by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1717.45 UP $7.85

SILVER: $18.81 UP 31 CENTS

ACCESS MARKET:

GOLD $1717.30

SILVER: $18.84

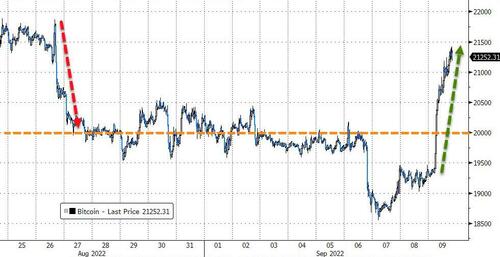

Bitcoin morning price: $21,073 UP 1875

Bitcoin: afternoon price: $21,188 UP 1990

Platinum price closing UP $14.45 AT $882.65

Palladium price; closing UP $96.45 at $2143.20

END

DONATE

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,708.000000000 USD

INTENT DATE: 09/08/2022 DELIVERY DATE: 09/12/2022

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 127

435 H SCOTIA CAPITAL 129

624 H BOFA SECURITIES 667

657 C MORGAN STANLEY 8 16

661 C JP MORGAN 940

709 C BARCLAYS 621

737 C ADVANTAGE 21 69

800 C MAREX SPEC 5 22

880 C CITIGROUP 5

905 C ADM 24

TOTAL: 1,327 1,327

MONTH TO DATE: 3,791

JPMorgan stopped: 940/1327

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR SEPT CONTRACT:

1327 NOTICES FOR 132,700 OZ //4.1275 TONNES

total notices so far: 3791 contracts for 379,100 oz (11.7916 tonnes)

SILVER NOTICES: 169 NOTICES FILED FOR 845,000 OZ/

total number of notices filed so far this month 6156 : for 30,780,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $7.85

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: ////

WITHDRAWALS OF 2.90 TONNES AND 1.51 TONNES FROM THE GLD//

INVENTORY RESTS AT 966.64 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $.31

AT THE SLV// ://SMALL CHANGES IN SILVER INVENTORY AT THE SLV//:A DEPOSIT OF 138,000 OZ INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 467.557 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GOOD SIZED 546 CONTRACTS TO 138,237. AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE LOSS IN OI WAS ACCOMPLISHED DESPITE OUR $0.16 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.16) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD A STRONG GAIN OF 1098 CONTRACTS ON OUR TWO EXCHANGES,; WE HAD HUGE SPECULATOR LIQUIDATION.

WE MUST HAVE HAD:

I) HUGE/ SPECULATOR SHORT LIQUIDATIONS ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 200,000 OZ QUEUE JUMP / // V) SMALL SIZED COMEX OI LOSS/(//CONSIDERABLE SPEC LIQUIDATION/)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: +919 ??

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTACTS for 6 days, total 6972 contracts: 34.86 million oz OR 6.972 MILLION OZ PER DAY. (1162 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 34.86 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 34.86 MILLION OZ///

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 546 WITH OUR $0.16 GAIN IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1481 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /SOME BANKER ADDITIONS A// HUGE SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 200,000 OZ QUEUE JUMP // .. WE HAD A HUGE SIZED GAIN OF 2027 OI CONTRACTS ON THE TWO EXCHANGES FOR 10.135 MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 169 NOTICE(S) FILED TODAY FOR 845,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 572 CONTRACTS TO 464,841 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:–266 CONTRACTS.

.

THE SMALL SIZED INCREASE IN COMEX OI CAME DESPITE OUR FALL IN PRICE OF $6.10//COMEX GOLD TRADING/THURSDAY / WE MUST HAVE HAD HUGE SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND /STRONG SPECULATOR SHORT COVERINGS//CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 8.401 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG JUMP OF 1100 OZ //NEW STANDING 12.373 TONNES

YET ALL OF..THIS HAPPENED WITH OUR STRONG FALL IN PRICE OF $6.10 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 1652 OI CONTRACTS 5.138 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1918 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 464,841

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1652 CONTRACTS WITH 572 CONTRACTS INCREASED AT THE COMEX AND 1080 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1652 CONTRACTS OR 5.138 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1080) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (572): TOTAL GAIN IN THE TWO EXCHANGES 1652 CONTRACTS. WE NO DOUBT HAD 1) STRONG SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 8.409 TONNES FOLLOWED BY TODAY’S QUEUE. JUMP OF 1100 oz. 3) ZERO LONG LIQUIDATION//// //.,4) SMALL SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

13,927 CONTRACTS OR 1,392,700 OZ OR 43.32 TONNES 6 TRADING DAY(S) AND THUS AVERAGING: 2321 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAY(S) IN TONNES: 43.32 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 43.32/3550 x 100% TONNES 1.23% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 43.32 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT., FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GOOD SIZED 546 CONTRACT OI TO 138,237 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1481 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 1481 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1481 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 546 CONTRACTS AND ADD TO THE 1481 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 2027 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 10.135 MILLION OZ

OCCURRED WITH OUR GOOD GAIN IN PRICE OF $0.16

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED UP 26.47 PTS OR 0.82% //Hang Sang CLOSED UP 507,63 OR 2.69% /The Nikkei closed UP 149.47 OR 0.53%. //Australia’s all ordinaires CLOSED UP 0.76% /Chinese yuan (ONSHORE) closed UP AT 6.9197//OFFSHORE CHINESE YUAN UP 6.9296// /Oil UP TO 85.13 dollars per barrel for WTI and BRENT AT 90.80 / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 572 CONTRACTS TO 465,107 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR FALL IN PRICE OF $6.10 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A SMALL SIZED EFP (1080 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1080 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :1080 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1080 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED SIZED TOTAL OF 1652 CONTRACTS IN THAT 838 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 572 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $6.10. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING SEPT (12.3730),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 12.3730 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $6.10) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 1652 CONTRACTS // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS COVERED SOME OF THEIR POSITIONS////// WE HAVE REGISTERED A FAIR SIZED GAIN OF 5.138 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR SEPT. (12.3730 TONNES)…

WE HAD -266 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 235 CONTRACTS OR 23,500 OZ OR 0.7307 TONNES

Estimated gold volume 156,341/// poor/

final gold volumes/yesterday 194,107/ poor

INITIAL STANDINGS FOR SEPT ’22 COMEX GOLD //SEPT 9

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 86,827.014 oz Brinks HSBC |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 1327 notice(s) 132700 OZ 4.1275 TONNES |

| No of oz to be served (notices) | 187 contracts 18,700 oz 0.5816TONNES |

| Total monthly oz gold served (contracts) so far this month | 3791 notices 379,100 OZ 11.7916 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

2 customer withdrawals:

i) Out of Brinks 80,292.980 oz

ii) Out of HSBC: 6534.034 oz

total: 86,827.014 oz

total in tonnes: 2.7 tonnes

Adjustments: 1

HSBC: 9457.799 oz dealer to customer

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPT.

