS TO 1.0519

3b Japan 10 YR bond yield: FALLS TO. +.234/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 136.055/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.907%/Italian 10 Yr bond yield RISES to 4.03% /SPAIN 10 YR BOND YIELD RISES TO 3.03%…ALL BLOWING UP!!

3i Greek 10 year bond yield FALLS TO 3.88//

3j Gold at $1838.00 silver at: 21.49 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 & 65/100 roubles/dollar; ROUBLE AT 53.12

3m oil into the 104 dollar handle for WTI and 110 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 136.23DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9648– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0151well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

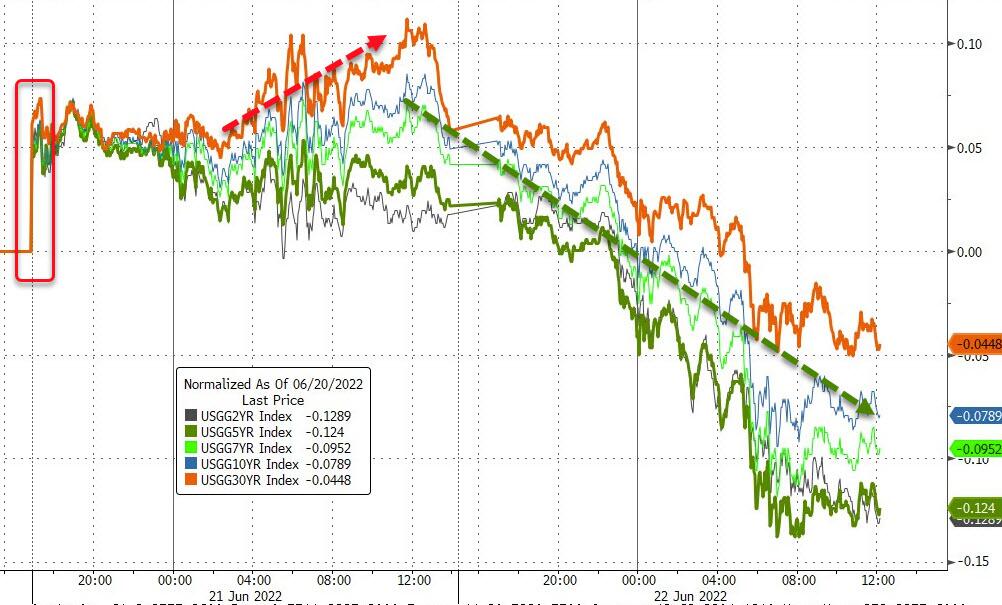

USA 10 YR BOND YIELD: 3.201 DOWN 10 BASIS PTS

USA 30 YR BOND YIELD: 3.284 DOWN 11 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.33

Futures, Oil Tumble As Attention Turns To Coming Recession, Powell Senate Testimony

WEDNESDAY, JUN 22, 2022 – 07:52 AM

Tuesday’s euphoric market mood has U-turned into sheer despair with most of yesterday’s gains gone overnight as attention turns to the coming US recession (now made official by Bill “The Fed Should Crush Donald Trump” Dudley who just published an Op-Ed “The US Economy Is Headed for a Hard Landing“) and as traders await Jerome Powell before Senate testimony. S&P 500 futures declined 1.2%, down 45 points to 3,722 while Nasdaq 100 futures were down 1.5% by 715 a.m. in New York, indicating more declines for heavyweight technology stocks, which have already been hammered by rising rates. Treasury yields and oil both slumped while the broader commodity sector tipped back toward pre-war levels, as traders increasingly price in a recession.

Optimism evaporated that policy makers can achieve a soft landing as they navigate a course of aggressive monetary tightening to tame inflation. Fed Chair Jerome Powell is expected to reinforce the commitment to fighting price pressures when he speaks in front of US lawmakers Wednesday even as a growing number of banks warn that the Fed chair is pushing Biden’s economy into a recession. Previewing Powell’s appearance before the Senate Banking Committee as part of the Fed’s semiannual Monetary Policy Report, DB economists write that they expect him to reiterate the same themes he gave at his post-meeting press conference last week, where he signaled that they’d likely be deciding between 50bps and 75bps at the July meeting. Fed funds futures are currently implying that another 75bps move is more likely, with +71.8bps currently priced in, but don’t forget that there’s still plenty yet to happen ahead of that meeting in just over a month, including the subsequent CPI release and jobs report for June, and as we found out at the last meeting, it’s not implausible that unexpected data releases throw the previous guidance off course.

“Overall, we have a very cautious outlook for equity markets and we would be sellers of all rallies,” said Marija Veitmane, senior strategist at State Street Global Markets. “We continue to see strong inflation and central banks determined to crush it, even if the price for that is economic slowdown.”

