GOLD PRICE CLOSE: UP $5.20 to $1672.95

SILVER PRICE CLOSE: UP 10 cents to $19.60

Access prices: closes

Gold ACCESS CLOSE 1671.50

Silver ACCESS CLOSE: 19.62

Bitcoin morning price: $19,100 down $34

Bitcoin: afternoon price: $19,484 UP $350

Platinum price closing DOWN $2.75 AT $918.40

Palladium price; closing DOWN $23.55 at $2123.75

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,664.600000000 USD

INTENT DATE: 09/21/2022 DELIVERY DATE: 09/23/2022

FIRM ORG FIRM NAME ISSUED STOPPED

323 C HSBC 4

624 H BOFA SECURITIES 34

657 C MORGAN STANLEY 9

661 C JP MORGAN 510 456

686 C STONEX FINANCIA 1

709 C BARCLAYS 243

737 C ADVANTAGE 6 4

880 H CITIGROUP 299

905 C ADM 30

TOTAL: 798 798

MONTH TO DATE: 8,573

________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR SEPT CONTRACT:

798 NOTICES FOR 79,800 OZ //2.4821 TONNES

total notices so far: 8573 contracts for 857,300 oz (26.665 tonnes)

SILVER NOTICES: 107 NOTICES FILED FOR 535,000 OZ/

total number of notices filed so far this month 6595 : for 32,975,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $5.20

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: //// A WITHDRAWAL OF 5.79 TONNES FROM THE GLD/

INVENTORY RESTS AT 952.16 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $.10

AT THE SLV// ://GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF OF 0.691 MILLION OZ INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 481.424 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A FAIR SIZED 403 CONTRACTS TO 131.704 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE FAIR LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.33 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.33) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD A SMALL GAIN OF 98 CONTRACTS ON OUR TWO EXCHANGES. WE DID HAVE A STRONG SILVER SHORT COVERING. THE SPECS ARE FLEEING AS FAST AS THEIR LITTLE FEET WILL CARRY THEM.

WE MUST HAVE HAD:

I) STRONG SPECULATOR SHORT COVERING ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 95,000 OZ QUEUE JUMP / // V) SMALL SIZED COMEX OI LOSS/(//CONSIDERABLE SPEC LIQUIDATION/)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -49

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 15 days, total 12,205 contracts: 61.045 million oz OR 4.069 MILLION OZ PER DAY. (814 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 61.045 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 61.045 MILLION OZ///

RESULT: WE HAD A FAIR SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 403 DESPITE OUR $0.33 GAIN IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE CONTRACTS: 452 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /GOOD BANKER ADDITIONS A// CONSIDERABLE NET SPEC SHORT COVERINGS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 95,000 OZ QUEUE JUMP // .. WE HAD A SMALL SIZED GAIN OF 49 OI CONTRACTS ON THE TWO EXCHANGES FOR 0.245MILLION OZ AS..THE SPECS STILL ARE BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 107 NOTICE(S) FILED TODAY FOR 535,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 3228 CONTRACTS TO 466,167 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED – 133 CONTRACTS.

.

THE FAIR SIZED DECREASE IN COMEX OI CAME DESPITE OUR RISE IN PRICE OF $4.70//COMEX GOLD TRADING/WEDNESDAY / WE MUST HAVE HAD MAJOR SPECULATOR SHORT COVERINGS ACCOMPANYING OUR SMALL SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND //CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 8.401 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 126,900 OZ //NEW STANDING 24.951 TONNES

YET ALL OF..THIS HAPPENED WITH OUR RISE IN PRICE OF $4.70 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A SMALL SIZED GAIN OF 703 OI CONTRACTS 2.186 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3931 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 466,167

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 836 CONTRACTS WITH 3228 CONTRACTS DECREASED AT THE COMEX AND 3931 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 703 CONTRACTS OR 2.186 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3931) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (3228): TOTAL GAIN IN THE TWO EXCHANGES 703 CONTRACTS. WE NO DOUBT HAD 1) CONSIDERABLE SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS/// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 8.409 TONNES FOLLOWED BY TODAY’S MONSTROUS QUEUE JUMP OF 136,900 oz. 3) ZERO LONG LIQUIDATION//// //.,4) FAIR SIZED COMEX OPEN INTEREST LOSS 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

39,290 CONTRACTS OR 3,929,000 OZ OR 122.21 TONNES 15 TRADING DAY(S) AND THUS AVERAGING: 2619 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAY(S) IN TONNES: 122.21 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 122.21/3550 x 100% TONNES 3.43% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 122.21 TONNES (SLIGHTLY FALLING THIS MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT., FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER,FELL BY A FAIR SIZED 403 CONTRACT OI TO 131,704 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 452 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 452 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 452 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 354 CONTRACTS AND ADD TO THE 452 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED GAIN OF 49 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 0.245 MILLION OZ

OCCURRED WITH OUR GAIN IN PRICE OF $0.33

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 8.27 PTS OR 0.27% //Hang Sang CLOSED UP 296.67 PTS OR 1.61% /The Nikkei closed DOWN 159.30 PTS OR 0.58% //Australia’s all ordinaires CLOSED DOWN 1.55% /Chinese yuan (ONSHORE) closed DOWN AT 7.0732//OFFSHORE CHINESE YUAN DOWN 7.0709// /Oil DOWN TO 84.14 dollars per barrel for WTI and BRENT AT 90.88 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 3228 CONTRACTS TO 466,167 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED DESPITE OUR RISE IN PRICE OF $4.70 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A GOOD SIZED EFP (3931 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3931 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :3931 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3931 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED SIZED TOTAL OF 836 CONTRACTS IN THAT 3931 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 3095 CONTRACTS..AND THIS SMALL GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR RISE IN PRICE OF GOLD $4.70. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING SEPT (28.898),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 28.898 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $4.70) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A SMALL SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 703 CONTRACTS // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS TRIED TO COVER ON THEIR POSITIONS WITH MINIMAL SUCCESS////// WE HAVE REGISTERED A SMALL GAIN OF 836 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR SEPT. (28.898 TONNES)…

WE HAD 133 CONTRACTS ADDED FROM COMEX TRADES. THESE WERE ADDED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 703 CONTRACTS OR 70,300 OZ OR 2.186 TONNES

Estimated gold volume 149,852/// poor//

final gold volumes/yesterday 244,043/ fair

INITIAL STANDINGS FOR SEPT ’22 COMEX GOLD //SEPT 22

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 114,232.595 oz BRINKS DELAWARE HSBC |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 798 notice(s) 79,800 OZ 2.4821 TONNES |

| No of oz to be served (notices) | 718 contracts 71800 oz 2.2332 TONNES |

| Total monthly oz gold served (contracts) so far this month | 8573 notices 857,300 OZ 26.665 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

3 customer withdrawals:

i) Out of Brinks 106,034.000 oz( 3298 kilobars)

ii) Our of Delaware 482.265 oz (15 kilobars)

iii) Out of HSBC: 7716.240 oz (240 kilobars)

total: 114,232.505 oz

total in tonnes: 3.55 tonnes

Adjustments: 1

JPM/ customer to dealer: 76,370.776 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPT.

For the front month of SEPT we have an oi of 1516 contracts having LOST 401 contracts .

We had1670 notices filed on WEDNESDAY so we gained a whopping 1269 contracts or an additional 126,900 oz

will stand for gold in this very non active delivery month of September.

October LOST ONLY 898 contracts LOWERING TO 42,048. Oct is generally a poor active delivery month. It WILL change!! (Look for a very unusually large Oct. delivery month.)

November GAINED 37 contracts to stand at 340

December lost 2201 contracts DOWN to 376,423

We had 798 notice(s) filed today for 79,800 oz FOR THE SEPT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 510 notices were issued from their client or customer account. The total of all issuance by all participants equate to 798 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 456 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2022. contract month,

we take the total number of notices filed so far for the month (8573) x 100 oz , to which we add the difference between the open interest for the front month of (SEPT 1516 CONTRACTS) minus the number of notices served upon today 798 x 100 oz per contract equals 929,100 OZ OR 28.898 TONNES the number of TONNES standing in this NON active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month:

No of notices filed so far (8573) x 100 oz+ (1591) OI for the front month minus the number of notices served upon today (798} x 100 oz} which equals 929,100 oz standing OR 28.898 TONNES in this NON active delivery month of SEPTEMBER.

TOTAL COMEX GOLD STANDING: 28.898 TONNES (A HUMONGOUS STANDING FOR A SEPT ( NON ACTIVE) DELIVERY MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,250,165.318 oz 76.21 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 26,833,781.698 OZ

TOTAL REGISTERED GOLD: 12,987,212.627 OZ (403.95 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 13,846,569.063 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,737,047. OZ (REG GOLD- PLEDGED GOLD) 333.96 tonnes//rapidly declining

END

SILVER/COMEX/SEPT 22

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,241,773.970 oz Brinks CNT Loomis HSBC Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 107 CONTRACT(S) 535,000 OZ) |

| No of oz to be served (notices) | 36 contracts (180,000 oz) |

| Total monthly oz silver served (contracts) | 6595 contracts 32,975,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

total deposit: nil oz

JPMorgan has a total silver weight: 164.074 million oz/316.337million =51.84% of comex

Comex withdrawals: 5

i) out of HSBC 1006.35 oz

ii) Out of Brinks: 2904.550 oz

iii)Out of CNT 583,979.400 oz

iv)Out of Loomis: 600,048.570 oz

v) Out of Manfra: 53,835.100 o

total: 1,241,773.970 oz

adjustments: 3// DEALER to customer

i) Brinks 338,371.00

ii) 19,143.325 oz

iii) Manfra 311,918.690 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 43.511 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 316.337 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF SEPT OI: 143 CONTRACTS HAVING LOST 7 CONTRACTS. WE HAD

26 CONTRACTS SERVED ON TUESDAY SO WE GAINED 19 CONTRACTS OR AN ADDITIONAL

95,000 OZ WILL STAND FOR METAL IN THIS VERY ACTIVE MONTH OF SEPT.