For the front month of SEPT we have an oi of 1514 contracts having LOST 259 contracts .

We had 270 notices filed on THURSDAY so we gained A STRONG 11 contracts or an additional 1100 oz

will stand for gold in this very non active delivery month of September.

October LOST 354 contracts DOWN to 42,022

November GAINED 71 contracts to stand at 77

December LOST 1249 contracts DOWN to 378,494.

We had 1327 notice(s) filed today for 132,700 oz FOR THE SEPT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1327 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 940 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2022. contract month,

we take the total number of notices filed so far for the month (3791) x 100 oz , to which we add the difference between the open interest for the front month of (SEPT 1514 CONTRACTS ) minus the number of notices served upon today 1327 x 100 oz per contract equals 397,800 OZ OR 12.3730 TONNES the number of TONNES standing in this NON active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month:

No of notices filed so far (3791) x 100 oz+ (1514) OI for the front month minus the number of notices served upon today (1327} x 100 oz} which equals 397,800 oz standing OR 12.3730 TONNES in this NON active delivery month of SEPTEMBER.

TOTAL COMEX GOLD STANDING: 12.3730 TONNES (A GREAT STANDING FOR A SEPT ( NON ACTIVE) DELIVERY MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,397,641.955 oz 74.574 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 27,422,651.143 OZ

TOTAL REGISTERED GOLD: 13,552,488.148 OZ (421.52 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 13,880,162.395 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 11,154,847. OZ (REG GOLD- PLEDGED GOLD) 346.96 tonnes//rapidly declining

END

SILVER/COMEX/SEPT 9

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 243,977.430 oz BRINKS JPMORGAN |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 169 CONTRACT(S) 845,000 OZ) |

| No of oz to be served (notices) | 150 contracts (750,000 oz) |

| Total monthly oz silver served (contracts) | 6156 contracts 30,780,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

total deposit: nil oz

JPMorgan has a total silver weight: 167.889 million oz/324.024million =51.81% of comex

Comex withdrawals:2

i) Out of Brinks 5018.900 oz

ii) Out of JPMorgan: 238,958.530 oz

total: 243,977.430 oz

adjustments: 1/dealer to customer

CNT: 282,381.800 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 45.991 MILLION OZ

TOTAL REG + ELIG. 324.024 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF SEPT OI: 319 CONTRACTS HAVING GAINED 1 CONTRACT. WE HAD

39 CONTRACTS SERVED ON THURSDAY SO WE GAINED 40 CONTRACTS OR AN ADDITIONAL

200,000 OZ WILL STAND FOR METAL IN THIS VERY ACTIVE MONTH OF SEPT.

WE WILL GAIN IN TOTAL SILVER STANDING EACH TRADING DAY UNTIL THE END OF THE MONTH

(CONTINUAL QUEUE JUMPING BY OUR BANKERS SEARCHING FOR SILVER METAL)

OCTOBER GAINED 16 CONTRACTS TO STAND AT 692 CONTACTS.

NOVEMBER GAINED 2 CONTRACTS TO STAND AT 14

DECEMBER SAW A GAIN OF 380 CONTRACTS DOWN TO 125,190

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 169 for 845,000 oz

Comex volumes:42,137// est. volume today// poor

Comex volume: confirmed yesterday: 55,307 contracts ( poor)

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 6156 x 5,000 oz = 30,780,000 oz

to which we add the difference between the open interest for the front month of SEPT(319) and the number of notices served upon today 169 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT./2022 contract month: 6,156 (notices served so far) x 5000 oz + OI for front month of SEPT (319) – number of notices served upon today (169) x 5000 oz of silver standing for the SEPT contract month equates 31,530,000 oz. .

We have an inventory of 45.991 million oz of registered silver at the comex so Sept delivery of 31.530 MILLION OZ represents 68.55% of that category of silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:49,341// est. volume today// poor

Comex volume: confirmed yesterday: 51,749 contracts ( poor)

END

GLD AND SLV INVENTORY LEVELS

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 968.15 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

AUGUST 10//WITH GOLD UP $2.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES

AUGUST 9/WITH GOLD UP $6.70: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES.

AUGUST 8/WITH GOLD UP $13.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FORM THE GLD//INVENTORY RESTS AT 999.16 TONNES

AUGUST 5/WITH GOLD DOWN $14.25: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .33 TONNES FROM THE GLD////INVENTORY RESTS AT 1000.32 TONNES

AUGUST 4 WITH GOLD UP $29.00 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES FROM THE GLD///INVENTORY REST AT 1000.65 TONNES

AUGUST 2/WITH GOLD UP $3.70; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD//INVENTORY RESTS AT 1002.97 TONNES//

AUGUST 1/WITH GOLD UP $5.75: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1005.87 TONNES

GLD INVENTORY: 966.64 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTO THE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 10/WITH SILVER UP 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 9/WITH SILVER DOWN 25 CENTS TODAY: TWO CHANGES IN SILVER INVENTORY AT THE SLV: FIRST: A DEPOSIT OF 461,000 OZ INTO THE SLV AND THEN A WITHDRAWAL OF 1.014 MILLION OZ..//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 8/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 5/WITH SILVER DOWN 28 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 922,000 OZ FROM THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 4 WITH SILVER UP 21 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 527,000 OZ FROM THE SLV////INVENTORY RESTS AT 486.634 MILLION OZ

AUGUST 2/WITH SILVER DOWN 21 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.504 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.161 MILLION OZ//

AUGUST 1/WITH SILVER UP 17 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE GLD: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 483.657 MILLION OZ//

CLOSING INVENTORY 467.557 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

The Fed Is About To Start Losing Money; What Does That Mean?

