by harveyorgan · in Uncategorized · Leave a comment·Edit

Uncategorized · Leave a comment·Edit

GOLD; $1757.75 DOWN $5.75

SILVER: $19.54 DOWN 27 CENTS

ACCESS MARKET:

GOLD $1758.85

SILVER: $19.54

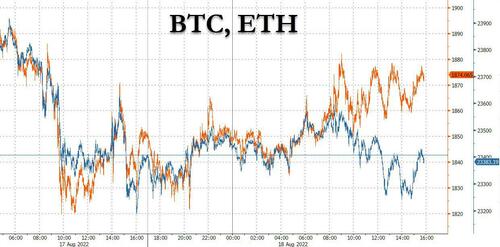

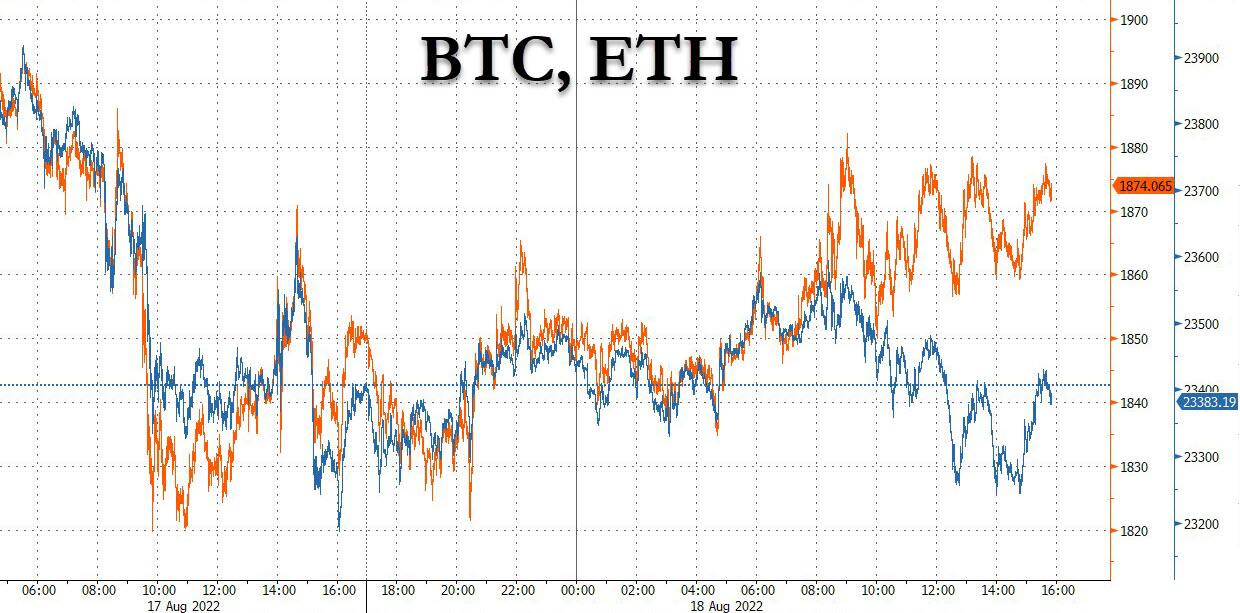

Bitcoin morning price: $23,494 UP 203

Bitcoin: afternoon price: $23,404. UP 113

Platinum price closing DOWN $9.25 AT$917.35

Palladium price; closing up $19.00 at $2157.65

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,760.300000000 USD

INTENT DATE: 08/17/2022 DELIVERY DATE: 08/19/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 3

072 H GOLDMAN 5

104 C MIZUHO 2

132 C SG AMERICAS 64

167 C MAREX 2

190 H BMO CAPITAL 1

624 H BOFA SECURITIES 38

657 C MORGAN STANLEY 3

661 C JP MORGAN 29

686 C STONEX FINANCIA 1

737 C ADVANTAGE 1

800 C MAREX SPEC 1 4

880 C CITIGROUP 149

880 H CITIGROUP 5

TOTAL: 154 154

MONTH TO DATE: 32,673

JPMorgan stopped: 29,154

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR AUGUST CONTRACT:

154 NOTICES FOR 15400 OZ //0.4790 TONNES

total notices so far: 32,673 contracts for 3,267,300 oz (101.626 tonnes)

SILVER NOTICES: 13 NOTICES FILED FOR 65,000 OZ/

total number of notices filed so far this month 936 : for 4,680,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $12.00

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.718 TONNES FROM THE GLD.

INVENTORY RESTS AT 985.83 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $0.32 CENTS

AT THE SLV// ://A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 0.369 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 485.482 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 945 CONTRACTS TO 143,369. AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN OI WAS ACCOMPLISHED WITH OUR $0.32 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.32) AND WERE SOMEWHAT SUCCESSFUL IN KNOCKING OFF SOME SPEC SILVER LONGS AS WE HAD A STRONG LOSS OF 835 CONTRACTS ON OUR TWO EXCHANGES. HOWEVER WE HAD A SOME LIQUIDATION OF SPECULATOR SHORTS.

WE MUST HAVE HAD:

I) SOME SPECULATOR SHORT LIQUIDATIONS//CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A ZERO ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A FAIR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 55,000 OZ QUEUE JUMP / // V) STRONG SIZED COMEX OI LOSS/(//SOME SPEC LIQUIDATION)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -10

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTACTS for 14 days, total 6650 contracts: 33.250 million oz OR 2.375 MILLION OZ PER DAY. (475 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 33.250 MILLION OZ

.

LAST 16 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 33.25 MILLION OZ (A LOT LESS THAN NORMAL//THE CROOKS ARE SCARED TO ISSUE MORE EFP’S)

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 945 WITH OUR $0.32 LOSS IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 100 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /SOME BANKER ADDITIONS AND SOME SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 55,000 OZ QUEUE JUMP // .. WE HAD A STRONG SIZED LOSS OF 845 OI CONTRACTS ON THE TWO EXCHANGES FOR 4.225 MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 13 NOTICE(S) FILED TODAY FOR 65,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2379 CONTRACTS TO 456,339 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:–85 CONTRACTS.

.

THE FAIR SIZED INCREASE IN COMEX OI CAME DESPITE OUR FALL IN PRICE OF $12.00//COMEX GOLD TRADING/WEDNESDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERINGS//CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 98.367 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S TINY E.F.P. JUMP TO LONDON OF 300 OZ//NEW STANDING 104.027 TONNES

YET ALL OF..THIS HAPPENED WITH OUR FALL IN PRICE OF $12.00 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 4776 OI CONTRACTS 14,855 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2397 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 456,339

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4776 CONTRACTS WITH 2379 CONTRACTS INCREASED AT THE COMEX AND 2397 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4776 CONTRACTS OR 14.885 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2397) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (2379): TOTAL GAIN IN THE TWO EXCHANGES 4776 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR AUGUST. AT 99.272 TONNES FOLLOWED BY TODAY’S E.F.P. JUMP OF 300 oz. 3) ZERO/ LONG LIQUIDATION//// //.,4) FAIR SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

33,357 CONTRACTS OR 3,335,700 OZ OR 103.97 TONNES 14 TRADING DAY(S) AND THUS AVERAGING: 2382 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 14 TRADING DAY(S) IN TONNES: 103.97 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 103.97/3550 x 100% TONNES 2.92% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 103.97 TONNES (DRAMATICALLY FALLING AGAIN)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT., FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 945 CONTRACT OI TO 143,369 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 100 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 100 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 100 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 945 CONTRACTS AND ADD TO THE 100 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF 845 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 4.225 MILLION OZ

OCCURRED WITH OUR FALL IN PRICE OF $0.32

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 14.94 PTS OR 0.46% //Hang Sang CLOSED DOWN 158.54 OR 0.80% /The Nikkei closed DOWN 280.63 OR % 0.96. //Australia’s all ordinaires CLOSED DOWN 0.32% /Chinese yuan (ONSHORE) closed DOWN AT 6.7882//OFFSHORE CHINESE YUAN DOWN 6.7946// /Oil UP TO 89.02 dollars per barrel for WTI and BRENT AT 95.04// / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 2379 CONTRACTS TO 456,339 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED WITH OUR FALL OF $12.00 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2397 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF AUGUST.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2397 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :2397 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2397 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED SIZED TOTAL OF 4776 CONTRACTS IN THAT 2397 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 2379 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR STRONG FALL IN PRICE OF GOLD $ 12.00. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING AUGUST (104.027),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.027 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $12.00) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS // COMMERCIAL LONGS ADDED TO THE POSITIONS, BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS////// WE HAVE REGISTERED A FAIR SIZED GAIN OF 5.112 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR AUGUST (104.027 TONNES)…

