by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSE: DOWN $33.50 to $1668.20

SILVER PRICE CLOSE: DOWN $0.65 to $19.59

Access prices: closes

Gold ACCESS CLOSE 1667.70

Silver ACCESS CLOSE: 19.61

New: early yesterday morning//

Bitcoin morning price: $19,254 DOWN 228

Bitcoin: afternoon price: $19,254 DOWN 228

Platinum price closing DOWN 19.65 AT $899.65

Palladium price; closing DOWN $39.40 at $2156.25

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/closing ACCESS

CANADIAN GOLD $2296.90 CDN DOLLARS PER OZ DOWN $25.75 CDN DOLLARS

BRITISH GOLD IN POUNDS: 1507.00 POUNDS PER OZ DOWN 18.57 BRITISH POUNDS PER OZ/

EURO GOLD: 1717.50 EUROS PER OZ// DOWN 18.30 EUROS PER OZ///

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: OCTOBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,700.500000000 USD

INTENT DATE: 10/07/2022 DELIVERY DATE: 10/11/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 1

118 C MACQUARIE FUT 8

132 C SG AMERICAS 138 3

323 H HSBC 2

624 C BOFA SECURITIES 1

624 H BOFA SECURITIES 29

661 C JP MORGAN 81

800 C MAREX SPEC 6 17

880 C CITIGROUP 2

TOTAL: 144 144

MONTH TO DATE: 21,519

JPMORGAN STOPPED 81/144

GOLD: NUMBER OF NOTICES FILED FOR OCT CONTRACT: 144 NOTICES FOR 14400 OZ //.4477 TONNES

total notices so far: 21,519 contracts for 2,151,900 oz (66.933 tonnes)

SILVER NOTICES: 38 NOTICES FILED FOR 190,000 OZ/

total number of notices filed so far this month 359 : for 1,795,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $33.50

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: ////A WITHDRAWAL OF 2.03 TONNES FROM THE GLD/

INVENTORY RESTS AT 944.31 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 65 CENTS

AT THE SLV// ://NO CHANGES IN SILVER INVENTORY AT THE SLV//:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 473.130 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A SMALL SIZED 83 CONTRACTS TO 126,402 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE TINY LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR HUGE $0.37 LOSS IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.37). HOWEVER OUR SPEC SHORTS ARE DESPERATELY TRYING TO COVER THEIR MASSIVE COMEX OI SHORTFALL. BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS.

WE MUST HAVE HAD:

I) MINIMAL SPECULATOR SHORT COVERINGS ////CONTINUED BANKER OI COMEX ADDITIONS /// SOME NEWBIE SPEC SHORT ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.580 MILLION OZ FOLLOWING A 185,000 OZ QUEUE JUMP / // V) SMALL SIZED COMEX OI LOSS/ MINIMAL SPEC COVERING THEIR SHORTS.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: –263

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT:

TOTAL CONTRACTS for 8 days, total 49,775 contracts: 24.887 million oz OR 3.1109MILLION OZ PER DAY. (622 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 24.887 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 24.887 MILLION OZ INITIAL

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 83 WITH OUR CONSIDERABLE $0.37 LOSS IN SILVER PRICING AT THE COMEX// FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 350 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /SOME BANKER ADDITIONS // SMALL SHORT ADDITIONS//SMALL NEWBIE SPEC LONG ADDITIONS// /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT. OF 1.580 MILLION OZ FOLLOWED BY TODAY’S 185,000 QUEUE JUMP .. WE HAD A SMALL SIZED GAIN OF 267 OI CONTRACTS ON THE TWO EXCHANGES FOR 1.335 MILLION OZ..

WE HAD 38 NOTICE(S) FILED TODAY FOR 190,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 6 CONTRACTS TO 433,153 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED — -750 CONTRACTS.

.

THE TINY SIZED INCREASE IN COMEX OI CAME DESPITE OUR LOSS IN PRICE OF $10.70//COMEX GOLD TRADING/FRIDAY // SOME SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT. AT 66.099 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 7300 OZ//NEW STANDING 67.906 TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED DESPITE OUR LOSS IN PRICE OF $10.70 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 2192 OI CONTRACTS 6.818 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1436 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 433,253

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1442 CONTRACTS WITH 6 CONTRACTS INCREASED AT THE COMEX AND 1436 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1442 CONTRACTS OR 4.48 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1436) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (6): TOTAL GAIN IN THE TWO EXCHANGES 1442 CONTRACTS. WE NO DOUBT HAD 1) MINOR SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS///NEWBIE SPEC SHORT ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 66.099 TONNES FOLLOWED BY TODAY’S 7300 OZ QUEUE JUMP///NEW STANDING 67.906 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) SMALL SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT. :

16,585 CONTRACTS OR 1,658,500 OZ OR 51.58 TONNES 8TRADING DAY(S) AND THUS AVERAGING: 2073 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES: 51.58 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 57.58/3550 x 100% TONNES 1.63% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 57.58 TONNES INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A SMALL SIZED 83 CONTRACT OI TO 126,209 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 350 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 350 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 83 CONTRACTS AND ADD TO THE 350 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED GAIN OF 267 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 1.335 MILLION OZ

OCCURRED WITH OUR LOSS IN PRICE OF $0.37

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED DOWN 50.24 PTS OR 1.66% //Hang Seng CLOSED DOWN 523.39 OR 2.95% /The Nikkei closed DOWN 195.19PTS OR 0.71% //Australia’s all ordinaires CLOSED DOWN 1.49% /Chinese yuan (ONSHORE) closed DOWN TO 7.1474 //OFFSHORE CHINESE YUAN DOWN 7.1514// /Oil UP TO 91,87 dollars per barrel for WTI and BRENT AT 97.25 / Stocks in Europe OPENED MOSTLY RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 6 CONTRACTS TO 433,253 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS SMALL COMEX INCREASE OCCURRED WITH DESPITE OUR STRONG FALL IN PRICE OF $10.70 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (1436 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1436 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :1436 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1436 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2192 CONTRACTS IN THAT 1436 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 756 CONTRACTS..AND THIS FAIR GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $10.70//WE HAD SPEC SHORTS ADDING TO THEIR POSITIONS WITH BANKERS TAKING THE OTHER SIDE AS BUYERS OF COMEX GOLD CONTRACTS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING OCT (67.906),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 67.906 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $10.70) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 1442 CONTRACTS // WE HAVE REGISTERED A FAIR GAIN OF 6.818 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR OCT. (67.906 TONNES)…THIS WAS ACCOMPLISHED WITH A FALL IN PRICE OF $10.70

WE HAD -750 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 2192 CONTRACTS OR 219200 OZ OR 6.818 TONNES

Estimated gold volume 153,932// poor//

final gold volumes/yesterday 168,097/ poor

INITIAL STANDINGS FOR OCT ’22 COMEX GOLD //OCT 10

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 157,218.396oz BRINKS Delaware JPMorgan includes 8 and 2948 kilobars |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 353,661 oz Brinks 11 kilobars |

| No of oz served (contracts) today | 144 notice(s) 14400 OZ 0.4479 TONNES |

| No of oz to be served (notices) | 457 contracts 45700oz 1.421 TONNES |

| Total monthly oz gold served (contracts) so far this month | 21,375 notices 2,137,500 66.485 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

Into Brinks: 353.661 (11 kilobars)

total deposits 353.661 oz

customer withdrawals: 3

i) Out of Brinks: 62,180.04 oz

ii) Out of Delaware: 257.208 oz (8 kilobars)

iii) Out of JPMorgan: 94,781.148 oz (2948 kilobars)

total: 157,218.396 oz

total in tonnes: 4.89 tonnes

Adjustments: 2// all dealer to customer

Brinks: 16,636.767 oz

Manfra: 1101.154 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT we have an oi of 601 contracts having GAINED 32 contracts . We had 41 contracts

filed on FRIDAY, so we gained 73 contracts or an additional 7300 oz will stand in this active delivery month of Oct.

