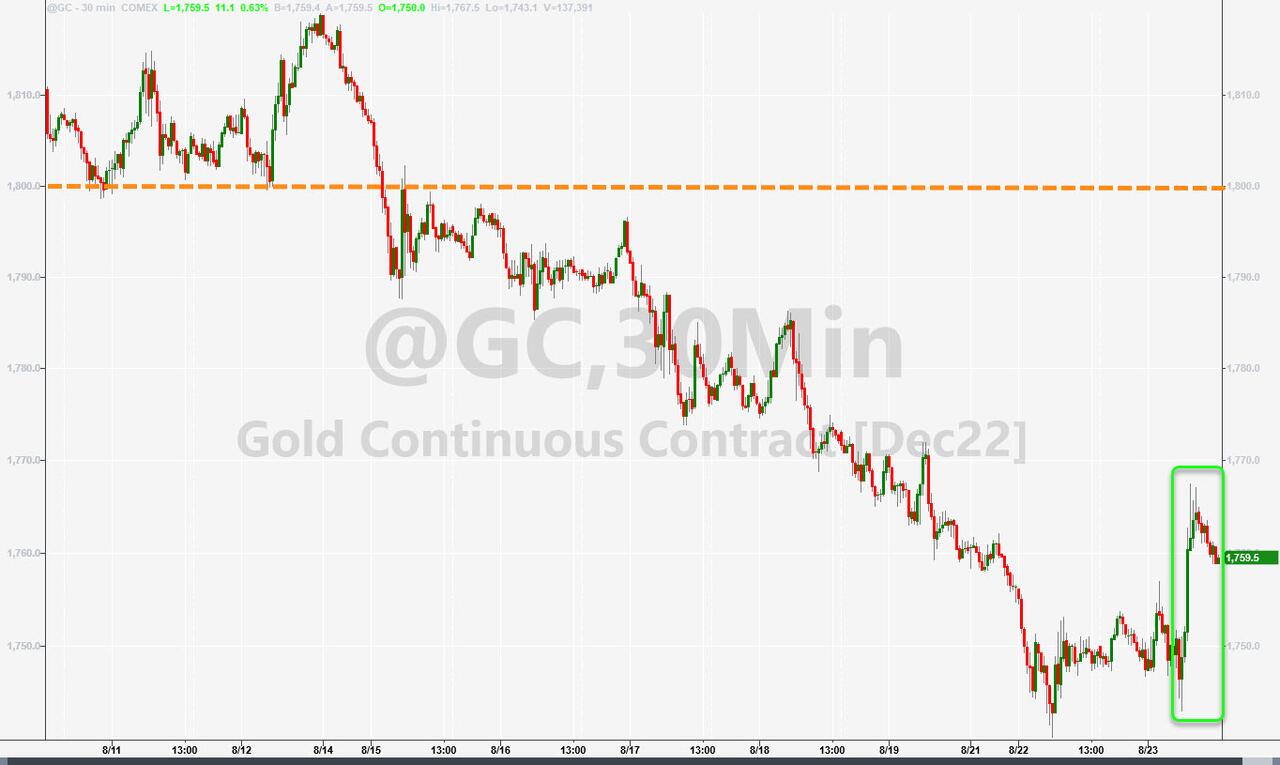

AUGUST 23/GOLD CLOSED UP $12.25 TO $1748.00//SILVER CLOSED UP 16 CENTS TO $19.15//PLATINUM CLOSED DOWN $10.00 TO $885.10//PALLADIUM CLOSED DOWN $2.10 TO $1987.30//COVID UPDATES//VACCINE INJURY/VACCINE IMPACT//EUROPEAN CORN YIELDS THE WORST IN 500 YEARS//EUROPEAN PMI FLASH INDICATES THE DROUGHT HAVING A TERRIBLE EFFECT ON THEIR ECONOMY//POOR USA SERVICE PMI//USA NEW HOMES SALES CRASH!!/PRICE WATERHOUSE COOPER FINALLY REVEALS THE TRUTH BEHIND THE COOKED JOB NUMBERS//WHISTLEBLOWER COMES FORTH REVEALING THE CROOKED DATA FROM TWITTER//SWAMP STORIES FOR YOU TONIGHT//

GOLD: NUMBER OF NOTICES FILED FOR AUGUST CONTRACT:

139 NOTICES FOR 13,900 OZ //0.4323 TONNES

total notices so far: 33,257 contracts for 3,325,700 oz (103.443 tonnes)

SILVER NOTICES: 34 NOTICES FILED FOR 170,000 OZ/

total number of notices filed so far this month 979 : for 4,895,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $12.25

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES TONNES INTO THE GLD.

INVENTORY RESTS AT 987.66 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $0.16 CENTS

AT THE SLV// ://A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 479.490 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 792 CONTRACTS TO 144,255. AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN OI WAS ACCOMPLISHED DESPITE OUR $0.17 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.17) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD A SMALL GAIN OF 145 CONTRACTS ON OUR TWO EXCHANGES. HOWEVER WE HAD A SOME LIQUIDATION OF SPECULATOR SHORTS.

WE MUST HAVE HAD: I) SOME SPECULATOR SHORT LIQUIDATIONS//CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A FAIR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 175,000 OZ QUEUE JUMP / // V) STRONG SIZED COMEX OI LOSS/(//SOME SPEC LIQUIDATION)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -49

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTACTS for 17 days, total 8874 contracts: 44.370 million oz OR 2.773 MILLION OZ PER DAY. (522 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 44.37 MILLION OZ

.

LAST 16 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 44.370 MILLION OZ (A LOT LESS THAN NORMAL//THE CROOKS ARE SCARED TO ISSUE MORE EFP’S)

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 792 DESPITE OUR $0.17 LOSS IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 888 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /SOME BANKER ADDITIONS AND SOME SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 175,000 OZ QUEUE JUMP // .. WE HAD A SMALL SIZED GAIN OF 145 OI CONTRACTS ON THE TWO EXCHANGES FOR 0.725 MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 34 NOTICE(S) FILED TODAY FOR 170,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 674 CONTRACTS TO 457,457 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:–191 CONTRACTS.

.

THE SMALL SIZED DECREASE IN COMEX OI CAME DESPITE OUR FALL IN PRICE OF $14.00//COMEX GOLD TRADING/MONDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERINGS//CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 98.367 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 12,700 OZ //NEW STANDING 104.559 TONNES

YET ALL OF..THIS HAPPENED WITH OUR FALL IN PRICE OF $14.00 WITH RESPECT TO MONDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 3576 OI CONTRACTS 11.122 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4059 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 457,648

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3385 CONTRACTS WITH 674 CONTRACTS DECREASED AT THE COMEX AND 4059 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3576 CONTRACTS OR 11.172 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4059) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (674): TOTAL GAIN IN THE TWO EXCHANGES 3385 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR AUGUST. AT 99.272 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 12,700 oz. 3) ZERO/ LONG LIQUIDATION//// //.,4) SMALL SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

45,781 CONTRACTS OR 4,578,100 OZ OR 142.39 TONNES 17 TRADING DAY(S) AND THUS AVERAGING: 2693 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES: 142.39 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 142.39/3550 x 100% TONNES 4.00% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT., FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 743 CONTRACT OI TO 144M304 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 888 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 888 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 888 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 792 CONTRACTS AND ADD TO THE 888 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED GAIN OF 96 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 0.480 MILLION OZ

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED DOWN 1.57 PTS OR 0.05% //Hang Sang CLOSED DOWN 153.73 OR 0.78% /The Nikkei closed DOWN 341.75 OR % 1.19. //Australia’s all ordinaires CLOSED DOWN 1.21% /Chinese yuan (ONSHORE) closed DOWN AT 6.8463//OFFSHORE CHINESE YUAN DOWN 6.8657// /Oil UP TO 91.93 dollars per barrel for WTI and BRENT AT 97.78// / Stocks in Europe OPENED MOSTLY ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 674 CONTRACTS TO 457,457 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR FALL OF $14.00 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (4059 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF AUGUST.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4059 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :4059 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4059 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED SIZED TOTAL OF 3385 CONTRACTS IN THAT 4059 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 483 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $ 14.00. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING AUGUST (104.569),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.569 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $14.00) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A GOOD SIZED TOTAL GAIN ON OUR TWO EXCHANGES // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS////// WE HAVE REGISTERED A GOOD SIZED GAIN OF 17.928 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR AUGUST (104.569 TONNES)…

WE HAD -191 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE ADDED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3576 CONTRACTS OR 357,600 OZ OR 11.172 TONNES

Estimated gold volume 142,789/// extremely poor/

final gold volumes/yesterday 153,908/extremely poor

INITIAL STANDINGS FOR AUGUST ’22 COMEX GOLD //AUGUST 23

Total monthly oz gold served (contracts) so far this month

33,257 notices 3,325,700 OZ 103.443 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 2

i)Into HSBC: 64,598.526 oz

ii) Into Manfra: 67,208.860 oz

total deposits 131,807.386 oz

2 customer withdrawals:

i) Out of JPMorgan 25,592.193 (796 kilobars)

ii) Out of Loomis: 77,323.155 oz (2405 kilobars)

total: 102,915.348 oz

total in tonnes:3.201 tonnes

Adjustments: dealer to customer //3

JPMorgan: 203,976.081 oz

HSBC: 10,036.399 oz

Manfra: 1444.594 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 498 contracts having GAINED 122 contracts .

We had 5 notices served upon yesterday so we GAINED 127 contracts or an additional 12,700 oz will stand for delivery in this very active month of August

Sept. lost 29 contracts to 3517 contracts.

October gained 59 contracts up to 40,146

We had 139 notice(s) filed today for 13,900 oz FOR THE AUGUST 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 139 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 133 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2022. contract month,

we take the total number of notices filed so far for the month (33,257) x 100 oz , to which we add the difference between the open interest for the front month of (AUGUST 498 CONTRACTS ) minus the number of notices served upon today 139 x 100 oz per contract equals 3,361,600 OZ OR 104.559 TONNES the number of TONNES standing in this active month of AUGUST.

thus the INITIAL standings for gold for the AUGUST contract month:

No of notices filed so far (33,257) x 100 oz+ (498) OI for the front month minus the number of notices served upon today (139} x 100 oz} which equals 3,3616 oz standing OR 104.569 TONNES in this active delivery month of August.

