by harveyorgan · in Uncategorized · Leave a comment·Edit

Uncategorized · Leave a comment·Edit

GOLD; $1749.75 DOWN $8.00

SILVER: $19.16 DOWN 38 CENTS

ACCESS MARKET:

GOLD $1747.20

SILVER: $19.06

Bitcoin morning price: $21,424 DOWN 1980

Bitcoin: afternoon price: $21.425. DOWN 1981

Platinum price closing DOWN $20.25 AT$897.10

Palladium price; closing DOWN $30.15 at $2127.65

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,755.300000000 USD

INTENT DATE: 08/18/2022 DELIVERY DATE: 08/22/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 334 3

072 H GOLDMAN 10

104 C MIZUHO 3

118 C MACQUARIE FUT 3

132 C SG AMERICAS 157

167 C MAREX 2

190 H BMO CAPITAL 4

323 H HSBC 1

435 H SCOTIA CAPITAL 8

624 H BOFA SECURITIES 79

661 C JP MORGAN 157

661 H JP MORGAN 1

685 C RJ OBRIEN 10

737 C ADVANTAGE 1

800 C MAREX SPEC 4

878 C PHILLIP CAPITAL 1

880 C CITIGROUP 91 3

880 H CITIGROUP 8

TOTAL: 440 440

MONTH TO DATE: 33,113

JPMorgan stopped: 157/440

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR AUGUST CONTRACT:

440 NOTICES FOR 44,00000 OZ //1.3685 TONNES

total notices so far: 33,113 contracts for 3,311,300 oz (102.993 tonnes)

SILVER NOTICES: 7 NOTICES FILED FOR 35,000 OZ/

total number of notices filed so far this month 943 : for 4,715,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $8.00

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.718 TONNES FROM THE GLD.

INVENTORY RESTS AT 985.83 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $0.38 CENTS

AT THE SLV// ://A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 483.684 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GOOD SIZED 437 CONTRACTS TO 143,806. AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GOOD GAIN IN OI WAS ACCOMPLISHED DESPITE OUR $0.27 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.27) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD A STRONG GAIN OF 655 CONTRACTS ON OUR TWO EXCHANGES. HOWEVER WE HAD A SOME LIQUIDATION OF SPECULATOR SHORTS.

WE MUST HAVE HAD:

I) SOME SPECULATOR SHORT LIQUIDATIONS//CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A FAIR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 35,000 OZ QUEUE JUMP / // V) GOOD SIZED COMEX OI GAIN/(//SOME SPEC LIQUIDATION)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -93

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTACTS for 15 days, total 6775 contracts: 33.875 million oz OR 2.258 MILLION OZ PER DAY. (452 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 33.875 MILLION OZ

.

LAST 16 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 33.875 MILLION OZ (A LOT LESS THAN NORMAL//THE CROOKS ARE SCARED TO ISSUE MORE EFP’S)

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 437 DESPITE OUR $0.27 LOSS IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 125 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /SOME BANKER ADDITIONS AND SOME SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 35,000 OZ QUEUE JUMP // .. WE HAD A STRONG SIZED GAIN OF 655 OI CONTRACTS ON THE TWO EXCHANGES FOR 3.275 MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 7 NOTICE(S) FILED TODAY FOR 35,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 516 CONTRACTS TO 456,855 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:+25 CONTRACTS.

.

THE SMALL SIZED INCREASE IN COMEX OI CAME DESPITE OUR FALL IN PRICE OF $5.75//COMEX GOLD TRADING/THURSDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERINGS//CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 98.367 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG 4900 OZ QUEUE JUMP //NEW STANDING 104.1804 TONNES

YET ALL OF..THIS HAPPENED WITH OUR FALL IN PRICE OF $5.75 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 4393 OI CONTRACTS 13.664 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3877 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 456,856

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4393 CONTRACTS WITH 516 CONTRACTS INCREASED AT THE COMEX AND 3877 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4393 CONTRACTS OR 13.664 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3877) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (437): TOTAL GAIN IN THE TWO EXCHANGES 4393 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR AUGUST. AT 99.272 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 4900 oz. 3) ZERO/ LONG LIQUIDATION//// //.,4) SMALL SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

37,234 CONTRACTS OR 3,723,400 OZ OR 115.81 TONNES 15 TRADING DAY(S) AND THUS AVERAGING: 2482 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAY(S) IN TONNES: 115.81 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 103.97/3550 x 100% TONNES 2.92% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 115.81 TONNES (DRAMATICALLY FALLING AGAIN)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT., FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GOOD SIZED 427 CONTRACT OI TO 143,806 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 125 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 125 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 125 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 437 CONTRACTS AND ADD TO THE 125 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 562 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 2.810 MILLION OZ

OCCURRED DESPITE OUR FALL IN PRICE OF $0.27

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED DOWN 19.47 PTS OR 0.59% //Hang Sang CLOSED UP 9.12 OR 0.05% /The Nikkei closed DOWN 11.81 OR % 0.04. //Australia’s all ordinaires CLOSED UP 0.01% /Chinese yuan (ONSHORE) closed DOWN AT 6.8181//OFFSHORE CHINESE YUAN DOWN 6.8395// /Oil DOWN TO 88.41 dollars per barrel for WTI and BRENT AT 94.47// / Stocks in Europe OPENED MOSTLY RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 510 CONTRACTS TO 456,855 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR FALL OF $5.75 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (3877 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF AUGUST.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3877 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :3877 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3877 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED SIZED TOTAL OF 4393 CONTRACTS IN THAT 3877 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 516 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $ 5.75. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING AUGUST (104.1804),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.1804 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $5.75) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A GOOD SIZED TOTAL GAIN ON OUR TWO EXCHANGES // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS////// WE HAVE REGISTERED A GOOD SIZED GAIN OF 13.664 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR AUGUST (104.1804 TONNES)…

WE HAD + 25 CONTRACTS ADDED TO COMEX TRADES. THESE WERE ADDED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 4393 CONTRACTS OR 439300 OZ OR 13.664 TONNES

Estimated gold volume 135,004/// extremely poor/

final gold volumes/yesterday 130,177/extremely poor

INITIAL STANDINGS FOR AUGUST ’22 COMEX GOLD //AUGUST 19

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 155,624.053 oz Brinks Manfra includes 2750 kilobars Brinks |

| Deposit to the Dealer Inventory in oz | 32,215.302 OZ Brinks 1000 kilobars |

| Deposits to the Customer Inventory, in oz | 48,826.033 oz Loomis |

| No of oz served (contracts) today | 440 notice(s) 4400 OZ 1.3685 TONNES |

| No of oz to be served (notices) | 381 contracts 38,100 oz 1.185 TONNES |

| Total monthly oz gold served (contracts) so far this month | 33,113 notices 3,311,300 OZ 102.995 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 1

i) Into Brinks: 32,215.302 oz (1000 kilobars)

total dealer deposit: 32,215.302 oz

No dealer withdrawals

Customer deposits: 1

i)Into Loomis: 48,826.033 oz

total deposits 48,826.033 oz

2 customer withdrawals:

i) Out of Manfra 67,208.870 oz

ii) Out of Brinks: 88,415.183 oz (2750 kilobars)

ii) Out of Brinks 22,673,738 oz

total: 155,624.053 oz

total in tonnes: 4.84 tonnes

Adjustments: dealer to customer //4

Brinks: 6,390.149oz

HSBC: 44,206.108 oz

Manfra: 6409.609 oz

JPmorgan: 10,721.326

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 821 contracts having LOST 105 contracts .

