by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1729.75 UP $12.30

SILVER: $19.85 UP $1.04

ACCESS MARKET:

GOLD $1724.50

SILVER: $19.80

Bitcoin morning price: $22,263 UP 1075

Bitcoin: afternoon price: $22406 UP 1218

Platinum price closing UP $24.20 AT $906,85

Palladium price; closing UP $125.60 at $2268.80

END

DONATE

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,716.200000000 USD

INTENT DATE: 09/09/2022 DELIVERY DATE: 09/13/2022

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 18

323 C HSBC 5

435 H SCOTIA CAPITAL 2

657 C MORGAN STANLEY 2

661 C JP MORGAN 49

690 C ABN AMRO 6

737 C ADVANTAGE 69 2

800 C MAREX SPEC 22 5

905 C ADM 2

TOTAL: 91 91

MONTH TO DATE: 3,882

JPMorgan stopped: 49/91

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR SEPT CONTRACT:

91 NOTICES FOR 9100 OZ //0.2830 TONNES

total notices so far: 3882 contracts for 388,200 oz (12.0746 tonnes)

SILVER NOTICES: 19 NOTICES FILED FOR 95,000 OZ/

total number of notices filed so far this month 6175 : for 30,825,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $1.230

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD: ////

INVENTORY RESTS AT 966.64 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $1.04

AT THE SLV// ://SMALL CHANGES IN SILVER INVENTORY AT THE SLV//:TWO DEPOSIT OF 553,000 OZ AND 464,000 INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 468.571 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A FAIR SIZED 300 CONTRACTS TO 138,537. AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GAIN IN OI WAS ACCOMPLISHED WITH OUR $0.31 GAIN IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.31) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD A STRONG GAIN OF 582 CONTRACTS ON OUR TWO EXCHANGES,; WE HAD CONSIDERABLE SPECULATOR LIQUIDATION.

WE MUST HAVE HAD:

I) CONSIDERABLE/ SPECULATOR SHORT LIQUIDATIONS ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 135,000 OZ QUEUE JUMP / // V) GOOD SIZED COMEX OI GAIN/(//CONSIDERABLE SPEC LIQUIDATION/)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -232

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTACTS for 7 days, total 7022 contracts: 35.11 million oz OR 5.015 MILLION OZ PER DAY. (1003 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 35.11 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 35.11 MILLION OZ///

RESULT: WE HAD A FAIR SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 300 WITH OUR $0.31 GAIN IN SILVER PRICING AT THE COMEX// FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 50 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /SOME BANKER ADDITIONS A// CONSIDERABLE SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 135,000 OZ QUEUE JUMP // .. WE HAD A FAIR SIZED GAIN OF 350 OI CONTRACTS ON THE TWO EXCHANGES FOR 1.75MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 19 NOTICE(S) FILED TODAY FOR 95,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 19 CONTRACTS TO 464,822 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:–289 CONTRACTS.

.

THE SMALL SIZED DECREASE IN COMEX OI CAME DESPITE OUR RISE IN PRICE OF $7.85//COMEX GOLD TRADING/FRIDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND /SOME SPECULATOR SHORT COVERINGS//CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 8.401 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S GIGANTIC JUMP OF 38,000 OZ //NEW STANDING 13.555 TONNES

YET ALL OF..THIS HAPPENED WITH OUR STRONG RISE IN PRICE OF $7.85 WITH RESPECT TO FRIDAY’S TRADING

WE HAD A SMALL SIZED GAIN OF 1196 OI CONTRACTS 3.720 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1215 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 464,822

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1196 CONTRACTS WITH 19 CONTRACTS DECREASED AT THE COMEX AND 1215 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1196 CONTRACTS OR 3.720 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1215) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (19): TOTAL GAIN IN THE TWO EXCHANGES 1196 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 8.409 TONNES FOLLOWED BY TODAY’S QUEUE. JUMP OF 38,000 oz. 3) ZERO LONG LIQUIDATION//// //.,4) SMALL SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

15,142 CONTRACTS OR 1,514,200 OZ OR 47.09 TONNES 7 TRADING DAY(S) AND THUS AVERAGING: 2163 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAY(S) IN TONNES: 47.09 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 47.09/3550 x 100% TONNES 1.32% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 47.09 TONNES (MUCH LESS ISSUANCE THIS MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT., FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FAIR BY A GOOD SIZED 300 CONTRACT OI TO 138,769 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 50 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 50 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 50 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 300 CONTRACTS AND ADD TO THE 50 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A FAIR SIZED GAIN OF 350 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 1.75 MILLION OZ

OCCURRED WITH OUR GOOD GAIN IN PRICE OF $0.31

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED HOLIDAY //Hang Sang CLOSED HOLIDAY /The Nikkei closed UP 327.36 OR 1.16%. //Australia’s all ordinaires CLOSED UP 0.97% /Chinese yuan (ONSHORE) closed DOWN AT 6.9265//OFFSHORE CHINESE YUAN UP 6.9169// /Oil UP TO 87.45 dollars per barrel for WTI and BRENT AT 93.77 / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 19 CONTRACTS TO 465,111 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS TINY COMEX INCREASE OCCURRED DESPITE OUR STRONG RISE IN PRICE OF $7.85 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A SMALL SIZED EFP (1080 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1215 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :1215 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1215 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED SIZED TOTAL OF 1196 CONTRACTS IN THAT 1215 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI LOSS OF 19 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR RISE IN PRICE OF GOLD $7.85. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING SEPT (13.555),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 13.555 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $7.85) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 1196 CONTRACTS // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS COVERED SOME OF THEIR POSITIONS////// WE HAVE REGISTERED A FAIR SIZED GAIN OF 3.720 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR SEPT. (13.555 TONNES)…

WE HAD -289 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1196 CONTRACTS OR 119600 OZ OR 3.720 TONNES

Estimated gold volume 148,830/// poor/

final gold volumes/yesterday 167,706/ poor

INITIAL STANDINGS FOR SEPT ’22 COMEX GOLD //SEPT 12

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 319,689.569 oz Brinks JPMorgan Malca |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 105,393.571 oz Brinks HSBC |

| No of oz served (contracts) today | 91 notice(s) 9100 OZ 0.2830 TONNES |

| No of oz to be served (notices) | 476 contracts 47600 oz 1.480TONNES |

| Total monthly oz gold served (contracts) so far this month | 3882 notices 388,200 OZ 12.0746 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 2

i) Into Brinks 15,992.900 oz

ii)Into HSBC 89,400.671 oz

total deposits 105,393,571 oz

3 customer withdrawals:

i) Out of Brinks 169,416.197 oz

ii) Out of JPMorgan: 64,622.104 oz

iii) Out of Malca: 85,650.214 oz

total: 319,689.569 oz

total in tonnes: 9.94 tonnes

Adjustments: 1

JPM: 13,598.791 oz dealer to customer

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPT.

For the front month of SEPT we have an oi of 567 contracts having LOST 947 contracts .

We had 1327 notices filed on FRIDAY so we gained A WHOPPING 380 contracts or an additional 38,000 oz

will stand for gold in this very non active delivery month of September.

October GAINED 98 contracts UP to 42,120

November GAINED 1 contracts to stand at 78

December GAINED 303 contracts UP to 378,797.