We will gain gold oz standing on each and every trading day from this day forth until the conclusion of October.

(remember that queue jumping is really EFP’s exercised from London for gold underwritten by COMEX based bankers)

November GAINED 113 contracts to stand at 2959

December lost 2026 contracts down to 370,723

We had 144 notice(s) filed today for 14400 oz FOR THE OCT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 144 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 144 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT /2022. contract month,

we take the total number of notices filed so far for the month (21,519) x 100 oz , to which we add the difference between the open interest for the front month of (OCT 601 CONTRACTS) minus the number of notices served upon today 144 x 100 oz per contract equals 2,183200 OZ OR 67.906 TONNES the number of TONNES standing in this active month of OCT. (TOTALS CORRECTED FROM FRIDAY)

thus the INITIAL standings for gold for the OCT contract month:

No of notices filed so far (21,519) x 100 oz+ (601) OI for the front month minus the number of notices served upon today (144} x 100 oz} which equals 2,183,200, oz standing OR 67.906 TONNES in this NON active delivery month of OCTOBER.

TOTAL COMEX GOLD STANDING: 67.906 TONNES (A HUMONGOUS STANDING FOR OCT (GENERALLY THE POOREST DELIVERY MONTHS FOR AN ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,067,434 OZ (REG GOLD- PLEDGED GOLD) 340.166 tonnes//rapidly declining

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 26,125,011.865 OZ

TOTAL REGISTERED GOLD: 12,796,922.668 OZ (398.03 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 13,328,089.202 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,729,579OZ (REG GOLD- PLEDGED GOLD) 333.73 tonnes//rapidly declining

END

SILVER/COMEX

OCT 10//INITIAL OCT SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 671,353.473oz Brinks JPM CNT |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 38 CONTRACT(S) 190,000 OZ) |

| No of oz to be served (notices) | 37 contracts (185,000 oz) |

| Total monthly oz silver served (contracts) | 359 contracts 1,795,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

Total deposits: nil oz

JPMorgan has a total silver weight: 160.806million oz/311.952million =51.54% of comex

Comex withdrawals: 3

i)Out of CNT 67,412.873 oz

ii) Out of Brinks 3807.600 oz

iii) OUt of JPMorgan: 600,133.000

total withdrawals: 671,353.473 oz

adjustments: // 1

Brinks: dealer to customer: 14,577.213 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 40.130 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 311.952 MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF OCT OI: 77 CONTRACTS HAVING LOST 31 CONTRACT(S.)

WE HAD 68 NOTICES FILED ON FRIDAY SO WE GAINED 37

SILVER CONTRACTS OR AN ADDITIONAL 185,000 OZ WILL STAND FOR OCT.

NOVEMBER GAINED 6 CONTRACTS TO STAND AT 402

DECEMBER SAW A LOSS OF 2026 CONTRACTS DOWN TO 105,311

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 68 for 340,000 oz

Comex volumes:60,009// est. volume today// fair

Comex volume: confirmed yesterday: 67,161 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 359 x 5,000 oz = 1,795,000 oz

to which we add the difference between the open interest for the front month of OCT(77) and the number of notices served upon today 38 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT./2022 contract month: 359 (notices served so far) x 5000 oz + OI for front month of OCT (77) – number of notices served upon today (38) x 5000 oz of silver standing for the OCT contract month equates 1,980,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:61,618// est. volume today// poor

Comex volume: confirmed yesterday: 54,383contracts ( poor)

END

GLD AND SLV INVENTORY LEVELS

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

GLD INVENTORY: 944.31 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

CLOSING INVENTORY 473.170 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: You’ll Need Gold When The Fed Loses This Inflation Fight

MONDAY, OCT 10, 2022 – 08:40 AM

Some people in the mainstream have been talking about gold’s demise as an important financial asset. Meanwhile, central banks continue to buy gold. What are the gold naysayers missing? Peter Schiff appeared on Fox Business with Charles Payne to talk about the price of gold and why some investors are starting to realize they’ll need gold as the Fed loses its inflation fight.

Payne opened up the interview by saying, “You’ve heard about the death of gold a million times. But what is it that people forget about gold? When it’s going down, moving flat, not moving, and it feels like, OK, it’s no longer what it might have been in the past.”

Peter said, “I didn’t get the memo!”

And had I gotten that memo, I would have just thrown it in the trash. But what a lot of people don’t realize about gold is that it’s money. It is liquidity. It’s everything else that loses value in relationship to gold. Gold is a better form of money than anything governments have come up with to replace it. And in times like this, where we have inflation that’s going to run out of control, and central banks that are powerless to rein it in because they’ve created it, and they’ve created economies that are dependent on it, more and more people, including central banks, are going to be returning to gold.”

Peter pointed out that gold sold off based on the notion that the Federal Reserve was going to win its fight against inflation. We had a rally in gold after the Bank of England surrendered to inflation and pivoted back to lose monetary policy to rescue its pension system. Peter said some people might be starting to realize that the Fed isn’t going to win either.

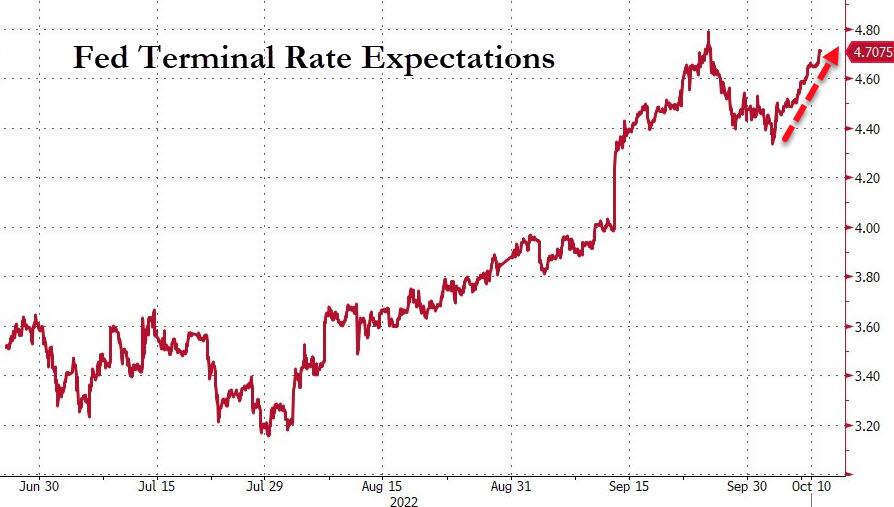

The Bank of England was just as committed to fighting inflation as Powell, but as soon as it created the beginnings of a financial crisis, they did an about-face and went right back to quantitative easing. I think the same predicament is going to befall the Federal Reserve, and before too long, inflation is going to take a back seat to an even greater crisis — a financial crisis and a worsening recession. And the Fed is going to go right back to more quantitative easing. There’ll be no more rate hikes. In fact, there may be rate cuts. Inflation is going to be nowhere near 2% when they do that. In fact, it’s headed closer to 20%.”

Payne agreed with Peter, saying the Fed’s best weapon has been “jaw-boning,” and that he doesn’t see the central bank going as far as it claims. He also brought up the issue of the $31 trillion national debt. Will higher interest rates spark a debt crisis for the US government?

