y harveyorgan · in Uncategorized · Leave a comment·Edit

by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSE: DOWN $26.50 to $1643.70

SILVER PRICE CLOSE: DOWN $0.77 to $18,20

Access prices: closes

Gold ACCESS CLOSE 1643.50

Silver ACCESS CLOSE: 18.26

New: early yesterday morning//

Bitcoin morning price: $19,698 UP 333

Bitcoin: afternoon price: $19,195 DOWN 170.

Platinum price closing DOWN $6.10 AT $901.40

Palladium price; closing DOWN $113.75 at $2006.80

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD $2281 CDN DOLLARS PER OZ DOWN $8.98 CDN DOLLARS

BRITISH GOLD IN POUNDS: 1468.95 POUNDS PER OZ DOWN 2.82 BRITISH POUNDS PER OZ/

EURO GOLD: 1688.70 EUROS PER OZ// DOWN 14.30 EUROS PER OZ///

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: OCTOBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,670.000000000 USD

INTENT DATE: 10/13/2022 DELIVERY DATE: 10/17/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 2

132 C SG AMERICAS 1

323 C HSBC 495

435 H SCOTIA CAPITAL 57

624 C BOFA SECURITIES 1

661 C JP MORGAN 203 17

690 C ABN AMRO 251

800 C MAREX SPEC 5

TOTAL: 516 516

MONTH TO DATE: 22,205

JPMORGAN STOPPED 17/516

GOLD: NUMBER OF NOTICES FILED FOR OCT CONTRACT: 516 NOTICES FOR 51,600 OZ or 1.6049 TONNES

total notices so far: 22,205 contracts for 2,220,500 oz (69.066 tonnes)

SILVER NOTICES: 0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month 418 : for 2,090,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $26.50

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////A WITHDRAWAL OF 1.16 TONNES INTO THE GLD//

INVENTORY RESTS AT 944.31 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 77 CENTS

AT THE SLV// :/BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A HUGE DEPOSIT OF 2.211 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 484.920 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 3097 CONTRACTS TO 131,153 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE GIGANTIC GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.02 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS/HFT WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.02)., BUT UNSUCCESSFUL IN KNOCKING OFF ANY SPEC LONGS. SOME SPECS CONTINUE TO ADD TO THEIR SHORTFALLS FROM WHICH OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS.

WE MUST HAVE HAD:

I) MINIMAL SPECULATOR SHORT COVERINGS ////CONTINUED BANKER OI COMEX ADDITIONS /// CONSIDERABLE NEWBIE SPEC SHORT ADDITIONS. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.580 MILLION OZ FOLLOWING A 60,000 OZ QUEUE JUMP / // V) GIGANTIC SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: — 51

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT:

TOTAL CONTRACTS for 12 days, total 52,302 contracts: 26.151 million oz OR 2.179MILLION OZ PER DAY. (435 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 26.151 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 26.151 MILLION OZ INITIAL

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3097 DESPITE OUR $0.02 LOSS IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1155 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /STRONG BANKER ADDITIONS // STRONG SHORT ADDITIONS//CONSIDERABLE NEWBIE SPEC LONG ADDITIONS// /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT. OF 1.580 MILLION OZ FOLLOWED BY TODAY’S 60,000 QUEUE JUMP .. WE HAD AN ATMOSPHERIC SIZED GAIN OF 4252 OI CONTRACTS ON THE TWO EXCHANGES FOR 21.26 MILLION OZ..

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 224 CONTRACTS TO 435.797 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED — -632 CONTRACTS.

.

THE SMALL SIZED INCREASE IN COMEX OI CAME WITH OUR LOSS IN PRICE OF $0.40//COMEX GOLD TRADING/THURSDAY // MINIMAL SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT. AT 66.099 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE. JUMP OF 56,300 OZ//NEW STANDING 70.793 TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END)

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $0.40 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 2337 OI CONTRACTS 7.269 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2113 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 435,797

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2337 CONTRACTS WITH 224 CONTRACTS INCREASED AT THE COMEX AND 2113 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2337 CONTRACTS OR 7.269 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2113) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (224): TOTAL GAIN IN THE TWO EXCHANGES 2337 CONTRACTS. WE NO DOUBT HAD 1) ZERO SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS///NEWBIE SPEC SHORT ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 66.099 TONNES FOLLOWED BY TODAY’S 56,300 OZ QUEUE. JUMP ///NEW STANDING 70.793 TONNES//. 3) ZERO LONG LIQUIDATION //// //.,4) SMALL SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT. :

26,861 CONTRACTS OR 2,686,100 OZ OR 83.54 TONNES 12 TRADING DAY(S) AND THUS AVERAGING: 2230 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES: 83.54 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 83.54/3550 x 100% TONNES 2.36% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 83.54 TONNES INITIAL ( MUCH SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GIGANTIC SIZED 3097 CONTRACT OI TO 131,157 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1155 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 1155 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1155 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3097 CONTRACTS AND ADD TO THE 1155 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF 4252 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 21.260 MILLION OZ

OCCURRED DESPITE OUR LOSS IN PRICE OF $0.02

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED UP 58.35 PTS OR 1.85% //Hang Seng CLOSED UP 198.53 OR 1.21% /The Nikkei closed UP 853.34PTS OR 3.25% //Australia’s all ordinaires CLOSED UP 1.51% /Chinese yuan (ONSHORE) closed DOWN TO 7.1939 //OFFSHORE CHINESE YUAN DOWN 7.2286// /Oil DOWN TO 87.50 dollars per barrel for WTI and BRENT AT 92.73 / Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 224 CONTRACTS TO 435,797 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS SMALL COMEX INCREASE OCCURRED WITH OUR FALL IN PRICE OF $0.40 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2113 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF OCT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2113 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :2113 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2113 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2337 CONTRACTS IN THAT 2113 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 224 CONTRACTS..AND THIS FAIR GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR FALL IN PRICE OF GOLD $0.40//WE HAD SPEC SHORTS ADDING TO THEIR POSITIONS WITH BANKERS TAKING THE OTHER SIDE AS BUYERS OF COMEX GOLD CONTRACTS. WE ALSO HAD SOME ADDITIONAL SPECS GOING LONG DUE TO THE ATTRACTIVE PRICE (EARLIER IN THE SESSION)

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING OCT (70.793),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 70.793 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $0.40) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS (THEY ADDED TO THEIR POSITIONS) AS WE HAD A FAIR SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 2969 CONTRACTS // WE HAVE REGISTERED A FAIR GAIN OF 7.269 PAPER TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR OCT. (70.793 TONNES)…THIS WAS ACCOMPLISHED WITH A RISE IN PRICE OF $0.40

WE HAD -632 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 2337 CONTRACTS OR 233700 OZ OR 7.269 TONNES

Estimated gold volume 178,705// poor//

final gold volumes/yesterday 252,515/ fair

INITIAL STANDINGS FOR OCT ’22 COMEX GOLD //OCT 14

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 68,710.375oz JPMorgan 2010 kilobars Brinks 5kilobars Delaware 15 kilobars Manfra |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 516 notice(s) 51,600 OZ 1.6049 TONNES |

| No of oz to be served (notices) | 555 contracts 55500oz 1.726 TONNES |

| Total monthly oz gold served (contracts) so far this month | 22,205 notices 2,220,500 69.066 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits NIL oz

customer withdrawals:4

i) Out of JPMorgan: 64,623.510 oz (2010 kilobars)

ii) out of Delaware: 482.26 0z (15 kilobars)

iii) Out of Brinks 160.76 oz (5 kilobars

iv) Out of Manfra: 3443.84 oz

total: 68,710.375 oz

total in tonnes: 2.13 tonnes

Adjustments: 4// all dealer to customer

i)HSBC 5601.916 oz

ii) JPMorgan 34,433.718 ox

iii) Malca 7137.527 oz

iv) Manfra 289.354 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT we have an oi of 1071 contracts having GAINED 452 contracts . We had 111 contracts

filed on THURSDAY, so we GAINED A WHOPPING 563 contracts or an additional 56,300 oz will stand in this active delivery month of Oct. From this point

we should gain in total gold standing through to the end of Oct.( This is queue jumping and in reality it is the exercising of London based EFP;s for gold at the comex)

November GAINED 10 contracts to stand at 3141

December lost 4085 contracts down to 361,143

We had516 notice(s) filed today for 51,600 oz FOR THE OCT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 203 notices were issued from their client or customer account. The total of all issuance by all participants equate to 516 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 17 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT /2022. contract month,

we take the total number of notices filed so far for the month (22,205) x 100 oz , to which we add the difference between the open interest for the front month of (OCT 1071 CONTRACTS) minus the number of notices served upon today 516 x 100 oz per contract equals 2,286,000 OZ OR 70.793 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT contract month:

No of notices filed so far (22,205) x 100 oz+ (1071) OI for the front month minus the number of notices served upon today (516} x 100 oz} which equals 2,286000, oz standing OR 70.793 TONNES in this NON active delivery month of OCTOBER.

