AUGUST 22/GOLD DOWN $14.00 TO $1735.75//SILVER DOWN 17 CENTS TO $18.99//PLATINUM UP $22.00 TO $875.10//PALLADIUM DOWN $138.35 TO $1989.30//EURO BREAKS THE PARITY BARRIER TRADING AT 0.9933 TO THE DOLLAR//COVID UPDATES/VACCINE IMPACT/DR PAUL ALEXANDER//TED BUTLER AND EGON VON GREYERZ IMPORTANT READS//EUROPEAN ENERGY CRISIS ESCALATE WITH ANOTHER RUSSIAN SHUTDOWN//UK PORTS HIT WITH A MASSIVE STRIKE//USA NATURAL GAS HITS 14 YR HIGHS//SWAMP STORIES FOR YOU TONIGHT//

GOLD: NUMBER OF NOTICES FILED FOR AUGUST CONTRACT:

5 NOTICES FOR 500 OZ //0.0155 TONNES

total notices so far: 33,118 contracts for 3,311,800 oz (103.01 tonnes)

SILVER NOTICES: 2 NOTICES FILED FOR 10,000 OZ/

total number of notices filed so far this month 945 : for 4,725,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $14.00

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.718 TONNES FROM THE GLD.

INVENTORY RESTS AT 985.83 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $0.17 CENTS

AT THE SLV// ://A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 483.684 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 1276 CONTRACTS TO 145,047. AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GOOD GAIN IN OI WAS ACCOMPLISHED DESPITE OUR $0.38 LOSS IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.38) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD A STRONG GAIN OF 655 CONTRACTS ON OUR TWO EXCHANGES. HOWEVER WE HAD A SOME LIQUIDATION OF SPECULATOR SHORTS.

WE MUST HAVE HAD: I) SOME SPECULATOR SHORT LIQUIDATIONS//CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A FAIR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 25,000 OZ QUEUE JUMP / // V) HUGE SIZED COMEX OI GAIN/(//SOME SPEC LIQUIDATION)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -105

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTACTS for 16 days, total 7986 contracts: 39.930 million oz OR 2.495 MILLION OZ PER DAY. (532 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 39.930 MILLION OZ

.

LAST 16 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 39.930 MILLION OZ (A LOT LESS THAN NORMAL//THE CROOKS ARE SCARED TO ISSUE MORE EFP’S)

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1346 DESPITE OUR $0.38 LOSS IN SILVER PRICING AT THE COMEX// FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1211 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /SOME BANKER ADDITIONS AND SOME SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 25,000 OZ QUEUE JUMP // .. WE HAD A HUGE SIZED GAIN OF 2557 OI CONTRACTS ON THE TWO EXCHANGES FOR 12.785 MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 2 NOTICE(S) FILED TODAY FOR 10,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 1276 CONTRACTS TO 458,131 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:–254 CONTRACTS.

.

THE SMALL SIZED INCREASE IN COMEX OI CAME DESPITE OUR FALL IN PRICE OF $8.00//COMEX GOLD TRADING/FRIDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERINGS//CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 98.367 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S EFP JUMP TO LONDON OF 1500 OZ //NEW STANDING 104.164 TONNES

YET ALL OF..THIS HAPPENED WITH OUR FALL IN PRICE OF $8.00 WITH RESPECT TO FRIDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 5764 OI CONTRACTS 17,928 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4488 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 458,131

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5764 CONTRACTS WITH 1276 CONTRACTS INCREASED AT THE COMEX AND 4488 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 6018 CONTRACTS OR 18.718 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4488) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (1276): TOTAL GAIN IN THE TWO EXCHANGES 5764 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR AUGUST. AT 99.272 TONNES FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 1500 oz. 3) ZERO/ LONG LIQUIDATION//// //.,4) FAIR SIZED COMEX OPEN INTEREST GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

41,722 CONTRACTS OR 4,172,200 OZ OR 129.77 TONNES 16 TRADING DAY(S) AND THUS AVERAGING: 2607 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES: 129.77 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 129.77/3550 x 100% TONNES 3.66% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT., FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A HUGE SIZED 1241 CONTRACT OI TO 145,047 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1211 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 1211 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1211 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1241 CONTRACTS AND ADD TO THE 1211 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 2452 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 12.260 MILLION OZ

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED UP 19.72 PTS OR 0.61% //Hang Sang CLOSED DOWN 116.05 OR 0595% /The Nikkei closed DOWN 135.83 OR % 0.47. //Australia’s all ordinaires CLOSED DOWN 0.97% /Chinese yuan (ONSHORE) closed DOWN AT 6.8423//OFFSHORE CHINESE YUAN DOWN 6.8445// /Oil UP TO 88.97 dollars per barrel for WTI and BRENT AT 96.55// / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1276 CONTRACTS TO 458,131 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR FALL OF $8.00 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (4488 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF AUGUST.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4488 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :4488 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4488 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED SIZED TOTAL OF 5764 CONTRACTS IN THAT 4488 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 1276 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $ 8.00. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING AUGUST (104.164),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.164 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $8.00) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED TOTAL GAIN ON OUR TWO EXCHANGES // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS////// WE HAVE REGISTERED A GOOD SIZED GAIN OF 17.928 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR AUGUST (104.164 TONNES)…

WE HAD 254 CONTRACTS ADDED TO COMEX TRADES. THESE WERE ADDED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 5764 CONTRACTS OR 576,400 OZ OR 17.928 TONNES

Estimated gold volume 141,740/// extremely poor/

final gold volumes/yesterday 148,081/extremely poor

INITIAL STANDINGS FOR AUGUST ’22 COMEX GOLD //AUGUST 22

Total monthly oz gold served (contracts) so far this month

33,118 notices 3,311,800 OZ 103.01 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

i)

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i)Into Brinks: 1279.092 oz

total deposits 1279.092, oz

2 customer withdrawals:

i) Out of Manfra 9467.661 oz

ii) Out of Brinks:226.842 oz

ii) Out of Brinks 9694.503 oz

total: 9654.503 oz

total in tonnes: 0.30029 tonnes

Adjustments: dealer to customer //4

HSBC 201.610oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 376 contracts having LOST 455 contracts .

We had 440 notices served upon yesterday so we LOST 15 contracts or an additional 1500 oz will NOT stand for delivery in this very active month of August as they were EFP’d over to London.

Sept. lost 77 contracts to 3550 contracts.

October gained 120 contracts up to 40,087

We had 5 notice(s) filed today for 500 oz FOR THE AUGUST 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 5 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 5 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2022. contract month,

we take the total number of notices filed so far for the month (33,118) x 100 oz , to which we add the difference between the open interest for the front month of (AUGUST 376 CONTRACTS ) minus the number of notices served upon today 5 x 100 oz per contract equals 3,348,900 OZ OR 104.164 TONNES the number of TONNES standing in this active month of AUGUST.

thus the INITIAL standings for gold for the AUGUST contract month:

No of notices filed so far (33,118) x 100 oz+ (376) OI for the front month minus the number of notices served upon today (5} x 100 oz} which equals 3,349,400 oz standing OR 104.164 TONNES in this active delivery month of August.

