by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1706.90 DOWN $22.85

SILVER: $19.54 DOWN $0.31

ACCESS MARKET:

GOLD $1702.30

SILVER: $19.35

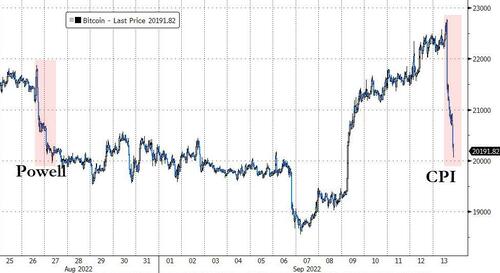

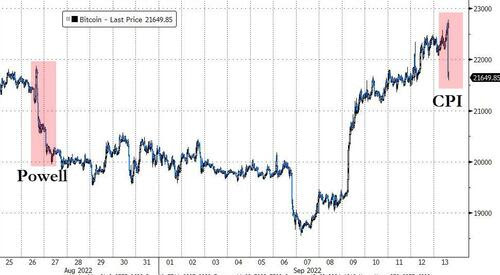

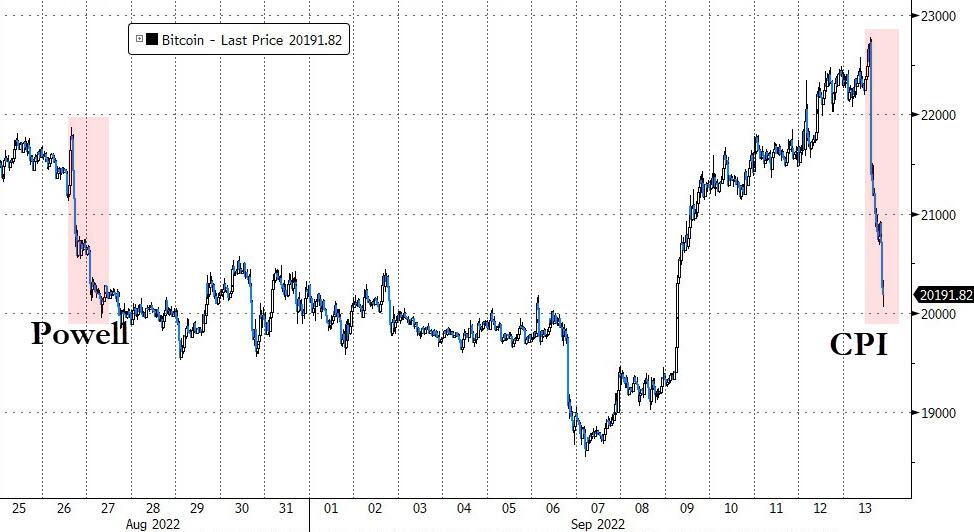

Bitcoin morning price: $22,552 UP 146

Bitcoin: afternoon price: $20,208 DOWN 2198

Platinum price closing DOWN $13.16 AT $893.69

Palladium price; closing DOWN $135.10 at $2133.70

END

DONATE

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

COMEX

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,728.100000000 USD

INTENT DATE: 09/12/2022 DELIVERY DATE: 09/14/2022

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 2

661 C JP MORGAN 4

690 C ABN AMRO 1

737 C ADVANTAGE 2

800 C MAREX SPEC 5

TOTAL: 7 7

MONTH TO DATE: 3,889

JPMorgan stopped: 4/7

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR SEPT CONTRACT:

7 NOTICES FOR 700 OZ //0.0217 TONNES

total notices so far: 3889 contracts for 388,900 oz (12.096 tonnes)

SILVER NOTICES: 129 NOTICES FILED FOR 645,000 OZ/

total number of notices filed so far this month 6384 : for 31,520,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $22.85

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: //// A WITHDRAWAL OF 1.73 TONNES FROM THE GLD/

INVENTORY RESTS AT 964.91 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $.31

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//: HUGE WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 465.899 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 1837 CONTRACTS TO 136,700. AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $1.04 GAIN IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $1.04) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD A SMALL GAIN OF 392 CONTRACTS ON OUR TWO EXCHANGES,; HOWEVER WE HAD HUGE SPECULATOR LIQUIDATION.(SHORT COVERING)

WE MUST HAVE HAD:

I) HUGE/ SPECULATOR SHORT LIQUIDATIONS ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 630,000 OZ QUEUE JUMP / // V) GIGANTIC SIZED COMEX OI LOSS/(//STRONG SPEC LIQUIDATION/)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -119

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTACTS for 8 days, total 9132 contracts: 45.166 million oz OR 5.639 MILLION OZ PER DAY. (1141 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 45.166 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 45.166 MILLION OZ///

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1837 DESPITE OUR $1.04 GAIN IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A GIGANTIC SIZED EFP ISSUANCE CONTRACTS: 2110 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /SOME BANKER ADDITIONS A// HUGE SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 630,000 OZ QUEUE JUMP // .. WE HAD A SMALL SIZED GAIN OF 273 OI CONTRACTS ON THE TWO EXCHANGES FOR 1.365MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 129 NOTICE(S) FILED TODAY FOR 645,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 817 CONTRACTS TO 465,639 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:+36 CONTRACTS.

.

THE SMALL SIZED DECREASE IN COMEX OI CAME DESPITE OUR RISE IN PRICE OF $12.30//COMEX GOLD TRADING/MONDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND /SOME SPECULATOR SHORT COVERINGS//CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 8.401 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 4300 OZ //NEW STANDING 13.6889 TONNES

YET ALL OF..THIS HAPPENED WITH OUR STRONG RISE IN PRICE OF $12.30 WITH RESPECT TO MONDAY’S TRADING

WE HAD A SMALL SIZED GAIN OF 1216 OI CONTRACTS 3.894 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1215 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 465,639

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1252 CONTRACTS WITH 817 CONTRACTS INCREASED AT THE COMEX AND 435 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1252 CONTRACTS OR 3.894 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (435) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (817): TOTAL GAIN IN THE TWO EXCHANGES 1252 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 8.409 TONNES FOLLOWED BY TODAY’S QUEUE. JUMP OF 4,300 oz. 3) ZERO LONG LIQUIDATION//// //.,4) SMALL SIZED COMEX OPEN INTEREST GAIN 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

15,849 CONTRACTS OR 1,584,900 OZ OR 49.29 TONNES 8 TRADING DAY(S) AND THUS AVERAGING: 1981 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES: 49.29 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 49.29/3550 x 100% TONNES 1.38% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 49.29 TONNES (MUCH LESS ISSUANCE THIS MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT., FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER,FELL FAIR BY A GIGANTIC SIZED 1837 CONTRACT OI TO 136,700 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 2110 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 2110 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2110 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1837 CONTRACTS AND ADD TO THE 2110 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED LOSS OF 273 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 1.365 MILLION OZ

OCCURRED WITH OUR GOOD GAIN IN PRICE OF $1.04

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 1.74 PTS OR .05% //Hang Sang CLOSED DOWN 35.39 PTS OR .18% /The Nikkei closed UP 72.52 OR 0.25%. //Australia’s all ordinaires CLOSED UP 0.63% /Chinese yuan (ONSHORE) closed UP AT 6.9257//OFFSHORE CHINESE YUAN DOWN 6.9264// /Oil UP TO 89.10 dollars per barrel for WTI and BRENT AT 95.36 / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING AOBVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 817 CONTRACTS TO 465,639 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS TINY COMEX INCREASE OCCURRED DESPITE OUR STRONG RISE IN PRICE OF $12.30 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A SMALL SIZED EFP (435 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 435 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :435 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 435 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED SIZED TOTAL OF 1252 CONTRACTS IN THAT 435 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 817 CONTRACTS..AND THIS SMALL GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR STRONG RISE IN PRICE OF GOLD $12.30. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING SEPT (13.698),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 13.698 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $12,30) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A SMALL SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 1252 CONTRACTS // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS COVERED SOME OF THEIR POSITIONS////// WE HAVE REGISTERED A SMALL SIZED GAIN OF 3.894 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR SEPT. (13.698 TONNES)…