WE HAD –85 CONTRACTS ADDED TO COMEX TRADES. THESE WERE ADDED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 4776 CONTRACTS OR 477,600 OZ OR 14.885 TONNES

Estimated gold volume 118,234/// extremely poor/

final gold volumes/yesterday 144,897/extremely poor

INITIAL STANDINGS FOR AUGUST ’22 COMEX GOLD //AUGUST 18

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 55,085.995 oz Brinks Manfra Malca JPMorgan |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | 0 oz |

| No of oz served (contracts) today | 154 notice(s) 15,400 OZ 0.4790 TONNES |

| No of oz to be served (notices) | 772 contracts 77,200 oz 2.401 TONNES |

| Total monthly oz gold served (contracts) so far this month | 32,673 notices 3,267,300 OZ 101.626 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits niL oz

2 customer withdrawals:

4) Out of Manfra 32.151 oz (one kilobar)

ii) Out of Brinks 22,673,738 oz

iii) out of JPMorgan: 21,673.823 oz

iv)Out of Malca: 10,706.283 oz

total: 55,085.945 oz

total in tonnes: 1.71 tonnes

Adjustments: dealer to customer //1

Brinks: 96,453.000oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 926 contracts having LOST 34 contracts .

We had 31 notices served upon yesterday so we gained a TINY 3 contracts or an additional 300 oz will stand for delivery in this very active month of August.

Sept. LOST 24 contracts to 3604 contracts.

October GAINED 517 contracts UP to 39,832

We had 154 notice(s) filed today for 15,400 oz FOR THE AUGUST 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 154 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 29 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2022. contract month,

we take the total number of notices filed so far for the month (32,673) x 100 oz , to which we add the difference between the open interest for the front month of (AUGUST x926 CONTRACTS ) minus the number of notices served upon today 154 x 100 oz per contract equals 3,344,800 OZ OR 104.027 TONNES the number of TONNES standing in this active month of AUGUST.

thus the INITIAL standings for gold for the AUGUST contract month:

No of notices filed so far (32,673) x 100 oz+ (926) OI for the front month minus the number of notices served upon today (154} x 100 oz} which equals 3,344,800 oz standing OR 104.027 TONNES in this active delivery month of August.

TOTAL COMEX GOLD STANDING: 104.027 TONNES (A HUGE STANDING FOR AUGUST ( ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,320,942.458 oz 72.19 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 28,647,719.934 OZ

TOTAL REGISTERED GOLD: 14,408,882.049 OZ (448,76 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 14,238,897.885 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 12,087,940.0 OZ (REG GOLD- PLEDGED GOLD) 375.98 tonnes//rapidly declining

END

SILVER/COMEX/AUGUST 18

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 632,919.520 oz Delaware JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 732,390.646 oz Loomis Delaware |

| No of oz served today (contracts) | 13 CONTRACT(S) 65,000 OZ) |

| No of oz to be served (notices) | 50 contracts (250,000 oz) |

| Total monthly oz silver served (contracts) | 936 contracts 4,680,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i) Into Loomis: 578,912.910 0z

ii)Into Delaware: 153,417.736 oz

total deposit: 159,475.740 oz

JPMorgan has a total silver weight: 172.782 million oz/332.705 million =51.90% of comex

Comex withdrawals: 2

i) Out of Brinks 974.05 oz

ii) Out of JPMorgan: 580,932.700 oz

iii) out of JPMorgan: 626,039.370 oz

total: 632,919.570 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 55.478 MILLION OZ

TOTAL REG + ELIG. 332.705 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR AUGUST

silver open interest data:

FRONT MONTH OF AUGUST OI: 63 CONTRACTS HAVING LOST 85 CONTRACTS. WE HAD 96 NOTICES FILED ON WEDNESDAY

SO WE GAINED 11 CONTRACTS OR AN ADDITIONAL 55,000 OZ OF SILVER WILL STAND FOR DELIVERY. THE AMOUNT STANDING

WILL NOW INCREASE//(OR REMAIN CONSTANT) ON A DAILY BASIS AS BANKERS SCOUR THE PLANET FOR BADLY NEEDED SILVER.

SEPTEMBER HAD A LOSS OF 3051 CONTRACTS DOWN TO 55,177

OCTOBER LOST 2 CONTRACTS TO STAND AT 112

CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 13 for 65,000 oz

Comex volumes:50,546// est. volume today// fair

Comex volume: confirmed yesterday: 59,160 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 936 x 5,000 oz = 4,680,000 oz

to which we add the difference between the open interest for the front month of AUGUST(63) and the number of notices served upon today 13 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST./2022 contract month: 936 (notices served so far) x 5000 oz + OI for front month of AUGUST (63) – number of notices served upon today (13) x 5000 oz of silver standing for the AUGUST contract month equates 4,930,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

AUGUST 10//WITH GOLD UP $2.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES

AUGUST 9/WITH GOLD UP $6.70: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES.

AUGUST 8/WITH GOLD UP $13.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FORM THE GLD//INVENTORY RESTS AT 999.16 TONNES

AUGUST 5/WITH GOLD DOWN $14.25: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .33 TONNES FROM THE GLD////INVENTORY RESTS AT 1000.32 TONNES

AUGUST 4 WITH GOLD UP $29.00 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES FROM THE GLD///INVENTORY REST AT 1000.65 TONNES

AUGUST 2/WITH GOLD UP $3.70; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD//INVENTORY RESTS AT 1002.97 TONNES//

AUGUST 1/WITH GOLD UP $5.75: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 29//WITH GOLD UP $12.50; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1005.29 TONNES

JULY 28/WITH GOLD UP $31.25; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 27.//WITH GOLD UP $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 26/WITH GOLD DOWN $1.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.29 TONNES

JULY 25/WITH GOLD DOWN $7.85: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 1005.87 TONNES

JULY 22/WITH GOLD UP $17.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 21/WITH GOLD UP $11.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.101 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.87 TONNES

JULY 20/WITH GOLD DOWN $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1009.06 TONNES

JULY 19/WITH GOLD DOWN $.35 :BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22 TONNES FROM THE GLD//INVENTORY RESTS AT 1009.06 TONNES

JULY 18/WITH GOLD UP $7.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.28 TONNES

JULY 15/WITH GOLD DOWN $3.75:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD///INVENTORY RESTS AT 1016.89 TONNES//

JULY 14/WITH GOLD DOWN $28.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD//INVENTORY RESTS AT 1019.79 TONNES

JULY 13/WITH GOLD UP $10.55:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD//INVENTORY RESTS AT 1021.53TONNES

JULY 12/WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESS AT 1023.27 TONNES

GLD INVENTORY: 985.83 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTOT HE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 10/WITH SILVER UP 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 9/WITH SILVER DOWN 25 CENTS TODAY: TWO CHANGES IN SILVER INVENTORY AT THE SLV: FIRST: A DEPOSIT OF 461,000 OZ INTO THE SLV AND THEN A WITHDRAWAL OF 1.014 MILLION OZ..//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 8/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 5/WITH SILVER DOWN 28 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 922,000 OZ FROM THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 4 WITH SILVER UP 21 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 527,000 OZ FROM THE SLV////INVENTORY RESTS AT 486.634 MILLION OZ

AUGUST 2/WITH SILVER DOWN 21 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.504 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.161 MILLION OZ//

AUGUST 1/WITH SILVER UP 17 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE GLD: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 483.657 MILLION OZ//

JULY 29/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 461,000 OZ FROM THE SLV..//INVENTORY RESTS AT 483.657 MILLION OZ/

JULY 28/WITH SILVER UP $1.24 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 484.118 MILLION OZ/

JULY 27/.WITH SILVER UP 4 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL 11.479 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 484.118MILLION OZ//

JULY 26/WITH SILVER UP 16 CENTS: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.504 MILLION OZ FROM THE SLV//: //INVENTORY RESTS AT 495.597 MILLION OZ//

JULY 25/WITH SILVER DOWN 24 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.383 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 499.101 MILLION OZ//

JULY 22/WITH SILVER DOWN 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 500.484 MILLION OZ//

JULY 21/WITH SILVER UP 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.19 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 500.484MILLION OZ/

JULY 20/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 8.253 MILLION OZ FORM THE SLV/INVENTORY RESTS AT 507.585 MILLION OZ//

JULY 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ//

JULY 18/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 4.995 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ.

JULY 15/WITH SILVER UP 31 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 3.226 MILLION OZ FORM THE SLV//INVENTORY RESTS AT 510.443 MILLIONOZ//

JULY 14/WITH SILVER DOWN 88 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 OZ FROM THE SLV// //INVENTORY RESTS AT 513.671 MILLION OZ

JULY 13/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SV//INVENTORY RESTS AT 514.501 MILLION OZ.