Meanwhile, fears about the economy spread to commodities, putting oil in line for a monthly loss: “Markets are flip-flopping between recession fears and inflation fears,” UBS Wealth Mgmt chief economist Paul Donovan said in a note. “Today it is recession fears.”

In premarket trading, major US technology and internet stocks were lower in premarket trading, poised to snap the two-session rising streak amid mounting concerns of a global recession. Stocks related to cryptocurrencies fell as the price of Bitcoin briefly slipped below $20,000 after rebounding strongly on Tuesday. Alibaba and other US-listed Chinese stocks pare losses in premarket trading after a Bloomberg News report that Jack Ma’s Ant may apply to become a financial holding company as soon as this month. Other notable premarket movers:

- La-Z-Boy’s (LZB US) shares jumped as much as 8.9% with KeyBanc saying that the furniture maker’s sales and EPS remain strong. The company reported adjusted earnings per share for the fourth quarter that beat the average analyst estimate.

- Precision BioSciences (DTIL US) shares jump as much as 40% in US premarket trading amid a collaboration and license agreement with Novartis effective June 15.

- Ormat Technologies (ORA US) shares fell 4.6% in postmarket trading on Tuesday after the company said it will offer $350 million aggregate principal amount of Green Convertible Senior Notes due 2027 in a private offering to institutional buyers.

- Equity Residential (EQR US) stock may be in focus as it was raised to outperform from sector perform at RBC on the view that the apartment owner is well placed to weather a downturn.

- Keep an eye on Cigna (CI US) shares as Morgan Stanley upgraded the stock to overweight from equal-weight. The brokerage also downgraded Anthem to equal-weight from overweight.

- Watch Scotts Miracle-Gro (SMG US) shares as they were downgraded to equal-weight from overweight at Wells Fargo, which said there’s “just not much to get excited about” for the stock in the second half of the year.

US equities have been roiled in the past few months amid worries that aggressive monetary tightening by the Fed would spark an economic recession. The S&P 500 is in a bear market after a rout that erased almost $2 trillion from the benchmark last week, and is tracking declines of nearly 9% in June alone. Fed Bank of Richmond President Thomas Barkin said the central bank should raise rates as fast as it can without causing undue harm to financial markets or the economy.

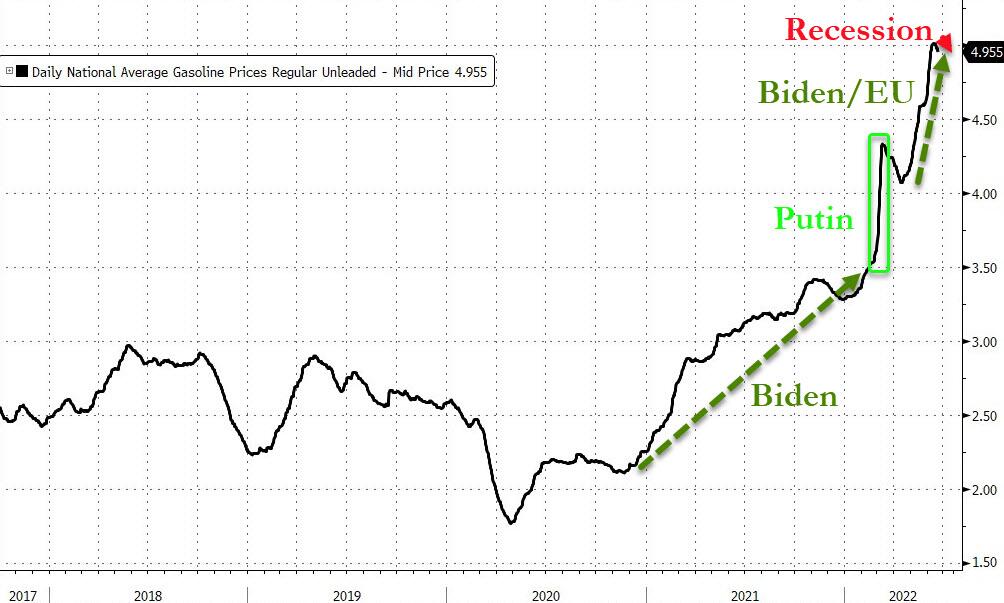

Elsewhere, Joe Biden plans call on Congress to enact a gasoline tax holiday to cool soaring pump prices and alleviate the pressure on consumers. The move is expected to do nothing at all for gas prices.

In Europe, the Stoxx 600 Index was down 1.6% after rallying for three days in a row; the Euro Stoxx 50 dropped as much as 2.3%, Italy’s FTSE MIB underperforms. The FTSE 100 outperformed as the pound weakened after UK inflation rose to a fresh four-decade high in May after broad increases in the cost of everything from fuel and electricity to food and beverages. Risk assets slumped with most European cash equity indexes erasing the week’s gains as recession fears, hot inflation data and energy concerns weigh on sentiment. Miners, energy and autos lead broad losses across all Stoxx 600 sectors. Here are the biggest European movers:

- European mining stocks sink as a selloff in iron ore worsened amid signs of weakening global demand, while steel shares were pressured by downgrades from JPMorgan. Rio Tinto dropped as much as 3.6%, Glencore -6.1%, Salzgitter -15%, ArcelorMittal -8.2%, Voestalpine -11%

- Umicore shares plunged as much as 17% after the materials technology company announced plans to spend EU5b by 2026, “meaningfully” higher capital expenditure than Jefferies had expected.