TOTAL COMEX GOLD STANDING: 104.1804 TONNES (A HUGE STANDING FOR AUGUST ( ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 945 x 5,000 oz = 4,725,000 oz

to which we add the difference between the open interest for the front month of AUGUST(55) and the number of notices served upon today 2 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST./2022 contract month: 945 (notices served so far) x 5000 oz + OI for front month of AUGUST (55) – number of notices served upon today (2) x 5000 oz of silver standing for the AUGUST contract month equates 4,990,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

AUGUST 10//WITH GOLD UP $2.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES

AUGUST 9/WITH GOLD UP $6.70: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES.

AUGUST 8/WITH GOLD UP $13.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FORM THE GLD//INVENTORY RESTS AT 999.16 TONNES

AUGUST 5/WITH GOLD DOWN $14.25: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .33 TONNES FROM THE GLD////INVENTORY RESTS AT 1000.32 TONNES

AUGUST 4 WITH GOLD UP $29.00 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES FROM THE GLD///INVENTORY REST AT 1000.65 TONNES

AUGUST 2/WITH GOLD UP $3.70; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD//INVENTORY RESTS AT 1002.97 TONNES//

AUGUST 1/WITH GOLD UP $5.75: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 29//WITH GOLD UP $12.50; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1005.29 TONNES

JULY 28/WITH GOLD UP $31.25; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 27.//WITH GOLD UP $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 26/WITH GOLD DOWN $1.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.29 TONNES

JULY 25/WITH GOLD DOWN $7.85: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 1005.87 TONNES

JULY 22/WITH GOLD UP $17.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 21/WITH GOLD UP $11.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.101 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.87 TONNES

JULY 20/WITH GOLD DOWN $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1009.06 TONNES

JULY 19/WITH GOLD DOWN $.35 :BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22 TONNES FROM THE GLD//INVENTORY RESTS AT 1009.06 TONNES

GLD INVENTORY: 985.83 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTO THE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 10/WITH SILVER UP 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 9/WITH SILVER DOWN 25 CENTS TODAY: TWO CHANGES IN SILVER INVENTORY AT THE SLV: FIRST: A DEPOSIT OF 461,000 OZ INTO THE SLV AND THEN A WITHDRAWAL OF 1.014 MILLION OZ..//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 8/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 5/WITH SILVER DOWN 28 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 922,000 OZ FROM THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 4 WITH SILVER UP 21 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 527,000 OZ FROM THE SLV////INVENTORY RESTS AT 486.634 MILLION OZ

AUGUST 2/WITH SILVER DOWN 21 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.504 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.161 MILLION OZ//

AUGUST 1/WITH SILVER UP 17 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE GLD: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 483.657 MILLION OZ//

JULY 29/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 461,000 OZ FROM THE SLV..//INVENTORY RESTS AT 483.657 MILLION OZ/

JULY 28/WITH SILVER UP $1.24 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 484.118 MILLION OZ/

JULY 27/.WITH SILVER UP 4 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL 11.479 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 484.118MILLION OZ//

JULY 26/WITH SILVER UP 16 CENTS: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.504 MILLION OZ FROM THE SLV//: //INVENTORY RESTS AT 495.597 MILLION OZ//

JULY 25/WITH SILVER DOWN 24 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.383 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 499.101 MILLION OZ//

JULY 22/WITH SILVER DOWN 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 500.484 MILLION OZ//

JULY 21/WITH SILVER UP 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.19 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 500.484MILLION OZ/

JULY 20/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 8.253 MILLION OZ FORM THE SLV/INVENTORY RESTS AT 507.585 MILLION OZ//

JULY 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ//

CLOSING INVENTORY 483.684 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

END

3.Chris Powell of GATA provides to us very important physical commentaries

A good commentary for us.

see below

Ted Butler: Why I own SLV despite its fraud and crooks

Submitted by admin on Fri, 2022-08-19 15:10Section: Daily Dispatches

3:14p ET Friday, August 19, 2022

Dear Friend of GATA and Gold (and Silver):

Silver market analyst Ted Butler’s new commentary, “The Short Position in SLV,” explains why, while the huge short position in the big exchange-traded fund cheats its investors (something about which he has complained again to the U.S. Securities and Exchange Commission), and while the custodian of the fund’s metal, JPMorganChase, is a bunch of crooks, he still considers the fund well worth investing in, as he has done.

Butler’s commentary is headlined “The Short Position in SLV” and it’s posted at GoldSeek’s companion site, SilverSeek, here:

For the sake of SLV’s investors, one may hope that Butler is right, even as those investors might do well to keep in mind a more famous episode of short selling that somehow did not involve JPMorganChase:

Having mentioned the sharp recent increase in the short position on SLV, the big silver ETF, in my last two missives to subscribers, I thought it proper to expand on the matter. As always, this is not a suggestion to buy, sell or hold shares of SLV and in the interest of full disclosure, I (my wife) still hold the same positions in SLV and PSLV, since the last time I wrote about this issue.

The important point is that SLV is the single largest repository of physical silver in the world, owned and sponsored by the world’s largest asset manager, BlackRock, and its custodian is JPMorgan. That combination alone is enough to set off anyone paying the slightest bit of attention to the workings of the silver market on a tangent and gets just about everyone’s juices flowing, most often in a negative manner. While the quest for a balanced view on SLV is challenging, it is also quite important, given the place SLV holds in the world of silver.

Having followed the fortunes of SLV since when it was first proposed, even before it commenced trading in April 2006, I’ve always tried to analyze it as objectively as possible. In fact, back in the day, more than 14 years ago, I helped convince the then-sponsor of SLV, Barclays Global Investors, to publicly list the serial numbers, specific weights and hallmarks for each 1000 bar held by the trust – the one true safeguard that the metal held to back the trust was actually held.

Trying to be as objective as possible about such an important security – the world’s largest holder of physical silver – the one thing that always struck me as manipulative and fraudulent was short selling in SLV. I let my feelings be known to the sponsors of the trust whenever the short position grew excessively large, both when Barclays owned the trust and when BlackRock bought and took over Barclays’ I-Shares ETF operations.

Long-time readers may recall my last tussle with BlackRock ten years ago, when my objections about short selling in SLV, prompted BlackRock to have their outside attorneys allege that I was defaming BlackRock and its CEO and President, which was not my intent. The issue blew over and the short position on SLV remained moderate until recently.

Quite ironically, in Feb 2021, at the height of the “meme stock” phenomenon, which spilled over into silver and SLV, important new amendments to the prospectus of SLV, in the form of new risk factors were published, including the admission that there might not be enough physical silver available to continue operations as had been in the past. Included were warnings to those selling short shares of SLV, which ironically, was along the same lines of what I had warned BlackRock about ten years earlier.

The recent sharp increase in the short position on SLV is important enough to have prompted me to complain, only this time not to BlackRock, but to the Securities and Exchange Commission. Last week, I sent this letter to several sections of the SEC –

August 11, 2022

Dear Sir;

I am contacting you to lodge a complaint against BlackRock, Inc. for failing to uphold its fiduciary responsibilities both to shareholders of its I-Shares Silver Trust (SLV) and in its own shares (BLK). The matter involves manipulative and fraudulent short selling in shares of SLV, an issue which I have raised with its senior management in the past (to no avail). BlackRock is the sponsor of SLV.