We had 154 notices served upon yesterday so we gained a strong 49 contracts or an additional 4,900 oz will stand for delivery in this very active month of August.

Sept. gained 23 contracts to 3627 contracts.

October gained 13 5 contracts up to 39,967

We had 440 notice(s) filed today for 44,000 oz FOR THE AUGUST 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 440 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 157 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2022. contract month,

we take the total number of notices filed so far for the month (33,113) x 100 oz , to which we add the difference between the open interest for the front month of (AUGUST 821 CONTRACTS ) minus the number of notices served upon today 440 x 100 oz per contract equals 3,349,400 OZ OR 104.1804 TONNES the number of TONNES standing in this active month of AUGUST.

thus the INITIAL standings for gold for the AUGUST contract month:

No of notices filed so far (33,113) x 100 oz+ (821) OI for the front month minus the number of notices served upon today (440} x 100 oz} which equals 3,349,400 oz standing OR 104.1804 TONNES in this active delivery month of August.

TOTAL COMEX GOLD STANDING: 104.1804 TONNES (A HUGE STANDING FOR AUGUST ( ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,320,942.458 oz 72.19 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 28,573,370.159 OZ

TOTAL REGISTERED GOLD: 14,373,370.159 OZ (447,07 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 14,199,827.057 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 12,052,94280 OZ (REG GOLD- PLEDGED GOLD) 374.89 tonnes//rapidly declining

END

SILVER/COMEX/AUGUST 19

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 728,828/138 oz CNT JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 988.41 oz cnt |

| No of oz served today (contracts) | 7 CONTRACT(S) 35,000 OZ) |

| No of oz to be served (notices) | 50 contracts (250,000 oz) |

| Total monthly oz silver served (contracts) | 943 contracts 4,715,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) Into CNT: 988.41 oz

total deposit: 988.41 oz

JPMorgan has a total silver weight: 172.521 million oz/331.997 million =51.97% of comex

Comex withdrawals: 2

i) Out of CNT 99,458.63 oz

ii) Out of JPMorgan: 629,369.500 oz

total: 728,828.138 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 55.478 MILLION OZ

TOTAL REG + ELIG. 331.997 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR AUGUST

silver open interest data:

FRONT MONTH OF AUGUST OI: 57 CONTRACTS HAVING LOST 6 CONTRACTS. WE HAD 13 NOTICES FILED ON THURSDAY

SO WE GAINED 7 CONTRACTS OR AN ADDITIONAL 35,000 OZ OF SILVER WILL STAND FOR DELIVERY. THE AMOUNT STANDING

WILL NOW INCREASE//(OR REMAIN CONSTANT) ON A DAILY BASIS AS BANKERS SCOUR THE PLANET FOR BADLY NEEDED SILVER.

SEPTEMBER HAD A LOSS OF 1286 CONTRACTS DOWN TO 53,891

OCTOBER GAINED 8 CONTRACTS TO STAND AT 120

CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 7 for 35,000 oz

Comex volumes:61,561// est. volume today// fair

Comex volume: confirmed yesterday: 54,769 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 943 x 5,000 oz = 4,715,000 oz

to which we add the difference between the open interest for the front month of AUGUST(57) and the number of notices served upon today 7 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST./2022 contract month: 943 (notices served so far) x 5000 oz + OI for front month of AUGUST (57) – number of notices served upon today (7) x 5000 oz of silver standing for the AUGUST contract month equates 4,965,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

AUGUST 10//WITH GOLD UP $2.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES

AUGUST 9/WITH GOLD UP $6.70: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES.

AUGUST 8/WITH GOLD UP $13.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FORM THE GLD//INVENTORY RESTS AT 999.16 TONNES

AUGUST 5/WITH GOLD DOWN $14.25: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .33 TONNES FROM THE GLD////INVENTORY RESTS AT 1000.32 TONNES

AUGUST 4 WITH GOLD UP $29.00 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES FROM THE GLD///INVENTORY REST AT 1000.65 TONNES

AUGUST 2/WITH GOLD UP $3.70; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD//INVENTORY RESTS AT 1002.97 TONNES//

AUGUST 1/WITH GOLD UP $5.75: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 29//WITH GOLD UP $12.50; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1005.29 TONNES

JULY 28/WITH GOLD UP $31.25; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 27.//WITH GOLD UP $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 26/WITH GOLD DOWN $1.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.29 TONNES

JULY 25/WITH GOLD DOWN $7.85: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 1005.87 TONNES

JULY 22/WITH GOLD UP $17.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 21/WITH GOLD UP $11.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.101 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.87 TONNES

JULY 20/WITH GOLD DOWN $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1009.06 TONNES

JULY 19/WITH GOLD DOWN $.35 :BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22 TONNES FROM THE GLD//INVENTORY RESTS AT 1009.06 TONNES

JULY 18/WITH GOLD UP $7.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.28 TONNES

JULY 15/WITH GOLD DOWN $3.75:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD///INVENTORY RESTS AT 1016.89 TONNES//

JULY 14/WITH GOLD DOWN $28.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD//INVENTORY RESTS AT 1019.79 TONNES

JULY 13/WITH GOLD UP $10.55:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD//INVENTORY RESTS AT 1021.53TONNES

JULY 12/WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESS AT 1023.27 TONNES

GLD INVENTORY: 985.83 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTO THE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 10/WITH SILVER UP 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 9/WITH SILVER DOWN 25 CENTS TODAY: TWO CHANGES IN SILVER INVENTORY AT THE SLV: FIRST: A DEPOSIT OF 461,000 OZ INTO THE SLV AND THEN A WITHDRAWAL OF 1.014 MILLION OZ..//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 8/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 5/WITH SILVER DOWN 28 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 922,000 OZ FROM THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 4 WITH SILVER UP 21 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 527,000 OZ FROM THE SLV////INVENTORY RESTS AT 486.634 MILLION OZ

AUGUST 2/WITH SILVER DOWN 21 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.504 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.161 MILLION OZ//

AUGUST 1/WITH SILVER UP 17 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE GLD: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 483.657 MILLION OZ//

JULY 29/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 461,000 OZ FROM THE SLV..//INVENTORY RESTS AT 483.657 MILLION OZ/

JULY 28/WITH SILVER UP $1.24 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 484.118 MILLION OZ/

JULY 27/.WITH SILVER UP 4 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL 11.479 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 484.118MILLION OZ//

JULY 26/WITH SILVER UP 16 CENTS: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.504 MILLION OZ FROM THE SLV//: //INVENTORY RESTS AT 495.597 MILLION OZ//

JULY 25/WITH SILVER DOWN 24 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.383 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 499.101 MILLION OZ//

JULY 22/WITH SILVER DOWN 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 500.484 MILLION OZ//

JULY 21/WITH SILVER UP 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.19 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 500.484MILLION OZ/

JULY 20/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 8.253 MILLION OZ FORM THE SLV/INVENTORY RESTS AT 507.585 MILLION OZ//

JULY 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ//

JULY 18/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 4.995 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ.

JULY 15/WITH SILVER UP 31 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 3.226 MILLION OZ FORM THE SLV//INVENTORY RESTS AT 510.443 MILLIONOZ//

JULY 14/WITH SILVER DOWN 88 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 OZ FROM THE SLV// //INVENTORY RESTS AT 513.671 MILLION OZ

JULY 13/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SV//INVENTORY RESTS AT 514.501 MILLION OZ.