FRIDAY, SEP 09, 2022 – 08:50 AM

Authored by Michael Maharrey via SchiffGold.com,

What happens if the Federal Reserve loses money?

The Fed typically earns interest income from all of the bonds it holds on its balance sheet. It also collects fees for services that it provides. Most of any Fed operating profit is remitted to the US Treasury under federal law. That money becomes part of the federal government’s operating budget. In other words, the central bank serves as a revenue source for Uncle Sam.

In 2021, the central bank reported a net income of $107.8 billion and sent $107.4 billion to the US Treasury.

But it is possible for the Fed to lose money. In fact, it will likely do so in 2023. If so, it would be the first operating loss since 1915.

While the Federal Reserve earns significant income from its massive balance sheet, it also has expenses. It pays commercial banks interest on reserve balances held at the central bank, along with interest on reverse repurchase agreements. The Fed also sends dividend payments to Fed member banks, and it has its own operating expenses.

As the Fed raises interest rates, it increases its own interest expenses. The interest generated by the bonds held on the balance sheet remains unchanged. Meanwhile, quantitative tightening decreases its balance sheet and reduces its interest income. The recent rapid increase in rates puts the central bank in a position that will likely mean an operating loss in the next fiscal year.

That raises a question: how will this loss affect the federal budget?

The most obvious impact is the US government will see a reduction in revenue which will increase the federal budget deficit.

Given that the US government reaps the benefit of central bank profits, you might think it would also bear the burden of a loss.

Not exactly.

We live in a world where the Federal Reserve gets to make its own accounting rules. And according to its own accounting rules, any net loss magically turns into a “deferred asset.”

[I]n the unlikely scenario in which realized losses were sufficiently large enough to result in an overall net income loss for the Reserve Banks, the Federal Reserve would still meet its financial obligations to cover operating expenses. In that case, remittances to the Treasury would be suspended and a deferred asset would be recorded on the Federal Reserve’s balance sheet.”

Under this scheme, an operating loss will not reduce the Fed’s reported capital or surplus. The bank will simply create an “asset” on its balance sheet out of thin air equal to the loss and business will continue as usual. (This is kind of like money printing.) Once the Fed returns to profitability, it will retain profits in order to reduce the amount of this imaginary asset. In other words, the US government won’t get any money from the Fed until this “asset” is zeroed out. At that point, the Fed will resume sending money to the federal government.

In effect, this means the US government will see a reduction in revenue resulting in a budget deficit higher than it otherwise would have been.

The American Institute for Economic Research sums it up.

Simple accounting logic suggests that if the federal budget deficit is reduced when the Fed earns revenues in excess of expenses and remits these profits to the US Treasury, Fed losses should increase the reported federal budget deficit. This is especially true since Federal Reserve System losses now include the hundreds of millions of dollars of off-budget funding it is required to transfer to run the Consumer Financial Protection Bureau. If the current accounting rules remain unchallenged, the Congress could pass new legislation requiring the Federal Reserve to fund any number of activities off-budget without any impact on the reported federal budget deficit.”

This isn’t good news for a government already buried in debt and running massive budget deficits month after month. It means the US government will have to borrow even more money that the Fed will ultimately have to monetize.

This is yet another reason the Fed will find it very difficult to reduce inflation. Raising rates and shrinking its balance sheet to tame the inflation dragon means more pressure on the central bank to prop up the borrow and spend economy. This necessitates lower interest rates and quantitative easing.

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

GOLD/SILVER

END

3.Chris Powell of GATA provides to us very important physical commentaries

Your weekend reading material and a must read

(Alasdair Macleod)

Alasdair Macleod: An Asian Bretton Woods may be on the way

Submitted by admin on Thu, 2022-09-08 12:08Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, September 8, 2022

The financial war between Russia with China’s tacit backing on one side, and America and her NATO allies on the other has escalated rapidly. It appears that President Putin was thinking several steps ahead when he launched Russia’s attack on Ukraine.

We have seen sanctions fail. We have seen Russia achieve record export surpluses. We have seen the rouble become the strongest currency on the foreign exchanges.

We are seeing the West enter a new round of European monetary inflation to pay everyone’s energy bills. The euro, yen, and sterling are already collapsing — the dollar will be next. From Putin’s point of view, so far, so good.

Russia has progressed her power over Asian nations, including populous India and Iran. She has persuaded Middle Eastern oil and gas producers that their future lies with Asian markets, not Europe. She is subsidising Asia’s industrial revolution with discounted energy. Thanks to the West’s sanctions, Russia is on its way to confirming Halford Mackinder’s predictions made over a century ago that Russia is the true geopolitical centre of the world.

There is one piece in Putin’s jigsaw yet to be put in place: a new currency system to protect Russia and her allies from an approaching Western monetary crisis. This article argues that under cover of the West’s geopolitical ineptitude, Putin is now assembling a new gold-backed multi-currency system by combining plans for a new Asian trade currency with his new Moscow World Standard for gold. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/an-asian-bretton-woods?gmrefcode=gata

END

With the death of Queen Elizabeth II, what happens to Canadian bills and coins?

Submitted by admin on Fri, 2022-09-09 10:17 Section: Daily Dispatches

From The Canadian Press, Toronto

Thursday, September 8, 2022

OTTAWA — Canadians are used to seeing Queen Elizabeth II on their money, but that could change following the death of the longest-serving British monarch and Canadian head of state.

However, the Bank of Canada, which produces Canada’s paper bills, said changes likely won’t be seen immediately.

The current $20 bank note featuring the Queen, is intended to circulate for years to come, the central bank said, and there is no legislative requirement to change the design within a prescribed period when the monarch changes. New bank notes, including the portrait subject, are approved by the finance minister.

One observer says he doesn’t know if Canadians will ultimately see King Charles III, as he’s now known, on our bills.

“I don’t know if we will, since there is only the $20 that has the Queen on it, and Canadians may want to change this,” said University of Toronto business history professor Dimitry Anastakis.

But the government will likely keep the queen on the $20 bill for a while before any changes are made, he noted.

The Royal Canadian Mint, which manufactures and distributes Canada’s coins, said the government has exclusive jurisdiction over their design.