SLV is a particularly unique security in which shareholders are led to believe that each share is backed by a specific quantity of physical silver – one ounce of silver for every share, minus the accumulated management fee since the trust’s introduction in 2006. The problem with the short selling of shares, even if borrowed and not sold naked short, is that the shorted shares are actually “phantom” shares in which share owners are deprived of metal backing as set out in the prospectus.

What prompts my (renewed) complaint at this time is a recent and rather shocking increase in the short position of SLV, as of the most recent reporting date of July 29, 2022, in which the short position grew to 47.5 million shares, or 9% of total shares outstanding. This means that roughly one out of every 10 shares outstanding has no physical silver backing.

Compounding the problem is that in February 2021, at the height of intense retail investor interest in SLV and silver in general, a whole set of new risk factors were issued in a prospectus amendment, in which important new risk factors were laid out, including an admission that there may not be sufficient physical silver available to conduct business as usual. Included in those new risk factors was a specific warning to short sellers to be advised that short selling in SLV may be particularly risky. At the time of the prospectus revisions, the short position in SLV was 17 million shares or 2.8% of total shares outstanding.

The most recent short position in SLV is now close to three times larger in total shares shorted and more than three times larger in terms of a percent of total shares outstanding, so obviously BlackRock is ignoring its own prospectus amendments issued in Feb 2021.

Not only are the unbacked shares created by the excessive short selling of real concern to shareholders of SLV (of which my wife holds in her retirement account), but shareholders of BlackRock itself are being cheated due to the phantom shares created by the excessive short selling not paying the annual management fee on shares not officially issued, thus depriving shareholders of BLK an important source of income.

The most plausible explanation for the large increase (50% over the past month) in SLV shares shorted is that the short sellers didn’t wish to abide by the prospectus to deposit silver for newly created shares to avoid upward price pressure in the physical silver market – clearly a manipulative and fraudulent ploy.

If you need any additional information, please don’t hesitate to contact me, as this is very much a serious market crime in progress.

Theodore Butler

Whether the SEC acts on this is beyond my control, but I believe it should. Excessive short selling has no place in shares of SLV, for the reasons contained in my letter. At the same time, however, I would anticipate that the haters of SLV, of which there are many, may attempt to put this short-selling of shares into another reason to hate SLV. I suppose it’s somewhat natural for many to diss SLV, considering the competition it provides for those offering other forms of silver, as the vast majority of SLV critics just happen to market silver in other forms. Please allow me to present some counterbalancing factors.

Generally speaking, a large short position in any stock can be a very bullish market factor, unless the stock being shorted represents a company that is failing. Since SLV is a play on silver and not a company, it’s not as if silver can go out of business or cease to exist as a going concern. The most plausible reason for the recent excessive shorting in SLV revolves around the short sellers not being able or willing to buy physical silver due to the upward price pressure that would exert on silver and SLV. In fact, I can’t think of another possible reason, particularly considering the recent sharp decrease in commercial shorts positions on the COMEX.

Please remember, what set off the meme stock phenomenon of early 2021 was excessive shorting in stocks like GameStop, which came to be recognized and exploited by buyers. It seems more than reasonable that a similar recognition of what is occurring in SLV could have the same results, namely, of a rush to buy, particularly considering the recent resurgence in meme stock buying enthusiasm.

Back in early 2021, as the meme stock phenomenon was exploding, silver and SLV were considered included in the group, although that proved to be fleeting. I find it particularly ironic that the short position in SLV is now three times larger than it was back then, not something that exists in the other meme stocks to my knowledge. The irony is that excessively large short positions were the prime theme that set off the meme stock phenomenon.

Even though I recognize the low opinion in which many hold JPMorgan, the custodian of SLV, and even BlackRock itself, I am more persuaded that their importance to the financial system would work to the benefit of investors in SLV in the long run. No one could be more convinced of JPMorgan’s manipulative role in silver and gold than me and I believe I was the first to identify JPM as the big silver and gold head crook. That said, following JPM’s deferred criminal prosecution with the Justice Department, I don’t think it would dare jeopardize the agreement by further precious metals criminality. As for BlackRock, I’m still of the opinion that it would be foolish for it to risk severe reputational harm by allowing a scandal to occur on a security that represents less than a tenth of one percent (0.1%) of its total assets under management, said to be upwards of $10 trillion.

One thing to keep in mind is that if my contention is correct that interests related to JPMorgan hold as much as 50% (or more) of the 2 billion oz of silver that exists in 1000 oz bar form, it would be impossible that this is not also the case with the 500 million oz held in SLV. You can be sure that these JPMorgan interests would seek to protect their holdings in SLV, thereby strengthening those interests holding SLV not related to JPM as well.

One other thing I’m not sure I’ve mentioned previously is the possibility that shares of SLV could very well come to trade at a premium to physical silver, in the event the warnings from BlackRock in Feb 2021 ever come to pass. While I was, admittedly, skeptical at first about Izzy Friedman’s warnings of big premiums developing on Silver Eagles some 20 years ago, such premiums are now a fact. I remember hearing many opinions back in the day how it wasn’t worth paying a dollar or two more for Silver Eagles than competing coins, only to have witnessed recently that those buying Silver Eagles back then could now be getting the full price they paid for the coins back in the form of premium alone, with the appreciation in the price of silver as a bonus.

Likewise, I consider it quite possible that a premium on shares of SLV could develop to 1000 oz bars, as and when a shortage deepens. The convenience of holding silver in common stock form in a physical silver shortage could easily boost the shares of SLV and other silver ETFs over spot prices. Even the slightest premium could easily offset the cumulative annual management fee discount built into the current price. Knowing that interests associated with JPMorgan would also benefit from a premium developing in SLV and other silver ETFs is far from a negative strike against such a future occurrence.

Therefore, while I find the recent excessive increase in the short position on SLV to be fraudulent and manipulative, that’s not to say it is bearish from this point. Once a short position is established, the suppressive force it has on price has already been spent. As shorted shares are then bought back (or physical metal is deposited to offset the short sale), a counter-balancing upward price force is exerted.

The world economy and especially the political and economic situation today consists of a potpourri of lethal ingredients which will have dire consequences…

Let’s look at what this deadly potion consists of:

Debts at levels that can never be repaid – sovereign, corporate & private

Epic global bubbles in stocks, bonds & property – all about to collapse

Major geopolitical conflicts with no desire for peace – major wars likely

Energy imbalances and shortages, most self-inflicted

Food shortages leading to major famine and civil unrest

Inflation, leading to hyperinflation & global poverty

Political and economic corruption in US, Europe and most countries

No country will afford social security, medical or pension payments

So what are governments around the world doing to solve these problems?

Nothing of course.

The only thing they know is to print more money. They have never understood that a debt problem cannot be solved with more debt. All they can try to achieve is to pass the baton to the next leader so it will be his problem.