TOTAL COMEX GOLD STANDING: 104.569 TONNES (A HUGE STANDING FOR AUGUST ( ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 979 x 5,000 oz = 4,895,000 oz

to which we add the difference between the open interest for the front month of AUGUST(88) and the number of notices served upon today 34 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST./2022 contract month: 979 (notices served so far) x 5000 oz + OI for front month of AUGUST (88) – number of notices served upon today (34) x 5000 oz of silver standing for the AUGUST contract month equates 5,165,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

AUGUST 10//WITH GOLD UP $2.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES

AUGUST 9/WITH GOLD UP $6.70: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES.

AUGUST 8/WITH GOLD UP $13.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FORM THE GLD//INVENTORY RESTS AT 999.16 TONNES

AUGUST 5/WITH GOLD DOWN $14.25: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .33 TONNES FROM THE GLD////INVENTORY RESTS AT 1000.32 TONNES

AUGUST 4 WITH GOLD UP $29.00 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES FROM THE GLD///INVENTORY REST AT 1000.65 TONNES

AUGUST 2/WITH GOLD UP $3.70; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD//INVENTORY RESTS AT 1002.97 TONNES//

AUGUST 1/WITH GOLD UP $5.75: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 29//WITH GOLD UP $12.50; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1005.29 TONNES

JULY 28/WITH GOLD UP $31.25; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 27.//WITH GOLD UP $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 26/WITH GOLD DOWN $1.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.29 TONNES

JULY 25/WITH GOLD DOWN $7.85: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 1005.87 TONNES

JULY 22/WITH GOLD UP $17.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 21/WITH GOLD UP $11.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.101 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.87 TONNES

JULY 20/WITH GOLD DOWN $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1009.06 TONNES

JULY 19/WITH GOLD DOWN $.35 :BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22 TONNES FROM THE GLD//INVENTORY RESTS AT 1009.06 TONNES

GLD INVENTORY: 987.66 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVEWR INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTO THE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 10/WITH SILVER UP 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 9/WITH SILVER DOWN 25 CENTS TODAY: TWO CHANGES IN SILVER INVENTORY AT THE SLV: FIRST: A DEPOSIT OF 461,000 OZ INTO THE SLV AND THEN A WITHDRAWAL OF 1.014 MILLION OZ..//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 8/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 5/WITH SILVER DOWN 28 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 922,000 OZ FROM THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 4 WITH SILVER UP 21 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 527,000 OZ FROM THE SLV////INVENTORY RESTS AT 486.634 MILLION OZ

AUGUST 2/WITH SILVER DOWN 21 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.504 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.161 MILLION OZ//

AUGUST 1/WITH SILVER UP 17 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE GLD: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 483.657 MILLION OZ//

JULY 29/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 461,000 OZ FROM THE SLV..//INVENTORY RESTS AT 483.657 MILLION OZ/

JULY 28/WITH SILVER UP $1.24 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 484.118 MILLION OZ/

JULY 27/.WITH SILVER UP 4 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL 11.479 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 484.118MILLION OZ//

JULY 26/WITH SILVER UP 16 CENTS: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.504 MILLION OZ FROM THE SLV//: //INVENTORY RESTS AT 495.597 MILLION OZ//

JULY 25/WITH SILVER DOWN 24 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.383 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 499.101 MILLION OZ//

JULY 22/WITH SILVER DOWN 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 500.484 MILLION OZ//

JULY 21/WITH SILVER UP 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.19 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 500.484MILLION OZ/

JULY 20/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 8.253 MILLION OZ FORM THE SLV/INVENTORY RESTS AT 507.585 MILLION OZ//

JULY 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ//

CLOSING INVENTORY 479.490 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

LAWRIE WILLIAMS: China back on top for Swiss gold exports

After several months of low imports of Swiss gold with India very much the major recipient of the re-refined high ultra high purity product from that country’s gold refineries in July. China moved back comfortably as the major recipient of the Swiss product, taking no less than 80.8 tonnes – or fully 42.9% of the amount exported that month. Almost 45% if one includes Hong Kong in the Chinese figure. Turkey and Thailand’s gold imports from Switzerland in the month also exceeded those headed to India with 20.1 and 17.8 tonnes respectively, high numbers for both countries, while India absorbed 16.2 tonnes in fourth place- still a respectable import total. All in all, Switzerland exported 188.3 tonnes of gold that month, comfortably in excess of imports of 110.4 tonnes, and more than counterbalancing export deficits for the previous 3 months.

So why are gold exports from this small European nation with no gold production of its own so significant as to warrant this kind of comment. For historic reasons, the Swiss gold refineries, as readers of my columns will be aware, have always handled an important proportion of global gold and have been a key element in its global flow. They specialise in taking doré bullion from mines, gold scrap and very slightly lower tenor good delivery gold bars and re-refining all this to the wafer and kilobar sizes, gold coins and ultra high purities most in demand in the global marketplace, particularly to stronger hands in the Asian markets to which much of this re-refined gold is destined. Sometimes the volumes match, or even exceed, as in July, an equivalent of over half the global tonnage of new mined gold so it is an extremely valuable window on world gold flows, and one we have always followed closely. For July, for example, some 87% was destined for Asia and the Middle East assuming one includes Turkey in the latter.

The apparent resurrection of Chinese demand ties in well with other data we have been picking up too, notably the improving month-by-month gold withdrawal figures from the Shanghai Gold Exchange (See: Chinese gold demand picking up nicely despite lockdowns). China is the world’s largest gold consumer and the state of Chinese consumption has to be vital to overall world gold demand figures. While we doubt this will return this year back to its previous peak levels at least it seems to be on the right track.

23 Aug 2022

END

3.Chris Powell of GATA provides to us very important physical commentaries

A good commentary for us.

see below

4. OTHER GOLD/SILVER COMMENTARIES

-END-

A very important read.

5.OTHER COMMODITIES: EUROPE/CORN

European corn yields are now expected to plunge amid the worst drought in 500 years

(zerohedge)

European Corn Yields Expected To Plunge Amid Worst Drought In 500 Years

TUESDAY, AUG 23, 2022 – 06:55 AM

Besides the news of record high electricity prices, a troubling new crop failure report about Europe’s upcoming harvest was published Monday. The bloc’s Monitoring Agricultural Resources forecasted corn yields could drop by nearly a fifth due to a devastating drought, according to Bloomberg.

Before we dive into the crop report, Europe’s centuries-old ‘hunger stones’ were recently revealed in the Elbe River, which runs from the mountains of Czechia through Germany to the North Sea. The stones date back to a drought in 1616 and read: “Wenn du mich siehst, dann weine.” That translates to “if you see me, then weep.”

The warning on the stones appears correct because the new crop report forecasts corn yields will drop 16% below the five-year average. That compares with a July forecast of an 8% decline.

The plunge in corn output could result in further food inflation. It will boost feed costs for livestock herds, adding to even more woes for farmers who are plagued with elevated diesel and fertilizer prices.

“Water and heat stress periods partly coincided with the sensitive flowering stage and grain filling,” according to the crop monitoring report. “This resulted in irreversibly lost yield potential.”

In late August, about half of Europe is under a drought warning. Crops, power plants, industry, and fish populations have been devastated by the heat and lack of rainfall. The European Commission Joint Research Centre warned earlier this month the ongoing drought is the worst in 500 years as vast amounts of farmland turn to dust.

Heading into the fall, western and central Europe face a very high risk of dry conditions over the next three months that could result in water shortages.

Increasing crop failures because of drought will only exacerbate the food crisis due to Ukrainian disruptions. Supermarket prices for meat in the EU jumped 12% in July versus a year earlier. Milk, cheese, and eggs are also skyrocketing at record rates.

This leaves us with the idea that inflation in Europe will remain sticky, as explained by Germany’s central bank chief Joachim Nagel: “The issue of inflation will not go away in 2023.”

end

COMMODITIES IN GENERAL/COAL

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.8465

OFFSHORE YUAN: 6.8657

HANG SENG CLOSED DOWN 153.73 PTS OR 0.78%

2. Nikkei closed DOWN 341.75 OR 0.78%

3. Europe stocks CLOSED MOSTLY ALL RED

USA dollar INDEX DOWN TO 108.96/Euro FALLS TO 0.99248

3b Japan 10 YR bond yield: RISES TO. +.215/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 137.40/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.305%/Italian 10 Yr bond yield RISES to 3.63% /SPAIN 10 YR BOND YIELD RISES TO 2.49%…

3i Greek 10 year bond yield RISES TO 3.821//

3j Gold at $1737.40 silver at: 19.00 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 17/100 roubles/dollar; ROUBLE AT 59.70//

3m oil into the 91 dollar handle for WTI and 97 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 137.40DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 9668–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9595well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.015 DOWN 2 BASIS PTS

USA 30 YR BOND YIELD: 3.209 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,12

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Flat As Traders Freak Over Jackson Hawk