WE HAD +34 CONTRACTS ADDED FROM COMEX TRADES. THESE WERE ADDED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1196 CONTRACTS OR 119600 OZ OR 3.720 TONNES

Estimated gold volume 241,696/// fair/

final gold volumes/yesterday 163,312/ poor

INITIAL STANDINGS FOR SEPT ’22 COMEX GOLD //SEPT 13

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 24,434.622 oz Brinks Loomis Manfra |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 14,230,170 oz Malca |

| No of oz served (contracts) today | 7 notice(s) 700 OZ 0.0217 TONNES |

| No of oz to be served (notices) | 515 contracts 51500 oz 1.6018TONNES |

| Total monthly oz gold served (contracts) so far this month | 3889 notices 388,900 OZ 12.096 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i) Into Malca: 14,230.170 oz

total deposits 14,230.170 oz

3 customer withdrawals:

i) Out of Brinks 16,589.910 oz

ii) Out of Loomis: 6430.200 oz (200 kilobars)

iii) Out of Manfra: 1414.512 oz (44 kilobars)

total: 24,434.622 oz

total in tonnes: 0.76 tonnes

Adjustments: 2 Brinks:

96,453.10 oz dealer to customer

and JPMorgan 42,342.84 oz dealer to customer

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPT.

For the front month of SEPT we have an oi of 522 contracts having LOST 45 contracts .

We had 91 notices filed on MONDAY so we gained 46 contracts or an additional 4600 oz

will stand for gold in this very non active delivery month of September.

October GAINED 156 contracts UP to 42,276

November LOST 18 contracts to stand at 60

December GAINED 224 contracts UP to 379.021.

We had 7 notice(s) filed today for 700 oz FOR THE SEPT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 7 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 4 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2022. contract month,

we take the total number of notices filed so far for the month (3889) x 100 oz , to which we add the difference between the open interest for the front month of (SEPT 522 CONTRACTS ) minus the number of notices served upon today 7 x 100 oz per contract equals 440,400 OZ OR 13.698 TONNES the number of TONNES standing in this NON active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month:

No of notices filed so far (3889) x 100 oz+ (522) OI for the front month minus the number of notices served upon today (7} x 100 oz} which equals 440,400 oz standing OR 13.698 TONNES in this NON active delivery month of SEPTEMBER.

TOTAL COMEX GOLD STANDING: 13.698 TONNES (A GREAT STANDING FOR A SEPT ( NON ACTIVE) DELIVERY MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,414,231.831 oz 75.092 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 27,218,150.643 OZ

TOTAL REGISTERED GOLD: 13,410,094.117 OZ (417.11 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 13,808,086.576 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,995.863. OZ (REG GOLD- PLEDGED GOLD) 342.01 tonnes//rapidly declining

END

SILVER/COMEX/SEPT 13

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2,111,737.141oz BRINKS Int. Delaware Loomis JPMorgan Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 129 CONTRACT(S) 645,000 OZ) |

| No of oz to be served (notices) | 158 contracts (775,000 oz) |

| Total monthly oz silver served (contracts) | 6304 contracts 31,520,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

total deposit: nil oz

JPMorgan has a total silver weight: 167.857 million oz/322.135million =52.09% of comex

Comex withdrawals: 5

i) Out of Int. Delaware 38,790.930 oz

ii) Out of CNT: 715,104.400 oz

iii) Out of Loomis: 120,140.571 oz

iv) Out of jPMorgan: 622,861.330 oz

v) Out of Manfra 614,839.810 oz

total: 2,111,737.141 oz

adjustments: 2

i) customer to dealer: Delaware 76,894.712 oz

ii) dealer to customer Manfra 121,098.88oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 45.946 MILLION OZ

TOTAL REG + ELIG. 322.135 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF SEPT OI: 284 CONTRACTS HAVING GAINED 107 CONTRACTS. WE HAD

19 CONTRACTS SERVED ON MONDAY SO WE GAINED A WHOPPING 126 CONTRACTS OR AN ADDITIONAL

630,000 OZ WILL STAND FOR METAL IN THIS VERY ACTIVE MONTH OF SEPT.

WE WILL GAIN IN TOTAL SILVER STANDING EACH TRADING DAY UNTIL THE END OF THE MONTH

(CONTINUAL QUEUE JUMPING BY OUR BANKERS SEARCHING FOR SILVER METAL)

OCTOBER LOST 116 CONTRACTS TO STAND AT 535 CONTACTS.

NOVEMBER GAINED 6 CONTRACTS TO STAND AT 32

DECEMBER SAW A LOSS OF 2516 CONTRACTS UP TO 122,778

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 129 for 645,000 oz

Comex volumes:74,106// est. volume today// good

Comex volume: confirmed yesterday: 86,127 contracts ( good)

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 6304 x 5,000 oz = 31,520,000 oz

to which we add the difference between the open interest for the front month of SEPT(284) and the number of notices served upon today 129 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT./2022 contract month: 6,304 (notices served so far) x 5000 oz + OI for front month of SEPT (284) – number of notices served upon today (129) x 5000 oz of silver standing for the SEPT contract month equates 32,295,000 oz. .

We have an inventory of 45.946 million oz of registered silver at the comex so Sept delivery of 32.295 MILLION OZ represents 70.28% of that category of silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:49,341// est. volume today// poor

Comex volume: confirmed yesterday: 51,749 contracts ( poor)

END

GLD AND SLV INVENTORY LEVELS

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

GLD INVENTORY: 964.91 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTO THE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

CLOSING INVENTORY 465.899 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Queen Elizabeth’s Death Puts Squeeze On Already Tight Bullion Coin Market

TUESDAY, SEP 13, 2022 – 07:20 AM

The recent death of Queen Elizabeth II is squeezing gold and silver bullion coin markets that were already strained by tight supplies.

There was an immediate and dramatic surge in demand for gold and silver bullion coins bearing the queen’s effigy upon her passing. According to News.com.au in Australia, “Collectors are scrambling to get their hands on coins with Queen Elizabeth’s face as prices skyrocket after her death.”

The owner of a Melbourne coin shop called the demand for coins with the queen’s likeness “insane.”

“Collectors are frenzied, and post-market prices are soaring,” he said, adding that business increased five-fold in the days after the queen’s death.

On Sunday morning, there was a wait to access the British Royal Mint website. Visitors were greeted with a message apologizing for “a particularly high volume of traffic.”

While the Melbourne coin shop owner couldn’t put an exact figure on the future value of coins with the queen’s image, he told News.com.au that demand for the first and last issues under any particular monarch would be constant. “The 2022 official set of coins, for instance, was totally sold out on my site yesterday,” he said.

The spike in demand could spill over into the broader bullion market that is already dealing with tight supply, causing spot prices to rise.

The silver bullion market has been hit particularly hard by supply problems. In March, the US Mint suspended production of Morgan and Peace Silver Dollars for the rest of the year. According to a press release, the “calculated pause is directly related to the global pandemic’s impact upon the availability of silver blanks from the Mint’s suppliers.”

