by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1669.70 DOWN $4.80

SILVER: $19.35 DOWN $0.02

ACCESS MARKET:

GOLD $1675.60

SILVER: $19.54

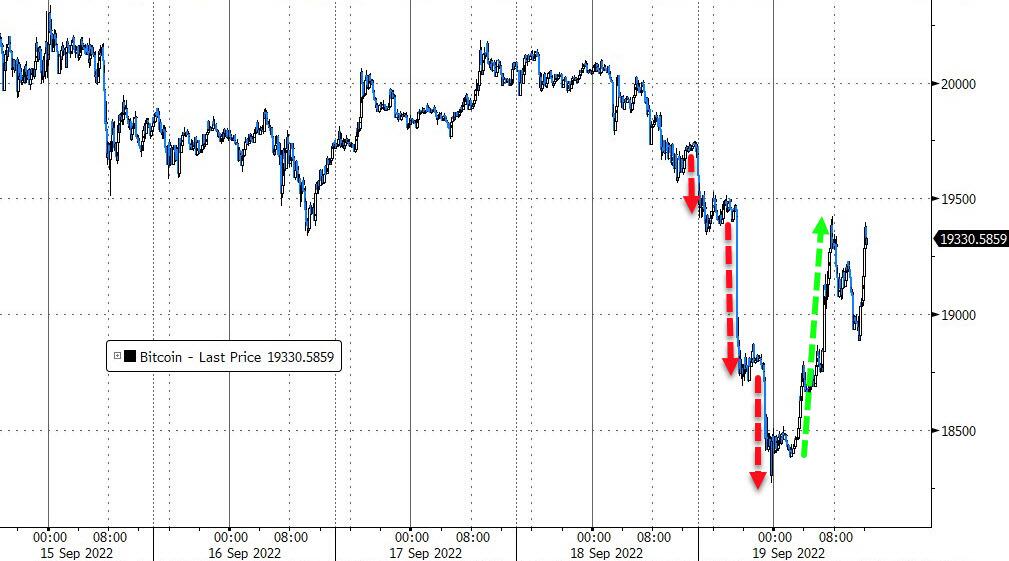

Bitcoin morning price: $18682 DOWN 913

Bitcoin: afternoon price: $19,479 DOWN 116

Platinum price closing UP $12.25 AT $918.70

Palladium price; closing UP $93.40 at $2216.40

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,671.700000000 USD

INTENT DATE: 09/16/2022 DELIVERY DATE: 09/20/2022

FIRM ORG FIRM NAME ISSUED STOPPED

323 C HSBC 231

435 H SCOTIA CAPITAL 19

624 H BOFA SECURITIES 4

657 C MORGAN STANLEY 1

661 C JP MORGAN 409 162

737 C ADVANTAGE 1 3

800 C MAREX SPEC 4 8

905 C ADM 12

TOTAL: 427 427

MONTH TO DATE: 5,760

________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR SEPT CONTRACT:

427 NOTICES FOR 42,700 OZ //1.328 TONNES

total notices so far: 5760 contracts for 576,000 oz (17.916 tonnes)

SILVER NOTICES: 31 NOTICES FILED FOR 155,000 OZ/

total number of notices filed so far this month 6459 : for 32,295,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $4.80

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: //// A WITHDRAWAL OF 1.16 TONNES FROM THE GLD/

INVENTORY RESTS AT 960.85 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $.02

AT THE SLV// ://GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 8.108 MILION OZ INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 477.738 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A SMALL SIZED 293 CONTRACTS TO 134,211. AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.08 GAIN IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.08) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD A HUGE OF 1025 CONTRACTS ON OUR TWO EXCHANGES DUE TO A GIGANTIC ISSUANCE OF 1220 EFP CONTRACTS,; WE DID HOWEVER HAVE STRONG SPECULATOR SHORT LIQUIDATIONS

WE MUST HAVE HAD:

I) STRONG SPECULATOR SHORT LIQUIDATIONS ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A POWERFUL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 200,000 OZ QUEUE JUMP / // V) SMALL SIZED COMEX OI LOSS/(//CONSIDERABLE SPEC LIQUIDATION/)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -118

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTACTS for 12 days, total 11,582 contracts: 57.910 million oz OR 4.825 MILLION OZ PER DAY. (965 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 57.910 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 57.910 MILLION OZ///

RESULT: WE HAD A VERY SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 293 DESPITE OUR $0.08 GAIN IN SILVER PRICING AT THE COMEX// FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A GIGANTIC SIZED EFP ISSUANCE CONTRACTS: 1200 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /GOOD BANKER ADDITIONS A// CONSIDERABLE NET SPEC SHORT ADDITIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 200,000 OZ QUEUE JUMP // .. WE HAD A VERY STRONG SIZED GAIN OF 1025 OI CONTRACTS ON THE TWO EXCHANGES FOR 5.125MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 31 NOTICE(S) FILED TODAY FOR 155,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 5809 CONTRACTS TO 465,469 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:—714 CONTRACTS.

.

THE STRONG SIZED DECREASE IN COMEX OI CAME DESPITE OUR RISE IN PRICE OF $5.70//COMEX GOLD TRADING/FRIDAY / WE MUST HAVE HAD MAJOR SPECULATOR SHORT COVERINGS ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD MINOR LONG LIQUIDATION //AND //CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 8.401 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 19,300 OZ //NEW STANDING 18.463 TONNES

YET ALL OF..THIS HAPPENED WITH OUR RISE IN PRICE OF $5.70 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A SMALL SIZED LOSS OF 1321 OI CONTRACTS 4.108 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4488 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 465,469

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 607 CONTRACTS WITH 5095 CONTRACTS DECREASED AT THE COMEX AND 4488 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 607 CONTRACTS OR 1.888 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4488) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (5809): TOTAL LOSS IN THE TWO EXCHANGES 1321 CONTRACTS. WE NO DOUBT HAD 1) CONSIDERABLE SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS/// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 8.409 TONNES FOLLOWED BY TODAY’S QUEUE. JUMP OF 19,300 oz. 3) MINOR LONG LIQUIDATION//// //.,4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

33,654 CONTRACTS OR 3,365,400 OZ OR 104.67 TONNES 12 TRADING DAY(S) AND THUS AVERAGING: 2804 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21 TRADING DAY(S) IN TONNES: 104.67 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 104.67/3550 x 100% TONNES 2.95% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 104.67 TONNES (SLIGHTLY RISING THIS MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT., FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER,FELL BY A SMALL SIZED 293 CONTRACT OI TO 134,211 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1200 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 1200 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1200 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 175 CONTRACTS AND ADD TO THE 1200 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 907 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 4.535 MILLION OZ

OCCURRED WITH OUR GAIN IN PRICE OF $0.08

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

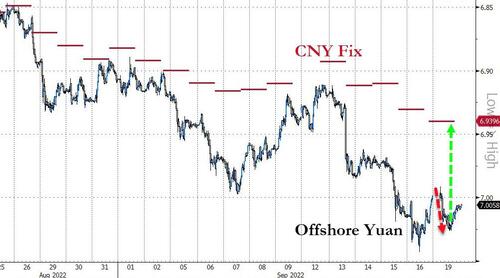

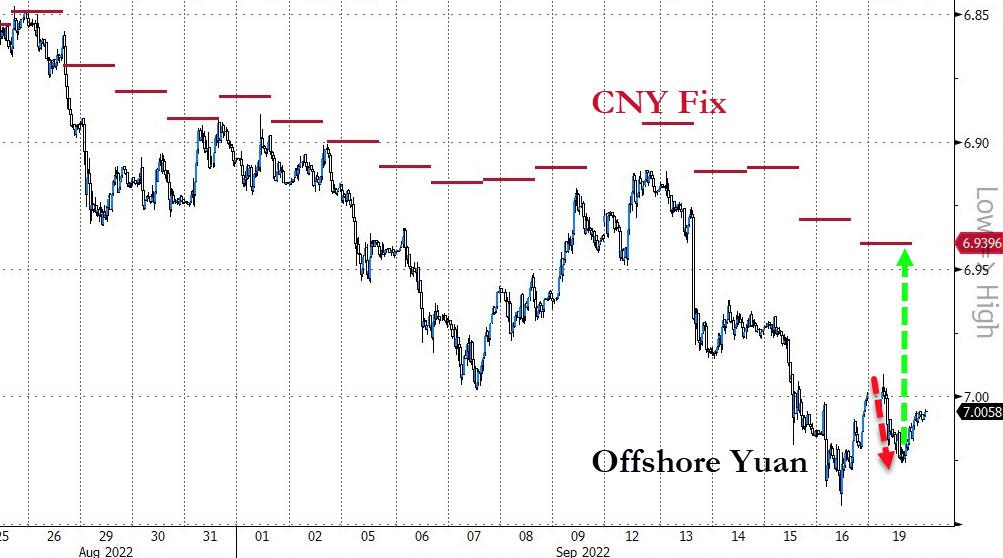

SHANGHAI CLOSED DOWN 10.80 PTS OR 0.35% //Hang Sang CLOSED DOWN 195.73 PTS OR 1.04% /The Nikkei closed HOLIDAY //Australia’s all ordinaires CLOSED DOWN 0.38% /Chinese yuan (ONSHORE) closed DOWN AT 7.0137//OFFSHORE CHINESE YUAN DOWN 7.0185// /Oil DOWN TO 82.77 dollars per barrel for WTI and BRENT AT 89.03 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 5809 CONTRACTS TO 465,469 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX DECREASE OCCURRED DESPITE OUR RISE IN PRICE OF $5.70 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A GOOD SIZED EFP (4488 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4488 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :4488 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4488 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED SIZED TOTAL OF 1321 CONTRACTS IN THAT 4488 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 5809 CONTRACTS..AND THIS SMALL GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR RISE IN PRICE OF GOLD $5.70. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING SEPT (18.463),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 18.463 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $5.70) BUT WERE SUCCESSFUL IN KNOCKING OFF SOME MINOR SPECULATOR LONGS AS WE HAD A SMALL SIZED TOTAL LOSS ON OUR TWO EXCHANGES OF 607 CONTRACTS // COMMERCIAL LONGS HUGELY ADDED TO THE POSITIONS, AND SPECULATOR SHORTS TRIED TO COVER ON THEIR POSITIONS////// WE HAVE REGISTERED A SMALL LOSS OF 607 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR SEPT. (18.463 TONNES)…