TOTAL COMEX GOLD STANDING: 70.793 TONNES (A HUMONGOUS STANDING FOR OCT (GENERALLY THE POOREST DELIVERY MONTHS FOR AN ACTIVE MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,968,238.247 OZ 61.220 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 25,746,418.721 OZ

TOTAL REGISTERED GOLD: 12,267,870.325 OZ (381.58 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 13,478,148.396 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,299,632 OZ (REG GOLD- PLEDGED GOLD) 320.36 tonnes//rapidly declining

END

SILVER/COMEX

OCT 14//INITIAL OCT SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,238,792.498oz Brinks CNT Delaware Int. Delaware |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 957,251.160 oz CNT HSBC JPM Manfra |

| No of oz served today (contracts) | 0 CONTRACT(S) (nil OZ) |

| No of oz to be served (notices) | 105 contracts (525,000 oz) |

| Total monthly oz silver served (contracts) | 418 contracts 2,090,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 4 deposits into the customer account

i) into CNT 13m635.870 oz

ii) Into HSBC: 600,081.690 oz

iii) Into JPMorgan: 305,489.900 oz

iv) Into Manfra: 38,043.700 oz

Total deposits: 957.251.160 oz

JPMorgan has a total silver weight: 161.106million oz/309.122million =52.12% of comex

Comex withdrawals: 4

i)Brinks 595,807.37 oz

ii) Out of CNT 598,055.327 oz

iii) Out of Delaware 7941.011 oz

iv) Out of Int. Delaware 36,968.790 oz

total withdrawals: 1,238,792.498 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 40.077 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 309.122 MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF OCT OI: 105 CONTRACTS HAVING GAINED 11 CONTRACT(S.)

WE HAD 1 NOTICE FILED ON THURSDAY SO WE GAINED 12

SILVER CONTRACTS OR AN ADDITIONAL 60,000 OZ WILL STAND FOR OCT.

NOVEMBER GAINED 1 CONTRACTS TO STAND AT 398

DECEMBER SAW A GAIN OF 2005 CONTRACTS UP TO 106,475

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes:65,610// est. volume today// good

Comex volume: confirmed yesterday: 77,237 contracts ( good)

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 418 x 5,000 oz = 2,090,000 oz

to which we add the difference between the open interest for the front month of OCT(105) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT./2022 contract month: 418 (notices served so far) x 5000 oz + OI for front month of OCT (105) – number of notices served upon today (0) x 5000 oz of silver standing for the OCT contract month equates 2,615,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:56,736// est. volume today// poor

Comex volume: confirmed yesterday: 64,896 contracts ( poor)

END

GLD AND SLV INVENTORY LEVELS

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 11/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

OCT 10//WITH GOLD DOWN $33.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 944.31 TONNES

OCT 7/WITH GOLD DOWN $10.70: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 946.34 TONNES

OCT 6/WITH GOLD UP $.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.45 TONNES INTO THE GLD//INVENTORY RESTS AT 946.34 TONNES

OCT 4/WITH GOLD UP $28.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD//INVENTORY RESTS AT 942.89 TONNES

OCT 3.WITH GOLD UP $29.30 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD AND A BIG SURPRISE: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 939.70 TONNES

SEPT 30 WITH GOLD UP $3.75 TODAY : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES FROM THE GLD////INVENTORY RESTS AT 941.15 TONNES

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

GLD INVENTORY: 944.31 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

Oct 12/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.196 MILLION OZ

OCT 11/WITH SILVER DOWN 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.066 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.196 MILLION OZ

OCT 10//WITH SILVER DOWN 65 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 7/WITH SILVER DOWN 37 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.447 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 473.130 MILLION OZ/

OCT 6/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY: A WITHDRAWAL OF 5.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 475.617 MILLION OZ//

OCT 4WITH SILVER UP $.51 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ

OCT 3/WITH SILVER UP $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 30/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.013 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 480.917 MILLION OZ//

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

CLOSING INVENTORY 484.920 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

Egon Von Greyerz…

WITH STOCKS AND DEBT UP 50X IN 50 YEARS HOW FAR WILL THEY COLLAPSE?

Egon von Greyerz

October 14, 2022

With stocks, bonds and property in major bear markets, investors are desperately hoping (and praying) that the Fed and other Central banks will come to their rescue. But this time it is different. (You have heard that before). Central banks are determined to kill off inflation and with that the economy. They will of course panic at regular intervals, just like the Bank of England recently did with their £65 billion emergency injection to save the pension funds and the gilt market.

But just like the bull market in stocks is turning into a long term bear market, the 40 year down trend in rates finished in 2021. As inflation rages around the world, the coming rapid rise in interest rates will not just shock investors. It will turn the global $300 trillion debt and the $2 quadrillion derivatives (mainly interest derivatives) into a lethal weapon of mass destruction.

Yes, Central banks will panic occasionally and lower rates. But the heavy weight of the debt will lead to both private and sovereign defaults and sell offs which will put continuous upward pressure on rates.

As the world enters the biggest economic and (geo)-political storm in history, few investors are prepared for the total annihilation of their wealth.

DOW UP 55X

In December 1974, the Dow bottomed at 677 and47 years later the Dow peaked at 37,000 – an increase of 55X. With a compound annual growth of 9%, the Dow doubled every 8 years during this period.

WILL ALFRED LOSE ALL HIS MONEY

Let’s return to Alfred a US citizen who was born at the end of WWII, I wrote an article about him in February 2019 called “Stock Investors like Alfred to Lose 98% of their Investment”

Well, Alfred was very lucky throughout his investment life. By putting all his savings and excess earnings into the Dow Jones he managed to amass a fortune of $14 million until the end of February 2019. He was even more fortunate to see the US market gain another 45% (including dividends) until the end of 2021. So his wealth had by that time grown another $6 million to $20.3 million.

As I wrote in the 2019 article, Alfred never sold and sat through every vicious correction for 77 years. So until January 2022, buy and hold had worked like a dream.

By the end of the first week of October 2022 Alfred’s portfolio is down from $20.3 in January to $16.2 million which is a loss of $4.1 million in 2022.

Currently Alfred is not the slightest bit worried as he has seen many corrections of 20% to 60% in the last 77 years.

Based on his experience, Alfred is not concerned although $4 million is a big paper loss.

But what if the dream is over for Alfred and turns into a nightmare with all his gains evaporating in a market collapse of 90% or more like in 1929-32?

Well, in my view the odds are very high that we will see a fall of that magnitude.

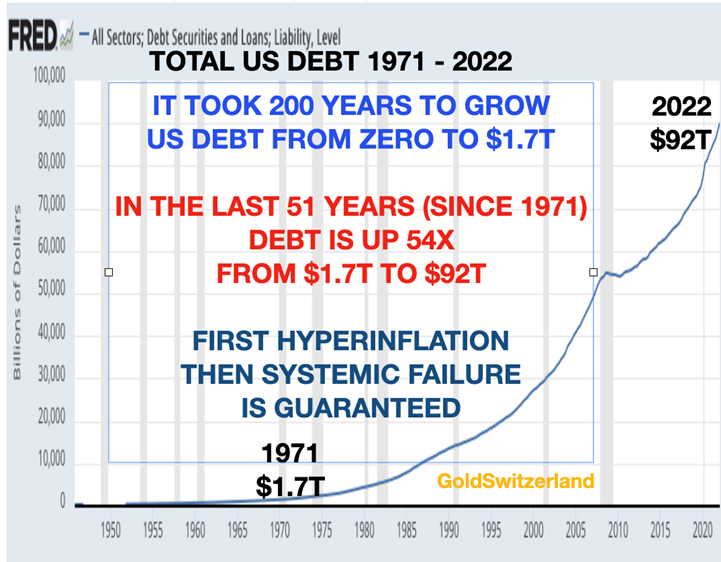

A DEBT INFESTED WORLD

A debt infested world has lived on borrowed time since the debt feast started in 1971 when Nixon took the dollar, and therefore most currencies, off the gold standard.

And what a feast it has been with total US debt going from $1.7 trillion in 1971 to $92 trillion today.

That is a staggering 54X increase in US debt in 52 years!

Just look at the Dow Jones chart at the beginning of the article which shows a 55X increase in the index during the same time period.

It is clearly no coincidence that stocks are up 54X and debt 55X since the early 1970s

Stocks have not risen due to a sound and well managed economy. No, stocks only went up because printed money was handed to investors to inflate the economy and asset prices.

We must remember that during the same period since 1971 when the gold window was closed that the US dollar has lost 98% of its value in real terms.

Thus the debt explosion has created inflated values which will deflate much faster when the debt implodes in the next few years.

So it took 200 years to go from zero debt to $1.7t. But when you remove the shackles of the monetary discipline that the gold standard enforces, irresponsible and incompetent governments and central bankers only have one objective. Their principal policy is to hang on to power for as long as possible.

When money runs out, like it did in 1971, there is only one way to stay in power and that is to buy votes. Thus the creation of $90 trillion debt since 1971 has been the most expensive bribery in history.

We must also remember that US Federal debt has increased every year since 1930 (with only a handful of years with surpluses).

The dilemma of creating money out of thin air of such a magnitude is that it leads to debts that can never be repaid, fake asset values which will implode and false human values resulting in misery and decadence. The inevitable consequences are economic and financial collapse. And that sadly is what the US and the world is facing next.

So what will be the market consequences of the coming (hyper)-inflationary depression followed by a deflationary implosion?