WE WILL GAIN IN TOTAL SILVER STANDING EACH TRADING DAY UNTIL THE END OF THE MONTH

(CONTINUAL QUEUE JUMPING BY OUR BANKERS SEARCHING FOR SILVER METAL)

OCTOBER LOST 23 CONTRACTS TO STAND AT 509 CONTACTS.

NOVEMBER GAINED 7 CONTRACTS TO STAND AT 106

DECEMBER SAW A LOSS OF 570 CONTRACTS DOWN TO 116,324

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 26 for 130,000 oz

Comex volumes:37,859// est. volume today// poor

Comex volume: confirmed yesterday: 72,880 contracts ( good)

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 6595 x 5,000 oz = 32,975,000 oz

to which we add the difference between the open interest for the front month of SEPT(143) and the number of notices served upon today 107 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT./2022 contract month: 6,595 (notices served so far) x 5000 oz + OI for front month of SEPT (143) – number of notices served upon today (105) x 5000 oz of silver standing for the SEPT contract month equates 33,155,000 oz. .

We have an inventory of 44.240 million oz of registered silver at the comex so Sept delivery of 33.155 MILLION OZ represents 74.94% of that category of silver.

If we add August’s final delivery (to Sept) for silver at 5.51 million oz, we have a total of 38.665 million oz delivered upon with a REGISTERED INVENTORY of 44.20 million oz or 87.47% of that category of silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:50,941// est. volume today// poor

Comex volume: confirmed yesterday: 43,847contracts ( poor)

END

GLD AND SLV INVENTORY LEVELS

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

GLD INVENTORY: 952.16 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

CLOSING INVENTORY 481.424 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Fed Policy In A Nutshell: Live In Hope; Die In Despair

THURSDAY, SEP 22, 2022 – 10:59 AM

Authored by Michael Maharrey via SchiffGold.com,

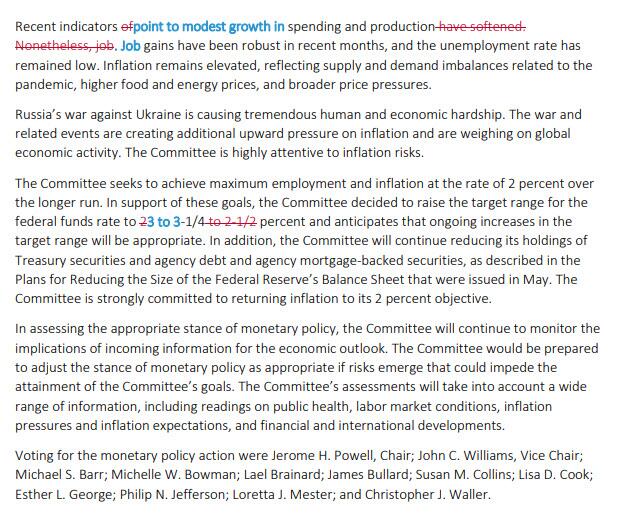

During his post- FOMC meeting press conference, Federal Reserve Chairman Jerome Powell said, “Hope for the best; plan for the worst.”

I think he meant, “Live in hope; die in despair.”

The Federal Reserve raised interest rates another 75 basis points to 3.25% in another attempt to cool “transitory” inflation. The move was widely anticipated after the Consumer Price Index (CPI) came in hotter than expected in August.

The last time interest rates were this high was January 2008.

You remember what happened in 2008, right?

In its official statement, the FOMC said the central bank is “strongly committed” to bringing inflation back to the mythical 2% target, and that it “anticipates that ongoing increases in the target range will be appropriate.”

Unfortunately, by the Fed’s own admission, that’s going to take a while. Meanwhile, get ready to feel some pain.

“I wish there were a painless way” to get inflation down, Powell said during his post-meeting press conference, “but there isn’t.”

The central bank now projects its favorite inflation measure (core personal consumption expenditure index) to hit 2.3% in 2024 and 2.1% in 2025. CPI won’t likely fall to the 2% range until 2025. Powell specifically talked about rising prices for shelter, saying, “We’re looking for it to come down, but it’s not exactly clear when that will happen. It may take some time. Hope for the best, plan for the worst.”

And in fact, projecting inflation to fall to 2% in the next couple of years seems like a plot from a fantasy novel. As aggressive as the Fed moves may seem, they remain totally inadequate to rein in inflation galloping along at an 8.3% clip.

Officials now project interest rates will hit 4.4% by the end of the year and top out at 4.6% in 2023. That’s up from a projected 3.8% peak at the last FOMC meeting. But in order to tackle inflation, the Fed needs to push rates above the CPI. I don’t need tell you that 4.6 is below 8.3. That’s why Peter Schiff insists the Fed won’t bend this inflation curve.

As long as we have interest rates below the inflation rate, even if they’re higher, they’re still negative, and negative interest rates put upward pressure on inflation. You can’t fight inflation with negative interest rates. It’s like saying, ‘I’m going to fight this fire by pouring gasoline on it. It’s just that I’m only going to pour a little bit of gasoline, not as much gasoline as I was pouring on before.’”

On top of that, Fed rate hikes alone won’t tame inflation.

A paper published by the Kansas City Federal Reserve Bank even conceded this point, arguing that the central bank can’t slay inflation unless the US government gets its spending under control. In a nutshell, the authors argue that the Fed can’t control inflation alone. US government fiscal policy contributes to inflationary pressure and makes it impossible for the Fed to do its job.

Trend inflation is fully controlled by the monetary authority only when public debt can be successfully stabilized by credible future fiscal plans. When the fiscal authority is not perceived as fully responsible for covering the existing fiscal imbalances, the private sector expects that inflation will rise to ensure sustainability of national debt. As a result, a large fiscal imbalance combined with a weakening fiscal credibility may lead trend inflation to drift away from the long-run target chosen by the monetary authority.”

That seems unlikely.

But while the Fed’s tight monetary policy is unlikely to end inflation, it will continue to drive the economy into the ground. As Skanda Amarnath, executive director at Employ America told Reuters, “Everyone should assume the Fed is committed to engineering a recession.”

The Fed even concedes this fact – thus Powell’s warning about pain. But don’t worry. The Fed chair said once the central bank gets inflation under control, “things will start to feel better for people.”

So, look forward to brighter days — in 2025.

Maybe.

In fact, the central bank seems to be wildly underestimating the pain in store for the economy.

The Fed projects GDP year-end growth will come in at 0.2% and then rise to 1.2% in 2023. But we’ve already had back-to-back quarters of negative GDP growth. That used to be the definition of a recession until the spinmeisters at the White House updated the definition. And things aren’t looking much better for Q3. The Atlanta Fed recently downgraded its third-quarter growth projection to 0.3%.

Most people seem resigned to the fact that a recession is in the cards. But they insist it will be short and shallow. This is almost certainly more wishful thinking. Why should anybody believe it will be short and shallow?

As Schiff pointed out, the bust needs to be proportional to the boom.

We’ve never had a boom this big. We’ve never had interest rates this low for this long. We’ve never had an economy more screwed up than the one we have right now. We’ve never had bigger asset bubbles, bigger debt bubbles, more misallocations of capital and resources. So, we have more mistakes that we need to fix now than ever before. So, how are we going to do that with a short shallow recession? We’re not. It’s going to be a massive recession.”

The question is how long will the Fed keep making a show of fighting inflation? At what point will the central bank pivot back to blowing air into the bubble economy? Schiff said the Fed has “no stomach” for the kind of economic chaos coming down the pike. “And that’s why the Fed is going to pivot.”

That leads to other questions. Will the Fed pivot as soon as it can no longer plausibly deny the imploding economy? Or will it keep pushing the envelope until it rips and then pivot? Schiff said, either way, the end result is the same.

As long as it pivots at all, that means inflation is going to run out of control.”