We had 91 notice(s) filed today for 9100 oz FOR THE SEPT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 91 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 49 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2022. contract month,

we take the total number of notices filed so far for the month (3882) x 100 oz , to which we add the difference between the open interest for the front month of (SEPT 567 CONTRACTS ) minus the number of notices served upon today 91 x 100 oz per contract equals 435,800 OZ OR 13.555 TONNES the number of TONNES standing in this NON active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month:

No of notices filed so far (3882) x 100 oz+ (567) OI for the front month minus the number of notices served upon today (91} x 100 oz} which equals 435,800 oz standing OR 13.555 TONNES in this NON active delivery month of SEPTEMBER.

TOTAL COMEX GOLD STANDING: 13.555 TONNES (A GREAT STANDING FOR A SEPT ( NON ACTIVE) DELIVERY MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,414,231.831 oz 75.092 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 27,228,355.145 OZ

TOTAL REGISTERED GOLD: 13,548,889.957 OZ (421.42 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 13,679,465.145 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 11,134,668. OZ (REG GOLD- PLEDGED GOLD) 346.33 tonnes//rapidly declining

END

SILVER/COMEX/SEPT 12

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 348,098.180oz BRINKS CNT Loomis |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 570,971.180 oz JPMorgan |

| No of oz served today (contracts) | 19 CONTRACT(S) 95,000 OZ) |

| No of oz to be served (notices) | 158 contracts (790,000 oz) |

| Total monthly oz silver served (contracts) | 6175 contracts 30,875,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) Into JPMorgan 570,971.180 oz

total deposit: 570,971.180 oz

JPMorgan has a total silver weight: 168.460 million oz/324.247million =51.94% of comex

Comex withdrawals:3

i) Out of Brinks 17,915.360 oz

ii) Out of CNT: 30,333.150 o

iii) Out of Loomis: 299,849.670 oz

total: 348,098.180 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 45.991 MILLION OZ

TOTAL REG + ELIG. 324.241 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF SEPT OI: 177 CONTRACTS HAVING LOST 142 CONTRACTS. WE HAD

169 CONTRACTS SERVED ON FRIDAY SO WE GAINED 27 CONTRACTS OR AN ADDITIONAL

135,000 OZ WILL STAND FOR METAL IN THIS VERY ACTIVE MONTH OF SEPT.

WE WILL GAIN IN TOTAL SILVER STANDING EACH TRADING DAY UNTIL THE END OF THE MONTH

(CONTINUAL QUEUE JUMPING BY OUR BANKERS SEARCHING FOR SILVER METAL)

OCTOBER LOST 41 CONTRACTS TO STAND AT 651 CONTACTS.

NOVEMBER GAINED 12 CONTRACTS TO STAND AT 26

DECEMBER SAW A GAIN OF 104 CONTRACTS UP TO 125,294

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 19 for 95,000 oz

Comex volumes:78,394// est. volume today// good

Comex volume: confirmed yesterday: 46,047 contracts ( poor)

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 6175 x 5,000 oz = 30,875,000 oz

to which we add the difference between the open interest for the front month of SEPT(177) and the number of notices served upon today 19 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT./2022 contract month: 6,175 (notices served so far) x 5000 oz + OI for front month of SEPT (177) – number of notices served upon today (19) x 5000 oz of silver standing for the SEPT contract month equates 31,665,000 oz. .

We have an inventory of 45.991 million oz of registered silver at the comex so Sept delivery of 31.665 MILLION OZ represents 68.85% of that category of silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:49,341// est. volume today// poor

Comex volume: confirmed yesterday: 51,749 contracts ( poor)

END

GLD AND SLV INVENTORY LEVELS

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

GLD INVENTORY: 966.64 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTO THE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

CLOSING INVENTORY 468.571 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

GOLD/SILVER

END

3.Chris Powell of GATA provides to us very important physical commentaries

A very important interview of Chris Powell on gold price suppression

(Chris Powell/GATA)

In interview with The Jist, GATA secretary gives overview of gold price suppression

Submitted by admin on Fri, 2022-09-09 21:01Section: Daily Dispatches

9:06p ET Friday, September 9, 2022

Dear Friend of GATA and Gold:

Your secretary/treasurer was interviewed this week by Josh Hamilton, founder of The Jist internet site in the United Kingdom, discussing the purposes and mechanisms of the longstanding U.S. government and Western central bank policy of gold price suppression.

Your secretary/treasurer stresses that gold price suppression isn’t “conspiracy theory” but policy that is heavily documented in government’s own public and private archives.

Gold, your secretary/treasurer says, is a determinant of all prices everywhere, which is why central banks feel so compelled to control the monetary metal’s price.

The interview is an hour and 16 minutes long and be watched at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

The BIS data shows a tiny increase in August gold swaps.

It will end by Dec 2022.

(Courtesy Robert Lambourne/GATA)

Robert Lambourne: BIS shows tiny increase in its August gold swaps

Submitted by admin on Sat, 2022-09-10 20:35Section: Daily Dispatches

By Robert Lambourne

Saturday, September 10, 2022

The recently released August statement of account of the Bank for International Settlements —

— shows that the recent trend of significant decreases in the bank’s gold swaps has stopped for the moment.

The total of the BIS gold swaps outstanding at August 31 was 75 tonnes versus 56 tonnes on July 29. This increase of 19 tonnes is modest, since as of June 30 there were 202 tonnes of swaps, and as is clear from Table B below, the swaps have been far higher in recent months. For example, at the end of January 2022 there were 501 tonnes of gold swaps.

It remains clear that the BIS continues to be an active trader of gold swaps on a regular basis, and the recent data still suggests that the downward trend in the bank’s swaps is continuing and if the current rate of decline is maintained the BIS may well be reporting no gold swaps by the end of the year.

The decline of the bank’s gold swaps could indicate that an exit from the swaps, potentially due to “Basel III” regulations, is happening. But as usual, it seems unlikely that the BIS will provide any additional information on what is happening with its gold swaps.

… Historical context …

The BIS rarely comments publicly on its gold activities, but its first use of gold swaps was considered important enough to cause the bank to give some background information to the Financial Times for an article published July 29, 2010, coinciding with publication of the bank’s 2009-10 annual report.

The general manager of the BIS at the time, Jaime Caruana, said the gold swaps were “regular commercial activities” for the bank, and he confirmed that they were carried out with commercial banks and so did not involve central banks. It also seems highly likely that the BIS’ remaining swaps are still all made with commercial banks, because the BIS annual report has never disclosed a gold swap between the BIS and a major central bank.

The swap transactions potentially create a mismatch at the BIS, which may end up being long unallocated gold (the gold held in BIS sight accounts at major central banks) and short allocated gold (the gold required to be returned to swap counterparties). This possible mismatch has not been reported by the BIS.

The gold banking activities of the BIS have been a regular part of the services it offers to central banks since its establishment 90 years ago. The first annual report of the BIS explains these activities in some detail:

http://www.bis.org/publ/arpdf/archive/ar1931_en.pdf

A June 2008 presentation made by the BIS to potential central bank members at its headquarters in Basel, Switzerland, noted that the bank’s services to members include secret interventions in the gold and foreign exchange markets:

https://www.gata.org/node/11012

The use of gold swaps to take gold held by commercial banks and then deposit it in gold sight accounts held in the name of the BIS at major central banks doesn’t appear ever to have been as large a part of the BIS’ gold banking business as it has been in recent years.

As of March 31, 2010, excluding gold owned by the BIS itself, there were 1,706 tonnes held in gold sight accounts at major central banks in the name of the BIS, of which 346 tonnes or 20% were sourced from gold swaps from commercial banks.

