by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1709.60 DOWN $6.10

SILVER: $18.50 UP 16 CENTS

ACCESS MARKET:

GOLD $1708.50

SILVER: $18.53

Bitcoin morning price: $19,298 UP 169

Bitcoin: afternoon price: $19,198 UP 69

Platinum price closing UP $14.45 AT $882.65

Palladium price; closing UP $96.45 at $2143.20

END

DONATE

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,715.300000000 USD

INTENT DATE: 09/07/2022 DELIVERY DATE: 09/09/2022

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 35

435 H SCOTIA CAPITAL 39

657 C MORGAN STANLEY 5

661 C JP MORGAN 249

690 C ABN AMRO 9

709 C BARCLAYS 360

737 C ADVANTAGE 8 21

800 C MAREX SPEC 2 5

905 C ADM 7

TOTAL: 370 370

MONTH TO DATE: 2,464

JPMorgan stopped: 249/370

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR SEPT CONTRACT:

159 NOTICES FOR 27,000 OZ //0.8398 TONNES

total notices so far: 2464 contracts for 246,400 oz (7,6680 tonnes)

SILVER NOTICES: 39 NOTICES FILED FOR 195,000 OZ/

total number of notices filed so far this month 5987 : for 29,935,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $6.10

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: NO CHANGESIN GOLD INVENTORY AT THE GLD////

INVENTORY RESTS AT 971.05 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $.16

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 467.419 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GOOD SIZED 609 CONTRACTS TO 137,691. AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE LOSS IN OI WAS ACCOMPLISHED DESPITE OUR $0.34 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.34) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD A SMALL GAIN OF 161 CONTRACTS ON OUR TWO EXCHANGES,; WE HAD HUGE SPECULATOR LIQUIDATION.

WE MUST HAVE HAD:

I) HUGE/ SPECULATOR SHORT LIQUIDATIONS ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 170,000 OZ QUEUE JUMP / // V) GOOD SIZED COMEX OI LOSS/(//CONSIDERABLE SPEC LIQUIDATION/)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: –20

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTACTS for 5 days, total 5491 contracts: 27.455 million oz OR 5.491 MILLION OZ PER DAY. (1098 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 27,455 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 27.455 MILLION OZ///

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 609 DESPITE OUR $0.34 GAIN IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 740 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /SOME BANKER ADDITIONS A// HUGE SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 170,000 OZ QUEUE JUMP // .. WE HAD A SMALL SIZED GAIN OF 131 OI CONTRACTS ON THE TWO EXCHANGES FOR 0.655 MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 39 NOTICE(S) FILED TODAY FOR 195,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1639 CONTRACTS TO 464,269 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:–49 CONTRACTS.

.

THE FAIR SIZED DECREASE IN COMEX OI CAME DESPITE OUR STRONG RISE IN PRICE OF $13.70//COMEX GOLD TRADING/WEDNESDAY / WE MUST HAVE HAD HUGE SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND /STRONG SPECULATOR SHORT COVERINGS//CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 8.401 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG JUMP OF 26,100 OZ //NEW STANDING 12.3390 TONNES

YET ALL OF..THIS HAPPENED WITH OUR STRONG RISE IN PRICE OF $13.70 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A SMALL SIZED GAIN OF 186 OI CONTRACTS 0.578 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1825 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 464,269

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 186 CONTRACTS WITH 1639 CONTRACTS DECREASED AT THE COMEX AND 1825 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 186 CONTRACTS OR 0,7307 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1825) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (1639): TOTAL GAIN IN THE TWO EXCHANGES 186 CONTRACTS. WE NO DOUBT HAD 1) STRONG SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 8.409 TONNES FOLLOWED BY TODAY’S QUEUE. JUMP OF 26,100 oz. 3) ZERO LONG LIQUIDATION//// //.,4) FAIR SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

12,847 CONTRACTS OR 1,284,700 OZ OR 39.96 TONNES 5 TRADING DAY(S) AND THUS AVERAGING: 2569 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAY(S) IN TONNES: 39.96 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 39,96/3550 x 100% TONNES 1.12% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 39.96 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT., FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GOOD SIZED 609 CONTRACT OI TO 137,691 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 740 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 740 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 740 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 609 CONTRACTS AND ADD TO THE 740 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED GAIN OF 131 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 0.655 MILLION OZ

OCCURRED WITH OUR GOOD GAIN IN PRICE OF $0.34

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 10,71 PTS OR 0.33% //Hang Sang CLOSED DOWN 189.68 OR 1.09% /The Nikkei closed UP 634.98 OR 2.31%. //Australia’s all ordinaires CLOSED UP 1.81% /Chinese yuan (ONSHORE) closed UP AT 6.9513//OFFSHORE CHINESE YUAN UP 6.9530// /Oil DOWN TO 82.52 dollars per barrel for WTI and BRENT AT 88.52 / Stocks in Europe OPENED ALL MIXED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1639 CONTRACTS TO 464,318 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR STRONG RISE IN PRICE OF $13.70 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (1825 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1825 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :1825 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1825 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED SIZED TOTAL OF 186 CONTRACTS IN THAT 1825 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 1639 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR RISE IN PRICE OF GOLD $13.70. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING SEPT (12.3390),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 12.3390 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $13.70) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A SMALL SIZED TOTAL GAIN ON OUR TWO EXCHANGES // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS COVERED SOME OF THEIR POSITIONS////// WE HAVE REGISTERED A SMALL SIZED GAIN OF 0.578 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR SEPT. (12.3390 TONNES)…

WE HAD -49 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 235 CONTRACTS OR 23,500 OZ OR 0.7307 TONNES

Estimated gold volume 183,937/// poor/

final gold volumes/yesterday 187,486/ poor

INITIAL STANDINGS FOR SEPT ’22 COMEX GOLD //SEPT 8

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 160,589.703 oz Brinks JPMorgan includes (12 kilobars) |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 60,285.766 oz Manfra |

| No of oz served (contracts) today | 270 notice(s) 27000 OZ 0.8398 TONNES |

| No of oz to be served (notices) | 1503 contracts 150,300 oz 4.6749 TONNES |

| Total monthly oz gold served (contracts) so far this month | 2464 notices 246400 OZ 7,6649 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i) Into Malca: 60,285.766 oz

total deposits 60,285.766 oz

2 customer withdrawals:

i) Out of Brinks 385.710 (12 kilobars)

ii) Out of JPMorgan: 160,203.893 oz

total: 160,203.893 oz

total in tonnes: 4.996 tonnes

Adjustments: 2

Brinks 67,517.100 oz dealer to customer

and Loomis: 4822.65 oz dealer to customer

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPT.

For the front month of SEPT we have an oi of 1773 contracts having GAINED 102 contracts .

We had 159 notices filed on WEDNESDAY so we gained A WHOPPING 261 contracts or an additional 26,100 oz

will stand for gold in this very non active delivery month of September.

October LOST 327 contracts DOWN to 42,376

November GAINED 0 contracts to stand at 6

December LOST 2028 contracts DOWN to 377,245.

