by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1708.40 DOWN $28.75

SILVER: $18.36 DOWN 88 CENTS

ACCESS MARKET:

GOLD $1710.75

SILVER: $18.44

Bitcoin morning price: $19,716 UP 13

Bitcoin: afternoon price: $20.676. UP 973

Platinum price: closing DOWN $16.30 to $843.65

Palladium price; closing DOWN $125.70 at $1914.80

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JULY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,734.200000000 USD

INTENT DATE: 07/13/2022 DELIVERY DATE: 07/15/2022

FIRM ORG FIRM NAME ISSUED STOPPED

323 H HSBC 93

657 C MORGAN STANLEY 1

661 C JP MORGAN 360 316

690 C ABN AMRO 60

800 C MAREX SPEC 3

880 C CITIGROUP 12

905 C ADM 1

TOTAL: 423 423

MONTH TO DATE: 4,893

no. of contracts issued by JPMorgan: 316/423

_____________________________________________________________________________________

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT 423 NOTICE(S) FOR 482300 Oz//1.3157 TONNES)

total notices so far: 4893 contracts for 489300 oz (15.219 tonnes)

SILVER NOTICES:

111 NOTICE(S) FILED 555,000 OZ/

total number of notices filed so far this month 2860 : for 14,300,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $28.75

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROMTHE GLD///

INVENTORY RESTS AT 1019.79 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 88 CENTS

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 830,000 OZ FROM THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 513.671 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 2151 CONTRACTS TO 144,410 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GAIN IN OI WAS ACCOMPLISHED WITH OUR $0.24 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.24) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS AS WE HAD A STRONG GAIN OF 2501 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A POOR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.220 MILLION OZ FOLLOWED BY TODAY’S 720,000 OZ QUEUE JUMP / // V) STRONG SIZED COMEX OI GAIN

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -39

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTACTS for 9 days, total 8197 contracts: 40.535 million oz OR 4.503 MILLION OZ PER DAY. (910 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 40.535 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 40.535 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2151 WITH OUR $0.24 GAIN IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 350 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A POOR INITIAL SILVER OZ STANDING FOR JUNE. OF 15.22 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 720,000 OZ // .. WE HAD A STRONG SIZED GAIN OF 2501 OI CONTRACTS ON THE TWO EXCHANGES FOR 12.505 MILLION OZ WITH THE GAIN IN PRICE..

WE HAD 111 NOTICES FILED TODAY FOR 555,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 6941 CONTRACTS TO 535.552 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: —1967 CONTRACTS.

.

THE STRONG SIZED DECREASE IN COMEX OI CAME WITH OUR RISE IN PRICE OF $10.55//COMEX GOLD TRADING/WEDNESDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD MINOR LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERING

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JULY AT 2.914 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 36,600 OZ

YET ALL OF..THIS HAPPENED DESPITE OUR GAIN IN PRICE OF $10.55 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A FAIR SIZED LOSS OF 2168 OI CONTRACTS 6.743 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6941 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 535,552

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2168 CONTRACTS WITH 6941 CONTRACTS DECREASED AT THE COMEX AND 4723 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 201 CONTRACTS OR 0.6251 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4773) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (6941,): TOTAL LOSS IN THE TWO EXCHANGES 2168 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING AND SOME ADDITION TO SPECULATOR SHORTS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JULY. AT 2.914 TONNES FOLLOWED BY TODAY’S 36,600 OZ QUEUE JUMP 3) MINOR LONG LIQUIDATION//SOME SPECULATOR SHORT COVERING//SOME SPECULATOR SHORT ADDITIONS //.,4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

50,019 CONTRACTS OR 5,001,900 OZ OR 155.58 TONNES 9 TRADING DAY(S) AND THUS AVERAGING: 5557 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES: 155.58 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 155.58/3550 x 100% TONNES 4.39% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 155.58 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 2151 CONTRACT OI TO 144,410 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 350 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 350 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE:350 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2151 CONTRACTS AND ADD TO THE 350 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A VERY STRONG SIZED GAIN OF 2501 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 12.505 MILLION OZ

OCCURRED DESPITE OUR RISE IN PRICE OF $0.24 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 2.85 PTS OR 0.08% //Hang Sang CLOSED DOWN 46.74 OR 0.22% /The Nikkei closed UP 164.62 OR % 0.62. //Australia’s all ordinaires CLOSED UP 0.60% /Chinese yuan (ONSHORE) closed DOWN 6.7553 /Oil DOWN TO 94.41 dollars per barrel for WTI and DOWN TO 97.83 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7755 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7718: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 6941 CONTRACTS TO 535,552 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX DECREASE OCCURRED DESPITE OUR GAIN OF $10.55 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A GOOD SIZED EFP (4773 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY.. THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4773 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :4773 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4773 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: AN FAIR SIZED SIZED TOTAL OF 2168 CONTRACTS IN THAT 6941 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 6941 CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR RISE IN PRICE OF GOLD $10,55.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JULY (16.618),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 16.618 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $10.55) BUT WERE SUCCESSFUL IN KNOCKING OFF A FEW SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED A FAIR SIZED LOSS OF 6.743 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR JULY (16.618 TONNES)…

WE HAD -1967 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 2168 CONTRACTS OR 216,800 OZ OR 6.743 TONNES

Estimated gold volume 318,260/// good/

final gold volumes/yesterday 408,347 / very strong

INITIAL STANDINGS FOR JULY ’22 COMEX GOLD //JULY 14

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 322,976.873 oz Manfra Brinks Int. Delaware Loomis Delaware32 kilobars and 76 kilobars Delaware//.Loomis |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 423 notice(s)42,300 OZ 1.3157 TONNES |

| No of oz to be served (notices) | 450 contracts 45,000 oz 1.3996 TONNES |

| Total monthly oz gold served (contracts) so far this month | 4893 notices 489,300 OZ 15.219 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

5 customer withdrawals:

i)Out of Brinks 2977.97 oz

ii) Out of Delaware: 1028.832. oz (32 kilobars)

iii) Out of Int. Delaware: 199,878.465 oz

iii) Loomis: 2443.476 oz (76 kilobars)

iv) out of Manfra; 116,708.130 oz

total withdrawal: 322,976.873 oz

ADJUSTMENTS:2 dealer to customer

Brinks: 86,572.695 oz

Manfra: 55,395.792 oz

1 adjustment customer to dealer: jPM

42,246.414 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 873 contracts LOST 115 contracts . We had

481 notices filed on Wednesday so we gained a HUGE 366 contracts or an additional 33,600 oz will stand in this non active

delivery month of July.

August has a LOSS OF 28,503 contracts down to 277,197 contracts

Sept. gained 26 contracts to 2524 contracts.

We had 423 notice(s) filed today for 42,300 oz FOR THE July 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 360 notices were issued from their client or customer account. The total of all issuance by all participants equate to 423 contract(s) of which 316 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2022. contract month,

we take the total number of notices filed so far for the month (4893) x 100 oz , to which we add the difference between the open interest for the front month of (JULY 873 CONTRACTS ) minus the number of notices served upon today 423 x 100 oz per contract equals 497,700 OZ OR 16.618 TONNES the number of TONNES standing in this active month of July.

thus the INITIAL standings for gold for the JULY contract month:

No of notices filed so far (4893) x 100 oz+ (873) OI for the front month minus the number of notices served upon today (423} x 100 oz} which equals 497,700 oz standing OR 16.618 TONNES in this active delivery month of JULY.

TOTAL COMEX GOLD STANDING: 16.618 TONNES (A FAIR STANDING FOR A JULY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,443,533.842 oz 76.00 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 32,147,458.538 OZ

TOTAL ELIGIBLE GOLD: 15,744,578.019 OZ

TOTAL OF ALL REGISTERED GOLD: 16,372,850.519 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 13,29,317.0 OZ (REG GOLD- PLEDGED GOLD) 421 tonnes

END

SILVER/COMEX/JULY 14

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,592,325.028 oz JPM Loomis Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 3,492,673.200oz CNT JPM Loomis |

| No of oz served today (contracts) | 111CONTRACT(S) 555,000 OZ) |

| No of oz to be served (notices) | 184 contracts (920,000 oz) |

| Total monthly oz silver served (contracts) | 2971 contracts 14,855,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 3 deposits into the customer account

i) Into JPMorgan: 1,189,525.400 oz

ii) Into CNT: 1,697,410.980 oz

iii0 Into Loomis 605,756.820

total deposit: 3,492,673.200 oz

JPMorgan has a total silver weight: 175.749 million oz/341.277 million =51.52% of comex

Comex withdrawals: 3

i) Out of CNT: 951.200 oz

ii) Out of loomis 55,008.828 oz

iii)Out of JPMorgan: 1,182,454.300 oz

iv) out of Manfra: 354,861.900 oz

total withdrawal 1,592,325.028 oz

adjustments: 2/dealer to customer

i) JPMorgan: 467,315.300 oz

ii)Manfra 35,478.820 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 62.196 MILLION OZ

TOTAL REG + ELIG. 341.277 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JULY OI: 298 CONTRACTS HAVING LOST 25 CONTRACTS HAD 169 NOTICES FILED

ON WEDNESDAY, SO WE GAINED 144 CONTRACTS OR AN ADDITIONAL 720,000 OZ WILL STAND FOR METAL AT THE COMEX.