The Royal Mint, the Perth Mint in Australia, and the Royal Canadian Mint will begin phasing out the production of coins featuring the queen’s effigy and replace them with coins bearing the image of King Charles III. This includes the Canadian Maple Leaf, the British Brittania, and the Australian Kangaroo coins. The logistics of this transition have not been announced, although it doesn’t appear there will be any immediate stoppage in coin production.

In a statement on its website, the Royal Mint said, “As we respect this period of respectful mourning, we continue to strike coins as usual.”

The Royal Canadian Mint had a bit more detailed statement on the transition.

The Royal Canadian Mint wishes to remind consumers and businesses that the royal succession has no impact on coins currently in circulation. A change in Monarch does not require the replacement of circulation coins. Therefore, Canadian consumers and businesses can continue using all coins currently in circulation. We are working on a plan to issue a variety of coins commemorating Her Majesty Queen Elizabeth II’s lifetime of service as Queen of Canada. The Mint will also support the Government of Canada as it works to determine a new obverse (heads) design for future Canadian coins.”

Even if the production of coins continues as normal for the time being, it remains unclear whether the transition to new coins featuring King Charles III will result in any production delays or limit the availability of new coins. A supplier for SchiffGold wrote, “Nobody is exactly sure what that’s going to look like yet but it seems to be pushing markets up on all coins with the queen’s effigy.”

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

GOLD/SILVER

END

3.Chris Powell of GATA provides to us very important physical commentaries

Ed Steer’s weekend gold and silver letter is posted in the clear at SilverSeek

Submitted by admin on Mon, 2022-09-12 18:20Section: Daily Dispatches

6:20p ET Monday, September 12, 2022

The weekend letter from GATA board member Ed Steer’s Gold and Silver Digest, headlined “Another Hugely Bullish Commitment of Traders Report, Especially in Silver,” has been posted in the clear at GoldSeek’s companion site, SilverSeek, here:

https://silverseek.com/article/another-hugely-bullish-cot-reportespecially-silver

CHRIS POWELL, Secretary/Treasurer

Goldl Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Please support GATA as they are the only guys who are helping us

(Chris Powell)

When buying gold or silver, consider the dealers who support GATA

Submitted by admin on Mon, 2022-09-12 09:26Section: Daily Dispatches

9:23a ET Monday, September 12, 2022

Dear Friend of GATA and Gold:

Being the only forms of money without counterparty risk, at least when held directly by their owners, gold and silver are often seen as the foundation of a sound investment portfolio.

This principle was put into graphic format by the U.S. economist John Exter, who served as the Federal Reserve Bank of New York’s vice president in charge of international banking and precious metals operations, as well as a member of the Federal Reserve’s Board of Governors, long before suppressing the gold price became the Fed’s primary objective.

n Exter’s inverted pyramid of financial asset risk, gold is the ultimate asset, with all other assets posing greater risk to their owners:

But you can do more than protect yourself when you buy gold and the other monetary metal, silver. You can also help GATA fight the price suppression we long have been exposing, documenting, and sometimes litigating against:

That is you can buy metal from dealers who support GATA and have been recommended by our supporters over the years.

A list of those dealers is included with every GATA Dispatch and is posted at GATA’s internet site here:

So please give them a chance to meet your investment needs.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Seems that Maduro has finally realized the value of gold:

(Reuters)

Venezuela pushes out small gold miners as Maduro seeks more revenue

Submitted by admin on Tue, 2022-09-13 01:15Section: Daily Dispatches

By Maria Ramirez and Mayela Armas

Reuters

Monday, September 12, 2022

EL CALLAO and CARACAS, Venezuela — In Venezuela’s El Callao mining region, countless small, artisanal miners who once sold gold to the government have left the area in the last year because accessible local supplies are depleted and President Nicolas Maduro has been striking deals with bigger miners, seeking more production and more revenue for the treasury.

Nationalizations in 2011 pushed out private miners and gold production stagnated. Now Maduro wants to ramp up production by building “strategic alliances” with select private companies, a dozen sources told Reuters. These partnerships are forcing out informal miners in places like El Callao, in the country’s south, businessmen, government officials, and miners said.

“They are looking to have more gold. It is what the state has always wanted,” said Alexis Chauran, director of an association of gold millers in La Ramona in eastern Venezuela, near the Brazilian border.

The government has granted 12 private companies permissions to build 30 processing plants, which use sophisticated equipment to extract gold-bearing sand from nearby mines, sources said. Most are already up and running. …

… For the remainder of the report:

END

4. OTHER GOLD/SILVER COMMENTARIES

-END-

.

end

5.OTHER COMMODITIES: RICE

end

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.9257

OFFSHORE YUAN: 6.9264

SHANGHAI CLOSED: UP 1.74 PTS OR .05%

HANG SENG CLOSED DOWN 35.52 PTS OR .18%

2. Nikkei closed UP 72.52 PTS OR .25%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 107.53/Euro RISES TO 1.0178

3b Japan 10 YR bond yield: FALLS TO. +.238/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 142.04/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.654%/Italian 10 Yr bond yield FALLS to 3.89% /SPAIN 10 YR BOND YIELD FALLS TO 2.78%…

3i Greek 10 year bond yield FALLS TO 4.157//

3j Gold at $1730.30 silver at: 19.90 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 57/100 roubles/dollar; ROUBLE AT 59.67//

3m oil into the 89 dollar handle for WTI and 95 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 142.04DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9497– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9667well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

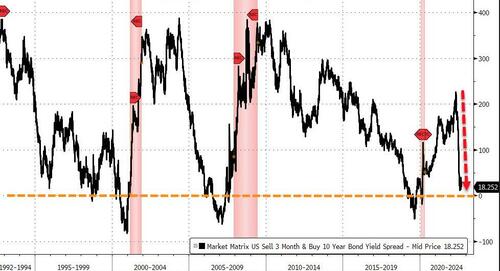

USA 10 YR BOND YIELD: 3.308 DOWN 5 BASIS PTS

USA 30 YR BOND YIELD: 3.471 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,24