- Saipem shares tumble as much as 19% after the company set terms for a EU2b capital hike, offering about 2 billion new shares at EU1.013. The subscription period will run from June 27 through July 11, with the final results to be announced on July 15, according to terms seen by Bloomberg.

- Samhallsbyggnadsbolaget i Norden and Swedish real estate peers added to months of declines as European equities resumed their selloff, with fresh concerns about the possibility of recession. SBB falls as much as 13%, Sagax -6%, Fabege -4%, Castellum -3.7%

- Kone shares drop as much as 7.5% after the Finnish elevator manufacturer was downgraded at Goldman Sachs and Berenberg, which both cited headwinds from China and the impact of slowing economic growth.

- Energy stocks are among the worst-performing sectors as oil slumps amid concerns about the US economy, while the Biden administration is set to step up its fight against higher gasoline prices. Shell declines as much as 4.6%, TotalEnergies -4.6%, Repsol -5.1%

- Accor shares drop as much as 3.8% after the hospitality company said it entered into exclusive negotiations to sell a 10.8% stake in Ennismore for EU185m.

- JD Sports shares gain as much as 5.2%. The company reported FY results that are in line overall with consensus expectations, and the market should be reassured that the sneaker seller’s recent performance is still on track, according to RBC.

- NatWest shares gain as much as 4% after the stock was raised to buy from hold at Jefferies, which said its re-rating potential is now more obvious. The UK government also extended its plan to sell more of its stake in the group by a year.

Earlier in the session, Asian stocks resumed their slide Wednesday as renewed fears of a crackdown hit Chinese technology shares. The MSCI Asia Pacific Index slipped as much as 1.7%, cutting short a rebound in the previous session. TSMC, Alibaba and Tencent were the biggest drags, with a gauge of Chinese tech firms in Hong Kong falling more than 4%. Shares of online drug sellers slumped on a report that Beijing may ban third-party platforms from offering medicines over the internet.

Elsewhere, a sub-gauge on the region’s information tech companies headed for the lowest close since September 2020 amid growing worries over a global recession. South Korea’s benchmark slumped 2.7% as the tech-heavy market continued to face selling pressure amid foreign outflows. The Asian stock benchmark is hovering near a two-year low as the prospect of a slowdown in the US driven by aggressive interest-rate hikes unsettle investors. Tesla Inc. Chief Executive Officer Elon Musk said Tuesday that a recession in the US looks likely in the near future, adding to the growing drumbeat of warnings. “Markets are still looking for the catalyst for a more sustained rebound as headwinds surrounding tightening financial conditions,” said Jun Rong Yeap, a market strategist at IG Asia Pte, adding that gains from any technical rebound may be capped by some wait-and-see sentiments. After falling more than 18% this year, a technical indicator is suggesting the MSCI’s Asian benchmark has reached oversold levels and may be poised for a reprieve. Investors will now shift their focus to Federal Reserve Chair Jerome Powell’s testimony on monetary policy to Congress later Wednesday, which may provide further clues on inflation and rates outlook.

Indian markets snapped a two-day advance as growing concerns of slowing global growth potentially leading to a recession dragged down world equity markets. The S&P BSE Sensex dropped 1.4% to 51,822.53 in Mumbai, while NSE Nifty 50 Index fell by an equal measure. Reliance Industries, a major drag on both the key gauges, declined 3%, its biggest plunge since May 9. All of the 19 sectoral indexes compiled by BSE Ltd. slipped, led by a measure of metal companies. All but four of 30 companies in the Sensex declined. All major stock markets, including Asia, traded lower as investors fear that aggressive monetary tightening moves by global central banks could lead to an economic downturn. “Traders are advised to keep a hedge position, while investors should focus on stock selection,” according to Religare Broking analyst Ajit Mishra. The monsoon’s progress, a correction in oil prices and currency movements will be important factors to watch for the Indian stock market’s outlook, he said.

