by harveyorgan · in Uncategorized · Leave a comment·Edit

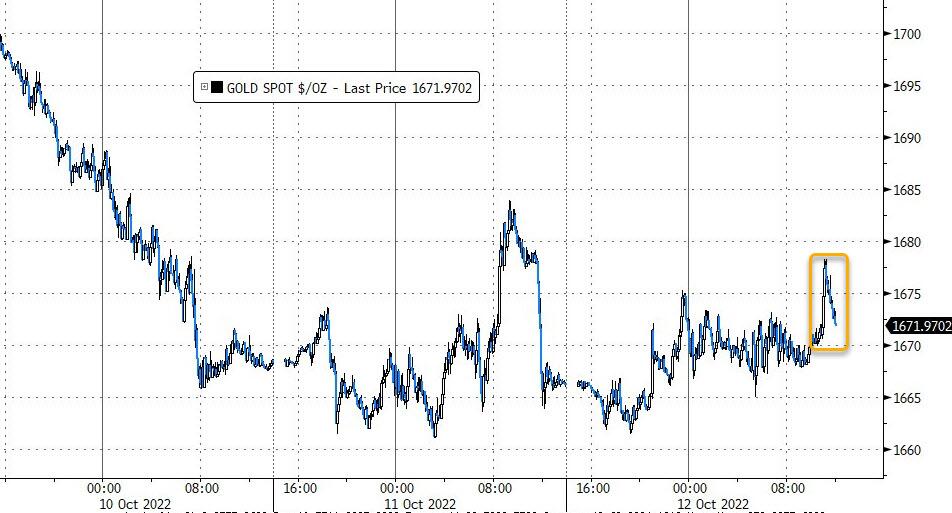

GOLD PRICE CLOSE: UP $4.00 to $1670.70

SILVER PRICE CLOSE: DOWN $0.18 to $18,99

Access prices: closes

Gold ACCESS CLOSE 1674.50

Silver ACCESS CLOSE: 19.05

New: early yesterday morning//

Bitcoin morning price: $19,140 UP 145

Bitcoin: afternoon price: $19,158 UP 127

Platinum price closing UP 4.65 AT $904.30

Palladium price; closing DOWN 0 at $2156.25

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD $2318 CDN DOLLARS PER OZ UP $18.35 CDN DOLLARS

BRITISH GOLD IN POUNDS: 1509.03 POUNDS PER OZ DOWN 8.63 BRITISH POUNDS PER OZ/

EURO GOLD: 1725.88 EUROS PER OZ// UP 10.34 EUROS PER OZ///

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: OCTOBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,678.700000000 USD

INTENT DATE: 10/11/2022 DELIVERY DATE: 10/13/2022

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 20

323 C HSBC 24

661 C JP MORGAN 6

800 C MAREX SPEC 2 1

905 C ADM 9

TOTAL: 31 31

MONTH TO DATE: 21,578

JPMORGAN STOPPED 8/28

GOLD: NUMBER OF NOTICES FILED FOR OCT CONTRACT: 31 NOTICES FOR 3100 OZ //.0964 TONNES

total notices so far: 21,576 contracts for 2,157,600 oz (67.116 tonnes)

SILVER NOTICES: 20 NOTICES FILED FOR 100,000 OZ/

total number of notices filed so far this month 359 : for 1,795,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP 4.00

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD: /////

INVENTORY RESTS AT 944.31 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 18 CENTS

AT THE SLV// :/BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A HUGE DEPOSIT OF 5.066 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 478.196 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A TINY SIZED 125 CONTRACTS TO 125,623 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE TINY LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.11 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS/HFT WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.11).SPECS CONTINUE TO ADD TO THEIR SHORTFALLS. OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS.

WE MUST HAVE HAD:

I) MINIMAL SPECULATOR SHORT COVERINGS ////CONTINUED BANKER OI COMEX ADDITIONS /// SOME NEWBIE SPEC SHORT ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.580 MILLION OZ FOLLOWING A 235,000 OZ QUEUE JUMP / // V) TINY SIZED COMEX OI LOSS/ MINIMAL SPEC COVERING THEIR SHORTS.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: — 53

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT:

TOTAL CONTRACTS for 10 days, total 50,475 contracts: 25.237 million oz OR 2.527MILLION OZ PER DAY. (505 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 25.237 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 25.237 MILLION OZ INITIAL

RESULT: WE HAD A TINY SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 125 WITH OUR $0.11 LOSS IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE CONTRACTS: 425 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /SOME BANKER ADDITIONS // SOME SHORT ADDITIONS//SMALL NEWBIE SPEC LONG ADDITIONS// /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT. OF 1.580 MILLION OZ FOLLOWED BY TODAY’S 235,000 QUEUE JUMP .. WE HAD A SMALL SIZED GAIN OF 300 OI CONTRACTS ON THE TWO EXCHANGES FOR 1.50 MILLION OZ..

WE HAD 20 NOTICE(S) FILED TODAY FOR 100,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 3631 CONTRACTS TO 431,395 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED — -492 CONTRACTS.

.

THE FAIR SIZED DECREASE IN COMEX OI CAME DESPITE OUR GAIN IN PRICE OF $10.30//COMEX GOLD TRADING/TUESDAY // SOME SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT. AT 66.099 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 10,900 OZ//NEW STANDING 69.045 TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $10.30 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A TINY SIZED GAIN OF 93 OI CONTRACTS 0.2892 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3538 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 431,395

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 399 CONTRACTS WITH 3139 CONTRACTS DECREASED AT THE COMEX AND 3538 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 399 CONTRACTS OR 1.241 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3538) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (3631): TOTAL GAIN IN THE TWO EXCHANGES 93 CONTRACTS. WE NO DOUBT HAD 1) MINOR SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS///NEWBIE SPEC SHORT ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 66.099 TONNES FOLLOWED BY TODAY’S 10,900 OZ QUEUE JUMP///NEW STANDING 69.045 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) FAIR SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT. :

22,326 CONTRACTS OR 2,232,600 OZ OR 69.44 TONNES 10 TRADING DAY(S) AND THUS AVERAGING: 2233 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAY(S) IN TONNES: 69.44 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 69.44/3550 x 100% TONNES 1.95% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 69.44 TONNES INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A TINY SIZED 125 CONTRACT OI TO 125,623 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 425 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 425 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 125 CONTRACTS AND ADD TO THE 425 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED GAIN OF 300 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 1.500 MILLION OZ