Let’s look at some enlightening charts:

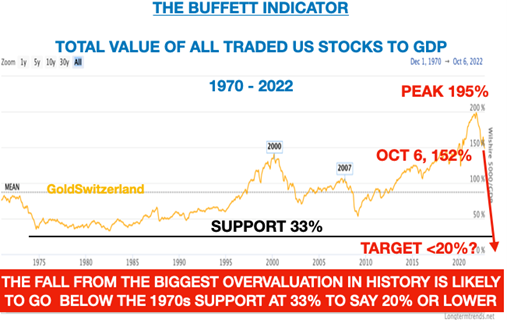

1. THE BUFFETT INDICATOR – VALUE OF STOCK MARKET TO GDP

The total value of US stocks (Wilshire 5000) to GDP is one of Warren Buffett’s favourite indicators. It reached almost 200% in November 2021. The previous record valuations were 140% in 2000 (Dot Com Bubble) and 106% in 2007 (Sub Prime Crisis). A strong support area is the lows in the1970s at around 33%.

I doubt however that the 1970s support will hold after the Epic mega bubble we have just seen totally fueled by tens of trillions of exploding dollar debt.

Especially since 2009, the debt intoxication of investors has driven stocks to dizzy heights which is likely to result in a hangover that will not only take years but probably decades to recover from.

So poor Alfred, this is not what he needed at the tail end of his investment life. But sadly he like most investors don’t know better since the Fed until now has saved them.

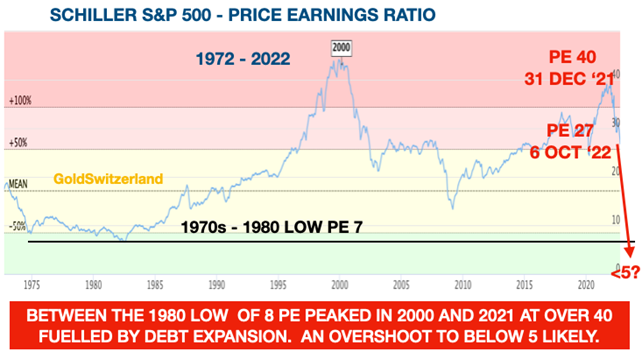

2. PRICE EARNINGS RATIO – BOTH PRICE AND EARNINGS TO DECLINE

I remember well when I moved to the UK in 1972 and worked for Dixons first as Finance Director and later as Vice-Chairman. Dixons was a camera and audio/TV retailer at the time, quoted on the London stock exchange. I received my first options at £1.32.

Two years later after an oil crisis in the Middle East and a coal miners’ strike in the UK (with only 3 days of electricity) stocks crashed across the globe. Dixons’ share price collapsed from 132 English pence to 10 pence. So my options were 93% out of the money!

Dixons had a strong balance sheet and was still profitable. But profits declined by around 75%. (It wasn’t easy to demonstrate TVs and HIFI in candle light.)

So Dixons’ earnings per share of 6.6 pence in 1972 went down by 75% to 1.6 pence and the PE ratio went from 20 to 6. That was the best lesson I ever learnt to as a young man to experience what can happen to markets. Anyway, I then joined the board at 29 and we went on to build the business to the biggest consumer electronics retailer in the UK and a FTSE 100 company.

Most investors today, including Alfred, would not believe that the shares of a successful company can decline as much as 93% but I was fortunate to experience this when I was young and did not have much to lose.

So as the debt bubble fueled market collapses from a historical and epic uber-valuation, I would would not be surprised to see the S&P PE ratio to undershoot the 7 level in 1980 and go below 5 as shown in the chart above.

3. DOW / GOLD RATIO TO GO TO HISTORICAL LOWS

Since the gold window was closed in 1971, the fluctuations in the Dow/Gold ratio have been dramatic. This is what can be expected when most of the gold trading takes place in a heavily manipulated paper market. The whole false financial system based on worthless paper assets is now under tremendous pressure.

For example, the UK’s mini-budget two weeks ago led to a massive decline in the pound and a near collapse of the UK bond market. The bank of England, at the request of pension funds, had to support the bond market to the extent of 65 billion pounds.

This shows the fragility of markets today when a relatively minor event can lead to a near collapse of the UK financial system and therefore also the global system, since everything is connected.

The problem was as expected in the $2 quadrillion derivative market which had been used to hedge interest risk by the pension funds. Virtually every financial instrument traded today includes a major element of derivatives.

So when we look at the Dow/Gold Chart we must bear in mind that most of the trading in the Dow and Gold is in derivatives and that by a multiple of many 100 times.

The Dow/Gold ratio was at 1 in 1980 which means that the Dow was 850 and gold $850. The ratio then reached a peak in 1999 as gold fell and the Dow was strong. Since then the ratio has gone down to 17 or 62%. This means that gold has strongly outperformed the Dow.

If the Dow goes down by over 90% like in 1932, we would expect the ratio to reach the support of 0.5 which means for example 3500 Dow and $7,000 gold.

But the current massive over valuation of stocks and undervaluation of gold is likely to take the ratio to the 0.2 level of the early 1800s and even overshoot.

As the gold paper market collapses, and gold can trade freely but with massive physical demand and very little gold available, I would not be surprised to see a 0.1 ratio. That could lead to 3,500 Dow and $35,000 gold.

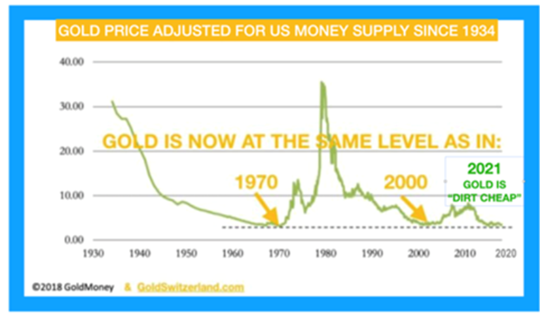

That gold price would also more accurately reflect the massive growth in money supply as gold today is massively under valued in relation to the growth in US money supply as the chart below shows.

FORECASTNG IS A MUG’S GAME

By definition, a forecast will always be wrong. Only future historians will give the world the correct retrospective forecast since hindsight is the most perfect of all sciences.

Thus the above projections are just an indication where the biggest global bubble asset market in history could implode to when things go really wrong – which I fear they will do.

The most important thought I would like to leave investors with is that risk is today at a historical extreme.

Therefore today is not the time for greed, hoping that markets will grow to the sky. Instead, now is the time for wealth preservation and protecting what you have. Otherwise, wealth which has been acquired over several decades could easily evaporate in the next few years.

Physical gold and silver have throughout history acted as the ultimate insurance of wealth. This time will not be different.

end

Lawrie Williams

END

3.Chris Powell of GATA provides to us very important physical commentaries

This is a must read

(Alasdair Macleod)

Alasdair Macleod: Banking crisis prompts the great unwind

Submitted by admin on Thu, 2022-10-13 12:11Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, October 13, 2022

There is a growing feeling in markets that a financial crisis of some sort is now on the cards. Credit Suisse’s very public struggle to refinance itself is proving to be a wake-up call for markets, alerting investors to the parlous state of global banking.

This article identifies the principal elements leading us into a global financial crisis. Behind it all is the threat from a new trend of rising interest rates, and the natural desire of commercial banks everywhere to reduce their exposure to falling financial asset values both on their balance sheets and held as loan collateral. And there are specific problems areas, which we can identify.

The phenomenal growth of over-the-counter derivatives and regulated futures has been against a background of generally declining interest rates since the mid-1980s. That trend is now reversing, so we must expect the $600 trillion of global OTC derivatives and a further $100 trillion of futures to contract as banks reduce their derivative exposure.

In the last two weeks, we have seen the consequences for the gilt market in London, warning us of other problem areas to come.

Commercial banks are overleveraged, with notable weak spots in the eurozone, Japan, and the UK. It will be something of a miracle if banks in these jurisdictions manage to survive contracting bank credit and derivative blow-ups. If they are not prevented, even the better-capitalized American banks might not be safe.

Central banks are mandated to rescue the financial system in troubled times. However, we find that the European Central Bankand its entire euro system of national central banks, the Bank of Japan, and the U.S. Fed are all deeply in negative equity and in no condition to underwrite the financial system in this rising interest rate environment. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/banking-crisis-the-great-unwind?gmrefcode=gata

end

Demand for gold/silver coins huge at the UK’s royal mint

(London Financial Times/GATA)

UK’s Royal Mint lifted by market turmoil as demand for gold surges

Submitted by admin on Thu, 2022-10-13 17:13Section: Daily Dispatches

By Daniel Thomas

Financial Times, London

Thursday, October 13, 2022

Market turmoil during the past year has boosted the performance of the Royal Mint as demand for gold coins and precious metals surged, pushing the profits of the UK’s oldest surviving manufacturer to a record high.

The wholly state-owned company has supplied the country’s coins since the reign of King Alfred the Great more than 1,100 years ago. But in its modern form it has expanded into sales of precious metals, historic coins, jewellery, and luxury collectibles.