AUGUST GAINED 8 CONTRACTS TO STAND AT 1144

SEPTEMBER HAD A GAIN OF 1297 CONTRACTS UP TO 117,981 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 111 for 555,000 oz

Comex volumes:79,470// est. volume today// strong

Comex volume: confirmed yesterday: 67,557 contracts ( good )

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 2971 x 5,000 oz = 14,855,000 oz

to which we add the difference between the open interest for the front month of JULY(298) and the number of notices served upon today 111 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY./2022 contract month: 2971 (notices served so far) x 5000 oz + OI for front month of JULY (298) – number of notices served upon today (111) x 5000 oz of silver standing for the JULY contract month equates 15,775,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JULY 14/WITH GOLD DOWN $28.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD//INVENTORY RESTS AT 1019.79 TONNES

JULY 13/WITH GOLD UP $10.55:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROMTHE GLD//INVENTORY RESTS AT 1021.53TONNES

JULY 12/WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESS AT 1023.27 TONNES

JULY 11/WITH GOLD DOWN $4.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWL OF 1.16 TONNES FROM THE GLD./INVENTORY RESTS AT 1023.27 TONNES

JULY 7/WITH GOLD UP $1.35: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.61 TONNES FORM THE GLD///INVENTORY REST AT 1024.43 TONNES

JULY 6/WITH GOLD DOWN $26.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 9.86 TONNES FROM THE GLD//INVENTORY REST AT 1032.04 TONNES

JULY 5/WITH GOLD DOWN $36.55//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.41 TONNES FROM THE GLD///INVENTORY RESTS AT 1041.90 TONNES

JULY 1/WITH GOLD DOWN $5.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES//INVENTORY RESTS AT 1050.31 TONNES

JUNE 30/WITH GOLD DOWN $9.20: big CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 1052.63 TONNES//

JUNE 28/WITH GOLD DOWN $3.05//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.64 TONNES FROM THE GLD///INVENTORY RESTS AT 1056.40 TONNES

JUNE 27/WITH GOLD DOWN $4.90 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.04 TONNES

JUNE 24/WITH GOLD UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

JUNE 21/WITH GOLD DOWN $2.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1075.54 TONES

JUNE 17/WITH GOLD DOWN $11.25: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.60 TONNES INTO THE GLD.///INVENTORY RESTS AT 1075.54 TONNES

JUNE 16/WITH GOLD UP $28.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.74 TONNES

JUNE 15/WITH GOLD UP $6.50/BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD////INVENTORY RESTS AT 1063.74 TONNES

JUNE 14/WITH GOLD DOWN $18.80/NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 13/WITH GOLD DOWN $41.55: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 10/WITH GOLD UP $21.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

GLD INVENTORY: 1019.79 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 14/WITH SILVER DOWN 88 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 OZ FROM THE SLV// //INVENTORY RESTS AT 513.671 MILLION OZ

JULY 13/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SV//INVENTORY RESTS AT 514.501 MILLION OZ.

JULY 12/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A IWTHDRAWAL OF 3.228 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 514.501 MILLION OZ//

JULY 11/WITH SILVER DOWN 17 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 5.533 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 517.729 MILLION OZ

JULY 7/WITH SILVER UP 3 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.889 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 523.262 MILLION OZ/

JULY 6/WITH SILVER UP ONE CENT: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 12.558 MILLION OZ FORM THE SLV///INVENTORY RESTS AT 528.151 MILLION OZ

JULY 5/WITH SILVER DOWN 55 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 540.709MILLION OZ//

JULY 1/WITH SILVER DOWN 61 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ//INVENTORY RESTS AT 540.709 MILLION OZ//

JUNE 30/WITH SILVER DOWN 41 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 738,000 OZ FROM THE SLV//INVENTORY RESTS AT 541.262 MILLION OZ//

JUNE 28/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.00 MILLION OZ..

JUNE 27/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

JUNE 21/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.506 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 547.166 MILLION OZ//

JUNE 17/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 739,000 OZ FROM THE SLV./:INVENTORY RESTS AT 543.660 MILLION OZ/

JUNE 16/WITH SILVER UP 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 15/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 14/WITH SILVER DOWN 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 13/WITH SILVER DOWN 62 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 10.WITH SILVER UP 13 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 Z FROM THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FROM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

CLOSING INVENTORY 513.671 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

A must read.

Egon Von Greyerz/

Beware Of Markets Full Of Fool’s Gold

THURSDAY, JUL 14, 2022 – 07:20 AM

Authored by Egon von Greyerz via GoldSwitzerland.com,

Fool’s Gold comes in many guises, whether it is in fake paper money, Ponzi investment schemes, fake and manipulated gold derivatives, Bitcoin or just fake gold discoveries in Uganda, all of which are discussed in this article.

‘The tendency of an inconvertible paper money is to create fictitious wealth, bubbles, which by their bursting, produce inconvenience.’ – Lord Liverpool 1810 (UK Prime Minister 1812-27)

The elegant and understated courtesy of the English is well known. “Inconvenience” is for an early 19th century aristocrat what a modern Englishman today would call “bloody mess.“

Confucius described this trait already 2,500 years ago:

“The noble-minded are calm and steady. Little people are forever fussing and fretting.” – Confucius

As we know from history, paper money doesn’t just cause an inconvenience, as Lord Liverpool said, but a collapse of the monetary system and of the economy involved.

In today’s decadent and morally bankrupt world, leaders tend to be “fussing and fretting little people” who frantically “create fictitious money and wealth”. This is why, as we enter the final stage of this era, we will see more sackings of leaders (Boris Johnson), assassinations (Abe) and escapes (Gotabaya Rajapaksa, Sri Lanka President).

Social unrest and civil wars will sadly be commonplace too.

The combination of weak leaders and fake money is a fitting end to a major economic cycle. It actually couldn’t end in any other way.

But the world has of course not yet seen the end of the current era, which started with private bankers taking control of the US monetary system in 1913.

Some of us believe we have a good idea how this will all end, but only future historians and other observers will tell us the exact course of events.

The Austrian economist Ludwig von Mises gave us a very likely outcome of how the financial system will end:

“There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.”

IMPOSSIBLE FOR CENTRAL BANKERS TO TURN OFF THE MONEY SPIGOTS

Von Mises first alternative of a voluntary abandonment is of course totally unacceptable to current governments and central bankers. Don’t believe for one moment that Powell or Lagarde would contemplate turning off the tap that has kept them and their money forging friends in power for decades.

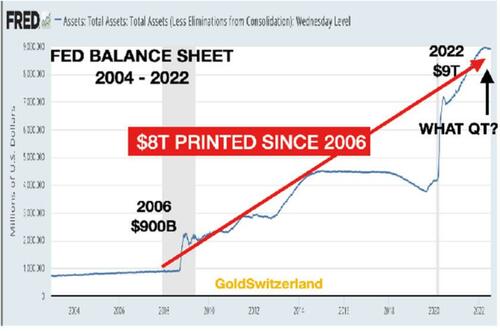

Yes, they will make gestures like the Fed is now attempting with QT (quantitative tightening). So the balance sheet of the Fed has come down $70 billion since mid March – BIG DEAL!

That’s a 0,7% reduction in 3 1/2 months for a balance sheet that has grown by 240% or $5.3 trillion since end of August 2019. In 2006 the Fed balance sheet was $900 billion and today it is $9 trillion, a mere 10-fold increase.

Let’s just remind ourselves that the current problems in the world did not start with Covid in early 2020, but with irreparable damage to the financial system which central banks couldn’t conceal beyond August 2019.

The beginning of the end of this 100+ year financial era was the Great Financial Crisis -GFC- which started in 2006.

As I have illustrated in many articles, the cast producing this damage to the financial system changes, but their actions are all the same. Through the privately owned Fed, they are all working for their own “charitable” purpose of personal gain and control for the private bankers.

