by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSE: DOWN $0.40 to $1670.30

SILVER PRICE CLOSE: DOWN $0.02 to $18,97

Access prices: closes

Gold ACCESS CLOSE 1666.90

Silver ACCESS CLOSE: 18.99

New: early yesterday morning//

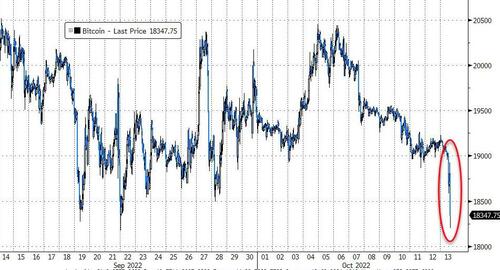

Bitcoin morning price: $18,758 DOWN 400

Bitcoin: afternoon price: $19,365 UP 207.

Platinum price closing UP 3.20 AT $907.50

Palladium price; closing DOWN $35.70 at $2120.55

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD $2291 CDN DOLLARS PER OZ DOWN $22.89 CDN DOLLARS

BRITISH GOLD IN POUNDS: 1470.09 POUNDS PER OZ DOWN 38.18 BRITISH POUNDS PER OZ/

EURO GOLD: 1703.77 EUROS PER OZ// DOWN 21.50 EUROS PER OZ///

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: OCTOBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,670.300000000 USD

INTENT DATE: 10/12/2022 DELIVERY DATE: 10/14/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 1

118 C MACQUARIE FUT 2

323 C HSBC 85

435 H SCOTIA CAPITAL 82

657 C MORGAN STANLEY 7

661 C JP MORGAN 18

800 C MAREX SPEC 1 5

905 C ADM 21

TOTAL: 111 111

MONTH TO DATE: 21,689

JPMORGAN STOPPED 18/111

GOLD: NUMBER OF NOTICES FILED FOR OCT CONTRACT: 111 NOTICES FOR 11,100 OZ or 0.3451 TONNES

total notices so far: 21,689 contracts for 2,168,900 oz (67.4618 tonnes)

SILVER NOTICES: 1 NOTICE(S) FILED FOR 5,000 OZ/

total number of notices filed so far this month 418 : for 2,090,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $.40

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////A DEPOSIT OF 1.16 TONNES INTO THE GLD//

INVENTORY RESTS AT 945.47 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 2 CENTS

AT THE SLV// :/BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A HUGE DEPOSIT OF 4.513 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 482.709 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 2437 CONTRACTS TO 128,060 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE TINY LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.18 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS/HFT WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.18).SPECS CONTINUE TO ADD TO THEIR SHORTFALLS. OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS.

WE MUST HAVE HAD:

I) ZERO SPECULATOR SHORT COVERINGS ////CONTINUED BANKER OI COMEX ADDITIONS /// SOME NEWBIE SPEC SHORT ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.580 MILLION OZ FOLLOWING A 135,000 OZ QUEUE JUMP / // V) GIGANTIC SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: — 26

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT:

TOTAL CONTRACTS for 11 days, total 51,147 contracts: 25.574 million oz OR 2.324MILLION OZ PER DAY. (465 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 25.574 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 25.574 MILLION OZ INITIAL

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2437 DESPITE OUR $0.18 LOSS IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 672 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /STRONG BANKER ADDITIONS // STRONG SHORT ADDITIONS//CONSIDERABLE NEWBIE SPEC LONG ADDITIONS// /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT. OF 1.580 MILLION OZ FOLLOWED BY TODAY’S 135,000 QUEUE JUMP .. WE HAD A GIGANTIC SIZED GAIN OF 3135 OI CONTRACTS ON THE TWO EXCHANGES FOR 15.675 MILLION OZ..

WE HAD 1 NOTICE(S) FILED TODAY FOR 5,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 4378 CONTRACTS TO 435,773 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED — -103 CONTRACTS.

.

THE GOOD SIZED INCREASE IN COMEX OI CAME WITH OUR GAIN IN PRICE OF $4.00//COMEX GOLD TRADING/WEDNESDAY // MINIMAL SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT. AT 66.099 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 100 OZ//NEW STANDING 69.042 TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $4.00 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 6800 OI CONTRACTS 21.11 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2422 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 435.876

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6800 CONTRACTS WITH 4481 CONTRACTS INCREASED AT THE COMEX AND 2422 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 6800 CONTRACTS OR 21.11 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2422) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (4378): TOTAL GAIN IN THE TWO EXCHANGES 6800 CONTRACTS. WE NO DOUBT HAD 1) ZERO SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS///NEWBIE SPEC SHORT ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 66.099 TONNES FOLLOWED BY TODAY’S 100 OZ E.F.P. JUMP TO LONDON///NEW STANDING 69.042 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) FAIR SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT. :

24,748 CONTRACTS OR 2,474,800 OZ OR 76.87 TONNES 11 TRADING DAY(S) AND THUS AVERAGING: 2249 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAY(S) IN TONNES: 76.87 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 76.87/3550 x 100% TONNES 1.95% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 76.87 TONNES INITIAL ( MUCH SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GIGANTIC SIZED 2437 CONTRACT OI TO 128,060 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 672 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 672 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 672 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2463 CONTRACTS AND ADD TO THE 425 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 3109 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 15.545 MILLION OZ

OCCURRED DESPITE OUR LOSS IN PRICE OF $0.18

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 9.15 PTS OR 0.30% //Hang Seng CLOSED DOWN 311.92 OR 1.87% /The Nikkei closed DOWN 159.41PTS OR 0.60% //Australia’s all ordinaires CLOSED DOWN 0.12% /Chinese yuan (ONSHORE) closed DOWN TO 7.1818 //OFFSHORE CHINESE YUAN DOWN 7.1894// /Oil DOWN TO 87.39 dollars per barrel for WTI and BRENT AT 92.71 / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED 4378 CONTRACTS TO 435,773 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS FAIR COMEX INCREASE OCCURRED WITH OUR RISE IN PRICE OF $4.00 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2422 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2422 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :2422 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2422 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 6800 CONTRACTS IN THAT 2422 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI GAIN OF 4378 CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR RISE IN PRICE OF GOLD $4.00//WE HAD SPEC SHORTS ADDING TO THEIR POSITIONS WITH BANKERS TAKING THE OTHER SIDE AS BUYERS OF COMEX GOLD CONTRACTS. WE ALSO HAD SOME ADDITIONAL SPECS GOING LONG DUE TO THE ATTRACTIVE PRICE

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING OCT (69.042),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 69.042 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $4.00) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS (THEY ADDED TO THEIR POSITIONS) AS WE HAD A STRONG SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF6800 CONTRACTS // WE HAVE REGISTERED A STRONG GAIN OF 21.11 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR OCT. (69.042 TONNES)…THIS WAS ACCOMPLISHED WITH A RISE IN PRICE OF $4.00

WE HAD -103 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 6800 CONTRACTS OR 680,000 OZ OR 21.11 TONNES

Estimated gold volume 236,985// fair//

final gold volumes/yesterday 143,607/ poor

INITIAL STANDINGS FOR OCT ’22 COMEX GOLD //OCT 13

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 12,249.576oz JPMorgan Brinks includes 15 kilobars and 366 kilobars |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 111 notice(s) 11100 OZ 0.3452 TONNES |

| No of oz to be served (notices) | 620 contracts 54,100oz 1.5800 TONNES |

| Total monthly oz gold served (contracts) so far this month | 21,689 notices 2,168,900 67.418 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits NIL oz

customer withdrawals:2

i) Out of JPMorgan: 11,767.266 oz (266 kilobars)

ii) out of Brinks: 482.26 0z (15 kilobars)

total: 12,249.576 oz

total in tonnes: 0.3809 tonnes

Adjustments: 0//

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT we have an oi of 619 contracts having LOST 32 contracts . We had 31 contracts

filed on WEDNESDAY, so we LOST ONE TINY contract or an additional 100 oz will NOT stand in this active delivery month of Oct as

this one contract was EFP’d over to London.