OCCURRED DESPITE OUR LOSS IN PRICE OF $0.11

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 45.71 PTS OR 1.52% //Hang Seng CLOSED DOWN 131.39 OR 0.78% /The Nikkei closed DOWN 4.42PTS OR 0.02% //Australia’s all ordinaires CLOSED DOWN 0.03% /Chinese yuan (ONSHORE) closed DOWN TO 7.1711 //OFFSHORE CHINESE YUAN DOWN 7.1802// /Oil UP TO 89.57 dollars per barrel for WTI and BRENT AT 94.71 / Stocks in Europe OPENED ALL MIXED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 3631 CONTRACTS TO 431,395 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS FAIR COMEX DECREASE OCCURRED DESPITE OUR STRONG RISE IN PRICE OF $10.30 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (3538 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3538 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :3538 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3538 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A TINY SIZED TOTAL OF 93 CONTRACTS IN THAT 3538 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 3631 CONTRACTS..AND THIS TINY GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR RISE IN PRICE OF GOLD $10.30//WE HAD SPEC SHORTS ADDING TO THEIR POSITIONS WITH BANKERS TAKING THE OTHER SIDE AS BUYERS OF COMEX GOLD CONTRACTS. WE ALSO HAD SOME ADDITIONAL SPECS GOING LONG DUE TO THE ATTRACTIVE PRICE

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING OCT (69.045),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 69.045 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $10.30) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS (THEY ADDED TO THEIR POSITIONS) AS WE HAD A TINY SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 93 CONTRACTS // WE HAVE REGISTERED A SMALL GAIN OF 0.2892 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR OCT. (69.045 TONNES)…THIS WAS ACCOMPLISHED WITH A RISE IN PRICE OF $10.30

WE HAD -492 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 93 CONTRACTS OR 9300 OZ OR 0.2892 TONNES

Estimated gold volume 127,081// poor//

final gold volumes/yesterday 181,858/ poor

INITIAL STANDINGS FOR OCT ’22 COMEX GOLD //OCT 12

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 99,287.070oz JPMorgan MALCA includes 1183 kilobars |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 31 notice(s) 3100 OZ 0.0964 TONNES |

| No of oz to be served (notices) | 620 contracts 54,100oz 1.928 TONNES |

| Total monthly oz gold served (contracts) so far this month | 21,578 notices 2,157,800 67.116 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits NIL oz

customer withdrawals:2

i) Out of JPMorgan: 61,252.437oz

ii) out of Malca: 38,034.633 0z (1183 kilobars)

total: 99,287,070 oz

total in tonnes: 3.08 tonnes

Adjustments: 1// dealer to customer

Brinks: 4147.479 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT we have an oi of 651 contracts having GAINED 81 contracts . We had 28 contracts

filed on TUESDAY, so we gained 109 contracts or an additional 10,900 oz will stand in this active delivery month of Oct.

We will gain gold oz standing on each and every trading day from this day forth until the conclusion of October.

(remember that queue jumping is really EFP’s exercised from London for gold underwritten by COMEX based bankers)

November GAINED 123 contracts to stand at 3131

December lost 5022 contracts down to 363,678

We had 31 notice(s) filed today for 3100 oz FOR THE OCT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 23 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 6 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT /2022. contract month,

we take the total number of notices filed so far for the month (21,578) x 100 oz , to which we add the difference between the open interest for the front month of (OCT 651 CONTRACTS) minus the number of notices served upon today 28 x 100 oz per contract equals 2,219,800 OZ OR 69.045 TONNES the number of TONNES standing in this active month of OCT. (TOTALS CORRECTED FROM FRIDAY)

thus the INITIAL standings for gold for the OCT contract month:

No of notices filed so far (21,578) x 100 oz+ (651) OI for the front month minus the number of notices served upon today (31} x 100 oz} which equals 2,219,800, oz standing OR 69.045 TONNES in this NON active delivery month of OCTOBER.

TOTAL COMEX GOLD STANDING: 69.045 TONNES (A HUMONGOUS STANDING FOR OCT (GENERALLY THE POOREST DELIVERY MONTHS FOR AN ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,067,434 OZ (REG GOLD- PLEDGED GOLD) 340.166 tonnes//rapidly declining

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 23,826,978.622 OZ

TOTAL REGISTERED GOLD: 12,315,332.840 OZ (383.06tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 13,511,645.782 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,247,898 OZ (REG GOLD- PLEDGED GOLD) 318.75 tonnes//rapidly declining

END

SILVER/COMEX

OCT 12//INITIAL OCT SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 932,339.270 oz CNT Int. Delaware Manfra Delaware |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 628,720.874 oz Delaware CNT |

| No of oz served today (contracts) | 20 CONTRACT(S) 100,000 OZ) |

| No of oz to be served (notices) | 67 contracts (335,000 oz) |

| Total monthly oz silver served (contracts) | 417 contracts 2,085,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i) into Delaware: 32,654.266 oz

ii) Into CNT: 596,066.608 oz

Total deposits: 682,720.874 oz

JPMorgan has a total silver weight: 160.801million oz/310,427million =51.86% of comex

Comex withdrawals: 4

i)Out of CNT 299,941.400 oz

iv) Out of Delaware 961.000 oz

v) Out of Int. Delaware 30,193.150 oz

vi_ Out of Manfra: 600,245,720 oz

total withdrawals: 931,339.270 oz

adjustments: // 3 dealer to customer

Brinks: dealer to customer: 15,041.320 oz

CNT 4795.510 oz

Manfra: 4869.658 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 40.082 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 310.422 MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF OCT OI: 87 CONTRACTS HAVING GAINED 9 CONTRACT(S.)

WE HAD 38 NOTICES FILED ON TUESDAY SO WE GAINED 47

SILVER CONTRACTS OR AN ADDITIONAL 235,000 OZ WILL STAND FOR OCT.

NOVEMBER GAINED 0 CONTRACT TO STAND AT 400

DECEMBER SAW A LOSS OF 785 CONTRACTS DOWN TO 103,385

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 20 for 100,000 oz

Comex volumes:55,855// est. volume today// fair

Comex volume: confirmed yesterday: 63,623 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 417 x 5,000 oz = 2,085,000 oz

to which we add the difference between the open interest for the front month of OCT(87) and the number of notices served upon today 20 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT./2022 contract month: 417 (notices served so far) x 5000 oz + OI for front month of OCT (87) – number of notices served upon today (20) x 5000 oz of silver standing for the OCT contract month equates 2,420,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:56,736// est. volume today// poor

Comex volume: confirmed yesterday: 64,896 contracts ( poor)

END

GLD AND SLV INVENTORY LEVELS

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

GLD INVENTORY: 944.31 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

CLOSING INVENTORY 478.196 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

end

Lawrie Williams

END

3.Chris Powell of GATA provides to us very important physical commentaries

Are we close to Fed capitulation?

Ambrose thinks so:

(Ambrose Evans Pritchard/UKTelegraph)

Ambrose Evans-Pritchard: Rejoice, for we may be close to Fed capitulation

Submitted by admin on Tue, 2022-10-11 09:55Section: Daily Dispatches

By Ambrose Evans-Pritchard

The Telegraph, London

Tuesday, October 11, 2022

Warnings about monetary overkill by central banks are growing louder. This time the insurgency is coming from within America’s New Keynesian elite.

That matters. It suggests that the Federal Reserve may be closer to a blissful “policy pivot” than markets think. The moment that investors discern signs of any such Fed capitulation, there will be a massive bear-trap rally in battered global equities — at least until the bulls are hit by the oncoming steam-train of deflating profits.