If the BIS was adopting the level of disclosure made by publicly held companies, such as commercial banks, some explanation of these changes probably would have been required by the accounting regulators. This irony may not be lost on those dealing with regulatory activities at the BIS. Presumably the shrinkage of the BIS’ gold banking business shows that even central banks now prefer to hold their own gold or hold it in earmarked form — that is, as allocated gold.

A review of Table B below highlights recent BIS activity with gold swaps, and despite the trend of declines, the recent positions estimated from the BIS monthly statements have remained large, especially in early 2022, and the volume of trading has been significant.

No explanation for this continuing use of swaps has been published by the BIS. Indeed, no comment on the bank’s use of gold swaps has been offered since 2010.

The gold of the swaps is supplied by bullion banks to the BIS. The gold is then deposited in BIS gold sight accounts (unallocated gold accounts) at major central banks such as the Federal Reserve.

The reasons for this activity have never been fully explained by the BIS and various conjectures have been made as to why the BIS is facilitating it. One conjecture is that the swaps are a mechanism by which gold that was secretly supplied by central banks to cover shortfalls in the gold markets is returned to those central banks. The use of the BIS to facilitate this trade suggests of a desire to conceal the reasons for the transactions.

As can be seen in Table A below, the BIS has used gold swaps extensively since its financial year 2009-10. No use of swaps is reported in the bank’s annual reports for at least 10 years prior to the year ended March 2010.

The February 2021 estimate of the bank’s gold swaps (552 tonnes) is higher than any level of swaps reported by the BIS at its March year-end since March 2010. The swaps reported at March 2021 were the highest year-end level reported, as is clear from Table A.

—–

Table A — Swaps reported in BIS annual reports

March 2010: 346 tonnes.

March 2011: 409 tonnes.

March 2012: 355 tonnes.

March 2013: 404 tonnes.

March 2014: 236 tonnes.

March 2015: 47 tonnes.

March 2016: 0 tonnes.

March 2017: 438 tonnes.

March 2018: 361 tonnes.

March 2019: 175 tonnes.

March 2020: 326 tonnes.

March 2021: 490 tonnes.

March 2022: 358 tonnes.

—–

The table below reports the estimated swap levels since August 2018. It can be seen that the BIS has been actively trading gold swaps and other gold derivatives, with changes from month to month above 100 tonnes in this period.

—–

Table B — Swaps estimated by GATA from BIS monthly statements of account

Month ….. Swaps

& year … in tonnes

Aug-22 ….. / 75

Jul-22 ….. / 56

Jun-22 ….. / 202

May-22 ….. / 270

Apr-22 ….. / 315

Mar-22 …. / 358

Feb-22 …. / 472

Jan-22 ….. / 501

Dec-21…. / 414

Nov-21…. / 451

Oct-21…. / 414

Sep-21 …. / 438

Aug-21 …. / 464

Jul-21 …. / 502

Jun-21 …./ 471

May-21 …./ 517

Apr-21 …. / 472

Mar-21…. / 490±

Feb-21 …../ 552

Jan-21 …. / 523

Dec-20 …. / 545

Nov-20 …. / 520

Oct-20 …. / 519

Sep-20…../ 520

Aug-20…../ 484

Jul-20 ….. / 474

Jun-20 …. / 391

May-20 …. / 412

Apr-20 …. / 328

Mar-20 …. / 326*

Feb-20 …. / 326

Jan-20 …. / 320

Dec-19 …. / 313

Nov-19 …. / 250

Oct-19 …. / 186

Sep-19 …. / 128

Aug-19 …. / 162

Jul-19 ….. / 95

Jun-19 …. / 126

May-19 …. / 78

Apr-19 ….. / 88

Mar-19 …. / 175

Feb-19 …. / 303

Jan-19 …. / 247

Dec-18 …. / 275

Nov-18 …. / 308

Oct-18 …. / 372

Sep-18 …. / 238

Aug-18 …. / 370

± The estimate originally reported by GATA was 487 tonnes, but the BIS annual report states 490 tonnes. It is believed that slightly different gold prices account for the difference.

* The estimate originally reported by GATA was 332 tonnes, but the BIS annual report states 326 tonnes. It is believed that slightly different gold prices account for the difference.

GATA uses gold prices quoted by USAGold.com to estimate the level of gold swaps held by the BIS at month-ends.

—–

As noted already, the BIS in recent times has refused to explain its activities in the gold market, nor for whom the bank is acting:

https://www.gata.org/node/17793

Despite this reticence, in undertaking these swaps the BIS is almost certainly acting on behalf of central banks, as they are the BIS’ owners and control its Board of Directors.

This refusal to explain prompts some observers to believe that the BIS acts as an agent for central banks intervening surreptitiously in the gold and currency markets, providing those central banks with access to gold as well as protection from exposure of their interventions.

A recent report by Bullion Star’s Ronan Manly on the Bank of Portugal’s use of its gold reserves reinforces this point, since the Bank of Portugal confirms that 20 tonnes of its gold is stored with the BIS:

https://www.gata.org/node/21950

This disclosure seems a little economic with the truth as the BIS has no gold storage facilities of its own. Gold held by the BIS on behalf of central banks is either deposited into a BIS gold sight (unallocated) account or a BIS earmarked (allocated) gold account and usually deposited with one of the central banks based at a major gold trading center, such as the Federal Reserve in New York.

Since Manly shows that the Bank of Portugal is focused on earning income from its gold, it seems highly likely that this gold is held in a BIS sight account, though its ultimate location is unclear.

It is possible that the swaps provide a mechanism for bullion banks to return gold originally lent to them by central banks to cover bullion bank shortfalls of gold. Some commentators have suggested that a portion of the gold held by exchange-traded funds and managed by bullion banks is sourced directly from central banks.

—–

END

4. OTHER GOLD/SILVER COMMENTARIES

GATA ( Ronan Manly: London silver inventories continue to plummet as metal exits LBMA vaults

By Ronan Manly

Bullion Star, Singapore

Monday, September 12, 2022

There is an unprecedented situation emerging in London, where the relentless hemorrhaging of one of the worlds largest stockpiles of silver is now well and truly under way.

For the last nine months, this stockpile of silver, held in the LBMA vaults in London, has been consistently falling each and very month, and has now reached an all-time low (since vault holdings records began in July 2016). …

… For the remainder of the analysis:

-END-

.