In rates, havens were re underpinned with major yield curves bull-steepening. A Treasury rally was led by the front-end of the curve, following wider gains across gilts after UK May inflation matches median estimates, trimming expectations for more aggressive BOE rate hikes. US yields richer by 10bp-6bp across the curve with front-end-led advance steepening 2s10s by ~2bp, 5s30s by ~4bp; 10-year yields around 3.20%, richer by nearly 8bp on the day, while gilts outperform by additional 6bp in the sector. Short-dated gilts outperform, richening ~13bps in 2s after another hot inflation print. Gilts lead bunds, Treasuries higher, with traders pulling back from wagers on three 50 basis-points hikes by year end after UK inflation accelerated in line with estimates in May. MPC-dated OIS rates pare back some of the more aggressive pricing seen in recent days. German 10y yields fall 10bps to near 1.67%, Treasury 10-year yield eases ~6bps to near 3.22% ahead of Fed Chair Powell’s semi-annual testimony on monetary policy. Peripheral spreads widen, with long-dated BTPs underperforming.

In FX, early in the session we saw a push toward the dollar, which subsequently was partly faded, but in any case it snapped two days of losses to rise by around 0.2% and the greenback advanced versus all of its Group-of-10 peers apart from the yen. JPY and CHF were the strongest performers in G-10 FX, NZD and AUD underperform. Antipodean currencies and the Norwegian krone were the worst performers and each of them fell by more than 1% against the greenback. The euro traded near $1.05 after dropping to a day low of 1.0469 in early European trading. The yen rebounded after making a fresh multi-decade low versus the greenback. The yen not only held the lead in short-term realized volatility, but traders also bet that it won’t lose its crown any time soon. Demand for low-delta exposure in the Japanese currency is by far the highest among the Group-of-10 peers, with Antipodean and Scandinavian currencies trailing.

In commodities, West Texas Intermediate tumbled to $104 a barrel, with prices falling alongside other raw materials including copper. WTI sunk as much as 5.7% before recovering back above $104. Base metals trade poorly; LME tin falls 4.9%, underperforming peers. Spot gold falls roughly $8 to trade near $1,825/oz. Concerns about a broad economic slowdown are eclipsing the fallout from the war in Ukraine and signs of still-tight supply.

Bitcoin is pressured and briefly dipped again below the USD 20k mark, to a trough of USD 19.95k. Though, it remains someway from last week’s USD 17.5k low.

Looking at the day ahead now, and the main highlight will be Fed Chair Powell’s testimony before the Senate Banking Committee. Other central bank speakers include the Fed’s Barkin, Evans and Harker, as well as BoE Deputy Governor Cunliffe. Otherwise, data releases include UK and Canadian CPI for May, as well as the European Commission’s preliminary consumer confidence indicator for the Euro Area in June.

Market Snapshot

- S&P 500 futures down 1.7% to 3,702.50

- STOXX Europe 600 down 1.6% to 401.86

- MXAP down 1.7% to 156.08

- MXAPJ down 2.3% to 517.35

- Nikkei down 0.4% to 26,149.55

- Topix down 0.2% to 1,852.65

- Hang Seng Index down 2.6% to 21,008.34

- Shanghai Composite down 1.2% to 3,267.20

- Sensex down 1.2% to 51,918.86

- Australia S&P/ASX 200 down 0.2% to 6,508.54

- Kospi down 2.7% to 2,342.81

- German 10Y yield little changed at 1.69%

- Euro down 0.2% to $1.0509

- Brent Futures down 3.8% to $110.24/bbl

- Brent Futures down 3.9% to $110.18/bbl

- Gold spot down 0.4% to $1,825.23

- U.S. Dollar Index up 0.23% to 104.67

Top Overnight News from Bloomberg

A more detailed summary of Global Markets courtesy of Newsquawk

Asia-Pac stocks were subdued after the risk-on mood from Wall Street waned overnight amid pressure in commodities and with global markets lacking any fresh macro catalysts. ASX 200 pared early gains as resilience in energy and defensives was offset by losses in tech and financials. Nikkei 225 was indecisive after the Japanese currency bounced off its weakest level since 1998. Hang Seng and Shanghai Comp. were subdued amid ongoing COVID woes as Macau closed most public services through to Friday and with the Chinese city of Zhuhai also shutting entertainment venues in some areas, while there was some encouragement for the property sector with Chinese property developers planning to meet with banks regarding relief measures in July.

Top Asian News

- Chinese property developers are planning to meet with banks regarding relief measures in July, according to Shanghai Securities News.

- Chinese Premier Li Keqiang’s struggle to revive China’s economy under the zero-Covid policy championed by President Xi Jinping has spurred rumours of rifts between the country’s top two leaders and considerable speculation over succession plans, according to SGH Macro Advisors.

- BoJ April meeting minutes stated board members agreed on no change in the BoJ’s stance of taking additional easing steps as needed and a member noted that rising raw material costs would hurt the economy so they must keep powerful monetary easing. Furthermore, it was stated that Japan’s monetary policy challenge is to address too-low inflation, unlike in western economies, while a member said it is inappropriate to change the monetary policy stance as Russia’s invasion of Ukraine added to the downside risks for Japan’s economy.