WE HAD 714 CONTRACTS ADDED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 1321 CONTRACTS OR 132,100 OZ OR 4.108 TONNES

Estimated gold volume 138,461/// poor//

final gold volumes/yesterday 232,490/ fair

INITIAL STANDINGS FOR SEPT ’22 COMEX GOLD //SEPT 19

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 41,912.247 oz Brinks Loomis includes 4 kilobars/Brinks |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 427 notice(s) 42700 OZ 1.328 TONNES |

| No of oz to be served (notices) | 176 contracts 17600 oz 0.5474 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5760 notices 5760 OZ 17.916 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

2 customer withdrawals:

i) Out of Brinks: 128.600 oz 4 kilobars

ii) Out of Loomis: 41,683.647 ( oz)

total: 41,912.247 oz

total in tonnes: 1.305 tonnes

Adjustments: 1

Brinks/dealer to customer: 251,356.518 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPT.

For the front month of SEPT we have an oi of 603 contracts having LOST 276 contracts .

We had 469 notices filed on FRIDAY so we gained a whopping 193 contracts or an additional 19,300 oz

will stand for gold in this very non active delivery month of September.

October gained 1144 contracts DOWN to 43,212. Oct is generally a poor active delivery month. It may change!! (Look for a very unusually large delivery month.)

November gained 51 contracts to stand at 285

December lost 6255 contracts DOWN to 376,771

We had 427 notice(s) filed today for 42,700oz FOR THE SEPT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 409 notices were issued from their client or customer account. The total of all issuance by all participants equate to 427 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 162 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2022. contract month,

we take the total number of notices filed so far for the month (5760) x 100 oz , to which we add the difference between the open interest for the front month of (SEPT603 CONTRACTS) minus the number of notices served upon today 427 x 100 oz per contract equals 593,600 OZ OR 18.463 TONNES the number of TONNES standing in this NON active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month:

No of notices filed so far (5760) x 100 oz+ (603) OI for the front month minus the number of notices served upon today (427} x 100 oz} which equals 574,300 oz standing OR 18.463 TONNES in this NON active delivery month of SEPTEMBER.

TOTAL COMEX GOLD STANDING: 18.463 TONNES (A HUMONGOUS STANDING FOR A SEPT ( NON ACTIVE) DELIVERY MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,436,250.551 oz 75.77 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 27,089,536.444 OZ

TOTAL REGISTERED GOLD: 13,030,951.043 OZ (405.317 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 14,058,585.401 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,794.701. OZ (REG GOLD- PLEDGED GOLD) 335.76 tonnes//rapidly declining

END

SILVER/COMEX/SEPT 19

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,328,654.855oz BRINKS CNT HSBC JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,267,157.650 oz Loomis CNT Delaware |

| No of oz served today (contracts) | 31 CONTRACT(S) 155,000 OZ) |

| No of oz to be served (notices) | 141 contracts (705,000 oz) |

| Total monthly oz silver served (contracts) | 6459 contracts 32,295,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 3 deposits into the customer account

i)Into CNT: 600,382.200oz

ii) Into Delaware: 559,298.560 oz

iii) IntoLoomis: 107,476.900 oz

total deposit: 1,267,157.680 oz

JPMorgan has a total silver weight: 165.282 million oz/319.156million =51.75% of comex

Comex withdrawals: 4

i) Out of Brinks: 13,551.100 oz

ii) Out of CNT 92,653.350 oz

iii) out of HSBC 600,559.400 oz

iv) Our of JPMorgan: 620,882.760 oz

total: 1,328,654.855 oz

adjustments: 1//dealer to customer

Brinks 300,538.150 oz

2. customer to dealer CNT 9750.050 o

3. customer to dealer Delaware 48,290.710 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 44.274 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 319.156 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF SEPT OI: 172 CONTRACTS HAVING LOST 19 CONTRACT. WE HAD

59 CONTRACTS SERVED ON FRIDAY SO WE GAINED 40 CONTRACTS OR AN ADDITIONAL

200,000 OZ WILL STAND FOR METAL IN THIS VERY ACTIVE MONTH OF SEPT.

WE WILL GAIN IN TOTAL SILVER STANDING EACH TRADING DAY UNTIL THE END OF THE MONTH

(CONTINUAL QUEUE JUMPING BY OUR BANKERS SEARCHING FOR SILVER METAL)

OCTOBER GAINED 1 CONTRACT TO STAND AT 518 CONTACTS.

NOVEMBER GAINED 3 CONTRACTS TO STAND AT 57

DECEMBER SAW A LOSS OF 509 CONTRACTS DOWN TO 119,271

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 31 for 155,000 oz

Comex volumes:74,106// est. volume today// good

Comex volume: confirmed yesterday: 86,127 contracts ( good)

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 6459 x 5,000 oz = 32,295,000 oz

to which we add the difference between the open interest for the front month of SEPT(172) and the number of notices served upon today 31 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT./2022 contract month: 6,459 (notices served so far) x 5000 oz + OI for front month of SEPT (172) – number of notices served upon today (31) x 5000 oz of silver standing for the SEPT contract month equates 33,000,000 oz. .

We have an inventory of 44.516 million oz of registered silver at the comex so Sept delivery of 33.000 MILLION OZ represents 74.13% of that category of silver.

If we add August’s final delivery (to Sept) for silver at 5.51 million oz, we have a total of 38.51 million oz delivered upon with a REGISTERED INVENTORY of 44.515 million oz or 86.506% of that category of silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:41,262// est. volume today// poor

Comex volume: confirmed yesterday: 59,964contracts ( poor)

END

GLD AND SLV INVENTORY LEVELS

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

GLD INVENTORY: 960.85 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTO THE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

CLOSING INVENTORY 477.738 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: FedEx Exposes The Myth Of The “Soft Landing”

MONDAY, SEP 19, 2022 – 12:05 PM

Inflation continues to surprise to the upside. Meanwhile, the economy continues to surprise to the downside. But the markets continue to believe that the Federal Reserve can slay the inflation monster while still guiding the economy to a so-called “soft landing.” FedEx announced some news last week that undercuts this narrative. In his podcast, Peter Schiff talked about why the landing is going to be hard. And when the economy crashes, the Fed inflation fight will be over.

Peter said in the short run, investors are not reacting properly to what’s going on.

I knew we were getting higher inflation. I knew we were getting weaker growth. Most people didn’t know that. But what’s still happening is every time investors are surprised with a hotter-than-expected inflation number, that makes them feel that the Fed is now going to have to fight harder to bring inflation back down to 2%. Nobody doubts the Fed’s resolve, or its ability to bring inflation back down to 2%. So, the higher inflation goes, the harder everybody expects the Fed to fight to win. And that keeps propping up the dollar, and that keeps suppressing gold.”

Peter said he has no idea when the markets are going to figure out that higher inflation just means the Fed is losing the fight, and no matter how hard it fights, it’s going to keep losing.

It’s not fighting hard enough because it can’t.”

Even if the Fed comes out with a 100-basis point hike this week, real rates will remain at -5%.

In what universe can you fight inflation with negative five percent real rates? You can’t, It is impossible.”

As Peter said in a previous podcast, the Fed falls further behind the inflation curve every time it hikes.

The Fed won’t succeed in killing inflation. But it will kill the economy. And that’s because it’s a bubble. The entire economy is based on artificially low interest rates.”

The economy can’t just levitate in midair. It has to fall down when the monetary supports are pulled out from under it.

There is no way to normalize interest rates after more than a decade of abnormally low interest rates and not let everything come toppling down.”

There are already signs that the economy is shaky. We’ve already had two quarters of negative GDP growth and the Atlanta Fed lowered its Q3 estimate to 0.5% last week. The housing market is falling apart. And last week, FedEx dropped a bombshell, announcing office closures and layoffs due to falling demand for shipping.

As Peter pointed out, it’s no wonder that package volume is dropping. Consumers are spending more, but they’re not buying more stuff. They’re just paying more for everything. FedEx exposes the underlying rot in the economy, and it’s going to get worse. Peter said when that happens, the Fed will abandon the inflation fight.