… For the remainder of the report:

END

With ascension of King Charles III, the look of British currency will change

Submitted by admin on Fri, 2022-09-09 10:00Section: Daily Dispatches

By Anthony Grant

New York Sun

Friday, September 8, 2022

The face of King Charles III instead of that of Queen Elizabeth II will begin to be seen on new British coins and banknotes issued in the United Kingdom and Commonwealth countries beyond the British Isles. These include Canada, Australia, New Zealand, British territories in the Caribbean, Gibraltar, the Falkland Islands, and the English Channel islands of Jersey, Guernsey, and the Isle of Man.

Exactly when Britons will notice these changes is not immediately clear, and existing currency with a rendition of Queen Elizabeth will remain in circulation as legal tender, but the Bank of England will likely not wait long to begin effecting the change. There are 4 1/2 billion pound notes in circulation, adding up to about $93 billion. These will have to be replaced, a process likely to be carried out over several years.

During the short reign of King Edward VIII, new coins with his likeness were struck but the monarch abdicated the throne before they could be put into circulation.

New Royal Mail postage stamps will also bear the king’s image or profile, but according to British media reports the cypher of Queen Elizabeth, ER, that now adorns Royal Mail post boxes will remain. The Guardian reported that some post boxes still bear the cypher GR, that of King George VI, who preceded Elizabeth II on the throne.

The ER cypher also appears on police helmets. Those may start to be modified in consideration of the new monarch. The royal cypher EIIR that is emblazoned on flags that fly on official buildings and sometimes on vessels of the Royal Navy is likely to change. …

END

4. OTHER GOLD/SILVER COMMENTARIES

ANDREW MAGUIRE/KINESIS//EPISODE 90

-END-

.

end

5.OTHER COMMODITIES: COOPER

We now have a copper shortage

(Zaremba/OilPrice.com)

The Energy Transition Could Be Derailed By A Looming Copper Shortage

FRIDAY, SEP 09, 2022 – 06:30 AM

By Haley Zaremba of OilPrice.com

“Think of copper as a common carrier, so to speak, of decarbonization. It is literally the wiring that connects the present to the future,” writes Nathaniel Bullard, BloombergNEF’s Chief Content Officer. While many of us imagine renewable energies to be just that – infinitely renewable, with no use of finite resources – the reality is that solar planes, wind turbines, energy transmission infrastructure, batteries for energy storage, and motors for your electric cars and electric bicycles all rely on metals that are not infinitely sourceable. Much lip service has been paid to the extraction and exploitation of lithium to power electric vehicle batteries, but one could argue that copper is even more central to – and therefore potentially threatened by – a large-scale green energy transition.

The reverse is also true – a looming copper shortage threatens to completely derail the clean energy transition, and by extension, climate pledges across the world. According to a recent report from S&P Platts, if copper shortfalls follow projected trends, climate goals will be “short-circuited and remain out of reach.”

Copper is particularly effective in a wide range of low-carbon alternatives because of its relatively high electrical conductivity and low reactivity. It’s not that traditional energy production and transmission and gas-powered vehicles don’t use copper in their manufacturing – it’s just that renewables and electric vehicles require a whole lot more of it. “An EV requires 2.5 times as much copper as an internal combustion engine vehicle,” reports CNBC. “Meanwhile, solar and offshore wind need two times and five times, respectively, more copper per megawatt of installed capacity than power generated using natural gas or coal.”

Copper production is already struggling to keep up with booming demand, and S&P projects that current levels of demand will nearly double by the year 2035, climbing to a whopping 50 million metric tons. That figure will climb to more than 53 million metric tons by 2050, which amounts to “more than all the copper consumed in the world between 1900 and 2021.” BloombergNEF’s projections are a bit more conservative, but still striking, finding that copper demand will increase by over 50% by 2040. Worryingly, the same report projects that primary copper production can increase by just 16% in the same time period.

This damning differential does not necessarily mean, however, that the world will be “structurally short of copper” for the next 18 years. It is likely that the economics of the copper deficit will suppress demand due to prohibitively high prices, ultimately helping to balance out the supply deficit. “That would happen, however, at the expense of expansions of clean power and electrified transportation,” reports Bloomberg.

What the world needs – today’s world as well as the future, increasingly climate-threatened one – is a bigger emphasis and greater expenditures on copper discovery and exploration. Considering copper’s central role in the essential public project of climate change mitigation and adaptation, the public sector should be as active as the private sector in facilitating more, cheaper, and lasting primary copper production. This should be paired with robust copper recycling and recovery programs.

Secondary copper production – essentially, recycling copper – is already a strong and well developed economic sector, completely filling the “4.6 million-ton-per-year gap between primary production and demand” with industrial copper scrap. But there is a huge opportunity – and indeed, imperative – to improve copper scrap collection from consumers. Currently, the copper collection rate from consumer and electronic goods stands at just 53%. As copper becomes increasingly scarce and increasingly expensive, the economics of better copper recovery will likely encourage far greater recovery in this respect, making copper not only better suited to support renewable, but more renewable itself.

end

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.9197

OFFSHORE YUAN: 6.9290

HANG SENG CLOSED UP 507,63 PTS OR 2.69%

2. Nikkei closed UP 149.47 OR 0.53%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 108.92/Euro RISES TO 1.0051

3b Japan 10 YR bond yield: RISES TO. +.244/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 143.38/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP -// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.707%/Italian 10 Yr bond yield RISES to 3.99% /SPAIN 10 YR BOND YIELD RISES TO 2.85%…

3i Greek 10 year bond yield RISES TO 4.22//

3j Gold at $1720.25 silver at: 18.68 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 42/100 roubles/dollar; ROUBLE AT 60.32//

3m oil into the 85 dollar handle for WTI and 90 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 142.38DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 9605– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9652well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.264 DOWN 3 BASIS PTS

USA 30 YR BOND YIELD: 3.440 DOWN 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,24

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures, Euro, Oil All Jump As Dollar Tumbles

FRIDAY, SEP 09, 2022 – 07:56 AM

US equity futures, European stocks, and pretty much all risk assets rose on Friday morning as the dollar finally stumbled, dropping by the most in a month to the lowest level in Septemember, after hitting an all time high just two days earlier.