JULY 12/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.228 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 514.501 MILLION OZ//

CLOSING INVENTORY 485.482 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

3.Chris Powell of GATA provides to us very important physical commentaries

How commodity fraud works in China

(zerohedge)

Bloomberg details how commodity fraud works but of course omits gold

Submitted by admin on Wed, 2022-08-17 11:43Section: Daily Dispatches

“Overpledging” goes far beyond copper trading.

* * *

Why Metals Keep Going Missing in Commodity Trading

From Bloomberg News

Tuesday, August 16, 2022

A group of Chinese traders discovered in August that a copper merchant in northern China wasn’t holding the half a billion dollars’ worth of ore that was meant to be their collateral. This followed an episode in June involving missing aluminum.

The incidents highlight rising risks in commodity financing as China’s growth model is tested. And they carry disturbing echoes of a much bigger scandal eight years ago — the Qingdao fraud — that triggered a sweeping overhaul of the commodities business at international banks and trading houses.

How could a stockpile go missing?

There are several ways things can go awry.

Commodities trading, whether that’s wheat, copper, or oil, is typically a high-volume, low-margin business. To fund purchases and optimize cash flow, traders take out loans backed by the commodity they’re trading.

In the metals business, that collateral is often in the form of so-called warehouse warrants or receipts, which record details like the quantity, quality, ownership, and location of the goods.

The dependence on paper makes an easy target for fraud.

Warrants can be faked, using fictitious material. A single pile of metal can be collateralized for multiple loans — often known as over-pledging.

Or a stretched trader might simply sell on the goods to which the lenders have a claim, without paying back the loan.

There’s a rich record of risk and fraud stretching back through the history of global commodities trading. …

… For the remainder of the report:

END

4. OTHER GOLD/SILVER COMMENTARIES

(courtesy Market Watch)

China is importing a huge 80 tonnes of gold last month from Switzerland (refined gold)

Swiss gold exports to China surge to 5-1/2-year high

LONDON, Aug 18 (Reuters) – Swiss exports of gold to China in July rose to their highest since December 2016, Swiss customs data showed on Thursday, as demand in the world’s largest bullion market improved.

Switzerland shipped 80.1 tonnes of gold worth 4.4 billion Swiss francs ($4.6 billion) to mainland China, up from 32.5 tonnes in June and the second-highest monthly total in figures that stretch back to 2012.

Gold prices slipped below $1,700 an ounce in July from more than $2,000 earlier in the year as rising interest rates triggered selling by Western investors.

Retail consumers in markets like China often buy less when prices rise and more when they fall. China had also in July emerged from COVID-19 lockdowns earlier in the year.

The surge in shipments to China lifted Switzerland’s total gold exports to 186.2 tonnes in July, again the most since 2016.

Switzerland is the biggest refining and transit hub for gold and its data offer insight into global market trends.

It shipped 15.8 tonnes of gold in July to India, another top bullion consumer, up from 7.7 tonnes in June but only around half the monthly average over the last year.

The customs data also showed that Switzerland imported 261 kg of gold from Russia, taking the total imported during May, June and July to 3.6 tonnes worth 225 million Swiss francs ($235 million).

Customs authorities have said the imports in May and June were of Russian gold but that the metal came from Britain, a major gold storage centre. They said they had no evidence that the gold was produced after Russia invaded Ukraine.

-END-

5.OTHER COMMODITIES: USA/COTTON

end

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

end

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7802

OFFSHORE YUAN: 6.7946

HANG SENG CLOSED DOWN 158.54 PTS OR 0.80%

2. Nikkei closed DOWN 158.54 OR 0.96%

3. Europe stocks CLOSED ALL GREEN

USA dollar INDEX DOWN TO 106.41/Euro FALLS TO 1.0187

3b Japan 10 YR bond yield: RISES TO. +.197/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 134.95/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.092%/Italian 10 Yr bond yield FALLS to 3.32% /SPAIN 10 YR BOND YIELD RISES TO 2.24%…

3i Greek 10 year bond yield RISES TO 3.53//

3j Gold at $1770.50 silver at: 19.90 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1 AND 34/100 roubles/dollar; ROUBLE AT 59.41//RUSSIAN GOLD IN USA $2617.00

3m oil into the 89 dollar handle for WTI and 95 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 134.95DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9517– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9698well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.8693 DOWN 3 BASIS PTS

USA 30 YR BOND YIELD: 3.132 DOWN 1 BASIS PTS

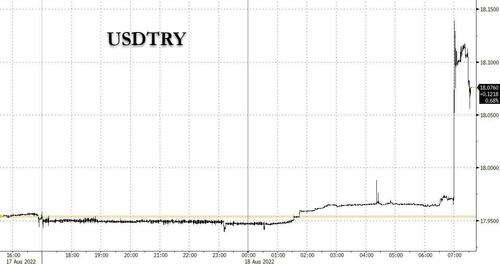

USA DOLLAR VS TURKISH LIRA: 18,09

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Levitate Higher After China Vows To Accelerate Reopening

THURSDAY, AUG 18, 2022 – 08:18 AM

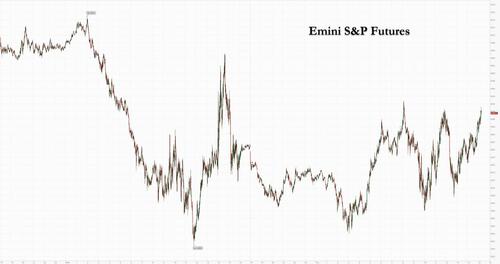

US futures were flat as the Fed minutes did not help resolve the uncertainty about the path of Federal Reserve monetary tightening, while fresh prospects about China’s economic reopening sent oil higher. Nasdaq 100 and S&P 500 futures were up 0.2% at 745am ET having recovered from an earlier loss, as traders assessed minutes from the Fed’s last meeting which noted that officials saw risks from tightening more than necessary even as they planned on hiking until inflation was on a steady downward slope, while President Xi Jinping’s comments that China will persist with opening up its economy were also in focus and boosted commodities. The dollar gave up gains, and Treasury yields dipped, reversing some of this week’s sharp gains. Bitcoin traded in a tight range around $23,500.

In US premarket trading, Cisco Systems advanced after issuing an upbeat forecast for quarterly sales as chip-supply shortages ease and the company is able to fill more orders. Keep an eye on US building products stocks as Deutsche Bank initiates coverage on 22 names, saying the US housing market is in the midst of a “mid-cycle crisis,” but that this is likely to be different from the downturn seen in the mid-2000s. Here are some other notable premarket movers:

- Bluebird Bio’s (BLUE) shares rise as much as 10% as analysts digest yesterday’s FDA clearance of its Zynteglo therapy, ahead of its launch call due later today.

- BJ’s Wholesale (BJ) shares gain 6% after the warehouse club operator reported adjusted earnings per share for the second quarter that beat the average analyst estimate.

- Cisco Systems (CSCO) rose 6% after issuing an upbeat forecast for quarterly sales as chip-supply shortages ease and the company is able to fill more orders.

- Elanco Animal Health (ELAN) cut to equal-weight from overweight at Morgan Stanley as visibility on the firm’s outlook remains weak. Elanco shares fall 1.7% in US premarket trading.

- Estee Lauder (EL) falls 1.3% after the beauty company’s forecasts for first quarter and the full year trailed consensus estimates. In Europe, shares of L’Oreal declined after EL’s release.

- Five months after disclosing a stake in Bed Bath & Beyond Inc., (BBBY) activist shareholder Ryan Cohen wants out, sparking a selloff in the shares of the home goods retailer. Shares fall 13%.

- Kohl’s (KSS) drops 7% after slashing its guidance for the year, including adjusted earnings per share, operating margin and net sales growth. Peer Macy’s (M), which reports Aug. 23, falls 3%.

- Mattel (MAT) rises 0.8% after it was initiated with a buy rating at BofA, which said that the company has “successfully” completed its turnaround and is now in growth mode.

- MoffettNathanson cut the recommendation on Verizon Communications Inc. (VZ) to underperform from market perform, as T-Mobile widens its competitive advantage in 5G and AT&T undercuts it with aggressive promotions. Verizon shares fall 0.8%.

- NetEase (NTES) shares rise as much as 3% after the Chinese video-game giant’s 2Q revenue came in slightly above the consensus analyst estimate.

- NuScale Power (SMR) was initiated with a recommendation of buy at Guggenheim Securities, as analyst Shahriar Pourreza says its “shares represent one of the only opportunities for public exposure to the next generation of nuclear.” Shares gain 4%.