Peter reminded us that a year ago, Treasury Secretary Janet Yellen said there was no reason to worry about the national debt because interest rates were so low.

Well, now interest rates have skyrocketed.”

When Janet Yellen made that comment, the yield on a 1-year T-bill was about .25%. Now it’s 4%.

You’ve got a 16-fold increase in the cost of funding that debt. And remember, that debt keeps having to be rolled over. The government has very short financing on this national debt. So, it’s already a problem. And it’s going to become a much bigger problem. It’s one of the reasons the Fed is going to chicken out in the fight against inflation. Because the US government would be forced to default on that debt if it actually let interest rates rise high enough to bring inflation down to 2%.”

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

Shhh! Don’t Tell the Fed or Mainstream Media that Systemic Contagion at Wall Street Banks Is Already Here

By Pam Martens and Russ Martens: October 10, 2022

At Fed Chairman Jerome Powell’s last press conference on September 21 he said that there is “good reason to think that this will continue to be a reasonably strong economy.” Unfortunately, the U.S. can’t have a strong economy without strong banks willing and able to lend. And there are serious storm fronts in that area that the Fed Chair and mainstream media are choosing to ignore.

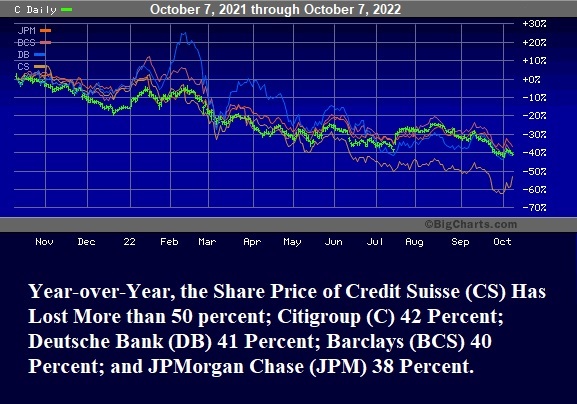

Last week multiple news outlets raised the question as to whether the troubles at Credit Suisse signaled another “Lehman moment.” (See here, here, and here, for example.) A “Lehman moment” refers to the former 158-year old Wall Street investment bank, Lehman Brothers, collapsing into bankruptcy on September 15, 2008 during a widening financial crisis on Wall Street. Because Lehman was the only major Wall Street firm that the Fed allowed to collapse into bankruptcy (rather than orchestrating a bailout), it has been mistakenly viewed all these years as the catalyst for the carnage that followed. As we will explain shortly, that role rightfully belongs to Citigroup.

According to documents released by the Financial Crisis Inquiry Commission (FCIC), at the time of Lehman Brothers’ bankruptcy it had more than 900,000 derivative contracts outstanding and had used the largest banks on Wall Street as its counterparties to many of these trades. The FCIC data shows that Lehman had more than 53,000 derivative contracts with JPMorgan Chase; more than 40,000 with Morgan Stanley; over 24,000 with Citigroup’s Citibank; over 23,000 with Bank of America; and almost 19,000 with Goldman Sachs.

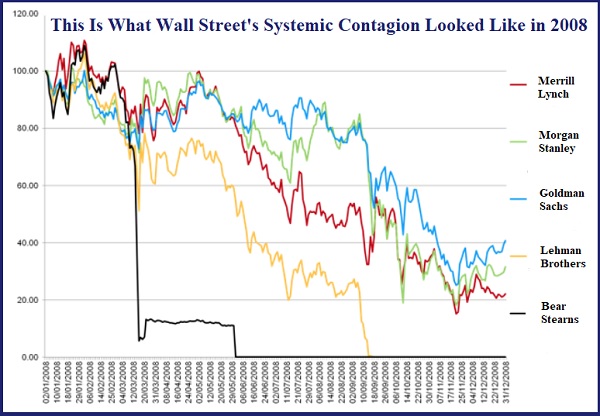

Below is a share price chart of what contagion looked like on Wall Street in 2008. Notice the highly correlated share price pattern in 2008 and the highly correlated share price pattern in the chart above in 2022.

Lehman’s interconnectedness with other major Wall Street firms certainly fueled some of the systemic contagion on Wall Street in 2008. But the real culprit was Citigroup – a reckless trading house on Wall Street which owned, both then and now, a large federally-insured commercial bank, Citibank. These are just a few of the headlines about Citigroup that ran long before Lehman’s collapse into bankruptcy:

January 10, 2008, Wall Street Journal: “Citigroup, Merrill Seek More Foreign Capital,” noting: “Two of the biggest names on Wall Street are going hat in hand, again, to foreign investors.”

January 17, 2008, Los Angeles Times: “Citigroup Loses Nearly $10 Billion”

March 5, 2008, MarketWatch: “Citigroup CEO Says Firm ‘Financially Sound’” with the opening sentence explaining that “The chief executive of Citigroup sought to allay investor fears Wednesday, a day after the stock hit a multiyear low…”

April 20, 2008, New York Times: “Citigroup Records a Loss and Plans 9000 Layoffs,” explaining that the bank reported a $5.1 billion loss and would have to slash jobs.

June 26, 2008, Wall Street Journal: “Citigroup: Worth Less and Less Every Day,” shares the news that the stock was worth one-third of where it had been at its 52-week high.

July 23, 2008, Bloomberg News: “Citigroup Unravels as Reed Regrets Universal Model.”

On July 14, 2008, Bloomberg News reported that in addition to holding $2.2 trillion in assets on its balance sheet, Citigroup has $1.1 trillion of “mysterious” assets off its balance sheet, including “trusts to sell mortgage-backed securities, financing vehicles to issue short-term debt and collateralized debt obligations, or CDOs, to repackage bonds.”

Sheila Bair, the Chair of the Federal Deposit Insurance Corporation in 2008, wrote the following about Citigroup in her book Bull by the Horns:

“By November [2008], the supposedly solvent Citi was back on the ropes, in need of another government handout. The market didn’t buy the OCC’s and NY Fed’s strategy of making it look as though Citi was as healthy as the other commercial banks. Citi had not had a profitable quarter since the second quarter of 2007. Its losses were not attributable to uncontrollable ‘market conditions’; they were attributable to weak management, high levels of leverage, and excessive risk taking. It had major losses driven by their exposures to a virtual hit list of high-risk lending; subprime mortgages, ‘Alt-A’ mortgages, ‘designer’ credit cards, leveraged loans, and poorly underwritten commercial real estate. It had loaded up on exotic CDOs and auction-rate securities. It was taking losses on credit default swaps entered into with weak counterparties, and it had relied on unstable volatile funding – a lot of short-term loans and foreign deposits. If you wanted to make a definitive list of all the bad practices that had led to the crisis, all you had to do was look at Citi’s financial strategies…What’s more, virtually no meaningful supervisory measures had been taken against the bank by either the OCC or the NY Fed…Instead, the OCC and the NY Fed stood by as that sick bank continued to pay major dividends and pretended that it was healthy.”

Notice the sentence in the above paragraph that reads: “It was taking losses on credit default swaps entered into with weak counterparties….” Bair was describing the situation in 2008. Now consider this headline we ran just last week at Wall Street On Parade: New Study: Wall Street Banks Are Doubling Down on Risk by Selling Credit Default Swaps on their Risky Derivatives Counterparties. It is nothing less than an indictment of the U.S. Congress that this is allowed to happen after derivatives caused the greatest U.S. economic collapse in 2008 since the Great Depression.