Episodes of Fed tightening are often brutal for the rest of the world. This one is especially ferocious. The broad dollar index is at an epic high, which means slow torture for emerging and frontier markets with $4.2 trillion of debt denominated in dollars. There is $13.4 trillion of offshore dollar debt outside U.S. jurisdiction (BIS data) with no clear lender-of-last-resort. South Korea is already having to approach the Fed for dollar swap lines.

Borrowers are being hit by the double shock of both the higher dollar and surging dollar loan-rates. Some of this debt must be rolled over on the three-month lending markets, with a rising risk premium for good measure. …

… For the remainder of the report:

https://www.telegraph.co.uk/business/2022/10/11/rejoice-may-close-fed-capitulation/

end

This should be interesting; UK court says that the hedge funds, Elliot and Jane Street can sue the LME for the cancelled nickel trades

(zerohedge)

UK court says hedge funds can sue LME for cancelled nickel trades

Submitted by admin on Tue, 2022-10-11 10:46Section: Daily Dispatches

By Pratima Desai

Reuters

Monday, October 10, 2022

LONDON — A British court has granted permission for U.S.-based hedge fund Elliot Associates and Jane Street Global Trading to sue the London Metal Exchange (LME) for cancelling nickel trades in March, a court document showed.

Elliott and Jane Street are demanding damages of $456.4 million and $15.34 million respectively, after the nickel price topped a record $100,000 per tonne on March 8, prompting the LME’s suspension of nickel trading and voiding of trades.

The nickel trading episode has been the biggest crisis to hit the world’s oldest metals forum in decades. The LME has 28 days from Oct. 3 when the ruling was made to file its defence. …

… For the remainder of the report:

end

I have been detailing this to you on a daily basis: paper silver is being converted into real physical metal

(Craig Hemke/Sprott Money)

Craig Hemke at Sprott Money: A flow out of paper silver and into real metal

Submitted by admin on Tue, 2022-10-11 17:17Section: Daily Dispatches

By Craig Hemke

SprottMoney.com

Tuesday, October 11, 2022

An interesting dichotomy has developed in the “silver market.” What does it mean? Does it mean anything at all? We’ll know soon enough, I guess.

What an interesting year this has been, and the last six months have been positively brutal. While we await the eventual central bank pivot back toward easing and QE, Comex digital gold and silver have been whacked, cracked, and shellacked.

But as we have seen multiple times in the past, this has led to a widening gap between the futures price and the physical price.

There’s a lot going on behind the scenes in the commodity markets.

For example, crude oil demand should be falling with the global economic slowdown. However, crude oil supply is also falling, save for the shortsighted U.S. policy of draining its “strategic reserves.”

And have you noticed the dwindling stockpiles of copper, not only in London but in China, in part due to the unwinding of loans and credit where copper was used as collateral?

But let’s focus today on silver, as it’s of the greatest interest to all of us precious metal stackers. Most know that the price of silver that’s prominently featured in financial media is the price “discovered” on futures exchanges like Comex. As with anything else, this price is often dependent upon supply and demand — in this case, the supply and demand of the futures contracts themselves.

What’s interesting is that the current supply of futures contracts is at a nine-year low. …

… For the remainder of the analysis:

4. OTHER PHYSICAL SILVER/GOLD

5.OTHER COMMODITIES: ALUMINUM

Aluminum prices surge after Biden weighs on a ban on Russian made metal

(zerohedge)

Aluminum Price Surges After White House Weighs Ban On Russian Metal

WEDNESDAY, OCT 12, 2022 – 01:01 PM

The Biden administration’s economic war against Russia could soon be stepped up a few notches as Bloomberg reports the White House is considering a complete ban on Russian aluminum.

People familiar with the matter said the White House is reviewing three options: an outright ban, expanding tariffs to levels that would impose an effective ban, and or sanctioning the country’s top metal producer, United Co. Rusal International PJSC.

Whatever route the White House takes against Russia could have severe consequences for global metal markets, forcing customers in the US, Europe, and elsewhere into a panic to source replacement metal.

LME aluminum prices jumped as much as 7% on the news.

Russia is the world’s second-largest producer of aluminum after China. Bloomberg cited trade data showing Russia supplies about 10% of US aluminum imports. It also showed Russia was the third largest exporter to the US in August.

We noted last week that the London Metal Exchange (LME) considered plans for a potential ban on new Russian metal supplies. Alcoa Corp., the US’ largest aluminum producer, recently sent a letter to the LME indicating Russian metal could be dumped on global markets and suppress prices.

Today’s news has sent Alcoa shares up more than 8%. Other aluminum makers surged as well.

The Biden administration has held off sanctioning Russian aluminum for fear of disrupting global markets, but now that might not be the case as the ongoing war, now in its eight-month, continues with no end in sight. Meanwhile, US/EU sanctions against Russia to limit energy flows into global markets have backfired.

The sources said the high-level discussions about banning Russian aluminum have been ongoing for weeks.

end

COMMODITIES IN GENERAL/

END

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.1711

OFFSHORE YUAN: 7.1802

SHANGHAI CLOSED UP 45.71 PTS OR 1.53%

HANG SENG CLOSED DOWN 131.33 OR 0.78%

2. Nikkei closed DOWN 4.42 PTS OR 0.02%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UPN TO 113.17/Euro RISES TO 0.97078

3b Japan 10 YR bond yield: RISES TO. +.248/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 146.64/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.392%***/Italian 10 Yr bond yield RISES to 4.834%*** /SPAIN 10 YR BOND YIELD RISES TO 3.56%…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.975//

3j Gold at $1669.05//silver at: 19.15 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND36/100 roubles/dollar; ROUBLE AT 64.02//

3m oil into the 89 dollar handle for WTI and 94 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 146.64DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9954– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9661well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.962 UP 3 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.944 UP 4 BASIS PTS//(USA 30 YR INVERTED TO THE USA 10)

USA DOLLAR VS TURKISH LIRA: 18,59…GETTTING DANGEROUS

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Bounce, Gilts Tumble In BOE-Driven Rollercoaster Session

WEDNESDAY, OCT 12, 2022 – 08:03 AM

US stocks were set to bounce, ending a brutal five-day losing streak, amid confusion over what the BOE will do in two days, amid hope that tomorrow’s CPI print will come in lower than expected, and as Treasury yields eased off multi-year highs – at least initially – and investors put aside concerns that overheating inflation could offer more fodder to hawkish Federal Reserve policy makers amid speculation that things are breaking in far too many markets after it emerged that the Fed had sent a substantial amount of dollars to Switzerland this week in the first material use of the dollar swap facility in 2022. Nasdaq futures gained 0.9% by 7:30 a.m. in New York while S&P 500 futures rose 0.7% a day after the benchmark index nearly erased its October gains, while UK bonds tumbled and the pound rose amid UK policy confusion. While global risk sentiment earlier received a boost from a report suggesting the Bank of England could extend its emergency bond repurchases, a bank spokesperson quashed that speculation and said the program would still end on Friday, leaving traders in the dark as to what will happen.