Layoffs are coming as real spending is going down, and that’s when the Fed ultimately is going to pivot. Once the economy really starts to buckle, the Fed is going to turn.”

Peter said he thinks the only reason Federal Reserve Chairman Jerome Powell continues to talk tough about fighting inflation is because he’s still delusional enough to think he can do it without destroying the economy. Powell still thinks he can manage a “soft landing.” He’s willing to put the economy in a mild recession and allow unemployment to tick up a little bit.

That would be getting out of Dodge with barely a scratch. So yes, he’s willing to do that. But is he willing to create a worse financial crisis than 2008? Is he willing to put the economy in the equivalent of a depression — great recession worse than we had in 2008? Of course not! He has zero tolerance for that.”

But Powell still doesn’t expect that, nor does anybody else in the mainstream. Most people concede that the US economy will move into a recession. But everybody thinks it will be “short and shallow.” But how do they know that? Why should it be short and shallow? As Peter pointed out, the bust needs to be proportional to the boom.

We’ve never had a boom this big. We’ve never had interest rates this low for this long. We’ve never had an economy more screwed up than the one we have right now. We’ve never had bigger asset bubbles, bigger debt bubbles, more misallocations of capital and resources. So, we have more mistakes that we need to fix now than ever before. So, how are we going to do that with a short shallow recession? We’re not. It’s going to be a massive recession. And again, the Fed has no stomach for that, and that’s why the Fed is going to pivot.”

And of course, this pivot is going to happen when inflation is still well above 2%. If the Fed goes back to zero percent interest rates and quantitative easing, it’s going to drive inflation even higher.

In other words — stagflation.

In this podcast, Peter also talks about silver as the silver lining in gold’s cloud, the declining stock market, the likelihood of a Black Monday in the near future, why bonds may crash harder than stocks, and the implications of that crash.

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

(Mathew Piepenburg)

a must read…

Jay Powell: A Breathing Weapon Of Mass Destruction?

SATURDAY, SEP 17, 2022 – 10:30 AM

Authored by Matthew Piepenburg via GoldSwitzerland.com,

Below we track how the Powell Fed serves as a contemporary weapon of mass destruction.

Powell’s so-called “war against inflation” will fail, but not before crushing everything from risk asset, precious metal and currency pricing to the USD. As importantly, Powell is accelerating global market shifts while sending a death knell to the ignored middle class.

Let’s dig in.

The Fed: Creators of Their Own Rock & Hard Place

In countless interviews and articles, we have openly declared that after years of drunken monetary driving, the Fed has no good options left and is literally caught between an inflationary rock and a depressionary hard-place.

That is, hawkishly tightening the Fed’s monthly balance sheet (starting in September at $95B) while raising the Fed Funds Rate (FFR) into a recession was, is and will continue to be an open head-shot to the markets and the economy; yet dovishly mouse-clicking more money (i.e., QE) would be fatally inflationary.

Again, rock and a hard place.

What’s remarkable and unknown to most, however, is that the Chicago Fed recently released a white paper during the Jackson Hole meeting which says the very same thing we’ve been warning: Namely, that Powell’s WMD “Volcker 2.0” stance (arrogance/delusion) is only going to make inflation (and stagflation) worse, not better.

To quote the Chicago Fed:

“In this pathological situation, monetary tightening would actually spur higher inflation and would spark a pernicious fiscal stagflation, with the inflation rate drifting away from the monetary authority’s target and with GDP growth slowing down considerably. While in the short run, monetary tightening might succeed in partially reducing the business cycle component of inflation, the trend component of inflation would move in the opposite direction as a result of the higher fiscal burden.”

In short, Powell can’t be Volcker.

Why?

Simple.

America Can’t Afford Powell (or His Rate Hikes)

This hard reality is economic and mathematical, not political or psychological, though Powell suffers from both political delusion and a psychological lack of self/historical awareness…

I’d like to ask Powell, for example, how the US plans to pay for its now rate-enhanced (i.e., even more expensive) debts and obligations regarding defense spending, Treasury obligations, social security and health care when just the interest payments alone on Uncle Sam’s current bar tab are unsustainable?

Powell, part of the so-called “independent Fed,”will now have to make a political choice (and trust me, the Fed IS political): Will he A) intentionally seek to crash the economy into the mother of all recessions to “fight” the inflation his own private bank’s balance sheet singularly created, or B) will he help turn America into the Banana Republic that it is already becoming by printing (debasing) trillions more US “dollars”?

The “inflation-fighting” Powell, embarrassed to go down in history as the next Arthur Burns, may just A) continue to hike rates and strengthen the USD (currently bad for gold), which is sending America to its knees, or B) sometime this autumn he’ll cave, pivot and let inflation rip (while the BLS, of course, under-reports inflation (i.e., lies) by at least ½).

In the meantime, we can only watch markets and economic conditions continue to tank as interest rates and the USD climbs toward a peak before the USD makes a record-breaking fall.

And why do I see a fall?

Easy.

The Credit Markets Are Screaming “Oh-Oh!”

To borrow/twist from Shakespeare: “The bond market is the thing.”

Everything, and I mean everything, hinges on credit markets. Even the cancerously expanding US money supply(M0-M4) is at root just 95% bank credit.

Understanding credit markets is fairly simple. When the cost of debt is cheap, things (from real estate to growth stocks) feel good; when the cost of debt is high (as measured by the FFR, but more importantly by the fatally rising yields on the US10Y), things collapse.

We saw the first (and media-ignored) warnings of this collapse in September of 2019 when the oh-so critical (yet media ignored) repo markets imploded, none of which can be blamed on COVID (2020), Putin (2022) or climate change.

As dollar liquidity dries up, so will markets, economies and lifestyles. Remember: All market crises are, at root, just liquidity crises.

A Summer of Credit Drought

As previously warned, signs of this drying liquidity are literally everywhere. The Fed’s own Quarterly Loan Officer Survey confirms that banks are lending less.

And given that 70% of the US bond market is composed of junk, high-yield and levered loans (i.e., the worst students in the class hitherto priced as PhD candidates), the rigged game of debt roll-overs and stock buy-backs is about to end in a stock and bond market near you as rates rise to unpayable levels.

Furthermore, it’s worth noting that US banks (levered 10X) and European banks (levered 20X due to years of negative nominal rates), will now use rising rates as the long-awaited excuse to de-lever their bloated balance sheets, which is fatal to risk asset markets.

Even more alarming, however, is what this de-leverage will mean to that massive, USD-based and expanding (1985 to now) Weapon of Mass Destruction otherwise known as the OTC and COMEX derivative markets.

Rather that expand, this fatal market will contract—all of which will have massive implications for the USD as debt markets slowly turn from a past euphoria to a current nightmare.

The Dangerous USD Powell Ignores

Measured by the DXY, the Dollar is ripping.

But you’ll note that Powell and his “data points” never address the Dollar.

Powell, like most DC-based Faustian deal-makers, lives in a US-centric glass house, which ignores the rest of the world (namely Emerging Markets, oil producers and mislead “allies”) who are de-dollarizing (i.e., repricing the USD) as I type this.

In case Powell never took an econ history class or read a newspaper that was not written in English, it might be worth reminding him that EM nations like Venezuela, Lebanon, Argentina, Turkey, and Sri Lanka, as well as, of course, the BRICS themselves, are tired of importing US inflation and paying trillions and trillions of Dollar-denominated debt or forced dollar-settled oil purchases.

As the Fed artificially strengthens the USD via rate hikes, debt-soaked nations are forced to either: A) debase their currencies to pay their debts (which might explain Argentina’s 69.5% official interest rate) or B) raise rates and look elsewhere for new trading partners or money.

Even “developed” economies are seeing their currencies at record lows vis-à-vis the rising USD (Japanese Yen at 50-year lows, UK’s currency at 37-year lows and the euro now at 20-year lows).

And as for those cornered EM nations, $650B of the IMF’s 2021 usurious (and dollar-based) loans to them have already dried up.

EM Markets Looking East Not West

So, where will EM countries go trade, survival, better energy pricing, and even fairer gold pricing?

The answer and trends are now open and obvious: East not West, and away from (rather than toward) the USD.

Russia and China are making trade and currency deals not only with the BRICS at a rapid pace, but with just about every nation not otherwise “friendly” (i.e., forced to be) with the USA (and which “friends” now face a cold winter on this side of the Atlantic.)

Even the notoriously corrupt LBMA gold market, which spends its every waking hour using forward contracts to artificially crush the paper gold price, is about to see a Moscow-based new gold exchange (the Moscow Gold Standard).

Of course, such a Moscow exchange makes sense given that 57% of the world’s gold comes from Eurasian zip codes where a post-sanction Putin sees yet another golden opportunity to fix what the West has broken.

Furthermore, and as stated above, as the derivatives markets de-lever, demand for the USD (and hence dollar-strength) will equally tank, as OTC settlements are done in USD, not Pesos, Yen, euros or Yuan.

As we warned within weeks of the failed sanctions against Putin, the world is de-dollarizing slowly yet steadily, and once the DXY inevitably slides from 108, to 107 and then below 106, the Greenback’s fall will mirror Hemingway’s description of poverty: “Slowly then all at once.”