We had 270 notice(s) filed today for 27000 oz FOR THE SEPT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 270 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 249 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2022. contract month,

we take the total number of notices filed so far for the month (2464) x 100 oz , to which we add the difference between the open interest for the front month of (SEPT 1773 CONTRACTS ) minus the number of notices served upon today 270 x 100 oz per contract equals 396,700 OZ OR 12.3390 TONNES the number of TONNES standing in this NON active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month:

No of notices filed so far (2464) x 100 oz+ (1773) OI for the front month minus the number of notices served upon today (270} x 100 oz} which equals 396,700 oz standing OR 12.3390 TONNES in this NON active delivery month of SEPTEMBER.

TOTAL COMEX GOLD STANDING: 12.3390 TONNES (A GREAT STANDING FOR A SEPT ( NON ACTIVE) DELIVERY MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,393,976.741 oz 74.462 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 27,529,478.157 OZ

TOTAL REGISTERED GOLD: 13,571,946.547 OZ (422.14 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 13,957,531.610 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 11,177,970. OZ (REG GOLD- PLEDGED GOLD) 347.68 tonnes//rapidly declining

END

SILVER/COMEX/SEPT 8

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2,073,923.178 oz CNT BRINKS JPMORGAN MANFRA |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 822,996.680 oz Delaware |

| No of oz served today (contracts) | 39 CONTRACT(S) 195,000 OZ) |

| No of oz to be served (notices) | 279 contracts (1,395,000 oz) |

| Total monthly oz silver served (contracts) | 5987 contracts 29,935,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 3 deposits into the customer account

i) Into Delaware 162,565.400 o

ii) Into HSBC 59,460.150 oz

iii) Into Loomis: 600,871.130 oz

total deposit: 822,996.650 oz

JPMorgan has a total silver weight: 168.128 million oz/324.265million =51.85% of comex

Comex withdrawals:4

i) Out of CNT: 813,326.610 oz

ii) Out of Brinks 100,734,000 oz

iii) Out of JPMorgan: 574,473.890 oz

iv) Out of Manfra: 585,428.678 oz

total: 2,073,963.178 oz

adjustments: 2/dealer to customer

Brinks 608,749.82 oz

and HSBC 567,428.800 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 46.273 MILLION OZ

TOTAL REG + ELIG. 324.265 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF SEPT OI: 318 CONTRACTS HAVING LOST 32 CONTRACTS. WE HAD

66 CONTRACTS SERVED ON TUESDAY SO WE GAINED 34 CONTRACTS OR AN ADDITIONAL

170,000 OZ WILL STAND FOR METAL IN THIS VERY ACTIVE MONTH OF SEPT.

WE WILL GAIN IN TOTAL SILVER STANDING EACH TRADING DAY UNTIL THE END OF THE MONTH

(CONTINUAL QUEUE JUMPING BY OUR BANKERS SEARCHING FOR SILVER METAL)

OCTOBER LOST 3 CONTRACTS TO STAND AT 676 CONTACTS.

NOVEMBER GAINED 0 CONTRACTS TO STAND AT 12

DECEMBER SAW A LOSS OF 838 CONTRACTS DOWN TO 124,838

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 39 for 195,000 oz

Comex volumes:46.682// est. volume today// poor

Comex volume: confirmed yesterday: 76,669 contracts ( good)

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 5987 x 5,000 oz = 29,935,000 oz

to which we add the difference between the open interest for the front month of SEPT(102) and the number of notices served upon today 39 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT./2022 contract month: 5,987 (notices served so far) x 5000 oz + OI for front month of SEPT (102) – number of notices served upon today (39) x 5000 oz of silver standing for the SEPT contract month equates 31,330,000 oz. .

We have an inventory of 46.273 million oz of registered silver at the comex so Sept delivery of 31.330 MILLION OZ represents 67.700% of that category of silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:49,341// est. volume today// poor

Comex volume: confirmed yesterday: 51,749 contracts ( poor)

END

GLD AND SLV INVENTORY LEVELS

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

AUGUST 10//WITH GOLD UP $2.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES

AUGUST 9/WITH GOLD UP $6.70: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES.

AUGUST 8/WITH GOLD UP $13.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FORM THE GLD//INVENTORY RESTS AT 999.16 TONNES

AUGUST 5/WITH GOLD DOWN $14.25: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .33 TONNES FROM THE GLD////INVENTORY RESTS AT 1000.32 TONNES

AUGUST 4 WITH GOLD UP $29.00 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES FROM THE GLD///INVENTORY REST AT 1000.65 TONNES

AUGUST 2/WITH GOLD UP $3.70; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD//INVENTORY RESTS AT 1002.97 TONNES//

AUGUST 1/WITH GOLD UP $5.75: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1005.87 TONNES

GLD INVENTORY: 971.05 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTO THE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 10/WITH SILVER UP 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 9/WITH SILVER DOWN 25 CENTS TODAY: TWO CHANGES IN SILVER INVENTORY AT THE SLV: FIRST: A DEPOSIT OF 461,000 OZ INTO THE SLV AND THEN A WITHDRAWAL OF 1.014 MILLION OZ..//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 8/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 5/WITH SILVER DOWN 28 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 922,000 OZ FROM THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 4 WITH SILVER UP 21 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 527,000 OZ FROM THE SLV////INVENTORY RESTS AT 486.634 MILLION OZ

AUGUST 2/WITH SILVER DOWN 21 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.504 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.161 MILLION OZ//

AUGUST 1/WITH SILVER UP 17 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE GLD: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 483.657 MILLION OZ//

CLOSING INVENTORY 467.419 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Inflation Is State-Sponsored Terrorism

THURSDAY, SEP 08, 2022 – 10:36 AM

Americans have been laboring under the burden of inflation for well over a year. We feel the pain everywhere, from the gas pump to the grocery store. Once it became impossible to sell the “inflation is transitory” narrative any longer, the Federal Reserve began raising interest rates to fight inflation. As a result, the bubble economy is getting shaky. But even some people at the Fed seem to realize this is a fight they can’t win.

In a talk at the Ron Paul Institute, Mises Institute president Jeff Deist called inflation “state-sponsored terrorism.”

Inflationism is both a fiscal and monetary regime, but its consequences go far beyond economics. It has profound social, moral, and even civilizational effects. And understanding how it terrorizes us is the task today.”

Following is a transcript of Deist’s talk.

The following article was originally published by the Mises Wire. The opinions expressed are the author’s and don’t necessarily reflect those of Peter Schiff or SchiffGold.

I. Introduction

Remember the quaint old days of 2019? We were told the US economy was in great shape. Inflation was low, jobs were plentiful, GDP was growing. And frankly, if covid had not come along, there is a pretty good chance Donald Trump would have been reelected.

At an event in 2019, my friend and economist Dr. Bob Murphy said something very interesting about the political schism in this country. He said: If you think America is divided now, what would things look like if the economy was terrible? If we had another crash like 2008?

Well, we might not have to imagine such a scenario much longer.

If you think Americans are divided today, and at each other’s throats—metaphorically, but more and more literally—imagine if they were cold and hungry!

Imagine if we had to live through something like Weimer Germany, Argentina in the 1980s, Zimbabwe in the 2000s, or Venezuela and Turkey today? What would our political and social divisions look like then?

