by harveyorgan · in Uncategorized · Leave a comment·Edit

by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSE: UP $10.30 to $1678.50

SILVER PRICE CLOSE: DOWN $0.11 to $19.40

Access prices: closes

Gold ACCESS CLOSE 1666.70

Silver ACCESS CLOSE: 19.17

New: early yesterday morning//

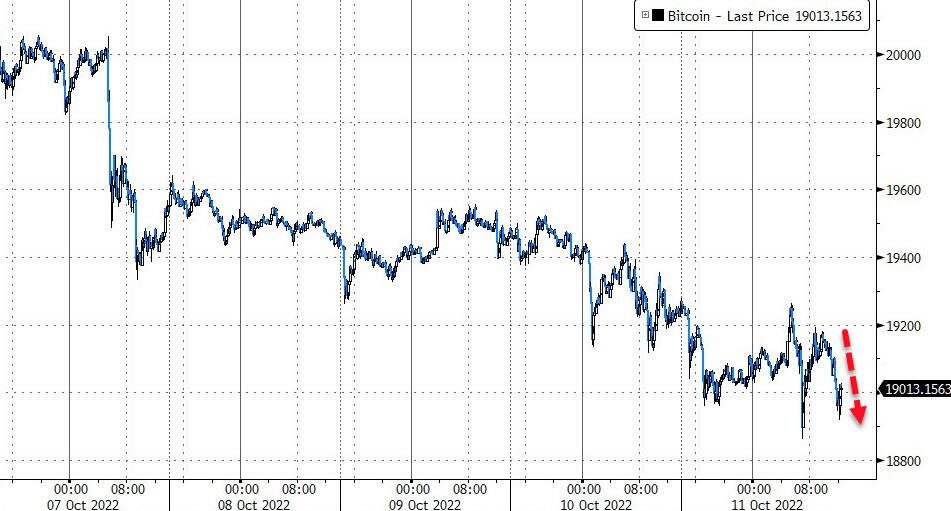

Bitcoin morning price: $19,093 DOWN 171

Bitcoin: afternoon price: $18,995 DOWN 269

Platinum price closing UP 4.65 AT $904.30

Palladium price; closing DOWN 0 at $2156.25

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/closing ACCESS

CANADIAN GOLD $2299.95 CDN DOLLARS PER OZ DOWN $0.30 CDN DOLLARS

BRITISH GOLD IN POUNDS: 1519.20 POUNDS PER OZ UP 11.87 BRITISH POUNDS PER OZ/

EURO GOLD: 1717.50 EUROS PER OZ// DOWN 2 EUROS PER OZ///

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: OCTOBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,667.300000000 USD

INTENT DATE: 10/10/2022 DELIVERY DATE: 10/12/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 1

323 C HSBC 17

435 H SCOTIA CAPITAL 9

657 C MORGAN STANLEY 2

661 C JP MORGAN 8

800 C MAREX SPEC 17 2

TOTAL: 28 28

MONTH TO DATE: 21,547

JPMORGAN STOPPED 8/28

GOLD: NUMBER OF NOTICES FILED FOR OCT CONTRACT: 28 NOTICES FOR 2800 OZ //.08709 TONNES

total notices so far: 21,547 contracts for 2,154,700 oz (67.020 tonnes)

SILVER NOTICES: 38 NOTICES FILED FOR 190,000 OZ/

total number of notices filed so far this month 359 : for 1,795,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP 10.30

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD: /////

INVENTORY RESTS AT 944.31 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 11 CENTS

AT THE SLV// :/BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A HUGE DEPOSIT OF 5.066 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 478.196 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A FAIR SIZED 461 CONTRACTS TO 125,743 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE FAIR LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR HUGE $0.65 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS/HFT WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.65).SPECS CONTINUE TO ADD TO THE SHORTFALLS. OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS.

WE MUST HAVE HAD:

I) MINIMAL SPECULATOR SHORT COVERINGS ////CONTINUED BANKER OI COMEX ADDITIONS /// SOME NEWBIE SPEC SHORT ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.580 MILLION OZ FOLLOWING A 185,000 OZ QUEUE JUMP / // V) FAIR SIZED COMEX OI LOSS/ MINIMAL SPEC COVERING THEIR SHORTS.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: +69

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT:

TOTAL CONTRACTS for 9 days, total 50,050 contracts: 25.025 million oz OR 2.777MILLION OZ PER DAY. (556 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 25.025 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 25.025 MILLION OZ INITIAL

RESULT: WE HAD A FAIR SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 461 WITH OUR HUGE $0.65 LOSS IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 275 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /SOME BANKER ADDITIONS // SOME SHORT ADDITIONS//SMALL NEWBIE SPEC LONG ADDITIONS// /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT. OF 1.580 MILLION OZ FOLLOWED BY TODAY’S 185,000 QUEUE JUMP .. WE HAD A SMALL SIZED LOSS OF 186 OI CONTRACTS ON THE TWO EXCHANGES FOR 0.930 MILLION OZ..

WE HAD 38 NOTICE(S) FILED TODAY FOR 190,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 173 CONTRACTS TO 435,083 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED — -57 CONTRACTS.

.

THE FAIR SIZED INCREASE IN COMEX OI CAME DESPITE OUR HUGE LOSS IN PRICE OF $33.80//COMEX GOLD TRADING/MONDAY // SOME SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT. AT 66.099 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 10,400 OZ//NEW STANDING 68.679 TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED DESPITE OUR LOSS IN PRICE OF $33.80 WITH RESPECT TO MONDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 3976 OI CONTRACTS 12.367 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2203 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 435,026

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3976 CONTRACTS WITH 1773 CONTRACTS INCREASED AT THE COMEX AND 2203 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3976 CONTRACTS OR 12.367 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2203) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (1773): TOTAL GAIN IN THE TWO EXCHANGES 3976 CONTRACTS. WE NO DOUBT HAD 1) MINOR SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS///NEWBIE SPEC SHORT ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 66.099 TONNES FOLLOWED BY TODAY’S 10,400 OZ QUEUE JUMP///NEW STANDING 68.702 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) FAIR SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT. :

18,788 CONTRACTS OR 1,878,800 OZ OR 58.43 TONNES 9TRADING DAY(S) AND THUS AVERAGING: 2087 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES: 58.43 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 58.43/3550 x 100% TONNES 1.63% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 58.43 TONNES INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A FAIR SIZED 461 CONTRACT OI TO 125,748 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 275 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 275 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 461 CONTRACTS AND ADD TO THE 275 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED LOSS OF 186 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 0.930 MILLION OZ

OCCURRED DESPITE OUR HUGE LOSS IN PRICE OF $0.65

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 5.65 PTS OR 0.19% //Hang Seng CLOSED DOWN 384.30 OR 2.23% /The Nikkei closed DOWN 714.86PTS OR 2.64% //Australia’s all ordinaires CLOSED DOWN 0.40% /Chinese yuan (ONSHORE) closed DOWN TO 7.1661 //OFFSHORE CHINESE YUAN DOWN 7.1662// /Oil DOWN TO 89.35 dollars per barrel for WTI and BRENT AT 94.34 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1773 CONTRACTS TO 435,026 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS FAIR COMEX INCREASE OCCURRED WITH DESPITE OUR STRONG FALL IN PRICE OF $33.80 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2203 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2203 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :2203 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2203 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 3976 CONTRACTS IN THAT 2203 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 1830 CONTRACTS..AND THIS GOOD GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR HUGE FALL IN PRICE OF GOLD $33.80//WE HAD SPEC SHORTS ADDING TO THEIR POSITIONS WITH BANKERS TAKING THE OTHER SIDE AS BUYERS OF COMEX GOLD CONTRACTS. WE ALSO HAD ADDITIONAL SPECS GOING LONG DUE TO THE ATTRACTIVE PRICE