end

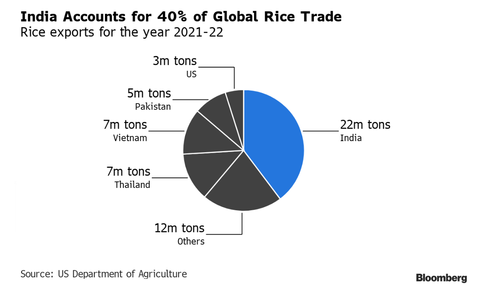

5.OTHER COMMODITIES: RICE

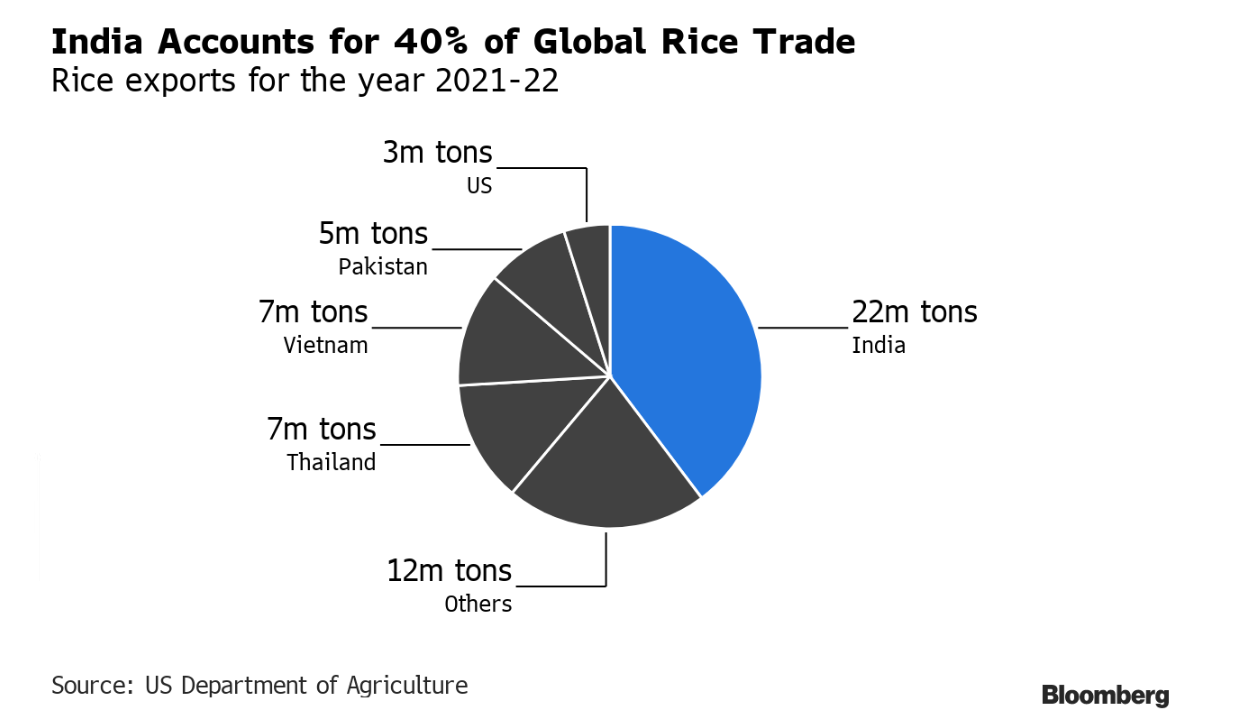

Top Rice-Exporter India Curbs Shipments, Adds To Fresh Food Inflation Fears

FRIDAY, SEP 09, 2022 – 07:20 PM

We told readers in April that the next challenge for the global food supply could be a plunge in rice production (read: here). Then in early August, severe heatwaves in India, the world’s biggest rice shipper, wreaked havoc across farmland in the country, depressing crop output. Today, India restricted some rice exports and placed levies on others, exacerbating a world already squeezed by a food crisis.

Bloomberg reported India imposed a 20% duty on white and brown rice exports and banned shipments of broke rice — parboiled and basmati rice were excluded from the export duty and/or trade restrictions. The new curbs apply to about 60% of India’s rice exports and go into effect Friday.

India’s clamp down on grain exports is to calm domestic prices after low rainfall during the monsoon season curtailed planting. The country accounts for 40% of global rice shipments and could spark yet another wave of food inflation for the poorest nations importing the grain.

“Such severe disruptions in global supplies, combined with a record level of consumption worldwide, should supercharge” prices and further fuel food inflation, said Sabrin Chowdhury, head of commodities at Fitch Solutions.

According to Chookiat Ophaswongse, honorary president of the Thai Rice Exporters Association, “imposing a 20% levy is a big deal … this move will cause global rice prices to rally.”

Ophaswongse said traders would be forced to purchase from rivals Thailand and Vietnam, struggling to increase shipments and will send prices even higher. India’s export restrictions will be a massive blow to importing nations in Asia and Africa that consume the grain.

Persistent inflation (especially food and energy) could spark further civil unrest worldwide over the next coming months. The forecast for impending global turmoil to deepen was published in a new note by Verisk Maplecroft, a UK-based risk consulting and intelligence firm (read: here).

end

COMMODITIES IN GENERAL/

END

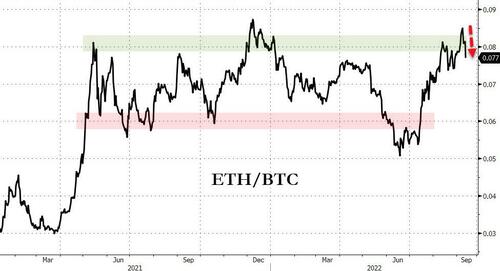

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings MONDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.9265

OFFSHORE YUAN: 6.9169

SHANGHAI CLOSED: HOLIDAY

HANG SENG CLOSED HOLIDAY

2. Nikkei closed UP 327.36 OR 1.16%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 107.92/Euro RISES TO 1.0136

3b Japan 10 YR bond yield: FALLS TO. +.242/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 142.51/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP -// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.638%/Italian 10 Yr bond yield FALLS to 3.94% /SPAIN 10 YR BOND YIELD FALLS TO 279%…

3i Greek 10 year bond yield RISES TO 4.20//

3j Gold at $1732.50 silver at: 19.49 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 32/100 roubles/dollar; ROUBLE AT 60.28//

3m oil into the 87 dollar handle for WTI and 93 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 142.51DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 9543– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9675well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.277 DOWN 4 BASIS PTS

USA 30 YR BOND YIELD: 3.425 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,22

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Jump As Dollar Slide Accelerates

MONDAY, SEP 12, 2022 – 07:49 AM

It appears that Goldman’s trading desk was right again. Just days after the vampire squid’s sellside researchers were warning that the market has not yet bottomed, the bank’s far more accurate flow traders said that “The Pain Trade Is Now Up, The CPI Doesn’t Matter At All, And The Q4 Chase Starts Early“, and on Monday morning it was all engines go in global stock markets, with US equities poised to extend their brisk rally from last week as investors braced for the final CPI before the Federal Reserve’s September decision. Futures for the S&P 500 and Nasdaq 100 both rose 0.5% each at 715 a.m. in New York, extending above their Friday session highs, putting the underlying gauges on track for a fourth day of gains, while Europe’s Stoxx 600 index climbed for a third day, and Asia was almost all green.

Treasury yields dropped and the dollar retreated further as traders bet inflation is near peaking even as Fed talking heads ramped up hawkish rhetoric (it’s ok, the Fed is always 9-12 months behind the curve). And as the USD slumps, the euro is extending gains, rising the most in six months against the dollar, as hawkish commentary from ECB policy makers continue. Crude oil and industrial metals gained as the greenback’s descent countered demand concerns, while speculation grows that China will ease on covid-zero policies after the coming plenum.

In US premarket trading, cryptocurrency-exposed stocks including Riot Blockchain and Coinbase edged higher as Bitcoin added to last week’s gains, rising above the $22,000 level. Meanwhile, Apple rose, with analysts positive on the company as pre-order data for the latest versions of its iPhone point to strong interest and demand. Here are some other notable premarket movers:

- Bristol Myers Squibb (BMY US) rises 6% in premarket trading after deucravatinib received approval from the US Food and Drug Administration for the treatment of moderate-to-severe psoriasis with no “black box” warnings.