Ladies and gentlemen, we live under the tyranny of inflationism. It terrorizes us, either softly or loudly. I suspect it will get a lot louder soon.

As the late Bill Peterson explained, “Inflationism, in today’s terms, is deficit-spending, deliberate credit expansion on a national scale, a public policy fallacy of monumental proportions, of creating too much money that chases too few goods. It rests on the ‘money illusion,’ a widespread confusion between income as a flow of money and income as a flow of goods and services—a confusion between ‘money’ and wealth.”

Inflationism is both a fiscal and monetary regime, but its consequences go far beyond economics. It has profound social, moral, and even civilizational effects. And understanding how it terrorizes us is the task today.

II. Understanding Inflationism

I’ll ask you to consider three things.

First, inflation is a policy. We should make them own it. Inflation is not something beyond our control that comes along periodically like the weather. Our monetary and fiscal regimes actually set out to create it and consider it a good thing. Let’s not forget—both Trump and Biden signed off on covid stimulus bills which combined injected roughly $7 TRILLION dollars directly into the economy—even as actual goods and services were dramatically reduced due to lockdowns. Deflation was the natural order of things in response to a crisis, a bullshit crisis in my view, but still a crisis. So of course Uncle Sam actively attempted to undo the natural desire to spend less and hold more cash during a time of uncertainty.

This $7 trillion was created on the fiscal side of things. It was not new Fed bank reserves exchanged for commercial bank assets as a roundabout monetization of Treasury debt, as we saw with quantitative easing. This was direct stimulus from the Treasury via Congress as express fiscal policy. Free money. This money went straight into the accounts of individuals (stimulus checks), state and local governments, millions of small businesses (PPP [Paycheck Protection Program] loans), the airline industry, and untold earmarks. This was actual cash, and it is being spent. So any economist who tells you today’s inflation is somehow a surprise is either charitably misinformed or gaslighting.

This is a policy. Inflation is engineered. The difference between supposedly desirable 2 percent CPI [Consumer Price Index] and very bad, awful, no good 9 percent CPI is only one of degree. The same mindset produces both. But the inflationists insist a little bit of virus is good for us, like a vaccine … So an express policy of some inflation is the mechanism to forestall too much inflation. This is a curious position.

Second, inflation is nothing less than sanctioned state terror, and we ought to treat it as such. It’s criminal. It makes us live in fear. Inflation is not just an economic issue, but in fact, produces deep cultural and social sickness in any society it touches. It makes business planning and entrepreneurship—which rely on profit and loss calculations using money prices—far more difficult and risky, which means we get less of both. How do you measure money profits when the unit of measurement keeps falling in value? It erodes capital accumulation, the driver of greater productivity and material progress. So inflation destroys both existing wealth and future wealth, which never comes into being and thus diminishes the world our children and grandchildren inhabit. And it makes us poor and vulnerable in our senior years.

After all, saving is for chumps. Current one-year CD rates are below 3 percent, while inflation is at least 9 percent. So you’re losing 6 points just by standing still! By the way, the last time official CPI approached double digits, in the early ’80s, a one-year CD earned 15 percent. I’d like to hear Jerome Powell explain that. By the way, ever since Alan Greenspan began this great experiment of four decades of lower and lower interest rates, guess who hasn’t benefited? Poor people and subprime borrowers, who still pay well over 20 percent for their car loans and credit cards.

But here is an unspoken truth: inflation also makes us worse people. It degrades us morally. It almost forces us to choose current consumption over thrift. Economists call this high time preference, preferring material things today at the expense of saving or investing. It makes us live for the present at the expense of the future, the opposite of what all healthy societies do. Capital accumulation over time, the result of profit, saving, and investing, is how we all got here today—a world with almost unimaginable material wealth all around us. Inflationism reverses this.

So this very human impulse, to save for a rainy day and perhaps leave something for your children, is upended. Inflationism is inescapably an antihuman policy.

Third, hyperinflation can happen here. It may not happen, and it may not happen soon. But it might well happen. And even steady 10 percent inflation means prices double roughly every seven years. We can pretend the laws of economics don’t apply to the world’s leading superpower, or that the world’s reserve currency is safe from the problems experienced by lesser countries. And it’s certainly true our reserve currency status insulates us and makes the world need dollars. Governments and industry mostly use US dollars to buy oil from OPEC countries, hence the term “petrodollar.” It’s certainly true governments, central banks, large multinational companies, worldwide investment funds, sovereign wealth funds, and pension funds all hold plenty of US dollars—and thus in a perverse way share our interest in maintaining King Dollar. It’s true we don’t have easy historical examples of a world reserve currency, like gold, suffering a rapid devaluation across the world (even the Spanish silver devaluation of the 1500 and 1600s was not necessarily caused by a glut in circulating currency). So we’re in uncharted territory, especially given the fiscal and monetary excesses of the last twenty-five years and especially the last two years. But this only means the potential contagion is greater and more dangerous. The whole world can be sickened at once.

III. A Story: When Money Dies

But as most of you surely know by now, we don’t turn the ship around or win hearts and minds simply with logic and facts and airtight arguments. We need stories, or narratives, in today’s awful media parlance, to gain influence. We need emotional reactions. So I will suggest a story with plenty of pathos to shake people out of their complacency and sound the warning.

That story is When Money Dies, Adam Fergusson’s brilliant cautionary account of hyperinflation in Weimar-era Germany. It is the story Americans desperately need to hear today.

Fergusson’s book should be assigned to central bankers stat (we wonder how many of them know of it). It’s not a book about economic policy per se—it’s a story, a historical account of folly and hubris on the part of German politicians and bureaucrats. It’s the story of a disaster created by humans who imagined they could overcome markets by monetary fiat. It’s a reminder that war and inflation are inextricably linked, that war finance leads nations to economic disaster and sets the stage for authoritarian bellicosity. We think Versailles and reparations created the conditions for Hitler’s rise, but without the Reichbank’s earlier suspension of its one-third gold reserve requirement in 1914, it seems unlikely Germany would have become a dominant European military power. Without inflationism, Hitler might have been a footnote.

Most of all, When Money Dies is a tale of privation and degradation. Not only for Germans, but also Austrians and Hungarians grappling with their own political upheavals and currency crises in the 1910s and ’20s. In a particularly poignant chapter, Fergusson describes the travails of a Viennese widow named Anna Eisenmenger. A friend of mine, @popeofcapitalism on Twitter, sent me her diary from Amazon.

The story starts with her comfortable life as the wife of a doctor and mother to a wonderful daughter and three sons. They are talented and cultured and musical and upper middle class. They even socialize with Archduke Franz Ferdinand and his wife, the Duchess of Hohenberg.

But in May 1914 their happy life is shattered. Ferdinand is assassinated at Sarajevo, and war breaks out. Wars cost money, and the gold standard wisely adopted by Austria-Hungary in 1892 is almost immediately seen as an impediment. So the government predictably begins to issue war bonds in huge numbers, and the central bank fires up the printing presses. This results in a sixteenfold increase in prices just during the war years.

But the human effects are catastrophic, even apart from the war itself.