European bourses are subdued, Euro Stoxx 50 -1.9%, as Tuesday’s positivity waned in the APAC session as commodities slipped in relatively limited newsflow. Unsurprisingly given this dynamic, the Basic Resources and Energy sectors are the European laggards, amid broader cyclical pressure. Stateside, futures are in-fitting with the above action, ES -1.4%, where participants are awaiting the first session of testimony from Chair Powell, newsquawk primer available here. Ant Group is reportedly to apply, as soon as this month, for a key financial license, via Bloomberg citing sources. Toyota (7203 JT) expects global vehicle production in July to be around 800k. China’s CPCA says domestic car rales rose 39% in the week to June 13th Y/Y, +55% M/M, via Reuters.

Top European News

- UK PM Johnson is of the view that the government must win its battle with the rail unions and is prepared for the stand-off to last months, according to The Times.

- Italy is reportedly preparing EUR 3bln of aid to curb energy bills, according to la Repubblica

- Italian Foreign Minister Di Maio quit the 5-Star Movement (5SM) to set up a new group, according to Reuters.

FX

- Dollar regains bullish momentum on risk dynamics ahead of Fed testimony; DXY on a firmer footing, but capped ahead of 105.000 within 104.950-430 range.

- Yen also in demand as a safe haven as sentiment sours, USD/JPY reverses course from around 136.71 to sub-136.00 at one stage.

- Kiwi and Aussie undermined by risk-off mood, with latter also hampered by heavy decline in iron ore; NZD/USD hovers above 0.6250 and well below 1bln option expiries at 0.6300, AUD/USD capped around 0.6900.

- Loonie, Nokkie and Peso ruffled by collapse in WTI and Brent crude, USD/CAD rebounds towards 1.3000, EUR/NOK tests 10.5000 and USD/MXN straddles 20.1800.

- Euro holds around 1.0500 and 10 DMA close by amidst hawkish ECB vibe, Pound pivots 1.2200 after somewhat mixed UK inflation data.

Central Banks

- ECB’s de Guindos says he expects inflation to ease after the summer but stay near current levels in the coming months; Governing Council is yet to discuss details of the anti-fragmentation tool. New tool should be different from the prior OMT tool as the circumstances are different, will also differ from APP and PEPP.

- Norwegian Gov’t names Paal Longva as Deputy Norges Bank chief.

Fixed Income

- Bonds bounce firmly as risk sentiment turns bearish again on global inflation and recession concerns.

- Bunds up to 144.87 before fading after a reasonable 2038 German auction.

- Gilts top out at 111.89 and largely ignored mixed UK inflation metrics vs consensus.

- 10 year T-note hovers closer to 116-19 overnight peak than 115-28+ trough pre-Fed chair Powell and 20 year supply plus other Fed speakers.

Commodities

- WTI and Brent are, alongside broader commodities, pressured with fresh catalysts somewhat thin and focused on known themes.

- Currently, they are lower by over 4% on the session and ahead of Biden’s announcement on gas prices; though, if implemented, such measures could serve to push demand and ultimately prices higher.

- US President Biden will deliver remarks on gas prices at around 14:00EDT/19:00BST on Wednesday and will call on Congress to implement a suspension to the federal fuel tax.

- Subsequently, multiple Democratic sources said that the effort to to suspend the federal gas tax for three months stands almost no chance of passing, according to Politico.

- IEA warns Europe to prepare for a complete shutdown of Russian gas exports and that governments should keep ageing nuclear plants open and take other contingency measures, according to FT.

- World Steel says global steel output -3.5% Y/Y in May at 162.7mln tonnes (prev. -5.1% Y/Y in April); China crude steel output -3.5% Y/Y to 96.6mln tonnes (prev. -5.2% Y/Y in April).

- Spot gold is softer in-line with other metals, though the magnitude is more contained given its haven allure; broader action that sees LME Copper clipped despite the expected commencement of Chile strike action.

US Event Calendar

- 07:00: June MBA Mortgage Applications, prior 6.6%

Central Bank Speakers

- 09:00: Fed’s Barkin Speaks to West Virginia Chamber of Commerce

- 09:30: Powell Delivers Semi-Annual Testimony Before Senate Panel

- 12:00: Fed’s Barkin Speaks to the Federal City Council

- 12:50: Fed’s Evans Discusses Economic Outlook

- 13:30: Fed’s Harker and Barkin Discuss the Economic Outlook

DB’s Jim Reid concludes the overnight wrap

Whilst the question of whether we’re about to face a recession is still dominating markets, risk assets posted a sharp rebound yesterday as the US got back from holiday. In fact by the close of trade, the S&P 500 (+2.45%) had put in its strongest daily performance in nearly a month, with every sector higher on the day and energy (+5.13%) doing most of the legwork. Even though the chart book showed that before yesterday the S&P was on course for the worst H1 since 1932 we did show in the CoTD (link here) that the top 5 H1 declines over the last 90 years were all followed by strong H2 performance. Before you think it’s safe to come out from behind the sofa, S&P futures are around -1% lower this morning as the recession narrative makes a bit of a comeback. European futures are indicating that yesterday’s gains (STOXX 600 +0.35%) will be eradicated which could end a three day winning streak. Oil prices are lower overnight with Brent Crude futures weakening -3.23% to $110.95/bbl while WTI futures are down -4.69% at $105.46/bbl amid a push by US President Joe Biden to bring down soaring fuel costs by calling for a temporary suspension of the 18.4-cents a gallon federal tax on gasoline. The demand destruction narrative is making a comeback in Asia as well.