TUESDAY, AUG 23, 2022 – 08:04 AM

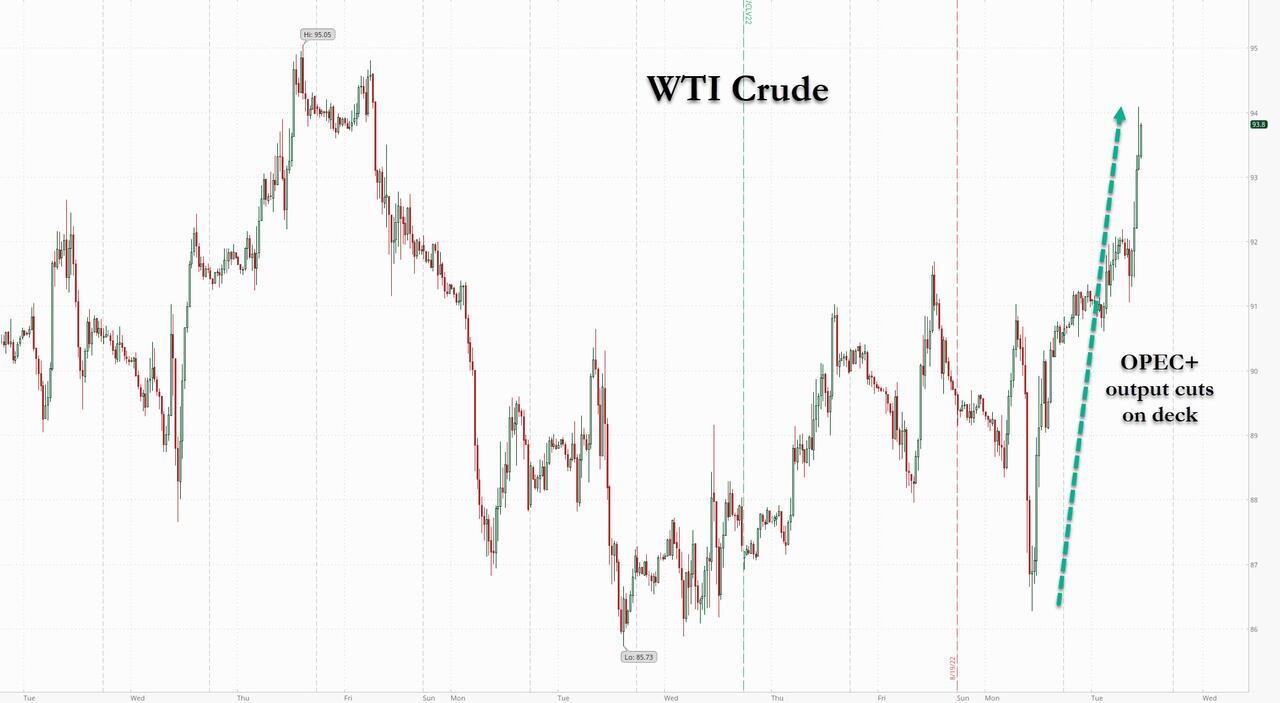

After Monday’s furious selloff which sent stocks tumbling the most in two months when the yield on 10-year Treasuries breached 3%, S&P futures have stabilized overnight, and after earlier dropping as low as 4,120 – or some 200 points below last week’s 200DMA resistance – have since rebounded to unchanged, if near the bottom of Monday’s range as nervous traders increasingly fear Powell will unleash a Hawk-ano during his Friday Jackson Hole speech. The 10-year Treasury yield held above 3% and the Bloomberg dollar index hovered at a five-week high as the EUR briefly dropped to 0.99, a fresh 20-year low, amid exponentially increasing energy costs. Oil futures climbed another 2% amid fears OPEC+ will cut output, as the market finally grasped what we were saying back in July 8 in “Inside The Oil Market’s Jekyll-And-Hyde Moment” after the Saudi Energy minister said that “The paper and physical markets have become increasingly more disconnected.”

In US premarket trading, Zoom Video Communications tumbled 9% after the communications software company cut its full-year forecast. Meanwhile, Palo Alto Networks rallied 8.7% after the security software company reported fiscal fourth- quarter results that beat expectations and gave a full-year forecast that is ahead of the analyst consensus. Here are some of the biggest US movers today:

Bed Bath & Beyond (BBBY US) shares rise as much as 6.6% in US premarket trading, set to end three days of losses, as a rout in retail-trader favorites eases, though worries over more challenging economic conditions remain

Dlocal (DLO US) shares fall as much as 9.5% in US premarket trading after the Uruguay payments firm reported second-quarter earnings that Morgan Stanley said were “good,” but not an “outright beat.”

Ocugen (OCGN US) shares rise as much as 6.8% in US premarket trading as Mizuho initiates the biopharma firm with a buy rating and $5 PT

Grocery Outlet (GO US) slips 4% after Morgan Stanley cut to underweight with the risk-reward on the grocery stores operator now looking negative

Kohl’s (KSS US) rose 2.1% in extended trading after a filing with the SEC showed Chairman Peter Boneparth bought $750,130 of shares

As discussed countless times before, the J-Hole symposium starting Friday with a keynote speech from J-Powell will be a key catalyst for equities, which have started pulling back again amid renewed fears of a more hawkish Fed. The Nasdaq has been under the most pressure after its valuation climbed above the 10-year average as higher rates weigh on the present value of future profits, hurting pricier growth stocks, like tech.

“For the moment, global sentiment is both skittish and volatile,” said Richard Hunter, head of markets at Interactive Investor. “There is little cause for optimism on the immediate horizon, with any glimmers of economic hope yet to take hold on a sustainable basis.”

“We expect equity markets to remain volatile as investor sentiment oscillates between hopes that the Fed will succeed in steering the US economy to a ‘soft landing,’ and fears that it will not,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. “Against this uncertain backdrop, we have recommended that investors retain a selective approach toward equities, and we believe this remains the right strategy.”

Meanwhile, looking at market technicals, Citi’s Chris Montagu said that the disjointed set of flows from both exchange-traded funds and futures last week paint a “muddled picture,” reflecting various assessments of whether the current rally has reached its near-term peak. The recent bullish sentiment appears weak and investors are uncertain with muted flows, they wrote in a note.

In Europe, the Stoxx 600 fluctuated near a three-week low after euro-area economic activity declined for a second month, signaling that fears of a recession may already be coming to pass as record inflation saps demand. While German PMIs came in a little stronger, a gauge of French private-sector activity dropped in August to its lowest level since the pandemic-related disruptions of early 2021, suggesting France is joining Germany in recession. It fell more than economists had expected, dipping below the threshold that separates expansion from contraction.

Energy stocks advanced thanks to a boost for crude oil from the possibility of OPEC+ output cuts. The euro hovered near a two-decade through, and only stronger than expected German PMI data prevented the EURUSD from sliding below 0.99; bond yields edged higher.

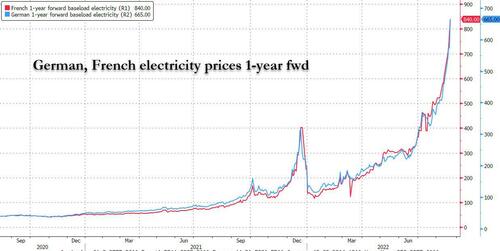

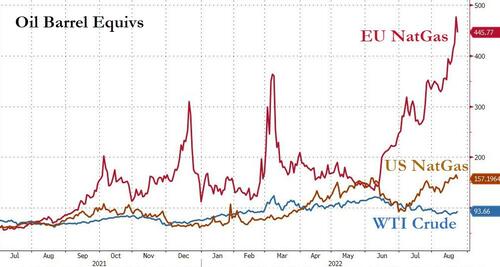

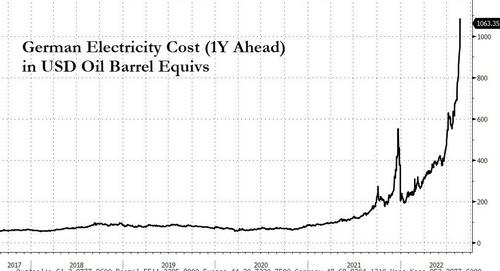

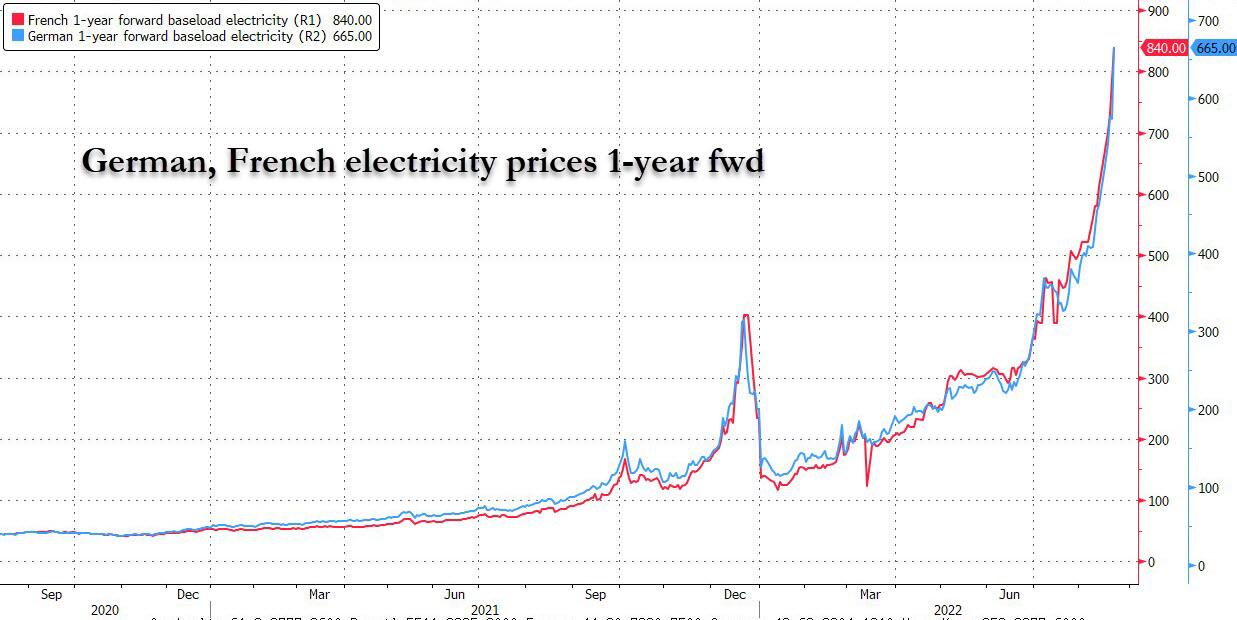

The looming European recession and the drop in the euro-area PMIs presents a dilemma for the ECB, which is raising interest rates to curb the hottest inflation in decades, even as uncertainty about the outlook is high and economic momentum fades. Meanwhile, the surge in European electricity prices continued and investors are finally waking up to the prospect that German stocks have further to fall due to the spiraling energy crisis according to Bloomberg. In the panic over Russian supplies, German power surged to above 700 euros a megawatt-hour for the first time and the Belgian prime minister said Europe could face up to 10 difficult winters.

European stocks tumbled, with the DAX a notable laggard, down over 2% Monday although it steadied on Tuesday. The DAX is now the worst-performing major Western European equity benchmark so far this month. Investors may be coming to realize that the energy crisis will put long-term strain on economies and companies, with the official start of the winter heating season just over a month away. Equities, especially in Germany, have not fully priced the energy stew. Cyclical German stocks are particularly at risk from this cocktail of soaring energy, inflation and recession risk, with chemicals, autos and industrials making up about 45% of the DAX, whose negative 30-day correlation with nat gas prices is the highest since April. That month German stocks fell 2.2%, more than the Stoxx 600. The correlation was most negative in late February/early March, when Russia invaded Ukraine. The DAX slumped 6.5% in February, also more than the Stoxx 600. European 2Q earnings were better than feared but there are signs conditions will get tougher from this cocktail of soaring energy, inflation and recession risk.