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING OCT (68.706),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 68.706 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $33.80) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS (THEY ADDED TO THEIR POSITIONS) AS WE HAD A GOOD SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 4033 CONTRACTS // WE HAVE REGISTERED A FAIR GAIN OF 12.367 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR OCT. (68.706 TONNES)…THIS WAS ACCOMPLISHED WITH A HUGE FALL IN PRICE OF $33.80

WE HAD -57 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 4033 CONTRACTS OR 403,300 OZ OR 12.544 TONNES

Estimated gold volume 156,972// poor//

final gold volumes/yesterday 166,494/ poor

INITIAL STANDINGS FOR OCT ’22 COMEX GOLD //OCT 11

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 199,336.173oz JPMorgan includes 6200 kilobars |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 590.00 oz Delaware |

| No of oz served (contracts) today | 28 notice(s) 2800 OZ 0.08709 TONNES |

| No of oz to be served (notices) | 541 contracts 54,100oz 1.6827 TONNES |

| Total monthly oz gold served (contracts) so far this month | 21,547 notices 2,154,700 67.020 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

Into Delaware: 590.000 oz

total deposits 590.000 oz

customer withdrawals: 1

iii) Out of JPMorgan: 199,336.173oz (6200 kilobars)

total: 199,336.173 oz

total in tonnes: 6.2 tonnes

Adjustments: 1// dealer to customer

Brinks:144,679.494 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT we have an oi of 570 contracts having LOST 31 contracts . We had 144 contracts

filed on MONDAY, so we gained 113 contracts or an additional 11,300 oz will stand in this active delivery month of Oct.

We will gain gold oz standing on each and every trading day from this day forth until the conclusion of October.

(remember that queue jumping is really EFP’s exercised from London for gold underwritten by COMEX based bankers)

November GAINED 9 contracts to stand at 2968

December lost 2023 contracts down to 368,700

We had 28 notice(s) filed today for 2800 oz FOR THE OCT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 28 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 8 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT /2022. contract month,

we take the total number of notices filed so far for the month (21,547) x 100 oz , to which we add the difference between the open interest for the front month of (OCT 570 CONTRACTS) minus the number of notices served upon today 28 x 100 oz per contract equals 2,208,000 OZ OR 68.678 TONNES the number of TONNES standing in this active month of OCT. (TOTALS CORRECTED FROM FRIDAY)

thus the INITIAL standings for gold for the OCT contract month:

No of notices filed so far (21,547) x 100 oz+ (570) OI for the front month minus the number of notices served upon today (28} x 100 oz} which equals 2,208,900, oz standing OR 68.706 TONNES in this NON active delivery month of OCTOBER.

TOTAL COMEX GOLD STANDING: 68.706 TONNES (A HUMONGOUS STANDING FOR OCT (GENERALLY THE POOREST DELIVERY MONTHS FOR AN ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,067,434 OZ (REG GOLD- PLEDGED GOLD) 340.166 tonnes//rapidly declining

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 23,926,265.692 OZ

TOTAL REGISTERED GOLD: 12,319,480.319 OZ (383.18tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 13,606,785.373 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,252,046OZ (REG GOLD- PLEDGED GOLD) 318.88 tonnes//rapidly declining

END

SILVER/COMEX

OCT 11//INITIAL OCT SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,654,666.794oz Brinks JPM Loomis Manfra Delaware CNT |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 427,300.587 oz Delaware |

| No of oz served today (contracts) | 38 CONTRACT(S) 190,000 OZ) |

| No of oz to be served (notices) | 40 contracts (200,000 oz) |

| Total monthly oz silver served (contracts) | 359 contracts 1,795,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) into Delaware: 427,300.587 oz

Total deposits: 427,300.587 oz

JPMorgan has a total silver weight: 160.801million oz/310/725million =51.81% of comex

Comex withdrawals: 6

i)Out of CNT 1943.944 oz

ii) Out of Brinks 451,327.200 oz

iii) Out of JPMorgan: 4965.800 oz

iv) Out of Delaware 1003.100 oz

v) Out of Loomis 599,360.140 oz

vi_ Out of Manfra: 596,066.610 oz

total withdrawals: 1,654,666.794 oz

adjustments: // 1

Brinks: dealer to customer: 23,950.930 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 40.106 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 310.725 MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF OCT OI: 78 CONTRACTS HAVING GAINED 1 CONTRACT(S.)

WE HAD 38 NOTICES FILED ON MONDAY SO WE GAINED 39

SILVER CONTRACTS OR AN ADDITIONAL 195,000 OZ WILL STAND FOR OCT.

NOVEMBER LOST 1 CONTRACT TO STAND AT 400

DECEMBER SAW A LOSS OF 1141 CONTRACTS DOWN TO 104,170

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 38 for 190,000 oz

Comex volumes:55,855// est. volume today// fair

Comex volume: confirmed yesterday: 63,623 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 397 x 5,000 oz = 1,985,000 oz

to which we add the difference between the open interest for the front month of OCT(78) and the number of notices served upon today 38 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT./2022 contract month: 397 (notices served so far) x 5000 oz + OI for front month of OCT (78) – number of notices served upon today (38) x 5000 oz of silver standing for the OCT contract month equates 1,985,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:61,618// est. volume today// poor

Comex volume: confirmed yesterday: 54,383contracts ( poor)

END

GLD AND SLV INVENTORY LEVELS

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

GLD INVENTORY: 944.31 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

CLOSING INVENTORY 478.196 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

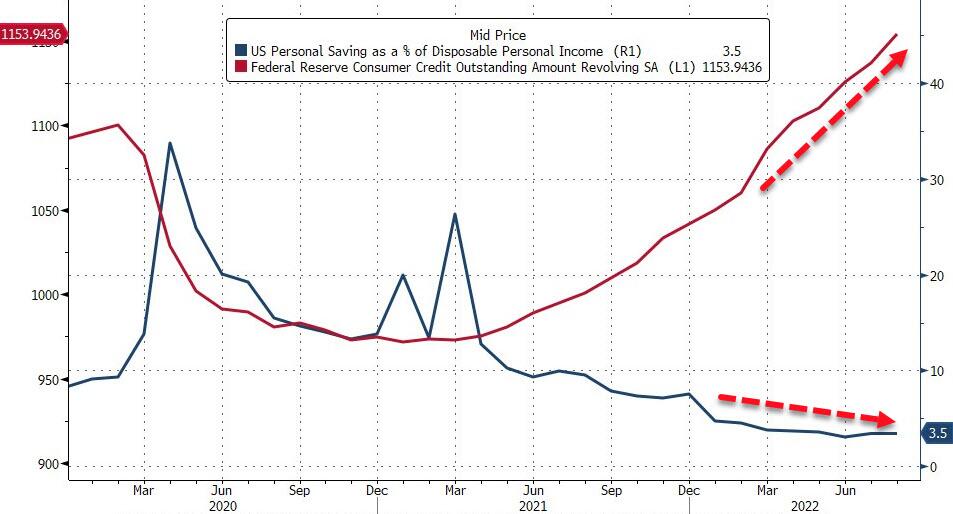

Americans Continue To Pay For Inflation With Credit Cards

TUESDAY, OCT 11, 2022 – 11:05 AM

Authored by Michael Maharrey via SchiffGold.com,

Credit card debt continues to spiral higher as consumers struggle with rising prices and depleted savings.