Today’s big event is Fed Chair Powell’s appearance before the Senate Banking Committee as part of the Fed’s semiannual Monetary Policy Report that they deliver to Congress. According to our US economists, they expect him to reiterate the same themes he gave at his post-meeting press conference last week, where he signalled that they’d likely be deciding between 50bps and 75bps at the July meeting. Fed funds futures are currently implying that another 75bps move is more likely, with +71.8bps currently priced in, but don’t forget that there’s still plenty yet to happen ahead of that meeting in just over a month, including the subsequent CPI release and jobs report for June, and as we found out at the last meeting, it’s not implausible that unexpected data releases throw the previous guidance off course.

With all that to look forward to, Treasuries built on their selloff from last week, with the 10yr yield up +4.9bps to 3.27% as it echoed the higher yields we’d seen in Europe the previous day. In Asia, US 10yr yields (-1.89 bps) have dipped back down to 3.25%. They haven’t had much in the way of Fedspeak to go off over the last 24 hours, although Richmond Fed President Barkin (a non-voter this year) said he “didn’t have a problem” with Powell’s guidance for the decision next month, and that he was in favour of the 75bps hike they did. Those moves in Treasuries also led to a steepening in the curve, with the 2s10s slope up +3.4bps to 7.2bps as they edged slightly further away from the inversion territory that they’ve briefly fallen into twice this year now. In Europe there was more of a divergence between core and peripheral yields however, and those on 10yr bunds (+2.2bps) closing at a post-2014 high, just as those on BTPs fell by -1.2bps.

Some of the most significant news over the last 24 hours has been on the FX front, where the Japanese Yen fell to a fresh low for the 21st century of 136.71 per US Dollar this morning before bouncing back to 136.20 as I type. You’ve got to go all the way back to 1998 for the last time the currency was trading at a weaker level though. Prime Minister Fumio Kishida did not seem too concerned about BoJ monetary policy divergence and the impact on weakening the yen, saying in a debate policy needed to remain easy, perhaps lending more political support to the BoJ’s policies.

Stocks across Asian markets are trading lower this morning, with the Kospi (-1.89%) the largest underperformer followed by the Hang Seng (-1.26%) after a two-day winning streak earlier this week. Markets in mainland China are also sliding with the Shanghai Composite (-0.33%) and CSI (-0.62%) both weak. Elsewhere, the Nikkei (+0.04%) gave up its early gains, hovering just above the flatline as I type. Bitcoin is at $20,332 in Asian trading.

Here in the UK, gilts underperformed their counterparts elsewhere in Europe following remarks from BoE Chief Economist Pill that they would act “more aggressively” if required. In response, 10yr gilt yields rose +5.0bps to reach a fresh post-2014 high of 2.65%. Overnight index swaps are continuing to price in 50bp moves by the BoE at the next 3 meetings, with a path that would leave Bank Rate above 3% by year-end.

There were also reports that former Italian Prime Minister Giuseppe Conte was considering leaving Mario Draghi’s coalition. While Draghi’s party would still likely retain a majority in both chambers of Parliament, it would leave a very narrow path to push through legislation to fix the economy or to resist dissent from coalition members – a theme all too familiar to Senate Democrats in the US.

There wasn’t much in the way of data yesterday, although US existing home sales fell broadly as expected to an annualised rate of 5.41m in May (vs. 5.40m expected), which is their lowest level since June 2020 as the numbers were recovering after the initial wave of the pandemic.

To the day ahead now, and the main highlight will be Fed Chair Powell’s testimony before the Senate Banking Committee. Other central bank speakers include the Fed’s Barkin, Evans and Harker, as well as BoE Deputy Governor Cunliffe. Otherwise, data releases include UK and Canadian CPI for May, as well as the European Commission’s preliminary consumer confidence indicator for the Euro Area in June.