The official report from the Financial Crisis Inquiry Commission, following an in- depth investigation of the 2008 collapse, wrote this about Credit Default Swaps:

“OTC derivatives contributed to the crisis in three significant ways. First, one type of derivative—credit default swaps (CDS)—fueled the mortgage securitization pipeline. CDS were sold to investors to protect against the default or decline in value of mortgage-related securities backed by risky loans…

“Second, CDS were essential to the creation of synthetic CDOs. These synthetic CDOs were merely bets on the performance of real mortgage- related securities. They amplified the losses from the collapse of the housing bubble by allowing multiple bets on the same securities and helped spread them throughout the financial system…

“Finally, when the housing bubble popped and crisis followed, derivatives were in the center of the storm. AIG, which had not been required to put aside capital reserves as a cushion for the protection it was selling, was bailed out when it could not meet its obligations. The government ultimately committed more than $180 billion because of concerns that AIG’s collapse would trigger cascading losses throughout the global financial system. In addition, the existence of millions of derivatives contracts of all types between systemically important financial institutions—unseen and unknown in this unregulated market—added to uncertainty and escalated panic, helping to precipitate government assistance to those institutions.”

This morning the Bank of England is in full blown crisis mode, setting up another emergency bailout facility that is very similar to that used by the Fed during the 2008 financial crisis. And, once again, derivatives are at the heart of the problem.

For its part, the Fed announced last year that it had, for the first time in its 109-year history, created a Standing Repo Facility where, on a permanent basis it will make $500 billion available to bail out the hubris on Wall Street. The Fed Chair has the power to increase that $500 billion on a temporary basis at his “discretion.”

And if all of this wasn’t sickening enough, the Fed Chairman who set the Fed on the course of endless Wall Street bailouts, quantitative easing, and destructive meddling in markets — Ben Bernanke — was one of three receiving the Nobel Prize in economic sciences this morning. (You can’t make this stuff up.)

It’s long past the time for the United States Congress to put an end to these serial bailouts of Wall Street by the Fed and pass legislation to restore the Glass-Steagall Act so that the casinos on Wall Street are permanently separated from the nation’s federally-insured banks.

-END-

end

Lawrie Williams

END

3.Chris Powell of GATA provides to us very important physical commentaries

Fascinating!

New Wyoming currency, the Goldback, is printed with actual gold

Submitted by admin on Fri, 2022-10-07 20:46Section: Daily Dispatches

By Kevin Killough

Cowboy State Daily, Cheyenne, Wyoming

Monday, September 26, 2022

A private currency company is hoping its new Wyoming currency has the Midas touch for users.

Utah-based Goldback Inc. has released a Wyoming Series of its Goldback bills printed with physical gold in the currency, which the company says makes its value more stable than the U.S. dollar.

Nearly 40 Cowboy State businesses are featured on the company’s website as expressing interest in accepting Wyoming Goldbacks.

Trying to make purchases with actual gold runs into a few impracticalities. If you plopped down an ounce of gold to buy groceries — putting aside the fact that businesses don’t accept gold as payment — that ounce of gold is worth nearly $2,000. Shaving that down to pay for $100 worth of groceries isn’t easy. …

In spring 2019, Jeremy Cordon, president and founder of Goldbacks Inc., began working on a way that small consumer purchases could be made with physical gold.

Buying a pack of gum could cost a couple bucks. In physical gold, that’s about a sixth the size of a BB from a BB gun.

“No one could ever weigh it. No one can ever verify its purity,” he said. “So in raw gold form, you can’t circulate it because it just doesn’t make sense.”

That’s where the Goldback comes in. Goldbacks are bills you can put into your wallet. The bill with the least amount of gold contains 1/1,000th of an ounce, but they also come with larger amounts of gold. The bill has a layer of polymer with all the artwork on it, as well as six anti-counterfeiting measures, Mills said.

The gold is atomized and layered onto the polymer “literally atom by atom,” Mills said. …

For the remainder of the report:

end

How a ban on Russia’s mining giants could shake the metals world

Submitted by admin on Sat, 2022-10-08 10:36Section: Daily Dispatches

By Jack Farchy

Bloomberg News

Saturday, October 8, 2022

A possible ban on Russian supplies by the London Metal Exchange would be a seismic event for the metals industry, cutting some of the world’s biggest companies off from the main global marketplace.

The exchange has yet to make a decision, but on Thursday launched a formal three-week discussion process on the possibility of banning Russian metal, potentially as soon as next month.

In practice, a ban would simply mean that metal from Russia — which accounts for about 9% of global nickel production, 5% of aluminum and 4% of copper — could no longer be delivered into any warehouses around the world in the LME network, which store metal used to deliver against futures contracts when they expire.

But the debate, and potential fallout, provide a stark case study of how deeply the LME is intertwined with all corners of the physical metals industry. Despite being a private company owned by Hong Kong Exchanges & Clearing Ltd., the exchange’s decisions have far-reaching consequences for the way in which metal is priced and traded globally. …

… For the remainder of the report:

4. OTHER PHYSICAL SILVER/GOLD

Another Ponzi scheme

special thanks to John Adams for providing this for us:

Release Number 8606-22

CFTC Charges Delaware Precious Metals Dealer, Depository, and Their Owner with Ongoing Fraud

October 05, 2022

Washington, D.C. — The Commodity Futures Trading Commission today announced that it filed a civil enforcement action in the U.S. District Court for the District of Delaware against a precious metals dealer, Argent Asset Group LLC (Argent), and a precious metals depository, First State Depository Company, LLC (FSD), both of Wilmington, Delaware, and their owner, Robert Leroy Higgins (Higgins) of West Chester, Pennsylvania, charging them with fraud in connection with a multimillion-dollar precious metals scheme.

On September 29, U.S. District Court Judge Richard Andrews signed an ex parte statutory restraining order freezing assets controlled by the defendants, preserving records, and appointing a temporary receiver. A status hearing is scheduled for October 11.

In continuing litigation against the defendants, the CFTC seeks restitution, disgorgement, civil monetary penalties, permanent trading and registration bans, and a permanent injunction against further violations of the Commodity Exchange Act (CEA) and CFTC regulations, as charged.

“As this enforcement action shows, the CFTC will vigorously investigate and seek to hold accountable those who make false promises and misappropriate customer funds,” said Acting Director of Enforcement Gretchen Lowe.

Case Background

The complaint alleges that from approximately January 2014 through the present, Argent and FSD, acting as a common enterprise controlled by Higgins, engaged in a fraudulent and deceptive scheme to solicit and misappropriate at least $7 million in funds and silver from at least 200 customers in connection with a fraudulent silver leasing program referred to as the “Maximus Program.” The complaint further alleges Higgins either directly engaged in deceptive conduct in furtherance of the scheme or did so indirectly by virtue of his being the control person of Argent and FSD.

As alleged in the complaint, the Maximus Program purported to offer customers guaranteed monthly lease payments in exchange for the use of silver purportedly purchased from Argent or silver owned by customers. Customers were told they would earn a monthly “lease” payment based on a sliding scale that in part depended on the amount of silver the Maximus customers leased to Argent. Customers were falsely told, among other things, that Argent would acquire silver on their behalf, their silver was securely stored by FSD in a storage facility, and their investments were guaranteed and fully insured.

In reality, as alleged in the complaint, customers’ precious metals were not securely stored at FSD, but instead were misappropriated by the defendants. Moreover, on several occasions, the defendants also misappropriated funds intended to be used to purchase metals.