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

END

3.Chris Powell of GATA provides to us very important physical commentaries

end

4. OTHER GOLD/SILVER COMMENTARIES

5.OTHER COMMODITIES: COFFEE

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.0732

OFFSHORE YUAN: 7.0709

SHANGHAI CLOSED: DOWN 8.27 PTS OR 0.27%

HANG SENG CLOSED DOWN 296.67 PTS OR 1.61%

2. Nikkei closed DOWN 159.30 PTS OR 0.58%

3. Europe stocks SO FAR: ALL RED

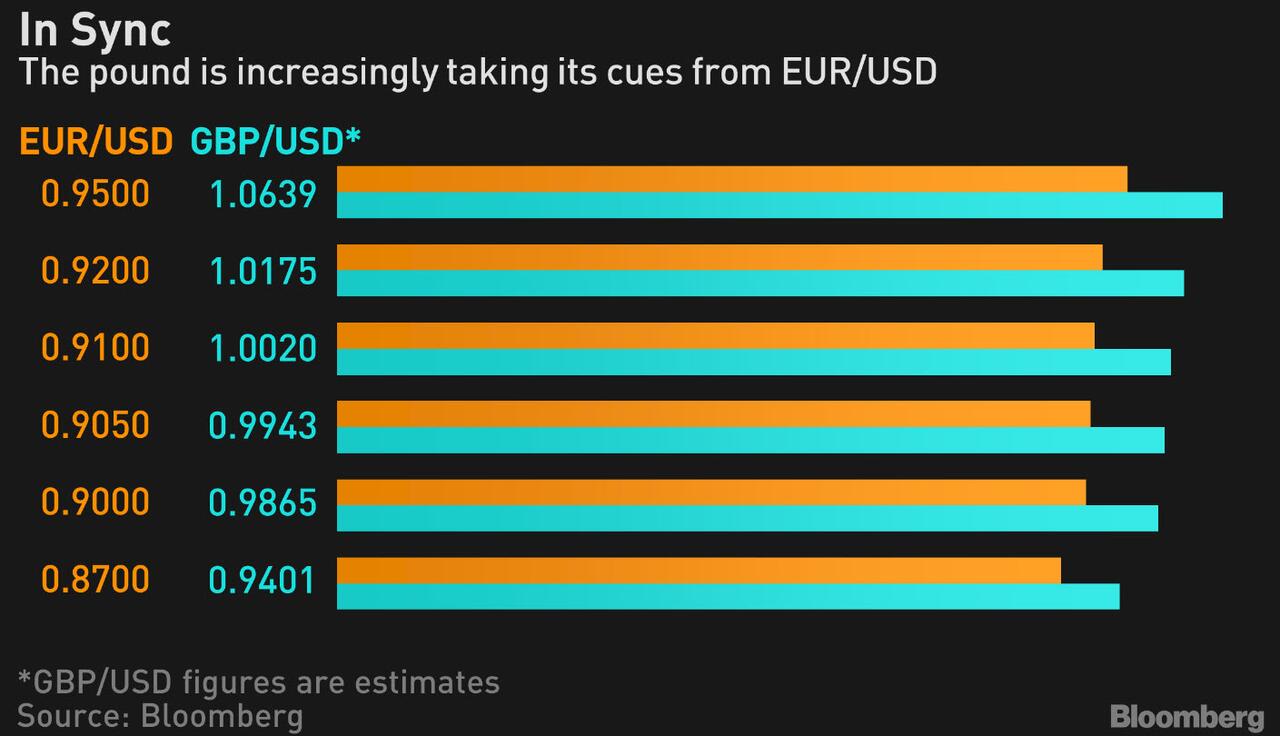

USA dollar INDEX UP TO 110.66/Euro RISES TO 0.98612

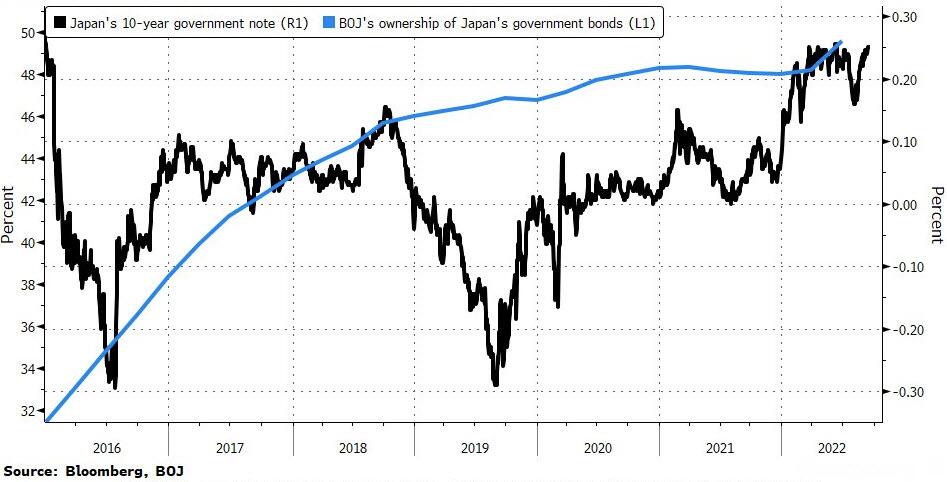

3b Japan 10 YR bond yield: FALLS TO. +.234/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 141.72/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.877%***/Italian 10 Yr bond yield FALLS to 4.09%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.000%…** DANGEROUS

3i Greek 10 year bond yield FALLS TO 4.43//

3j Gold at $1672.80 silver at: 19.62 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1 AND 64/100 roubles/dollar; ROUBLE AT 59.05//

3m oil into the 84 dollar handle for WTI and 90 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 141.72DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9816– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9680well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

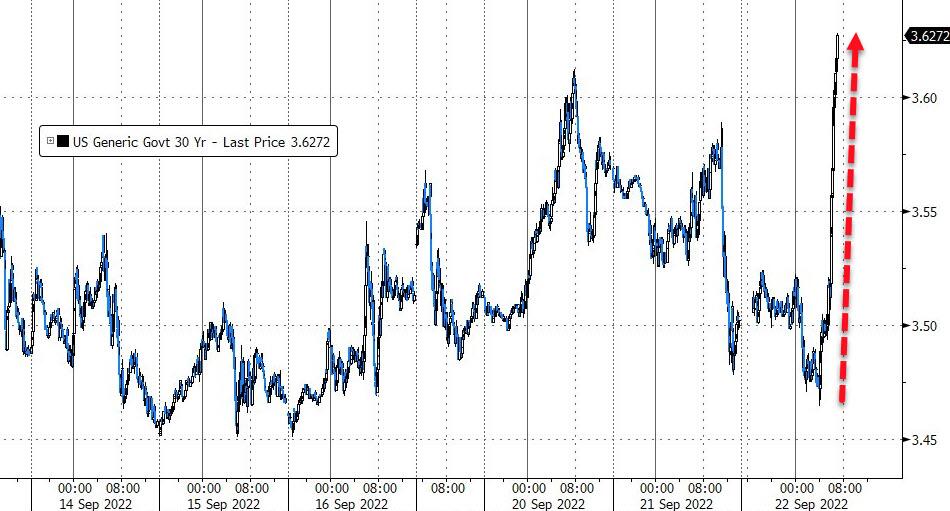

USA 10 YR BOND YIELD: 3.559 UP 5 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.505 DOWN 2 BASIS PTS//(USA 30 YR INVERTED TO THE USA 10)

USA DOLLAR VS TURKISH LIRA: 18,38…GETTTING DANGEROUS

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

‘Economic Discontent’ Is On The Rise As Central-Bank-Nado Strikes Markets Overnight

THURSDAY, SEP 22, 2022 – 08:13 AM

A herd of wild central banks stormed across markets overnight – following The Fed’s uber-hawkish 75bps hike and dot-plot projections – sparking chaotic swings in everything from Yen to Gilts. Everyone hiked or held rates… except Turkey which cut!

Japan

- BoJ kept its monetary policy unchanged, as expected, with rates at -0.10% and QQE with yield curve control maintained to target the 10yr JGB yield at around 0% through a unanimous decision.

- Japanese Government and BoJ intervened in FX markets for the first time since 1998, according to the Japanese Vice Finance Minister – the government and the BoJ stepped into the market to buy JPY for USD.

Switzerland

- SNB hikes its Policy Rate by 75bps to 0.5% as expected; willing to be active in FX market as necessary; further rate hikes cannot be ruled out; no CHF classification in release.

- SNB Chair Jordan says SNB ready to intervene to prevent excessive weakening or strengthening of the CHF; recent appreciation has helped dampen inflation. If there were to be an excessive appreciation of the Swiss franc, we would purchase foreign currency. If the Swiss franc were to weaken, however, we would consider selling foreign currency.

Norway

- Norges hikes its Key Policy Rate by 50bps as expected to 2.25%; policy rate will most likely be raised further in November; This may suggest a more gradual approach to policy rate setting ahead.

- Norges Bank Governor Bache says the central bank is likely to hike by 25bps in November.