Here are some of the biggest European movers today:

On the Beach shares rose as much as 6.6% after CEO Simon Cooper notified the company he had increased his stake in the company with a purchase of ~1.53m shares at 129.54 pence per share

TAG Immobilien shares gained as much as 4.8% before paring gains after the German real estate company reported 2Q earnings following a capital increase in July

Zurich Airport shares rose as much as 3.9% and was among the top performers on the Stoxx 600 Industrial Goods and Services index as analysts praised 1H results that came in ahead of consensus expectations

BT shares rose as much as 1.7% after the telecom firm said the UK government decided to take no action on Altice UK’s stake in the company, after announcing in May that it would review it under the national security act

Virgin Money UK shares rose as much as 1% after Liberum increased the price target on the stock, saying the company is delivering on its accelerated digital strategy

Wood shares dropped as much as 12% before paring declines, with Jefferies saying the engineering services firm’s outlook “looks light”

Halfords shares slid as much as 11%, dropping to the lowest since July 2020, after Panmure Gordon cut the retailer of auto parts and bicycles to hold from buy and halved its price target to a Street-low

Grieg Seafood shares fell as much as 6%, to the lowest intraday since May 13, after the salmon and trout farmer cut its harvest guidance for the year

Dermapharm shares declined as much as 4.4% after the company posted 1H results that Jefferies called “solid but still not exciting”

Evotec shares fell as much as 3.8%, the worst performer in the Stoxx 600 Health Care index. RBC (outperform) cuts its PT on the German pharma firm, though says it still sees upside for the stock

Bakkafrost shares fell as much as 2.8%, hitting the lowest since June, with DNB saying the salmon farmer’s 2Q results were weaker than anticipated

Earlier in the session, Asian shares dropped as investors reduced bets on tech and other growth stocks amid receding expectations of slower monetary tightening by the Federal Reserve. The MSCI Asia Pacific Index fell as much as 1.2% to the lowest level in five weeks. TSMC, Sony and Samsung were among the biggest contributors to the drop. Benchmarks in most countries were in the red, with key measures in Japan, South Korea, Australia and the Philippine tumbling more than 1%. Expectations are building ahead of this week’s Jackson Hole central banker meeting that Federal Reserve Chair Jerome Powell will double down on the need to tame inflation. That’s helped cool the recent equity rally that was fueled by bets on slower interest rate hikes.

“It’s hard to profit more from here — the dollar is strengthening again on views that the rate hike pace won’t slow down,” said Heo Pil-Seok, chief executive officer at Midas International Asset Management in Seoul. “Risk-off sentiment is spreading again.” In addition to currency, traders were monitoring the impact of expected tighter Fed policy on bonds, with the 10-year Treasury yield holding above 3%. Corporate earnings are also in focus, with more than 340 members of the MSCI Asian benchmark reporting this week.

Japanese stocks tumbled amid deepening investor concerns over the Federal Reserve’s monetary policy plans as the Jackson Hole meeting draws near. The Topix fell 1.1% to close at 1,971.44, while the Nikkei declined 1.2% to 28,452.75. Sony Group Corp. contributed the most to the Topix decline, decreasing 3.3%. Out of 2,170 stocks in the index, 453 rose and 1,624 fell, while 93 were unchanged. “For the time being, we will have to wait and see what Powell has to say throughout the week, as Jackson Hole is still the most important factor to watch,” said Hideyuki Suzuki, general manager at SBI securities. “However, it’s also difficult to take a position since it’s the end of the month, and there should be more moves in the beginning of September with employment statistics and the major SQ.”

India’s benchmark equities index ended higher after fluctuating between gains and losses for much of the session, with heavyweight Reliance Industries among the winners. The S&P BSE Sensex rose 0.4% to 59,031.30 in Mumbai, after falling as much as 1% earlier in the session. The measure had lost 2.5% in previous two days. The NSE Nifty 50 Index climbed 0.5% on Tuesday. Traders are bracing for hawkish talks at the Federal Reserve’s Jackson Hole symposium later this week amid concerns that the central bank may not slow the pace of monetary tightening to tackle price pressures. “Markets may witness bouts of volatility in coming days as global factors will continue to keep investors on tenterhooks,” said Shrikant Chouhan, head of research at Kotak Securities Ltd. Reliance Industries advanced 1.5%, the most in over a week. Among the 30 stocks in the Sensex, 21 ended higher. All but two of 19 sectoral sub-indexes compiled by BSE Ltd. gained, led by a gauge of metal companies.

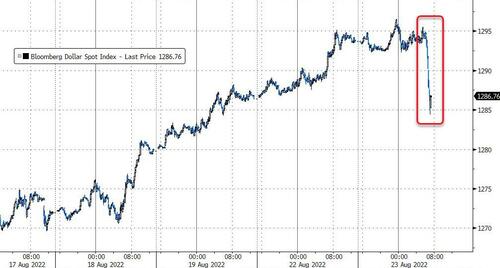

In FX, the Bloomberg Dollar Spot Index was little changed as the greenback traded mixed against its Group-of-10 peers. Risk- sensitive Scandinavian and Antipodean currencies advanced along with the yen. Two-year Treasury yields rose by 2bps, while 10- year yields were little changed. The euro briefly erased losses against the dollar and German benchmark 10-year bonds erased earlier gains, following stronger-than-forecast German manufacturing PMI data. The common currency was earlier on the verge of falling below the $0.99 handle. One-month implied volatility in euro-dollar is up for an eighth day, for the first time since April 2017. The pound fell against a broadly stronger dollar, slipping below $1.18 to approach its lowest since March 2020. China’s onshore and offshore yuan extend declined to their lowest level in two years as the currency continued to be weighed by the dollar’s strength. Additional policies to support the nation’s property sector did little to alleviate growth concerns.

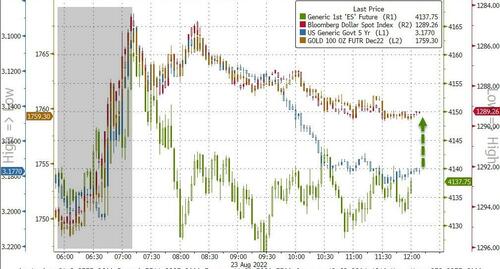

In rates, Treasuries extended flattening with long-end yields slightly richer on the day, front-end cheaper led by 2-year sector with yields ~2bp higher on the day ahead of $44BN auction at 1pm. 10-year are yields little changed around 3.015% with bunds and gilts in the sector cheaper by ~1bp and ~3bp; long-end outperforms, flattening 2s10s, 5s30s spreads by ~2bp each. Bunds, gilts underperformed following stronger-than-forecast German manufacturing PMI. US S&P Global PMIs are due later in the session. The yield on bunds 10-year is up about 1 bp to 1.31%; gilts curve flattens, with belly underperforming. Peripheral spreads widen to Germany with 10y BTP/Bund adding 2.1bps to 233.9bps. The Treasury auction cycle begins with $44b 2-year note sale at 1pm ET, followed by $45b five-year Wednesday and $37b seven-year Thursday.

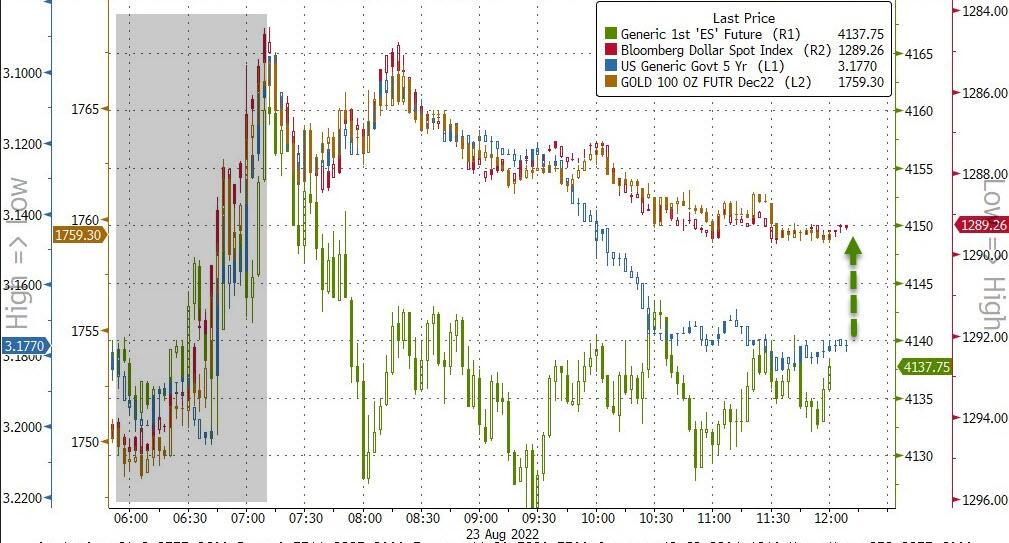

In commodities, WTI drifts 1.5% higher to trade below $92. Base metals are mixed; LME nickel falls 1.6% while LME aluminum gains 1%. Spot gold rises roughly $4 to trade near $1,740/oz

To the day ahead now, flash PMIs from around the world will be the main data highlight. Otherwise, there’s also the Euro Area’s preliminary consumer confidence reading for August, and in the US there’s new home sales for July and the Richmond Fed’s manufacturing index for August. From central banks, the ECB’s Panetta will speak, and earnings releases include Intuit and Medtronic.