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

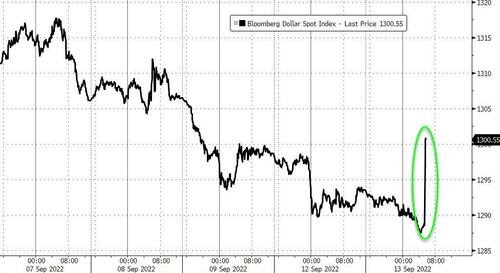

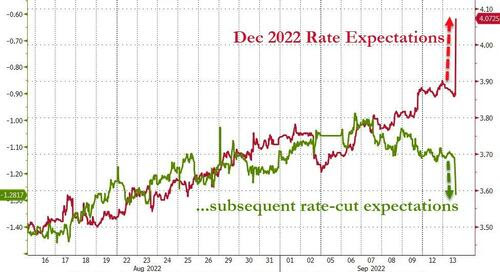

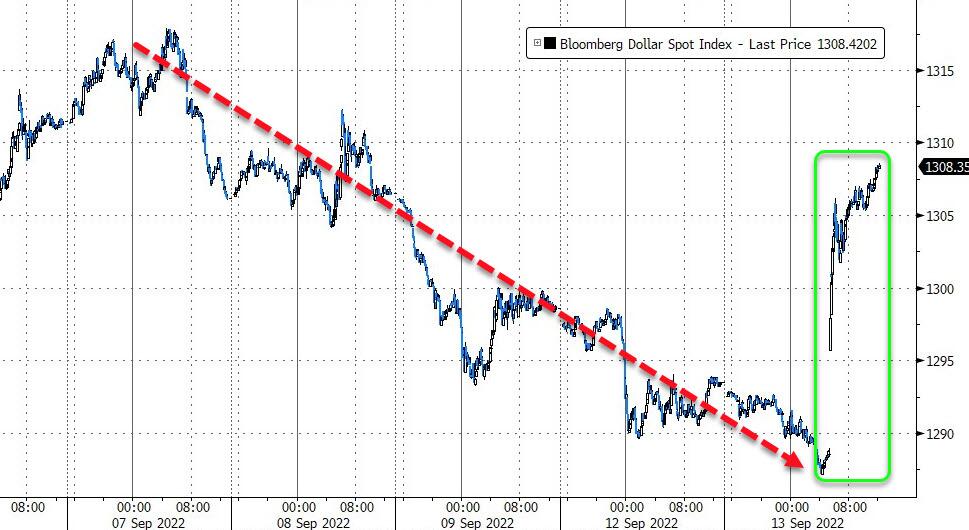

Futures Surge, Dollar Crumbles Ahead Of Pivotal CPI Print

TUESDAY, SEP 13, 2022 – 07:58 AM

US futures extended their gains for fifth consecutive day – their longest winning streak since July – rising ahead of today’s “pivotal” CPI data.

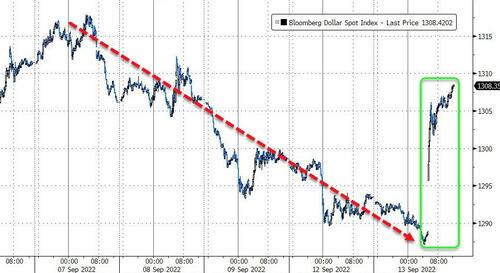

Futures on the S&P 500 and Nasdaq 100 gained 0.7% at 7:45 a.m. in New York ahead of the data that’s due at 8:30 a.m. The underlying gauges advanced Monday for a fourth straight day amid hopes that inflation will show further signs of cooling with the headline print actually declining for the first time in two years, before the Fed’s decision on interest rates next week. Treasury yields dipped while the Bloomberg dollar index extended its recent decline, sliding 0.3% to a two week low as traders bet that US inflation is near peaking, therefore challenging the dollar-dominance narrative, in the process pushing oil and bitcoin higher.

In premarket trading, tech giants including Apple and Microsoft climbed. Satellite-imaging company Planet Labs shares gained as much as 12% in US premarket session after raising full year forecasts for both revenue and adjusted gross margin. Oracle shares rose 1.9% as analysts are positive on the company’s 1Q top-line growth amid accelerating cloud revenue expansion. More bearish commentators, however, highlight a drop in operating margin as the integration of health records provider Cerner pushes up costs. Here are some other notable premarket movers:

- Rent the Runway (RENT US) shares slump 23% in premarket trading after reporting a drop in subscribers in the second-quarter and announcing a restructuring of the company.

- Dow (DOW US) shares declined 0.7% in premarket trading as Jefferies downgraded the stock to hold, saying that it is likely to be range-bound in the near term, with downside risk as rising interest rates further hit customer confidence.

- Peloton (PTON US) shares may be in focus as Citi analysts say that the departure of the company’s founders, including Executive Chairman John Foley, completes the organizational changes at Peloton and should improve its free cash flow picture.

- Keep an eye on Innovid (CTV US) shares as Morgan Stanley initiates coverage with an underweight rating, saying that the company has good positioning in connected TV, but the stock appears to be “more than fully valued”.

Previewing the CPI (our full preview here), UBS chief economist Paul Donovan writes that while US August consumer price inflation is due “Consumer prices do not measure the cost of living. Fantasy numbers in US CPI calculation further divorce this price measure from the cost of living. However, the Fed’s June policy error elevated the importance of consumer price inflation. Disinflation and deflation in durable goods, the longest period of gasoline price deflation for years, and some evidence of squeezing profit margins all suggest a lower reading.”

“It’s way to early to expect the Fed to react to the fact that we’re past peak inflation,” Nannette Hechler-Fayd’Herbe, chief investment officer at Credit Suisse International Wealth Management, told Bloomberg TV. “When you look at S&P 500 we have seen very big support levels from a technical point of view, so I can very well envisage that volatility takes us down to these levels once the market finally realizes the Fed will not cut rates as early as 2023.”

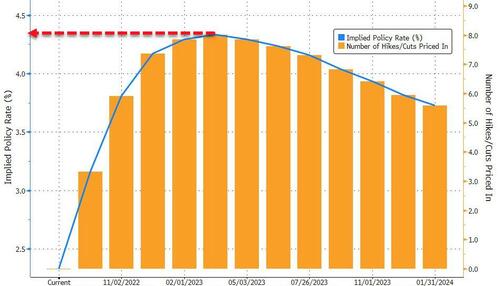

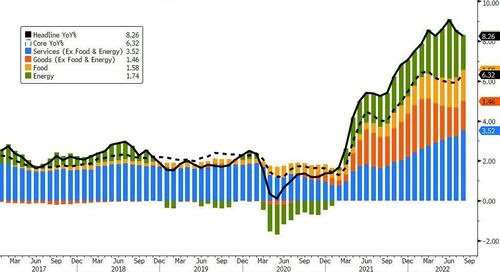

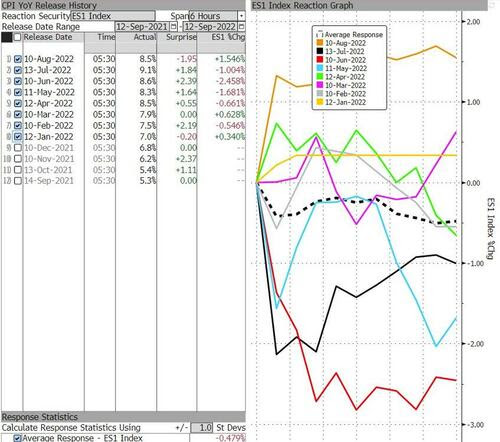

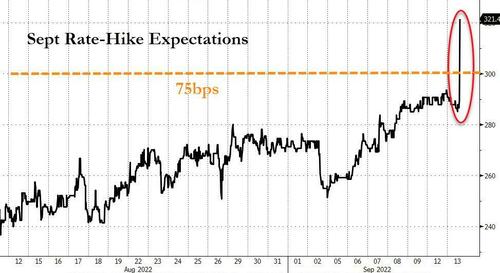

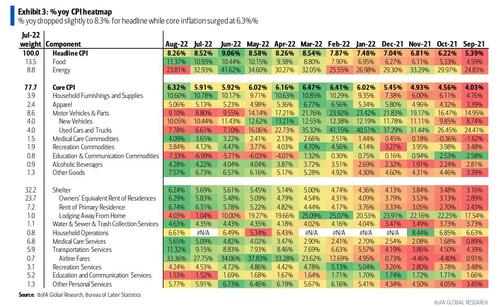

The government’s report is expected to show that consumer inflation increased 8.1% in August from the same month last year, down from 8.5% in July yet still historically elevated. The figures aren’t likely to sway the Fed’s September decision, with traders almost fully expecting another 75-basis-point increase next week, taking their cue from officials supporting that view. Still, solid signs of peaking inflation can affect the US central bank’s policy in later meetings.