Meanwhile, Treasury yields and the dollar were little changed as traders await a key US inflation measure due Thursday that’s set to return to a four-decade high, underscoring broad and elevated price pressures that are pushing the Federal Reserve toward yet another large interest-rate hike next month. US investors are also looking to corporate earnings for clues about Fed policy.

Among notable moves in premarket trading, Uber Technologies edged back up after the previous session’s 10% slump that was driven by the Biden administration’s proposal on classifying gig workers’ employment status. Analysts said there was limited near-term risk, given implementation was “far from imminent.” Chip stocks were set to recoup some of this week’s losses stemming from fresh curbs on China’s access to US semiconductor technology. Norwegian Cruise Line Holdings also gained in premarket trading, after UBS raised its recommendation on the stock to buy, amid strong improvement in bookings. PepsiCo gained 1.9% in premarket trading after the company raised its forecast for the full year and said consumers continue to purchase more of its snack foods and soft drinks despite rising inflation.

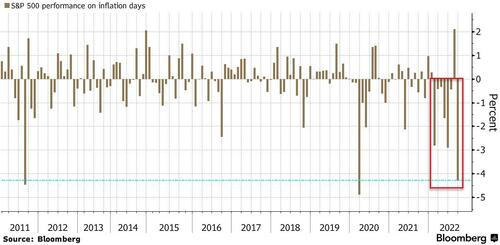

In the US, investors have been laser-focused on how the Fed might respond to inflation figures due Thursday. While economists expect the consumer price index reading for September to have declined slightly versus a year earlier, a surprise increase could send stocks tumbling, JPMorgan’s trading desk warned. Given the Fed has so far shown little sign of toning down its hawkishness, even in the face of a potential economic recession and weaker company earnings, many analysts expect equity bounces to be short-lived.

“In the back of everyone’s mind is tomorrow’s CPI print, with many investors worried that it may be as strong as the jobs report on Friday,” said Neil Campling, head of TMT research at Mirabaud Securities. “Bears are firmly in control and any rallies could be incapable of sustaining a bid for more than a few days.”

“While futures positioning is now slightly less extreme, it is still a very bearish set up into what is seen as a binary market event tomorrow,” said Carl Dooley, head of EMEA trading at Cowen in London. That makes it “natural to see some bear covering, with the remaining bulls having another roll of the dice.”

The big story overnight was the flip-flopping rollercoaster from the BOE: the yield on 30-year gilts rose above 5% for the first time since late September after the Bank of England confirmed its plan to end emergency bond purchases on Friday and a report showed the UK economy shrank unexpectedly in August. Sterling rallied more than 1% after a report from Politico that the government may make further fiscal U-turns.

“The Bank of England is a test case for how hawkish central banks can be without doing damage to financial stability,” said Michael Metcalfe, global head of macro strategy at State Street Global Markets. So far the “test” is failing miserably.

In other news, Q3 earniungs season kicks off on Friday when several top Wall Street banks are set to report including JPMorgan, although analysts have already downgraded estimates for corporate America in recent weeks, a glum outlook by management teams could further pressure stocks. Lori Calvasina, head of US equity strategy at RBC Capital Markets, cut her year-end target for the S&P 500 Index to 3,800 from 4,200 citing a weak economic backdrop through the end of 2023. However, her new target implies a nearly 6% gain from Tuesday’s close.

In European equities, consumer products, chemicals and food & beverages are the strongest-performing sectors. Euro Stoxx 50 rose 0.4% as Spain’s IBEX lagged, dropping 0.5% Credit Suisse drops as much as 5.0%, adding to a tumultuous month for the Swiss lender, after Bloomberg reported that the Justice Department is investigating whether it continued to help US clients hide assets from authorities. Here are other notable European movers:

- LVMH rises as much as 3.2% on stronger-than-expected organic revenue growth, signaling that the wealthy are still spending, and allaying fears of a China slowdown from Covid-19 curbs.

- Chr. Hansen climbs as much as 15%, the most since 2012, after the Danish enzymes and food cultures manufacturer reported better- than-expected 4Q results, including a wide topline beat, Jefferies says.

- Leonteq rallies as much as 7.8% after the company responded to a Financial Times report that had driven the stock lower in recent days.

- Bossard rises as much as 4.2% after nine- month sales beat estimates.

- UK domestic stocks underperform amid gilt market volatility following earlier speculation over the timing of an end to the Bank of England’s bond-buying program. Homebuilders, real estate, retail and domestic banks are among biggest decliners with Barclays falling as much as 5.3%.

- Philips slumps as much as 12%, hitting the lowest in more than a decade, after the Dutch medical technology company cut its outlook due to worse-than-expected supply-chain difficulties, prompting analysts to doubt its ability to meet 2022 targets.

- Kloeckner falls as much as 14%, the most intraday since May 2020, after the steel company revised its full-year guidance, which Jefferies said implies a 20%-25% reduction to consensus estimates.

Earlier in the session, Asian equities were mixed after a three-day rout, as Chinese shares rebounded in a volatile trading session, while overall sentiment remained jittery ahead of the release of the US inflation report. The MSCI Asia Pacific Index erased an early-session loss of as much as 0.8% and traded down just 0.1% as of 5:02 p.m. in Hong Kong Wednesday, with financial shares lifting the broader market. Still, the benchmark hovered near a two-year low. Chinese stocks bounced back strongly in afternoon trading as bargain hunters piled into the nation’s battered shares, with the CSI 300 Index closing 1.5% higher, the most in two months. Investors were worried about the Covid-Zero policy and an economic slowdown despite an upbeat set of aggregate financing and loans data released on Tuesday.

“With supportive valuations and better earnings outlook, downside may be limited from current levels,” said Vey-Sern Ling, an analyst at Union Bancaire Privee. Still, “China has too many outstanding issues currently that drag investor sentiment. Investors may not be willing to buy equities given the macro uncertainties.” Sentiment also remained fragile after Bank of England Governor Andrew Bailey said the bank would end emergency gilt purchases as planned this week, in the face of market pressure to expend the program. US consumer price data due Thursday will be crucial in defining the size of the Federal Reserve’s interest-rate hike at the November meeting. Economists expect inflation to top 8% again. “The tightening of US financial conditions, global and China growth slowdowns have sharply weighed on Asian equities this year,” said Rajat Agarwal, Asia equity strategist at Societe Generale SA. “Korea and Taiwan, the two semiconductor-driven markets have been the worst affected. A fading semiconductor cycle, geopolitical issues and more recently the semiconductor exports curbs have pushed the valuations to a more than five-year low on the two markets.” South Korean stocks erased losses to close higher after the central bank pivoted back to half-point interest-rate increases

Japanese stocks closed a directionless day slightly lower, pushing losses to a third day, weighed down by electronics makers. The Topix fell 0.1% to close at 1,869.00, while the Nikkei was virtually unchanged at 26,396.83. Tokyo Electron Ltd. contributed the most to the Topix Index decline, decreasing 4.4%. Out of 2,168 stocks in the index, 908 rose and 1,151 fell, while 109 were unchanged.