Market Snapshot

S&P 500 futures up 0.3% to 4,153.00

MXAP down 0.9% to 158.27

MXAPJ down 0.7% to 515.06

Nikkei down 1.2% to 28,452.75

Topix down 1.1% to 1,971.44

Hang Seng Index down 0.8% to 19,503.25

Shanghai Composite little changed at 3,276.22

Sensex up 0.4% to 59,011.72

Australia S&P/ASX 200 down 1.2% to 6,961.81

Kospi down 1.1% to 2,435.34

STOXX Europe 600 little changed at 433.29

German 10Y yield little changed at 1.31%

Euro little changed at $0.9939

Gold spot up 0.3% to $1,741.69

U.S. Dollar Index down 0.11% to 108.92

Top Overnight News from Bloomberg

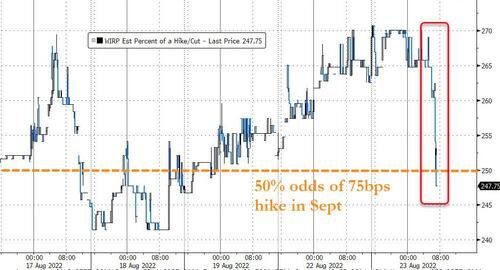

Hedge funds are unleashing record bets the Federal Reserve will stick to its hawkish script at Jackson Hole to rein in the fastest inflation in four decades. The group has collectively placed a big short across futures for a key overnight rate that moves in line with the Fed’s benchmark. The position, which has more than tripled in the past month, will benefit if Fed Chair Jerome Powell effectively rules out a dovish pivot when he speaks at this week’s symposium

The Global Inflation-Linked Bond Index has plunged 17% in 2022 — the worst-performing of the 20 key fixed-income benchmarks offered by Bloomberg. The reason has everything to do with the kind of bonds that make up the benchmark. Linker indexes are concentrated in longer-maturity debt that have absorbed the worst losses as central banks around the world lift interest rates.

The UK economy almost ground to a halt in August as falling demand and a shortage of labor and materials disrupted work of all kinds, a closely-watched survey showed. S&P Global said its index of private-sector growth fell to 50.9 this month. That’s the worst reading since the height of the UK lockdown in February 2021 and close to the level of 50 that separates expansion from contraction

Swedish home prices continued to fall last month as the surging cost of living threatens to upend what has been one of Europe’s hottest housing markets. The downturn has raised fears that what currently looks like a correction may accelerate into a crash with more wide- ranging implications. Prices had dropped the most since the financial crisis in June

China’s property market crisis is testing whether central bank Governor Yi Gang can stick to his stimulus-lite strategy. Over the past couple of weeks, Yi has cut key lending rates, announced special loans to struggling property developers via policy banks and urged state-owned lenders to extend more credit. Meantime, speculation of a cut to reserve requirement ratios grows

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly lower after the negative mood rolled over from global counterparts amid growth and energy-related concerns. ASX 200 was subdued as losses in financials and the consumer sectors overshadowed the gains in the mining and energy industries, while sentiment was also dampened after Flash PMI data weakened from the previous month in which Services and Composite PMIs slipped into contraction territory. Nikkei 225 declined as Japan suffered a similar fate on the data front which showed factory activity cooled to its slowest pace in 19 months. Hang Seng and Shanghai Comp weakened at the open amid a slew of earnings although the mainland gradually recovered as developers benefitted from China’s plans to offer CNY 200bln in special loans to troubled developers, while the PBoC also recently called on the major financial institutions to maintain stable growth of loans and pledged support for the platform industry and infrastructure construction.

Top Asian News

PBoC could reduce RRR this year to compensate for MLF maturities and further RRR cuts could lower lending prime rates, according to Security Times.

Japan’s government is preparing to increase the daily cap of arrivals to Japan to 50k from 20k, according to FNN. In relevant news, Japanese Chief Cabinet Secretary Matsuno said border controls will be lightened in a way to prevent COVID spread and aid economic activity, while he added that they cannot comment on the timing of new measures but will respond appropriately based on conditions at home and abroad.

Shimao Group (0813 HK) is proposing offshore creditors to repay USD 11.8bln over three-eight years as part of a restructuring plan, according to Reuters sources; proposes payment based on a two-tier structure.

European bourses have reversed initial pressure following EZ Flash PMIs, Euro Stoxx 50 +0.2%, which were mostly mixed though noted of less intense price pressures. FTSE 100 -0.3% lags following its respective measures which posted a surprise manufacturing drop into contractionary territory. Stateside, futures are firmer, ES +0.2%, and have been in-fitting with European peers throughout the morning awaiting their own Flash PMI metrics. “Twitter has major security problems that pose a threat to its own users’ personal information, to company shareholders, to national security, and to democracy”, according to CNN citing a whistle-blower.

Top European News

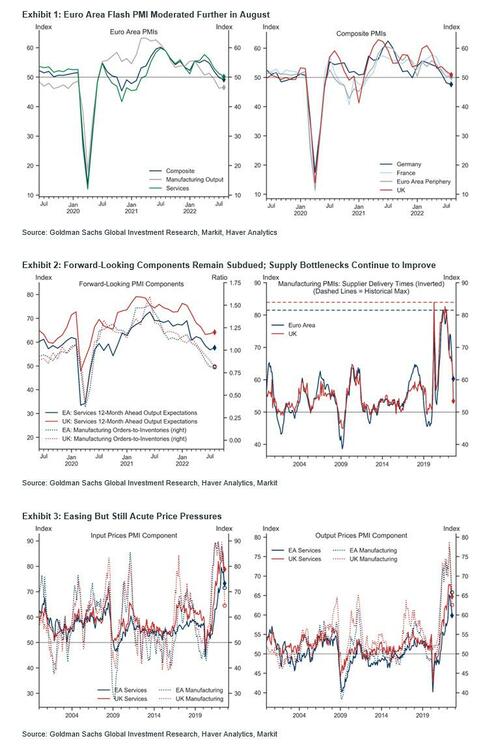

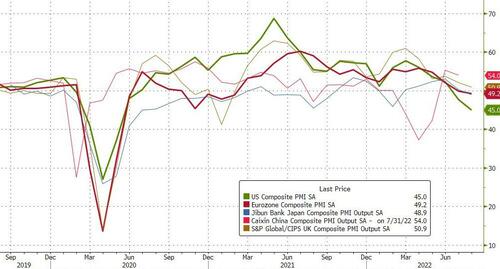

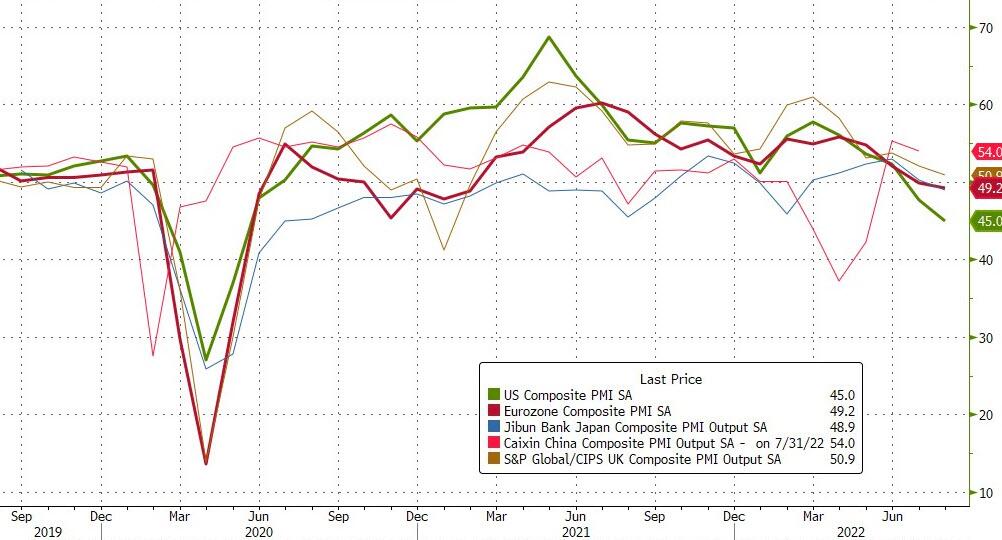

French S&P Global Composite Flash PMI (Aug) 49.8 vs. Exp. 50.8 (Prev. 51.7); Manufacturing Flash PMI (Aug) 49.0 vs. Exp. 49.0 (Prev. 49.5); Services Flash PMI (Aug) 51.0 vs. Exp. 53.0 (Prev. 53.2)

German S&P Global Composite Flash PMI (Aug) 47.6 vs. Exp. 47.4 (Prev. 48.1); Manufacturing Flash PMI (Aug) 49.8 vs. Exp. 48.2 (Prev. 49.3); Services Flash PMI (Aug) 48.2 vs. Exp. 49.0 (Prev. 49.7)

EU S&P Global Composite Flash PMI (Aug) 49.2 vs. Exp. 49.0 (Prev. 49.9); Manufacturing Flash PMI (Aug) 49.7 vs. Exp. 49.0 (Prev. 49.8); Services Flash PMI (Aug) 50.2 vs. Exp. 50.5 (Prev. 51.2)

UK Flash Composite PMI (Aug) 50.9 vs. Exp. 51.1 (Prev. 52.1); Services PMI (Aug) 52.5 vs. Exp. 52.0 (Prev. 52.6); Manufacturing PMI (Aug) 46.0 vs. Exp. 51.1 (Prev. 52.1)

FX

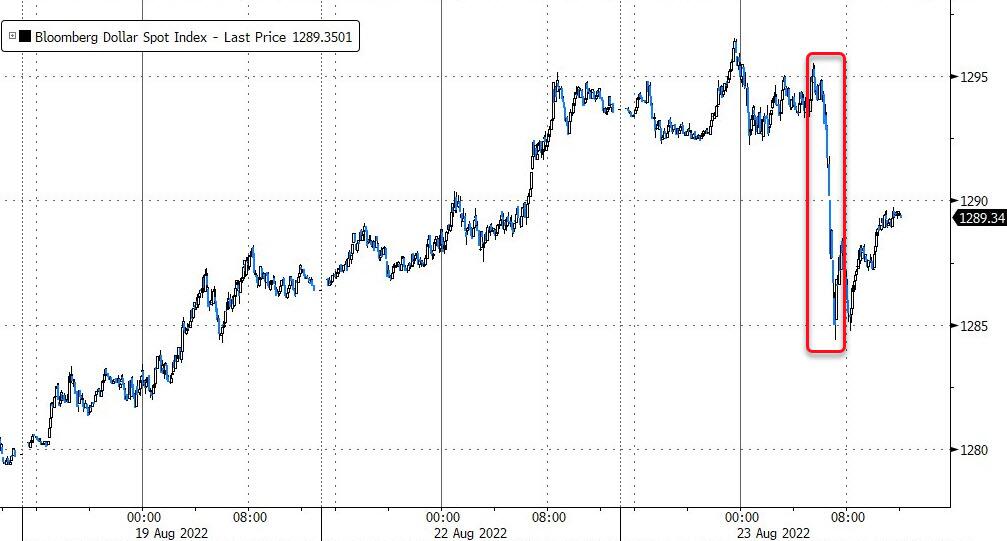

DXY reversed earlier gains after coming close to the YTD peak at 109.29 before pulling back.