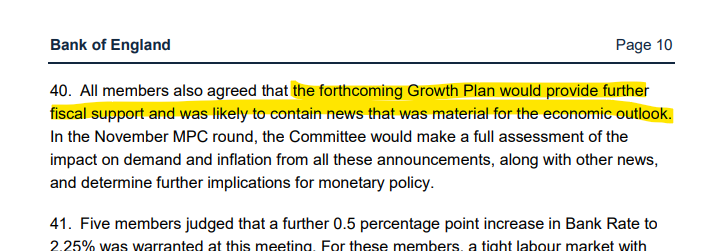

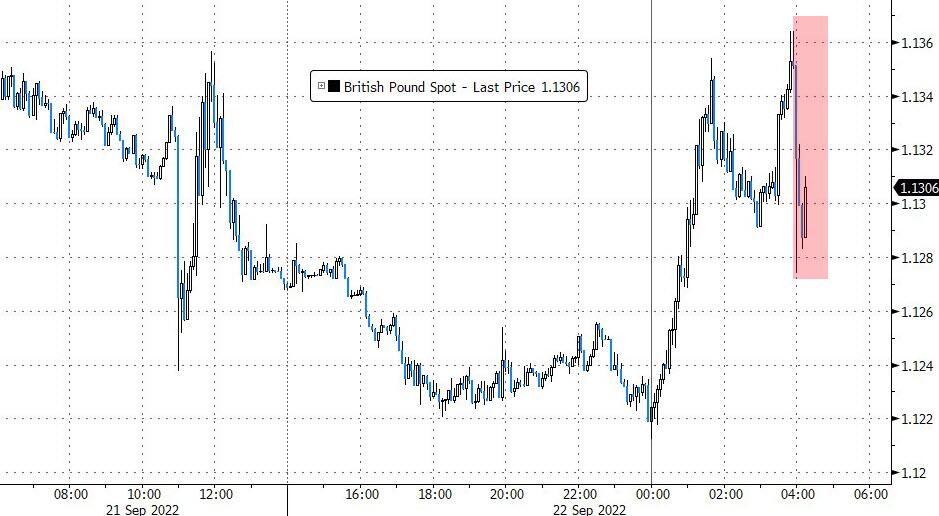

UK

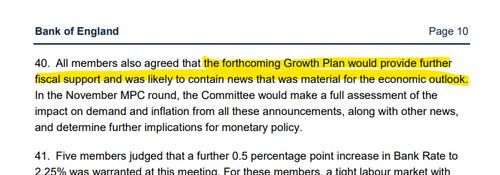

- The Bank of England hiked rates a softer-than-markets-expected 50bps (in 5-3-1 50-75-25bps split decision) while warning about the potential inflationary impact of PM Truss’ new fiscal plans.

- MPC also confirmed the start of QT – active-selling of gilts will begin in October.

Europe

- While no decisions from the ECB today, it is worth noting that ECB’s Schnabel says we must increase interest rates further, “I assume that the ECB Governing Council will hike interest rates further at its next meeting. At the moment, I cannot say how large this interest rate hike will be and up to what level we will”. In the short-term inflation could increase further, despite rate hikes. We do not currently see any indications of a wage-price spiral; wage growth has increased, but is still moderate

Brazil

- Brazil Central Bank maintained the Selic Rate at 13.75% as expected via unanimous decision, while it will assess if the prospect of holding the Selic Rate long enough will ensure inflation convergence and stated that future policy steps could be adjusted. Furthermore, it will remain vigilant and will not hesitate to resume the cycle of rate adjustments if disinflation does not happen as expected.

Hong Kong

- Hong Kong Monetary Authority raised the base rate by 75bps to 3.50%, as expected.

Rest of Asia

- Bank of Taiwan, Bank of Indonesia, and Bank of Philippines all raised rates in-line with expectations.

Turkey

- Turkey’s central bank delivered another shock cut to interest rates, despite inflation running at a 24-year high and with the lira trading at a record low.

- The Monetary Policy Committee led by Governor Sahap Kavcioglu lowered the benchmark to 12% from 13% on Thursday. In a statement accompanying its decision, the central bank said there was a “loss of momentum in economic activity.”

Amid all that chaos, here are some of the main moves in markets:

Stocks

- Futures on the S&P 500 were little changed as of 7:54 a.m. New York time

- Futures on the Nasdaq 100 fell 0.2%

- Futures on the Dow Jones Industrial Average were little changed

- The Stoxx Europe 600 fell 1.1%

- The MSCI World index fell 0.2%

Currencies

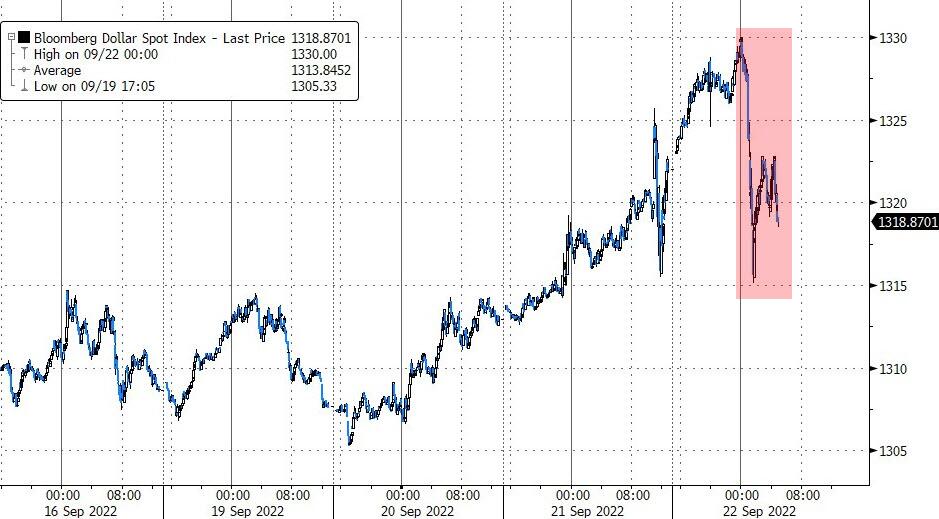

- The Bloomberg Dollar Spot Index fell 0.2%

- The euro rose 0.3% to $0.9864

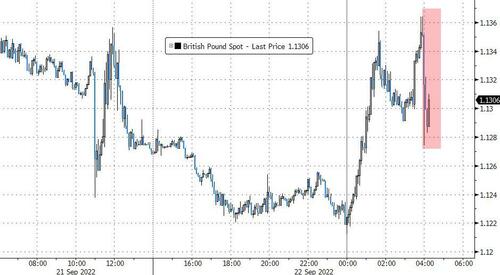

- The British pound rose 0.3% to $1.1304

- The Japanese yen rose 1.7% to 141.59 per dollar

Bonds

- The yield on 10-year Treasuries advanced two basis points to 3.55%

- Germany’s 10-year yield was little changed at 1.89%

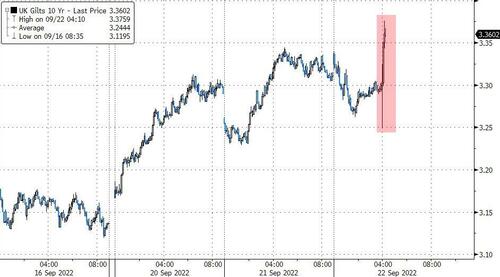

- Britain’s 10-year yield advanced 11 basis points to 3.42%

Commodities

- West Texas Intermediate crude rose 1.5% to $84.22 a barrel

- Gold futures rose 0.2% to $1,678.50 an ounce

TOP OVERNIGHT NEWS (via Bloomberg):

- Powell Signals Recession May Be the Price for Crushing Inflation

- Stock Bulls Reluctantly Fold on the Fed’s Grim Economic Message

- Traders Ramp Up BOE, ECB Rate Hike Bets After Hawkish Fed

- Gold Risks Collapse Into Bear Market as Fed Targets Inflation

- Bond Market Pushes Recession Trades as Fed Hawks Take Flight

- Goldman Lifts Forecasts for Fed Hikes on Powell’s Hawkish Signal

- Japan Intervenes in Market After BOJ Defiance Sends Yen Sliding

- BOJ Curve-Control Policy Bolstered as US Yields Fall After Fed

- Deutsche Bank CFO Says on Track for Top End of Revenue Guidance

- Credit Suisse Mulls Plan to Resurrect ‘Bad Bank,’ FT Reports

- Wall Street CEOs Grilled on China, Russia Ties by US Lawmakers

- Citi Mulls N.J., Connecticut Facilities to Ease NYC Commutes

- Porsche’s Gray Market Trading Points to Bumper Debut Next Week

- Bankman-Fried’s FTX Is in Talks to Raise $1 Billion, Says CNBC

- Dimon Calls Out Crypto as ‘Decentralized Ponzi Schemes’

- Bitcoin Pares Drop Sparked by Fed’s Warning of Rate-Hike Pain

- Intel Executive With Industry’s Toughest Job Plots Comeback

- Kittyhawk, Larry Page’s Flying-Car Company, Will Shut Down

- Ukraine Seizes Dozens of Russian Tanks Left by Fleeing Forces

- Suns Owner Sarver Set to Sell Teams Amid Harassment Scandal

- Trump-Picked World Bank Boss Faces Calls for Ouster Over Climate

- House Votes to Raise Bar for Challenging Presidential Elections

US EVENT CALENDAR:

