Uncategorized · Leave a comment·Edit

Uncategorized · Leave a comment·Edit

GOLD; $1748.50 UP $0.50

SILVER: $19.03 DOWN 12 CENTS

ACCESS MARKET:

GOLD $1752.10

SILVER: $19.13

Bitcoin morning price: $21,425 DOWN 121

Bitcoin: afternoon price: $21,541. up 493

Platinum price closing DOWN $7.80 AT$877.30

Palladium price; closing UP $45/90 at $2035.20

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,746.800000000 USD

INTENT DATE: 08/23/2022 DELIVERY DATE: 08/25/2022

FIRM ORG FIRM NAME ISSUED STOPPED

365 H ED&F MAN CAPITA 1

661 C JP MORGAN 16

690 C ABN AMRO 11

905 C ADM 4

TOTAL: 16 16

MONTH TO DATE: 33,273

JPMorgan stopped: 16/16

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR AUGUST CONTRACT:

16 NOTICES FOR 1600 OZ //0.0497 TONNES

total notices so far: 33,273 contracts for 3,327,300 oz (103.493 tonnes)

SILVER NOTICES: 45 NOTICES FILED FOR 225,000 OZ/

total number of notices filed so far this month 1024 : for 5,120,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $0.50

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES TONNES FROM THE GLD.

INVENTORY RESTS AT 984.38 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $0.12

AT THE SLV// ://A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 475.066 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 102 CONTRACTS TO 144,357. AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE SMALL GAIN IN OI WAS ACCOMPLISHED WITH OUR $0.16 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.16) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD A STRONG GAIN OF 1500 CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE LIQUIDATION OF SPECULATOR SHORTS.

WE MUST HAVE HAD:

I) CONSIDERABLE SPECULATOR SHORT LIQUIDATIONS//CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A FAIR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 220,000 OZ QUEUE JUMP / // V) SMALL SIZED COMEX OI GAIN/(//CONSIDERABLE SPEC LIQUIDATION)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -84

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTACTS for 18 days, total 10,188 contracts: 50.940 million oz OR 2.830 MILLION OZ PER DAY. (566 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 50.940 MILLION OZ

.

LAST 16 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 50.940 MILLION OZ (A LOT LESS THAN NORMAL//THE CROOKS ARE SCARED TO ISSUE MORE EFP’S)

RESULT: WE HAD A SMALL SIZED INECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 104 WITH OUR $0.16 GAIN IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 1314 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /SOME BANKER ADDITIONS AND CONSIDERABLE SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 220,000 OZ QUEUE JUMP // .. WE HAD A STRONG SIZED GAIN OF 1500 OI CONTRACTS ON THE TWO EXCHANGES FOR 7.500 MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 45 NOTICE(S) FILED TODAY FOR 225,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 305 CONTRACTS TO 457,762 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:–199 CONTRACTS.

.

THE SMALL SIZED INCREASE IN COMEX OI CAME WITH OUR RISE IN PRICE OF $12.25//COMEX GOLD TRADING/TUESDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT SHORT COVERINGS ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND CONSIDERABLE SPECULATOR SHORT COVERINGS//CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 98.367 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 17,900 OZ //NEW STANDING 105.116 TONNES

YET ALL OF..THIS HAPPENED WITH OUR RISE IN PRICE OF $12.25 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 3853 OI CONTRACTS 11.96 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 3548 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 457,762

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3853 CONTRACTS WITH 305 CONTRACTS INCREASED AT THE COMEX AND 3548 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3853 CONTRACTS OR 11.98 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3548) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (305): TOTAL GAIN IN THE TWO EXCHANGES 3853 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR AUGUST. AT 99.272 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 17,900 oz. 3) ZERO/ LONG LIQUIDATION//// //.,4) SMALL SIZED COMEX OPEN INTEREST GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

49,329 CONTRACTS OR 4,932,900 OZ OR 153.43 TONNES 18 TRADING DAY(S) AND THUS AVERAGING: 2740 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAY(S) IN TONNES: 153.43 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 153.43/3550 x 100% TONNES 4.33% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 153.43 TONNES (DRAMATICALLY FALLING AGAIN)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT., FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A SMALL SIZED 102 CONTRACT OI TO 144,357 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1314 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 1314 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1314 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 102 CONTRACTS AND ADD TO THE 1314 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 1416 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 7.080 MILLION OZ

OCCURRED WITH OUR RISE IN PRICE OF $0.16

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 61.02 PTS OR 1.86% //Hang Sang CLOSED DOWN 234.51 OR 1.20% /The Nikkei closed DOWN 139.28 OR % 0.49. //Australia’s all ordinaries CLOSED UP 0.60% /Chinese yuan (ONSHORE) closed DOWN AT 6.8678//OFFSHORE CHINESE YUAN DOWN 6.8827// /Oil UP TO 94.81 dollars per barrel for WTI and BRENT AT 101.10// / Stocks in Europe OPENED MOSTLY ALL MIXED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 305 CONTRACTS TO 457,762 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR RISE OF $12.25 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (3548 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF AUGUST.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3548 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :3548 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3548 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED SIZED TOTAL OF 3853 CONTRACTS IN THAT3548 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 305 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR RISE IN PRICE OF GOLD $ 12.25. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING AUGUST (105.116),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:105.116 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $12.25) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A GOOD SIZED TOTAL GAIN ON OUR TWO EXCHANGES // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS////// WE HAVE REGISTERED A GOOD SIZED GAIN OF 12.603 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR AUGUST (105.116 TONNES)…

WE HAD -199 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE ADDED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3853 CONTRACTS OR 385,300 OZ OR 11.98 TONNES

Estimated gold volume 112,061/// extremely poor/

final gold volumes/yesterday 153,266/extremely poor

INITIAL STANDINGS FOR AUGUST ’22 COMEX GOLD //AUGUST 24

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 6998.556 oz JPMorgan Brinks Manfra contains 797 kilobars/loomis |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 99,079.347 oz HSBC Loomis |

| No of oz served (contracts) today | 16 notice(s) 1600 OZ 0.0497 TONNES |

| No of oz to be served (notices) | 522 contracts 52,200 oz 1.6236 TONNES |

| Total monthly oz gold served (contracts) so far this month | 33,273 notices 3,327,300 OZ 103.493 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 3

i)Into HSBC: 72,531.659 oz

ii) Into Loomis: 25,592.196 oz (796 kilobars)

iii) Into Brinks 955.492 oz

total deposits 99,079.347 oz

3 customer withdrawals:

i) Out of JPMorgan 5,594.234 oz

ii) Out of Brinks 448.790 oz

iii) Out of Manfra 955.492 oz

total: 6998.556 oz

total in tonnes:0.217 tonnes

Adjustments: dealer to customer //3

JPMorgan: 60,203.893 oz

Brinks 160,996.855 oz

iii) Delaware: 699.990 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 538 contracts having GAINED 40 contracts .

We had 139 notices served upon yesterday so we GAINED 179 contracts or an additional 17,900 oz will stand for delivery in this very active month of August

Sept. lost 459 contracts to 3058 contracts.

October gained 379 contracts up to 40,425

We had 16 notice(s) filed today for 1600 oz FOR THE AUGUST 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 16 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 16 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2022. contract month,

we take the total number of notices filed so far for the month (33,257) x 100 oz , to which we add the difference between the open interest for the front month of (AUGUST 538 CONTRACTS ) minus the number of notices served upon today 139 x 100 oz per contract equals 3,379,500 OZ OR 105.116 TONNES the number of TONNES standing in this active month of AUGUST.

thus the INITIAL standings for gold for the AUGUST contract month:

No of notices filed so far (33,257) x 100 oz+ (538) OI for the front month minus the number of notices served upon today (139} x 100 oz} which equals 3,379,500 oz standing OR 105.116 TONNES in this active delivery month of August.