In August, revolving credit increased by a staggering 18.1% as total consumer debt surged to a record $4.68 trillion, according to the latest consumer credit data from the Federal Reserve.

Total consumer debt increased by $32.2 billion in August, an 8.3% increase on an annual basis. That was well above the $24 billion projection.

In July, it appeared debt growth was cooling slightly, but the August data showed a big jump from July’s 6.8% increase.

The Federal Reserve consumer debt figures include credit card debt, student loans, and auto loans, but do not factor in mortgage debt. When you include mortgages, US consumers are buried under more than $16 trillion in debt.

US consumer debt grew by an average of over $31 billion per month through the first eight months of the year.

Americans are burning up their plastic in order to make ends meet in these inflationary times. Revolving credit, primarily reflecting credit card debt, rose by another $17.1 billion in August. To put the 18.1% increase into perspective, the annual increase in 2019, prior to the pandemic, was 3.6%. It’s pretty clear that with stimulus money long gone, Americans have turned to plastic in order to make ends meet as prices continue to skyrocket.

Total revolving debt now stands at $1.154 trillion — well above the pre-pandemic record.

Meanwhile, average credit card interest rates have eclipsed the record high of 17.87% set in April 2019. The average annual percentage rates (APR) currently stand at 18.45%. That’s up from 18.03% just a month ago.

And it appears that the Fed isn’t finished raising interest rates. This is bad news for Americans depending on credit to pay their bills. With interest rates rising, Americans are paying higher and higher interest charges every month with minimum payments rising. With every Federal Reserve interest rate increase, the cost of borrowing will go up more, putting a further squeeze on American consumers.

As a result, more people are keeping higher credit card balances for longer. According to a CreditCards.com report, 60% of credit-card debtors say they have been in credit card debt for at least a year. That’s up from 50% just one year ago. The number of people in debt for over two years also increased, from 32% to 40%. According to Bloomberg, “With inflation exceeding wage gains, more households have relied on revolving debt.”

Non-revolving credit also charted a healthy jump in August increasing by $15 billion, an 5.2% year-on-year jump. This includes auto loans and student loans. Total non-revolving credit now stands at $3.526 trillion.

By and large, the mainstream doesn’t fret over growing consumer debt.

In fact, many mainstream reports will tell you credit card spending is a sign of a healthy economy. A couple of months ago, MarketWatch reported, “How much credit households use is seen as a good window into the strength of the economy. Consumers tend to borrow more when times are good and cut back when the economy is weak.”

Meanwhile. Fed chair Jerome Powell keeps telling us that “households are in very strong financial shape.”

But some people in the mainstream seem to be getting concerned about the growing level of debt.

After the August data came out, Marketwatch reported, “Some experts are alarmed at the pace of growth in consumer credit and think that households are using expensive debt to keep spending with inflation so elevated.”

And it is clear that Americans are laboring under the growing debt load, along with rising prices. According to a recent report by LendingTree, 32% of Americans have paid a bill late in the past six months, and 61% said it was because they didn’t have the money on hand to cover the cost.

The bottom line is that Americans continue to borrow at an excessive rate because they don’t have any other way to make ends meet. People don’t run up their Visa balance month after month to buy groceries when they are in “very strong” financial shape.

The stimulus checks are long gone.

Savings are being depleted.

The average person has no choice but to pull out the plastic. Of course, this is not a sustainable trajectory. A credit card has this inconvenient thing called a limit.

Peter Schiff pointed out in a tweet that the spiraling level of debt has even deeper roots. It was intentionally incentivized by the central bank.

end

Peter Schiff: The Fed Didn’t Create The Inflation Problem Last Year; It Was Decades In The Making

TUESDAY, OCT 11, 2022 – 08:42 AM

It’s easy to look back over the post-pandemic era and say the Federal Reserve stayed too loose for too long in the face of rising CPI. For months, the central bank ignored the inflation problem, claiming it was transitory. But as Peter Schiff pointed out in a podcast, the loose money problem isn’t anything new. It’s been going on for decades.

You can trace the Fed’s inflationary monetary policy all the way back to 1998 and the Long-Term Capital Management bailout.

That’s when the Fed really started printing money. And then it printed even more money in advance of Y2K. And then even more money after the NASDAQ bubble popped in 2000. And even more money after the real estate bubble popped in 2008. So, it’s not just one year of excess money printing. The Fed has been too loose for almost 25 years, flooding the economy with cheap money.”

Wharton School of Business finance professor Jeremy Siegel was recently on CNBC arguing that if the Fed had simply started hiking interest rates and ended quantitative easing sooner, instead of claiming that inflation was transitory, we wouldn’t be having the inflation problem today.

That’s short-sighted. The seeds were sown years ago.

But why didn’t Federal Reserve Chairman Jerome Powell act sooner? Peter said it was because he didn’t want to create a problem by fighting inflation because, at the time, he could claim inflation wasn’t a problem.

They didn’t want to fight it in 2021 because it would have created a problem for the economy. Now, the inflation they didn’t want to fight because doing so would have created a problem has itself become the problem. And so, they’ve got a problem either way. They’re damned if they do, and they’re damned if they don’t. So, that’s why they’re fighting inflation now. But even if they had chosen to fight it earlier, before it got this out of hand, they still would have created a crisis. Because it’s not just being too loose for a year. Again, it’s 25 years of reckless money printing — of malinvestments and misallocations of resources. This is a gigantic credit bubble. We just added even more fuel to that bubble in the last year.”

Peter said there was no way around this. There wasn’t a “correct” decision the Fed could have made last year.

All [the Fedf] did was make the only decision that would allow them to postpone the pain for a little longer. They had no idea how much time they were buying by being that reckless. But they didn’t care. The name of the game for the Fed is always ‘don’t create a problem even if it solves a bigger problem.’ Wait for that bigger problem to become a crisis.”

Peter said he knew 2008 wasn’t the real crash. The reckless monetary policy in the response to the Great Recession simply papered things over and kicked the looming crisis down the road.

Well, the real crash is the one we’re headed for right now. And we were going to have that crash regardless of the mistakes the Fed made in 2021. We were going to have it because of all the mistakes it made — not just going back to 2008 — but going all the way back to 1998.”

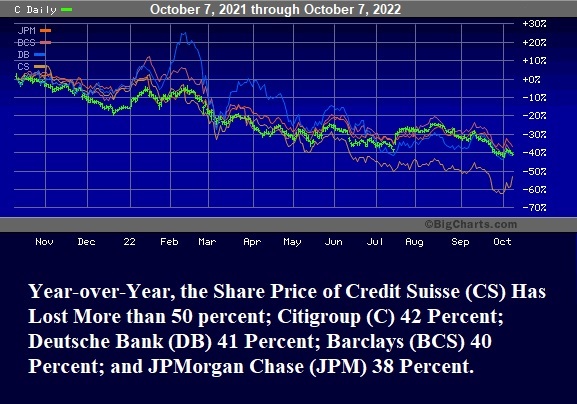

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

Shhh! Don’t Tell the Fed or Mainstream Media that Systemic Contagion at Wall Street Banks Is Already Here

By Pam Martens and Russ Martens: October 10, 2022

At Fed Chairman Jerome Powell’s last press conference on September 21 he said that there is “good reason to think that this will continue to be a reasonably strong economy.” Unfortunately, the U.S. can’t have a strong economy without strong banks willing and able to lend. And there are serious storm fronts in that area that the Fed Chair and mainstream media are choosing to ignore.