This means that all the political, economic and financial mismanagement of the past 50 years will result in a global collapse never seen before in history.

The consequences will be both dire and unpredictable since the world has no experience of this magnitude and complexity of problems.

So what are global leaders doing?

What is clear is that Western leaders will not assume any responsibility for the coming calamities.

Covid will obviously be blamed although there is a lot of evidence that it was manmade and could have been controlled with simple and cheap existing medicines. And all the lockdowns and restrictions have certainly had a bigger impact than the disease itself. Sweden for example virtually had no lockdowns or mask requirements and did not suffer more deaths than countries in total lockdown.

Special interests like Big Pharma clearly had the politicians in their hands. They had trillions of dollars to gain and nothing to lose since they are immune against any prosecution.

Anyway, it has happened and we can’t go back. The future will tell us if, as many scientists believe, the people’s immune system will have been severely weakened by the vaccines.

Secondly, the Russians will be blamed for the current global economic problems of inflation, energy shortages and decline of global trade. The fact that these problems started well before the Russian invasion of Ukraine is quickly forgotten.

WILL THE WAR DRUMS BECOME LOUDER?

Since 3600BC, governments have fought 14,000 wars against each other. As far as I am aware, there is no period in history without an important war.

At the end of the 30-year war, European nations tried to put a stop to unprovoked wars with the 1648 Treaty of Westphalia. The peace conference in Muenster involved 194 states. The start of the war in 1618 was the Protestant Bohemians rising against the Catholic Holy Roman Empire. The major opponents to the Roman Catholics were the Habsburgs supported by Sweden and the Netherlands. Spain and France were also involved in the war together with many other nations.

Interestingly, my two home countries benefitted from the peace. Sweden by virtue of being a major military power at that time gained substantial territories around the Baltic and Switzerland gained formal independence from Austria.

But the major result of the Westphalian peace treaty in 1648 was:

National self-determination

Precedent for ending wars through diplomatic congresses

Peaceful coexistence among sovereign nations

Acceptance of the principle of non-interference in the affairs of other nations if there was not a clear present danger to the aggressor.

Almost all wars in history have been between neighbouring countries. But in the 20th century the US changed that.

Without provocation and far from its borders, the US invaded Vietnam, Serbia, Iraq, Libya and Syria. So the 300 year old Westphalian principle of non-interference was properly buried by the US on multiple occasions. But not only did the US break this principle but also failed in each single one of the aforementioned conflicts.

One could of course argue that Japan broke the treaty first with the Pearl Harbour attack. But like all aggressors they claimed self defence against potential US interference in Japan’s ambitions in the Pacific.

The Russians will of course argue that they haven’t broken the Westphalian treaty since Ukraine historically has been part of Russia. In the Maidan revolution in 2014, a US inspired coup ousted the Soviet friendly Ukrainian leader and replaced him by a Western friendly leader. Since then Russia has always warned the West that it cannot accept being surrounded by an increasing number of NATO countries just like the Russian missiles on Cuba in 1962 directed against the US.

What we do know is that sadly wars are an integral part of history and as long as there are people on earth, there will be wars

The risk is that what now seems a local conflict in eastern Ukraine will become a major international conflict.

This is not a war between a small innocent country and a superpower. No this is a major conflict between the US and Russia. And since China has declared it is supporting Russia, this is a conflict between the three major super powers in the world.

And since the US has coerced the EU to join against Russia with weapons, money and sanctions, this is a conflict of major proportions.

GERMANY BITING OFF THE HAND THAT FEEDS THEM

The lack of statesmen and strong leadership in the US and EU has created an absurd situation with the EU not just biting the hand that feeds them but actually biting it off totally.

With many European countries being dependent on Russian gas, oil, cereal and fertilisers, EU’s left hand doesn’t know what the right one is doing. Not only is this a human and economic catastrophe of major proportions but one which will have major implications for Europe for a long time. Germany used to be the economic and financial engine of Europe but is now on the way to becoming a basket case. But sadly they haven’t discovered it yet.

Scholz inherited ludicrous Marxist policies from Merkel. For example to close down both nuclear energy and coal was always a recipe for disaster with no medium term viable alternatives. And her immigration policy will not only be economically ruinous for Germany but also lead to major social unrest.

The demographics of Germany is also another irreparable problem. With the lowest fertility rate in Europe combined with the highest life expectancy, Germany is entering a long term cycle of economic contraction.

Add to this that Germany has financed a major part of the Mediterranean EU countries’ woes through the Target2 transfer payment system.

As the Target2 graph shows below, the transfer payments to Italy of €596 billion, Spain €526b, to the ECB €358b, Greece €107b and Portugal €69b have been mainly financed by Germany to the extent of €1.2 trillion.

Add to that the balance sheet of the ECB which has grown more than 8X since 2004 to €8.7 trillion GRAPH and we can confidently state that the whole European Economic Community -ECB- has now become -EDC- or the Economic Debt Community.

It is clear that the old basket cases of Greece, Italy and Spain which were forced by Brussels to change leadership and to take on more debt are the immediate danger to the EU and the Eurozone.

If we just take Italy, their debt has doubled since 2000 to €2.7 trillion which at 150% of GDP means that the country is on the verge of bankruptcy.

But it is not only Italy’s debt that has surged, but even worse, the cost of financing it. Since September 2021, 10 year Italian bond yields have gone up 6X from 0.5% to 3.4%.

This is obviously more than Italy can afford!

GREECE AND ITALY SHOULD LEAVE THE EU NOW

The head of the Bundesbank Joachim Nagel has made it clear that it would be fatal for the ECB to hold borrowing costs down for ill-disciplined Eurozone states. He declared that such action would be “treacherous waters”. So Italy and Greece can no longer expect subsidised rates from the EU.

Italy needs to roll over €300 billion of debt annually plus finance its annual deficit of €100 billion, a real Sisyphean task. When Germany was the rich uncle of the EU, these debt levels were tolerated just to keep this dinosaur from falling apart. But with the coming severe German economic downturn combined with insoluble debt and structural problems in all EU countries, the inevitable collapse of the European dream is now reality as I have predicted for over 20 years.

Politicians always learn too late that political dreams and economic reality are as far apart as heaven and hell. If these politicians ever studied history, they would have learnt that all these illusions of grandeur always end not just in tears but in total collapse.

If I were in charge of Greece and Italy I would quickly default on the debt and create new Drachmas and Liras. That would give these countries a short term relative advantage rather than to sink in the general quagmire of the EU at a later stage. If they stay in the EU, Brussels will force Greece and Italy to take on more debt and impose unacceptable conditions. No country will ever repay their debt anyway or be in a position to finance it so better to run for the exit now rather than to wait for the EU’s total collapse.

So with Germany, Greece, Italy and Spain all having their problems, so does Macron in France. Having lost a working majority, he can no longer afford to be arrogant and will find it hard to reduce the French budget deficits, a condition to get German agreement for joint debt issuance.

So the EU and the Euro is now entering a final chapter. Like all political monstrosities, the fall will take a number of years. Brussels and government leaders in especially Germany and France will remain on the barricades for a long time although everything around them will fall apart. The only thing that could precipitate the fall is a debt default by the ECB when investors instead of buying the worthless debt paper will use it for fuel as they have run out of energy sources.