AFTER US THE FLOOD

After Us The Flood is what Louis XV mistress Madame de Pompadour told the French King after they lost a critical battle against Prussia in the 18th century. That event was the beginning of the downfall of France and the French Revolution.

AFTER US THE FLOOD – Après Nous Le Déluge

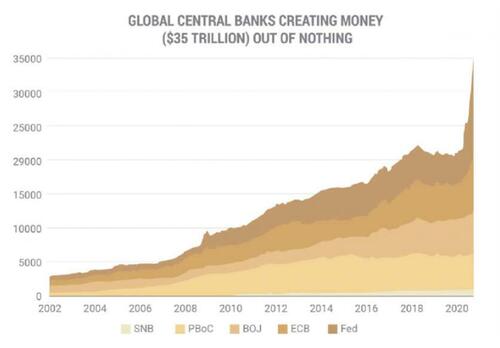

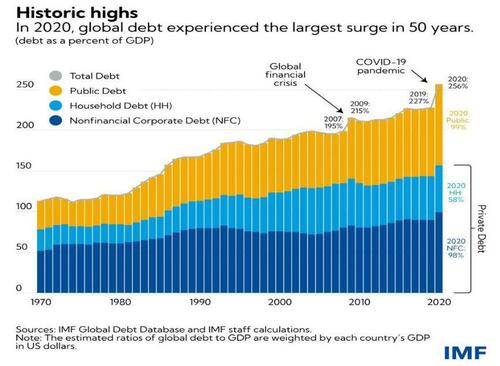

Since 2006, the balance sheets of the major central banks (Swiss National Bank, Bank of China, Bank of Japan, ECB, Fed) have grown exponentially from under $5 trillion to $36 trillion – a 7-fold increase!

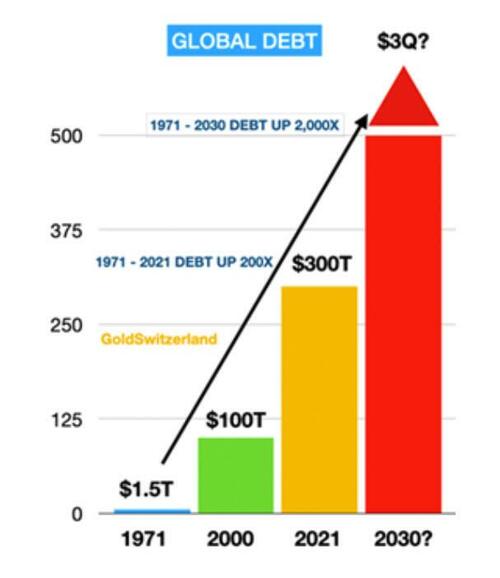

GLOBAL DEBT UP 200X SINCE 1971 AND GOING TO 2,000X

But we must remember that irresponsible debt creating central banks are only part of the problem. The real money printers are the commercial banks. So if we look at total global debt, it has grown from $100 trillion in 2000 to $300 trillion today. In 2006 (not shown) total global debt was $120 trillion.

As the graph below shows, total global debt including derivatives and unfunded liabilities is over $3 quadrillion. When the financial system crashes, these derivatives will prove worthless as counterparties fail and the central banks will print $2-3 quadrillion in a futile attempt to save the banks and the system.

Sensible historic comparisons are no longer possible since the debt creation folly of the last 50 years is totally unprecedented in history.

In 1971, when Nixon closed the gold window, global debt was $1.5T.

After 50 years of irresponsible monetary policies debt has grown 200X. When we reach a total debt of $3 quadrillion in the next 5 to 10 years, with the assistance of the derivative collapse, the increase will be 2,000X since 1971.

I can hear some people calling this sensational scaremongering. But I am sure that these people would have said the same about the 200X debt expansion since 1971.

THE COMING EXPONENTIAL MOVE WILL BE TERMINAL

Also, it is important to understand how exponential moves happen. I explained this in an article from 2017 called “Only Contrarians Will Survive”

In that article I illustrated that exponential moves really move exponentially and that they are terminal:

“Imagine a football stadium which is filled with water. Every minute one drop is added. The number of drops doubles every minute. Thus it goes from 1 to 2, 4, 8 16 etc. So how long would it take to fill the entire stadium? One day, one month or a year? No it would be a lot quicker and only take 50 minutes! That in itself is hard to understand but even more interestingly, how full is the stadium after 45 minutes? Most people would guess 75-90%. Totally wrong. After 45 minutes the stadium is only 7% full! In the final 5 minutes the stadium goes from 7% full to 100% full.”

So for the same reason, debt is likely to grow exponentially in the next 5-10 years, as the world experiences hyperinflation. But we must also remember that as commodities such as food and energy plus many raw materials like precious metals go up exponentially, all the bubble assets (stocks, bonds and property) will implode in real terms. See my recent article “Concurrent Deflation and Hyperinflation Will Ravage The World”

We could of course blame Nixon for the debt disaster that the world is now in. But that would be too simple. Governments have throughout history interfered with the laws of nature and the simple law of supply and demand.

As clueless central bankers (and before that governments) interfere in the natural ebb and flood waves of the economy, these natural cycle movements become extreme tops and bottoms. These excessive moves lead to speculative asset and credit bubbles (inflation/hyperinflation) followed by a deflationary collapse or implosion just as von Mises said (see quote above).

As I explain above, it is totally natural that the end of major cycles creates exponential moves, as we have experienced in this century in both debt and assets such as stock and property.

But what few people realise is that the frantic money printing and debt creation which has taken place in this century indicate the end of a 100 year old monetary era.

The next few years will be like the final 5 Stadium minutes when the debt goes up exponentially by say 14X (the Stadium going from 7% to 100% full) before it all collapses.

CRYPTOS – FOOL’S GOLD

These final moves also lead to the creation of instruments that become “fool’s gold”.

In my view, cryptocurrencies are a form of fool’s gold. Cryptos might have been a wonderful speculative investment for a few investors, but many who entered late have experienced losses of 70 to 90% so far.

As far as I am concerned, and the investors we advise, cryptos have nothing to do with wealth preservation and will certainly never replace gold. Bitcoin is a binary investment that might go to $1 million but it could just as well go to ZERO, so obviously not a good risk.

“Blockchain is a fraud” – Brazilian professor

A Brazilian Professor of computer science, Jorge Stolfi, tweeted in May this year:

“Every computer scientist should be able to see that cryptocurrencies are totally dysfunctional payment systems and that “blockchain technology” (including “smart contracts”) is a technological fraud.”

Stolfi explains how he and 1,500 specialists, including Harvard lecturers and Google’s principal Cloud engineer, delivered a critical letter to the US congress, warning about crypto currencies.

He explains in an interview why cryptos are a pyramid scheme similar to Madoff.

Stolfi: “These pyramid schemes collapse when there are no more fools to fool.”

He also says that Bitcoin won’t exist in 20 years. He calls blockchain a technological fraud that can never be used as a payment system, due to its snail processing speed compared to Visa for example.

El Salvador and Fool’s Gold

El Salvador clearly believed in Fool’s Gold as they announced last year that they would be the first country to accept Bitcoin as legal tender. They were also going to fund the project by issuing $1 billion in bonds secured with Bitcoin. That project is obviously delayed after BTC fall of 2/3. Bitcoin City would be built and would have no taxes except VAT. And now it seems the City would have no revenues either after the BTC losses.

Sounds like Shangri-la turned to hell to me. Sadly for them, they have lost more on their BTC purchases than the country can afford to lose and their debt is now JUNK.

All the Bitcoiners who hailed El Salvador as the future model of money and went there on Pilgrimages are now very quiet.

Well, Ponzi schemes always collapse without fail and it seems that this might be the destiny of Bitcoin and other Cryptos. Most of them are down 70% or more on their way to oblivion.

We will certainly stick to physical gold!

Fool’s Gold in Uganda

So Uganda has officially declared that they have discovered 31 million tonnes of gold ore deposits, which is expected to produce 320,000 tonnes of refined gold!

Let’s remind ourselves that all the gold ever mined in history is around 190,000 tonnes. So this find would treble the gold in the world.

Sounds to me like another Fool’s Gold story. Uganda is quite notorious for corruption and fraud. They clearly hope to borrow major amounts of money based on this so-called find, which is in no way properly proven or documented.

Or maybe this comes from the Bitcoin crowd. They are of course elated by this “fake” gold discovery since it makes BTC much more unique with a limit of 21 million coins issued.

Or could the Ugandan government have confused tonnes with ounces?