Frau Eisenmenger is luckier than most Viennese women. She owns small investments which produce modest income—fixed in kronen. Her banker quietly urges her to immediately exchange any funds for Swiss francs. She demurs, as dealing in foreign currency has been made illegal. But soon she realizes he was right. There is probably a lesson here for all of us!

As the war unfolds, she is forced into black markets and pawning assets to procure food for her war-damaged children. Her currency and Austrian bonds become almost worthless. She exchanges her husband’s gold watch for potatoes and coal. The downward spiral of her life, marked by hunger and hoarding anything with real value, happens so quickly she barely has time to adjust.

But her misery doesn’t stop with the end of the war. On the contrary, the Saint-Germain Treaty in 1919 gives way to a period of hyperinflation: the money supply increases from 12 to 30 billion kronen in 1920, and to about 147 billion kronen at the end of 1921 (does this sound like America 2020, by the way?). By August 1922, consumer prices are fourteen thousand times greater than before the start of the war eight years earlier.

In just a few short years she endures countless tragedies, all made worse by privation, cold, and hunger. Her husband dies. Her daughter contracts tuberculosis and dies, leaving Frau Eisenmenger to take care of her infant daughter and young son. One son goes missing in the war, one son is blinded, and her son-in-law becomes crippled following the loss of both legs. Food and coal are rationed, so her apartment is a miserable hovel—and she is forced to dodge searches by the “Food Police” looking for illegal hoarding. Ultimately, she is shot in the lung by her own Communist son, Karl, in a fit of rage.

There is a haunting and historically accurate silent film about conditions in Vienna during this era called The Joyless Street, starring a young Greta Garbo. Her character sees everything deteriorate around her; even her father beats her with his cane for returning home without food. Once friendly neighbors become suspicious of each other’s stores of bread and cheese, while prostitution becomes rampant. Angry people jostle in line, waiting for the butcher to open; when he does, only the most attractive women receive the scraps of meat available that day. Fistfights become common. Starving children beg for food in front of restaurants and cafes like stray dogs. Everything familiar and beautiful in society becomes degraded and cheapened seemingly overnight.

Like a Stephen King horror movie, something very familiar changes into a strange and menacing place. Your neighborhood takes on a different light. People you thought you knew became malevolent strangers. Scapegoating, blame, and snitching become commonplace.

Is this beginning to sound familiar, especially after Biden’s sick speech the other night?

So, next time one of these sociopaths in our political class wants to spend a few trillion more to pay for a green new deal or a war with China or free college, remember Frau Eisenmenger’s story.

IV. The Lessons for Today

How do we apply this grim historical lesson from the Weimar period to America today? How do we tell this story?

First, we explain inflationism in human terms, to personalize it and de-bamboozle it. Make monetary policy vital and immediate, not boring and dry and technocratic. Again, there are enormous moral and civilization components to monetary policy. Inflation not only harms our economy, it makes us worse people: profligate, shortsighted, lazy, and unconcerned with future generations. Professor Guido Hülsmann literally wrote the book on this. It’s called The Ethics of Money Production. This is maybe the greatest untold story in America today: the story of not only how the Fed fundamentally shifted our economy from one of production to consumption, but what it did to us as people. Don’t let them hide behind complex Fed speak the simple reality: monetary policy is nothing less than criminal theft from future generations, from savers, and from the poorest Americans, who are furthest from the money spigot. The idea that reasonably intelligent laypeople cannot understand monetary policy, that it is too important and complex for anyone but experts, is nonsense. We should expose it.

Second, ridicule the absurd idea that “policy” can make us richer. More goods and services, produced more and more efficiently, thanks to capital—and thereby creating price deflation—make us richer. That’s the only way. Not by legislative or monetary fiat.

So we should attack any notion of “public policy” and especially “monetary policy.” Inflationism creates a fake economy, a “make-believe” economy, as Axios recently put it. A fake economy depends on enormous levels of ongoing fiscal and monetary intervention. We call this “financialization,” but we all have a sense that our prosperity is borrowed. We all feel it. Capital markets are degraded: a lot of money moves around without creating any value for anyone. Companies don’t necessarily make profits or pay dividends; all that matters to shareholders is selling their stock for capital gains. It always requires a new Ponzi buyer. But we know intuitively this isn’t right: consider a restaurant or dry cleaner which operated without profit for years in the hope of selling for a gain years or decades later. Only the distorted incentives created by inflationism make this mindset possible. So down with “policy”—what we need is sound money!

Finally, let us not fear being accused of hyperbole or alarmism. Let me ask you this: what happens if we’re wrong, and what happens if they’re wrong? What they are doing, meaning central bankers and national treasuries, is unprecedented. Fake money is infinite, real resources are not. Hyperinflation may not be around the corner or even years away; no one can predict such a thing. But at some point the US economy must create real organic growth if we hope to maintain living standards and avoid an ugly inflationary reality. No amount of monetary or fiscal engineering can take the place of capital accumulation and higher productivity. More money and credit is no substitute for more, better, and cheaper goods and services. Political money can’t work, and we should never be afraid to attack it root and branch. We need private money, the only money immune from the inescapable political incentive to vote for things now and pay for them later. If this is radical, so be it.

History shows us how money dies. Yes, it can happen here. Only a fool thinks otherwise.

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

GOLD/SILVER

END

3.Chris Powell of GATA provides to us very important physical commentaries

David H. Smith, precious metals investing philosopher, is fondly remembered

Submitted by admin on Wed, 2022-09-07 20:28Section: Daily Dispatches

By Stefan Gleason

Money Metals Exchange, Eagle, Idaho

Wednesday, September 7, 2022

Many precious metals investors over the years have closely followed the writings of David H. Smith, the beloved senior analyst at The Morgan Report and monthly columnist for Money Metals Exchange.

I am saddened to report that my friend — our friend — David Smith lost his battle with cancer last weekend.

David was a phenomenal yet humble man. He was a teacher, a student, and a philosopher.

I have rarely a met a more optimistic, thoughtful, and wise person.

He was not just a pithy writer who informed and guided his readers; he was a trusted advisor to me personally. …

… For the remainder of the report:

end

END

4. OTHER GOLD/SILVER COMMENTARIES

-END-

.

end

5.OTHER COMMODITIES:

COMMODITIES IN GENERAL/COAL

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.9520

OFFSHORE YUAN: 6.9530

HANG SENG CLOSED DOWN 189.68 PTS OR 1.00%

2. Nikkei closed UP 634.98 OR 2.31%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 109.34/Euro RISES TO 1.0026

3b Japan 10 YR bond yield: RISES TO. +.243/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 143.38/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP -// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.565%/Italian 10 Yr bond yield FALLS to 3.84% /SPAIN 10 YR BOND YIELD FALLS TO 2.72%…

3i Greek 10 year bond yield RISES TO 4.14//

3j Gold at $1724.95 silver at: 18.69 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 15/100 roubles/dollar; ROUBLE AT 60.63//

3m oil into the 82 dollar handle for WTI and 88 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 143.38DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 9710– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9737well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.216 DOWN 5 BASIS PTS

USA 30 YR BOND YIELD: 3.385 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,24

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Flat Ahead Of ECB, Powell Doubleheader