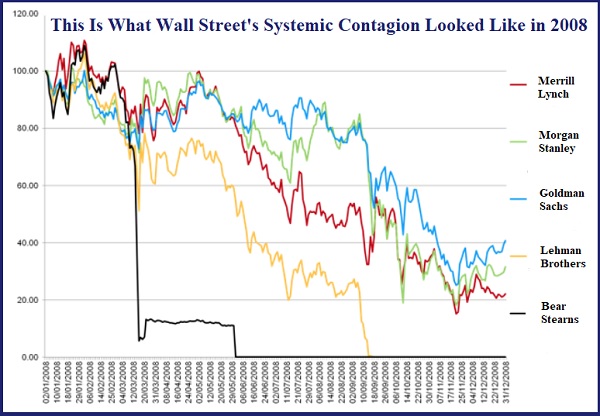

Last week multiple news outlets raised the question as to whether the troubles at Credit Suisse signaled another “Lehman moment.” (See here, here, and here, for example.) A “Lehman moment” refers to the former 158-year old Wall Street investment bank, Lehman Brothers, collapsing into bankruptcy on September 15, 2008 during a widening financial crisis on Wall Street. Because Lehman was the only major Wall Street firm that the Fed allowed to collapse into bankruptcy (rather than orchestrating a bailout), it has been mistakenly viewed all these years as the catalyst for the carnage that followed. As we will explain shortly, that role rightfully belongs to Citigroup.

According to documents released by the Financial Crisis Inquiry Commission (FCIC), at the time of Lehman Brothers’ bankruptcy it had more than 900,000 derivative contracts outstanding and had used the largest banks on Wall Street as its counterparties to many of these trades. The FCIC data shows that Lehman had more than 53,000 derivative contracts with JPMorgan Chase; more than 40,000 with Morgan Stanley; over 24,000 with Citigroup’s Citibank; over 23,000 with Bank of America; and almost 19,000 with Goldman Sachs.

Below is a share price chart of what contagion looked like on Wall Street in 2008. Notice the highly correlated share price pattern in 2008 and the highly correlated share price pattern in the chart above in 2022.

Lehman’s interconnectedness with other major Wall Street firms certainly fueled some of the systemic contagion on Wall Street in 2008. But the real culprit was Citigroup – a reckless trading house on Wall Street which owned, both then and now, a large federally-insured commercial bank, Citibank. These are just a few of the headlines about Citigroup that ran long before Lehman’s collapse into bankruptcy:

January 10, 2008, Wall Street Journal: “Citigroup, Merrill Seek More Foreign Capital,” noting: “Two of the biggest names on Wall Street are going hat in hand, again, to foreign investors.”

January 17, 2008, Los Angeles Times: “Citigroup Loses Nearly $10 Billion”

March 5, 2008, MarketWatch: “Citigroup CEO Says Firm ‘Financially Sound’” with the opening sentence explaining that “The chief executive of Citigroup sought to allay investor fears Wednesday, a day after the stock hit a multiyear low…”

April 20, 2008, New York Times: “Citigroup Records a Loss and Plans 9000 Layoffs,” explaining that the bank reported a $5.1 billion loss and would have to slash jobs.

June 26, 2008, Wall Street Journal: “Citigroup: Worth Less and Less Every Day,” shares the news that the stock was worth one-third of where it had been at its 52-week high.

July 23, 2008, Bloomberg News: “Citigroup Unravels as Reed Regrets Universal Model.”

On July 14, 2008, Bloomberg News reported that in addition to holding $2.2 trillion in assets on its balance sheet, Citigroup has $1.1 trillion of “mysterious” assets off its balance sheet, including “trusts to sell mortgage-backed securities, financing vehicles to issue short-term debt and collateralized debt obligations, or CDOs, to repackage bonds.”

Sheila Bair, the Chair of the Federal Deposit Insurance Corporation in 2008, wrote the following about Citigroup in her book Bull by the Horns:

“By November [2008], the supposedly solvent Citi was back on the ropes, in need of another government handout. The market didn’t buy the OCC’s and NY Fed’s strategy of making it look as though Citi was as healthy as the other commercial banks. Citi had not had a profitable quarter since the second quarter of 2007. Its losses were not attributable to uncontrollable ‘market conditions’; they were attributable to weak management, high levels of leverage, and excessive risk taking. It had major losses driven by their exposures to a virtual hit list of high-risk lending; subprime mortgages, ‘Alt-A’ mortgages, ‘designer’ credit cards, leveraged loans, and poorly underwritten commercial real estate. It had loaded up on exotic CDOs and auction-rate securities. It was taking losses on credit default swaps entered into with weak counterparties, and it had relied on unstable volatile funding – a lot of short-term loans and foreign deposits. If you wanted to make a definitive list of all the bad practices that had led to the crisis, all you had to do was look at Citi’s financial strategies…What’s more, virtually no meaningful supervisory measures had been taken against the bank by either the OCC or the NY Fed…Instead, the OCC and the NY Fed stood by as that sick bank continued to pay major dividends and pretended that it was healthy.”

Notice the sentence in the above paragraph that reads: “It was taking losses on credit default swaps entered into with weak counterparties….” Bair was describing the situation in 2008. Now consider this headline we ran just last week at Wall Street On Parade: New Study: Wall Street Banks Are Doubling Down on Risk by Selling Credit Default Swaps on their Risky Derivatives Counterparties. It is nothing less than an indictment of the U.S. Congress that this is allowed to happen after derivatives caused the greatest U.S. economic collapse in 2008 since the Great Depression.

The official report from the Financial Crisis Inquiry Commission, following an in- depth investigation of the 2008 collapse, wrote this about Credit Default Swaps:

“OTC derivatives contributed to the crisis in three significant ways. First, one type of derivative—credit default swaps (CDS)—fueled the mortgage securitization pipeline. CDS were sold to investors to protect against the default or decline in value of mortgage-related securities backed by risky loans…

“Second, CDS were essential to the creation of synthetic CDOs. These synthetic CDOs were merely bets on the performance of real mortgage- related securities. They amplified the losses from the collapse of the housing bubble by allowing multiple bets on the same securities and helped spread them throughout the financial system…

“Finally, when the housing bubble popped and crisis followed, derivatives were in the center of the storm. AIG, which had not been required to put aside capital reserves as a cushion for the protection it was selling, was bailed out when it could not meet its obligations. The government ultimately committed more than $180 billion because of concerns that AIG’s collapse would trigger cascading losses throughout the global financial system. In addition, the existence of millions of derivatives contracts of all types between systemically important financial institutions—unseen and unknown in this unregulated market—added to uncertainty and escalated panic, helping to precipitate government assistance to those institutions.”

This morning the Bank of England is in full blown crisis mode, setting up another emergency bailout facility that is very similar to that used by the Fed during the 2008 financial crisis. And, once again, derivatives are at the heart of the problem.