A record number of investors hedged their portfolios with physical precious metals such as gold and silver during the course of its latest financial year to the end of March, pushing the Mint’s pre-tax profits to L18 millon, up from L 12.4 millon in the previous 12 months. Revenues rose from £ 1.1 billionn to £1.4 billion. …

… For the remainder of the report:

https://www.ft.com/content/1591cafa-6ff1-4a53-99ae-778af37b6f43

end

4. OTHER PHYSICAL SILVER/GOLD

5.OTHER COMMODITIES:

end

COMMODITIES IN GENERAL/

END

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.1939

OFFSHORE YUAN: 7.2286

SHANGHAI CLOSED UP 58.35 PTS OR 1.85%

HANG SENG CLOSED UP 198.53 OR 1.21%

2. Nikkei closed UP 853.34 PTS OR 3.25%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 113.15/Euro FALLS TO 0.97144

3b Japan 10 YR bond yield: FALLS TO. +.243/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 146.73/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.205%***/Italian 10 Yr bond yield RISES to 4.663%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.378%…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.785//

3j Gold at $1654.90//silver at: 18.68 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1 AND06/100 roubles/dollar; ROUBLE AT 62.58//

3m oil into the 87 dollar handle for WTI and 92 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 147.75DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

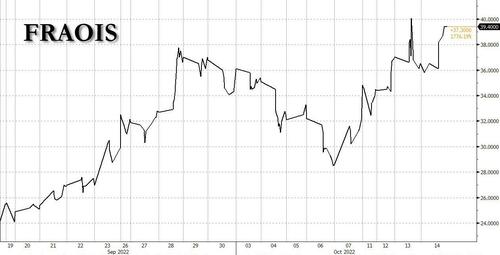

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 1.0042– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9755well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.895 DOWN 6 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.879 DOWN 5 BASIS PTS//(USA 30 YR INVERTED TO THE USA 10)

USA DOLLAR VS TURKISH LIRA: 18,59…GETTTING DANGEROUS

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Flat Amid Firehose Of News, Start Of Earnings Season

FRIDAY, OCT 14, 2022 – 08:34 AM

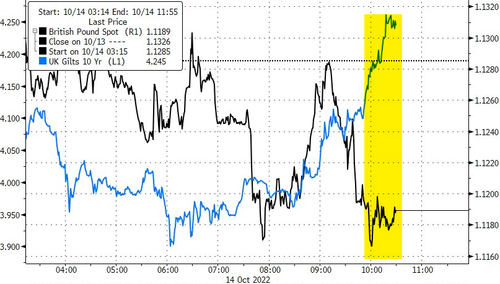

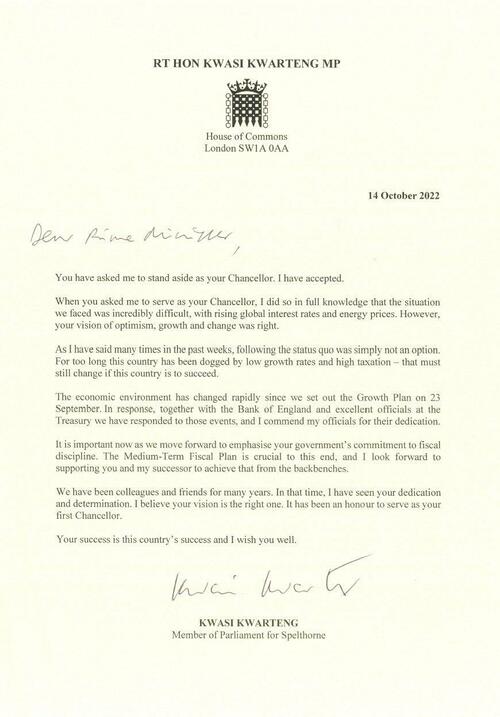

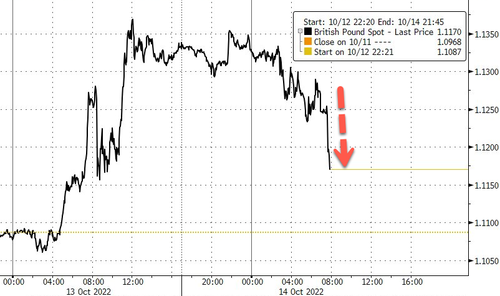

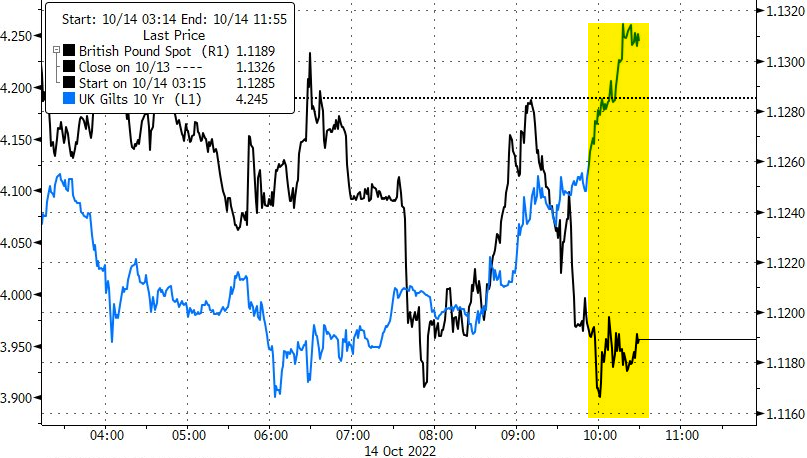

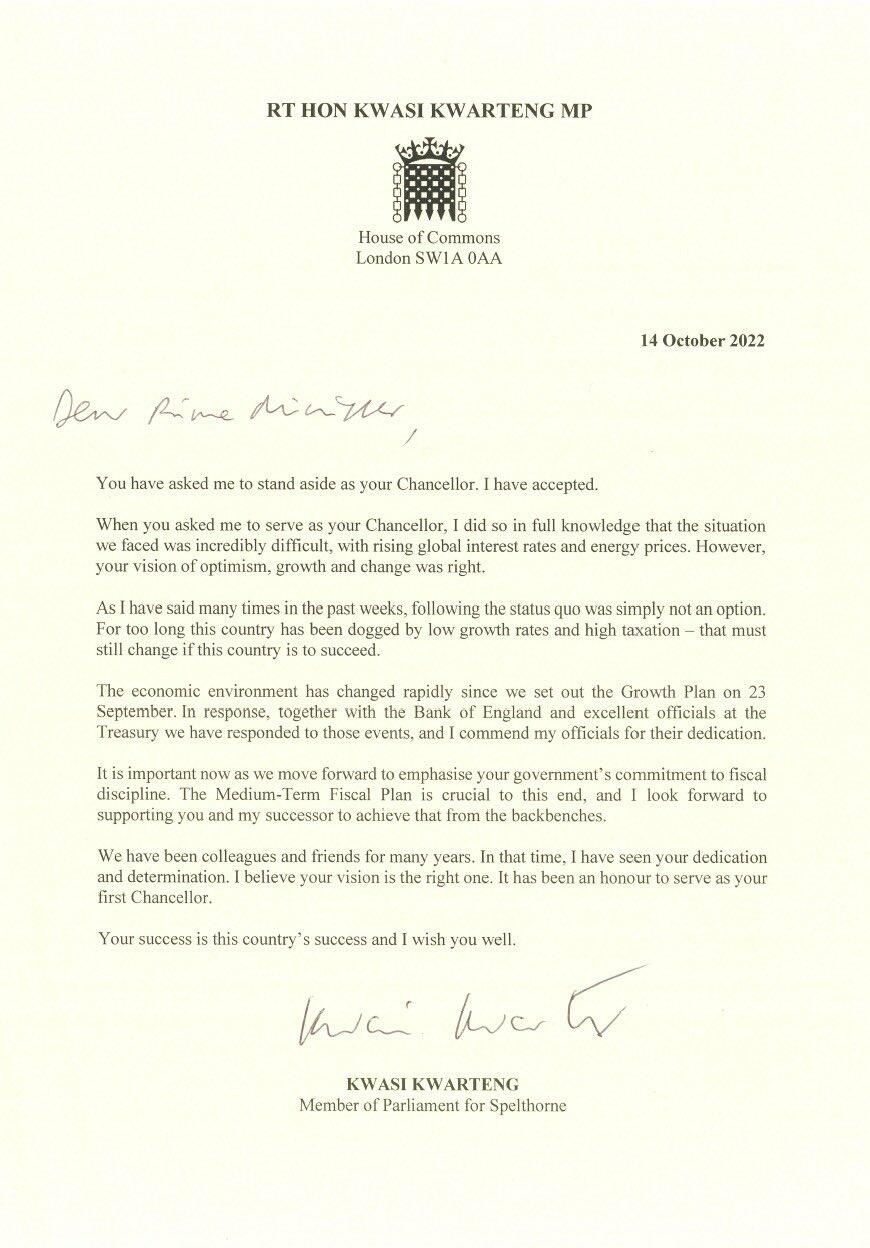

Welcome to the final day of the week and first day of Q3 earnings season, which coming after yesterday’s torrid post-CPI reversal, has already seen a flood of newsflow and market volatility: while JPM reported solid earnings this morning to launch the latest earnings season helping push its stock higher in the premarket, followed by mediocre results from Wells and Citi and a soggy update from Morgan Stanley which sent its price down 3%, the big news of the day is the unexpected termination of UK chancellor Kwasi Kwarteng who was summarily fired as a scapegoat for the unprecedented chaos gripping the UK over the past month.

And with traders desperately scrambling to stay on top of all the flashing red headlines, futures are surprisingly flat, as S&P 500 and Nasdaq 100 futures flip between losses and gains as corporate results started rolling in. US banks are expected to post the biggest profit decline of any S&P 500 Index sector, according to data compiled by Bloomberg Intelligence, even as energy props up the entire market. The fear is Fed tightening will spark defaults and force banks to set aside higher provisions against losses.

In premarket trading, tech shares continued to weaken as Jefferies became the latest bank to highlight the impact of higher rates and US restrictions on shipments to China. Nutanix shares rose as much as 18% in premarket trading after Dow Jones reported that the company is exploring a sale after receiving takeover interest, citing people familiar with the matter. Here are some other notable premarket movers:

- Delta Air Lines (DAL US) shares gain 1.3% in premarket trading after Cowen upgraded the carrier to outperform from market perform, noting that the third quarter was strong outside of Hurricane Ian, which took earnings slightly below the broker’s estimates.