November GAINED 0 contracts to stand at 3131

December gained 1550 contracts down to 365,228

We had1111 notice(s) filed today for 11100 oz FOR THE OCT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 111 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 18 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT /2022. contract month,

we take the total number of notices filed so far for the month (21,689) x 100 oz , to which we add the difference between the open interest for the front month of (OCT 619 CONTRACTS) minus the number of notices served upon today 111 x 100 oz per contract equals 2,219,700 OZ OR 69.042 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT contract month:

No of notices filed so far (21,689) x 100 oz+ (619) OI for the front month minus the number of notices served upon today (111} x 100 oz} which equals 2,219,700, oz standing OR 69.045 TONNES in this NON active delivery month of OCTOBER.

TOTAL COMEX GOLD STANDING: 69.042 TONNES (A HUMONGOUS STANDING FOR OCT (GENERALLY THE POOREST DELIVERY MONTHS FOR AN ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,968,238.247 OZ 61.220 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 25,814,729.096 OZ

TOTAL REGISTERED GOLD: 12,315,332.840 OZ (383.06tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 13,499,396.256 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,347,094 OZ (REG GOLD- PLEDGED GOLD) 321.83 tonnes//rapidly declining

END

SILVER/COMEX

OCT 13//INITIAL OCT SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,268,265.540 oz Brinks Loomis Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 250,192.973 oz Delaware |

| No of oz served today (contracts) | 1 CONTRACT(S) 5,000 OZ) |

| No of oz to be served (notices) | 93 contracts (465,000 oz) |

| Total monthly oz silver served (contracts) | 418 contracts 2,090,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) into Delaware: 250,192.973 oz

Total deposits: 250,192.973 oz

JPMorgan has a total silver weight: 160.801million oz/309.404million =52.03% of comex

Comex withdrawals: 3

i)Brinks 377,443.030 oz

ii) Out of Loomis: 585,332.610 oz

iii_ Out of Manfra: 305,489.900 oz

total withdrawals: 1m268,265.540 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 40.082 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 309.404 MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF OCT OI: 94 CONTRACTS HAVING GAINED 7 CONTRACT(S.)

WE HAD 20 NOTICES FILED ON WEDNESDAY SO WE GAINED 27

SILVER CONTRACTS OR AN ADDITIONAL 135,000 OZ WILL STAND FOR OCT.

NOVEMBER LOST 3 CONTRACTS TO STAND AT 397

DECEMBER SAW A GAIN OF 957 CONTRACTS UP TO 104,342

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1 for 5,000 oz

Comex volumes:70,941// est. volume today// good

Comex volume: confirmed yesterday: 62,330 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 418 x 5,000 oz = 2,090,000 oz

to which we add the difference between the open interest for the front month of OCT(94) and the number of notices served upon today 1 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT./2022 contract month: 418 (notices served so far) x 5000 oz + OI for front month of OCT (94) – number of notices served upon today (1) x 5000 oz of silver standing for the OCT contract month equates 2,555,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:56,736// est. volume today// poor

Comex volume: confirmed yesterday: 64,896 contracts ( poor)

END

GLD AND SLV INVENTORY LEVELS

OCT 13/WITH GOLD DOWN $0.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

GLD INVENTORY: 944.31 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

CLOSING INVENTORY 478.196 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

end

Lawrie Williams

END

3.Chris Powell of GATA provides to us very important physical commentaries

Chris Powell’s remarks at the New Orleans conference: a Gold market manipulation update

(Chris Powell)

a must read…

Chris Powell: Gold market manipulation update

Submitted by admin on Wed, 2022-10-12 19:52Section: Daily Dispatches

Illustrations for this presentation can be found here: NOIC-Slides-10-12-2022.pdf

* * *

ILLUSTRATION 1

Remarks by Chris Powell

Secretary/Treasurer, Gold Anti-Trust Action Committee Inc.

New Orleans Investment Conference

Hilton New Orleans Riverside Hotel

Wednesday, October 12, 2022

What a year has passed since we last gathered here.

The money supply in the United States and throughout the world exploded and inflation soared here and abroad.

The gold price in U.S. dollars went down.

Central banks steadily announced their purchases of gold and turned from net sellers to net buyers.

The gold price in U.S. dollars went down.

War in Ukraine pitted the United States and its NATO allies against Russia and upended the energy and food markets.

The price of gold in U.S. dollars went down again.

Russia began threatening to use nuclear weapons in that war.

The price of gold in U.S. dollars continued to fall.

A month ago the world began sinking into economic recession and still the gold price in U.S. dollars went down — until about a week ago, when it began to stabilize.

Many experts have explanations for the counterintuitiveness of the U.S. dollar gold price. We will hear from some of them at this conference. But for more than a decade the dollar gold price has been no stranger to counterintuitiveness. Fortunately during that time the experts have construed nearly everything as a reason for gold to go down.

Well, nearly everything. That is, very few experts have said gold priced in U.S. dollars has gone down because of largely surreptitious government intervention.

Exposing that intervention and complaining about how it has destroyed not just the gold market but ALL markets EVERYWHERE has been the work of the Gold Anti-Trust Action Committee since 1998. We have amassed a huge amount of documentation, displayed at our internet site, GATA.org.

For example, and most contemporary, consider something else that has gone down steadily this year: the gold swaps and loans reported in the monthly statements of account of the Bank for International Settlements, the central bank of the central banks, the broker that gives central banks cover for gold and other transactions they don’t want disclosed.

To potential central bank members, the BIS actually advertises its camouflaging services. Here is a page from a PowerPoint presentation by BIS officials to central bankers at a conference at BIS headquarters in Basel, Switzerland, in 2008.

ILLUSTRATION 2

You can see that interventions in the gold and currency markets are considered major services of the BIS to its members.

In a speech at a BIS conference in 2005, William R. White, then the head of the Monetary and Economic Department of the BIS, said that one of the main purposes of international central bank cooperation was “the provision of international credits and joint efforts to influence asset prices (especially gold and foreign exchange) in circumstances where this might be thought useful.”

That is, rigging the gold and currency markets long has been a primary purpose of the BIS on behalf of its members, who included all the major central banks.

White’s speech is still posted at the BIS internet site, and at GATA’s:

http://www.bis.org/publ/bppdf/bispap27.pdf

http://www.gata.org/files/BIS-WhiteSpeechCentralBankCooperation-June2005.pdf

So the BIS’ meddling with the gold price on behalf of its central bank members is a matter of record. Unfortunately it seems that nobody outside GATA dares to look at the record.

GATA’s consultant on the BIS, Robert Lambourne, examines the BIS’ monthly statements of account very closely. Those statements are formulated carefully to obscure fluctuations in the bank’s gold interventions, represented by gold swaps and leases. But Lambourne does the necessary calculations and has discovered a sharp decline in BIS gold swaps and leases this year. This is the trend of BIS gold interventions since January.

ILLUSTRATION 3

The annual report of the BIS, published in June for the year ending in March, confirmed the accuracy of Lambourne’s calculations of bank’s gold swaps. Lambourne had estimated 360 tonnes for March. The BIS reported 358.

ILLUSTRATION 4

This decline in the gold swaps at the BIS seems to correspond with the implementation in Europe and the United Kingdom of the “Basel III” rules requiring bullion banks to hold full collateral for their gold trading, rules that the London Bullion Market Association and World Gold Council warned would wreck the gold market — or at least wreck the part of the gold market most supported by the LBMA and the gold council — that is, the dominance of gold derivatives, “paper gold,” over physical gold.