JULY 12/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.228 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 514.501 MILLION OZ//

CLOSING INVENTORY 483.684 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

3.Chris Powell of GATA provides to us very important physical commentaries

Your weekend reading material and today’s topic is really good

(Alasdair Macleod/GATA)

Alasdair Macleod: The world is splitting in two and Putin has the winning hand

Submitted by admin on Thu, 2022-08-18 20:51Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, August 18, 2022

While we are being distracted by Ukraine, President Putin has advanced his geopolitical goals materially. Aided and abetted by President Xi, Putin is taking the Asian continent into his control. That mission is well on its way to being achieved. He now awaits the winter months to finally force the EU to reject America’s hegemony. Only then, will the western end of the Eurasian continent be truly free of American interference.

This article explains how he is achieving his strategic goals. It examines the geopolitics of the Asian landmass and the nations tied to it, which are commercially and financially turning their backs on the US-led western alliance.

I look at geopolitics from President Putin of Russia’s viewpoint, since he is the only national leader who seems to have a clear grasp of his long-term objectives. His active strategy conforms closely with Halford Mackinder’s predictive analysis of nearly 120 years ago. Mackinder is regarded by many experts as the founder of geopolitics.

Putin is determined to remove the American threat to his Western borders by squeezing the EU to that end. But he is also building political relationships based on control of global fossil-fuel supplies — a pathway opened for him by American and European obsessions over climate change. In partnership with China, the consolidation of his power over the Eurasian landmass has progressed rapidly in recent weeks.

For the Western Alliance, financially and economically his timing is particularly awkward, coinciding with the end of a 40-year period of declining interest rates, rising consumer price inflation, and a deepening recession driven by contracting bank credit.

It is the continuation of a financial war by other means, and it looks like Putin has an unbeatable hand. He is on course to push our fragile fiat currency based financial system over the edge. …

… For the remainder of the analysis:

https://www.goldmoney.com/research

END

Will the LBMA expel JPMorganChase from membership because of Nowak’s conviction?

(Ronan Manly)

Ronan Manly: Will LBMA expel JPMorganChase because of Nowak’s conviction?

Submitted by admin on Thu, 2022-08-18 20:46Section: Daily Dispatches

8:45p ET Thursday, August 18, 2022

Dear Friend of GATA and Gold:

Despite the market-rigging conviction of the chief of its monetary metals trading desk, Michael Nowak, JPMorganChase is still at the center of the world gold business generally and the London Bullion Market Association particularly, Bullion Star’s gold researcher, Ronan Manly, writes today.

Nowak was on the LBMA Board of Directors when he was indicted, Manly notes, and he wonders — or at least pretends to wonder — if the association now will expel JPMorganChase from membership.

Manly’s analysis is headlined “JP Morgan Gold Trading Boss and Former LBMA Board Member Found Guilty by U.S. Jury” and it’s posted at Bullion Star here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

4. OTHER GOLD/SILVER COMMENTARIES

-END-

5.OTHER COMMODITIES: USA/COTTON

end

COMMODITIES IN GENERAL/COAL

The use of coal is back and at higher prices

(Hagan/EpochTimes)

Across The World Coal Power Is Back

FRIDAY, AUG 19, 2022 – 05:00 AM

Authored by Chadwick Hagan via The Epoch Times (emphasis ours),A bucket-wheel dumping soil and sand removed from another area of the mine in Newcastle, Australia, the world’s largest coal exporting port, on Nov. 5, 2021. (Saeed Khan/AFP via Getty Images)

In the United States, coal consumption hit an all-time high in 2013, and soon after most every Wall Street bank and liberal activist declared coal as dead.

Still, coal energy was the dominant form of energy in the United States until 2016, and this year global coal consumption is set to reach 2013’s record levels.

In February of this year, Central Appalachian coal production hit a two-year high. Now the price of coal is rising to record levels in the United States and across the world.

Sounds like a tremendous amount of activity for an industry that has been declared dead.

What gives?

First off, let’s be honest, fossil fuels still account for much of America’s energy. According to the EIA’s Monthly Energy Review: “Fossil fuels—petroleum, natural gas, and coal—accounted for 79 percent of the 97 quadrillion British thermal units (quads) of primary energy consumption in the United States during 2021. About 21 percent of U.S. primary energy consumption in 2021 came from fuel sources other than fossil fuels, such as renewables and nuclear.”

In other words, fossil fuels made up nearly 80 percent of all energy produced in America in 2021.

Carbon Emissions Curbs Take a Backseat

Earlier this month CNBC reported on the continued coal consumption and price increases happening in domestic and global markets, stating: “coal prices are soaring and global coal consumption is expected to return to record levels reached almost 10 years ago as the global energy supply crunch continues. While investors in coal stocks are having a field day thanks to high coal prices, curbs on carbon emissions are taking a backseat as markets and governments scramble to stock up on traditional energy supply amid bottlenecks caused by the Ukraine war.”

At the moment there are a number of issues at play, ranging from the need to ramp up domestic supply for domestic energy security, to a years-long slowdown in domestic and international production, and now lingering supply issues from the Russian-Ukrainian war.

The ripple effect is being felt worldwide. International coal prices are also skyrocketing.

Mining and metals expert Pete O’Connor from Australian investment bank Shaw & Partners recently commented on the tight coal market and price increases seen across the globe, stating: “And supply [of coal] is tight. Why? Because nobody’s building capacity and markets will remain tight given the weather and Covid. So that market will stay higher for longer, probably well into the 2023 calendar year.”Alliant Energy’s coal plant in Sheboygan, Wisconsin, on the shore of Lake Michigan, on July 4, 2022. (Timothy Gardner/Reuters)

Additionally, the IAE reported in a recent coal market report: “After coal and power shortages led to high coal prices in October 2021, the Chinese government gave orders to boost domestic production, which reduced the need for imports. In the first six months of 2022, China’s coal production increased by 11%. At the same time, we estimate that its coal demand declined by 3%. As a result, coal imports fell by 18% year-on-year to 115 Mt. For the full year, we expect China’s coal imports to decline by 18%, or 45 Mt. India also started 2022 with reduced imports, but government measures to prevent coal shortages will likely increase import volumes in the second half. Overall, we expect India’s coal imports to increase slightly compared with 2021.”

IAE continued: “Indonesia, the world’s largest exporter of thermal coal, is also the most flexible. In 2021, it increased its exports by 27 Mt to 434 Mt, exporting more than twice as much as Australia (199 Mt). The United States, a swing supplier in the Atlantic market, increased exports by 12 Mt to 36 Mt.”

That’s right. U.S. coal exports increased by three times.

Costliest Coal Contract

Perhaps the most important coal market news came last month in late July when Bloomberg reported on a coal trade that could be one of the most expensive coal trades ever recorded in Japan. The deal was between Glencore and Nippon Steel, and the coal was sold at $375 per ton.

As Bloomberg reported: “Nippon Steel Corp. agreed on an annual supply deal through March with Glencore for power plant coal at $375 per ton, according to people with knowledge of the deal, who asked not to be identified because the information is private. The agreement is three times more expensive than similar deals done last year, and is likely one of the costliest coal contracts ever signed by a Japanese company.”Wind turbines spin near the coal-fired Mehrum Power Station on Feb.14, 2022 in Mehrum, Germany. (Sean Gallup/Getty Images)

The bottom line remains, thermal coal is back in demand and that’s not changing for a while. Yes coal is dirty but it is reliable. In fact many believe that there is a moral obligation to produce coal, the moral obligation being that we should mine for coal so others can have access to reliable power and energy.