For the last 14 months, the Dollar Index has been trading above its quarterly moving average, which as the always-brilliant Michael Oliver reminds, is like a runner who never exhales. At some point the USD’s lungs will collapse.

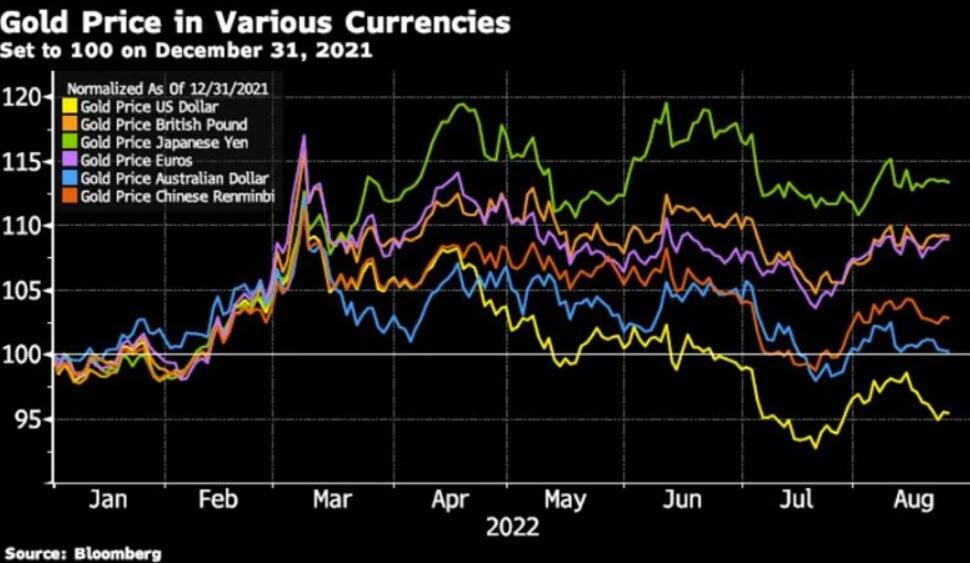

Gold: Waiting for the USD to Snap

The foregoing and seismic shifts in the derivative and EM markets portend the sick finale of the USD, and hence for the currently repressed gold price. In short: As the former tanks, the latter surges.

Many are nevertheless angry that gold hasn’t ripped in a world of geopolitical risk and rising/persistent inflation, but that’s because the artificially rigged USD has been their only (and short-lived) measure.

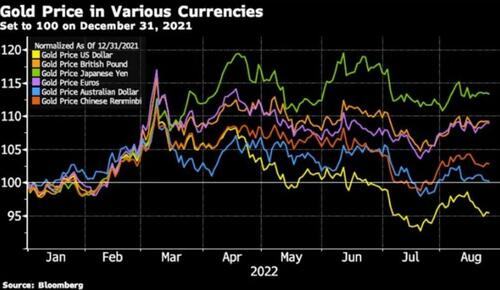

As risk assets in the US and around the world experience double-digit declines, gold in every major currency but the USD has been rising, not falling:

And even gold’s relative decline in US markets remains minimal compared to double-digit losses in traditional US risk-parity (i.e., stock/bond) portfolios for 2022.

A COMEX in Transition

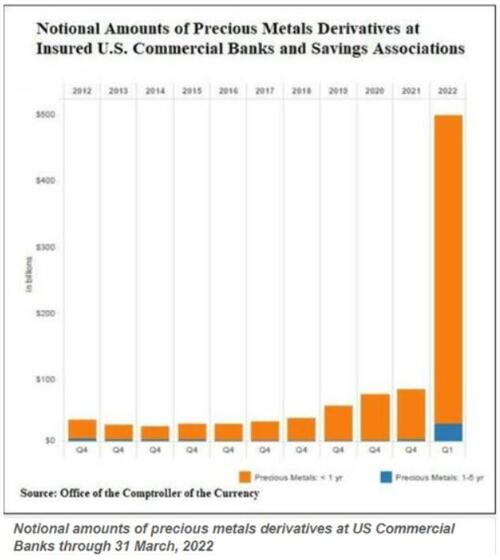

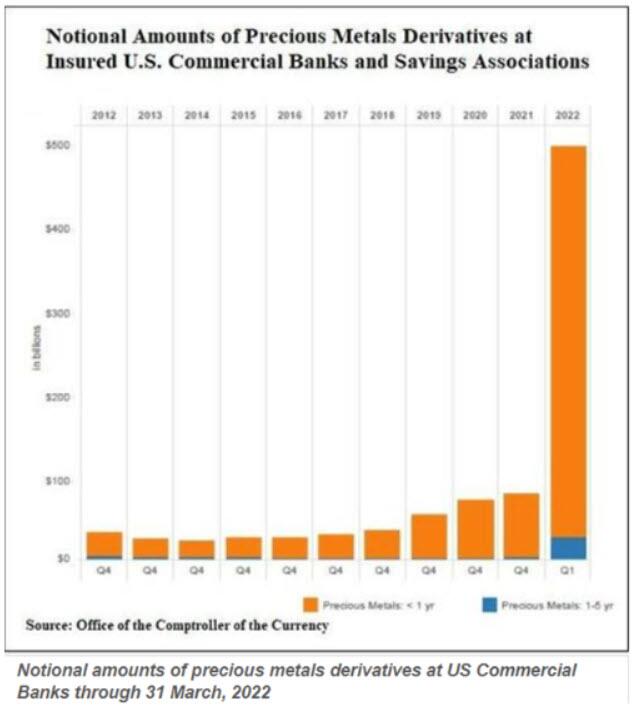

You also may have overlooked that those fat foxes over at the BIS recently unwound 90% of their gold swaps (from 500 to 50 tons) at precisely the same pace that JP Morgan and Citibank (which hold/control 90% of the US commercial banking gold derivatives) just expanded the notional value of their gold derivatives by 520% (!).

Anyone and everyone in the precious metals markets knows that the notional value of those contracts over-shoots the actual supply of the physical metal by 99%.

The COMEX is a nothing more than a legalized fairytale (fraud) whose non-fictional pains (and gold surges) are inevitable.

In the meantime, however, many players in the COMEX markets (the precious metal exchange in NY) are now (and increasingly) looking to take delivery of real rather than paper gold.

Why?

Because they see the writing on the wall.

Gold is a monetary metal not a paper card trick. The COMEX players want to get as much physical metal as they can before false idols like Powel and the global EM currents flowing East take down the USD’s post-Bretton Woods hegemony.

When/as that happens, gold does what it always does when nations and their debased currencies tank: It rises.

And you can be sure that JP Morgan and Citi will keep the paper gold price low until they have enough of the physical gold in hand when gold rips and the USD sinks.

For Now, More Lies, Empty Phrases and Distractions

In the meantime, Powell will act like the nervous captain of a sinking ship and play with rates and the USD as the DC information bureaus (i.e., BLS) spread more open fictions and false distractions on everything from the inflation and unemployment rate to suddenly forgotten viral threats (?), the freedom of Ukraine or the political theme of climate change.

And of this you can also be certain: Powell will continue the Fed’s historical role of crushing the US working class.

Translating Powell’s “Softening Demand”

As Powell wandered Jackson Hole, he warned Americans to prepare for “softening demand,” which is a euphemism for crushing the middle class via rising rates and long-term (rather than “transitory”) inflation ahead.

This rich.

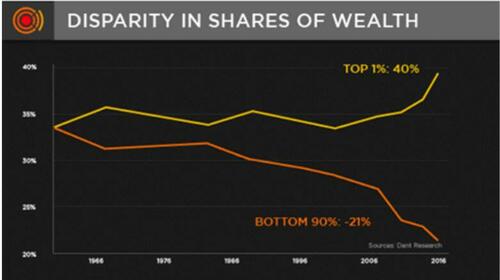

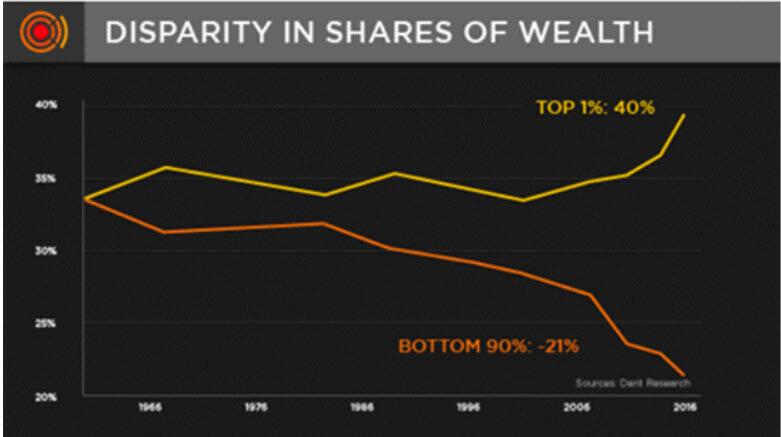

After being the sole tailwind for pushing equity markets up by hundreds of percentage points with mouse-click money since 2009, the Fed has made the top 10% (which owns 85% of the Fed-inflated stock market wealth) extremely rich.

Now, by deliberately cranking rates higher, Powell’s Fed is making the middle class (bottom 90%) even poorer.

Wealth inequality in the US has NEVER been higher, and this never bodes well for the future of an openly fracturing nation.