- Beyond Meat (BYND US) shares fell 10% in premarket trading after the company lowered its 2022 revenue outlook and said it’s reducing current workforce by approximately 200 employees.

- Keep an eye on Blue Owl (OWL US) as the stock was initiated with an overweight recommendation at Piper Sandler, which says the asset management firm is well positioned to take advantage of long-term industry tailwinds.

- Travere Therapeutics (TVTX US) fell 5.1% in postmarket trading on Thursday as the company announced that it sees a three-month extension of the previously assigned PDUFA target action date for its application for accelerated approval of sparsentan for the treatment of IgA nephropathy.

“Even though investors may look through a disappointing CPI print, it will be a much higher bar to look through weak corporate earnings.” Invesco global market strategist David Chao told clients. “Growth is below trend and decelerating because the Fed is still tightening. This is a tough backdrop for risk assets.”

In Europe, the Stoxx 50 adds 1%. IBEX outperforms peers, climbing 1.1%, DAX lags, adding 0.8%. Utilities, real estate and chemicals are the strongest-performing sectors. Here are the biggest movers:

- Bystronic shares rise as much as 1.9%, the most since June, after company reported a net revenue beat yoy for the nine-month period. Analysts welcome a more specified and positive outlook.

- Ahold Delhaize shares advance as much as 2.3% after Bryan Garnier said a potential Kroger-Albertsons tie-up removes concerns about Ahold merging with Albertsons, which had been rumored over the summer.

- Arcadis gains as much 5.3%, the most intraday in three months, after KBC Securities raised its rating on the engineering company to buy from accumulate, saying recent acquisitions have increased the company’s exposure to growth trends, while the stock’s valuation is “conservative.”

- Kone shares fall, paring earlier gains of as much as 4.3%, after the Finnish elevator firm reported preliminary adjusted Ebit for the third quarter that missed estimates.

- Temenos shares tumble as much as 23% to the lowest since 2016, after the banking software firm announced a sharp cut to FY Ebit target on the back of a 50% miss on bottom-line in 3Q.#

- International Distributions Services plunges as much as 17%, most since early days of Covid-19 pandemic, after reporting a loss at its Royal Mail unit and warning of possible job cuts in response to recent strike action.

- TomTom NV falls as much as 12%, the most since May 24, after it lowered guidance for free cash flow as a percentage of revenue to break-even from at least 5%.

In Britain, government bonds rallied sharply as Prime Minister Liz Truss prepared to reverse parts of her tax-cutting program and ousted chancellor Kwasi Kwarteng. The pound weakened. Her plans have roiled UK markets for weeks, forcing the Bank of England to launch an emergency bond-buying program. That program expires later on Friday.

“It does seem pretty clear that the government is preparing a U-turn on at least a very big chunk, if not half, the permanent tax cuts in the budget,” BlackRock Inc.’s chief macroeconomic strategist, Rupert Harrison, told Bloomberg Television. “And if we don’t get that, then the markets will react very negatively.”

Earlier in the session, Asian stocks took impetus from the aggressive rebound on Wall St where stocks made a remarkable comeback from the initial CPI-related selling with several factors attributed to the turnaround including a dovish ECB staff model view, speculation of a major U-turn in the UK’s fiscal plans and a touted short squeeze. ASX 200 was lifted in which energy led the broad strength across sectors and after Australian Treasurer Chalmers recently ruled out scrapping tax cuts in the budget. Nikkei 225 outperformed and breached the 27,000 level amid some earnings encouragement with index heavyweight Fast Retailing boosted after it posted a record annual profit. Hang Seng and Shanghai Comp. benefitted from the heightened risk appetite as the PBoC reiterated support pledges, while participants digested relatively inline inflation numbers and now await the latest Chinese trade data.

In FX, the Bloomberg Dollar Spot Index staged a modest rebound after yesterday’s loss and the greenback advanced versus most of its Group-of-10 peers.

- The pound led G-10 declines, halting a blistering rally that’s made it the best performer among major currencies this week amid reports of potential u-turns on the UK government’s proposed tax cuts.

- The euro pared some of yesterday’s advance, to trade at around $0.9750. Bunds and Italian bonds advanced for a second day, led by the belly.

- The Aussie was the best G-10 performer after China’s central bank pledged to do more to stimulate the economy. Shorter-maturity bonds declined, following losses in similar-dated Treasuries on Thursday.

- The yen headed for an eighth day of losses, but selling was tempered by speculation the authorities will step in to support the currency. A five-year auction drew solid demand

- The Hungarian forint rallied by as much as 3% versus the euro, the biggest jump in 11 years, after the central bank said it would provide 18% one-day deposit rate

In rates, Treasury yields fell by as much as 4bps, led by the front end following a sharp rally in gilts as UK bonds head toward their biggest weekly gains since 2011 amid expectations the British government is preparing to partially reverse its tax cuts plans. The UK curve aggressively bull-flattens with long-end yields richer by 30bp on the session; UK 2s10s, 5s30s spreads flatter by 17bp and 5bp. In the US, 10-year futures remain short of Thursday’s highs with cash yields richer by 3bp-5bp across the curve. Focal points of US session include retail sales data and three scheduled Fed speakers. US 10-year yields near lows of the day into early US session, richer by 4.5bp at around 3.90% with gilts outperforming by an additional 20bp in the sector; long-end of the US curve lags slightly, steepening 5s30s spread by ~1bp.

In commodities, WTI and Brent front-month futures are modestly softer on the day as the Dollar picked up in early European hours, but the contracts hold onto most of yesterday’s gains. Turkish President Erdogan has ordered the energy minister to build a gas hub in Turkey following talks with Russian President Putin; says both countries will immediately work on Putin’s proposal to transport Russian gas, via NTV cited by Reuters. Spot gold found resistance at it is 21 DMA (USD 1,671.50/oz) with the yellow metal edging lower as the USD extends on intraday highs. LME futures are mixed/contained with 3M copper holding onto levels above USD 7,500/t, but LME aluminium dips following the recent rise. Spot gold falls roughly $5 to trade near $1,662/oz.

Bitcoin posts modest gains after yesterday’s rebound, with the crypto above USD 19,500, whilst Ethereum holds a USD 1,300+ handle.

To the day ahead now, and data releases include US retail sales for September, and the University of Michigan’s preliminary consumer sentiment index for October. From central banks, we’ll hear from the ECB’s Holzmann, and the Fed’s George, Book and Waller. Finally, earnings releases include JPMorgan, Wells Fargo, Citigroup, Morgan Stanley and UnitedHealth.

Market Snapshot

- S&P 500 futures down 0.2% to 3,674.50

- STOXX Europe 600 up 1.1% to 393.36

- MXAP up 1.9% to 138.38

- MXAPJ up 1.7% to 446.58

- Nikkei up 3.3% to 27,090.76

- Topix up 2.3% to 1,898.19

- Hang Seng Index up 1.2% to 16,587.69

- Shanghai Composite up 1.8% to 3,071.99

- Sensex up 1.5% to 58,119.00

- Australia S&P/ASX 200 up 1.7% to 6,758.83

- Kospi up 2.3% to 2,212.55

- German 10Y yield little changed at 2.18%

- Euro down 0.3% to $0.9751

- Brent Futures down 0.6% to $93.97/bbl

- Gold spot down 0.2% to $1,663.18

- U.S. Dollar Index up 0.36% to 112.76

Top Overnight News from Bloomberg

- Hawkish European Central Bank officials aim to start unwinding the institution’s €5.1 trillion ($4.9 trillion) asset hoard by early 2023 while retaining interest rates as their primary monetary-policy tool, according to people familiar with the matter

- The euro-area economy may succumb to two consecutive quarters of contraction, European Central Bank Vice President Luis de Guindos told Verslo žinios, a Lithuanian newspaper

- Overstretched positioning in the options market is taking a hit after the dollar retreated following the release of the latest US inflation data

- Singapore’s central bank tightened monetary policy settings for a fifth time in the past year, warning of persistent price pressures and a clouded outlook for the global and local economy

- China’s consumer inflation remained subdued in September as lockdowns continued to impact spending habits, while soft commodity prices kept producer inflation in check. The consumer price index rose 2.8% last month from a year earlier

- A shift toward private markets is cushioning many of the world’s largest investors from the wreckage wrought by runaway inflation and spiraling interest rates

- Sweden’s nationalists, who emerged as the second largest political force in last month’s elections, will stay out of the new government that will take over from Magdalena Andersson’s Social Democrats

A more detailed look at global markets courtesy of Newsquawk

APAC stocks took impetus from the aggressive rebound on Wall St where stocks made a remarkable comeback from the initial CPI-related selling with several factors attributed to the turnaround including a dovish ECB staff model view, speculation of a major U-turn in the UK’s fiscal plans and a touted short squeeze. ASX 200 was lifted in which energy led the broad strength across sectors and after Australian Treasurer Chalmers recently ruled out scrapping tax cuts in the budget. Nikkei 225 outperformed and breached the 27,000 level amid some earnings encouragement with index heavyweight Fast Retailing boosted after it posted a record annual profit. Hang Seng and Shanghai Comp. benefitted from the heightened risk appetite as the PBoC reiterated support pledges, while participants digested relatively inline inflation numbers and now await the latest Chinese trade data.