S&P 500 and Nasdaq 100 futures gained more than 0.8% at 730am ET. Europe’s Stoxx 600 Index jumped as miners rallied on optimism over Chinese demand, while banks surged following the European Central Bank’s record rate hike. That’s even as BofA said an “appalling” mood fueled a $11 billion US stock exodus in the week to Sept. 7. The yen headed for its best day in a month as Japanese officials and BOJ governor Kuroda gave the strongest hint yet at possible direct market intervention as a response to weakness in the currency. Oil and cryptos jumped.

In premarket trading, DocuSign jumped 17% in premarket trading, after the e- signature company reported second-quarter results that beat expectations and raised its full-year billings forecast. Digital Media Solutions soared 73% in premarket trading after receiving a non-binding “go private” proposal from Prism Data for $2.50/share in cash, representing ~95% premium to last close. Other notable premarket movers:

- Zscaler (ZS US) was up 13% in premarket trading, after the security software company reported fourth-quarter results that beat expectations and gave an outlook that is seen as strong.

- Digital World Acquisition (DWAC US), the blank-check firm merging with Trump Media & Technology Group, rises 7.1% premarket, on course for a third day of gains.

- The shares have had a volatile week, falling 11% on Tuesday, amid uncertainty over a vote to extend the deadline to complete the Trump deal.

- Marathon Digital (MARA US) and Riot Blockchain (RIOT US) lead cryptocurrency-exposed stocks higher in premarket trading as Bitcoin rises the most in more than a month, breaching the closely watched $20,000 level. MARA +10%, RIOT +8%.

- RH (RH US) was little-changed in postmarket trading. Analysts were torn on the luxury home furnishings retailer’s results, noting that while the company beat expectations, it lowered its full-year forecast.

Global stocks are on course for their first weekly advance in four, a small measure of respite from the bear-market omens circling markets due to monetary tightening, energy woes and China’s growth slowdown.

“The market has been extraordinarily focused on the actions of the ECB and Fed as they try to bring inflation under control,” said Sebastien Galy, senior macro strategist at Nordea Asset Management. “Eventually this will change and the investment horizon will lengthen considerably. For now though, the market has good reasons not to. Inflation saps consumer confidence and overtightening could send the European and US economies into a recession.”

Speaking at a conference, Powell said “we need to act now, forthrightly, strongly as we have been doing” and added that “my colleagues and I are strongly committed to this project and will keep at it.”

In contrast with the buoyant mood in equity markets Friday, Bank of America Corp. strategists flagged that investors are rushing out of US stocks as the likelihood of an economic downturn increases amid a myriad of risks. US stock funds posted outflows of $10.9 billion in the week to Sept. 7, according to EPFR Global data cited by the bank, with the biggest exodus in 11 weeks led by technology stocks.

In Europe, nat gas prices eased as the region’s energy ministers gathered for a summit to draw up plans to fix an unprecedented crisis that threatens to undermine the broader economy. Expect the news to be a major letdown unless somehow Brussels figured out how to print commodities. The euro touched the highest level in three weeks after the ECB raised rates 75 basis points Thursday. Bets the Federal Reserve will hike by the same margin when it meets later this month increased after chair Jerome Powell reiterated the Fed is determined to curb price pressures.

Elsewhere in Europe, stocks rallied as all sectors trade in the green. Euro Stoxx 50 climbs 1.9%. Miners, banks and autos are the strongest-performing sectors. European miners soared, significantly outperforming the Stoxx Europe 600, as iron-ore and base-metals prices rose on improving sentiment surrounding the Chinese market. Here are some of the biggest European movers today:

- Deutsche Telekom shares gain as much as 3.1% after its unit T-Mobile US embarks on a buyback program of as much as $14b of shares, which Goldman Sachs sees as a positive catalyst for the telecom group

- Zealand Pharma shares rise as much as 8.7% after Morgan Stanley initiated coverage with overweight rating on near-term catalysts and the biotech’s rich pipeline

- Synlab shares rise as much as 7% after Berenberg initiated coverage at buy, saying the shares should benefit as investors start to focus on the potential for the diagnostics firm’s core business

- Rubis climbs as much as 8.9%, the most intraday since March, after the French oil and gas distributor reported a jumped in 1H profit helped by growth in its Caribbean operations

- TI Fluid Systems shares rise as much as 7.6% after Jefferies upgraded them to buy, saying concerns on the auto parts maker’s outlook are now sufficiently priced in

- Gear4Music shares plummet as much as 23% after the online retailer said summer trading was hit by the cost-of-living crisis and unusually hot weather. Peel Hunt sees a challenging winter ahead

- Computacenter shares fall as much as 12%, with analysts saying the IT services firm missed profit estimates in 1H amid continued supply constraints and tough comparisons

- Immobel shares drop as much as 5.1% after KBC downgraded the real estate developer to accumulate from buy and reduced the PT to a Street-low

- Melrose shares drop as much as 6.1% in a second day of declines after the company said it will spin off two units. Analysts said the change in strategy raises questions.

Earlier in the session, Asian equities advanced, poised to wipe out a weekly loss, as China’s consumer inflation came in lower than expected and the dollar rally showed signs of easing. The MSCI Asia Pacific Index advanced as much as 1.7%, with a materials sub-gauge set for its best day since March –climbing almost 3% — amid a rally in metals due to supply concerns. Stock gauges in Hong Kong led gains in the region as developer stocks climbed on speculation of more easing of home-purchase restrictions. Mainland Chinese shares had their best day in almost a month as August data showed an unexpected moderation in prices, giving the country’s central bank room to stay accommodative. Markets in South Korea and Taiwan were closed for holidays. A dollar gauge edged lower, helping to lift sentiment, as comments from Federal Reserve Chair Jerome Powell that hardened expectations of another jumbo rate hike appeared to have been largely priced in.

Asian equities fell to a May 2020 low earlier this week as the dollar’s strength put pressure on capital flows amid rising inflation. Meanwhile, China’s continued lockdowns have weighed on supply chains and investor sentiment, and the country is stepping up defenses ahead of a key Communist Party meeting with further restrictions on internal travel. “Growth, inflation and yields have been driving the markets since the beginning of the year and there is still no consensus,” Sanford C. Bernstein strategists including Rupal Agarwal wrote in a note. A global slowdown or recession has historically worked in favor of defensive styles such as high quality, high yield and low volatility in Asia, they added.