As alleged in the complaint, the defendants’ fraudulent scheme was not limited to the Maximus Program. The defendants misappropriated other client assets and misled and deceived those clients when they attempted to withdraw their assets or transfer them to another depository. In addition, the defendants lied about the insurance coverage FSD maintained and failed to adequately insure its clients’ assets despite representations and guarantees it made to the contrary.

The CFTC acknowledges and thanks the Financial Conduct Authority in the United Kingdom for their assistance in this matter.

The Division of Enforcement staff members responsible for this action are Erica Bodin, Michael Loconte, Brian A. Hunt, Michael Solinsky, and Rick Glaser.

CFTC’s Precious Metals Customer Fraud Advisory

The CFTC has issued several customer protection Fraud Advisories and Articles that provide the warning signs of fraud, including the Precious Metals Fraud Advisory, which alerts customers to precious metals fraud and lists simple ways to spot precious metals scams.

The CFTC also strongly urges the public to verify a company’s registration with the CFTC before committing funds. If unregistered, a customer should be wary of providing funds to that entity. A company’s registration status can be found at NFA BASIC.

Customers and other individuals can report suspicious activities or information, such as possible violations of commodity trading laws, to the Division of Enforcement via a toll-free hotline 866-FON-CFTC (866-366-2382), file a tip or complaint online, or contact the Whistleblower Office. Whistleblowers are eligible to receive between 10 and 30 percent of the monetary sanctions collected paid from the Customer Protection Fund financed through monetary sanctions paid to the CFTC by violators of the CEA.

-CFTC

5.OTHER COMMODITIES:

end

COMMODITIES IN GENERAL/

END

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings MONDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.1474

OFFSHORE YUAN: 7.1514

SHANGHAI CLOSED DOWN 50.24 PTS OR 1.66%

HANG SENG CLOSED DOWN 523.39 OR 2.85%

2. Nikkei closed DOWN 195.19 PTS OR 0.71%

3. Europe stocks SO FAR: MOSTLY RED

USA dollar INDEX UP TO 113.55/Euro FALLS TO 0.96960

3b Japan 10 YR bond yield: RISES TO. +.244/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 145.53/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.205%***/Italian 10 Yr bond yield RISES to 4.73%*** /SPAIN 10 YR BOND YIELD RISES TO 3.42%…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.882//

3j Gold at $1676/35//silver at: 19.80 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND71/100 roubles/dollar; ROUBLE AT 62.63//

3m oil into the 91 dollar handle for WTI and 97 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 145.53DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9987– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9682well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.888 UP 1 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.848 UP 1 BASIS PTS//(USA 30 YR INVERTED TO THE USA 10)