Radical activists who wax poetically about environmental destruction from fossil fuels are also obsessively determined on destroying industries that brought us into our era of hyper technology and industrialization. They are obsessively determined to destroy jobs instead of supporting energy security and carbon capture research and development.

After all, shouldn’t we look to utilize carbon capture in abandoned coal mines? Should we not find a way to filter flue gas from coal-burning power plants instead of flipping off the switch?

What is the point of destroying the coal mining industry, and taking thousands of jobs with it, if you are still supporting industries that cause harm to the environment?

These radicals—in my opinion—opportunistically fail to see the destruction caused by the manufacturing of renewables, which includes toxicity from lithium-ion batteries, wind turbines killing thousands and thousands of birds, and solar panel fields taking huge swaths of land for energy that only provides power during sunny days.

If there is a middle ground to be found here it will be using profits from fossil fuels to pay for the research and development of less harmful forms of energy.

I can tell you from an investment banking standpoint and from an economic analyst standpoint, that developing new energy is not cheap. It will take billions of dollars in investment, and those billions are going to come from the billions and billions of dollars fossil fuel providers make in profits during boom years.

Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times or Zero Hedge

END

6.CRYPTOCURRENCIES

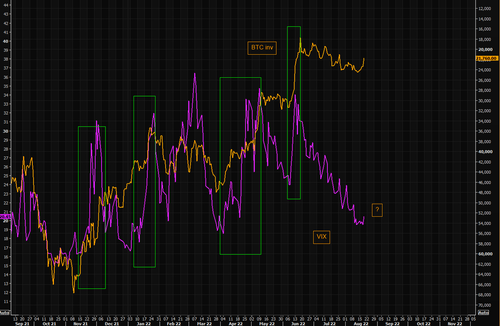

Cryptos falling badly today.

(Market Ear)

The bitcoin puke is back

FRIDAY, AUG 19, 2022 – 7:43

See TME’s daily newsletter email below. For the 24/7 market intelligence feed and thematic trading emails, sign up for ZH premium here.

BTC – the dog is back

The constant underperformer is back to puking. We have to admit we thought BTC would actually catch up to some of the equities squeeze momentum, but that was obviously wrong. The classical NASDAQ vs BTC gap is getting huge. Second chart shows the liquidation. There are absolutely zero institutions that want/need this type of volatility…and this remains as bitcoin’s biggest problem (chart 3).

Source: Refinitiv

Source: Coinalyze

Source: JPM

BTC – when you try to catch up…

…and what you are chasing reverses lower as well. The BTC vs ETH gap remains very wide…

Source: Refinitiv

Bitcoin – the huge trend stays intact

Bitcoin reversed right on the huge trend line and the 100 day moving average. The puke today has the BTC falling below the short term positive trend line. This is not what the bulls needed….

Source: Refinitiv

BTC vols are back

BTC volatility is moving sharply higher as investors are once again reminded about how unstable this asset really is, at least from a trading point of view. First chart shows the 1 and 2 month implied vols. Second chart shows the 1 month implied vs realized vol.

Source: Genesisvolatility

Source: Genesisvolatility

BTC – back below the “long long” term moving average

BTC is once again below the 200 week moving average. Caching falling knives anyone?

Source: Refinitiv

BTC skewed

BTC skew is moving again as puts become the preferred choice and are getting relatively more bid in terms of volatility. Chart shows the 1 week, 1 and 2 month skew.

Source: Genesisvolatility

BTC – you know where you won’t mine it

Chart showing BTC vs German 1 year baseload electricity prices (hitting another new record as of writing). The picture is similar in France and other countries.

Source: Refinitiv

BTC is a rate sensitive play

US 10 year (inverted) vs BTC needs little commenting.

Source: Refinitiv

VIX and bitcoin

We have not seen sharp moves lower in bitcoin without VIX participating. Our latest long VIX logic outlined in our thematic email earlier this week (premium subs only here) is very much intact. BTC is still a good indicator of the aggregate psychology of the masses…

Source: Refinitiv

end

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.8181

OFFSHORE YUAN: 6.8395

HANG SENG CLOSED UP 9.12 PTS OR 0.05%

2. Nikkei closed DOWN 11/80 OR 0.04%

3. Europe stocks CLOSED MOSTLY RED

USA dollar INDEX UP TO 107.94/Euro FALLS TO 1.0047

3b Japan 10 YR bond yield: RISES TO. +.198/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 136.99/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.221%/Italian 10 Yr bond yield FALLS to 3.50% /SPAIN 10 YR BOND YIELD RISES TO 2.38%…

3i Greek 10 year bond yield RISES TO 3.68//

3j Gold at $1752.55 silver at: 19.28 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 87/100 roubles/dollar; ROUBLE AT 58.67//

3m oil into the 88 dollar handle for WTI and 94 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 136.99DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9567– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9615well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

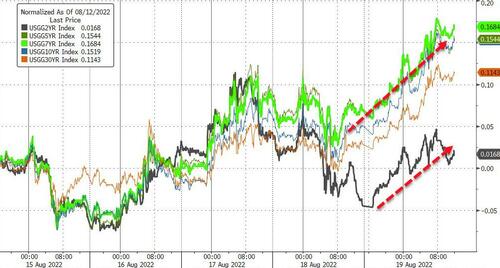

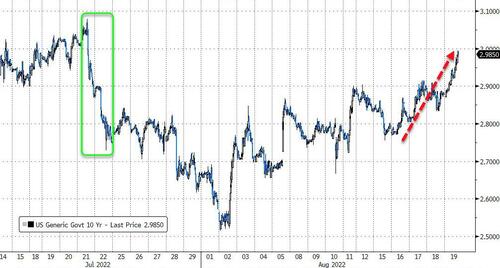

USA 10 YR BOND YIELD: 2.994 UP 6 BASIS PTS

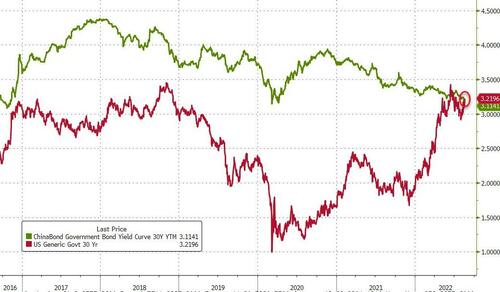

USA 30 YR BOND YIELD: 3.188 UP 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,11

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Plunge, Yields Roar Higher As Bear-Market Rally Slams Brick Wall On $2.1 Trillion Op-Ex

FRIDAY, AUG 19, 2022 – 08:02 AM

The combination of plunging bitcoin prices, the (latest) bursting of the meme bubble courtesy of Ryan Cohen’s historic pump and dump, rising Fed warnings that another 75bps rate hike is coming amid fears next week’s Jackson Hole meeting will be a hawkano, rising oil prices and TSY yields at the highest level in a month, and mix it all in on a day when there is absolutely no liquidity (one day after the lowest volume of the year) as $2.1 trillion in options expire…