WEDNESDAY /TUESDAY NIGHT

SHANGHAI CLOSED DOWN 39.52 PTS OR 1.20% //Hang Sang CLOSED DOWN 551.25 PTS OR 2.56% /The Nikkei closed DOWN 96.76 OR 0.57% //Australia’s all ordinaires CLOSED DOWN 0.28% /Chinese yuan (ONSHORE) closed DOWN 6.7144 /Oil DOWN TO 104.55 dollars per barrel for WTI and DOWN TO 110.12 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7144 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7185: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

3c CHINA

CHINA/HONG KONG

Troublesome for Hong Kong as the peg is starting to splinter. The culprit: the strong dollar against a much weaker HK dollar

(zerohedge)

HKMA Is Blowing Billions To Defend Dollar Peg

TUESDAY, JUN 21, 2022 – 06:40 PM

The Hong Kong Dollar dropped to its weakest against the US Dollar this morning since April 2018. This is a major problem for the Hong Kong Monetary Authority (HKMA) because, as a reminder for some, the Hong Kong Dollar (HKD) is pegged to a tight band of between 7.75 and 7.85 versus the U.S. dollar.

And today saw the HKD break below the lower bound of the peg, trading down to 7.8502/USD at its lows…

The main culprit behind the local currency’s slump is the carry trade which has been reignited by The Fed hiking rates and potential capital flight out of China/HK.

This is an arbitrage, where traders take advantage of differences in prices, selling a low-yielding product (the Hong Kong dollar) to buy a high-yielding product (the US dollar). In this case, the price difference is between the local borrowing cost known as the Hong Kong interbank offered rate (Hibor) and the US borrowing cost known as the Libor.

Simply put, traders are borrowing against the low Hibor, selling the Hong Kong dollar to buy the US currency for investments in high-yielding US assets. The difference between the two is widest since March 2019… and that is pressuring the HKD against its lower peg bound.

As more traders pile on to the carry, more pressure is placed on the Hong Kong dollar, causing it to weaken further against the US currency. As the chart above shows there has been some shift in the carry-trade-pressure since HKMA has stepped in.

Nevertheless, HKMA is forced to step in and as CNBC reported, HKMA’s Chief Executive Eddie Yue said last month that as it intervenes and funds flow out of Hong Kong’s system, local rates should rise, removing the incentive for market players to conduct “carry trades”, and hence keep the Hong Kong dollar trading within its band.

“All these are normal operations in accordance with the design of the Linked Exchange Rate System,” he said.

However, the size of the flows are starting to become significant… and are having less impact. According to HKMA, its aggregate balance will decrease to about HK$241.9 billion on June 23 (from HK$338 billion in May before the interventions began again).

That is almost HK$100 billion in reserves and The Fed’s plan to hike rates (as many as twelve more times this year) will do nothing to help ease the situation (especially since China will not be tightening its policy anytime soon) – meaning any USDs sold in defense of the weaker HKD will be battling global carry trade flows driven by The Fed’s tightening.

As we have detailed previously, China currently has a dilemma because it has to pick either to hike, and avoid capital flight, or cut and remain competitive with Japan, whose collapsing JPY means chinese exports are getting priced out of global markets.

The fund still has plenty of ammo to fight the carry trade pressure (for now) as we note the aggregate balance dropped to around HK$50 billion in 2019 after the last series of HKMA interventions to stop the currency weakening.

In 2018, as the HKD plunged on the same carry flow, the HKMA CEO reassured the public “Stay calm on the weakening of the Hong Kong dollar.” So far no such warning has been issued this time.

end

Chinese lockdowns and heavy rains eased the coal shortages in April and May

(zerohedge)

China’s Lockdowns And Heavy Rains Ease Coal Shortage

TUESDAY, JUN 21, 2022 – 09:40 PM

By John Kemp, senior energy analyst at Reuters

China’s electricity generation experienced rare declines in April and May compared with the same months a year earlier as lockdowns imposed to stop the spread of the coronavirus curbed consumption.

But slower consumption growth coupled with heavy rains across southern provinces, which has boosted hydro generation to a record high, has accelerated replenishment of coal inventories after shortages in 2021.

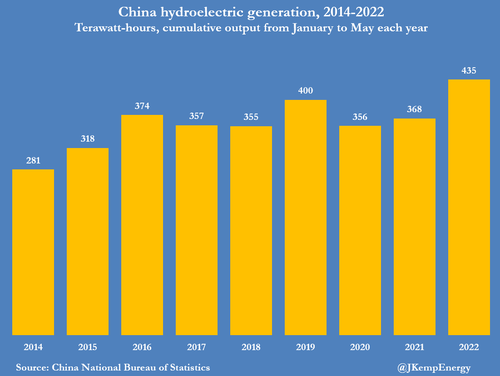

As a result, the coal supply situation is likely to be much more comfortable heading into the winter of 2022/23 than it was ahead of winter 2021/22. Generation from all sources was down 3%-4% in April and May compared with the same months in 2021, data from the National Bureau of Statistics (NBS) showed.

Generation has declined year-on-year in only 12 of the last 131 months; this was the first back-to-back decline since the first wave of the epidemic in 2020, illustrating the impact lockdowns have had on the economy.