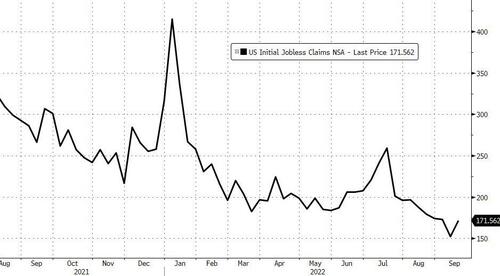

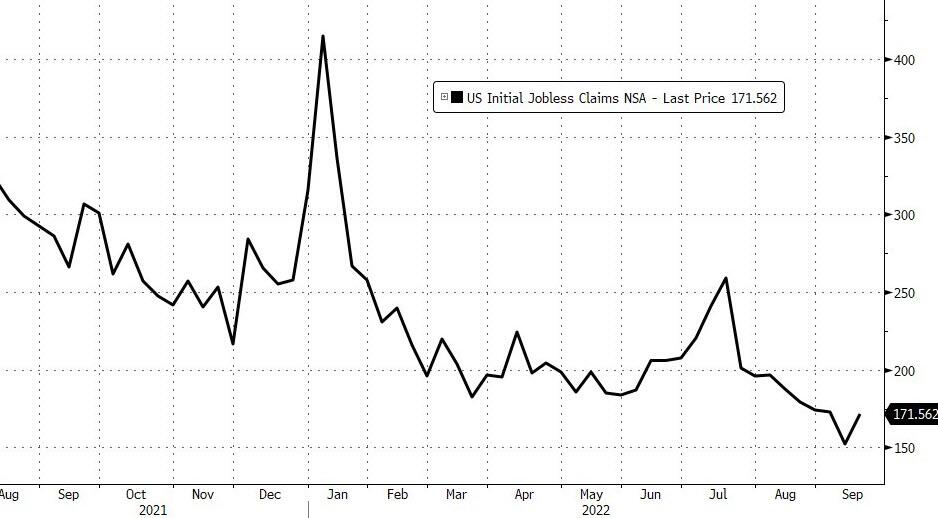

- 08:30: Sept. Continuing Claims, est. 1.42m, prior 1.4m

- 08:30: 2Q Current Account Balance, est. -$260b, prior -$291.4b

- 08:30: Sept. Initial Jobless Claims, est. 217,000, prior 213,000

- 10:00: Aug. Leading Index, est. -0.1%, prior -0.4%

- 11:00: Sept. Kansas City Fed Manf. Activity, est. 5, prior 3

Rabobank’s Michael Every concludes the overnight wrap:

Anxiety about the geopolitical risks overshadowed markets’ concerns about soaring inflation yesterday as Putin ‘doubled down’. In a television address to the Russian nation, he declared a ‘partial’ mobilization of 300,000 reservists. However, markets’ worries about the Russian President’s latest escalation pales in comparison to the anxiety amongst those whose lives it affects directly and dramatically. As the pundits pointed out, the official text of the decree does not specify an end date, nor an actual number of reservists to be called up. In fact, it’s a broad and open-ended statement that leaves any decision on quantities to top brass and regional military leadership. So the 300,000 is, well, just a number.

Google trends reveals that Russians flocked to the search engine to search for ways to avoid being called on in this act of mobilization. Fleeing the country was clearly the top tip, as evidenced by a surge in search queries that included any combination of airline tickets, visa, and specific destinations. Even the desperate question “where to flee to?” was increasingly being Googled, after the Moscow Times reported that “nearly all flights to available foreign destinations were sold out” almost immediately after the announcement. When the option of leaving the country seemed exhausted, people turned to more drastic ways to avoid being sent to the battlefield. “searches for ‘how to break an arm’ surged in russia today. anything to get out of combat…,” summarized Eurasia’s Ian Bremmer. That reaction illustrates why the Kremlin had resisted drawing upon such mobilization so far.

Some –including German Chancellor Scholz– are calling Putin’s move an act of desperation as he realizes that “Russia cannot win this criminal war.” However, even if this is true, it’s hardly a positive for risk sentiment. After all, Putin has also swept the rug from under those who were starting to believe that Russia was looking for an exit after China and India also increased pressure on Putin to de-escalate – at least, that was how many had interpreted Putin’s comments after meeting with Xi and Modi. And even if these new forces are only to be deployed in the Luhansk and Donetsk regions to prevent Ukraine from taking back these territories, it also raises the risk that the West gets dragged into the fight, as Russia would see an attack on these regions as an attack on its own sovereignty – especially after these regions ‘vote’ for annexation in the referendums that will be held this weekend.

Of course we could consider all this sabre-rattling and shift in focus from ‘fighting Ukraine’ towards the ‘fight against the West’ as specifically aimed at a domestic audience. The ‘partial’ mobilization decision has to be explained after all. But the sabre-rattling (with Sergei Markov, one of Putin’s ‘close advisors’ again warning on BBC radio yesterday that Russia is willing to use its nuclear arsenal against Western countries if it feels threatened) is also a signal that Putin is willing to play a game of attrition in which he hopes to drive a wedge into the Western coalition countries.

Playing into political disruption is the key weapon, as economic discontent –a result of the energy crisis– is on the rise. Giorgia Meloni, leading a coalition of radical right and more moderate factions, may soon take over the helm from Italian PM Draghi. In Sweden the far-right Sweden Democrats came in second in this month’s election and yesterday 5,000 protesters took to the streets in Slovakia to express anger about the economic impact of the war. Governments are taking measures to soften the cost of living crisis, but the medium-term consequences of these interventions on inflation could well be ‘higher for longer’.

Given the abovementioned backdrop the market’s reaction yesterday was actually rather modest. 10y yields in Europe fell around 6 basis points across the board, but partly recovered from that in the afternoon session. European stocks even managed to return into positive territory following a weak opening. This turn of sentiment was supported by a fall in energy commodity prices. In early trading the nearest futures for both Brent and gasoil (diesel) were both up around 3%, the Dutch TTF 1m forward gas jumped 5% higher, but all these gains evaporated and turned into small losses by the end of the day. The only constant in yesterday’s trading session was the stronger dollar, with the DXY dollar index up 0.6%, reaching its highest level in 10 years’ time. Concerns about the possibility of a 100bp hike by the Fed overshadowed those early on the day geopolitical sentiments. 2y UST yields pierced the 4% threshold for the first time since 2007.

At the end of the day, the Fed stuck with 75bp instead of surprising with a 100bp hike. Yet, there were some hawkish take-aways from yesterday’s FOMC meeting and this is also leading to further weakening of non-USD currencies in the aftermath of that. First of all, Powell reiterated the message that the Fed is strongly committed to reduce inflation back to target, and that the FOMC is purposefully moving its policy rates to a level where they are sufficiently restrictive.

Secondly, FOMC members indicated that they now expect the federal funds rate at 4.4% by year-end and that they see a terminal rate of 4.6% next year. That is a significant upward shift in the dot plot. The median member expects another 125bp in hikes this year, i.e., in line with our expectations of 75bp in November and 50 in December, but a large group in the Committee expects to hike by only 100bp. Moreover, though, the 4.6% terminal rate that the FOMC anticipates falls short of our prediction of 5%. As our US strategist explains, the main reason why our rates call remains above consensus and above the Fed’s own expectations is that we believe that a wage-price spiral has started in the US that will keep inflation persistent. The FOMC may not fully acknowledge this yet, but they have made it very clear that they will prioritize inflation and Powell is increasingly preparing the market for a not-so-soft economic landing. That intricate balance between higher for longer inflation and Fed rates combined with more economic pain ahead is reflected in a further flattening of the yield curve; 30y yields shed 7bp as a result.

AND NOW NEWSQUAWK

Japan intervened in FX markets on Super Central Bank Thursday – Newsquawk US Market Open

THURSDAY, SEP 22, 2022 – 06:26 AM

- Equities in Europe trade mostly lower but off worst levels; US equity futures trade on either side of the unchanged mark

- USD/JPY slumped as Japan announced FX market intervention via USD-selling and JPY-buying; DXY retreated from a 111.81 peak as a result

- Debt futures have witnessed some choppy price action at the sidelines, with the longer end of the curve outperforming

- Russian Deputy Chair of Security Council Medvedev said Russian weapons including nuclear can be used to defend territories in Russia

- Looking ahead, BoE, CBRT & SARB Policy Announcements, Speeches from BoE’s Haskel, Tenreyro & ECB’s Schnabel

View the full premarket movers and news report.

Or why not try Newsquawk’s squawk box free for 7 days?

22nd September 2022

LOOKING AHEAD

- BoE, CBRT & SARB Policy Announcements, Speeches from BoE’s Haskel, Tenreyro & ECB’s Schnabel

- Click here for the Week Ahead preview.

CENTRAL BANKS

BOJ/OFFICIALS

- Japanese Government and BoJ intervened in FX markets, according to the Japanese Vice Finance Minister – the government and the BoJ stepped into the market to buy JPY for USD.

- Japan Finance Minister Suzuki is concerned about excessive FX moves, that cannot be overlooked; will continue to closely watch FX markets, will take necessary steps against excessive moves; did not comment on size of intervention.

- BoJ kept its monetary policy unchanged, as expected, with rates at -0.10% and QQE with yield curve control maintained to target the 10yr JGB yield at around 0% through a unanimous decision. BoJ left its forward guidance unchanged in which it expects short- and long-term rates to remain at present or lower levels and maintained guidance on policy bias that it will take additional easing steps without hesitation as needed with an eye on the pandemic’s impact on the economy, while it extended the pandemic relief program.

- BoJ Governor Kuroda does not see the need to change forward guidance for about 2-3 years. Kuroda said will patiently continue powerful easing, will not hesitate to ease policy further if needed; closely watching financial and FX moves. JPY weakening is one-sided, nots there are speculative moves behind weakening JPY. Click here for full details.