“Paper gold” has been the main mechanism of gold price suppression in recent years — the creation of vast amounts of imaginary gold, unbacked gold claims and credits at bullion banks, substituting for the possession by investors of real metal. These claims and credits are backstopped as necessary by central bank lending and swapping of official gold reserves.

That is why central banks long have refused to disclose their gold lending.

ILLUSTRATION 5

As was acknowledged by the secret March 1999 report of the staff of the International Monetary Fund, candor in official gold reserve reporting would explode the “paper gold” system.

The decline in the BIS swaps and leases implies that the bank this year has been winding down the paper gold business of its member central banks.

It’s a fair suspicion but try asking the BIS what it does in the gold market, for whom, and why. If you get an answer, please let me know, for you’ll be the first one outside of central banking to get an answer.

Since we last met here other crucial questions about U.S. government intervention in the gold market have continued to be refused answers.

ILLUSTRATION 6

In 2021 U.S. Representative Alex X. Mooney, R-West Virginia, wrote to Treasury Secretary Janet Yellen to ask a few questions about the disposition of the U.S. gold reserve. A deputy of Yellen’s replied, refusing to answer most of the questions, including why Treasury gold is stored at the Federal Reserve Bank of New York.

The U.S. Commodity Futures Trading Commission continued to refuse to answer a question posed by both Mooney and GATA. That is, does the CFTC have jurisdiction over manipulative trading in the futures markets that is undertaken by or at the behest of the U.S. government?

This is a simple question about the commission’s jurisdiction. That the commission refuses to answer might give even Kitco News a hint about what really has been going on in the gold market – if Kitco News ever was open to hints.

But in 2001 at a hearing in U.S. District Court in Boston on GATA consultant Reginald Howe’s lawsuit against the U.S. Treasury Department, Federal Reserve, and several bullion banks, an assistant U.S. attorney declared that the U.S. government is fully authorized by the laws establishing the Federal Reserve and the Treasury Department’s Exchange Stabilization Fund to rig the gold market exactly as Howe’s lawsuit complained:

https://www.gata.org/node/4211

What else has happened in the last year to indicate both open and surreptitious involvement in the gold market by central banks?

ILLUSTRATION 7

— In March, as Russia began to be assaulted by Western financial sanctions in response to its invasion of Ukraine, the Bank of Russia briefly put a floor under the Russian domestic gold price, signifying that the bank considered the metal to be money and a strategic resource:

ILLUSTRATION 8

— In July the Russian government announced plans to create a gold exchange in Moscow using what it called a “‘Moscow World Standard” for gold to compete with the London Bullion Market Association. Indeed, according to Russian news reports, the goal of the Moscow World Standard exchange is to “‘break the monopoly” of the LBMA and facilitate the development of the gold industry outside the LBMA’s reach. Russia knows that gold is a world reserve currency, a competitor to the U.S. dollar. That is, gold is international money.

https://www.gata.org/node/22137

ILLUSTRATION 9

— In January Pam and Russ Martens of WallStreetOnParade.com, quoting a new book about the Federal Reserve, “The Lords of Easy Money: How the Federal Reserve Broke the American Economy” by Christopher Leonard, reported that the Federal Reserve Bank of New York’s trading room in New York City isn’t the bank’s only trading room. That is, the New York Fed also has a trading room in Chicago near the Chicago Mercantile Exchange. The Chicago Mercantile Exchange operates most commodity futures trading in the United States.

Of course no respectable financial journalist or market analyst ever asks the New York Fed what it is trading in either trading room, or why:

https://gata.org/node/21690

In June Wall Street on Parade reported that JPMorgan and Citibank hold 90% of all gold and other monetary metals derivatives held by U.S. banks. As far as I can tell, no respectable financial journalist or market analyst has wondered aloud why such a concentrated position in a sensitive financial market would be allowed if it was not actually a U.S. government position, with the two banks functioning as the government’s brokers.

But then as far as I can tell no respectable financial journalist or market analyst has ever explored the implications of the Central Bank Incentive Program offered by CME Group, the futures exchange operator. With the Central Bank Incentive Program, governments and central banks can receive volume trading discounts for secretly trading all major futures contracts in the United States – not just financial futures — provided that those governments and central banks use brokers approved by CME Group.

ILLUSTRATION 10

In July, after covering the trial of the JPMorgan gold and silver traders who were charged with spoofing the monetary metals markets and manipulating prices, Bloomberg News reported that documents submitted as evidence showed that while the bank’s traders were spoofing the monetary metals markets, the bank was vaulting and probably trading gold for at least 10 central banks. That is, JPMorgan, which in 2020 was fined $920 million for manipulating the gold and silver markets, was simultaneously working for at least 10 central banks. Were the JPMorgan traders ever front-running central bank transactions? We don’t know, but central banks wouldn’t be vaulting gold with JPMorgan if they weren’t also surreptitiously intervening in the gold market with JPMorgan providing cover as their broker:

In the last year banks that have been fined millions of dollars or paid millions in civil lawsuit settlements for gold and silver market rigging include not just JPMorgan but Barclays, Scotiabank, and Societe Generale, as well as the London Gold Market Fixing Ltd.

I would need another hour to detail these market-rigging cases. But strangely they never come up in expert analysis of the gold and silver markets and the often counterintuitive direction of prices.

My points are simple.

First — All the recent evidence fits perfectly with all the older documentation of U.S. government policy and Western government assistance in suppressing the price of gold, the former world reserve currency, to sustain the current world reserve currency, the U.S. dollar.

Second — Gold price suppression is no “‘conspiracy theory” but longstanding government POLICY. That is, gold price suppression is “‘conspiracy FACT.” Indeed, whenever government operates in secret to develop and implement a course of action, as it often does, government is conspiracy itself.

Third — There can be no meaningful analysis of the monetary metals and their markets without accounting for government intervention.

And fourth — The biggest advantages enjoyed by government’s monetary metals price suppression policy are the indifference and cowardice of financial news organizations and the monetary metals mining industry itself.

Government intervention against the monetary metals may diminish as the supply of real metal becomes tighter, or the intervention may change direction. That is, governments may decide to push monetary metals prices upward to devalue their currencies and debts and to reliquefy themselves, as they have done occasionally throughout history.

Such speculation has been offered by the U.S. economists Paul Brodsky and Lee Quaintance —

https://www.gata.org/node/11373

— and by the Scottish economist Peter Millar:

https://www.gata.org/node/4843

In any case, gold is the secret knowledge of the financial universe, a powerful mechanism for controlling the currency markets, a powerful weapon of imperialism, and an equally powerful defense against imperialism.

ILLUSTRATION 11

The U.S. government knows this very well. If you doubt it, read the transcript of the conversation between Secretary of State Henry Kissinger and Assistant Undersecretary of State Thomas O. Enders at the State Department on April 25, 1974. The transcript is posted at the internet site of the State Department historian —

https://history.state.gov/historicaldocuments/frus1969-76v31/d63

— and at GATA’s own internet site:

http://www.gata.org/files/StateDeptKissingerEnders1974.txt

Kissinger and Enders discuss what they consider the U.S. policy imperative of preventing the western European countries from bringing gold back into the international financial system. Enders explains that the Europeans collectively have more gold reserves than the United States and that gold is “‘the reserve-creating instrument,” the instrument of creating money through gold revaluation. Enders says that whoever controls the most gold can revalue it from time to time to create money and thereby change all financial valuations in the world.

Kissinger agrees that the Europeans must be prevented from remonetizing gold, adding that if the Europeans don’t back down, “We’ll bust them.”

Yes, the meeting in Kissinger’s office was conspiracy – conspiracy fact. The conspiracy continues.