Output in the first five months as a whole totalled 3,248 billion kilowatt-hours (kWh), an increase of just 71 billion kWh (2.2%) from the same period in 2021. Nearly all of the increase came from hydro-electric generators, which boosted output by 66 billion kWh compared with 2021.

There were also increases in generation from wind farms (+49 billion kWh), solar farms (+19 billion kWh) and nuclear units (+7 billion kWh). By contrast, output from thermal units, nearly all of which burn coal, declined by 71 billion kWh compared with the same period in 2021.

Southern Rainfall

Hydro output in the first five months totalled 435 billion kWh, up from 368 billion kWh in 2021, surpassing the previous seasonal record of 400 billion kWh in 2019.

The surge in hydro generation has been driven by the unusually heavy rainfall which has lashed southern China since the start of the year.

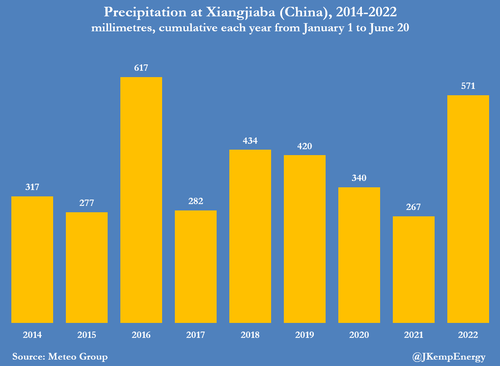

In some parts of southern China, rainfall has been the heaviest for 60 years (“Southern China hit by severe rains, floods as ‘dragon boat water’ peaks”, Reuters, June 21).

The Ministry of Water Resources has issued flood alerts across most southern provinces since the start of June (“China launches level-IV emergency response for rain in southern areas”, MWR, June 13).

In response, top officials from the central government have been supervising massive releases from the upstream dams to manage flood risk in the region’s major river systems.

For example, total precipitation at Xiangjiaba on Jinsha River, at the border of Yunnan and Sichuan provinces, and the site of one of the country’s mega-dams, has been more than 50% higher than the average in 2014-2021.

Cumulative precipitation at Xiangjiaba so far this year has been 571 millimetres, up from 267 at the same point in 2021, and the highest since 2016.

Xiangjiaba’s massive generating station has installed capacity of more than 6 Gigawatts and sends power through a high-voltage transmission link to Shanghai.

Torrential rainfall has allowed hydro-electric generators across southern China to ramp up output earlier this year and should enable them to sustain it at a higher level for longer, saving coal.

More output from hydro plus wind, solar and nuclear is in turn relieving pressure on thermal generators and should allow them to accumulate coal stocks faster ahead of next winter.

Since the start of the year, the central government has pressed both coal mining companies and power generators to increase stocks at power plants to prevent a re-run of last year’s shortages.

The slowdown in electricity consumption and boost in hydro and other alternatives has made that policy far more effective and should reduce the risk of power rationing later in the year.

4/EUROPEAN AFFAIRS//UK AFFAIRS/

EUROPEAN/POWER

Prices spike as the heat dome throughout Europe is straining the grid

(zerohedge)

European Power Prices Spike As Heat Dome Strains Grid

WEDNESDAY, JUN 22, 2022 – 02:45 AM

European day-ahead power prices continue to soar for the third day due to an early-season heat wave driving up cooling demand, lack of renewable energy generation, declining nuclear power, and soaring natural gas costs.

Large swaths of Europe over the weekend experienced temperatures above 100 degrees Fahrenheit (38 Celsius). The hottest temperatures were from Spain to Germany to France.

Bloomberg notes power grids were under stress as wind generation in Germany and Italy plunged, forcing the need to increase the capacity of fossil fuel power generators to make up for the lost power. This placed a bid under electricity prices as the cost to generate power soars because of tightening supplies due to declining Russian flows.

“Already high gas prices, combined with low wind output will require less efficient, higher cost gas plants to fire up, pushing up prices,” BloombergNEF’s Andreas Gandolfo said.

Day-ahead power prices in France traded at 383.14 euros ($404.08) a megawatt-hour, up more than 64% from last week.

Besides tight fossil fuel supplies and a lack of renewable power from Germany and Italy, half of France’s 56 nuclear reactors are offline. France was the biggest net exporter of power last year, supplying many European countries.

French nuclear power is needed when renewable energy is lacking. Also, Brussels’ drive for net-zero carbon emissions and weening off Russian fossil fuels has made the energy crisis on the continent worse.

To avert a more profound crisis, German Vice-Chancellor and Economy Minister Robert Habeck said Sunday that the country is increasing coal generation to increase power output.

The decision comes just days after Russian gas company Gazprom announced that it was reducing supplies through the Nord Stream 1 pipeline for “technical reasons.”

Meanwhile, the Netherlands is following Germany to increase coal-fired power station output to prevent an energy crisis (Greta Thunberg isn’t going to be happy about this).