“With a lot of US policymakers calling for a front-loading approach, the odds appear to favor a 75 basis-point move if markets are to be convinced the US central bank is serious about driving inflation lower on a ‘sustainable basis’,” said Michael Hewson, chief market analyst at CMC Markets UK. That “means today’s inflation numbers may not be terribly instructive.”

Meanwhile, JPMorgan permabullish strategists Marko Kolanovic and Nikolaos Panigirtzoglou said a soft landing is becoming the more likely scenario for the global economy, which will continue to provide tailwinds for risky assets. As a reminder, Marko has said to buy the dip pretty much every single week in 2022. Recent data pointing to moderating inflation and wage pressures, rebounding growth and stabilizing consumer confidence suggest the world will avoid a recession, they said. Not confirming their optimism, a Bank of America survey showed investors are fleeing equities en masse amid the specter of a recession, with allocations to stocks at record lows and cash exposure at all-time highs.

“The fact is that two consecutive reports showing a sharp deceleration combined with last month’s goldilocks jobs report will be a really encouraging sign and could trigger a broader risk rebound in the markets,” said Craig Erlam, a senior market analyst at Oanda Europe Ltd. “It may not be enough to tip the Fed balance in favor of a more modest 50 basis point rate hike next week but it may slow the pace of tightening thereafter.”

In Europe, corporate news helped buoy the Stoxx Europe 600 index, with UBS Group AG rising after raising its dividend and share-buyback target, and Bayer AG jumping more than 2% after starting the search for a new chief executive. Retailers and grocers pared some of their recent rally after Ocado Group Plc said inflation and energy costs will weigh on profit. The FTSE MIB outperformed peers, adding 0.3%. Utilities, consumer products and miners are the strongest performing sectors.

Earlier in the session, Asian stocks extended their recent rally as several markets returned from holidays, and as traders awaited a key US inflation data release due later Tuesday. The MSCI Asia Pacific Index rose as much as 0.7%, poised for a fourth-straight day of gains, driven by technology shares. South Korean stocks led advances among regional benchmarks in a catch-up rally following a four-day weekend. The US CPI report is expected to show a mixed picture, hinting that inflation may have peaked but remained elevated. This could provide more clues to the Federal Reserve’s rate decision next week, with traders currently expecting another 75-basis-point increase.

“Further pushback from the Fed could be likely but for now, with the Fed blackout period in place, market bulls may be hoping to see underperformance in the upcoming inflation data,” Jun Rong Yeap, a market strategist at IG Asia Pte, wrote in a note. How to trade dollar, bonds or equities ahead of the Fed decision? This week’s MLIV Pulse survey asks about the best trades going into the FOMC meeting. Please click here to share your views anonymously. Chinese equities edged higher as traders returned from a holiday. President Xi Jinping plans to travel to Central Asia this week in what would be his first trip abroad since the Covid pandemic began. Shares in Hong Kong fell.

Japanese equities rose for a fourth day, driven by optimism that inflation is close to the peak as investors await US CPI data to be announced late Tuesday. The Topix Index rose 0.3% to 1,986.57 as of market close Tokyo time, while the Nikkei advanced 0.3% to 28,614.63. Nintendo Co. contributed the most to the Topix Index gain, increasing 5.5%. Out of 2,169 stocks in the index, 1,126 rose and 903 fell, while 140 were unchanged. “Consumer surveys released by the New York Fed show that inflation expectations have receded, supporting stock prices to some extent,” said Masahiro Ichikawa, chief market strategist at Sumitomo Mitsui DS Asset Management.

In Australia, the S&P/ASX 200 index rose 0.7% to close at 7,009.70, boosted by gains in banks and mining shares. The benchmark reached the highest level since Aug. 26. Ramsay Health Care tumbled more than 10% after a consortium led by KKR & Co. indicated it won’t improve the terms of a takeover proposal, indicating the end of a A$20.1 billion ($14 billion) pursuit. In New Zealand, the S&P/NZX 50 index fell 0.4% to 11,762.15

Key equity gauges in India advanced for fourth consecutive session to edge closer to peaks seen in October as shares in the heavily weighted finance sector rebound following the resumption of inflows from foreigners. The S&P BSE Sensex gained 0.8% to 60,571.08 in Mumbai, while the NSE Nifty 50 Index rose by a similar measure. Both gauges are less than 3% short of their record highs after climbing more than 14% since the end of June. The rally in stocks comes despite surging consumer prices in the country. Retail inflation accelerated to 7% in August, slightly above the consensus estimate, data released Monday evening showed. Foreign investors have net bought more than $8 billion of local equities since end of June, with a large proportion going into shares of financial firms. “The current market buoyancy globally, including in India, is based on the expectation that inflation has peaked along with softening crude prices,” said Naveen Kulkarni, chief investment officer of Axis Securities’ PMS business. With the onset of winter, investors should watch energy prices in Europe and the US, which can re-ignite inflation, he added. HDFC Bank Ltd contributed the most to the Sensex’s gain, increasing 1.3%. Out of 30 shares in the benchmark index, 24 rose and 6 fell.

In FX, the Bloomberg Dollar Spot Index extended its recent losses, and after hitting an all time high at the start of the month, fell to a two-week low as the greenback weakened against all of its Group-of-10 peers apart from the Norwegian krone. CAD and NZD were the weakest performers in G-10 FX, SEK and JPY outperform.

- The euro rose a third day, to touch a day high of 1.0155 versus the greenback. European bonds traded mostly lower. German yields rose up to 4bps as they underperformed Italian bonds and with both countries tapping the market today

- The Norwegian krone posted a small drop versus the euro after a key survey of business sentiment by Norges Bank showed that the economy faces worsening prospects amid a “sharp” rise in prices.

- The yen reversed an Asia-session loss while the Australian and New Zealand dollars swung between modest gains and losses

In fixed income, Treasuries held gains into early US session, having pared most of Monday afternoon’s slide that followed weak 10-year note auction. US yields are richer by 4bp-5bp across the curve; the long-end lags, steepening 5s30s by about 1bp. The 10-year yield eased 4bps to near 3.31%. Bunds 10-year yield is up 1bp to around 1.66% and gilts 10-year yield is little changed. Treasuries outperform bunds and gilts as stock futures reach highest levels this month. The US auction cycle concludes with $18b 30-year bond reopening at 1pm. WI 30-year yield around 3.475% is above auction stops since 2014 and ~37bp cheaper than August’s, which tailed by 1.1bp. IG dollar issuance slate empty so far; Monday saw eight borrowers price $11.7b; activity expected to be lighter Tuesday with focus on August inflation data. Focal points of US session include CPI inflation and 30-year bond auction; Monday’s 3-year sale also tailed.

In commodities, WTI and Brent are firmer intraday as a function of the receding Dollar, but traders are wary of short-term upward moves as China continues with strings of lockdowns. WTI trades within Monday’s range, adding 1.1% to near $88.71. Spot gold trades on either side of the flat mark in the run-up to US CPI, under its 50 and 21 DMAs at 1,740.82/oz and USD 1,731.05/oz respectively. Base metals are mostly firmer amid the weaker Buck and upside across stocks.

Bitcoin trades on either side of USD 22,500, whilst Ethereum pulled back after reaching levels close to 1,800.

Looking to the day ahead, along with August CPI in the US, American data will include NFIB Small Business optimism (came in at 91.8, higher than the 90.8 expeected) and average hourly earnings, German and Eurozone ZEW survey results, UK August jobless claims, July average weekly earnings, and unemployment rate, Japanese August PPI, and Italian 2Q unemployment rate.