Indeed, inflation pains and rising rates certainly hurt all Americans.

For the wealthy, such inflationary pains sting; however, for the working class, they cripple.

And as far as this crippling effect of “softening demand” goes, we can blame that squarely on the narrow shoulders of such false idols like Greenspan, Bernanke, Yellen and Powell.

For years, they’ve been saying their mandate was to control inflation and manage employment.

But that employment (as confirmed by PWC, household surveys and our own two eyes) is about to see hiring freezes, downsizing and lay-offs as debt-soaked enterprises with tanking earnings and confidence levels cut costs and jobs.

Again: That’s not “softening,” that’s crippling.

But as I’ve shown in Rigged to Fail and Gold Matters, the Fed’s real mandate is providing (now increasingly scarce) liquidity to credit markets (and hence tailwinds for the equity markets), which benefit a minority, not a majority, of the population.

This easily explains Andrew Jackson’s prescient warning that a central bank simply boils down to the “prostitution of our government for the benefit of the few at the expense of the many.”

Truer words were never spoken, and we are now seeing these warnings playing out in real time, and will see even more pain ahead in this surreal new normal of “softening demand” and a current America of central-bank created serfs and lords.

Powell’s words, of course, do not match his or the Fed’s deeds, a profile flaw that has been hiding in plain site since the Fed’s not-so-immaculate conception in 1913.

The more that investors understand where the decisions are made and why, and the more they track the market signals (bond yields, credit markets and currency debasements), the more they can prepare for what is already here and what lies ahead.

GOLD/SILVER

END

3.Chris Powell of GATA provides to us very important physical commentaries

4. OTHER GOLD/SILVER COMMENTARIES

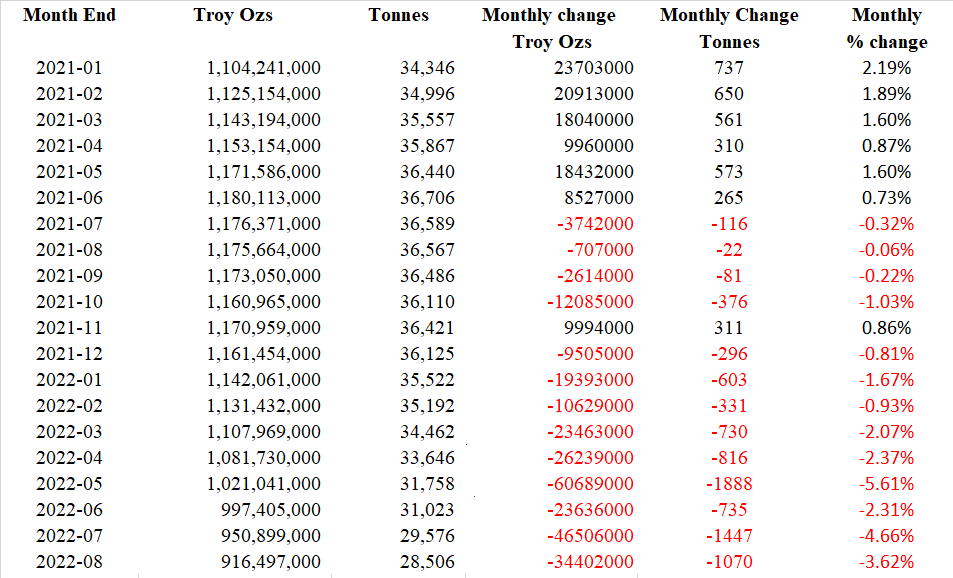

London Silver Inventories Continue To Plummet As Metal Exits LBMA Vaults

SATURDAY, SEP 17, 2022 – 08:10 AM

Submitted by Ronan Manly, BullionStar.com

There is an unprecedented situation emerging in London, where the relentless hemorrhaging of one of the world’s largest stockpiles of silver is now well and truly under way.

For the last 9 months, this stockpile of silver, held in the LBMA vaults in London, has been consistently falling each and every month, and has now reached an all time low (since vault holdings records began in July 2016).

These vaults comprise the precious metals storage facilities in and around London run by the bullion banks JP Morgan, HSBC and ICBC Standard Bank, as well as the London vaults of three security operators, namely Brinks, Malca-Amit and Loomis. Since the system of vaults is administered and coordinated by the London Bullion Market Association (LBMA), these vaults are collectively known as the ‘LBMA vaults’.

Back in July this year, BullionStar highlighted this developing trend in the article titled “LBMA Silver Inventories fall to a near 6 Year Low below 1 billion ounces”.

That article covered the vault data up to the end of June 2022, where the London silver holdings had reached the dubious milestone of having dropped below the 1 billion ounce level, specifically falling to 997.4 million ozs (31,022 tonnes).

London sub-Billion Market Association (LBMA)

Since then, however, the situation has only worsened. Latest data for July and August show that the downward trend is still very much intact. During July 2022, London silver inventories fell by another 4.66% month-on-month, with the vaults seeing an outflow of 46.5 million ozs of silver (1447 tonnes). This brought total LBMA London silver holdings down to 950.9 million ozs (29,576 tonnes), and a new all time low since records began. (Note the lowest previous low had been 951.4 million ozs at the end of July 2016).

Now that August 2022 vault data has been released (LBMA release vault data by the 5th business day of a new month), we can see that August saw no reprieve, because in August the London silver holdings fell by another 3.62% month-on-month, with the vaults seeing an outflow of 34.4 million ozs of silver (1070 tonnes). This brings the LBMA silver vault inventories down to 916.5 million ozs (28,506 tonnes).

In other words, during these two months of July and August 2022, the LBMA vaults have lost another 2517 tonnes of silver.

To put all of this into context, the Silver Institute estimates that world annual silver mining production will only be 843.2 million ozs this year. That’s 26,262 tonnes. So the LBMA vaults, with 28,506 tonnes as of the end of August 2022, now hold just less than one year’s mine supply of silver.

In addition, except for a blip during November 2021 in which LBMA silver inventories rose by 311 tonnes, the LBMA silver vaults have actually seen outflows for 13 of the last 14 months. This is because silver inventories in London also fell in each of the months of July, August, September and October 2021. Putting all of this together means that since the end of June 2021, the LBMA vaults in London have lost 8200 tonnes of silver (263.3 million ozs), and the vaults now hold silver representing just over one year’s mine production.

While LBMA silver inventories did rise during the first six months of 2021, the net outflow from January 2021 to the end of August 2022 is still 5102 tonnes. And people say there is no silver squeeze?

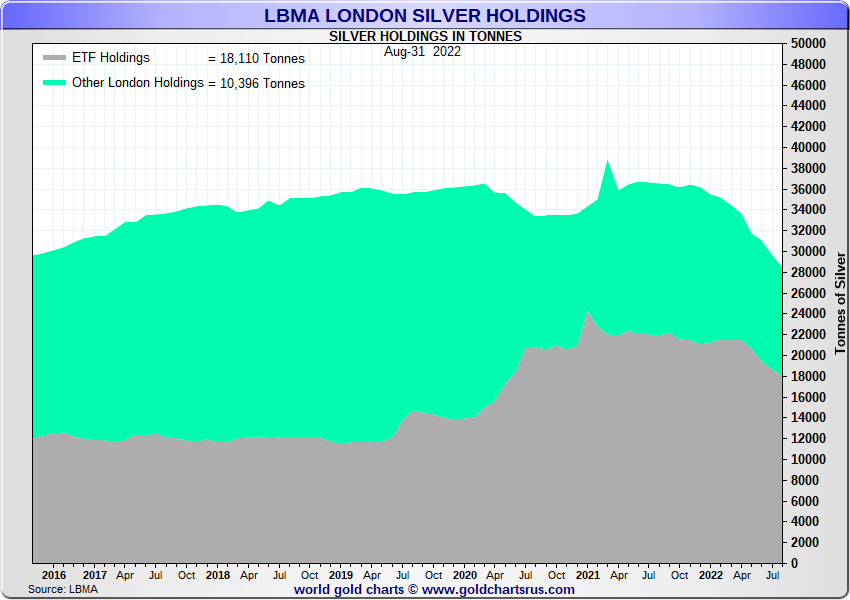

Backing this ETF silver out of the headline figure is thus even more revealing. According to the calculations of GoldCharts’R’Us, as of the end of August there were 18,110 tonnes of silver held by silver-backed ETFs which store their silver in London. This means that of the 28,506 tonnes of silver that the LBMA claims to be held in its London vaults, 63.5% of this is held in ETFs, and only 10,396 tonnes (36.4%) is not held by ETFs. This 10,396 tonnes also represents only about 40% of annual silver mining supply.

ETF Silver held in London

Just for completeness, I did some quick revised calculations to illustrate the amount of silver currently held by silver-backed ETFs and other ‘transparent’ silver holdings in London. These calculations are similar to the ETF silver calculations I did in July, and also similar to the methodology that is explained in the BullionStar article from February 2021 “‘Houston, we have a Problem’: 85% of Silver in London already held by ETFs.“

These calculations were done on 9 September using silver ETF bar lists dated 8 September. This ETF silver is held in the London vaults of JP Morgan, HSBC, Brinks, Malca Amit, and Loomis.