But gold market rigging can keep working only as long as it remains largely a secret for fooling other governments and investors into accepting gold derivatives, “paper gold.” I hope this conference can help bust the secret open.

ILLUSTRATION 12

For more history and documentation of gold price suppression policy and information about GATA, please visit our internet site, GATA.org. I’ll be glad to try to answer questions e-mailed to me at CPowell@GATA.org.

Thanks for your kind attentioN

Chris Powell/GATA Secretary

end

Stuart Englert interviewed about gold and silver price suppression

(GATA/Englert/Johnson)

‘Rigged’ author Stuart Englert interviewed about gold and silver price suppression

Submitted by admin on Wed, 2022-10-12 14:09Section: Daily Dispatches

1:08p CT Wednesday, October 12, 2022

Dear Friend of GATA and Gold (and Silver):

Stuart Englert, author of “Rigged: Exposing the Largest Financial Fraud in History,” was interviewed this week by Elijah Johnson for Finance and Liberty, discussing central banking’s use of derivatives to suppress gold and silver prices. Englert also addresses the possible end of price suppression.

The interview is 25 minutes long and can be viewed at YouTube here:

See below for information on purchasing Englert’s book in a way that will support GATA.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Kranzler shows that market indicators suggest a rally for monetary metals

(Dave Kranzler)

Dave Kranzler: The market indicators that suggest a rally for monetary metals

Submitted by admin on Wed, 2022-10-12 11:46Section: Daily Dispatches

10:46a CT Wednesday, October 12, 2022

Dear Friend of GATA and Gold (and Silver):

Writing at Kinesis Money, Dave Kranzler of Investment Research Dynamics in Denver cites technical data suggesting that the monetary metals are oversold and getting scarce and close to a rally in price. Of course the government-underwritten creation of vast supplies of “paper” gold and silver has kept the metals oversold for many years, and any technical analysis of manipulated markets must be viewed with some skepticism. But Kranzler writes that the gold-silver price ratio has served as a reliable indicator before.

His analysis is headlined “Market Indicators That Suggest A Precious Metals Rally May Be Imminent” and it’s posted at Kinesis Money here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

4. OTHER PHYSICAL SILVER/GOLD

5.OTHER COMMODITIES:

end

COMMODITIES IN GENERAL/

END

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.1818

OFFSHORE YUAN: 7.1894

SHANGHAI CLOSED DOWN 9.15 PTS OR 0.30%

HANG SENG CLOSED DOWN 311.92 OR 1.87%

2. Nikkei closed DOWN 159.41 PTS OR 0.60%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UPN TO 112.63/Euro RISES TO 0.97470

3b Japan 10 YR bond yield: FALLS TO. +.243/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 146.73/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.238%***/Italian 10 Yr bond yield FALLS to 4.60%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.40%…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.813//

3j Gold at $1677.70//silver at: 19.20 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND94/100 roubles/dollar; ROUBLE AT 63.47//

3m oil into the 87 dollar handle for WTI and 92 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 146.73DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9972– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9717well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

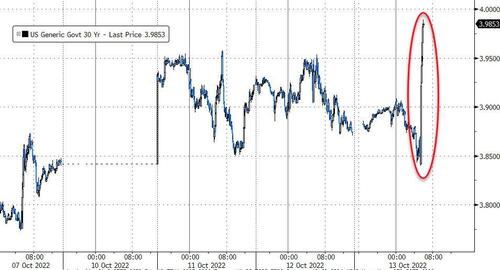

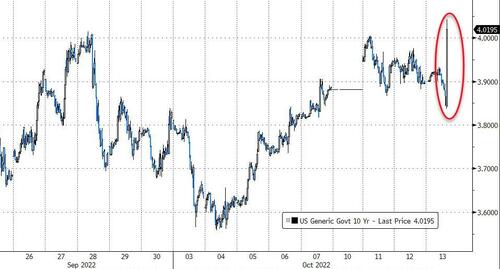

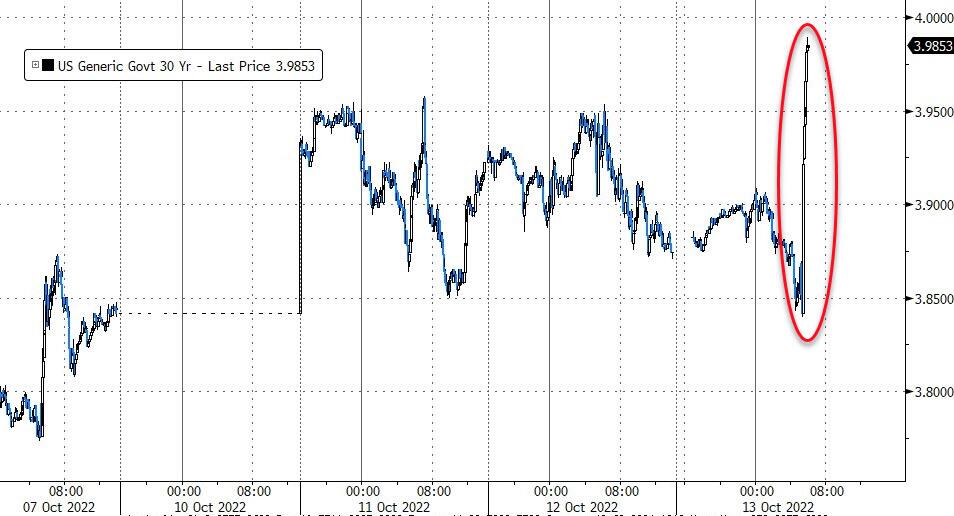

USA 10 YR BOND YIELD: 3.866 DOWN 4 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.856 DOWN 3 BASIS PTS//(USA 30 YR INVERTED TO THE USA 10)

USA DOLLAR VS TURKISH LIRA: 18,59…GETTTING DANGEROUS

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

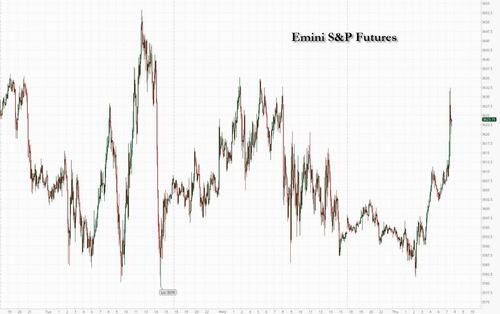

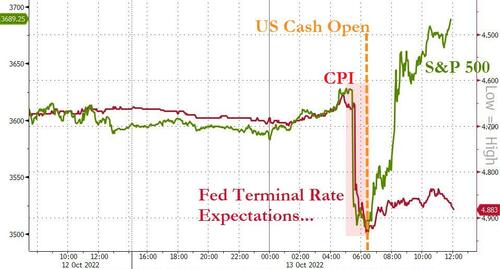

Futures Rip Higher Amid Reports Of Truss Mini Budget “U-Turn” As CPI Looms

THURSDAY, OCT 13, 2022 – 08:04 AM

US equity futures traded heavy for much of the overnight session ahead of the much-anticipated (and gloomy, having hammered stocks on 7 of 9 CPI days so far in 2022) inflation data at 830am ET (full preview here), even as gilt yields suspiciously slumped overnight as if someone was aware of some non-public news, before futures ripped sharply higher around 730am ET when first SkyNews…

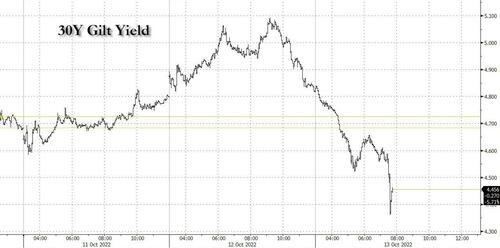

… and then Bloomberg reported that UK’s officials were likely to blink first in their showdown with the Bank of England (which recall is set to end its temporary bond buying tomorrow) and were discussing how they can back down from Prime Minister Liz Truss’s plans for a massive unfunded package of tax cuts. And while the officials are drafting options for Truss but no final decision has been taken and they are waiting for Chancellor of the Exchequer Kwasi Kwarteng to return to London from Washington, where he has been attending meetings of the International Monetary Fund, the person said, asking not to be identified commenting on private discussions. Meanwhile, UK long-end bonds surge in yield as the end of the BOE’s bond purchases intervention approaches.