Japanese equities advanced, driven by gains in telecoms and service providers, after a rally in US peers overnight and as the yen gained against the dollar. The Topix rose 0.4% to close 1,965.53, while the Nikkei advanced 0.5% to 28,214.75. Volumes were above the 30-day averages after special quotation settlement for futures and options. The yen strengthened as much as 1.1% against the greenback in afternoon trading. Nippon Telegraph & Telephone Corp. contributed the most to the Topix gain, increasing 0.7%. Out of 2,169 shares in the index, 1,354 rose and 684 fell, while 131 were unchanged

Australian stocks advanced, boosted by banks and miners. The S&P/ASX 200 index increased 0.7% to close at 6,894.20, making a weekly gain of 1%, as banks and mining shares rose. Mineral Resources led lithium shares higher after responding to a media report that the company is considering a spinoff of its lithium mining and processing operations arm, as well as a possible US listing. In New Zealand, the S&P/NZX 50 index rose 0.7% to 11,757.77.

In FX, the Bloomberg Dollar Spot Index fell to its lowest level this month as the greenback weakened against all of its G10 peers, while the pound, euro, yen and yuan all rallied against the greenback. Risk-sensitive currencies advanced most, led by Norway’s krone which rose by as much as 2%. The euro rallied by as much as 1.1% to trade around $1.01 for the first time since mid-August. Italian bonds tumbled, snapping the BTP-bund spread wider as money markets cranked up ECB hike bets after Bloomberg reported policy makers are prepared to tighten another 75bps next month, according to people familiar with the debate. The yen rebounded as traders mulled comments from Bank of Japan Governor Haruhiko Kuroda on the currency’s decline amid a broad dollar selloff. The dollar-yen pair fell 1.3% to around the 142.20 level, after climbing for four straight sessions. Kuroda held a meeting with Prime Minister Fumio Kishida in a sign of the nation’s heightened alert levels. The Australian dollar surged the most in a month as the greenback weakens and a rally in equities boosts risk-sensitive currencies

In rates, US Treasuries trimmed their retreat, with the policy-sensitive two-year yield still near the highest since 2007. Treasury futures push higher over early US session as S&P 500 futures advance, taking yields richer by up to 7bp across intermediates which lead the rally. The Advance followed wider bull-flattening move seen across UK curve as gilts pare a portion of Thursday’s losses. 10-year TSY yields were around 3.26%, richer by 6bp on the day although lagging gilts where yields drop as much as 9bp out to 10s; in Treasuries, intermediate-led gains richen 2s7s30s fly by 5bp. Bunds 10-year yield is down 1.5bps to 1.73%. Peripheral spreads widen to Germany with 10y BTP/Bund adding 2.2bps to 227.3bps.

Oil futures traded at session high, jumping 1.5% to below $85; gold jumped ~$18 to $1,727. Most base metals trade in the green; LME nickel rises 4.4%, outperforming peers. Bitcoin extended gains, rising 6.7% just shy of the $20,000-level, rising the most in more than a month.

Looking to To the day ahead now, and EU energy ministers will be meeting in Brussels to discuss emergency measures to deal with high energy prices. Otherwise, data releases include French industrial production for July and Canada’s employment report for August. Finally, central bank speakers includes ECB President Lagarde, and the Fed’s Evans, Waller and George.

Market Snapshot

- S&P 500 futures up 0.8% to 4,035.75

- STOXX Europe 600 up 1.4% to 419.91

- MXAP up 1.6% to 154.48

- MXAPJ up 1.6% to 506.33

- Nikkei up 0.5% to 28,214.75

- Topix up 0.4% to 1,965.53

- Hang Seng Index up 2.7% to 19,362.25

- Shanghai Composite up 0.8% to 3,262.05

- Sensex up 0.2% to 59,834.09

- Australia S&P/ASX 200 up 0.7% to 6,894.18

- Kospi up 0.3% to 2,384.28

- German 10Y yield little changed at 1.75%

- Euro up 1.0% to $1.0100

- Gold spot up 1.2% to $1,728.41

- U.S. Dollar Index down 1.12% to 108.47

Top Overnight News from Bloomberg

- The EU is throwing together a series of radical plans to tame runaway energy prices and keep the lights on across the continent, but governments across the region are going to need to find common ground and fast

- The ECB will continue raising interest rates until it reaches its inflation goal, according to Governing Council Member Klaas Knot. Governing Council Member Bostjan Vasle said the ECB will continue the strong normalization of monetary policy with more interest-rate hikes, while Peter Kazimir said euro-zone inflation is “unacceptably high” and sees more hikes in the near future to get inflation under control. Bank of France Governor Francois Villeroy de Galhau said the ECB must be “orderly and determined” with rate increases after hiking by a record 75 basis points

- Japanese officials sound increasingly alarmed over the yen’s weakness, and while intervention is not imminent, the market takes notice. The pair’s volatility skew turns bearish the dollar this week at the front-end yet topside trades better bid further out; this suggests that traders see risk of a yen rebound, but unilateral intervention won’t have a lasting effect as long as monetary policy divergence between the Fed and the BOJ remains in place

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks followed suit to the gains on Wall St although the upside was capped after recent global central bank activity including a 75bps rate hike by the ECB and Fed Chair Powell’s hawkish reiterations. ASX 200 was led by the mining-related sectors although advances were limited by weakness in defensives. Nikkei 225 extended on gains above the 28k level but with upside capped amid currency-related jawboning. Hang Seng and Shanghai Comp were also lifted with property and tech stocks spearheading the outperformance in Hong Kong owing to supportive policy-related headlines, while the mainland was somewhat contained in comparison after softer-than-expected inflation data from China and ahead of the long weekend with markets shut on Monday for the Mid-Autumn Festival.

Top Asian News

- US is considering an order to screen US investment in tech in China and elsewhere, according to WSJ.

- US Treasury Secretary Yellen said President Biden continues to consider tariff relief on Chinese imports and wants to make sure the decision is good for Americans, while she added that it is important to take a tough stance on China due to its economic practices and national security threat, according to Reuters.

- US reportedly relaxed Huawei curbs to counter China’s push on tech standards with the Commerce Department issuing a new rule to permit sharing of certain ‘low-level’ technologies and software, according to SCMP.