USA DOLLAR VS TURKISH LIRA: 18,58…GETTTING DANGEROUS

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

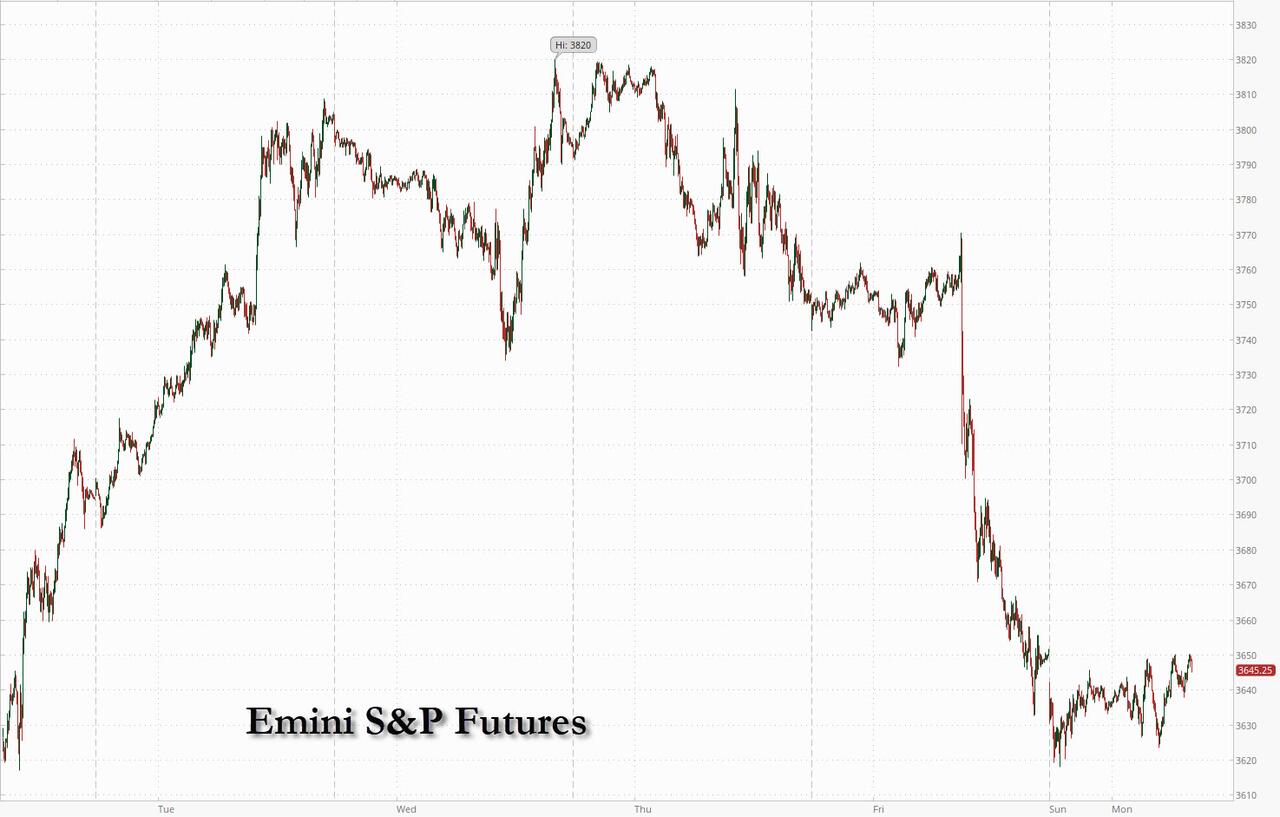

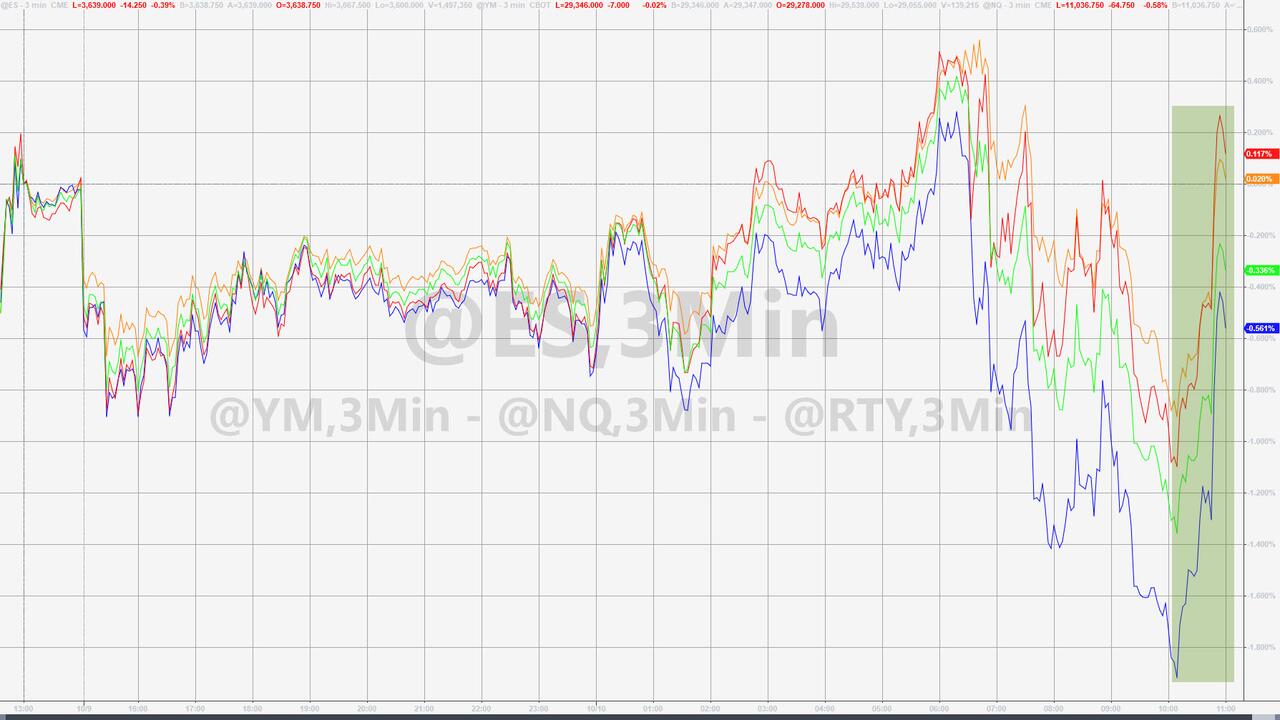

Futures Slide, Global Chip Stocks Tumble On Hard-Landing Fears, Latest China Tech Curbs

MONDAY, OCT 10, 2022 – 08:06 AM

US equity futures extended last week’s post-payrolls slump, and as of 730am ET traded -0.2% at 3,646, having bounced off the session’s worst levels down as much as -1%, while European stocks fell for the fourth straight day as concerns mounted that central bank policy-tightening would send the global economy into a hard landing (as Michael Hartnett warned) taking a heavy toll on the global economy and company earnings. The dollar extended its gains while bonds were closed for trading on the Columbus Day bond market holiday; cryptos were flat.

The semiconductor sector saw an across-the-board hit from Washington’s decision to further restrict exports of cutting-edge chips and chipmaking tools to China, adding to the headaches for an industry already hit by a slump in demand. Europe-listed Infineon, STMicro and OSRAM dropped, while in premarket New York trade, chipmakers Nvidia and Advanced Micro Devices shed more than 1% each. Hong Kong Hang Seng Tech index plunged as much as 4.1% after fresh US tech curbs send Chinese semiconductor stocks tumbling. Mainland shares fall after a week-long break as Caixin services PMI returns to contraction territory and reports show sharp slide in holiday spending.

In premarket trading, Ford shares dropped 3.9% after a downgrade to sell at UBS due to weak profit margins. Meanwhile, General Motors (GM US) falls 3% after being cut to neutral from buy, with UBS seeing “demand destruction” for its EV segment after a strong start. Kraft shares rose 1.4% in premarket trading, as Goldman upgrades the stock to buy and downgrades home/personal care “bellwether” P&G to neutral, adding more food exposure within US consumer staples coverage. Here are other notable premarket movers:

- Rivian (RIVN US) falls as much as 7.6% in premarket trading after the EV maker said it will recall about 13,000 vehicles it delivered to customers after discovering a minor structural defect.

- Grab Holdings (GRAB US) falls as much as 2.9% in US premarket trading after Barclays initiates coverage of the ride-sharing and delivery provider at equal-weight, questioning whether the business can continue to thrive as lower income levels and saying car ownership in Southeast Asia may have implications for longer-term profitability.

- US-listed Chinese stocks drop in premarket trading, with sentiment hurt by weak holiday spending data during the Golden Week and new Covid flareups across the country one week before the key Communist Party congress.

- Alibaba (BABA US) -1.6%, Baidu (BIDU US) -1.5%, Pinduoduo (PDD US) -2.1%, JD.com (JD US) -1.9%, Bilibili (BILI US) -5.6%

- US-listed Macau casino operators drop in New York premarket trading after Citigroup cut its estimate of Macau’s gross gaming revenue in October to 5.5 billion patacas from 7 billion patacas, citing disappointing revenue during the first nine days of this month.

- Las Vegas Sands (LVS US) shares -3.1%, Melco Resorts (MLCO US) -1.7%, Wynn Resorts (WYNN US) -2.2%, MGM Resorts (MGM US) -1.2%

- Keep an eye on Meta (META US) and Alphabet (GOOGL US), as Morgan Stanley trimmed its price targets on the stocks citing low visibility for the digital ads market. Even so, the brokerage expects October to be strong for the sector, given continued efforts to pull forward consumer holiday demand.

While the bond market is closed on Monday for the Columbus Day holiday and there is no macro on deck Monday, an action-packed week lies ahead, with inflation data due Thursday and the third-quarter earnings season kicking off in earnest. Hotter-than-expected CPI growth would heap pressure on policy makers to extend 75 basis-point rate hikes beyond this year. Minutes of the latest Fed policy meeting on Wednesday may provide insight into where the pain threshold lies for Fed officials, who are so far resolutely hawkish in their message that neither financial-market volatility nor the threat of an economic downturn will deter them from raising rates. Investors are also bracing for disappointment from the coming earnings season, with more than 60% of the 724 respondents to Bloomberg’s latest Pulse poll predicting the season would push the S&P 500 Index lower.

The poll underscored Wall Street’s fear that even after this year’s brutal selloff, stocks have not priced all the risks stemming from central banks’ aggressive tightening and stubbornly high inflation. Over the weekend, Goldman’s David Kostin warned that the soaring dollar could hammer corporate earnings. While JPMorgan, Citigroup and other big banks report this week, iPhone maker Apple is in particular focus as its report is expected to offer insight into themes ranging from global consumer demand to the impact of dollar strength.

“The narrative will start changing from central banks and inflation, to one of weaker growth and downward earnings revisions that is going to weigh on risk sentiment over coming weeks,” Jefferies strategist Mohit Kumar wrote in a note.

Doubling down on his relentless pessimism, Morgan Stanley’s Mike Wilson warned that the bear market in US stocks won’t be over until earnings forecasts are cut further or share valuations better reflect the risks.

European stocks declined for the 4th day in a row; the Euro Stoxx 50 dropped 0.8%. DAX outperforms peers, dropping 0.2%, CAC 40 lags, retreating 0.9%. Consumer products, tech and utilities are the worst-performing sectors. Here are the biggest European movers:

- Renault shares jump as much as 6.8% as analysts highlight press reports saying the French carmaker and Japanese partner Nissan are in talks to reshape their two decade-old alliance.

- DS Smith jumps as much as 12% after its trading update noted strong revenue growth and “effective cost mitigation,” which analysts said is set to trigger consensus upgrades to FY23 Ebita. Its paper-packaging peers Mondi and Smurfit Kappa also advanced.

- Unite Group’s shares rose as much as 4.2% after a trading update that Peel Hunt said shows robust demand, with a return of students en masse driving full occupancy and an uplift to 2023/24 rental growth guidance.

- Deutsche Bank shares rise as much as 3.4%, the most in the Stoxx 600 Bank Index, after Kepler Cheuvreux says it expects 3Q earnings to beat consensus.

- Credit Suisse shares gained as much as 3.7% after Bloomberg News reported that its SPG unit has drawn interest from bidders including Pimco and Centerbridge.