For its part, the Fed announced last year that it had, for the first time in its 109-year history, created a Standing Repo Facility where, on a permanent basis it will make $500 billion available to bail out the hubris on Wall Street. The Fed Chair has the power to increase that $500 billion on a temporary basis at his “discretion.”

And if all of this wasn’t sickening enough, the Fed Chairman who set the Fed on the course of endless Wall Street bailouts, quantitative easing, and destructive meddling in markets — Ben Bernanke — was one of three receiving the Nobel Prize in economic sciences this morning. (You can’t make this stuff up.)

It’s long past the time for the United States Congress to put an end to these serial bailouts of Wall Street by the Fed and pass legislation to restore the Glass-Steagall Act so that the casinos on Wall Street are permanently separated from the nation’s federally-insured banks.

-END-

end

Lawrie Williams

END

3.Chris Powell of GATA provides to us very important physical commentaries

Fascinating!

4. OTHER PHYSICAL SILVER/GOLD

Another Ponzi scheme

5.OTHER COMMODITIES:

end

COMMODITIES IN GENERAL/

END

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.1661

OFFSHORE YUAN: 7.1662

SHANGHAI CLOSED UP 5.65 PTS OR 0.19%

HANG SENG CLOSED DOWN 384.30 OR 2.23%

2. Nikkei closed DOWN 714.86 PTS OR 2.64%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 112.88/Euro RISES TO 0.97161

3b Japan 10 YR bond yield: RISES TO. +.248/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 145.59/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.317%***/Italian 10 Yr bond yield RISES to 4.724%*** /SPAIN 10 YR BOND YIELD RISES TO 3.48%…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.975//

3j Gold at $1670.75//silver at: 19.47 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND74/100 roubles/dollar; ROUBLE AT 63.43//

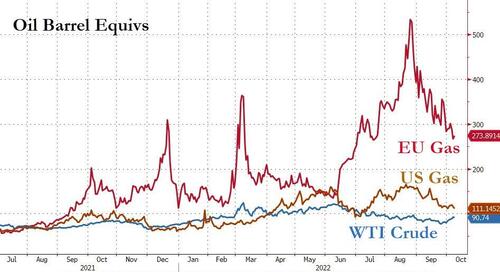

3m oil into the 89 dollar handle for WTI and 94 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 145.59DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

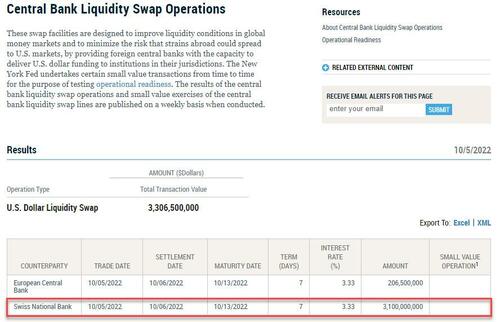

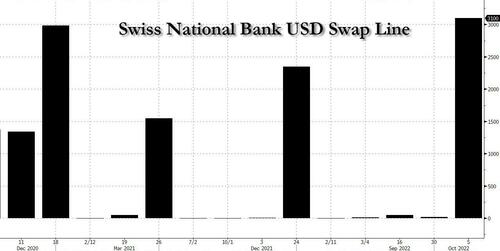

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9965– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9683well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.927 UP 4 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.896 UP 5 BASIS PTS//(USA 30 YR INVERTED TO THE USA 10)

USA DOLLAR VS TURKISH LIRA: 18,58…GETTTING DANGEROUS

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Tumble, Briefly Drop Below 3,600, Despite Latest Panic Pivot By Bank of England

TUESDAY, OCT 11, 2022 – 08:07 AM

Another day, another rout, only this time there was an even more ominous twist. It’s shaping up as another risk off day on Wall Street, and around the world, as stocks fell… again… as usual… pressured by the relentless rout in the chip sector (following Friday’s decision by the Biden administration to put fresh curbs on China’s access to US semiconductor technology) which sent chip giant Taiwan Semi conductor plunging 8.3%, its biggest drop on record, and wiped out $240 billion in market cap from the global semiconductor sector, while US futures extended their Monday slump amid general amid fears of persistently high inflation two days ahead of the CPI report, and signs that company earnings were set to disappoint. A gauge of the dollar climbed to the highest this month before reversing.

But the ominous twist today is that for the second time in two weeks, the BOE stepped in the market, this time boosting its “temporary” QE to add linker bonds to its usual array of gilt purchases to tackle what it called “fire-sale dynamics.” While this helped lift gilts and cable (if only briefly), its effect on futures was truly transitory, with the Emini dumping as much as 1% to a low of 3584, falling below the key level of 3,600, before stabilizing uneasily just above 3,600. It was down 0.6% at last check, while Nasdaq future were 0.5% lower as of 7:45am ET.

In US premarket trading, Meta Platforms slipped after it was cut to neutral from overweight by Atlantic Equities, which sees the social media giant’s growth outlook increasingly challenged by the strengthening macro headwinds and growing competition for advertising dollars; it was also added by Russia to a list of terrorist and extremist organizations. Here are some other notable premarket movers:

- Zoom shares decline 3% in premarket trading as Morgan Stanley cut the recommendation on the stock to equal-weight from overweight, saying the company’s online business needs to normalize post Covid for the firm to unlock the “tremendous value” in its enterprise platform.

- Roblox falls as much as 3.8% in premarket trading after Barclays initiates coverage with an underweight rating, saying the gaming platform’s daily users are “fairly saturated” and growth is decelerating post Covid.

- Amgen shares rise 1.7% in premarket trading after being upgraded to overweight from equal-weight by Morgan Stanley, which highlighted the “unappreciated upside” in the biopharma’s mid-term pipeline.

- Lululemon shares rise 1.3% in premarket trading after Piper Sandler upgraded the athletic apparel brand to overweight from neutral, noting the company’s momentum in the broker’s Spring 2022 Taking Stock With Teens survey.

- Elastic drops 2.4% in US premarket trading as Wells Fargo initiates at underweight, giving the application software company its only negative analyst rating.

- Leggett & Platt shares fell 8.6% in postmarket trading on Monday after the company lowered sales guidance for the full-year. Piper Sandler reduced the price target to a Street low, noting that the company’s speciality foam business is not only losing share but has been “disproportionately impacted” by weakness in the bed-in-a-box part of the market.

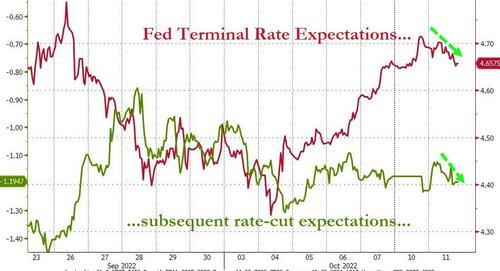

The mood remains extremely fragile ahead of Thursday’s US inflation data, with the case for another 75 basis-point rate hike likely to be strong if the reading comes in higher than than forecast. Fed officials until now show little sign they are in a mood to pause the rate-hiking cycle despite the potential hit to economic growth.

“We have not seen the impact of tightening,” Michael Kelly, head of the multi-asset team at PineBridge Investments told Bloomberg TV. “That lies ahead and when we see that, it’s another leg down for risk assets.”