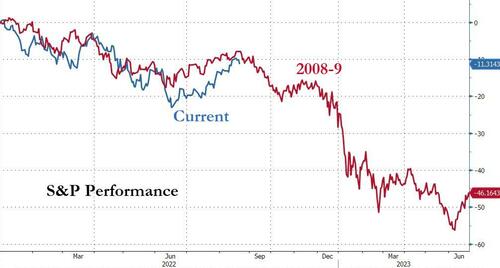

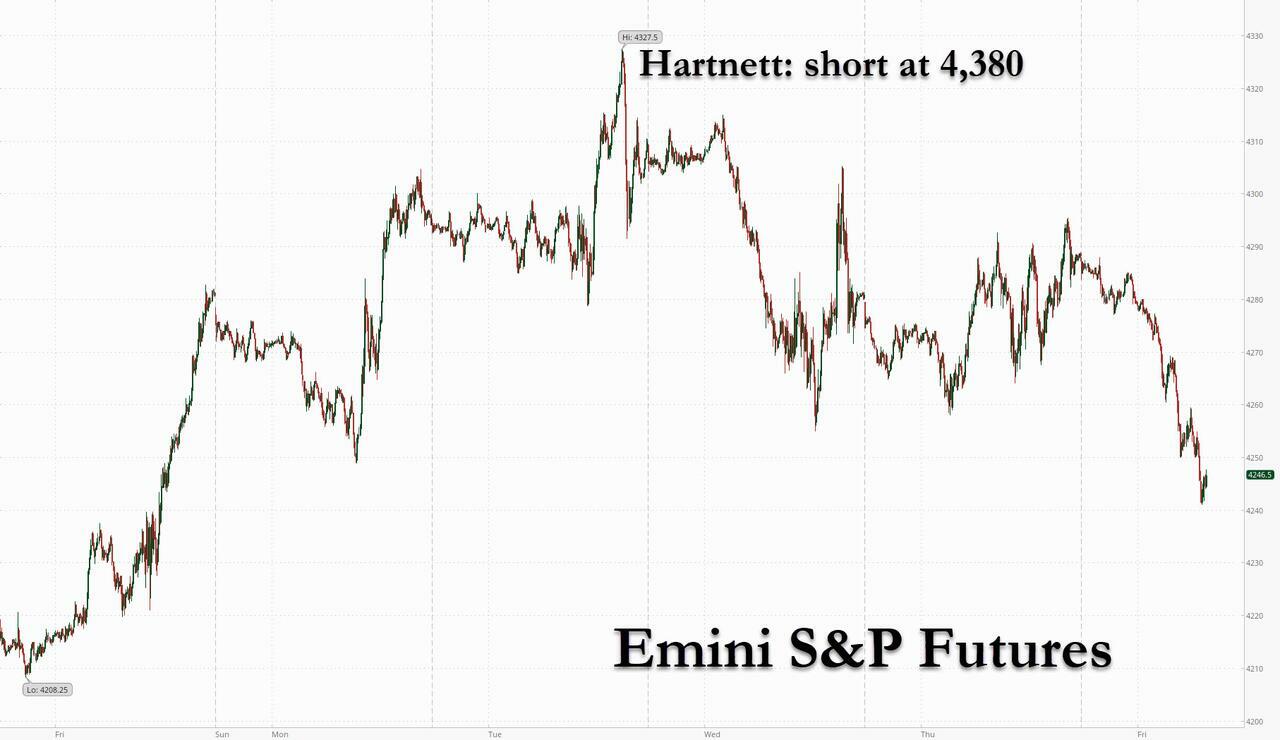

… and you get a perfect storm that has sent futures tumbling 40 points or 0.93%, but another confirmation that BofA’s Michael Hartnett is the best strategist on Wall Street (while his peers are nothing more than broken records).

Nasdaq 100 futures slumped 1.2% by 7.30 a.m. in New York as the yield on the 10-year Treasury climbed about 5 basis points to 2.95%, the highest level in one month amid divergent signals from Fed officials over the size of the next interest-rate hike.

The tech-heavy index is set to end the week lower after four weeks of gains; the Nasdaq 100 underperformed this week in the face of rising bond yields as higher rates weigh on the present value of future profits, hurting growth stocks with the highest valuations. The dollar headed for the biggest weekly rally since June 2021 and bitcoin plunged by $2,000 overnight, crashing below $21,500.

In premarket trading, Bed Bath & Beyond shares crashed 45%, after plunging more than 20% during the regular session, after top investor Ryan Cohen pulled the biggest pump and dump in history. Cryptocurrency-exposed stocks like Coinbase and Riot Blockchain also slid amid a broad selloff across digital tokens. Coinbase (COIN US) fell 7%, Marathon Digital (MARA US) -11%, Riot Blockchain (RIOT US) -9%. Here are other notable premarket movers:

- Applied Materials (AMAT US) rose as much as 1.4%, with analysts positive on the chip equipment maker’s results, saying it saw a strong performance amid a tough macroeconomic backdrop, though some brokers nudged down their price targets.

- Morgan Stanley analysts cut their price target on Meta Platforms (META US), saying the social media giant’s shift toward Reels and declining user-engagement rates pose a risk to its revenue growth. The stock was down 1.7%.

- Bill.com (BILL US) surged 21% after fiscal 4Q results from the infrastructure software firm that analysts said were “perfect” alongside guidance that “blew away” expectations.

- StoneCo (STNE US) dropped 9% after the Brazilian payments firm reported adjusted net for the second quarter that missed the average analyst estimate.

Traders have also turned cautious toward risk assets ahead of the Fed’s annual symposium next week in Jackson Hole. Beyond that, inflation and employment figures will also be closely monitored before the central bank’s highly anticipated interest-rate decision in September. Additionally, on Thursday two Fed voting members – St. Louis’s James Bullard and Kansas City’s Esther George – emphasized that the US central bank will continue to raise interest rates until inflation eased back to its 2% target although their views diverged on how big the Fed’s September move should be.

This is notable since traders had continued piling into stocks and bonds, completely ignoring the Fed’s repeated jawboning and dismissing the risk of a more aggressive Fed as they expect it to ease the pace of rate hikes while inflation pulls back from its peak, according to Bank of America strategists. US stocks saw $9.2 billion of inflows in the week through Aug. 17 BofA’s Michael Hartnett wrote in a note.

“The Fed would, in order to get inflation down to the 2% target, have to crush the economy,” said Ann-Katrin Petersen, a senior investment strategist at BlackRock Investment Institute. In order to bolster growth, the Fed will at some point “accept to live with inflation. This dovish pivot is not likely in the very near term, in contrast to what markets seem to be expecting right now, but this dovish pivot may come in 2023,” she told Bloomberg Television.

In Europe, the Stoxx 50 fell 0.8%. FTSE 100 outperforms, dropping 0.2%, Travel, real estate and autos are the worst-performing sectors. Italy’s FTSE MIB lags, dropping 1.4%. after a right-wing coalition led by Brothers of Italy party was seen reaching 49.8% level in voting intentions for Italy’s lower house of parliament for September election, according to a Tecne poll on August 18. Center-left bloc at 30%; Five Star Movement at 10.2%; Centrist coalition at 4.8%; Other parties at 5.2%. Here are some of the biggest European movers today:

- Just Eat Takeaway shares soar as much as 38% in Amsterdam trading, the most ever, after the food delivery firm agreed to sell its 33% stake in iFood for as much as EU1.8b

- Holmen rises as much as 5.3% on 2Q earnings that beat consensus on adjusted operating profit, net sales and operating profit. The report was strong, but expected, Jefferies writes

- Kingspan gains as much as 8.6% after 1H results from the Irish insulation supplier that Goodbody says were ahead of expectations

- U-blox surges as much as 16% after the Swiss semiconductor company lifted FY revenue and Ebit outlooks that it previously raised in May, citing a record- high order book