- ASML shares drop 3.2% as European semiconductor stocks continue to slide on Monday, after the US announcement of more restrictions on exports of cutting- edge chips and chipmaking tools to China added to the headaches for an industry already hit by a slump in demand.

- Stocks including SSE, Drax and Centrica post the biggest declines in the utilities sub-sector after the Financial Times reported the UK government is pushing ahead with plans to cap renewable electricity revenues with legislation that could be unveiled next week. Drax drop as much as -6.5%

- Casino shares slumped as much as 13% to a fresh all-time low after S&P lowered its credit rating on the French grocer, saying the company faces added pressure on its ability to refinance its debts because of the tougher retail environment in France.

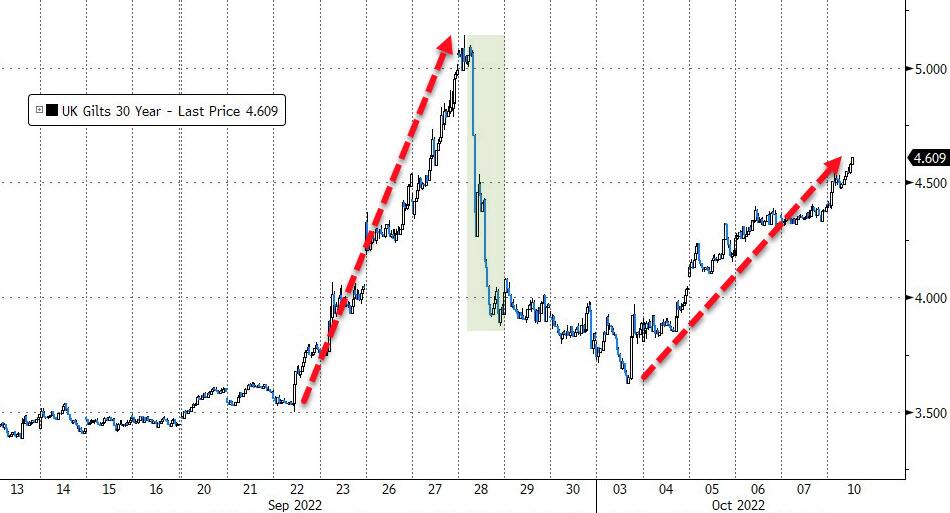

In Britain, the Bank of England stepped up its measures to support market functioning as its emergency gilt buying measures entered their final week. The UK central bank said it will increase the size of its buying operations for the next five days to a maximum of £10 billion ($10.8 billion), from £5 billion previously. However, UK long-dated bonds shrugged off the news, with 10-year yields rising 6 basis points.

Focus is also training on Italy where the yield premium demanded by investors to hold Italian debt compared to Germany has surged to the highest since 2020, after ratings agency Moody’s warned of the need to keep national debt on a sustainable path.

Earlier in the session, equities across Asia declined Monday as strong US jobs data quelled hopes for a less hawkish Fed, while China traders returning from holiday added to the selling pressure. The MSCI Asia Pacific Index declined as much as 1.4%, falling to its lowest in a week. Consumer discretionary and financials were the biggest drag. China’s CSI 300 closed at its lowest since April 2020 as bleak consumption data and lockdown fears gripped traders as markets reopened after a week-long break. Benchmarks in Hong Kong and the Philippines were among the worst decliners in the region after the US unemployment rate unexpectedly returned to a historic low, bolstering the case for another 75 basis point hike by the Fed. Japan, South Korea, Malaysia and Taiwan markets were closed for a holiday. The data and comments from Fed officials recently are “throwing cold water on the idea of a Fed pivot,” Nomura strategists including Chetan Seth wrote in a note.

While a much-softer-than-expected US CPI reading this week may lead to a stock rally, “it will likely not last as the market — and the Fed — will want to see a series of low monthly inflation readings before expecting a definite pause,” they added. US consumer inflation data will be released Thursday, helping set the tone for the Fed’s decision early next month. Traders are also turning their attention to the latest earnings season and China’s Covid restrictions ahead of the much-awaited party congress in mid October

Australian stocks tumbled the most in two weeks as the S&P/ASX 200 index fell 1.4% to 6,667.80 after strong US jobs data bolstered bets for more aggressive Fed hikes. The Australian benchmark dropped the most since Sept. 26 as all sectors retreated. Banks and miners contributed the most to the gauge’s decline. In New Zealand, the S&P/NZX 50 index fell 1.7% to 10,918.48.

Stocks in India extended their decline to a second day as investors booked profits in some of the recent sectoral outperformers, including consumer goods firms. Software makers were the top performers ahead of the start of the sector’s quarterly results season. The S&P BSE Sensex fell 0.3% to 57,991.11, its biggest single-day drop since Oct. 3. The NSE Nifty 50 Index ended 0.4% lower after paring a plunge of as much as 1.4%. All but two of 19 sectoral indexes compiled by BSE Ltd. declined, led by consumer durables makers. Tata Consultancy Services will kick-start the earnings season for the September quarter later on Monday. The software exporter’s shares advanced 1.8%. Reliance Industries contributed the most to the Sensex’s decline, decreasing 1.1%. Out of 30 shares in the index, 11 rose, while 19 fell.

In FX, the Bloomberg Dollar Spot Index rose as the greenback advanced versus all of its Group-of-10 peers.

- The euro dropped below 0.97 per dollar. The BOE said it will increase the size of its buying operations for the next five days to a maximum of £10 billion from £5 billion previously. Officials will also launch a Temporary Expanded Collateral Repo Facility.

- The pound fell against a broadly stronger dollar, edging lower to trade around 1.10 against the dollar, but rallied against the euro. The BOE said it will increase the size of its buying operations for the next five days to a maximum of £10 billion from £5 billion previously. Officials will also launch a Temporary Expanded Collateral Repo Facility

- The yen traded below 145 per dollar. One-week implied volatility in the dollar-yen has fallen to trade well below highs seen last month, even as the currency pair closes on 145.90 — a level that triggered a near $20 billion intervention from Japan’s Ministry of Finance. The Japanese currency has fallen for eight weeks in a row, its longest-losing streak since May

- The Aussie slid to the weakest level in more than two years after stronger-than-expected US payroll numbers on Friday boosted expectations for Federal Reserve interest-rate hikes

In rates, treasury futures drifted lower led by ultra-long contracts following a wider steepening move across the UK gilt curve with cash bond trading closed for Columbus Day in the US. Futures are lower by up to 23 ticks in the ultra-long bond contracts which lead losses on the session; 10-year note futures are lower by 3 ticks trading around 111-12 and inside Friday session range. UK gilts are cheaper by up to 16.5bp across 30-year sector, while UK long-end real yields surge ahead of Tuesday’s 2051 linker sale. US auctions resume Tuesday with 3-year note sale, followed by 10- and 30-year auctions Wednesday and Thursday. UK bonds also declined, led by long-end; 30-year yield rises above 4.5%. Bunds 10-year yield rises ~3bps to 2.16%. UK bonds fell even after the Bank of England stepped up measures to support market functioning as its emergency gilt buying measures entered their final week.

In commodities, WTI and Brent front-month futures are modestly softer after settling higher by over USD 4.00/bbl and USD 3.50/bbl respectively on Friday. WTI dipped below $92, down 0.7% after last week’s 17% gain, while Brent traded just around $97. French petrol station woes reportedly deepened as strikes continued and the French Energy Ministry stated that 29.7% of service stations were experiencing supply difficulties with at least one fuel product as of 3pm on Sunday vs 21% of service stations on Saturday. Furthermore, TotalEnergies (TTE FP) called on the responsibility of workers to ensure that the country is well supplied with fuel and proposed to bring forward the compulsory annual negotiations to October subject to the end of blockades, according to Reuters. Spot gold fell roughly $14 to trade near $1,681/oz; it traded lower in tandem with strength in the DXY, with the yellow metal’s 21 DMA around 1,678/oz. Base metals are mixed but LME copper and Chinese iron ore futures buck the trend.