Meanwhile, Russian President Vladimir Putin threatened further missile attacks on Ukraine after hitting Kyiv and other cities in the most intense barrage of strikes since the first days of its invasion. “It’s little wonder investors enter the week in a dreary mood, especially with headlines from Ukraine signaling a further escalation in geopolitical tensions,” said Christopher Smart, chief global strategist at Barings.

European stocks also declined with the Euro Stoxx 50 falling 0.9%. Energy, chemicals and miners are the worst performing sectors. IBEX outperforms peers, dropping 0.7%, FTSE MIB lags, dropping 1.4%. Here are the biggest premarket movers:

- Qiagen shares rise as much as 7.2%, the most intraday since November 2021, after a Dow Jones report that Bio-Rad Laboratories is in talks to combine with the German diagnostics firm.

- Airbus shares rise as much as 1.3% after September deliveries of 55 aircraft seen as “an encouraging data point,” compatible with the jetmaker reaching its target of 700 deliveries this year, Deutsche Bank analysts write in a note.

- Dustin shares rise as much as 10%, the most since January, after the Swedish computer and technology retail company reported 4Q results which Handelsbanken said included “solid” organic growth helped by its corporate and public sector unit.

- Boozt rises as much as 9%, the most since August, after Danske Bank upgraded the Swedish online fashion retailer to buy from hold, seeing an attractive share after recent weak performance despite a “more resilient business model than before.”

- Mining and energy stocks decline more than the broader European market on Tuesday as metals and crude slide amid concerns over weaker demand due to global economy slowdown and strengthening dollar. BP dropped as much as 3.4%, and Shell -2.4%

- European semiconductor stocks fall for a third day, following a rout in shares of Asian chip powerhouses including Samsung and TSMC. ASML declined as much as -2.8%

- Givaudan shares are down as much as 8.3%, reaching the lowest value since March 2020, after the company reported weaker-than-expected 3Q sales. Analysts are worried about soft growth in North America and a miss by the taste and wellbeing division amid a weakening consumer backdrop.

- Ferrexpo shares decline as much as 11% in early trading on Tuesday, most in three weeks, after the iron- ore maker said production has been temporarily suspended at group’s operations in Ukraine due to limited power supply.

Asian equities headed for a third day of declines amid a continued selloff in semiconductor shares, with markets in Taiwan, South Korea and Japan declining as trading resumed after holidays. The MSCI Asia Pacific Index dropped as much as 2.2%, with a technology sub-gauge falling more than 4%. Chip-related stocks in the region declined in the wake of fresh curbs on China’s access to US technology. The Hang Seng Tech Index also fell more than 3% amid the geopolitical tensions. Read: Chipmaker Rout Engulfs TSMC, Samsung With $240 Billion Wiped Out Hong Kong’s benchmark gauge slipped after a state-owned newspaper endorsed China’s Covid-Zero policy for the second day in a row, quashing investors’ hopes for a relaxation around the upcoming Communist Party congress. Chinese shares edged higher. Rising geopolitical risks are also weighing on sentiment, after Russia bombarded Kyiv and other Ukrainian cities. Meanwhile, investors remain on edge amid the prospect of more aggressive monetary tightening ahead of the release of US consumer-inflation data on Thursday.

“Thin volumes, high volatility and uncertainty, and a bearish sentiment globally means investors will overreact on the downside to any negative news,” Olivier d’Assier, head of APAC applied research at Qontigo, wrote in a note. Several data releases this week, as well as a further escalation in the war in Ukraine, may trigger further selling, he added. The MSCI’s Asian stock benchmark is once again approaching the lowest level since April 2020, having fallen more than 4% over a three-day period.

Japanese stocks fell, dragged by losses in technology shares amid concerns on earnings and the impact of new US curbs on chip-related exports to China. The Topix fell 1.9% to close at 1,871.24, while the Nikkei declined 2.6% to 26,401.25. Out of 2,168 stocks in the Topix, 285 rose and 1,833 fell, while 50 were unchanged. The market was closed for a holiday Monday. Tokyo Electron slid more than 5% after the Biden administration put fresh curbs on Chinese access to US chip technology. Tech sentiment was also hurt by a forecast cut at Yaskawa Electric, while Fast Retailing dropped more than 3% ahead of its earnings report this week. “With around 30% of Japanese tool makers’ orders coming from China, we think we are now likely to see cancelations hurting backlogs just when the chip market is facing a major oversupply,” said Amir Anvarzadeh, a strategist at Asymmetric Advisors Ltd., adding that Tokyo Electron would be among the hardest hit.

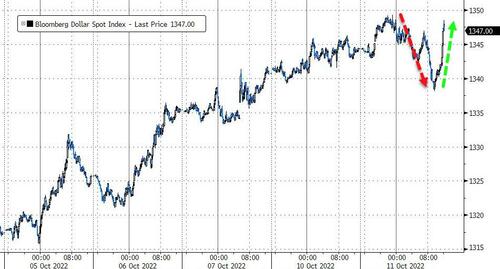

In FX, the Bloomberg Dollar Spot Index rose for fifth day as commodity currencies fell versus the greenback. Aussie and loonie were the worst G-10 performers as global growth concerns prompted traders to seek haven in the dollar; China signaled it may retain its strict Covid Zero policy, hitting stocks and commodities including iron ore

- The euro halted a four-day decline. German bonds advanced while Italy’s yield premium over Germany rose, paring some of Monday’s sharp drop amid doubts about Germany’s support for joint EU debt issuance.

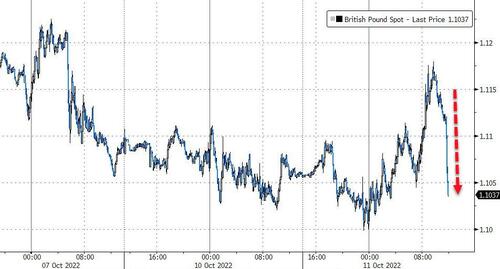

- UK bonds edged higher in a bull-steepening move after the Bank of England expanded its financial stability operations, adding inflation-linked debt to its purchases, while pausing the sale of corporate bonds. The focus is on the result of the BOE’s daily bond-buying operation, a sale of 2051 linkers by the government and Governor Andrew Bailey’s comments later. The pound traded weaker versus the euro and was little changed against the dollar. Options traders are adding downside exposure in the pound again as cable retreats toward the $1.10 handle.

- The yen traded in a narrow range amid caution the authorities will step in to prevent further currency losses. Government bonds fell in tandem with overseas peers.

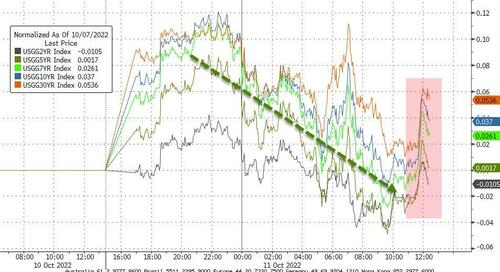

In rates, Treasuries pared a decline and the curve bear steepened after the panicking BOE expanded its QE operation. The 10-year yields pated Monday’s gilt-led losses led by gains in UK bond market, after earlier touching 4%, while the 30-year yield hit its highest level since 2014; yields on two-year Treasuries rose to the highest since 2007. US cash market, closed Monday’s for bank holiday, remains cheaper vs Friday’s close by as much as 6bp at long end. US 10-year yield is higher by ~4bp at 3.92%, steepening 2s10s by ~5bp vs Friday’s close, with 5s30s also ~5bp wider on the day; gilts bull-steepen with UK 2-year yields richer by 11bp on the day. As reported earlier, Monday’s record slide in gilts was arrested after BOE said inflation-linked notes will be included in this week’s remaining buybacks. US auctions resume at 1pm New York time with $40b 3-year note sale, followed by 10- and 30-year sales Wednesday and Thursday

In commodities, WTI drifts 2.6% lower to trade near $88.74. Spot gold falls roughly $3 to trade near $1,665/oz. Most base metals are in the red.