And despite conflicting reports from other reporters such as the Guardian’s political editor Pippa Crerar reporting that “No 10 rules out further changes to the mini-budget despite pressure from Tory MPs saying “the position has not changed””…

… the confusion was enough to spark some serious short covering across the risk complex which pushed futures more than 1% higher…

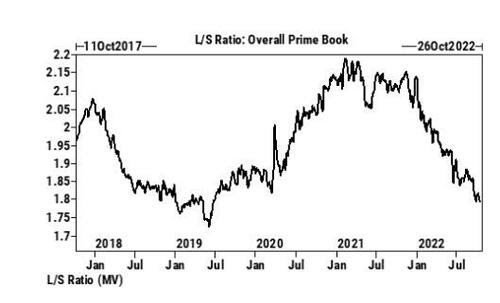

… because, as we noted earlier today, hedge fund positioning ahead of the CPI report is the lowest in 5 years!

The S&P index tumbled to its lowest since November 2020 yesterday, as concerns mounted about the impact of hawkish Fed policy, especially on rate-sensitive sectors such as semiconductors. Europe’s Stoxx 600 gauge steadied, while on currency markets, the dollar slumped as cable surged on hopes that Truss would U-turn and the BOE would go back to doing QT.

Among notable moves in premarket trading, US-listed Macau casino stocks fell amid concerns around the impact from China’s Covid Zero strategy, after the Communist Party’s People’s Daily newspaper ran a series of commentaries this week touting the benefits of the policy. Comcast Corp. and Altice USA Inc. rose after Citigroup Inc. analysts upgraded the cable company stocks given their ability to generate annual cash flow. Here are other notable premarket movers:

- American Express (AXP US) declines 0.9% in US premarket trading, as Citi downgraded the stock along with shares of SLM Corp. (SLM US) and Velocity Financial (VEL US) amid likely “rather large” EPS impact even from mild US recession as credit losses build.

- Applied Materials (AMAT US) falls as much as 1.3% in premarket trading after the chip- equipment maker slashed its earnings forecast as the semiconductor industry reacts to the Biden administration’s new restrictions on doing business with China.

- Chip stocks are in focus after Applied Materials cut its forecast. Taiwan Semiconductor Manufacturing Co., meanwhile, lowered its capital spending target while setting its 4Q gross-margin target above expectations. Watch KLA (KLAC US), Lam Research (LRCX US), Qualcomm (QCOM US), Nvidia (NVDA US), AMD (AMD US)

- US-listed Macau casino stocks fall in premarket trading amid concerns around the impact from China’s Covid Zero strategy, after the Communist Party’s People’s Daily newspaper ran a series of commentaries this week touting the benefits of the policy.

- Wynn Resorts (WYNN US) -2.2%, Las Vegas Sands (LVS US) -1.4%, MGM Resorts (MGM US) -2.2%

- Keep an eye on Owens & Minor (OMI US) stock as it was downgraded to neutral at Citi following the medical and surgical supplier’s “disappointing” third-quarter results on Wednesday. Analyst Daniel Grosslight said Wednesday’s 35% selloff seemed “punitive,” but was not “wholly unwarranted.”

- QuidelOrtho (QDEL US) jumped 9% in extended trading on Wednesday after the health-care services company reported better-than-expected preliminary revenue for the third quarter, thanks to higher Covid-19 testing revenue.

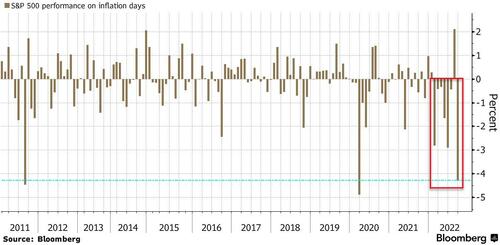

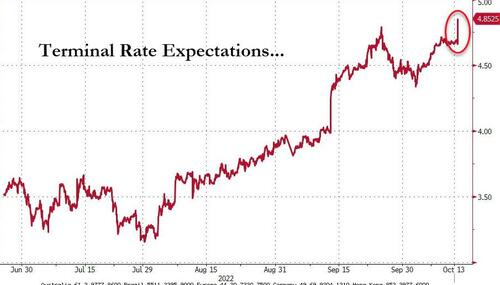

Away from the US rollercoaster, the September reading of the consumer price index, due at 8:30 a.m. today, is expected to decelerate to an 8.1% annual pace amid a decline in gasoline prices. However, the so-called core figure, which excludes food and energy, is projected to have returned to a four-decade high. With investors already worried that underlying strength in the economy will prompt the Fed to keep aggressively raising rates, strategists have warned that hotter-than-expected inflation data could firm up bets of another large rate hike next month and fuel further stock-market declines. The index is already down about 25% so far this year and is in a bear market.

“I don’t think it’s quite time to buy the dip right now,” Oliver Kettlewell, head of fixed income and global portfolios at Mashreq Capital, said on Bloomberg TV. “You need to see data bottoming first and I don’t think the Fed will pivot anytime soon. There is more weakness in the stock markets to come. I don’t think it will fall 40-50%, but it certainly looks like it will get weaker from here.”

The third-quarter company earnings season also kicks off tomorrow and the key question for investors is whether profit margins remained resilient amid surging costs. Although analysts have downgraded estimates in recent weeks, some strategists have warned that the cuts don’t yet reflect the bleaker outlook for economic growth.

In Europe, travel, energy and banks are the strongest performing sectors. Euro Stoxx 50 rises 0.4%. FTSE MIB outperforms peers, adding 1%, FTSE 100 lags, adding 0.2%. Here are the biggest movers:

- Norsk Hydro shares gain as much as 8% after people familiar with the matter said the Biden administration is considering a ban on Russian aluminum supplies.

- Entain rises as much as 4.5% following its third-quarter trading update, with some analysts highlighting rising market share in the US and benefits from upcoming sporting events such as the FIFA World Cup.

- UK domestic stocks gain as government bonds bounce back and the pound rises. British assets have been volatile as the Friday deadline for Bank of England’s emergency bond-buying program looms. Lloyds rises as much as 3.7% while Barclays gained as much as 1.8%.

- Zotefoams shares surge as much as 30% after the polyethylene foam manufacturer said it expects earnings to be significantly ahead of market expectations. Peel Hunt said positive trends in key end markets makes them confident in the near term and future.

- ASML shares fall as much as 3.2% after peer Applied Materials slashed its 4Q sales forecast, citing new US export control rules. Meanwhile, top customer TSMC reduced its 2022 capex target by about 10% amid a collapse in global chip demand.

- Shares of Banca Monte dei Paschi drop as much as 20%, to a record low, after the Italian lender set the terms of its rights offer at a discount to the theoretical ex-rights price.

- Aroundtown falls as much as 7.9% after Citi downgrades the stock to neutral and opens a negative catalyst watch on the real estate company as it prepares “for the worst.”