STOCK MARKETS FOOL’S GOLD – COLLAPSE IMMINENT

Current asset markets and especially stocks have also turned into fool’s gold. Investors now believe that stocks can only go up and that the Fed and other central banks will be there to save them indefinitely. How shocked these investors will soon be!

As I often say, forecasting markets is a mug’s game and that is why we prefer to focus on risk. And as I outlined in my last article, (“The Implosion Will Be Fast, Hold Onto your Seats”) risk is now extreme, both fundamentally and technically.

Most stock markets in the world are already down 20-30% in 2022. What few investors realise at this stage is that the fall we have seen so far is not just a normal correction but the beginning of a long-term secular bear market with dramatic falls to come.

Technically it looks like the next major fall is imminent. So protecting risk by being out of stocks is strongly advisable.

Precious metals are in a small correction of a major long term bull market which is the inevitable collapse of the currency system. Gold might come down initially with stocks by $100 or so but the next major move of gold up will be both substantial and long term.

Remember that physical precious metals must be owned, not as a speculative investment, but as the best form of wealth preservation you can hold.

END

3. Chris Powell of GATA provides to us very important physical commentaries

A must read.

The major players behind the criminal activity of JPMorgan (under RICO charges) are before the court.

Edmonds describes what spoofing (and everything else) did to cheat markets. This will be collaborated with their chat room discussions with other bankers

(Bloomberg/GATA)

JPMorgan gold desk’s ‘spoofing’ cheated market, former trader testifies

Submitted by admin on Wed, 2022-07-13 11:06Section: Daily Dispatches

By Tom Schoenberg and Eddie Spence

Bloomberg News

via Yahoo News, Sunnyvale, California

Wednesday, July 13, 2022

https://finance.yahoo.com/news/jpmorgan-gold-desk-cheated-market-211639062.html

JPMorgan Chase & Co.’s gold trading and sales team was so focused on making money that they scammed the market for years with so-called spoofing trades, according to a former colleague who testified at the trial of three former bank employees charged with fraud.

“Our job was to do whatever it takes to make money,” and using spoof trades to manipulate prices for all sorts of precious metals was an almost daily method for generating profit, said John Edmonds, who worked as a trader at the bank until 2017.

“Everyone at the time did it on the desk and it worked.”

Edmonds is testifying against his former boss, Michael Nowak, the longtime head of the trading desk, gold trader Gregg Smith and hedge funds salesman Jeffrey Ruffo. Edmonds told a federal jury in Chicago on Tuesday that the team wasn’t just buying and selling precious metals, but systematically cheating to help themselves and their top clients over the course of the decade that Edmonds worked as a trader.

Edmonds described how he learned to spoof at JPMorgan. If he wanted to sell at a higher price, he’d put orders in above the current market price, and then place a huge orders to buy at higher prices that he’d cancel before they could be executed. “I wanted to drive the price where I wanted it to go” by creating a false indication of demand, he said.

While the technique didn’t always work, it was successful enough that everyone on the trading desk used it several times a week, Edmonds said.

“If we wanted to buy low, we could,” he said. “If we wanted to sell high, we could.”

Edmonds is the first of a handful of cooperators slated to testify that prosecutors say will bolster their claim that Nowak, Smith and Ruffo participated in a racketeering enterprise from 2008 to 2016. Edmonds was the first on the precious-metals desk to admit to crimes and secretly cooperated against former colleagues. He pleaded guilty to conspiracy and commodities fraud charges related to spoofing in 2018.

Traders on Nowak’s desk engaged in spoofing as a core business practice, doing it more than 50,000 times over nearly a decade, prosecutors allege, though the jury will only hear about a tiny portion of those. Lawyers for the three said the government’s case is based on a misreading of evidence and the reliance on witnesses, like Edmonds, who are testifying in order obtain light punishments. If convicted of all charges, the three face decades in prison.

Edmonds, a Brooklyn native with a degree from St. Johns University in Queens, New York, joined JPMorgan’s precious-metals desk in 2009 at a salary of about $80,000. Edmonds’s supervisors and more senior members on the desk showed him how to layer trades, he told the jury, adding that it was understood on the desk that this was the way to trade precious-metals futures.

“I saw people trading for 20 years doing this,” Edmonds said. “How could I not do it?” Among members of the team, the use of spoofing techniques “was expected,” he said, adding that he watched both Smith and Nowak execute spoof trades to fill client orders at favorable prices.

Edmonds said he never reported anyone for violating the bank’s compliance policy on trading. When asked why not, he told the jury: “I would have been fired. This was my dream job.”

Prosecutors on Friday described the trading desk as a small area with no walls or doors where Nowak, Edmonds and the others sat shoulder to shoulder, just a few feet from one another. Lucy Jennings, a Justice Department fraud prosecutor, told the jury that everyone on the team “could see and hear what everyone is doing.”

David Meister, a lawyer for Nowak, told the jury that Edmonds was “eager to please” but that his trading skills “didn’t cut it” and his job was eliminated.

Edmonds was notable even among the JPMorgan traders. At times he had placed orders with as many as 400 contracts on the opposite side of a genuine one. Edmonds pleaded guilty for transactions involving silver futures.

Earlier on Tuesday, jurors heard testimony from Christopher Jackman, a consultant at Monument Economics Group LLC who was hired by the DOJ for $1.4 million to analyze CME data and document what the government claims are spoof trades, along with chat logs from members of the JPMorgan precious-metals desk.

Jackman described on instance in 2010, when CME data show Smith placed buy orders for five gold futures contracts at 50 cents below the best bid price, and then quickly followed with another 170 sell orders. At the time, Smith’s sell orders represented more than half of the visible order book on the market, Jackman said. Prices fell, Smith executed his five buy orders, and then canceled all 170 sell orders before they could be executed, all in the span of about three seconds, Jackman said.

In data from January 2012, data show Nowak put in orders to sell five gold contracts valued at around $800,000, followed by orders to buy 80 contracts valued at $13 million, which at the time accounted for more than a third of the orders visible to the market, Jackman said. After prices rose, Nowak executed all five sell orders and canceled all the buy orders, Jackman said, adding that the entire episode lasted less than 15 seconds.

—–

The case is US v. Smith et al, 19-cr-00669, US District Court, Northern District of Illinois (Chicago).

END

Pam and Russ say crypto and blockchain are shams

(Wall Street on Parade/Pam and Russ Martens)

Pam and Russ Martens: Brightest tech minds say crypto and blockchain are shams

Submitted by admin on Wed, 2022-07-13 11:19Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Wednesday, Junly 13, 2022

The letter is a punch in the gut to the Wall Street underwriters who have brought billions of dollars of crypto related companies to the public markets, most of which have now collapsed in price.

It makes the billionaire venture capitalists who have invested billions in crypto startups look like fools. And it renders the big-name celebrities who have promoted this garbage in TV commercials look like the shills that they are.

The letter was sent to key members of Congress and to the chairs of the Senate Banking and House Financial Services Committees. It is signed by more than 1,600 computer scientists, software engineers, and technologists from around the world.

There are 45 signatories who currently work at Google; 19 who work at Microsoft; and 11 employed at Apple. (Those three companies currently have a collective market capitalization of more than $5.75 trillion; they can afford to hire the best and the brightest.)

There are signatories that are Ph.Ds from the most prestigious universities, including the University of Oxford and MIT. And all 1,600 have signed a letter that says this about crypto and blockchain …

… For the remainder of the commentary:

END

Quite a case: Litigation over that 31 tonnes of Venezuelan gold resumes in London court

(Reuters/GATA)

Litigation over Venezuelan gold resumes in London court

Submitted by admin on Wed, 2022-07-13 21:35Section: Daily Dispatches

By Kirstin Ridley and Marc Jones

Reuters

Wednesday, July 13, 2022

LONDON — A long-running legal battle between Venezuelan President Nicolas Maduro and opposition leader Juan Guaido over who should hold the key to more than $1.5 billion of gold stored at the Bank of England resumed today at the London High Court.

The UK Supreme Court ruled last year that Guaido should be recognised as the Latin American country’s head of state, taking a lead from the British government’s position, and that he had the authority to determine the future of the 31 tonnes of bullion

The High Court will now grapple with the novel question, over a four-day trial, about how to treat rulings by the Venezuelan Supreme Tribunal of Justice that say Guaido’s appointments to an “ad hoc” central bank board are invalid.