While policy makers warned against over-tightening and signaled the potential for slower rate increases at some point, they also flagged the risk of inflation pressures becoming entrenched. The nuanced messaging wasn’t dovish enough for markets to sustain a risk-on stance into Thursday. Caution was the byword of the moment with further clues awaited at the Fed’s annual symposium in Jackson Hole, Wyoming next week.

“People are a little overly optimistic about how likely it is that we can solve the inflation problem quickly and in a way where we don’t have to include more policy and more rising rates,” Kathryn Kaminski, AlphaSimplex Group chief research strategist and portfolio manager, said on Bloomberg Television.

While most saw the FOMC minutes as dovish, others disagreed. According to Ipek Ozkardeskaya, a senior analyst at Swissquote, the Fed meeting minutes were more hawkish than what was needed to give another boost to US equities. “Investors quickly realized that there was no mention of cutting the rates in the foreseeable future. If anything, the Fed would continue lifting the rates, and keep them steady for a while.”

Equities had rallied in recent weeks as investors bet July’s softer inflation print would allow the Fed to rethink its aggressive pace of hiking rates. The Nasdaq 100 had led the advance amid relief at the prospect of easier policy, boosted by raging CTA buying, stock buybacks, a return of retail investors and hedge funds forced to FOMO-chase higher.

“This rally is over-extended in the technology sector,” said Freddie Lait, chief investment officer at Latitude Investment Management. “The relative valuation of most of those Nasdaq stocks compared to other stocks around the world has become extreme again, and positioning has become quite extreme again, and so I wouldn’t be surprised to see that rolling over into the end of the summer.” The Nasdaq 100 is now trading at 23.2 times forward earnings, above the average level of 20.2 times over the past decade.

In Europe, the Stoxx 600 index was 0.2% higher as the latest report of euro-area inflation met expectations, sparing traders of any ugly surprise. FTSE MIB outperforms, adding 0.4%, IBEX lags, dropping 0.2%. Autos, energy and chemicals are the strongest-performing sectors. Concerns of tightening monetary conditions increased after the European Central Bank’s Governing Council member Martins Kazaks said rate hikes will continue in the region. Thin trading exaggerated moves across markets. The Stoxx 600 witnessed a 33% drop in volumes relative to the 30-day average. Here are the biggest European movers:

- Siegfried shares jump as much as 13%, the most since October 1998, after 1H results analysts say were a significant beat, also noting effective management of macro risks.

- GN Store Nord shares rise as much as 10% after the Danish audio firm presented its latest earnings, which included a guidance cut that was less pessimistic than analysts expected.

- Zur Rose shares rise as much as 14%, the most since May, after its latest earnings report, which includes a goal to be profitable in 2023, a plan Jefferies call “very positive.”

- Nibe rise as much as 8.6% after the Swedish heat pump manufacturer published earnings. Analysts note solid results, which beat expectations, as well as a positive outlook.

- Global Fashion Group shares rise as much as 31%, the most intraday on record, after reporting better-than-expected earnings for the second quarter, also offering some FY clarity.

- Balfour Beatty shares rise as much as 3.8% after Peel Hunt further raised FY22 profit forecasts for the UK construction and engineering firm and saw scope for material share price upside.

- Adyen shares tumble the most since 2018 as 1H Ebitda and net revenue missed consensus analyst forecasts. Analysts point out that accelerated hiring is also a cause of Ebitda miss.

- AutoStore shares wipe out an earlier jump of 13% to fall as much as 6.8%. Analysts say results look strong, albeit they note a small miss on orders and guidance for more margin pressure in 2H.

- Made.com shares drop as much as 12%, biggest decliner in the FTSE All-Share Index, after the online furniture seller said it’s considering “all options” to strengthen its balance sheet.

Earlier in the session, Asian stocks fell as disappointing results from some key Chinese firms and worries about the outlook for the region’s biggest economy weighed on investor sentiment. The MSCI Asia Pacific Index slipped as much as 0.7%, with benchmarks in the biggest markets of Japan and China down close to 1%. Risk appetite improved a smidge after President Xi Jinping said China will persist with opening up its economy, the comments coming in after the nation’s markets closed. China’s largest developer Country Garden Holdings, saw its stock slump after it warned that first-half earnings probably tumbled by as much as 70% amid an escalating property crisis. Tencent, the nation’s most-valuable company, logged its first-ever revenue drop though its shares — which have fallen for three straight months — advanced.

Thursday’s losses in Asia tracked declines in US shares overnight. Minutes of the Fed’s latest meeting showed that officials agreed on the need to eventually dial back the pace of interest-rate hikes but also wanted to gauge how their monetary tightening was working toward curbing US inflation. The minutes “lacked fresh impetus needed to bring up the pricing of Fed’s rate hikes,” Saxo Capital Markets’ Asia-Pacific strategy team wrote in a note. “Chairman Powell’s speech at the Jackson Hole Symposium next week will be keenly watched for further inputs.” Meanwhile, consumer discretionary and technology were among the worst-performing sectors on the Asian benchmark. Goldman Sachs and Nomura further cut their forecasts for China’s economic growth, with a power supply crunch adding more uncertainty to the outlook.

Japanese stocks fell, following US peers lower after minutes from the Federal Reserve’s last meeting showed officials see risks from tightening more than necessary. The Topix fell 0.8% to close at 1,990.50, while the Nikkei declined 1% to 28,942.14. Toyota Motor Corp. contributed the most to the Topix decline, decreasing 1.8%. Out of 2,170 shares in the index, 565 rose and 1,503 fell, while 102 were unchanged.

Australia’s S&P/ASX 200 index fell 0.2% to close at 7,112.80 as investors assessed a slew of corporate results and jobs data. Australian employment unexpectedly dropped in July, giving the Reserve Bank scope for more flexibility in its tightening cycle. Telix Pharma slumped after reporting a net loss for the first half. IPH was the top performer after saying it’s buying Canadian firm Smart & Biggar. In New Zealand, the S&P/NZX 50 index fell 0.3% to 11,814.34.

In FX, the Bloomberg Dollar Spot Index advanced a second day and the greenback rose versus most of its Group-of-10 peers, with Norway’s krone as the best performer. The euro traded in a narrow range against the dollar for a third consecutive day. Norway’s krone extended an advance versus the euro after Norges Bank raised the key interest rate to 1.75% from 1.25%, in line with what most economists in a Bloomberg survey had expected. The central bank also said the policy rate “will most likely be raised further in September.” The pound extended losses against the dollar, hitting the lowest since July 26, amid broad-based greenback strength.

The yen fell in a volatile session as traders mulled rising US yields and their negative impact on stocks. Japan’s government bond yields rose

In rates, Treasuries were slightly richer across the curve with gains led by long-end, having outperformed bunds and gilts during European morning. US yields richer by ~2bp across long-end of the curve with 5s30s spread flatter by ~1bp on the day; 10-year yields around 2.87% within narrow overnight range, outperforming bunds by 4bp in the sector. Front-end German yields lag after ECB’s Isabel Schnabel says the euro area’s inflation outlook has not changed fundamentally. Bunds bear-flattened out to the 10-year sector as money markets added to ECB tightening bets after the ECB’s Schnabel said the euro area’s inflation outlook has not changed fundamentally, in an interview cited by Reuters, suggesting that another hike of similar magnitude may be coming next month. Australia’s bond yields trimmed opening gains and the nation’s currency eased after employment contracted for the first time since October 2021.

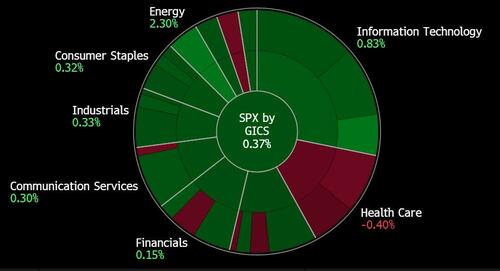

In commodities, oil jumps to session high after Xi says China will persist with opening up its economy. WTI rises 1.5% to trade around $89. Spot gold rises roughly $4 to trade near $1,766/oz. Most base metals trade in the red; LME nickel falls 0.5%, underperforming peers. LME copper outperforms, adding 1%, after Xi’s comments

Looking at the day ahead, the FOMC minutes from July will be the main highlight, and the other central bank speaker will be Fed Governor Bowman. Otherwise, earnings releases include Target, Lowe’s and Cisco Systems, and data releases include US retail sales and UK CPI for July.