Market Snapshot

- S&P 500 futures up 0.5% to 4,129.25

- STOXX Europe 600 up 0.3% to 429.10

- MXAP up 0.5% to 156.38

- MXAPJ up 0.6% to 513.28

- Nikkei up 0.3% to 28,614.63

- Topix up 0.3% to 1,986.57

- Hang Seng Index down 0.2% to 19,326.86

- Shanghai Composite little changed at 3,263.80

- Sensex up 0.8% to 60,577.61

- Australia S&P/ASX 200 up 0.6% to 7,009.69

- Kospi up 2.7% to 2,449.54

- Gold spot down 0.1% to $1,723.41

- U.S. Dollar Index down 0.22% to 108.09

- German 10Y yield little changed at 1.67%

- Euro up 0.2% to $1.0140

Top Overnight News from Bloomberg

- Pacific Investment Management Co. is advocating a radical solution to fix the liquidity woes plaguing the world of bonds: The entire $23.7 trillion Treasury market should move to a model where investors can transact directly with each other — reducing their unhealthy dependence on balance-sheet-constrained banks

- The euro is up by almost 3% from two-decade lows hit a week ago against the dollar, and option markets suggest the rally has more room to run. The bet is that US consumer price data due later Tuesday will show inflation is near peaking, therefore challenging the dollar-dominance narrative. That view is behind the greenback’s recent retreat versus its major peers

- Germany is set to use a fund created to help companies cope with the economic hit from the pandemic to provide loan guarantees for struggling energy firms, according to a person familiar with the plan. The volume of loan guarantees available would be around 67 billion euros ($68 billion)

- China’s Premier Li Keqiang called for more policies to drive up consumption in the economy as latest figures show a further plunge in travel and spending over a three-day public holiday amid tight Covid controls

- For the better part of a decade, a US hedge-fund manager who has never even set foot in China has been patiently betting that the yuan will stage a massive collapse, one so deep that its value could be cut in half

- It’s not a common sight for euro overnight volatility to trade above 20% on non-central bank decision days. Yet this is what investors face this morning as everyone is on the lookout for the release of the US inflation report

- Britain’s unemployment rate fell to the lowest since 1974 as more people dropped out of the workforce, fanning upward pressure on wages. The government said 3.6% of adults were out of work and looking for jobs in the three months through July, lower than the 3.8% pace in the previous months. Economists had expected no change

- Secretary of State Antony Blinken said it was ‘unlikely’ the US and Iran would reach a new nuclear deal anytime soon, adding to Western officials’ downbeat assessment over the prospects for reviving an accord that President Donald Trump abandoned in 2018

- Japan has more firepower in its foreign exchange reserves than it did the last time it intervened in markets to support its currency, though a unilateral move is seen as unlikely to succeed without US support

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded positive after the advances in global peers including on Wall St. where sentiment was helped by slowing inflation expectations, although gains were capped ahead of US CPI data and amid further China COVID woes. ASX 200 reclaimed the 7,000 level with advances led by the commodity-related sectors and with the risk tone also helped by an improvement in business and consumer sentiment data. Nikkei 225 marginally gained amid hopes of further supportive measures with Japan to potentially implement a nationwide travel incentive this month. Hang Seng and Shanghai Comp were slightly firmer but with upside contained after fresh COVID restrictions including in Sanhe near Beijing and with Shijiazhuang city in Hebei also locking down a district due to coronavirus.

Top Asian News

- Emmys for Netflix’s Squid Game Boost ‘K-Drama’ Stocks in Seoul

- Fosun Chief Says Many Overseas Units Resilient Amid Pandemic

- Holders of Fosun’s 2b Yuan Bond Request Early Repayment in Full

- Netflix’s Megahit ‘Squid Game’ Wins Top Emmy Awards

- Woodford Administrator Faces Possible £306 Million Hit, UK Says

European bourses tread water with modest gains following a relatively mixed APAC lead. European sectors are mostly higher with no overarching theme or bias. Stateside, futures are edging higher in early European trade with a broad-based performance seen across the ES, NQ, YM, and RTY.

Top European News

- UK Chancellor Kwarteng told Treasury officials to adapt to a new approach focused on boosting GDP to 2.5%, the long-term average pre-GFC, ahead of the mini-Budget announcement next week which includes tax cuts and increased borrowing, according to FT.

- UK and EU are reportedly seeking to avoid a September 15th legal deadline over ‘grace periods’ becoming a flashpoint in talks, according to officials from both sides cited by the FT.

- The EU is delaying plans to cut the use of pesticides amid food production fears and subsequent price increases as a result, according to the FT.

- UK’s Felixstowe port has received notice from union of further strike action from 27th Sept to 5th Oct; collective bargaining process has been exhausted – no prospect of an agreement being reached with union.

- EU Commission President is to call another energy meeting by end-September, according to the Spanish Energy Minister, according Reuters.

- German Economy Ministry report says early indicators and polls point to a rising number of insolvencies in H2, but there is no ‘insolvency wave’ in sight, via Reuters.

- EU is reportedly mulling a EUR 180-200 price cap from lower-cost sources (vs guided EUR 200); eyes taking 33% of extra profits from fossil fuel companies, according to Bloomberg sources.

- Ocado Plummets as Shoppers Cut Back and Energy Costs Bite

- Mercedes-Benz Wins Dismissal of German Climate Lawsuit

- Some 17 Million in Europe Got Long Covid in First Pandemic Years

FX

- DXY is softer and trades on either side of 108.00, ahead of yesterday’s 107.80 low and the 50 DMA at 107.52.

- EUR/USD faded at 1.0160 with decent option expiry interest between 1.0170-80 (1.21bn).

- The JPY continued its correction to almost 142.00 against the Greenback, irrespective of mixed Japanese PPI prints.

Fixed Income

- Choppy and divergent price action in debt futures as EZ bonds digest decent auction results from Germany and Italy.

- Gilts regroup after underperformance on the back of better than expected UK data.

- Bunds are holding above 144.00 having fallen to a marginal new Eurex low at 143.86

- US Treasuries are firmer across the board pre-US CPI, irrespective of Monday’s poorly received 3 and 10 year offerings.

Commodities

- WTI and Brent are firmer intraday as a function of the receding Dollar, but traders are wary of short-term upward moves as China continues with strings of lockdowns.

- Spot gold trades on either side of the flat mark in the run-up to US CPI, under its 50 and 21 DMAs at 1,740.82/oz and USD 1,731.05/oz respectively

- Base metals are mostly firmer amid the weaker Buck and upside across stocks.

Crypto

- Bitcoin trades on either side of USD 22,500, whilst Ethereum pulled back after reaching levels close to 1,800.

US Event Calendar

- 06:00: Aug. SMALL BUSINESS OPTIMISM, 91.8, est. 90.8, prior 89.9

- 08:30: Aug. Real Avg Hourly Earning YoY, prior -3.0%

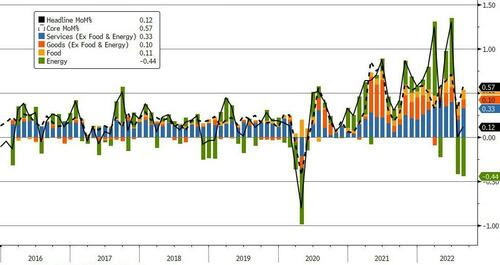

- 08:30: Aug. CPI Ex Food and Energy MoM, est. 0.3%, prior 0.3%

- 08:30: Aug. CPI Core Index SA, est. 296.250, prior 295.275

- 08:30: Aug. CPI Index NSA, est. 295.588, prior 296.276

- 08:30: Aug. CPI Ex Food and Energy YoY, est. 6.1%, prior 5.9%

- 08:30: Aug. CPI YoY, est. 8.1%, prior 8.5%

- 08:30: Aug. Real Avg Weekly Earnings YoY, prior -3.6%

- 08:30: Aug. CPI MoM, est. -0.1%, prior 0%

- 14:00: Aug. Monthly Budget Statement, est. -$217b, prior -$170.6b

DB’s Jim Reid concludes the overnight wrap

It’s that time again. US CPI will clearly be the major focus today and could shape next week’s FOMC and the rest of the month’s trading. Or, of course, it could be a damp squib but I’m sure they’ll be something in it to move markets.