THURSDAY, SEP 08, 2022 – 08:01 AM

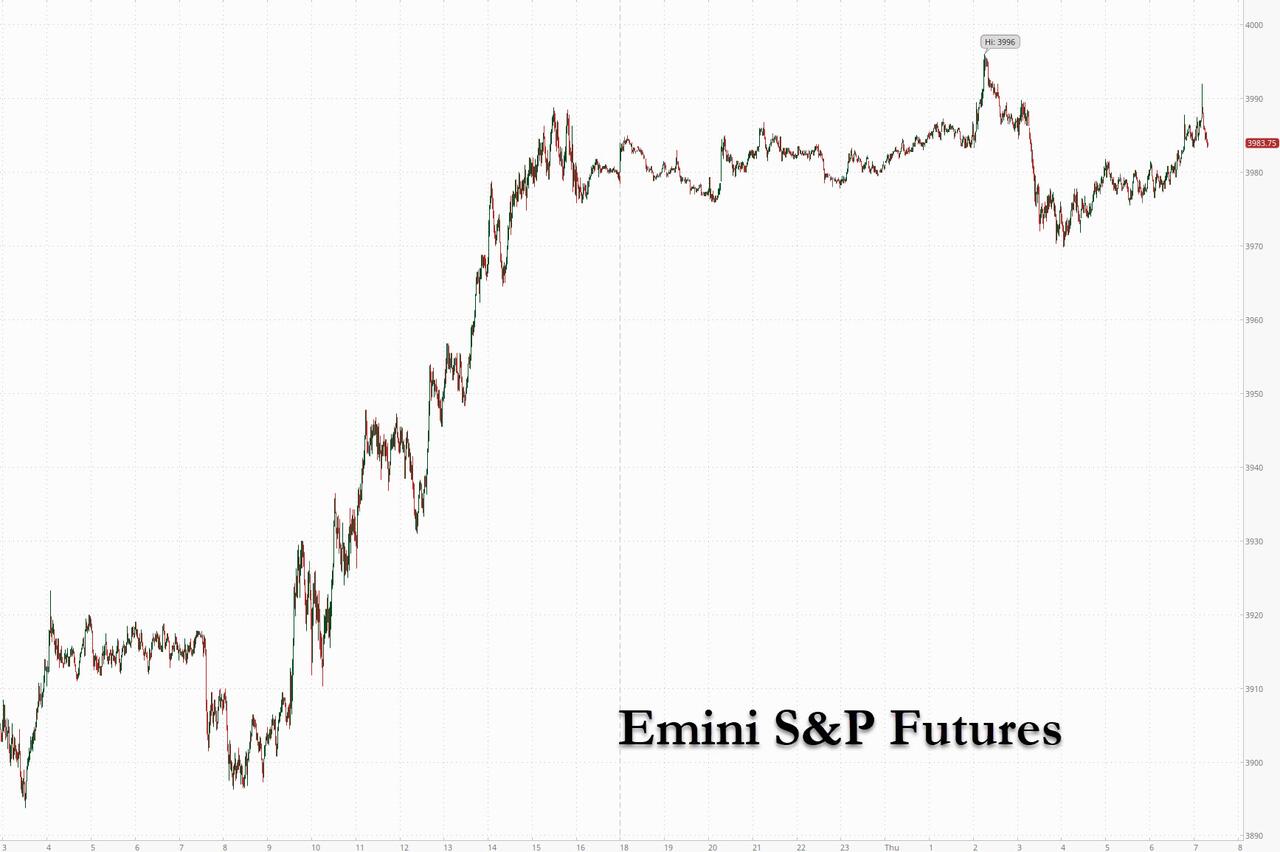

US stock futures traded flat, erasing modest earlier gains and losses in the overnight session as investors remained cautious while watching for signs of a softening in the Federal Reserve’s policy. Nasdaq 100 futures were little changed by 7:15 a.m. in New York after earlier gaining as much as 0.6%. S&P 500 contracts were up less than 0.1%, at 3,983.75 after hitting 3,996 overnight and following small gains in Estoxx50. The underlying index notched its biggest gain in a month on Wednesday which was sparked by yet another short squeeze, and is attempting to rebound following three straight weeks of declines that were fueled by fading bets on a Fed policy pivot and as investors braced for the impact of a potential economic contraction. Crude oil futures managed a feeble, +0.5% bounce after falling 5.7% Wednesday. The dollar reversed earlier gains helping lift the badly beaten EUR and JPY higher.

Among notable movers in premarket trading, American Eagle Outfitters slumped as much 16% after the retailer reported results for a quarter that Citigroup analysts described as “rough,” while also pausing its quarterly cash dividend. GameStop jumped as much as 12% in US premarket trading after the announcement of a partnership with cryptocurrency exchange FTX US, though the gaming company reported net sales for the second quarter that missed estimates. Here are some other notable premarket movers:

- Asana gains 18% in premarket trading after the software company boosted its revenue guidance for the full year. Separately, the company said CEO Dustin Moskovitz bought $350 million of shares in a private placement.

- Moderna (MRNA US) gains 2.2% in premarket trading after Deutsche Bank upgraded the stock to buy from hold after its “solid” second quarter earnings beat and the “welcome” late- July news of additional fall 2022 orders from the US.

- Apple (AAPL US) shares were steady in premarket trading as analysts say the biggest takeaway from the company’s product event was its pricing strategy, with the iPhone maker opting not to raise average prices for its latest smartphone and watch models.

- Keep an eye on Intel (INTC US) as the stock is started with a hold rating and $32 price target at Stifel, which cites uncertainty over the chipmaker’s turnaround strategy. Stifel also started Nvidia (NVDA US) with a hold recommendation and AMD (AMD US) with a buy rating.

- Chipmakers may also be in focus after TSMC, the world’s largest supplier of made-to-order chips, said sales rose 59% in August from a year earlier. In the US, watch equipment stocks such as Applied Materials (AMAT US), KLA (KLAC US), Lam Research (LRCX US), Entegris (ENTG US), Teradyne (TER US), and MKS Instruments (MKSI US)

Sentiment improved on Wednesday after Fed Vice Chair Lael Brainard warned that “two-sided” risks will eventually emerge from tightening monetary policy — remarks that were considered to have a more dovish tone than some other recent Fed comments. Focus on Thursday will be on a speech by Chair Jerome Powell, who is scheduled to speak just after a monetary policy decision by the European Central Bank.

Still, strategists warn that risks to a sustained rally are growing. “Sentiment is very depressed and markets are oversold,” Frederique Carrier, head of investment strategy at RBC Wealth Management, said on Bloomberg TV. “It’s possible that there is a rally, but as long as the Fed is increasing interest rates, it’s very difficult for the upside to be very strong.”

As central banks are walking a tightrope, moving sharply to tackle price pressures while remaining leery of sparking a damaging economic contraction in the process, today we get a central bank doubleheader with the ECB expected to hike rates by 75bps at 8:15am, while Jerome Powell speaks at a monetary conference at 9:10am ET. The Euro is holding around parity against the dollar ahead of the ECB, where money markets price in around 65bp of rate hikes for the meeting, with most economists expecting a 75bp rate hike. The focal point of US session after ECB is Powell participation in moderated discussion at a monetary policy conference.