Top Asian News

- Xi Faces ‘Rockiest Economy in Decades’ on Eve of Party Congress

- Singapore Unveils New $1.05 Billion Inflation-Relief Package

- Japan Keeps Up Yen Warnings, Declines to Say If Intervened

- Iron Ore Heads for Longest Run of Weekly Losses in Almost a Year

European bourses trade on a firmer footing in an extension of yesterday’s gains. There hasn’t been a clear factor behind today’s moves with some desks continuing to cite oversold conditions, evidence of disinflationary impulses in more timely indicators (e.g. NY Fed survey) and hopes of a policy u-turn in the UK. Sectors in Europe mostly firmer, with outperformance in Real Estate and Utilities. To the downside but still in positive territory, Tech, Autos and Telecom names lag peers. Stateside, Stateside, US futures are showing a more contained performance with the e-mini S&P back below 3700 as pausing for breath from yesterday’s rally.

Top European News

- UK PM Truss is to reverse some economic plans later today, according to Bloomberg sources.; UK PM Truss is to hold a press conference today (timing TBC), according to Bloomberg.

- UK Trade Department Minister Hands said there are absolutely no plans to change anything; there is no change to plans on corporation tax, according to Reuters.

- UK PM Truss and Chancellor Kwarteng are weighing up whether to announce corporation tax rise today after chancellor’s early flight back from the US, according to Times’ Swinford; no decision has yet been taken.

- UK Tory whips warned that UK PM Truss could face a leadership challenge if Chancellor Kwarteng’s economic statement on October 31st fails to end the turbulence in financial markets, according to the Daily Mail front page.

- UK senior Tories are reportedly holding talks about replacing PM Truss with a joint ticket of Rishi Sunak and Penny Mordaunt, according to The Times.

- The 1922 Committee is ready to suspend the rule that prevents a vote to oust the Conservative leader within a year of taking office, according to the New Statesman.

- ECB’s Lagarde said inflation in the EZ is far too high, and likely to stay above the ECB’s target for an expected period of time; governing council expects to raise the interest rate further over the next several meetings

- ECB’s Kazimir said 75bps hike in October is appropriate; Deposit Rate must rise above Neutral but start of balance sheet reduction can wait until next year

FX

- DXY attempts to claw back some of yesterday’s losses and briefly reclaimed 113.00 to the upside vs yesterday’s 113.92 peak.

- GBP sits as the laggard as it unwinds some of the prior day’s gains.

- USD/JPY topped yesterday’s high of 147.67 whilst BoJ Kuroda reiterated the need to maintain stimulus.

- HUF strengthened following an unexpected NBH hike to the Overnight Collateral Loan Rate.

- Hungarian Central Bank unexpectedly hikes the Overnight Collateral Loan Rate to 25% from 15.5%. NBH will launch a new one-day deposit tender from today with an 18% interest rate.

Fixed Income

- Bunds are well within a 136.75-138.52 range vs their prior 136.22 prior close.

- Gilts are back above 97.00 between from yesterday’s 94.52 Liffe settlement amidst further reports that some economic plans may be reversed by the PM later today.

- T-note towards the top of its 111-14/110-27 overnight extremes ahead of US retail sales and Fed speakers

Commodities

- WTI and Brent front-month futures are modestly softer on the day as the Dollar picked up in early European hours, but the contracts hold onto most of yesterday’s gains.

- Turkish President Erdogan has ordered the energy minister to build a gas hub in Turkey following talks with Russian President Putin; says both countries will immediately work on Putin’s proposal to transport Russian gas, via NTV cited by Reuters.

- Spot gold found resistance at it is 21 DMA (USD 1,671.50/oz) with the yellow metal edging lower as the USD extends on intraday highs.

- LME futures are mixed/contained with 3M copper holding onto levels above USD 7,500/t, but LME aluminium dips following the recent rise.

Geopolitics

- Japan’s Chief Cabinet Secretary Matsuno said North Korea’s repeated ballistic missile launches are unacceptable and he believes North Korea will take further provocative action including a possible nuclear test. Matsuno added it is getting more difficult to detect North Korea’s missiles early and react, while they are considering all options including counterattack capabilities, according to Reuters.

- North Korea fires artillery shells off sea, according to South Korean military; into the buffer zones in the east and west seas during the afternoon, Yonhap reported