“At stake is the question of whether the English courts can sit in judgment on the validity of decisions made by another sovereign nation’s highest court,” said Sarosh Zaiwalla, a partner at law firm Zaiwalla & Co., who is representing the Maduro-led Banco Central de Venezuela. …

… For the remainder of the report:

https://www.reuters.com/world/americas/venezuelan-gold-legal-battle-resumes-london-2022-07-13/

END

4. OTHER GOLD COMMENTARIES

END

5.OTHER COMMODITIES:

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7553

OFFSHORE YUAN: 6.7718

HANG SANG CLOSED DOWN 46.74 PTS OR 0.22%

2. Nikkei closed UP 164.62 OR 0.62%

3. Europe stocks CLOSED ALL RED

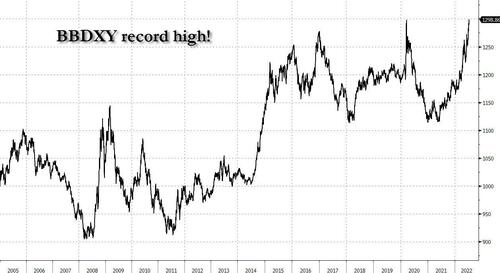

USA dollar INDEX UP TO 108.50/Euro FALLS TO 1.0006

3b Japan 10 YR bond yield: FALLS TO. +.227/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 138.89/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN -// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.188%/Italian 10 Yr bond yield RISES to 3.40% /SPAIN 10 YR BOND YIELD RISES TO 2.35%…

3i Greek 10 year bond yield RISES TO 3.53//

3j Gold at $1713.00 silver at: 18.60 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 9/100 roubles/dollar; ROUBLE AT 58.36

3m oil into the 94 dollar handle for WTI and 97 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 137.07DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9835– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9841well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.923 UP 2 BASIS PTS

USA 30 YR BOND YIELD: 3.084 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.48

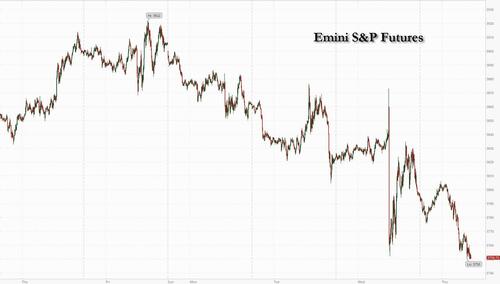

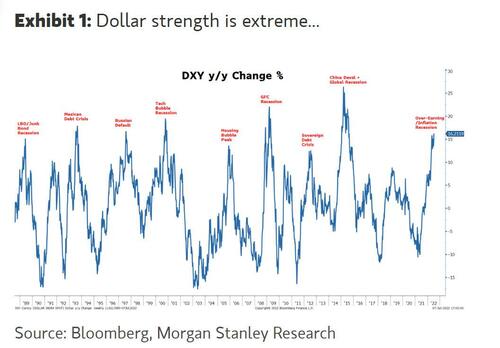

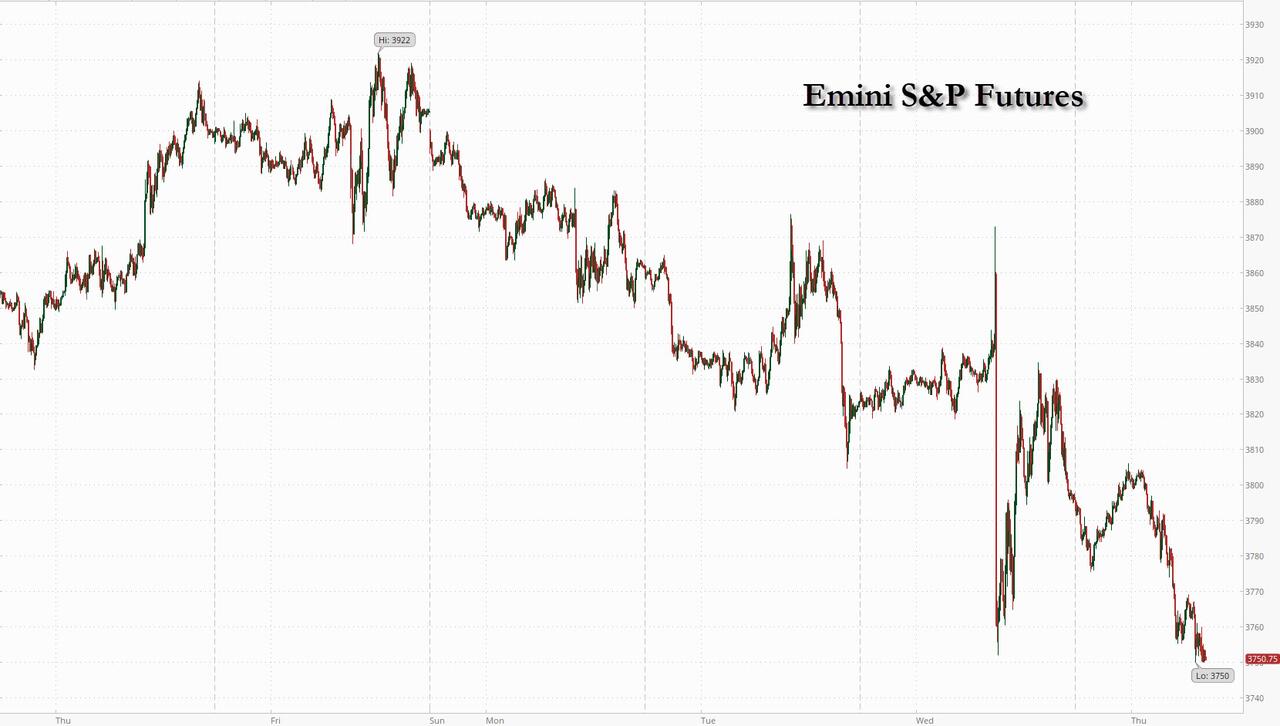

Futures Tumble As Dollar Hits Record High; JPM, Morgan Stanley Slide

THURSDAY, JUL 14, 2022 – 08:24 AM

US futures were already sliding fast as the reality of the Fed’s upcoming 100bps rate hike was fully appreciated by the market, as even Goldman was shocked by the kneejerk move higher yesterday, saying “Does it makes sense for mkt to move higher after a 9.1% print and BOC hiking by 100bps…of course not…but that was max pain trade today and this market seeks max pain.”

Well, this morning the max pain was clearly lower, as US equity futures fell along with stocks in Europe and Asian, while the Bloomberg dollar index rose to a record Thursday, surpassing the record hit during the covid 2020 crash when the Fed launched unlimited swap lines to ease the global dollar crunch…

… after high US inflation hardened expectations for more aggressive Federal Reserve monetary tightening that could trigger a recession.

S&P 500 futures tumbled more than 1%, down almost 200 points since Friday, as the US second-quarter earnings season got underway. All risk assets were lower, as well as gold and oil, while all non-USD currencies are getting steamrolled by the relentless surge in the dollar. 10Y yields dropped to 2.93% after rising just shy of 3.00% overnight. The inversion between two-year and 10-year yields — a potential recession indicator — is the deepest since 2000

But wait there’s more, because while markets are freaking out over soaring inflation, Fed hikes and crashing earnings, Europe is about to enter the 9th circle of hell: France’s Macron warns that citizens and companies will need to reduce energy usage as Germany reports that gas storage is already being withdrawn, even before peak usage in the winter. Meanwhile, Italian bonds and banks are tumbling amid speculation Mario Draghi’s government is about to collapse as coalition partner Five Star threatens to pull out.

Looking at premarket movers, JPMorgan plunged more than 5% in premarket trading after reporting results that missed analyst expectations. Tesla also dipped after the company’s top artificial-intelligence executive and an architect of its Autopilot self-driving system announced plans to depart the maker of electric vehicles and as Morgan Stanley makes “material” cuts to its forecasts across its auto portfolio. Some other notable premarket movers:

- Theravance Biopharma (TBPH US) shares jump as much as 25% in premarket trading after the biotech firm agrees to sell royalty interests in Trelegy Ellipta to Royalty Pharma.

- ContraFect (CFRX US) sinks as much as 77% in US premarket trading after the biotech company said that the Data Safety Monitoring Board recommended stopping its Exebacase phase 3 study.

- Netflix’s (NFLX US) decision to pick Microsoft (MSFT US) as a technology and sales partner for its new advertising-supported streaming service was a surprise to the industry. Analysts say the move makes sense. Netflix slips 1% in premarket trading, Microsoft -0.9%.