TOTAL COMEX GOLD STANDING: 105.116 TONNES (A HUGE STANDING FOR AUGUST ( ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,320,942.458 oz 72.19 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 28,593,673.843 OZ

TOTAL REGISTERED GOLD: 14,154,032.797 OZ (440.24 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 14,439,641.046 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 11,833090. OZ (REG GOLD- PLEDGED GOLD) 368.05 tonnes//rapidly declining

END

SILVER/COMEX/AUGUST 24

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 602,029.850 oz CNT JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 661,873.002 oz Brinks Delaware |

| No of oz served today (contracts) | 45CONTRACT(S) 225,000 OZ) |

| No of oz to be served (notices) | 53 contracts (265,000 oz) |

| Total monthly oz silver served (contracts) | 1024 contracts 5,120,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i) Into Brinks 51,003.630 oz

ii) Into Delaware: 610,869.372 oz

total deposit: 661,873.002 oz

JPMorgan has a total silver weight: 171.371 million oz/331.952 million =51.61% of comex

Comex withdrawals: 2

i) Out of CNT: 20,227.050 oz

i) Out of JPMorgan: 581,802.800 oz

total: 602,029.850 oz

adjustments: 4

i) Brinks 336,549.470 oz

ii) HSBC 158,626.500 oz

iii) JPMorgan 603,890.310 oz

iv) Manfra 1,698,259.381 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 52.015 MILLION OZ

TOTAL REG + ELIG. 331.952 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR AUGUST

silver open interest data:

FRONT MONTH OF AUGUST OI: 98 CONTRACTS HAVING GAINED 10 CONTRACTS. WE HAD 34 NOTICES FILED ON MONDAY

SO WE GAINED 44 CONTRACTS OR AN ADDITIONAL 220,000 OZ OF SILVER WILL STAND FOR DELIVERY. THE AMOUNT STANDING

WILL NOW INCREASE//(OR REMAIN CONSTANT) ON A DAILY BASIS AS BANKERS SCOUR THE PLANET FOR BADLY NEEDED SILVER.

SEPTEMBER HAD A LOSS OF 6009 CONTRACTS DOWN TO 40,483

OCTOBER GAINED 97 CONTRACTS TO STAND AT 294

CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 45 for 225,000 oz

Comex volumes:64,342// est. volume today// fair

Comex volume: confirmed yesterday: 70,376 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 1024 x 5,000 oz = 5,120,000 oz

to which we add the difference between the open interest for the front month of AUGUST(98) and the number of notices served upon today 45 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST./2022 contract month: 1024 (notices served so far) x 5000 oz + OI for front month of AUGUST (98) – number of notices served upon today (45) x 5000 oz of silver standing for the AUGUST contract month equates 5,385,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

AUGUST 10//WITH GOLD UP $2.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES

AUGUST 9/WITH GOLD UP $6.70: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES.

AUGUST 8/WITH GOLD UP $13.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FORM THE GLD//INVENTORY RESTS AT 999.16 TONNES

AUGUST 5/WITH GOLD DOWN $14.25: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .33 TONNES FROM THE GLD////INVENTORY RESTS AT 1000.32 TONNES

AUGUST 4 WITH GOLD UP $29.00 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES FROM THE GLD///INVENTORY REST AT 1000.65 TONNES

AUGUST 2/WITH GOLD UP $3.70; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD//INVENTORY RESTS AT 1002.97 TONNES//

AUGUST 1/WITH GOLD UP $5.75: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 29//WITH GOLD UP $12.50; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1005.29 TONNES

JULY 28/WITH GOLD UP $31.25; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 27.//WITH GOLD UP $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 26/WITH GOLD DOWN $1.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.29 TONNES

JULY 25/WITH GOLD DOWN $7.85: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 1005.87 TONNES

JULY 22/WITH GOLD UP $17.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 21/WITH GOLD UP $11.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.101 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.87 TONNES

JULY 20/WITH GOLD DOWN $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1009.06 TONNES

JULY 19/WITH GOLD DOWN $.35 :BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22 TONNES FROM THE GLD//INVENTORY RESTS AT 1009.06 TONNES

GLD INVENTORY: 984.38 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTO THE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 10/WITH SILVER UP 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 9/WITH SILVER DOWN 25 CENTS TODAY: TWO CHANGES IN SILVER INVENTORY AT THE SLV: FIRST: A DEPOSIT OF 461,000 OZ INTO THE SLV AND THEN A WITHDRAWAL OF 1.014 MILLION OZ..//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 8/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 5/WITH SILVER DOWN 28 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 922,000 OZ FROM THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 4 WITH SILVER UP 21 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 527,000 OZ FROM THE SLV////INVENTORY RESTS AT 486.634 MILLION OZ

AUGUST 2/WITH SILVER DOWN 21 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.504 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.161 MILLION OZ//

AUGUST 1/WITH SILVER UP 17 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE GLD: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 483.657 MILLION OZ//

JULY 29/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 461,000 OZ FROM THE SLV..//INVENTORY RESTS AT 483.657 MILLION OZ/

JULY 28/WITH SILVER UP $1.24 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 484.118 MILLION OZ/

JULY 27/.WITH SILVER UP 4 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL 11.479 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 484.118MILLION OZ//

JULY 26/WITH SILVER UP 16 CENTS: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.504 MILLION OZ FROM THE SLV//: //INVENTORY RESTS AT 495.597 MILLION OZ//

JULY 25/WITH SILVER DOWN 24 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.383 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 499.101 MILLION OZ//

JULY 22/WITH SILVER DOWN 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 500.484 MILLION OZ//

JULY 21/WITH SILVER UP 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.19 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 500.484MILLION OZ/

JULY 20/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 8.253 MILLION OZ FORM THE SLV/INVENTORY RESTS AT 507.585 MILLION OZ//

JULY 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ//

CLOSING INVENTORY 475.066 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

The Numbers Don’t Lie; The Fed Won’t Win This Inflation Fight

WEDNESDAY, AUG 24, 2022 – 07:20 AM

Authored by Michael Maharrey via SchiffGold.com,

The central bankers at the Federal Reserve continue to talk tough about fighting inflation.

But is it a fight they can win?

The numbers say no.

After the CPI data cooled a bit in July, many observers expected the Fed to declare victory and begin pivoting away from tightening monetary policy. Instead, the central bankers doubled down on the tough talk. Minneapolis Federal Reserve Bank President Neel Kashkari said the Fed remains “far, far away from declaring victory” on inflation. He went on to say he hasn’t seen anything that changes the trajectory of the Fed’s inflation fight. Kaskari remained adamant that the central bank needs to raise rates to 3.9% by the end of the year and to 4.4% by the end of 2023. He even insisted he won’t be deterred by a recession.

The markets seem to have faith in the Fed’s ability to bring inflation down to 2% and keep it there for most of the next 30 years. Peter Schiff said they are “living in fantasy land.”

There is no way the Fed is going to even come close to achieving that for 30 years. They’re not even going to achieve it for three years. Yet, investors are still operating under the delusion that the Federal Reserve can do what it claims it’s going to do.

Peter is right.