The only problem is of course that the debt is electronic and therefore unsuitable for burning- Hmmm.

US & GLOBAL INFLATION

Going across the pond, the US elite has never hated someone more than Trump. They tried all they could during his reign and now he is the first ex-president who is being raided by the FBI.

The US regime shot themselves in the foot with the sanctions against Russia. The Russians are still selling their energy to Germany, China, India etc and instead the suffering parties are the US, Europe and the rest of the world with high inflation and energy shortages.

With already high support for the Republicans and Trump, this raid is likely to have the opposite effect of the one desired by the regime. How many times can you shoot yourself in the foot before it really hurts?

UN AGENDA 2030 – THE (UN-)SUSTAINABLE DEVELOPMENT GOALS

This UN programme, supported by Schwab and the WEF (World Economic Forum) was always going to fail.

Starting in 2016, bureaucrats with no understanding of the real economy created this programme signed by 194 nations. There are 17 admirable but unrealistic goals like No Poverty, Zero Hunger, Good Health, Clean Energy, Climate Action etc.

Today almost half way into the programme, every single goal is hopelessly behind schedule with no chance of achieving the target.

How could anyone believe that 194 nations could jointly achieve these 17 goals when not even one single country can do it?

More about Agenda 2030 and Schwab’s attempt to take over the UN in a later article.

MARKETS

As generally is the case before major turns in markets, optimism is still high. But this autumn is likely to change all that as the realities outlined at the beginning of this article finally hit the world.

Stock markets are now extremely near finishing the correction and to resume the downtrend in earnest. It is possible that the real falls in markets will wait until September but the risk is here now and very dangerous.

What we know with certainty is that the world is facing a wealth destruction and wealth transfer of major proportions.

Most paper assets will die a relatively quick death and that includes paper money.

This will obviously include stocks, bonds, property and all derivatives. Falls of 75-95% in the next few years will not be uncommon.

As currencies finish their journey to ZERO (they are already down 97-99% since 1971) no use betting on the horse that comes last to the bottom whether it is the Dollar or the Euro.

They will all get there!

Instead, the only money which has survived in history is gold and silver and these metals will continue to maintain their purchasing power or even enhance it as all fiat money is killed off by governments and central banks by the creation of an unlimited supply.

It is so simple really but still only 0.5% of financial assets are in physical gold in spite of the metal’s golden 5,000 year record. That percentage is about to change drastically.

5.OTHER COMMODITIES: USA/

end

COMMODITIES IN GENERAL/COAL

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings MONDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.8423

OFFSHORE YUAN: 6.8445

HANG SENG CLOSED DOWN 116,05 PTS OR 0.59%

2. Nikkei closed DOWN 135.83 OR 0.47%

3. Europe stocks CLOSED ALL RED

USA dollar INDEX UP TO 108.33/Euro FALLS TO 0.9997

3b Japan 10 YR bond yield: RISES TO. +.212/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 137.00/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.234%/Italian 10 Yr bond yield FALLS to 3.516% /SPAIN 10 YR BOND YIELD RISES TO 2.39%…

3i Greek 10 year bond yield RISES TO 3.701//

3j Gold at $1731.90 silver at: 18.88 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 87/100 roubles/dollar; ROUBLE AT 58.67//

3m oil into the 91 dollar handle for WTI and 96 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 137.00DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 9582–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9582well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.974 DOWN 2 BASIS PTS

USA 30 YR BOND YIELD: 3.217 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,12

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Tumble As Market Braces For Jackson Hole Hawk-ano

MONDAY, AUG 22, 2022 – 08:01 AM

The staggering “most hated rally” melt-up, which we warned back in June would steamroll shorts, and which ended up being one of the biggest summery rallies on record, is officially over…

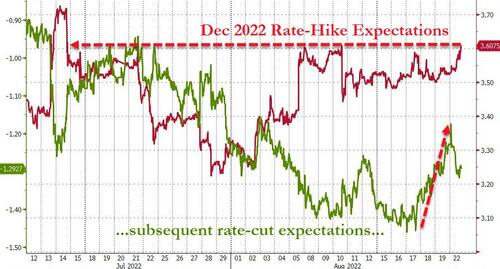

… with BofA superstar strategist Michael Hartnett proven correct again this morning, as stocks retreated further from the bear market peak he called at 4,328 last week, with US equity futures sliding more than 1% on Monday along with stocks in Europe as a risk-off mood took hold at the start of a critical week for global markets when central bankers gather at their annual Jackson Hole symposium starting on Thursday. Both S&P and Nasdaq futures slumped more than 1.1%, with spoos down 50 points to 4,180, as 10-year Treasury yields are little changed after briefly kissing 3.0%, while two-year yields rose about six basis points, deepening the yield-curve inversion that’s seen as a harbinger of a recession. The dollar spot index climbed to a five-week high, while gold and bitcoin slumped.

In China, banks lowered the one-year and five-year loan prime rates on Monday in the aftermath of a decision by the nation’s central bank last week to cut a key policy rate. The Chinese demand outlook has weighed on oil, which briefly sank below $90 a barrel in New York before rebounding and turning green. Traders are monitoring Iran nuclear talks that could lead to more supplies.

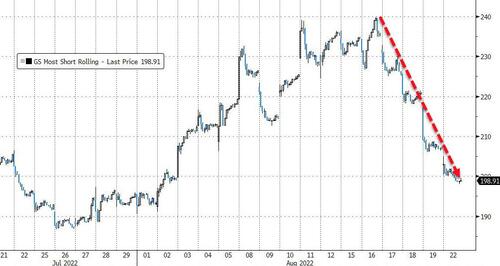

In premarket trading, GameStop and Bed Bath & Beyond led the declines in meme stocks as the latest frenzy in the cohort loses steam. GameStop -5.6%, Bed Bath & Beyond -8.6%; Fellow retail trading favorite AMC Entertainment Holdings was also down as the cinema theater operator’s preferred stock will start trading on the New York Stock Exchange under the ticker “APE” on Monday. Here are some of the biggest U.S. movers today:

Signify Health (SGFY US) jumps 35% in premarket trading after reports of UnitedHealth (UNH US), Amazon.com (AMZN US), CVS (CVS US) and Option Care Health (OPCH US) vying to buy the health- care technology provider.

Tesla (TSLA US) and fellow electric-vehicle makers fall amid worries over a hawkish Fed ahead of Jackson Hole symposium this week, and following data showing China EV registrations declined in July.

Tesla drops as much as 2.7%; Rivian (RIVN US) -2.3%, Nikola (NKLA US) -2.8%.

CFRA cut its recommendation on Netflix (NFLX US) to sell from hold, saying the stock may underperform the S&P 500 Index for the rest of the year after rallying 40% from mid-July lows.

Netflix falls 2.2% amid a decline for Nasdaq futures.

GigaCloud (GCT US) shares rally as much as 40%, before paring gains to trade around 12% higher. The Chinese e-commerce firm is on course for its third session of straight gains following its Nasdaq debut last week.