Market Snapshot

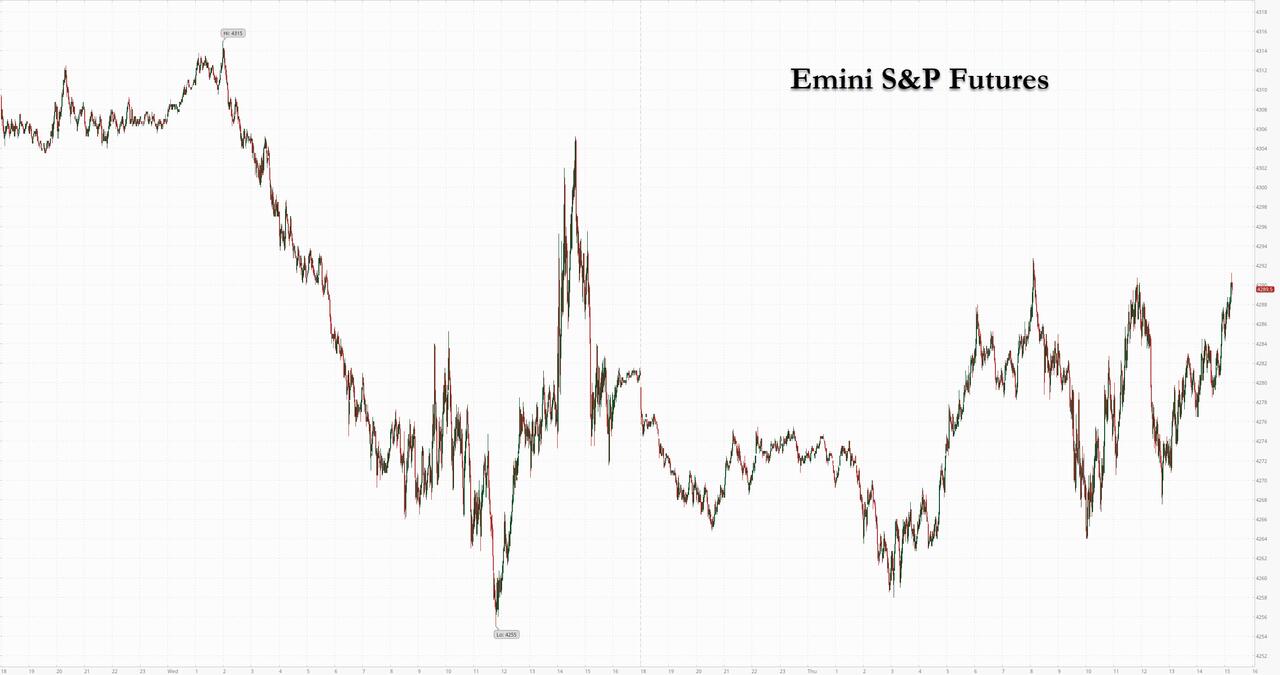

- S&P 500 futures down 0.3% to 4,265.50

- STOXX Europe 600 down 0.1% to 438.54

- MXAP down 0.6% to 161.98

- MXAPJ down 0.5% to 526.40

- Nikkei down 1.0% to 28,942.14

- Topix down 0.8% to 1,990.50

- Hang Seng Index down 0.8% to 19,763.91

- Shanghai Composite down 0.5% to 3,277.54

- Sensex down 0.3% to 60,079.59

- Australia S&P/ASX 200 down 0.2% to 7,112.78

- Kospi down 0.3% to 2,508.05

- German 10Y yield little changed at 1.11%

- Euro down 0.1% to $1.0165

- Gold spot up 0.1% to $1,763.18

- U.S. Dollar Index up 0.20% to 106.79

Top Overnight News from Bloomberg

- Biden Freeze on Oil and Gas Leasing Is Reinstated for Now

- China Plans More Fiscal Stimulus as Economy Outlook Darkens

- China Attacks US Chip Handouts While Warning of Market Slowdown

- China’s Covid Cases Surge to Three-Month High on Hainan Outbreak

- PetroChina Said to Consider Spinoff of Energy Marketing Business

- Russia’s Sakhalin-2 LNG Plant Asks Buyers to Pay Gazprombank

- Rhine Reopens gin Germany for Vessels Moving Goods Upstream

- Adyen Shares Slump as Travel Costs Hits First-Half Results

- NetEase Shares Rise After 2Q Revenue Meets Estimates

- Swiss Watch Exports at Near-Record Levels as Industry Booms

- Abu Dhabi AI Firm Sets Up $10 Billion Fund for Tech Deals

- Singapore to Be Asia’s Millionaire Capital by 2030, HSBC Says

- Peter Thiel’s Planned Luxury Tourist Lodge in NZ Thwarted

- Investment Bank Behind 32,000% IPO Probed by Hong Kong Regulator

- Trump Warrant Judge Urged to Release Most of FBI Affidavit

- Covid’s Harmful Effects on the Brain Reverberate Years Later

- After 2,240% Run, Tesla Visionary Leaves UK Fund Bleeding Money

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly declined following the weak handover from global counterparts which were pressured as yields climbed on the back of the red-hot UK inflation data and with only a brief reprieve seen after the FOMC Minutes noted many officials saw a risk the Fed could tighten more than necessary. ASX 200 was subdued as participants digested the latest influx of earnings releases and disappointing jobs data which showed a surprise contraction in headline Employment Change. Nikkei 225 slipped back beneath the 29,000 level in tandem with the overall downbeat sentiment. Hang Seng and Shanghai Comp conformed to the glum mood after both Goldman Sachs and Nomura cut their China GDP growth forecasts and with focus also on earnings releases including Tencent after it posted its first-ever decline in quarterly revenue although its shares were lifted and it had vowed a return to growth, while Country Garden led the declines after the developer issued a profit warning of as much as an 87% drop in H1 net.

Top Asian News

- China may issue CNY 1.5tln in additional debt as part of an investment push, according to China Securities News.

- China’s COVID-19 cases rose to a 3-month high of 3,424 on Wednesday from 2,888 the day before.

- Nomura cut its China 2022 GDP growth forecast to 2.8% from 3.3%.

- China’s MOFCOM says, re. US CHIPS act, some provisions restrict normal economic, trade and investment activities of relevant enterprises in China. Will, when necessary, take forceful measures to safeguard interests.

- China’s President Xi says they will persist with opening up the economy, via CCTV.

- China’s banking regulator is reportedly looking into the property sector loan portfolios of some local/foreign lenders to assess systemic risk, via Reuters citing sources.

European bourses began the session mixed/flat and are yet to gain any real traction in relatively limited newsflow, Euro Stoxx 50 +0.5%. Though, it is worth pointing out DAX 40 +1.0% outperformance, after lagging on Wednesday, amid strength in their heavyweight industry names. Stateside, performance is similar ahead of a few corporate updates, data and Fed speak, ES +0.1%

Top European News

- The FTSE 100’s Weirdly Good Run of Form Hits a Wall of Problems

- Norway Raises Rates to Highest in Decade to Stem Inflation

- Embracer CEO Eyes IP Windfall After Buying ‘Lord of the Rings’

- PwC Raises UK Partner Pay to £1 Million for First Time

- ‘Enough Is Enough’ Rally Pulls UK Crowds as Rail Strike Begins

- Truss Planning Review of Regulators in City of London Shakeup

FX

- Buck bounces after brief post-FOMC minutes dip on dovish elements, DXY touches Fib at 106.960 from 106.500 low.

- Euro derives more support from rising EGB yields amidst hawkish ECB commentary, EUR/USD holds around 1.0150 amidst raft of option expiries extending beyond 1.0200.

- Norwegian Krona underpinned by another half point hike from Norges Bank and signal for further tightening in September, EUR/NOK towards base of 9.8550-9.9150 range.

- Aussie finds support at psychological level against Greenback after mixed jobs data, but Kiwi cautious ahead of NZ trade, AUD/USD nearer 0.6950 than 0.6900, NZD/USD closer to 0.6250 than 0.6300.

- Sterling still stunned by double digit UK CPI and economic ramifications, Cable ducks under 1.2000, albeit fractionally and briefly.

- Loonie gleans some traction from firmer oil prices pre-Canadian PPI, USD/CAD closer to 1.2900 than 1.2950.

- Yuan retreats amidst reports of property loan portfolio probes and PBoC LPR cuts, USD/CNY 6.7900+ and USD/CNH 6.8000+.

Fixed Income

- EGBs and Gilts regain some poise after extended and heavy declines on hawkish ECB rhetoric.

- Bunds back up near 154.00 within 154.47-153.24 range, UK benchmark 114.00+ between 114.41-113.63 parameters.