EUR has been in focus; EUR/USD tested 0.9900 to the downside before rebound post-PMI.

The JPY has remained in the green vs the USD throughout the European session thus far as the earlier soured sentiment improved and the Dollar pulled back from near-YTD highs.

CAD and NZD lead the G10 gains whilst the EUR and CHF lag vs the USD.

Fixed Income

Pronounced two-way action on the French and German Flash PMI metrics, resulting in a ~200 tick range for Bunds thus far.

Initial upside was driven on the French release though this reversed in short-order and session lows then printed following the German figures.

Gilts were comparably contained on a surprise Manufacturing contraction, currently near the lower-end of 112.86-111.89 parameters.

USTs have been dictated by EGB action thus far but, now that the morning’s risk events have passed, have detached themselves somewhat and regained a positive foothold.

UK DMO says Gilt dealers suggested 2039 or 2073 I/L Gilts for November syndication, investors had mixed views on the November syndication some believe the current risk appetite for ultra-long I/L Gilt could be muted.

Commodities

WTI and Brent October contracts have been edging higher since the resumption of futures trading overnight.

Spot gold is choppy under USD 1,750/oz and moving in tandem with the Dollar.

Base metals are mixed but 3M LME copper maintains its head above USD 8,000/t.

Caspian Pipeline Consortium (CPC) says it will take a month to repair each mooring point in suitable weather, according to Interfax.

China’s Agricultural Ministry cautions that drought and high temperatures poses a “serious threat” to autumn crops; necessary to do everything possible to expand water source and relieve drought.

US Event Calendar

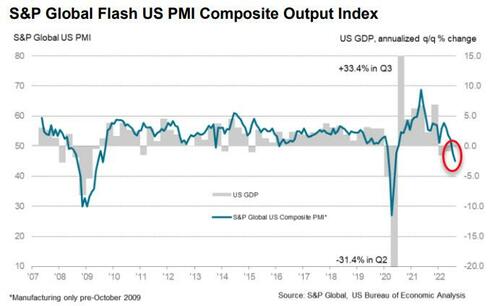

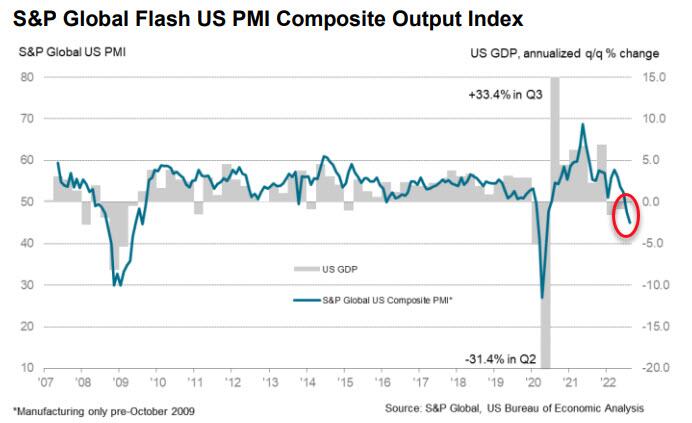

09:45: Aug. S&P Global US Manufacturing PM, est. 51.8, prior 52.2

09:45: Aug. S&P Global US Services PMI, est. 49.8, prior 47.3

09:45: Aug. S&P Global US Composite PMI, prior 47.7

10:00: Aug. Richmond Fed Index, est. -4, prior 0

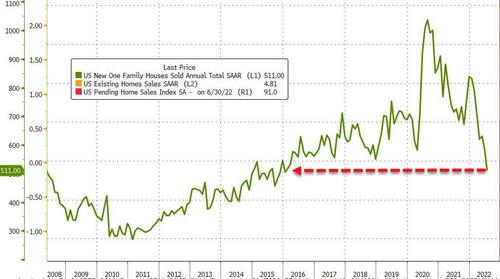

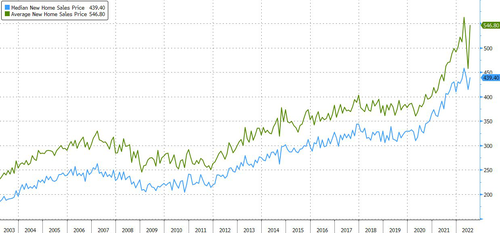

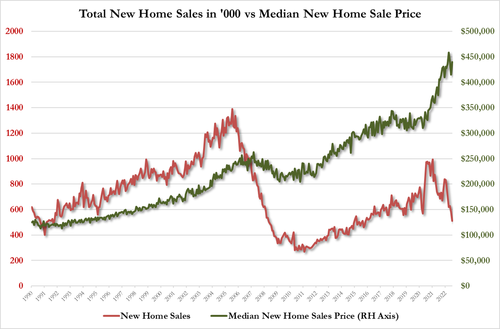

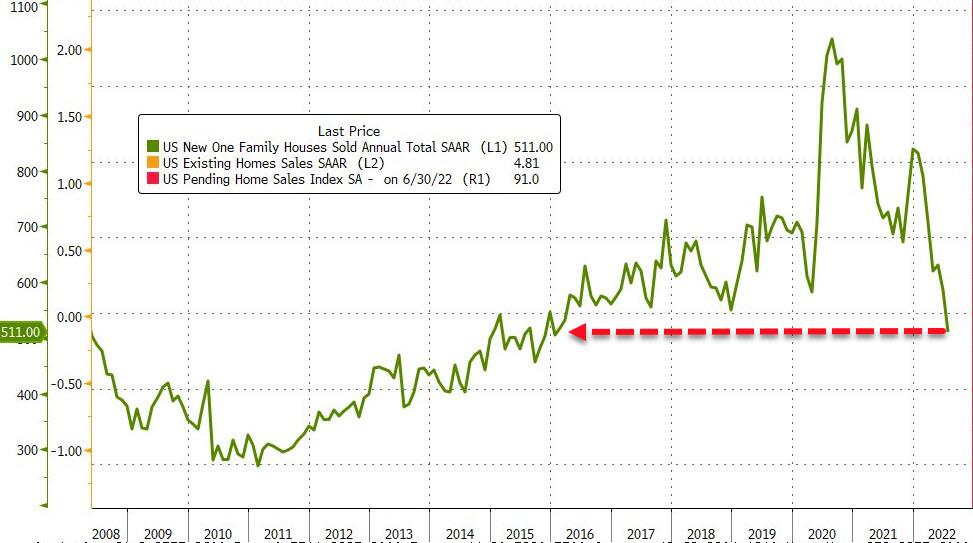

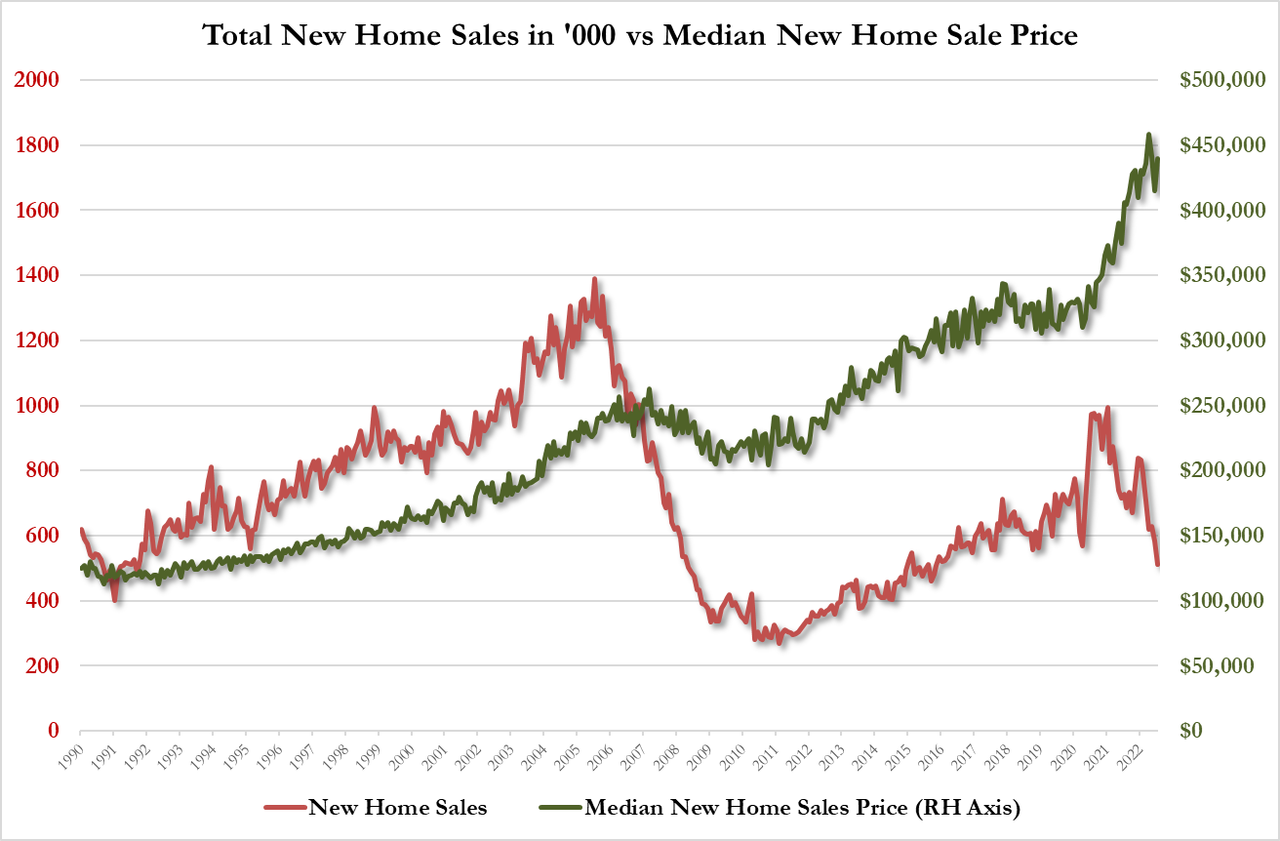

10:00: July New Home Sales MoM, est. -2.5%, prior -8.1%

10:00: July New Home Sales, est. 575,000, prior 590,000

DB’s Jim Reid concludes the overnight wrap

Yesterday was a sea of red for risk assets and sovereign bonds, as the energy crisis intensified in Europe, contributing to the specter of global central bank tightening already weighing on asset markets. Diving right in …

Starting in Europe, the energy crisis intensified yet further, after news over the weekend that Nord Stream would be shut for maintenance at the end of the month introduced fresh fears it would not re-open. European natural gas prices ratcheted +14.59% higher to €280/MWH, a record high. German power prices surged +18.60% to another record as well, closing at €663 and breaching €700/MWH intraday for the first time ever. The threat of climbing prices drove 10yr bund yields +7.6bps higher, led by a +5.9bp widening in 10yr breakevens to 2.54%, their widest levels since early May. 10yr OATs were +9.0bps higher, while BTPs increased +13.3bps, widening their spread to bunds to 230bps, the widest in nearly a month. In turn, the front end also climbed as additional ECB tightening was factored into market pricing, with the amount of tightening expected by March 2023 increasing +10.5bps.