- Watch Cable One (CABO US) after it was downgraded to equal-weight at Wells Fargo, which took less positive stance on the sector, even as the stock remains “the best house in the cable neighborhood.”

- Keep an eye on Bill.com Holdings (BILL US) as the stock was initiated with an overweight rating at Morgan Stanley, which cites multiple growth drivers for the infrastructure software firm.

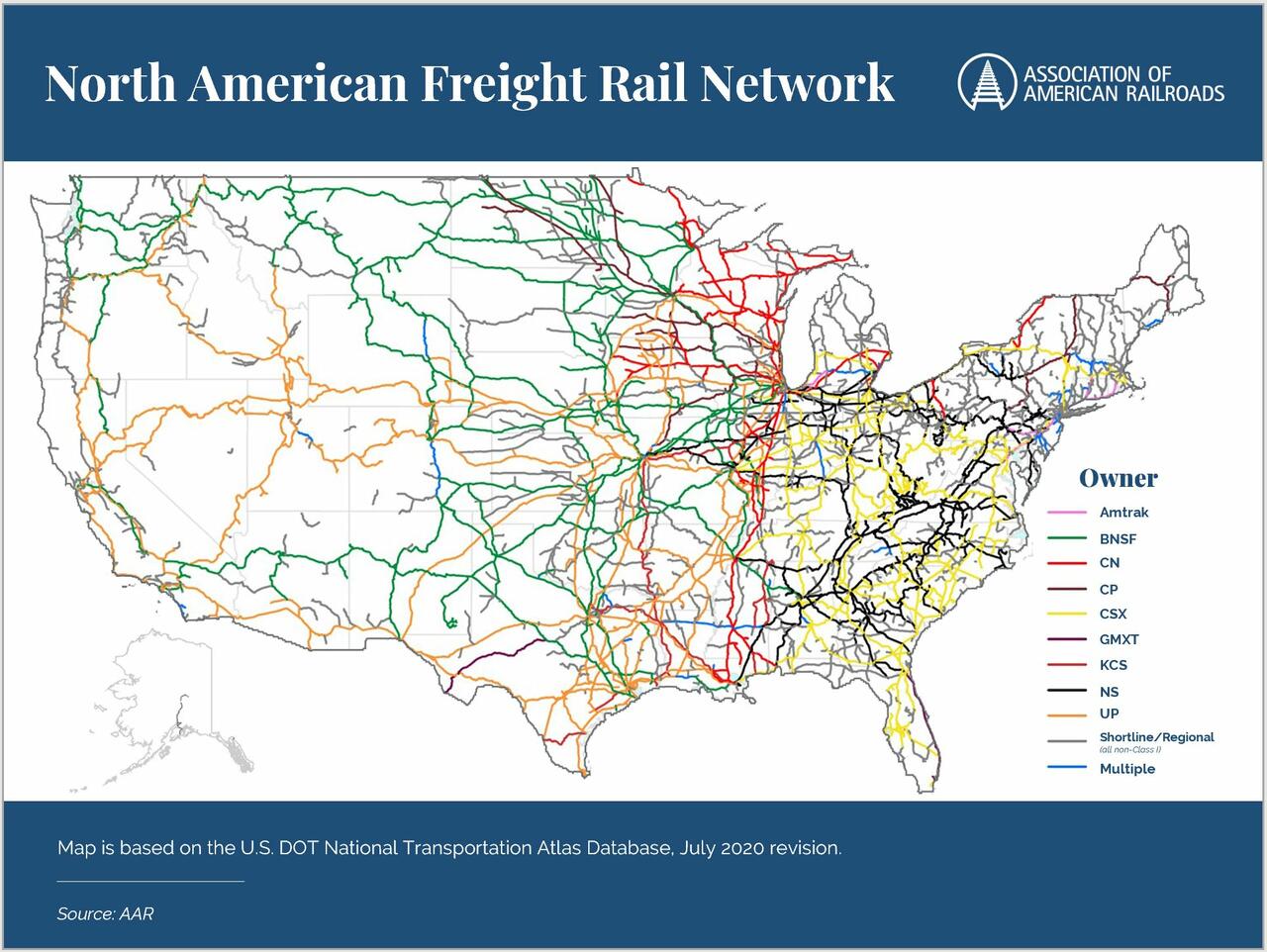

- US railroad stocks may be in focus as tens of thousands of industry workers could be on strike by the end of this week. Keep an eye on CSX (CSX US), Norfolk Southern (NSC US) and Union Pacific (UNP US).

- US chipmakers could be in focus after Reuters reports the Biden administration plans to broaden curbs on US shipments of semiconductors for artificial intelligence and chipmaking tools to China. Watch Lam Research (LRCX US), Applied Materials (AMAT US), KLA (KLAC US), Nvidia (NVDA US) and AMD (AMD US).

- Keep an eye on CoStar Group (CSGP US) as it was initiated at market perform by BMO Capital Markets, which sees the commercial real estate information provider as a “poster child” for the info services sector, but finds it hard to justify an outperform recommendation.

Stocks have rebounded amid more speculation of oversold systematic funds and another short squeeze – conditions similar to the mid-June bounce. Now, traders are preparing for tomorrow’s inflation data which are expected to show an 8% increase in the overall August consumer price index from the same month last year, down from 8.5% in July yet still historically elevated, and to cement the point that peak inflation has been hit. The outcome will be significant for the Fed’s decision next week and could sway equities in either direction, although the worst case scenario is now fully priced in: traders almost fully expect another jumbo-sized Fed hike next week, following two 75-basis-point increases, and forward guidance by Fed officials in the run-up to the policy meeting has supported that view. Any easing in the Fed’s tightening resolve would be seen a very dovish and send stocks surging even more.

“It seems policy makers were keen to reinforce their hawkish position ahead of the blackout period — which we’re now in — potentially with an eye on that data point,” said Craig Erlam, a senior market analyst at Oanda. “There was perhaps a feeling that a softer reading could see market expectations slip which they clearly want to avoid. It will be interesting to see how traders now respond as we’ve seen how keen they were to hop aboard the ‘dovish pivot’ train before.”

Indeed, on Friday, Fed Governor Christopher Waller said he favors “another significant” increase in interest rates when the central bank meets later this month, signaling his backing for a 75 basis-point move. Fed Bank of St. Louis President James Bullard said he was leaning “more strongly” toward a third straight boost of that magnitude, while his Kansas City counterpart Esther George noted officials have a “clear-cut” case for continuing to remove monetary support.

Meanwhile, thanks to receding inflation fears, markets are pricing in little prospect of a recession, according to Tatjana Puhan, deputy chief investment officer at Tobam SAS. Risk assets are buying into the narrative of a soft landing even though a hard landing is more likely, she said. “We should be ready for a significant impact on the economy,” Puhan told Bloomberg Television. “I can easily see markets going down another 20%,”she said, echoing Guggneheim’s Scott Minerd.