For all the tough talk about stopping inflation, the Fed’s plan isn’t enough.

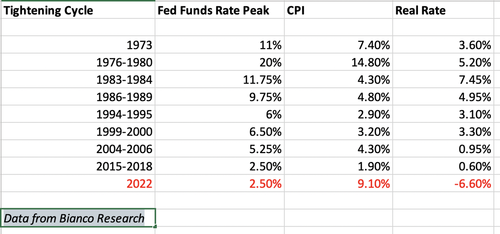

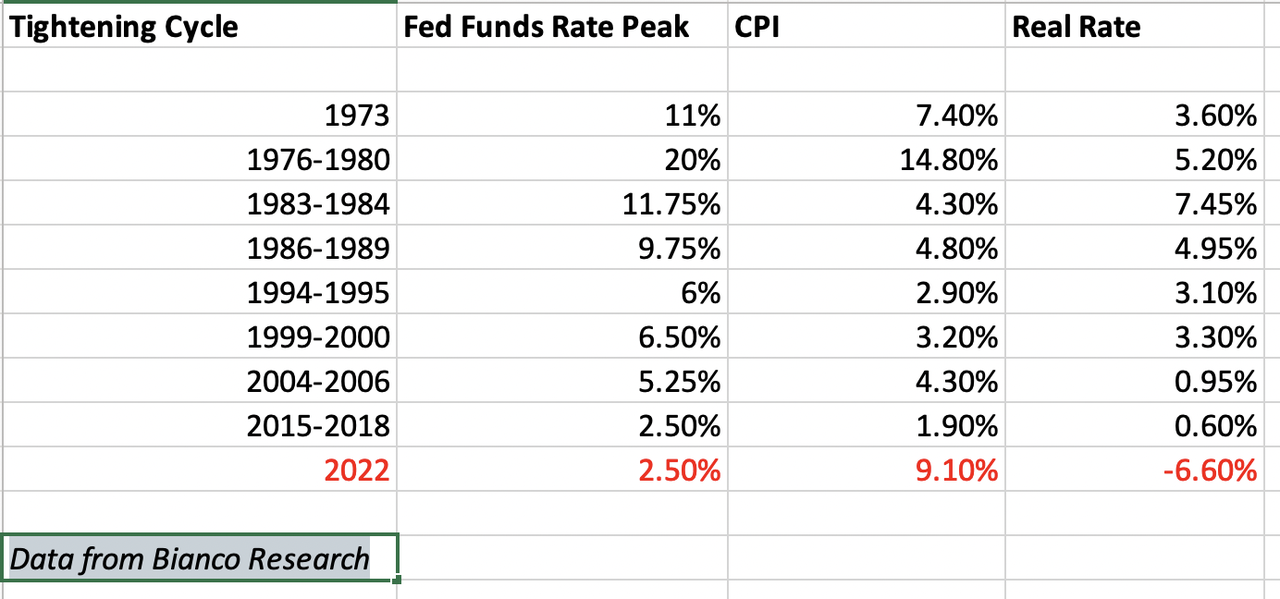

Pushing rates to 3 or 4 percent won’t tame 8.5% CPI.

If you look at all of the Fed tightening cycles since 1973, the central bank has never stopped tightening before the Fed funds rate was higher than the CPI.

It’s clear from the chart that the Fed has a lot of tightening to do before it brings the real rate positive. It’s also clear that 3 or 4 percent isn’t going to get the job done.

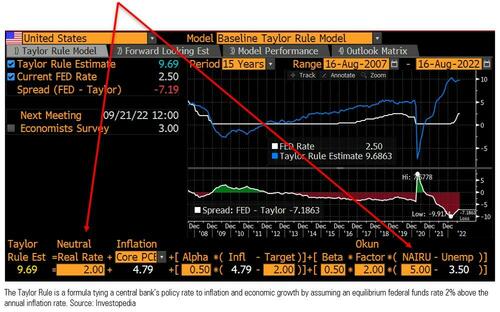

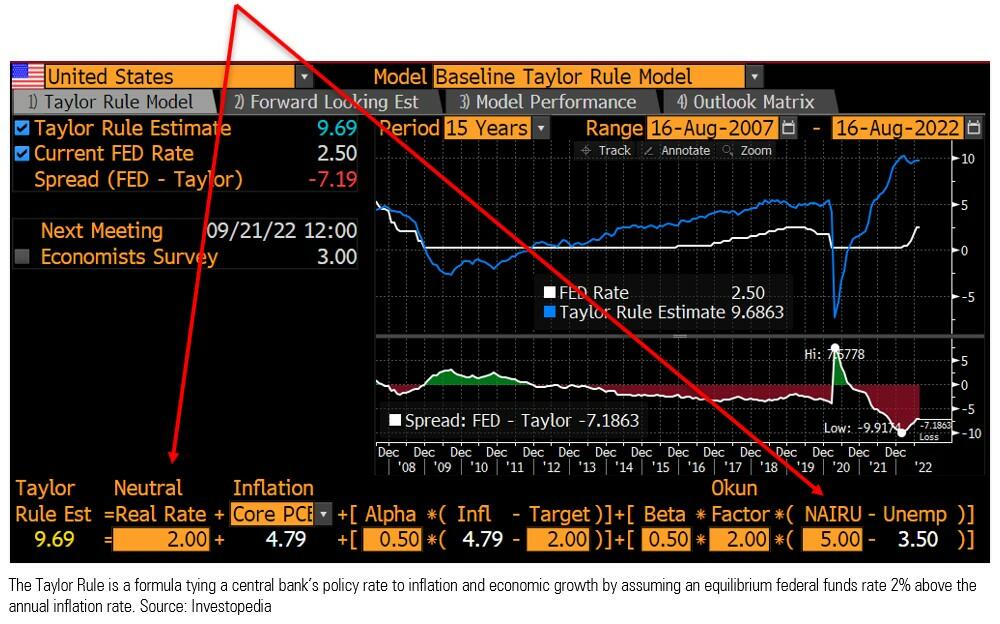

Analyzing interest rates based on the Taylor Rule leads us to the same conclusion.

Economist John Taylor came up with a formula that links the Federal Reserve’s benchmark interest rate to levels of inflation and economic growth. Based on the Taylor Rule, the Fed fund rate needs to be 9.69% assuming 2% real neutral rates.

Given the history and the model, it is difficult to fathom how exactly the Federal Reserve is going to tame inflation over the long term.

Keep in mind that the CPI is actually higher than the government numbers suggest. If we use the CPI formula from the 1970s, rates would need to be over 17% in order to slay inflation.

And while the 3 or 4 percent interest rate won’t stop the inflation freight train, it will pop the bubble economy that was built on easy money and debt. In fact, we’re already in a recession despite mainstream pleading to the contrary. This is why Peter Schiff says we are about to experience the worst of both worlds – high inflation and a recession.

I’m not going to give credit to the Federal Reserve for trying to put out a fire that it lit. And by the way, they’re not even putting enough water on it to put it out. The Fed should have raised interest rates a lot more than it already has. And it should be raising them a lot more. It’s gone much too slow. And not because the economy can handle it. It can’t. We’re already in a recession. They just want to ignore that. The recession is going to get worse if the Fed continues to raise interest rates. But it shouldn’t stop just because it’s going to put the economy into a depression or create a financial crisis. It has to do that. The only way to fight inflation is to remove all the inflation from the economy that the Fed put in there. So, they have to shrink their balance sheet. They have to let interest rates go way up. They have to force the government to slash government spending. But unfortunately, none of that is going to happen. This recession is going to get much worse, and Powell is going to pivot in defeat. He’s going to focus his attention on trying to stimulate the economy and let inflation run out of control.”