Tighter policy and growing energy fears naturally weighed on risk sentiment, with the STOXX 600 falling -0.96%, while the DAX fared even worse, falling -2.32%. It was the worst daily performance in more than a month for both indices. The poor sentiment weighed on the euro as well, which, despite short-dated nominal (if not real) yield differentials keeping pace with Treasury markets (more below), broke parity again with the dollar, closing at $0.9943, the first close below parity in 20 years.

The story was much the same in the United States. 2yr Treasury yields increased +7.6bps while fed fund futures moved to price a terminal rate above 3.75% in the second quarter next year. 10yr yields were +4.3bps higher. Another day, another day flatter. More of the 10yr move came in real yields (+3.0bps), as sentiment is building toward a potentially hawkish rebuke of recent financial conditions easing from Chair Powell at Jackson Hole this week. Futures positioning is matching sentiment, where short positions in Eurodollar and SOFR futures (that is, positioning for higher short-term rates), has been building. That sentiment is already impacting rates markets, but it caught up with risk yesterday, as well, as the S&P 500 fell -2.14%, with the more rate sensitive NASDAQ underperforming, down -2.55%. It was the worst daily return for both indices since mid-June. . Yields on the 10yr USTs (-0.19 bps) are fairly stable as we go to print, trading at 3.01%.

Brent crude futures were as much as -4.52% lower intraday following cautious optimism around continued progress on the Iran negotiations and weaker broader risk sentiment. However, futures recovered to touch green before finishing -0.25% lower after the Saudi Arabian Energy Minister said the disconnect between volatile and illiquid markets and underlying fundamentals may force OPEC+ to cut production. The rally in oil helped drive medium-term breakevens wider; 5yr breakevens were around 2bps narrower before the remarks, and ended the day +2.4bps wider at 2.77%, their widest in almost a month. The next OPEC meeting is scheduled for September 5. Elsewhere, oil prices continue to gain momentum in early Asian session trading with Brent futures +0.81% higher at $97.26/bbl.

It was very light on the data front, but the Chicago National Activity Index for July printed at 0.27 versus expectations of a -0.25 print. The positive print of the comprehensive index indicated economic activity was still in expansionary territory despite recent growth jitters.

Asian equity markets are tracking sharp losses on Wall Street amid mounting rate hike concerns. The Nikkei (-1.24%) is leading losses across the region with the Kospi (-0.89%), the Hang Seng (-0.84%), the CSI (-0.61%) and the Shanghai Composite (-0.35%) all trading in the red. Elsewhere, the S&P/ASX 200 (-0.55%) is also sliding as Australia’s private sector activity contracted. Moving ahead, US equity futures are indicating a slight rebound with the contracts on the S&P 500 (+0.16%) and NASDAQ 100 (+0.20%) inching upwards.

Early morning data showed that the S&P Global Inc’s Flash Australia composite PMI fell to 49.8 in August from 51.1 in July while at the same time the services PMI Index dropped to a contractionary 49.6 from 50.9 indicating that the nation’s services sector is struggling. There was some encouraging data on the manufacturing activity with the headline index remaining in expansionary territory but eased slightly from 55.7 to 54.5.

Moving to Japan, factory activity decelerated to a 19-month low as the Jibun Bank manufacturing PMI dropped to 51.0 in August from 52.1 in July as output and new order declines deepened amid weakening global demand. Also, the nation’s services sector activity contracted for the first time in five months with the services PMI slipping to 49.2 in August from July’s final of 50.3 because of a lackluster demand at home.

To the day ahead now, and the flash PMIs from around the world will be the main data highlight. Otherwise, there’s also the Euro Area’s preliminary consumer confidence reading for August, and in the US there’s new home sales for July and the Richmond Fed’s manufacturing index for August. From central banks, the ECB’s Panetta will speak, and earnings releases include Intuit and Medtronic.

END

AND NOW NEWSQUAWK

Pronounced PMI-driven price action in EGBs, DXY tested 109.29 YTD peak before easing – Newsquawk US Market Open

TUESDAY, AUG 23, 2022 – 06:45 AM

European bourses have reversed initial pressure following EZ Flash PMIs, Euro Stoxx 50 +0.2%, which were mostly mixed though noted of less intense price pressures.

Stateside, futures are firmer, ES +0.2%, and have been in-fitting with European peers throughout the morning awaiting their own Flash PMI metrics.

DXY reversed earlier gains after coming close to the YTD peak at 109.29 before pulling back; EUR/USD tested 0.99 before rebounding.

Pronounced two-way action on the French and German Flash PMI metrics, resulting in a ~200 tick range for Bunds thus far.

Crude benchmarks have edged higher while metals are mixed/choppy amid USD price action.

Iran has reportedly dropped some key nuclear deal demands, though gaps remain, via Reuters citing a US official

Looking ahead, highlights include US Flash PMIs, EZ Consumer Confidence Flash, US New Home Sales, Fed Discount Rate Minutes, Supply from the US.

As of 11:15BST/06:15ET

For the full report and more content like this check out Newsquawk.

Try a 14 day trial with Newsquawk and hear breaking trading news as it happens.

LOOKING AHEAD

US Flash PMIs, EZ Consumer Confidence Flash, US New Home Sales, Fed Discount Rate Minutes, Supply from the US.

US reportedly has intelligence that Russia is preparing strikes on Ukraine’s infrastructure in the coming days, according to a US official cited by Reuters.

US President Biden’s administration warned Turkish businesses against working with sanctioned Russian institutions and individuals, according to WSJ.

Japanese Finance Minister Suzuki said he discussed with PM Kishida and other ministers the Ukraine situation, while they are to continue to coordinate with the G7 on sanctions against Russia and support for Ukraine. Suzuki said that Japan’s sanctions dealt a blow to Russia but added that there has been no discussion of new sanctions against Russia, according to Reuters.

Russian Defence Ministry says two Russian strategic bombers patrolled neutral waters over the Sea of Japan, via IFX. Additionally, Russian military aircraft enters Korea’s air defense zone without prior notice, according to the South Korean military cited by Yonhap.

IRAN

Iran has dropped some key demands with regards to the Iranian Nuclear Deal, but gaps remain and it is not clear there will be a deal, according to a US official cited by Reuters; will respond to proposal “soon”.

EU Foreign Policy Chief Borrell says most countries involved in nuclear talks with Iran agree on the EU proposal.

EUROPEAN TRADE

EQUITIES

European bourses have reversed initial pressure following EZ Flash PMIs, Euro Stoxx 50 +0.2%, which were mostly mixed though noted of less intense price pressures.

FTSE 100 -0.3% lags following its respective measures which posted a surprise manufacturing drop into contractionary territory.

Stateside, futures are firmer, ES +0.2%, and have been in-fitting with European peers throughout the morning awaiting their own Flash PMI metrics.

“Twitter has major security problems that pose a threat to its own users’ personal information, to company shareholders, to national security, and to democracy”, according to CNN citing a whistle-blower.

DXY reversed earlier gains after coming close to the YTD peak at 109.29 before pulling back.

EUR has been in focus; EUR/USD tested 0.9900 to the downside before rebound post-PMI.

The JPY has remained in the green vs the USD throughout the European session thus far as the earlier soured sentiment improved and the Dollar pulled back from near-YTD highs.

CAD and NZD lead the G10 gains whilst the EUR and CHF lag vs the USD.

Pronounced two-way action on the French and German Flash PMI metrics, resulting in a ~200 tick range for Bunds thus far.

Initial upside was driven on the French release though this reversed in short-order and session lows then printed following the German figures.

Gilts were comparably contained on a surprise Manufacturing contraction, currently near the lower-end of 112.86-111.89 parameters.

USTs have been dictated by EGB action thus far but, now that the morning’s risk events have passed, have detached themselves somewhat and regained a positive foothold.

UK DMO says Gilt dealers suggested 2039 or 2073 I/L Gilts for November syndication, investors had mixed views on the November syndication some believe the current risk appetite for ultra-long I/L Gilt could be muted.

WTI and Brent October contracts have been edging higher since the resumption of futures trading overnight.

Spot gold is choppy under USD 1,750/oz and moving in tandem with the Dollar.

Base metals are mixed but 3M LME copper maintains its head above USD 8,000/t.

Caspian Pipeline Consortium (CPC) says it will take a month to repair each mooring point in suitable weather, according to Interfax.

China’s Agricultural Ministry cautions that drought and high temperatures poses a “serious threat” to autumn crops; necessary to do everything possible to expand water source and relieve drought.

Bitcoin is modestly firmer and holding just above USD 21k despite a brief foray below the figure.

APAC TRADE

APAC stocks were mostly lower after the negative mood rolled over from global counterparts amid growth and energy-related concerns.

ASX 200 was subdued as losses in financials and the consumer sectors overshadowed the gains in the mining and energy industries, while sentiment was also dampened after Flash PMI data weakened from the previous month in which Services and Composite PMIs slipped into contraction territory.

Nikkei 225 declined as Japan suffered a similar fate on the data front which showed factory activity cooled to its slowest pace in 19 months.

Hang Seng and Shanghai Comp weakened at the open amid a slew of earnings although the mainland gradually recovered as developers benefitted from China’s plans to offer CNY 200bln in special loans to troubled developers, while the PBoC also recently called on the major financial institutions to maintain stable growth of loans and pledged support for the platform industry and infrastructure construction.

NOTABLE APAC HEADLINES

PBoC could reduce RRR this year to compensate for MLF maturities and further RRR cuts could lower lending prime rates, according to Security Times.

Japan’s government is preparing to increase the daily cap of arrivals to Japan to 50k from 20k, according to FNN. In relevant news, Japanese Chief Cabinet Secretary Matsuno said border controls will be lightened in a way to prevent COVID spread and aid economic activity, while he added that they cannot comment on the timing of new measures but will respond appropriately based on conditions at home and abroad.