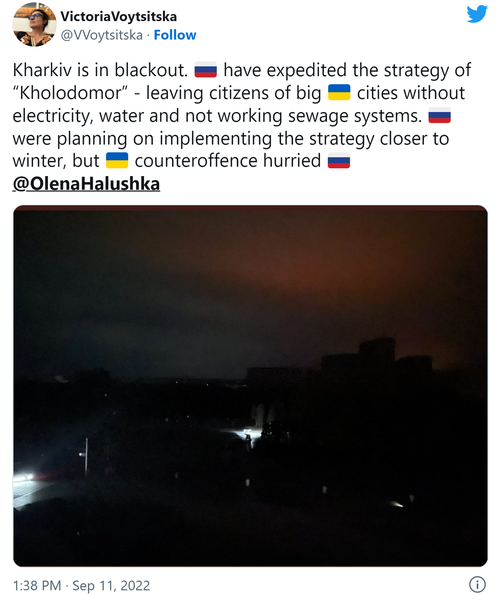

Markets also have to digest the implications of Ukraine’s counter-offensive, after its forces continued their rapid advance in the Kharkiv region, exploiting a retreat of Russian defenses.

In Europe, the Stoxx 50 rallied 1.4% climbing for a third day, with retailers leading the advance amid optimism plans to curb energy bills will provide some relief for consumers squeezed by a cost-of-living crisis. The FTSE MIB outperforms, adding 1.8%, Stoxx 600 lags, adding 0.9%. Retailers, miners and autos are the strongest-performing sectors. Here are some of the biggest European movers today:

- Mining stocks outperform the broader European market again on Monday as metals rise on increased demand amid China’s peak construction season, a weaker dollar and risks to supply

- Ferrexpo and shares in other companies with operations in Ukraine surge in European trading Monday as the country’s military continued a rapid advance in the Kharkiv region at the weekend

- Atos shares jump for a second day, as much as 6.9%, as minority shareholder Sycomore Asset Management called for the chairman to resign during an interview with Reuters

- Pernod Ricard shares rise after declining as much as 1.2% after Deutsche Bank cut the recommendation to hold on macro headwinds and lagging advertising & promotional/sales

- Thule shares drop as much as 16% after a profit warning from the Swedish bike, car and outdoor equipment manufacturer. Handelsbanken says “considerable 2023 uncertainty remains”

- Tate & Lyle falls as much as 7.1% after Jefferies downgrades to hold from buy on increasing cost pressures in Europe, saying is now more exposed to “tricky” European market

- Electrolux shares fall as much as 6.8% as the Swedish appliance producer expects 3Q earnings to decline sharply. Handelsbanken says “significant cuts” to 2022-2023 estimates are needed

- HelloFresh shares fall as much as 6.7% on Monday after the USDA warned of possible E. coli contamination for some ground beef packages in HelloFresh meal kits shipped in July

- Orpea slumps as much as 21% as the company warns that profit will be lower than expected, citing rising energy and salary costs, with analysts noting there are still downside risks to shares

According to another group of Goldman Sachs strategists – the ones who are pretty much always wrong – said US firms that do most of their business at home will fare better than those exposed to Europe, where a recession is all but guaranteed. A team led by David Kostin say that while the path of US growth may be “uncertain,” the economic situation in Europe is dire. Translation: buy European stocks.

Earlier in the session, Asian stocks began the week by heading for a third straight daily advance, bolstered by the weakening of the dollar and oil prices. The MSCI Asia Pacific Index climbed as much as 0.8% on Monday, poised for its highest close in nearly two weeks, as tech and materials shares rallied. TSMC rose 2.4%, boosting Taiwan’s gauge, after the firm said August sales rose 59% from a year ago and Reuters reported that the US plans to broaden curbs on chip shipments to China. Markets were closed for holidays in China, Hong Kong and South Korea. Benchmarks in the Philippines, Taiwan, Japan and Australia were all up. India’s S&P BSE Sensex Index also rose ahead of the nation’s retail inflation data for August, while Thailand’s main gauge was higher for a fifth-straight day to erase this year’s decline amid optimism the economic recovery has momentum. The dollar and oil prices weakened ahead of a much-awaited US inflation report on Tuesday, with investors preparing for super-sized interest-rate hikes in the US. Investors are also watching for Russia’s response after reports overnight of the advance of Ukraine forces in Kharkiv region.

Japanese stocks advanced for a third day, driven by gains in electronics makers, while reopening plays rallied on reports of reduced restrictions for inbound tourists. The Topix rose 0.7% to 1,980.22 as of 3:02 p.m. Tokyo time, while the Nikkei advanced 1.2% to 28,542.11. The yen resumed weakening after regaining more than 1% against the dollar Friday. Keyence Corp. contributed the most to the Topix gain, increasing 1.9%. Out of 2,169 shares in the index, 1,449 rose and 596 fell, while 124 were unchanged.

“On many measures, positioning continues to appear quite extreme to us and thus there is a possibility that a lower than expected m-m core CPI print may lead to a knee-jerk positive reaction in stocks,” Chetan Seth, Asia Pacific equity strategist at Nomura wrote in a note. On Ukraine, he said that “it’s too early to extrapolate this event for the market,” and that the supply of some key commodities will likely take time to increase. The pause in the dollar’s rally has given Asian stocks some breathing room, with the MSCI measure up about 3% from a trough last week. But with many signals indicating more dollar strength and China’s lockdowns continuing, flows into the region are likely to remain under pressure.

In FX, the Bloomberg Dollar Spot Index extended declines, with all G-10 FX rising, barring the yen, which trades at around 142.75/USD. Some more details:

- The BBDXY Index was set for its biggest two-day drop in a month as the greenback weakened against all of its Group-of-10 peers apart from the yen.

- The euro rose as much as 1.6% against the greenback on Monday to trade just shy of the 1.02 handle. Bunds, Italian bonds fell across the curve and money markets rose ECB tightening bets after Bundesbank President Joachim Nagel said the central bank must take further clear steps if the inflation picture stays the same. ECB Executive Board member Frank Elderson said more hikes will come as “it’s very important that the expectations that the people have on how the inflation will develop in the medium to long term will not become deanchored”

- The pound rose against a broadly weaker dollar though trailed the euro and other European currencies. Data show the UK economy recovered more slowly than expected from a slump triggered by an extra bank holiday in June, with industrial production and construction both shrinking

- Sweden’s krona was the best-performing G-10 currency as the nation is on the cusp of a power shift, casting aside the ruling Social Democrats in favor of a center-right opposition bloc as vote counting nears the finish line

- The yen resumed its downtrend after jumping more than 1% on Friday as players adjusted positions before US inflation figures due on Tuesday. JGBs followed Treasuries lower. On Sunday, Deputy Chief Cabinet Secretary Seiji Kihara said during a TV program that Japan has “to take necessary steps while closely monitoring developments including excessive, one-sided moves in the exchange rate”

In rates, US Treasuries edged higher with gains led by front-end of the curve, steepening spreads slightly while the dollar retreats. US yields were richer by up to 2.5bp across front-end of the curve with 2s10s, 5s30s spreads steeper by 0.5bp and 1.5bp on the day; 10-year yields around 3.29%, trading 1bp cheaper vs. bunds and slightly outperforming gilts in the sector. A US double auction of 3- and 10-year notes imposes an obstacle for further Treasuries advance. The US double auction kicks off at 11:30am with $41b 3-year note sale, followed by $32b 10-year reopening at 1pm. 3-year WI around 3.567% is above auction stops since 2007 and ~36.5bp cheaper than August stop-out which traded 0.3bp through the WI level. Auctions conclude Tuesday with $18b 30-year bond reopening.

In commodities, WTI crude jumps 1% to around $87.63; spot gold rises roughly $9 to trade near $1,726/oz. Natural gas prices fall as the market awaits details of the European Union’s intervention plan.