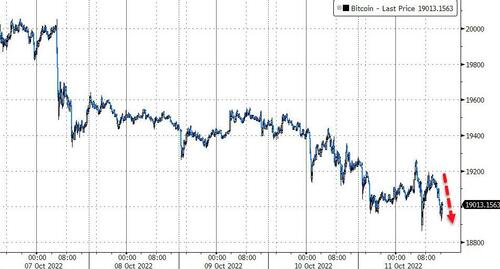

Bitcoin hovers around the USD 19,000 mark whilst Ethereum remains under 1,300.

Looking to the day ahead now, it’s another quiet event calendar with just the NFIB’s small business optimism index from the US for September out today (92.1, above 91.6 expected). From central banks, we’ll hear from BoE Governor Bailey and Deputy Governor Cunliffe, the ECB’s Lane and Villeroy, as well the Fed’s Mester. Finally, the IMF will be publishing their latest World Economic Outlook.

Market Snapshot

- S&P 500 futures down 0.7% to 3,599.25

- STOXX Europe 600 down 0.9% to 386.58

- MXAP down 2.0% to 137.94

- MXAPJ down 2.1% to 445.19

- Nikkei down 2.6% to 26,401.25

- Topix down 1.9% to 1,871.24

- Hang Seng Index down 2.2% to 16,832.36

- Shanghai Composite up 0.2% to 2,979.79

- Sensex down 0.7% to 57,610.70

- Australia S&P/ASX 200 down 0.3% to 6,644.99

- Kospi down 1.8% to 2,192.07

- Brent Futures down 1.5% to $94.71/bbl

- Gold spot down 0.1% to $1,667.26

- U.S. Dollar Index little changed at 113.21

- German 10Y yield little changed at 2.30%

- Euro little changed at $0.9708

Top Overnight News from Bloomberg

- Record inflation and the danger of winter energy shortages are sinking confidence in the euro-zone economy. As the hard data gradually worsen, the hawks who currently steer ECB policy have only a limited opportunity to deliver more big hikes

- UK unemployment fell unexpectedly to the lowest since 1974 as people dropped out of the workforce at a record rate. The government said 3.5% of adults were looking for work in the three months through August, down from 3.6% the month before. Economists had expected no change

- From Japanese pensions and life insurers to foreign governments and US commercial banks, where once they were lining up to get their hands on US government debt, most have now stepped away. And then there’s the Federal Reserve, which a few weeks ago upped the pace that it plans to offload Treasuries from its balance sheet to $60 billion a month

- Credit Suisse Group AG is the last of 16 banks to face a US class-action lawsuit accusing it of conspiring with others to rig the foreign exchange market

A more detailed breakdown courtesy of RanSquawk

APAC stocks traded with a negative bias as several markets returned from the long weekend and reacted to the recent bearish themes with tech stocks hit due to the US’s chip tech curbs on China and with global sentiment not helped by the heightened geopolitical concerns after Russia’s missile assault on Ukrainian cities. ASX 200 was indecisive after mixed data and with the index subdued by underperformance in tech and energy. Nikkei 225 declined with the reopening of Japan’s borders overshadowed by tech sector woes which also saw heavy selling pressure on South Korean and Taiwanese chipmakers. Hang Seng and Shanghai Comp. were mixed with notable losses in tech and casino stocks in which the latter suffered after domestic trips in China during the National Day Golden Week holiday fell by 18% Y/Y, while sentiment was also dampened by increased lockdown concerns as China tightened COVID controls ahead of the Communist Party congress including the rollout of mandatory biweekly mass testing in Shanghai.

Top Asian News

- China Securities Daily suggested that China may cut RRR in Q4.

- People’s Daily said China must stick to zero-COVID policy which is sustainable and key to stabilising the economy.

- China’s Xi’an announced on Tuesday to suspend onsite classes for some students amid the COVID-19 flare-ups, other areas including culture venues, tourist attractions and cinemas also suspended services on Tuesday, according to Global Times.

- PBoC set USD/CNY mid-point at 7.1075 vs exp. 7.1038 (prev. 7.0992)

- Japanese PM Kishida said the BoJ needed to maintain policy until wages increase, while he urged companies that increase prices to raise pay also and said the government will prepare measures to help companies raise salaries, according to FT.

- Japanese Finance Minister Suzuki said they are closely watching FX moves with a strong sense of urgency and will respond to excess FX moves, according to Reuters.

- Japan’s MOF top currency official Kanda said they are always ready to take necessary steps against FX volatility and said he can make a decision on FX intervention anywhere even from an aeroplane, according to TBS.

- Japanese Chief Cabinet Secretary Matsuno said they are closely watching FX moves with a high sense of urgency; to take appropriate steps on excess FX moves, via Reuters.

- Japan is to draw up economic measures before the end of October, according to NHK.

- RBI likely sold USD in spot and received forwards via state-run banks, according to traders cited by Reuters.

- RBNZ Governor Orr said in the Annual Report that there is more work to do and increasing the OCR is the most effective way we can reduce inflation and support maximum sustainable employment over the coming years, consistent with our monetary policy remit.

European bourses are once again underwater as the selling pressure from yesterday has bled through into today’s session. Sectors in Europe are mostly softer but Retail is the standout outperformer. Stateside, US futures are also on the backfoot with the e-mini S&P Dec contract dipping below 3600 in a continuation of yesterday’s losses.

Top European News

- Barclaycard UK consumer spending rose 1.8% Y/Y in September which was the slowest pace since February 2021.

- Germany’s government rejected the report about Chancellor Scholz backing joint EU debt for loans to ease the energy crisis and said “such plans are not known in the government”, according to a source cited by Reuters.

- German Chancellor Scholz said Germany will discuss inflation reduction act with the US; there must be no customs war, via Reuters.

- EU trade commissioner said it is working on a new temporary state aid framework which will allow countries to support firms hit by high energy bills; adds that decoupling from China is not an option for EU companies, via Reuters.

- UK Chancellor Kwarteng will need to plug a GBP 60bln hole in the public finances with either spending reductions or a tax raid, according to the IFS via the Telegraph.

- BoE said it intends to purchase index-linked Gilts, effective from Oct 11-14, and announced a temporary pause to corporate bond sales. Linker purchases will act as a backstop to restore order; purchases are time limited.

- Many pension funds feel that the BoE intervention in gilts market should be extended to October 31st “and possibly beyond”, according to the Pension Fund Trade Body cited by Reuters.

- Brookfield, DigitalBridge Said to Weigh Vantage Stake Bid

- European Gas Rises on Supply Risks as Russia Escalates War

- Apollo Makes Quick Gains on CLOs Dumped by UK Pension Funds

- Credit Suisse Is Final Holdout in FX Rigging Case Going to Trial

- Discounted Fuel, Grains Make Taliban Boost Trade With Russia

FX

- DXY is firmer on the day with a current intraday high of 113.50 (vs a 112.95 low)

- G10s are mixed vs the USD with the CAD and AUD the laggards, in-fitting with losses across oil and base metals respectively.