US event calendar

- 08:30: Sept. Import Price Index YoY, est. 6.2%, prior 7.8%

- 08:30: Sept. Import Price Index MoM, est. -1.1%, prior -1.0%

- 8:30: Sept. Export Price Index YoY, est. 9.3%, prior 10.8%

- 08:30: Sept. Export Price Index MoM, est. -1.0%, prior -1.6%

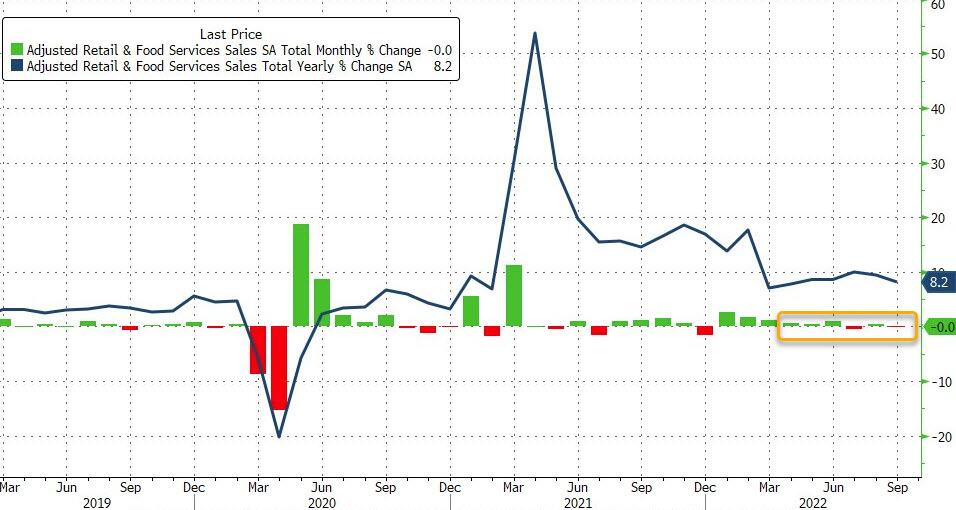

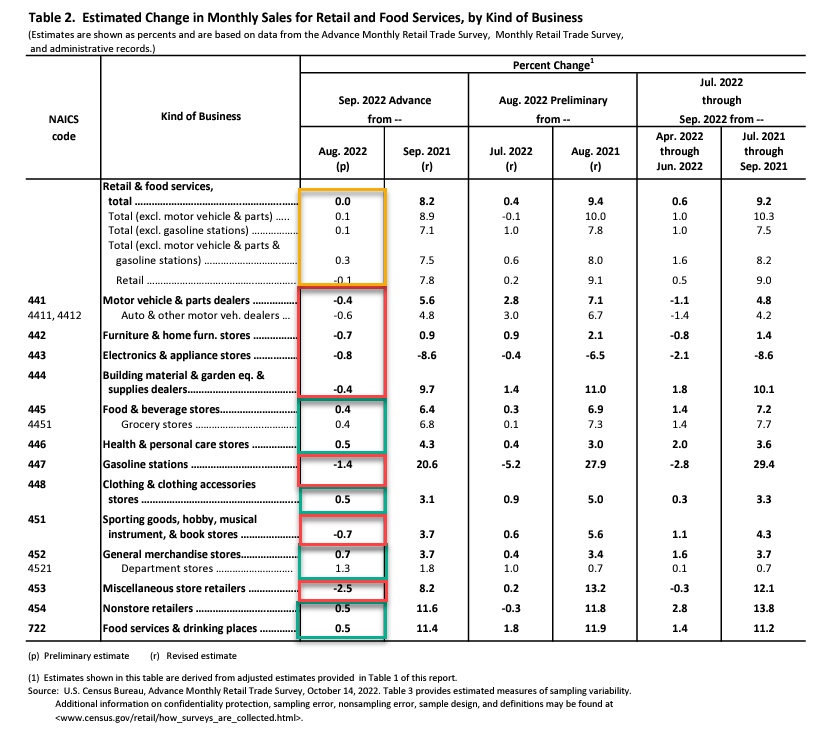

- 08:30: Sept. Retail Sales Advance MoM, est. 0.2%, prior 0.3%

- 08:30: Sept. Retail Sales Control Group, est. 0.3%, prior 0%

- 08:30: Sept. Retail Sales Ex Auto MoM, est. -0.1%, prior -0.3%

- 10:00: Aug. Business Inventories, est. 0.9%, prior 0.6%

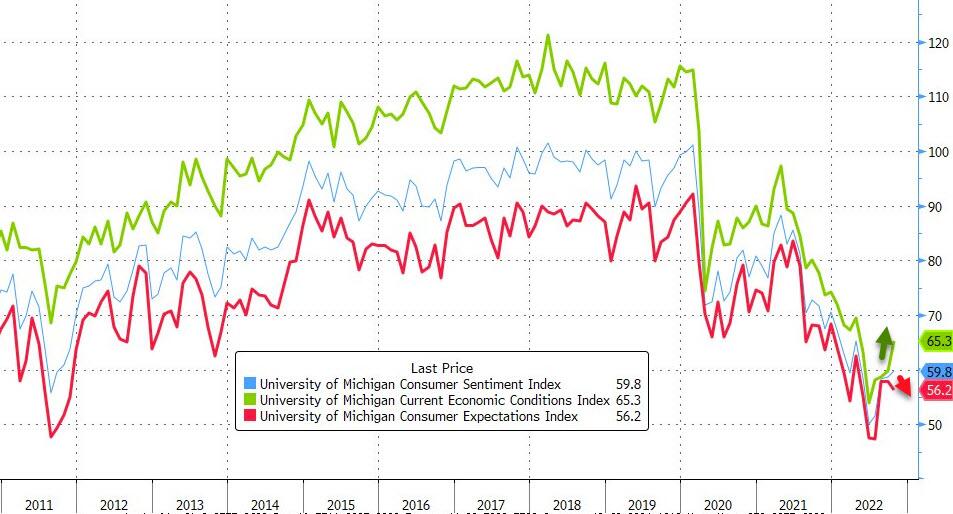

- 10:00: Oct. U. of Mich. 5-10 Yr Inflation, est. 2.8%, prior 2.7%

- 10:00: Oct. U. of Mich. 1 Yr Inflation, est. 4.6%, prior 4.7%

- 10:00: Oct. U. of Mich. Expectations, est. 58.2, prior 58.0

- 10:00: Oct. U. of Mich. Current Conditions, est. 59.5, prior 59.7

- 10:00: Oct. U. of Mich. Sentiment, est. 58.8, prior 58.6

DB’s Jim Reid concludes the overnight wrap

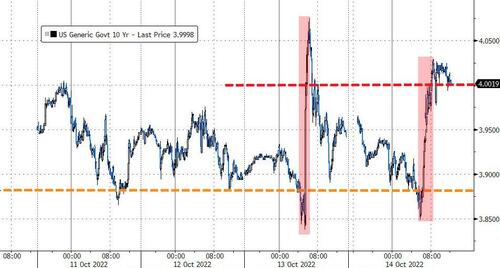

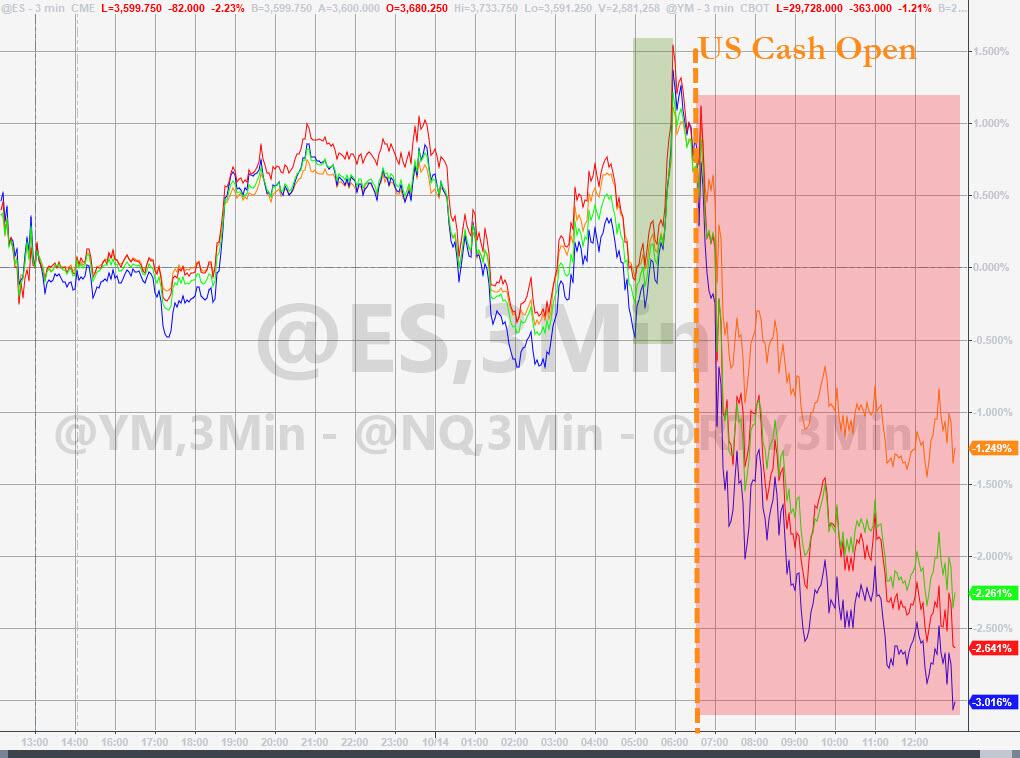

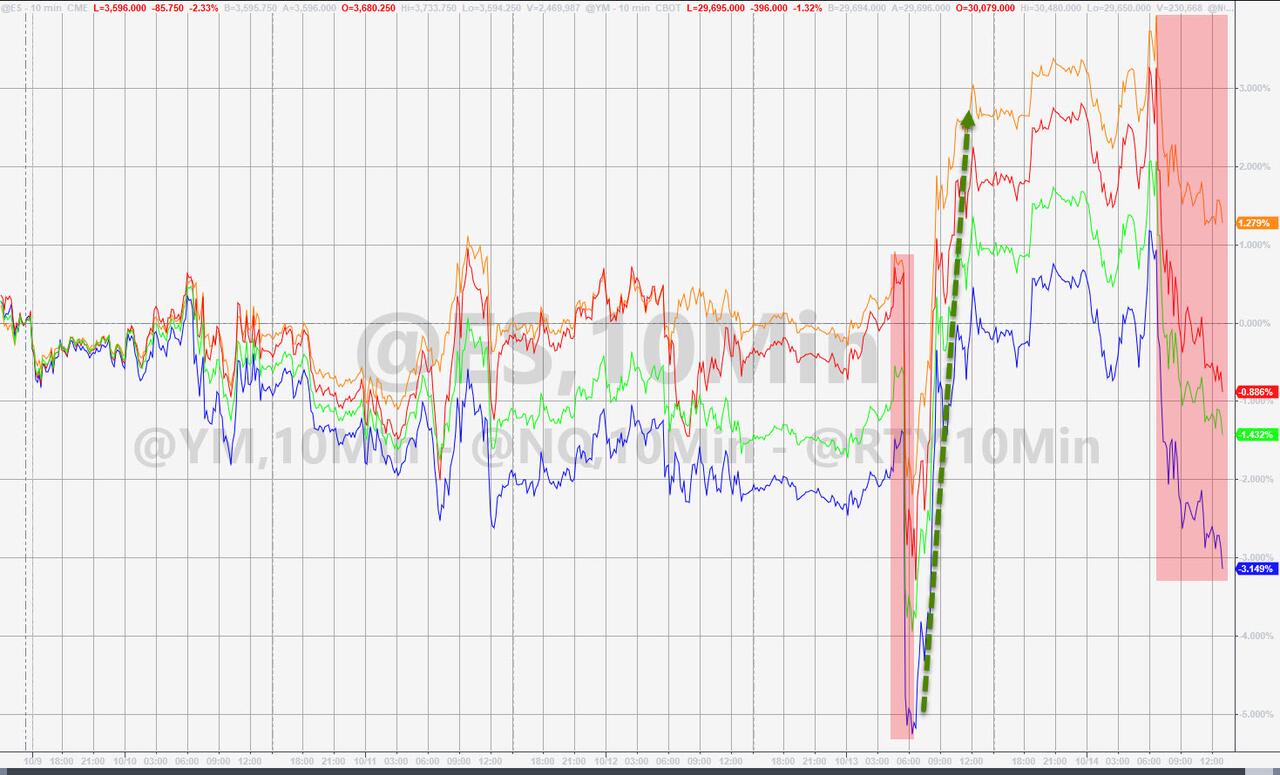

The term rollercoaster is one of the most overused, lazy terms to describe markets, but the last 24 hours are best summed up by being a major rollercoaster ride and actually home to one of the biggest intra-day turnarounds in living memory.

The white-knuckle ride started with a boost amidst reports of a potential fiscal U-turn out of the UK before then slumping on another upside surprise in US inflation, before rallying again (and rallying very hard) for no obvious reason other than potentially stretched bearish positioning ahead of the CPI. If that was the case one can only imagine how bullish markets would have been if CPI was soft. If you’re looking to further explain the unexplainable, Bloomberg suggested that the S&P 500 had given back 50% of the post-covid rally at the lows which triggered technical buy programs. Who knows if this was true.

To give you an idea of the ride, futures on the S&P were up +1.57% before CPI, down -2.40% around an hour later, but with the main index closing +2.60% and thus putting a spectacular end to a run of 6 consecutive declines, in spite of a CPI report that was another case of bad news from whatever angle you wanted to look at it. The index had a remarkable intraday range of 5.52%. Let’s see what US bank earnings bring today as they herald in the unofficial start of earnings season.

In terms of the details of that CPI report, the headline price gains for the month came in at +0.4%, which was above the +0.2% reading expected and meant that the year-on-year measure only ticked down to +8.2% (vs. +8.1% expected). Second, and more concerning from the Fed’s point of view, core CPI was also stronger than expected, with monthly core CPI at +0.6% (vs. +0.4% expected) for a second month running, thus taking the year-on-year measure up to +6.6%, which is the fastest that core inflation has been since 1982. Third, it wasn’t just a case of outliers driving inflation higher, since it continued to remain broad-based across the consumer basket. In fact, the Cleveland Fed’s trimmed mean measure that excludes the biggest outliers in either direction was still up +0.56% on the month (or +6.96% on an annualised basis), so still far from levels that the Fed can be comfortable with. And fourth, if you look at the Atlanta Fed’s measure that divides the consumer basket into sticky prices that change slowly and flexible prices that change quickly, then the monthly gain in sticky prices in September was the biggest since June 1982 at +0.68%, so things are getting even worse on that measure.