As discussed yesterday, Fed officials will be debating a historic one percentage-point rate hike later this month in an attempt to combat inflation. Markets price in 69% odds that the Fed will raise interest rates by 100 basis points when it meets July 26-27, which would be the largest increase since the Fed started directly using overnight interest rates to conduct monetary policy in the early 1990s. Technology stocks will be in focus as higher rates mean a bigger discount for the present value of future profits, hurting growth stocks with the highest valuations.

A 100 basis points hike is now likely and the “inflation reading should also raise the odds of recession, which we now estimate is likely sooner rather than later and possibly more severe,” said Tiffany Wilding, an economist at Pacific Investment Management Co.

“The market has already priced in the unexpected extreme tightening, so there isn’t that much more the Fed can do to prepare the markets,” said Mehvish Ayub, a senior strategist at State Street Global Advisors. “We need to position portfolios accordingly and expect volatility to continue as it has since the beginning of the year,” she said in an interview with Bloomberg Television.

“It is clear that central banks around the world are laser-focused on fighting the entrenched inflation they helped to create, growth-be-damned,” said Jeffrey Halley, a senior market analyst at Oanda Asia Pacific Ltd. “US markets are pricing in faster Fed tightening, and a recession is on the way imminently.”

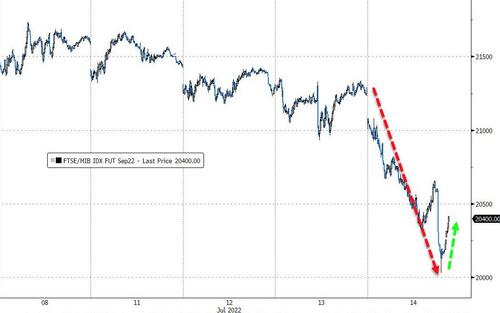

In Europe, the Stoxx 50 index slumped 1.2%. DAX outperforms peers, dropping 0.9%, FTSE MIB lags, dropping 2.3%. Miners, energy and telecoms are the worst-performing Stoxx 600 sectors. Here are the biggest European movers:

- Ericsson tumbles as much as 12% to the lowest level since March 2020, after a mixed quarterly report with revenue ahead of expectations but margin and earnings missing estimates.

- Sabre Insurance plunged more than 30% after warning that everything related to an insurance claim — the car parts, paint, labor and the cost of replacing the vehicle — has risen faster than expected.

- Peers Admiral and Direct Line dropped 13% and 7.9%, respectively.

- Hugo Boss shares rise as much as 3.2% to the highest since late February after what analysts say was a “blow- out” second-quarter for the luxury apparel firm.

- Entain rises as much as 5.2%, rallying after last week’s heavy losses, as the owner of the Ladbrokes and Coral betting brands publishes a video updating on the progress of Enlabs since last year’s acquisition of the firm.

- Technogym shares fall as much as 6.8% as Goldman Sachs cuts its PT on the Italian gym-equipment maker on a weaker medium-term growth outlook and low visibility on near- term consumption patterns.

- Acciona slumped after newspaper Expansion said the Spanish government is analyzing 16 companies, including renewable unit Acciona Energia, to impose a new windfall profit levy announced earlier in the week.

- Storebrand rises as much as 4% in Oslo trading after second-quarter pretax profit beat the average analyst estimate.

- SBB posted a surprise pretax loss and the Swedish property company’s stock price tumbled as much as 17%.

- SEB shares gain as much as 4.7% in early European trading after the lender posted 2Q earnings that showed higher deposit margins and decent loan growth, Handelsbanken writes in a note.

- Hunting’s steep slide since its June 30 trading update offers a good entry point, Berenberg writes in note, upgrading the stock to buy from hold. Hunting shares up as much as 7.1%.

Asian stocks declined, as markets in Singapore and the Philippines fell after surprise monetary tightening by the two Southeast Asian nations, while Chinese bank shares weighed amid a property crisis. The MSCI Asia Pacific Index dropped as much as 0.6%, with the financials gauge weighing the most on the measure. Ping An Insurance was the single biggest drag, leading a fall among Chinese lenders as home buyers in China refused to pay mortgages on delayed construction projects. Shares in Singapore and Manila declined after local monetary authorities unexpectedly tightened policy rates to tackle inflation. Their declines helped put a key Southeast Asian equities gauge on track for a bear market. Taiwan’s benchmark rose for a second day after a government support pledge, while Chinese tech firms also climbed.

The region’s mixed performance comes as investors continue to digest the prospect of a recession on hardened expectations of more aggressive Federal Reserve monetary tightening after sizzling US inflation data. Traders in Asia also are waiting for Friday’s release of China’s second-quarter GDP growth figure. “Even while central banks in most of the rest of the world are moving in one direction, here in Asia we’ve got a very, very large player doing something different,” said Alexander Treves, head of investment specialists for Asia Pacific equities at JPMorgan Asset Management, referring to China in an interview with Bloomberg TV. “The government has got quite ambitious growth targets for this year and it might be they don’t meet them but they are going to try very, very hard to stimulate in that direction.” The higher-than-expected consumer prices data from the US overnight was “lagged bad news,” according to David Kelly, chief global strategist at J.P. Morgan Asset Management. “But we do expect lagged good news in the coming months, with energy prices diving lower, food prices cooling and consumer demand stepping back,” Kelly wrote in a note. “This should provide some inflation relief to the Fed and consumers, and hopefully lead sentiment to recover from its record-lows.”

Japanese equities erased earlier losses as the yen weakened after US inflation data hardened expectations of more aggressive Federal Reserve monetary tightening. The Topix index closed 0.2% higher at 1,893.13 in Tokyo, while the Nikkei 225 advanced 0.6% to 26,643.39. Keyence Corp. contributed the most to the Topix’s gain, increasing 3.5%. Out of 2,170 shares in the index, 1,229 rose and 803 fell, while 138 were unchanged. “The weak yen and continuation of monetary easing in Japan, which is completely different from the situation in the US and Europe, will help to support stock prices,” said Tomo Kinoshita, a global market strategist at Invesco Asset Management.

Australia’s S&P/ASX 200 index rose 0.4% to close at 6,650.60, climbing for a third session. Miners contributed the most to the benchmark’s gain. EML Payments was the top performer, bouncing back after three days of losses. Lake Resources was the biggest laggard after responding to a short-seller report. Investors also assessed jobs data. Australia’s hiring boom gathered pace in June, sending the unemployment rate to the lowest in almost 50 years and bolstering the case for a supersized interest rate hike next month. In New Zealand, the S&P/NZX 50 index rose 0.7% to 11,187.97

India’s benchmark equity index erased early gains to close at its lowest level in more than a week as shares of technology firms Infosys and TCS weighed. The S&P BSE Sensex fell 0.2% to 53,416.15 in Mumbai, while the NSE Nifty 50 Index declined by the same magnitude. Axis Bank was the worst performer on the Sensex, which saw 17 of its 30 member stocks trading lower. India’s biggest technology company TCS fell to the lowest level since March last year, setting the pace for a tech selloff. India’s headline inflation rose 15.18% compared to last year, which was below estimates for the first time since June 2021.

In FX, the Bloomberg Dollar Spot Index rose by around 0.5% hitting an all time high, as the greenback advanced against all of its Group-of-10 peers. AUD and DKK are the strongest performers in G-10 FX, JPY and CAD underperform. COP (+3%), RUB (+1.4%) lead gains in EMFX. The euro fluctuated, but held above parity. An early decline in the face of widespread dollar demand paused at buy orders from a reserve manager based in Asia seeking to diversify away from the greenback, according to Asia-based FX traders. One-week volatility in euro-dollar rallied as the tenor now captures the next ECB decision on July 21, the same day when a key Russian gas pipeline is scheduled to reopen. German and UK short-end bonds fell, led by the front-end, underperforming on their curves as money markets cranked up ECB and BOE rate-hike wagers for a second day. Investors were dumping Italian assets as political turmoil puts Prime Minister Mario Draghi’s government at risk of collapse and complicates efforts by the European Central Bank to support the market. Swedish 2-year bonds slumped after inflation rose faster than forecast in June. The yen approached 140 per dollar as the currency is decoupling from its close relationship with US bonds amid a broad rally in the dollar.

In rates, the treasuries curve extends Wednesday’s flattening move with 2s10s spread reaching -27bp during European morning, as political turmoil in Italy has investors dumping its bonds. US yields cheaper by up to 5bp in front end and belly of the curve, flattening 2s10s, 5s30s spreads by ~2bp and ~5bp on the day; 10-year yields around 2.95%, cheaper by ~3bp vs Wednesday’s close; Italian bonds underperform by more 20bp in the sector. In front end, investors continue to anticipate front-loaded and aggressive Fed hikes to peak by year-end; swaps price 92bp of hikes into the July policy meeting and 213bp of additional hikes into the December FOMC, where policy rate is expected to peak. Bund, and gilt curves bear-flatten; UST 2s10s yield-curve inversion deepens. Peripheral spreads widen to Germany with 10y BTP/Bund adding 9.7bps to 209.2bps.