Bitcoin has risen above USD 22k amid the broader risk appetite, whilst Ethereum topped USD 1,750 in early trade.

Looking at today’s calendar, we have Japan’s August machine tool orders, UK July monthly GDP, construction output, industrial and manufacturing production, index of services, trade balance, Germany July current account balance, Italy July industrial production. There is nothing on the US calendar.

Market Snapshot

- S&P 500 futures up 0.5% to 4,087.25

- STOXX Europe 600 up 0.8% to 423.90

- MXAP up 0.7% to 155.35

- MXAPJ up 0.8% to 509.68

- Nikkei up 1.2% to 28,542.11

- Topix up 0.7% to 1,980.22

- Hang Seng Index up 2.7% to 19,362.25

- Shanghai Composite up 0.8% to 3,262.05

- Sensex up 0.7% to 60,217.05

- Australia S&P/ASX 200 up 1.0% to 6,964.46

- Kospi up 0.3% to 2,384.28

- Gold spot up 0.5% to $1,724.64

- U.S. Dollar Index down 1.05% to 107.86

- German 10Y yield little changed at 1.71%

- Euro up 1.5% to $1.0188

Top Overnight News from Bloomberg

- The Biden administration plans to broaden curbs on US shipments of semiconductors for artificial intelligence and chipmaking tools to China, Reuters reported, citing unidentified people familiar with the matter

- The ECB’s jumbo increase in interest rates last week was designed to keep inflation expectations anchored, according to Vice President Luis de Guindos

- German inflation will only peak in the first quarter of 2023 as surging energy costs trickle down to consumers, weighing on purchasing power and tipping the country into recession during the winter months, according to the Ifo institute

- French Finance Minister Bruno Le Maire said the government will cut a levy on industrial production at a slower pace than initially planned as it seeks to meet deficit reduction targets despite lower economic growth

- Natural gas prices fell as the market awaits details of the European Union’s plan to intervene in an unprecedented energy crisis that is already destroying demand for the fuel

- Russia hit power plants deep behind Ukrainian lines, causing blackouts across the northeast of the country as Kyiv’s forces pressed a lightning offensive that’s reversed months of Moscow’s advances

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks took impetus from last Friday’s gains on Wall Street in a holiday-thinned start to the week. ASX 200 traded higher with the mining-related sectors and tech resuming their recent outperformance, while the top-weighted financials sector was also kept afloat as the major banks increased mortgage rates after last week’s RBA rate hike. Nikkei 225 rose above 28,500 as Japan mulls steps to open its borders including scrapping its daily limit of 50k arrivals of overseas visitors by October and waiving visa requirements. Hang Seng, Shanghai Comp and KOSPI were closed for the Mid-Autumn Festival.

Top Asian News

- US is reportedly planning to broaden curbs on sales to China of semiconductors used for AI and chipmaking tools, according to Reuters sources.

- Chinese President Xi will visit Central Asia and meet with Russian President Putin in his first trip outside of China since the pandemic began, according to Reuters.

- PBoC called for efforts to facilitate the broader use of the digital yuan, according to Xinhua.

- Japanese Deputy Chief Cabinet Secretary Kihara said the government must take steps as needed against excessive, one-sided currency moves. Kihara also said they won’t rule out issuing government bonds to fund an expected increase in defence costs and they are ready to consider steps in the not-so-distant future to further open Japan’s borders to overseas visitors including scrapping its daily limit of 50k arrivals of overseas visitors by October, according to Nikkei.

- Japan is eyeing allowing foreign visitors to travel freely without travel agency bookings and waiving visa requirements, with PM Kishida to make the decision as early as this week, according to FNN.

European bourses extend on the upside seen at the open despite a lack of news catalysts during the European morning. European sectors are mostly firmer, with Autos & Parts outperforming closely followed by Banks, Retail, and Basic Resource, whilst the flip side sees defensive sectors, with Healthcare, Food & Beverages, and Telecoms in the red. Stateside, US equity futures are posting gains, with marginal outperformance seen in the NQ vs peers.

Top European News

- EU offers to reduce Northern Ireland border controls, with EU’s Sefcovic encouraged by the UK’s intention for a negotiated settlement on trade, while the EU could cut customs checks across the Irish Sea to just a few lorries a day. Furthermore, Sefcovic said the border would be ‘invisible’ under European Commission plans provided that the UK gave the EU real-time data on trade movements, according to FT. However, Senior UK officials are reportedly downplaying EU’s offer on Brexit this weekend, with one reason being that the offer does not go far enough, according to Eurasia’s Rahman.

- ECB’s de Guindos said the 75bps hike last week was aimed at anchoring inflation expectations; higher rates may also weigh on economic growth, via Bloomberg. ECB’s de Guindos said he does not know how much rates will climb.

- Orpea Slumps 21% After Suprise Profit Warning

- Bulgaria Says in Talks to Double Gas Supplies From Azerbaijan

- Russia Strikes Power Plants as Ukrainian Forces Extend Advances

- Euro Climbs Most in Five Months as Traders Eye Hawkish ECB Speak

FX

- DXY recoiled further from 108.860 at best, through 108.500 and 108.00, to 107.800 and its lowest level since late August.

- EUR/USD saw a boost to levels close to 1.0200 from a 1.0061 low on a combination of factors, including hawkish ECB rhetoric and reports that Russian troops withdrew from key areas in Eastern Ukraine following a counterattack over the weekend.

- The JPY sits as the G10 laggard following hefty recovery gains on Friday, whilst Deputy Chief Cabinet Secretary Kihara was the latest to join the Japanese verbal intervention.

Fixed Income

- Recovery momentum is building towards a breach of big figures in the major contracts, with no major catalyst for the upside.

- Bunds, Gilts and the 10 year T-note recently topped out at 144.01, 105.87 and 115-30 respectively.

Commodities

- WTI and Brent futures are once again choppy as prices initially fell at the resumption of electronic trade, before recovering as European players entered the fray.

- Spot gold is firmer amid the softer Dollar, and eyes its 21 and 50 DMAs to the upside at USD 1,733.70/oz and USD 1,741.62/oz.

- Base metals in general are boosted by the weaker Dollar; 3M LME copper eyes USD 8,000/t to the upside.

- Russian official reiterates that some aspects of the grain deal need to be reviewed, via Interfax.

US Event Calendar

- Nothing on deck

DB’s Jim Reid concludes the overnight wrap

Keep an eye out for the monthly survey results published soon after this email arrives this morning. It’s fair to say that respondents are pretty bearish. Overall the whole report, which is in presentation form for the first time, should be a good guide to current sentiment.

One bit of potentially positive news over the weekend was that a Ukrainian counter offensive operation in the north-east of the country seems to have led to it successfully claiming back land. Although this will be greeted well by markets, the surprise success does increase the chances of a more aggressive response from Russia. In market terms, actual war developments have been relatively quiet of late with most of the focus on Russian gas (or lack of it) into Europe. So this brings the military progress back in some focus. So all eyes back on the next step from both sides.

For the rest of the week, there’s only one focal point and that’s the US CPI report tomorrow, the last before the Fed’s September 21st meeting. The Fed are now in their blackout period so that will reduce the central bank chatter somewhat this week. Our economists last week raised their forecast to a 75bps hike at next week’s meeting while keeping the terminal rate at 4.1% for early next year. They believe the risks are on the upside. See here for more on their latest thinking. Importantly for the Fed, on Friday, we will also get inflation expectations from the University of Michigan consumer survey. US Retail sales data on Thursday will also be closely watched too but is unlikely to move the dial for the Fed.