SNB

- SNB hikes its Policy Rate by 75bps to 0.5% as expected; willing to be active in FX market as necessary; further rate hikes cannot be ruled out; no CHF classification in release. Click here for full details.

- SNB Chair Jordan says SNB ready to intervene to prevent excessive weakening or strengthening of the CHF; recent appreciation has helped dampen inflation. If there were to be an excessive appreciation of the Swiss franc, we would purchase foreign currency. If the Swiss franc were to weaken, however, we would consider selling foreign currency. Click here for full details.

- SNB Chair Jordan reiterates that the SNB can do interim rate decisions if needed.

NORGES

- Norges hikes its Key Policy Rate by 50bps as expected to 2.25%; policy rate will most likely be raised further in November; This may suggest a more gradual approach to policy rate setting ahead. Click here for full details.

- Norges Bank Governor Bache says the central bank is likely to hike by 25bps in November.

ECB

- ECB’s Schnabel says we must increase interest rates further, “I assume that the ECB Governing Council will hike interest rates further at its next meeting. At the moment, I cannot say how large this interest rate hike will be and up to what level we will”. In the short-term inflation could increase further, despite rate hikes. We do not currently see any indications of a wage-price spiral; wage growth has increased, but is still moderate, via t-online.

- ECB spokesperson says the central bank did not intervene in FX markets, via Reuters

OTHER

- Riksbank‘s Ohlsson says we do not have a target for the SEK.

- China’s PBoC says it will further improve macroprudential policy framework

- PBoC set USD/CNY mid-point at 6.9798 vs exp. 6.9946 (prev. 6.9536).

- Brazil Central Bank maintained the Selic Rate at 13.75% as expected via unanimous decision, while it will assess if the prospect of holding the Selic Rate long enough will ensure inflation convergence and stated that future policy steps could be adjusted. Furthermore, it will remain vigilant and will not hesitate to resume the cycle of rate adjustments if disinflation does not happen as expected.

- Hong Kong Monetary Authority raised the base rate by 75bps to 3.50%, as expected.

- Bank of Taiwan, Bank of Indonesia, and Bank of Philippines all raised rates in-line with expectations.

GEOPOLITICS

RUSSIA-UKRAINE

- Russian Deputy Chair of Security Council Medvedev says Russian weapons including nuclear can be used to defend territories in Russia, via Reuters.

- Ukrainian President Zelensky laid out five conditions for peace with Russia and said that they are non-negotiable, while conditions included punishment for Russian aggression, restoration of Ukraine’s security and territorial integrity, as well as security guarantees. Zelensky also stated that Ukrainian neutrality is out of the question and he ruled out that a settlement can happen on a different basis than the Ukrainian peace formula, according to Reuters.

OTHER

- The Iraqi Foreign Minister says “There is a discussion that the next session between Riyadh and Tehran will be at a level other than foreign ministers”, via Al Jazeera.

- Iranian Chief of Staff says “We will conduct a naval exercise in the Northern Ocean with Russia, China, and possibly Pakistan, Oman and other countries”, according to Al Jazeera

EUROPEAN TRADE

EQUITIES

- Equities in Europe trade mostly lower but off worst levels after an initial downbeat open following the fallout from the FOMC.

- Sectors are mostly negative but do not portray as much of a defensive bias as they did at the cash open, but banks outperform.

- US equity futures have been similarly clambering off lows into positive territory with little in the way of drivers to explain the trimming of losses

- Click here for more detail.

FX

- USD/JPY slumped as Japan announced FX market intervention via USD-selling and JPY-buying.

- DXY initially extended on gains to a current peak of 111.81 before recoiling as Japan intervened to stem the sliding JPY

- CHF buckles after markets were disappointed by the 75bps SNB hike as market expectations skewed towards 100bps.

- Other G10s are all off worst levels vs the Greenback.

- Click here for more detail.

- Click here for OpEx for the NY Cut.

FIXED INCOME

- Debt futures have witnessed some choppy price action at the sidelines, with the longer end of the curve outperforming on spread positioning and perhaps some relief buying.

- Bunds topped out at 142.02 vs 140.58 at the other end of the scale having closed at 141.20 on Wednesday, Gilts at 104.28 from a 103.40 low.

- T-note is midway between 114-00/113-18+ overnight extremes.

- Click here for more detail.

COMMODITIES

- WTI and Brent front-month futures have been climbing as a result of the pullback in the Dollar which was triggered by Japan intervening in the FX market.

- Spot gold also moved on the aforementioned Dollar action – with the yellow metal rising from a USD 1,655/oz intraday base towards closer to its 10 DMA (USD 1,685.87/oz).

- Base metals, a similar story, LME copper feels a boost from the Buck but fails to hold into gains north of USD 7,750/t.

- US Senator Manchin released the energy permitting bill to speed up energy projects which is expected to be included in the funding bill and his staff said the bill had the votes to pass the Senate, according to Reuters.

- Click here for more detail.

CRYPTO

- Bitcoin reclaimed the USD 19,000 level as the Dollar eased, whilst Ethereum extends gains towards 1,300.

NOTABLE EUROPEAN HEADLINES

- UK PM Truss wants to resolve the Northern Ireland Protocol dispute by the 25th anniversary of the Good Friday Agreement, according to FT.

APAC TRADE

- APAC stocks were mostly negative in the aftermath of the FOMC where the Fed hiked rates by 75bps and raised their dot plot projections, with the terminal rate forecast increased to 4.6% from 3.8%

- ASX 200 was closed today due to the National Day of Mourning for the Queen.

- Nikkei 225 briefly fell below 27,000 although bounced off its lows as the BoJ stuck to its dovish policy.

- Hang Seng and Shanghai Comp were pressured with notable losses in casino stocks and underperformance in the tech sector amid the higher rate environment as the HKMA also raised rates by 75bps in lockstep with the Fed.

NOTABLE APAC HEADLINES

- US Senators asked for a review of Apple’s (AAPL) plan to use Chinese chips, according to Washington Post.

- Japanese PM Kishida said they will further ease border restrictions from October, according to TBS.

- Hong Kong Gov’t expects, next week, to announce the removal of COVID hotel quarantine policy for overseas arrivals, via HKO1 citing sources.

NOTABLE APAC DATA

- New Zealand Trade Balance (Aug) -2447M (Prev. -1092.0M, Rev. -1406M)

- New Zealand Exports (Aug) 5.48B (Prev. 6.68B, Rev. 6.35B); Imports (Aug) 7.93B (Prev. 7.77B, Rev. 7.76B)

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 8.27 PTS OR 0.27% //Hang Sang CLOSED UP 296.67 PTS OR 1.61% /The Nikkei closed DOWN 159.30 PTS OR 0.58% //Australia’s all ordinaires CLOSED DOWN 1.55% /Chinese yuan (ONSHORE) closed DOWN AT 7.0732//OFFSHORE CHINESE YUAN DOWN 7.0709// /Oil DOWN TO 84.14 dollars per barrel for WTI and BRENT AT 90.88 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

3 a./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

EARLY LAST NIGHT:

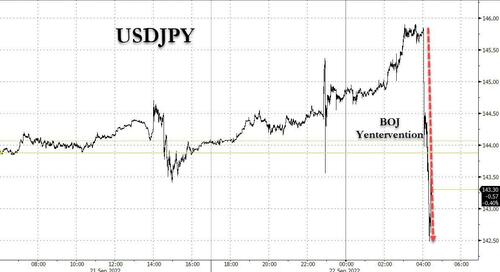

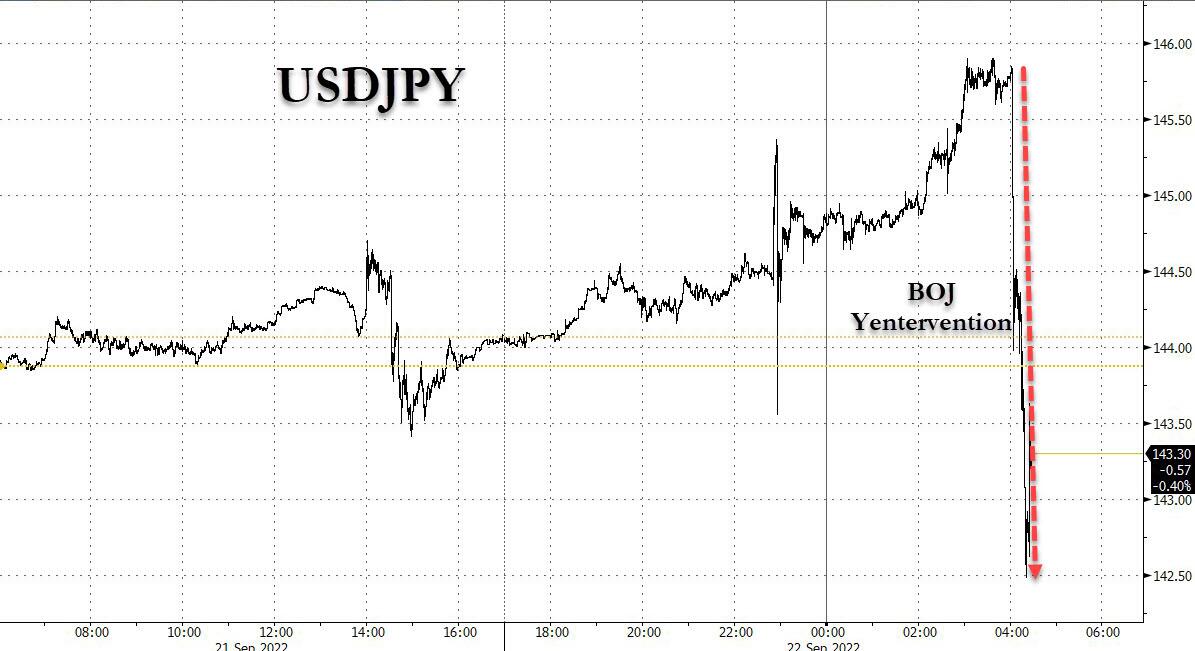

Last night the Yen disintegrated trading well above the 145 yen to dollar level. The Bank of Japan then decided to intervene

where it is now trading 141.72 to the dollar

(zerohedge)