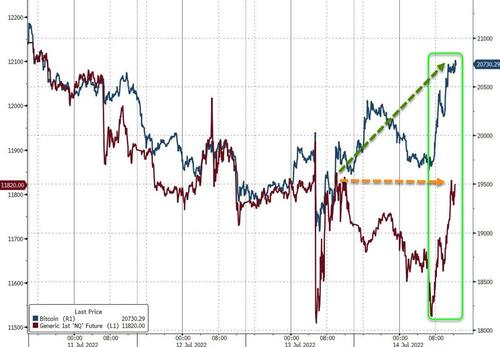

Bitcoin is bid but has reverted below the USD 20k mark once more, despite a brief foray to USD 20.4k initial highs.

In commodities, crude futures decline. WTI trades within Wednesday’s range, falling 2.3% to trade near $94.08. Brent falls 1.9% near $97.66. Most base metals trade in the red; LME nickel falls 5.1%, underperforming peers. Spot gold falls roughly $19 to trade near $1,717/oz. Spot silver loses 1.4% near $19.

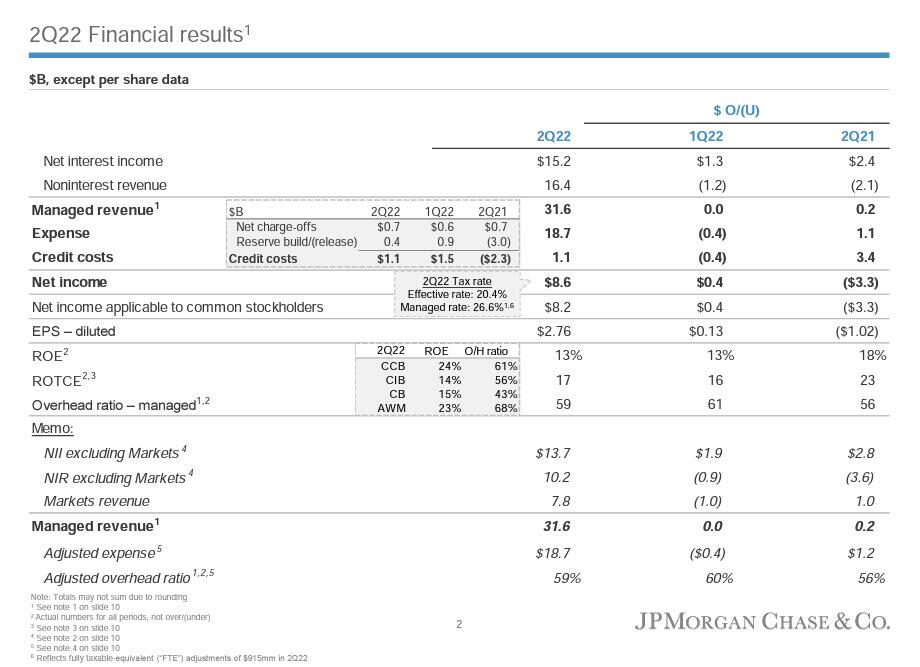

To the day ahead now, data releases include the US PPI reading for June and the weekly initial jobless claims. Otherwise, central bank speakers include the Fed’s Waller and the ECB’s Centeno. Earnings releases include JPMorgan Chase and Morgan Stanley. The European Commission will be publishing their latest economic forecasts, and UK Conservative MPs will hold another ballot on their next leader.

Market Snapshot

- S&P 500 futures down 0.9% to 3,768.75

- MXAP down 0.6% to 154.55

- MXAPJ down 0.2% to 510.23

- Nikkei up 0.6% to 26,643.39

- Topix up 0.2% to 1,893.13

- Hang Seng Index down 0.2% to 20,751.21

- Shanghai Composite little changed at 3,281.74

- Sensex down 0.4% to 53,290.44

- Australia S&P/ASX 200 up 0.4% to 6,650.62

- Kospi down 0.3% to 2,322.32

- STOXX Europe 600 down 0.7% to 409.97

- German 10Y yield little changed at 1.24%

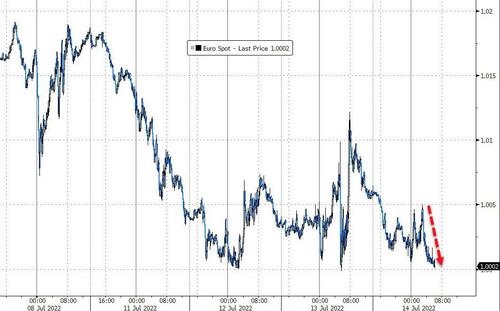

- Euro down 0.4% to $1.0023

- Gold spot down 1.0% to $1,717.77

- US Dollar Index up 0.57% to 108.57

Top Overnight News from Bloomberg

- The three-month euribor’s seven-year foray in to negative territory ended as money markets prepared for the ECB’s first rate hike in more than a decade

- Italy’s Five Star Movement will refuse to back Mario Draghi’s government in a confidence vote on Thursday, raising the prospect that the prime minister offers to resign, potentially leading to an early election. A financial- market crisis focused on Italy might augur the worst turmoil in the history of the euro

- Singapore’s central bank unexpectedly tightened monetary policy on Thursday, its second surprise move this year, as rising inflation fanned the risk of economic contraction

- China will take further measures to stabilize employment as the country grapples with a flagging economy battered by the Covid-19 pandemic and a crumbling real-estate market

- Chinese regulators have been asked to exercise greater caution when it comes to reviewing new overseas spending and investment plans amid concerns among senior leaders that higher US interest rates could spur capital outflows, according to people familiar with the matter

- The euro area’s rebound from the pandemic will be weaker than anticipated while inflation will be faster because of Russia’s war in Ukraine, according to draft projections by the European Commission

- Central banks across the globe are speeding up interest-rate hikes, seeking to crush an inflation surge partly of their own making. Wednesday saw Canada’s central bank hike a greater-than-expected full percentage point following two half-point moves, South Korea raise by a half point after several quarter-point moves, and New Zealand increase by a half point for a third straight meeting

A more detailed look at global markets courtesy of Newsquawk

Asia-pac stocks mostly traded with cautious gains after the recent hotter-than-expected US inflation data which printed at a fresh 40-year high and spurred hawkish market pricing with Fed Fund Rate futures leaning towards a 100bps Fed rate hike this month. ASX 200 was kept afloat amid strength in the commodity-related sectors although gains were capped as blockbuster jobs data raised the odds for the RBA to deliver a more aggressive 75bps hike at its next meeting. Nikkei 225 outperformed its major counterparts on the back of further currency depreciation. Hang Seng and Shanghai Comp. were initially pressured by weakness in the property sector although the downside in the broader market was cushioned and eventually reversed after recent policy support pledges in which the PBoC said it will step up support for the real economy and deepen interest rate reforms. STI and PSEi were the laggards and traded in the red after both the Monetary Authority of Singapore and the Philippines Central Bank tightened their monetary policies in unscheduled announcements.

Top Asian News

- Tokyo is expected to raise the COVID warning to its highest level, according to FNN.

- Monetary Authority of Singapore announced to re-centre the mid-point of the SGD NEER policy band up to the prevailing level in an unscheduled meeting, while there was no change to the slope and width of the band. MAS said the move is to help slow the momentum of inflation and that inflation pressures are to remain elevated in months ahead, while it is appropriate to further tighten monetary policy further.

- Philippines Central Bank raised its key rates by 75bps to 3.25% in an unscheduled policy decision. Philippines Central Bank Governor said they recognised that a significant further tightening of monetary policy was warranted by sustained broadening price pressures, while they are ready to take further action and said the economy can accommodate further tightening.