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

END

3.Chris Powell of GATA provides to us very important physical commentaries

this is interesting: a loan company in India is now planning to offer big loans using gold.

Good luck if they hope to get their gold back

(Business Today/India/GATA)

Loan company plans big business monetizing gold in India

Submitted by admin on Tue, 2022-08-23 21:56Section: Daily Dispatches

Capri Loans Plans to Open 1,500 Gold Loan Branches Over 5 Years

By Teena Jain Kaushal

Business Today, Noida, India

Tuesday, August 23, 2022

Capri Loans, a non-banking financial company forcused on micro, small, and medium-sized enterprise credit and housing finance, plans to open 1,500 gold loan branches over the next five years in Tier 3 and 4 cities to target the unorganised sector.

It aims to build a gold loan book size of R8,000 crore given the rise in credit needs among people.

The company commenced operations of its gold loan business on Tuesday with 108 branches. Capri Loans will provide loans up to 75% of the total pledged gold along with complimentary insurance equivalent to the pledged value of gold ornaments.

“During and post Covid, credit need has increased for multiple reasons,” said Ravish Gupta, head of gold loan business for Capri Global Capital.

“One of the reasons is that credit options have reduced. In India, huge amounts of gold are available in households — around 30,000 tonnes, according to a study. Instead of selling gold, people are unlocking the value by taking the loan.

“For those who have a limited source of credit and do not have proper documentation and need cash on an emergency basis, a gold loan is one of the best methods for unlocking the value.” …

… For the remainder of the report:

END

4. OTHER GOLD/SILVER COMMENTARIES

-END-

A very important read.

5.OTHER COMMODITIES: EUROPE/”

end

COMMODITIES IN GENERAL/COAL

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.8678

OFFSHORE YUAN: 6.8827

HANG SENG CLOSED DOWN 234.81 PTS OR 1.20%

2. Nikkei closed DOWN 139.28 OR 0.49%

3. Europe stocks CLOSED MOSTLY MIXED

USA dollar INDEX DOWN TO 108.86/Euro FALLS TO 0.9925

3b Japan 10 YR bond yield: RISES TO. +.220/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 136.83/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.359%/Italian 10 Yr bond yield RISES to 3.687% /SPAIN 10 YR BOND YIELD RISES TO 2.56%…

3i Greek 10 year bond yield RISES TO 3.933//

3j Gold at $1743.85 silver at: 19.02 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 4/100 roubles/dollar; ROUBLE AT 59.88//

3m oil into the 94 dollar handle for WTI and 101 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 136.83DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 9642– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9571well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.056 DOWN 0 BASIS PTS

USA 30 YR BOND YIELD: 3.265 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,16

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Flat After Hawkish Fed Comments, Dollar Ascent Resumes

WEDNESDAY, AUG 24, 2022 – 07:33 AM

The downbeat market mood continued for a fourth day, with US stock futures turning red and erasing earlier gains after a three-day drop saw the S&P 500 lose $1.4 trillion in market capitalization amid renewed concerns about a hawkish Fed and a potential J-Pow bomb during Friday’s J-Hole symposium (that said, with expectations so bearish, there is almost no way Powell can sound hawkish). S&P 500 futures dropped 0.1% at 7:00am ET after falling as much as 0.5%. Nasdaq 100 futures were also modestly red as the yield on the 10-year Treasury hit 3.05%. The US dollar reversed yesterday’s sharp drop and extended its recent surge as the EURUSD resumed its plunge trading ever farther from parity, and at 0.992 last. Oil meanwhile has continued its ascent, pushing Brent above $100, and leading to the first Diesel price increase at the Pump since mid-June.

“Globally we haven’t seen a deceleration like this that has been so synchronized in many decades,” Frances Stacy, director of strategy at Optimal Capital Advisors LLC, said on Bloomberg Television. “I don’t want to be directional” in picking trades, she added.

The latest data showed economic activity weakening from the US to Europe and Asia, underlining the dire dilemma the Fed faces in hiking interest rates to bring down high inflation without sparking a recession. Still, Minneapolis Fed President Neel Kashkari said inflation is very high and the central bank must act to bring it back down to 2% and it is “very clear” they need to tighten monetary policy. Kashkari also stated that half to two-thirds of US high inflation is driven by supply-side shocks and help is needed on the supply side to get inflation down, with the more help they get from the supply side, the less the Fed has to do and will be better able to avoid a hard landing. Furthermore, he said there is currently no trade-off between employment and inflation mandates and they can only relax on rate hikes when they see compelling evidence inflation is heading toward 2%.

In US pre-market trading, Nordstrom plunged as much as 14% and was set for its biggest drop in nine months, after an outlook cut prompted analyst worries that the need to clear inventory and discounting could hurt margins in the second half. Brokers said that the higher-end department store owner’s results have been more volatile than expected and show that the company is “not immune” to a difficult macroeconomic backdrop. Bed Bath & Beyond shares rose as much as 18% in premarket trading following a WSJ report that the home goods retailer told prospective lenders that it has selected a lender for a loan after a marketing by JPMorgan Chase. Other notable premarket movers:

- Urban Outfitters (URBN US) delivered quarterly results that look broadly in line with other apparel retailers, with a slowdown in lower-end brands and pressure on margins from markdowns, analysts say.

- Frontier GroupHoldings (ULCC US) is resumed with an overweight rating at Morgan Stanley, with broker saying that the company is “the quintessential ultra-low-cost carrier” and has attractive margins.

- Starbox (STBX US) shares jump as much as 30% in US premarket trading, with the Malaysian digital payments firm set for another day of gains after soaring in Tuesday’s Nasdaq Stock Market debut.

Stock futures were rangebound in muted volumes, as traders assessed the fact that directors at two of the Fed’s 12 regional branches favored a 100 basis-point increase in the discount rate in July. One of them, Minneapolis President Neel Kashkari, said US inflation is very high and the central bank must act to bring it back under control. All eyes remain on Fed officials as they head to Jackson Hole, Wyoming, this week for an annual conference, where Chair Jerome Powell will have a chance to reset investor expectations when he speaks on the economic outlook at 10am on Friday.

“We’ve been getting mixed signals from the Fed, highlighting risks of over-tightening but also concerns over still elevated inflation,” Madison Faller, global strategist at JPMorgan Private Bank, told Bloomberg Television. “It’s going to take more than one reading, we are going to have to see inflation fall over several months before we can really get a sense of whether a Fed pivot is on the way.”

According to an analysis of 13F reports by Goldman, last quarter hedge funds ramped up bets on megacap US tech stocks and whittled down overall holdings to concentrate on favored names, with conviction growing to levels last seen before the pandemic. The funds boosted tech and consumer discretionary holdings, while cutting energy and materials wagers, a trade which once again backfired spectacularly as tech crashed and energy soared. Since then however, the story has changed as Nasdaq 100 valuations rose well above the average for the past decade as the index soared from its June lows. The gauge remains under pressure, however, as higher rates weigh on the present value of future profits, hurting growth sectors like tech.