- BoJ Governor Kuroda said he met with PM Kishida to explain domestic and overseas economic developments and markets, but noted there was no specific request from PM Kishida on the economy or markets. Kuroda said hediscussed FX moves with Kishida and noted that rapid FX moves are undesirable and heighten uncertainty, as well as make it difficult for companies to do business, according to Reuters.

- Japanese Finance Minister Suzuki said they are to tap JPY 3.5tln in budget reserves to speedily deliver measures against the negative impact of price hikes, while he added that sharp FX moves are undesirable and won’t rule out any options on FX, according to Reuters.

- Japanese Chief Cabinet Secretary Matsuno said he is concerned about abrupt FX moves and noted that speculation is a factor behind recent moves, while he added that the strong USD is affecting other currencies, not just the JPY, according to Reuters. Matsuno said watching FX carefully, ready to take necessary steps if current FX moves continue, without ruling out options; recent JPY moves show excessive volatility

European bourses trade firmer across the board following constructive leads from APAC and Wall Street, with the softer-than-expected Chinese inflation data overnight also lifting spirits. European sectors are in the green but portray a clear anti-defensive bias – Utilities, Healthcare, Food & Beverages, Media, and Personal Care reside at the bottom of the bunch. Stateside, US equity futures are also higher across the board, with the tech-laden NQ leading the charge

Top European News

- ECB’s Kazimir said discussion on what levels of rate the ECB aims to reach is premature; priority is to continue fiercely with normalisation of monetary policy, via Reuters.

- ECB’s Knot said ECB has sent a forceful signal with rate rise; sees big risks of second-round effects, via Bloomberg.

- ECB’s Villeroy said half of the current inflation is not linked to energy or agricultural prices; says inflation should be brought back to around 2% by 2024; earlier we act the easier it is to achieve results, via Reuters. Villeroy added that neutral can be estimated in the Euro Area at below or close to 2% according to him, should not speculate on the size of the next rate move – “we did not create a jumbo habit”.

- ECB is said to be ramping up scrutiny of banks’ readiness for a gas halt by Russia, according to Bloomberg sources.

FX

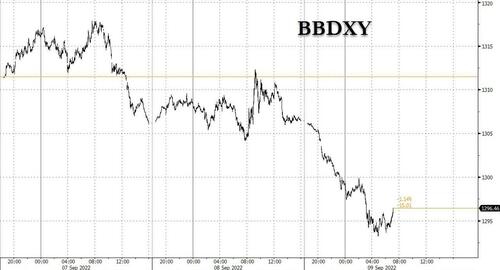

- DXY suffers from a large fall amid risk appetite, ECB sources yesterday and Japanese verbal intervention, with the index back around 108.50 from a 109.54 peak.

- The EUR is probing 1.0100 from a sub-0.9900 midweek trough and pulling away from decent option expiry interest below.

- The AUD stands as the outperformer amid renewed risk appetite and the revival of base metals.

Fixed Income

- UK Gilts have rebounded to extend well beyond prior session peaks to almost 106.00

- Bunds are back around par within extended 143.82-142.46 extremes

- US Treasuries are near the top of a 116-07+/115-22 range.

Commodities

- WTI and Brent front-month futures have been climbing since the start of the APAC session as a function of the declining Dollar and overall risk appetite in the market.

- Spot gold is firmer as the DXY losses further ground, with the yellow metal topping yesterday’s high as it eyes its 50 DMA at USD 1,744.12/oz.

- Base metals are bolstered by the softer Chinese inflation metrics – which also lowers the chances of further state intervention.

- Indian food secretary said rice production could drop due to droughts; output could drop by 7-8mln tonnes, via Reuters

- Black Sea grain deal is being fulfilled badly, according to the Russian Foreign Ministry, its extension will depend on implementation, via Ria.

US Event Calendar

- 10:00: July Wholesale Trade Sales MoM, est. 0.8%, prior 1.8%

- 10:00: July Wholesale Inventories MoM, est. 0.8%, prior 0.8%

- 12:00: 2Q US Household Change in Net Wor, prior -$544b

Central Banks

- 10:00: Fed’s Evans Discusses Careers in Economics

- 12:00: Fed’s Waller Discusses Economic Outlook

- 12:00: Fed’s George Discusses the Economic Outlook

DB’s Jim Reid concludes the overnight wrap

Markets struggled for direction yesterday as it dawned on investors that central banks still aren’t ready to slow down their rate hikes just yet. First, we had the ECB who hiked by 75bps for the first time in their history and signalled that further hikes were still to come. Then we had a Bloomberg report suggesting that ECB officials were prepared to move by the same amount again in October. And finally in the US, Fed Chair Powell delivered remarks that cemented expectations that the Fed are set to hike by 75bps for a third consecutive meeting this month. That combination of hawkish developments meant that sovereign bonds struggled on both sides of the Atlantic, with a fresh surge in real yields that left the 5yr real Treasury yield at a post-2019 high of 0.95%.

Looking at the ECB decision in more detail, the Governing Council decided to take their main rates up by 75bps as expected by the consensus, leaving the deposit rate at 0.75% and the main refinancing rate at 1.25%. A number of details also tilted in a hawkish direction, including their statement that they expected “to raise interest rates further to dampen demand and guard against the risk of a persistent upward shift in inflation expectations.” We even got some detail from Lagarde on what they meant when they said there’d be “several” future hikes, which was that it meant “probably more than two, including this one, but it’s also probably also going to be less than five.” Furthermore, they upgraded their inflation forecasts yet again, now seeing 2023 inflation +5.5% (vs. +3.5% in June), and 2024 inflation at +2.3% (vs. +2.1% in June), so still above their +2.0% target even in a couple of years. They also significantly downgraded growth in 2023, now expecting +0.9% (vs. +2.1% in June), and said that they expected the economy “to stagnate later in the year and in the first quarter of 2023.”

Here at DB, our own European economists have now shifted their view for the next meting in October, and now expect another 75bps hike. They write that the guidance from President Lagarde that rates are “far away” from appropriate levels for getting inflation back to target underscores the ECB’s insensitivity to the growth headwinds and their focus on bringing inflation down. They maintain their 2.5% terminal rate forecast for the deposit rate, but the timing for that has moved forward to March 2023, with that 75bp hike in October being followed by a 50bp move in December, and then 25bp moves in February and March. You can see their full reaction note here.