- Mobilezone rises as much as 5.3%, the most intraday since March, as analysts note the Swiss firm’s robust 1H earnings and confirmation of guidance in the face of powerful FX headwinds

- Joules plunges as much as 41% after the UK apparel retailer forecast an FY adjusted pretax loss significantly bigger than market views. Liberum cut its rating on the stock to hold from buy

- Bachem drops as much as 3.9% after Baader published a note saying the company’s first-half results due on Aug. 25 may be a trigger for a downward revision to consensus

- Oponeo.pl falls as much as 12% after the Polish distributor of tires, tools and bikes reported a 70% y/y drop in 2Q net income due to higher costs and lower sales of tires

- Hypoport declines as much as 12% after Metzler downgrades to sell on a slowdown in growth for its Europace unit and as the company’s insurance application “fails to convince” at this stage

Earlier in the session, Asian stocks headed for their first weekly drop in five, as renewed concerns about growth in China — the region’s biggest economy — damped investor sentiment. The MSCI Asia Pacific Index retreated as much as 0.7%, set for a decline of more than 1% this week. Meanwhile, a gauge of China stocks listed in Hong Kong posted its worst week in August, losing 2%. Shares in South Korea and India were among the region’s worst performers Friday. Concerns about China’s growth resurfaced as the country planned more fiscal stimulus over a gloomy outlook and as banks were expected to lower borrowing costs next week. Goldman Sachs, Nomura and Citi further cut their growth estimates for China’s gross domestic product earlier this week as a power supply crunch adds more uncertainty to the outlook.

“Regulatory issues and sluggish economic recovery are behind the weak performance of stocks in Hong Kong as many of the stocks listed there are related to the real estate sector and regulations,” said Kim Kyung Hwan, a China equity strategist at Hana Financial Investment in Seoul. “There are lingering concerns that China’s economic fundamentals may take an L-shaped recovery and the government’s intervention in the property crisis may be delayed,” he added.

Improved appetite for haven assets was also reflected in the dollar, which rose to the highest in nearly a month following a Bloomberg News report that China’s President Xi Jinping and Russia’s leader Vladimir Putin will attend the G-20 summit in Indonesia later this year. All but two sectoral indexes declined in Asia’s key benchmark, with health care and financials the biggest losers. Samsung Electronics and NetEase were among the biggest drags on the measure, with the latter tumbling on profit-taking following earnings results. Caution also prevailed with next week expected to be the busiest period for quarterly earnings announcements from MSCI Asia Pacific Index members. Chinese tech giants Meituan and JD.com Inc. are among the more than 300 companies set to release results

In FX, the Bloomberg Dollar Spot Index advanced for a third day and the greenback strengthened against all of its Group-of-10 peers. The pound fell to a one-month low while the euro was steady against the dollar. UK retail sales volumes unexpectedly rose 0.3% last month, but the cost of those sales increased more rapidly by 1.3%. UK consumer confidence fell to a record low as concerns about a recession increased and soaring inflation tightened a squeeze on household finances. GfK said its gauge of confidence declined 3 points to minus 44 in August. The New Zealand dollar was weighed by comments from RBNZ Governor Adrian Orr that the central bank would “retain optionality” over the pace of future rate increases. The yen is headed for its biggest weekly decline in two months as hawkish comments from Fed officials spurred bets for another outsized rate hike. Options traders are finally betting on a rise in the dollar-yen currency pair after staying bearish for two months, as they await cues from the next week’s Jackson Hole symposium by the Federal Reserve.

In rates, Treasuries held losses into early US session, leaving yields cheaper by up to 6bp across front-end of the curve, following wider gilt-led selloff after stronger-than-forecast UK retail sales figures in July. US yields cheaper by 6bp to 3.5bp across the curve with front- end led losses flattening 2s10s, 5s30s by around 1bp each; 10- year yields around 2.95%, trading 8.5bp and 7bp richer in the sector vs. gilts and bunds. Bunds and Italian bonds declined for a fourth day, the longest streak since June and July respectively, as 125bps of ECB hikes were briefly priced by year-end, or two half-point increases. Money markets ramped up ECB tightening wagers following hawkish Fed talk and stronger-than-forecast UK retail sales figures in July. Peripheral spreads widen to Germany with 10y BTP/Bund adding 2.3bps to 224.3bps.

WTI trades within Thursday’s range, falling 1.4% to trade around $89. Spot gold falls roughly $4 to trade around $1,754/oz. Spot silver loses 1.4% around $19. Most base metals trade in the red; LME tin falls 1.2%, underperforming peers. LME nickel outperforms, adding 0.8%.

Luckily, there is nothing on today’s calendar. Central bank speakers include Richmond Fed President Barkin, and earnings releases include Deere & Company.

Market Snapshot

- S&P 500 futures down 0.9% to 4,250.00

- STOXX Europe 600 down 0.6% to 437.98

- MXAP down 0.6% to 161.10

- MXAPJ down 0.5% to 524.13

- Nikkei little changed at 28,930.33

- Topix up 0.2% to 1,994.52

- Hang Seng Index little changed at 19,773.03

- Shanghai Composite down 0.6% to 3,258.08

- Sensex down 1.3% to 59,517.87

- Australia S&P/ASX 200 little changed at 7,114.46

- Kospi down 0.6% to 2,492.69

- German 10Y yield little changed at 1.18%

- Euro little changed at $1.0084

- Gold spot down 0.3% to $1,752.91

- U.S. Dollar Index up 0.19% to 107.69

Top Overnight News from Bloomberg

- China’s efforts to stomp out a lucrative carry trade by banks in the nation’s bond market and divert cash to the real economy is meeting with limited success. The spread between the 10-year yield and the overnight borrowing rate remained around 140 basis points, even though the latter rose for four straight days amid the central bank’s cash withdrawals. That means banks can still make a profit by funding from each other in the interbank market and purchasing government bonds

- A larger-than-forecast £4.9 billion ($5.8 billion) UK budget deficit in July took the total for 2022-23 so far to £55 billion pounds — £3 billion more than officials forecast in March

- Investors continued piling into stocks and bonds, dismissing the risk of a more aggressive Federal Reserve as they expect it to ease the pace of rate hikes while inflation pulls back from its peak, according to Bank of America Corp. strategists. Global equity funds attracted $7.9 billion in the week through Aug. 17, strategists led by Michael Hartnett wrote in a note, citing EPFR Global data

- The right-wing coalition led by Giorgia Meloni’s Brothers of Italy party neared a landmark level of support, registering 49.8% of voter approval for Italy’s Sept. 25 election, in a survey by the Tecne research institute

A more detailed look at global markets courtesy of Newsquawk

APAC stocks lacked firm direction despite the mild tailwinds from the US where sentiment was somewhat underpinned by mostly encouraging data. ASX 200 just about kept afloat amid outperformance in energy on recent oil price gains although the upside was limited by weakness in financials and amid another influx of earnings results. Nikkei 225 returned to flat territory beneath the 29k level after early momentum petered out. Hang Seng and Shanghai Comp were indecisive amid a lack of macro drivers and with newsflow dominated by earnings, while markets await a cut to the benchmark lending rates early next week.