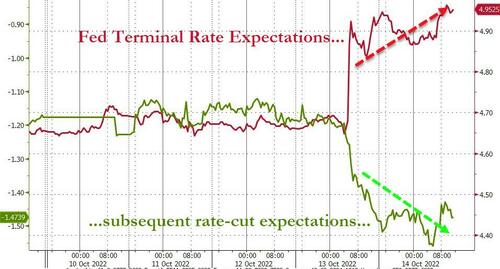

Against that backdrop, investors swiftly moved to upgrade their expectation of future tightening from the Federal Reserve, with a 75bp hike at the November meeting now fully priced in for the first time. In addition, markets placed a growing probability on the chances of the Fed continuing at a 75bps pace in December rather than slowing down. That’s in line with our US econ team’s updated call following the release, where they now expect the Fed to maintain the +75bp pace of hikes through December (link here). In markets a total of 143bps of hikes are now priced in by year-end. Looking further out into 2023, the peak rate priced for March rose +25.5bps on the day to a new high of 4.92% to reflect the extra 25bps of hikes, and the rate priced for end-2023 similarly rose +22.0bps to a fresh high of 4.57%.

With more tightening being priced in for the months ahead, Treasuries sold off across the curve with the front-end particularly impacted. By the close of trade, yields on 2yr Treasuries surged +17.2bps on the day to a post-2007 high of 4.46%, and their 10yr counterparts were also up +4.7bps to 3.94% after trading in a 23.8bps range. This morning yields are less than a bps lower across most of the curve.

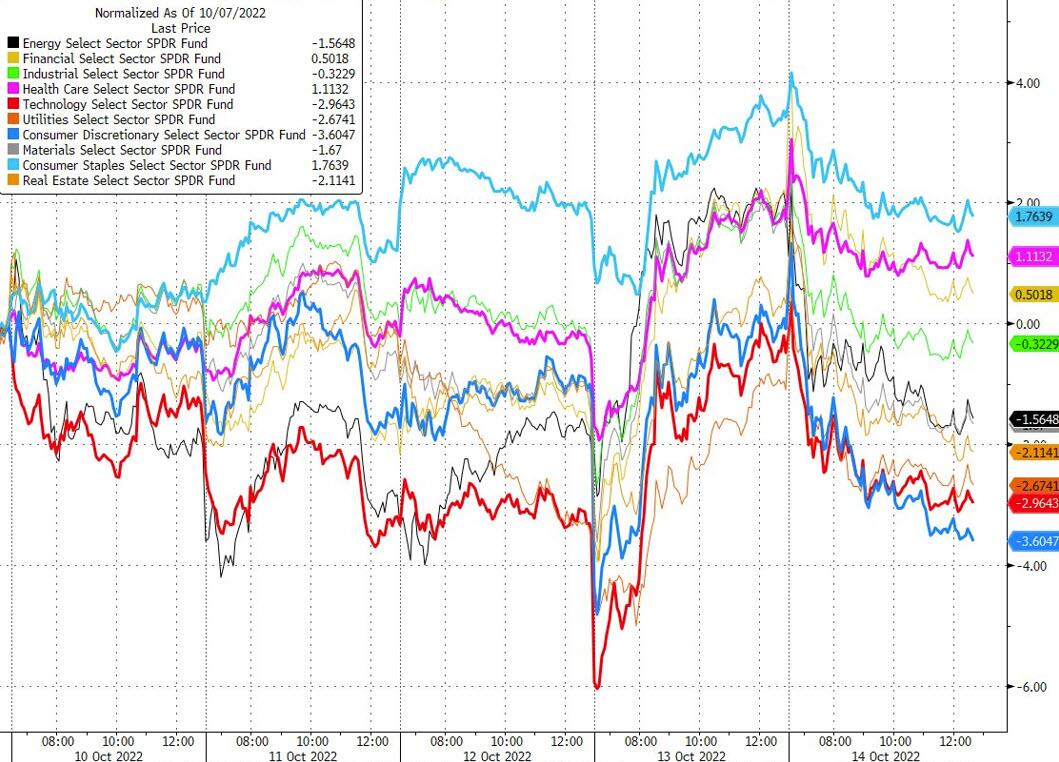

Decomposing the S&P, the best performers were the cyclically-sensitive energy, financial, information tech, and materials sectors, which, again, bucks against the macro news from yesterday. The Nasdaq lagged slightly behind the S&P, gaining +2.23%. In overnight trading, US equity futures are pointing to further gains with contracts on the S&P 500 (+0.54%) and the NASDAQ 100 (+0.47%) higher ahead of the big bank earnings.

Whilst there was plenty of interest in the US CPI, here in the UK there was also lots of market action going on amidst speculation that the government could be on the verge of a U-turn over their recent mini-budget. Sterling surged on the reports, which came from multiple outlets all suggesting that talks were taking place on reversing course. The biggest centre of speculation was with regard to corporation tax, which had been set to go up to 25% from April before Truss came to office, before that was then scrapped by Truss. Not going ahead with that increase was one of the biggest single items in terms of cost in the mini-budget, which totalled £19bn of the £45bn package of tax cuts announced, although it’s not clear yet to what extent they’ll reverse, and whether that might be to a lower rate than 25%. Overnight it’s been confirmed that Chancellor Kwarteng has left the IMF conference early which has further raised speculation of an imminent U-turn.

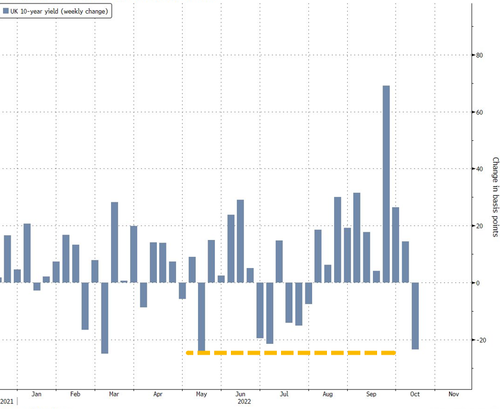

For now we haven’t had anything officially confirmed, but sterling surged by +2.04% on the day. Admittedly it had a helping hand from general dollar weakness, but that was still the largest daily increase in sterling since the Covid-related volatility of March 2020, so not the sort of moves we’re used to seeing every day. In the meantime, there was also an incredible rally for gilts as speculation of a U-turn mounted, with the 10yr yield down -23.5bps to 4.19% and 30yr yields down -26.1bps to 4.54% having been 5.09% at the highs in the previous session. That also came as the Bank of England bought a record £4.68bn of bonds yesterday, which is the largest so far, ahead of the scheduled end to their intervention in the gilt market today. Whether that actually happens we’ll see next week.

That sovereign bond rally was echoed elsewhere in Europe, with yields on 10yr bunds (-2.8bps), OATs (-3.7bps) and BTPs (-6.0bps) all moving lower on the day. And Euro equities put in a decent performance too, with the STOXX 600 recovering from its initial losses to gain +0.85%. That came in spite of investors also moving to ratchet up their expectations of future ECB tightening, with the rate priced in by year-end up +1.9bps on the day. Nevertheless, there was some better news on the inflation side from natural gas futures, which dropped to their lowest levels since early July, falling -3.98% on the day to €154 per megawatt-hour.

This morning in Asia, stock markets are tracking US equities with the Nikkei (+3.44%) leading gains and the Hang Seng (+3.38%) trading sharply higher while the Kospi (+2.45%), the CSI (+2.14%) and the Shanghai Composite (+1.74%) are also trading in positive territory.

Moving on to China, inflation has remained subdued amid persistent lockdowns and soft commodity prices. Early morning data showed that CPI advanced +2.8% y/y in September, up from +2.5% in August, pushed higher by food costs. While it rose at the fastest pace since April 2020, it fell short of market forecasts for a +2.9% gain. At the same time, the producer price index (PPI) dropped to its slowest pace in 20 months, rising by +0.9% (v/s +1.0% expected), down from +2.3% growth in August.

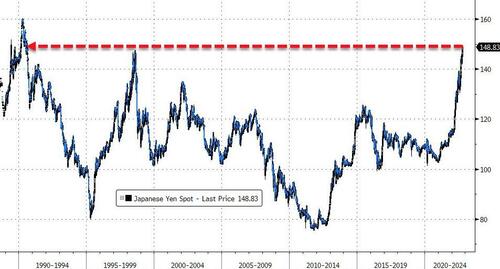

In the FX market, the Japanese yen has hit a fresh 32-yr low of 147.45 versus the US dollar, below the level when the Japanese authorities intervened last month. Yesterday, the BOJ Governor Haruhiko Kuroda in a speech indicated that he intends to stick to his policy of large-scale monetary easing as raising interest rates now seems inappropriate given Japan’s economic and price conditions.

The CPI was the main data focus yesterday, but we also got the weekly initial jobless claims from the US, which showed an increase to 228k in the week through October 8. That was a bit above the 225k reading expected and above the 219k reading the previous week, although it partly reflected a rise in Florida claims following Hurricane Ian.