- US Treasuries idling post-FOMC minutes and pre-busy agenda – 10 year T-note flat at 118.24+ vs 119-01+ high and 118-18 low.

Commodities

- WTI and Brent were bolstered by rhetoric from the Russian Defence Ministry re. Zaporizhia and as China’s President Xi spoke

- Currently, the benchmarks are in proximity to their respective highs of USD 89.56/bbl and USD 95.44/bbl.

- Spot gold experienced a marginal haven bid bringing the yellow metal to an incremental new session peak of USD 1767/oz and eclipsing the 21-DMA at USD 1764/oz.

- Broader metal space is mixed and features essentially unchanged action for Aluminium, after Wednesday’s noted rally, while LME Copper has climbed back towards a test of the USD 8k handle

Central Banks

- ECB’s Schnabel says a recession alone would not be enough to control inflation, growth is going to slow and a technical EZ recession is possible. Inflation concerns from before the July hike have not alleviated, outlook is unchanged. Number of indicators point to a de-anchoring of inflation expectations. Short-term inflation could still accelerate. Re. fragmentation: markets are more stable now, but volatility is elevated and liquidity is low.

- Norwegian Key Policy Rate 1.75% vs. Exp. 1.75% (Prev. 1.25%) via a unanimous decision; policy rate will most likely be raised further in September. Click here for reaction & newsquawk analysis.

- BoE will aim to unwind the full stock of Corporate Bond Purchase Scheme (CBPS) holdings at end-2023/early-2024, subject to market conditions.

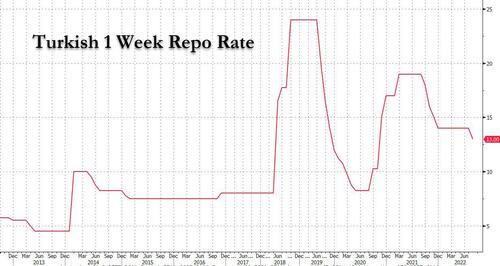

- Turkey’s central bank shocked markets when it unexpectedly cut rates by 100bps to 13% from 14%. All 21 economists polled by Bloomberg had expected an unchanged print.

DB’s Tim Wessel concludes the overnight wrap

Starting in Europe, where the looming energy crisis remains at the forefront. An update from our team, who just published the fourth edition of their indispensable gas monitor (link here), where they note the surprisingly fast rebuild of German gas storage, driven by reductions in industrial activity, reduces the risk that rationing may become reality this winter. Many more insights within, so do read the full piece for analysis spanning scenarios. Keep in mind, that while gas may be available, it is set to come at a higher clearing price, which manifest itself in markets yesterday where European natural gas futures rose a further +2.64% to €226 per megawatt-hour, just shy of their closing record at €227 in March. But, that’s still well beneath their intraday high from March, where at one point they traded at €345. Further, one-year German power futures increased +6.30%, breaching €500 for the first time, closing at €507. Germany is weighing consumer relief measures in light of climbing consumer prices and also announced that planned nuclear facility closures would be “temporarily” postponed.

The upward energy price pressure and attenuated (albeit, not eliminated) risk of rationing pushed European sovereign yields higher. 10yr German bunds climbed +7.1bps to 0.97%, while 10yr OATs kept the pace, increasing +7.4bps. 10yr BTPs increased +15.9bps, widening sovereign spreads, while high yield crossover spreads widened +10.2bps in the credit space.

Equities were resilient, however, with the STOXX 600 posting a +0.16% gain after flitting around a narrow range all day. Regional indices were also robust to climbing energy prices, with the DAX up +0.68% and the CAC +0.34% higher. In the States the S&P 500 registered a modest +0.19% gain, with the NASDAQ mirroring the index, falling -0.19%. Retail shares drove the S&P on the day, with the two consumer sectors both gaining more than +1%, following strong earnings reports from Wal Mart and Home Depot.

Treasury yields also climbed, but the story was the further flattening in the curve. 2yr yields were +7.5bps higher while 10yr yields managed to increase just +1.6bps, leaving 2s10s at its second most negative close of the cycle at -46bps. 10yr yields are another basis point higher this morning. A hodgepodge of data painted a mixed picture. Housing permits beat expectations (+1674k vs. +1640k) while starts (+1446k vs. +1527k) fell to their slowest pace since February 2021. However, under the hood, even permits weren’t necessarily as strong as first glance, as single family permits fell -4.3% with gains in multifamily pushing the aggregate higher. Indeed, year-over-year, single family permits have now fallen -11.7% while multifamily permits are +23.5% higher. So the single family housing market continues to feel the impact of Fed tightening. Meanwhile, industrial production climbed +0.6% month-over-month (vs. +0.3%), with capacity utilization hitting its highest level since 2008 at 80.3%.

Drifting north of the border, Canadian inflation slowed to 7.6% YoY in July in line with estimates, while the average of core measures climbed to a record 5.3%. Bank of Canada Governor Macklem penned an opinion piece saying that while it looks like inflation may have peaked, “the bad news is that inflation will likely remain too high for some time.” In turn, Canadian OIS rates by December climbed +16.2bps.

In other data, the expectations component of the German ZEW survey fell to -55.3, its lowest level since October 2008 at the depths of the GFC. In the UK, regular pay (excluding bonuses) fell by -3.0% in real terms over the year to April-June 2022, its fastest decline on record.

On the Iranian nuclear deal, EU negotiators reportedly found Iran’s response constructive, though Iran still had some concerns. Notably, Iran is looking for guarantees that if a future US administration withdraws from the JCPOA the US will “have to pay a price”, seeking insulation from the vagaries of representative democracy.

Asian equity markets are trading higher after Wall Street’s solid performance overnight. The Nikkei (+0.76%) is leading gains across the region with the Hang Seng (+0.57%), the Shanghai Composite (+0.23%) and the CSI (+0.51%) all rebounding from its opening losses this morning. US futures are struggling to gain traction this morning with the S&P 500 (-0.02%) and NASDAQ 100 (-0.09%) trading just below flat.

The Reserve Bank of New Zealand lifted its official cash rate (OCR) for the fourth consecutive time by an expected +50bps to 3%, a seven-year high, while bringing forward the estimate of future rate increases. The central bank expects the OCR will reach 3.69% at the end of this year and expects it to peak at 4.1% in March 2023, higher and sooner than previously forecast.

Early morning data coming out from Japan showed that exports rose +19.0% y/y in July (v/s +17.6% expected) posting 17 straight months of gains while imports advanced +47.2% (v/s +45.5% expected) driven by global fuel inflation and a weakening yen. With the imports outweighing exports, the nation reported trade deficit for the 14th consecutive month, swelling to -2.13 trillion yen in July (v/s -1.91 trillion yen expected) compared to a revised deficit of -1.95 trillion yen in June.

In terms of the day ahead, the FOMC minutes from July will be the main highlight, and the other central bank speaker will be Fed Governor Bowman. Otherwise, earnings releases include Target, Lowe’s and Cisco Systems, and data releases include US retail sales and UK CPI for July.

END

AND NOW NEWSQUAWK

Crude climbs amid Russian rhetoric, Fixed steady after Schnabel induced pressure – Newsquawk US Market Open

THURSDAY, AUG 18, 2022 – 06:44 AM

- European bourses began the session mixed/flat and are yet to gain any real traction in relatively limited newsflow, Euro Stoxx 50 +0.5%.

- Stateside, performance is similar ahead of a few corporate updates, data and Fed speak, ES +0.1%

- WTI and Brent were bolstered by rhetoric from the Russian Defence Ministry re. Zaporizhia and as China’s President Xi spoke

- Spot gold experienced a marginal haven bid while broader metals are more mixed.

- DXY lifted to near 107.00, EUR relatively resilient amid hawkish Schnabel commentary while NOK climbs post-Norges

- Core fixed have stabilised after initial pronounced pressure in Bunds on ECB rhetoric USTs essentially unchanged

- Looking ahead, highlights include US IJC, Philadelphia Fed, Existing Home Sales, New Zealand Trade Balance, CBRT Policy Announcement Speeches from Fed’s George, Fed’s Kashkari & ECB’s Schnabel.

As of 11:15BST/06:15ET

For the full report and more content like this check out Newsquawk.

Try a 14 day trial with Newsquawk and hear breaking trading news as it happens.

LOOKING AHEAD

- US IJC, Philadelphia Fed, Existing Home Sales, New Zealand Trade Balance, CBRT Policy Announcement Speeches from Fed’s George, Fed’s Kashkari & ECB’s Schnabel.

- Click here for the Week Ahead preview.

GEOPOLITICS

RUSSIA-UKRAINE

- US senior administration official said the US supports Ukraine conducting strikes on Russian-occupied Crimea if Kyiv deems it is necessary, according to Politico.