Yen Disintegrates Below 145 After BOJ Decision As Traders Call Japan’s Intervention Bluff

THURSDAY, SEP 22, 2022 – 02:58 AM

After much bluster and jawboning, the BOJ’s repeated verbal intervention attempts to keep the USDJPY below 145 proved to be nothing but one giant bluff, at least for now.

Asian currencies – especially those like China and Japan refuse to tighten in sympathy – were already under huge pressure on Thursday after the Federal Reserve continued to tighten U.S. monetary policy when the Bank of Japan decided to counter the global tightening trend again, and stuck to its ultraloose stance.

The Japanese yen initially toyed with, then decisively weakened past 145 to the dollar, a fresh 24-year low, after the BOJ said it would maintain its monetary policy under which it is buying unlimited quantities of Japanese government bonds necessary to control the yield curve. And since the BOJ is caught in an impossible dilemma, where it can’t maintain Yield Curve Control (i.e., unlimited bond buying and thus currency printing) and a stable currency, Kuroda – whose shock and awe QE legacy is on the line, hyperinflation be damned – has again picked to sacrifice the yen which is in free fall this morning, with some speculating it could plummet as much as 147 today unless the BOJ steps in with intervention.

The BOJ announced its decision hours after the Federal Open Market Committee on Wednesday raised its key policy rate 75 basis points, or three-quarters of a percentage point, to a range of 3.0% to 3.25%, tightening for the third straight meeting, following increases June and July.

The decisions reiterated the widening gap between the Japanese central bank’s dovish policy stance and the Fed’s hawkish stance, stimulating investors to buy the dollars and sell the yen.

“We are ready to take action anytime,” said Masato Kanda, Japan’s vice finance minister for international affairs, after the yen crossed 145. “We cannot tolerate excess volatility and disorderly currency moves.” But his words this time did nothing to contain the slide, as the is sinking at an accelerating pace, much to the shock of Japanese pensioners who are not only seeing their purchasing power evaporate but are assured of importing massive inflation in the months ahead.

What happens next? According to Jun Kato, chief market analyst at Shinkin Asset Management in Tokyo, the dollar/yen could fall as low as 147 later on Thursday though the pace of yen selling is expected to slow from current levels.

The probability isn’t “zero” for USD/JPY to try its upside at the 1998 high of 147.66 later today, Kato said. “But players largely seem to have digested all the news of Fed and BOJ, and a Swiss rate hike is already factored in to limit much more upside for dollar/yen.”

Commenting on the repeated – and increasingly laughable – warnings from Japan’s top currency official Masato Kanda’s warnings which are aimed at lowering USD/JPY levels, Kato said that actual intervention is unlikely and Kanda’s comments are “nothing more than a gesture without real ammunition in store, as physical intervention can only adjust positioning and pace and will not alter a trend.” And once transitory adjustments are made, he expects the USDJPY to continue rising given fundamentals of higher US yields as the Fed makes its hawkish stance clear, adding that if the US yield curve flattens further and concerns grow more strongly about aggressive rate hikes now hurting future growth, dollar/yen may see a peak between 145-150.

Sony Financial Group agreed that there is a possibility of further rate checks by the Bank of Japan, though intervention is unrealistic: “The BOJ has conducted a rate check at 145 yen, so we are aware of that level as an upside potential,” said Juntaro Morimoto, a Tokyo-based currency analyst with Sony Financial. However, since “the gap in monetary policy between the US and Japan is widening, it is only a matter of time before it breaks through 145 yen again.” Ultimately, Morimoto sees probability of Yen at 150 against the dollar a little too far on limited room for US interest rates to rise.

Perhaps that’s true, but at this moment, the BOJ – whose bluff to intervene in the FX market has been called and the central bank has folded like a rank amateur- has effectively given the market a carte blanche to destroy the yen, especially since all those rate “checks” we read so much about proved to be just typical Japanese hot air.

The Japanese central bank conducted a foreign exchange “check” on Sept. 14, asking market participants about exchange rates. This is believed to be a move to prepare for foreign exchange intervention aimed at easing the excessive depreciation of the yen.

However, many analysts believe intervention will be next to impossible. In the case of intervention where the yen is bought and dollars sold, the maximum amount that can be used depends on the dollar cash balance in a special account for foreign exchange funds, which is under the control of the Ministry of Finance.

“As the maximum amount of foreign exchange intervention is known in advance, and [if] the BOJ decides to intervene by selling dollars and buying yen, it may inadvertently trigger speculative selling of the yen,” Masahiro Ichikawa, chief market strategist at Sumitomo Mitsui DS Asset Management, pointed out in a note.

“If the Japanese government and the BOJ are to work together to prevent the yen from depreciating, it is likely that a revision of the ultraloose monetary policy will come first, rather than currency intervention,” he added. However, in that case, “a full explanation will be required as to how the price target should be considered before the revision is made.”

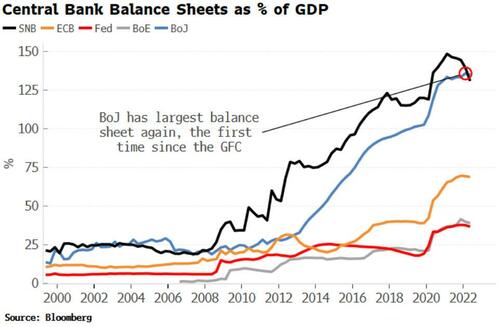

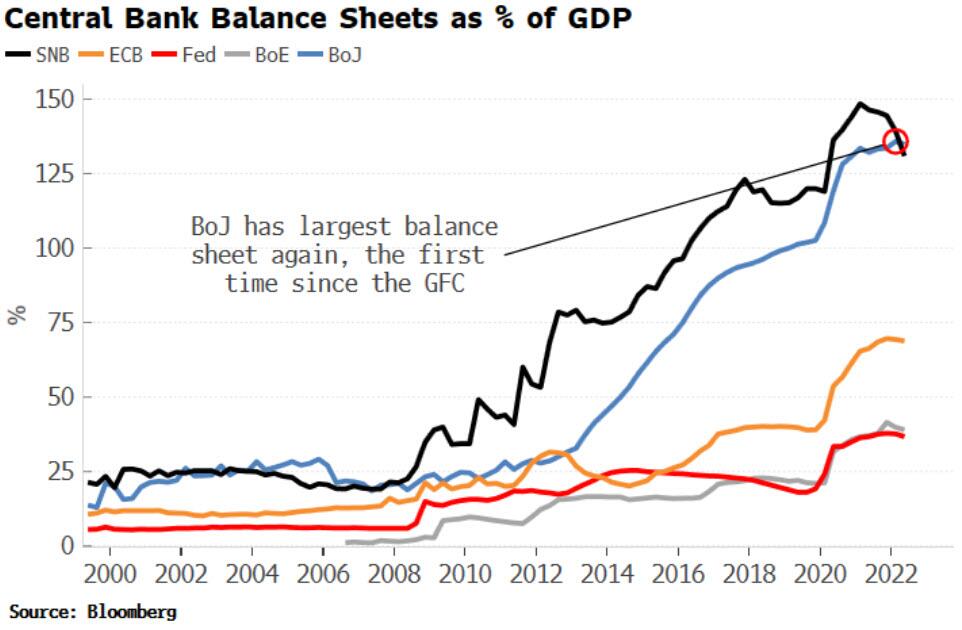

There is another reason why Kuroda is in deep fecal matter as Japan’s currency collapse accelerates: as Bloomberg notes, the Bank of Japan once again is the world’s largest central bank in GDP terms. The growing risks to financial stability will put further pressure on the bank to exit its ultra-loose monetary policy. As shown in the chart below, that mantle of the largest central-bank balance sheet was held by the Swiss National Bank since around 2007, but in recent months the SNB has been selling assets to support the franc in a bid to limit inflation.

The size of the BoJ’s balance sheet, at 135% of GDP (the real-time figure will be higher due to recent BoJ asset buying) highlights the scale of the mounting problem given the risks to financial stability.