Top Asian News

- Indonesia May Impose Nickel Export Tax in 2022, Jokowi Says

- H.K. Home Prices Could Fall 10% After HSBC, StanChart Hike Rates

- Hong Kong Monetary Authority Deputy CEO Edmond Lau Resigns

- Moody’s Reviews Huarong AMC’s Ratings for Downgrade

- Some Country Garden, CIFI USD Notes Set for Record Weekly Gains

- Modi to Be Challenged by Local Leaders in 2024 India Elections

European bourses are under modest pressure, Euro Stoxx 50 -0.6%, in a session of limited newsflow with focus on continuing hawkish price action. Stateside, given the hawkish action, NQ -1.0% is the incremental underperformer ahead of commentary from 2024 voter Barkin. China’s CPCA forecast shows August passenger car sales lifting MM to 1.88mln (prev. 1.77mln), latest COVID outbreak is expected to have a relatively limited impact on the auto market. Deere & Co (DE) Q2 2022 (USD): EPS 6.16 (exp. 6.69), Revenue 14.1bln (exp. 12.78bln); FY view Net 7.0-7.2bln (prev. 7.0-7.4bln, exp. 7.1bln).

Top European News

- Gas Heading for Another Weekly Rise Intensifies Europe’s Pain

- Germany’s Drive to Replace Russian Gas Can’t Rely on Canada

- Germany Risks a Factory Exodus as Energy Prices Bite Hard

- Food Banks for Pets Show UK Inflation Reaching Cats and Dogs

- Londoners Wake to Transit Headaches as Strike Hobbles City

FX

- Dollar continues to reign as risk sentiment sours again and yields ratchet higher, DXY up to 107.930 and close to mid-July high just shy of 108.000

- Euro remains relatively resistant amidst further EGB retracement and strong Eurozone inflation data, EUR/USD sub-1.0100, but above 1.0050.

- No retail therapy for Sterling as wider UK economic worries weigh on the Pound, Cable under 1.1900 and EUR/GBP eyeing 0.8500.

- NZ trade data fails to give Kiwi a lift as deficit remains wide, NZD/USD hovering above 0.6200.

- Yen shrugs off Japanese CPI as UST-JGB spreads widen further, USD/JPY touches 136.76 before waning.

- Loonie and Nokkie undermined by softer oil prices as former awaits Canadian retail sales for independent impetus, USD/CAD 1.2950+, EUR/NOK around 9.8500

- Yuan retreats as Moody’s joins list of those downgrading forecasts for Chinese growth this year, USD/CNY over 6.8100 and USD/CNH almost 6.8300 overnight.

Fixed Income

- Only dead cat bounces in debt as hawkish Central Bank and hot inflation vibes persist.

- Bunds through trendline support to 152.61 and 10 year yield above 1.15% Fib resistance.

- Gilts probing 113.00 vs 113.45 at best and T-note towards base of 118-11/118-29+ range .

Commodities

- Under broad pressure given USD strength with crude curtailed as it awaits another JCPOA response; benchmarks lower by circa. USD 1.50/bbl, vs USD 7/bbl ranges for the week.

- Spot gold clipped by the USD, though only by just over USD 5/oz compared to weekly parameters of over USD 50/oz; broader metals in-fitting in limited newsflow.

- China’s daily coal output +19.4% YY, between August 1st and 17th, via the Energy Administration.

US Event Calendar

- Nothing major scheduled

DB’s Tim Wessel concludes the overnight wrap

Filling in again from Stateside much like the rumored involvement of yank Elon Musk in the English product Manchester United. The metaphor does not have much life beyond that, however. Despite what you may have heard, I am not a billionaire nor do I have any designs on going to space, while on the product side, the EMR has a chance of success this year.

Taking the developments by time zones. In Europe, yields crept slightly higher on the now familiar formula of tighter expected ECB policy and concerns about energy pricing. On the former, in a Reuters interview, the ECB’s Schnabel said that “The concerns we had in July have not been alleviated… I do not think this outlook has changed fundamentally.” She also said that “I would not exclude that, in the short run, inflation is going to increase further”. The ECB’s Kazaks also echoed this, saying that “we will continue to increase interest rates” so as to prevent inflation becoming entrenched. Markets continue to fully price in another 50bp move at the next meeting in September, with 52bps currently priced in, so some probability of an even larger hike. On the energy front, price pressures continue to get worse, where natural gas futures closed at a record high of €241 per megawatt-hour, with year-ahead German power registering a fresh record of their own, closing at €540 per megawatt-hour. In line with what we’ve covered, Germany is offering fiscal support to alleviate price pressures, as German Chancellor Scholz announced a temporary VAT cut on natural gas from 19% to 7%, which will apply for 18 months from October 1. It’s worth plugging our team’s latest gas supply monitor again, link here to stay on top of the latest.

All told, the yield move was rather modest, with 10yr bunds +1.9bps higher, outpacing increases in OATs (+1.7bps) and BTPs (+0.4bps), which helped support risk assets on the day. For their part, equities also posted a modest gain, as the STOXX 600 climbed +0.39%, the DAX gained +0.52%, and the CAC increased +0.45%.

In the US, it was another day of mixed, but supportive data on balance. Initial jobless claims fell to 250k (vs. 264k expected). Continuing claims, which our US econ team has identified as one of the best leading indicators for recessionary risk, also came in below expectations at 1437k (vs. 1455k). Reminder, our team has found that when the rolling 4-week average of continuing claims increases around 11% above the last year’s nadir, near-term recession risk increases. That warning level would be around 1456k, still some ways above the 4-week average of 1413k. Indeed, one need go back to the first week of April to find any individual print, let alone moving average, that has breached 1456k, and that was as claims were still falling, only to hit their lows in late May. Elsewhere in data, the Philadelphia Fed Business Outlook surprised to the upside at 6.2, versus expectations of -5.0 and a prior print of -12.3. On the downside, housing activity continued to be strangled by Fed tightening, with existing home sales falling to a 4.81m pace (vs. 4.86m expectations), their lowest since the summer of 2020’s stilted homebuying season.

There was a suite of Fed officials on the tape yesterday. Across speakers, they still sounded a resolute tone around current inflationary ills, but offered different prescriptions for the path of policy going forward. On one end, San Francisco Fed President Daly expressed support for a 50bp hike to the fed funds target range at the September FOMC, with policy rates getting “a little” above 3% by then end of this year, reserving the right to go higher if the data call for that. St. Louis Fed President Bullard played the customary foil, preferring to hike rates 75bps in September, getting policy closer to 4% by year-end. Bullard noted that the Fed “shouldn’t drag out process of raising rates”. Splitting the difference, Kansas City President George noted it was too early to declare victory over inflation, so the case for continued hikes remained strong, even if the Committee had to be mindful of what the lagged impact of tightening may look like, echoing the July meeting minutes. Finally, Minneapolis President Kashkari was ambivalent about the prospects of a soft landing, saying he didn’t know if the Fed could bring inflation back to target without a recession given he couldn’t count on supply side expansion, particularly in the labor market. Like other speakers, he re-emphasized breaking inflation’s back was urgent.

In short, nothing explicitly new from Fed speakers, so it holds that Chair Powell’s Jackson Hole remarks next Friday, August 26, (confirmed by the Fed yesterday), along with the inflation and employment data before the September FOMC are the key events for policy over the near-term.

Yields on 2yr Treasuries fell -8.8bps, while increased +2.7bps, while 10yr yields were -1.5bps lower, driving the 2s10s yield curve to its steepest level in more than two weeks at -32bps. Like their European counterparts, US equities were similarly subdued, with the S&P 500 gaining +0.23%. Energy shares climbed +2.53%, following a +3.14% increase in Brent crude oil, but otherwise sector dispersion was rather narrow between Tech gaining +0.49% and Real Estate lagging at -0.75%.