- Russia’s Defence Ministry says Ukraine is preparing a ‘provocation’ at the Zaporizhzhia nuclear plant on August 19th. Subsequently, saying the Zaporizhia nuclear plant could be shut down if Ukraine continues shelling, via Ria and that back-up support systems at the nuclear site have been damaged by shelling activity. In the event of an accident at the plant, radioactive substances will cover Poland, Germany and Slovakia.

- Russian President Putin hinted he could meet with Ukrainian President Zelensky, via CNN Turk citing Russian sources; hint reportedly occurred at the August 5th Sochi summit, when Putin met Turkish President Erdogan.

- EU Foreign Ministers to discuss on August 31st possible visa code changes for a considerable reduction in the issuance of visa’s to Russians, via Nexta.

TAIWAN

- US top diplomat for East Asia Kritenbrink said China overreacted and that several warships remain around Taiwan, while he expects China’s pressure campaign around Taiwan to continue and said the US remains committed to the One China policy. Furthermore, he noted the US approach on Taiwan has remained consistent and that they do not support Taiwan’s independence, but added that what has changed is Beijing’s increasing coercion and that China’s words and actions are deeply destabilising.

- US and Taiwan are to begin formal trade talks “early this fall, according to Bloomberg.

OTHER NEWS

- US and South Korea’s joint statement noted that their expanding military drills point to closer bilateral ties and said the next North Korean nuclear test could lead the US to deploy strategic assets to South Korea, according to SCMP.

EUROPEAN TRADE

CENTRAL BANKS

- ECB’s Schnabel says a recession alone would not be enough to control inflation, growth is going to slow and a technical EZ recession is possible. Inflation concerns from before the July hike have not alleviated, outlook is unchanged. Number of indicators point to a de-anchoring of inflation expectations. Short-term inflation could still accelerate. Re. fragmentation: markets are more stable now, but volatility is elevated and liquidity is low.

- Norwegian Key Policy Rate 1.75% vs. Exp. 1.75% (Prev. 1.25%) via a unanimous decision; policy rate will most likely be raised further in September. Click here for reaction & newsquawk analysis.

- BoE will aim to unwind the full stock of Corporate Bond Purchase Scheme (CBPS) holdings at end-2023/early-2024, subject to market conditions.

EQUITIES

- European bourses began the session mixed/flat and are yet to gain any real traction in relatively limited newsflow, Euro Stoxx 50 +0.5%.

- Though, it is worth pointing out DAX 40 +1.0% outperformance, after lagging on Wednesday, amid strength in their heavyweight industry names.

- Stateside, performance is similar ahead of a few corporate updates, data and Fed speak, ES +0.1%

- Click here for more detail.

FX

- Buck bounces after brief post-FOMC minutes dip on dovish elements, DXY touches Fib at 106.960 from 106.500 low.

- Euro derives more support from rising EGB yields amidst hawkish ECB commentary, EUR/USD holds around 1.0150 amidst raft of option expiries extending beyond 1.0200.

- Norwegian Krona underpinned by another half point hike from Norges Bank and signal for further tightening in September, EUR/NOK towards base of 9.8550-9.9150 range.

- Aussie finds support at psychological level against Greenback after mixed jobs data, but Kiwi cautious ahead of NZ trade, AUD/USD nearer 0.6950 than 0.6900, NZD/USD closer to 0.6250 than 0.6300.

- Sterling still stunned by double digit UK CPI and economic ramifications, Cable ducks under 1.2000, albeit fractionally and briefly.

- Loonie gleans some traction from firmer oil prices pre-Canadian PPI, USD/CAD closer to 1.2900 than 1.2950.

- Yuan retreats amidst reports of property loan portfolio probes and PBoC LPR cuts, USD/CNY 6.7900+ and USD/CNH 6.8000+.

- Click herefor more detail.

Notable FX Expiries, NY Cut:

- EUR/USD: 1.0145-55 (1.61BN), 1.0165-75 (1.61BN), 1.0185 (265M), 1.0200-05 (1.81BN), 1.0215-25 (1.82BN)

- Click here for more detail.

FIXED INCOME

- EGBs and Gilts regain some poise after extended and heavy declines on hawkish ECB rhetoric.

- Bunds back up near 154.00 within 154.47-153.24 range, UK benchmark 114.00+ between 114.41-113.63 parameters.

- US Treasuries idling post-FOMC minutes and pre-busy agenda – 10 year T-note flat at 118.24+ vs 119-01+ high and 118-18 low.

- Click here for more detail.

COMMODITIES

- WTI and Brent were bolstered by rhetoric from the Russian Defence Ministry re. Zaporizhia and as China’s President Xi spoke

- Currently, the benchmarks are in proximity to their respective highs of USD 89.56/bbl and USD 95.44/bbl.

- Spot gold experienced a marginal haven bid bringing the yellow metal to an incremental new session peak of USD 1767/oz and eclipsing the 21-DMA at USD 1764/oz.

- Broader metal space is mixed and features essentially unchanged action for Aluminium, after Wednesday’s noted rally, while LME Copper has climbed back towards a test of the USD 8k handle

- Click here for more detail.

NOTABLE DATA

- EU HICP Final YY (Jul) 8.9% vs. Exp. 8.9% (Prev. 8.9%); X F & E Final YY (Jul) 5.1% vs. Exp. 5.0% (Prev. 5.0%)

- X F, E, A & T Final YY (Jul) 4.0% vs. Exp. 4.0% (Prev. 4.0%)

APAC TRADE

- APAC stocks mostly declined following the weak handover from global counterparts which were pressured as yields climbed on the back of the red-hot UK inflation data and with only a brief reprieve seen after the FOMC Minutes noted many officials saw a risk the Fed could tighten more than necessary.

- ASX 200 was subdued as participants digested the latest influx of earnings releases and disappointing jobs data which showed a surprise contraction in headline Employment Change.

- Nikkei 225 slipped back beneath the 29,000 level in tandem with the overall downbeat sentiment.

- Hang Seng and Shanghai Comp conformed to the glum mood after both Goldman Sachs and Nomura cut their China GDP growth forecasts and with focus also on earnings releases including Tencent after it posted its first-ever decline in quarterly revenue although its shares were lifted and it had vowed a return to growth, while Country Garden led the declines after the developer issued a profit warning of as much as an 87% drop in H1 net.

NOTABLE APAC HEADLINES

- China may issue CNY 1.5tln in additional debt as part of an investment push, according to China Securities News.

- China’s COVID-19 cases rose to a 3-month high of 3,424 on Wednesday from 2,888 the day before.

- Nomura cut its China 2022 GDP growth forecast to 2.8% from 3.3%.

- China’s MOFCOM says, re. US CHIPS act, some provisions restrict normal economic, trade and investment activities of relevant enterprises in China. Will, when necessary, take forceful measures to safeguard interests.

- China’s President Xi says they will persist with opening up the economy, via CCTV.

- China’s banking regulator is reportedly looking into the property sector loan portfolios of some local/foreign lenders to assess systemic risk, via Reuters citing sources.

DATA RECAP

- Australian Employment (Jul) -40.9k vs. Exp. 25.0k (Prev. 88.4k); Full-Time Employment (Jul) -86.9k (Prev. 52.9k)

- Australian Unemployment Rate (Jul) 3.4% vs. Exp. 3.5% (Prev. 3.5%); Participation Rate (Jul) 66.4% vs. Exp. 66.8% (Prev. 66.8%)

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 14.94 PTS OR 0.46% //Hang Sang CLOSED DOWN 158.54 OR 0.80% /The Nikkei closed DOWN 280.63 OR % 0.96. //Australia’s all ordinaires CLOSED DOWN 0.32% /Chinese yuan (ONSHORE) closed DOWN AT 6.7882//OFFSHORE CHINESE YUAN DOWN 6.7946// /Oil UP TO 89.02 dollars per barrel for WTI and BRENT AT 95.04// / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

3 a./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

Young Japanese not drinking as much and that cuts Japanese government tax haul

(zerohedge)

Japan Wants People To Drink More Alcohol As Generational Trend Cuts Tax Haul

THURSDAY, AUG 18, 2022 – 10:00 AM

In some sort of Bizarro World scenario, declining alcohol consumption is causing alarm in the halls of Japanese government, as the trend is putting a big dent in the country’s tax haul.

Average adult alcohol intake dropped from 100 liters a year in 1995 to 75 liters in 2020. Meanwhile, alcohol taxes declined from providing 3% of Japan’s tax revenue in 2011 to 2% in 2020.