As Bloomberg’s Simon White notes, the SNB, who are likely to raise rates later this morning, were pretty quick to change track when global inflation became a problem. They are likely to have a small sense of relief that, while their balance sheet is still large, it is now falling, and is no longer the world’s largest.

END

LATER IN THE EVENING LAST NIGHT:

After a couple of weeks the Yen will resume its downwardly direction

(zerohedge)

Yentervention! Japan “Boldly” Enters FX Market, Sends USDJPY Tumbling… But Not For Long

THURSDAY, SEP 22, 2022 – 04:36 AM

With the yen plummeting earlier today, after the BOJ decided to keep its YCC and abandon the yen to its collapsing fate, we said that the BOJ better intervene soon or all hell would break loose:

Two hours later, the BOJ has done just that, and after warning earlier in the session of “stealth intervention”, it decided to finally put money where its endlessly big mouth is with the first Japanese FX intervention in 24 years that was anything but stealth:

- The Japanese government intervened in the foreign exchange market to prop up the yen, the country’s top currency official Masato Kanda says.

- Kanda, vice finance minister for international affairs, spoke to reporters after the yen climbed sharply against the dollar, erasing most of its decline following the Bank of Japan’s decision to maintain ultra-easy monetary policy

- Kanda says Japan took “bold action” in markets

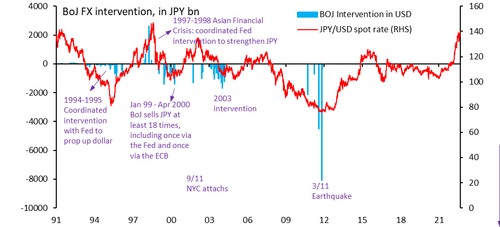

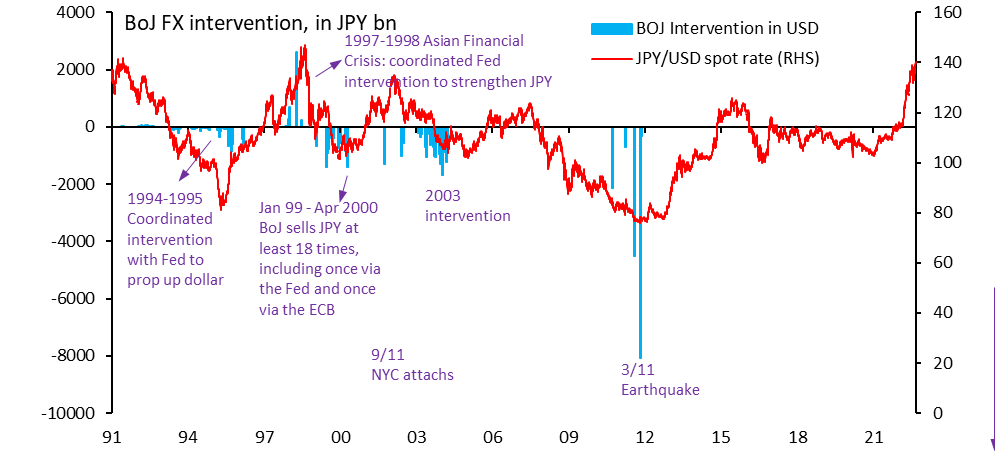

Here a quick primer: in Japan, FX interventions are carried out by the Bank of Japan on behalf of the Ministry of Finance. The last time Japan intervened to sell dollars and buy yen in June 1998 at the height of the Asian currency crisis, while the last time officials stepped into markets to sell yen to weaken the currency was in November 2011.

In kneejerk response, the Yen predictably soared, jumping as much as 1.1% as the USDJPY collapsed by a whopping 300 pips from 145.50 to 142.50!

It now appears that the new market level which the BOJ is comfortable with is around 143. However, now that the BOJ has fired its yentervention bazooka, with fundamentals screaming for a far weaker yen for years to come, especially with Kuroda stating that there will be no change in policy for at least two years…

- *BOJ’S KURODA: NO NEED TO CHANGE GUIDANCE FOR 2 OR 3 YEARS

… as the BOJ has no choice but to prop up the YCC while ignoring the collapse in the yen, it is only a matter of time before this BOJ/MOF intervention fizzles, as have all previous attempts to contain the USDJPY through direct currency intervention…

… and the yen resumes its march toward 150, then 200 and so on, on its irreversible way to the scrapheap of MMT-destroyed currencies.

In kneejerk response, we said that while the BOJ panic may prop up the JPY for a few weeks, only a coordinated intervention has any chance of a sustained response.

And sure enough, the Oversea-Chinese Banking Corp. agrees with us, writing that Japan’s intervention to prop up the yen will have more impact if the move is coordinated with other central banks. “The move may still wow markets because they are doing it to buy JPY for the first time in more than 20 years,” says Christopher Wong, a currency strategist at OCBC, adding that “based on historical observation of BOJ intervention, JPY typically moves between 3% and 5% in the direction of intervention and the impact is more pronounced within the first 48 hours.”

But as we also said, “while intervention may slow the pace of JPY depreciation, the move alone is not likely to alter the underlying trend unless USD, UST yields turn lower or the BOJ changes/tweaks its monetary policy. Instead, “at best, their action can help to slow the pace of JPY depreciation.”

An analysis by Bloomberg echoes our skepticism: they write that historically, the yen boost post intervention is likely to endure over a 1-week horizon. However, the effect will diminish soon after — even with repeated yen buying. A study of 5 distinct historical intervention periods shows:

- USD/JPY dived in the week following intervention, and by an average of 1.7%, with the trade-weighted exchange rate up 2.6%

- But, that was it. The average peak impact occurred after one week

- A month later, the effect had waned, even with follow-up interventions. One-month trade-weighted changes averaged 1.7%. That is, the yen had declined 0.9% on average between 1-week and 1-month

Translation: USDJPY 150 and much more is now guaranteed, even if the time to reach it is delayed by one or two weeks.

end

Nobody has traded the 10 yr Japanese bond for the past two days

(ZEROHEDGE)

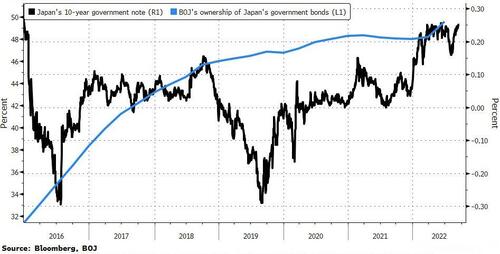

Nobody Has Traded 10Y Japanese Govt Bonds For 2 Days!

WEDNESDAY, SEP 21, 2022 – 05:20 PM

No trades (none!) were reported overnight in the benchmark 10Y Japanese Government Bond (JGB) for the second straight day.

This is the first such occurrence since 1999.

As Bloomberg reports, trading volumes in JGBs have dried up over the years as the BOJ scooped up sizable chunks of the debt to keep a cap on yields.

“The BOJ’s fixed-rate operations have become the JGB trading floor,” said Katsutoshi Inadome, a strategist at Mitsubishi UFJ in Tokyo.

“Players are guaranteed to find a solid buyer who also buys large lots.”

Traders also lack the incentive to trade benchmark 10-year notes because they expect yields to rise as the Fed aggressively tightens monetary policy, according to Mitsubishi UFJ Morgan Stanley Securities.

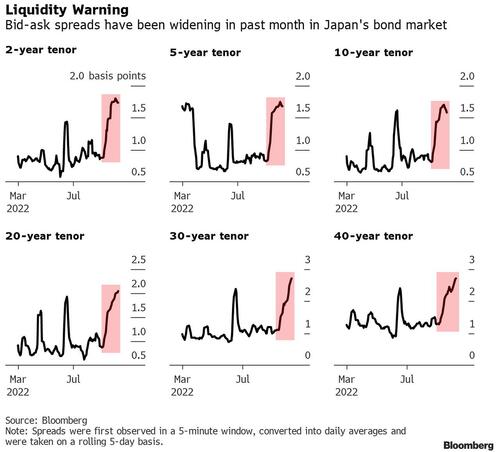

Bid-ask spreads for JGBs have exploded since March as inflation fears ripped through global bond markets (but BoJ remains stuck in its easing policy framework)…

The irony of all this is that at the same time as liquidity in the JGB market has disappeared, The Bank of Japan bought 1.26 trillion yen ($8.8 billion) of government bonds, the largest daily amount since June as it aggressively defended the upper bound of its yield curve control band…

Pressure is building on the BOJ to defend its yield-curve-control policy tonight after The Fed hikes (75bps is consensus) today. Widening yield differentials between the US and Japan have resulted in the yen sliding to a 24-year low.

Finally, we note that the issue of diminishing liquidity isn’t limited to Japanese bonds.

Bank of America analysts warned in a note this month that shrinking trading volumes in the US Treasury market may be one of the greatest threats to global financial stability.

end

3c CHINA

CHINA/RUSSIA

END

CHINA/

end

4/EUROPEAN AFFAIRS//UK AFFAIRS

FRANCE//EUROPE//ENERGY/

Now it is France’s turn to nationalize its struggling nuclear industry.

(Zaremba/OilPrice.com)

France Prepares To Nationalize Its Struggling Nuclear Industry

THURSDAY, SEP 22, 2022 – 03:30 AM

By Haley Zaremba of OilPrice.com