A huge squeeze in global shares from June’s bear-market lows, stoked by the market’s expectations for a pivot to slower rate hikes, is rapidly fizzling after repeated Fed policy makers warned that interest rates are going higher. This weekend’s Jackson Hole symposium gives Jerome Powell a platform to reset those bets, which are vulnerable to the possibility of persistently elevated price pressures even as economic growth stumbles. Investors are also waking up to the looming acceleration of the Fed’s balance-sheet reduction: quantitative tightening kicks into top gear next month, and will add to pressure on riskier assets which have benefited from ample liquidity.

“It is likely central bankers, including Fed Chair Powell, will remain hawkish in dealing with inflation albeit with a bit of caution creeping in given the emerging economic downturn,” Shane Oliver, head of investment strategy at AMP Services Ltd., wrote in a note.

Of course, the irony would be if markets melt up again next week just as hedge funds aggressively reset shorts: “The expectation is still that Powell will reaffirm what he and his colleagues have been saying in public recently,” said Craig Erlam, a senior market analyst at Oanda. “The risk is that he says something dovish — intentionally or otherwise — after investors position for the opposite and triggers another risk-on rally in the markets.”

The selling also accelerate in Europe, where the Stoxx 600 index dropped to its lowest level in more than three weeks, with autos, chemicals and tech the worst-performing industries as all sectors fall. The DAX lags, dropping 2%. S&P futures slide 1.3%, Nasdaq contracts tumble 1.6%. Here are some of the biggest European movers today:

Fresenius SE shares rose as much as 7.1% after the company said Fresenius Kabi CEO Michael Sen will replace CEO Stephan Sturm. Berenberg says the choice is sensible and expected

EVS Broadcast Equipment shares jumped as much as 4% after the company announced a 10-year, $50m contract with a US-based broadcast and media production company on Friday

Scandinavian Tobacco Group shares fell as much as 19% after the Danish cigar and pipe tobacco manufacturer published its preliminary 2Q numbers and lowered its FY22 guidance

Deliveroo shares dropped as much as 6.8% amid a broader decline among European food delivery stocks. FY23 growth expectations for Deliveroo seem “stretched,” according to Morgan Stanley

B&S Group shares slid as much as 13%, dropping to the lowest since April 2020, after the company reported interim results ING described as a “weak set” of numbers

Intrum shares fell as much as 7.5%, their biggest decline since early May, after the board of the credit management firm replaced CEO Anders Engdahl with immediate effect

Covestro fell as much as 5.9%, hitting lowest since May 2020, after Stifel slashed its price target to EU34 from EU53, citing “shaky prospects” for the company

Dassault Aviation shares were down as much as 4.7% after French Transport Minister Clement Beaune said he wanted to regulate private jet use, according to an interview with Le Parisien newspaper

Earlier in the session, Asian stocks fell to more than a two week low as investors braced for a hawkish stance by US officials at the upcoming Jackson Hole symposium. The MSCI Asia Pacific Index declined as much as 0.7%, with the region’s tech giants TSMC and Tencent Holdings dragging down the measure the most.

MSCI Inc.’s Asia-Pacific share index fell for a third day with losses evident in most major markets except for some gains in China, where a move by banks to trimlending rates aided property developers.

Philippine stocks were the region’s biggest losers, sinking more than 2% as the central bank there signaled more hikes. Chinese equities advanced. Jerome Powell’s Friday speech at the central bankers’ gathering will be the highlight of the week, with markets expecting the Fed chair to reaffirm his determination to get inflation under control. Traders have already been paring back risky bets after Richmond Fed President Thomas Barkin said Friday that the central bank was resolved to curb red-hot inflation even at the risk of a recession.

“The bear market rally seems to be fading ahead of the Jackson Hole symposium this week, which may see the Fed pushing back further on easing expectations for next year,” said Charu Chanana, a senior strategist at Saxo Capital Markets. Equities in mainland China posted rare gains in the region after the nation’s banks lowered their borrowing costs in a bid to stabilize the property market. That gave a positive boost, said Banny Lam, head of research at Ceb International Inv Corp. But markets are still on a bumpy ride as the dollar’s rise extends the outflow of liquidity from Asian assets, he added. Other key issues on the radar include corporate earnings results. More than 340 members of the MSCI Asia Pacific Index, including battery heavyweight Contemporary Amperex Technology and e-commerce giant JD.com, are expected to release their financial results this week.

Japanese stocks fell as hawkish comments from a Federal Reserve official put investors on edge ahead of the Jackson Hole symposium later this week. The Topix Index fell 0.1% to 1,992.59 in Tokyo on Monday, while the Nikkei declined 0.5% to 28,794.50. Keyence Corp. contributed the most to the Topix’s decline, as the producer of sensors and scanners decreased 1.3%. Out of 2,170 stocks in the index, 1,123 fell, 924 rose and 123 were unchanged. “There is a bit of hawkishness coming out from the Fed as its seen trying to correct the direction of the market,” said Naoki Fujiwara, a chief fund manager at Shinkin Asset Management. “In the end, it’s profit taking as the market has gone up so far.”

Indian stocks fell for a second session on concerns the US Federal Reserve may remain committed to tightening monetary policy, which could impact foreign inflows to local equities. The S&P BSE Sensex declined 1.5%, its biggest drop since June 16, to 58,773.87 in Mumbai. The NSE Nifty 50 Index fell by a similar magnitude. Of the 30 member stocks of the Sensex, all but two declined. ICICI Bank Ltd. slipped 2.1% and was the biggest drag on the index. All 19 sectoral sub-indexes compiled by BSE Ltd. dropped, with a gauge of metal companies the worst performer. “While a correction was overdue for sometime after the recent upsurge, fresh concerns of a likely hawkish stance by the US Fed in its September meet and strengthening dollar index turned investors jittery and triggered a massive fall in banking, IT, metal & realty stocks,” Shrikant Chouhan, head of equity research at Kotak Securities Ltd., wrote in a note. Overseas investment into local stocks totaled $6.3 billion from end-June through Aug. 18, after record outflows since October. The Fed’s symposium at Jackson Hole, Wyoming this week will be key for markets for clues on how the central bank plans to tackle price pressures.

In Australia, the S&P/ASX 200 index fell 1% to close at 7,046.90, tracking Friday’s losses on Wall Street as investors weighed the Fed’s next steps. The benchmark posted its worst session since July 11 as all sectors declined in Australia. Adbri was the biggest laggard after reporting a drop in 1H underlying Npat and trimming its interim dividend. EML Payments gained after announcing a buyback. In New Zealand, the S&P/NZX 50 index rose 0.7% to 11,763.95.

In FX, the Bloomberg Dollar Spot Index advanced for a fourth consecutive day, to the highest level since July 18, while the greenback advanced versus most of its Group-of-10 peers. The euro fell to a seven-year low against the Swiss franc, extending losses as concerns about a global economic slowdown prompted demand for the safe-haven Swiss currency. Australia’s dollar gained for the first time in six days after Chinese banks cut their loan prime rates in an effort to bolster the struggling property sector. Aussie bonds extended opening declines. The yen slipped to its lowest level in nearly a month as higher US yields amid growing bets for a hawkish Federal Reserve stance weighed on sentiment. Bonds fell, tracking US Treasuries.