Earlier in the session, Asian equities fell for the fifth straight session as caution prevailed ahead of key US inflation data due later Thursday. The MSCI Asia Pacific Index slid as much as 1%, with consumer discretionary and communication services shares falling the most. Chinese tech shares plunged for a sixth day, the longest streak in almost a year, dragging down Hong Kong’s benchmark. Stocks in Japan and South Korea were also down. Chinese shares lost momentum amid a pick-up in Covid cases, after staging a strong intraday rebound in the previous session. Investors also monitored developments ahead of the upcoming Communist Party congress, which may introduce further policies to shore up growth.

A hot US consumer price index reading may spur another outsized interest-rate hike by the Federal Reserve at its next meeting. Minutes released Wednesday from the last meeting suggested some officials considered reducing the pace of rate hikes, but overall market sentiment remains jittery. Fed Officials Commit to Restrictive Rates But Calibration Needed The main MSCI Asian stock gauge is trading around its lowest level since April 2020, having fallen almost 30% this year. The region’s stocks are “pricing in low expectations and limited investor appetite, after significant earnings and price underperformance as an asset class over the last decade,” said Sundeep Bihani, a portfolio manager at Eastspring Investments. But “a rising rate cycle, delayed Covid-19 re-opening versus the West and cash-rich balance sheets provide a good pathway to grow out of this underperformance,” he added.

Japanese stocks fell for a fourth day, dragged by telecoms and services providers, ahead of anxiously awaited US inflation data due later Thursday. The Topix fell 0.8% to close at 1,854.61, while the Nikkei declined 0.6% to 26,237.42. Daikin Industries Ltd. contributed the most to the Topix decline, decreasing 2.9%. Out of 2,167 stocks in the index, 381 rose and 1,725 fell, while 61 were unchanged.

Australian stocks, meanwhile, were steady ahead of the CPI report. The S&P/ASX 200 index closed 0.1% lower at 6,642.60 ahead of the US inflation data due later Thursday. Gains in financial shares were partly offset by losses in miners as gold price retreated. Qantas Airways was the best performer after the airline returned to profit following a streak of five consecutive half-yearly losses. Nib dropped after announcing a share placement. In New Zealand, the S&P/NZX 50 index fell 0.5% to 10,817.48.

In FX, Bloomberg dollar spot index falls 0.1%. CHF and JPY are the weakest performers in G-10 FX, NOK and GBP outperform. Pound reclaims $1.11.

In rates, treasuries were mixed after erasing declines, with 10-year note futures near Wednesday’s high ahead of the key CPI data at 8:30am New York time. US yields in belly of curve are richer by 1bp-2bp, steepening 5s30s spread; 10-year erased a 3.7bp increase, is near flat at 3.89% with gilts in the sector richer by 18bp. Sharp bull-flattening in gilts drove earlier price action; 30-year UK yields fall some 29bps to 4.53% while 10-year declines 20bps to 4.22%. Bunds 10-year yield -3.7bps to 2.27% and USTs 10-year yield is little changed. After CPI, focal point of US session is 30-year bond auction at 1pm. This week’s Treasury auction cycle concludes with $18b 30-year bond reopening; its 3- and 10-year note sales tailed.

In commodities, WTI trades within Wednesday’s range at near $87.33. Like OPEC, the IEA Monthly Oil Market Report lowered 2022 oil demand growth outlook by 60k BPD to 1.9mln BPD, 2023 cut by 470k BPD to 1.7mln BPD. World oil demand will contract by 340k BPD Y/Y in Q4. Spot gold gains traction as the Dollar declines ahead of US CPI, with the yellow metal back above its 21 DMA (1,672.50/oz). Base metals are firmer across the board amid the Dollar’s recent decline alongside the gains across stocks, with 3M copper back above USD 7,500/t, whilst LME aluminium outperforms.

Bitcoin tumbled again, sliding to $18,760 while ethereum dropped to a session low of $1,260.

To the day ahead now, and the main data highlight will be the US CPI release for September. Otherwise from central banks, we’ll hear from the ECB’s Nagel and the BoE’s Mann.

Market Snapshot

- S&P 500 futures up 0.5% to 3,605.25

- STOXX Europe 600 down 0.3% to 384.73

- MXAP down 1.0% to 136.16

- MXAPJ down 1.1% to 440.03

- Nikkei down 0.6% to 26,237.42

- Topix down 0.8% to 1,854.61

- Hang Seng Index down 1.9% to 16,389.11

- Shanghai Composite down 0.3% to 3,016.36

- Sensex down 0.7% to 57,242.19

- Australia S&P/ASX 200 little changed at 6,642.61

- Kospi down 1.8% to 2,162.87

- German 10Y yield little changed at 2.31%

- Euro little changed at $0.9705

- Brent Futures up 1.0% to $93.35/bbl

- Gold spot up 0.0% to $1,673.32

- U.S. Dollar Index little changed at 113.28

Top Overnight News from Bloomberg

- Chancellor of the Exchequer Kwasi Kwarteng said the Bank of England will be responsible if UK markets suffer renewed volatility after its bond-buying program ends on Friday

- UK pension funds are dumping assets to meet margin calls as the BOE confirmed it will end emergency bond buying, and the reverberations are being felt everywhere from Sydney to Frankfurt and New York

- Sweden’s inflation rate reached a three- decade high last month, driven by electricity prices and the weakness of the country’s currency, keeping alive bets that the central bank could opt for faster rate hikes than its current path suggests

- Yen traders are readying for another volatile session Thursday with the release of key US inflation figures — data which sent the Japanese currency tumbling 2% in a matter of minutes last month on its path toward intervention

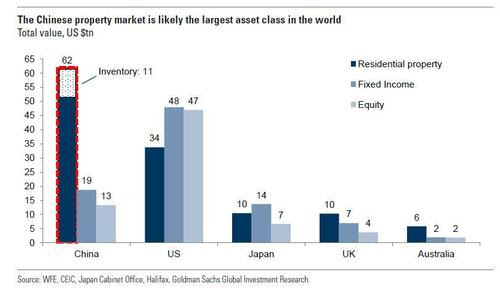

- A Chinese developer with state backing for domestic funding has defaulted on a convertible bond and warned it may face a similar fate on offshore debt, fueling concern about Beijing’s ability to contain a broader property debt crisis

- European natural gas jumped as worries over major facilities in Norway added to supply risks from Russia. Benchmark futures rose as much as 9.2%, after earlier swinging between gains and losses. Norway’s Nyhamna gas project is being evacuated, Dagens Naeringsliv reported

A more detailed global summary of global markets courtesy of Newsquawk

European bourses saw a choppy start to the session but have since been trending higher despite a lack of fresh fundamental drivers. Sectors are now mostly firmer, although tech remains the laggard after TSMC cut its capex guidance and flagged a decline in overall chip industry next year. Stateside, futures have been moving in tandem with their European counterparts, whilst the tech-laden NQ lags vs its peers.

Top European News

- ECB’s Wunsch said it is better to start QT sooner than later, via a pre-recorded CNBC interview.

- EDF Working Council said in the event of a normal or very cold winter, EDF will be forced to take some users off the electricity grid; capacities will not suffice.

- Goldman Analyst Sees UK Property Prices Falling 20% on Rate Rise

- NATO Countries Back German Plan for European Anti-Missile Shield

- Monte Paschi Sets Terms on Rights Offer as Banks Back Deal

Asia stocks traded cautiously following the soft handover from Wall Street where markets ended the session marginally lower after hot PPI data and mixed FOMC Minutes which spurred a short-lived dovish reaction. ASX 200 was kept afloat by outperformance in its top-weighted financials sector and as earnings optimism provided a tailwind with Qantas shares flying high on expectations for a return to profit for the current 6-month period. Nikkei 225 was lacklustre following recent currency weakness and firm PPI data which climbed to a 5-month high. KOSPI underperformed after North Korean leader Kim guided a test firing of long-range strategic cruise missiles which hit a target 2,000km away and are capable of carrying nuclear weapons. Hang Seng and Shanghai Comp. were both subdued as China continued to advocate the strict zero-COVID approach with a Foreign Ministry spokesperson noting that China needs COVID security to achieve economic growth, although downside in the mainland was contained amid support for the property industry with China local governments to purchase houses as stimulus to help developers.