Australian stocks snapped a three day rout, led by financial stocks. The S&P/ASX 200 index edged higher to close at 6,647.50 after a three-day drubbing, with traders awaiting US inflation data due Thursday for further clues on Federal Reserve interest rate hikes. Financial stocks gained, led by Bank of Queensland, offsetting losses in mining and energy stocks. Coronado Global Resources was among the top gainers after the coal miner confirmed it’s in talks with Peabody Energy on a merger. In New Zealand, the S&P/NZX 50 index fell 0.8% to 10,873.23.

Stocks in India gained for the first time in four sessions, helped by real estate and consumer goods companies that had seen sharp declines earlier this week. Investors will be monitoring India’s consumer inflation data for September to be released later Wednesday to gauge the outlook for local shares. Software exporter Wipro reported quarterly earnings below consensus estimates. The S&P BSE Sensex rose 0.8% to 57,625.91 in Mumbai, while the NSE Nifty 50 Index was higher by an equal measure. All of BSE Ltd.’s 19 sector sub-indexes advanced.

In FX, the Bloomberg Dollar Spot Index was little changed as the greenback traded mixed versus its Group-of-10 peers. the yen led G-10 losses and slipped to a fresh 24- year low of 146.43 per dollar as traders tested the resolve of Japanese authorities to intervene as key US inflation data may drive further weakness. The British pound led G-10 gains after volatile session. It earlier erased gains against the dollar while gilts extended a decline after the BOE confirmed that the bond-buying scheme will still end on Friday. Sterling had risen after the Financial Times reported that the BOE told lenders it was prepared to extend the program past Oct. 14 end date if market conditions demanded it. Bearish sentiment in the pound is the strongest in two weeks when it comes to short-term bets as hedging costs keep rallying. The euro was steady around $0.97 as Bunds and Italian bonds fell led by the long end of the curve. The Aussie inched lower.

In rates, Treasuries are mixed with the curve steeper as US trading gets under way, led by dramatic steepening in UK bond market after Bank of England Governor Andrew Bailey late Tuesday said the central bank’s bond buying would end this week. Focal points of US session include September PPI and 10-year auction, following cool reception for Tuesday’s 3-year. US yields little changed at front end, the 10Y yield rises by 1bp to 3.95%, steepening 2s10s by ~1.5bp, 5s30s by ~2bp. US auction cycle continues with $32b 10- year note reopening at 1pm New York time, concludes Thursday with 30-year reopening. WI 10-year yield at around 3.96% is above auction stops since 2009 and ~63bp cheaper than last month’s result. UK gilts remain near worst levels of the session with 30-year yields cheaper by ~18bp on the day and UK 2s10s, 5s30s spreads steeper by 30bp and 15bp. Australia’s bonds gained for the first day in five after RBA Assistant Governor Luci Ellis said the central bank’s neutral interest rate is likely to be at least 2.5%, compared with the current cash-rate target of 2.6%.

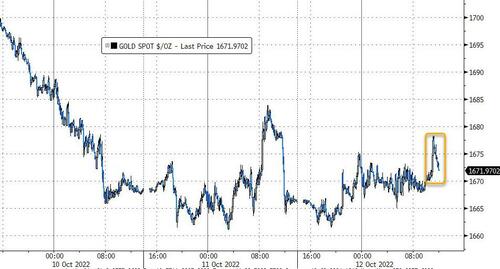

In commodities, WTI trades within Tuesday’s range, marginally falling to near $89.33. Polish pipeline operator said on Tuesday evening it detected a leak in the Druzhba pipeline; cause is unknown; leak detected in one of two lines, second line is working as normal. Russia’s Transfneft said it has received notice from Polish operator PERN about the leak at Druzbha; oil pumping towards Poland continues, according to IFX. Polish top official for energy infrastructure said there are no grounds to believe leak in Druzhba pipeline was sabotage, adds leak was probably caused by accidental damage. Spot gold is modestly firmer as the upside for the Buck remains capped for now, but the yellow metal remains under its 21DMA (USD 1,673.34/oz). LME metals are mixed with copper relatively flat but aluminium is underperforming following a large build in LME warehouse stocks.

To the day ahead now, and data releases include the US PPI reading for September, along with UK GDP and Euro Area industrial production for August. From central banks, we’ll get the FOMC minutes from the September meeting, and hear from the Fed’s Barr, Kashkari and Bowman, ECB President Lagarde, the ECB’s Knot and De Cos, as well as the BoE’s Pill, Haskel and Mann. Finally, earnings releases include PepsiCo.

Market Snapshot

- S&P 500 futures up 0.5% to 3,617.00

- MXAP little changed at 137.63

- MXAPJ little changed at 444.71

- Nikkei little changed at 26,396.83

- Topix down 0.1% to 1,869.00

- Hang Seng Index down 0.8% to 16,701.03

- Shanghai Composite up 1.5% to 3,025.51

- Sensex up 0.6% to 57,503.85

- Australia S&P/ASX 200 little changed at 6,647.54

- Kospi up 0.5% to 2,202.47

- STOXX Europe 600 down 0.2% to 387.21

- German 10Y yield little changed at 2.34%

- Euro up 0.1% to $0.9719

- Brent Futures up 0.3% to $94.55/bbl

- Gold spot up 0.3% to $1,671.92

- U.S. Dollar Index little changed at 113.12

Top Overnight News from Bloomberg

- Giorgia Meloni’s euphoria at winning the Italian election is running into reality as the far-right leader struggles to put together a coalition government and the gas-dependent country’s financial outlook darkens

- Bank of England Governor Andrew Bailey’s blunt warning that fund managers have to cut vulnerable positions before the central bank ends debt purchases is sending a shiver around already fragile global bond markets

- The UK economy shrank unexpectedly in August for the second time in three months, raising the possibility that the country is now in a recession. The 0.3% drop in output was driven by a sharp decline in manufacturing and a small contraction in services

- The Bank of England has warned that some UK households may face a strain over debt repayments that is as great as before the 2008 financial crisis, if economic conditions continue to be difficult

- Bank of England policy maker Jonathan Haskel said one of the key issues ailing the UK economy is lackluster levels of business innovation and productivity

- The European Union is moving closer to proposing a temporary overhaul of the electricity market by limiting prices of gas used for power generation even as pressure mounts for the bloc to impose a broader cap

- Germany’s biggest service-sector union is demanding 10.5% pay increases amounting to at least 500 euros ($486) a month for public-sector employees to avoid real losses amid record inflation

A more detailed look at global markets courtesy of Newsquawk

Asian stocks were subdued with price action indecisive as the region took its cue from the choppy performance and late selling stateside after BoE Governor Bailey rejected industry calls for an extension to Gilt purchases, although a report from FT overnight suggested the contrary. ASX 200 was rangebound with strength in the real estate and the top-weighted financials sector offsetting the losses in tech, utilities and mining-related stocks, while there were also comments from RBA’s Assistant Governor Ellis who suggested nominal rates have already passed neutral and that policy was no longer expansionary. Nikkei 225 lacked conviction following the disappointing Machinery Orders data although the downside was contained with Japan reportedly to draw up economic measures before month-end. Hang Seng and Shanghai Comp. were the worst hit despite the jump in loans and financing data in China with markets constrained by lockdown concerns after China’s Xi’an announced to suspend onsite classes for some students and shut other venues, while the Shenzhen Metro suspended three stations due to coronavirus.