- USD/JPY held within a 145.86-50 range (vs YTD high of 145.90) following more jawboning from Japanese Chief Cabinet Secretary Matsuno.

Fixed Income

- Schatz and Bund futures both retreated to new intraday lows and the latter is just under Monday’s 135.83 session base, at 135.81.

- The 10yr UK debt future also recoiled to a deeper Liffe low (92.06) before bouncing and thereby remaining ‘comfortably’ off yesterday’s 91.46 trough.

- US Treasuries are narrowly mixed and side-lined awaiting the return of cash traders, more Fed speakers and USD 40bln 3 year issuance.

Commodities

- WTI and Brent front-month futures are weaker intraday amid several factors including technicals, a firmer Dollar, alongside further bearish COVID-related headlines emanating from China.

- Spot gold is relatively flat despite the firmer Dollar, but remains under its 21 DMA (1,674/oz) as the clock ticks down to US CPI on Thursday.

- LME metals meanwhile are mostly lower with 3M copper softer on the day amid the stronger Buck, sullied risk tone, and with the Chinese COVID restrictions an ongoing tail risk with the metal moving on either side of USD 7,500/t.

- Iranian State News Agency denied reports of worker strikes at Abadan refinery, according to Reuters.

Geopolitics

- US President Biden and G7 leaders will hold a virtual meeting today to discuss their commitment to support Ukraine, according to the White House.

- US Democrat Senator Menendez threatened to block US cooperation with Saudi amid its deepening ties with Russia, while he ripped into the decision to cut oil output and effectively accused Saudi of fuelling Russia’s war machine, according to Business Insider.

- Russian Deputy Foreign Minister Ryabkov said direct conflict with the US and NATO is not in Moscow’s interests but noted that Russia will take adequate countermeasures in response to the West’s growing involvement in the Ukraine conflict, according to RIA.

- Russian Deputy Foreign Minister said Russia does not threaten anyone with the use of nuclear weapons, via Al Jazeera

US Event Calendar

- 06:00: Sept. SMALL BUSINESS OPTIMISM, 92.1, est. 91.5, prior 91.8

Central Banks

- 12:00: Fed’s Mester Speaks to Economics Club of New York

DB’s Jim Reid concludes the overnight wrap

It’s been another rough 24 hours for markets, with a major European bond selloff after Bloomberg reported that German Chancellor Scholz would support issuing joint EU debt to deal with the energy crisis. At this stage it’s just a report without formal confirmation and we’ll have to see how it might be executed, so we shouldn’t get ahead of ourselves. However, the details from the story suggested that Scholz had signalled an openness to common borrowing at last week’s EU summit in Prague, so long as the money was distributed in the form of loans rather than grants. So perhaps the common borrowing announced during the pandemic will prove to have been the first of many rather than a one-off. If the last decade was all about how Europe/Germany could get away with as little fiscal spending as they could, this decade seems to be all about spending. This continues to change the macro dynamics of the continent completely from where it was, especially with regards bond yields and the depo rate.

We should note however, that after Europe closed, Reuters suggested that a German government source rejected the story that Berlin backed such joint EU debt for this purpose. So we’ll see if there is any retracement in yields this morning as the initial market reaction was substantial.

Yields on 10yr bunds surged +14.3bps on the day (+11bps after the story hit) to close at 2.33%, thus leaving them at their highest closing level since 2011. There were similar moves across the continent, with yields on 10yr OATs up +11.5bps to a post-2012 high of 2.91%. However, the big outperformer were Italian BTPs where yields actually fell on the day following the news, with the spread between 10yr BTPs over bunds down by -21.3bps to 230bps. That was a big change from earlier in the session, when the Italian spread had been on track to close at its widest level since April 2020 as nerves built ahead of Italian draft budget proposals.

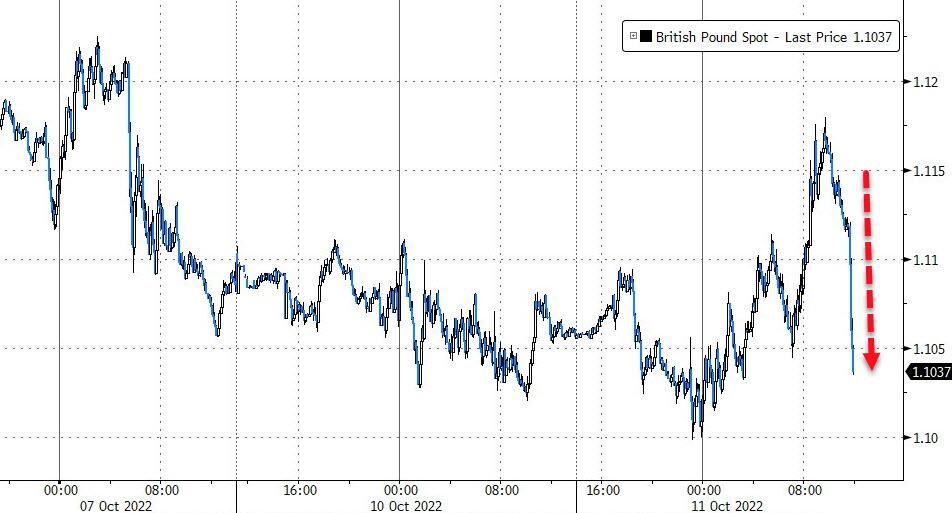

However it was a case of anything Europe could do, the UK could do worse, as the 10yr Gilt yield soared by +23.6bps on the day to 4.46% after the BoE announced fresh measures (see below) which seemed to scare investors of what might be out there rather than reassured them. The moves were eerily reminiscent of the late-September turmoil after the mini-budget, with rises in yields taking place across all maturities, with the 30yr yield up by an even-larger +28.8bps. It’s clear that LDI trades are still creating some tension in the market. If nominal yield moves weren’t enough for you, the movements in real yields were even more astonishing, with the 10yr real yield up by +64.1bps on the day to close at 1.23%, which is its highest closing level since 2009. In the meantime, sterling (-0.28%) lost ground against the US Dollar for a 4th consecutive session, closing at $1.1055, and implied sterling-dollar volatility over the next month has also been creeping back up to near its levels shortly after the mini-budget.

Those movements for gilts came in spite of numerous announcements from UK policymakers yesterday as they sought to deal with the mini-budget’s legacy. First, the Bank of England said that as part of their ongoing intervention to purchase long-dated government gilts, they would increase the maximum auction sizes for this week, which comes ahead of the planned end to the operation on Friday. In addition, they announced the launch of a “Temporary Expanded Collateral Repo Facility”, which is designed to help ease pressures on liability driven investment funds. Second, we heard that the government were bringing forward the Medium-Term Fiscal Plan to October 31 from November 23, which will be published alongside a forecast from the independent OBR. And finally, it was confirmed that James Bowler would be the new Permanent Secretary to the Treasury (the most senior civil servant in the department). Bowler is currently Permanent Secretary at the Department for International Trade but has over 20 years’ experience working in the Treasury, and the appointment was widely reported as a U-turn by PM Truss to reassure markets. That’s because Truss had pledged when running for PM that she would combat the “Treasury orthodoxy”, but has instead opted for someone with lengthy experience in the department.