- Chinese authorities reportedly met with banks regarding the mortgage payment boycott, according to Bloomberg sources

European bourses are pressured across the board, Euro Stoxx 50 -0.8%, but off worst levels while the FTSE MIB -1.9% languishes on domestic turmoil. Sectors are essentially all in the red with Tech giving up its initial TSMC-driven strength and succumbing to risk/yield moves. Stateside, futures are off lows but in-fitting European benchmarks awaiting guidance from the key banking names due to report imminently. TSMC (2330 TT) Q2 (TWD): Net Profit 237bln (exp. 219bln), Revenue 534bln (prev. 372bln YY), Operating Income 262bln (prev. 145bln YY); excess inventory in chip supply will take a few quarters to rebalance; expect capacity to remain tight this year; expects some capex this year to be pushed into next year due to tool supply issues. 2022 Capex closer to the lower end of prior guidance of USD 40-44bln. 2023 will see more of a typical downcycle in chip demand, unlike the large downcycle in 2008. Intel (INTC) has reportedly informed customers it will increase prices on a majority of its microprocessors and peripheral chip products later this year, citing rising costs, via Nikkei; Increases have not been finalized, likely to range from a minimal single-digit increase to over 10% or 20% in some cases, according to sources.

Top European News

- The first round of the Conservative leadership ballot saw Sunak, Mordaunt, Truss, Tugendhat, Badenoch, and Braverman make it to the next round, while Hunt and Zahawi were eliminated.

- Italy’s 5-Star leader Conte said the party will not participate in the confidence vote on Thursday, according to Reuters.

- EU draft report cut 2022 EU GDP forecast to 2.6% from 2.8% and for 2023 to 1.4% from 2.3%.

FX

- Yen yields to inevitable further widening in BoJ/Fed policy rates as markets place 2/3 probability on 100bp July FOMC hike; USD/JPY jumps through 139.00 towards October 1998 peak at 139.50, but pares back below 1.48bln option expiry interest at the round number.

- DXY rebounds firmly after post-US CPI retreat to set new YTD peak before fading, index tops out at 108.650 vs 108.190 bottom and 107.470 midweek low.

- Loonie loses all and more BoC boost as oil tanks, USD/CAD close to 1.3100 compared to Wednesday’s sub-1.2950 trough.

- Euro is still defiant above parity vs the Buck but facing Italian political risk via a vote of no confidence.

- Aussie underpinned by upbeat labour market report and more speculation that China may lift embargo on coal, UAD/USD holds around 0.6750.

- Kiwi flanked by decent option expiry interest either side of 0.6100.

- Yuan unable to avoid broad Dollar revival, as CNH slips under 200 WMA circa 6.7330.

Fixed Income

- Debt under renewed pressure post-US CPI as 100bp hike odds continue to shorten and keep curves in bear-flattening mode

- Bunds down to 151.21 from 153.01 at best, Gilts reverse from 116.05-115.14 and 10-year T-note retreats to 118-10+ from 118-30

- Italian bonds underperform awaiting no-confidence vote in PM Draghi’s coalition Government

Commodities

- The complex is broadly pressured amid the general risk tone and ongoing USD strength, crude benchmarks lower by over USD 2.00/bbl.

- China is said to be mulling ending the Australian coal ban on Russian supply fears, according to Bloomberg.

- White House Economic Adviser Rouse said President Biden is focused on getting more oil into the market and his Saudi visit will help get more oil into the market.

- Spot gold is dented on the USD move which is far outweighing any possible haven allure thus far; base metals broadly lower.

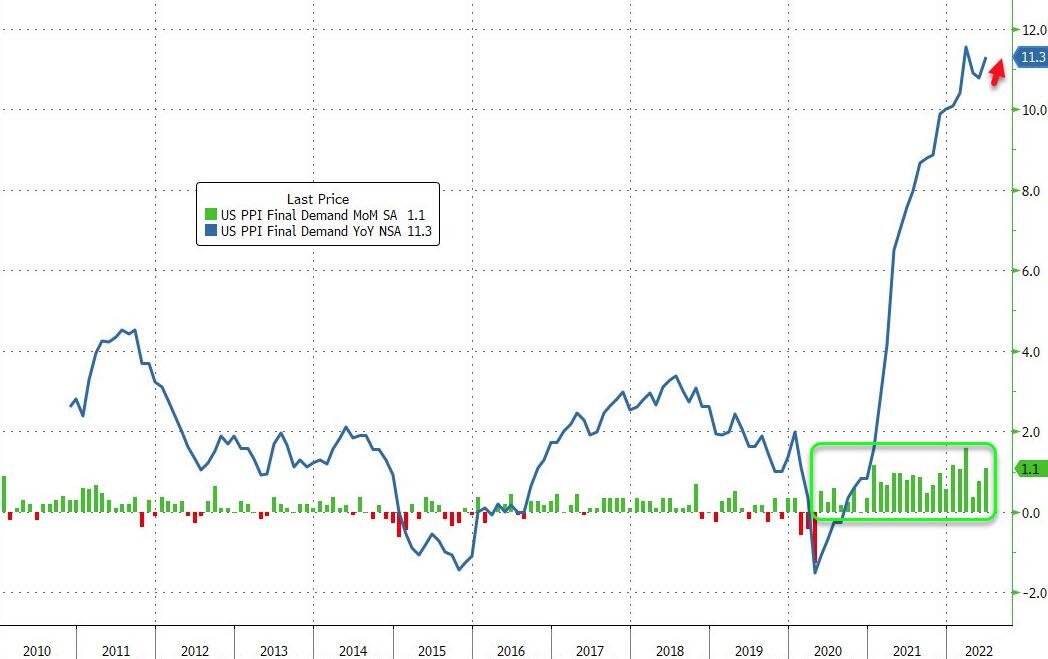

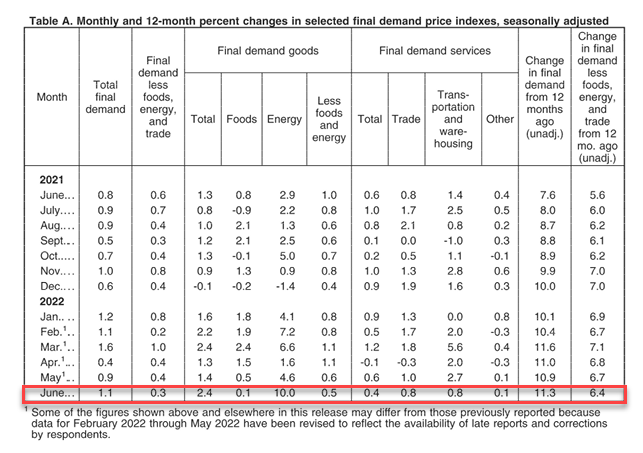

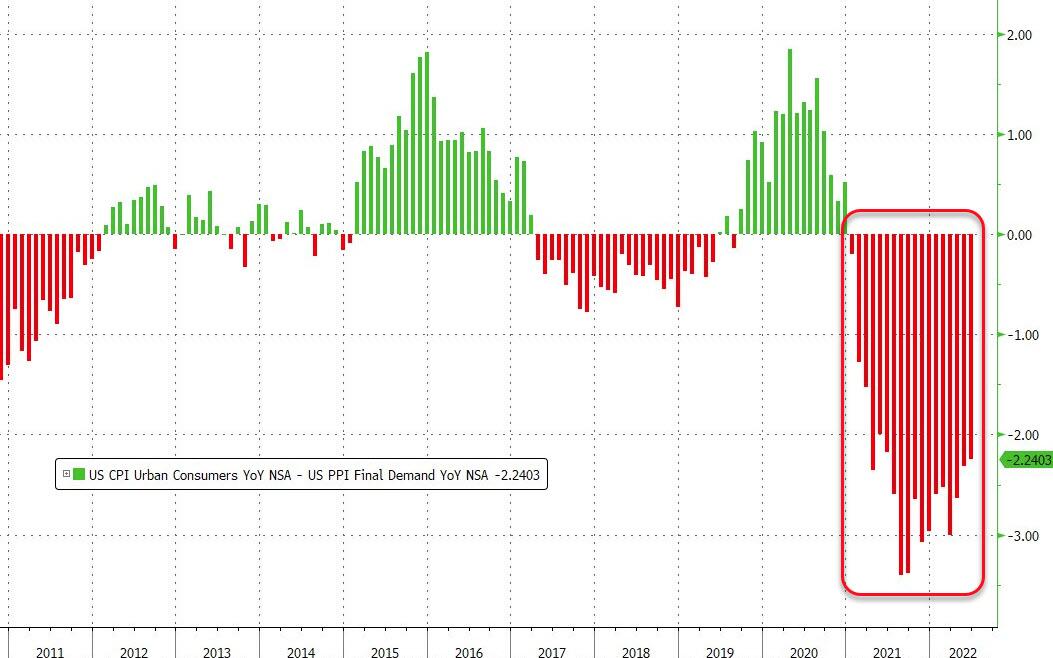

US Event Calendar

- 08:30: June PPI Final Demand YoY, est. 10.7%, prior 10.8%; MoM, est. 0.8%, prior 0.8%