For US inflation, our economists expect a slight decline in the headline CPI number (-0.09% MoM) but an acceleration of +0.30% in core, which would continue the pattern from July’s reading (unchanged and +0.3%, respectively) which came in lower than expected. They believe the YoY headline CPI should fall five-tenths to 8.0%, while core should tick up a tenth to 6.0%.

The recent slump in commodities, with WTI firmly below $100 per barrel throughout the month, is likely to put downward pressure on the headline number as are gas prices being down -12% over the month. However, the resilience of the labour market is among the forces that could propel the core gauge higher. Expect a fair amount of attention on what now seems to be sharp falls in used cars after runaway price rises during covid. On the flip side our models suggest rents should continue to climb for a few more months before falling. So they’ll likely be a few opposing forces in the release.

Speaking of the consumer, we will get retail sales data for August on Thursday and our US economists expect a +0.6% MoM reading, up from last month’s flat print. As gasoline prices continue their downward trend, whether this assuages the inflationary pressures on consumer spending will be important. US PPI (Wednesday), business inventories and industrial production data (both Thursday) will provide more insight into supply-side pressures.

Turning to Europe now, and the BoE planned meeting has been postponed a week due to the period of mourning following the Queen’s death. However the UK will remain in the spotlight when it comes to economic data, with inflation (Wednesday), monthly GDP (today), retail sales (Friday) and labour market data (tomorrow) all due. For the record headline UK CPI is expected to stay at 10.1% YoY. Elsewhere in the region, we will also get the ZEW survey for Germany and the Eurozone tomorrow. Late on Friday our economists updated their GDP forecasts and with the NS1 gas shut off now looking terminal they expect 2023 GDP to fall -3 to -4%. To be fair their zero gas scenario earlier in the summer suggested -5 to -6% growth for 2023 but the impressive gas build over the intervening period means the worse case isn’t quite as bad as feared. Lots of moving parts though. See here for their update.

At the end of the week, an array of economic activity indicators will be out in China, in their usual monthly data dump, including industrial production, retail sales, new home prices and property investment (Friday). The gauges will follow this week’s downside surprises in trade data and inflation, so markets will be parsing the numbers to assess the magnitude of the economic softness. Our Chief China economist overviews the impact of China’s covid policy on its economy and mobility here and the team has downgraded their Q3 GDP forecast to 2.5% YoY (previously 3.5%).

Overnight in Asia equity markets have kicked off higher building on Friday’s broad-based rally on Wall Street amid thin trading this morning. As I type, the Nikkei (+1.11%) is trading higher while the S&P/ASX 200 (+1.09%) is also trading in positive territory on improved risk sentiment. Elsewhere, in mainland China, Hong Kong and South Korea markets are closed for a holiday.

In overnight trading, US stock futures are flat with contracts on the S&P 500 (-0.07%) and NASDAQ 100 (-0.06%) just below flat, so not much market reaction to the news out of Ukraine in the earliest hours of the week. Meanwhile, yields on the 10yr USTs (3.32%) are less than a basis point higher in Asia.

Over the weekend, Seiji Kihara a senior Japanese government official, expressed concerns about the yen’s slide by opining that the government must take necessary steps to counter excessive declines in the Japanese yen as the currency has weakened to a 24-year low versus the US dollar.

Crude oil prices are trading lower at the start of the week in early Asian trade as the imposition of strict COVID-19 restrictions in China is dampening the commodity’s demand outlook from the world’s second largest economy. As we go to print, Brent futures are down -1.41% at $91.53/bbl with the WTI futures (-1.47%) lower trading at $85.51/bbl.

Looking back at last week now and the magic number was 75, with the ECB and BoC delivering 75bp hikes, and pricing moving closer to certainty that the Fed would do the same at their September meeting next week. In line sovereign yields legged higher in advanced economies. Notably, risk sentiment held in though, driving equities up on the week.

Starting with bonds, the ECB raised rates +75bps, with President Lagarde hinting more rate hikes were still forthcoming, noting inflation was “far too high” and policy rates were “far away” from adequate levels to bring inflation down. The entire bund curve shifted higher, albeit with some flattening, given the stricter stance in policy. 2yr bunds climbed +22.6bps (-0.7bps Friday) and 10yr bunds were +17.3bps higher (-1.9bps Friday) on the week. 10yr BTPs kept the pace, increasing +17.6bps over the week (+4.4bps Friday).

EU energy ministers met Friday, agreeing a comprehensive plan was necessary to combat the current gas crisis. While specifics weren’t agreed upon (as expected), they noted a wide suite of tools – including gas price caps, emergency liquidity for utilities, and further demand reduction plans – would be leveraged. In the first trading week since the announcement that Nord Stream 1 flows would not resume due to a “leak”, European natural gas futures prices actually fell -3.53% on the week (-6.10% Friday). Part of that was probably from the tough talk from energy and fiscal ministers, but there was probably also an element of taking out risk premium; NS1 flows can’t go below zero so we are possibly getting closer to peak bad news. However as my CoTD (link here) showed on Friday, next winter could also be pretty tough for gas supplies in Europe. But I suppose at least we should know that by now. The lack of upward follow through in gas prices contributed to better risk sentiment over the week with the STOXX 600 climbing +1.06% (+1.52% Friday), and the DAX scraping out a modest +0.29%, helped by a +1.43% bump on Friday.

In the US, Chair Powell took his last opportunity before the September meeting blackout period to express a steadfast resolve in the fight against inflation, which left the market pricing +72.7bps of tightening at the September meeting, so pretty close to a full +75bp hike priced in, and pricing of terminal rates breaching 4% early next year, finally catching up closing to the long standing house view. Treasury yields sold off and the curve flattened like their European counterparts. 2yr Treasuries were +16.9bps higher (+5.3bps Friday) and 10yrs increased +12.0bps (-0.7bps Friday), leaving the 2s10s curve at -25.3bps. The S&P 500 was strong, increasing +3.65% (+1.53% Friday), while the interest rate sensitive NASDAQ was very resilient in the face of tighter Fed policy and up +4.14% (+2.11% Friday).

AND NOW NEWSQUAWK

European bourses extend on the upside seen at the open; DXY briefly dips under 108.00 – Newsquawk US Market Open

MONDAY, SEP 12, 2022 – 06:26 AM

- European bourses extend on the upside seen at the open; US equity futures are posting gains with marginal outperformance seen in the NQ vs peers

- DXY recoiled further to its lowest level since late August in early hours, EUR/USD was boosted towards 1.0200 at one point, JPY remains the G10 laggard

- Recovery momentum is building towards a breach of big figures in the major fixed income contracts, with no major catalyst for the upside

- WTI and Brent futures are once again choppy as prices initially fell at the resumption of electronic trade, before recovering as European players entered the fray

- Looking ahead, highlights include a speech from ECB’s Schnabel and supply from the US

For the full report and more content like this check out Newsquawk

Try a 14-day trial with Newsquawk and hear breaking trading news as it happens.

12th September 2022

- Click here for the Week Ahead preview.

GEOPOLITICS

RUSSIA-UKRAINE

- Russian forces have withdrawn from key towns in Eastern Ukraine as the Ukrainian counter-attack has made further progress, according to the BBC