In Europe, the Stoxx 600 index edged lower, heading for a fourth straight day of declines, with retailers under pressure after US peer Nordstrom trimmed its full-year outlook. Luxury-goods giant Richemont surged after selling a stake in its online business. European natural gas prices increased, with outages at plants in the US and Norway adding to supply curbs from Russia. Here are some of the biggest European movers today:

- Richemont shares rise as much as 3.3% after the luxury retailer announced the sale of its YNAP stake to US online retailer Farfetch, which was up 9.4% in US premarket trading

- Tenaris gains as much as 3.3%, extending Tuesday’s 8.8% jump, with Banca Akros upgrading the company to buy from accumulate noting its outlook remains positive

- ASR Nederland shares jump as much as 4.1% after the insurer reported interim results. KBC says the company delivered solid results despite headwinds from Non-Life segment

- Lookers shares gain as much as 8%. The motor vehicle dealer’s pretax profit beat last year’s “exceptional performance” and was “comfortably ahead” of expectations, Peel Hunt (buy) says

- CTS Eventim shares gain as much as 4% after the ticket seller’s 2Q results, with Jefferies pointing to a significant beat driven by ticketing

- Norwegian fish farming stocks drop, led by Mowi, Leroy and Austevoll after the trio reported their respective quarterly results, with DNB expecting cuts to Mowi consensus estimates

- Vimian shares sink as much as 14% to a record low after the animal health company reported 2Q results that saw only slight organic growth and a lower Ebita margin

- Sydbank shares slide as much as 6.1% after the Danish lender’s latest results included a miss on net income, while saying its 2022 net profit will likely be in upper end of the previously reported range

- Agfa-Gevaert shares decline as much as 11%, the most intraday since May 2021, despite a 2Q revenue beat as ING questioned the quality of the earnings

Earlier in the session, Asian stocks headed for a fifth day of declines, weighed down by losses in China, with investors trimming risky bets as they await clarity on the Federal Reserve’s policy path at the Jackson Hole meeting. The MSCI Asia Pacific Index dropped as much as 0.7%, set for its longest losing streak in two months. The consumer discretionary sector was the biggest drag. China’s CSI 300 Index slumped 1.9%, the most among regional benchmarks, with electric-vehicle linked shares leading the declines after CATL reported weaker battery margins. Fed Minneapolis President Neel Kashkari said US inflation is very high and the central bank must act to bring it under control, in the latest run of hawkish remarks by US officials. That, coupled with weak US business activity data overnight, renewed concerns about global growth as central bankers gather for an annual symposium in Jackson Hole.

“We could see more short-term pressure on equities, starting in the US. This could also spill over to Asia given that corporate earnings in APAC are relatively sensitive to the region’s export performance,” said Tai Hui, APAC chief global market strategist at JP Morgan Asset Management. “We expect market sentiment to remain cautious as we approach the Jackson Hole meeting.” In addition to a flurry of earnings this week from the region’s heavyweights, investors are also closely watching the impact of a drought in China that has led to shutdown of factories.

Japanese equities ended lower, erasing earlier gains, as investors assess the potential for further tightening by the Federal Reserve to fight inflation. The Topix Index fell 0.2% to 1,967.18 as of market close Tokyo time, while the Nikkei declined 0.5% to 28,313.47. Sony Group Corp. contributed the most to the Topix Index decline, decreasing 1.4%. Out of 2,170 stocks in the index, 1,165 rose and 861 fell, while 144 were unchanged. “The key point to watch on the Jackson Hole is whether Powell will be hawkish, or a little less hawkish,” said Ayako Sera, a market strategist at Sumitomo Mitsui Trust Bank.

India’s benchmark equities index closed slightly higher, after seesawing between gains and losses several times throughout the day, helped by an advance in lenders. The S&P BSE Sensex rose 0.1% to close at 59,085.43 in Mumbai, after falling as much as 0.5% earlier in the session. The NSE Nifty 50 Index added 0.2%. ICICI Bank Ltd. provided the biggest boost to the Sensex, which saw 16 of the 30 member stocks ending higher. Fourteen of 19 sectoral sub-indexes compiled by BSE Ltd. rose, led by a gauge of realty companies. Investors will focus on Fed Chair Jerome Powell’s speech at the Jackson Hole symposium on Friday for a sense of how aggressive the US central bank will be in the face of weak economic trends. “Market strategists blamed the three-day losing streak in U.S. stocks on a number of factors, including nerves ahead of Federal Reserve Chairman Jerome Powell’s speech on Friday, combined with a drumbeat of downbeat economic news, along with anxieties about rising Treasury yields and a stronger U.S. dollar,” Deepak Jasani, head of retail research at HDFC Securities Ltd., wrote in a note.

In FX, the Bloomberg Dollar Spot Index was little changed and the greenback advanced against most of its Group-of-10 peers. Treasuries advanced, outperforming European peers, amid some paring of Fed rate hike bets. The euro traded in a narrow range around $0.950. Germany’s 10-year yield climbed to the highest since July 1 as money markets added to ECB rate-hike wagers before paring most of that rise. The pound slipped against the dollar and was steady versus the euro. Gilts underperformed with UK 2-, 5 and 30-year yields extending their advance to the highest since 2008, 2011 and 2014 respectively, before paring; the 10-year yield rose to the highest in two months.

In rates, Treasuries were mixed with 20-year sector outperforming, and broader market faring better than UK and euro-zone bond markets, where a full point of ECB hikes by October is priced in for the first time with energy seen adding to inflationary pressures. The 10Y TSY yield rose modestly to 3.05% after trading north of 3.00% all session. The New 2-year is ~1bp richer on the day with UK 2-year cheaper by ~15bp, German 2-year by ~6bp; 20-year Treasuries are richer by ~1bp outright and ~2bp on the 10s20s30s fly. The US Treasury auction cycle resumes with $45b 5-year at 1pm ET, concludes with $37b seven-year Thursday; Tuesday’s 2-year sale tailed by 1.4bp.

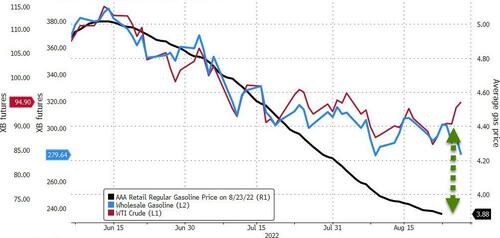

In commodities, WTI crude drifted above $94 a barrel, bolstered by shrinking US stockpiles and possible OPEC+ output cuts.

Bitcoin is incrementally softer but resides towards the mid-point of relatively contained parameters and remains comfortably above the USD 21k mark.

Looking at the day ahead now, and data releases from the US include the preliminary durable goods orders and core capital goods orders for July, along with pending home sales for that month too. Otherwise, earnings releases include Nvidia, Salesforce and Royal Bank of Canada.