In rates, Treasuries were cheaper, the 10- year US yield rising as much as three basis points to 2.9997%, adding to Friday’s climb, before falling back. 2-year yields rose by around 5bps, inverting the curve further with losses led by front-end of the curve where two-year yields trade 6bp higher versus Friday’s close. Further out the curve, bunds and gilts both lag with notable bear steepening move seen across UK curve. US yields cheaper by 6bp to 1bp across the curve in bear flattening move which sees 2s10s, 5s30s spreads trade tighter by 6bp and 1.5bp on the day; 10-year yields around 2.98% after peaking at 2.9997% in early Asia session. Focus this week is on US auctions which kick-off Tuesday with $44b two-year note sale, followed by $45b five-year Wednesday and $37b seven-year Thursday. IG dollar issuance slate empty so far; issuance expectations are low for the week and dependent on market conditions with the Federal Reserve’s annual symposium in Jackson Hole, Wyoming, due to commence Thursday. Bunds and Italian bonds snapped four- day sliding streaks, with German debt gains led by the belly and Italy’s yield curve bull flattening as stock futures drop. Belgium sells five- and 10-year notes.

In commodities, WTI trades within Friday’s range, first falling as much as 1% before spiking and recovering all losses, with Brent jumping from a session low of $94.50 to a high of $96.90. Most base metals are in the red; LME copper falls 1%, underperforming peers. Spot gold falls roughly $15 to trade near $1,732/oz.

It’s a busy week for the calendar, but we kick off on a day quiet note, with the day at hand featuring the Chicago Fed’s national activity index and earnings from Zoom and Palo Alto Networks.

Market Snapshot

S&P 500 futures down 1.1% to 4,183.75

STOXX Europe 600 down 1.1% to 432.35

MXAP down 0.6% to 159.83

MXAPJ down 0.9% to 518.65

Nikkei down 0.5% to 28,794.50

Topix little changed at 1,992.59

Hang Seng Index down 0.6% to 19,656.98

Shanghai Composite up 0.6% to 3,277.79

Sensex down 1.2% to 58,934.14

Australia S&P/ASX 200 down 0.9% to 7,046.88

Kospi down 1.2% to 2,462.50

Gold spot down 0.7% to $1,735.45

U.S. Dollar Index up 0.18% to 108.36

German 10Y yield little changed at 1.20%

Euro down 0.3% to $1.0006

Top Overnight News from Bloomberg

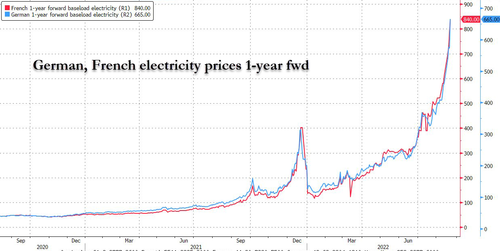

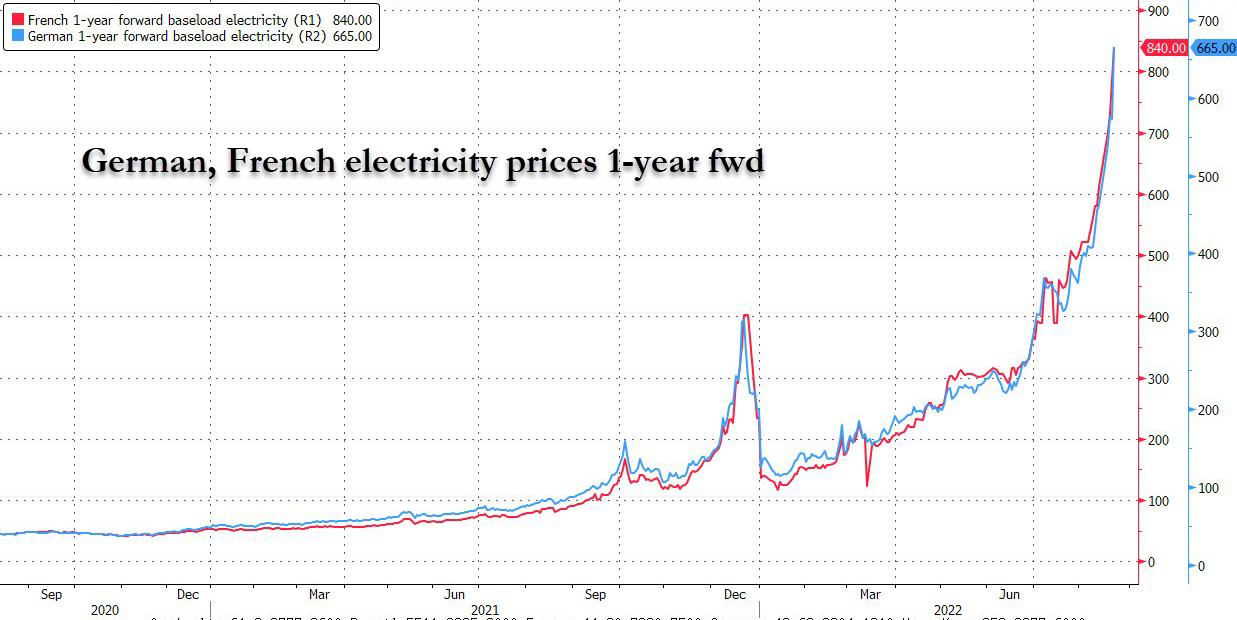

European gas prices surged after Moscow’s move to shut a major pipeline ramped up fears of a prolonged supply halt, leaving Germany once again guessing as to how much Russian fuel it can count on this winter

About 2,000 dockers at the Port of Felixstowe began an eight-day walkout on Sunday, halting the flow of goods through the UK’s largest gateway for containerized imports and exports

Federal Reserve Chair Jerome Powell will have a chance — if he wants to take it — to reset expectations in financial markets when central bankers gather this week at their annual Jackson Hole retreat

A sober warning for Wall Street and beyond: The Federal Reserve is still on a collision course with financial markets. Stocks and bonds are set to tumble once more even though inflation has likely peaked, according to the latest MLIV Pulse survey, as rate hikes reawaken the great 2022 selloff

New Zealand’s central bank is open to the possibility of raising its benchmark rate as high as 4.25% amid uncertainty over the amount of tightening needed to regain control of inflation, Deputy Governor Christian Hawkesby said

Swedish kronor bonds tied to environmental, social and governance goals are helping keep the country’s waning issuance market afloat this year

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks were mostly lower after last Friday’s declines in stocks and bonds across global markets in the aftermath of red-hot PPI data from Germany which rose by a new record high and stoked inflationary concerns, while the region also digests the PBoC’s latest actions on its benchmark lending rates. ASX 200 was pressured with all sectors subdued and as the influx of earnings continued. Nikkei 225 declined at the open as it took its cue from global peers and following reports that PM Kishida tested positive for COVID-19, although the index clawed back around half of the losses with help from a weak currency. Hang Seng and Shanghai Comp were mixed with early indecision as participants reflected on the PBoC’s rate actions in which it cut the 1-Year LPR by 5bps to 3.65% and reduced the 5-Year LPR by 15bps to 4.30% vs expectations for a 10bps cut to both, while the reduction in the 5-Year LPR which is the reference for mortgages, also followed recent measures to support the construction and delivery of unfinished residential projects through special loan schemes from policy banks. This provided some early support for developers although the broader sentiment was restricted amid the extension of factory power cuts in Sichuan.