- SLV iShares Silver Trust 11,329.3 tonnes

- SSLN iShares Physical Silver ETC 707.5 tonnes

- PHAG Wisdomtree Physical Silver ETC 2,488.1 tonnes

- PHPP Wisdomtree Physical PM ETC 41.8 tonnes

- SIVR Aberdeen Physical Silver Shares ETF 1,450.3 tonnes

- GLTR Aberdeen PM Baskets shares ETF 377.5 tonnes

- PMAG ETFS Physical Silver 238.9 tonnes

- PMPM ETFS Physical PM Basket (part of PMAG total)

- SSLV Invesco physical silver ETC 356.6 tonnes

- 4 ETFs Xtrackers Physical silver ETCs (4 combined) 769.7 tonnes

Together these 13 ETFs currently hold 17,759.7 tonnes of silver in the LBMA London vaults.

The LBMA London vaults figures also include silver held by clients of BullionVault and GoldMoney. BullionVault clients hold 491.2 tonnes of silver in the LBMA vaults in London (same as at the end of June, while GoldMoney clients hold 186.8 tonnes in the LBMA vaults (one tonne less than in June). Adding these two figures to the ETF total means that as of 8 September 2022, there were 18,437.6 tonnes of silver held by silver-backed ETFs and private client investors in the LBMA London vaults, which to reiterate, has nothing to do with “London’s ability to underpin the physical OTC market”.

This means that of the 28,506.28 tonnes of silver as of the end of August 2022, only 10,068.7 tonnes of silver is not held in ETFs. And another caveat as usual: of the London silver not held in ETFs, some of this too represents allocated silver holdings of the wealth management sector, such as physical silver held by investment institutions, family offices and High Net Worth individuals.

So as more and more silver drains out of the LBMA London vaults due to continued strong global demand, the free float (the amount of silver that is available to ‘underpin’ trading), is diminishing.

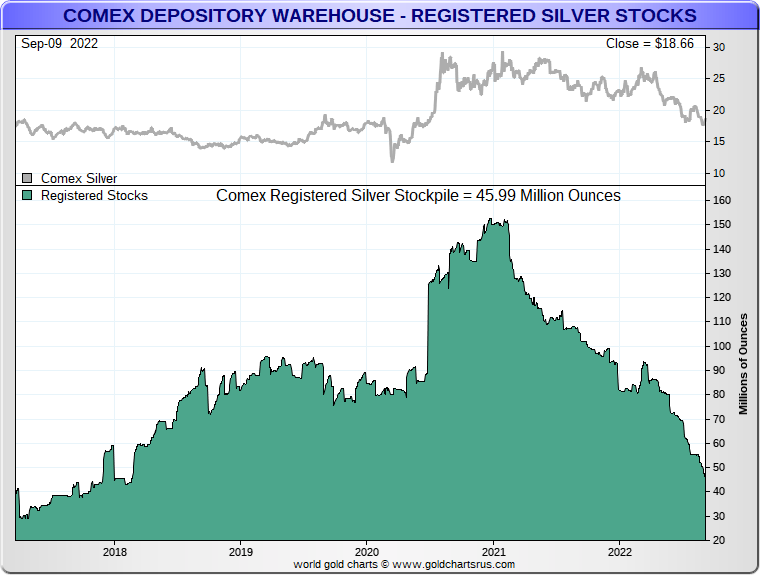

COMEX Silver also in Crisis

Over on COMEX in New York, the silver situation is also precarious, with ‘Registered’ silver inventories in the COMEX approved warehouses practically in freefall, and at a four and a half low. See the following chart. Latest figures for 9 September show that registered inventories (those that are warranted and available to back COMEX silver futures contract delivery) are now only 46 million ozs (1430 tonnes). This is insanely low. For example, more silver left the LBMA vaults during July 2022 (1447 tonnes) than there is currently in COMEX registered silver stockpiles.

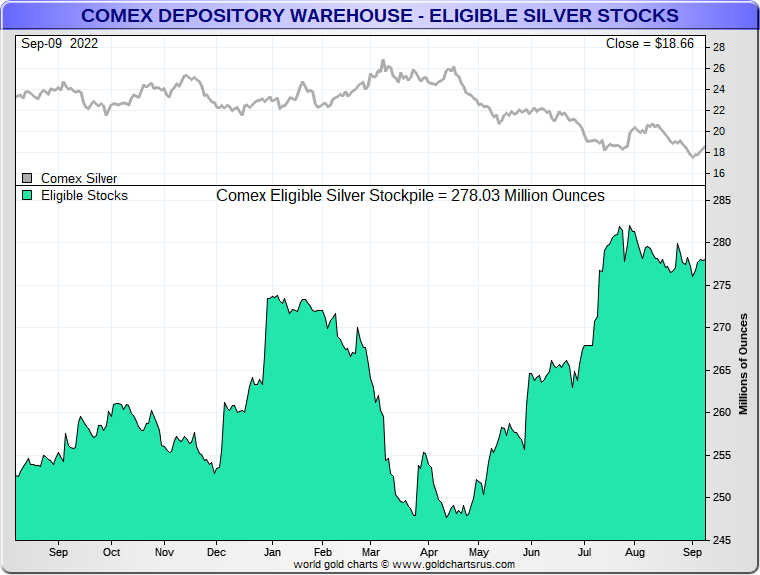

Regarding the COMEX category of ‘Eligible’ silver (which merely represents silver stored in the COMEX approved vaults which could be traded if it was put under warrant, but which realistically may have nothing to do with COMEX trading), the amount of silver in the COMEX eligible category hasn’t really fluctuated much so far in 2022 and has ebbed and flowed by about 30 million ozs (930 tonnes) within the 250-280 million ozs range. See the following chart.

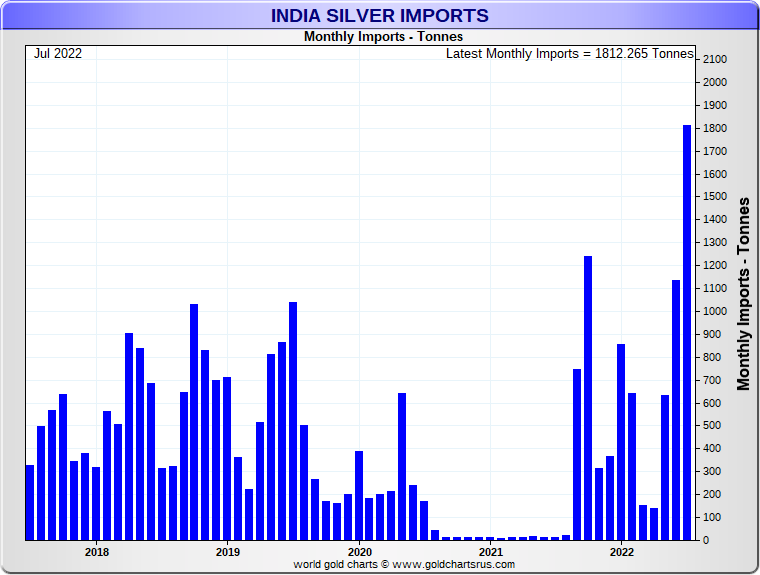

A Resurgence in Indian Silver Demand

Apart from 2022’s strong global investment and industrial demand for silver which is detailed by the Silver Institute here, there is now huge new physical demand entering at the margin, a case in point being India. Indian silver imports are now seeing some of their strongest monthly figures in recent years. See chart below which includes silver imports into India up to the end of July 2022.

Reports out of India also say that July has been a record month, according to the following interview with Metals Focus India.

LBMA bullion banks / ETF Authorised Participants appear to use London silver ETFs as a top up fund for physical silver, scaring the market by bringing the paper silver price lower and flushing out / triggering institutions and retail to sell ETF units, at which point the bullion banks pick up and convert these units, thereby obtaining extra metal that’s needed to meet physical demand. In fact, as physical silver demand rises, bullion banks will try to get the price lower so as to have access to the silver that is held by the ETFs.

But the bullion banks know that in the West, a higher silver price brings in more ETF buyers, which in turn leads to more of the silver that is in the LBMA vaults being ‘spoken for’ by the ETFs. Which is why the bullion banks have a vested interest in keeping a lid on the silver price, because they don’t want a situation (such as early 2021) where ETF investor demand gobbles up a greater and greater proportion of LBMA silver holdings, as then this silver cannot be used to supply other industrial and investor demand (i.e. global demand outside London). See BullionStar article “LBMA acknowledges “Buying Frenzy” in Silver Market and silver shortage Fears” from April 2021.

This circus trick, where the bullion banks have to keep all the plates spinning at the same time, only works when they can control the various sources of demand and borrow silver from the ETFs. Which they do via controlling the silver price.

But as demand for physical silver continues to accelerate globally and silver continues to flow out of London at an astounding rate (which are factors which the bullion banks seem to have lost control of), is this crunch time again for the LBMA?

Or will the LBMA mislead the market again like it did in March 2021 when it released eroneous data that overstated the London silver inventories by 3,300 tonnes and then kept the pretense all through April and early May 2021, maintaining that silver inventories were far higher than they actually were?

Only time will tell, but with physical silver demand firing on all cylinders and massive amounts of silver leaving the LBMA London vaults, the bullion bank tactics of rinse and repeat in creating a ‘paper’ silver price unconnected to physical demand and supply is becoming more and more exposed.