Our economists are expecting a slight decline in the headline number, (-0.09% MoM) but for core to pick up (+0.30%). On a YoY basis, headline CPI should fall five-tenths to 8.0% while core should increase a tenth to 6.0%. With the market pricing a near certainty of a 75bp move next week (now at 73.4bps), that profile above won’t be enough to meaningfully reduce chances of a 75bp hike, and markets will turn to this Friday’s inflation expectations data as the last hurdle to clear before the Fed delivers (barring any late breaking news stories to the contrary). On that front, the New York Fed’s 3-year inflation expectations measure fell to its lowest level in 2 years yesterday, clocking in at 2.8% in August from 3.2% in July. For context, it’s retreated from a high of 4.2% in October of last year. Uncertainty remains near record highs, though, which will continue to give policymakers pause even as the 75th and 25th percentile of survey responses have also fallen.

Ahead of CPI, the S&P 500 rallied (+1.06% and a 5-day rally for the first time since late-January/early-February) alongside the global risk complex, led by energy and big tech stocks, with the NASDAQ outperforming, up +1.27%. Apple (+3.85%) led the way in the first full trading day since their new iPhone went on sale on Friday. Orders have been strong so far. I upgrade every year but this time I decided not to…. until one minute before the virtual shop opened for the new products. As with every year I got seduced.

While European sovereign curves rallied and flattened, the Treasury curve steepened, and yields climbed ahead of today’s inflation data. 2yr yields climbed +1.5bps while 10yr yields were +4.8bps higher, but some +9.8bps higher than their lunchtime lows. Much of that was after the Europe close as 10yr Bunds and BTP rallied -4.4bps and -5.7bps, respectively. One theory for the US yield sell-off was the fact that yesterday brought the first batch of US Treasury coupon auctions since the Fed doubled the size of their monthly QT runoff, with yields marching higher after both the 3yr and 10yr auction, as the market has to absorb additional collateral. There’s been a partial pullback in Asia this morning with yields on 10yr USTs down -2.12bps to 3.34%.

The initial risk appetite yesterday was led by Europe, as most of the early focus was on the news we discussed 24 hours ago, namely Ukraine’s successful counter-offensive operation over the weekend. Risk sentiment enjoyed a boost, with the Euro also having its best day against the US dollar in a month, appreciating +0.80%. The wider implications of this success are still up for debate though. In particular, it seems like this pushes out the timeline on any potential peace talks, as Ukraine will be emboldened to double down on their red lines. In that vein, the Kremlin said yesterday there were no prospects for talks at the moment. On the downside, this potentially raises the spectre of escalation as well, whether it’s on the battlefield via unconventional weapons or a mass mobilisation from Russia, or on the economic front with Russia applying more pressure through natural gas markets through the remaining pipeline to Europe. European natural gas futures were trading in line with the broader risk sentiment yesterday though, rather than on potential tail risk scenarios, falling another -8.0%, closing below EUR 200 for the first time in a month. We peaked at EUR 342 eleven days ago, so down -44.23% since then. As hinted, European equities rallied strongly, with the STOXX 600 climbing +1.76%, the DAX +2.40% higher, and the CAC increasing +1.95%.

Sticking with the theme of the war and energy, a draft EU proposal, to be officially unveiled this week, included mandatory power cut targets, bringing the bloc closer to rationing. The draft also includes a levy on extra profits at energy producers used to fund relief to consumers. These are still merely draft proposals, which would ultimately need member state buy-in to be implemented, so the negotiation process may wind up watering down the proposal. Nevertheless, as mentioned, natural gas futures fell on the news, with German and French power prices also falling -8.10% and -3.60%, respectively.

The UK’s own energy support plan that we’ve recently covered is due to take effect come October. Whilst US CPI out later today will gain the lion’s share of attention over the near term, the UK has its own CPI print out tomorrow, as well. Our economists are expecting headline inflation to stay put at 10.1% yoy and core to increase to 6.4% yoy. With the new Energy Price Guarantee program in place, they’re lowering their peak forecast for CPI from 14% to 10.5%.

Asian equity markets are firmly in the green while extending a global rally this morning on optimism that inflation is peaking. Across the region, the Kospi (+2.56%) is leading gains with the CSI (+0.70%), the Shanghai Composite (+0.33%) and the Hang Seng (+0.44%) catching up after reopening following a public holiday. Elsewhere, the Nikkei (+0.16%) is trading in positive territory in early trade.

In overnight trading, US stock futures are pointing to slightly higher with the S&P 500 (+0.11%) and NASDAQ 100 (+0.10%).

Early morning data indicated that pipeline prices in Japan appear to have stabilised as factory gate inflation (+9.0% y/y) in August remained unchanged (vs +9.4% in June), albeit a tenth above expectations. Looking at the data, the decline in global oil prices seems to have led the way despite the weakening in the Japanese yen.

Oil prices are slightly lower in early Asian trade with Brent crude futures -0.18% at $93.83/bbl as China’s harsh zero-Covid policy continues to negatively impact the demand from the world’s top oil importer.

To the day ahead, along with August CPI in the US, American data will include NFIB Small Business optimism and average hourly earnings, German and Eurozone ZEW survey results, UK August jobless claims, July average weekly earnings, and unemployment rate, Japanese August PPI, and Italian 2Q unemployment rate.

end

AND NOW NEWSQUAWK

European bourses tread water with modest gains, DXY trades on either side of 108 – Newsquawk US Market Open

TUESDAY, SEP 13, 2022 – 06:21 AM

- European bourses tread water with modest gains following a relatively mixed APAC lead; US futures post mild gains

- DXY is softer and trades on either side of 108.00, EUR/USD faded at 1.0160, JPY continues its correction vs the USD

- Choppy and divergent price action in debt futures as EZ bonds digest decent auction results from Germany and Italy

- WTI and Brent are firmer intraday as a function of the receding Dollar, but traders are wary as China continues with lockdowns

- Looking ahead, highlights include US CPI and supply from the US

For the full report and more content like this check out Newsquawk

Try a 14-day trial with Newsquawk and hear breaking trading news as it happens.

13th September 2022

LOOKING AHEAD

- US CPI and supply from the US

- Click here for the Week Ahead preview.

- Click here for the Newsquawk US CPI preview.

GEOPOLITICS

RUSSIA-UKRAINE

- Ukraine Deputy Defence Minister says that fighting is continuing in the Kharkiv region and it is too early to say if Ukraine has restored full control over the region.

CHINA-TAIWAN

- Chinese President Xi Jinping is expected to stack the country’s senior military leadership during next month’s Communist Party congress with loyalists aligned on his goal of unifying Taiwan and the mainland, according to Nikkei.