Shimao Group (0813 HK) is proposing offshore creditors to repay USD 11.8bln over three-eight years as part of a restructuring plan, according to Reuters sources; proposes payment based on a two-tier structure.

Australian Composite PMI Flash (Aug) 49.8 (Prev. 51.1)

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED DOWN 1.57 PTS OR 0.05% //Hang Sang CLOSED DOWN 153.73 OR 0.78% /The Nikkei closed DOWN 341.75 OR % 1.19. //Australia’s all ordinaires CLOSED DOWN 1.21% /Chinese yuan (ONSHORE) closed DOWN AT 6.8463//OFFSHORE CHINESE YUAN DOWN 6.8657// /Oil UP TO 91.93 dollars per barrel for WTI and BRENT AT 97.78// / Stocks in Europe OPENED MOSTLY ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

3 a./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

end

3c CHINA

CHINA//

END

CHINA/POWER CRISIS

China extends further power cuts as the drought continues. This will hurt its Lithium production, its metals production, solar and risk

(zerohedge)

China Extends Power Cuts On Menacing Drought As Lithium, Metals, Solar, And Rice At Risk

MONDAY, AUG 22, 2022 – 09:20 PM

Sichuan’s worst drought in over half a century forced the Chinese province to extend power cuts for industrial plants. Power rationings are essential to ease electricity demand due to a menacing heatwave and limited rainfall that is driving down hydropower generation while cooling demand skyrockets — the combination is dangerous in terms of grid stability and is primarily why power cuts were prolonged.

Morgan Stanley analyst Simon Lee told clients Sunday that the provinces with 84 million people and a key manufacturing hub for semiconductor and solar panels faced “the hottest temperatures and the worst drought of the past 60 years.”

Sichuan heavily relies on hydropower generation for 82% of its power needs. About half of the renewable energy source has been slashed because rainfall along the Yangtze River since July has been 45% below average, the lowest since 1961. Falling hydropower generation comes as electricity demand in the province jumped 65 gigawatts, nearly a quarter higher than last year.

Goldman Sachs’ Trina Chen wrote power curtailments pose the most significant risk to rice supplies, followed by aluminum and battery materials.

Bloomberg outlines the largest impacts of the heatwave and power rationings on an industrial basis.

Lithium & Batteries

Sichuan produces more than a fifth of China’s lithium, according to BloombergNEF, making it one of the industries most exposed to the province’s power cuts. Top global battery producer Contemporary Amperex Technology Co., which has its second-biggest production base in Sichuan, has already halted production there.

Goldman said the power curbs could cost about 5% of China’s monthly output for lithium chemicals, but flagged a potentially bigger impact on lithium hydroxide and so-called “LFP” cathode used in batteries. But it also said EV-related sectors will probably get priority when industries are allowed to ramp up again.

The Sichuan disruptions add fuel to lithium’s blistering rally in the past year. The price of lithium carbonate reached its highest since April by the end of last week, and isn’t far from a new record.

Aluminum & Copper

Power-intensive aluminum smelters are often at high risk when governments want to cut electricity use. Goldman says some 360,00 tons of annualized aluminum capacity has been closed, with a further 300,000 tons at risk — adding up to about 1.5% of China’s capacity. While Sichuan is a notable aluminum producer, it lags far behind top provinces Shandong and Xinjiang. And neighboring Yunnan — a major source of new output — hasn’t been hit by weather disruptions.

Earlier in August, one of China’s biggest copper producers based in Anhui province cut output as local authorities ordered power curbs.

Solar Sector

About 15% of polysilicon used in solar panels comes from Sichuan, and prices for the material were already at a decade-high on strong demand for clean energy. The extension of the electricity curbs will reduce supply and likely offer more support to prices of both polysilicon and lithium, Daiwa Capital Markets wrote in a note.

Jinko Solar Co., one of the world’s largest solar module manufacturers, said two of its plants in Sichuan have been affected by the power shortage, and said it was unclear when the units could return to full capacity. At least two polysilicon plants — run by GCL Technology Holdings Co. and Tongwei Co. — face production interruptions, the China Silicon Industry Association said last week.

Rice

The six areas suffering drought — Sichuan, Chongqing, Hubei, Henan, Jiangxi and Anhui — accounted for almost half of China’s rice output in 2021, Goldman wrote in a note. China’s agriculture ministry said over the weekend that high temperatures and unusually low rains since July have posed “a severe challenge” to fall grain production.

The ministry has asked local authorities to strengthen capital and resources investment to combat the drought, and properly allocate drought-resistant equipment and seeds. In Henan province, more than 15 million mu (1 million hectares) of crops have been affected, according to a CCTV report.

Diesel

There’s also a demand boost for some sectors. Diesel purchasing is on the rise in Sichuan as industries seek alternative fuels. Local suppliers of diesel generators have already sold out after electricity rationing spurred some business owners to find alternative power supplies, industry consultant OilChem said in an online note. Some industrial users were loading diesel into barrels from retail stations, and demand has risen by up to 6%, it said.

The ongoing drought and power curtailments across a large swath of southern China compound economic woes for an economy already decelerating at an alarming pace, forcing the country’s central bank to cut its key interest rates last week.

Capital Economics believes more policy support is ahead, yet “it will probably be too late too little to prevent output from stagnating this year.”

end

4/EUROPEAN AFFAIRS//UK AFFAIRS/

EUROPE/ENERGY//PMI

The all important PMI which measures manufacturing and service sectors paints a grim picture for Europe’s finances

(zerohedge)

Euro Area Flash PMI Paints A Grim Picture

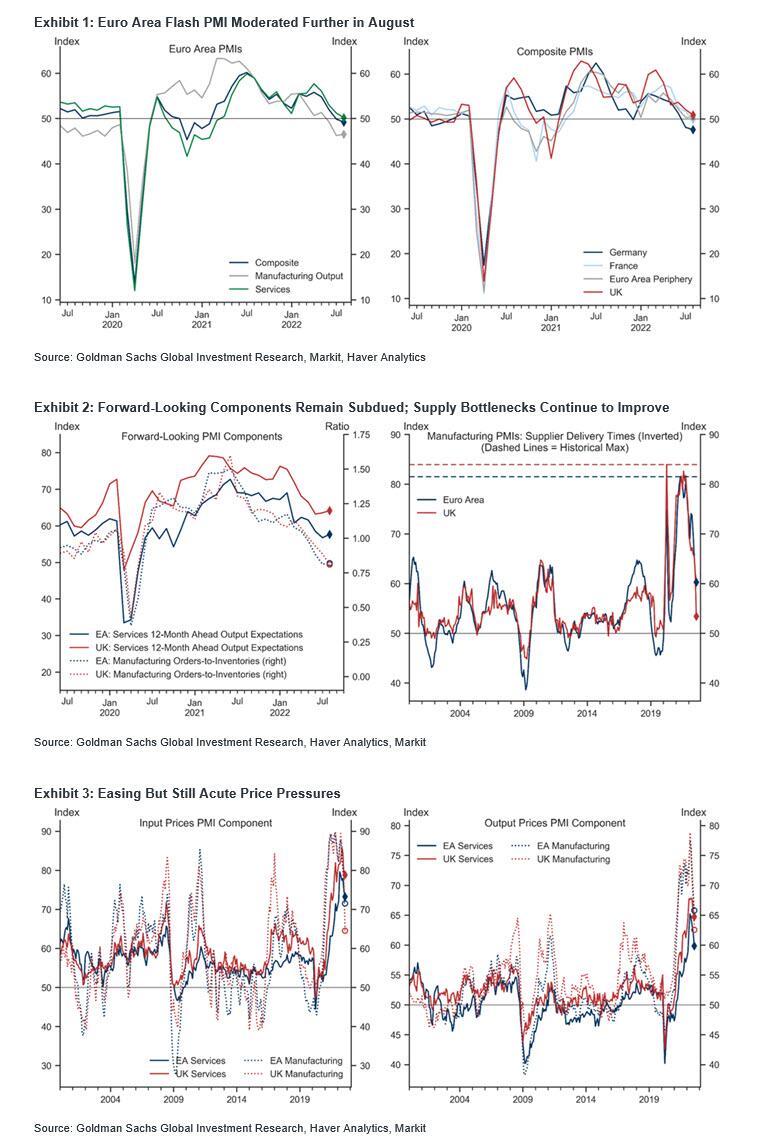

TUESDAY, AUG 23, 2022 – 08:53 AM

The Euro area composite flash PMI decreased by 0.7pt to 49.2 in August, slightly above consensus expectations but with material weakness among the components. Across sectors, the decline was driven by services, while across countries the weakening was led by France and, to a lesser extent, Germany, while the periphery composite index improved marginally. Expectations of future output edged up after having declined for three consecutive months but remain well below their historical average.

Commenting on the report, Bloomberg markets live reporter and commentator Nour al Ali writes that the flash PMIs point to uncertainty and struggling businesses across the euro area as services slow and manufacturing remains in downturn. European bond yields could rise further as a tough winter approaches while policymakers work to tame inflation regardless of the economic situation.

Key points to highlight from the reports for August include:

In the euro area, the overall reduction in business activity was mainly centred on the largest national economies such as Germany and France. Declining demand undermined business activity due to strong inflationary pressures. Economic weakness has become more broad based, with declining output seen in a range of sectors, from basic resources and autos to tourism and real estate.

In Germany, weaker export sales were once again a key driver of the downturn as a slowdown in services sector is compounding continued weakness in manufacturing, the report showed. Average prices charged for goods and services continued to rise sharply but the rate of inflation eased for the fourth month running in August. A further easing of supply bottlenecks was seen.

In France, flash data suggest the economy has now entered into contraction for the first time in a year and a half as a sharp manufacturing downturn more than offset only a marginal increase in service sector activity, according to the report.

The data adds to a growing chorus that says a recession is more likely than not in the euro area. The possibility of the ECB raising rates into a recession comes as the continent braces for a cold winter and an energy crisis that leaves much uncertainty up in the air.

Summarizing today’s PMI data, Goldman writes that “we continue to forecast below-consensus growth in H2 and look for a technical recession in coming quarters in the Euro area.”

end

end

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS/

END

6. GLOBAL ISSUES AND COVID COMMENTARIES

Fauci will leave his position in December. He knows that his time is up