As the Financial Times explains, much of the trend can be attributed to demographics:

A fall in the total volume of alcohol consumed in Japan was inevitable once the indigenous population began to shrink over a decade ago and the proportion of citizens aged over 65 increased to more than a quarter of the country eight years ago.

Reflecting a worldwide phenomenon, Japan’s younger generations aren’t drinking as much as their parents and grandparents did.

The general downtrend gained steam when the Covid-19 pandemic disrupted lifestyles. Restaurants and bars closed or limited their operations, and people socialized less and shifted to working from home. “Many people may have come to question whether they need to continue the habit of drinking with colleagues to deepen communication,” a tax official told the Japan Times.

The drop in revenue from 2018 to 2020 was the largest in 31 years. Taxes took a big hit in 1989 with a major change in Japan’s Liquor Tax Law.

Fear not — having admitted it has an alcohol problem, Japan’s tax agency will no longer sit idle while sobriety insidiously spreads throughout the population. A government campaign is afoot to encourage people to hit the bottle.

The first phase of the drinking drive is a contest called “Sake Viva!“, which asks Japanese citizens between the ages of 20 and 39 to come up with fresh ideas for juicing the country’s alcohol business. In addition to seeking “new products and designs” and new sales methods, the tax agency also wants strategies to encourage people to drink at home, reports The Guardian.

After winners are named at a gala in November, the tax office plans to promote the adoption of the winning ideas by alcohol-related businesses. Japan’s health ministry isn’t participating in the contest, but said it trusted the ensuing campaigns would emphasize drinking only “the appropriate amount of alcohol.”

end

3c CHINA

CHINA//

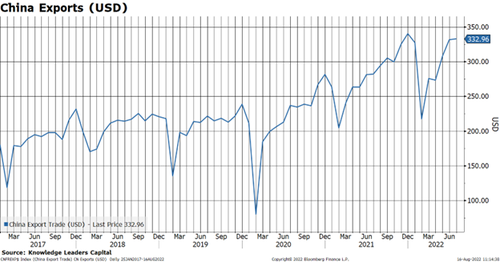

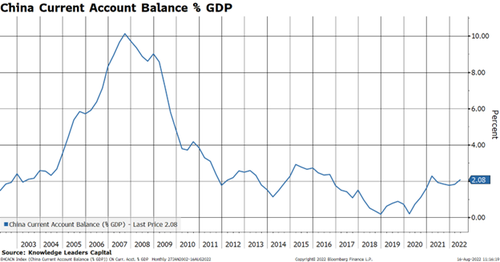

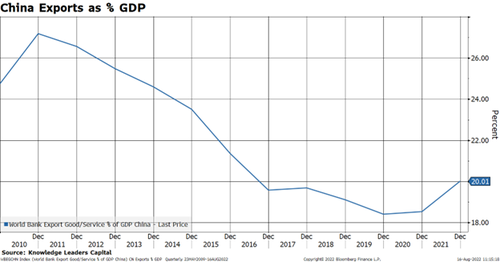

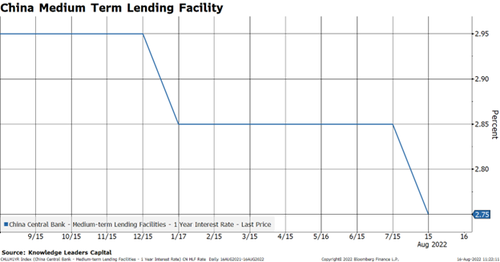

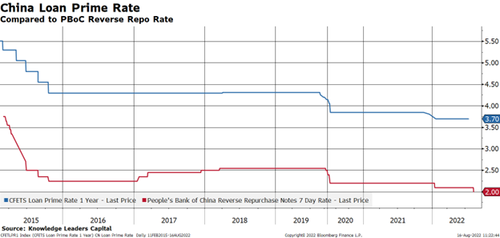

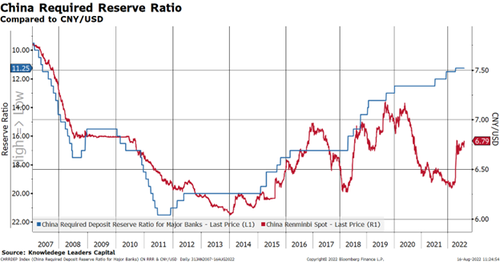

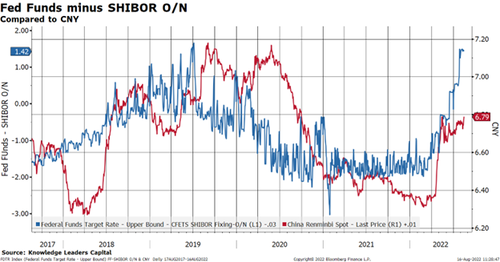

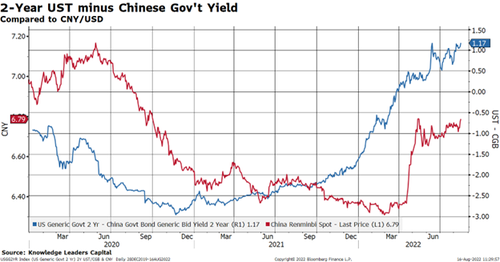

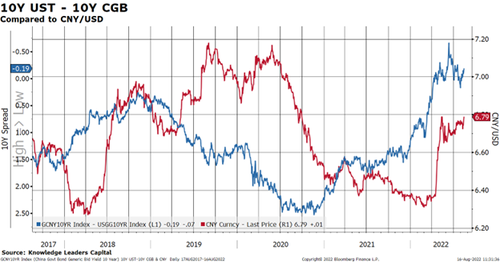

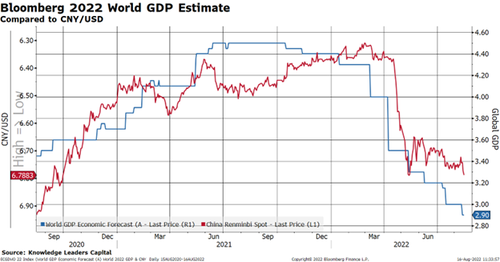

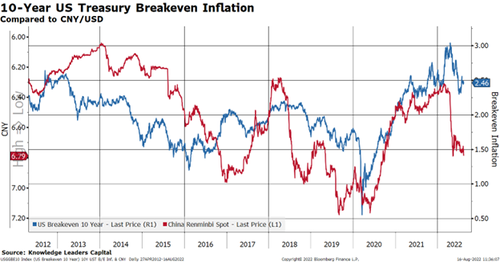

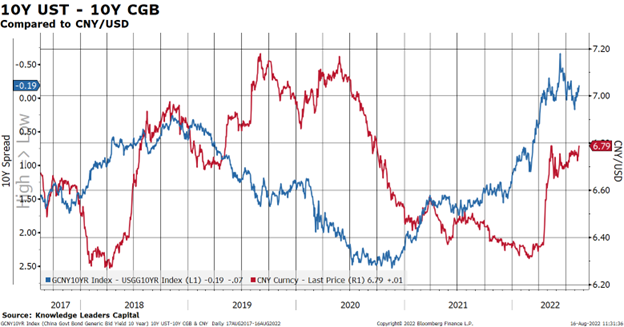

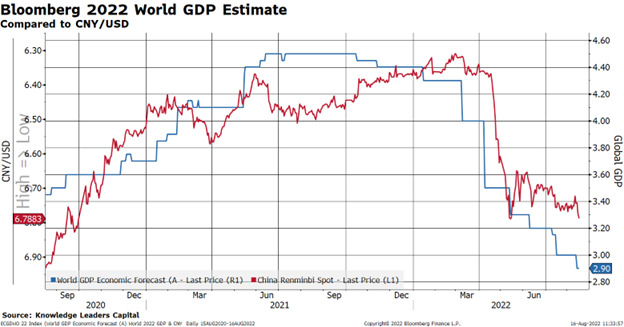

Are we heading for a China devaluation? Looks like it

(Vannelli/Knowledge Leaders Capital Blog)

Is A Chinese Devaluation Imminent?

WEDNESDAY, AUG 17, 2022 – 05:15 PM

Authored by Steven Vannelli via Knowledge Leaders Capital blog,

Over the weekend, we got a slew of data showing a generally weak economy. Below are the actual data compared with the expectations from Bloomberg.

Of course, the headline grabber was the -31.4% drop in residential property sales, but across the board, from industrial production to retail sales to investment came in shy of estimates.

This makes it incredibly unlikely that China is going to hit its growth target this year when all the components are running below estimates. Retail sales are currently running 0.5% behind calendar year estimates, while industrial production is running 0.7% behind and fixed asset investment is 0.3% behind.