Bitcoin is on a softer footing and remains under the USD 19,500 mark whilst Ethereum holds onto 1,300 status.

There is nothing on today’s US economic calendar; Fed speakers include Evans and Brainard.

Market Snapshot

- S&P 500 futures down 0.8% to 3,625.50

- STOXX Europe 600 down 0.8% to 388.37

- MXAP down 1.4% to 140.77

- MXAPJ down 1.9% to 454.16

- Nikkei down 0.7% to 27,116.11

- Topix down 0.8% to 1,906.80

- Hang Seng Index down 3.0% to 17,216.66

- Shanghai Composite down 1.7% to 2,974.15

- Sensex down 0.8% to 57,712.89

- Australia S&P/ASX 200 down 1.4% to 6,667.75

- Kospi down 0.2% to 2,232.84

- German 10Y yield little changed at 2.18%

- Euro down 0.6% to $0.9688

- Brent Futures down 0.8% to $97.11/bbl

- Gold spot down 0.9% to $1,680.29

- U.S. Dollar Index up 0.42% to 113.27

Top Overnight News from Bloomberg

- The Biden administration’s new restrictions on technology exports to China could undercut the country’s ability to develop wide swaths of its economy, from semiconductors and supercomputers to surveillance systems and advanced weapons

- Missiles struck Kyiv and other Ukrainian cities early Monday, two days after an attack on a key bridge to Crimea that Russian President Vladimir Putin blamed on Ukraine

- Norway’s inflation hit a new 34-year high last month, in a development that may boost expectations of another half-point hike by Norges Bank in November. Headline inflation accelerated to 6.9% in September, above the median projection of 6.2% in Bloomberg analyst poll, and the central bank’s forecast of 6%

- The Danish island of Bornholm, located in the Baltic Sea near the Nord Stream pipelines, was been hit by a complete power failure on Monday, broadcaster DR reported, citing the local energy company

- Malaysian Prime Minister Ismail Sabri Yaakob announced the dissolution of parliament on Monday, paving the way for elections this year as his ruling party seeks to strengthen its position following a run of successful local polls

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks were negative in a holiday-thinned start to the week with market closures in Japan, South Korea and Taiwan, while the region digested a contraction in Chinese Caixin PMI data and the recent stronger-than-expected US jobs data which paves the way for the Fed to continue with its hawkish normalisation. ASX 200 was led lower by gold miners and tech stocks after the post-NFP rise in yields and with risk appetite also not helped by a deterioration in the AIG Services Index. Hang Seng and Shanghai Comp. weakened with Hong Kong pressured by notable losses in the tech sector after the US recently announced new curbs on exports to China on certain tools essential for high-end chip production. Furthermore, sentiment was also dampened following the PBoC’s largest weekly net drain in eight months and after Chinese Caixin Services and Composite PMIs fell into contraction territory, although losses in the mainland are somewhat cushioned following the return of participants from a week-long holiday.

Top Asian News

- PBoC injected CNY 17bln via 7-day reverse repos for CNY 594bln net daily drain on Saturday and injected CNY 2bln through 7-day reverse repos with the rate kept at 2.00% on Sunday which resulted in the largest net weekly drain in eight months. PBoC also injected CNY 2bln via 7-day reverse repos with the rate kept at 2.00% on Monday, according to Reuters.

- PBoC noted that it issued CNY 400bln via MLF during September and outstanding MLF loans fell to CNY 4.55tln at end-September vs. CNY 4.75tln at end-August, while it issued a total of CNY 969mln via SLF in September and its outstanding PSL was at CNY 2.65tln at end-September vs CNY 2.54tln at end-August, according to Reuters.

- PBoC survey found that 53% of bankers believe Q3 monetary policy is appropriate and 45.8% believe Q3 monetary policy is loose, according to Reuters.

- China was placed on high alert amid increases in COVID cases ahead of the Communist Party Congress, according to FT.

- Chinese Foreign Ministry said the US is abusing trade measures to maintain technological hegemony following the recent announcement of controls targeting Chinese chip manufacturers, according to Reuters.

- China’s Shanghai requires arrivals to take three COVID tests within three days, according to Bloomberg.

European bourses have kicked the week off on the backfoot as the negativity from last Friday has continued into this week. Sectors in Europe are predominantly softer with the exception of Retail and Telecoms. To the downside, Consumer Products, Tech and Utilities lag. Stateside, futures are softer across the board but to a lesser extent than European peers.

Top European News

- UK Cabinet Office Minister Zahawi said it is extremely unlikely that Britain will have planned power cuts over the winter, according to Reuters.

- UK PM Truss is prepared to listen to Conservative critics who oppose proposals to raise benefits by less than inflation, according to Telegraph sources.

- Retailers in London’s West End warned that the capital faces a consumer growth slowdown with footfall in London’s main shopping area remaining about a fifth lower than pre-pandemic levels, according to research by New West End Company cited by FT.

FX

- DXY extends on Friday’s gains with the index back above the 113.00 mark with a current intraday peak of 113.31, with G10s softer vs the USD to varying degrees.

- EUR/USD tested 0.9700 to the downside from a high just over 0.9750 and retreated further from decent option expiry interest spanning 0.9800-55 (around EUR 2.8bln).

- AUD sits as the current laggard with China’s sub-50 PMIs overnight adding to the pressure, whilst USD/CNH topped 7.1500.

- PBoC set USD/CNY mid-point at 7.0992 vs exp. 7.1215 (prev. 7.0998).

- Turkish President Erdogan said the CBRT will keep cutting rates every month for as long as he is in power, according to Reuters.

Fixed Income

- Bunds and US Treasuries are off best levels amidst hawkish ECB rhetoric and an upturn in overall risk sentiment that has perked up hitherto weak Italian bonds.

- Gilts are still deeply underwater with the BoE remaining on course to end its temporary buy-back auctions at the end of the week and is switching to liquidity support via expanded collateral repos.

Commodities

- WTI and Brent front-month futures are modestly softer after settling higher by over USD 4.00/bbl and USD 3.50/bbl respectively on Friday.

- French petrol station woes reportedly deepened as strikes continued and the French Energy Ministry stated that 29.7% of service stations were experiencing supply difficulties with at least one fuel product as of 3pm on Sunday vs 21% of service stations on Saturday. Furthermore, TotalEnergies (TTE FP) called on the responsibility of workers to ensure that the country is well supplied with fuel and proposed to bring forward the compulsory annual negotiations to October subject to the end of blockades, according to Reuters.

- Spot gold has been ebbing lower in tandem with strength in the DXY, with the yellow metal’s 21 DMA around 1,678/oz.

- Base metals are mixed but LME copper and Chinese iron ore futures buck the trend.

- Kumba Iron Ore declared a force majeure due to strike action; export sales will be impacted by around 120k tonnes per day.

Geopolitics: Russia/Ukraine

- Ukrainian media reported a large explosion at the Kerch bridge in Crimea where a fuel tank was on fire at one of the sections of the bridge, while there were comments from a Ukrainian presidential adviser who called the bridge explosion ‘the beginning’ and said ‘everything illegal must be destroyed’ but did not directly claim responsibility, according to Reuters.