Market Snapshot

- S&P 500 futures little changed at 4,133.25

- STOXX Europe 600 little changed at 431.26

- MXAP down 0.5% to 157.88

- MXAPJ down 0.6% to 512.64

- Nikkei down 0.5% to 28,313.47

- Topix down 0.2% to 1,967.18

- Hang Seng Index down 1.2% to 19,268.74

- Shanghai Composite down 1.9% to 3,215.20

- Sensex little changed at 58,991.22

- Australia S&P/ASX 200 up 0.5% to 6,998.12

- Kospi up 0.5% to 2,447.45

- German 10Y yield little changed at 1.32%

- Euro down 0.2% to $0.9949

- Gold spot up 0.1% to $1,750.10

- U.S. Dollar Index little changed at 108.65

Top Overnight News from Bloomberg

- Federal Reserve Bank of Minneapolis President Neel Kashkari said US inflation is very high and the central bank must act to bring it back under control

- The head of macro and FICC research at Sweden’s biggest lender, SEB AB, has urged the Riksbank to stop selling off its own currency because it risks hurting the economy

- The latest round of euro weakness has resulted in a series of bearish options structures for hedge funds and macro accounts. First stop for the common currency could be the $0.98 handle

- The world’s largest pension fund said its equity investments based on environmental, social and governance criteria have outperformed as global stocks slump on concerns over inflation and monetary tightening

- Oil rose for a second day as an industry report signaled another drawdown in US crude inventories, adding to a tightening supply outlook after Saudi Arabia flagged possible cuts to production

- The UK imported no fuel from Russia for the first time on record in June as the government achieved its ambition to phase out all purchases of natural gas and oil in the wake of the invasion of Ukraine

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks were mixed and only partially shrugged off the lacklustre lead from global counterparts. ASX 200 reclaimed the 7,000 level and was led by the tech and commodity-related sectors although gains were capped amid another busy day of earnings releases. Nikkei 225 failed to sustain opening advances following reports that Japan is considering lowering the COVID employment subsidy. Hang Seng and Shanghai Comp declined with property names pressured by several bearish factors including weak developer earnings and a default warning by Guangzhou R&F Properties, while China is also reportedly probing real estate executives for possible law violations.

Top Asian News

- China Securities Times noted that moderate CNY depreciation is positive for export competitiveness and that the widening US-China interest rate spread has a limited impact on CNY.

- Hong Kong is considering a storm level 8 from 18:00 local time 11:00BST/06:00EDT which could result in a market closure on Thursday, according to Bloomberg.

- Japanese PM Kishida announced to relax border rules on COVID and will waive tests for vaccinated passenger arrivals from September 7th, but added there was no decision yet on raising the number of daily arrivals, according to Reuters.

Cautious price action in European hours with fresh drivers limited and the docket sparse ahead of Jackson Hole commencing on Thursday (Powell Friday), Euro Stoxx 50 -0.1% Stateside, futures are in-fitting both directionally and in terms of magnitude, ES -0.1%. In Europe, the FTSE 100 is the marginal laggard with metals (ex-aluminium) under broad pressure as the USD gains momentum.

Top European News

- Scottish Power CEO proposed to UK Business Secretary Kwarteng capping household energy bills at around GBP 2000/year which would need funding of over GBP 100bln over two years, according to FT citing sources.

- ECB’s Rehn says the investigation phase for the digital EUR is expected to conclude in October 2023, will then determine whether to embark on actually building a digital EUR.

- Ukraine Latest: US to Mark Kyiv’s Independence With New Arms

- BNP Hires Zink Secher as Head of ESG Ratings Advisory for EMEA

- Cineworld Short Seller Argonaut Says Shareholders to Get Nothing

- Euro Traders Bet on Move Below $0.98 as Bold Wagers Also in Play

FX

- DXY attempted to claw back some of Tuesday’s losses overnight but lost momentum at a current session peak of 108.81.

- EUR is subdued as the bearish bias persists, GBP/USD is under similar mild pressure around (and marginally below) 1.1800.

- Non US-dollars are all softer against the USD whilst havens JPY and CHF outperform.

Fixed Income

- Initial pronounced EGB pressure briefly abated and brought benchmarks into positive territory; though, this failed to cement itself.

- Gilts are leading the downside though are circa. 20 ticks off worst levels, complex cognisant of the upcoming Ofgem announcement and inflation/rate implications.

- USTs are bucking the trend once more and are incrementally positive with 5yr issuance due and the curve incrementally steeper.

Commodities

- WTI and Brent October futures have been grinding higher since the European entrance following an APAC session of consolidation.

- Spot gold has been drifting higher after mounting the USD 1,750/oz mark.

- Base metals are mixed with 3M LME copper lower but still north of USD 8,000/t, whilst aluminium outperforms.

- US Private Inventory report (bbls): Crude -5.6mln (exp. -0.9mln), Cushing +0.7mln, Gasoline +0.3mln (exp. -1.5mln), Distillates +1.1mln (exp. +0.6mln).

- Canada and Germany signed a hydrogen alliance deal to accelerate exports of Canadian hydrogen to Germany by 2025, according to Reuters.

- Russia’s Sakhalin has scrapped a gas shipment to a buyer due to a payment issue, via Bloomberg.

- Major oil traders and some producers have ceased direct sales of crude to India’s Nayara energy amid concerns regarding Russian sanctions, according to Reuters sources.

- American Automobile Association says that US diesel pump prices have climbed for the first time since mid-June.

- Indonesia extends the palm oil export levy waiver until October 31st, according to the Trade Minister.

US Event Calendar

- 07:00: Aug. MBA Mortgage Applications, prior -2.3%

- 08:30: July Durable Goods Orders, est. 0.8%, prior 2.0%; Durables-Less Transportation, est. 0.2%, prior 0.4%

- July Cap Goods Orders Nondef Ex Air, est. 0.3%, prior 0.7%

- July Cap Goods Ship Nondef Ex Air, est. 0.5%, prior 0.7%

- 10:00: July Pending Home Sales (MoM), est. -2.6%, prior -8.6%; YoY, est. -21.4%, prior -19.8%

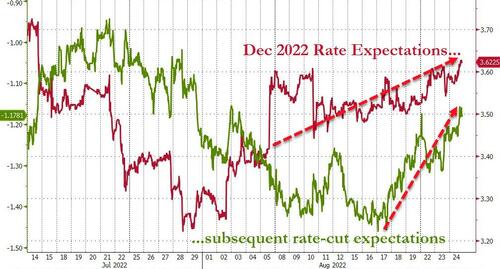

DB’s Tim Wessel concludes the overnight wrap

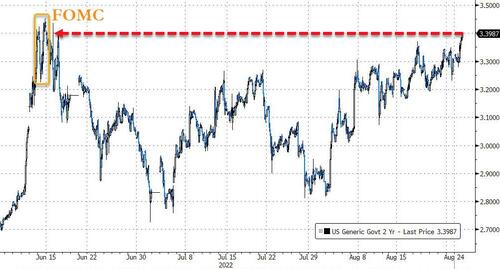

Despite the best efforts of data releases, US rates markets just do not want to fundamentally re-price the outlook until Chair Powell’s remarks this Friday at Jackson Hole (and, to an extent, the next round of employment and inflation data before the September FOMC). Our US economists have published a preview for his remarks (link here), with the one-line takeaway being they are looking for the Chair to fill in reaction function details. These being my last hours on the clock before the Chair’s remarks (as we here at EMR HQ navigate the summer holiday minefield that my inbox stuffed with automatic out-of-office replies suggest is ubiquitous across the financial sector) I can’t help but leave you, dear reader, with my final thoughts. The retracement of every rally following downside data surprises, along with the build up in short policy futures positions, suggests that the market is looking for a very hawkish tone from the Chair. That a priori expectations are for such hawkish messaging, the bar to clear for rates to selloff further is that much higher. It does not seem like the Chair can deliver the sort of shock necessary to drive a material re-pricing of policy, especially with inflation and employment data still due before the September FOMC, but time will tell. The case that a hawkish shock is to come is that the Chair most frequently has to speak publicly on behalf of the Committee, and this is his opportunity to slant his remarks towards his own personal bias. The Chair may well personally weigh the balance of risks toward worse inflation outcomes, but let’s see if his lean is strong enough to satiate the market’s appetite.