“What we are seeing in Europe is very, very concerning, what is happening there is the worst energy crisis we have seen since the oil embargo in 70s,” Ryan Lemand, Securrency Capital advisor to the board, said on Bloomberg Television. “Europe will face a recession, one of the worst recessions it will have faced and I don’t think risky assets are pricing this in correctly.”

Fed officials reiterated their determination to get inflation under control. Vice Chair Lael Brainard said interest rates will need to rise to restrictive levels, while cautioning risks would become more two-sided in the future. The Fed’s Beige Book report said US economic expansion prospects were weak, while adding that price growth showed signs of decelerating.

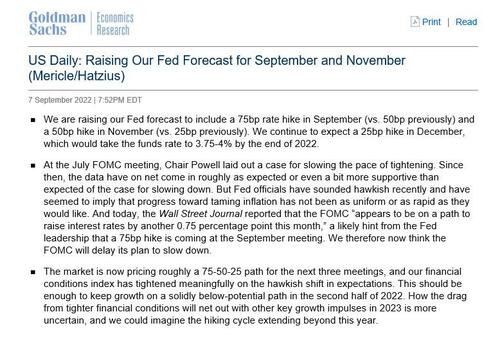

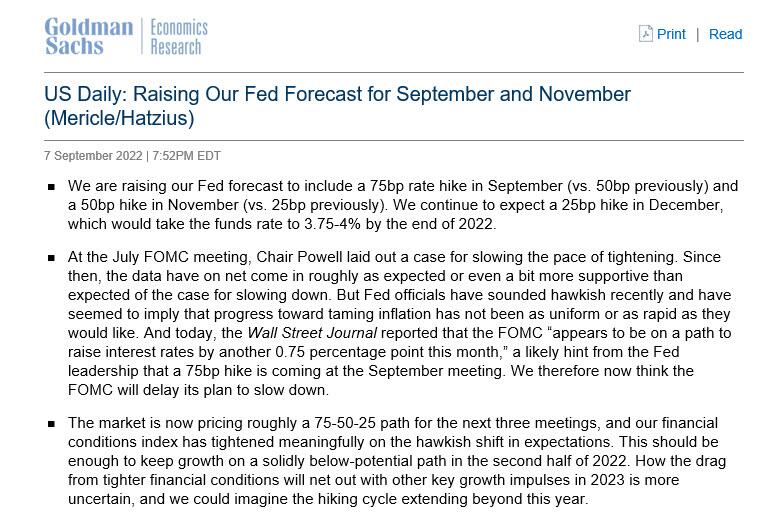

Goldman economists lifted their forecast for the pace of Fed interest rate increases, expecting the Fed to hike by 75 basis points this month and 50 basis points in November, up from previous forecasts of 50 basis points and 25 basis points respectively. They are tipping a 25 basis points move in December.

Deutsche Bank AG strategists also said that elevated “late-cycle earnings,” higher valuations and the risk of a recession limit the fundamental case for a sustained rally in US stocks. In their worst case scenario, they see the S&P 500 slumping to 3,000 points in the event of a recession — almost 25% below its latest close. However, their base case still calls for equities to rise by year end.

In Europe, the Stoxx 50 rose 0.1%, surrendering most of an initial 0.6% advance as retailers slumped after a profit warning from Primark-owner Associated British Foods Plc. The FTSE 100 outperformed peers, adding 0.4%, IBEX lags, dropping 0.2%. Insurance, banks and miners are the strongest-performing sectors. Here are the biggest European movers:

- Genus shares jump as much as 16%, the most since May 2019, after Peel Hunt upgraded the firm to buy, saying its business was “back on the front foot” after publishing FY earnings

- SBB shares jumped as much as 11% during early trading in Stockholm after signing a letter of intent to sell SEK9 billion worth of properties to an unidentified institutional investor

- European semiconductor stocks rise on Thursday, after chipmaking bellwether TSMC reported an acceleration in sales in August and Apple launched a new lineup of devices

- Ocado shares advance as much as 4.4% after being upgraded to equal-weight from underweight at Barclays, which says the risks are now “more evenly balanced” for the online grocer

- Alleima gains as much as 6.1% after Danske Bank initiated coverage of the shares with a buy recommendation, where it sees “plenty of value,” also expecting it to benefit from a cyclical recovery

- Munters shares rise as much as 7.6% after Nordea upgraded the Swedish climate and cooling manufacturer to buy on “surging order intake,” raising adjusted Ebita estimates for 2023 and 2024

- Energean shares rise as much as 15% after it increased medium-term financial targets in its 1H report and a quarterly dividend helped by what Peel Hunt called “robust operational performance”

- Atos shares tumble to the lowest level since 1993 after Goldman Sachs downgrades the French tech firm to sell from neutral, citing low visibility and a long path to recovery

- Darktrace shares plunge as much as 35%, the most on record, after M&A talks with Thoma Bravo collapsed, with the suitor not intending to make an offer for the UK cybersecurity company

- AB Foods shares drop as much as 8.6% after the Primark owner said it expects FY23 adjusted operating profit and adjusted earnings per share to be lower than this financial year

- Somfy fell as much as 13% after the French maker of windows and doors warned of a possible pullback in consumer spending after its 1H results were hurt by a slowdown in growth

Earlier in the session, Asian stocks rebounded from their lowest level in more than two years as oil prices eased and the region’s suppliers to Apple Inc. climbed after the US company unveiled new lineups for its iPhones and watches. The MSCI Asia Pacific Index rose as much as 1.3%, snapping a five-day slump, as technology and industrial shares advanced. Japan gained along with Australia and Taiwan, while China dropped as Chengdu extended a week-long lockdown in most downtown areas after Covid-19 cases increased. Asian stocks regained some footing amid a rout that still has the market on course for its fourth-straight week of losses. A two-day retreat in long-term US Treasury yields and Wednesday’s plunge in oil prices helped lift sentiment that had been hurt by concerns over a hawkish Federal Reserve.

“Markets have started to price in a less aggressive Fed, while falling oil and other commodity prices have also helped to ease profit-margin pressures for Asian companies,” Soo Hai Lim, head of Asia ex-China equities at Barings, wrote in a note. “In the longer term, we believe the performance of individual Asian markets will be driven by country-specific growth factors.” Asian stocks are down more than 4% this month amid an outflow of funds from the region. Still, some investors believe that attractive valuations will lure money back and spur a rebound. Read: ‘Massive Discount’ Has Robeco Eyeing 2003-Like Asia Stock Bounce

Japanese stocks gained, with the Topix climbing the most since July 20, after a rally in US shares and a weak yen boosted exporters. The Topix rose 2.2% to 1,957.62 at the 3pm close in Tokyo, while the Nikkei 225 advanced 2.3% to 28,065.28. Toyota Motor contributed the most to the Topix’s gain, increasing 2.3%. Out of 2,169 stocks in the index, 1,947 rose and 161 fell, while 61 were unchanged. Shares also climbed after Japanese GDP data showed the economy grew at a faster pace last quarter than earlier estimates. “Japanese stocks look attractive to dollar-denominated investors in the short term,” said Tetsuo Seshimo, portfolio manager at Saison Asset Management. “It makes it easier to buy when there’s a bit of a risk-on mood.”