Top Asian News

- China Semiconductor Industry Association said it opposes the US Commerce Department’s export control regulations and hopes the US government can correct wrong practices in a timely manner, while it was separately reported that TSMC (2330 TT) received a 1-year US licence for China chip expansion.

- TSMC (2330 TT/TSM) Q3 2022 (TWD): Net profit 280.9bln (exp. 265.64bln), Gross margin 60.4% (exp. 58.9%), and said the Co. faces challenges from rising inflationary costs in 2023; 2022 Capex seen around USD 36bln (vs prev. guidance of USD 40-44bln); sees Q4 business around flat; not considering share buyback

- Samsung (005930 KS) has been granted a 1yr exemption from new US restrictions that block exports of advanced chips and related equipment to China, according to WSJ sources.

- Chinese Health Official said China will continue to strengthen COVID prevention and control, will resolutely guard against large-scale outbreaks, Reuters.

- Chinese local governments are to purchase houses as stimulus to support developers, according to China Securities Times.

- Japanese Finance Minister Suzuki said excess FX volatility and disorderly moves can hurt the economy and financial stability, while he told the G20 that Japan is deeply worried about recent sharp FX volatility and explained that recent intervention was prompted by excess moves by speculators. Furthermore, Suzuki said they cannot tolerate excess FX moves by speculators and will take decisive action on speculative FX moves in which they are focused on FX volatility rather than the yen level regarding intervention, according to Reuters.

FX

- DXY declined under 113.00 ahead of the US CPI metric, although likely as a function of GBP strength throughout the European morning.

- EUR benefits from the pullback in the Buck, with EUR/USD back above 0.9700.

- Antipodeans are also faring well alongside the improved risk tone across markets.

- USD/CNH tested 7.2000 to the upside, whilst China continues with its zero-COVID policy ahead of the CCP National Congress.

Fixed Income

- US Treasuries are still observing some caution before potentially key CPI data, but EU bonds are flying just a day after diving to new cycle lows.

- UK debt is leading the mainstream recovery whilst there is chat in UK markets about another possible fiscal U-turn and/or the BoE relenting on buy-backs to offer further assistance beyond tomorrow, albeit all speculation at this stage.

Commodities

- WTI and Brent front-month futures are modestly firmer intraday but off best levels after settling lower yesterday.

- IEA Monthly Oil Market Report: lowers 2022 oil demand growth outlook by 60k BPD to 1.9mln BPD, 2023 cut by 470k BPD to 1.7mln BPD. World oil demand will contract by 340k BPD Y/Y in Q4.

- Spot gold gains traction as the Dollar declines ahead of US CPI, with the yellow metal back above its 21 DMA (1,672.50/oz).

- Base metals are firmer across the board amid the Dollar’s recent decline alongside the gains across stocks, with 3M copper back above USD 7,500/t, whilst LME aluminium outperforms

Geopolitics

- Sites in Ukraine’s capital of Kyiv were targeted by shelling early today, according to the administration in Kyiv cited by Sky News Arabia. Furthermore, Ukrainian President Zelensky’s office later said that a critical infrastructure facility was hit by drone strikes in the Kyiv region, according to Reuters.

- Ukraine President Zelenskiy said cannot have diplomacy with Russia today and cannot respect leaders who are killing and not respecting international law.

- Saudi Arabia fully rejected statements criticising the kingdom after the OPEC+ output cut decision, while it said that statements critical of the kingdom are not based on facts and set the OPEC+ decision outside its economic context.

- US officials are concerned the Russian oil price cap will fail as a result of the OPEC+ cut, according to Bloomberg.

- North Korean leader Kim guided a test firing of long-range strategic cruise missiles which hit a target 2,000km away and are capable of carrying nuclear weapons, while North Korean leader Kim said focus should be on developing nuclear forces, according to Yonhap and KCNA.

- North Korea reportedly cancelled a meeting with the EU diplomatic service, while the reason was unclear but followed two recent statements from Brussels that may have impacted DPRK decision-making, according to NK News citing sources.

- Japan’s Defence Minister said North Korea has likely achieved the capability of mounting a nuclear warhead on a ballistic missile that could reach Japan, according to Reuters.

- US FCC is set to ban all US sales of new Huawei and ZTE equipment as well as some sales of video surveillance equipment from three other Chinese firms amid national security concerns, according to Axios citing sources.