European sovereign bonds sold off following the decision, with yields on 10yr bunds (+13.8bps), OATs (+11.0bps) and BTPs (+10.8bps) all moving higher. That also followed an announcement that they were temporarily removing the 0% interest rate ceiling on the remuneration of government deposits, which they said would “prevent an abrupt outflow of deposits into the market”. Instead, the ceiling will be at the lower of either the Eurosystem’s deposit facility rate or the euro short-term rate, with the measure intended to remain in effect until 30 April 2023. Later, we then heard in a Bloomberg article that ECB officials were prepared to move by 75bps again in October, with the report further saying that Chief Economist Lane’s presentation “struck a much more hawkish tone than his latest speech”. All in all, investors took away a very hawkish message, with the rate priced in by the December meeting rising +21.2bps on the day to its highest level to date.

Today, attention will remain on Europe since we have the much-awaited meeting of EU energy ministers in Brussels. They’ll be discussing emergency measures to help with high energy prices, and we’re expecting a press conference at 14:30 Brussels time. We’ll have to see what happens, but the tone among policymakers has remained incredibly downbeat, with Belgian Prime Minister De Croo warning that “A few weeks like this and the European economy will just go into a full stop”. In the meantime, natural gas futures recovered +3.40% yesterday, which still leaves them at €221 per megawatt-hour, or more than quadruple their levels from a year ago. For those after more info on the situation, our research colleagues in Frankfurt published their latest gas supply monitor yesterday as well, where they update their scenarios for how fast German gas storages will be depleted, assuming zero gas flows from Russia to Germany. Their model shows that even with a 20% year-on-year reduction in total gas consumption, that would largely deplete the country’s gas storage by the end of the heating season. They also preview what to expect from today’s meeting (link here).

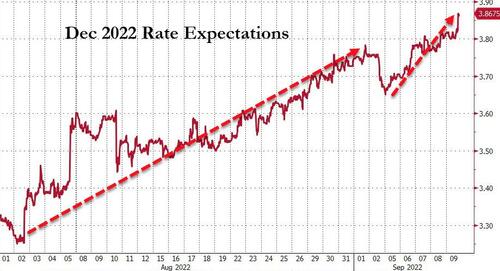

Otherwise yesterday, there were mounting expectations that the Fed would hike by 75bps again at their meeting on September 21, which would mark the third consecutive hike of that magnitude. That followed a further set of remarks from Fed Chair Powell, in which he stuck to his resolute tone on beating inflation, saying that “We need to act now, forthrightly, strong as we have been doing”. The FOMC are entering their blackout period tomorrow, so today is the last day ahead of the meeting we’ll hear from any of them, but Chicago Fed President Evans also said that they “could very well do 75 in September”. Fed funds futures responded accordingly, with +71.6bps worth of hikes now priced in for that meeting, and the rate priced in for December went up +4.3bps to 3.82%, which is the most hawkish market pricing to date.

The effects of the Fed’s hikes are being increasingly seen in the real economy, and yesterday we got data from Freddie Mac showing that the average 30-year mortgage rate hit a post-2008 high of 5.89%. However, there was a further round of decent data on the labour market, as the weekly initial jobless claims for the week ending September 3 fell to 2322k (vs. 235k expected). That’s their 4th consecutive weekly fall and brings them to their lowest level since May, so it’s becoming harder and harder to dismiss the better-than-expected data as just a blip. There have been some other tailwinds recently too, and daily data from the American Automobile Association is now showing that gasoline prices are down by just over a quarter from their peak in June, having fallen from $5.02/gallon back then to $3.75/gallon on Wednesday.

When it came to Treasuries, the hawkish rhetoric and more robust economic data helped yields rise further yesterday, with the 10yr yield up +5.4bps to 3.32%, although there’s been a partial pullback in Asia this morning, with yields down -2.3bps. The rise was driven by higher real yields, with those at shorter maturities hitting their highest levels since before the Covid-19 pandemic. For equities however, the day was marked by significant swings between gains and losses, before the S&P 500 eventually ended the day up +0.66%. It was a similar story in Europe too, where the STOXX 600 eventually ended the day up +0.50%. Looking forward, US stock futures are pointing to further gains today and contracts on the S&P 500 (+0.38%) and the NASDAQ 100 (+0.59%) have both risen.

Here in the UK, Prime Minister Truss outlined the government’s plan on consumer energy bills, with a new Energy Price Guarantee that will mean a typical UK household only pays up to an average of £2,500 a year on energy. This applies to all households, and once you take into account the existing £400 discount this winter, it means that average costs over the coming year will be roughly around where the current energy price cap stands, rather than going up to a new cap of £3,549 as had been previously planned. Against that backdrop, we also saw 10yr gilt yields (+11.3bps) rise to a new post-2011 high yesterday, although yesterday’s move was broadly in line with what we saw elsewhere in Europe following the ECB decision.

Overnight in Asia, equities are advancing this morning as they follow up the rise on Wall Street yesterday. The Hang Seng (+2.24%) is leading gains followed by the CSI (+1.26%), the Shanghai Composite (+0.84%) and the Nikkei (+0.55%). Elsewhere, markets in South Korea are closed for a holiday. Risk appetite was supported by Chinese inflation data that showed a slowing in the rate of both consumer and producer price growth, which offers the authorities more space to support the economy without sparking further inflation. Consumer prices were up by +2.5% in August (vs. +2.8% expected), while producer prices were up +2.3% (vs. +3.2% expected), and both readings were down on the previous month. Finally, the Japanese Yen has strengthened for the first time this week after BoJ Governor Kuroda commented that “The rapid weakening of the yen is undesirable”, gaining +0.94% against the US Dollar.

To the day ahead now, and EU energy ministers will be meeting in Brussels to discuss emergency measures to deal with high energy prices. Otherwise, data releases include French industrial production for July and Canada’s employment report for August. Finally, central bank speakers includes ECB President Lagarde, and the Fed’s Evans, Waller and George.

AND NOW NEWSQUAWK

Risk appetite is firmer across the board following constructive leads from APAC and Wall Street – Newsquawk US Market Open

FRIDAY, SEP 09, 2022 – 06:33 AM

- European bourses trade firmer across the board following constructive leads from APAC and Wall Street

- DXY suffers from a large fall amid risk appetite, ECB sources yesterday, and Japanese verbal intervention, with the index back around 108.50