Top Asian News

- US permitted at least two non-Chinese chipmakers in China to receive goods and support that are restricted under new US export rules, according to industry sources. It was later reported that SK Hynix (000660 KS) received authorisation from the US Commerce Department to receive equipment for a chip production facility in China for a year without seeking a separate permit from the US, according to Reuters.

- China will be declared an official threat in a new strategic review of Britain’s enemies, according to The Sun.

- RBA Assistant Governor Ellis said the neutral rate is a guide rail for policy not a destination and that the real neutral rate is uncertain but should be positive even if low which implies a nominal neutral rate of at least 2.5% for Australia, while Ellis added that policy is no longer in an expansionary place, according to Reuters.

- BoK hiked the base rate by 50bps to 3.00%, as expected and said inflation will remain high in the 5%-6% range for a considerable time. BoK Governor Rhee said board members Joo Sang-Yong and Shin Sung-Hwan dissented at Wednesday’s rate decision, while he added that the board’s views on the rate hike pace in November differ but added that a majority of board members see the BoK’s terminal rate at 3.5%.

European bourses saw a choppy start to the session, but have since titled to the upside as US traders prepare to enter the fray. Sectors are mixed with Consumer Products bolstered by luxury names after LVMH earnings, with Tech following whilst Banks and Real Estate lag. Stateside, US equity futures trade on a firmer footing with the ES back above 3600 as the index futures attempt to claw back some of the lost ground yesterday.

Top European News

- It was reported that the BoE signalled to lenders that it is prepared to prolong bond purchases with officials privately indicating a flexible approach if market volatility flares up, according to FT. It was later reported that BoE affirmed that its bond-buying scheme will end on Friday 14th October, via Bloomberg.

- BoE said the bank has made it clear from the outset its temporary and targeted purchases of gilts will end on October 14th, and beyond Oct 14th, a number of facilities are in place to ease liquidity pressures on LDIs.

- Pensions and Lifetime Savings Association said the announcement by the BoE to purchase index-linked Gilts is a positive additional intervention, while it noted that the concern of pension funds has been that the period of purchasing should not be ended too soon, according to Reuters.

- UK’s trade deal with India is reportedly on the verge of collapse after Indian ministers reacted “furiously” to comments by Home Secretary Braverman, according to The Times.

- There is growing speculation that UK PM Truss “could ditch yet more aspects of the mini-budget”, according to Politico’s Courea, adds “Think we’re looking at “deferring” tax cuts and maybe a further windfall tax””. However, Downing St source said that despite claims, there’s no delay to April income tax cut, former Chancellor Sunak’s corporation tax hike still is cancelled, according to a Sun reporter.

- ECB’s Villeroy said fears of a recession must not derail ECB normalisation and that the current level of inflation requires ECB determination, while he also noted that a short recession is less detrimental than stagflation and said discussion about a 50bps or 75bps hike in October is premature amid volatile markets. Furthermore, Villeroy said the ECB may move more slowly after reaching a neutral rate and the APP unwind could begin earlier than 2024 with partial reinvestments.

FX

- DXY is softer but off worst levels after testing levels close to 113.00 to the downside.

- GBP was volatile but currently stands as the outperformer following speculation over the Government ‘ditching’ or ‘deferring’ more of the tax cut proposals.

- The USD extended its bull run against the JPY to a fresh 2022 and multi-year best beyond prior Japanese intervention levels and 146.00, with little resistance from officials other than the usual verbal interjections

Fixed Income

- Bunds slipped to a fresh intraday low on Eurex at 135.64 for an 81 tick loss on the day having been 9 ticks above par at one stage.

- Gilts remain 100+ ticks adrift within extremes spanning 90.90-92.81 vs yesterday’s 92.83 Liffe close.

- US Treasuries are holding steady before PPI data, 10 year note supply, FOMC minutes and further Fed rhetoric.

Commodities

- WTI and Brent front-month futures are flat intraday but off the worst levels seen overnight.

- NHC said Tropical Storm Karl is expected to strengthen today as it moves slowly over the southwestern Gulf of Mexico.