The latest example of rates markets retracing back to their starting point came yesterday, when PMIs, the Richmond Fed Manufacturing Index, and New Home Sales all missed to the downside in quick succession. In particular, the Services PMI (44.1 v 49.8 expected) fell to its lowest on record outside of the pandemic, with the survey showing weakness across new sales, new orders, and employment elements, along with abating price pressures. Nevertheless, respondents were optimistic about the path ahead, not making it any easier for market participants to disentangle signal from noise. Rounding out the other morning data, Manufacturing PMI fared better than Services, printing at 51.3 vs. 51.8 expected, still leaving the Composite at 45.0, its worst reading since February 2021. The Richmond Fed Manufacturing index was -8 vs. -2 expectations, while there were 511k new home sales in July vs. 575k expectations, another print on the downbeat for US housing markets.

Following the lackluster data, 2yr Treasury yields fell -11.8bps peak-to-trough, only, as intimated, to stage a retracement to end the day a mere -1.0bp lower. Similarly, 10yr Treasury yields were -9.3bps lower, peak-to-trough, but retraced with more vigor, nearly returning to intraday highs, ultimately closing +3.2bps higher at 3.05%. The S&P 500 followed a similar cadence, staging an initial bad-news-is-good-news rally following the data, increasing +0.53%, reverting to a narrow range just in the red the rest of the day, finishing down -0.22%. The NASDAQ danced to the same tune, but was even more reluctant to re-evaluate the outlook, closing perfectly flat, day-over-day. Futures are currently lower as we go to press, with the S&P 500 (-0.37%), NASDAQ 100 (-0.46%) and DAX (-0.65%) all in the red.

Most European assets were similarly subdued, with 10yr bunds (+1.2bps), OATs (+2.0bps), and BTPs (+1.8bps) trading near the prior day’s levels. The bund curve also twist steepened, with 2yr yields falling -3.8bps. Risk fared a touch worse; the STOXX 600 fell -0.42% and the DAX was -0.27% lower. Eurozone PMIs were a bit stronger than US counterparts, across Manufacturing (49.7 vs. 49.0), Services (50.2 vs. 50.5), and the Composite (49.2 vs. 49.0). Meanwhile, consumer confidence bounced back from record lows set in July, printing at -24.9 (vs. -28.0). Sentiment in Europe was boosted by a slight retrenchment in energy prices; German power fell -1.92%, the first daily decline in more than two weeks, while natural gas futures were -2.78% lower. The euro was able to temporarily break through parity versus the US dollar after the weak US data, but finished the day below the mark at $0.997.

Gilt yields increased more than other core sovereign bonds, with 2yr yields +9.8bps higher and 10yr benchmarks +6.1bps higher. UK Manufacturing PMI registered a poor 46.0 (vs. 51.0), though Services (52.5 vs. 51.6) and the Composite (50.9 vs. 51.0) fared better. However, the fear that UK inflation will continue to present a large problem is forcing gilts to underperform. On top of that, the threat of looming labour strife only intensifies the risks ahead. The FTSE 100 underperformed, falling -0.61%.

Following headlines from the Saudi energy minister yesterday, Brent crude oil rallied +3.39% closing above $100/bbl for the first time since late July. While progress on the Iranian nuclear deal still seemed positive, up to nine OPEC+ members confirmed they would support production cuts if Iranian supply came back online or if the global economy entered a recession, fueling the rally.

Overnight, Asian equity markets are again slipping into the red this morning amid growth fears. The Hang Seng (-1.49%) is leading losses with the Shanghai Composite (-1.38%), the CSI (-0.63%) and the Nikkei (-0.40%) all trading in negative territory. Elsewhere, the Kospi (+0.02%) is oscillating between gains and losses after opening higher.

Moving on to FX news, the Chinese Yuan (-0.42%) fell to its weakest level in almost two years against the US dollar, trading at 6.86 per dollar, as the PBOC looks to ease policy to support the economy while property sector troubles remain top of mind.

Minneapolis Fed President Kashkari in an overnight speech reiterated the need for more aggressive rate hikes to control inflation and sees another two full percentage points by the end of next year. Kashkari downplayed the two-sided risk of Fed tightening that has permeated recent discourse, noting that if inflation were at 4%, he would be willing to consider a more gradual path to avoid the risk of overdoing tightening. Alas, it is not.

To the day ahead now, and data releases from the US include the preliminary durable goods orders and core capital goods orders for July, along with pending home sales for that month too. Otherwise, earnings releases include Nvidia, Salesforce and Royal Bank of Canada.

END

AND NOW NEWSQUAWK

Cautious equity action with drivers limited, USD recoups & EGBs/USTs diverge – Newsquawk US Market Open

WEDNESDAY, AUG 24, 2022 – 06:38 AM

- Cautious price action in European hours with fresh drivers limited and the docket sparse ahead of Jackson Hole commencing on Thursday (Powell Friday), Euro Stoxx 50 -0.1%

- Stateside, futures are in-fitting both directionally and in terms of magnitude, ES -0.1%.

- DXY has recouped some of Tuesday’s pressure, but has failed to make much ground above 108.80; GBP lags while havens outperform

- Initial pronounced EGB pressure briefly abated and brought benchmarks into positive territory; though, this failed to cement itself

- Crude benchmarks continue to grind higher while spot gold is steady and base metals are mixed

- Looking ahead, highlights include US Durable Goods, Ukraine Independence Day, Supply from the US.

As of 11:10BST/06:10ET

For the full report and more content like this check out Newsquawk

Try a 14 day trial with Newsquawk and hear breaking trading news as it happens.

LOOKING AHEAD

- US Durable Goods, Ukraine Independence Day, Supply from the US.

- Click here for the Week Ahead preview.

GEOPOLITICS

RUSSIA-UKRAINE

- Zaporizhzhia regional administration head confirmed that Russian strikes hit the city of Zaporizhzhia in Ukraine, according to Twitter sources.

- US is to announce USD 3bln arms package to Ukraine, according to AP.

- Norway’s Defence Ministry said Norway and Britain joined forces to donate Black Hornet micro-drones to Ukraine, according to Reuters.

- Ukrainian President Zelensky says they will recapture the eastern region of Donbass and Crimea, whatever the path will be. On how the war is seen ending, says: “we used to say peace, now we say victory”

- Russian Defence Minister Shoigu says the “special operation” in Ukraine has slowed down to avoid civilian casualties, according to Tass.

- US Deputy Secretary of Treasury says has seen “no evidence” of Indian companies circumventing sanctions on Russia, according to Business Standard citing PTI.

OTHER

- US military said it conducted strikes in Syria targeting facilities used by groups affiliated with Iran’s IRGC, according to Reuters.

- US officials expect to respond to Iran’s comments on a European draft proposal by Wednesday and anticipate another round of negotiations in Vienna to finalize the details of a potential deal will likely be needed, according to Washington Post.

EUROPEAN TRADE

EQUITIES

- Cautious price action in European hours with fresh drivers limited and the docket sparse ahead of Jackson Hole commencing on Thursday (Powell Friday), Euro Stoxx 50 -0.1%

- Stateside, futures are in-fitting both directionally and in terms of magnitude, ES -0.1%.

- In Europe, the FTSE 100 is the marginal laggard with metals (ex-aluminium) under broad pressure as the USD gains momentum.

- Click here for more detail.

FX

- DXY attempted to claw back some of Tuesday’s losses overnight but lost momentum at a current session peak of 108.81.

- EUR is subdued as the bearish bias persists, GBP/USD is under similar mild pressure around (and marginally below) 1.1800.

- Non US-dollars are all softer against the USD whilst havens JPY and CHF outperform.