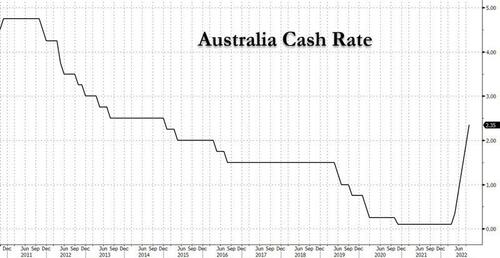

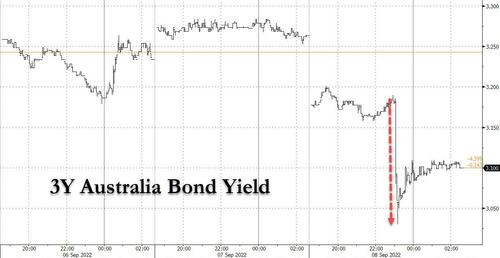

Australian stocks gained most in ten weeks on RBA Lowe’s comments. The S&P/ASX 200 index rose 1.8% to close at 6,848.70, staging an afternoon rally after the RBA’s chief signaled a potential end to outsized interest rate hikes. Mining and banking shares provided the biggest boost to the benchmark. Reserve Bank Governor Philip Lowe said the case for a slower pace of tightening becomes stronger as the cash rate moves higher. The central bank delivered a fourth straight half-point hike this week to take the cash rate to 2.35%. Energy shares declined as oil fell to a near eight-month low before steadying, with investors assessing the outlook for demand as China pushes on with its Covid Zero policy and central banks tighten monetary policy. In New Zealand, the S&P/NZX 50 index rose 1.1% to 11,677.93

Indian stocks rose, snapping two sessions of declines, as a drop in crude oil prices below $90 per barrel raised optimism of lower import costs and softer consumer prices. The S&P BSE Sensex gained 1.1% to 59,688, its highest level in three weeks, while the NSE Nifty 50 Index advanced 1%. ICICI Bank contributed the most to the Sensex, which had 24 of 30 member shares ending higher. Fourteen of 19 sectoral sub-indexes compiled by BSE Ltd. advanced, led by a gauge of banks. Price of Brent crude, a major import for India, hovered around $88 per barrel, their lowest level since early February

In FX, the pound pared a decline as UK Prime Minister Liz Truss outlined plans to provide relief on rising energy costs to British households and businesses, which she said is expected to curb inflation. There has been widespread speculation that the government’s aid proposals will require further debt sales to fund it that could drive up bond yields. Short-end gilts steadied after rallying Wednesday on bets the plan would calm inflation. Other notable movers:

- A dollar gauge was steady as traders assessed comments from Federal Reserve officials on their commitment to fighting inflation.

- The euro was little changed against the dollar. On European bond markets, two-year German yields rose by around 5 basis points, while the Italian two-year yield fell by one basis point. Market pricing for the following ECB meetings picked up slightly. Just one jumbo rate hike from the European Central Bank may not cut it for euro bulls looking for a sustainable move above parity with the dollar

- The yen gave up an earlier modest advance to trade below 144 per dollar after senior Japanese officials met for the first time since June to discuss markets but said their stance remained the same

- The Australian dollar slumped and Australian sovereign bonds jumped after Reserve Bank Governor Philip Lowe signaled a potential end to outsized interest-rate increases. Australian dollar underperformed all its Group-of-10 peers

In rates, Treasuries steadied after rallying as Australia’s central bank chief signaled a potential end to outsized policy moves; they were slightly richer from belly out to the long-end of the curve with price action light ahead of ECB policy rate decision at 8:15am ET. US yields were richer by up to 2bp across belly of the curve with 2s5s, 2s10s spreads both flatter by around 2bp on the day as front-end underperforms; 10-year yields around 3.25% with bunds and gilts lagging by 3bp and 2bp in the sector after an earlier rally spurred by RBA signaling a potential end to outsized interest-rate increases, making it an outlier in G-10. Bunds yield curve bear-flattens with 2-year yield up 3.6bps to around 1.12%, underperforming USTs and gilts. Both 10-year and 2-year gilts yields trade around 3% as traders gear for details of the new economic package from Truss. Futures gained during Asia session after RBA’s dovish policy pivot, following Aussie bonds higher before fading slightly over London morning. IG dollar issuance slate includes Mitsubishi HC $500m 5Y; six borrowers priced $10b on Wednesday, follows Tuesday’s massive $33b over 44 tranches. Three-month dollar Libor +4.17bp to 3.23571%.

In commodities, oil trimmed a sharp slide this week sparked by demand risks from monetary tightening and China’s Covid travails — the megacity of Chengdu extended a weeklong lockdown in most downtown areas. Gold added $1 to ~$1,719. Most base metals trade in the green; LME aluminum rises 1.4%, outperforming peers. LME nickel lags, dropping 1.3%.

Bitcoin trades relatively flat just above USD 19,000 whilst Ethereum remains north of USD 1,600.

To the day ahead now, and the ECB policy decision will be the main highlight, along with President Lagarde’s press conference. Otherwise, we’ll also hear from Fed Chair Powell and the Fed’s Evans and Kashkari. Finally, data releases include the weekly initial jobless claims from the US.

Market Snapshot

- S&P 500 futures down 0.1% to 3,975.00

- STOXX Europe 600 little changed at 412.42

- MXAP up 1.0% to 152.06

- MXAPJ up 0.3% to 498.31

- Nikkei up 2.3% to 28,065.28

- Topix up 2.2% to 1,957.62

- Hang Seng Index down 1.0% to 18,854.62

- Shanghai Composite down 0.3% to 3,235.59

- Sensex up 0.8% to 59,518.06

- Australia S&P/ASX 200 up 1.8% to 6,848.67

- Kospi up 0.3% to 2,384.28

- German 10Y yield little changed at 1.59%

- Euro down 0.2% to $0.9984

- Gold spot down 0.1% to $1,717.37

- U.S. Dollar Index little changed at 109.81

Top Overnight News from Bloomberg

- With the greenback supercharged by expectations of higher-for- longer US interest rates, traders are struggling to pick the bottom for Asian currencies

- The European Union may need additional stimulus measures if the economic downturn worsens, according to the bloc’s economy chief, who warned that the coming winter could be “one of the worst in history”

- Investors are bracing for details of UK Prime Minister Liz Truss’s new economic package, with some warning that a new wave of debt issuance to fund the spending risks roiling debt markets and pressuring the battered pound

- Inflation in Hungary accelerated to the highest level since 1998 in August as food prices increased by almost a third, according to stats office data. Consumer prices rose an annual 15.6% in August after 13.7% growth in July

- Russian Deputy Finance Minister Timur Maksimov said the government plans to resume sales of its bonds, known as OFZs, as early as this month, Interfax reports

A more detailed look at global markets

Asia-Pacific stocks were mostly positive after the relief rally on Wall St where a lower yield environment and declines in oil prices underpinned risk appetite, although Chinese markets underperformed on COVID woes. ASX 200 was positive with tech and gold miners leading the advances across nearly all sectors aside from energy after the recent fall in oil. Nikkei 225 surged towards the 28,000 level with sentiment lifted following the larger-than-expected upward revisions to Q2 GDP. Hang Seng and Shanghai Comp underperformed their regional peers after the megacity of Chengdu extended its lockdown in most areas and Shenzhen also temporarily lowered its entry quota for Hong Kong travellers amid a resource squeeze from the ongoing outbreak.