ARMENIA-AZERBAIJAN

- Twitter sources reported fighting in the Kalbajar-Lachin border regions between Azerbaijan and Armenia, while Armenia’s Foreign Minister was said to have informed Russian Foreign Minister Lavrov about the situation resulting from Azerbaijan’s aggression. Furthermore, Tehran Times reported that Azerbaijan’s Defence Ministry said a number of its forces were killed in an exchange of fire with Armenian forces.

- Click here for Newsquawk analysis on the developments.

EUROPEAN TRADE

EQUITIES

- European bourses tread water with modest gains following a relatively mixed APAC lead.

- European sectors are mostly higher with no overarching theme or bias.

- Stateside, futures are edging higher in early European trade with a broad-based performance seen across the ES, NQ, YM, and RTY.

- Click here for more detail.

FX

- DXY is softer and trades on either side of 108.00, ahead of yesterday’s 107.80 low and the 50 DMA at 107.52.

- EUR/USD faded at 1.0160 with decent option expiry interest between 1.0170-80 (1.21bn).

- The JPY continued its correction to almost 142.00 against the Greenback, irrespective of mixed Japanese PPI prints.

- Click here for more detail.

FIXED INCOME

- Choppy and divergent price action in debt futures as EZ bonds digest decent auction results from Germany and Italy.

- Gilts regroup after underperformance on the back of better than expected UK data.

- Bunds are holding above 144.00 having fallen to a marginal new Eurex low at 143.86

- US Treasuries are firmer across the board pre-US CPI, irrespective of Monday’s poorly received 3 and 10 year offerings.

- Click here for more detail.

COMMODITIES

- WTI and Brent are firmer intraday as a function of the receding Dollar, but traders are wary of short-term upward moves as China continues with strings of lockdowns.

- Spot gold trades on either side of the flat mark in the run-up to US CPI, under its 50 and 21 DMAs at 1,740.82/oz and USD 1,731.05/oz respectively

- Base metals are mostly firmer amid the weaker Buck and upside across stocks.

- Click here for more detail.

CRYPTO

- Bitcoin trades on either side of USD 22,500, whilst Ethereum pulled back after reaching levels close to 1,800.

NOTABLE EUROPEAN HEADLINES

- UK Chancellor Kwarteng told Treasury officials to adapt to a new approach focused on boosting GDP to 2.5%, the long-term average pre-GFC, ahead of the mini-Budget announcement next week which includes tax cuts and increased borrowing, according to FT.

- UK and EU are reportedly seeking to avoid a September 15th legal deadline over ‘grace periods’ becoming a flashpoint in talks, according to officials from both sides cited by the FT.

- The EU is delaying plans to cut the use of pesticides amid food production fears and subsequent price increases as a result, according to the FT.

- UK’s Felixstowe port has received notice from union of further strike action from 27th Sept to 5th Oct; collective bargaining process has been exhausted – no prospect of an agreement being reached with union.

- EU Commission President is to call another energy meeting by end-September, according to the Spanish Energy Minister, according Reuters.

- German Economy Ministry report says early indicators and polls point to a rising number of insolvencies in H2, but there is no ‘insolvency wave’ in sight, via Reuters.

- EU is reportedly mulling a EUR 180-200 price cap from lower-cost sources (vs guided EUR 200); eyes taking 33% of extra profits from fossil fuel companies, according to Bloomberg sources.

NOTABLE EUROPEAN DATA

- UK Avg Earnings (Ex-Bonus) (Jul) 5.2% vs. Exp. 5.0% (Prev. 4.7%)

- UK ILO Unemployment Rate (Jul) 3.6% vs. Exp. 3.8% (Prev. 3.8%)

- UK HMRC Payrolls Change (Aug) 71k (Prev. 73k)

- EU ZEW Survey Expectations (Sep) -60.7 (Prev. -54.9)

- German ZEW Current Conditions (Sep) -60.5 vs. Exp. -52.2 (Prev. -47.6)

- German ZEW Economic Sentiment (Sep) -61.9 vs. Exp. -60.0 (Prev. -55.3)

APAC TRADE

- APAC stocks traded positive after the advances in global peers including on Wall St. where sentiment was helped by slowing inflation expectations, although gains were capped ahead of US CPI data and amid further China COVID woes.

- ASX 200 reclaimed the 7,000 level with advances led by the commodity-related sectors and with the risk tone also helped by an improvement in business and consumer sentiment data.

- Nikkei 225 marginally gained amid hopes of further supportive measures with Japan to potentially implement a nationwide travel incentive this month.

- Hang Seng and Shanghai Comp were slightly firmer but with upside contained after fresh COVID restrictions including in Sanhe near Beijing and with Shijiazhuang city in Hebei also locking down a district due to coronavirus.

NOTABLE APAC HEADLINES

- PBoC set USD/CNY mid-point at 6.8928 vs exp. 6.9080 (prev. 6.9098)

- China’s city of Sanhe near Beijing is reportedly to be under lockdown for 4 days, while Shijiazhuang city in Hebei province locked down a district due to coronavirus.

- China Securities Daily noted that analysts expect the PBoC to maintain the MLF rate.

- Japan may implement a nationwide travel incentive this month, according to Kyodo.

- China’s state planner says a second batch of pork reserves will be released this week, according to Reuters.

DATA RECAP

- Japanese Corp Goods Price YY (Aug) 9.0% vs. Exp. 8.9% (Prev. 8.6%, Rev. 9.0%)

- Japanese Corp Goods Price MM (Aug) 0.2% vs. Exp. 0.4% (Prev. 0.4%, Rev. 0.7%)

- Japanese Business Survey Index* (Q3) 1.7% (Prev. -9.9%)

- Australian NAB Business Confidence* (Aug) 10 (Prev. 7, Rev. 8)

- Australian NAB Business Conditions* (Aug) 20 (Prev. 20, Rev. 19)

- Australian Westpac Consumer Sentiment Index (Sep) 84.4 (Prev. 81.2)

Source: Newsquawk

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 1.74 PTS OR .05% //Hang Sang CLOSED DOWN 35.39 PTS OR .18% /The Nikkei closed UP 72.52 OR 0.25%. //Australia’s all ordinaires CLOSED UP 0.63% /Chinese yuan (ONSHORE) closed UP AT 6.9257//OFFSHORE CHINESE YUAN DOWN 6.9264// /Oil UP TO 89.10 dollars per barrel for WTI and BRENT AT 95.36 / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING AOBVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE STRONGER

3 a./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

3c CHINA

CHINA/

This could be trouble: the typhoon is heading straight for Shanghai

(zerohedge)

Typhoon Barrels Towards Asia’s Largest Container Port

MONDAY, SEP 12, 2022 – 05:20 PM

Asia’s largest container-shipping port is in the crosshairs of another menacing typhoon with the risk of a direct hit by mid-week that could disrupt supply chains.

The US Joint Typhoon Warning Center forecasts Typhoon Muifa will hit Shanghai and nearby Ningbo ports on China’s east coast late Wednesday into early Thursday.

Currently, Muifa is located east of Taiwan and is headed northwest with maximum wind gusts of 115 mph.

Last week, super Typhoon Hinnamnor passed by Shanghai, sending vessels out to sea to avoid damage. This storm is not as strong as Hinnamnor, but forecast models show a direct hit on the largest containerized ports in Asia could be a massive headache for China as an economic slump worsens due to zero-Covid policies shuttering multiple metro areas/industrial zones and a worsening property downturn.

There’s also the risk the typhoon could disrupt containerized shipping to the US.

END

CHINA

A good measure on how the Chinee economy is doing: shipping. Demand sinks across multiple cargo markets

(Freightwaves)