- Click herefor more detail.

Notable FX Expiries, NY Cut:

- Click here for more detail.

FIXED INCOME

- Initial pronounced EGB pressure briefly abated and brought benchmarks into positive territory; though, this failed to cement itself.

- Gilts are leading the downside though are circa. 20 ticks off worst levels, complex cognisant of the upcoming Ofgem announcement and inflation/rate implications.

- USTs are bucking the trend once more and are incrementally positive with 5yr issuance due and the curve incrementally steeper.

- Click here for more detail.

COMMODITIES

- WTI and Brent October futures have been grinding higher since the European entrance following an APAC session of consolidation.

- Spot gold has been drifting higher after mounting the USD 1,750/oz mark.

- Base metals are mixed with 3M LME copper lower but still north of USD 8,000/t, whilst aluminium outperforms.

- US Private Inventory report (bbls): Crude -5.6mln (exp. -0.9mln), Cushing +0.7mln, Gasoline +0.3mln (exp. -1.5mln), Distillates +1.1mln (exp. +0.6mln).

- Canada and Germany signed a hydrogen alliance deal to accelerate exports of Canadian hydrogen to Germany by 2025, according to Reuters.

- Russia’s Sakhalin has scrapped a gas shipment to a buyer due to a payment issue, via Bloomberg.

- Major oil traders and some producers have ceased direct sales of crude to India’s Nayara energy amid concerns regarding Russian sanctions, according to Reuters sources.

- American Automobile Association says that US diesel pump prices have climbed for the first time since mid-June.

- Indonesia extends the palm oil export levy waiver until October 31st, according to the Trade Minister.

- Click here for more detail.

NOTABLE HEADLINES

- Scottish Power CEO proposed to UK Business Secretary Kwarteng capping household energy bills at around GBP 2000/year which would need funding of over GBP 100bln over two years, according to FT citing sources.

- ECB’s Rehn says the investigation phase for the digital EUR is expected to conclude in October 2023, will then determine whether to embark on actually building a digital EUR.

NOTABLE US HEADLINES

- Fed’s Kashkari (2023 voter) said inflation is very high and it is the Fed’s job to curb it, while he added that they need to get the underlying inflation trend back down to 2% and it is very clear they need to tighten monetary policy. Kashkari also stated that half to two-thirds of US high inflation is driven by supply-side shocks and help is needed on the supply side to get inflation down, with the more help they get from the supply side, the less the Fed has to do and will be better able to avoid a hard landing. Furthermore, he said there is currently no trade-off between employment and inflation mandates and they can only relax on rate hikes when they see compelling evidence inflation is heading toward 2%.

- Click here for the US Early Morning Note.

CRYPTO

- Bitcoin is incrementally softer but resides towards the mid-point of relatively contained parameters and remains comfortably above the USD 21k mark.

APAC TRADE

- APAC stocks were mixed and only partially shrugged off the lacklustre lead from global counterparts.

- ASX 200 reclaimed the 7,000 level and was led by the tech and commodity-related sectors although gains were capped amid another busy day of earnings releases.

- Nikkei 225 failed to sustain opening advances following reports that Japan is considering lowering the COVID employment subsidy.

- Hang Seng and Shanghai Comp declined with property names pressured by several bearish factors including weak developer earnings and a default warning by Guangzhou R&F Properties, while China is also reportedly probing real estate executives for possible law violations.

NOTABLE APAC HEADLINES

- China Securities Times noted that moderate CNY depreciation is positive for export competitiveness and that the widening US-China interest rate spread has a limited impact on CNY.

- Hong Kong is considering a storm level 8 from 18:00 local time 11:00BST/06:00EDT which could result in a market closure on Thursday, according to Bloomberg.

- Japanese PM Kishida announced to relax border rules on COVID and will waive tests for vaccinated passenger arrivals from September 7th, but added there was no decision yet on raising the number of daily arrivals, according to Reuters.

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 61.02 PTS OR 1.86% //Hang Sang CLOSED DOWN 234.51 OR 1.20% /The Nikkei closed DOWN 139.28 OR % 0.49. //Australia’s all ordinaires CLOSED UP 0.60% /Chinese yuan (ONSHORE) closed DOWN AT 6.8678//OFFSHORE CHINESE YUAN DOWN 6.8827// /Oil UP TO 94.81 dollars per barrel for WTI and BRENT AT 101.10// / Stocks in Europe OPENED MOSTLY ALL MIXED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

3 a./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

A good article on the yen by Bruce Wilds. He questions whether the yen is about to resume its path lower. The Chinese economy plays a major part in the yen strength.

(Bruce Wilds)

Is The Yen About To Resume Its Path Lower?

TUESDAY, AUG 23, 2022 – 08:05 PM

Authored by Bruce Wilds via Advancing Time blog,

Much of the recent strength in the yen can be explained in one word and that is China. While I have seen no other currency watchers espouse this theory, I continue to contend the yen has become a major conduit by which wealth is being transferred out of China. This tight relationship can be seen each time trouble surfaces in China’s economy. When this happens the yen rises in value as wealth exits China through business back-channels.

Let’s be frank, most economic watchers think the Chinese economy is in big trouble, this makes it logical many people would want to get their wealth out of the country. This, however, is easier said than done. China has very strict rules related to taking money in and out of the country.

These rules regulate the actions of individuals attempting to move money out of China. We can assume, that most people moving large amounts of money would rather go under the radar and avoid running into problems with the Chinese government.

A few other factors feed into the recent bounce in the yen but do not be surprised if this recent strength rapidly fades.

One factor playing into the bounce is the decline in the yen’s value over the last several months may have been a bit overdone. Another could be related to the fact energy prices have come down reducing the cost of imports needed to fuel the economy. Still, we are again beginning to see the yen slip down towards its lows and should be repaired to see it again slip into new low territory.

Japan’s basic problems still remain.

As stated in an earlier post, higher interest rates are toxic to the highly indebted nation. Also, unfavorable demographics will continue to haunt the small island nation. Simply put, the fundamentals for Japan are lousy. Much of the risk of who gets hurt in the case of a falling yen or a default has shifted from the private sector to the Japanese public since the BOJ has continued splurging on JGBs.

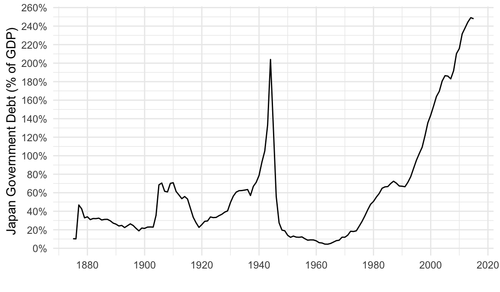

The Japanese Government Is Heavily In Debt

As Japan continues down this path it is only a matter of time before the credibility of the BOJ is lost and the yen plunges. To support their stock market the BOJ has even gone to buying stock. When investors in Japan’s government bonds begin to believe that inflation is about to return it would be logical for owners of Japanese debt to rush out of the low-yielding securities and buy foreign bonds or equities.

Unlike many other leading economies, Japan has been battling deflation or falling prices for the best part of the past two decades. We may have reached the point where reality has now taken hold. This has been a long time coming. When Japan crumbles it will be felt across the world and add to doubts about the whole fiat currency system.

END

In Stunning Post-Fukushima Shift, Japan Revisits Nuclear Power As Global Energy Turmoil Worsens

WEDNESDAY, AUG 24, 2022 – 09:05 AM