On the war in Ukraine, talks with President Zelenskiy, UN Secretary General Guterres, and Turkish President Erdogan were staged in Lviv. Following the meeting, Turkey is set to evaluate the talks with President Putin, cementing Turkeys status as the key interlocutor between Ukraine and Russia. Reports from the meeting suggested diplomatic progress seemed possible, and our team took it as a positive that both sides appeared to be open to indirect communication, though much work remains.

Asian stock markets are mixed this morning following a quiet US session. The Nikkei (+0.10%) and the Hang Seng (+0.46%) are trading in positive territory while the Shanghai Composite (-0.28%), the CSI (-0.27%) and the Kospi (-0.10%) are trading lower. US equity futures are likewise sleepy, with the S&P 500 (-0.08%) and NASDAQ (-0.08%) flitting around zero.

Japan’s headline inflation rose +2.6% y/y in July, in line with market expectations and against a +2.4% rise in June, edging past the Bank of Japan’s 2% inflation goal for a fourth straight month. The increase in core CPI (+2.4% y/y from +2.2% in June) was the sharpest in about seven and half years.

To the day ahead now, and data releases include UK retail sales and German PPI for July. Central bank speakers include Richmond Fed President Barkin, and earnings releases include Deere & Company.

END

AND NOW NEWSQUAWK

Further hawkish price action in relatively limited newsflow, Fed’s Barkin due – Newsquawk US Market Open

FRIDAY, AUG 19, 2022 – 06:45 AM

- European bourses are under modest pressure, Euro Stoxx 50 -0.6%, in a session of limited newsflow with focus on continuing hawkish price action.

- Stateside, given the hawkish action, NQ -1.0% is the incremental underperformer ahead of commentary from 2024 voter Barkin.

- Commodities are under broad pressure given USD strength with crude curtailed as it awaits another JCPOA response.

- Dollar continues to reign as risk sentiment sours again and yields ratchet higher and steeper.

- Looking ahead, highlights include commentary from Fed’s Barkin.

As of 11:15BST/06:15ET

For the full report and more content like this check out Newsquawk.

Try a 14 day trial with Newsquawk and hear breaking trading news as it happens.

LOOKING AHEAD

- Speech from Fed’s Barkin.

- Click here for the Week Ahead preview.

GEOPOLITICS

RUSSIA-UKRAINE

- US President Biden’s administration is readying about USD 800mln in additional security aid for Ukraine with an announcement as early as Friday, according to Reuters sources.

- Ukraine’s Energoatom says Russian forces are planning to switch off functioning power blocks at the Zaprozhzia power plant and disconnect them from the Ukrainian grid, via Reuters.

- Turkish President Erdogan says he will discuss the Zaprozhzia power plant with Russian President Putin following talks with Ukraine President Zelenskiy in Lviv. Zelenskiy requested that Russia removes all mines near the power plant.

OTHER

- North Korean leader Kim’s sister said North Korea will never deal with South Korea’s “audacious initiative” offer and North Korea stated it will not respond to South Korea’s proposals, according to Yonhap citing state media.

- South Korean Presidential office expressed regret over North Korea’s vow to continue nuclear development, while the Unification Minister also expressed regret over North Korea’s ‘very disrespectful’ criticism against President Yoon, according to Reuters.

- WSJ’s Norman, on the Iranian nuclear deal, says “A reasonable assumption, if unconfirmed, that the US will respond to Iranian concerns/issues today via EU.”.

EUROPEAN TRADE

EQUITIES

- European bourses are under modest pressure, Euro Stoxx 50 -0.6%, in a session of limited newsflow with focus on continuing hawkish price action.

- Stateside, given the hawkish action, NQ -1.0% is the incremental underperformer ahead of commentary from 2024 voter Barkin.

- China’s CPCA forecast shows August passenger car sales lifting MM to 1.88mln (prev. 1.77mln), latest COVID outbreak is expected to have a relatively limited impact on the auto market.

- Deere & Co (DE) Q2 2022 (USD): EPS 6.16 (exp. 6.69), Revenue 14.1bln (exp. 12.78bln); FY view Net 7.0-7.2bln (prev. 7.0-7.4bln, exp. 7.1bln).

- Click here for more detail.

FX

- Dollar continues to reign as risk sentiment sours again and yields ratchet higher, DXY up to 107.930 and close to mid-July high just shy of 108.000

- Euro remains relatively resistant amidst further EGB retracement and strong Eurozone inflation data, EUR/USD sub-1.0100, but above 1.0050.

- No retail therapy for Sterling as wider UK economic worries weigh on the Pound, Cable under 1.1900 and EUR/GBP eyeing 0.8500.

- NZ trade data fails to give Kiwi a lift as deficit remains wide, NZD/USD hovering above 0.6200.

- Yen shrugs off Japanese CPI as UST-JGB spreads widen further, USD/JPY touches 136.76 before waning.

- Loonie and Nokkie undermined by softer oil prices as former awaits Canadian retail sales for independent impetus, USD/CAD 1.2950+, EUR/NOK around 9.8500

- Yuan retreats as Moody’s joins list of those downgrading forecasts for Chinese growth this year, USD/CNY over 6.8100 and USD/CNH almost 6.8300 overnight.

- Click herefor more detail.

Notable FX Expiries, NY Cut:

- Click here for more detail.

FIXED INCOME

- Only dead cat bounces in debt as hawkish Central Bank and hot inflation vibes persist.

- Bunds through trendline support to 152.61 and 10 year yield above 1.15% Fib resistance.

- Gilts probing 113.00 vs 113.45 at best and T-note towards base of 118-11/118-29+ range .

- Click here for more detail.

COMMODITIES

- Under broad pressure given USD strength with crude curtailed as it awaits another JCPOA response; benchmarks lower by circa. USD 1.50/bbl, vs USD 7/bbl ranges for the week.

- Spot gold clipped by the USD, though only by just over USD 5/oz compared to weekly parameters of over USD 50/oz; broader metals in-fitting in limited newsflow.

- China’s daily coal output +19.4% YY, between August 1st and 17th, via the Energy Administration.

- Click here for more detail.

NOTABLE HEADLINES

- German Finance Ministry said the German economic outlook is gloomy and clouded by energy price rises and supply chain issues, according to Reuters.

- Rhine water level at the Kaub crossing point forecast to hit ~148cm on August 23rd.

DATA RECAP

- UK Retail Sales MM (Jul) 0.3% vs. Exp. -0.2% (Prev. -0.1%, Rev. -0.2%); YY (Jul) -3.4% vs. Exp. -3.3% (Prev. -5.8%, Rev. -6.1%)

- UK Retail Sales Ex-Fuel MM (Jul) 0.4% vs. Exp. -0.2% (Prev. 0.4%); YY (Jul) -3.0% vs. Exp. -3.1% (Prev. -5.9%)

- UK GfK Consumer Confidence (Aug) -44 vs. Exp. -42.0 (Prev. -41.0)

- German Producer Prices MM (Jul) 5.3% vs. Exp. 0.6% (Prev. 0.6%); YY (Jul) 37.2% vs. Exp. 32.0% (Prev. 32.7%)

NOTABLE US HEADLINES

- Apple (AAPL) disclosed serious security vulnerabilities for iPhones, iPads and Macs, which could potentially allow attackers to take complete control of devices, according to Sky News.

- Click here for the US Early Morning Note.

APAC TRADE