US Event Calendar

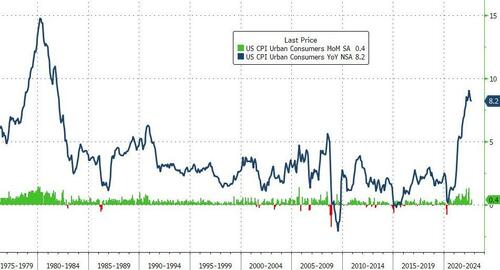

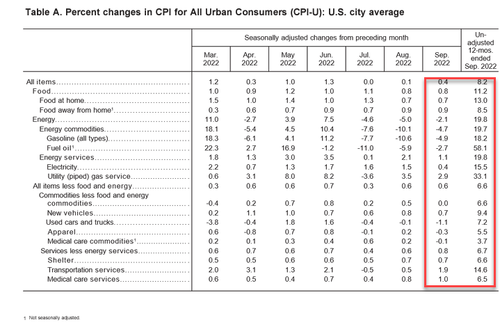

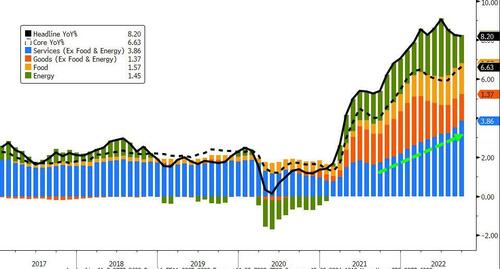

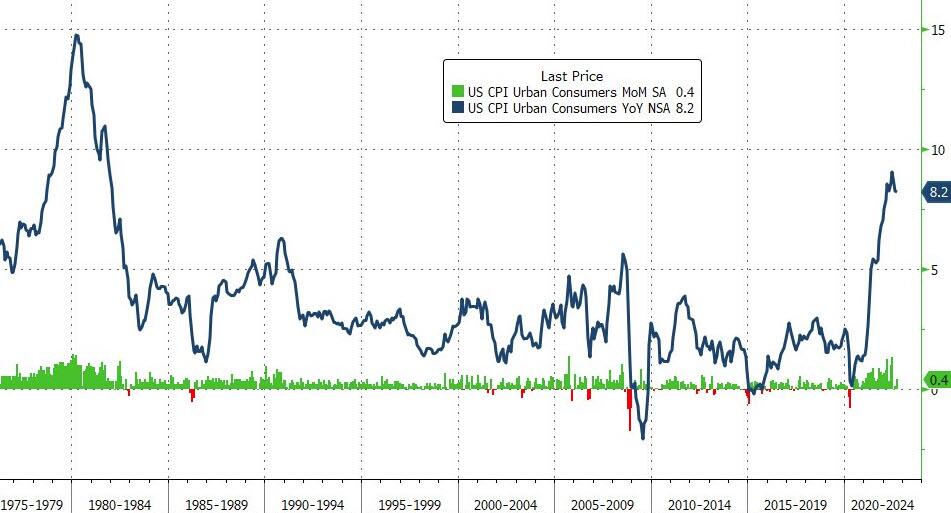

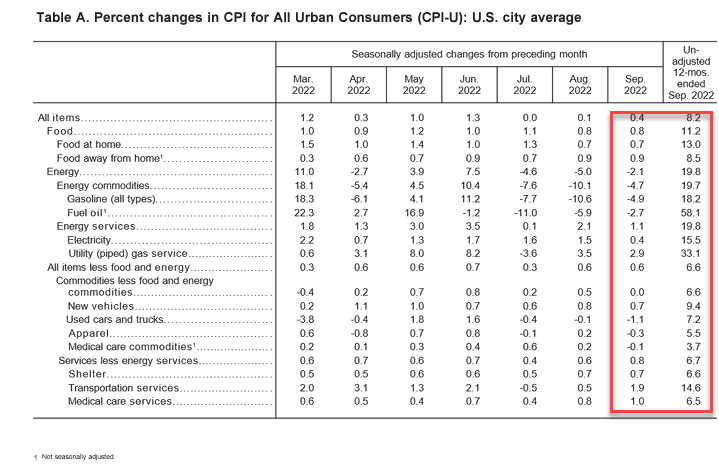

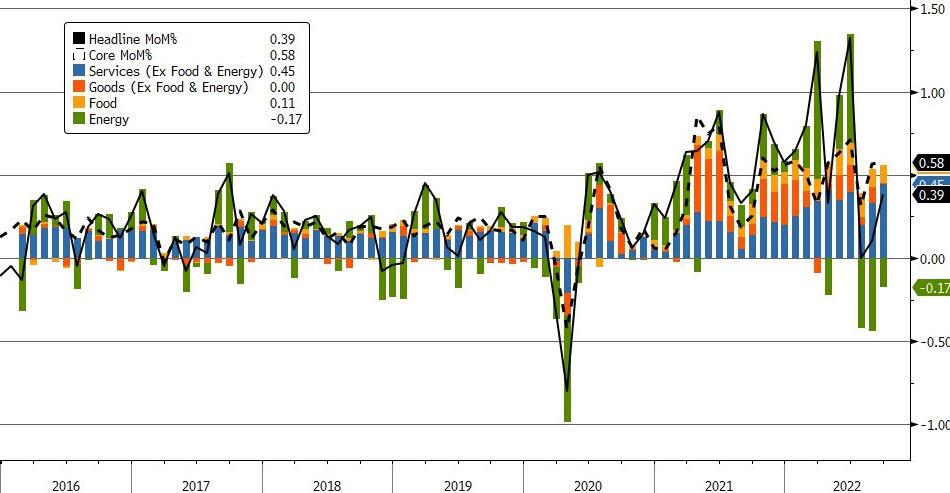

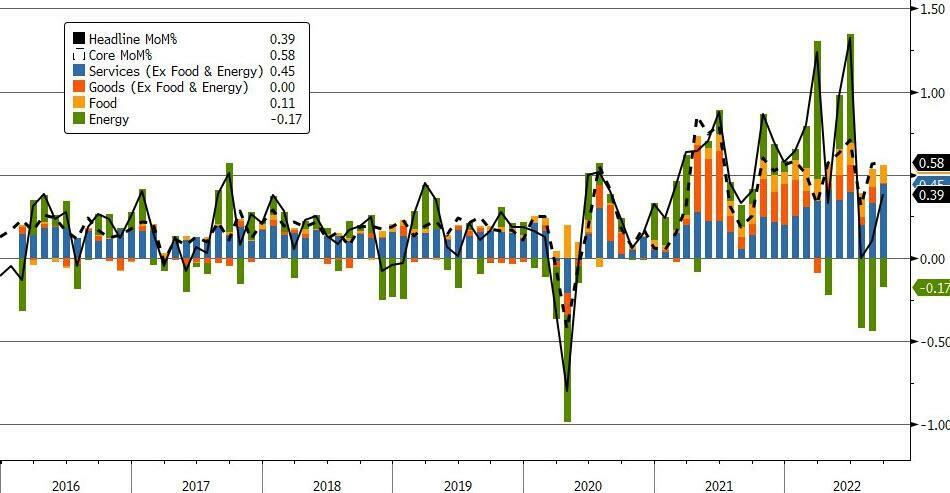

- 08:30: Sept. CPI MoM, est. 0.2%, prior 0.1%

- CPI YoY, est. 8.1%, prior 8.3%

- CPI Ex Food and Energy MoM, est. 0.4%, prior 0.6%

- CPI Ex Food and Energy YoY, est. 6.5%, prior 6.3%

- 08:30: Oct. Initial Jobless Claims, est. 225,000, prior 219,000

- Continuing Claims, est. 1.37m, prior 1.36m

DB’s Jim Reid concludes the overnight wrap

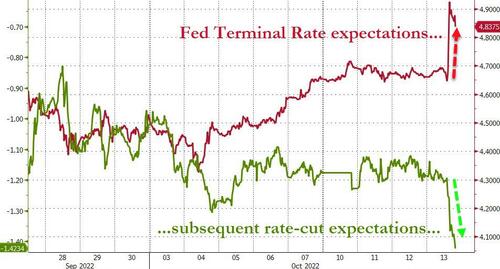

There’s been little relief for investors over the last 24 hours, with the major asset classes fluctuating between gains and losses as markets were left with plenty of global developments to digest. For much of the day it had looked as though we might see equities begin to stabilise, but ultimately the S&P 500 (-0.33%) nose-dived into the close to decline for a 6th consecutive session and hit its lowest level since November 2020. For reference, if we get a 7th consecutive decline, that would be the worst run for the index since February 2020 as fears about the global spread of Covid-19 ramped up. Whether that happens could largely hinge on today’s all-important CPI print from the US, which is the last big piece of data the Fed will get ahead of their next decision in just under 3 weeks’ time. Bear in mind it was only last month that the stronger-than-expected reading on core CPI sparked a big re-evaluation about when the Fed would slow down their rate hikes, with futures pricing out the chances they’d adjust to 50bp hikes in November in favour of a continued 75bps pace. In turn, that triggered the biggest one-day decline in the S&P 500 since June 2020, with a -4.32% move, so investors will be keenly attuned for any fresh surprises today.

Ahead of that release, we got an advance look yesterday at US inflation pressures last month from the PPI reading. That showed the monthly headline measure coming in above expectations at +0.4% (vs. +0.2% expected), which also meant that the year-on-year measure only fell back to +8.5% (vs. +8.4% expected). The core measure excluding food and energy was more in line with expectations however, coming in at +0.3%, with the year-on-year core reading at +7.2% (vs. +7.3% expected). In terms of what our US economists are expecting for today, they think that the headline CPI print will come in at +0.28% (vs. +0.12% in August) as energy continues to drag on the main print. However, they see core CPI which excludes energy and food prices coming in at a stronger +0.44% (vs. +0.57% in September), and it’s that reading which should get the most focus given last month’s upside surprise. In turn, those numbers should push the year-on-year CPI down to +8.1%, while core CPI should pick up to +6.5%.

As we look forward to the CPI print later, there are some initial signs of markets recovering their poise, with the VIX index of volatility (-0.06pts) ticking lower for the first time in a week. That coincided with continued falls in US equities, as mentioned, with the S&P 500 down -0.33% and the NASDAQ a hair lower at -0.09%, although futures today are pointing modestly higher, with contracts on the S&P 500 (+0.16%) and the NASDAQ 100 (+0.11%) both advancing. One factor supporting the amidst the broader uncertainty was some positive corporate news as we head into earnings season, with PepsiCo (+4.18%) being one of the top performers in the S&P after they increased their profit and sales outlook for the rest of the year. That said, the European indices were much less positive, with the STOXX 600 (-0.53%) losing ground for a 6th consecutive session, and European equity futures are pointing towards further losses again today.