Top Asian News

- China Health Authority encourages people to stay put during China National Day holidays (Oct 1st-7th), and to avoid travel outside their cities, via Reuters. China Transport Ministry Official said daily average travel for mid-Autumn festival expected to drop 32% Y/Y.

- RBA Governor Lowe said further rate rises will be required but they are not on a preset path and said the case for a slower pace of rate hikes becomes stronger as the level of the Cash Rate increases. Lowe also commented that demand has to grow more slowly to bring it back in line with supply and there is a significant demand element to higher inflation, while he added it is very possible that wage growth does not pick up much further and said quantitative tightening is not on the agenda.

- Japanese top currency diplomat Kanda said MoF, BoJ, and FSA meeting produced no statement this time as basic understanding on FX remains unchanged from the prior meeting. Japanese top currency diplomat Kanda agreed at the meeting on the need to watch markets with a strong sense of urgency, will not rule out any step, and are ready to take action in the FX market; BoJ and Govt are extremely worried about the recent JPY moves.

- Japan Deputy Chief Cabinet Secretary said it is watching FX moves with high sense of urgency, ready to take necessary steps if recent FX moves continue. When asked about potential intervention, said he would not comment on specific market views. Will make decisions at the appropriate time regarding both economic sentiment and inflation when asked about supplementary budget

European bourses trade with a directionless bias on ECB day after waning off best levels, and following a mixed APAC handover. European sectors are now mixed (vs mostly firmer at the open), with defensives making their way up the ranks. Stateside, US equity futures are portraying a similar tentativeness as their European counterparts, with the main contracts trading on either side of the flat mark but holding onto yesterday’s gains.

Top European News

- Primark Drags Down AB Foods Outlook as Energy Costs Rise

- Commerzbank Says Profit Target Remains Despite Energy Crisis

- Euro Holding Parity Needs Uber-Hawkish Meet: ECB Cheat Sheet

- Sampo Plans Dual Listing in Stockholm to Boost Liquidity

- Zurich Cuts Swimming Pool Temperatures to Save Energy

FX

- DXY pulled back further from Wednesday’s new y-t-d and multi-year peak before finding support just under 109.500.

- The EUR briefly popped over parity and the JPY pared more losses from its worst levels in around 24 years vs the USD.

- The Kiwi and Aussie both have cause to underperform given a deceleration in NZ manufacturing sales, bleak Australian trade data and remarks from RBA Governor Lowe.

Fixed Income

- Bunds and Gilts sit far from best levels between 145.82-144.71 and 106.84-105.75 parameters.

- Conversely, US Treasuries are treading water ahead of jobless claims and Fed chair Powell, albeit also off overnight peaks

Commodities

- WTI and Brent front-month futures trade volatile with two-way action seen in the European morning.

- JPMorgan believes OPEC+ will need to cut another 1mln BPD to stabilise the market.

- Spot gold holds onto yesterday’s gains north of USD 1,700/oz, but under the USD 1,726.79/oz high set on Tuesday

- Base metals are mostly firmer but the upside is capped by China’s COVID woes, nonetheless, 3M LME copper is supported by reports that Workers at Chile’s Escondida copper mine voted to strike over safety concerns.

- Russian Finance Minister considers it reasonable to build reserves in gold and Yuan, according to Tass.

US Event Calendar

- 08:30: Aug. Continuing Claims, est. 1.44m, prior 1.44m

- 08:30: Sept. Initial Jobless Claims, est. 235,000, prior 232,000

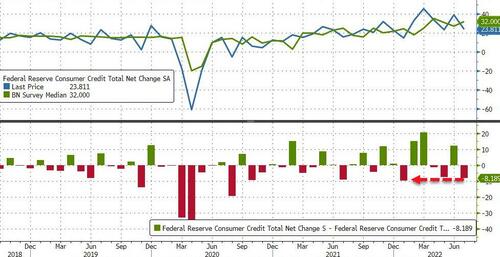

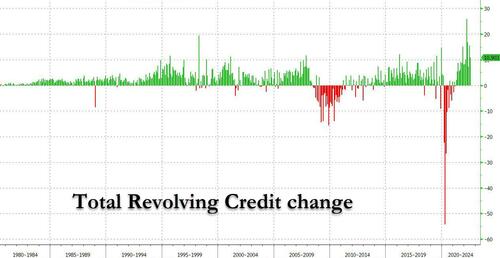

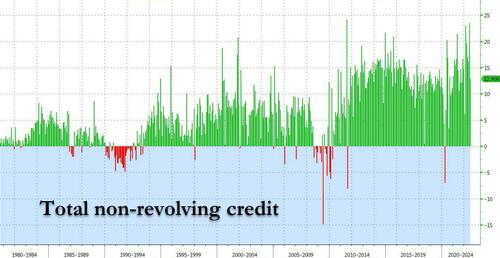

- 15:00: July Consumer Credit, est. $32b, prior $40.2b

Central Banks

- 09:10: Powell Speaks at Monetary Policy Conference

- 12:00: Fed’s Evans speaks on economy, policy at DuPage forum

- 14:20: Fed’s Kashkari Makes Introductory Remarks at Labor Market…

DB’s Jim Reid concludes the overnight wrap

Readers could be forgiven for losing track of the various themes in markets right now, after a volatile 24 hours that’s seen oil prices crash to their lowest level in months, the dollar reach another multi-decade high, a WSJ article that cemented expectations for another 75bps Fed hike this month, but an S&P 500 that relentlessly marched higher all day to close +1.83%. Indeed even as the likelihood rose that we could see a more rapid pace of near-term hikes, both equities and sovereign bonds rallied yesterday, since the commodity declines raised hopes that central banks could afford to slow up on rate hikes when we get to 2023. Today could put that narrative under pressure however, as there’s a decent chance we’ll see the largest ECB hike in their history, and we’re also set to hear from Fed Chair Powell in his last appearance before the next FOMC meeting.

Running through those specific moves, oil prices took a significant tumble yesterday as concerns about the strength of global demand continued to fester. Indeed, Brent crude (-5.55%) closed beneath $90/bbl for the first time since early February, before Russia’s invasion of Ukraine began, whilst WTI fell -5.69% to $81.85/bbl. Brent futures are back up c.+1% this morning in Asia. One factor behind the declines has been the continued pursuit of the zero-Covid strategy in China, and we got confirmation yesterday that Chengdu (population 21 million) would be extending its lockdown in most of the city. Even European Gas (-10.82%) fell and is now down -28.47% from the intra-day peak on Monday as the market digested the latest NS1 closure announced after the close on Friday. Since then we’re actually down -14.78%. How much of this is a demand destruction story this week and how much is a “we now have peak bad news on European gas supplies” is one to debate.