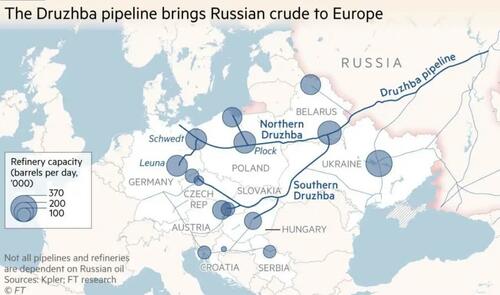

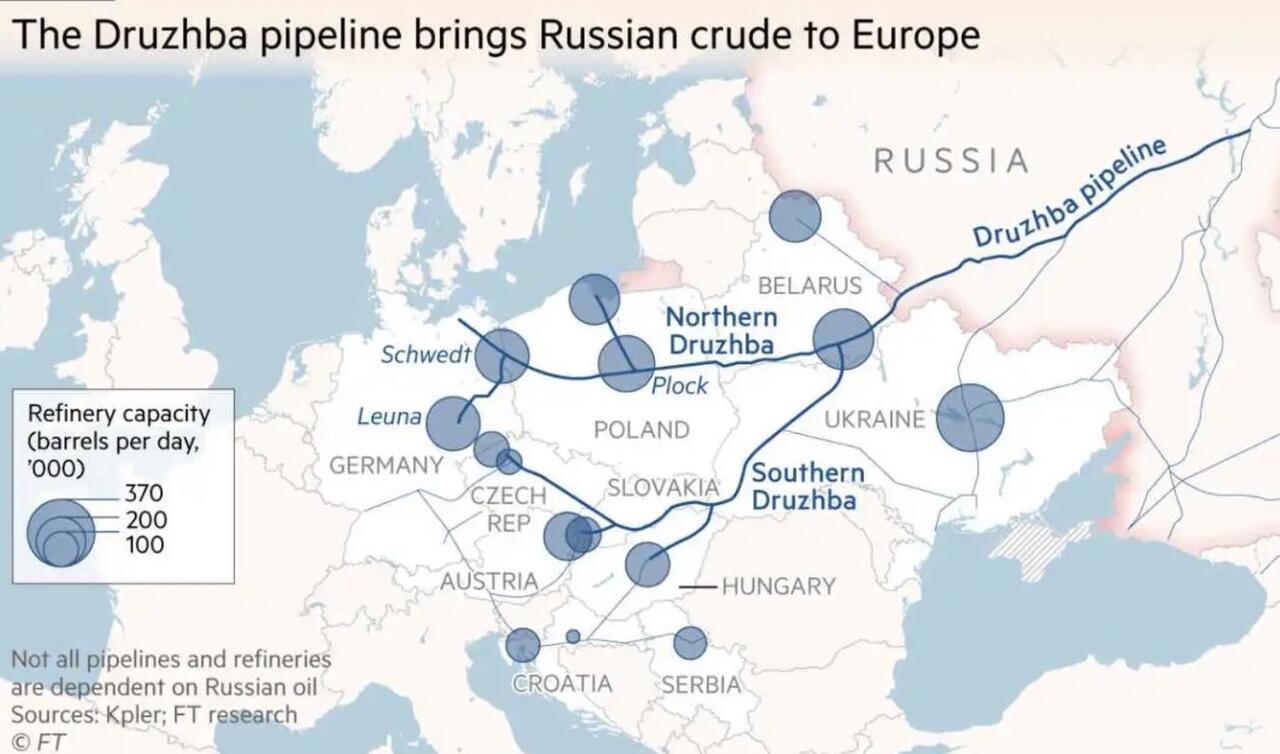

- Polish pipeline operator said on Tuesday evening it detected a leak in the Druzhba pipeline; cause is unknown; leak detected in one of two lines, second line is working as normal. Russia’s Transfneft said it has received notice from Polish operator PERN about the leak at Druzbha; oil pumping towards Poland continues, according to IFX. Polish top official for energy infrastructure said there are no grounds to believe leak in Druzhba pipeline was sabotage, adds leak was probably caused by accidental damage. Germany State of Brandenburg Economy Minister said there was a pressure drop in Druzhba’s main pipeline No.2, according to dpa. Polish pipeline operator PERN said supply to German clients is continuing taking into account technical possibilities; Polish refineries are receiving oil in line with nominations.

- SGH Macro said the understanding in Beijing is that Saudi Crown Prince Mohammad bin Salman assured Russia’s President Vladimir Putin that OPEC+ will cooperate to ensure that global crude oil prices do not fall below USD 80/bbl at least until the end of the military conflict between Russia and Ukraine, even if there is a global economic crisis.”.

- Spot gold is modestly firmer as the upside for the Buck remains capped for now, but the yellow metal remains under its 21DMA (USD 1,673.34/oz).

- LME metals are mixed with copper relatively flat but aluminium is underperforming following a large build in LME warehouse stocks.

Geopolitics

- US President Biden told CNN that he doesn’t think Russian President Putin will use a tactical nuclear weapon.

- US President Biden said the Saudis face consequences after the OPEC+ production cut, according to Bloomberg.

- Two delegations of US congressmen led by Republican Brad Wenstrup and Democrat Seth Moulton have arrived in Taiwan and will stay until Thursday, according to Sputnik.

US Event Calendar

- 07:00: Oct. MBA Mortgage Applications -2.0%, prior -14.2%

- 08:30: Sept. PPI Final Demand MoM, est. 0.2%, prior -0.1%

- Sept. PPI Final Demand YoY, est. 8.4%, prior 8.7%

- Sept. PPI Ex Food, Energy, Trade MoM, est. 0.2%, prior 0.2%

- Sept. PPI Ex Food, Energy, Trade YoY, est. 5.6%, prior 5.6%

- Sept. PPI Ex Food and Energy YoY, est. 7.3%, prior 7.3%

- Sept. PPI Ex Food and Energy MoM, est. 0.3%, prior 0.4%

- 14:00: Sept. FOMC Meeting Minutes

DB’s Jim Reid concludes the overnight wrap

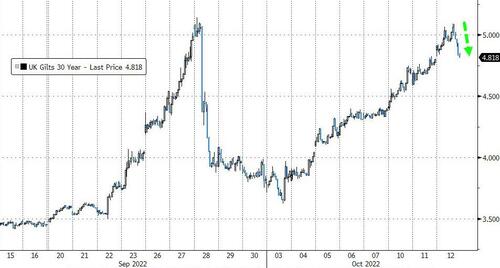

Have we got 3 days to avert some kind of financial crisis here in the UK? That seemed to be the implicit message from the BoE governor Bailey last night in Washington in what were extraordinary comments that shook global markets after what was slowly turning into a pretty positive session up until the remarks less than 90 minutes before the US close.

His exact words were “My message to the funds involved and all the firms is you’ve got three days left now…. You’ve got to get this done.” He was referring to the fact that the APF purchases are slated to end on Friday and that there won’t be any extension. Whether that’s the case or not the extra actions from BoE this week and the stern words from Bailey hint at some big issues still for UK pension funds which will scare the market. Bailey’s language was also a little scary elsewhere saying that he’d been up all night addressing UK market issues and that recent market volatility went beyond their bank stress tests. I suppose the problem with all of this is that if you want pension funds to sort all their issues out in the next three days, he may have made their job a lot harder with the explicit public comments as the market will be really concerned there’s a bigger problem now than they thought beforehand. This is unlikely to help pension funds delever. So we could be in for some major volatility in UK assets for the next few days. The only caveat is that the FT reported at 5am this morning that the BoE have privately communicated to bankers that it would extend the emergency bond buying program if market conditions required it.

The first reaction to Bailey’s comments was felt in Sterling which fell -1.35% from the comments to the close (-0.79% on the day overall) landing at $1.097. Overnight it has rebounded (+0.54%) a bit as I type purely on the FT article I mentioned above. 10yr treasury yields spiked +6.6bps into the close after Bailey having been roughly unchanged immediately before the remarks (after volatile intraday moves) and global equities retreated after their own volatile session. Initially the S&P 500 fell -1.23% after the open, hitting intraday lows that were last matched in November 2020, immediately following Pfizer’s positive Covid trial results, before steadily rallying throughout the day to +0.76%, only to reverse course and nose dive into the close, finishing -0.65% lower following Bailey’s comments. The continued bout of volatility and warnings around broader financial stability saw the Vix index of volatility increase +1.2pts to 33.63pts, its highest levels since immediately before June’s financial conditions easing. Big tech stocks led the way down, with the NASDAQ falling -1.10% to hit its lowest level since July 2020. European stocks may have missed the intraday gyrations and the late US sell-off, but ended up much in the same place, with the STOXX 600 (-0.56%) down for a 5th consecutive session

Back to the UK, earlier, the Bank of England announced they were widening the scope of their daily gilt purchases to include index-linked gilts as well. The move followed some astonishing increases in real yields on Monday, which were so big that they surpassed what we saw during the market turmoil following the mini-budget, with the 10yr index-linked gilt yield rising by an incredible +64.1bps. This widening in the BoE’s intervention is now occurring alongside their existing conventional gilt purchases. 10yr Gilts closed +1.0bps, while real 10yr yields fell back -5.6bps. Nevertheless, nominal 30yr yields increased +10.9bps to 4.78%, and that was before Bailey’s comments after the close.