Top Asian News

China’s Sichuan extended its factory power cuts to August 25th, according to Caixin.

Japanese PM Kishida tested positive for COVID-19 and is recuperating at his official residence, according to NHK.

Singapore PM Lee announced to reduce mask requirements as the COVID-19 situation stabilises with masks to only be required for public transport and healthcare settings with everywhere else optional. PM Lee also confirmed that Deputy PM Wong has been chosen to be the next leader and said authorities will soon announce new initiatives to attract talent, according to Reuters

Aluminum Up as China’s Worsening Power Shortages Tighten Supply

Debt Audit, Constitution Change on Angolan Opposition’s Agenda

Shanghai United Imaging Jumps 65% in Debut Post $1.6 Billion IPO

China Province Extends Power Cuts on Worst Drought Since ‘61

European bourses are under pressure, Euro Stoxx 50 -1.8%, amid Nord Stream 1 maintenance. Updates that sparked a continuation of Friday’s downbeat price action and has caused particular downside for the likes of Uniper (-10%) while defenisve sectors outperform slightly. S futures are in-fitting both in terms of direction and magnitude, ES -1.3%, amid global recession and inflation fears. Panasonic (6752 JT) is to increase prices on 17 products from September 1st due to increasing material and manufacturing costs, hike will range between 2-33%.

Top European News

Cineworld Says It Considers Filing for Bankruptcy in the US

Vodafone Agrees to Sell Hungary Unit for 1.8 Billion Euros (1)

Borealis Curbs Fertilizer Output for Economic Reasons

UK Trial Lawyers Vote to Strike Indefinitely Over Fees

Biggest Rate Hike in Decades Is in Play in Israel: Day Guide

FX

DXY sees a firm start to the week as the index extends gains above 108.00, topping Friday’s peak.

EUR/USD has again dipped under parity amid jitters over a potential supply disruption as Russia is to shut the Nord Stream 1 pipeline.

The Antipodeans are the relative outperformers but have waned off best levels amid the broader deterioration in sentiment.

The JPY has climbed its way up the ranks having experienced mild losses in APAC trade owing to widening yield differentials alongside losses in broad APAC FX.

Turkey’s Central Bank revised rules for Lira government bond collateral for FX deposits in which it raised the RRR for credit from 20% to 30% for bond collateral, according to Reuters.

Fixed Income

A session of pronounced two-way action for fixed benchmarks as energy and inflation vie for the limelight.

Initial upside (Bunds tested 152.85 Fib of Friday) occurred as sentiment deteriorate on Nord Stream 1’s unscheduled maintenance announcement.

However, this then swiftly retraced with core benchmarks modestly negative at worst, perhaps as attention pivoted to the associated inflation implications.

Stateside, USTs have been moving in tandem though the move lower was somewhat more contained as participants look to Jackson Hole at the tail-end of the week.

Commodities

WTI and Brent October contracts have continued trending downwards in a resumption of Friday’s action.

The main focus of this morning has been on European gas prices surging on news that Russia’s Gazprom will shut down the Nord Stream 1 pipeline for three days.

Dutch TTF October surged over 18% whilst European coal for the next year rose over 5% to a new record.

Metals markets are hit by the firmer Dollar with spot gold losing further ground under USD 1,750/oz while LME copper eyes USD 8,000/t to the downside

Libya’s NOC said oil production was running at 1.211mln bpd, while the Waha Oil Co said gas output from the Faragh field increased to 149mcfd on Sunday from 95mcfd on Saturday, according to Reuters.

Caspian Pipeline Consortium suspended oil loadings from two of three single mooring points at its Black Sea terminal for inspection, while CPC exports continue from the third mooring point and August loadings are currently unaffected, according to Reuters sources. Subsequently confirmed

Turkey has increased its imports of Russian oil to over 200k BPD so far this year (vs 98k BPD in the same period last year), according to Refinitiv data.

Norway Prelim. July production: Oil 1.646mln BPD (vs 1.298mln BPD in June); gas 10.9bcm (vs 10.0bcm in June), according to the Norway Oil Directorate.

US Event Calendar

08:30: July Chicago Fed Nat Activity Index, est. -0.25, prior -0.19

DB’s Tim Wessel concludes the overnight wrap

The annual plenary of the global central bank cognoscenti kicks off in Jackson Hole this week. The main macro dish of the deep dog days of summer – where this year’s theme is “Reassessing Constraints on the Economy and Policy” – will be highlighted by Chair Powell’s remarks due on Friday morning. Global production data will serve as suitable hors d’oeuvres throughout the week, while US PCE data on Friday will be a side dish commanding ample attention. Elsewhere, we receive the second estimate of 2Q US GDP; will the poor aftertaste of two consecutive quarterly retractions continue to overwhelm the otherwise supportive ingredients that comprise near-term growth?

Back to Jackson Hole, as the market looks for direction on the uncertain economic outlook and Fed reaction function, Chair Powell’s remarks are one of the key events that can jolt US policy expectations from their recent range, along with inflation and employment data preceding the September FOMC. Indeed, since the day of the July CPI print, 2yr Treasury yields are on net less than a basis point lower, while pricing of the September rate hike has oscillated in a narrow range that effectively has placed equal probabilities on a 50 or 75bp hike, as conviction around the terminal rate and intervening path of policy is low until the market can assess which way inflation (and the Fed) is breaking. The Chair will likely strike an imposing tone against the inflationary scourge, all the more given his remarks last year noted the bout of inflationary pressure was likely to be a transitory phenomenon (important to keep in mind how much the policy outlook can evolve over a 12-month time frame, let alone when uncertainty is this high here). While the Fed has taken to emphasizing two-way risks around the tightening cycle, most visibly in the minutes at the July meeting, the easing of financial conditions since the July meeting may force the Chair to re-orient expectations away from the balance of risks back toward the primary objective of bringing inflation lower.

Executive Board member Schnabel will be the highest profile ECB speaker at the gathering, where focus is on calibrating the ECB’s next policy action, which our team takes careful measure of, here, preserving another 50bp hike as their base case. Before Schnabel, due on a panel Saturday, the ECB’s account of the July meeting’s 50bp hike will provide yet more detail into the super-sized kickoff to the ECB’s tightening cycle. Elsewhere in Europe, the looming energy crisis will remain top of mind. German Chancellor Scholz and Vice Chancellor Habeck are in Canada to try and plug the energy gap left by dwindling Russian gas supplies. Along with alternative imports, the government is still weighing whether to extend the life of heretofore condemned nuclear facilities if sufficient supplies cannot be secured.