This article was originally published on the BullionStar.com website under the same title “London Silver Inventories Continue to Plummet as Metal Exits LBMA Vaults”.

.

end

Hi all,

See the following link:

Why is Australia’s financial crimes watchdog investigating the Perth Mint? – ABC News

https://www.abc.net.au/news/2022-09-19/austrac- investigates-perth-mint/101438128

—

yours faithfully,

John Adams

end

5.OTHER COMMODITIES: COFFEE

Coffee bean supply hits a a record low as global scarcity worsens

(zerohedge)

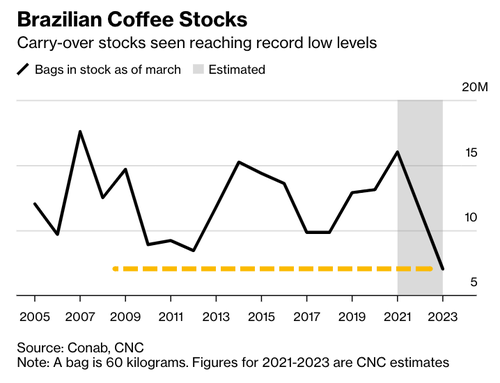

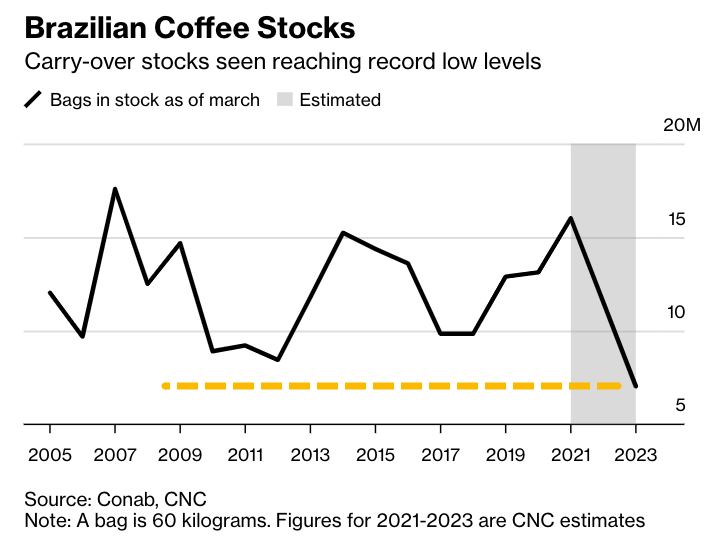

Brazil’s Coffee Bean Supply To Hit Record-Low As Global Scarcity Worsens

SUNDAY, SEP 18, 2022 – 03:00 PM

How much are consumers willing to pay for a cup of coffee?

That’s a great question, considering the world’s top arabica producer, Brazil, is headed for record low inventory, highlights tighter global supplies plus robust demand should continue boosting prices.

Bloomberg quoted Silas Brasileiro, president of the National Coffee Council, who said inventories in the South American country could decline to just 7 million bags (each weighing 60 kilograms) by the end of 1Q23. Brazil usually has 9-12 million bags in inventory.

Readers have been well informed regarding the global supply deficit of arabica coffee beans, which has materialized over the last few years. Recall “Arabica Stockpiles Experience Largest Plunge Since ’98 Amid Severe Shortage” and “Arabica Coffee Set For Largest Annual Increase Since 1994” because multiple years of a weather phenomenon known as La Nina have produced adverse weather conditions in the country’s top growing regions.

Stockpiles “are so low that even if we have a good crop next year, Brazil may just barely have enough to serve demand,” said Nelson Carvalhaes, a board member of exporters group Cecafe.

Tight global supplies have doubled arabica coffee futures in New York since 2020. Prices have traded in a lateral pattern for most of 2022 between $2-$2.5 per pound.

Guilherme Morya, Rabobank’s senior economic analyst, said prices would continue increasing on Brazilian supply woes.

In late 2021, restaurant chain Caribou Coffee Co. began panic hoarding coffee beans because the supply outlook was souring.

“We continue to increase safety stock on key items,” CEO John Butcher told Bloomberg about one year ago.

In Colombia, the world’s second top arabica coffee producer, crops are drowned in too much rain due to persisting La-Nina-related conditions. Yields are expected to decline in Guatemala, Honduras, and Nicaragua, while Vietnam, the largest robusta supplier, will also see stockpiles tumble because of poor harvest.

Analyst Natalia Gandolphi from hEDGEpoint outlined this will be the second year of declining global stockpiles with increasing demand.

Given the worsening global supply situation, there’s no immediate relief as higher demand indicates arabica prices should move higher. Consumers will find robusta a cheaper alternative to arabica, but even then, all bean quality might move higher.

Good luck to the central banks, who believe they can solve food inflation and overall inflation by crushing demand through higher interest rates.

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings MONDAY morning 7:30 AM

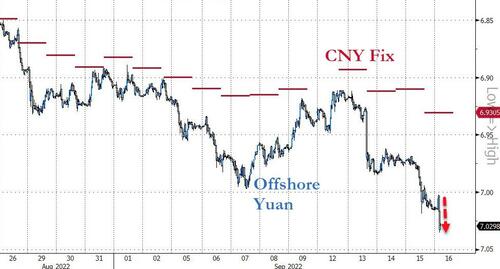

ONSHORE YUAN: CLOSED DOWN 7.0137

OFFSHORE YUAN: 7.0185

SHANGHAI CLOSED: DOWN 10.80 PTS OR 0.35%

HANG SENG CLOSED DOWN 195.73 PTS OR 1.04%

2. Nikkei closed

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 109.71/Euro FALLS TO 0.9920

3b Japan 10 YR bond yield: RISES TO. +.250/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 143.60/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

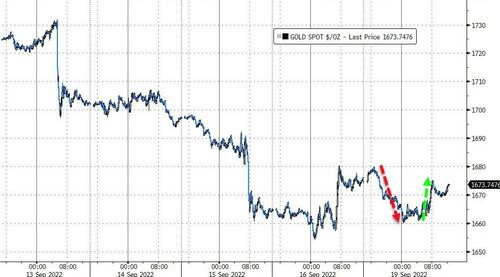

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.799%/Italian 10 Yr bond yield FALLS to 4.081% /SPAIN 10 YR BOND YIELD RISES TO 2.95%…

3i Greek 10 year bond yield FALLS TO 4.44//

3j Gold at $1661.70 silver at: 19.32 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 23/100 roubles/dollar; ROUBLE AT 60.04//

3m oil into the 82 dollar handle for WTI and 89 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 143.60DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9664– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9655well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.498 UP 5 BASIS PTS

USA 30 YR BOND YIELD: 3.555 UP 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,29