Elsewhere, today we start the shift back towards inflation with today’s PPI release from the US setting the stage for the all-important CPI reading tomorrow, with those prints having led to some of the biggest selloffs we’ve seen this year. There’s little doubt in markets that the Fed are going to go for another 75bps hike in 3 weeks’ time, particularly after last week’s jobs report, but there’s more uncertainty about the subsequent meetings, and any upside inflation surprises today and tomorrow could put any slowdown in rate hikes even further into the distance. Alternatively softer numbers could help encourage a big rally given bearish risk positioning.

We won’t get the producer price reading until 13:30 London time, but ahead of that we did get the New York Fed’s latest Survey of Consumer Expectations for September, which showed a divergent picture on inflation expectations. At the one-year horizon, expectations fell back to 5.4%, which is their lowest in a year, and some further good news for the Fed. But the longer-term data was somewhat less positive, with three-year expectations ticking back up to 2.9% following three consecutive monthly declines, and five-year expectations advanced to 2.2% following four consecutive monthly declines. Clearly that could just be a blip, but well-anchored inflation expectations have regularly been cited as a reason for the Fed not moving even more aggressively, so any signs that expectations are going in the wrong direction again would raise the prospect of yet more tightening ahead.

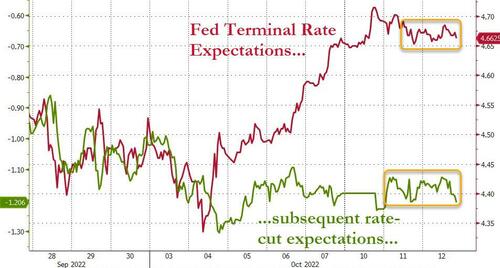

In the meantime, Fed officials continued to strike a hawkish note in their remarks yesterday, with Cleveland Fed President Mester saying that “the larger risks come from tightening too little and allowing very high inflation to persist and become embedded in the economy”. Recall, there’s been a brewing philosophical divergence on the Committee about the risks of over-tightening given the long and variable lags of monetary policy, which should gather more steam once we get through the last two FOMC meetings in 2022, so it was instructive to hear an official come down so starkly on the other side of the balance of risks debate. That backdrop saw futures price in a 75bps hike for November as more likely than at any point to date so far, with +73.8bps priced in by the close.

Elsewhere among central bankers, we heard from ECB Chief Economist Lane as well yesterday, although he didn’t reveal much in the way of policy conclusions to draw from. One line was that he said “the ECB’s Governing Council is fully aware that further ground needs to be covered in the next several meetings to exit from the prevailing highly accommodative level of policy rates”. So a clear signal that more rate hikes are coming over the meetings ahead. Against that backdrop, sovereign bonds in Europe had oscillated between gains and losses throughout the day, in line with the volatility seen across global markets. But by the close yields had mostly fallen across the continent, with those on 10yr bunds (-4.1bps) and OATs (-3.0bps) both falling back. 10yr BTPs rose +4.2bps as some of the previous day’s excitement over possible joint EU issuance to help with the energy crisis faded.

Asian equity markets are sliding again this morning with the Hang Seng (-1.92%) leading losses followed by the Shanghai Composite (-1.22%) and the CSI (-1.19%) as the rising number of Covid-19 cases has prompted Beijing to impose fresh lockdowns and travel restrictions ahead of the 20th Party Congress. Elsewhere, the Nikkei (-0.14%) is slightly weaker with the Kospi (-0.16%) also moving lower as the Bank of Korea (BOK) raised interest rates by a half percentage point to 3%. The statement indicated that it sees upside risks to its August inflation projection for this year of 5.2%, which warrants additional rate hikes. Additionally, it warned of slower growth with the Korean economy expected to grow next year at a slower pace than the August forecast of 2.1%.

Moving ahead, US stock futures are ticking higher with contracts on the S&P 500 (+0.43%) and the NASDAQ 100 (+0.52%) edging higher with US 10yrs -2bps overnight. In FX, the Japanese yen touched a new 24-yr low of 146.23 against the dollar.

Elsewhere yesterday, the IMF released their latest round of economic projections as the IMF/World Bank annual meetings get underway. In terms of the headlines, they left their 2022 global growth forecast unchanged at +3.2%, but their 2023 forecast was downgraded to +2.7% (vs. +2.9% in July). Those reductions were particularly concentrated in the advanced economies, with Germany seeing one of the biggest downgrades as they’re now forecasting a -0.3% contraction for 2023 (vs. +0.8% in July). They also upgraded their global inflation forecasts, and are now projecting that world consumer prices will have risen by +8.8% in 2022 (vs. +8.3% in July) and +6.5% in 2023 (vs. +5.7% in July).

Finally on the data front, the UK unemployment rate fell to 3.5% (vs. 3.6% expected) in the three months to August, which is its lowest level since 1974. In addition, the number of payrolled employees in September was up +69k (vs. +35k expected).

To the day ahead now, and data releases include the US PPI reading for September, along with UK GDP and Euro Area industrial production for August. From central banks, we’ll get the FOMC minutes from the September meeting, and hear from the Fed’s Barr, Kashkari and Bowman, ECB President Lagarde, the ECB’s Knot and De Cos, as well as the BoE’s Pill, Haskel and Mann. Finally, earnings releases include PepsiCo.

AND NOW NEWSQUAWK

US equity futures trade on a firmer footing with the ES back above 3600, GBP outperforms whilst JPY lags – Newsquawk US Market Open

WEDNESDAY, OCT 12, 2022 – 06:41 AM

- European bourses saw a choppy start to the session, but have since titled to the upside; US equity futures trade on a firmer footing with the ES back above 3600

- GBP was volatile but currently stands as the outperformer, DXY is softer but off worst levels, USD/JPY to a fresh 2022 and multi-year best

- BoE said the bank has made it clear from the outset that its temporary and targeted purchases of gilts will end on October 14th

- Polish pipeline operator said it detected a leak in the Druzhba pipeline; Polish top official said there are no grounds to believe it was sabotage

- Looking ahead, US PPI Final Demand, FOMC Minutes, G20 Finance Ministers’ meeting, Astana Summit, Speeches from BoE’s Pill & Mann, ECB’s Lagarde, Fed’s Kashkari, Barr & Bowman Supply from US

View the full premarket movers and news report.

Or why not try Newsquawk’s squawk box free for 7 days?

12th October 2022

- Click here for the Week Ahead preview.

EUROPEAN TRADE

EQUITIES

- European bourses saw a choppy start to the session, but have since titled to the upside as US traders prepare to enter the fray.

- Sectors are mixed with Consumer Products bolstered by luxury names after LVMH earnings, with Tech following whilst Banks and Real Estate lag.

- Stateside, US equity futures trade on a firmer footing with the ES back above 3600 as the index futures attempt to claw back some of the lost ground yesterday.

- Click here for more detail.

FX