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

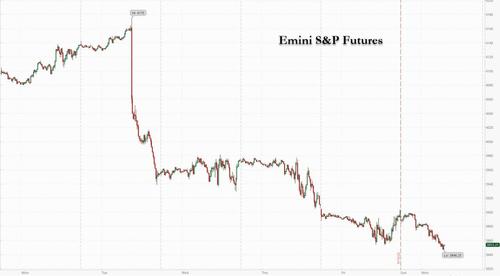

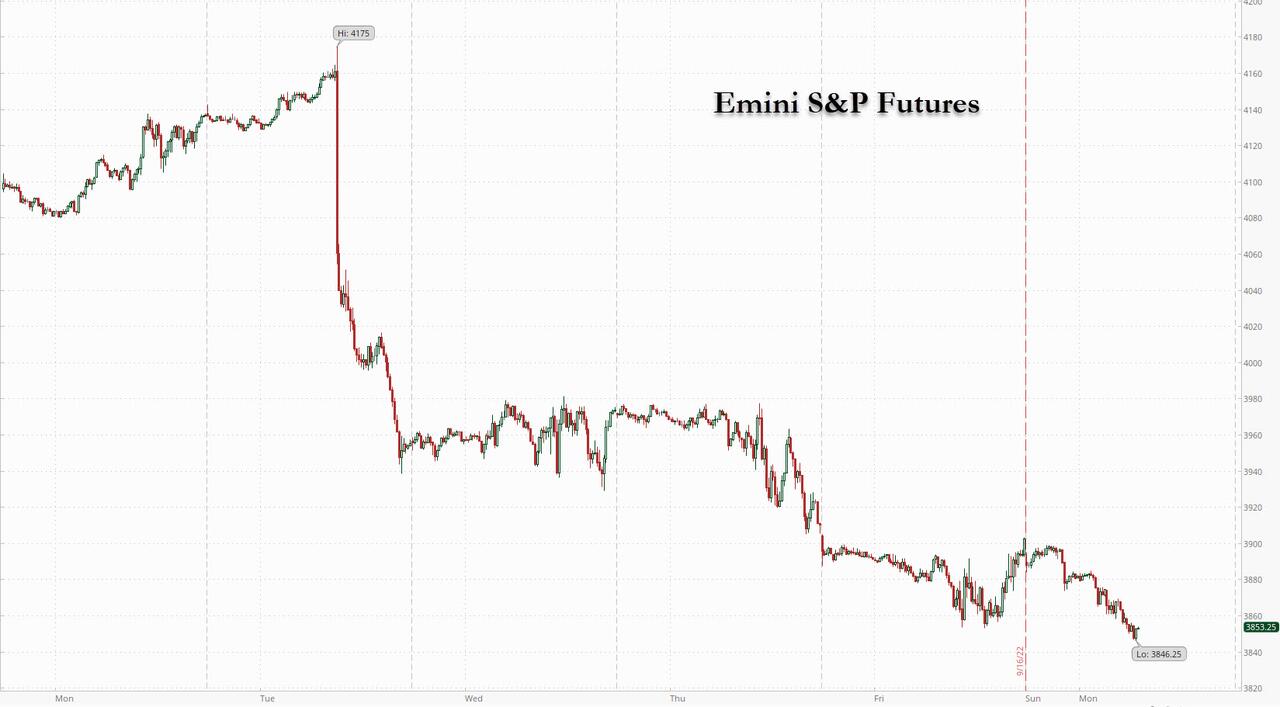

Futures, Bitcoin Crater As Yields And Dollar Surge

MONDAY, SEP 19, 2022 – 07:32 AM

After a dismal week for risk assets, which saw equities drop the most since June 17, global markets and US equity futures are tumbling in another extremely illiquid session (Japan and UK are both closed, the latter for the state funeral of QE2) as the realization sparked by Fedex that the world is in a global recession, is starting to finally seep through. Add to that Wednesday’s 75bps rate hike by the Fed (which however is more than priced in by now) as well as the previously discussed start of the buyback blackout period, and CTAs and pensions becoming forced sellers with investor sentiment that can at best be described as pervasive record doom and gloom, and it becomes clear why this week could be an even bigger bloodbath for stocks.

And sure enough, Nasdaq contracts have tumbled 1.2% as S&P futures are down 1.0%…

…the dollar is back into record territory, with rumors of a new imminent plaza accord growing louder by the day…

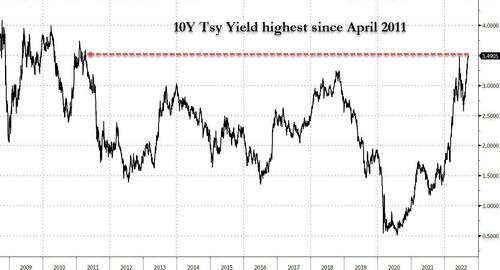

… 10Y yields are just shy of 3.50%, hitting a new post-2011 high this morning…

… which in turn is hammering European and Asian markets, as oil plunges in response to the fresh highs in the dollar.

In permarket trading, tech shares are lower and poised to extend last week’s decline, as investors expect the Fed to deliver a 75bps rate hike when it meets on Wednesday, putting pressure on pricier growth stocks. Tesla (TSLA US) -1.4%, Google (GOOGL US) -1.2%. Here are some other notable premarket movers:

- Marathon Digital (MARA US) plunged as much as 8.4% in premarket trading on Monday alongside other cryptocurrency- related stocks, after Bitcoin dropped toward the lowest level since 2020 on monetary tightening concerns.

- US-listed Chinese stocks edged lower in premarket trading Monday after Chinese stocks listed in Hong Kong dropped, putting them on track to enter bear-market territory. Alibaba (BABA US) -1.5%, Nio (NIO US) -1.6%.

- FOXO Technologies (FOXO US) surges in premarket trading after tumbling 52% on its debut on Friday via its combination with special purpose acquisition company Delwinds Insurance Acquisition Corp.

- Take-Two Interactive Software Inc. (TTWO US) falls 6.5% in US premarket trading Monday after a hacker published pre-release footage from development of Grand Theft Auto VI, its most anticipated video game.

In addition to the startling FedEx warning which sent the stock crashing by the most on record, investors also face potential volatility from policy decisions this week by the Bank of England, the Bank of Japan and a host of other central banks. The British pound sank to its weakest level against the dollar since 1985 on Friday and the yen remains under pressure, though it has backed off from just below the key 145 level versus the dollar.

“The aggressive tightening of policy in the coming 4-6 months, not just in the US but globally, increases the risk of a recession next year,” said Maria Landeborn, a senior strategist at Danske Bank A/S. “We expect uncertainty will remain high surrounding inflation, rates and the overall economy, which is negative for market sentiment and risk assets.”

With the Fed poised to hike 75bps (and perhaps even 100bps) and keep rising until it hits 4.50%, top Wall Street strategists see mounting risks for US earnings and equity valuations. Both Morgan Stanley’s Michael J. Wilson and Goldman Sachs Group Inc.’s David J. Kostin said headwinds to profitability are building, highlighting tighter monetary policy and pressure on company margins.

In Europe, the Stoxx 50 fell 0.9% with Spain’ IBEX outperforming, dropping just 0.3%, CAC 40 lags, dropping 1.1%. Energy, financial services and real estate are the worst performing sectors. Rate-sensitive European real estate shares are among the worst-performing in Europe in Monday trading, with the region’s equity market dropping further after seeing the biggest weekly decline in three months, as investors await a Federal Reserve monetary policy meeting this week. Here are some of the biggest European movers today:

- Porsche Automobil Holding advances; Volkswagen AG said it’s looking to raise as much as EU9.4 billion from the IPO of its sports-car maker in what could be Europe’s largest listing in more than a decade

- European energy stocks fall, making them the worst-performing sector in Europe on Monday, as oil prices dipped, erasing earlier gains, with the Stoxx 600 Energy index declining 1.8%

- European real estate shares are among the worst- performing in Europe in Monday trading, with the region’s equity market dropping as investors await a Federal Reserve monetary policy meeting this week

- TF1 and M6 slumped after the French TV companies called off a planned combination because of objections from the country’s antitrust regulator; also today, Oddo cut TF1 to neutral

- Valneva falls as much as 16% after the French vaccines maker said it will terminate a Covid-19 vaccine collaboration with IDT Biologika, agreeing to pay as much as EU36.2 million in cash.

Earlier in the session, Asian equities fell, poised for a fifth session of decline, as the dollar strengthened ahead of the Federal Reserve’s meeting this week. The MSCI Asia Pacific ex-Japan index erased early gains and fell as much as 0.8%, dragged by consumer discretionary and tech shares. Benchmarks in Hong Kong and South Korea were among the worst performers in the region. Japan’s market was shut for a holiday. The dollar’s gains put pressure on regional currencies, and stocks tumbled in the Philippines, Malaysia and Vietnam. Traders are watching the Federal Open Market Committee’s interest-rate decision on Wednesday for signals on further policy tightening, pricing in a 75-basis-point hike. The Hang Seng China Enterprises Index fell more than 1%, taking its losses from a June 28 peak to just short of 20%, which will mark the start of a bear market. Mainland China stocks traded little changed Monday as megacity Chengdu exited a lockdown.

MSCI’s broadest Asia Pacific stock gauge has clocked five consecutive weeks of losses as investors factor in higher US interest rates and a strong dollar. Optimism over any easing of China’s Covid-Zero stance after the party congress in October is also waning. “Unless the Fed is done with rate hikes, the US dollar bull market is not over yet,” Lim Say Boon, chief investment strategist at CGS-CIMB Securities wrote in a note.

In Australia, The t&P/ASX 200 index fell 0.3% to close at 6,719.90, the lowest since July 19, dragged by losses in health care and energy shares. In New Zealand, the S&P/NZX 50 index fell 0.4% to 11,531.99. The nation’s economic outlook is sound, despite increasing domestic and international turbulence, S&P said in a statement

Stocks in India snapped three days of declines, helped by a rally in consumer and auto firms on expectations of a boost in demand during the upcoming festive season. The S&P BSE Sensex rose 0.5% to 59,141.23 in Mumbai, while the NSE Nifty 50 Index also gained by a similar magnitude. Out of 30 shares in the Sensex index, 20 rose and 10 fell. A gauge of fast-moving consumer-goods makers was the best performer among 19 sectoral sub-indexes compiled by BSE Ltd. Most stocks across Asia declined ahead of key rate decisions by various central banks, including the US Federal Reserve. A higher-than-expected inflation in the US has raised expectations of another 75-basis-point hike when Fed policymakers meet on Wednesday. Housing Development Finance Corp contributed the most to the Sensex’s gains, increasing 1.5%.

In rates, Treasuries re-opened with yields cheaper by up to 5.5bp across front end of the curve in a bear flattening move. Into the weakness 10-year yields top at 3.506% and cheapest levels since June 2011. Cash market was closed overnight as UK observes a day of mourning for Queen Elizabeth II and Japan is out on holiday. Treasury yields 3.5bp to 5.5bp cheaper across the curve with long end outperforming slightly, flattening 2s10s, 5s30s spreads by 0.5bp and 1bp on the day. IG dollar issuance slate empty so far; up to $20b expected for the week with Monday and Tuesday potentially busy ahead of Wednesday FOMC. Latest CFTC positioning data shows hedge fund net short in two-year note futures, biggest since June 2021. Bund yields climb some 3bps across the curve. Australia’s bonds rose for the first time in four days. Yields fell 3-5bps across the curve.

In FX, the dollar strengthens against all FX majors; euro trades below parity while cable trades at around 1.13/USD and the yen slides near 143.43/USD. UK observes a day of mourning for Queen Elizabeth II. Some more details: